Embed Size (px)

Citation preview

Annual results 2000Annual results 2000

Randstad Holding nv

February/March 2001

TopicsTopics

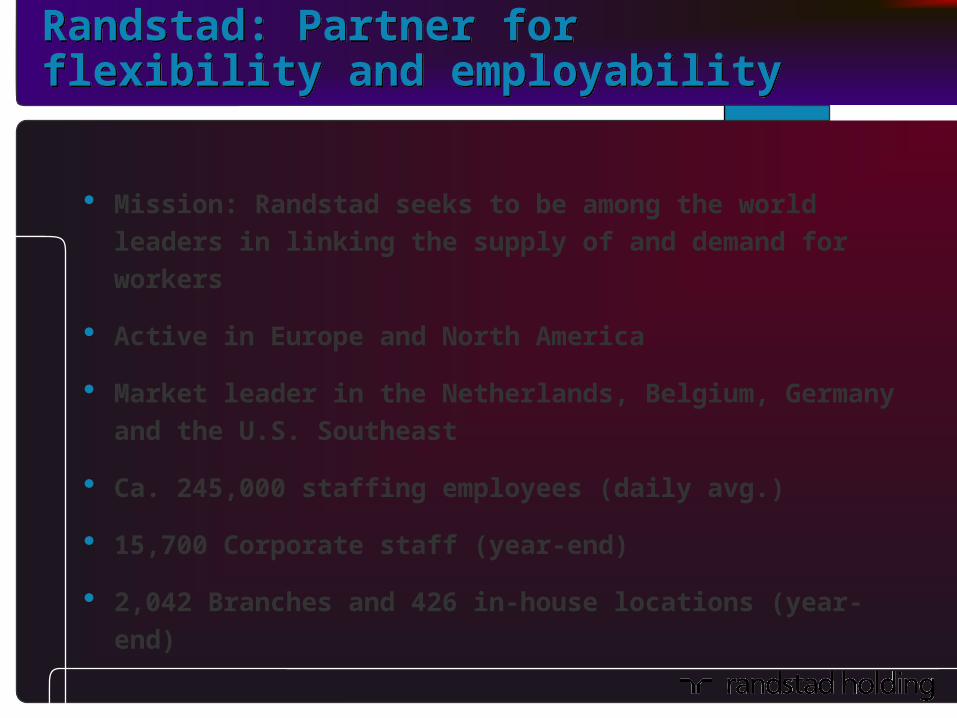

Randstad: partner for flexibility and employability

The Randstad agenda

The year 2000

Key figures and financial report

Strategy

Outlook and prospects

Randstad: Partner for flexibility and employabilityRandstad: Partner for flexibility and employability

Mission: Randstad seeks to be among the world leaders in linking the supply of and demand for workers

Active in Europe and North America

Market leader in the Netherlands, Belgium, Germany and the U.S. Southeast

Ca. 245,000 staffing employees (daily avg.)

15,700 Corporate staff (year-end)

2,042 Branches and 426 in-house locations (year-end)

The Randstad agendaThe Randstad agenda

Internationalization

Segmentation

Information and communication technology

Cost control

Accountability

2000: Operations2000: Operations

Internationalization

212 total new branches 134 branches through acquisitions

Segmentation divisional structure

Randstad GroupRandstad Group

Randstad Holding

Shared Service Centers

Professionalsstaffing

Mass-customized staffing

Large scale

staffing

Europe & North America

2000: Operations2000: Operations

Information and communication technologyintegrated ICT approachnew business models Hedson and

newmonday.comwebsites in Europe and North America

Accountabilityvalue-based management

Cost controlfar-reaching measures

2000: Various market developments2000: Various market developments

Leveling off in regions important to Randstad

Disappointing and strongly changing ICT market

Rapid market growth in other regions

Investment program maintained

Results under pressure

Measures in November 2000

The NetherlandsGermanyBelgium *FranceSpainUnited KingdomSwitzerlandItalyDenmark

North America

* Belgium including Luxembourg** Autonomous growth in brackets*** Market share Spain, including FY Umano

Market growth

0%15%12%20%15%

9%6%

200%20%

5.5%

Revenue growth **

-2.6% (-2.5)%13.4%

7.1%40.3% (26.0%)

217.5% (44.5%)

17.2%5.4%

2,515.9%28.3%

2.1% (1.0%)

Market share***

+/-+/-

-+++-

++

-

Development Randstad in Europe and North America 2000

Development Randstad in Europe and North America 2000

Growth in local currency, revenues from temporary staffing and secondment only

Market position

***

11162-5

5-104

7

EUR mln

Net revenues

Operating result as % revenues

Income after tax

Net income

Earnings per ordinary share from operations

Earnings per ordinary share

2000

6,168.1

250.64.1%

151.8

207.2

1.24

1.72

10.8

-17.6

-26.7

0.1

-27.9

0.0

1999

5,565.5

304.35.5%

207.0

207.0

1.72

1.72

Key financial data 2000Key financial data 2000

EUR mln

Net revenues

Gross profitas % revenues

Operating result (EBIT) as % revenues

Financial income and expenses, net TaxesResult non-consolidated participations

Income from ordinary operations after tax

Extraordinary result after tax

Net income

Earnings per ordinary share from operations

Earnings per ordinary share

2000

6,168.1

1,482.824.0

250.64.1

-20.5-67.2-11.1

151.8

55.4

207.2

1.24

1.72

10.8

13.3

-17.6

-26.7

-27.9

0.0

1999

5,565.4

1,308.723.5

304.35.5

-10.6-86.7

207.0

207.0

1.72

1.72

Income statement dataIncome statement data

EUR mln

Net revenues

Gross profitas % revenues

Operating result (EBIT) as % revenues

2000

3,216.7

753.6

23.4

147.8

4.6

%

10.4

14.8

-1.4

1999

2,913.3

656.3

22.5

149.9

5.1

Key data Randstad EuropeKey data Randstad Europe

2000

1,590.0

383.1

24.1

49.0

3.1

%

18.1

18.1

-42.5

1999

1,346.6

324.5

24.1

85.2

6.3

Key data Randstad North AmericaKey data Randstad North America

EUR mln

Net revenues

Gross profitas % revenues

Operating result (EBIT) as % revenues

2000

282.4

82.6

29.2

-10.7

-3.8

%

-1.4

-13.8

-159.

4

1999

286.4

95.8

33.4

18.0

6.3

Key data YACHTKey data YACHT

EUR mln

Net revenues

Gross profitas % revenues

Operating result (EBIT) as % revenues

EUR mln

Net revenues

Gross profitas % revenues

Operating result (EBIT) as % revenues

Operating result Capac (EBIT)as % revenues

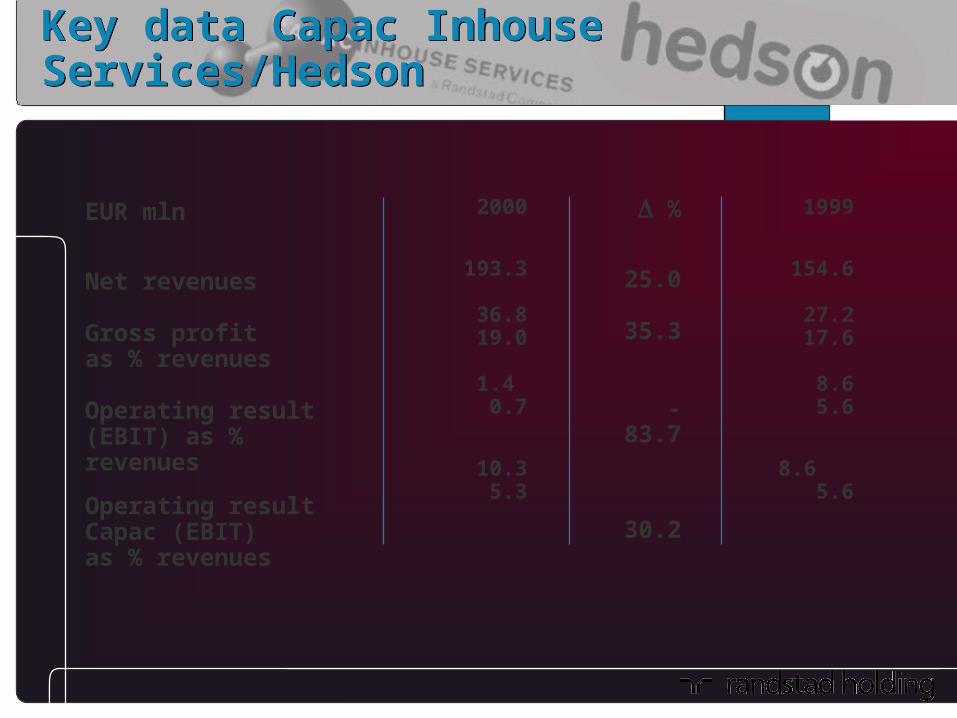

2000

193.3

36.819.0

1.4 0.7

10.35.3

%

25.0

35.3

-83.7

30.2

1999

154.6

27.2

17.6

8.6

5.6

8.65.6

Key data Capac Inhouse Services/HedsonKey data Capac Inhouse Services/Hedson

2000

627.8

176.0

28.0

61.3

9.8

%

-3.2

9.0

27.7

1999

648.8

161.5

24.9

48.0

7.4

Key data Tempo-Team/Otter-Westelaken GroupKey data Tempo-Team/Otter-Westelaken Group

EUR mln

Net revenues

Gross profitas % revenues

Operating result (EBIT) as % revenues

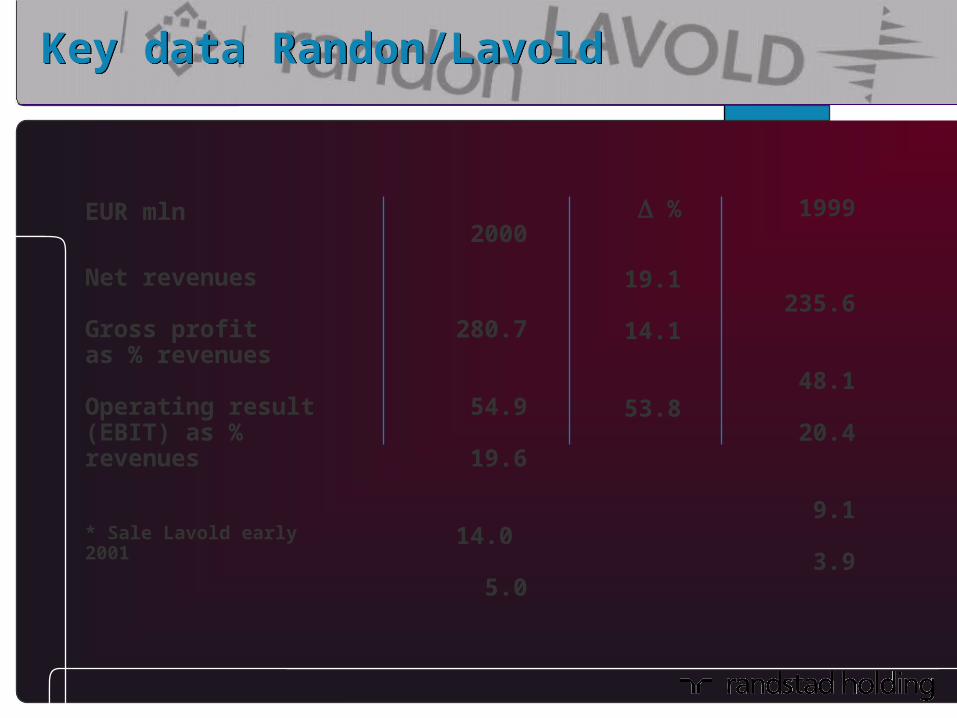

2000

280.7

54.9

19.6

14.0

5.0

%

19.1

14.1

53.8

1999

235.6

48.1

20.4

9.1

3.9

Key data Randon/LavoldKey data Randon/Lavold

EUR mln

Net revenues

Gross profitas % revenues

Operating result (EBIT) as % revenues

* Sale Lavold early 2001

After profit appropriation,EUR mln

Tangible fixed assetsOperational working capitalOperational capital employed

Interest-bearing debtCashNet debt

Interest coverage

Shareholders’ equity

Key balance sheet data (year-end)Key balance sheet data (year-end)

2000

253.4

489.1

742.5

591.8

53.6

538.2

14.9

301.4

%

28.1113.

874.1

73.2-

70.5236.

8

1999

197.8

228.8426.6

341.7

181.9

159.8

33.0

331.0

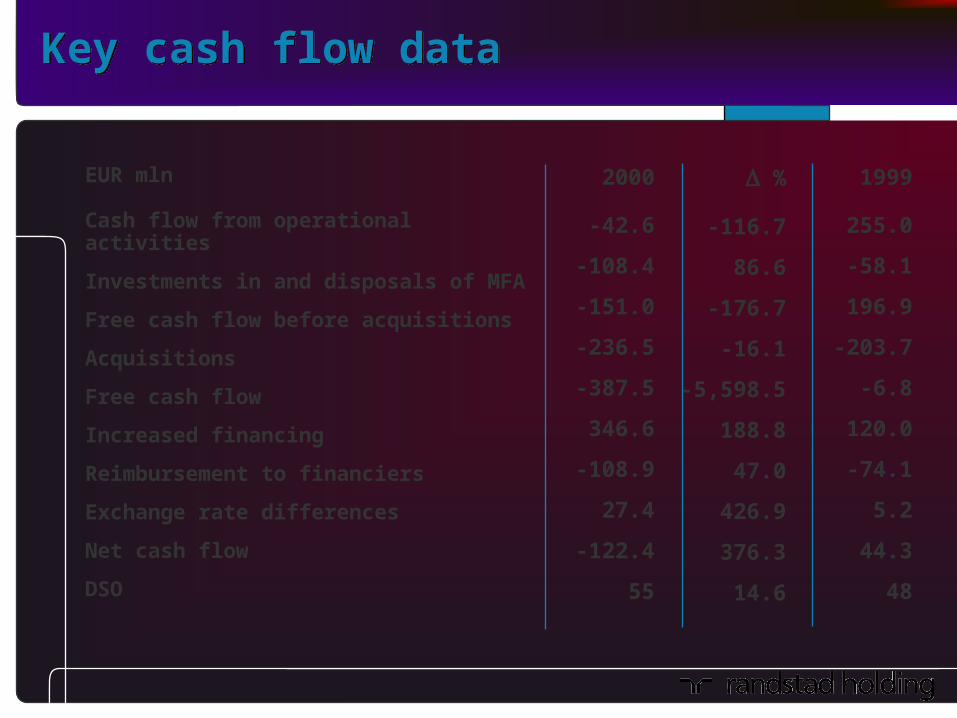

Key cash flow dataKey cash flow data

EUR mln

Cash flow from operational activities

Investments in and disposals of MFA

Free cash flow before acquisitions

Acquisitions

Free cash flow

Increased financing

Reimbursement to financiers

Exchange rate differences

Net cash flow

DSO

2000

-42.6

-108.4

-151.0

-236.5

-387.5

346.6

-108.9

27.4

-122.4

55

%

-116.7

86.6

-176.7

-16.1

-5,598.5

188.8

47.0

426.9

376.3

14.6

1999

255.0

-58.1

196.9

-203.7

-6.8

120.0

-74.1

5.2

44.3

48

StrategyStrategy

Goal:Creation of value for all stakeholders, through growth of revenues and profits, through which continuity over the long term is assured.

Autonomous growth and supplementary acquisitions

Geographic spread of revenues

Segmentation and focus

ICT

Multi-channel approach

Strategy: Growth plus supplementary acquisitionsStrategy: Growth plus supplementary acquisitions

Priority on rapid autonomous growth

Supplementary acquisitions to accelerate growth attaining more prominent market position

Strategy: Growth perspectiveStrategy: Growth perspective

The Netherlands

United Kingdom

France

Belgium

Spain

Germany

Italy

European Union

North America 5 - 7%

5-15%

35 - 43%

13 - 21%

15 - 19%

8 - 11%

4 - 7%

2 - 4%

3 - 5%

Average combined growth, 1998-2010

Source: CIETT Randstad estimates

Source: CIETT 2000

Strategy: Market enlargementStrategy: Market enlargement

Self-employed

Fixed term contracts

Private employment agencies

Spain

Italy

France

The Netherlands

Belgium

Germany

United Kingdom

52.4%

32.9%

25.0%

23.3%

22.7%

22.3%

18.5%

20.1

24.5

10.9

11.0

15.2

10.0

12.1

31.6

8.4

11.6

7.8

5.9

11.7

3.2

0.7

2.5

4.5

1.6

0.6

3.2

0.0

Strategy: Geographic spread of revenuesStrategy: Geographic spread of revenues

0%

20%

40%

60%

80%

100%

1996 1997 1998 1999 2000

The Netherlands

Europe, excl. theNetherlandsNorth America

2,701.4 3,209.5 4,223.8 5,565.4 6,168.1

7 6 1124 26

3027

272826

4449

626667

Strategy: Segmentation and focusStrategy: Segmentation and focus

Addressing the market through divisions

• Randstad

• YACHT

• Capac Inhouse Services/Hedson

Addressing the market via formulas en labels

• Randstad formulas

• Tempo-Team SME

• YACHT ICT, Finance, Management, Technology

Strategy: ICT objectivesStrategy: ICT objectives

Amplifying efficiency and raising productivity

Possibility to realize innovative service concepts

Increase scope for personalized services through staff

Strategy: ICT projectsStrategy: ICT projects

Infrastructure

Databases

Corporate data model & standards

Clients

Needs & Personalities

Attitude & behavior

Employees

Strategy: Multi-channelStrategy: Multi-channel

Serviceproviders

(Portal)

Temping

Secondment

Recruitment

Other services

Data

Outlook and forecastOutlook and forecast

• Estimated revenue growth: 5-10%

• Result H1 2001 < H1 2000

• Net effect measures clearly visible in H2 2001

• 2001: net income growth from ordinary operations > revenue growth

EUR

Earnings per ordinary share from operations

2000

1.22

%

-29

2001

1.35

Average analyst expectationsAverage analyst expectations

1999

1.72

%

11.2