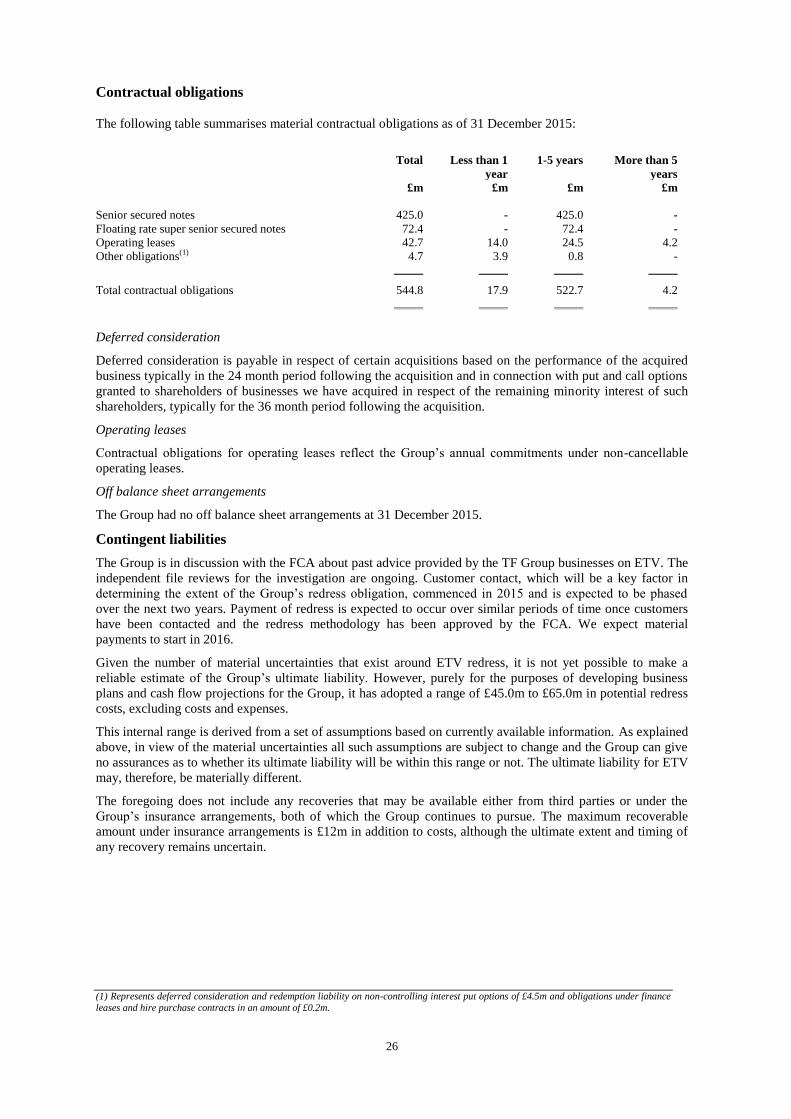

Embed Size (px)

Citation preview

Annual report For the year ended 31 December 2015

Issued: 23 March 2016

2

Table of contents Page

General 3

Recent Developments 3

Presentation of financial and other information 6

Forward looking statements 7

Summary unaudited pro forma financial information and other data 8

Business review 11

Management’s discussion and analysis of financial condition and results of operations 21

Risk factors 27

Management 32

Principal shareholders 36

Related party transactions 36

Description of share capital 36

Appendices

1. Detailed unaudited pro forma financial information and other pro forma data 38

2. Consolidated statutory information 45

3. Consolidated financial statements 48

3

General

This annual report should be read in conjunction with the audited consolidated financial statements of TIG

Finco Plc (Finco) and TIG Topco Limited (Topco) for the year ended 31 December 2015. The consolidated

financial statements can be found in appendix 3 of this report.

On 2 April 2015 the Group completed a financial restructuring in relation to the senior secured creditors and

senior unsecured creditors of Towergate Finance Plc (a former intermediate parent company of Towergate

Insurance Limited). Historical consolidated results are presented for Towergate Insurance Limited together

with its subsidiary companies, forming the predecessor group (TIL or TIL Group). As part of the Group’s

financial restructuring Finco, a newly formed holding company, acquired TIL. Topco, also a newly formed

holding company, is the indirect parent company of Finco. Sentry Holdings Limited (Sentry) is the ultimate

parent company and is the largest group in which the results will be consolidated.

This annual report presents consolidated unaudited pro forma financial information and other pro forma data

for the period ended 31 December 2015 for Finco and Topco and its subsidiary companies, together with the

results of TIL and its subsidiary companies for the period prior to 2 April 2015 (together, Towergate or

Group). For comparative purposes, the results of TIL and its subsidiary companies have been used for the

years ended 31 December 2014 and 31 December 2013. Unless otherwise stated the results and financial

position of Finco and Topco are the same.

This annual report has been prepared under International Financial Reporting Standards as adopted by the

European Union (IFRSs as adopted by the EU).

Recent developments

The following items have been noted as updates to ongoing matters or items to bring to the attention of the

reader:

Continued discussions with the Financial Conduct Authority (FCA) in relation to client money and advice provided by the Towergate Financial (TF) business

Acquisitions and disposals Group financial restructuring Impairment Senior management changes Financial review Post balance sheet events

FCA

During Q3 2013 the Group identified that £15.0 million (m) of client and insurer monies had been

misallocated to an unrestricted account between November 2007 and January 2011. As soon as the

misallocation was confirmed management transferred £15.0m to the relevant client and insurer accounts. The

FCA was notified.

The Group is continuing discussions with the FCA in connection with past advice provided by the Towergate

Financial business on pension Enhanced Transfer Values (ETV) and Unregulated Collective Investment

Schemes (UCIS).

During the year £19.8m has now been recognised as management’s best estimate of future obligations to pay

UCIS redress costs. Further information is provided within the provisions and contingent liabilities discussion

on page 26.

Acquisitions and disposals

No acquisitions were made during the year ended 31 December 2015. During the year TIL disposed of three

businesses, of which two were small portfolios. On 16 March 2015 TIL disposed of its Towergate Financial

business to Palatine Private Equity for a gross consideration of £8.6m. TF was a provider of independent

financial and mortgage advice and operated outside the Group’s core UK specialist personal lines and SME

markets. Provisions and contingent liabilities in respect of ETV and UCIS were not transferred to Palatine

Private Equity and remain with the Group.

4

Group financial restructuring

On 2 April 2015 the Group completed a financial restructuring in relation to the senior secured creditors and

senior unsecured creditors of Towergate Finance Plc (a former intermediate parent company of TIL). As part

of these arrangements, Finco acquired TIL for the consideration of £735.0m. This was made up of the issue of

£425.0m of senior secured notes by Finco and the issue of new shares in Finco’s indirect parent company,

Topco, valued at £310.0m.

As a result of these arrangements, on 2 April 2015 funds controlled or managed by Highbridge Principal

Strategies LLC (Highbridge) became the Group’s majority shareholder.

As part of the financial restructuring, additional capital of £122.0m was received by the Group through the

issue by Topco of new shares for £50.0m and the issue by Finco of £75.0m of super senior secured notes at a

discount of £3.0m.

The additional funds provided liquidity to the Group and have enabled it to fund the costs of the restructuring

of £40.9m, the vesting of long term incentive plans which have crystallised or will in the future crystallise as a

result of the restructuring of £30.5m, retention bonuses of £8.0m and minority interest buy outs of £1.6m.

Impairment

International accounting standards require that a full impairment review of goodwill is performed annually.

The carrying value of goodwill at 31 December 2015 has been assessed based on its value in use. This has

resulted in an impairment of £86.4m which has been recognised in the consolidated statement of

comprehensive income. The impairment arises as a result of a fall in expected future cash flows from the Small

Business Unit (SBU) in Manchester which forms part of the Retail segment.

Senior management changes

There have been a number of senior management changes since 1 January 2015 including:

Alastair Lyons resigned from his role as Non-Executive Chairman as of 29 June 2015.

John Tiner was appointed as Non-Executive Chairman with effect from 29 June 2015.

It was announced that Pat Butler would be joining as Non-Executive Director on 22 February 2016.

Scott Egan changed his role from Chief Financial Officer to Interim Chief Executive Officer on 10

February 2015. He resigned from this position as of 14 September 2015.

David Ross joined Towergate on 2 November 2015 as Chief Executive Officer.

Mark Mugge was appointed as Chief Operating Officer on 26 February 2015. He subsequently accepted

the position of Chief Financial Officer with effect from 6 July 2015. Mark continued with his

responsibilities as Chief Operating Officer until Adrian Brown joined on 14 September 2015.

Oliver Corbett was appointed Interim Chief Financial Officer on 10 March 2015 and resigned from this

role on 31 July 2015.

Adrian Brown joined Towergate on 14 September 2015 as Interim Chief Executive Officer. Following the

appointment of David Ross, Adrian was appointed as Chief Operating Officer and Chief Executive Officer

for Underwriting.

Janice Deakin joined as Chief Executive Officer of Insurance Broking on 12 August 2015.

Steve Wood was appointed as Chief Executive Officer of Paymentshield with effect from 16 March 2015.

Clive Nathan resigned from his position as Chief Executive Officer for Underwriting as of 30 October

2015.

Mike Lawton resigned from his position as Chief Executive Officer for Broking as of 9 October 2015.

James Tugendhat was appointed Chief Commercial Officer with effect from 15 October 2015 and has since

resigned with effect from 1 April 2016.

Keith Jackson resigned from his role as Chief Risk Officer with effect from 31 August 2015.

Sarah Dalgarno joined as Strategic Risk Officer on 4 September 2015.

Jill Lucas departed from her role as Group Chief Information Officer with effect from 31 December 2015.

Gordon Walters was appointed as Interim Group Chief Information Officer on 14 August 2015, a role he

was appointed to on a permanent basis from 31 January 2016.

Carole Jones resigned from her role as Interim Group HR Director with effect from 31 July 2015.

Steve Pratt was appointed Interim Group HR Director with effect from 1 August 2015, pending the arrival

of Catherine Lynch, who arrived on 9 November 2015.

Catherine Lynch was appointed Group HR Director with effect from 9 November 2015.

Jennifer Owens resigned from her role as of General Counsel with effect from 29 February 2016.

Geoff Gouriet was appointed as General Counsel with effect from 1 March 2016.

5

Financial review

Despite the challenges faced during 2015, Towergate remains the UK’s largest independent insurance broking

platform, the largest SME focused UK broker and largest underwriting managing general agent that continues

to serve over two million customers.

We go into 2016 with the entire new Executive team in place, plus new senior hires in key leadership roles to

support the business turnaround. Towergate is focused on creating the UK’s most trusted and recommended

adviser, leveraging a fully integrated operating infrastructure underpinned by the right control and conduct

framework.

Post balance sheet events

Additional funding

During Q1 2016 Towergate secured two sources of additional funding totalling up to £65m from Highbridge

Principal Strategies LLP (Highbridge). Binding heads of terms have been signed for both of these transactions.

Details are as follows:

• Disposal of the entire issued share capital of The Broker Network Limited and Countrywide Insurance

Management Limited, both wholly owned subsidiaries of the Group, and the assets of Broker Network

Underwriting, a trading style of Towergate Underwriting Group Limited. The consideration for the

acquisition shall be satisfied in part by the allotment to Towergate of approximately 19.9% of the shares

(subject to adjustment) in the acquisition vehicle; and;

• A five year facility from Highbridge secured by certain legacy assets of the Group.

Both initiatives remain subject to appropriate consents and / or approvals and will result in a cash injection to

the Group.

In addition to the above, the Towergate secured a short term loan facility from Highbridge for an amount of up

to £28m which will result in a cash injection to the Group if it is drawn.

Proceeds from these initiatives will be largely applied towards an acceleration of the strategic investments in

the group transformation plan.

IT Transformation

During February 2016 the Group signed a contract with Accenture under which Accenture will become the

Group’s information technology (IT) strategic partner, overseeing its IT Transformation change program.

Under the contract Accenture will also manage service support across the whole IT Infrastructure estate for a

period of five years. The Group is currently undertaking a number of major change programs designed to

improve efficiency across the business, to build regulatory resilience, to position the Group to exploit future

scale advantages and to enhance the customer proposition.

6

Presentation of financial and other information

This annual report is prepared by the Group in connection with the indentures relating to the £425.0m senior

secured notes and £75.0m floating rate super senior secured notes (together the Notes) issued by Finco on 2

April 2015 and the shareholders’ deed relating to Topco and the Group dated 2 April 2015.

In accordance with guidance issued by the Institute of Chartered Accountants in England and Wales, the

independent auditor’s report in the consolidated financial statements for Finco and Topco (together, the

Companies) state that: they were made solely to the members of Finco and Topco as a body in accordance with

Chapter 3 of Part 16 of the UK Companies Act 2006; the independent auditor’s work was undertaken so that

the independent auditor might state to the members of Finco and Topco those matters that were required to be

stated to them in an auditor’s report and for no other purpose; and, to the fullest extent permitted by law, the

independent auditor does not accept or assume responsibility to anyone other than the Companies and their

members as a body for its audit work or the opinions it has formed. The independent auditor’s reports for the

Companies for the period ended 31 December 2015 was unqualified. KPMG LLP was the auditor of the

Companies for the accounting period ended 31 December 2015.

Investors in the Notes should understand that in making these statements, the independent auditor confirmed

that it does not accept or assume any liability to parties (such as the purchasers of the Notes) other than to the

Companies and their members as a body with respect to the report and to the independent auditor’s audit work

and opinions. The US Securities and Exchange Commission would not permit such limiting language to be

included in a registration statement or a prospectus used in connection with an offering of securities registered

under the US Securities Act or in a report filed under the US Exchange Act. If a US court (or any other court)

were to give effect to such limiting language, the recourse that investors in the Notes may have against the

independent auditor based on its report or the consolidated financial statements to which it relates could be

limited.

The consolidated financial statements of the Group have been prepared in accordance with IFRS’s as adopted

by the EU.

On 2 April 2015 the group completed a financial restructuring in relation to the senior secured creditors and

senior unsecured creditors of Towergate Finance Plc (a former intermediate parent company of TIL). The

unaudited financial information has been presented in this annual report on a pro forma basis as if this group

structure had been in place form 1 January 2015. However in the financial statements of Finco and Topco the

transaction has been presented as an acquisition of the TIL group and accounted for in accordance with IFRS3

Business Combinations.

The unaudited financial information of the Group presented in this annual report and discussed in the

management’s discussion and analysis of financial condition and results of operations has been prepared on a

pro forma basis in order to present a two-year financial track record. Adjustments have therefore been made in

respect of:

Subtraction of the results of disposed businesses:

o Hayward Aviation Limited for the period 1 January 2013 to 23 December 2014.

o Folgate Insurance Company Ltd (FICL) for the period 1 January 2013 to 29 August 2014.

o TF for the period 1 January 2014 to 16 March 2015.

Addition of the trading results of TIL for the period 1 January 2013 to 1 April 2015.

Inclusion of the new debt structure for the period 1 January 2013 to 1 April 2015.

Certain data contained in these financial results, including financial information, have been subject to rounding

adjustments. Accordingly, in certain instances, the sum of the numbers in a column or a row in tables may not

conform exactly to the total figure given for that column or row.

These financial results include certain financial measures and ratios, including EBITDA, Adjusted EBITDA,

Adjusted EBITDA margin and certain leverage and coverage ratios that are not presented in accordance with

IFRS.

EBITDA

In these financial results, references to EBITDA are to profit / (loss) on ordinary activities before interest

payable and similar charges, tax, depreciation and amortisation of intangibles. Accordingly, EBITDA can

be extracted from the consolidated financial statements of Finco, Topco and TIL by taking profit / (loss) on

ordinary activities and adding back interest payable and similar charges, tax, depreciation and amortisation

of intangibles.

7

Adjusted EBITDA

References to Adjusted EBITDA for Finco, Topco and TIL represent EBITDA as adjusted for acquisition

and financing costs, group reorganisation costs, regulatory costs, loss on disposal of business, asset write-

downs in connection with business restructuring, long term incentive plan charges, business investment

costs and acquisition costs.

EBITDA-based measures

EBITDA-based measures are not presented as measures of the results of operations. EBITDA-based

measures have important limitations as an analytical tool, and should not be considered in isolation or as

substitutes for analysis of the Group’s results of operations. Management believes that the presentation of

EBITDA-based measures is helpful to investors as a measure of the operating performance and ability to

service debt. EBITDA-based measures may not be comparable to similarly titled measures used by other

companies.

EBITDA, Adjusted EBITDA, Adjusted EBITDA margin and leverage and coverage ratios are not

measurements of financial performance under IFRS and should not be considered as alternatives to other

indicators of the Group’s operating performance, cash flows or any other measure of performance derived in

accordance with IFRS.

The discussion includes forward looking statements, which, although based on assumptions that are considered

reasonable, are subject to risks and uncertainties which could cause actual events or conditions to differ

materially from those expressed or implied herein. Undue reliance cannot be placed on these forward looking

statements. These forward looking statements are made as of the date of this report and are not intended to

give any assurance as to future results.

Segmental analysis is presented in this financial information. From time to time structural changes are made

within the business and trading businesses may move between the reported segments. When this occurs

financial information is restated in respect of the corresponding prior year period to facilitate the discussion

and analysis of the results.

Forward looking statements

This report contains statements under the caption management’s discussion and analysis of financial condition

and results of operations, and in other sections that are, or may be deemed to be, forward-looking statements.

In some cases, these forward-looking statements can be identified by the use of forward-looking terminology,

including the words “aims”, “believes”, “estimates”, “anticipates”, “expects”, “intends”, “may”, “will”,

“plans”, “predicts”, “assumes”, “shall”, “continue” or “should” or, in each case, their negative or other

variations or comparable terminology or by discussions of strategies, plans, objectives, targets, goals, future

events or intentions.

Many factors may cause the Group’s operations, financial condition, liquidity and the development of the

industries in which it operates to differ materially from those expressed or implied by the forward-looking

statements contained in this annual report. The Group treats these as risks to its objectives, as discussed in the

Risk factors section of this annual report. The Group takes a systematic approach to the management of risks,

as described in the Risk management section on page 16.

Any forward-looking statements are only made as of the date of this report, and the Group does not intend, and

does not assume any obligation, to update forward-looking statements set forth in this report. Readers of this

document should interpret all subsequent written or oral forward-looking statements attributable to the Group

or to persons acting on its behalf as being qualified by the cautionary statements in this report. As a result,

readers of this document should not place undue reliance on these forward-looking statements.

8

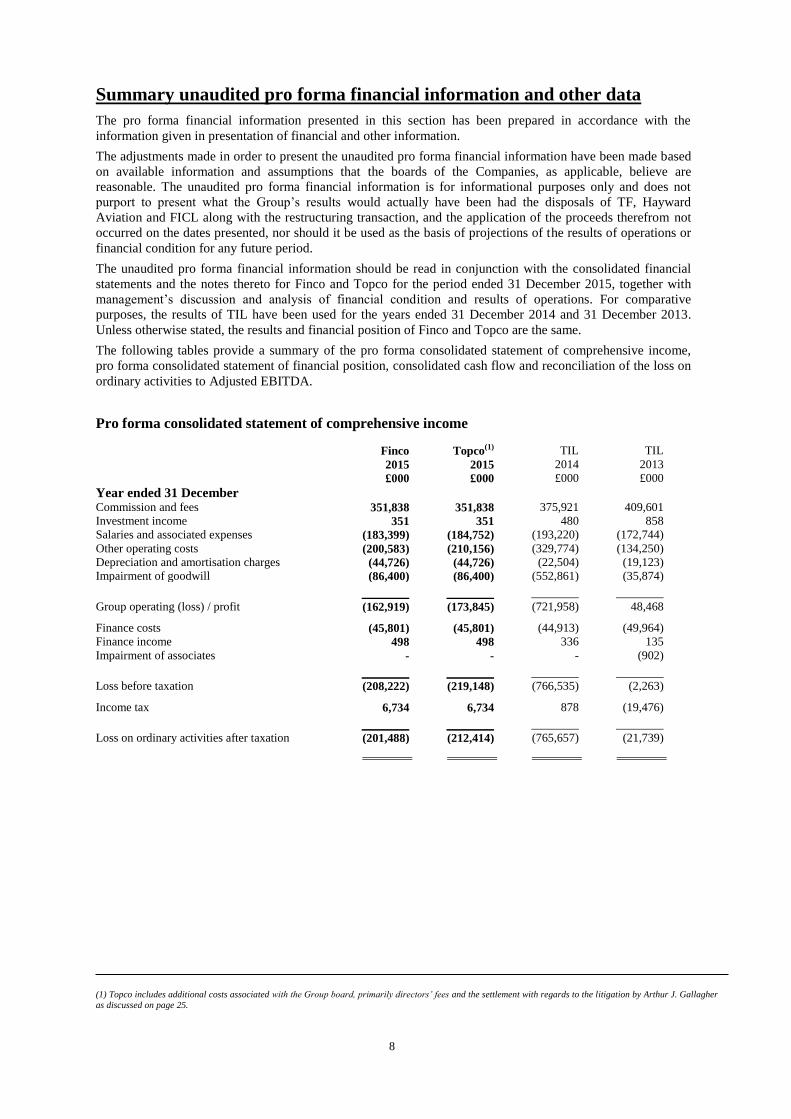

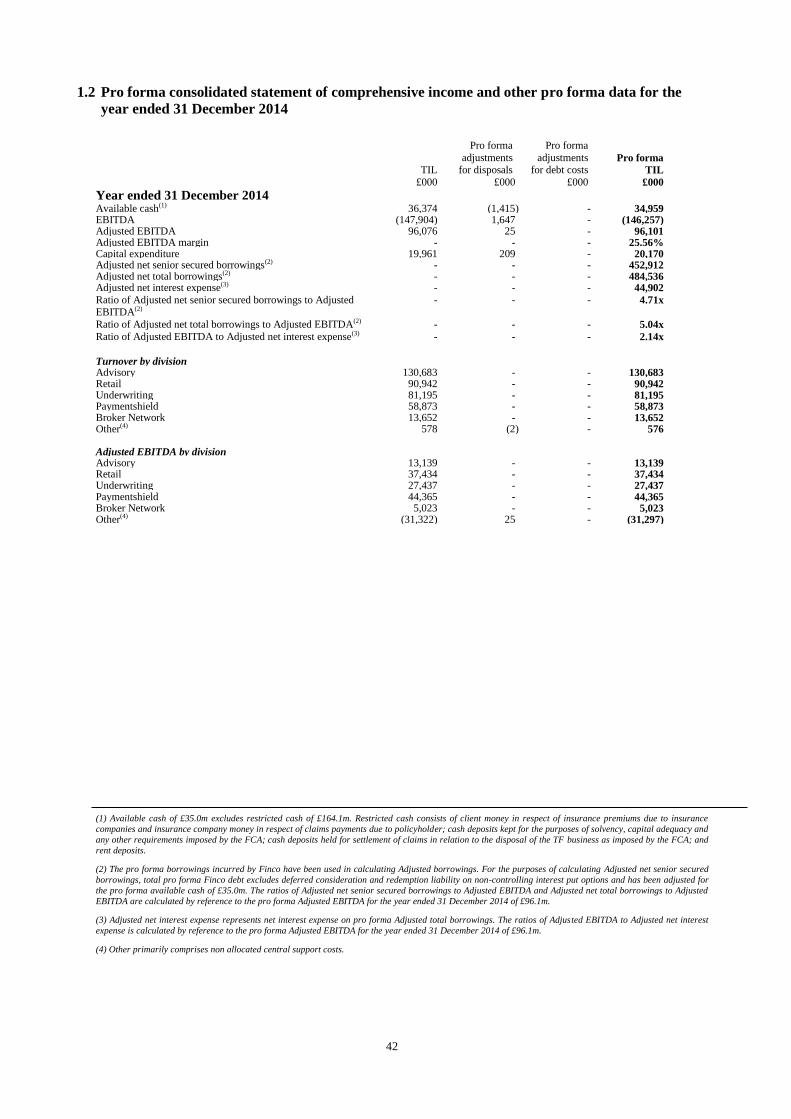

Summary unaudited pro forma financial information and other data

The pro forma financial information presented in this section has been prepared in accordance with the

information given in presentation of financial and other information.

The adjustments made in order to present the unaudited pro forma financial information have been made based

on available information and assumptions that the boards of the Companies, as applicable, believe are

reasonable. The unaudited pro forma financial information is for informational purposes only and does not

purport to present what the Group’s results would actually have been had the disposals of TF, Hayward

Aviation and FICL along with the restructuring transaction, and the application of the proceeds therefrom not

occurred on the dates presented, nor should it be used as the basis of projections of the results of operations or

financial condition for any future period.

The unaudited pro forma financial information should be read in conjunction with the consolidated financial

statements and the notes thereto for Finco and Topco for the period ended 31 December 2015, together with

management’s discussion and analysis of financial condition and results of operations. For comparative

purposes, the results of TIL have been used for the years ended 31 December 2014 and 31 December 2013.

Unless otherwise stated, the results and financial position of Finco and Topco are the same.

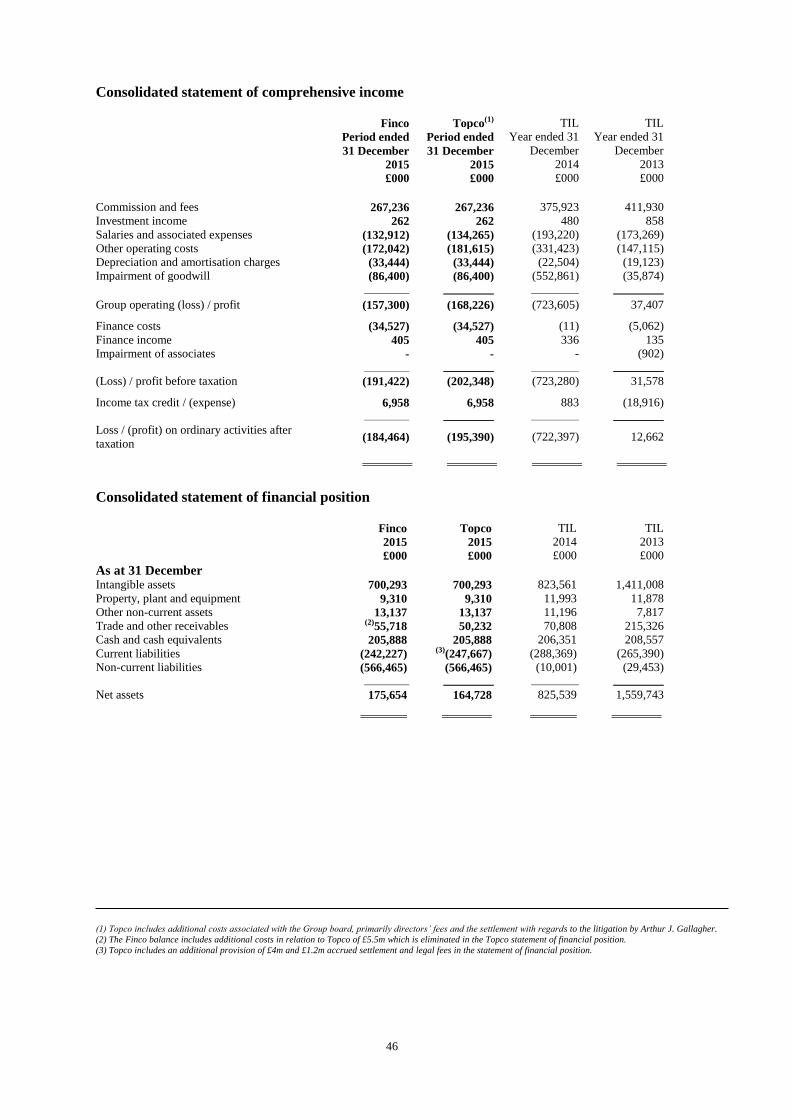

The following tables provide a summary of the pro forma consolidated statement of comprehensive income,

pro forma consolidated statement of financial position, consolidated cash flow and reconciliation of the loss on

ordinary activities to Adjusted EBITDA.

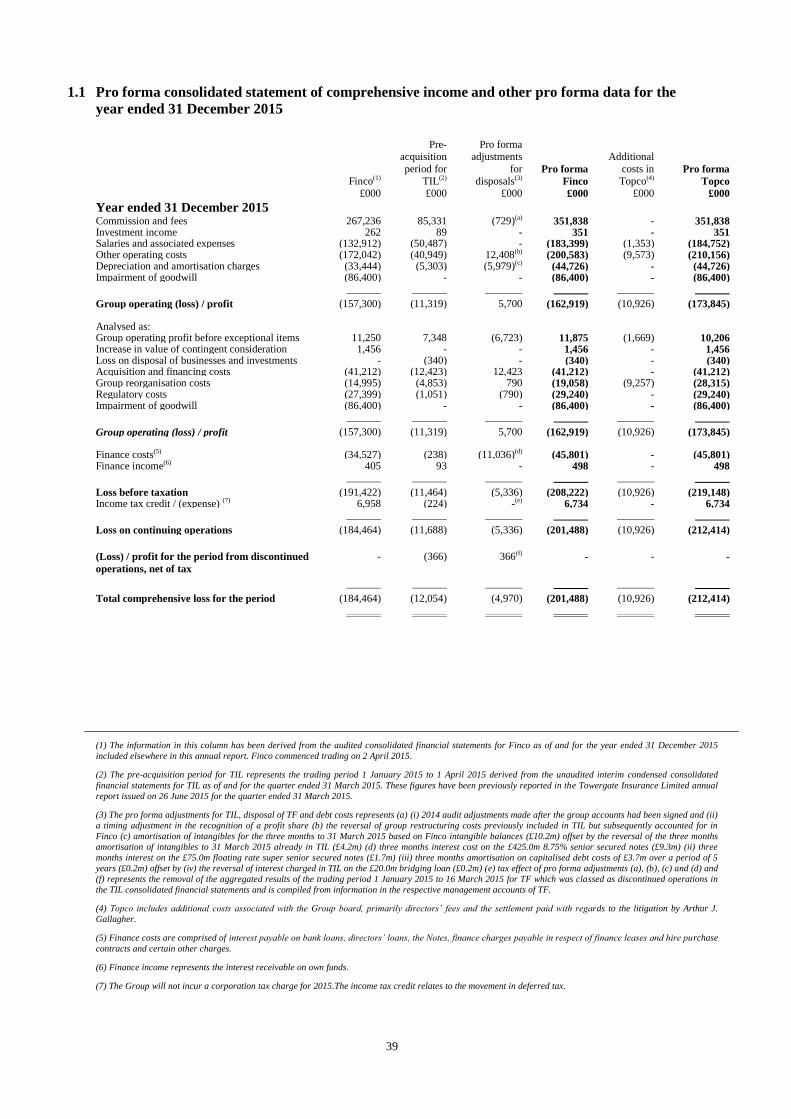

Pro forma consolidated statement of comprehensive income

Finco Topco(1) TIL TIL

2015 2015 2014 2013

£000 £000 £000 £000

Year ended 31 December

Commission and fees 351,838 351,838 375,921 409,601

Investment income 351 351 480 858

Salaries and associated expenses (183,399) (184,752) (193,220) (172,744)

Other operating costs (200,583) (210,156) (329,774) (134,250)

Depreciation and amortisation charges (44,726) (44,726) (22,504) (19,123)

Impairment of goodwill (86,400) (86,400) (552,861) (35,874)

Group operating (loss) / profit (162,919) (173,845) (721,958) 48,468

Finance costs (45,801) (45,801) (44,913) (49,964)

Finance income 498 498 336 135

Impairment of associates - - - (902)

Loss before taxation (208,222) (219,148) (766,535) (2,263)

Income tax 6,734 6,734 878 (19,476)

Loss on ordinary activities after taxation (201,488) (212,414) (765,657) (21,739)

(1) Topco includes additional costs associated with the Group board, primarily directors’ fees and the settlement with regards to the litigation by Arthur J. Gallagher

as discussed on page 25.

9

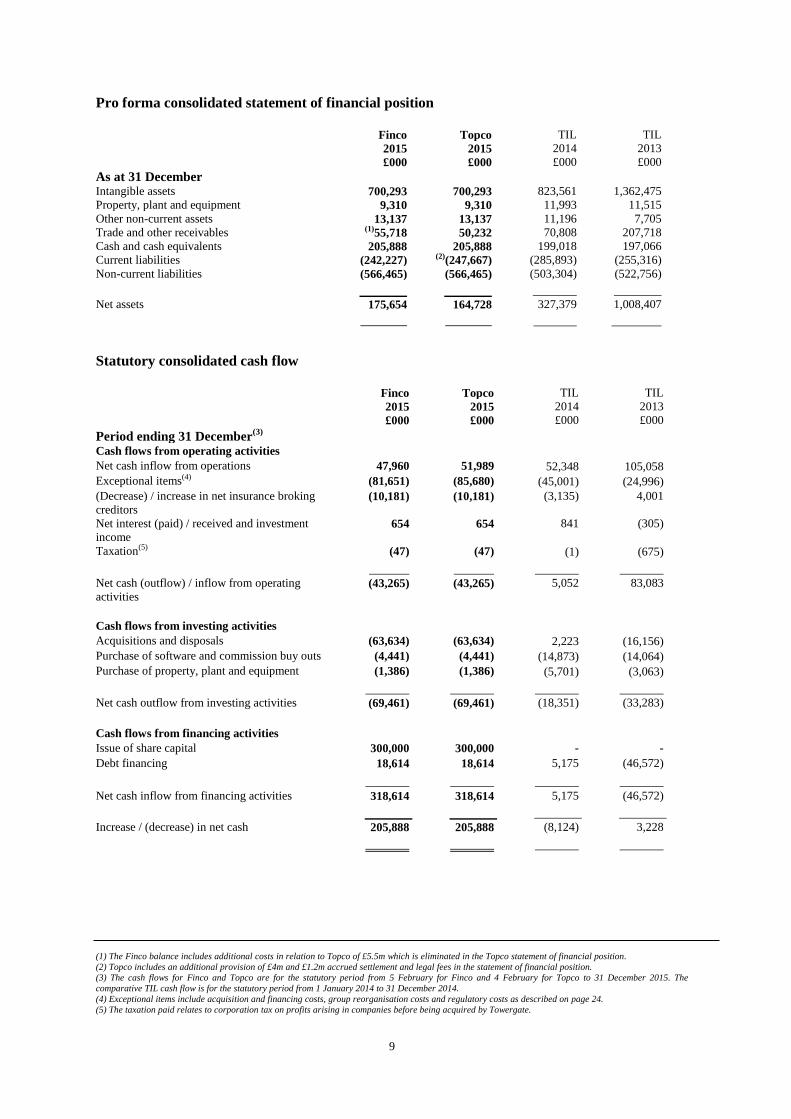

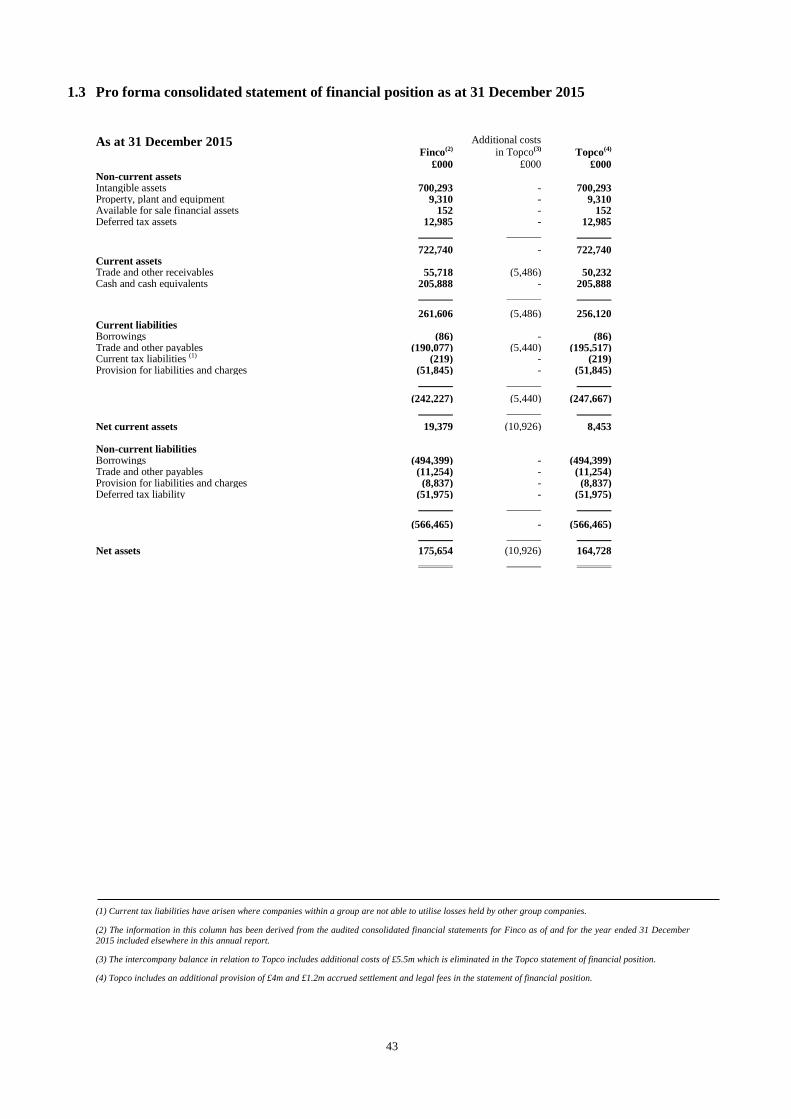

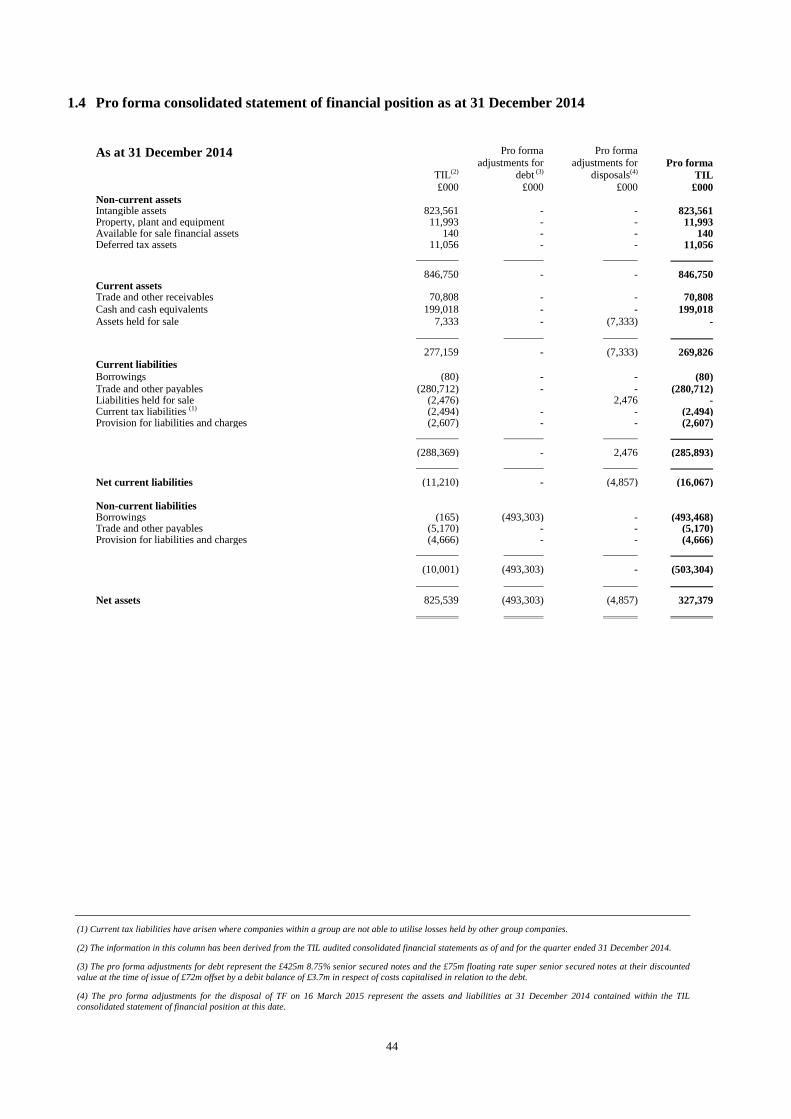

Pro forma consolidated statement of financial position

Finco Topco TIL TIL

2015 2015 2014 2013

£000 £000 £000 £000

As at 31 December

Intangible assets 700,293 700,293 823,561 1,362,475

Property, plant and equipment 9,310 9,310 11,993 11,515

Other non-current assets 13,137 13,137 11,196 7,705

Trade and other receivables (1)55,718 50,232 70,808 207,718

Cash and cash equivalents 205,888 205,888 199,018 197,066

Current liabilities (242,227) (2)(247,667) (285,893) (255,316)

Non-current liabilities (566,465) (566,465) (503,304) (522,756)

Net assets 175,654 164,728 327,379 1,008,407

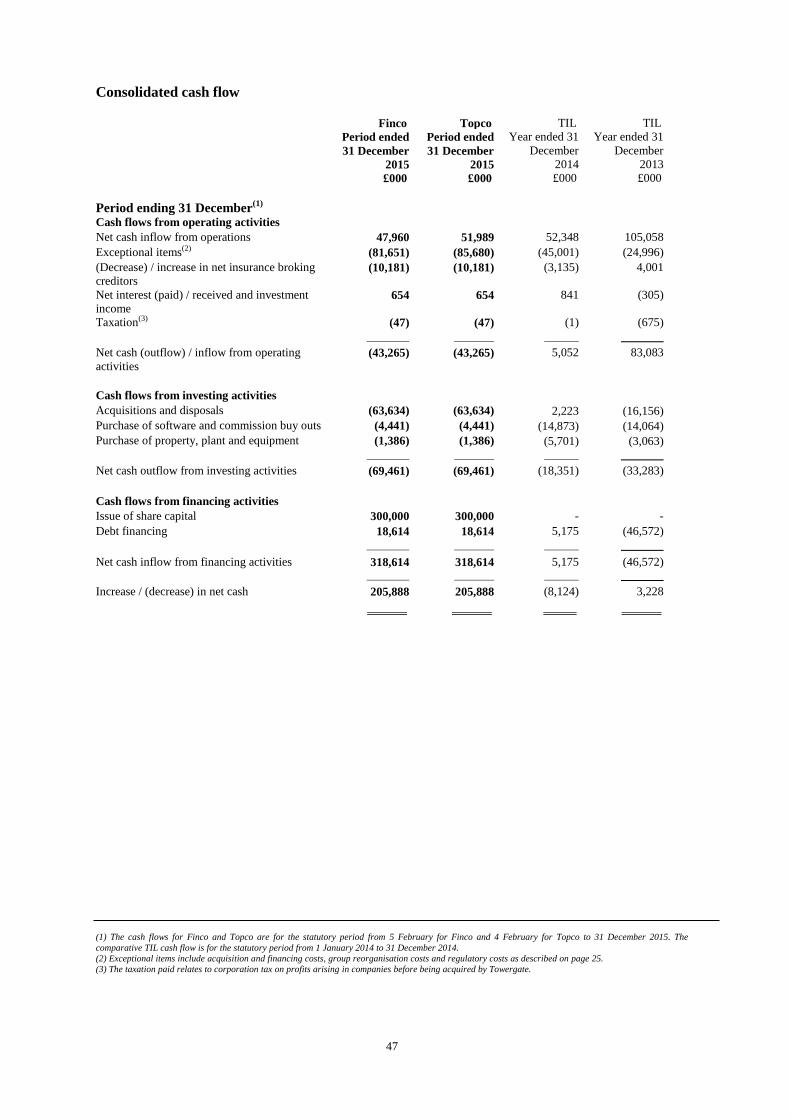

Statutory consolidated cash flow

Finco Topco TIL TIL

2015 2015 2014 2013

£000 £000 £000 £000

Period ending 31 December(3)

Cash flows from operating activities

Net cash inflow from operations 47,960 51,989 52,348 105,058

Exceptional items(4) (81,651) (85,680) (45,001) (24,996)

(Decrease) / increase in net insurance broking

creditors (10,181) (10,181) (3,135) 4,001

Net interest (paid) / received and investment

income 654 654 841 (305)

Taxation(5) (47) (47) (1) (675)

Net cash (outflow) / inflow from operating

activities (43,265) (43,265) 5,052 83,083

Cash flows from investing activities

Acquisitions and disposals (63,634) (63,634) 2,223 (16,156)

Purchase of software and commission buy outs (4,441) (4,441) (14,873) (14,064)

Purchase of property, plant and equipment (1,386) (1,386) (5,701) (3,063)

Net cash outflow from investing activities (69,461) (69,461) (18,351) (33,283)

Cash flows from financing activities

Issue of share capital 300,000 300,000 - -

Debt financing 18,614 18,614 5,175 (46,572)

Net cash inflow from financing activities 318,614 318,614 5,175 (46,572)

Increase / (decrease) in net cash 205,888 205,888 (8,124) 3,228

(1) The Finco balance includes additional costs in relation to Topco of £5.5m which is eliminated in the Topco statement of financial position.

(2) Topco includes an additional provision of £4m and £1.2m accrued settlement and legal fees in the statement of financial position.

(3) The cash flows for Finco and Topco are for the statutory period from 5 February for Finco and 4 February for Topco to 31 December 2015. The

comparative TIL cash flow is for the statutory period from 1 January 2014 to 31 December 2014.

(4) Exceptional items include acquisition and financing costs, group reorganisation costs and regulatory costs as described on page 24.

(5) The taxation paid relates to corporation tax on profits arising in companies before being acquired by Towergate.

10

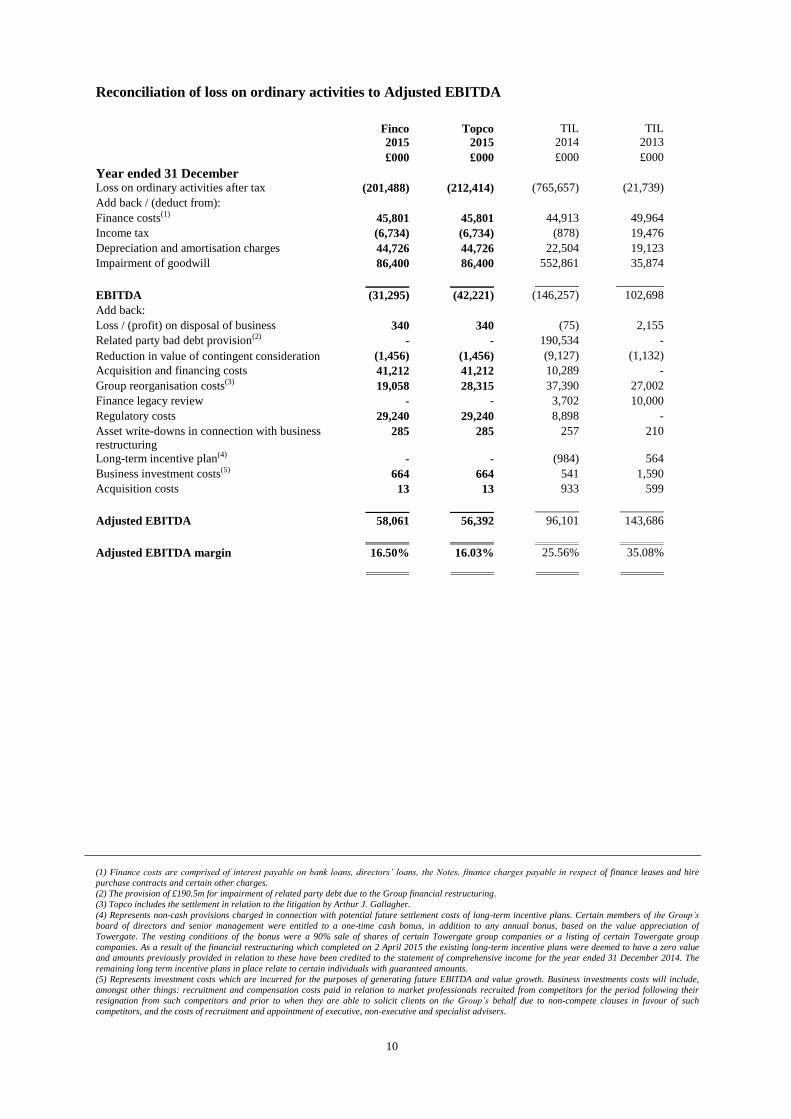

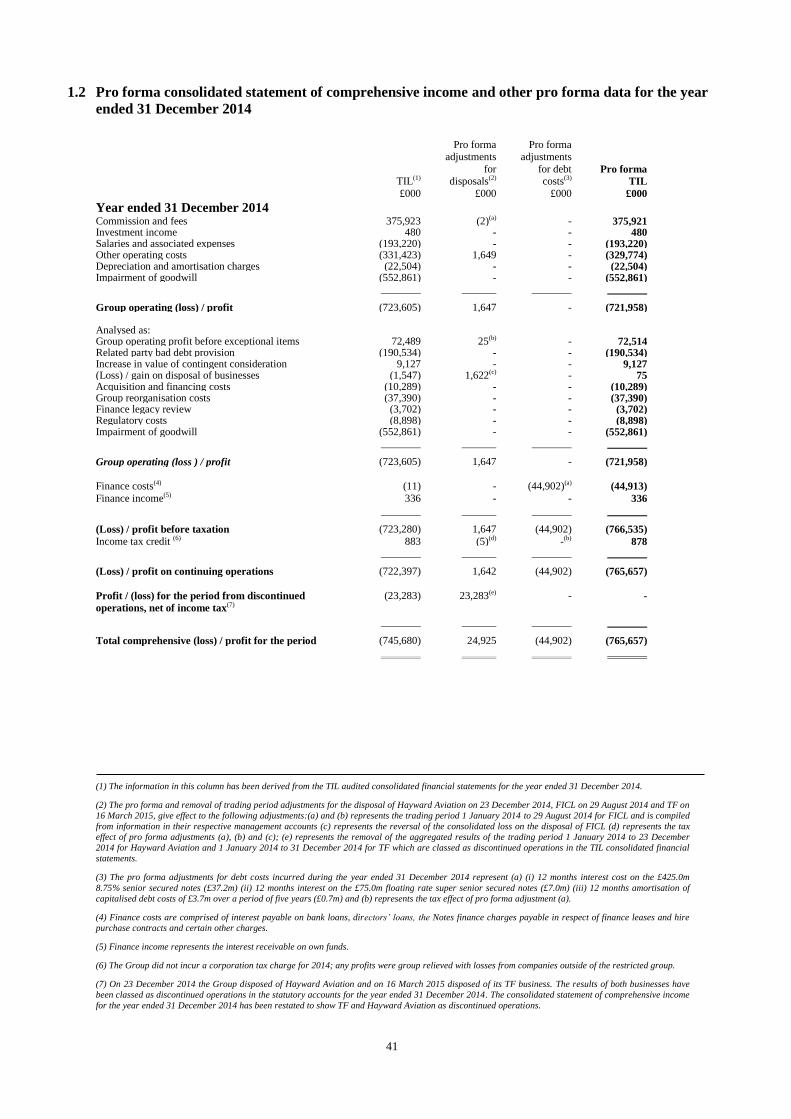

Reconciliation of loss on ordinary activities to Adjusted EBITDA

Finco Topco TIL TIL

2015 2015 2014 2013

£000 £000 £000 £000

Year ended 31 December

Loss on ordinary activities after tax (201,488) (212,414) (765,657) (21,739)

Add back / (deduct from):

Finance costs(1) 45,801 45,801 44,913 49,964

Income tax (6,734) (6,734) (878) 19,476

Depreciation and amortisation charges 44,726 44,726 22,504 19,123

Impairment of goodwill 86,400 86,400 552,861 35,874

EBITDA (31,295) (42,221) (146,257) 102,698

Add back:

Loss / (profit) on disposal of business 340 340 (75) 2,155

Related party bad debt provision(2) - - 190,534 -

Reduction in value of contingent consideration (1,456) (1,456) (9,127) (1,132)

Acquisition and financing costs 41,212 41,212 10,289 -

Group reorganisation costs(3) 19,058 28,315 37,390 27,002

Finance legacy review - - 3,702 10,000

Regulatory costs 29,240 29,240 8,898 -

Asset write-downs in connection with business

restructuring 285 285 257 210

Long-term incentive plan(4) - - (984) 564

Business investment costs(5) 664 664 541 1,590

Acquisition costs 13 13 933 599

Adjusted EBITDA 58,061 56,392 96,101 143,686

Adjusted EBITDA margin 16.50% 16.03% 25.56% 35.08%

(1) Finance costs are comprised of interest payable on bank loans, directors’ loans, the Notes, finance charges payable in respect of finance leases and hire

purchase contracts and certain other charges.

(2) The provision of £190.5m for impairment of related party debt due to the Group financial restructuring.

(3) Topco includes the settlement in relation to the litigation by Arthur J. Gallagher.

(4) Represents non-cash provisions charged in connection with potential future settlement costs of long-term incentive plans. Certain members of the Group’s

board of directors and senior management were entitled to a one-time cash bonus, in addition to any annual bonus, based on the value appreciation of

Towergate. The vesting conditions of the bonus were a 90% sale of shares of certain Towergate group companies or a listing of certain Towergate group

companies. As a result of the financial restructuring which completed on 2 April 2015 the existing long-term incentive plans were deemed to have a zero value

and amounts previously provided in relation to these have been credited to the statement of comprehensive income for the year ended 31 December 2014. The

remaining long term incentive plans in place relate to certain individuals with guaranteed amounts.

(5) Represents investment costs which are incurred for the purposes of generating future EBITDA and value growth. Business investments costs will include,

amongst other things: recruitment and compensation costs paid in relation to market professionals recruited from competitors for the period following their

resignation from such competitors and prior to when they are able to solicit clients on the Group’s behalf due to non-compete clauses in favour of such

competitors, and the costs of recruitment and appointment of executive, non-executive and specialist advisers.

11

Business review

Overview of Towergate

Towergate is a leading independently-owned insurance intermediary group distributing general insurance

products in the UK. In 2015 it distributed insurance products with an aggregated value (in terms of gross

written premiums) of approximately £2.9 billion. Towergate is not an underwriting business and does not

assume insurance risk in relation to the products it distributes. Its business model and capital requirements

reflect the agency (as opposed to principal) nature of its activities.

Insurance products are distributed through Group and third party brokers as well as mortgage intermediaries.

Towergate’s end customers are primarily retail consumers and small and medium sized enterprises (SMEs).

The Group also provides services to members of its broker network. Historically Towergate has been an

acquisition-led business and since 1997 has acquired nearly 300 broking and underwriting agency businesses

however no acquisitions were made during the year ended 31 December 2015.

Towergate has five operating divisions or segments as follows:

Advisory: the Advisory division distributes personal lines and SME-focused products via 81 advisory offices

located across the UK. Brokers place the insurance policies of customers through underwriting agencies or

directly with insurance carriers depending on customer needs.

Historically, a part of Advisory offered regulated and unregulated financial advisory services to corporate and

private clients across the UK under the brand name Towergate Financial. The Towergate Financial business

was sold by the Group to Palatine Private Equity on 16 March 2015 and the Group ceased to offer these

services on that date although liabilities in relation to past sales remain with the Group.

Retail (previously known as Direct): the Retail division distributes insurance products to specialist customer

segments ranging from military personnel and high net worth individuals to caravan owners. Services are

provided to multiple niche retail markets, as well as to SME businesses including members of the Federation

of Small Businesses. The division operates from eight locations in the UK.

Underwriting: the Underwriting division provides insurance products to Group businesses and around 3,000

third party insurance brokers who in turn act on behalf of insured customers. The division prices insurance

coverage, issues insurance policies and in most cases handles insurance claims on behalf of the underlying

insurance companies on whose behalf it is acting. Insurance companies (and not Towergate) are ultimately

responsible for insurance claim costs and thus carry the associated principal risk. There are over 200 insurance

products within the Underwriting division covering a wide variety of risks. As in the Advisory and Retail

divisions, these insurance products are aimed both at personal lines customers and the SME marketplace. The

division has offices in 15 locations across the UK.

Paymentshield: Paymentshield is one of the UK’s leading providers of general insurance products to the

mortgage intermediary market. It is focused on the supply of household-related insurance products such as

buildings and contents, mortgage payment protection (MPPI), income protection and landlord insurance

products. Paymentshield’s principal route to market is the mortgage broking channel, where its relationships

include two of the UK’s largest mortgage networks as well as independent financial advisers and estate agents.

It also distributes a small amount of business direct to retail customers. As with the Advisory, Retail and

Underwriting businesses, underwriting or principal risk is carried by insurance partners.

Broker Network: the Broker Network division is the largest and longest established full service general

insurance network for insurance brokers in the UK. The Broker Network division provides community based,

independent insurance brokers with access to insurance products and a variety of business support services.

Members typically receive enhanced commission rates negotiated by the Broker Network. The business

support services provided to members assist them in managing their business and range from client money

under the FCA CASS rules, compliance services and advice, HR support, marketing, web design, e-trade

products and access to restricted markets.

Central: The Central division provides core support to the rest of the business divisions. It is made up of nine

functions: IT; Property; Finance, including IBA; Internal Audit; Human Resources; Legal; Compliance and

Risk; Communications; Executive costs. All costs are monitored centrally and are fully allocated out to the

businesses using various methodologies.

12

Strategy

The strategic focus concentrates on the remediation and streamlining of the back office support functions and

IT systems, with continued focus on revenue generation.

No acquisitions are currently planned for 2016.

Towergate’s key strengths include:

Its market position in a profitable industry: Towergate is one of the largest specialist personal lines and SME-

focused intermediary and insurance managing general agent in the UK. Towergate’s core proposition of strong

distribution and underwriting excellence offers compelling value for both consumers and insurers.

Its knowledge base and expertise in a highly regulated industry: insurance distribution is a regulated activity

in the UK. The Financial Conduct Authority (FCA) is the Group’s principal regulator. The intensity and

complexity of regulation is growing, providing a competitive advantage for large and well-resourced market

participants.

Demand for the insurance products it distributes is linked to economic activity: the continued improvement

in the economic performance of the UK is likely to present Towergate with opportunities for growth.

The strength of its financial characteristics and business model: the Group generates attractive operating

margins. It has the potential to be highly cash generative.

Significant organisational change is well progressed: Restructuring and operational changes in the

Manchester unit were completed by the end of 2015. Full integration into the Retail SME business will take

place as we move into 2016, as well as continued streamlining of the IT and Finance centres of excellence and

focus on cost efficiencies.

Towergate has an experienced management team: We go into 2016 with the entire new Executive team in

place, supported by a further 26 key new hires that strengthen the leadership of all areas of the business.

Support staff attrition levels are reducing and retention of key client-facing staff is high.

Disposal of non-core businesses: the disposal of non-core businesses has enabled the Group to improve its

strategic focus.

Advisory

Overview

The Advisory business places the insurance requirements of commercial and individual customers with

insurers. As part of the service, Towergate brokers offer advice on insurance needs and risk management to

customers and negotiate competitive policy terms with insurance companies on their behalf. Advisory also

offers customers access to certain third-party products and services such as premium financing arrangements

for the payment of premium by instalments, legal expenses insurance and claims assistance. With 81 broking

offices located across the UK, Advisory offers a local service with access to expert advice, risk management

and a wide selection of insurance products.

Products

The Advisory business offers a wide variety of specialist and non-specialist commercial and personal lines

products, including over 200 products available from the Underwriting division.

The Advisory business has offices throughout the United Kingdom. The national coverage is an advantage in

the preferred SME market, in which customers appreciate local contact and service. The (as it was then called)

Insurance Broking business set up a specialist unit in Manchester to service small premium business through a

dedicated contact centre with extended opening times. This has caused material disruption to the business.

Advisory distributes all types of personal lines business but has particular expertise in specialist lines such as

non-standard household, motor, caravans and park homes, and yachts and pleasure craft.

Competition

The Advisory business operates in a highly competitive market in which numerous national and local broking

firms actively compete for customers. Differentiation in the Advisory business is based on knowledge of our

customer’s needs, product breadth, innovation, quality of service and price. Some of the largest retail broker

competitors are Aon, Marsh, Willis, Arthur J Gallagher and Bluefin. In addition there is competition from

insurance companies that solicit customers directly without the assistance of a broker and with insurance

companies that have their own broker distribution capacity such as AXA, which controls Bluefin.

13

Retail

Overview

Retail is one of the leading providers of specialist personal lines and small business insurance in the UK. It

serves distinct communities such as caravan owners with products tailored to their needs and distributes via

both telephone and the internet. Retail markets directly to consumers through Towergate own brands and

works through affinity partners and aggregators such as comparethemarket.com.

Being in the specialist arena, the Retail business is less likely to come under price attack than the more

commoditised personal lines segment, particularly in the online mass market. Retail is looking to grow its

online channel over time, although currently most customers complete their sale via telephone. Strategically,

online sales and service will increase as consumer behaviour changes, even in the niche areas, but currently the

Retail business uses digital primarily for lead generation. Connecting with customers through affinity partners

with strong consumer brands also helps the Retail business access volume and this has been demonstrated

through a range of partnerships. The Retail business has relationships in place with Lloyds, the AA, SAGA,

comparethemarket.com, Ageas, Admiral, Confused, FSB, NICEIC and multiple IFA networks together with

smaller more localised trade associations and networks.

Products

The Retail business is compensated for its services through commissions paid by insurance companies and

these differ by product, market opportunity and other similar factors. As commission rates for specialist

products are typically higher than for other products it generates a greater margin than some of its competitors.

Retail’s main lines of business are:

Non-standard home and specialist household

Let property (residential and commercial)

Small business insurance

Van

Caravans and boats

Military insurance

Car hire insurance

Commercial care products

Fleet and large truck

Classic car / bike

Competition

Many of the markets in which the Retail business operates are fragmented without clear market leaders,

particularly in the small business sector. Although the Retail business is prominent in all its chosen markets,

there is headroom for growth in the majority of the segments.

Underwriting

Overview

The Underwriting business provides services in commercial and personal lines insurance across a wide variety

of products. The business consists principally of issuing insurance policies on behalf of insurance companies

to customers through the internal Advisory and Retail businesses and third-party brokers. The Underwriting

business operates as a virtual insurer, performing most of the functions of an insurance company other than the

provision of capital in respect of insurance claims. The Underwriting business does not incur liability in

respect of insurance claims.

The Underwriting business assesses risks, issues policies, administers policies, handles renewals and handles

claims. In writing an insurance policy, it will agree the underwriting criteria and the delegated authority under

which it will operate on behalf of the insurance company. In respect of most policies, it will take the lead in

rating and pricing risks, as it has the expertise in various commercial and personal lines products and

knowledge in the specialist market segments in which it operates. This expertise in rating and pricing risks

means that the Underwriting business aims to offer stable performance to insurance company partners and

attractive prices to customers.

14

The Underwriting division is made up of three units as follows:

Commercial Lines, which is further divided into:

o Fusion Insurance: which provides tailored commercial insurance and risk management solutions

for SME businesses operating in a wide range of trades.

o Arista: which was acquired in April 2014 and provides commercial combined, motor and package

insurance for SME clients via eight branch offices around the UK.

o Towergate Commercial Underwriting: which focuses on e-traded SME package commercial

products.

Personal Lines, which is further divided into:

o Towergate Underwriting Household: providing standard and non-standard household and let

property products distributed by brokers and providing specialist white labelled products on the

home panels of corporate partners.

o Private Clients: offering insurance solutions to high and mid-net worth individuals

o Travel: providing insurance solutions from individual trip travel and tour operators needs, to major

travel crises and failure of travel.

Agriculture: which operates two brands in the farm market, AIUA and BiBU, whose combined

market share makes Towergate the second largest participant in the UK agricultural insurance market.

The Underwriting business obtains its underwriting capacity from a panel of leading insurance companies,

which provide capital and incur all liability in respect of insurance claims. During 2015 approximately 76% of

the underwriting capacity was provided by five insurance companies, RSA, Allianz, Canopius, QBE and

Cardif Pinnacle.

Products

The Underwriting business currently offers underwriting services in respect of over 200 different insurance

products. These products are developed in conjunction with insurance company partners and range from farm

motor vehicles to events cancellation insurance.

Commercial lines insurance focuses primarily on SMEs. Personal lines insurance focuses primarily on

specialist lines, such as non-standard household insurance and private clients (including cherished cars and

high net worth).

Competition

Commercial Lines: As an MGA, the Underwriting business works with a number of insurer partners which

gives us a wide underwriting footprint. We are in a soft market with almost unprecedented levels of

competition and we have seen the larger insurers be particularly aggressive on pricing during the last year.

Whilst there is a drive to more digital solutions for the smaller SME customer, regional brokers still dominate

the SME market and continue to value access to known underwriters who have the ability and authority to

respond in a timely manner. This will remain the case for the foreseeable future.

Personal Lines: The top 10 insurers make up approximately 80% of the market and their action in the first half

of 2016 will determine market profitability, which has already been adversely impacted by recent weather

conditions. Towergate has sought to mitigate this by applying rate increases, following the market up and

improving loss ratios with insurers.

The distribution landscape for Household is dominated by Bancassurers, and Towergate has a good foothold in

this space with a number of large distributors. The primary opportunity for Towergate lies with aggregators.

We estimate circa 300,000 Home quotations are processed per day by the four largest comparison sites,

highlighting the scale of the opportunity.

In a market with these competitive dynamics, Towergate must be able to react more quickly than the

competition and a key priority for 2016 is to invest in new systems to drive pricing and product, allowing the

business to “think and act” like a direct insurer.

15

Paymentshield

Overview

Paymentshield administers and distributes its products primarily to the mortgage intermediary market, acting

as an intermediary between mortgage brokers and underwriters. It earns commission from its underwriters,

paying away a share to brokers, together with fee and instalment income from customers.

It distributes products through mortgage brokers, estate agents, independent financial advisors, loan brokers

and networks. In many cases, Paymentshield has exclusive agreements in place with networks of mortgage

intermediaries.

The majority of policies administered are household insurance policies. Paymentshield also administers a

mortgage protection payment insurance book underwritten by Aviva and a short-term income protection

product underwritten by Cardif Pinnacle, although new business levels for these products have declined over

the last few years, with 97% of new business sales in 2015 relating to household products. Paymentshield

administers all of the policies it places, except those within its British Insurance brand, and handles the claims

for the mortgage payment protection insurance business on behalf of Aviva. Other claims are handled by the

relevant insurer. Paymentshield issues legal expenses insurance policies on behalf of ULR and home

emergency policies on behalf of DAS. The liability in respect of insurance claims is retained by insurers.

Paymentshield has profit commission arrangements in place across the household and mortgage insurance

books.

Products

Products include mortgage payment protection insurance, short-term income protection insurance, household

insurance and certain other related insurance products including home emergency insurance and legal expenses

insurance relating to home ownership. The household insurance includes buildings-only cover, contents-only

cover and combined buildings and contents cover. Short-term income protection insurance includes

unemployment-only insurance coverage.

Paymentshield designs its own household-related insurance products in partnership with insurance companies

and distributes them to mortgage intermediaries via its Inertia point-of-sale software system, a front-end

software system linked to a web-based platform through which its products can be accessed.

Competition

The main sources of competition for the general insurance associated with mortgage activity are price

comparison websites, direct providers/insurers or via insurers’ affinity relationships with banks, building

societies or retailers.

Competition to secure the activity of mortgage brokers, especially the larger networks, comes direct from

insurers and other home and contents insurance panel operators who exist in the market, but who are not of a

comparable size to Paymentshield.

Broker Network

Overview

As a member of Broker Network, independent brokers benefit from different levels of insurer and business

support services, depending on their level of membership.

The Broker Network business offers brokers three levels of membership: Premier, Advantage and Connect

(previously branded as Countrywide).

Before Premier membership is granted, all prospective Premier members are subject to due diligence which

includes external credit checks, a review of financial statements, confirmation from insurance companies of

credit issues, review of client money reconciliations and a review of their general control environment

including their regulatory reporting submissions. Within three months of a broker joining the network, a

compliance audit is conducted to assess areas of weakness in satisfying FCA requirements and the network

business works with the member to remedy where necessary.

The Broker Network receives commission and fees from both members and insurance companies for services

in respect of all membership categories.

16

Products

Premier members benefit from access to the products and services of insurance companies and intermediaries

at commission rates that would not ordinarily be available to them. With the combined buying power of all

members, the Broker Network business is able to negotiate enhanced commission rates with partner insurance

companies and intermediaries for the members.

Competition

The Broker Network business competes with other networks; the five top competitors are Compass (part of

Arthur J. Gallagher), Cobra, Willis Networks, Purple (part of Marsh) and Bluefin.

Risk management

Towergate encounters a variety of risks, most of which are operational in nature. The effective management of

these risks is critical to the running of the business and provides a greater prospect of achieving both Group

and divisional objectives.

An effective Risk Management Framework (RMF) can inform the Group’s decision making by helping to

identify business opportunities and potential risks to profitability, capital and long-term sustainability. An

RMF gives a competitive advantage and is an integral part of maintaining financial stability for customers and

other stakeholders. The Group’s board agrees the appetite for taking individual risks and gains assurances that

they are being appropriately identified and managed within the boundaries set. The Group aims to take risks

that will give consistent long-term returns and manage those risks that could prevent it from achieving its

objectives.

The management of risk is underpinned by the application of a three lines of defence governance model, which

may be defined as follows:

The first line: this sits in the business and is responsible for the identification and management of all

material risks

The second line: is made up of Group Risk and Compliance and which provides challenge, guidance

and support to the business on the first line risk assessment

The third line: is delivered by Group Internal Audit, which independently assesses the effectiveness

of the internal controls, governance and risk management

Risk management process

The RMF defines the approach for identifying, managing and reporting risk within Towergate as part of the

Group’s overall governance and control arrangements. The RMF and associated governance is overseen

centrally, although individual businesses are responsible for implementation and ensuring that the RMF is

appropriate for their specific needs.

Towergate made some significant enhancements to its risk management framework in 2014 and in 2015 the

focus was on the implementation and embedding of the framework. The key areas that were implemented in

2015 were:

A more robust process for risk identification and monitoring, including more effective tools for the

reporting of risks.

More co-ordinated recording of risk events that occur, focusing on those that could have a significant

financial or reputational impact on the organisation.

Improved trend analysis on risks and risk events, ensuring that lessons learned from incidents or risks

are shared across the Group to facilitate better mitigating strategies.

Risk reports enhanced to focus on those areas where risks are above appetite, with an increased

emphasis on the actions being taken to bring the risk back within appetite.

A stronger link developed between the issues being raised by Internal Audit and Compliance

Monitoring reviews and recent control failures, and the identification and assessment of the risks,

including ensuring the analysis uses a similar basis for assessment.

All business and control functions within the Group are required to review their risk profiles on a quarterly

basis. These are formally reported to the Group’s Leadership Team and Group Risk Committee. The Group

Risk and Compliance function provides robust challenge to business management as to their risk assessments,

with particular focus on the consistency of the assessment, the effectiveness of the controls, the exposure of the

risk against appetite and the adequacy of any actions being taken to reduce or mitigate the risk.

17

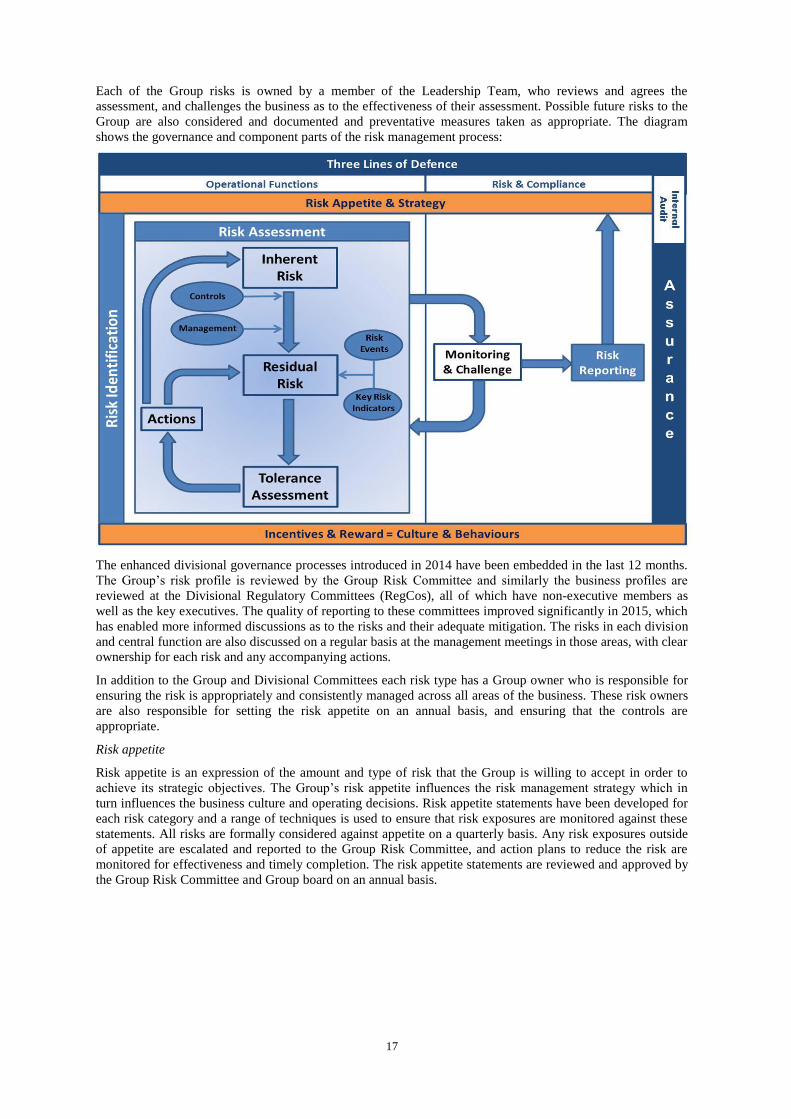

Each of the Group risks is owned by a member of the Leadership Team, who reviews and agrees the

assessment, and challenges the business as to the effectiveness of their assessment. Possible future risks to the

Group are also considered and documented and preventative measures taken as appropriate. The diagram

shows the governance and component parts of the risk management process:

The enhanced divisional governance processes introduced in 2014 have been embedded in the last 12 months.

The Group’s risk profile is reviewed by the Group Risk Committee and similarly the business profiles are

reviewed at the Divisional Regulatory Committees (RegCos), all of which have non-executive members as

well as the key executives. The quality of reporting to these committees improved significantly in 2015, which

has enabled more informed discussions as to the risks and their adequate mitigation. The risks in each division

and central function are also discussed on a regular basis at the management meetings in those areas, with clear

ownership for each risk and any accompanying actions.

In addition to the Group and Divisional Committees each risk type has a Group owner who is responsible for

ensuring the risk is appropriately and consistently managed across all areas of the business. These risk owners

are also responsible for setting the risk appetite on an annual basis, and ensuring that the controls are

appropriate.

Risk appetite

Risk appetite is an expression of the amount and type of risk that the Group is willing to accept in order to

achieve its strategic objectives. The Group’s risk appetite influences the risk management strategy which in

turn influences the business culture and operating decisions. Risk appetite statements have been developed for

each risk category and a range of techniques is used to ensure that risk exposures are monitored against these

statements. All risks are formally considered against appetite on a quarterly basis. Any risk exposures outside

of appetite are escalated and reported to the Group Risk Committee, and action plans to reduce the risk are

monitored for effectiveness and timely completion. The risk appetite statements are reviewed and approved by

the Group Risk Committee and Group board on an annual basis.

18

Information technology

The Towergate IT systems are managed collectively by an in-house team of IT professionals, relying heavily

on a series of outsource contracts with key suppliers.

The main ongoing focus of the IT department is on continuing to provide secure and performant services

whilst addressing the underlying complex, expensive and ageing infrastructure through comprehensive

renewal programmes.

IT initiatives

IT systems are critical in providing the tools for the business to manage its customers efficiently and cost-

effectively. System stability was a key challenge through 2015 and key measures being undertaken to

remediate this are:

Current system stability and security. A programme of tactical initiatives has resulted in a more stable

environment with a significant increase in performance and decrease in incidents impacting the ability to

transact business.

Redesigning infrastructure. The Infrastructure Transformation Programme (ITTP) has been developed

and has gained Group board approval to renew all of the WAN/LAN, data centres and end-user

environments across the estate. The first of these, mobile telephony and printing are well advanced

through delivery. The overall architecture, approach and business case has been developed and ratified

and the programme will move into delivery from the end of Q1 2016.

System access controls and information security

System access controls manage authentication procedures and allow controlled access to data and applications.

There are in place multiple firewalls and mail filtering, virus scanning and spam controls to protect the

network. The IT department also employs a certified security manager to review data protection and network

security. In addition, a specialist security organisation performs penetration testing and highlights any potential

system weaknesses. As part of the Control Framework programme, Towergate has developed a Group-wide

Information Governance framework to protect its information assets. In line with industry standards,

Towergate has appointed a Data Protection Officer to oversee data security and standards.

Business continuity and disaster recovery

The business sites are connected to one of two data centres in Birmingham and Reading. Each of the data

centres is built to support highly resilient power services, as well as banking security and communication

standards. Whilst business continuity and disaster recovery plans exist these are not considered optimal and

these will be materially upgraded as part of the ITTP delivery.

Intellectual property

Towergate relies on copyright and trademark laws, confidentiality procedures and contractual provisions to

protect its intellectual proprietary rights. Towergate actively takes steps to protect the Group’s intellectual

property rights when and where deemed appropriate.

Towergate markets the majority of its products and services under approximately 130 trademarks, all of which

are registered in the United Kingdom. The Towergate trademark, as well as major service and product brands,

enhance the competitive advantage and are essential to the business.

Towergate has registered an extensive number of internet domain names. These domain names are either used

by the businesses to deliver services and information to customers or held to protect trading names and brands

developed by the businesses.

Although the businesses have contributed to the development of certain of the software platforms that are

licensed, such as Landscape and Guidewire, the proprietary rights in the intellectual property of these software

platforms rests with their licensors. However, the businesses exclusively own the business process intellectual

property resulting from the integration of these software platforms with the existing systems and the

customisation of these platforms. Towergate has no patents or patent applications pending.

Environmental matters

Towergate believes that it does not have any material environmental compliance costs or environmental

liabilities.

19

Property portfolio

Towergate leases its registered office, which is located at Towergate House, Eclipse Park, Sittingbourne,

Maidstone, Kent, ME14 3EN, England. It also leases over 100 properties, circa 85 of which are advisory and

retail offices. The remainder are principally offices which conduct underwriting, mortgage broker solutions

and network operations in various locations throughout the United Kingdom.

The property portfolio is managed internally by a property team, supported by external specialists where

appropriate. This team is responsible for ensuring that each site is in compliance with the relevant statutory

requirements, including health and safety requirements.

Insurance

The operations are subject to various actual and potential claims, lawsuits and other proceedings relating

principally to alleged errors and omissions in connection with the placement of insurance in the ordinary

course of business. Errors and omissions claims, lawsuits and other proceedings arising in the ordinary course

of business are covered in part by professional indemnity or other appropriate insurance.

Regulation

Towergate businesses are regulated by the FCA. The FCA Rules include rules that impose, among other

things, high level standards on the establishment and maintenance of proper systems and controls and

minimum threshold conditions that must be satisfied for an insurance firm to remain authorised as well as rules

on the conduct of business and treating customers fairly. The FCA Rules also impose certain minimal capital

and liquidity requirements on firms. Firms have an ongoing obligation to provide the FCA with certain

information regularly. Monitoring is carried out by the FCA to assess compliance with regulatory requirements

and the FCA has almost unlimited investigative and disciplinary powers. A number of senior individuals in

Towergate are approved persons (under FCA rules) and are required to satisfy certain fitness and propriety

criteria.

Towergate has regular contact with the FCA who has a scheduled programme of update meetings with

members of the senior management. There are a few areas, such as governance and operational controls where

the FCA has required Towergate to take some action to improve its position. These areas are making good

progress and are expected to be completed in 2016.

Legal proceedings

At any given point in time the Group is subject to various actual and potential claims, lawsuits and proceedings

relating principally to alleged errors, omissions or unfair provisions in connection with the placement of

insurance or the provision of financial services advice in the ordinary course of business. As the Group often

assists its customers with matters, including the placement of insurance coverage and the handling of related

claims and the provision of financial services advice, involving substantial amounts of money, errors and

omissions claims against the Group may arise that allege its potential liability for all or part of the amounts in

question. Claimants can seek large damage awards and these claims can involve potentially significant defence

costs.

The Group maintains professional indemnity insurance for errors and omissions claims, the terms of which

vary by policy year. In recent years, the Group’s self-insured risks have increased. In respect of such risks, the

Group has established a provision for claims in respect of outstanding errors and omissions claims that the

Group believes to be adequate in light of current information and legal advice and the Group adjusts such

provision from time to time according to developments.

Currently the most significant errors and omissions notifications relate to the ETV and UCIS reviews which is

discussed further on page 26. In addition in the normal course of business the Group has a provision of £2.2m

to cover potential claims based on an estimate of the likely outcome of outstanding and potential claims.

20

Employees

The Group had an average of 4,618 (2014: 4,969) full time equivalent employees. Virtually all of the

employees are located in the United Kingdom. The table below shows the Group’s number of full time

equivalent employees by division.

2015 2014

Advisory 1,725 2,002

Retail 1,234 1,295

Underwriting 791 803

Paymentshield 252 271

Broker Network 138 143

Central Support 478 455

4,618 4,969

None of the employees is represented by a labour union. The Group considers the relations with employees to

be good.

21

Management’s discussion and analysis of financial condition and results of

operations

Significant factors affecting results of operations

Commissions and fees

Insurance brokers and underwriting agents derive the majority of their revenue from commissions and fees.

Commissions are generally based on insurance premiums and negotiated commission rates. Fees are paid for

individual services based on negotiated amounts. As rating is currently soft, commission income is depressed.

The net commission rates are mostly affected by up front trading deals signed between 2013 and 2014 and

operational complexity linked to the high number of Policy Administration Systems.

The Group also enters into profit sharing arrangements, fees for the provision of payment instalment plans and

other one-off deals with third parties which are recognised over the life of the relevant arrangement or when

they can be measured with reasonable certainty. Such trading deal income includes contributions to marketing

or product development, volume payments and profit commissions receivable. The amount and timing of

trading deal income is inherently uncertain and individual amounts may be material. Amounts accrued at the

year end and recognised as assets may be subject to judgement.

Acquisitions

The TIL Group has historically pursued a strategy of acquisitions to deliver scale advantage.

This acquisition strategy was focussed on both intermediary (or broking) business and on underwriting

agencies. In evaluating potential acquisitions, the TIL Group considered the market position, growth prospects

and underwriting performance of target businesses, as well as their geographic, distribution channel and

product mix fit with its existing operations. The price paid for acquisitions was based primarily on the

commission and fee income streams of the target business and the potential to increase such streams following

the acquisition.

Acquisitions affect the results of operations in several ways. First, the results for the period during which an

acquisition takes place includes the results of the acquired business in that and subsequent accounting periods.

Second, the results for subsequent periods may be affected by applying the Group’s enhanced commission

arrangements to the policies that the acquired business places, and by cross-selling products. Third, the results

for subsequent periods may be affected if synergies are realised from shared services and infrastructure.

Insurance cycle

The insurance industry is inherently cyclical, meaning that the pricing and terms and conditions of cover vary

over time. The insurance cycle is characterised by soft and hard market conditions. Soft conditions reflect

muted demand, low or negative premium rates, widening coverage and the free availability of capital. As a

result soft markets generally result in a lower level of underlying profitability for both insurance carriers and

intermediaries. Hard market conditions generally follow a period of heightened loss activity and capital

erosion. As a result the supply of insurance is limited, rating or pricing increases and coverage narrows. It

follows that underlying profitability for both insurance carriers and intermediaries generally rises in a hard

market, although there can be a lag between the market turn and the effect on reported profits.

Seasonality

The Group experiences some seasonality in the volumes of insurance policies transacted and, consequently, in

commission and fees. The Group historically transacted less business from November to February than in most

other months of the year. Accordingly, although volumes typically increase in March, commission and fees for

the first quarter tends to be lower than the second and third quarter, before declining again in the fourth quarter.

22

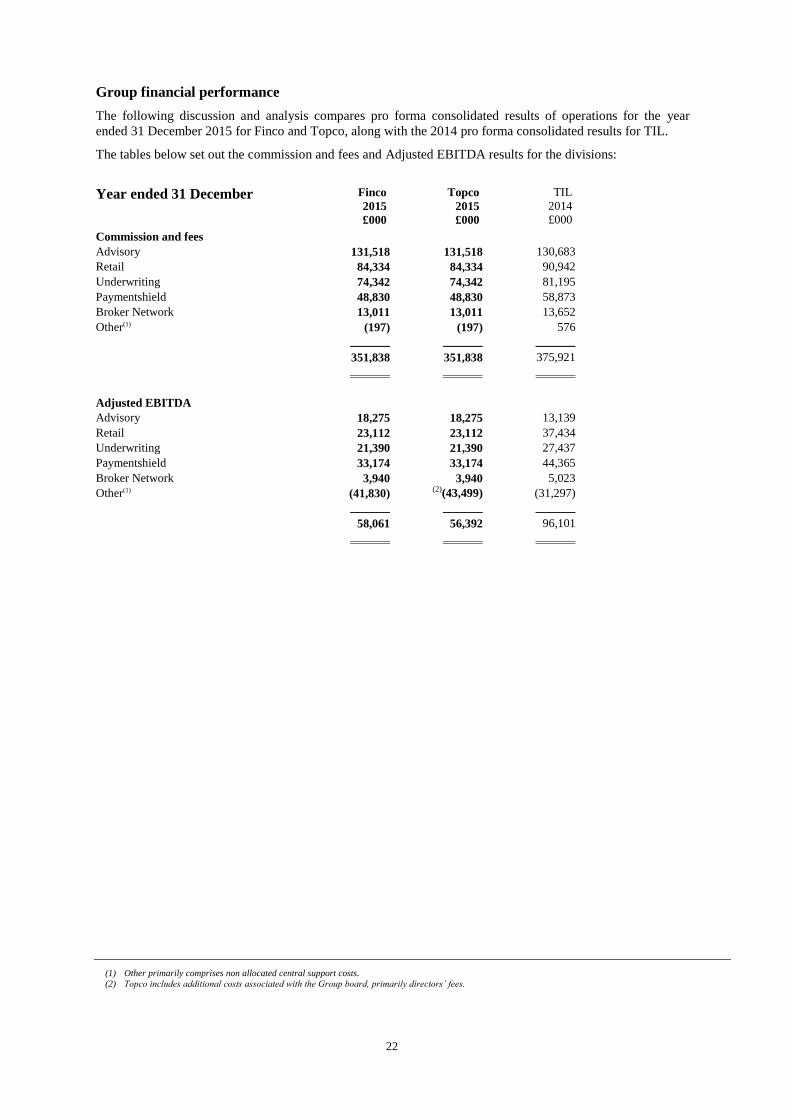

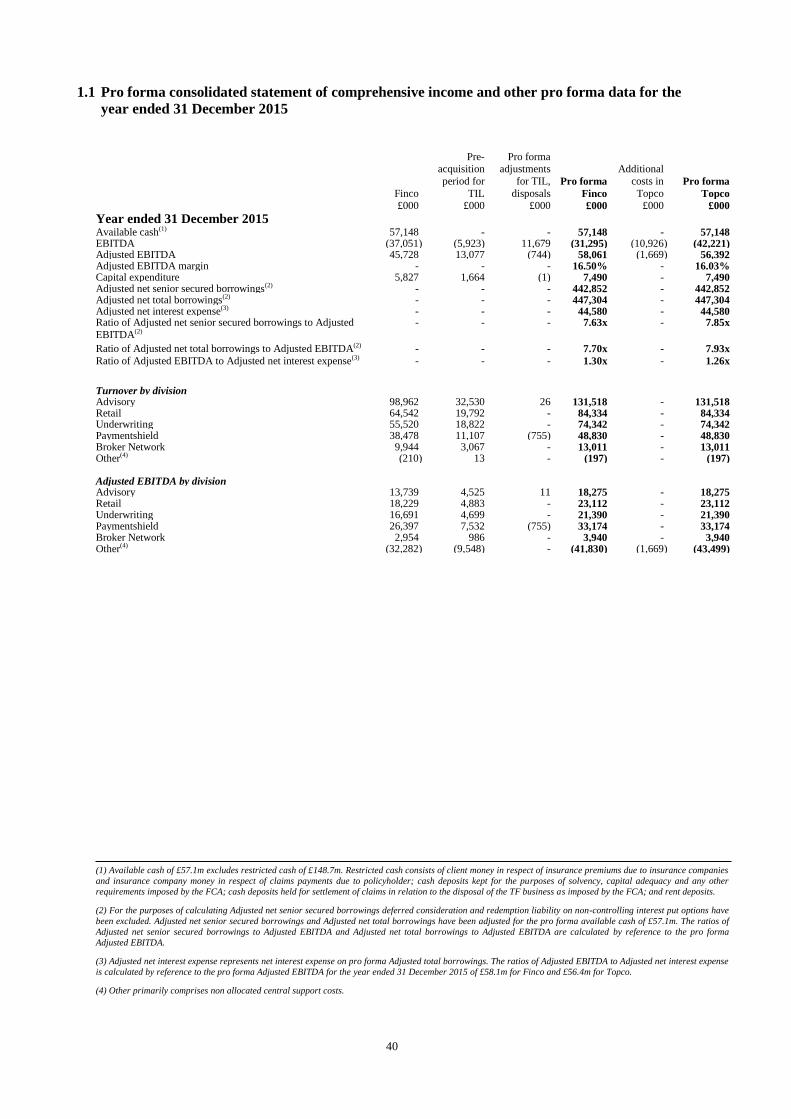

Group financial performance

The following discussion and analysis compares pro forma consolidated results of operations for the year

ended 31 December 2015 for Finco and Topco, along with the 2014 pro forma consolidated results for TIL.

The tables below set out the commission and fees and Adjusted EBITDA results for the divisions:

Year ended 31 December

Finco

2015

£000

Topco

2015

£000

TIL

2014

£000

Commission and fees

Advisory 131,518 131,518 130,683

Retail 84,334 84,334 90,942

Underwriting 74,342 74,342 81,195

Paymentshield 48,830 48,830 58,873

Broker Network 13,011 13,011 13,652

Other(1) (197) (197) 576

351,838 351,838 375,921

Adjusted EBITDA

Advisory 18,275 18,275 13,139

Retail 23,112 23,112 37,434

Underwriting 21,390 21,390 27,437

Paymentshield 33,174 33,174 44,365

Broker Network 3,940 3,940 5,023

Other(1) (41,830) (2)(43,499) (31,297)

58,061 56,392 96,101

(1) Other primarily comprises non allocated central support costs.

(2) Topco includes additional costs associated with the Group board, primarily directors’ fees.

23

Description and performance of key line items

Set out below is a brief description and performance of the composition of the key line items of the Group’s

consolidated statement of comprehensive income.

Commission and fees

Commissions and fees represents income received from third parties net of commissions paid to sub-agents and

brokers. When a sub-agent or broker refers a customer to the Group, it typically shares that commission with

the sub-agent or broker. For the purposes of the analysis of results below, commission and fees are analysed by

division. Income from trading deals with insurers is included in commission and fees.

Advisory:

Commission and fees are broadly in line with last year. Retention rates have strengthened towards the end of

the year and are getting back to the levels achieved prior to the change programme. Adjusted EBITDA has

increased by 39.1% resulting from a reduction in expenses which include the Group restructuring fair value

adjustments.

Retail:

The SBU and Direct divisions were combined to form the Retail division in 2015. Commission and fees

declined by 7.3%, mainly due to continued challenges in the SBU division, this has been partly offset by a

strong and resilient performance in Direct which has seen new business increase year on year. Adjusted

EBITDA has declined by 38.3%, impacted by both the decrease in income as well as an increase in costs,

notably the annualised effect of the old SBU division which was originally launched during 2014.

Underwriting:

Commission and fees declined by 8.4% resulting from a challenging year in 2015 and the impact of the

financial restructuring, notably felt in retention and new business. Other negative impacts include lost revenues

as internal broking businesses declined and the exit from certain lines that didn’t meet required returns.

Adjusted EBITDA has decreased by 22.0% driven by the shortfall in income. Expenses are broadly flat, in line

with last year.

Paymentshield:

Commission and fees declined by 17.1%, impacted by a £6m non-cash income adjustment in 2014. The

underlying income decline is 10.1%, excluding this adjustment, which is driven by the continued reduction in

back books of MPPI and Household. Adjusted EBITDA has decreased by 25.2% largely due to the decrease in

income, with expenses broadly in line with last year.

Broker Network:

Commission and fees declined by 4.7% due to a fall in member numbers and refreshed pricing of the existing

book in response to an increasingly competitive market. Adjusted EBITDA has declined by 21.6%, resulting

from a decrease in income and an increase in expenses. The uplift in costs includes higher bonuses and one-off

premises costs in 2015.

Investment income

Investment income represents the interest received on restricted cash.

In the year ended 31 December 2015 investment income has decreased by £0.1m (26.9%) for Finco and Topco

compared to TIL for the same period in 2014.

Salaries and associated expenses

Salaries and associated expenses represent the costs of staff and staff related costs incurred in the operations of

the Group and will include staff related costs for exceptional spend not in the normal course of operations of

the Group.

Salaries and associated expenses have decreased in the year ended 31 December 2015 by £9.8m (5.1%) at

Finco and £8.5m (4.4%) at Topco reflecting a decrease in the cost of the workforce compared to TIL for the

same period in 2014.

24

Other operating expenses

Other operating expenses represent all other administrative costs and will include exceptional spend not in the

normal course of operations of the Group.

Other operating expenses decreased in the year ended 31 December 2015 by £129.2m (39.2%) at Finco and

£119.6m (36.3%) at Topco compared to TIL for the same period in 2014. This is primarily due to the related

party bad debt write off in 2014 offset by additional expenditure on acquisition and financing costs, group

reorganisation costs and regulatory costs in 2015 not incurred in 2014.

Depreciation and amortisation charges

Depreciation and amortisation charges represent the depreciation charge of tangible assets and the amortisation

of intangible assets.

Depreciation and amortisation charges have increased by £22.2m (98.7%) in the year ended 31 December

2015 compared to TIL for the same period in 2014. This is primarily due to increased amortisation on

intangibles, where fair values increased as a result of the Group restructuring.

Impairment of Goodwill

Impairment of goodwill in 2015 and 2014 represented the impairment of the goodwill based on the value in use

or fair value less costs to sell of the Group. This was conducted at cash generating unit level which reflects the

divisional structure of the Group.

Finance costs

Finance costs represent the interest and other financing costs of the Group.

Finance costs have been subject to pro forma adjustments in order to present the cost of the current debt as if it

was in place for both comparative periods.

Finance income

Finance income represents the interest on available cash and the changes in fair value of the financial

instruments in the statement of financial position.

Finance income has increased by £0.2m in the year to 31 December 2015 compared to 2014, primarily due to

increased office cash balances being held following the Group restructuring on 2 April 2015.

Income tax credit

An income tax credit arises on the unwinding of the deferred tax liability in respect of the amortisation charged

on the intangible assets and due to a change in corporation tax rate which has been applied to the deferred tax

asset and liability.

Exceptional costs

Group change programmes

During 2014 and 2015 the Group has undertaken a number of change programmes. These programmes were

designed to improve efficiency across the business, to build regulatory resilience, to position the Group to

exploit future scale advantages and to enhance the customer proposition. These programmes have been

separately disclosed within exceptional items on the face of the consolidated statement of comprehensive

income.

Acquisition and financing costs and bad debt provision for related parties

The Group has undergone a financial restructuring which completed on 2 April 2015. Costs of £41.2m were

incurred in the year to 31 December 2015 (2014: £10.3m). In addition in 2014, TIL recognised a provision of

£191.2m against amounts due from previous holding companies which are considered irrecoverable following

the restructuring, of which £0.7m relates to the Towergate Financial business and has been re-analysed as part