Embed Size (px)

Citation preview

Towergate Insurance

Limited

Quarterly report

For the quarter ended 31 March 2015

TIG Finco plc £425,000,000 8.75% senior secured notes due 2020

TIG Finco plc £75,000,000 floating rate super senior secured notes due

2020

Issued: 26 June 2015

Table of contents Page

General and recent developments 1 Presentation of financial and other information 3 Forward looking statements 4 Summary unaudited pro forma financial information and other data 5 Management’s discussion and analysis of financial condition and results of operations 14 Appendix 1 – Interim financial statements of Towergate Insurance limited 20

1

General

This quarterly report should be read in conjunction with the unaudited interim consolidated financial statements of

Towergate Insurance Limited (TIL or the Company) for the quarter ended 31 March 2015.

This quarterly report has been prepared under International Financial Reporting Standards (IFRS). This quarterly

report presents unaudited interim consolidated financial and other information on TIL and its subsidiary companies

(together the Group or Towergate).

Recent developments

The following items have been noted as updates to ongoing issues or a summary of transactions to bring to the

attention of the reader:

Updates on the ongoing issues with the Financial Conduct Authority (FCA) in relation to client money and

advice provided by the Towergate Financial business

A summary of the Group financial restructuring

Senior management changes

A summary financial review and outlook

FCA

During Q3 2013 the Group identified that £15.0m of client and insurer monies had been misallocated to an

unrestricted account between November 2007 and January 2011. As soon as the misallocation was confirmed

management transferred £15.0m to the relevant client and insurer accounts. The FCA was notified and

investigations into this matter are continuing.

The Group is continuing discussions with the FCA in connection with past advice provided by the Towergate

Financial businesses on pension Enhanced Transfer Values (ETV) and Unregulated Collective Investment Schemes

(UCIS). There remain material uncertainties over the level of redress costs as customer contact has commenced but

is not significantly complete and the redress methodology has not been agreed. Purely for internal purposes a range

of £65.0m-£85.0m is used in cash flow projections. Given the level of uncertainty this item remains a contingent

liability in the Group’s financial statements.

Acquisitions and disposals

The Group made seven acquisitions in the fifteen months to 31 March 2015 (consisting of two companies and five

portfolios) for an aggregate consideration of approximately £21.9m. The Group disposed of five businesses during

this period. The material transactions were:

On 17 April 2014 the Group completed the acquisition of Arista Insurance Limited (Arista), a leading UK

commercial managing general agent specialising in property, liability and motor insurance, for a

consideration of £16.7m. Arista has a clearly defined regional distribution network and fits well with the

Group’s strategy of acquiring specialist businesses with strong growth potential

On 29 August 2014 the Group disposed of Folgate Insurance Company Limited (FICL) to Anglo London

for a consideration of £1.9m. Folgate Insurance was an insurance company in run off and as such operated

outside the Group’s core UK specialist lines and small and medium sized businesses (SME) markets

On 23 December 2014 the Group disposed of The Hayward Holding Group Limited (Hayward Aviation) to

Jardine Lloyd Thompson for a consideration of £27.0m. As an international aviation insurance broker,

Hayward Aviation operated outside the Group’s core UK specialist personal lines and SME markets

On 16 March 2015 the Group disposed of its Towergate Financial business (TF) to Palatine Private Equity

for a consideration of £8.6m. The Towergate Financial business was a provider of independent financial

and mortgage advice and operated outside the Group’s core UK specialist personal lines and SME markets

Group financial restructuring

On 2 April 2015 the Group completed a financial restructuring in relation to the senior secured creditors and senior

unsecured creditors of Towergate Finance plc, a former intermediate parent company. As part of these

arrangements TIG Finco plc (a newly formed holding company) acquired the Group for consideration of £735.0m

made up of the issue of £425.0m of Senior Secured Notes by TIG Finco plc and the issue of new shares in TIG

Finco plc’s indirect parent company, TIG Topco Limited, valued at £310.0m.

2

As a result of these arrangements, in April 2015 Highbridge Principal Strategies LLC became the Group’s majority

shareholder.

As part of the financial restructuring, additional capital of £122.0m was received by the Group through the issue by

TIG Topco Limited of new shares for £50.0m and the issue by TIG Finco plc of £75.0m of Super Senior Secured

Notes at a discount of £3.0m. The additional funds provide liquidity to the Group and have enabled it to fund the

costs of the restructuring of £42.0m, the vesting of long term incentive plans which have crystallised or will in the

future crystallise as a result of the restructuring of £30.0m, retention bonuses of £8.0m and minority interest buy

outs of £2.0m.

Senior management changes

There have been a number of senior management changes in the period since 31 December 2014 including:

Scott Egan has changed his role from Chief Financial Officer to Interim Chief Executive Officer

Alastair Lyons has changed his role from Executive Chairman to Non-executive Chairman

The appointment of Mark Mugge as Chief Operating Officer and Steve Wood as Chief Executive Officer

of Paymentshield

The appointment of John Tiner as Chairman with effect from 29 June 2015

Financial review and outlook

Q1 2015 was a challenging period. Confidence in Towergate was tested with performance in all divisions affected

by both the Group financial restructuring and the change programme.

However significant progress has been made in multiple areas. Towergate has attracted long term supportive

shareholders in Highbridge, KKR and Sankaty. Over the last fifteen months much of the comprehensive change

programme has been implemented. Towergate continues to attract talent. The Board remains focussed on

operational delivery in 2015 and there are some early signs of recovery as the business stabilises.

The Group is focussed on retention and new business and aims to deliver this through a concentration on customer

service and operational excellence. The expectation is that expenses will fall through the completion of the change

programme and continued integration of businesses. The Board will continue to invest in the business to deliver

profitable growth in its chosen markets.

3

Presentation of financial and other information

This quarterly report is prepared by the Company in connection with the issuance by TIG Finco plc of £425.0m

senior secured notes and £75.0m floating rate super senior secured notes (together the Notes) on 2 April 2015.

The unaudited interim consolidated financial statements of the Group have been prepared in accordance with IFRS.

The unaudited financial information of the Group presented in this quarterly report and discussed in the

management’s discussion and analysis of financial condition and results of operations has been prepared on a pro

forma basis in order to present a two-year financial track record. Adjustments have been made in respect of:

Subtraction of the results of disposed businesses:

Hayward Aviation for the period 1 January 2014 to 23 December 2014

FICL for the period 1 January 2014 to 29 August 2014

TF for the period 1 January 2014 to 16 March 2015

Inclusion of the Group debt which was in Towergate Finance plc at the date of this report, to reflect the

impact on the Group’s unaudited interim consolidated financial statements.

These financial results include certain financial measures and ratios, including EBITDA, Adjusted EBITDA,

Adjusted EBITDA margin and certain leverage and coverage ratios that are not presented in accordance with IFRS.

In these financial results, references to EBITDA for the parent guarantor are to profit/(loss) on ordinary activities

before interest payable and similar charges, tax, depreciation, amortisation of intangibles and group reorganisation

costs. Accordingly, EBITDA can be extracted from the consolidated financial statements of TIL by taking

profit/(loss) on ordinary activities and adding back interest payable and similar charges, tax, depreciation,

amortisation of intangibles and group reorganisation costs.

References to Adjusted EBITDA for TIL represent EBITDA as adjusted for certain redundancy and restructuring

costs, financing transaction costs, asset write downs in connection with business restructuring, long-term incentive

plan charges and business investment costs.

EBITDA-based measures are not presented as measures of the results of operations. EBITDA-based measures have

important limitations as an analytical tool, and should not be considered in isolation or as substitutes for analysis of

the Group’s results of operations. Management believes that the presentation of EBITDA-based measures is helpful

to investors as a measure of the operating performance and ability to service debt. EBITDA-based measures may

not be comparable to similarly titled measures used by other companies.

EBITDA, Adjusted EBITDA, Adjusted EBITDA margin and leverage and coverage ratios are not measurements of

financial performance under IFRS and should not be considered as alternatives to other indicators of the Group’s

operating performance, cash flows or any other measure of performance derived in accordance with IFRS.

Certain data contained in these financial results, including financial information, have been subject to rounding

adjustments. Accordingly, in certain instances the sum of the numbers in a column or a row in tables may not

conform exactly to the total figure given for that column or row.

The discussion includes forward looking statements, which, although based on assumptions that are considered

reasonable, are subject to risks and uncertainties which could cause actual events or conditions to differ materially

from those expressed or implied herein. Undue reliance cannot be placed on these forward looking statements.

These forward looking statements are made as of the date of this annual report and are not intended to give any

assurance as to future results.

Segmental analysis is presented in this financial information. From time to time structural changes are made within

the business and trading businesses may move between the reported segments. When this occurs financial

information is restated in respect of the corresponding prior year period to facilitate the discussion and analysis of

the results.

In these financial results, all capitalised terms not otherwise defined are defined in the indenture agreements dated 2

April 2015 related to the issuance of the Notes.

4

Forward looking statements

This annual report contains statements under the captions risk factors, business, management’s discussion and

analysis of financial condition and results of operations, and in other sections that are, or may be deemed to be,

forward-looking statements. In some cases, these forward-looking statements can be identified by the use of

forward-looking terminology, including the words “aims”, “believes”, “estimates”, “anticipates”, “expects”,

“intends”, “may”, “will”, “plans”, “predicts”, “assumes”, “shall”, “continue” or “should” or, in each case, their

negative or other variations or comparable terminology or by discussions of strategies, plans, objectives, targets,

goals, future events or intentions.

Many factors may cause the Group’s results of operations, financial condition, liquidity and the development of the

industries in which it operates to differ materially from those expressed or implied by the forward-looking

statements contained in this annual report. These factors include among others:

The impact of current economic conditions on the Group’s results of operations and financial condition

The risk of a downturn in the property market

Volatility or declines in the premiums on which the Group’s commissions are based and declines in

commission rates

The Group’s dependence on insurance companies providing us underwriting capacity and on third-party

brokers, mortgage intermediaries and networks of mortgage intermediaries to distribute its products

The impact of any adverse changes to relationships with brokers and mortgage intermediaries

The impact of competition

The Group’s exposure to potential regulatory sanctions and fines

The unpredictable nature of profit commissions

Legislative, taxation and regulatory changes, inquiries or enforcement actions, affecting the Group’s ability to

operate or the profit generated from its activities

Exposure to potential liabilities arising from errors and omissions claims against the Group

The impact of acting outside the scope of the Group’s delegated authority from insurance companies

Interruption or loss of the Group’s information processing systems or failure to maintain secure information

systems and technological changes

Risks relating to the Group’s acquisition strategy

Risks of increased competition from consolidators limiting potential growth opportunities

The Group’s ability to retain its senior management and underwriters, account executives, sales personnel and

other client facing employees

The Group’s ability to gain technological expertise and apply technology effectively

The risk that the Group may have to write down the value of its goodwill

The interests of the Group’s shareholders

Risk relating to conflicts of interest and transactions with affiliated companies

The Group’s substantial debt

Fluctuations in interest and foreign exchange rates

The other factors discussed in more detail under Risk factors

These risks and others described under Risk factors are not exhaustive. Other sections of this annual report describe

additional factors that could adversely affect the Group’s results of operations, financial condition, liquidity and the

development of the industries in which it operates. New risks can emerge from time to time, and it is not possible

for the Group to predict all such risks, nor can it assess the impact of all such risks on its business or the extent to

which any risks, or combination of risks and other factors, may cause actual results to differ materially from those

contained in any forward-looking statements. Given these risks and uncertainties, readers of this document should

not rely on forward-looking statements as a prediction of actual results.

Any forward-looking statements are only made as of the date of this annual report, and the Group does not intend,

and does not assume any obligation, to update forward-looking statements set forth in this annual report. Readers of

this document should interpret all subsequent written or oral forward-looking statements attributable to the Group or

to persons acting on its behalf as being qualified by the cautionary statements in this annual report. As a result,

readers of this document should not place undue reliance on these forward looking statements.

5

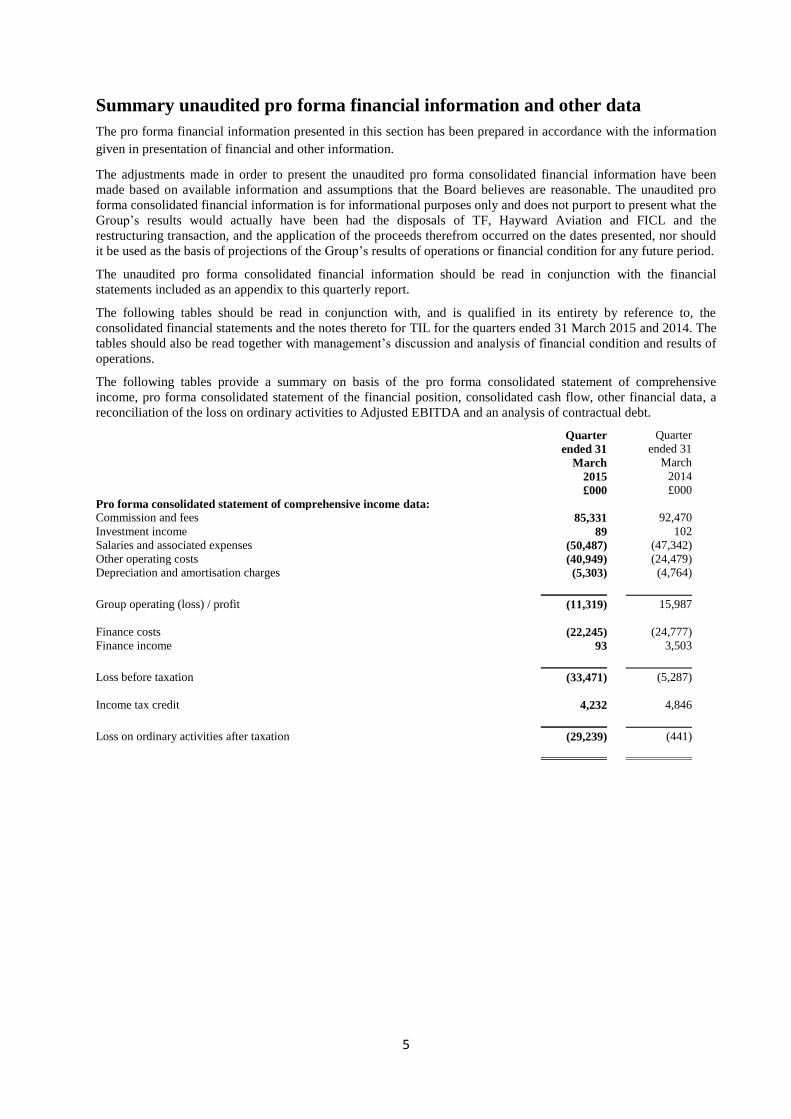

Summary unaudited pro forma financial information and other data

The pro forma financial information presented in this section has been prepared in accordance with the information

given in presentation of financial and other information.

The adjustments made in order to present the unaudited pro forma consolidated financial information have been

made based on available information and assumptions that the Board believes are reasonable. The unaudited pro

forma consolidated financial information is for informational purposes only and does not purport to present what the

Group’s results would actually have been had the disposals of TF, Hayward Aviation and FICL and the

restructuring transaction, and the application of the proceeds therefrom occurred on the dates presented, nor should

it be used as the basis of projections of the Group’s results of operations or financial condition for any future period.

The unaudited pro forma consolidated financial information should be read in conjunction with the financial

statements included as an appendix to this quarterly report.

The following tables should be read in conjunction with, and is qualified in its entirety by reference to, the

consolidated financial statements and the notes thereto for TIL for the quarters ended 31 March 2015 and 2014. The

tables should also be read together with management’s discussion and analysis of financial condition and results of

operations.

The following tables provide a summary on basis of the pro forma consolidated statement of comprehensive

income, pro forma consolidated statement of the financial position, consolidated cash flow, other financial data, a

reconciliation of the loss on ordinary activities to Adjusted EBITDA and an analysis of contractual debt.

Quarter

ended 31

March

Quarter

ended 31

March

2015 2014

£000 £000

Pro forma consolidated statement of comprehensive income data:

Commission and fees 85,331 92,470

Investment income 89 102

Salaries and associated expenses (50,487) (47,342)

Other operating costs (40,949) (24,479)

Depreciation and amortisation charges (5,303) (4,764)

Group operating (loss) / profit (11,319) 15,987

Finance costs (22,245) (24,777)

Finance income 93 3,503

Loss before taxation (33,471) (5,287)

Income tax credit 4,232 4,846

Loss on ordinary activities after taxation (29,239) (441)

6

Quarter ended

31 March

Quarter ended

31 March

2015 2014

£000 £000

Pro forma consolidated statement of financial position data:

Intangible assets 818,271 1,365,880

Property, plant and equipment 11,130 10,785

Other non-current assets 11,347 7,528

Trade and other receivables 76,871 231,492

Cash at bank and in hand 185,396 182,785

Other current assets - -

Current liabilities (405,791) (334,633)

Non-current liabilities (929,804) (936,705)

Net (liabilities) / assets (232,580) 527,132

Quarter

ended 31

March

Quarter

ended 31

March

2015 2014

£000 £000

Consolidated cash flow:

Cash flows from operating activities

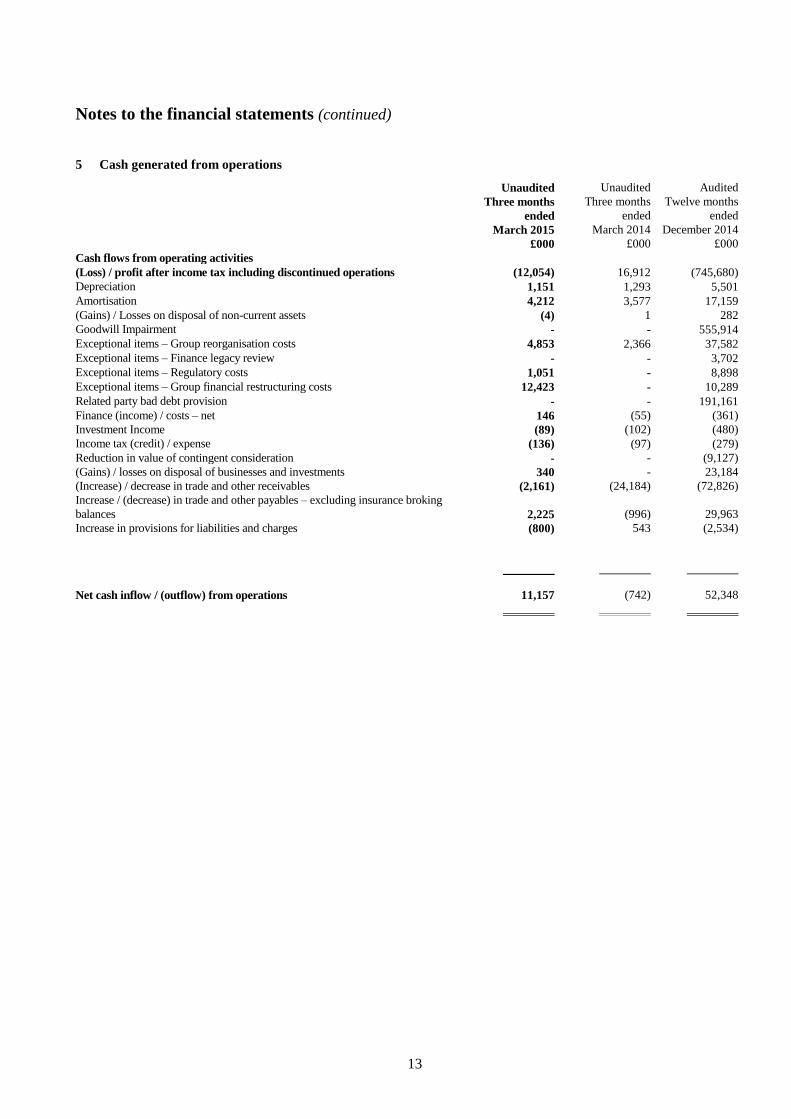

Cash generated from / (used in) operations 11,157 (742)

Exceptional items (18,302) (2,366)

(Decrease) / increase in net insurance broking creditors (25,237) (14,769)

Net interest (paid) / received and investment income 182 157

Taxation (paid) / received - 16

Net cash used in operating activities (32,200) (17,704)

Cash flows from investing activities

Acquisitions and disposals 2,205 (2,792)

Purchase of intangible assets – computer software and commission buy outs (1,316) (2,912)

Purchase of property, plant and equipment (372) (520)

Net cash generated from / (used in) investing activities 517 (6,224)

Cash flows from financing activities

Financing 16,646 10,854

Net cash generated from financing activities 16,646 10,854

Decrease in net cash in the year (15,037) (13,074)

Quarter

ended 31

March

Quarter

ended 31

March

2015 2014

£000 £000

Other financial data:

EBITDA 12,404 23,167

Adjusted EBITDA 13,077 23,787

Adjusted EBITDA margin 15.33% 25.72%

Net borrowings(1) 1,010,418 989,157

(1) Net borrowings represent pro forma total borrowings excluding accrued interest and capitalised fees plus deferred consideration and less

available cash and cash equivalents.

7

Quarter

ended 31

March

Quarter

ended 31

March

2015 2014

Reconciliation of loss on ordinary activities to Adjusted EBITDA

£000 £000

Loss on ordinary activities after tax (29,239) (441)

Add back:

Finance costs and income (related to derivative financial instruments)(A) 22,245 21,324

Group reorganisation costs 4,853 2,366

Regulatory costs 1,051 -

Group financial restructuring costs 12,423 -

Income tax (4,232) (4,846)

Depreciation and amortisation charges 5,303 4,764

EBITDA 12,404 23,167

Add back / (deduct from):

(Profit) / loss on disposal of business(B) 340 -

Asset write-downs in connection with business restructuring(C) 294 213

Long-term incentive plan charges(D) - 150

Business investment costs(E) 32 41

Acquisition costs(F) 7 216

Adjusted EBITDA 13,077 23,787

(A) Finance costs are comprised of interest payable on bank loans, directors’ loans, the Notes, finance charges payable in respect of finance leases and hire

purchase contracts, hedging costs and certain other charges. Finance income represents the fair value gains on derivative (interest rate swap) financial

instruments.

(B) Represents in 2015 the loss on disposal of the sale of a portfolio from Towergate Underwriting Group Limited.

(C) Represents costs incurred in relation to potential acquisitions and disposals of businesses.

(D) Represents non-cash provisions charged in connection with potential future settlement costs of long-term incentive plans. Certain members of the Group’s

board of directors and senior management are entitled to a one-time cash bonus, in addition to any annual bonus, based on the value appreciation of Towergate.

The vesting conditions of the bonus were a 90% sale of shares of Towergate or a listing of Towergate. As a result of the financial restructuring which completed

on 2 April 2015 the existing long term incentive plans were deemed to have a zero value and amounts previously provided in relation to these have been credited to

the statement of comprehensive income for the year ended 31 December 2014.

(E) Represents investment costs which are incurred for the purposes of generating future EBITDA and value growth. Business investments costs will include,

amongst other things; recruitment and compensation costs paid to market professionals recruited from competitors for the period following their resignation from

such competitors and prior to when they are able to solicit clients on the Group’s behalf due to non-compete clauses in favour of such competitors and the costs of

recruitment and appointment of executive, non-executive and specialist advisers.

(F) Represents (i) transaction costs in respect of acquisitions (ii) adjustments to acquisitions that are more than one year post-acquisition and (iii) adjustments to

the valuation of deferred consideration and redemption liability non-controlling interest put options on acquisitions that are more than one year post-acquisition.

8

Unaudited pro forma financial information and other data

for the quarter ended 31 March 2015

Pro forma consolidated statement of comprehensive income

Quarter ended

31 March 2015

for Towergate

Insurance(1)

Removal of the

results and pro

forma

adjustments for

the disposal of

TF (2)

Pro forma

adjustments for

debt costs(3)

Pro forma

quarter ended

31 March 2015

£000 £000 £000 £000

Pro forma consolidated statement of comprehensive income

Commission and fees 85,331 - - 85,331 Investment income 89 - - 89 Salaries and associated expenses (50,487) - - (50,487) Other operating costs (40,949) - - (40,949) Depreciation and amortisation charges (5,303) - - (5,303) Group operating loss (11,319) - - (11,319) Analysed as:

Group operating profit before exceptional items 7,348 - - 7,348 (Loss) on disposal of businesses and investments (340) - - (340) Group reorganisation costs (4,853) - - (4,853) Regulatory costs (1,051) - - (1,051) Group financial restructuring costs (12,423) - - (12,423)

Group operating loss (11,319) - - (11,319) Finance costs(4) (238) - (22,007)(a) (22,245) Finance income(5) 93 - - 93

Loss before taxation (11,464) - (22,007) (33,471) Income tax (expense) / credit (6) (224) - 4,456(b) 4,232

Loss on continuing operations (11,688) - (17,551) (29,239)

Loss for the period from discontinued operations, net of tax (366) 366(a) - -

Total comprehensive (loss)/profit for the period (12,054) 366 (17,551) (29,239)

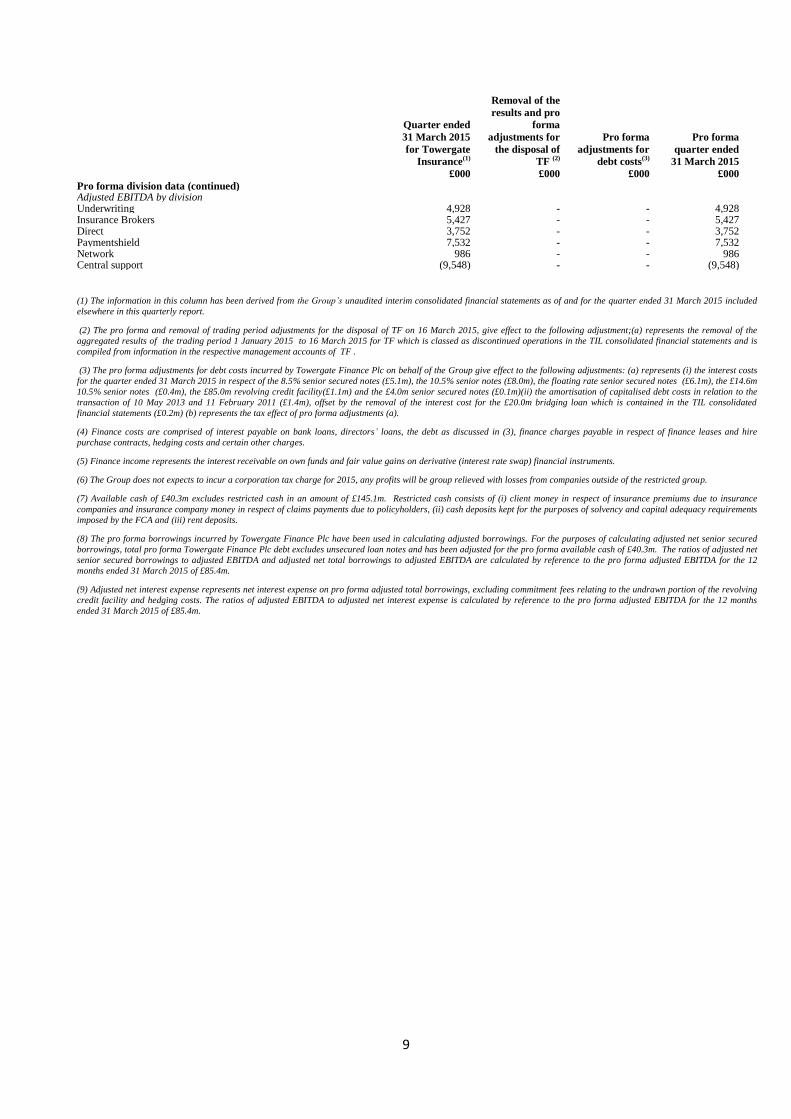

Other pro forma data Available cash(7) 40,280 - - 40,280 EBITDA 12,404 - - 12,404 Adjusted EBITDA 13,077 - - 13,077 Adjusted EBITDA margin - - - 15.33% Adjusted EBITDA 12 months to 31 March 2015 86,191 (799) - 85,392 Capital expenditure 1,664 (1) - 1,663 Adjusted net senior borrowings(8) - - - 674,700 Adjusted net total borrowings(8) - - - 1,010,418 Adjusted net interest expense(9) - - - 22,250 Ratio of adjusted net senior secured borrowings to adjusted EBITDA(8) - - - 7.90x Ratio of adjusted net total borrowings to adjusted EBITDA(8) - - - 11.83x Ratio of adjusted EBITDA to adjusted net interest expense(9) - - - 3.84x

Pro forma division data Turnover by division Underwriting 19,498 - - 19,498 Insurance Brokers 36,666 - - 36,666 Direct 14,980 - - 14,980 Paymentshield 11,107 - - 11,107 Network 3,067 - - 3,067 Central support 13 - - 13

9

Quarter ended

31 March 2015

for Towergate

Insurance(1)

Removal of the

results and pro

forma

adjustments for

the disposal of

TF (2)

Pro forma

adjustments for

debt costs(3)

Pro forma

quarter ended

31 March 2015

£000 £000 £000 £000

Pro forma division data (continued) Adjusted EBITDA by division Underwriting 4,928 - - 4,928 Insurance Brokers 5,427 - - 5,427 Direct 3,752 - - 3,752 Paymentshield 7,532 - - 7,532 Network 986 - - 986 Central support (9,548) - - (9,548)

(1) The information in this column has been derived from the Group’s unaudited interim consolidated financial statements as of and for the quarter ended 31 March 2015 included

elsewhere in this quarterly report.

(2) The pro forma and removal of trading period adjustments for the disposal of TF on 16 March 2015, give effect to the following adjustment;(a) represents the removal of the

aggregated results of the trading period 1 January 2015 to 16 March 2015 for TF which is classed as discontinued operations in the TIL consolidated financial statements and is

compiled from information in the respective management accounts of TF .

(3) The pro forma adjustments for debt costs incurred by Towergate Finance Plc on behalf of the Group give effect to the following adjustments: (a) represents (i) the interest costs

for the quarter ended 31 March 2015 in respect of the 8.5% senior secured notes (£5.1m), the 10.5% senior notes (£8.0m), the floating rate senior secured notes (£6.1m), the £14.6m

10.5% senior notes (£0.4m), the £85.0m revolving credit facility(£1.1m) and the £4.0m senior secured notes (£0.1m)(ii) the amortisation of capitalised debt costs in relation to the

transaction of 10 May 2013 and 11 February 2011 (£1.4m), offset by the removal of the interest cost for the £20.0m bridging loan which is contained in the TIL consolidated

financial statements (£0.2m) (b) represents the tax effect of pro forma adjustments (a).

(4) Finance costs are comprised of interest payable on bank loans, directors’ loans, the debt as discussed in (3), finance charges payable in respect of finance leases and hire

purchase contracts, hedging costs and certain other charges.

(5) Finance income represents the interest receivable on own funds and fair value gains on derivative (interest rate swap) financial instruments.

(6) The Group does not expects to incur a corporation tax charge for 2015, any profits will be group relieved with losses from companies outside of the restricted group.

(7) Available cash of £40.3m excludes restricted cash in an amount of £145.1m. Restricted cash consists of (i) client money in respect of insurance premiums due to insurance

companies and insurance company money in respect of claims payments due to policyholders, (ii) cash deposits kept for the purposes of solvency and capital adequacy requirements

imposed by the FCA and (iii) rent deposits.

(8) The pro forma borrowings incurred by Towergate Finance Plc have been used in calculating adjusted borrowings. For the purposes of calculating adjusted net senior secured

borrowings, total pro forma Towergate Finance Plc debt excludes unsecured loan notes and has been adjusted for the pro forma available cash of £40.3m. The ratios of adjusted net

senior secured borrowings to adjusted EBITDA and adjusted net total borrowings to adjusted EBITDA are calculated by reference to the pro forma adjusted EBITDA for the 12

months ended 31 March 2015 of £85.4m.

(9) Adjusted net interest expense represents net interest expense on pro forma adjusted total borrowings, excluding commitment fees relating to the undrawn portion of the revolving

credit facility and hedging costs. The ratios of adjusted EBITDA to adjusted net interest expense is calculated by reference to the pro forma adjusted EBITDA for the 12 months

ended 31 March 2015 of £85.4m.

10

Unaudited pro forma financial information and other data

for the quarter ended 31 March 2015

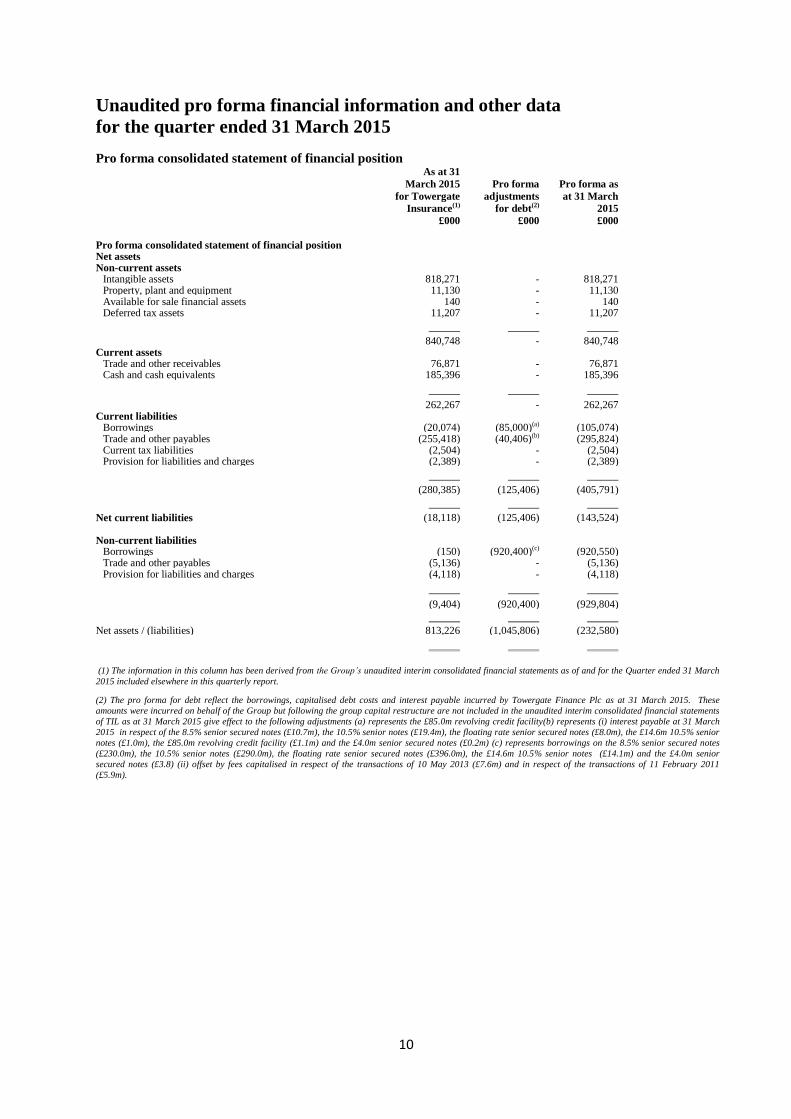

Pro forma consolidated statement of financial position

As at 31

March 2015

for Towergate

Insurance(1)

Pro forma

adjustments

for debt(2)

Pro forma as

at 31 March

2015

£000 £000 £000

Pro forma consolidated statement of financial position Net assets Non-current assets

Intangible assets 818,271 - 818,271 Property, plant and equipment 11,130 - 11,130 Available for sale financial assets 140 - 140 Deferred tax assets 11,207 - 11,207

840,748 - 840,748 Current assets

Trade and other receivables 76,871 - 76,871 Cash and cash equivalents 185,396

- 185,396

262,267 - 262,267 Current liabilities

Borrowings (20,074) (85,000)(a) (105,074) Trade and other payables (255,418) (40,406)(b) (295,824) Current tax liabilities (2,504) - (2,504) Provision for liabilities and charges (2,389) - (2,389)

(280,385)

85)

(125,406) (405,791)

Net current liabilities (18,118) (125,406) (143,524) Non-current liabilities

Borrowings (150) (920,400)(c) (920,550) Trade and other payables (5,136) - (5,136) Provision for liabilities and charges (4,118) - (4,118)

(9,404) (920,400) (929,804)

Net assets / (liabilities) 813,226 (1,045,806) (232,580)

(1) The information in this column has been derived from the Group’s unaudited interim consolidated financial statements as of and for the Quarter ended 31 March

2015 included elsewhere in this quarterly report.

(2) The pro forma for debt reflect the borrowings, capitalised debt costs and interest payable incurred by Towergate Finance Plc as at 31 March 2015. These

amounts were incurred on behalf of the Group but following the group capital restructure are not included in the unaudited interim consolidated financial statements

of TIL as at 31 March 2015 give effect to the following adjustments (a) represents the £85.0m revolving credit facility(b) represents (i) interest payable at 31 March

2015 in respect of the 8.5% senior secured notes (£10.7m), the 10.5% senior notes (£19.4m), the floating rate senior secured notes (£8.0m), the £14.6m 10.5% senior

notes (£1.0m), the £85.0m revolving credit facility (£1.1m) and the £4.0m senior secured notes (£0.2m) (c) represents borrowings on the 8.5% senior secured notes

(£230.0m), the 10.5% senior notes (£290.0m), the floating rate senior secured notes (£396.0m), the £14.6m 10.5% senior notes (£14.1m) and the £4.0m senior

secured notes (£3.8) (ii) offset by fees capitalised in respect of the transactions of 10 May 2013 (£7.6m) and in respect of the transactions of 11 February 2011

(£5.9m).

11

Unaudited pro forma financial information and other data for the quarter ended 31 March 2014

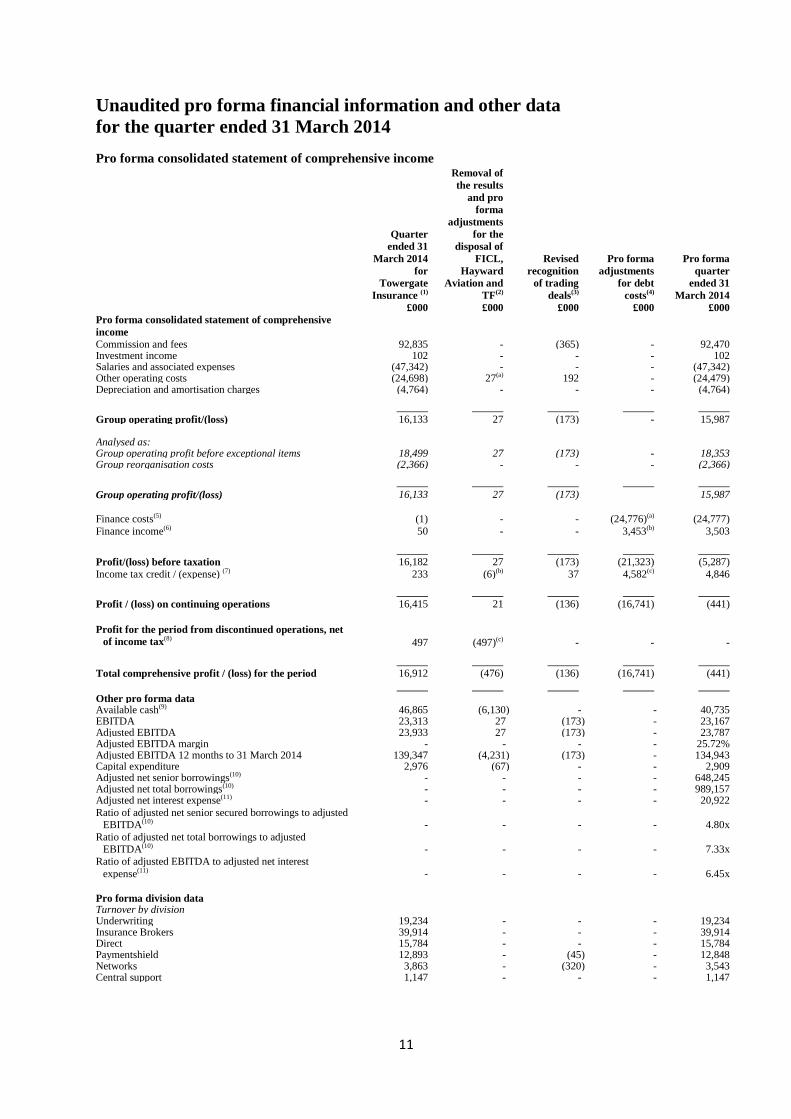

Pro forma consolidated statement of comprehensive income

Quarter

ended 31

March 2014

for

Towergate

Insurance (1)

Removal of

the results

and pro

forma

adjustments

for the

disposal of

FICL,

Hayward

Aviation and

TF(2)

Revised

recognition

of trading

deals(3)

Pro forma

adjustments

for debt

costs(4)

Pro forma

quarter

ended 31

March 2014

£000 £000 £000 £000 £000

Pro forma consolidated statement of comprehensive

income

Commission and fees 92,835 - (365) - 92,470 Investment income 102 - - - 102 Salaries and associated expenses (47,342) - - - (47,342) Other operating costs (24,698) 27(a) 192 - (24,479) Depreciation and amortisation charges (4,764) - - - (4,764)

Group operating profit/(loss) 16,133

27 (173) - 15,987

Analysed as:

Group operating profit before exceptional items 18,499 27 (173) - 18,353 Group reorganisation costs (2,366) - - - (2,366)

Group operating profit/(loss) 16,133 27 (173) 15,987

Finance costs(5) (1) - - (24,776)(a) (24,777)

Finance income(6) 50 - - 3,453(b) 3,503

Profit/(loss) before taxation 16,182 27 (173) (21,323) (5,287)

Income tax credit / (expense) (7) 233 (6)(b) 37 4,582(c) 4,846

Profit / (loss) on continuing operations 16,415 21 (136) (16,741) (441)

Profit for the period from discontinued operations, net

of income tax(8) 497 (497)(c) - - -

Total comprehensive profit / (loss) for the period 16,912 (476) (136) (16,741) (441)

Other pro forma data Available cash(9) 46,865 (6,130) - - 40,735 EBITDA 23,313 27 (173) - 23,167 Adjusted EBITDA 23,933 27 (173) - 23,787 Adjusted EBITDA margin - - - - 25.72% Adjusted EBITDA 12 months to 31 March 2014 139,347 (4,231) (173) - 134,943 Capital expenditure 2,976 (67) - - 2,909 Adjusted net senior borrowings(10) - - - - 648,245 Adjusted net total borrowings(10) - - - - 989,157 Adjusted net interest expense(11) - - - - 20,922

Ratio of adjusted net senior secured borrowings to adjusted EBITDA(10) - - - - 4.80x

Ratio of adjusted net total borrowings to adjusted EBITDA(10) - - - - 7.33x

Ratio of adjusted EBITDA to adjusted net interest

expense(11) - - - - 6.45x

Pro forma division data Turnover by division Underwriting 19,234 - - - 19,234 Insurance Brokers 39,914 - - - 39,914 Direct 15,784 - - - 15,784 Paymentshield 12,893 - (45) - 12,848 Networks 3,863 - (320) - 3,543 Central support 1,147 - - - 1,147

12

Quarter

ended 31

March 2014

for

Towergate

Insurance (1)

Removal of

the results

and pro

forma

adjustments

for the

disposal of

FICL,

Hayward

Aviation and

TF(2)

Revised

recognition

of trading

deals(3)

Pro forma

adjustments

for debt

costs(4)

Pro forma

quarter

ended 31

March 2014

£000 £000 £000 £000 £000

Pro forma division data (continued) Adjusted EBITDA by division Underwriting 6,765 - 4 - 6,769 Insurance Brokers 7,388 (181) (98) - 7,109 Direct 5,198 - - - 5,198 Paymentshield 9,015 - 55 - 9,070 Network 1,800 - (320) - 1,480 Central support (6,233) 208 186 - (5,839)

(1) The information in this column has been derived from the Group’s unaudited interim consolidated financial statements as of and for the Quarter ended 31 March 2014

included elsewhere in this quarterly report.

(2) The pro forma and removal of trading period adjustments for the disposal of Hayward Aviation on 23 December 2014, FICL on 29 August 2014 and TF on 16 March 2015,

give effect to the following adjustments:(a) represents the trading period 1 January 2014 to 31 March 2014 for FICL and is compiled from information in their respective

management accounts (b) represents the tax effect of pro forma adjustment (a); (c) represents the removal of the aggregated results of the trading period 1 January 2014 to 31

March 2014 for Hayward Aviation and TF which are classed as discontinued operations in the TIL consolidated financial statements.

(3)The Group as part of year end revised the basis of estimation of revenue recognition related to long term deal income; this adjustment makes this year end adjustment in the

period to which it relates. Year end adjustments to expense charges have been recognised in the period to which they relate.

(4) The pro forma adjustments for debt costs incurred by Towergate Finance Plc on behalf of the Group give effect to the following adjustments: (a) represents (i) the interest

costs for the quarter to 31 March 2014 in respect of the 8.5% senior secured notes (£4.9m), the 10.5% senior notes (£7.6m), the floating rate senior secured notes (£5.9m), the

£14.6m 10.5% senior notes (£0.4m), the interest rate swap agreement (£3.7m), the £85m revolving credit facility (£0.8m) and the £4.0m senior secured notes (£0.1m)(ii) the

amortisation of capitalised debt costs in relation to the transaction of 10 May 2013 and 11 February 2011 (£1.4m) (b)represents the fair value gain on the interest rate swap

derivative (c) represents the tax effect of pro forma adjustments (a) and (b).

(5) Finance costs are comprised of interest payable on bank loans, directors’ loans, the debt as discussed in (4), finance charges payable in respect of finance leases and hire

purchase contracts, hedging costs and certain other charges.

(6) Finance income represents the interest receivable on own funds and fair value gains on derivative (interest rate swap) financial instruments.

(7) The Group does not expects to incur a corporation tax charge for 2014, any profits will be group relieved with losses from companies outside of the restricted group

(8) On 23 December2014 the Group disposed of Hayward Aviation. The Group also committed to a plan to dispose of its TF business. The results of both businesses have been

classed as discontinued operations in the statutory accounts for the year ended 31 December 2014 and the consolidated statement of comprehensive income for the quarter

ended 31 March 2014 has been restated to show TF and Hayward Aviation as discontinued operations.

(9) Pro forma available cash of £40.7m excludes restricted cash in an amount of £148.6m. Restricted cash consists of (i) client money in respect of insurance premiums due to

insurance companies and insurance company money in respect of claims payments due to policyholders, (ii) cash deposits kept for the purposes of solvency and capital

adequacy requirements imposed by the FCA and (iii) rent deposits.

(10) The pro forma borrowings incurred by Towergate Finance Plc have been used in calculating adjusted borrowings. For the purposes of calculating adjusted net senior

secured borrowings, total pro forma Towergate Finance Plc debt excludes unsecured loan notes and has been adjusted for the pro forma available cash of £40.7m. The ratios

of adjusted net senior secured borrowings to adjusted EBITDA and adjusted net total borrowings to adjusted EBITDA are calculated by reference to the pro forma adjusted

EBITDA for the 12 months ended 31 March 2014 of £134.9m.

(11) Adjusted net interest expense represents net interest expense on pro forma adjusted total borrowings, excluding commitment fees relating to the undrawn portion of the

revolving credit facility and hedging costs. The ratios of adjusted EBITDA to adjusted net interest expense is calculated by reference to the pro forma adjusted EBITDA for the

12 months ended 31 March 2014 of £134.9m.

13

Unaudited pro forma financial information and other data

for the quarter ended 31 March 2014

Pro forma consolidated statement of financial position

As at 31

March 2014

for Towergate

Insurance(1)

Pro forma

adjustments

for debt (2)

Pro forma

adjustments for

the disposal of

Hayward, FICL

and TF(3)

Pro forma as

at 31 March

2014

£000 £000 £000 £000

Pro forma consolidated statement of financial position

Net assets Non-current assets

Intangible assets 1,414,385 - (48,505) 1,365,880 Property, plant and equipment 11,104 - (319) 10,785 Available for sale financial assets 203 - (16) 187 Deferred tax assets 7,437 - (96) 7,341

1,433,129 - (48,936) 1,384,193 Current assets

Trade and other receivables 239,498 - (8,006) 231,492 Cash and cash equivalents 195,483 - (12,698) 182,785

434,981 - (20,704) 414,277

Current liabilities

Borrowings (92) (59,000)(a) - (59,092)

Trade and other payables (229,826) (14,315)(b) 8,570 (235,571) Derivative financial instruments - (14,857)(c) - (14,857) Current tax liabilities (22,657) - 769 (21,888) Provision for liabilities and charges (3,473) - 248 (3,225)

(256,048) (88,172) 9,587 (334,633)

Net current assets / (liabilities) 178,933 (88,172) (11,117) 79,644

Non-current liabilities Borrowings (160) (913,535)(d) - (913,695) Trade and other payables (19,863) - - (19,863) Provision for liabilities and charges (3,147) - - (3,147)

(23,170) (913,535) - (936,705)

Net assets / (liabilities) 1,588,892 (1,001,707) (60,053) 527,132

(1) The information in this column has been derived from the Group’s unaudited interim consolidated financial statements as of and for the Quarter ended 31 March

2014 included elsewhere in this quarterly report.

(2) The pro forma adjustments for debt reflect the borrowings, capitalised debt costs and interest payable incurred by Towergate Finance Plc as at 31 March 2014.

These amounts were incurred on behalf of the Group but following the group capital restructure are not included in the unaudited interim consolidated financial

statements of TIL give effect to the following adjustments (a) represents the amount drawn on the £85m revolving credit facility(b) represents (i) interest payable at 31

March 2014 in respect of the 8.5% senior secured notes (£2.4m), the 10.5% senior notes (£3.8m), the floating rate senior secured notes (£3.8m), the interest rate

swap agreement (£3.7m), the £14.6m 10.5% senior notes (£0.2m), the £85.0m revolving credit facility(£0.3m) and the £4.0m senior secured notes (£0.1m) (c)

represents the fair value of Towergate Finance plc’s interest rate swap derivative which expires on December 31, 2014 (d) represents borrowings on the senior

secured notes (£230m), the 10.5% senior notes (£290m), the floating rate senior secured notes (£396.0m), the £14.6m 10.5% senior notes (£14.0m) and the £4.0m

senior secured notes (£3.8) (ii) offset by fees capitalised in respect of the transactions of 10 May 2013 (£10.7m) and in respect of the transactions of 11 February 2011

(£9.6m).

(3) The pro forma adjustments for the disposal of Hayward Aviation on 23 December 2014, FICL on 29 August 2014 and TF on 16 March 2015 represents the assets

and liabilities at 31 March 2014 contained within the TIL consolidated statement of financial position at this date.

14

Management’s discussion and analysis of financial condition and results of

operations

Significant factors affecting results of operations

Insurance industry dynamics

Insurance cycle

The insurance industry is inherently cyclical, meaning that the pricing and terms and conditions of cover vary over

time. The insurance cycle is characterised by soft and hard market conditions. Soft conditions reflect muted

demand, low or negative premium rates, widening coverage and the free availability of capital. As a result soft

markets generally result in lower level of underlying profitability for both insurance carriers and intermediaries.

Hard market conditions generally follow a periodic of heightened loss activity and capital erosion. As a result the

supply of insurance is limited, rating or pricing increases and coverage narrows. It follows that underlying

profitability for both insurance carriers and intermediaries generally rises in a hard market, although there can be a

lag between the market turn and the effect on reported profits.

Insurance rating

The outlook for rating is likely to remain soft for some time reflecting the ready availability of capital, the absence

of major loss events and the absence of withdrawal of underwriting capacity or of insurance carriers from the

markets in which the Group operates.

Commissions and fees

Insurance brokers and underwriting agents derive the majority of their revenue from commissions and fees.

Commissions are generally based on insurance premiums and negotiated commission rates. Fees are paid for

individual services based on negotiated amounts. As rating is currently soft, commission income is relatively

depressed.

The Group also enters into profit sharing arrangements, fees for the provision of payment instalment plans and other

one off deals with third parties which are recognised over the life of the relevant arrangement or when they can be

measured with reasonable certainty. Such trading deal income includes contributions to marketing or product

development, volume payments and profit commissions receivable. The amount and timing of trading deal income

is inherently uncertain and individual amounts may be material. Amounts accrued at the year end and recognised as

assets may be judgemental. A change in estimation of trading deal income could have a material effect on the

Group’s financial performance.

Acquisitions and disposals

The Group has pursued a strategy of acquisitions to deliver scale advantage.

This acquisition strategy has been focussed on both intermediary (or broking) business and on underwriting

agencies. In evaluating potential acquisitions, the Group considers the market position, growth prospects and

underwriting performance of target businesses, as well as their geographic, distribution channel and product mix fit

with its existing operations. The price paid for acquisitions is based primarily on the commission and fee income

streams of the target business and the potential to increase such streams following the acquisition.

Acquisitions affect the results of operations in several ways. First, the results for the period during which an

acquisition takes place includes the results of the acquired business in that and subsequent accounting periods.

Second, the results for subsequent periods may be affected by applying the Group’s enhanced commission

arrangements to the policies that acquired business places, and by cross-selling products. Third, the results for

subsequent periods may be affected if synergies are realised from shared services and infrastructure.

The Group made seven acquisitions in the fifteen months to 31 March 2015 (consisting of two companies and five

portfolios) for an aggregate consideration of approximately £21.9m. The Group disposed of five businesses during

this period. The material transactions were:

On 17 April 2014 the Group completed the acquisition of Arista Insurance (Arista), a leading UK

commercial managing general agent specialising in property, liability and motor insurance, for a

consideration of £16.7m. Arista has a well-defined regional distribution network and fits well with the

Group’s strategy of acquiring specialist businesses with strong growth potential

On 29 August 2014 the Group disposed of Folgate Insurance (FICL) to Anglo London for a consideration

of £1.9m. Folgate Insurance was an insurance company in run off and as such operated outside the

Group’s core UK specialist lines and small and medium sized businesses (SME) markets

15

On 23 December 2014 the Group disposed of Hayward Aviation Limited (Hayward Aviation) to Jardine

Lloyd Thompson for a consideration of £27.0m. As an international aviation insurance broker, Hayward

Aviation operated outside the Group’s core UK specialist personal lines and SME markets

On 16 March 2015 the Group disposed of its Towergate Financial (TF) business to Palatine Private Equity

for a consideration of £8.6m. The Towergate Financial business was a provider of independent financial

and mortgage advice and operated outside the Group’s core UK specialist personal lines and SME markets

Seasonality

The Group experiences some seasonality in the volumes of insurance policies transacted and, consequently, in

commission and fees. The Group has historically transacted less business from November to February than in most

other months of the year. Accordingly, although volumes typically increase in March, commission and fees for the

first quarter tends to be lower than the second and third quarter, before declining again in the fourth quarter.

Description of key line items

Set out below is a brief description of the composition of the key line items of the Group’s income statement.

Commission and fees

Commissions and fees represents income received from third parties net of commissions paid to sub-agents and

brokers. When a sub-agent or broker refers a customer to the Group, it typically shares that commission with the

sub-agent or broker. For purposes of the analysis of results below, commission and fees are analysed by division.

Income from trading deals with insurers is included in commission and fees.

Investment income

Investment income represents the interest received on restricted cash.

Salaries and associated expenses

Salaries and associated expenses represent the costs of staff and staff related costs incurred in the operations of the

Group and will include staff related costs for exceptional spend not in the normal course of operations of the Group.

Other operating expenses

Other operating expenses represent all other administrative costs which are not staff or staff related and will include

exceptional spend not in the normal course of operations of the Group.

Depreciation and amortisation charges

Depreciation and amortisation charges represent the depreciation charge and the amortisation of intangible assets.

Impairment of goodwill

Impairment of goodwill represents the impairment of the goodwill balance based on the value in use or fair value

less costs to sell of the Group. This is conducted at a cash generating unit level which reflects the divisional

structure of the Group.

Finance costs

Finance costs represent the interest and other financing costs of the Group.

Finance income

Finance income represents the interest on available cash and the change in fair value of any financial instrument in

the statement of financial condition.

Impairment of associate

Impairment of associate represents the write down in the fair value of associates in the statement of financial

condition.

Income tax

Income tax represents the addition of the current income tax charge based on the profit or loss before taxation and

the deferred tax charge based on the temporary timing differences between the carrying value of assets in the

statement of financial condition and the amount carried for tax purposes.

Group financial performance

The following discussion and analysis compares pro forma consolidated results of operations for the quarter ended

16

31 March 2015 and pro forma consolidated results of operations for the quarter ended 31 March 2014.

Turnover and EBITDA by division

The tables below set out the commission and fees and adjusted earnings results for the divisions of the Group:

Pro forma basis

Commission and fees

2015

£m

2014

£m

Insurance Brokers 36.7 39.9

Direct 15.0 15.8

Underwriting 19.5 19.2

Paymentshield 11.1 12.9

Network 3.0 3.5

Other 0.0 1.2

85.3 92.5

Pro forma basis

Adjusted earnings

2015

£m

2014

£m

Insurance Brokers 5.4 7.1

Direct 3.8 5.2

Underwriting 4.9 6.8

Paymentshield 7.5 9.0

Network 1.0 1.5

Other (9.5) (5.8)

13.1 23.8

Insurance Brokers: commission and fees declined by 8.1% compared to last year. Adjusted earnings declined by

23.7% compared to last year. Commission and fees for Q1 continue to be impacted by the change programme and

uncertainty caused by the Group financial restructuring. The impact of the reduced income was mitigated by

reduced expenses as the benefits of the change programme start to emerge. Gross margins remain strong at 20%,

consistent with last year.

Direct: commission and fees declined by 5.1% compared to last year. Adjusted earnings declined by 27.8%

compared to last year. This is due to a more competitive environment leading to reduced retention rates and new

business. There are some early signs of improvement with new business growing and retention rates ahead of last

year’s average.

Underwriting: commission and fees increased by 1.4% compared to last year. Adjusted earnings declined by

27.2% compared to last year. Commission and fees have increased due to the acquisition of Arista, which has also

led to an increase in expenses. Organic commission and fees have declined due to the impact of the financial

restructuring and the challenging rate environment. Underlying retention levels remain steady and a long term

strategic deal has been extended with Allianz which will provide up to £770m of maximum capacity.

Paymentshield: commission and fees declined by 13.6% compared to last year. Adjusted earnings declined by

17.0% compared to last year. Commission and fees continue to be affected by the reduction in the mortgage

premium protection insurance product. Household panel quote conversion has stabilised, with household new

business volumes and margin improving over the quarter.

Network: commission and fees declined by 13.4% compared to last year. Adjusted earnings declined by 33.4%

compared to last year. Commission and fees has reduced due to one off income items included in 2014,

discontinued insurer deals and corrective rating actions.

Investment income

Investment income has fallen by £0.01m (12.7%); this is due to a fall in the average return during 2014.

17

Salaries and associated expenses

Salaries and associated expenses have risen by £3.1m (6.6%); staff numbers have remained stable in the quarter

with the increase in cost reflecting as increase in pay of 2.5% last year and provision for bonuses.

Other operating costs

Other operating costs have risen by £16.5m (67.3%); this is mainly due to the exceptional items of £12.4m relating

to the Group financial restructuring, £1.1m in respect of regulatory costs and an increase of £2.5m in relation to

Group reorganisation costs.

Depreciation and amortisation charge

The depreciation and amortisation charge has risen by £0.5m (11.3%); this is due to an increase in the level of

software development costs resulting from the change programmes and of intangible assets following acquisitions

made in 2013 and 2014.

Finance costs

Finance costs have fallen by £2.5m (10.2%); this is due to the settlement of derivative contracts which were used to

hedge floating rate debt.

Finance income

Finance income has risen by £3.4m (97.3%); this represents the change in value of the derivative instrument used to

hedge floating rate debt.

Group change programmes

During 2014 the Group undertook a number of major change programmes. These programmes were designed to

improve efficiency across Towergate, to build regulatory resilience, to position the Group to exploit future scale

advantages and to enhance the customer proposition.

Group reorganisation costs

In April 2014 the Group announced the creation of a new business unit in Manchester. This unit is designed to

service small premium business through a dedicated contact centre with extended opening times. In addition the

Group has undertaken a site consolidation to rationalise its office network across its Insurance Brokers, Direct and

Underwriting businesses.

In February 2014 the Group began a major finance transformation with the creation of accounting centres in Leeds

and Maidstone. All insurance broking accounting and client money processing was consolidated into an in-house

facility in Leeds. In parallel, financial accounting and management accounting was centralised in a second in-house

facility in Maidstone. These two centres are developing standardised policies and procedures and will allow future

investment to be focused and prioritised. They will also allow IT hardware and software used by the Group to be

streamlined and re-focused with the objective, over time, of improving control while exploiting scale advantage.

These initiatives had an aggregate cost of £4.9m during Q1 2015 (Q1 2014: £2.4m), which has been treated as an

exceptional item.

Regulatory costs

The Group has incurred exceptional regulatory costs of £1.1m in Q1 2015 (Q1 2014: £Nil). These items primarily

represent costs incurred in relation to regulatory investigations into advice provided by Towergate Financial on

pension Enhanced Transfer Values (ETV) and Unregulated Collective Investment Schemes (UCIS), investigation

into client money issues and a strengthening of the Group’s control framework.

Group financial restructuring costs

Towergate has undergone a financial restructuring which completed in April 2015. Costs of £12.4m (Q1 2014:

£Nil) related to this restructuring have been recognised in the Q1 2015 results.

Financial strength

On a statutory basis the Group had net assets of £815.7m at 31 March 2015 (£1,588.9m at 31 March 2014) and net

current liabilities of £15.0m at 31 March 2015 (net current assets of £178.9m at 31 March 2014). The Group had

regulatory capital requirements within its regulated companies of £19.8m at 31 March 2015 and £19.9m at 31 March

2014.

Following the restructuring on 2 April 2015 the level of debt supported by the Group has significantly reduced and

18

the overall leverage position of the Group has reduced from 10.4x at 31 March 2015 to 4.6x after adjusting to pro

forma for the Group financial restructuring on 2 April 2015.

Cash flow

For Q1 2015 the net cash flow generated from operating activities was an outflow of £32.2m (Q1 2014: £17.7m) and

net decrease in cash balances of £15.0m (Q1 2014: £13.1m).

The cash generated from operating activities has declined due to the level of expenditure on exceptional items, being

£18.3m Q1 2015 and £2.4m Q1 2014. Cash from investing activities is positive due to the sale of TF in the period.

The cash generated from financing activity is positive reflecting the £20.0m bridging loan in the period; for Q1 2014

the positive inflow was due to the £12.1m cash injection by Advent to fund the acquisition of Arista.

Outlook

Q1 2015 was a challenging period. Confidence in Towergate was tested with performance in all divisions affected

by both the Group financial restructuring and the change programme.

However significant progress has been made in multiple areas. Towergate has attracted long term supportive

shareholders in Highbridge, KKR and Sankaty. Over the last fifteen months much of the comprehensive change

programme has been implemented. Towergate continues to attract talent. The Board remains focussed on

operational delivery in 2015 and there are some early signs of recovery as the business stabilises.

The Group is focussed on retention and new business and aims to deliver this through a concentration on customer

service and operational excellence. The expectation is that expenses will fall through the completion of the change

programme and continued integration of businesses. The Board will continue to invest in the business to deliver

profitable growth in its chosen markets.

19

Contractual obligations

The following table summarises material contractual obligations as of 31 March 2015 and includes disclosures for

the pro forma debt held by Towergate Finance plc at that date:

Contractual obligations

Total

Less than 1

year 1-5 years

More than 5

years

£m £m £m £m

Senior secured notes 233.9 - 233.9 -

Revolving credit facility 85.0 85.0 - -

Senior secured floating rate notes 396.0 - 396.0 -

10.5% senior notes 304.1 - 304.1 -

Bridging loan 20.0 20.0 - -

Other obligations(1) 11.4 9.0 2.4 -

Operating leases 46.5 12.5 25.3 8.7

Total contractual obligations 1,096.9 126.5 961.7 8.7

(1) Represents deferred consideration and redemption liability on non-controlling interest put options in an amount of £11.1m and obligations under finance leases and hire purchase contracts in an amount of £0.3m.

Debt commitments are discussed further in the section description of debt

Deferred consideration

Deferred consideration is payable in respect of certain acquisitions based on the performance of the acquired

business typically in the 24-month period following the acquisition and in connection with put and call options

granted to shareholders of businesses we have acquired in respect of the remaining minority interest of such

shareholders typically for the 36-month period following the acquisition.

Operating leases

Contractual obligations for operating leases reflect the Group’s annual commitments under non-cancellable

operating leases.

Off balance sheet arrangements

The Group had no off balance sheet arrangements at 31 March 2015.

Contingent liabilities

ETV and UCIS

The Group continues to be in discussions with the FCA in relation to past advice provided by the Towergate

Financial Group businesses on ETV and UCIS. The independent file reviews for both investigations are ongoing.

Customer contact, which will be a key factor in determining the extent of the Group’s redress obligation,

commenced in Q1 2015 and is expected to be phased over three years. Payment of any necessary redress is

expected to occur over similar periods of time once the relevant customers have been contacted and the redress

methodology has been agreed. Payments are expected to commence in Q3 2015.

Given the number of material uncertainties that continue to exist, it is not yet possible to make a reliable estimate of

the Group’s ultimate liability in connection with these investigations. However, purely for the purposes of

developing business plans and cash flow projections for the Group, it has adopted a range of £65.0m to £85.0m in

potential redress costs for ETV and UCIS in aggregate, excluding costs and expenses.

This internal range is derived from a set of assumptions based on currently available information. As explained

above, in view of the material uncertainties all such assumptions are subject to change and the Group can give no

assurances as to whether its ultimate liability will be within this range or whether it will be lower or higher. The

ultimate liability for ETV and UCIS may, therefore, be materially different to this range.

In addition, the foregoing does not include any recoveries that may be available either from relevant third parties or

under the Group’s insurance arrangements, both of which the Group continues to pursue. The maximum

recoverable amount under insurance arrangements is £12.0m (subject to a deductible) in addition to costs, although

the ultimate extent and timing of any recoverability remains uncertain.

20

Appendix 1 – Interim condensed consolidated financial statements of Towergate Insurance Limited

Contents

Interim Report for the three months to 31 March 2015 2-3

Condensed consolidated statement of comprehensive income 4

Condensed consolidated statement of financial position 5

Condensed consolidated statement of changes in equity 6

Condensed consolidated statement of cash flows 7

Notes 8-18

2

Interim Report for the three months to 31 March 2015

The following items have been noted as updates to ongoing issues or a summary of transactions to bring to the attention of the

reader:

Updates on the ongoing issues with the Financial Conduct Authority (FCA) in relation to client money and advice

provided by the Towergate Financial business

A summary of the Group financial restructuring

Senior management changes

A summary financial review and outlook

FCA

During Q3 2013 the Group identified that £15.0m of client and insurer monies had been misallocated to an unrestricted account

between November 2007 and January 2011. As soon as the misallocation was confirmed management transferred £15.0m to

the relevant client and insurer accounts. The FCA was notified and investigations into this matter are continuing.

The Group is continuing discussions with the FCA in connection with past advice provided by the Towergate Financial

businesses on pension Enhanced Transfer Values (ETV) and Unregulated Collective Investment Schemes (UCIS). There

remain material uncertainties over the level of redress costs as customer contact has commenced but is not significantly

complete and the redress methodology has not been agreed. Purely for internal purposes a range of £65.0m-£85.0m is used in

cash flow projections. Given the level of uncertainty this item remains a contingent liability in the Group’s financial

statements.

Acquisitions and disposals

The Group made seven acquisitions in the fifteen months to 31 March 2015 (consisting of two companies and five portfolios)

for an aggregate consideration of approximately £21.9m. The Group disposed of five businesses during this period. The

material transactions were:

On 17 April 2014 the Group completed the acquisition of Arista Insurance Limited (Arista), a leading UK commercial

managing general agent specialising in property, liability and motor insurance, for a consideration of £16.7m. Arista

has a clearly defined regional distribution network and fits well with the Group’s strategy of acquiring specialist

businesses with strong growth potential

On 29 August 2014 the Group disposed of Folgate Insurance Company Limited (FICL) to Anglo London for a

consideration of £1.9m. Folgate Insurance was an insurance company in run off and as such operated outside the

Group’s core UK specialist lines and small and medium sized businesses (SME) markets

On 23 December 2014 the Group disposed of The Hayward Holding Group Limited (Hayward Aviation) to Jardine

Lloyd Thompson for a consideration of £27.0m. As an international aviation insurance broker, Hayward Aviation

operated outside the Group’s core UK specialist personal lines and SME markets

On 16 March 2015 the Group disposed of its Towergate Financial business (TF) to Palatine Private Equity for a

consideration of £8.6m. The Towergate Financial business was a provider of independent financial and mortgage

advice and operated outside the Group’s core UK specialist personal lines and SME markets

Group financial restructuring

On 2 April 2015 the Group completed a financial restructuring in relation to the senior secured creditors and senior unsecured

creditors of Towergate Finance plc, an intermediate parent company. As part of these arrangements TIG Finco plc (a newly

formed holding company) acquired the Group for consideration of £735.0m made up of the issue of £425.0m of Senior Secured

Notes by TIG Finco plc and the issue of new shares in TIG Finco plc’s indirect parent company, TIG Topco Limited, valued at

£310.0m.

As a result of these arrangements, in April 2015 Highbridge Principal Strategies LLC became the Group’s majority

shareholder.

As part of the financial restructuring, additional capital of £122.0m was received by the Group through the issue by TIG Topco

Limited of new shares for £50.0m and the issue by TIG Finco plc of £75.0m of Super Senior Secured Notes at a discount of

£3.0m. The additional funds provide liquidity to the Group and have enabled it to fund the costs of the restructuring of £42.0m,

the vesting of long term incentive plans which have crystallised or will in the future crystallise as a result of the restructuring of

£30.0m, retention bonuses of £8.0m and minority interest buy outs of £2.0m.

3

Interim Report for the three months to 31 March 2015 (continued)

Senior management changes

There have been a number of senior management changes in the period since 31 December 2014 including:

Scott Egan has changed his role from Chief Financial Officer to Interim Chief Executive Officer

Alastair Lyons has changed his role from Executive Chairman to Non-executive Chairman

The appointment of Mark Mugge as Chief Operating Officer and Steve Wood as Chief Executive Officer of

Paymentshield

The appointment of John Tiner as Chairman with effect from 29 June 2015

Financial review and outlook

Q1 2015 was a challenging period. Confidence in Towergate was tested with performance in all divisions affected by both the

Group financial restructuring and the change programme.

However significant progress has been made in multiple areas. Towergate has attracted long term supportive shareholders in

Highbridge, KKR and Sankaty. Over the last twelve months much of the comprehensive change programme has been

implemented. Towergate continues to attract talent. The Board remains focussed on operational delivery in 2015 and there are

some early signs of recovery as the business stabilises.

The Group is focussed on retention and new business and aims to deliver this through a concentration on customer service and

operational excellence. The expectation is that expenses will fall through the completion of the change programme and

continued integration of businesses. The Board will continue to invest in the business to deliver profitable growth in its chosen

markets.

4

Condensed consolidated statement of comprehensive income

for the period ended 31 March 2015 Unaudited

Three months ended

Unaudited

Three months ended

Audited

Twelve months ended

31 March 2015 31 March 2014 31 December 2014

£000 £000 £000

Commissions and fees 85,331 92,835 375,923

Investment income 89 102 480

Salaries and associated expenses (50,487) (47,342) (193,220)

Other operating costs (40,949) (24,698) (331,423)

Depreciation and amortisation charges (5,303) (4,764) (22,504)

Impairment of goodwill - - (552,861)

Operating (loss) / profit (11,319) 16,133 (723,605)

Analysed as:

Operating profit before exceptional items 7,348 18,499 72,489

Related party bad debt provision - - (190,534)

Reduction in value of contingent consideration - - 9,127

Loss on disposal of businesses and investments (340) - (1,547)

Group reorganisation costs (4,853) (2,366) (37,390)

Finance legacy review - - (3,702)

Regulatory costs (1,051) - (8,898)

Group financial restructuring costs (12,423) - (10,289)

Impairment of goodwill - - (552,861)

Operating (loss) / profit (11,319) 16,133 (723,605)

Finance costs (238) (1) (11)

Finance income 93 50 336

(Loss) / profit before taxation (11,464) 16,182 (723,280)

Income tax (expense) / credit (224) 233 883

(Loss) / profit for the year from continuing operations (11,688) 16,415 (722,397)

(Loss) / profit for the year from discontinued operations, net

of income tax

(366) 497 (23,283)

Total comprehensive (loss) / profit for the year (12,054) 16,912 (745,680)

Attributable to:

Owners of the parent (12,054) 16,912 (745,723)

Non-controlling interests - - 43

(12,054) 16,912 (745,680)

The notes on pages 8 to 18 form part of this condensed set of financial statements.

5

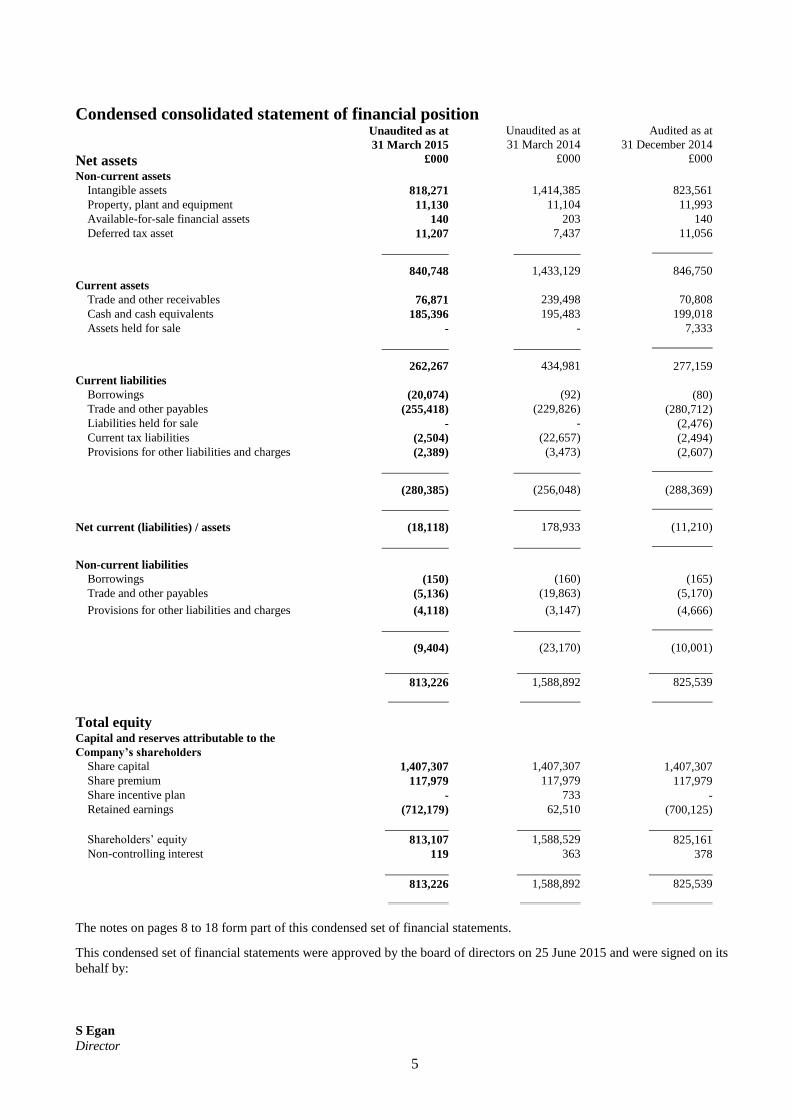

Condensed consolidated statement of financial position Unaudited as at Unaudited as at Audited as at

31 March 2015 31 March 2014 31 December 2014

Net assets £000 £000 £000

Non-current assets

Intangible assets 818,271 1,414,385 823,561

Property, plant and equipment 11,130 11,104 11,993

Available-for-sale financial assets 140 203 140

Deferred tax asset 11,207 7,437 11,056

840,748 1,433,129 846,750

Current assets

Trade and other receivables 76,871 239,498 70,808

Cash and cash equivalents 185,396 195,483 199,018

Assets held for sale - - 7,333

262,267 434,981 277,159

Current liabilities

Borrowings (20,074) (92) (80)

Trade and other payables (255,418) (229,826) (280,712)

Liabilities held for sale - - (2,476)

Current tax liabilities (2,504) (22,657) (2,494)

Provisions for other liabilities and charges (2,389) (3,473) (2,607)

(280,385) (256,048) (288,369)

Net current (liabilities) / assets (18,118) 178,933 (11,210)

Non-current liabilities

Borrowings (150) (160) (165)

Trade and other payables (5,136) (19,863) (5,170)

Provisions for other liabilities and charges (4,118) (3,147) (4,666)

(9,404) (23,170) (10,001)

813,226 1,588,892 825,539

Total equity

Capital and reserves attributable to the

Company’s shareholders

Share capital 1,407,307 1,407,307 1,407,307

Share premium 117,979 117,979 117,979

Share incentive plan - 733 -

Retained earnings (712,179) 62,510 (700,125)

Shareholders’ equity 813,107 1,588,529 825,161

Non-controlling interest 119 363 378

813,226 1,588,892 825,539

The notes on pages 8 to 18 form part of this condensed set of financial statements.

This condensed set of financial statements were approved by the board of directors on 25 June 2015 and were signed on its

behalf by:

S Egan

Director

6

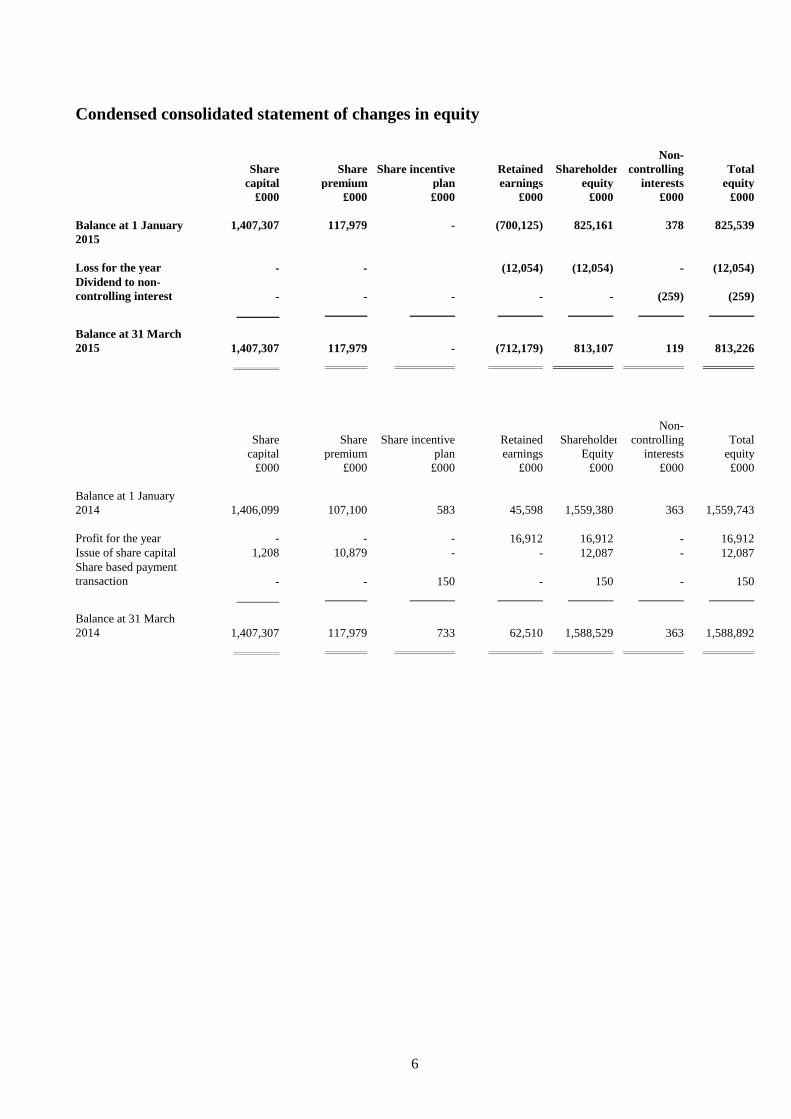

Condensed consolidated statement of changes in equity

Share

capital

Share

premium

Share incentive

plan

Retained

earnings

Shareholders

equity

Non-

controlling

interests

Total

equity

£000 £000 £000 £000 £000 £000 £000

Balance at 1 January

2015

1,407,307 117,979 - (700,125) 825,161 378 825,539

Loss for the year - - (12,054) (12,054) - (12,054)

Dividend to non-

controlling interest - - - - - (259) (259)

Balance at 31 March

2015 1,407,307 117,979 - (712,179) 813,107 119 813,226

Share

capital

Share

premium

Share incentive

plan

Retained

earnings

Shareholders

Equity

Non-

controlling

interests

Total

equity

£000 £000 £000 £000 £000 £000 £000

Balance at 1 January

2014 1,406,099 107,100 583 45,598 1,559,380 363 1,559,743

Profit for the year - - - 16,912 16,912 - 16,912

Issue of share capital 1,208 10,879 - - 12,087 - 12,087

Share based payment

transaction - - 150 - 150 - 150

Balance at 31 March

2014 1,407,307 117,979 733 62,510 1,588,529 363 1,588,892

7

Condensed consolidated statement of cash flows

Unaudited

Three months

ended

Unaudited

Three months

ended

Audited

Twelve months

ended

31 March 2015 31 March 2014 31 December 2014

£000 £000 £000

Cash flows from operating activities

Cash generated from / (used in) operations 11,157 (742) 52,348

Exceptional items (18,302) (2,366) (45,001)

Interest paid - (1) (11)

Interest received 93 56 372

Taxation (paid) / received - 16 (1)

Investment income 89 102 480

(Decrease) / increase in net insurance broking creditors (25,237) (14,769) (3,135)

Net cash (used in) / generated from operating activities (32,200) (17,704) 5,052

Cash flows from investing activities

Acquisition of businesses, net of cash acquired (8) (2,792) (11,197)

Purchase of property, plant and equipment (372) (520) (5,701)

Purchase of intangible fixed assets – computer software and CBO’s (1,316) (2,912) (14,873)

Disposal of businesses 7,544 - 24,606

Net cash disposed of with businesses (5,331) - (11,186)

Net cash generated from / (used in) investing activities 517 (6,224) (18,351)

Cash flows from financing activities

Proceeds from issue of shares - 12,088 12,088

Proceeds from borrowings 20,000

Loan to / (from) investment 10 12 43

Net settled deferred consideration (3,343) (1,228) (6,931)

Capital element of finance lease rental payments (21) (18) (25)