Embed Size (px)

Citation preview

1PB...Covering your risks beyond...

Annual Report andFinancial Statements

Annual Report andFinancial Statements

2017

32

Chairman’s Report Managing Director’s Report Performance Highlights Board of Directors Senior Management & Corporate Information Directors’ Report to Members Statement of Directors’ responsibilities Report of the independent auditors to the members of Prima Reinsurance Plc Income statement Statement of Comprehensive Income Statement of Changes in EquityStatement of Financial Position Statement of Cash Flows Notes to the financial statements Notice of the 12th Annual General Meeting Form of Proxy

4-58

9-111213

16-2223

24- 2627

28282930

31-545657

TABLE OFCONTENTS

4 5

Chairman’sReport

I have the pleasure once more of presenting the results of Prima Reinsurance Plc for the year ended 31 December 2017.

Economic Overview

Zambia’s economy continued to recover in 2017, with good rains which increased agricultural production and greatly reduced load shedding due to improved electricity generation. Inflation was maintained at single-digit levels and the exchange rate generally remained stable.Despite this and the easing of monetary policy, growth remained subdued at 3.8%. Going forward, demand for copper in China is projected to continue increasing in 2018 and combined with the forecasted copper supply deficit, prices are expected to remain at their current levels or rise slightly into 2018. Ongoing energy reforms, driven by higher electricity tariffs, will continue into 2018 and the reduction in subsidies to the electricity and oil subsectors will help offset some fiscal pressures caused by higher interest payments and continued infrastructure investment drive.The recent upgrade (January 2018) by Moody’s of the rating outlook for Zambia to stable from negative reflects reduced government liquidity pressures and a slowdown in government debt accumulation. Economic fundamentals, including its economic strength, have materially increased.Real GDP growth is projected at above 4% for 2018 and 2019.

Industry Review

The removal of the Insurance Levy on reinsurance premiums as announced by the Minister of Finance in his 2018 National Budget speech is indeed very welcome. This will reduce

the cost of local reinsurance and make it more competitive on the international platform.The Draft Insurance Bill which is expected to go to Parliament in 2018 will improve and strengthen the legal framework for the insurance industry. This will result in growth and stability of the sector.There has been great concern about the amount of premiums that is being taken out of the country through reinsurance, leaving the capacity of the local reinsurers largely unutilized. It is hoped that this loophole will be sealed through the draft Insurance Bill which will not only grow the local market but also enhance the retention of premiums locally for the benefit of the economy. It will also be in line with the practice in many other countries.

Performance

Prima Re celebrated its 10th Anniversary during 2017.During 2017, Prima Reinsurance Plc (Prima Re), focused on profitability rather than mere growth and this is evidenced by the increase in gross profit of over 40%.Prima Re recorded an increase in its Gross Written Premium of 6% and continues to strive to provide increased capacity to the domestic market.

The Life Business division established in 2017 performed well, exceeding its budget.

The earnings per share remained stable at 0.10 during the year under review.

Prima Re increased its market outreach and now has business emanating from over 18 countries within Africa, although the domestic market remains the main source of business.

The Company continues to restrict its business portfolio to the African continent.

The two-year moratorium on minimum capital requirement, as subscribed under the SI 71 (2015) came to an end on 31 October 2017, with some insurance companies struggling

to meet the capital requirements before the deadline.

Prima Re was not affected as the Company had already attained and exceeded the minimum capital requirement.

Dividend

The Directors recommend that a dividend of K 0.05 per share be proposed for the year ending 31 December 2017. This is 50% of the earnings per share.

Outlook

As we go forward into 2018, we expect the new Insurance Bill to be tabled before Parliament and it is expected that there is a provision for the exhaustion of local capacity before a risk is externalised.

The provision of “no premium no cover” regulations which the industry is lobbying for, will strengthen the domestic market and eliminate the huge debtors’ problem in the market, bringing it line with other markets in the region.

Prima Re remains confident about its future prospects particularly as it anticipates the enactment of the Insurance Bill in 2018.On behalf of the Board of Directors and Management, I wish to thank all our business partners for their support and loyalty during the year as well as the staff and Management for their commitment and efforts.

David KombeChairmanDate: 22rd February 2018

Prima Re increased its market outreach and now has business emanating from over 18 countries within Africa, although the domestic market remains the main source of business.

David KombeChairman

6 7

“If I have seen further than others, it is by standing upon the shoulders of giants.” Isaac Newton

8 9

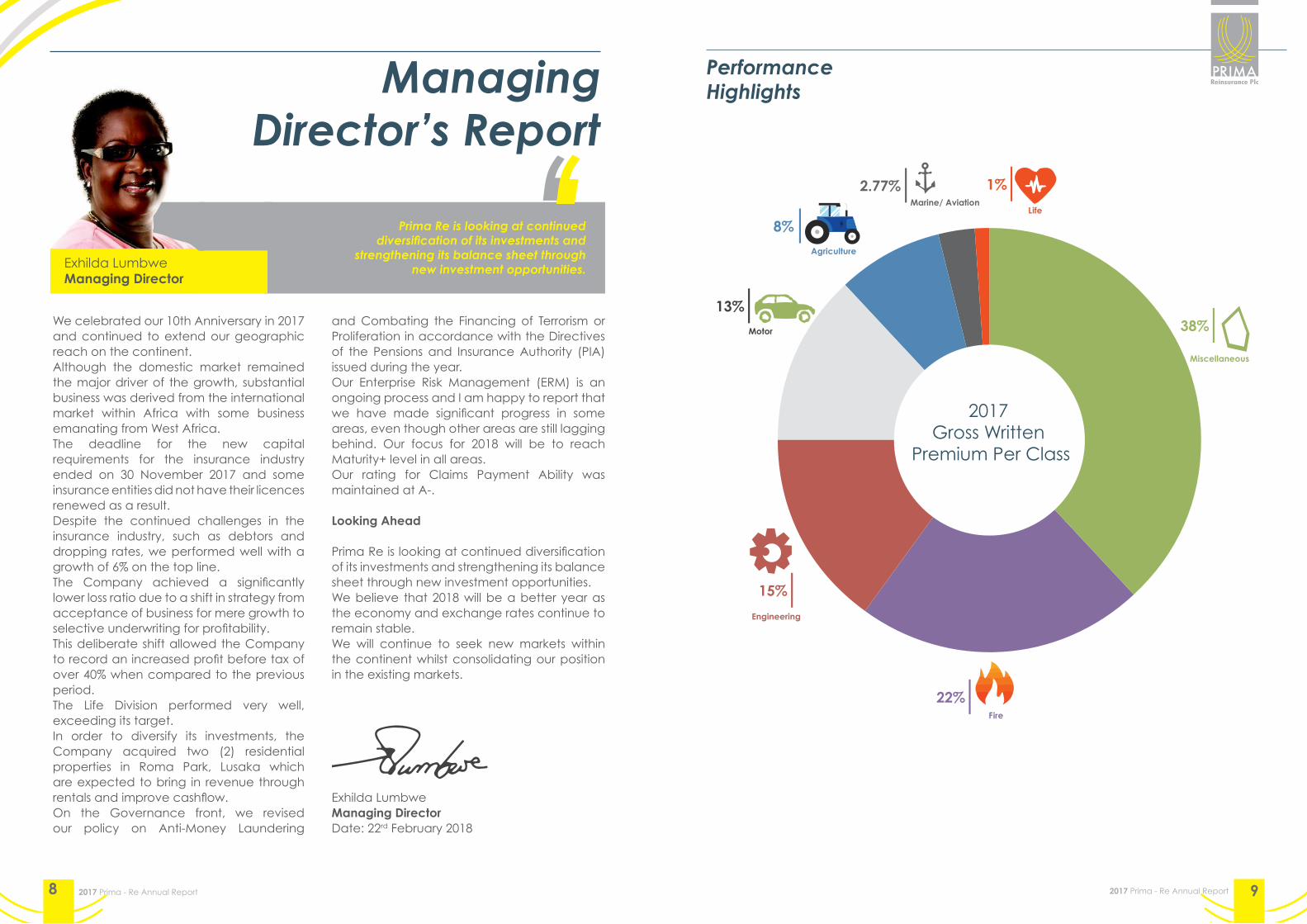

ManagingDirector’s Report

Prima Re is looking at continued diversification of its investments and

strengthening its balance sheet through new investment opportunities. Exhilda Lumbwe

Managing Director

We celebrated our 10th Anniversary in 2017 and continued to extend our geographic reach on the continent. Although the domestic market remained the major driver of the growth, substantial business was derived from the international market within Africa with some business emanating from West Africa.The deadline for the new capital requirements for the insurance industry ended on 30 November 2017 and some insurance entities did not have their licences renewed as a result. Despite the continued challenges in the insurance industry, such as debtors and dropping rates, we performed well with a growth of 6% on the top line.The Company achieved a significantly lower loss ratio due to a shift in strategy from acceptance of business for mere growth to selective underwriting for profitability. This deliberate shift allowed the Company to record an increased profit before tax of over 40% when compared to the previous period.The Life Division performed very well, exceeding its target. In order to diversify its investments, the Company acquired two (2) residential properties in Roma Park, Lusaka which are expected to bring in revenue through rentals and improve cashflow.On the Governance front, we revised our policy on Anti-Money Laundering

and Combating the Financing of Terrorism or Proliferation in accordance with the Directives of the Pensions and Insurance Authority (PIA) issued during the year.Our Enterprise Risk Management (ERM) is an ongoing process and I am happy to report that we have made significant progress in some areas, even though other areas are still lagging behind. Our focus for 2018 will be to reach Maturity+ level in all areas.Our rating for Claims Payment Ability was maintained at A-.

Looking Ahead

Prima Re is looking at continued diversification of its investments and strengthening its balance sheet through new investment opportunities. We believe that 2018 will be a better year as the economy and exchange rates continue to remain stable. We will continue to seek new markets within the continent whilst consolidating our position in the existing markets.

Exhilda LumbweManaging DirectorDate: 22rd February 2018

2.77%Marine/ Aviation

2017 Gross Written

Premium Per Class

Agriculture

8%

38%

Miscellaneous

1%

Life

15%

Engineering

22%Fire

13%

Motor

10 11

Gross Written Premium Per Class 2016/2017

AG

RIC

ULT

UR

E

MA

RIN

E

MIS

CEL

LAN

EOU

S

ENG

IREE

RIN

G

FIR

E

LIFE

MO

TOR

2016

2017

0%5%

10%15%20%25%30%35%40%

2011 2012 2013 2014 2015 2016 2017

Gross written Premium (Kwacha)

05,000

10,00015,00020,00025,00030,00035,00040,000

1110

12 13

Board Of Directors

David KombeChairman

Dorothy Soko Director

Munakopa Sikaulu Director

Nathan DeAssis Director

Simomo Akapelwa Director

Exhilda Lumbwe Managing Director

Joyce Muwo MwansaDirector

Senior Management

Exhilda Lumbwe Managing DirectorCharles Etemesi

Chief Operations Officer

Brian MateyoUnderwriting Manager

Chama Chipulu Finance Manager

CORPORATE INFORMATION

SECRETARYChoice Corporate Services Limited

AUDITORSGrant Thornton Chartered Accountants

BANKERSBarclays Bank Zambia Plc, Investrust Bank PlcBanc ABC Zambia Limited, Stanbic Bank Zambia Limited

LEGAL ADVISORSWilson & Cornhill5th Floor Premium House Independence AvenueP.O . Box 38906 Lusaka

REGISTERED OFFICESStand 3509 / No.7 Matandani Close RhodesparkP. O. Box 32565Lusaka

14 15

“A thousand may fall at your side, and ten thousand at your right hand; but it shall not come near you.”

Psalm 91:7

16 17

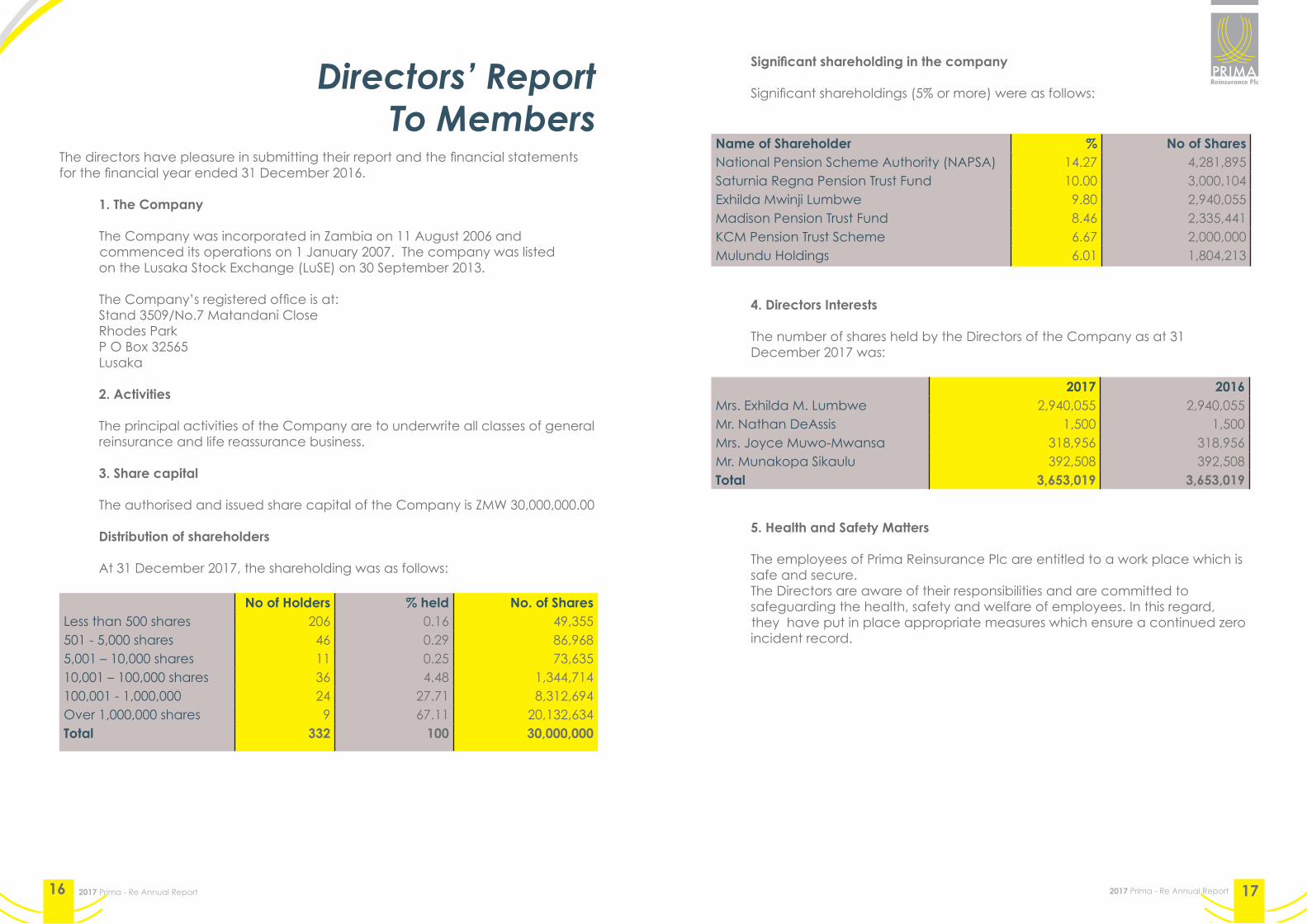

Directors’ Report To Members

The directors have pleasure in submitting their report and the financial statements for the financial year ended 31 December 2016.

1. The Company

The Company was incorporated in Zambia on 11 August 2006 and commenced its operations on 1 January 2007. The company was listed on the Lusaka Stock Exchange (LuSE) on 30 September 2013.

The Company’s registered office is at: Stand 3509/No.7 Matandani Close Rhodes Park P O Box 32565 Lusaka

2. Activities

The principal activities of the Company are to underwrite all classes of general reinsurance and life reassurance business.

3. Share capital

The authorised and issued share capital of the Company is ZMW 30,000,000.00 Distribution of shareholders At 31 December 2017, the shareholding was as follows:

No of Holders % held No. of SharesLess than 500 shares 206 0.16 49,355501 - 5,000 shares 46 0.29 86,9685,001 – 10,000 shares 11 0.25 73,63510,001 – 100,000 shares 36 4.48 1,344,714100,001 - 1,000,000 24 27.71 8,312,694Over 1,000,000 shares 9 67.11 20,132,634Total 332 100 30,000,000

Significant shareholding in the company

Significant shareholdings (5% or more) were as follows:

Name of Shareholder % No of SharesNational Pension Scheme Authority (NAPSA) 14.27 4,281,895Saturnia Regna Pension Trust Fund 10.00 3,000,104Exhilda Mwinji Lumbwe 9.80 2,940,055Madison Pension Trust Fund 8.46 2,335,441KCM Pension Trust Scheme 6.67 2,000,000Mulundu Holdings 6.01 1,804,213

4. Directors Interests

The number of shares held by the Directors of the Company as at 31 December 2017 was:

2017 2016Mrs. Exhilda M. Lumbwe 2,940,055 2,940,055Mr. Nathan DeAssis 1,500 1,500Mrs. Joyce Muwo-Mwansa 318,956 318,956Mr. Munakopa Sikaulu 392,508 392,508Total 3,653,019 3,653,019

5. Health and Safety Matters

The employees of Prima Reinsurance Plc are entitled to a work place which is safe and secure. The Directors are aware of their responsibilities and are committed to safeguarding the health, safety and welfare of employees. In this regard, they have put in place appropriate measures which ensure a continued zero incident record.

18 19

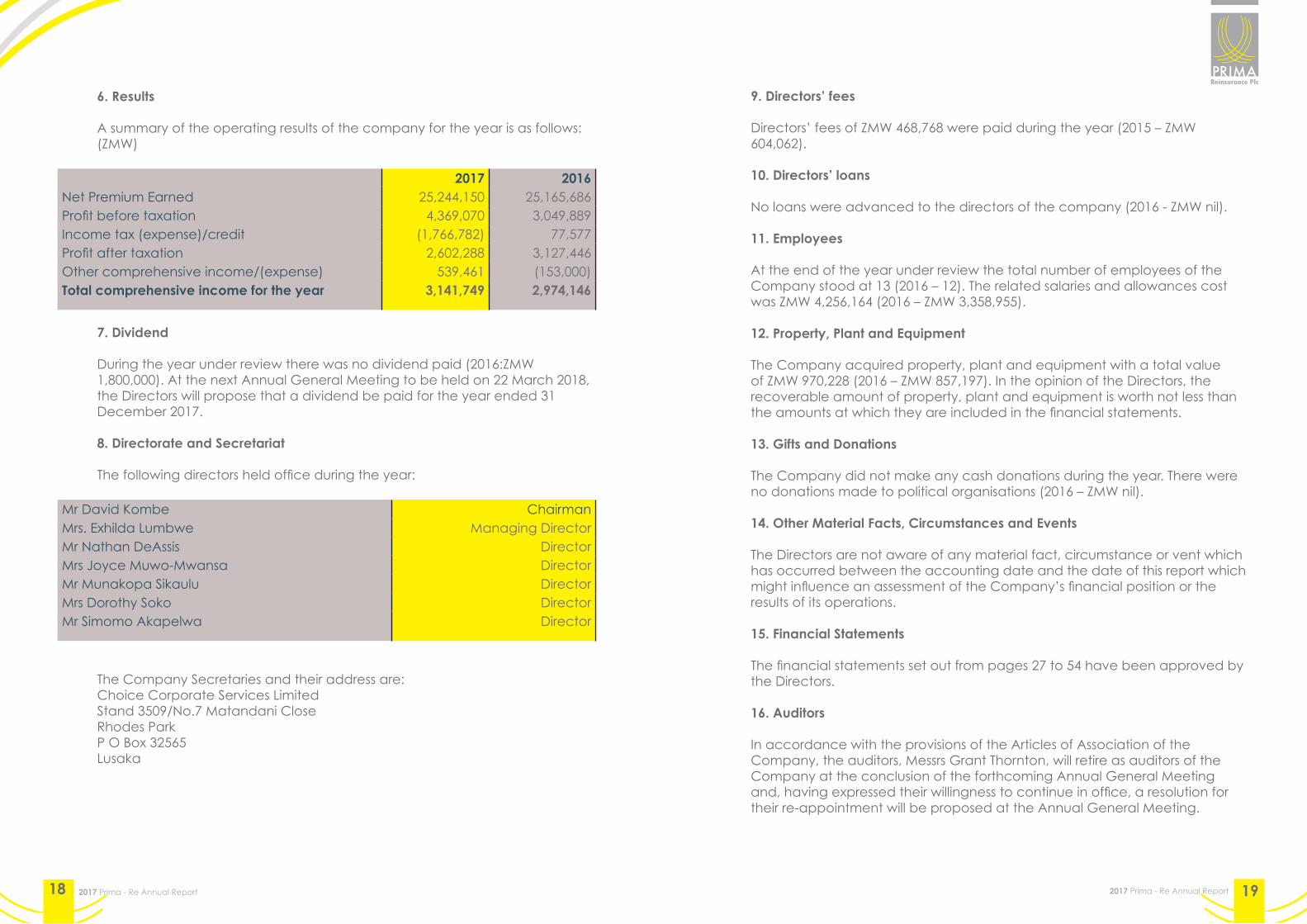

6. Results

A summary of the operating results of the company for the year is as follows: (ZMW)

2017 2016Net Premium Earned 25,244,150 25,165,686Profit before taxation 4,369,070 3,049,889Income tax (expense)/credit (1,766,782) 77,577Profit after taxation 2,602,288 3,127,446Other comprehensive income/(expense) 539,461 (153,000)Total comprehensive income for the year 3,141,749 2,974,146

7. Dividend

During the year under review there was no dividend paid (2016:ZMW 1,800,000). At the next Annual General Meeting to be held on 22 March 2018, the Directors will propose that a dividend be paid for the year ended 31 December 2017.

8. Directorate and Secretariat

The following directors held office during the year:

Mr David Kombe ChairmanMrs. Exhilda Lumbwe Managing DirectorMr Nathan DeAssis DirectorMrs Joyce Muwo-Mwansa DirectorMr Munakopa Sikaulu DirectorMrs Dorothy Soko DirectorMr Simomo Akapelwa Director

The Company Secretaries and their address are: Choice Corporate Services Limited Stand 3509/No.7 Matandani Close Rhodes Park P O Box 32565 Lusaka

9. Directors’ fees

Directors’ fees of ZMW 468,768 were paid during the year (2015 – ZMW 604,062).

10. Directors’ loans No loans were advanced to the directors of the company (2016 - ZMW nil).

11. Employees

At the end of the year under review the total number of employees of the Company stood at 13 (2016 – 12). The related salaries and allowances cost was ZMW 4,256,164 (2016 – ZMW 3,358,955).

12. Property, Plant and Equipment

The Company acquired property, plant and equipment with a total value of ZMW 970,228 (2016 – ZMW 857,197). In the opinion of the Directors, the recoverable amount of property, plant and equipment is worth not less than the amounts at which they are included in the financial statements.

13. Gifts and Donations

The Company did not make any cash donations during the year. There were no donations made to political organisations (2016 – ZMW nil). 14. Other Material Facts, Circumstances and Events

The Directors are not aware of any material fact, circumstance or vent which has occurred between the accounting date and the date of this report which might influence an assessment of the Company’s financial position or the results of its operations. 15. Financial Statements

The financial statements set out from pages 27 to 54 have been approved by the Directors. 16. Auditors

In accordance with the provisions of the Articles of Association of the Company, the auditors, Messrs Grant Thornton, will retire as auditors of the Company at the conclusion of the forthcoming Annual General Meeting and, having expressed their willingness to continue in office, a resolution for their re-appointment will be proposed at the Annual General Meeting.

20 21

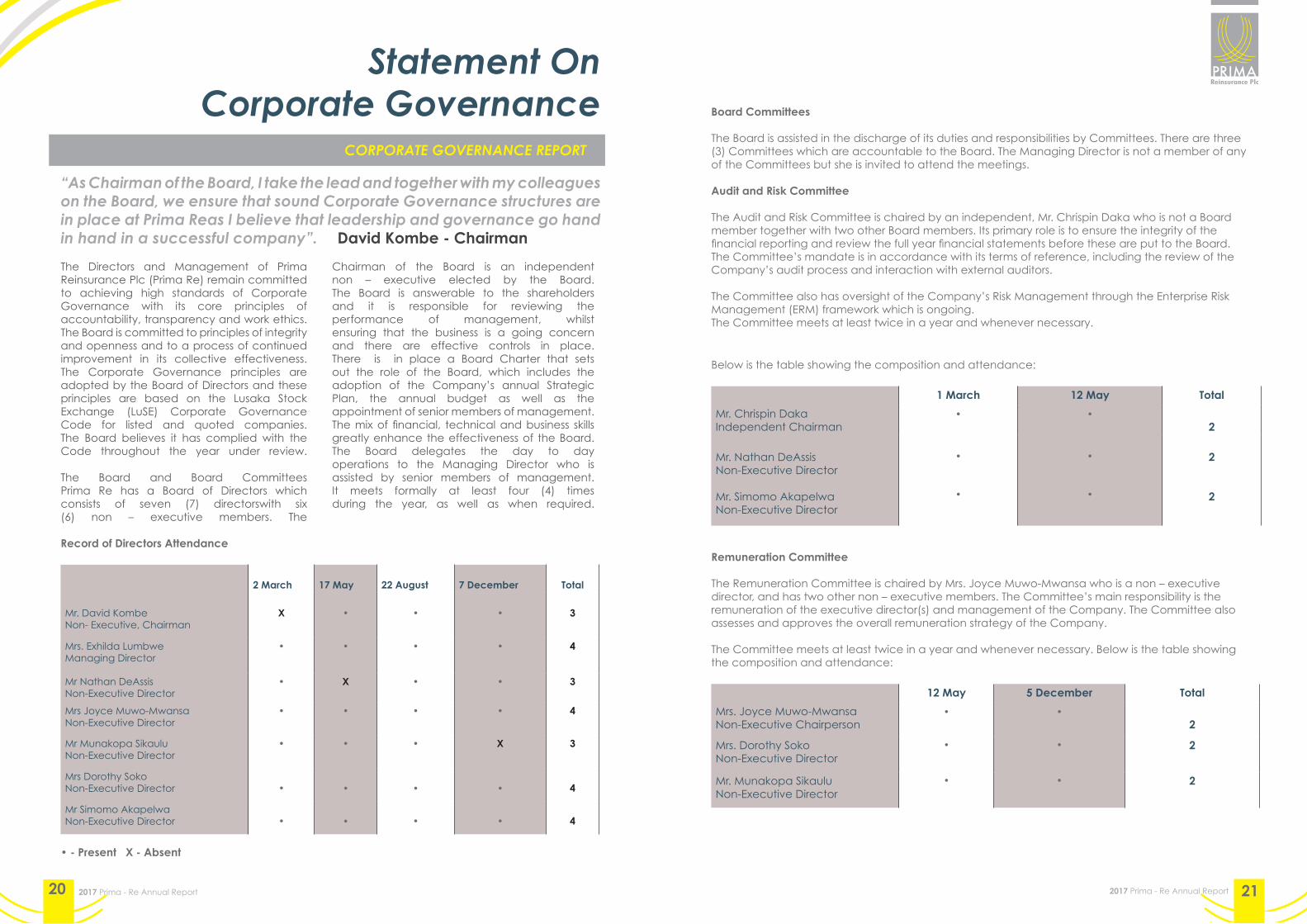

Statement On Corporate Governance

CORPORATE GOVERNANCE REPORT

“As Chairman of the Board, I take the lead and together with my colleagues on the Board, we ensure that sound Corporate Governance structures are in place at Prima Reas I believe that leadership and governance go hand in hand in a successful company”. David Kombe - Chairman

The Directors and Management of Prima Reinsurance Plc (Prima Re) remain committed to achieving high standards of Corporate Governance with its core principles of accountability, transparency and work ethics. The Board is committed to principles of integrity and openness and to a process of continued improvement in its collective effectiveness.The Corporate Governance principles are adopted by the Board of Directors and these principles are based on the Lusaka Stock Exchange (LuSE) Corporate Governance Code for listed and quoted companies.The Board believes it has complied with the Code throughout the year under review.

The Board and Board CommitteesPrima Re has a Board of Directors which consists of seven (7) directorswith six (6) non – executive members. The

Chairman of the Board is an independent non – executive elected by the Board.The Board is answerable to the shareholders and it is responsible for reviewing the performance of management, whilst ensuring that the business is a going concern and there are effective controls in place. There is in place a Board Charter that sets out the role of the Board, which includes the adoption of the Company’s annual Strategic Plan, the annual budget as well as the appointment of senior members of management.The mix of financial, technical and business skills greatly enhance the effectiveness of the Board.The Board delegates the day to day operations to the Managing Director who is assisted by senior members of management. It meets formally at least four (4) times during the year, as well as when required.

Board Committees

The Board is assisted in the discharge of its duties and responsibilities by Committees. There are three (3) Committees which are accountable to the Board. The Managing Director is not a member of any of the Committees but she is invited to attend the meetings.

Audit and Risk Committee

The Audit and Risk Committee is chaired by an independent, Mr. Chrispin Daka who is not a Board member together with two other Board members. Its primary role is to ensure the integrity of the financial reporting and review the full year financial statements before these are put to the Board.The Committee’s mandate is in accordance with its terms of reference, including the review of the Company’s audit process and interaction with external auditors.

The Committee also has oversight of the Company’s Risk Management through the Enterprise Risk Management (ERM) framework which is ongoing. The Committee meets at least twice in a year and whenever necessary.

Below is the table showing the composition and attendance:

1 March 12 May Total

Mr. Chrispin DakaIndependent Chairman

• •2

Mr. Nathan DeAssisNon-Executive Director

Mr. Simomo AkapelwaNon-Executive Director

•

•

•

•

2

2

Remuneration Committee

The Remuneration Committee is chaired by Mrs. Joyce Muwo-Mwansa who is a non – executive director, and has two other non – executive members. The Committee’s main responsibility is the remuneration of the executive director(s) and management of the Company. The Committee also assesses and approves the overall remuneration strategy of the Company.

The Committee meets at least twice in a year and whenever necessary. Below is the table showing the composition and attendance:

12 May 5 December Total

Mrs. Joyce Muwo-MwansaNon-Executive Chairperson

• •2

Mrs. Dorothy SokoNon-Executive Director

• • 2

Mr. Munakopa SikauluNon-Executive Director

• • 2

Record of Directors Attendance

2 March 17 May 22 August 7 December Total

Mr. David KombeNon- Executive, Chairman

X • • • 3

Mrs. Exhilda LumbweManaging Director

• • • • 4

Mr Nathan DeAssisNon-Executive Director

• X • • 3

Mrs Joyce Muwo-MwansaNon-Executive Director

• • • • 4

Mr Munakopa SikauluNon-Executive Director

• • • X 3

Mrs Dorothy SokoNon-Executive Director • • • • 4

Mr Simomo AkapelwaNon-Executive Director • • • • 4

• - Present X - Absent

22 23

Investment Committee

The Investment Committee is chaired by Mrs. Dorothy Soko and comprises of two other non- executive members. The Committee’s main responsibility is to review, evaluate and approve investment transactions as well as have oversight of the Company’s Investment Strategy and Investment Policy.

The Committee meets at least twice in a year and whenever necessary. Below is the table showing the composition and attendance:

Mrs. Dorothy SokoNon-Executive Chairperson

12 May

•

21 June

•

21 July

•

Total

3

Mr. Nathan DeAssisNon-Executive Director

Mr. Simomo AkapelwaNon-Executive Director

•

•

•

•

•

•

3

3

Whistle Blowing Policy

The Company has in place a Whistle Blowing Policy which has been made aware to all employees.The Company has zero tolerance to fraud and ethical abuses at the work place and it is committed to working ethically.

By order of the Board

Choice Corporate Services LimitedCompany Secretaries

Date: 22nd February 2018

Directors’ Statement

STATEMENT OF DIRECTORS’ RESPONSIBILITIES

The Companies Act 1994 and the Insurance Act 1997 require the directors to prepare financial statements for each financial year which give a true and fair view of the financial position of Prima Reinsurance PLC and of its financial performance and its cash flows for the year then ended. In preparing such financial statements, the directors are responsible for

• designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error;• selecting appropriate accounting policies and applying them consistently;• making judgements and accounting estimates that are reasonable in the circumstances; and• preparing the financial statements in accordance with the applicable financial reporting framework, and on the going concern basis unless it is inappropriate to presume that the Company will continue in business.The directors are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the Company and enable them to ensure that the financial statements comply with the Companies Act 1994 and the Insurance Act 1997. They are also responsible for safeguarding the assets of the Company and

hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.The Board of Directors confirm that in their opinion:

(a) the financial statements give a true and fair view of the financial position of Prima Reinsurance PLC as of 31 December 2017, and of its financial performance and its cash flows for the year then ended;

(b) at the date of this statement there are reasonable grounds to believe that the Company will be able to pay its debts as and when these fall due; and

(c) the financial statements are drawn up in accordance with International Financial Reporting Standards.

This statement is made in accordance with a resolution of the Board of Directors.

Signed at Lusaka on 22nd February 2018

Director

Director

24 25

Prima Reinsurance PLC Financial Statements 31 December 2017

Report Of The Independent Auditors To The Members Of

Prima Reinsurance PlcREPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS

Opinion

We have audited the financial statements of Prima Re-Insurance PLC which comprise the statement of financial position as at 31 December 2017, and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements give a true and fair view of the financial position of the Company as at 31 December 2017, and of its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards ( IFRSs).

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the International Ethics Standards Board for Accountants’ Code of Ethics for

Professional Accountants (IESBA Code) together with the ethical requirements that are relevant to our audit of the financial statements in Zambia, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Key Audit Matter

Key audit matter is that matter that, in our professional judgement, was of most significance in our audit of the financial statements of the current period. This matter was addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on this matter. The following matter was noted:-

Insurance reserves

Insurance reserves comprise Unearned Premium Reserves (UPR), accruals for claims notified but not yet settled, claims incurred but not yet reported (IBNR) and the related deferred acquisition costs. In setting aside the necessary reserves that are adequate but not excessive the management have to follow the

provisions of Insurance Act, Pensions and Insurance Authority (PIA) guidelines, past experience and actuarial estimations, coupled with management judgement.

Key Audit Matter (continued)

The Company uses the 24th method for apportioning the Unearned Premium Reserves (UPR). This method requires that the gross premiums earned net of the retrocession premiums be allocated to the month in which the business is acquired. Management has adopted a method of allocating the business to the start of the cover period for the Treaty business as the loss cover is limited to the particular period of the Treaty. This method was reviewed by the Company’s independent actuaries and found to be suitable. In accordance with the Insurance Act this method was approved by the Pensions and Insurance Authority (PIA).

We checked the underlying policy documents to identify when the business was acquired and the related period of insurance cover. The stated insurance reserves were recomputed and found to be reasonable.

Responsibilities of Management and Those Charged with Governance for the Financial Statements Management is responsible for the preparation of the financial statements that give a true and fair view in accordance with International Financial Reporting Standards and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatements, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.As part of an audit in accordance with ISAs, we exercise professional judgement and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk

Grant Thronton Zambia - Lusaka5th Floor, Mukuba Pension House5309 Dedan Kimathi RoadP O Box 30885T +(260) (211) 227722-8F +(260) (211) 223774E [email protected]

26 27

of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements, or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including significant deficiencies in internal control that we identify during our audit.

Report on Other Legal and Regulatory Requirements

In our opinion, the financial statements of Prima Reinsurance PLC as at 31 December 2017 have been properly prepared in accordance with the Companies Act 1994 and the Insurance Act 1997, and the accounting and other records and registers have been properly kept in accordance with the Acts.

Chartered Accountants

Edgar Hamuwele (AUD/F000111)Name of Partner signing on behalf of the Firm

Lusaka

Date: 22rd February 2018

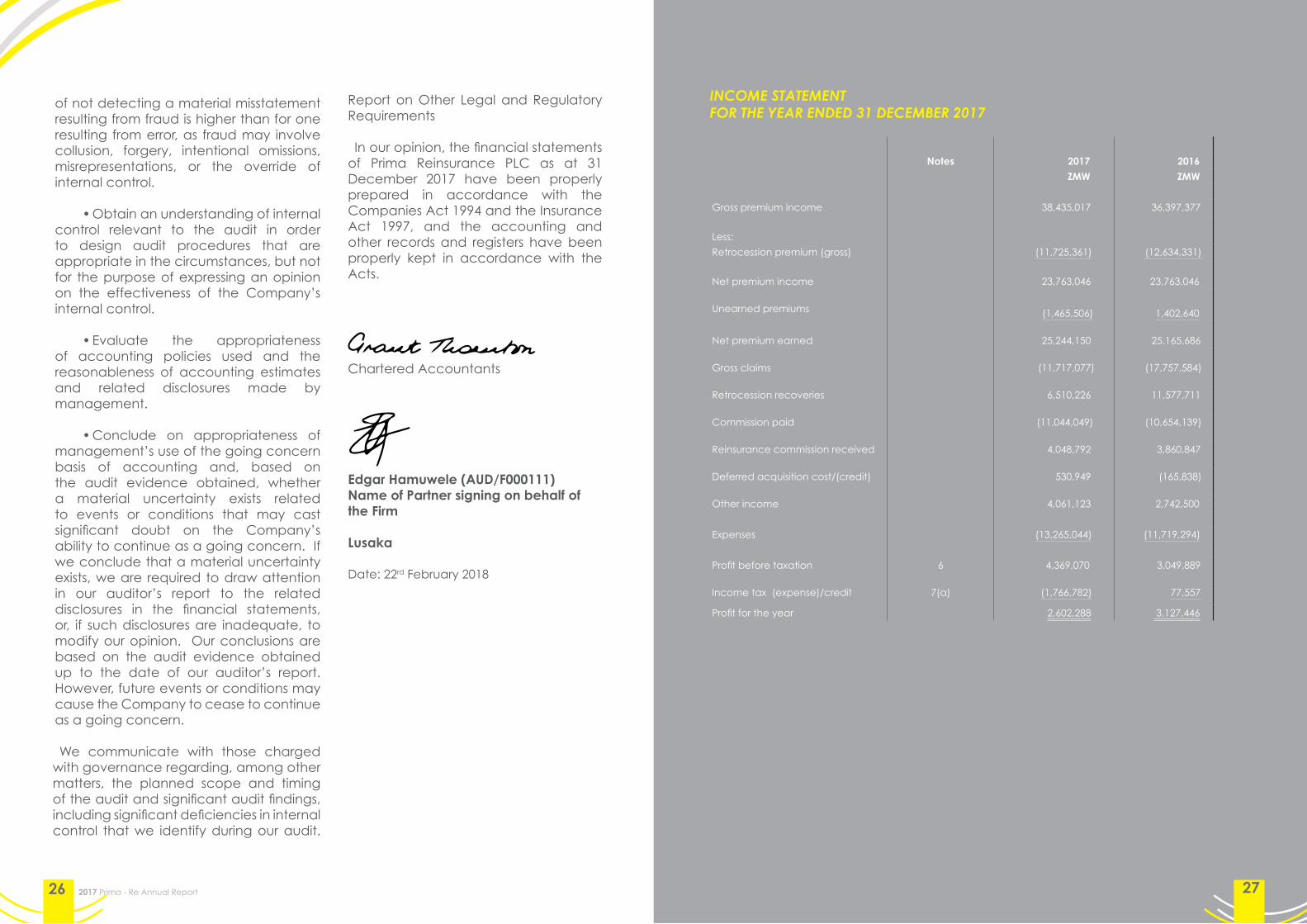

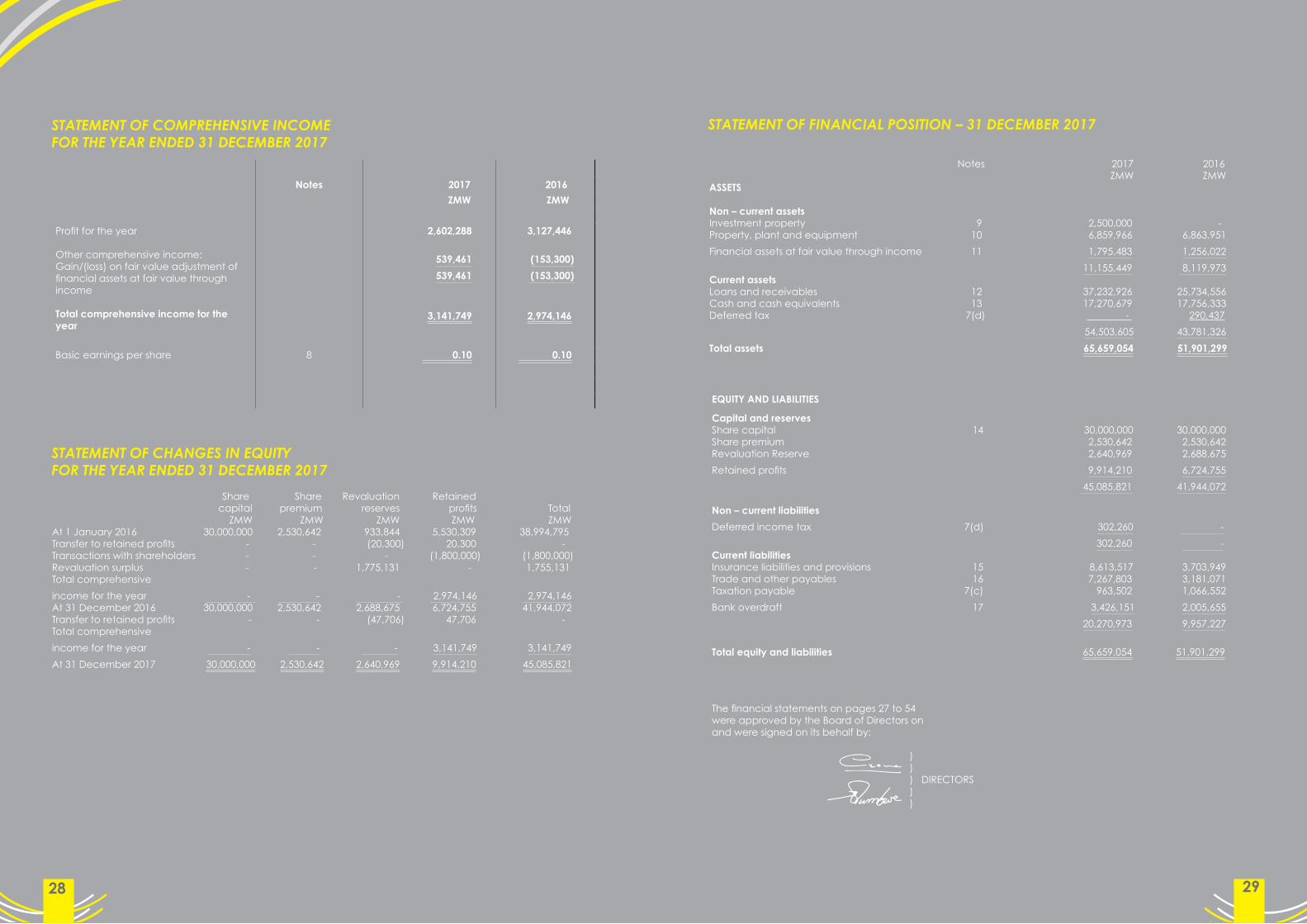

INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2017

Notes 2017 2016

ZMW ZMW

Gross premium income 38,435,017 36,397,377

Less:

Retrocession premium (gross) (11,725,361) (12,634,331)

Net premium income 23,763,046 23,763,046

Unearned premiums

(1,465,506)

1,402,640

Net premium earned 25,244,150 25,165,686

Gross claims (11,717,077) (17,757,584)

Retrocession recoveries 6,510,226 11,577,711

Commission paid (11,044,049) (10,654,139)

Reinsurance commission received 4,048,792 3,860,847

Deferred acquisition cost/(credit) 530,949 (165,838)

Other income 4,061,123 2,742,500

Expenses (13,265,044) (11,719,294)

Profit before taxation 6 4,369,070 3,049,889

Income tax (expense)/credit 7(a) (1,766,782) 77,557

Profit for the year 2,602,288 3,127,446

27

28 29

Notes 2017 2016

ZMW ZMW

Profit for the year

Other comprehensive income:Gain/(loss) on fair value adjustment of financial assets at fair value through income

Total comprehensive income for the year

2,602,288

539,461

539,461

3,141,749

3,127,446

(153,300)

(153,300)

2,974,146

Basic earnings per share 8 0.10 0.10

STATEMENT OF COMPREHENSIVE INCOMEFOR THE YEAR ENDED 31 DECEMBER 2017

STATEMENT OF CHANGES IN EQUITYFOR THE YEAR ENDED 31 DECEMBER 2017

Share Share Revaluation Retained capital premium reserves profits Total ZMW ZMW ZMW ZMW ZMWAt 1 January 2016 30,000,000 2,530,642 933,844 5,530,309 38,994,795Transfer to retained profits - - (20,300) 20,300 -Transactions with shareholders - - - (1,800,000) (1,800,000)Revaluation surplus - - 1,775,131 - 1,755,131Total comprehensive

income for the year - - - 2,974,146 2,974,146At 31 December 2016 30,000,000 2,530,642 2,688,675 6,724,755 41,944,072Transfer to retained profits - - (47,706) 47,706 - Total comprehensive

income for the year - - - 3,141,749 3,141,749

At 31 December 2017 30,000,000 2,530,642 2,640,969 9,914,210 45,085,821

STATEMENT OF FINANCIAL POSITION – 31 DECEMBER 2017

Notes 2017 2016 ZMW ZMWASSETS

Non – current assetsInvestment property 9 2,500,000 - Property, plant and equipment 10 6,859,966 6,863,951

Financial assets at fair value through income 11 1,795,483 1,256,022

11,155,449 8,119,973Current assets Loans and receivables 12 37,232,926 25,734,556Cash and cash equivalents 13 17,270,679 17,756,333 Deferred tax 7(d) - 290,437

54,503,605 43,781,326

Total assets 65,659,054 51,901,299

EQUITY AND LIABILITIES

Capital and reservesShare capital 14 30,000,000 30,000,000 Share premium 2,530,642 2,530,642 Revaluation Reserve 2,640,969 2,688,675

Retained profits 9,914,210 6,724,755

45,085,821 41,944,072

Non – current liabilities

Deferred income tax 7(d) 302,260 -

302,260 -Current liabilities Insurance liabilities and provisions 15 8,613,517 3,703,949 Trade and other payables 16 7,267,803 3,181,071 Taxation payable 7(c) 963,502 1,066,552

Bank overdraft 17 3,426,151 2,005,655

20,270,973 9,957,227

Total equity and liabilities 65,659,054 51,901,299

The financial statements on pages 27 to 54 were approved by the Board of Directors on and were signed on its behalf by:

) ) ) DIRECTORS ) )

2928

30 31

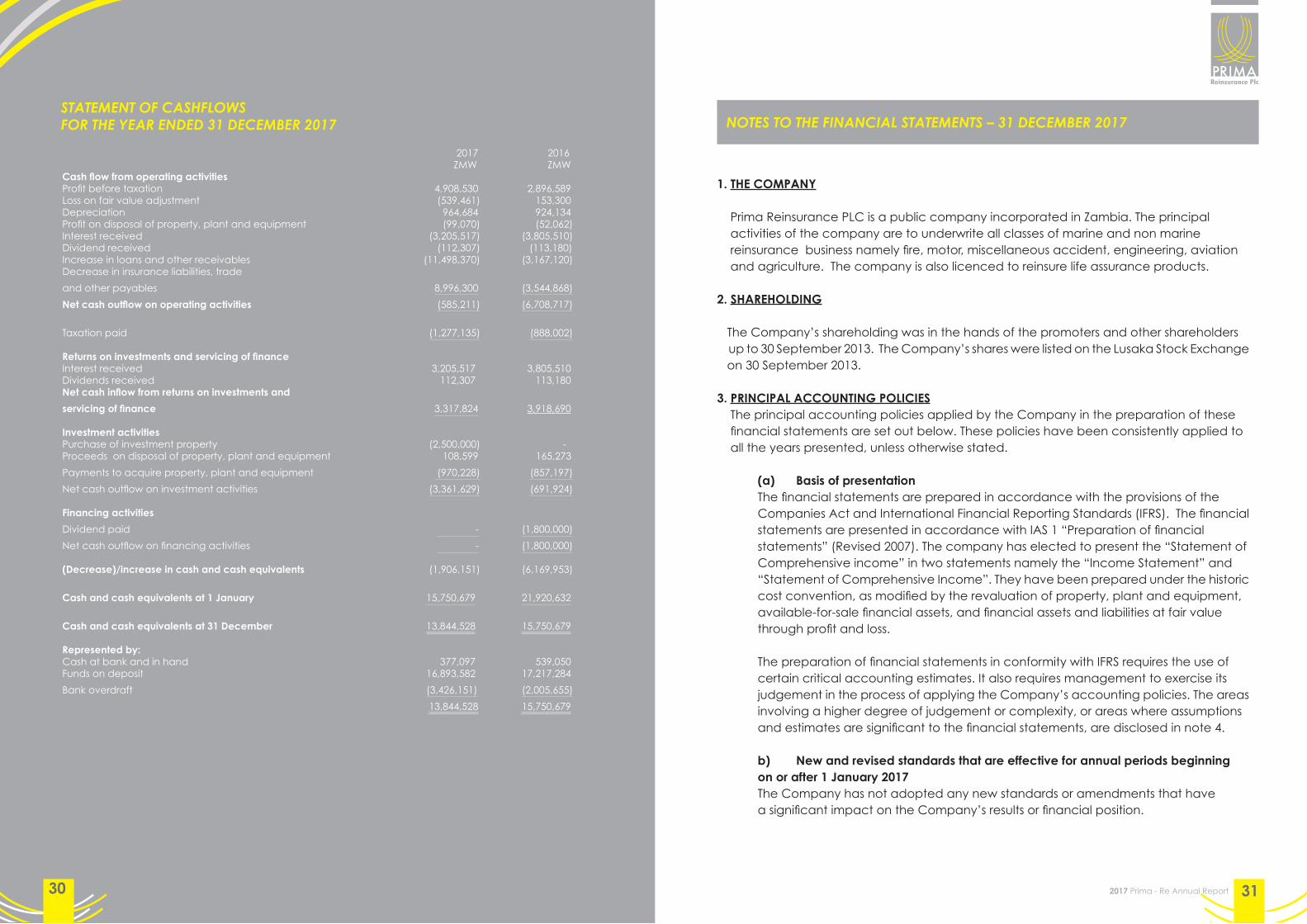

STATEMENT OF CASHFLOWSFOR THE YEAR ENDED 31 DECEMBER 2017

2017 2016 ZMW ZMWCash flow from operating activitiesProfit before taxation 4,908,530 2,896,589 Loss on fair value adjustment (539,461) 153,300 Depreciation 964,684 924,134 Profit on disposal of property, plant and equipment (99,070) (52,062)Interest received (3,205,517) (3,805,510)Dividend received (112,307) (113,180)Increase in loans and other receivables (11,498,370) (3,167,120)Decrease in insurance liabilities, trade

and other payables 8,996,300 (3,544,868)

Net cash outflow on operating activities (585,211) (6,708,717)

Taxation paid (1,277,135) (888,002)

Returns on investments and servicing of financeInterest received 3,205,517 3,805,510 Dividends received 112,307 113,180 Net cash inflow from returns on investments and

servicing of finance 3,317,824 3,918,690

Investment activities Purchase of investment property (2,500,000) -Proceeds on disposal of property, plant and equipment 108,599 165,273

Payments to acquire property, plant and equipment (970,228) (857,197)

Net cash outflow on investment activities (3,361,629) (691,924) Financing activities

Dividend paid - (1,800,000)

Net cash outflow on financing activities - (1,800,000)

(Decrease)/increase in cash and cash equivalents (1,906,151) (6,169,953)

Cash and cash equivalents at 1 January 15,750,679 21,920,632

Cash and cash equivalents at 31 December 13,844,528 15,750,679

Represented by:Cash at bank and in hand 377,097 539,050 Funds on deposit 16,893,582 17,217,284

Bank overdraft (3,426,151) (2,005,655)

13,844,528 15,750,679

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017

1. THE COMPANY

Prima Reinsurance PLC is a public company incorporated in Zambia. The principal activities of the company are to underwrite all classes of marine and non marine reinsurance business namely fire, motor, miscellaneous accident, engineering, aviation and agriculture. The company is also licenced to reinsure life assurance products.

2. SHAREHOLDING

The Company’s shareholding was in the hands of the promoters and other shareholders up to 30 September 2013. The Company’s shares were listed on the Lusaka Stock Exchange on 30 September 2013.

3. PRINCIPAL ACCOUNTING POLICIES The principal accounting policies applied by the Company in the preparation of these financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

(a) Basis of presentationThe financial statements are prepared in accordance with the provisions of the Companies Act and International Financial Reporting Standards (IFRS). The financial statements are presented in accordance with IAS 1 “Preparation of financial statements” (Revised 2007). The company has elected to present the “Statement of Comprehensive income” in two statements namely the “Income Statement” and “Statement of Comprehensive Income”. They have been prepared under the historic cost convention, as modified by the revaluation of property, plant and equipment, available-for-sale financial assets, and financial assets and liabilities at fair valuethrough profit and loss.

The preparation of financial statements in conformity with IFRS requires the use ofcertain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Company’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements, are disclosed in note 4.

b) New and revised standards that are effective for annual periods beginning on or after 1 January 2017The Company has not adopted any new standards or amendments that have a significant impact on the Company’s results or financial position.

30

32 33

The standards and amendments that are effective for the first time in 2017 (for entities with a 31 December 2017 year end) and could be applicable to the Company are:

• ‘Annual Improvements to IFRSs’ 2014 - 2016 cycle; • Classification and measurement of share-based payment transactions (Amendments to IFRS 2)• Recognition of Deferred tax assets for unrealized losses (Amendments to IAS 12); and• ‘Disclosure Initiative’ (Amendments to IAS 7)

These amendments do not have a significant impact on amounts recognised in prior periods and will not affect current or future periods.

c) Standards, amendments and interpretations to existing standards that are not yet effective and have not been adopted early by the Company

At the date of authorisation of these financial statements, certain new standards, and

amendments to existing standards have been published by the IASB that are not yet effective, and have not been adopted early by the Company. Information on those expected to be relevant to the Company’s financial statements is provided below.

Management anticipates that all relevant pronouncements will be adopted in the Company’s accounting policies for the first period beginning after the effective date of the pronouncement. New standards, interpretations and amendments not either adopted or listed below are not expected to have a material impact on the Company’s financial statements.

IFRS 9 ‘Financial Instruments’ The new standard for financial instruments (IFRS 9) introduces extensive changes to

IAS 39’s guidance on the classification and measurement of financial assets and introduces a new ‘expected credit loss’ model for the impairment of financial assets. IFRS 9 also provides new guidance on the application of hedge accounting.

Management has started to assess the impact of IFRS 9 but is not yet in a position to provide quantified information. At this stage the main areas of expected impact are as follows:

• the classification and measurement of the Company’s financial assets will need to be reviewed based on the new criteria that considers the assets’ contractual cash flows and the business model in which they are managed

• an expected credit loss-based impairment will need to be recognised on the Company’s trade receivables and investments in debt-type assets currently classified as Available For Sale (AFS) and Held To Maturity (HTM), unless classified as at fair value through profit or loss in accordance with the new criteria

• it will no longer be possible to measure equity investments at cost less impairment and

all such investments will instead be measured at fair value. Changes in fair value will be presented in profit or loss unless the Company makes an irrevocable designation to present them in other comprehensive income.

• if the Company continues to elect the fair value option for certain financial liabilities, fair value movements will be presented in other comprehensive income to the extent those changes relate to the Company’s own credit risk.

IFRS 9 is effective for annual reporting periods beginning on or after 1 January 2018.

IFRS 15 ‘Revenue from Contracts with Customers’IFRS 15 presents new requirements for the recognition of revenue, replacing IAS 18 ‘Revenue’, IAS 11 ‘Construction Contracts’, and several revenue-related Interpretations. The new standard establishes a control-based revenue recognition model and provides additional guidance in many areas not covered in detail under existing IFRSs, including how to account for arrangements with multiple performance obligations, variable pricing, customer refund rights, supplier repurchase options, and other common complexities.

IFRS 15 is effective for annual reporting periods beginning on or after 1 January 2018.

IFRS 15 introduces new guidance that will require the Company to evaluate the separability of multiple elements based on whether they are ‘distinct’. A promised good or service is ‘distinct’ if both:• the customer benefits from the item either on its own or together with other readily available resources, and• it is ‘separately identifiable’ (i.e. the company does not provide a significant service integrating, modifying or customising it).

The subsequent allocation of arrangement consideration to individual performance obligations is based on their relative stand-alone selling prices.

The company is currently in the process of reviewing all its contracts to ascertain how the new requirements will impact the identification of distinct goods or services and the allocation of consideration to them.

The standard allows adoption using either retrospectively in full to each prior reporting period or modified retrospective with application only to contracts that are not complete at the date of initial application.

IFRS 16 ‘Leases’IFRS 16 will replace IAS 17 and three related Interpretations. Leases will be recorded on the statement of financial position in the form of a right-of-use asset and a lease liability.

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017 (CONTINUED)

34 35

IFRS 16 is effective from periods beginning on or after 1 January 2019. Management is yet to fully assess the impact of the Standard and therefore is unable to provide quantified information. However, in order to determine the impact the Company are in the process of:

• performing a full review of all agreements to assess whether any additional contracts will now become a lease under IFRS 16’s new definition;

• deciding which transitional provision to adopt; either full retrospective application or partial retrospective application (which means comparatives do not need to be restated). The partial application method also provides optional relief from reassessing whether contracts in place are, or contain, a lease, as well as other reliefs. Deciding which of these practical expedients to adopt is important as they are one-off choices;

• assessing their current disclosures for finance leases (note 2(m)) and operating leases (note 2(m)) as these are likely to form the basis of the amounts to be capitalised and become right-of-use assets;

• determining which optional accounting simplifications apply to their lease portfolio and if they are going to use these exemptions; and

• assessing the additional disclosures that will be required.

(d) Revenue recognition – Gross PremiumGross premium is recognised in the year in which the Insurance risks are covered, net of any provisions for expired risks. The underwriting result is net of retrocession, provision for unearned premiums, net claims incurred, commission cost and other expenses. Premium revenue represents the fair value of the consideration receivable for insurance risks covered.

(e) Interest incomeInterest income is recognised on a time apportioned basis using the effective interest method.

(f) Property, plant and equipmentProperty, plant and equipment are stated at valuation.

Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the company and the cost of the item can be measured reliably. All other repairs and maintenance are charged to the statement of comprehensive income during the financial year in which they are incurred.

Increases in the carrying amount arising on revaluation of property, plant and

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017 (CONTINUED)

equipment are credited to the revaluation surplus in shareholders’ equity. Decreases that offset previous increases of the same asset are charged against fair value reserves directly in equity; all other decreases are charged to the statement of comprehensive income. Each year, the difference between depreciation based on the revalued carrying amount of the asset charged to the statement of comprehensive income and depreciation based on the asset’s original cost, net of any related deferred income tax, is transferred from the revaluation surplus to retained earnings.

Depreciation is calculated to write off the cost of property, plant and equipment on a straight line basis over the expected useful lives of the assets concerned. The principal annual rates used for this purpose are:

Land and buildings 2% Motor vehicles 25% Office equipment, fixtures and fittings 25% Office furniture 15% Computer software 20%

Capital work in progress and investment properties are not depreciated.

The assets’ residual values and useful lives are reviewed at each reporting date and adjusted if appropriate.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its recoverable amount.

Gains and losses on disposals are determined by comparing the proceeds with the carrying amount. These are included in the statement of comprehensive income in the other operating income. When revalued assets are sold, the amounts included in the revaluation surplus relating to these assets are transferred to retained earnings.

(g) Financial assetsThe company classifies its investments into the following categories: financial assets at fair value through profit or loss, loans and other receivables, held-to-maturity financial assets and available-for-sale financial assets. The classification depends on the purpose for which the investments were acquired.

Management determines the classification of its investments at initial recognition and re-evaluate this at every reporting date.

36 37

(i) Financial assets at fair value through incomeThis category has two sub-categories: financial assets held for trading and those designated at fair value through profit or loss at inception.

A financial asset is classified into the ‘financial assets at fair value through income’ category at inception if acquired principally for the purpose of selling in the short term, if it forms part of a portfolio of financial assets in which there is evidence of short term profit taking, or if so designated by management.

Financial assets designated as at fair value through profit or loss at inception are those that are:

• held in internal funds to match investment contracts liabilities that are linked to the changes in fair value of these assets. The designation of these assets to be at fair value through profit or loss eliminates or significantly reduces a measurement or recognition inconsistency that would otherwise arise from measuring assets or liabilities or recognising the gains and losses on them on different bases;

• managed and whose performance is evaluated on a fair value basis. Assets that are part of these portfolios are designated upon initial recognition at fair value through profit or loss.

(ii) Loans and other receivablesLoans and other receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market other than those that the Company intends to sell in the short term or that it has designated as at fair value through income or available for sale. Loans and other receivables are recognised at fair value, less provision for impairment. A provision for impairment of loans and other receivables is established when there is objective evidence that the Company will not be able to collect all amounts due according to their original terms. Receivables arising from insurance contracts are also classified in this category and are reviewed for impairment as part of the impairment review of loans and receivables.

(iii) Held-to-maturity financial assetsHeld-to-maturity financial assets are non-derivative financial assets with fixed or determinable payments and fixed maturities other than those that meet the definition of loans and other receivables that the Company’s management has the positive intention and ability to hold to maturity. These assets are recognised at fair value, less provision for impairment. A provision for impairment is established when there is objective evidence that the Company will not be able to collect all amounts due according to their original terms.

(g) Financial assets (continued)(iv) Available-for-sale financial assets Available-for-sale financial assets are non-derivative financial assets that are either designated in this category or not classified in any of the other categories.

Financial assets are derecognised when the rights to receive cash flows from them have expired or where they have been transferred and the Company has also transferred substantially all risks and rewards of ownership.

Available-for-sale financial assets and financial assets at fair value through profit or loss are subsequently carried at fair value. Loans and other receivables and held-to-maturity financial assets are carried at fair value. Realised and unrealised gains and losses arising from changes in the fair value of the ‘financial assets at fair value through profit or loss’ category are included in the income statement in the year in which they arise. Unrealised gains and losses arising from changes in the fair value of non-monetary securities classified as available for sale are recognised in equity. When securities classified as available for sale are sold or impaired, the accumulated fair value adjustments are included in the income statement as net realised gains or losses on financial assets.

Interest on available-for-sale securities is recognised in the income statement. Dividends on available-for-sale equity instruments are recognised in the income statement when the Company’s right to receive payments is established.

The fair values of quoted investments are based on current bid prices. If the market for a financial asset is not active, the company establishes fair value by using valuation techniques.

(h) Impairment of assets (i) Financial assets carried at amortised costThe company assesses at each reporting date whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or group of financial assets is impaired and impairment losses are incurred only if there is objective evidence of impairment as a result of one or more events that have occurred after the initial recognition of the asset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated. Objective evidence that a financial asset or group of assets is impaired includes observable data that comes to the attention of the Company about the following events:

• significant financial difficulty of the issuer or debtor;• a breach of contract, such as a default or delinquency in payments;•it becoming probable that the issuer or debtor will enter bankruptcy or other financial reorganisation; or• observable data indicating that there is a measurable decrease in t h e estimated future cash flow from a group of financial assets since the initial recognition of those assets, although the decrease cannot yet be identified with the individual financial assets in the company, including:- adverse changes in the payment status of issuers or debtors in the company; or- national or local economic conditions that correlate with defaults on the assets in the company.

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017 (CONTINUED)

38 39

The Company first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant. If the Company determines that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is or continues to be recognised are not included in a collective assessment of impairment.

If there is objective evidence that an impairment loss has been incurred on loans and other receivables or held-to-maturity investments carried at amortised cost, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have been incurred) discounted at the assets original effective interest rate. The carrying amount of the asset is reduced through the use of an allowance account, and the amount of the loss is recognised in the income statement. If a held to maturity investment or a loan has a variable interest rate, the discount rate for reasoning any impairment loss is the current effective interest rate determined under contract.

If in a subsequent year, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised, the previously recognised impairment loss is reversed by adjusting the allowance account. The amount of the reversal is recognised in the statement of comprehensive income.

(ii) Financial assets carried at fair valueThe Company assesses at each reporting date whether there is objective evidence that an available-for-sale financial asset is impaired including in the case of equity investments classified as available for sale, a significant or prolonged decline in the fair value of the security below its cost. If any such evidence exists for available-for-sale financial assets, the cumulative loss – measured as the difference between the acquisition cost and current fair value, less any impairment loss on the financial asset previously recognised in profit or loss – is removed from equity and recognised in the income statement. Impairment losses recognised in the income statement on equity instruments are not subsequently reversed. The impairment loss is reversed through the income statement, if in a subsequent year the fair value of a debt instrument classified as available for sale increases and the increase can be objectively related to an event occurring after the impairment loss was recognised in profit or loss.

(iii) Impairment of other non-financial assetsAssets that have an indefinite useful life, for example land, are not subject to amortisation and are tested annually for impairment. Assets that are subject to amortisation are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows (cash-generating

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017 (CONTINUED)

units).

(i) Cash and cash equivalentsCash and cash equivalents include cash in hand, deposits held at call with banks, other short-term highly liquid investments and balances held with banks. The category also includes bank overdrafts.

(j) BorrowingsBorrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings are subsequently stated at amortised cost; any difference between the proceeds (net of transaction costs) and the redemption value is recognised in the income statement over the period of the borrowings using the effective interest method.

(k) Short/long term indebtednessShort term indebtedness includes all amounts due to be repaid within twelve months from the reporting date, including instalments due on loans of longer duration. Long term indebtedness represents all amounts repayable more than twelve months from the reporting date.

(l) Income taxIncome tax expense is the aggregate of the charge to the income statement in respect of current income tax and deferred income tax.Current income tax is the amount of income tax payable on the profit for the year determined in accordance with the Zambia Income Tax Act.Deferred income tax is provided in full, using the liability method, on all temporary differences arising between the tax bases of assets and liabilities and their carrying values for financial reporting purposes. However, if the deferred income tax arises from the initial recognition of an asset or liability in a transaction other than a business combination that at the time of the transaction affects neither accounting nor taxable profit or loss, it is not accounted for. Deferred income tax is determined using tax rates enacted or substantively enacted at the reporting date and are expected to apply when the related deferred income tax liability is settled.

Deferred income tax assets are recognised only to the extent that it is probable that future taxable profits will be available against which the temporary differences can be utilised.

(m) Insurance contracts – classificationThe Company issues contracts that transfer insurance risk or financial risk or both. Insurance contracts are those contracts that transfer significant insurance risk. Such contracts may also transfer financial risk. The Company defines as significant

40 41

insurance risk the possibility of having to pay benefits on the occurrence of an insured event that are at least 10% more than the benefits payable if the insured event did not occur.

(n) Unearned premiumsUnearned premiums are those proportions of the premiums written in a year, less retrocession premium, that relate to the periods of unexpired risk at the reporting date. These are calculated on a time basis using the 24th method.

(o) Net claims incurredClaims incurred comprise gross claims paid and changes in the provisions for reinsurance contract liability. Outstanding claims include claims reported but unpaid at the reporting date, and incurred but not reported claims (IBNR). The provisions for IBNR claims include a provision for claims handling expenses, and are estimated on the basis of the latest information available at the time of the preparation of the financial statements.

(p) Commission costThis is the commission payable to insurance companies for acquiring business. Part of the cost is offset by the commission earned from other reinsurers on the retrocession business.

(q) Retrocession premium

Retrocession premium relates to the portion of the total premium income written which is passed on to another reinsurer as retrocession to get protection against associated risks and liabilities. Retrocession premium is computed on the basis of agreed terms under the retrocession programme.

(r) Retrocession recoveryThis is recovery of claims from the reinsurers under the retrocession programme based on agreed terms of treaty.

(s) Deferred acquisition costs

Acquisition costs which represent commission are deferred over the year in which the related premiums are earned. The deferred portion is calculated by applying the 24th method on net commission.

(t) Reinsurance commission This is commission earned from other reinsurers under the retrocession programme.

(u) Foreign currencies (i) Functional and presentation currency

Items included in the financial statements are measured using the currency of the primary economic environment in which the Company operates (the ‘functional currency’). The financial statements are presented in Zambian Kwacha, which is the Company’s presentation currency.

(ii) Transactions and balancesForeign currency transactions are translated into the functional currency using the rates of exchange prevailing at the date of transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the statement of comprehensive income.

Translation differences on non-monetary items, such as equity at fair value through profit and loss, are reported as part of the fair value gain or loss. Translation differences on non-monetary items, such as equities classified as available-for-sale financial assets, are included in fair value reserve in equity.

(v) Employee benefits(i) Pension obligations

The Company operates a pension scheme. The scheme is generally funded through payments to an insurance company or trustee-administered funds, determined by periodic actuarial calculations. The Company has a defined contribution plan. A defined contribution plan is a pension plan under which the company pays fixed contributions into a separate entity. The Company has no legal or constructive obligations to pay further contributions if the fund does not hold sufficient assets to pay all employees the benefits relating to employee service in the current and prior years.

For defined contribution plan, the Company pays contributions to publicly or privately administered pension insurance plans on a mandatory, contractual or voluntary basis. The Company has no further payment obligations once the contributions have been paid. The contributions are recognised as employee benefit expense when they are due. Prepaid contributions are recognised as an asset to the extent that a cash refund or a reduction in the future payments is available.

(ii) Termination benefitsTermination benefits are payable when employment is terminated before the normal retirement date, or whenever an employee accepts voluntary redundancy in exchange for these benefits. The Company recognises termination benefits when it is demonstrably committed to either: terminating the employment of current employees according to a detailed formal plan without possibility of withdrawal; or providing termination benefits as a result of an offer made to encourage voluntary redundancy.

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017 (CONTINUED)

42 43

5. MANAGEMENT OF REINSURANCE AND FINANCIAL RISKThe Company issues contracts that transfer reinsurance risk or financial risk or both. This section summarises these risks and the way the Company manages them.

5.1 Reinsurance riskThe risk under any one reinsurance contract is the possibility that the insured event occurs and the uncertainty of the amount of the resulting claim. By the very nature of a reinsurance contract, this risk is random and therefore unpredictable.

For a portfolio of reinsurance contracts where the theory of probability is applied to pricing and provisioning, the principal risk that the Company faces under its reinsurance contracts is that the actual claims and benefit payments exceed the carrying amount of the reinsurance liabilities. This could occur because the frequency or severity of claims and benefits are greater than estimated. Reinsurance events are random and the actual number and amount of claims and benefits will vary from year to year from the level established using statistical techniques.

Experience shows that the larger the portfolio of similar reinsurance contracts, the smaller the relative variability about the expected outcome will be. In addition, a more diversified portfolio is less likely to be affected by a change in any subset of the portfolio. The Company has developed its reinsurance underwriting strategy to diversify the type of reinsurance risks accepted and within each of these categories to achieve a sufficiently large population of risks to reduce the variability of the expected outcome.

Factors that aggravate reinsurance risk include lack of risk diversification in terms of type and amount of risk, geographical location and type of industry covered.

5.2 Financial riskThe Company is exposed to a range of financial risks through its financial assets, financial liabilities (investment contracts and borrowings), retrocession assets and reinsurance liabilities. In particular, the key financial risk is that in the long-term its investment proceeds are not sufficient to fund the obligations arising from its reinsurance and investment contracts. The most important components of this financial risk are interest rate risk, equity price risk, foreign currency risk and credit risk.

These risks arise from open positions in interest rate, currency and equity products, all of which are exposed to general and specific market movements. The risks that the Company primarily faces due to the nature of its investments

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017 (CONTINUED)

(w) ProvisionsRestructuring costs and legal claimsProvisions for restructuring costs and legal claims are recognised when: the company has a present legal or constructive obligation as a result of past events; it is more likely than not that an outflow of resources will be required to settle the obligation; and the amount has been reliably estimated. Restructuring provisions comprise lease termination penalties and employee termination payments. Provisions are not recognised for future operating losses. Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognised even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small.

(x) Dividend distributionDividend distribution to the Company’s shareholders is recognised as a liability in the financial statements in the year in which the dividends are approved by the Company’s shareholders.

4. CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTSThe Company makes estimates and assumptions that affect the reported amounts of assets and liabilities within the next financial year. Estimates and judgements are continually evaluated and based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

(a) The ultimate liability arising from claims made under reinsurance contractsThe estimation of the ultimate liability arising from claims made under reinsurance contracts is the Company’s most critical accounting estimate. There are several sources of uncertainty that need to be considered in the estimate of the liability that the company will ultimately pay for such claims. This includes the estimation of various reserves and provisions.

(b) Impairment of available-for-sale equity financial assetsThe Company determines that available-for-sale equity financial assets are impaired when there has been a significant or prolonged decline in the fair value below its cost. This determination of what is significant or prolonged requires judgement. In making this judgement, the Company evaluates among other factors, the normal volatility in share price, the financial health of the investee, industry and sector performance, changes in technology, and operational and financing cash flow. Impairment may be appropriate when there is evidence of deterioration in the financial health of the investee, industry and sector performance, changes in technology, and financing and operational cash flows.

44 45

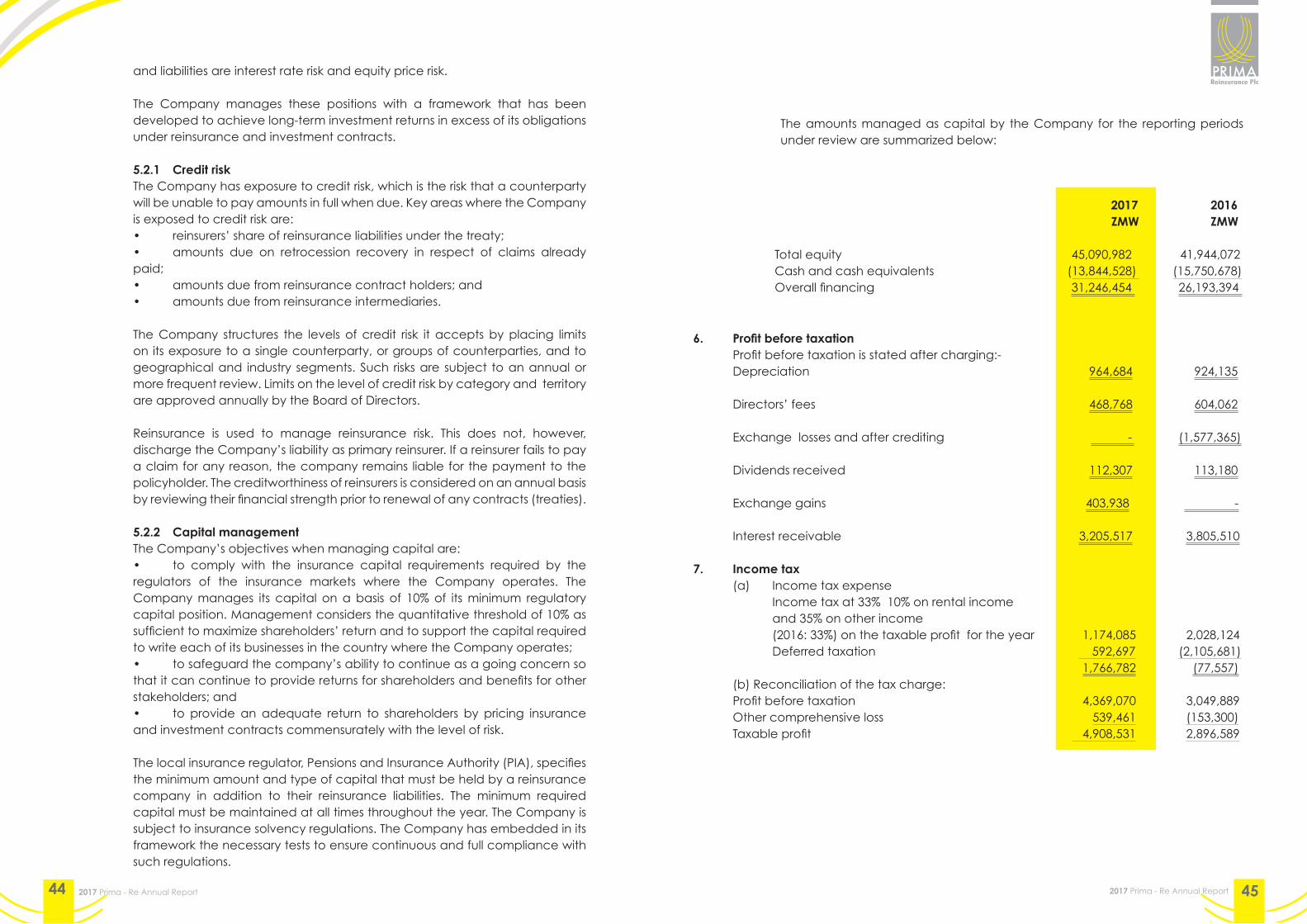

2017 2016 ZMW ZMW

Total equity 45,090,982 41,944,072Cash and cash equivalents (13,844,528) (15,750,678)Overall financing 31,246,454 26,193,394

6. Profit before taxation Profit before taxation is stated after charging:- Depreciation 964,684 924,135 Directors’ fees 468,768 604,062 Exchange losses and after crediting - (1,577,365) Dividends received 112,307 113,180 Exchange gains 403,938 - Interest receivable 3,205,517 3,805,510

7. Income tax (a) Income tax expense Income tax at 33% 10% on rental income and 35% on other income (2016: 33%) on the taxable profit for the year 1,174,085 2,028,124 Deferred taxation 592,697 (2,105,681) 1,766,782 (77,557)(b) Reconciliation of the tax charge:Profit before taxation 4,369,070 3,049,889Other comprehensive loss 539,461 (153,300)Taxable profit 4,908,531 2,896,589

and liabilities are interest rate risk and equity price risk.

The Company manages these positions with a framework that has been developed to achieve long-term investment returns in excess of its obligations under reinsurance and investment contracts.

5.2.1 Credit riskThe Company has exposure to credit risk, which is the risk that a counterparty will be unable to pay amounts in full when due. Key areas where the Company is exposed to credit risk are:• reinsurers’ share of reinsurance liabilities under the treaty;• amounts due on retrocession recovery in respect of claims already paid;• amounts due from reinsurance contract holders; and• amounts due from reinsurance intermediaries.

The Company structures the levels of credit risk it accepts by placing limits on its exposure to a single counterparty, or groups of counterparties, and to geographical and industry segments. Such risks are subject to an annual or more frequent review. Limits on the level of credit risk by category and territory are approved annually by the Board of Directors.

Reinsurance is used to manage reinsurance risk. This does not, however, discharge the Company’s liability as primary reinsurer. If a reinsurer fails to pay a claim for any reason, the company remains liable for the payment to the policyholder. The creditworthiness of reinsurers is considered on an annual basis by reviewing their financial strength prior to renewal of any contracts (treaties).

5.2.2 Capital managementThe Company’s objectives when managing capital are:• to comply with the insurance capital requirements required by the regulators of the insurance markets where the Company operates. The Company manages its capital on a basis of 10% of its minimum regulatory capital position. Management considers the quantitative threshold of 10% as sufficient to maximize shareholders’ return and to support the capital required to write each of its businesses in the country where the Company operates;• to safeguard the company’s ability to continue as a going concern so that it can continue to provide returns for shareholders and benefits for other stakeholders; and• to provide an adequate return to shareholders by pricing insurance and investment contracts commensurately with the level of risk.

The local insurance regulator, Pensions and Insurance Authority (PIA), specifies the minimum amount and type of capital that must be held by a reinsurance company in addition to their reinsurance liabilities. The minimum required capital must be maintained at all times throughout the year. The Company is subject to insurance solvency regulations. The Company has embedded in its framework the necessary tests to ensure continuous and full compliance with such regulations.

The amounts managed as capital by the Company for the reporting periods under review are summarized below:

46 47

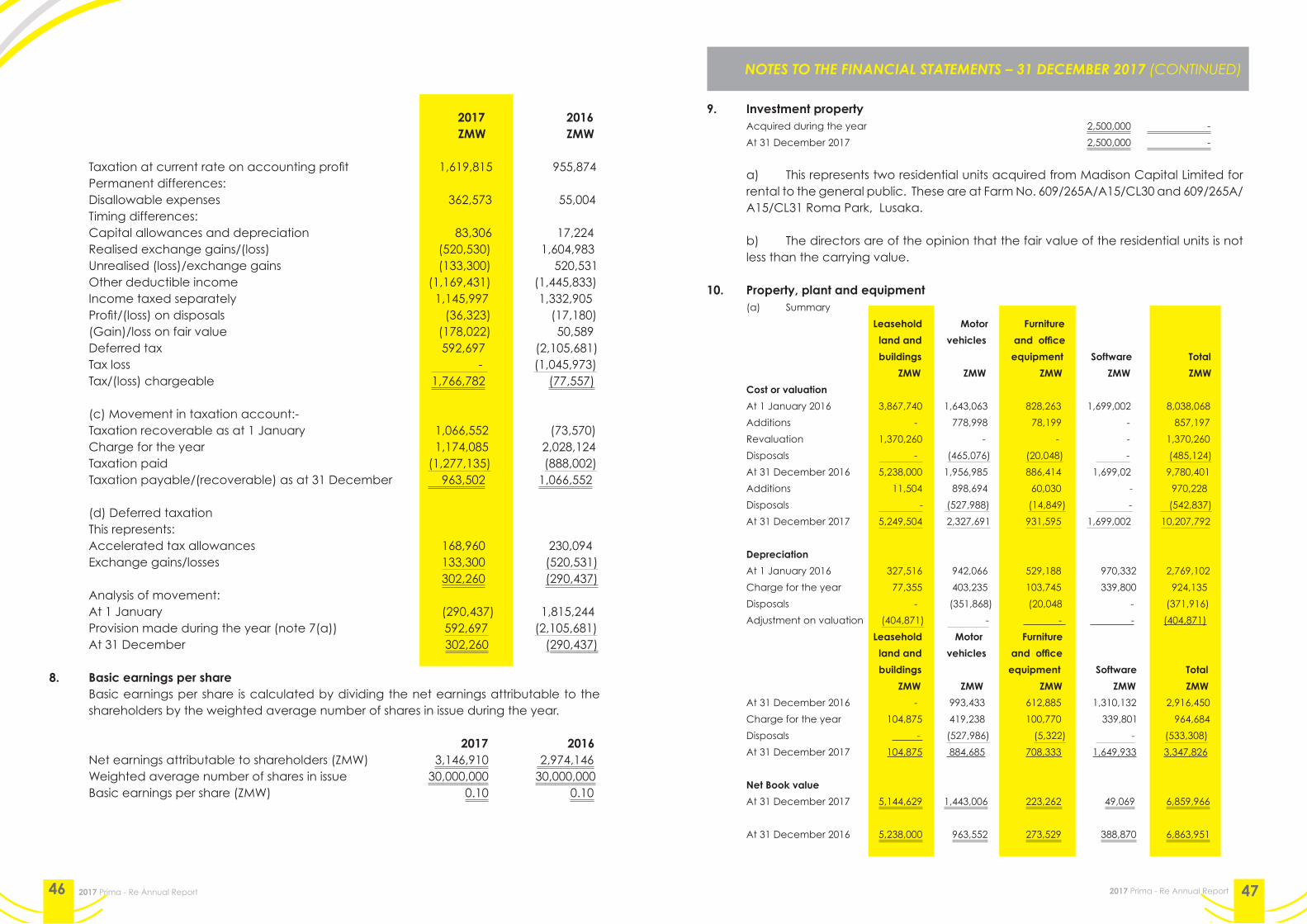

9. Investment property Acquired during the year 2,500,000 -

At 31 December 2017 2,500,000 -

a) This represents two residential units acquired from Madison Capital Limited for rental to the general public. These are at Farm No. 609/265A/A15/CL30 and 609/265A/A15/CL31 Roma Park, Lusaka.

b) The directors are of the opinion that the fair value of the residential units is not less than the carrying value.

10. Property, plant and equipment (a) Summary

Leasehold Motor Furniture

land and vehicles and office

buildings equipment Software Total

ZMW ZMW ZMW ZMW ZMW

Cost or valuation

At 1 January 2016 3,867,740 1,643,063 828,263 1,699,002 8,038,068

Additions - 778,998 78,199 - 857,197

Revaluation 1,370,260 - - - 1,370,260

Disposals - (465,076) (20,048) - (485,124)

At 31 December 2016 5,238,000 1,956,985 886,414 1,699,02 9,780,401

Additions 11,504 898,694 60,030 - 970,228

Disposals - (527,988) (14,849) - (542,837)

At 31 December 2017 5,249,504 2,327,691 931,595 1,699,002 10,207,792

Depreciation

At 1 January 2016 327,516 942,066 529,188 970,332 2,769,102

Charge for the year 77,355 403,235 103,745 339,800 924,135

Disposals - (351,868) (20,048 - (371,916)

Adjustment on valuation (404,871) - - - (404,871)

Leasehold Motor Furniture

land and vehicles and office

buildings equipment Software Total

ZMW ZMW ZMW ZMW ZMW

At 31 December 2016 - 993,433 612,885 1,310,132 2,916,450

Charge for the year 104,875 419,238 100,770 339,801 964,684

Disposals - (527,986) (5,322) - (533,308)

At 31 December 2017 104,875 884,685 708,333 1,649,933 3,347,826

Net Book value

At 31 December 2017 5,144,629 1,443,006 223,262 49,069 6,859,966

At 31 December 2016 5,238,000 963,552 273,529 388,870 6,863,951

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017 (CONTINUED)

2017 2016 ZMW ZMW

Taxation at current rate on accounting profit 1,619,815 955,874Permanent differences:Disallowable expenses 362,573 55,004Timing differences:Capital allowances and depreciation 83,306 17,224Realised exchange gains/(loss) (520,530) 1,604,983Unrealised (loss)/exchange gains (133,300) 520,531Other deductible income (1,169,431) (1,445,833)Income taxed separately 1,145,997 1,332,905Profit/(loss) on disposals (36,323) (17,180)(Gain)/loss on fair value (178,022) 50,589Deferred tax 592,697 (2,105,681) Tax loss - (1,045,973)Tax/(loss) chargeable 1,766,782 (77,557)

(c) Movement in taxation account:-Taxation recoverable as at 1 January 1,066,552 (73,570)Charge for the year 1,174,085 2,028,124Taxation paid (1,277,135) (888,002)Taxation payable/(recoverable) as at 31 December 963,502 1,066,552

(d) Deferred taxation This represents: Accelerated tax allowances 168,960 230,094Exchange gains/losses 133,300 (520,531) 302,260 (290,437)Analysis of movement:At 1 January (290,437) 1,815,244Provision made during the year (note 7(a)) 592,697 (2,105,681)At 31 December 302,260 (290,437)

8. Basic earnings per shareBasic earnings per share is calculated by dividing the net earnings attributable to the shareholders by the weighted average number of shares in issue during the year.

2017 2016Net earnings attributable to shareholders (ZMW) 3,146,910 2,974,146Weighted average number of shares in issue 30,000,000 30,000,000Basic earnings per share (ZMW) 0.10 0.10

48 49

a) The financial statements include the net (depreciation)/appreciation of investments in shares as follows:

Number of shares Market Value Capital Appreciation/

(Depreciation)

Cost

Opening

bal.

Closing bal. 01-Jan-17 31-Dec-17

01-Jan-17 31-Dec-17 ZMW ZMW ZMW

Investrust Bank PLC 14,090 14,090 190,215 - 190,215

Copperbelt

Energy PLC

568,835 568,835 494,886 324,236 819,121

Copperbelt

Energy-Rights issue

355,522 355,522 309,304 202,648 511,952

CEC Africa - 924,357 - - 1

Lafarge Zambia

PLC

19,231 19,231 99,617 20,577 120,194

Madison Financial

Services PLC

50,000 50,000 162,000 (8,000) 154,000

TOTAL 1,007,678 1,932,035 1,256,022 539,461 1,795,483

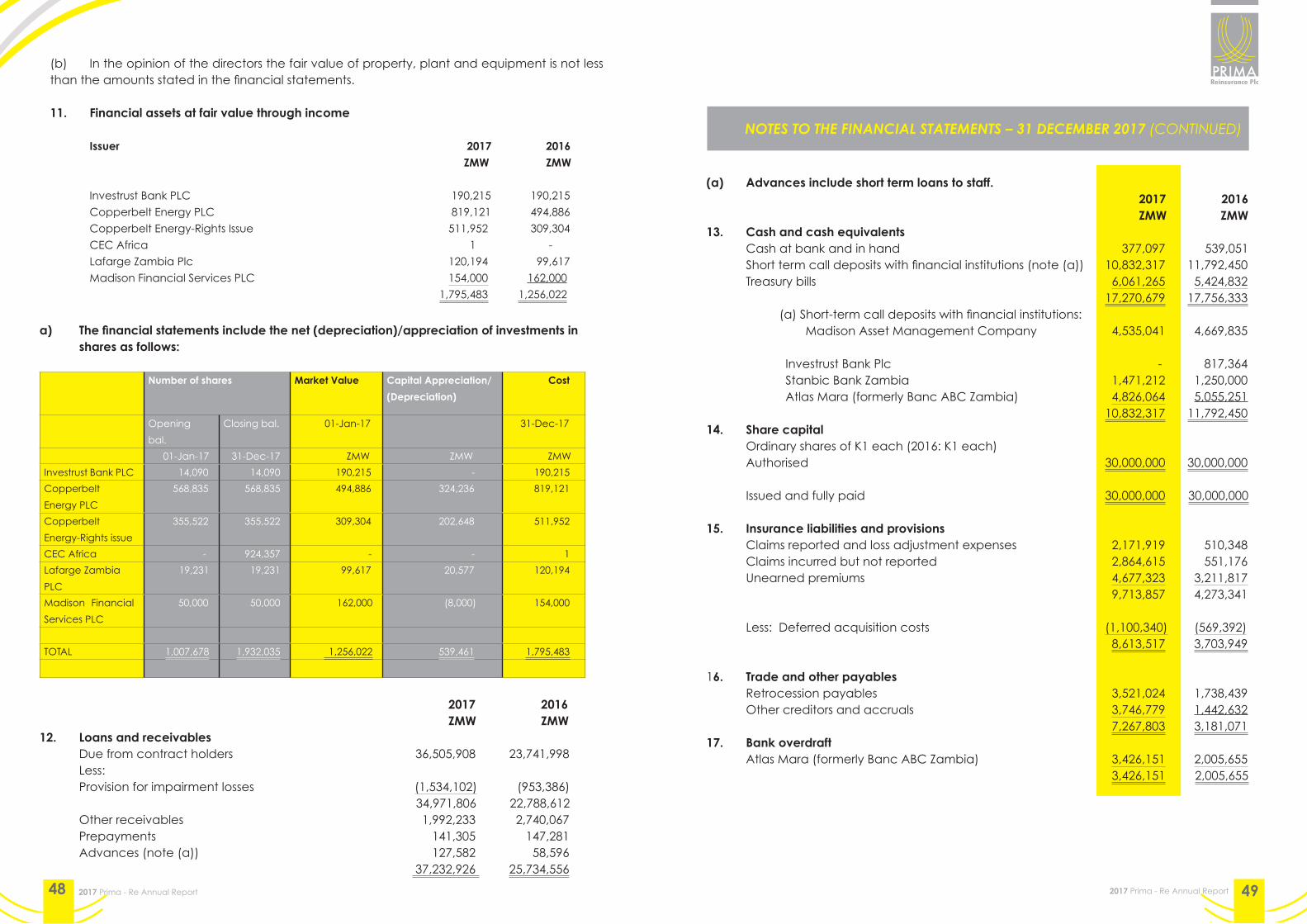

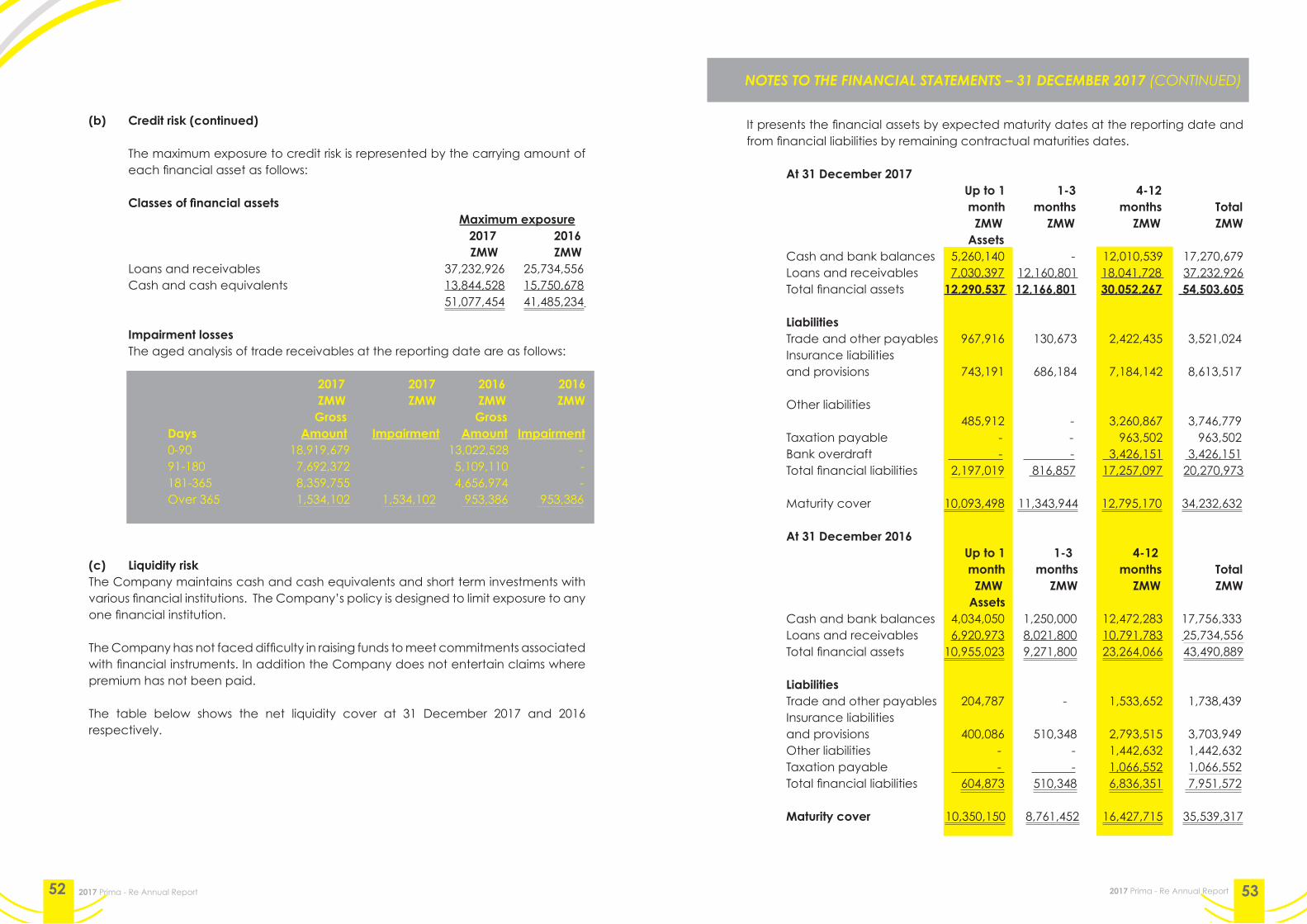

2017 2016 ZMW ZMW12. Loans and receivables Due from contract holders 36,505,908 23,741,998 Less: Provision for impairment losses (1,534,102) (953,386) 34,971,806 22,788,612 Other receivables 1,992,233 2,740,067 Prepayments 141,305 147,281 Advances (note (a)) 127,582 58,596 37,232,926 25,734,556

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2017 (CONTINUED)

(a) Advances include short term loans to staff. 2017 2016 ZMW ZMW13. Cash and cash equivalents Cash at bank and in hand 377,097 539,051 Short term call deposits with financial institutions (note (a)) 10,832,317 11,792,450 Treasury bills 6,061,265 5,424,832 17,270,679 17,756,333 (a) Short-term call deposits with financial institutions: Madison Asset Management Company 4,535,041 4,669,835 Investrust Bank Plc - 817,364 Stanbic Bank Zambia 1,471,212 1,250,000 Atlas Mara (formerly Banc ABC Zambia) 4,826,064 5,055,251 10,832,317 11,792,450 14. Share capital Ordinary shares of K1 each (2016: K1 each) Authorised 30,000,000 30,000,000 Issued and fully paid 30,000,000 30,000,000 15. Insurance liabilities and provisions Claims reported and loss adjustment expenses 2,171,919 510,348 Claims incurred but not reported 2,864,615 551,176 Unearned premiums 4,677,323 3,211,817 9,713,857 4,273,341 Less: Deferred acquisition costs (1,100,340) (569,392) 8,613,517 3,703,949

16. Trade and other payables Retrocession payables 3,521,024 1,738,439 Other creditors and accruals 3,746,779 1,442,632 7,267,803 3,181,07117. Bank overdraft Atlas Mara (formerly Banc ABC Zambia) 3,426,151 2,005,655 3,426,151 2,005,655

(b) In the opinion of the directors the fair value of property, plant and equipment is not less than the amounts stated in the financial statements.

11. Financial assets at fair value through income

Issuer 2017 2016 ZMW ZMW Investrust Bank PLC 190,215 190,215

Copperbelt Energy PLC 819,121 494,886

Copperbelt Energy-Rights Issue 511,952 309,304

CEC Africa 1 -

Lafarge Zambia Plc 120,194 99,617

Madison Financial Services PLC 154,000 162,000

1,795,483 1,256,022

50 51

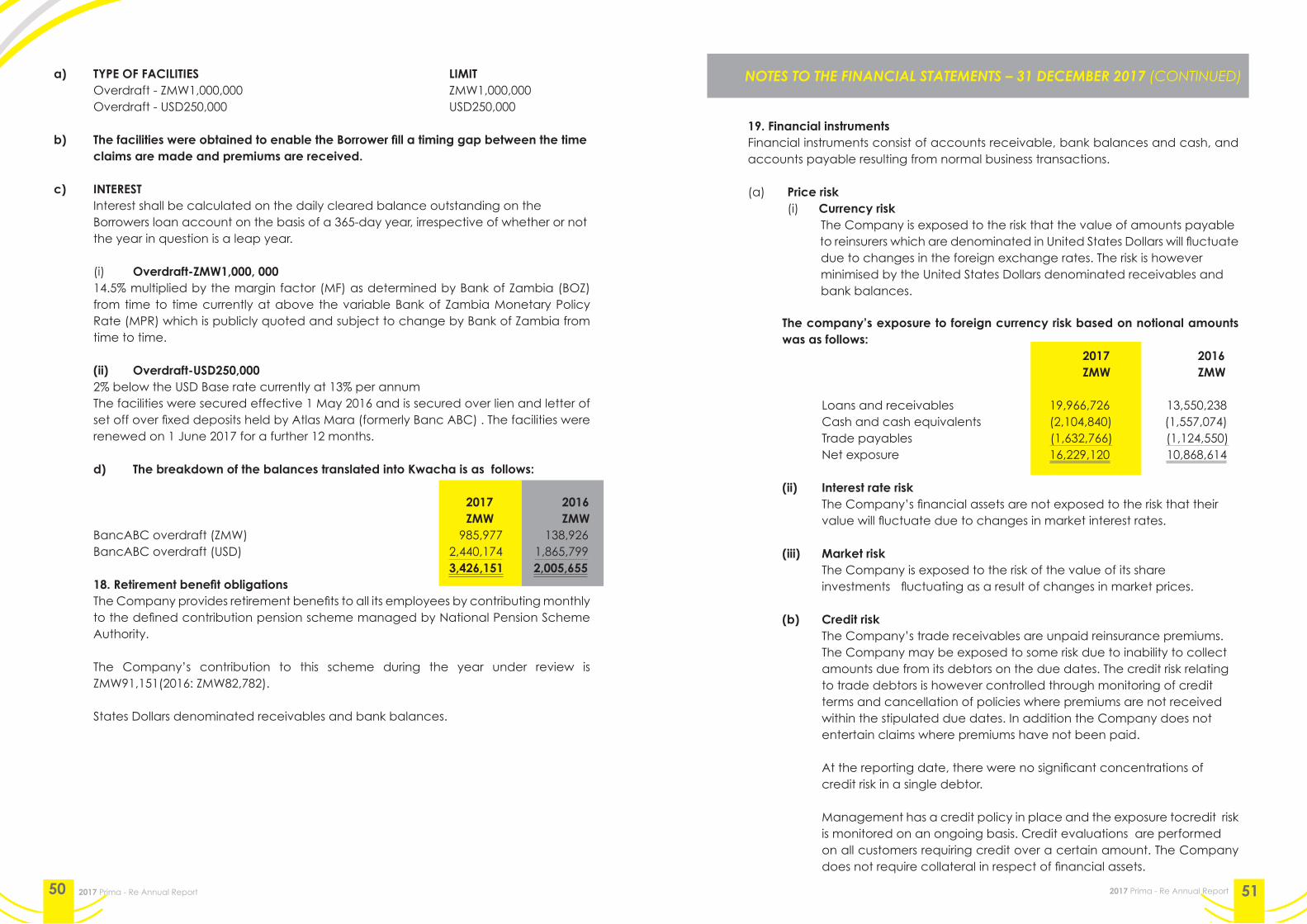

a) TYPE OF FACILITIES LIMIT Overdraft - ZMW1,000,000 ZMW1,000,000 Overdraft - USD250,000 USD250,000

b) The facilities were obtained to enable the Borrower fill a timing gap between the time claims are made and premiums are received.