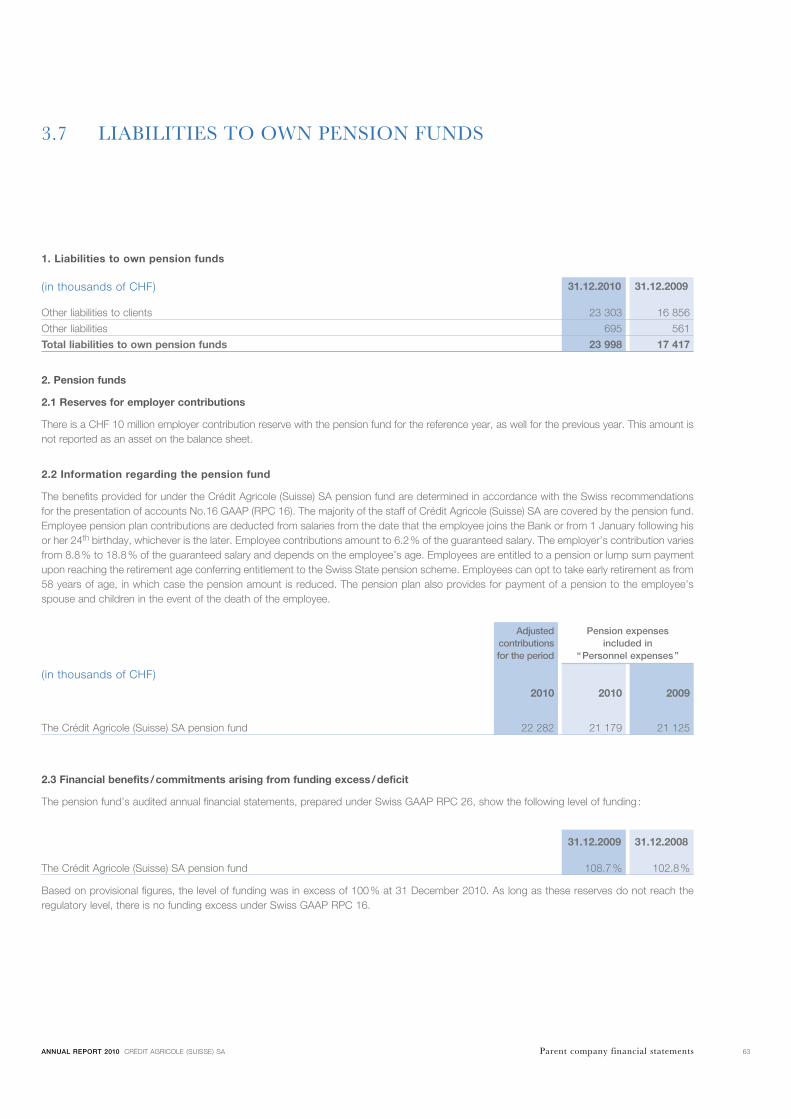

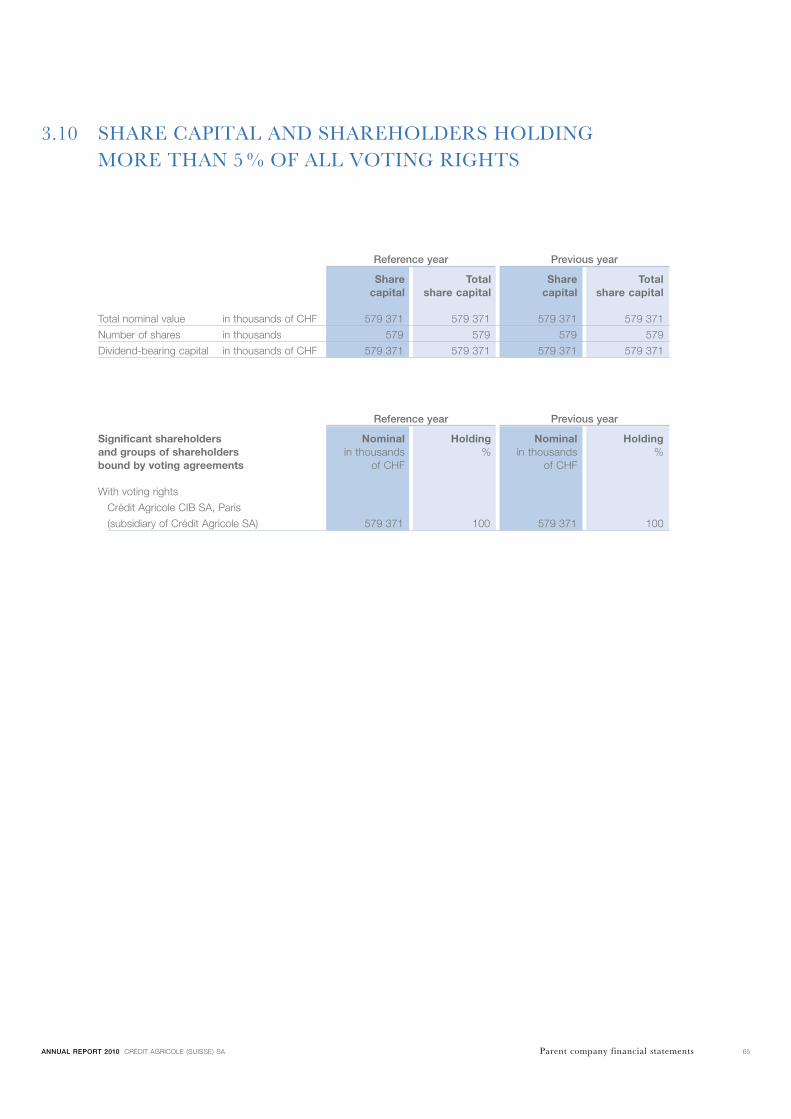

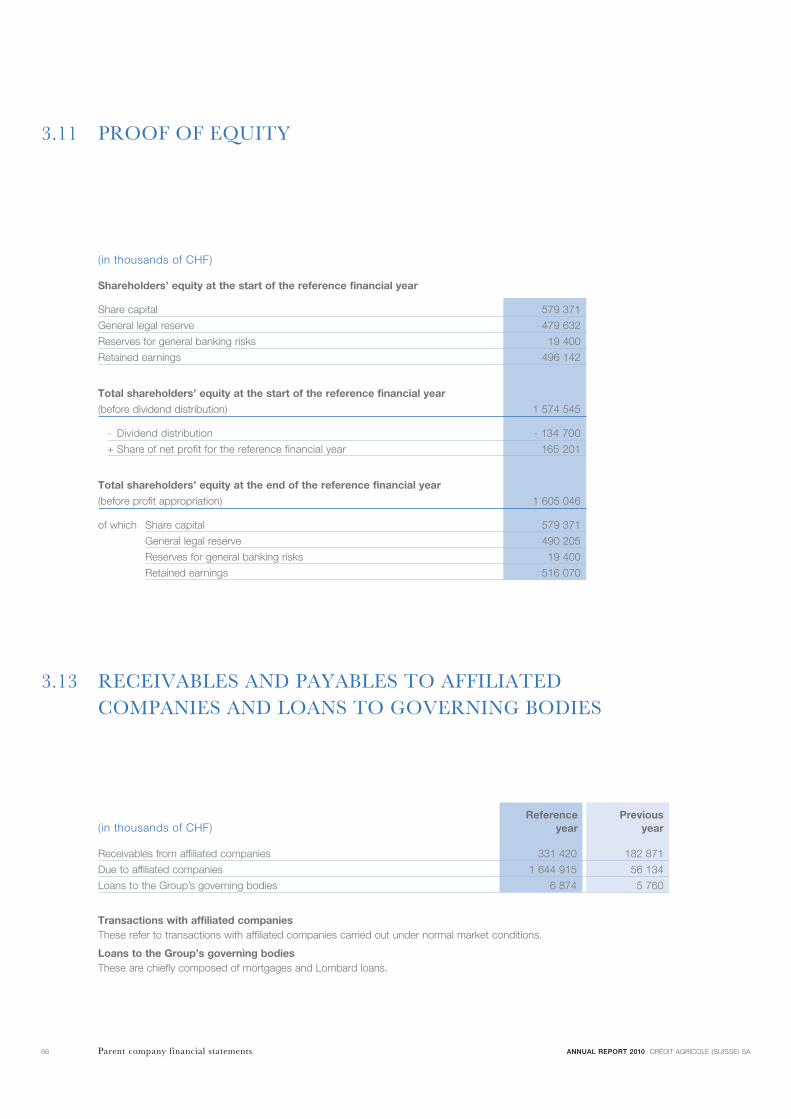

Embed Size (px)

Citation preview

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA

Our strength at the service of your future

Joumana Jamhouri’s work takes us on an original journey to the heart of industrial design, revealing unsuspected sensitivity and surprising beauty.

Lebanese-American Joumana Jamhouri, a graduate of New York Institute of Photography, focuses on industrial and architectural photography and also produces landscape and documentary work. She lives in Beirut, where she teaches photography at university. Bringing an original and human touch to the manufactured realism of her subjects, she creates captivating worlds in which mechanics give way to aesthetics. For Joumana Jahmouri, industry holds a store of little-explored treasures. Seeking to highlight the contrasts and paradoxes of a world widely perceived as cold and inhuman, she depicts volumes, perspectives, colours, lighting, shapes and materials with delicate and unexpected emotion. This convergence of contrasts is found throughout her work, inspired by the war years

of her childhood and by the desire to transcend and control chaos in order to achieve peace of mind and serenity. Her photographs have been published in numerous magazines and exhibited in Beirut, Abu Dhabi, Paris, Mexico, Washington and Munich, and at the prestigious Museum of Modern Art (MoMA) in New York.

Joumana Jamhouri’s well-grounded and realistic artistic approach to the world of industry perfectly reflects the strength and stability at the heart of Crédit Agricole (Suisse) SA’s values. Industry, a creator of value and an integral part of our modern environment, also upholds the common sense and real assets that we highlight in our invest- ment policy. Our Bank promotes lasting relationships that ensure our clients’ peace of mind and durability, even in today’s highly contrasted world economy.

This is why we have chosen to illustrate this year’s Annual Report with the photographic work of Joumana Jamhouri.

Shedding new light on industrial aesthetics

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 1

Ribeirao Preto

Nassau

Belo HorizonteRio de Janeiro

Sao Paulo

Montevideo

Hong Kong

Singapore

BrusselsFrance

Spain

KarachiDubai

DohaBeirutTel Aviv

Egypt

Switzerland

Monaco

Luxembourg

Abu DhabiBahrain

Miami

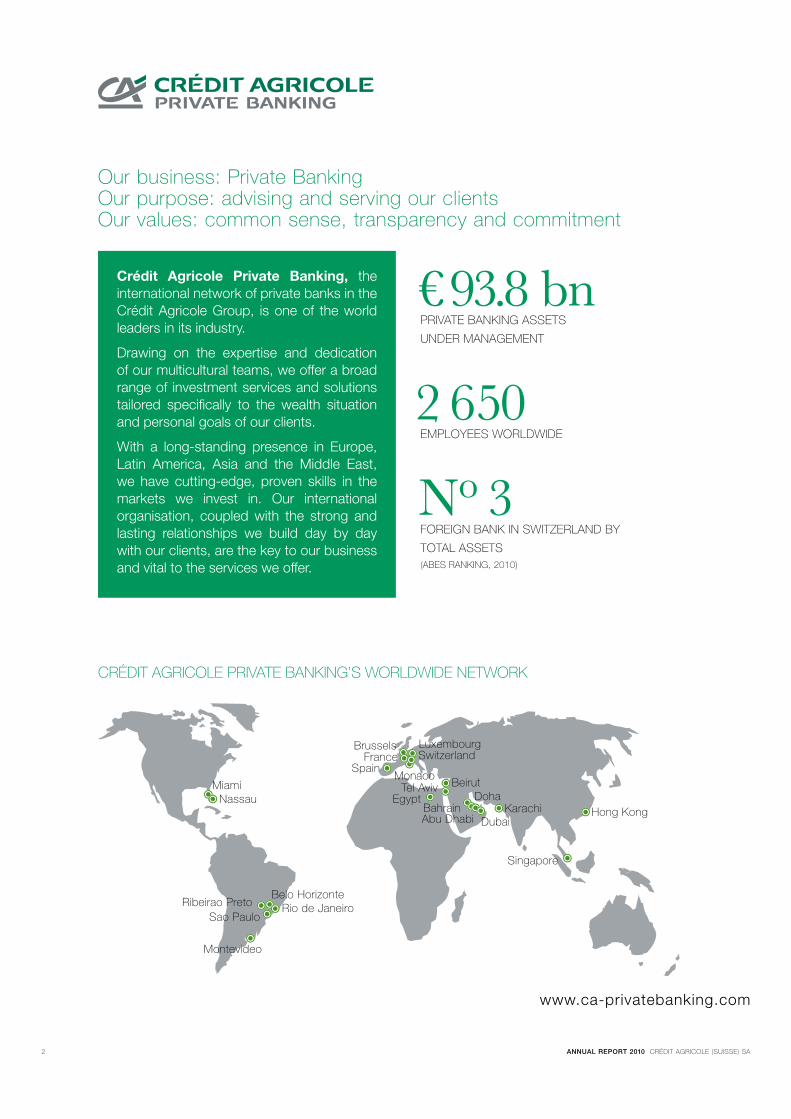

Our business: Private Banking Our purpose: advising and serving our clients Our values: common sense, transparency and commitment

CRÉDIT AGRICOLE PRIvATE BANKING’S wORLDwIDE NETwORK

www.ca-privatebanking.com

Crédit Agricole Private Banking, the international network of private banks in the Crédit Agricole Group, is one of the world leaders in its industry.

Drawing on the expertise and dedication of our multicultural teams, we offer a broad range of investment services and solutions tailored specifically to the wealth situation and personal goals of our clients.

With a long-standing presence in Europe, Latin America, Asia and the Middle East, we have cutting-edge, proven skills in the markets we invest in. Our international organisation, coupled with the strong and lasting relationships we build day by day with our clients, are the key to our business and vital to the services we offer.

€ 93.8 bnPRIvATE BANKING ASSETS

UNDER mANAGEmENT

2 650EmPLOyEES wORLDwIDE

No 3fOREIGN BANK IN SwITzERLAND By

TOTAL ASSETS (ABES RANKING, 2010)

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA2

4CRÉDIT AGRICOLE GROUP

7mESSAGE fROm ThE ChAIRmAN

AND ThE GENERAL mANAGEmENT

8mANAGEmENT BODIES

10ECONOmIC AND fINANCIAL ENvIRONmENT

12CRÉDIT AGRICOLE (SUISSE) SA

BUSINESS UPDATE

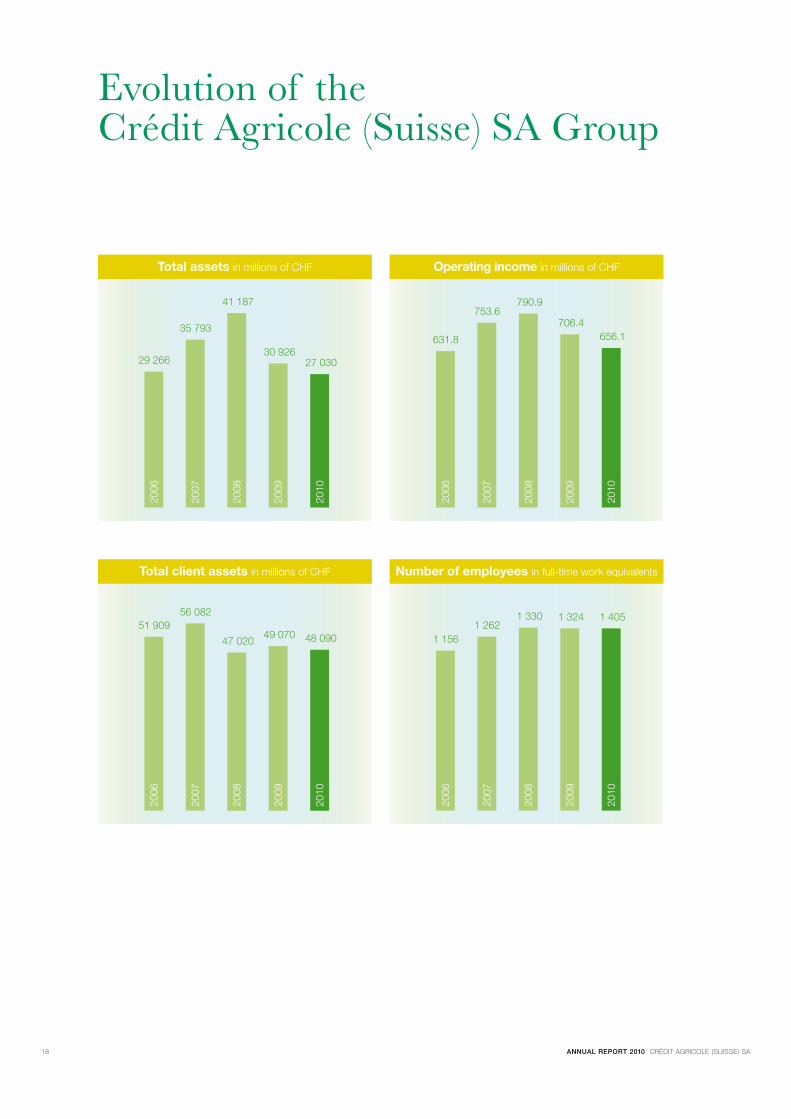

18EvOLUTION Of

ThE CRÉDIT AGRICOLE (SUISSE) SA GROUP

19CONSOLIDATED KEy fIGURES

20CONSOlidated

fiNaNCial StatemeNtS

22CONSOLIDATED BALANCE ShEET

AS AT 31 DECEmBER 2010

24CONSOLIDATED INCOmE STATEmENT

fOR ThE yEAR 2010

26CONSOLIDATED CASh fLOw STATEmENT

fOR ThE yEAR 2010

28NOTES TO ThE CONSOLIDATED

fINANCIAL STATEmENTS

53REPORT Of

ThE STATUTORy AUDITOR

54PareNt COmPaNy

fiNaNCial StatemeNtS

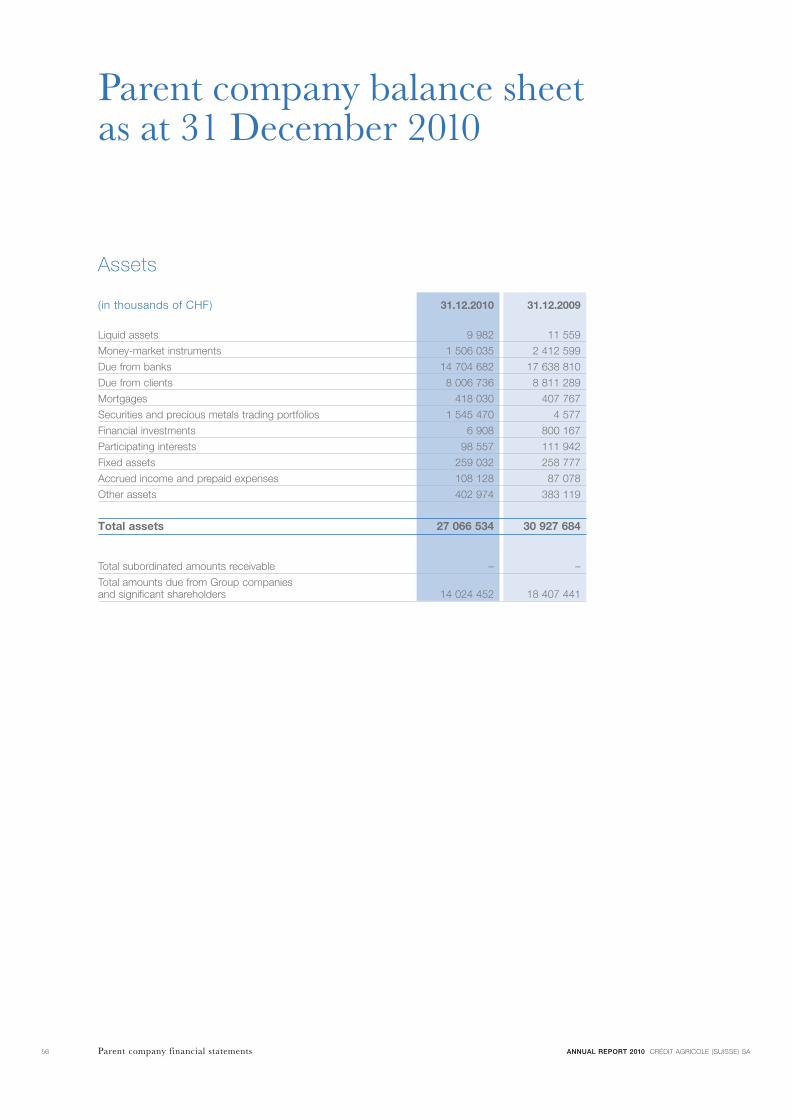

56PARENT COmPANy BALANCE ShEET

AS AT 31 DECEmBER 2010

58PARENT COmPANy INCOmE STATEmENT

fOR ThE yEAR 2010

60NOTES TO

ThE fINANCIAL STATEmENTS

68PrOPOSal tO

the aNNual GeNeral

meetiNG

69REPORT Of

ThE STATUTORy AUDITOR

70NetwOrk Of OffiCeS

Contents

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 3

The Crédit Agricole Group is market leader in full-service Retail Banking in France and one of the largest banks in Europe.

With operations in 70 countries, the Crédit Agricole Group is a leading partner in supporting clients with their projects in all areas of Retail Banking and associated specialised business lines : day-to-day banking, savings, home and consumer loans, insurance, Private Banking, asset management, leasing and factoring, and Corporate and Investment Banking.

On the strength of its cooperative and mutualist foundations, the Crédit Agricole Group’s expansion is underpinned by balanced growth serving the real economy and respecting the interests of its 54 million customers, 1.2 million shareholders, 6.1 million cooperative shareholders and its 160 000 employees.

Crédit Agricole is included in the three main sustainable development indices : Aspi Eurozone since 2004, FTSE4Good since 2005 and the DJSI since 2008 (Europe and worldwide). It is ranked the eighth most sustainable corporation in the world and No. 1 in France in the 2011 Global 100 List.

www.credit-agricole.com

Profile

3.6BILLION

NET INCOME - GROUP SHARE

71.5BILLION

SHAREHOLDERS’ EQUITY

– GROUP SHARE

10.3 %TIER ONE RATIO

4

• Institutional investors : 30.9 %

•Individual shareholders : 8.2 %

•Employees via employee mutual funds : 4.6 %

Retail Banking

In France– 25 % of share capital in the

Regional Banks (excl. the Regional Bank of Corsica)

– LCL

International Retail Banking– Cariparma FriulAdria Group– Emporiki– Crédit du Maroc– Crédit Agricole Egypt– Lukas Bank

Specialised business lines

Specialised financial services– Consumer finance– Lease finance– Factoring

Savings management– Asset management– Insurance– Private Banking

Corporate and Investment Banking

– Coverage and Investment Banking

– Equity Brokerage and Derivatives

– Fixed Income Markets– Structured Finance

55.9 % Of CRÉDIT AGRICOLE SA’S ShARE CAPITAL IS hELD By ThE 39 REGIONAL BANKS, vIA ThE hOLDING COmPANy SAS RUE LA BOÉTIE.

Listed since December 2001, Crédit Agricole SA ensures the cohesion of the strategic development and financial unity of the Group. Crédit Agricole SA manages and consolidates its subsidiaries in France and abroad.

43.7 % Of CRÉDIT AGRICOLE SA’S ShARE CAPITAL IS hELD By ThE PUBLIC

0.4 % TREASURy ShARES

Organisation of the Group

Other specialised subsidiariesCrédit Agricole Immobilier – Crédit Agricole Private Equity – Idia-Sodica – Uni-Editions.

6.1 million cooperative shareholders form the basis of Crédit Agricole’s cooperative organisational structure.

They hold the capital of the 2 533 Local Banks in the form of shares and select their representatives each year : a total of 32 496 administrators who convey their expectations within the Group.

The Local Banks own the majority of the Regional Banks’ share capital. The Regional Banks are cooperative regional banks that offer their clients a comprehensive range of products and services.

The policy assessment body for the Regional Banks is the Fédération Nationale du Crédit Agricole, where the Group’s main directions are decided.

55.9 %

0.4 %

4.6 %

8.2 %

30.9 %

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 5

6

message from the Chairman and the General managementFor developed countries, 2010 was the year marked both by the sovereign debt crisis and an upturn in corporate fortunes, while emerging countries such as China experienced strong growth built on solid economic fundamentals.

These stark global contrasts had very different effects on banks, depending on their geographic and industry exposures.

Against this uncertain and volatile backdrop, Crédit Agricole (Suisse) SA managed to grow its Private Banking and Corporate Banking businesses but saw its Capital Markets activities slow down.

Income for the year came to CHF 656 million, down 7 % on the previous year. Stripping out expenses, which rose 5 % to CHF 411 million, gross operating income was CHF 245 million, a decline of 22 %.

Basically, the Bank was adversely affected by the USD and EUR exchange rates against the CHF, since the bulk of its income is in USD and EUR while the majority of its expenses are in Swiss francs.

However, we considered this to be a temporary setback and continued to invest. In particular, we resumed hiring in order to better serve our clients.

Private Banking performed excellently, attracting CHF 3 billion across its areas of natural growth, including Asia, Africa and the Middle East. It broadened the range of products and services to satisfy clients.

Corporate Banking expanded significantly against a backdrop of rallying commodity prices. Risks were kept firmly under control.

Capital Markets saw a decline in income and earnings from 2009’s record highs. Nonetheless, its results were above forecast and better than those of the pre-crisis years 2006 and 2007.

The Banking Logistics Centre, CA-PBS, not only continued to provide high quality services; it also prepared the migration of Crédit Foncier de Monaco to our IT Platform S2i, a transfer which went ahead smoothly in January 2011. It also completed a number of developments that will enable Crédit Agricole (Suisse) SA to operate a new booking centre in Hong Kong as soon as regulatory approval is given.

The Coverage unit had another excellent year, giving Swiss firms and financial institutions access to the full range of skills available across the Crédit Agricole Group.

The year 2011 is off to a good start for all our businesses, although we shall remain cautious in the coming months in view of the general environment, notably the geopolitical situation.

With the full backing of the Crédit Agricole Group, the Bank intends to speed up development in all its businesses and historic areas of natural growth, building enduring and trust-based relations with clients by delivering a high-performance range of products and services.

Christophe GANCEL

Chief Executive

Officer

Jean BOUYSSET

Chairman of the

Board of Directors

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 7

Board of Directors Chairman

Jean BOUYSSET

Deputy Chairmen

Maurice MONBARON Advisor to the Chief Executive Officer

Edmond TAvERNIER * Attorney-at-Law, Geneva, Tavernier Tschanz

Administrators

Jean-François ABADIE Head of France and International Private Banking, Crédit Agricole Group From 16 December 2010, Director delegated, Crédit Agricole Luxembourg

Gilles DE MARGERIE, until 7 December 2010 Head of Private Banking, Private Equity and Real Estate Member of the Crédit Agricole SA Executive Committee

Emmanuel DUCREST * Attorney-at-Law, Geneva, Ducrest, Nerfin, Berta, Spira, Bory villa

Ariberto FASSATI Senior Country Officer for Italy, Crédit Agricole Member of the Crédit Agricole SA Executive Committee

Camille FROIDEvAUx * Attorney-at-Law, Geneva, Budin & Associés

Martin LENz * Attorney-at-Law, Basel, Lenz Caemmerer Bender

Jean-François MARCHAL Head of Structured Finance, Crédit Agricole CIB

Alain MASSIERA Deputy General Manager, Crédit Agricole CIB From 1 December 2010, Head of the Crédit Agricole SA Group Private Banking Business Line, Member of the Crédit Agricole SA Executive Committee

Christoph R. RAMSTEIN * Attorney-at-Law, zurich, Pestalozzi

Fabio SOLDATI * Attorney-at-Law, Lugano, Felder, Riva, Soldati, Marcellini, Generali

Senior managementChristophe GANCEL Chief Executive Officer

Jacques BOURACHOT General Manager, Head of Logistics

Pierre GLAUSER General Manager, Head of Commercial Banking Switzerland, Global Head of Transactional Commodity Finance Business Line

Philip ADLER Head of Capital Markets

Youssef DIB Head of Clientele, Private Banking

Laurent FRIEDLI Head of Coverage

viviane GABARD Head of Risks Management and Permanent Control

Frédéric LAMOTTE Head of Markets and Investment Solutions

Georges zECCHIN Chief Executive of Crédit Agricole Suisse in Asia

Natacha A. POLLI, from 1 February 2010 Head of General Secretariat, Compliance and Legal Affairs, Documentation, Planning and International Organisation

* Independent Members of the Board of Directors as defined in the FINMA circular 2008 / 24

AuditInternal Audit

Darius PUIU

Permanent Control

Stéphane REICHENBACH

Auditors

PricewaterhouseCoopers SA

management bodies

8 ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA

9

Economic climate and markets : How long will money remain cheap ?

Announced in late summer 2010, the details of a second round of quantitative easing, or QE2, in the United States confirmed that the Federal Reserve was concerned about the strength of domestic economic activity and the risk of deflation. And yet we believed that, although a slowdown was possible, the US economy was not headed for a double-dip recession. As it turned out, 2010 – the first post-recession year – was fairly disappointing. Growth in fact failed to rise above 2.8 % between fourth-quarter 2009 and fourth-quarter 2010.

The pace of price growth was sluggish but positive. The Fed found it too slow with regard to its mandate, which consists in keeping the level of employment as high as possible while maintaining price stability. And although job creation picked up again, it was nowhere near strong enough to offset the jobs lost in 2008-09.

In the eurozone, growth also trended downwards despite an extremely dynamic start to the year. The 4 % expansion seen in the second quarter slowed to a quarterly pace of some 0.3 %. Taking 2011 as a whole, the slowdown is likely to continue.

Growth and inflation rates continued to differ sharply from one country to another in 2010. Although, the developed economies experienced only a mild post-recession recovery, emerging economies continued to benefit from a favourable growth differential, accompanied by inflationary pressures in some countries.

Thus China and India registered strong year-on-year growth of some 8-10 %, while Russia’s GDP expanded nearly 6 % between fourth-quarter 2009 and fourth-quarter 2010 on the back of the economic recovery.

Brazil sought to engineer a soft landing. As a result, its growth trajectory crossed Russia’s on the way down : while the latter accelerate,

Brazil’s economy slowed down and the two BRICS ended the year at almost the same pace of growth.

In terms of inflation, rising energy and metals prices combined with bad weather in various parts of the globe to produce different price patterns from country to country. But in every case, inflation was significant owing to the high weights of food and energy in the emerging-market consumer basket. Specifically, measured from December to December, consumer prices rose from 1.9 % to 4.6 % in China and from 4.3 % to 5.9 % in Brazil, declined from 15 % to 9.5 % in India, and remained unchanged at 8.8 % in Russia.

Turning monetary policies around

Central banks did not finish the job in 2010. With the exception of the Bank of Japan and, possibly, the Fed, they must now implement strategies for discarding their extremely expansionary monetary policies. Fears of resurgent inflation are mounting as a result of economic expansion and improving fundamentals.

Emerging countries tightened monetary policy. In the eurozone, the policy pursued by the European Central Bank (ECB) began to return to normal at year’s end. In consequence, 3-month Euribor exceeded 1 %, the same level as the Central Bank’s Repo rate.

By contrast, the issue of policy normalisation was not on the agenda in the United States. The Fed’s main policy rate remained unchanged at its December 2008 level of 0.25 %, and is unlikely to rise for several months owing to the new QE2 liquidity injection.

After ticking up from 3.8 % to 4 % between the end of 2009 and the beginning of second quarter 2010, the yield on 10-year US Treasuries fell sharply, hitting 2.4 % in early October as speculation about the size of the QE2 programme ran rife. It then started to rise again, ending the year at 3.3 %.

In the eurozone, the yield on the 10-year German benchmark bond benefited both from contagion from the announcement of QE2 and from a flight to quality triggered by the fiscal problems of countries on the zone’s periphery. As a result, it softened from 3.4 % at the beginning of the year to 2.1 % in August, then moved in fits and starts towards 3 % but fell just short of that level at the end of the year. Swiss 10-year yields followed the same pattern, slipping from 1.9 % at the beginning of the year to 1 % in August before rebounding to 1.7 %.

The US dollar

Economic agents in Europe focused on the euro / dollar exchange rate. Although that attention was certainly warranted in terms of market liquidity and natural geographical positioning, it has tended to hide the crux of the problem, namely that the dollar is on a path of competitive devaluation. As a result, most Asian currencies have strengthened against the greenback since early 2010. The same is true, by and large, for the BRIC currencies : the Brazilian real gained 5 %, the Chinese yuan 3.3 % and the Indian rupee 4.1 %. Only the Russian ruble bucked the trend, losing 1.6 %. Not only do most emerging countries have solid fundamentals, but the more restrictive monetary policies sought by their authorities are paradoxically making their currencies more attractive because they show a serious determination to fight inflation.

The Swiss franc’s gains corresponded to periods of widespread rises in risk aversion or, vis-à-vis the euro, fears about government finances in some eurozone countries. For the year as a whole, the Swiss franc gained 10.7 % against the dollar and 18.6 % against the euro.

EUR / USD fluctuations may well reflect a battle between two currencies in poor health. From that standpoint, the dollar was in remission in 2010, going from 1.43 to 1.34 against the euro.

Economic and financial environment

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA10

Commodity price volatility

Investors have viewed commodities as a rampart against the weakness of the US dollar and renewed inflation. Between early 2010 and June, the Rogers International Commodity index lost nearly 14 % overall before rebounding. By year’s end it had put on more than 17 %.

China once again played a key role in the industrial metals market. Bouts of optimism or concern about the strength of Chinese demand impacted directly on prices. Copper, for example, fluctuated sharply from USD 7 342 / tonne at end 2009, USD 6 259 in early February, USD 7 960 in early April and 6 068 in early June to USD 9 650 at the end of the year, an all-time high.

Oil prices varied significantly in 2010. WTI crude started the year at USD 79 per barrel and subsequently fluctuated between a low of USD 66 and a high of more than USD 91 at year’s end. Gold set new records, starting the year at USD 1 100 per oz and subsequently exceeding USD 1 420.

Equity markets : contrasting performances

The MSCI World index in USD rose 13.9 % in the third quarter 2010, following a fall of 12.4 % in Q2 and a rise of 3.4 % in Q1. For the year as a whole it gained 9.1 %. On the whole, the gains were fairly evenly spread. Expressed in local currencies, however, some markets did not follow the trend: the Nikkei (-1.5 %) and Euro Stoxx 50 (-1.8 %) both remained in negative territory.

By contrast, some markets posted spectacular local-currency gains, including 19.1 % for Mumbai, 49.4 % for Jakarta, 22.2 % for Seoul, 24.7 % for Moscow, 19.4 % for Mexico City, and 54.1 % for Buenos Aires. These gains clearly reflect the significant exposure of index component companies to emerging economies, but they are also due to capital flows into these countries. In addition Germany’s DAx, which is strongly export oriented, put on 16.1 % in 2010 on the back of the robust performance in emerging markets.

11ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA

With 1 405 employees and CHF 48 billion in managed assets, Crédit Agricole (Suisse) SA is one of the Crédit Agricole Group’s largest international units and the chief centre of expertise for its international Private Banking network and Transactional Commodity Finance.

Through successive mergers with several banks long present in Switzerland, the Bank has developed numerous competitive advantages. These include deep roots in the Swiss banking industry, a mixture of cultural backgrounds, a strong international approach, acknowledged expertise in many business lines and a strategy focused firmly on client service.

Crédit Agricole (Suisse) SA is one of the leading foreign banks in Switzerland in terms of total assets, net profit, shareholders’ equity and number

of employees. This reflects its commitment to the Swiss financial market, where it has continued to develop for over 130 years.

Headquartered in Geneva, the Bank employs more than 1 200 staff in Switzerland alone. It has six offices in Basel, Lausanne, Lugano, zurich, Hong Kong and Singapore ; seven subsidiaries in Beirut, Doha, Nassau and Switzerland ; and five representative offices in Dubai, Abu Dhabi (since March 2010), Bahrain, Karachi and Tel Aviv.

Long established in regions with a variety of cul- tures and languages, Crédit Agricole (Suisse) SA has developed a keen sense of awareness and a human touch – essential qualities for understanding clients’ expectations and offering solutions and strategies best suited to their needs.

Drawing on the wide range of expertise available within the Crédit Agricole Group’s offices in over 70 countries, Crédit Agricole (Suisse) SA can offer an extensive range of solutions. With nearly 40 different nationalities, most of the Bank’s relationship managers are multilingual and come from a variety of cultural backgrounds, giving true meaning to the notion of personal relationships.

Constantly developing, especially internationally, the Bank will continue to expand particularly in Asia and the Middle East, with the aim of nearly doubling its headcount and assets under management in Hong Kong and Singapore by 2013. The Group is currently applying for a licence to open a booking centre in Hong Kong in 2011.

Crédit agricole (Suisse) Sa business update

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA12

focus on the Bank’s 2010 results Crédit Agricole (Suisse) SA has built its expertise around four major areas that form the foundations of its business : Private Banking, Capital Markets, Corporate Banking and Banking Logistics. This organisation ensures stable results by balancing the Bank’s revenue sources. In 2010 Corporate Banking achieved excellent results.

Despite tough conditions characterised by low interest rates and unfavourable currency impacts, consolidated gross profit, or gross operating income, reached CHF 245.3 million in 2010. Consolidated net profit for the Crédit Agricole (Suisse) SA Group remained stable at CHF 141.8 million in 2010 com- pared with CHF 142.9 million in 2009. Crédit Agricole (Suisse) SA Group shareholders’ equity, as defined in Article 17 OFR (Tier 1-3), was CHF 2 082.8 million this year after appropriation of earnings.

Crédit Agricole (Suisse) SA, on its own, recorded 2010 gross profit of CHF 261.4 million and net profit of CHF 165.2 million. It had CHF 2 014.1 million of shareholders’ equity after appropriation of earnings, as defined in Article 17 OFR (Tier 1-3). The Bank continued to enjoy strong financial backing from the Crédit Agricole Group and has a high-quality AA-rating from Standard & Poor’s.

The four main banking activities of Crédit Agricole (Suisse) SA

Private BankingPrivate Banking is Crédit Agricole (Suisse) SA’s principal activity, with around CHF 46 billion of client wealth under management in 2010. The Bank offers its clients a full array of bespoke services and an open-architectured range of investment products suited individual expectations :

– discretionary management mandates– investment advisory services– fund selection– estate and financial planning– foreign exchange transactions– precious metals– structured products, advised or under mandate– private equity– property loans– commercial transactions– e-Banking.

From an economic and financial standpoint, 2010 was yet another year of contrasts marked by a persistent disconnect between developed and emerging countries. Europe and the USA had to cope with sizeable budget deficits amid an anaemic economic recovery. Several European countries were hit by serious budgetary crises, leading to sanctions from financial markets and undermining the euro. Meanwhile emerging countries, led by Asia, had yet another year of strong growth based on sound public finances.

Regulatory developments affecting international Private Banking activities continued to weigh on the outlook of some markets, particularly in Europe.

Despite these mixed conditions, net new money reached a record high of CHF 3 billion. This was made possible by the quality and hard work of Crédit Agricole (Suisse) SA’s teams and the wide variety of regions in which the Bank is present, notably emerging markets. These encouraging results bear out the strategy that Crédit Agricole (Suisse) SA has actively pursued since 2008, aimed at strengthening its sales forces in these regions.

Despite these excellent commercial results, client assets under management fell CHF 535 million over the past year due to a weakening of major currencies, particularly the euro and US dollar, against the Swiss franc.

Overall, the Bank continued to take a cautious approach to managing its clients’ investments. The majority of portfolios were invested in cash and bonds, but the share of these asset classes contracted slightly in favour of exposure to equity markets.

Private Banking products and services

In 2010 the Marketing and Investment Division (DMI) became Markets & Investment Solutions (MIS). The idea of the name change was to showcase more clearly the division’s goals : to interface between clients and the various markets in which we have recognised expertise ; focus on long-term investment while continuing to offer trading services to our most experienced clients ; and, last but not least, highlight the bespoke nature of the solutions we devise and implement for our clients rather than a purely product- based approach. This is particularly important given the significant growth in our high net worth clientele.

“ the baNk CONtiNued tO take

a CautiOuS aPPrOaCh tO

maNaGiNG itS ClieNtS’

iNveStmeNtS ”.

Youssef Dib, Head of Clientele, Private Banking

“ fOr Private equity, 2010 waS

aN OutStaNdiNG year, with

a twO-fOld iNCreaSe iN vOlume

COmPared tO 2009 aNd the

lauNCh Of a Private debt Offer ”.

Frédéric Lamotte, Head of Markets and Investment Solutions

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 13

Buoyed by renewed volatility in currency markets, the Private Client Forex department experienced a record-breaking level of activity in 2010 in every region and client segment, while diversifying its active client roster. It is worth noting that, thanks to the high quality of the advice provided directly to clients handled by the desk, the vast majority of them were able to escape the effects of the US dollar’s steep fall against the euro and subsequent equally abrupt reversal. In parallel, the CHF continued to appreciate strongly throughout the year.

For the Private Equity business, too, 2010 was a banner year, with a two-fold increase in volumes compared with 2009. Over the period, the department successfully developed and promoted a Private Debt offering (via funds of LBO loans bought from banks at a large discount) and a Private Equity Real Estate offering (closed-end funds investing over the medium term in rental and / or commercial property assets). The department also continued to improve the quality of reporting on all these “ revenue stream assets ”.

After reaching a low in 2009, Structured Products experienced fresh demand in 2010, particularly for fixed income products in the first half-year and equity market products in the second. With the creation in early 2010 of an Investment Committee representing all MIS’ management skills, the volume of assets under “ Structured-Product Discretionary Management ” increased significantly.

Discretionary Portfolio Management, following an exceptional 2009, delivered results generally in line with its targets despite punitive currency impacts, which were partly offset by a very accurate analysis of the markets for risky assets (equities with an emerging market bias and commodities with a metals bias, both of which made strong contributions). International assets management in Swiss francs was hurt by the relative strength of the franc against all other currencies. By contrast, Absolute Return mandates performed in line with their target of LIBOR +1-2 % with a volatility of 2-3 %, and did so for the sixth year running.

The Investment Fund activity continued to expand with proprietary Crédit Agricole (Suisse) SA investment funds (Bel Air and PB Invest, a Luxembourg specialised investment fund offering investors total transparency). Two new subfunds

14 ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA

were created : “ World equities – Shariah compliant management ” and “ Brazil selected equities ”. One of the highlights of 2010 was the transfer of all pooled fund management business from the Bahamas to Bel Air / PB Invest funds. value dates were not affected and the transfer had no market impact for clients, who can now benefit from a more secure service on an investment that nonetheless retains its special feature, the preponderance of Canadian markets. Lastly, the Investment Fund department helped the Group make progress on formalising its socially responsible investment offering.

The Advisory department continued to garner business from the major accounts delegated to it, as clients increasingly looked for more direct interaction with markets. The Direct Access offering took shape in 2010 and met with strong demand from clients, prompting the creation of dedicated resources.

Low interest rates and the appeal of real assets continued to attract investors to Real Estate activity, generating success for this department. It set up an innovative model for monitoring the value of exceptional properties in order to improve the quality of risk management and thereby sustain this business.

Crédit Agricole Suisse Conseil SA, a subsidiary of Crédit Agricole (Suisse) SA, created a line of life insurance products in 2010 for the Bank’s clients with the aim of promoting our internationally diversified management services via dedicated funds. In addition, to meet the needs of the Bank’s biggest clients, an asset consolidation service in a “ family-office ” configuration was also initiated and put into operation. Throughout the year, the engineering teams made substantial contribu- tions. In particular, the subsidiary structured several aircraft financing deals and crafted ownership strategies for private individuals.

Product departments in Asia consolidated their growth around the two existing centres in Hong Kong and Singapore, with greater emphasis on local management approaches. In 2010 MIS created a Senior Investment Advisor (SIA) position in Beirut to assist relationship managers and clients in the Middle East region. Furthermore, all MIS department heads in Geneva received cross-training on the Bank’s full range of products and services so that they can act as SIA for all the Bank’s relationship managers.

Capital marketsThe Capital Markets department offers a range of innovative products and solutions to Private Banking, institutional and corporate clients. Its activities encompass :

• advisoryandtradingservicesincurrenciesand precious metals

• cashmanagement

• commodity,fixedincome,equityandcurrencyderivatives and structured products.

The most troublesome issue in 2010 was government debt management. The USA continued supporting debt-led growth while Europe opted for austerity, triggering volatility in currency markets.

In this climate of uncertainty and low interest rates, all our businesses managed to turn in fine performances. Our commitments are strictly monitored and, in all cases, respect the risk policies of the Crédit Agricole SA Group.

Revenues beat forecasts but still fell short of last year’s record-setting level. We made substantial investments throughout 2010 to optimise risk management.

Corporate BankingThe Corporate Banking division of Crédit Agricole (Suisse) SA handles all the financing and credit activities dedicated to large multinational groups and international commodity trading firms.

Organised around two main units, it is responsible for developing activities involved in the financing of international commodity trading under a global franchise, as well as for standard corporate financing activities.

The role of Corporate Banking obviously includes offering all the other types of credit available from the Crédit Agricole Group, in particular for aircraft, shipping and project financing.

After treading cautiously in 2009, we chose to ramp up our sales and marketing efforts in 2010, principally in commodities. Commodity prices held firm throughout the year on the back of strong momentum in Asian and South American markets.

Our Bank experienced strong demand from clients in this area, to whom it provided active support by making available its full range of

“ Our COmmerCial aCtivitieS

were buOyed by the dyNamiC

marketS Of aSia aNd SOuth

ameriCa ”.

Pierre Glauser, General Manager, Head of Commercial Banking Switzerland, Global Head of Transactional Commodity Finance Business Line

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 15

expertise, from advisory services to loans and credits facilities, and a host of operational resources. This positioning produced a significant improvement in results.

Transactional Commodity Finance is one of the flagship activities of Crédit Agricole (Suisse) SA, built up for over 25 years by our international trade experts with the support of top-notch operational and IT teams.

The department’s portfolio now includes many of the world’s major commodity market participants and is principally specialised in the energy sector, which represents nearly 80 % of its business. The remainder is split between metals, minerals and soft commodities.

Because of Switzerland’s role as a global centre, the department has to coordinate and develop Crédit Agricole SA Group’s worldwide network, which today – with the March 2010 opening of the Shanghai unit – spans all the strategically important sites linked to this activity. With teams in Asia (Singapore, Hong Kong and Shanghai), Europe (Paris, Moscow and Kiev) and the Americas (New York and Sao Paulo), Crédit Agricole (Suisse) SA has the resources to operate globally on behalf of its entire clientele.

The second Corporate Banking activity, Commer- cial Banking, relies on a multi-business, multi-service offering to forge dedicated partnerships with large corporations, middle market companies and private banking clients – all with the full backing of a solid banking group. Taking advantage of the economic recovery and a high-quality portfolio, in 2010 the Commercial Banking arm again demonstrated its ability to help clients grow their business.

With its Trade team based in Geneva, Crédit Agricole (Suisse) SA can offer clients a full range of Export and Trade Finance products and services, such as issuance of international market guarantees and preparation of export financing packages covered by export risk guarantees. The team can also rely on the entire interna-tional network of Crédit Agricole Corporate & Investment Bank.

The Crédit Agricole Private Banking Services Logistics CentreThe Crédit Agricole Private Banking Services Logistics Centre is an invaluable resource for banking activities.

Equipped with first-class administrative resources, it continues to develop cutting-edge IT logistics to carry out its role of services centre in charge of IT, back-office and accounting functions for the international private banking subsidiaries of the Crédit Agricole Group.

Relying on these skills, backed by ISO 9001: 2008 and SAS70 Type II certifications successfully renewed year after year, Crédit Agricole (Suisse) SA has offered banks outside the Group – in Switzer- land and abroad – a complete outsourcing package for IT services, back-office and accounting functions for over a decade. Close to 25 banks, or more than 3 000 total users, have already entrusted these services to the Crédit Agricole Private Banking Services platform, which develops according to their needs and those of their clients. In all more than CHF 110 billion in client wealth is managed using the S2i integrated banking software.

The Logistics Centre is continually improving its services, focusing on three areas : constantly striving to improve the quality of operations, boosting productivity and managing operating risks. In 2010 these efforts led to the completion or launch of numerous projects :

• ongoing enhancement of S2i with newfunctionalities that are increasingly adapted to banking needs,

• renewal of SAS 70 certification, which ensuresrigorous internal control of IT and operating processes and thus reassures client banks – and their auditors – about outsourcing their activities to Crédit Agricole Private Banking Services,

• creation of an S2i banking environment inHong Kong, ready to take on its first clients once it obtains a banking licence, to accelerate the Bank’s growth in Asia,

“ maNaGiNG baCk-OffiCe taSkS

requireS the mOSt advaNCed

SOftware aNd muCh mOre

hiGhly Skilled Staff thaN iN

the PaSt. thiS iS eNCOuraGiNG a

GrOwiNG Number Of baNkS tO

OutSOurCe theSe aCtivitieS. ”

Jacques Bourachot, Managing Director of Crédit Agricole Private Banking Services

Chf110 billiON

iN ClieNtS aSSetS

ON the S2i SyStem

3000

uSerS Of the S2i SyStem

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA16

• creation of an S2i banking environment inBelgium, operational in March 2011, to support the development of CA vMC, the brokerage company recently set up by Crédit Agricole Luxembourg,

• completion of the CFM Monaco migrationproject consolidated by the transition to the platform in January 2011, in keeping with the schedule announced in late 2008 ; as a result, the platform will now handle more than 90 % of the client wealth of the Group’s International Private Banking business line from Switzerland,

• signatureofseveralnewoutsourcingcontractscalling for operational start-up in 2011 ; these new contracts testify to the quality of Crédit Agricole (Suisse) SA’s IT and back- office outsourcing services.

Cross-departmental functions of the Bank

CoverageThe Coverage department, which Crédit Agricole (Suisse) SA created in early 2007, is responsible for developing and monitoring relations with corporate clients and Swiss financial institutions across business lines in the Crédit Agricole Group’s Corporate and Investment Banking activities. Coverage initiates and coordinates operations among all the Group’s business lines, but particularly in Investment Banking, Equity Brokerage and Derivatives, Capital Markets, Structured Finance and Corporate Financing.

Two highlights of 2010 were the robust growth in overall revenues generated with corporate clients and continued significant activity with financial institutions. This significant expansion was due to a number of factors, including Investment Banking / Corporate Equity Derivatives transactions ; M&A advisory contracts ; book- runner mandates for syndicated loans ; fixed income, currency and commodity derivative transactions ; a deal to deliver electricity over the medium term ; and export financing transactions.

General SecretariatThe General Secretariat continued to strengthen the internal control system and develop tools for controlling risk, combating money laundering and terrorist financing, and managing related issues such as countries under sanctions or embargos.

The General Secretariat was also kept busy by new regulations on banking secrecy, notably with respect to new double taxation treaties and projects announced by the FINMA, as well as various other foreign government projects involving tax and regulatory issues (cross-border activities).

The General Secretariat coordinated the creation of a new Board Committee, the Compensation Committee, and helped draft a directive issued by the Board on the Bank’s compensation policy.

The Bank was also granted licences to open two representation offices, in Dubai and Abu Dhabi, in March 2010.

human ResourcesFor Human Resources, 2010 was an intense year. It focused on :

• developing the Bank’s number of staff mem- bers organically through recruitment efforts, principally in Private Banking and Logistics (CA-PBS), and managing employees’ careers and internal job mobility ;

• strengthening salary guidelines in accordancewith the provisions of local regulators (the FINMA and the HKMA) as well as internal bodies ;

• fine-tuningourtrainingopportunities,especiallyfor the “ Itinéraires Métiers programme ” (creating a curriculum for management assistants), deve- loping the in-house magazine, WE MAG, and pursuing the apprenticeship programme,

• renewing ISO 9001:2008 certification, whichwas validated for the next three years, thus ensuring that all of our HR directives comply with legal and organisational guidelines.

17ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA

evolution of the Crédit agricole (Suisse) Sa Group

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA18

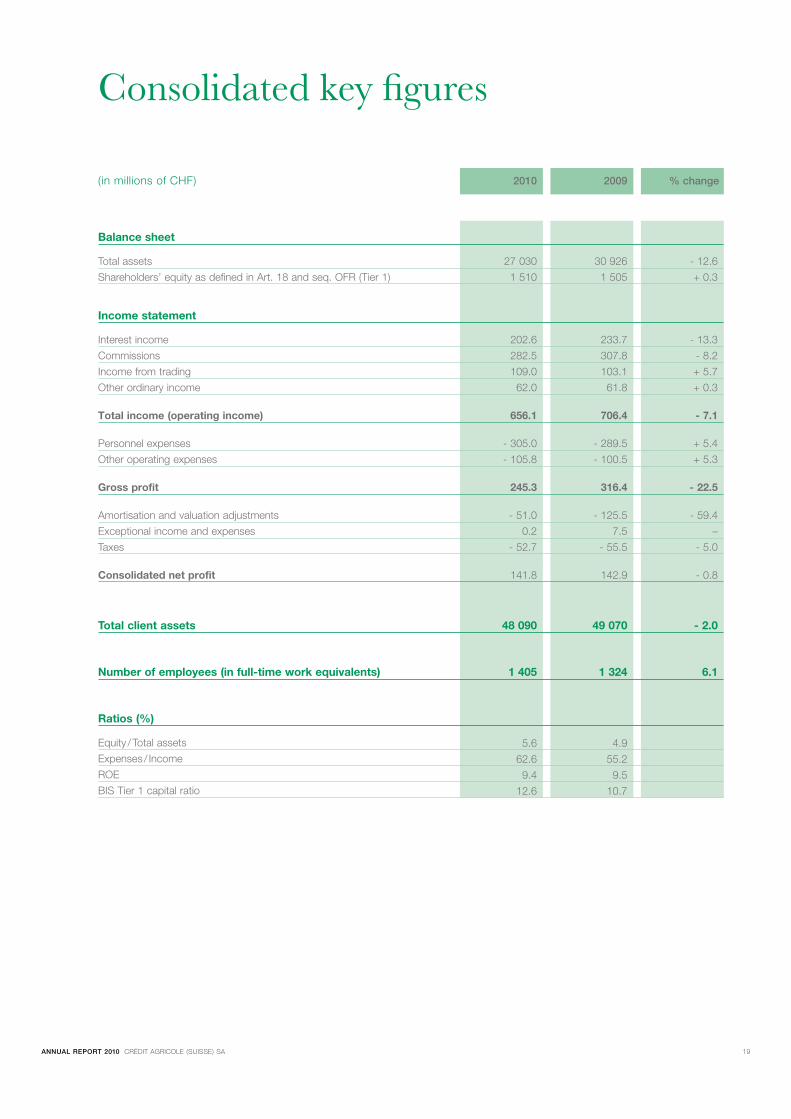

Consolidated key figures

Balance sheet

Total assets

Shareholders’ equity as defined in Art. 18 and seq. OFR (Tier 1)

Income statement

Interest income

Commissions

Income from trading

Other ordinary income

Total income (operating income)

Personnel expenses

Other operating expenses

Gross profit

Amortisation and valuation adjustments

Exceptional income and expenses

Taxes

Consolidated net profit

Total client assets

Number of employees (in full-time work equivalents)

Ratios (%)

Equity / Total assets

Expenses / Income

ROE

BIS Tier 1 capital ratio

(in millions of CHF) 2010 2009 % change

27 030 30 926 - 12.6

1 510 1 505 + 0.3

202.6 233.7 - 13.3

282.5 307.8 - 8.2

109.0 103.1 + 5.7

62.0 61.8 + 0.3

656.1 706.4 - 7.1

- 305.0 - 289.5 + 5.4

- 105.8 - 100.5 + 5.3

245.3 316.4 - 22.5

- 51.0 - 125.5 - 59.4

0.2 7.5 –

- 52.7 - 55.5 - 5.0

141.8 142.9 - 0.8

48 090 49 070 - 2.0

1 405 1 324 6.1

5.6 4.9

62.6 55.2

9.4 9.5

12.6 10.7

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 19

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA20

Consolidated financial statements

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 21

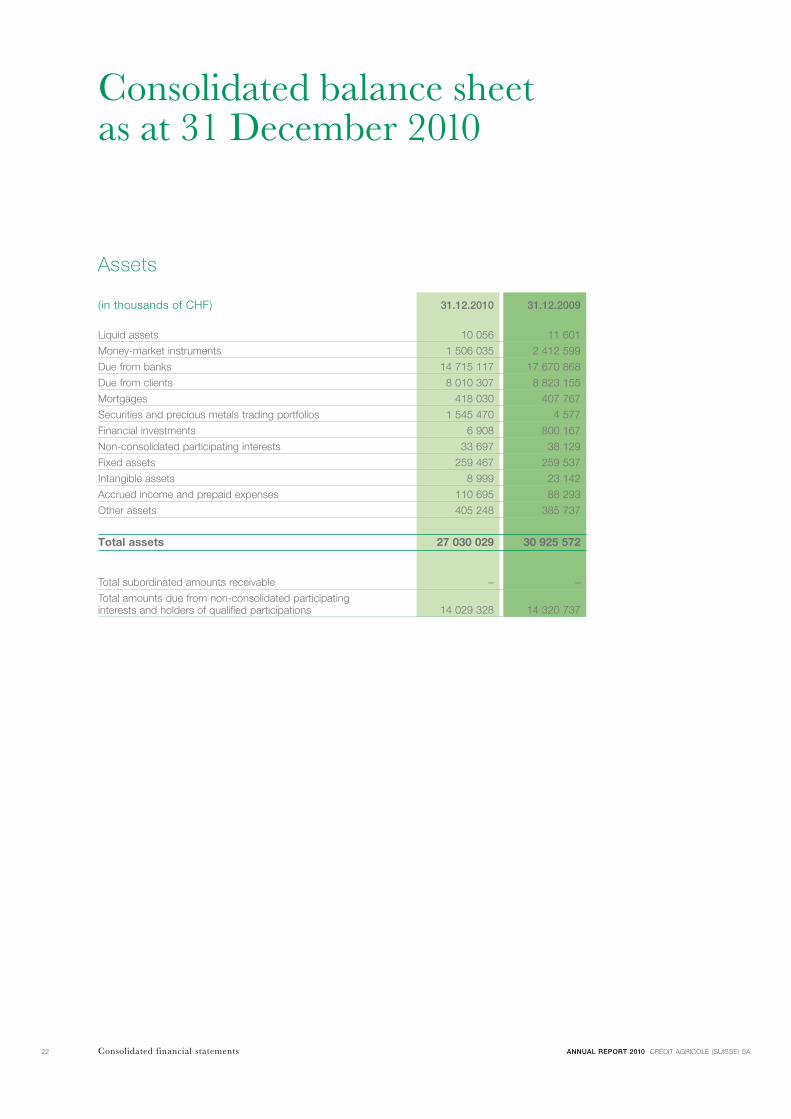

Consolidated balance sheet as at 31 december 2010

Assets

Liquid assets

Money-market instruments

Due from banks

Due from clients

Mortgages

Securities and precious metals trading portfolios

Financial investments

Non-consolidated participating interests

Fixed assets

Intangible assets

Accrued income and prepaid expenses

Other assets

Total assets

Total subordinated amounts receivable

Total amounts due from non-consolidated participating interests and holders of qualified participations

(in thousands of CHF) 31.12.2010 31.12.2009

10 056 11 601

1 506 035 2 412 599

14 715 117 17 670 868

8 010 307 8 823 155

418 030 407 767

1 545 470 4 577

6 908 800 167

33 697 38 129

259 467 259 537

8 999 23 142

110 695 88 293

405 248 385 737

27 030 029 30 925 572

– –

14 029 328 14 320 737

Consolidated financial statements ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA22

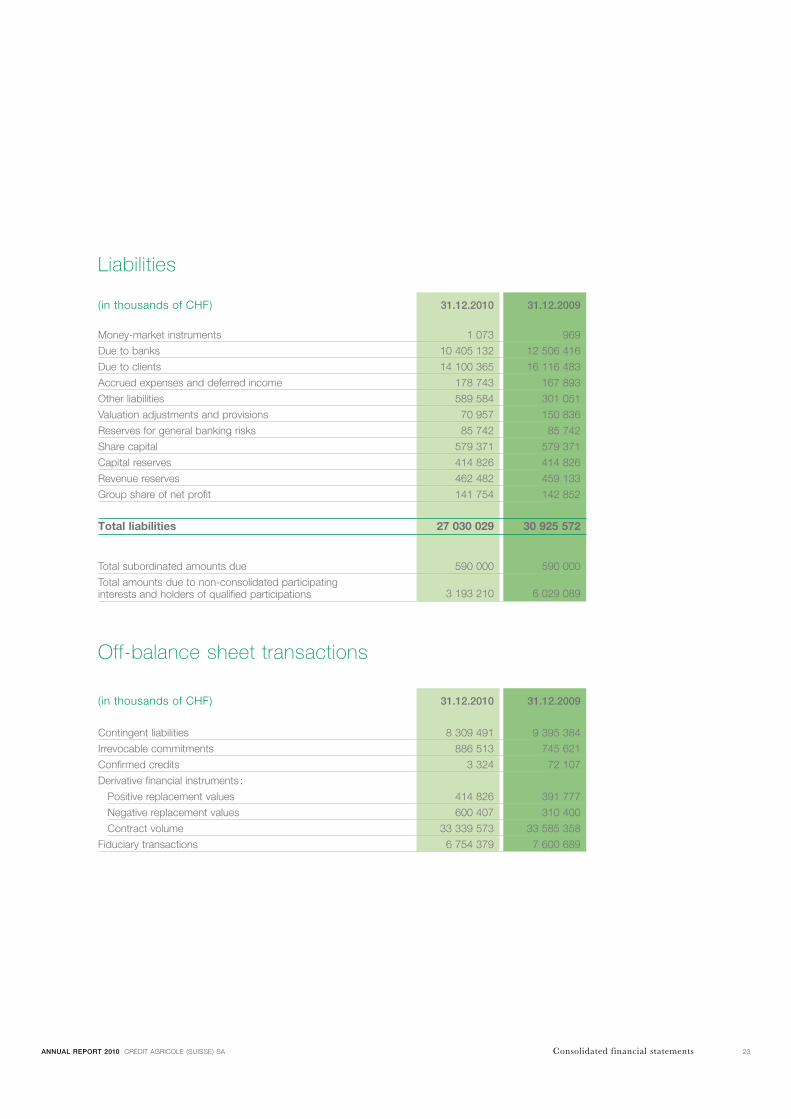

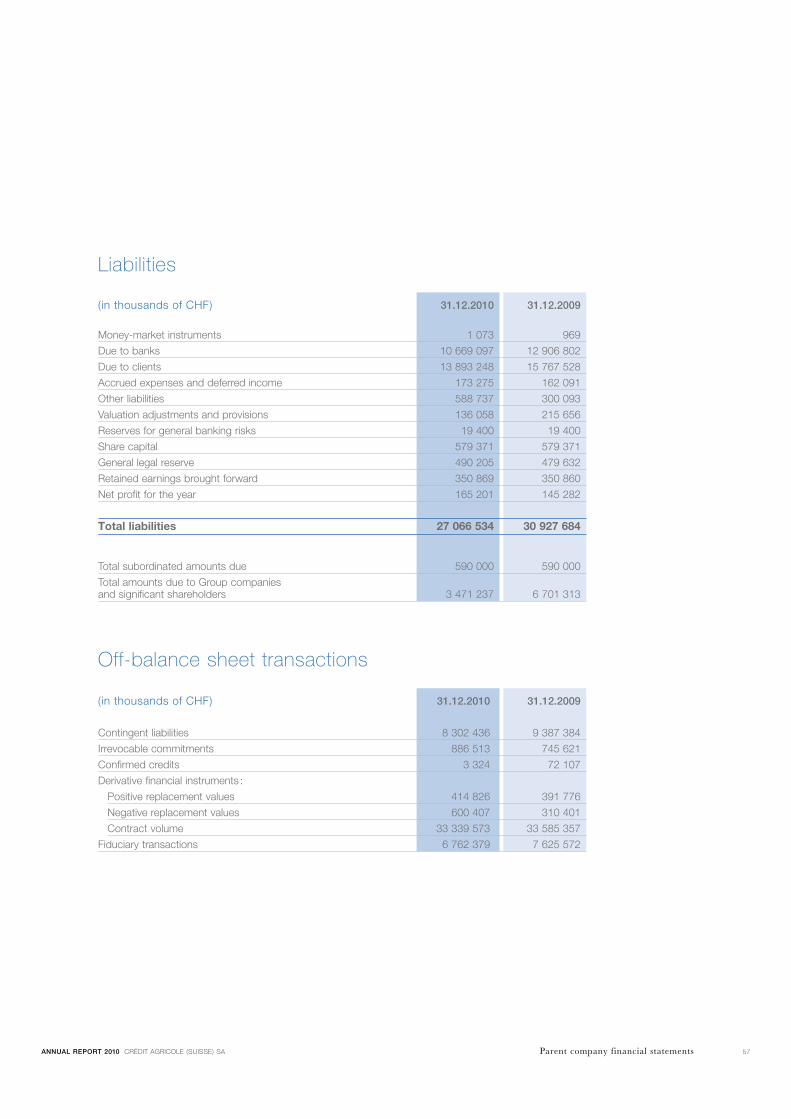

Liabilities

Off-balance sheet transactions

Money-market instruments

Due to banks

Due to clients

Accrued expenses and deferred income

Other liabilities

valuation adjustments and provisions

Reserves for general banking risks

Share capital

Capital reserves

Revenue reserves

Group share of net profit

Total liabilities

Total subordinated amounts due

Total amounts due to non-consolidated participating interests and holders of qualified participations

Contingent liabilities

Irrevocable commitments

Confirmed credits

Derivative financial instruments :

Positive replacement values

Negative replacement values

Contract volume

Fiduciary transactions

(in thousands of CHF) 31.12.2010 31.12.2009

(in thousands of CHF) 31.12.2010 31.12.2009

1 073 969

10 405 132 12 506 416

14 100 365 16 116 483

178 743 167 893

589 584 301 051

70 957 150 836

85 742 85 742

579 371 579 371

414 826 414 826

462 482 459 133

141 754 142 852

27 030 029 30 925 572

590 000 590 000

3 193 210 6 029 089

8 309 491 9 395 384

886 513 745 621

3 324 72 107

414 826 391 777

600 407 310 400

33 339 573 33 585 358

6 754 379 7 600 689

Consolidated financial statementsANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 23

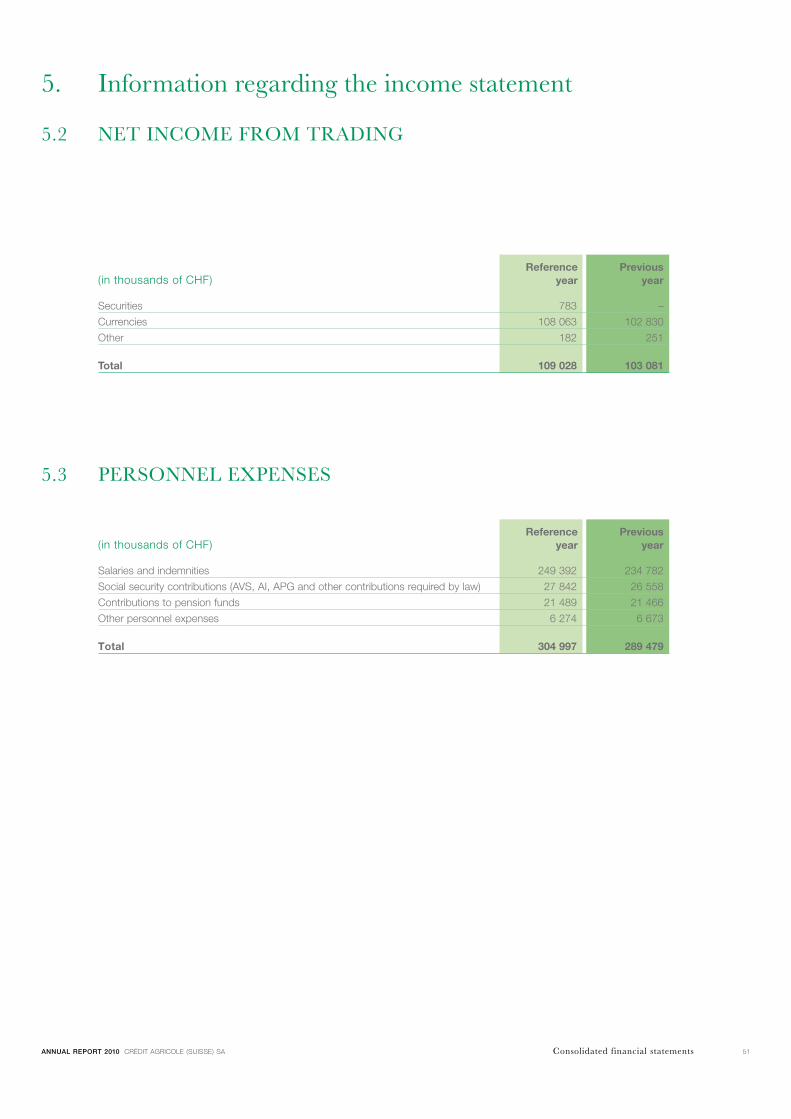

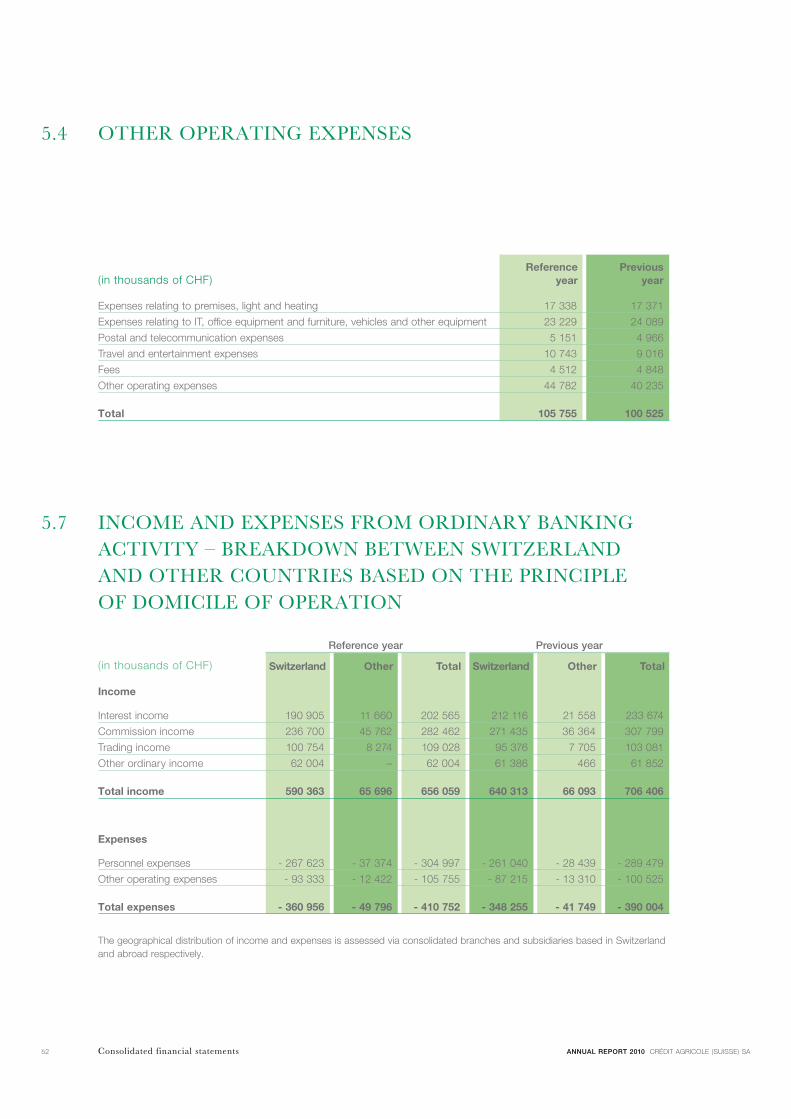

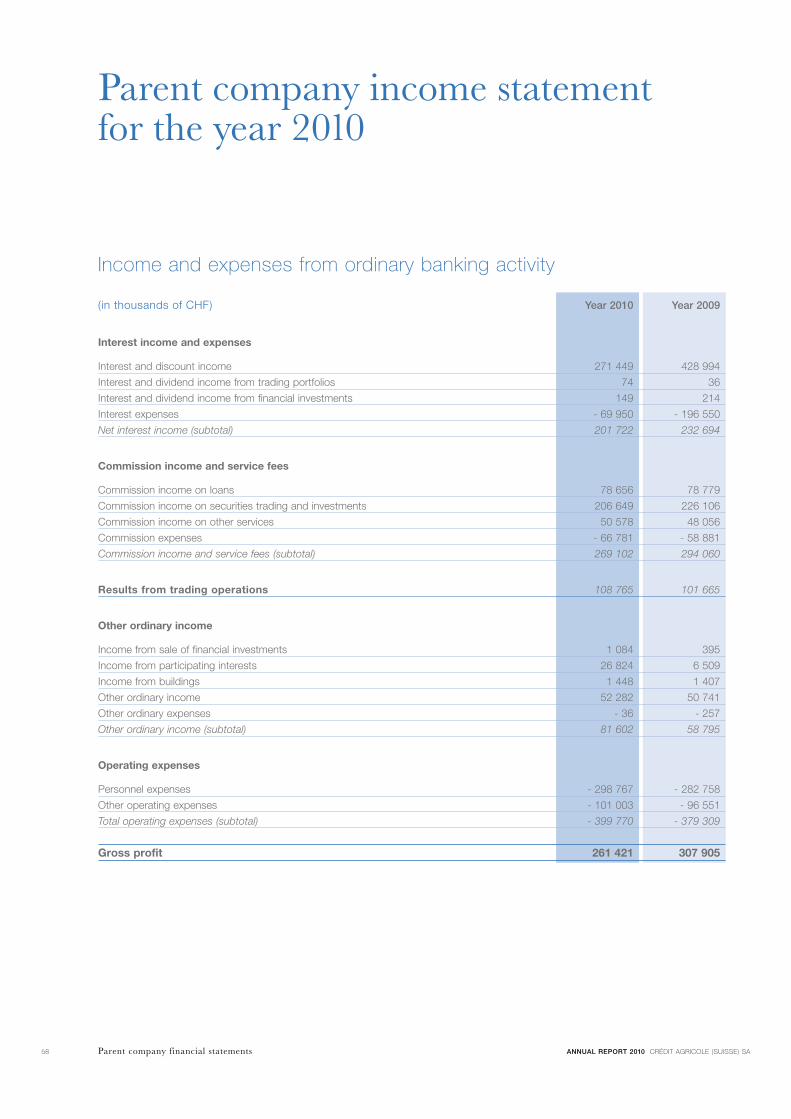

Income and expenses from ordinary banking operations

Consolidated income statement for the year 2010

Interest income and expenses

Interest and discount income

Interest and dividend income from trading portfolios

Interest and dividend income from financial investments

Interest expenses

Net interest income (subtotal)

Commission income and service fees

Commission income on loans

Commission income from securities trading and investments

Commission income from other services

Commission expenses

Net income from commissions and service fees (subtotal)

Trading income

Other ordinary income

Income from sale of financial investments

Total income from participating interests

– including participating interests accounted for using the equity method

– including other non-consolidated participating interests

Income from buildings

Other ordinary income

Other ordinary expenses

Other ordinary income (subtotal)

Operating expenses

Personnel expenses

Other operating expenses

Operating expenses (subtotal)

Gross profit

(in thousands of CHF) Year 2010 Year 2009

271 562 429 113

74 36

137 236

- 69 208 - 195 711

202 565 233 674

78 713 78 829

213 092 231 350

55 167 52 773

- 64 510 - 55 153

282 462 307 799

109 028 103 081

1 084 395

738 1 542

– 503

738 1 039

1 448 1 407

58 949 58 765

- 215 - 257

62 004 61 852

- 304 997 - 289 479

- 105 755 - 100 525

- 410 752 - 390 004

245 307 316 402

Consolidated financial statements ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA24

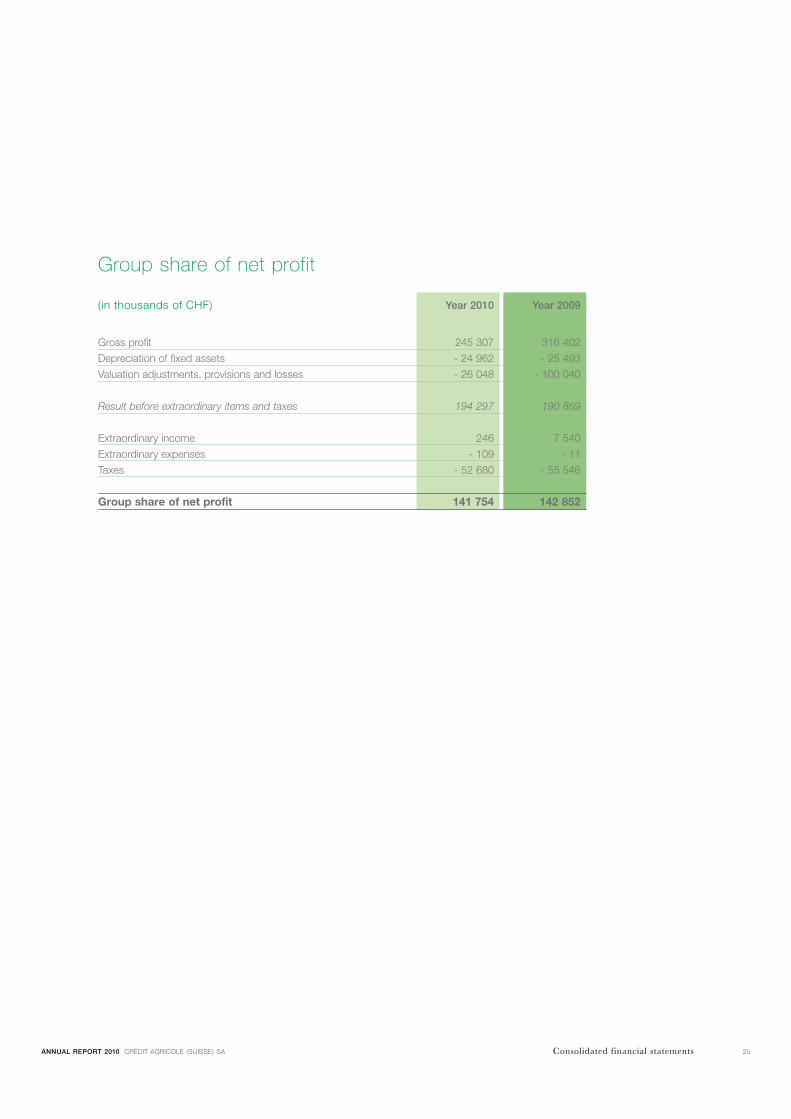

Group share of net profit

Gross profit

Depreciation of fixed assets

valuation adjustments, provisions and losses

Result before extraordinary items and taxes

Extraordinary income

Extraordinary expenses

Taxes

Group share of net profit

(in thousands of CHF) Year 2010 Year 2009

245 307 316 402

- 24 962 - 25 493

- 26 048 - 100 040

194 297 190 869

246 7 540

- 109 - 11

- 52 680 - 55 546

141 754 142 852

Consolidated financial statementsANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 25

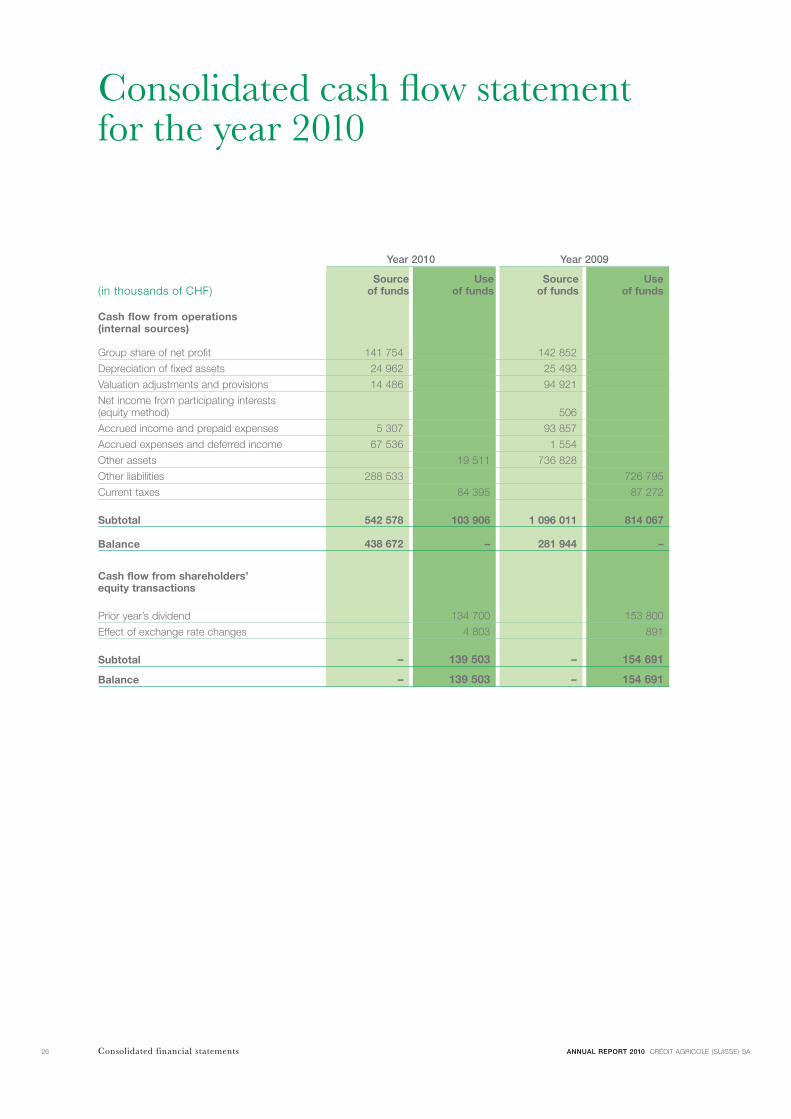

Consolidated cash flow statement for the year 2010

Cash flow from operations (internal sources)

Group share of net profit

Depreciation of fixed assets

valuation adjustments and provisions

Net income from participating interests (equity method)

Accrued income and prepaid expenses

Accrued expenses and deferred income

Other assets

Other liabilities

Current taxes

Subtotal

Balance

Cash flow from shareholders’ equity transactions

Prior year’s dividend

Effect of exchange rate changes

Subtotal

Balance

Source of funds

Use of funds

Source of funds

Use of funds(in thousands of CHF)

Year 2010 Year 2009

141 754 142 852

24 962 25 493

14 486 94 921

506

5 307 93 857

67 536 1 554

19 511 736 828

288 533 726 795

84 395 87 272

542 578 103 906 1 096 011 814 067

438 672 – 281 944 –

134 700 153 800

4 803 891

– 139 503 – 154 691

– 139 503 – 154 691

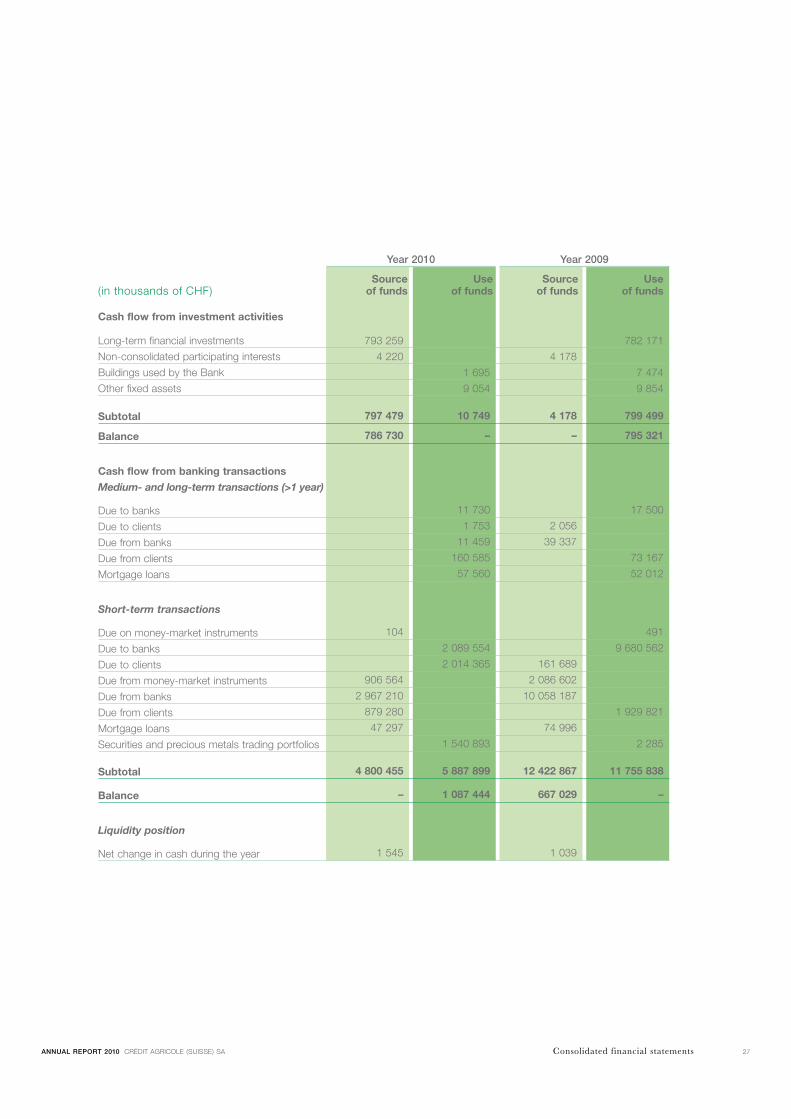

Consolidated financial statements ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA26

Source of funds

Use of funds

Source of funds

Use of funds

Cash flow from investment activities

Long-term financial investments

Non-consolidated participating interests

Buildings used by the Bank

Other fixed assets

Subtotal

Balance

Cash flow from banking transactions

Medium- and long-term transactions (>1 year)

Due to banks

Due to clients

Due from banks

Due from clients

Mortgage loans

Short-term transactions

Due on money-market instruments

Due to banks

Due to clients

Due from money-market instruments

Due from banks

Due from clients

Mortgage loans

Securities and precious metals trading portfolios

Subtotal

Balance

Liquidity position

Net change in cash during the year

(in thousands of CHF)

Year 2010 Year 2009

793 259 782 171

4 220 4 178

1 695 7 474

9 054 9 854

797 479 10 749 4 178 799 499

786 730 – – 795 321

11 730 17 500

1 753 2 056

11 459 39 337

160 585 73 167

57 560 52 012

104 491

2 089 554 9 680 562

2 014 365 161 689

906 564 2 086 602

2 967 210 10 058 187

879 280 1 929 821

47 297 74 996

1 540 893 2 285

4 800 455 5 887 899 12 422 867 11 755 838

– 1 087 444 667 029 –

1 545 1 039

Consolidated financial statementsANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 27

1. Comments on the Group’s operations and workforceCrédit Agricole (Suisse) SA is the parent company of Groupe Crédit Agricole (Suisse) SA (hereinafter “ the Group ”). It has branches in Basel, Lausanne, Lugano, zurich, Hong Kong and Singapore, subsidiaries in Switzerland, the Bahamas, Lebanon and Qatar, and representative offices in the United Arab Emirates, Bahrain, Israel and Pakistan.

The Group is active in Private Banking, Commercial Banking and Transactional Commodity Finance, as well as spot and forward trading in money market instruments, currencies and precious metals, both as an intermediary and on a proprietary basis. In addition, the Group’s Logistics Centre acts as a service centre in charge of IT, back-office and outsourcing accounting activities.

In 2010 the Group sold 4 % of the share capital of Crédit Agricole Financements (Suisse) SA, an equity affiliate. The company is now 16 % owned and is therefore no longer consolidated.

At 31 December 2010, the Group employed 1 405 people on a full-time equivalent basis, compared with 1 324 at 31 December 2009.

Risk managementGeneral risk policy

The Board of Directors establishes the risk policy on the basis of statutory requirements and head-office directives. Responsibility for implementing the policy lies with General Management.

The Group is active in several business areas, which expose it primarily to counterparty risk, market risk, operational risk, legal risk and reputation risk.

Risk assessment

The Board of Directors regularly examines the main operational risks to which the Group is exposed ; these are described below. The assessment takes account of measures which aim to limit the risks as well as internal controls planned for this purpose. The Board of Directors

ensures that measures are in place to carry out continuous control within the business lines and that the parameters influencing the risk profile are assessed and taken into account in the preparation of the financial statements.

Counterparty risk

Counterparty risk, or credit risk, represents the loss borne by the Group in the event of default by a counterparty.

Loans are granted according to a system of delegation of authority and are subject to a rating system.

A Credit Committee examines loan applications, granting authorisations on the basis of the aforementioned delegation and policy. This policy encompasses the commitments of the Group’s clients and correspondents that result from lending activities, issuance of guarantees, and trading in currencies, derivatives and securities. Risks are regularly monitored by the Credit and Risk division according to stringent procedures. General Management and the Board of Directors are kept informed on a regular basis.

Market risk

Market risk reflects the potential loss on the Group’s portfolio caused by fluctuations in exchange rates, interest rates and the prices of securities.

Managing market risk involves identifying, mea- suring and monitoring open positions. The trading portfolio is valued and compliance with assigned limits is monitored on a daily basis. These positions are followed on the basis of a value-at-risk model. Moreover, they are subject to sensitivity limits, which are also checked on a daily basis.

The main market risks faced by the Group are :

•Foreignexchangerisk

Foreign exchange risk relates to changes in the value of positions denominated in foreign currencies as a result of fluctuations in the exchange rates of the said currencies against the Swiss franc.

Positions in foreign currencies are adjusted as soon as the transaction is initiated. They are revalued several times a day at regular intervals. In

addition, limits are set for each currency in order to limit the risk.

With the exception of some strictly identified covering positions, all foreign exchange risk is included in the Group’s trading positions.

•Interestraterisk

Interest rate risk assesses the loss of value on the overall positions of the Group, both in the trading portfolio or resulting from the structure of the Group’s balance sheet.

The Group’s portfolio positions essentially cover the capital loans and acceptances business (net outstanding loans to clients and banks). The Group assesses this risk using asset-liability management (ALM) techniques in order to evaluate maturity structures and the impact of possible interest rate movements affecting on-balance sheet and off-balance sheet positions.

Within the framework of asset-liability management and on the basis of empirical statistical analyses, the Group then staggers certain positions with undetermined interest rate constraints.

•Liquidityrisk

The system put in place by the Group to manage liquidity risk ensures compliance with the relevant regulatory requirements at all times.

Securities received under repurchase and reverse repurchase agreements and those that the Group can dispose of freely are included in the liquidity ratio. The market value of the securities received or remitted is checked on a daily basis so that additional collateral may be put up or demanded.

Operational risk

Operational risk is defined as the risk resulting from inadequacies in the design, procurement or implementation of procedures for recording data relating to Group operations in information systems in general, and in accounting systems in particular.

This risk is limited through the use of highly automated processes and internal control measures. In addition, the Group has an Internal Control unit that ensures procedural compliance and analyses data flows. A database has been created to cater for the collection and analysis of any incidents which may occur.

Notes to the consolidated financial statements

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA28 Consolidated financial statements

Compliance and legal risk

Compliance and legal risk relates to the loss, whether financial or in terms of reputation, that could result from failing to comply with regulations or with due diligence duties specific to financial intermediaries.

The Group has a Compliance and Legal Affairs department whose role is to monitor compliance with regulations, notably in relation to the prevention of money laundering, the financing of terrorism and the prevention of fraudulent acts. This department also ensures that in-house directives are consistent with new legislation and regulations.

Regulatory ratio (Basel II)

In accordance with ref. No. 5 of the FINMA circular 2008 / 22, Crédit Agricole (Suisse) SA does not disclose information about its capital insofar as comparable information is published on an annual basis at the level of the Crédit Agricole Corporate & Investment Bank Group (see 2010 Annual Report, – Chapter : Pillar 3, available at www.ca-cib.fr) and on a half-yearly basis at the level of the Crédit Agricole SA Group (available at http://finance.credit-agricole.com).

Business policy when using derivative financial instruments

Transactions for the Group itself are carried out within the framework of internal directives applying to the management of market risk and interest rate risk.

Transactions carried out on behalf of clients include foreign exchange transactions (forward and options), stock options, stock exchange rates, interest rates, precious metals and futures.

The Group calculates an equivalent risk on these transactions to determine the amount of collateral required. This equivalent risk corresponds to the replacement value of the instruments plus an add-on or the usual margin calculated by the market. Margin calls are effected as soon as the value of the assets given as guarantee is no longer sufficient to hedge the risk run.

Outsourcing of activities

The Group does not outsource any of its activities as defined by the FINMA circular 2008 / 7.

2. accounting and valuation principles2.1 PriNCiPleS fOr PreParatiON Of the GrOuP’S fiNaNCial StatemeNtS

General principles

The Group’s accounting and valuation principles comply with the requirements of the Swiss Code of Obligations, the Swiss Federal Banking Act and the corresponding Implementing Ordi- nance, and also with the FINMA circular 2008 / 02 “ Accounting – Banks ”.

In accordance with the above, the consolidated financial statements of the Group are presented in accordance with the principle of presenting a true and fair view of the Group’s assets, liabilities, financial position and profit or loss.

Consolidation scope

The list of fully consolidated participating interests, participating interests accounted for using the equity method, non-consolidated participating interests and changes in the consolidation scope, is provided in note 3.3.

Year-end date of the consolidated financial statements

The consolidation period corresponds to the calendar year. The year end for all the compa-nies included within the consolidation scope is 31 December.

Consolidation method

Companies in the banking and financial sector in which the Group directly or indirectly holds the majority of the voting rights are consolidated according to the purchase method ; the acquisition

cost of the participating interest is offset by the amount of the shareholders’ equity at the time the Group took over control.

Participating interests of 20 % to 50 % in the banking and financial sectors are accounted for using the equity method. They are stated in the balance sheet at the proportional value of their net assets, including earnings.

However, participating interests that have no material impact on the objectives of the Group’s financial statements are not consolidated.

Depending on its nature, negative goodwill is attributed either to revenue reserves or to provisions. Positive goodwill is carried in the balance sheet and amortised over its economic life estimated to 5 years.

Conversion for consolidation purposes of individual company accounts expressed in a foreign currency

The balance sheets of companies domiciled outside Switzerland and drawn up in foreign currency are converted into Swiss francs at the year-end exchange rate. The income statements of these companies are converted at the average rate for the year. The currency gains and losses arising from this conversion are directly accounted for in Group shareholders’ equity.

2.2 aCCOuNtiNG PriNCiPleS

General principles

Assets, liabilities and off-balance sheet items reported under the same heading are always valued individually.

Recording of transactions and presentation in the balance sheet

Transactions are recorded in the books on their execution date and are valued thereafter according to the principles set out below. Until their settlement date, executed transactions are presented as off-balance sheet transactions, except for spot Forex and money-market transactions, which are directly accounted for in the balance sheet.

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 29Consolidated financial statements

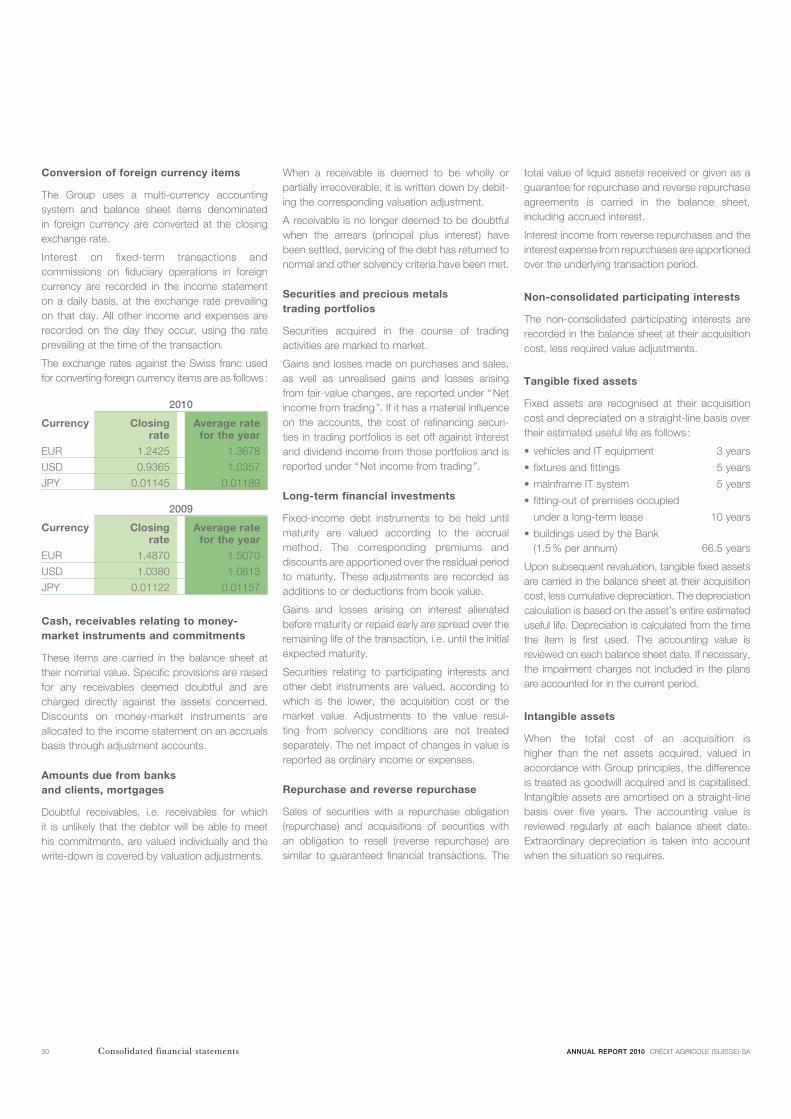

Conversion of foreign currency items

The Group uses a multi-currency accounting system and balance sheet items denominated in foreign currency are converted at the closing exchange rate.

Interest on fixed-term transactions and commissions on fiduciary operations in foreign currency are recorded in the income statement on a daily basis, at the exchange rate prevailing on that day. All other income and expenses are recorded on the day they occur, using the rate prevailing at the time of the transaction.

The exchange rates against the Swiss franc used for converting foreign currency items are as follows :

When a receivable is deemed to be wholly or partially irrecoverable, it is written down by debit- ing the corresponding valuation adjustment.

A receivable is no longer deemed to be doubtful when the arrears (principal plus interest) have been settled, servicing of the debt has returned to normal and other solvency criteria have been met.

Securities and precious metals trading portfolios

Securities acquired in the course of trading activities are marked to market.

Gains and losses made on purchases and sales, as well as unrealised gains and losses arising from fair-value changes, are reported under “ Net income from trading ”. If it has a material influence on the accounts, the cost of refinancing securi- ties in trading portfolios is set off against interest and dividend income from those portfolios and is reported under “ Net income from trading ”.

Long-term financial investments

Fixed-income debt instruments to be held until maturity are valued according to the accrual method. The corresponding premiums and discounts are apportioned over the residual period to maturity. These adjustments are recorded as additions to or deductions from book value.

Gains and losses arising on interest alienated before maturity or repaid early are spread over the remaining life of the transaction, i.e. until the initial expected maturity.

Securities relating to participating interests and other debt instruments are valued, according to which is the lower, the acquisition cost or the market value. Adjustments to the value resul- ting from solvency conditions are not treated separately. The net impact of changes in value is reported as ordinary income or expenses.

Repurchase and reverse repurchase

Sales of securities with a repurchase obligation (repurchase) and acquisitions of securities with an obligation to resell (reverse repurchase) are similar to guaranteed financial transactions. The

total value of liquid assets received or given as a guarantee for repurchase and reverse repurchase agreements is carried in the balance sheet, including accrued interest.

Interest income from reverse repurchases and the interest expense from repurchases are apportioned over the underlying transaction period.

Non-consolidated participating interests

The non-consolidated participating interests are recorded in the balance sheet at their acquisition cost, less required value adjustments.

Tangible fixed assets

Fixed assets are recognised at their acquisition cost and depreciated on a straight-line basis over their estimated useful life as follows :

•vehiclesandITequipment 3years

• fixturesandfittings 5years

•mainframeITsystem 5years

• fitting-outofpremisesoccupied

under a long-term lease 10 years

•buildingsusedbytheBank (1.5 % per annum) 66.5 years

Upon subsequent revaluation, tangible fixed assets are carried in the balance sheet at their acquisition cost, less cumulative depreciation. The depreciation calculation is based on the asset’s entire estimated useful life. Depreciation is calculated from the time the item is first used. The accounting value is reviewed on each balance sheet date. If necessary, the impairment charges not included in the plans are accounted for in the current period.

Intangible assets

When the total cost of an acquisition is higher than the net assets acquired, valued in accordance with Group principles, the difference is treated as goodwill acquired and is capitalised. Intangible assets are amortised on a straight-line basis over five years. The accounting value is reviewed regularly at each balance sheet date. Extraordinary depreciation is taken into account when the situation so requires.

Cash, receivables relating to money- market instruments and commitments

These items are carried in the balance sheet at their nominal value. Specific provisions are raised for any receivables deemed doubtful and are charged directly against the assets concerned. Discounts on money-market instruments are allocated to the income statement on an accruals basis through adjustment accounts.

Amounts due from banks and clients, mortgages

Doubtful receivables, i.e. receivables for which it is unlikely that the debtor will be able to meet his commitments, are valued individually and the write-down is covered by valuation adjustments.

Currency Closing Average rate rate for the year

EUR 1.2425 1.3678

USD 0.9365 1.0357

JPY 0.01145 0.01189

Currency Closing Average rate rate for the year

EUR 1.4870 1.5070

USD 1.0380 1.0813

JPY 0.01122 0.01157

2010

2009

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA30 Consolidated financial statements

Accrued income and expenses

Cut-off is applied to interest income and expenses, lending commissions considered as a component of interest, personnel and other operating expenses, safe-keeping fees, commissions on fiduciary transactions and asset management commissions.

Taxes

•Ordinarytaxes

Ordinary taxes on the income and the determining capital for the corresponding period are calculated in accordance with the relevant fiscal requirements. Direct taxes which are still due at the end of the financial year are recorded in the liabilities section of the balance sheet under the heading “ Accrued income and expenses ”.

•Deferredtaxes

The tax impact of temporary differences between the balance sheet value and the tax value of assets and liabilities is recorded in the “ valuation adjustments and provisions ” section of the balance sheet if the amounts are taxable and under “ Other assets ” if they are tax-deductible.

Claims resulting from deferred tax assets on temporary differences or on tax losses carried forward are only recorded if they are likely to be realised in the future through the existence of sufficient taxable profits.

Deferred taxes are determined annually on the basis of genuinely expected tax rates or, if they are not already known, on those in force at the time when the balance sheet is drawn up.

Deferred tax income and expenses are recorded in the income statement.

Valuation adjustments and provisions

The Group’s credit activity is limited mainly to Lombard loans and Transactional Commodity Finance. The particularity of these transactions is that repayment capacity is linked to the collateral put up during the transactions (self-liquidating transactions) as well as to the solvency of the debtor concerned.

When there is doubt as to a debtor’s ability to honour his commitments, the Group raises adequate provisions for the principal and interest, taking into account existing guarantees and collateral, as well as the economic environment. These valuation adjustments, which are made on an individual basis for each position, are charged directly against the balance sheet assets concerned. Interest deemed doubtful under this rule is provisioned from the date on which serious doubts first arise.

In accordance with the prudence principle, other identifiable risks are covered by provisions recognised in the balance sheet under “ valuation adjustments and provisions ”.

Reserves for general banking risks

Free provisions, included in valuation adjustments and provisions in the individual accounts, are transferred to the reserves for general banking risks after deduction of a tax provision.

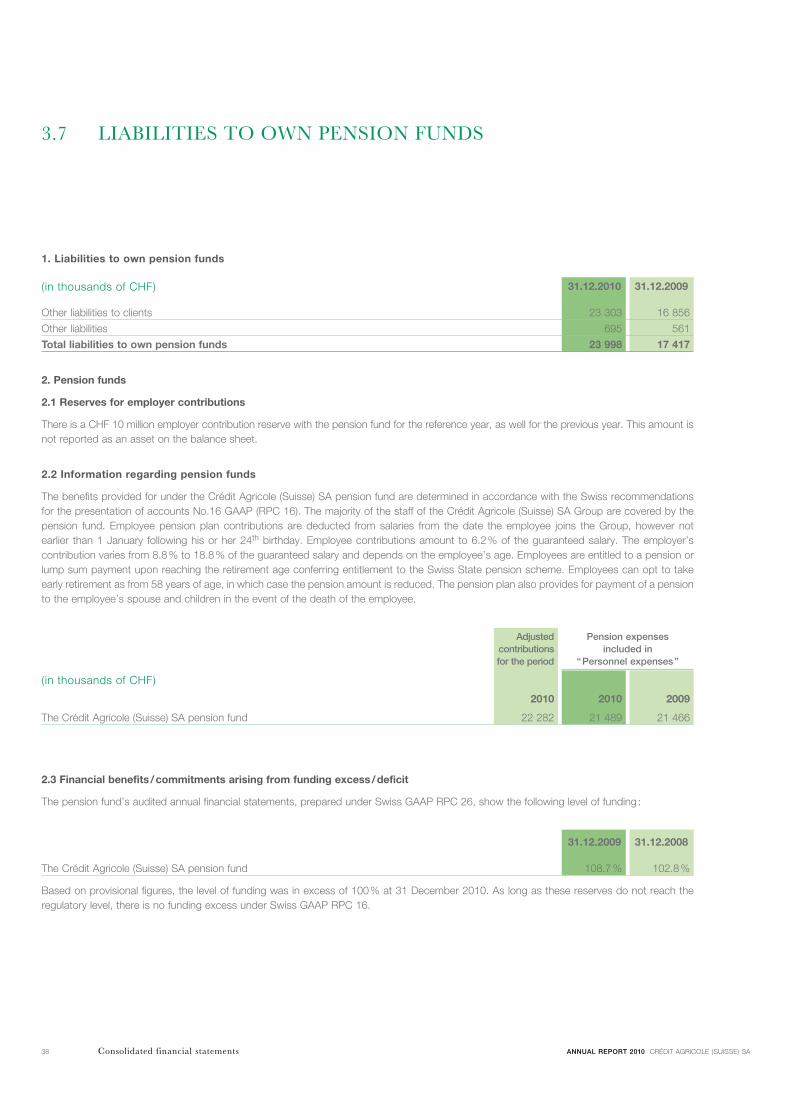

Pension commitments

The benefits provided for under the Crédit Agricole (Suisse) SA pension fund are determined in accordance with the Swiss recommendations for the presentation of accounts No. 16 GAAP (RPC 16). The majority of the staff of the Crédit Agricole (Suisse) SA Group are covered by the pension fund. Employee pension contributions are deducted from salaries from the date that the employee joins the Group or from 1 January following his or her 24th birthday, whichever is the later. Employee contributions amount to 6.2 % of the guaranteed salary. The employer’s contribution varies from 8.8 % to 18.8 % of the guaranteed salary and depends on the employee’s age. Employees are entitled to a pension or lump sum payment upon reaching the retirement age conferring entitlement to the Swiss State pension scheme. Employees can opt to take early retirement as from 58 years of age, in which case the pension amount is reduced. The pension plan also provides for payment of a pension to the employee’s spouse and children in the event of the death of the employee.

The pension commitments and the assets covering these commitments are held by a legally independent foundation. Contributions which have been adjusted to the period are presented as personnel expenses in the income statement. Furthermore, the foundation manages its assets through the Group, hence the related positions are recorded in the latter’s balance sheet.

Contingent commitments, irrevocable commitments, commitments to discharge and make supplementary payments, and confirmed credits

Off-balance sheet items are stated at their nominal value. A provision is made for identifiable risks and recorded under liabilities in the balance sheet.

Derivative financial instruments

The Group uses derivative financial instruments to manage its balance sheet structure, and also for trading purposes on behalf of its clients.

The positive or negative replacement values of all derivative instruments outstanding at the balance-sheet date are recorded gross in the balance sheet under “ Other assets ” and “ Other liabilities ” respectively.

Trading transactions are marked to market, whereas balance sheet management transac- tions are valued in the same way as the hedged positions.

valuation adjustments that are not recognised in the income statement at the closing date are recorded in a netting account, which is included in “ Other assets ” or “ Other liabilities ” depending on the balance on the account.

Layout of the notes to the consolidated financial statements

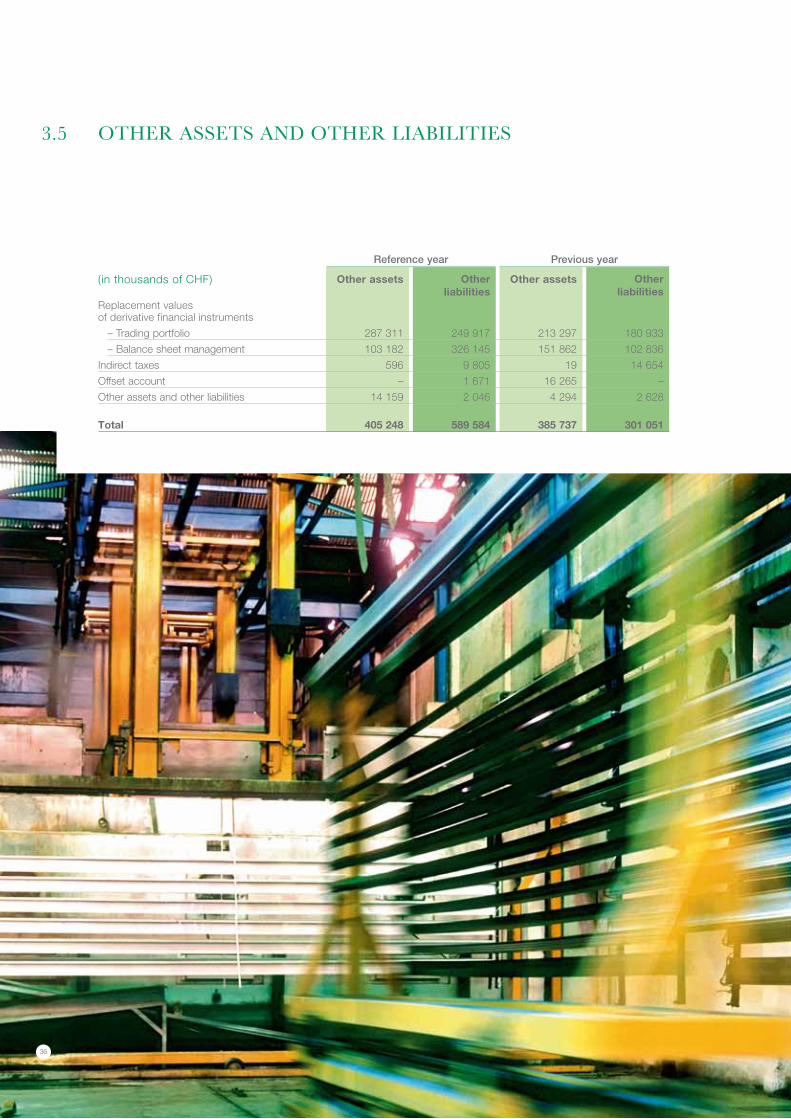

The numbering of the notes follows the layout stipulated by the FINMA in its directives governing the preparation of financial statements, except for note 3.5.

ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 31Consolidated financial statements

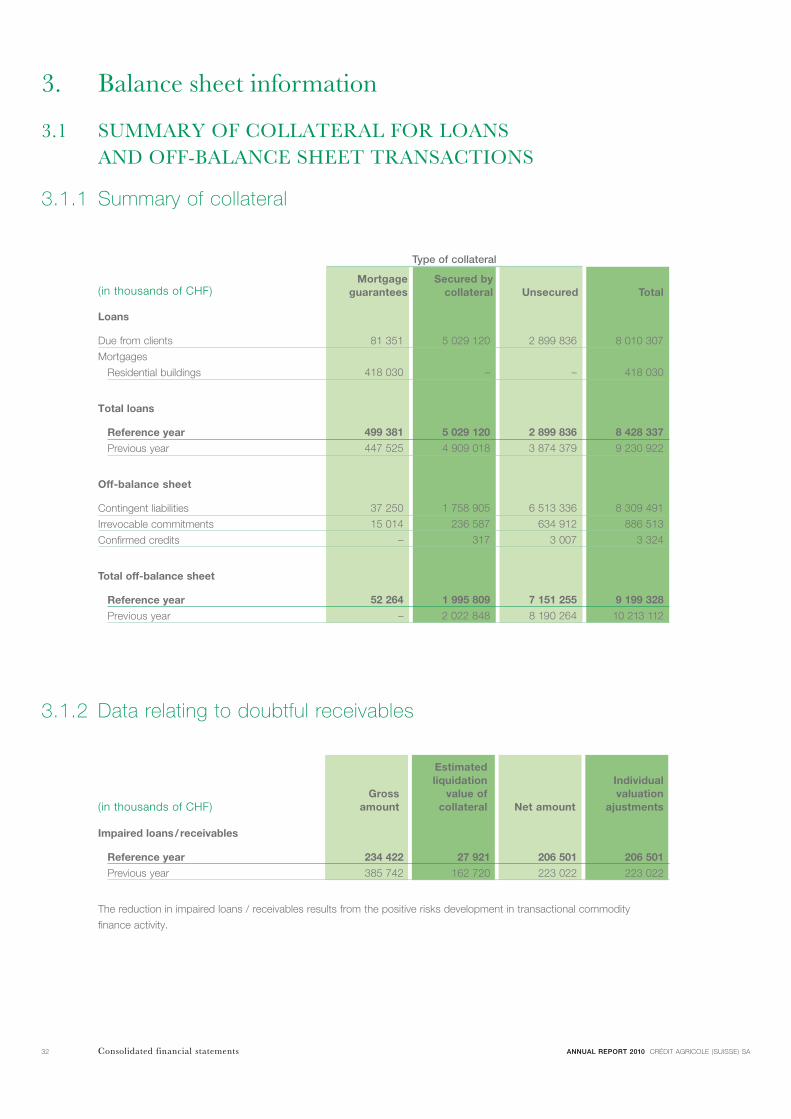

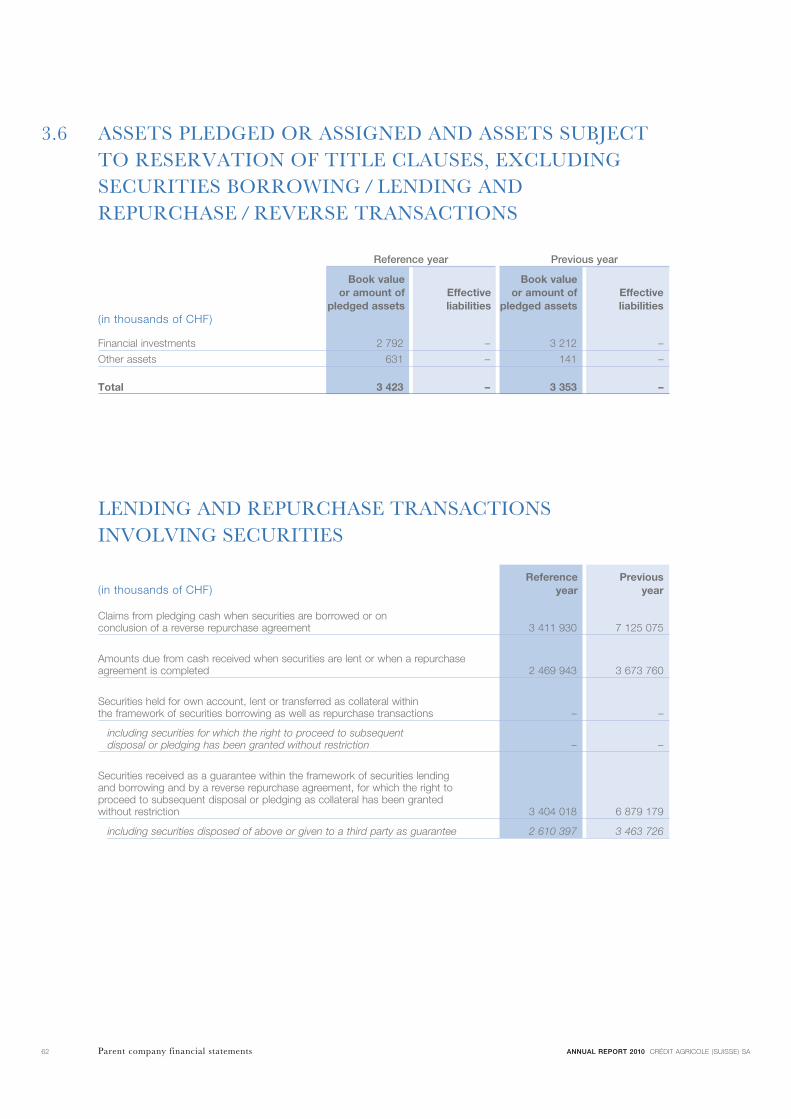

3.1.2 Data relating to doubtful receivables

3. balance sheet information

3.1 Summary Of COllateral fOr lOaNS aNd Off-balaNCe Sheet traNSaCtiONS

3.1.1 Summary of collateral

Loans

Due from clients

Mortgages

Residential buildings

Total loans

Reference year

Previous year

Off-balance sheet

Contingent liabilities

Irrevocable commitments

Confirmed credits

Total off-balance sheet

Reference year

Previous year

Impaired loans / receivables

Reference year

Previous year

The reduction in impaired loans / receivables results from the positive risks development in transactional commodity

finance activity.

Gross amount

Estimated liquidation

value of collateral Net amount

Individual valuation

ajustments

Mortgage guarantees

Secured by collateral

Unsecured

Total

(in thousands of CHF)

(in thousands of CHF)

Type of collateral

81 351 5 029 120 2 899 836 8 010 307

418 030 – – 418 030

499 381 5 029 120 2 899 836 8 428 337

447 525 4 909 018 3 874 379 9 230 922

37 250 1 758 905 6 513 336 8 309 491

15 014 236 587 634 912 886 513

– 317 3 007 3 324

52 264 1 995 809 7 151 255 9 199 328

– 2 022 848 8 190 264 10 213 112

234 422 27 921 206 501 206 501

385 742 162 720 223 022 223 022

Consolidated financial statements ANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA32

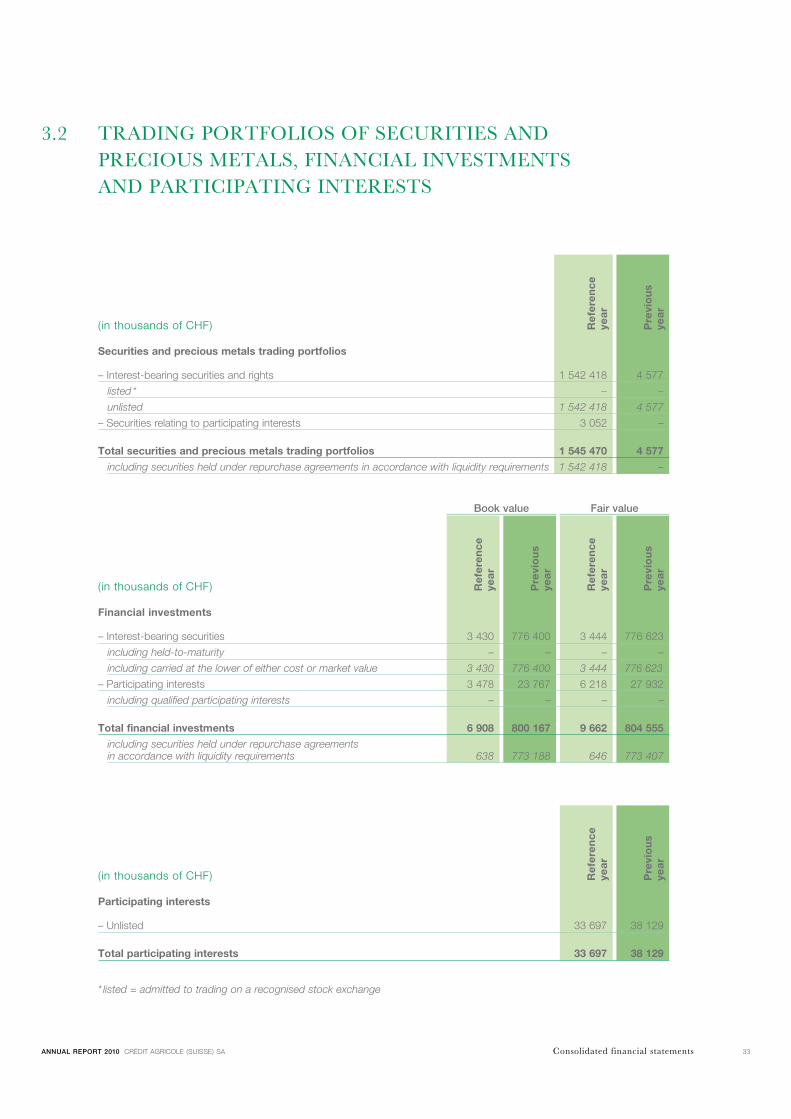

3.2 tradiNG POrtfOliOS Of SeCuritieS aNd PreCiOuS metalS, fiNaNCial iNveStmeNtS aNd PartiCiPatiNG iNtereStS

(in thousands of CHF)

(in thousands of CHF)

Book value Fair value

Ref

eren

ce

year

Pre

vio

us

year

Ref

eren

ce

year

Ref

eren

ce

year

Pre

vio

us

year

Pre

vio

us

year

(in thousands of CHF) Ref

eren

ce

year

Pre

vio

us

year

Financial investments

– Interest-bearing securities

including held-to-maturity

including carried at the lower of either cost or market value

– Participating interests

including qualified participating interests

Total financial investments

including securities held under repurchase agreements in accordance with liquidity requirements

Participating interests

– Unlisted

Total participating interests

* listed = admitted to trading on a recognised stock exchange

Securities and precious metals trading portfolios

– Interest-bearing securities and rights

listed *

unlisted

– Securities relating to participating interests

Total securities and precious metals trading portfolios

including securities held under repurchase agreements in accordance with liquidity requirements

1 542 418 4 577

– –

1 542 418 4 577

3 052 –

1 545 470 4 577

1 542 418 –

33 697 38 129

33 697 38 129

3 430 776 400 3 444 776 623

– – – –

3 430 776 400 3 444 776 623

3 478 23 767 6 218 27 932

– – – –

6 908 800 167 9 662 804 555

638 773 188 646 773 407

Consolidated financial statementsANNUAL REPORT 2010 CRÉDIT AGRICOLE (SUISSE) SA 33

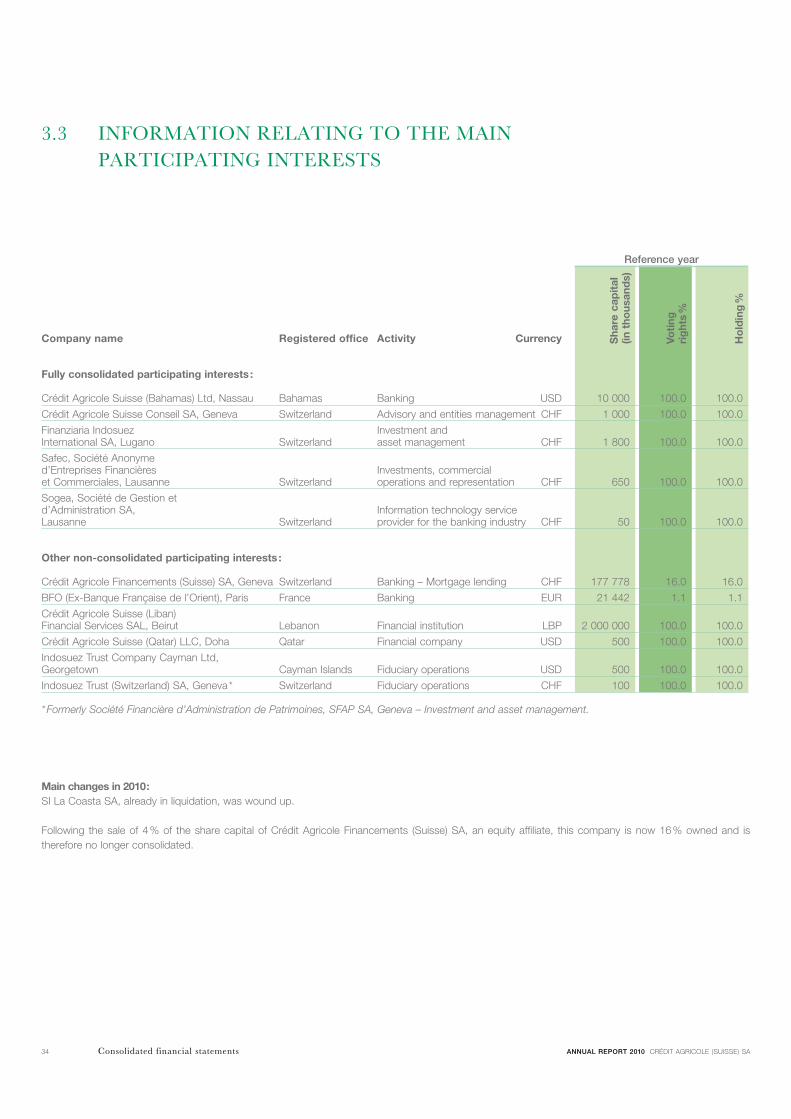

Main changes in 2010 :SI La Coasta SA, already in liquidation, was wound up.

Following the sale of 4 % of the share capital of Crédit Agricole Financements (Suisse) SA, an equity affiliate, this company is now 16 % owned and is therefore no longer consolidated.

3.3 iNfOrmatiON relatiNG tO the maiN PartiCiPatiNG iNtereStS

Company name Registered office Activity Currency Sha

re c

apit

al(in

tho

usan

ds)

Voti

ng

rig

hts

%

Ho

ldin

g %

Reference year

Fully consolidated participating interests :

Crédit Agricole Suisse (Bahamas) Ltd, Nassau Bahamas Banking USD

Crédit Agricole Suisse Conseil SA, Geneva Switzerland Advisory and entities management CHF

Finanziaria Indosuez Investment and International SA, Lugano Switzerland asset management CHF

Safec, Société Anonyme d’Entreprises Financières Investments, commercial et Commerciales, Lausanne Switzerland operations and representation CHF

Sogea, Société de Gestion et d’Administration SA, Information technology service Lausanne Switzerland provider for the banking industry CHF

Other non-consolidated participating interests :

Crédit Agricole Financements (Suisse) SA, Geneva Switzerland Banking – Mortgage lending CHF

BFO (Ex-Banque Française de l’Orient), Paris France Banking EUR

Crédit Agricole Suisse (Liban) Financial Services SAL, Beirut Lebanon Financial institution LBP

Crédit Agricole Suisse (Qatar) LLC, Doha Qatar Financial company USD

Indosuez Trust Company Cayman Ltd, Georgetown Cayman Islands Fiduciary operations USD

Indosuez Trust (Switzerland) SA, Geneva * Switzerland Fiduciary operations CHF

* Formerly Société Financière d’Administration de Patrimoines, SFAP SA, Geneva – Investment and asset management.

10 000 100.0 100.0

1 000 100.0 100.0