Embed Size (px)

Citation preview

Bringing

world class brands

to your home

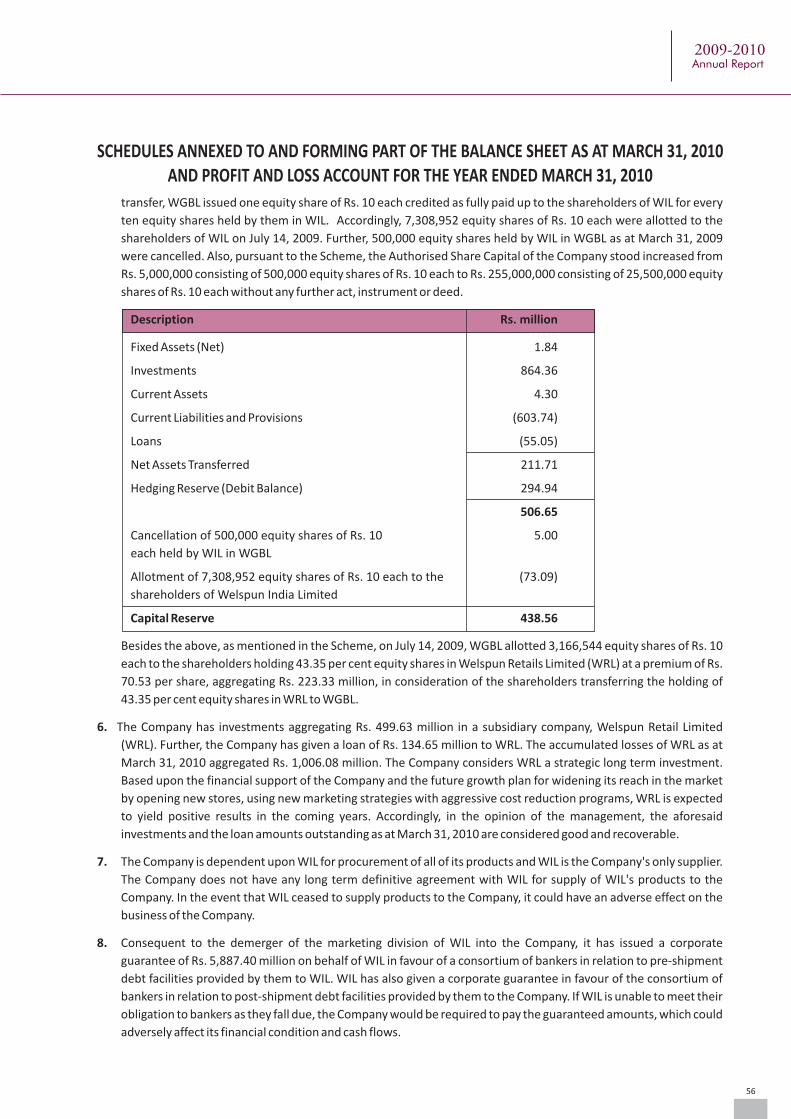

Annual Report

2009-10

Bringing

world class brands

to your home

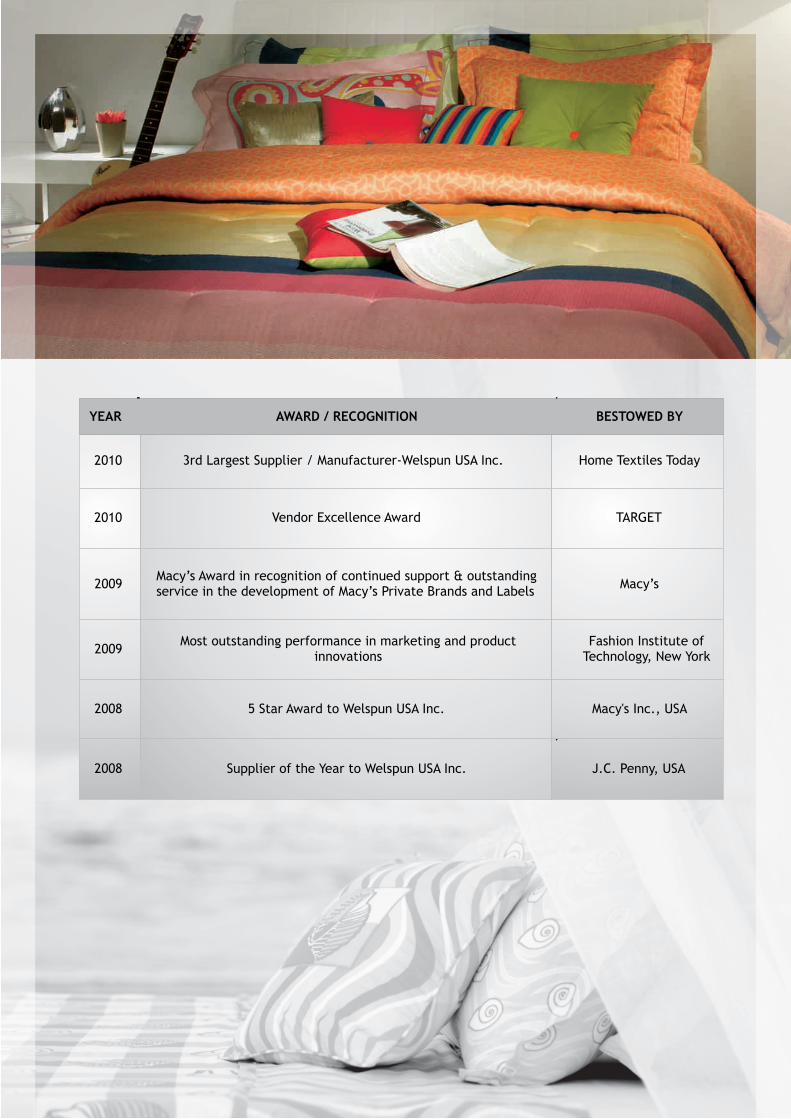

3rd Largest Supplier / Manufacturer-Welspun USA Inc. Home Textiles Today

Vendor Excellence Award TARGET

Macy’s Award in recognition of continued support & outstanding service in the development of Macy’s Private Brands and Labels

Macy’s

Most outstanding performance in marketing and product innovations

Fashion Institute of Technology, New York

5 Star Award to Welspun USA Inc. Macy's Inc., USA

Supplier of the Year to Welspun USA Inc. J.C. Penny, USA

2010

2010

2009

2009

2008

2008

AWARD / RECOGNITION BESTOWED BY YEAR

Contents

1Corporate Information

3Chairman’s Statement

7Directors' Report

11Corporate Governance Report

19Management Discussion and Analysis

39Financial Section

Forward looking statement

In this Annual Report we have disclosed forward-looking information to enable investors to comprehend our

prospects and take informed investment decisions. This report and other statements that set out anticipated

results based on the management's plans and assumptions. We have tried wherever possible to identify such

statements by using words as 'anticipate', 'estimate', 'expects', 'projects', 'intends', 'plans', 'believes', and words of

similar substance in connection with any discussion of future performance. We cannot guarantee that these

forward-looking statements will be realized, although we believe we have been prudent in assumptions. Should

known or unknown risks or uncertainties materialize, or should underlying assumptions prove inaccurate, actual

results could vary materially from those anticipated, estimated or projected. Readers should bear this in mind. We

undertake no obligation to publicity update any forward-looking statements, whether as a result of new information,

future events or otherwise.

Annual Report

2009-10

WELSPUN GLOBAL BRANDS LTD.

1

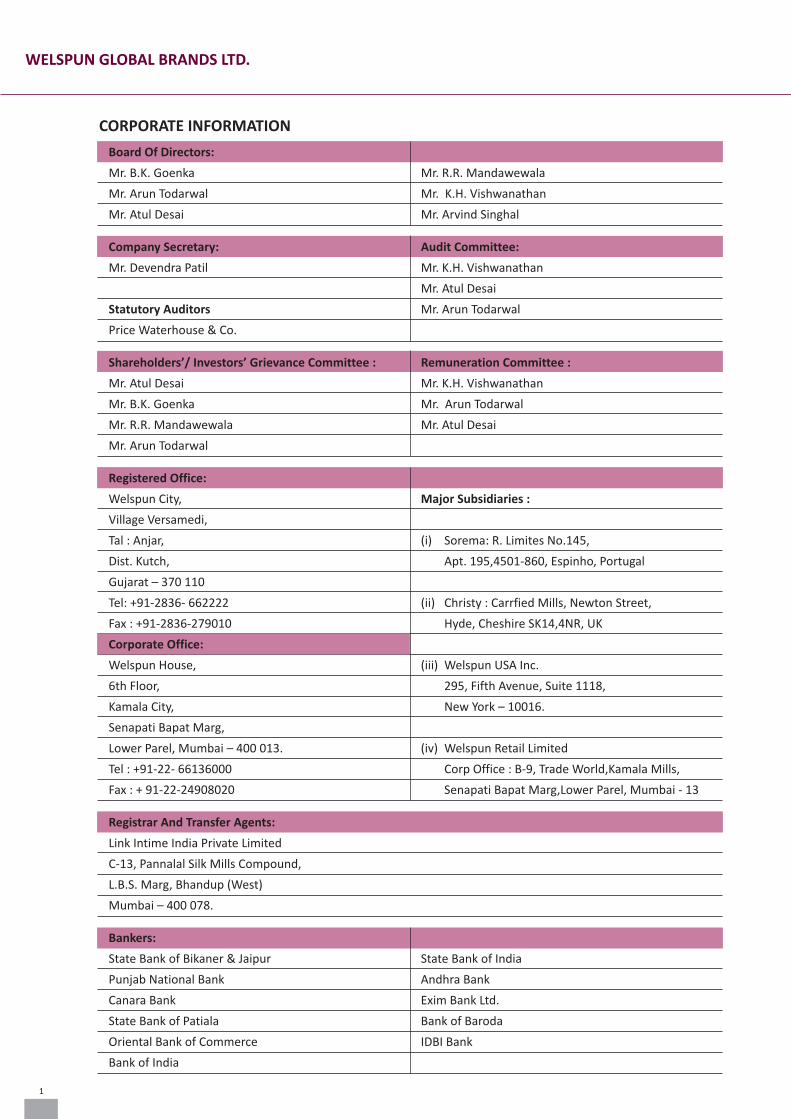

WELSPUN GLOBAL BRANDS LTD.

CORPORATE INFORMATION

Board Of Directors:

Mr. B.K. Goenka Mr. R.R. Mandawewala

Mr. Arun Todarwal Mr. K.H. Vishwanathan

Mr. Atul Desai Mr. Arvind Singhal

Company Secretary: Audit Committee:

Mr. Devendra Patil Mr. K.H. Vishwanathan

Mr. Atul Desai

Statutory Auditors Mr. Arun Todarwal

Price Waterhouse & Co.

Shareholders’/ Investors’ Grievance Committee : Remuneration Committee :

Mr. Atul Desai Mr. K.H. Vishwanathan

Mr. B.K. Goenka Mr. Arun Todarwal

Mr. R.R. Mandawewala Mr. Atul Desai

Mr. Arun Todarwal

Registered Office:

Welspun City, Major Subsidiaries :

Village Versamedi,

Tal : Anjar, (i) Sorema: R. Limites No.145,

Dist. Kutch, Apt. 195,4501-860, Espinho, Portugal

Gujarat – 370 110

Tel: +91-2836- 662222 (ii) Christy : Carrfied Mills, Newton Street,

Fax : +91-2836-279010 Hyde, Cheshire SK14,4NR, UK

Corporate Office:

Welspun House, (iii) Welspun USA Inc.

6th Floor, 295, Fifth Avenue, Suite 1118,

Kamala City, New York – 10016.

Senapati Bapat Marg,

Lower Parel, Mumbai – 400 013. (iv) Welspun Retail Limited

Tel : +91-22- 66136000 Corp Office : B-9, Trade World,Kamala Mills,

Fax : + 91-22-24908020 Senapati Bapat Marg,Lower Parel, Mumbai - 13

Registrar And Transfer Agents:

Link Intime India Private Limited

C-13, Pannalal Silk Mills Compound,

L.B.S. Marg, Bhandup (West)

Mumbai – 400 078.

Bankers:

State Bank of Bikaner & Jaipur State Bank of India

Punjab National Bank Andhra Bank

Canara Bank Exim Bank Ltd.

State Bank of Patiala Bank of Baroda

Oriental Bank of Commerce IDBI Bank

Bank of India

Key Management Team

Mr. B.K. GoenkaChairman, WGBL*

Mr. R.R. Mandawewala Managing Director, WGBL*

Ms. Dipali GoenkaExecutive Director, WIL

* Member of the Board of Directors

Mr. J Barry LeonardCEO, Welspun USA

Mr. Robert WalkerDirector, Christy

Mr. Anurag SharmaPresident, WGBL

Mr. Charles GaenslenCOO, Welspun USA

Mr. Duarte RelvasCEO, Sorema

Mr. Rajiv HandaCEO, WRL

Mr. Updeep SinghPresident, WIL

2

2009-2010Annual Report

My dear fellow Stakeholders,

Welspun Global Brands Limited (WGBL), an international brands, sales, marketing and distribution company of Welspun is

effectively operational from April 1, 2009, after demerger from Welspun India Limited (WIL). WGBL is focused on markets across

the globe with a vision to be the leading player in global Home Textiles. With some of the most prestigious brands under its

banner, WGBL is committed to excellence in product innovation, design, marketing and distribution, thereby creating strong

brand equity for our products.

We have cemented our place in the market through our international associations, which represent some of the most premium

international brands like Christy, Sorema and products retailed under Welspun USA. Christy, our brand in the UK is an iconic

name in towels and holds the coveted position of number one towel brand in that market. Christy is the exclusive supplier of

towels to the prestigious Wimbledon Tennis Championships, synonymous with tennis excellence. Besides Christy, we also offer

products under VFM brands like Kingsley, Pure Opulence and Humming Bird to cater to the bedding market in the UK. Similarly,

our European subsidiary, Sorema, is the number one rugs brand in Portugal and Spain.

WGBL is now investing in brands and expanding in new geographies like Europe, Japan, China, Russia, Canada, South America

and Australia. Our sales and distribution network has greatly contributed to our success, owing to excellent partnerships with

our top retailers like WALMART, TARGET, Costco Wholesale, KOHL's, J.C. Penny, Bed, Bath & Beyond and Macy's. We have been

able to augment replenishment business due to high quality and innovative products, support on design and development and

strategic input on consumer preferences. This relationship with marquee clients has been a significant factor to our success. Our

market presence of Welspun USA has grown tremendously in the US. Testament to its success is Welspun USA's ranking - 3rd

amongst the top 15 home textile suppliers in the US market (Source: Home Textiles Today).

In a few years, we aim to strengthen our association with the end customer, by way of the retail chain for home textiles through

our brands and private labels. With a focus on escalating our retail presence, our 79 retail outlets in the UK will act as a catalyst to

growth, strengthening our visibility to become the preferred choice of consumers. Similarly, Sorema's 67 outlets will facilitate a

direct connection to our customers, thereby increasing profitability. While our international subsidiaries are present in the retail

chains through our own and licensed brands, Welspun Retail, a subsidiary in India, has approximately 150 stores across the

country. We are the first of a kind retail chain in India, which is focused on Home Textiles. In India, retail is leaping ahead at a rate

of 12% on a base of $350 billion (Source: BMI India Retail Report). Organized retail is only around 6% of the retail sales and

provides ample opportunity for Welspun to capture a larger share of the Home Textiles business. As consumer sentiment picks

up, the Indian retail market is ripe with potential. In particular, Home Textiles is being viewed in a new light as consumers

increasingly identify home décor with fashion, creating a significant opportunity for WGBL.

Welspun aims to create value for the end user through innovative offerings and our skilled design studios. We employ extensive

market research to identify our consumers' aspirations, in order to cater to their specific needs. Innovation is therefore a part of

our corporate DNA, steering us in the creation of products like Hygrocotton, Drylon and Permaback. This pursuit of innovation

has been critical to our differentiation in the market, resulting in attaining a larger market share. We aim to earn 40% of our

revenues from innovative product offerings in the coming years, from the current ~ 20%.

Financial Scorecard

At a standalone level, WGBL had a revenue of Rs. 1,609.22 crores and a consolidated revenue of Rs. 2,153.78 crores. Despite the

recession and resultant reduction in consumer spend, WGBL posted a net EBITDA of Rs. 54 crore at the consolidated level. With a

focus on cementing our market presence to facilitate business growth, our subsidiaries have taken the necessary steps to

strengthen their position in the market. This process will help business growth, with increased profitability, strong brand

presence and a preferred relationship with top retailers of the world.

Message from Chairman

3

WELSPUN GLOBAL BRANDS LTD.

B. K. Goenka

Chairman

Human Capital

All our achievements in the past are a direct result of the

dedication and efforts of our employees, who have

shown unflinching commitment and drive towards

excellence, leading to this phenomenal growth. We have

been able to implement our geographic and brand

expansion strategy, owing to the dedicated efforts of

this team.

Sustainability & Corporate Social Responsibility

As a Group, Welspun has earmarked a large sum of

money for activities focused on the environment and

well-being of the community at large. Our initiatives

follow the 3 guiding principles of Education,

Empowerment and Environment. This philosophy has

led to empowering the women in our worker's families,

as they now create products that are sold through our

retail chains.

Finally, I would like to put on record my sincere

appreciation to the financial institutions, banks, equity

partners, Government authorities and each Welspunite

for their unflinching support. I believe we have all the

ingredients to become one of the largest and best home

textiles brand and marketing companies in the world

and for that, I solicit your continued support.

Welspun USA ranked 3rd

amongst the top 15 home textile

suppliers in the US market

“

4

2009-2010Annual Report

7

DIRECTORS' REPORT

To,

The Members,

WELSPUN GLOBAL BRANDS LIMITED

Your directors are pleased to present their 10th Annual Report together with the Audited Statement of Accounts for the

period ended March 31, 2010.

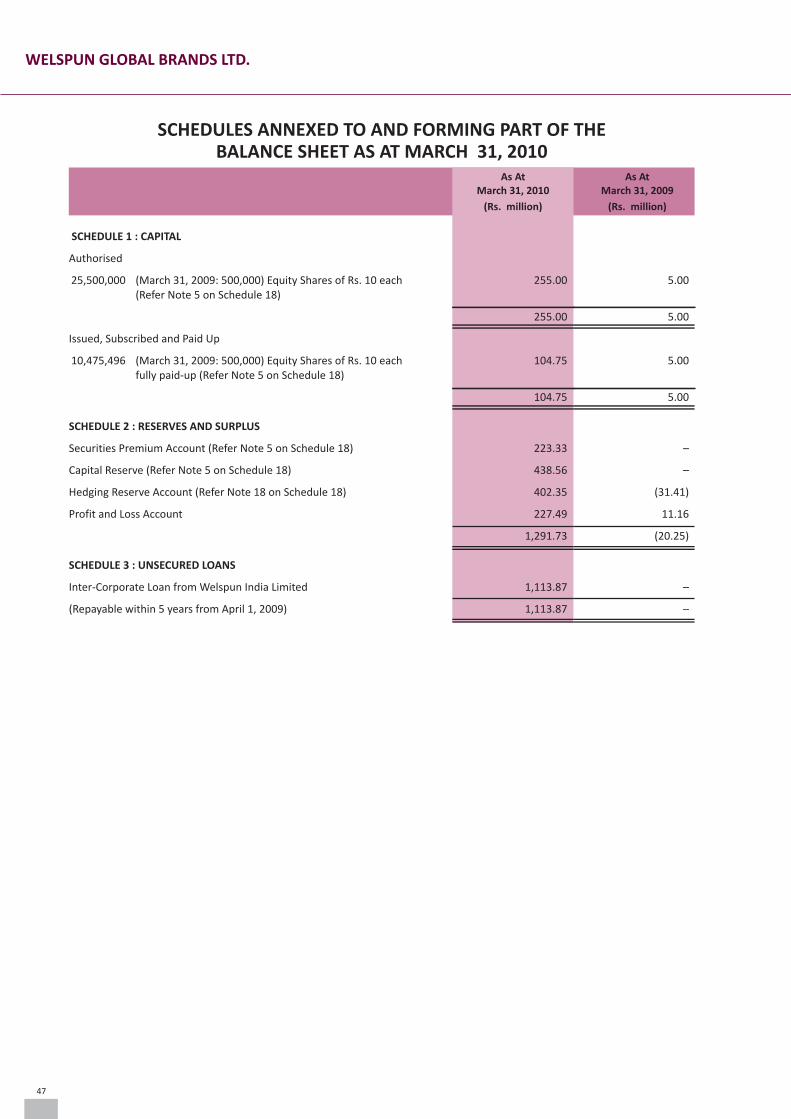

Acquisition of Marketing Division pursuant to a scheme of arrangement:

During the year under report, your Company has acquired the Marketing Division of Welspun India Limited pursuant to

the Composite Scheme of Arrangement in the nature of Demerger for transfer of Marketing Division of Welspun India

Limited to Welspun Global Brands Limited and Restructure of Capital of these companies (“Scheme”), which was

sanctioned by the Hon'ble High Court of Gujarat at Ahmedabad on May 8, 2009. The Scheme became effective on June

12,2009 i.e. the date of filing of a copy of the Order with the Registrar of Companies, Gujarat (“Effective Date”). Pursuant

to the Scheme, the Company has issued and allotted 7,308,952 equity shares of Rs. 10/- each on July 14, 2009 to the

equity shareholders of WIL holding equity shares as on record date, June 26, 2009 in the ratio of 1 (one) Equity Share of

Rs.10/- each for every 10 (ten) equity shares of Rs.10/- each held in Welspun India Limited, leaving apart fractional

entitlements which will be dealt with pursuant to the Scheme. Besides, as mentioned in the Scheme, the Company has

acquired 10,200,000 (then 51%) equity shares in Welspun Retail Limited (“WRL”) held by the other promoters of WRL,

at the price equivalent to the price at which 9,800,000 (then 49%) equity shares in WRL held by Marketing Division of

WIL and in consideration of that the Company has allotted 3,166,544 equity shares to them, which is proportionate to

the equity shares attributable to the shares transferred to the Company by WIL under the Scheme. As WRL had

increased its capital, the Company's shareholding in WRL amounted to 85% of the equity share capital in WRL.

Accordingly, as on March 31, 2010 , the aggregate paid up capital of the Company is Rs.10,47,54,960 consisting of

10,475,496 equity shares of Rs. 10/- each.

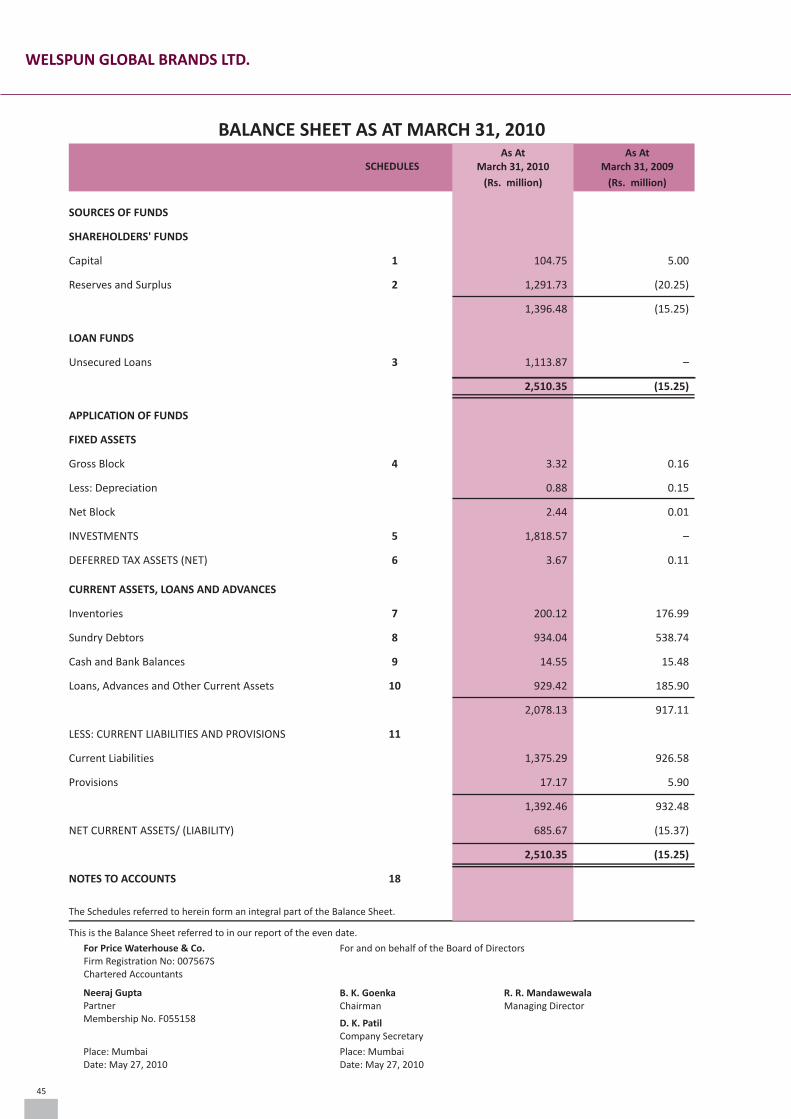

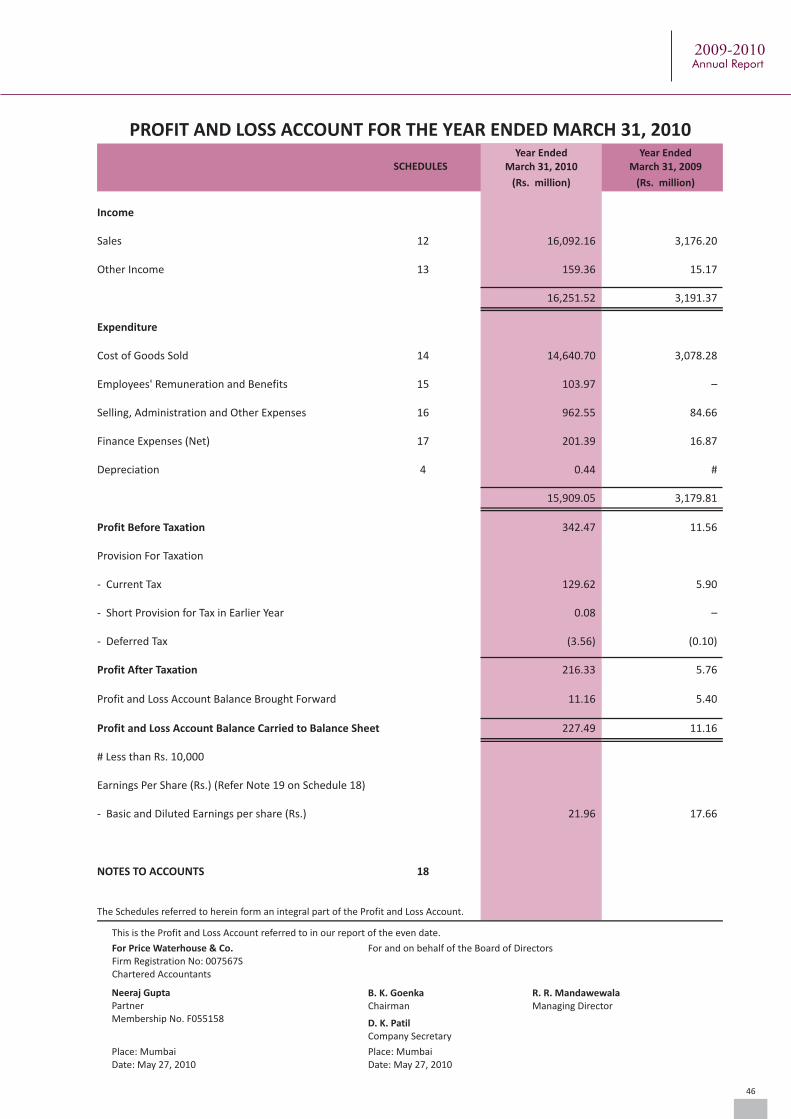

FINANCIAL RESULTS

2009-10 2008-09

(Rs. in million) (Rs. in million)

INCOME 16,251.52 3,191.37

EXPENDITURE 15,909.05 3,179.81

Profit Before taxation 342.47 11.56

Provision for taxation

– Current Tax 129.62 5.90

– Short Provision for Tax in Earlier Year 0.08 –

– Deferred Tax (3.56) (0.10)

PROFIT AFTER TAXATION 216.33 5.76

Profit and Loss Account Balance B/F 11.16 5.40

Balance Carried to Balance Sheet 227.49 11.16

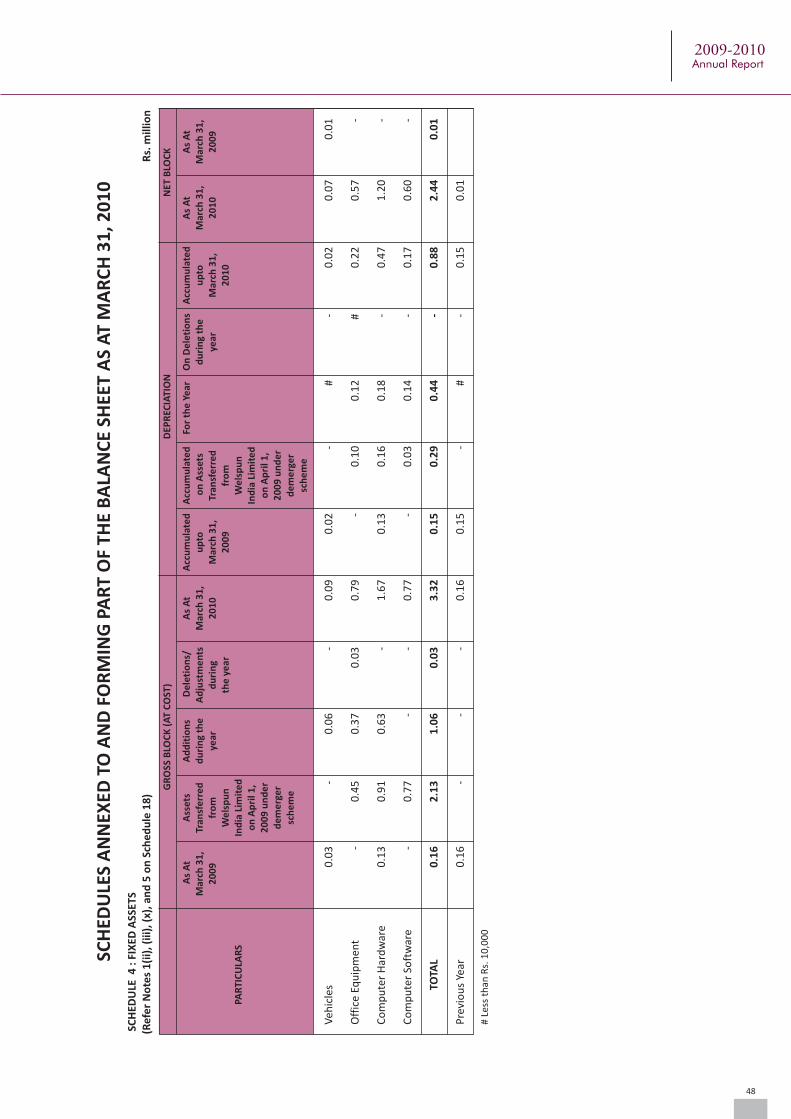

During the financial year under review, your Company has recorded an impressive performance with total income from

operations increasing from Rs. 3,191.37 million to Rs.16,251.52 million. Profit before tax has been Rs.342.47 million

compared to Rs.11.56 million last year, registering an increase of 2862.54 % over the last year. Profit after tax has been

Rs.216.33 million compared to Rs. 5.76 million last year, registering a rise of 3655.72 % over the last year. Considering

the transfer of division under the demerger, this performance is commendable. The performance has set the Company

on the path of rapid growth and many new initiatives have been taken to improve the operating efficiencies as well.

WELSPUN GLOBAL BRANDS LTD.

8

DIVIDEND

With a view to plough back the profits for consolidating financial position of the Company to achieve long term growth,

your directors do not recommend any dividend for the period ended March 31, 2010. Your directors are of the opinion

that this is in the long term interest of the Company as well as its stakeholders.

LISTING OF EQUITY SHARES

The Company has applied for permission for getting relaxation from applicability of Rule 19 (2) (b) under the Securities

Contract (Regulations) Rules, 1957 to Securities and Exchange Board of India (SEBI). After receipt of the said permission,

the equity shares of the Company will be listed on Bombay Stock Exchange Limited (BSE) and National Stock Exchange of

India Limited (NSE).

PUBLIC DEPOSITS

The Company does not accept any deposit from public and hence has not contravened provisions of section 58A of the

Companies Act, 1956 and Companies (Acceptance of Deposits) Rules, 1975 and Reserve Bank of India Rules, if any.

DIRECTORS

The Board of Directors of the Company at its meeting held on September 15, 2009, had appointed Mr. Arun Todarwal,

Mr. Arvind Singhal, Mr. Atul Desai and Mr. K.H. Vishwanathan as Additional Directors of your Company. As per the

provisions of Section 260 of the Companies Act, 1956 these Directors will hold office until the conclusion of the

forthcoming Annual General Meeting of the Company. The Company has received notices under Section 257 of the Act

along with requisite deposit in respect of the aforesaid persons, proposing their appointment as directors of the

Company.

Mr. M.L. Mittal and Mr. Mohan Manikkan ceased to be directors of the Company w.e.f September 15, 2009. The Board

of Directors places on record its appreciation for the valuable contribution made by both of them during their tenures as

directors of the Company.

In term of the provision of the Companies Act, 1956 and as per the Articles of Association of the Company, Mr. B.K.

Goenka, Director of the company retires by rotation and being eligible offers himself for re-appointment.

AUDITORS

The Auditors of the Company, M/s Price Waterhouse & Co. Chartered Accountants shall retire at the conclusion of the

ensuing Annual General Meeting of the Company and, being eligible, offer themselves for re- appointment.

CONSERVATION OF ENERGY, TECHNOLOGY ABSORPTION, FOREIGN EXCHANGE EARNINGS AND OUTGO

Your Company has no activity relating to Conservation of Energy and Technology absorption as stipulated in the

Companies (Disclosure of Particulars in the Report of Board of Directors) Rules, 1988.

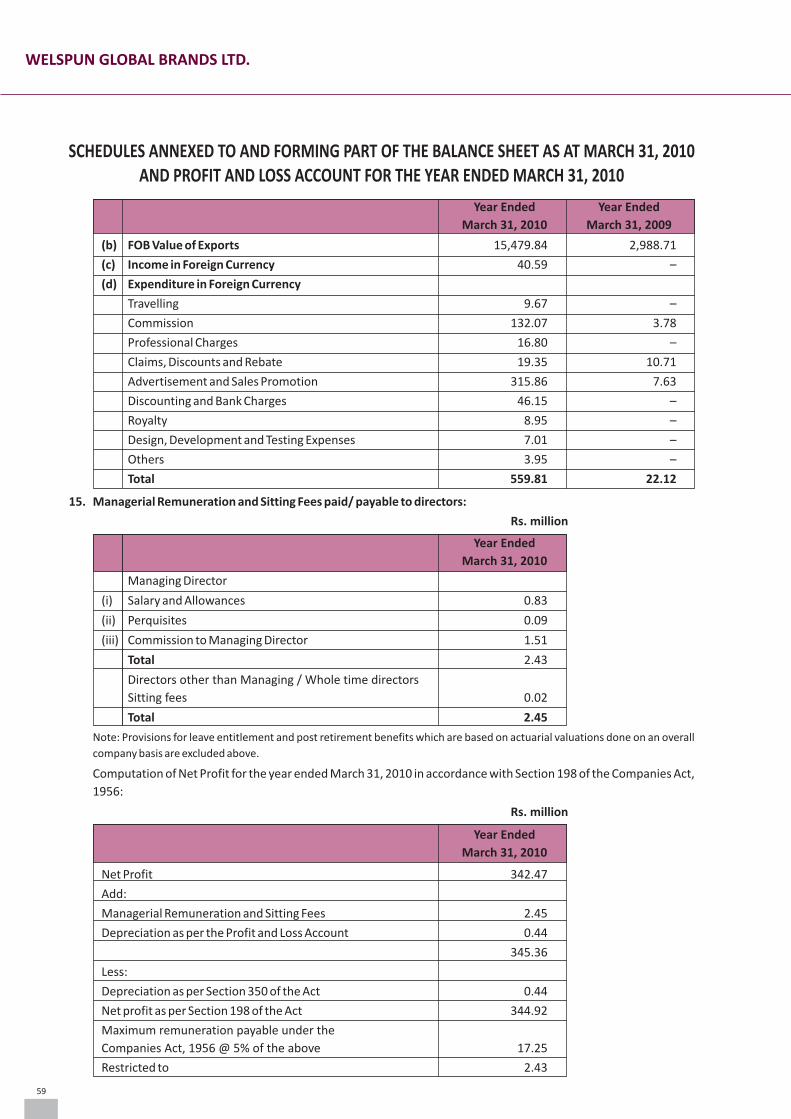

During the year under review, the expenditure of your company in foreign currency was Rs.559.81 million (previous

year Rs.22.12 million) and income in foreign currency was Rs. 40.59 million (previous year :nil)

PARTICULARS OF EMPLOYEES

A statement containing details of employees in receipt of remuneration equal to or exceeding the limits prescribed

under Section 217(2A) of the Companies Act, 1956 read with the Companies (Particulars of Employees) Rules, 1975 is

attached hereto and forms part of this report.

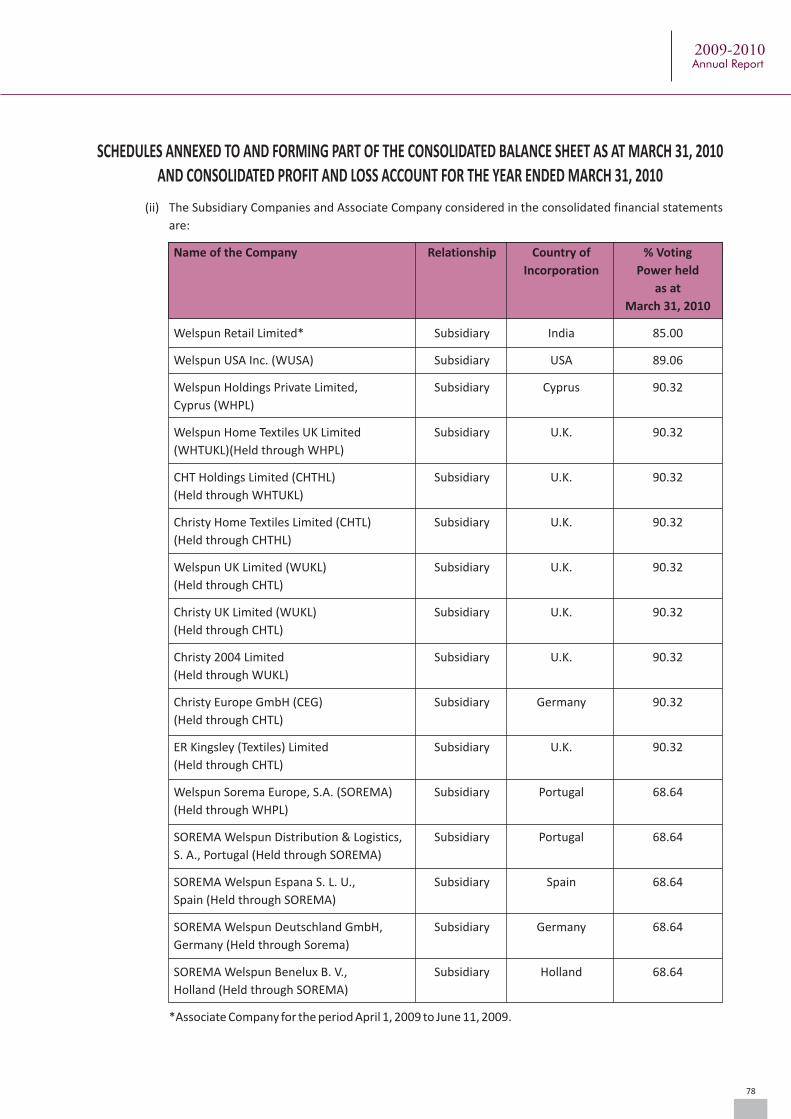

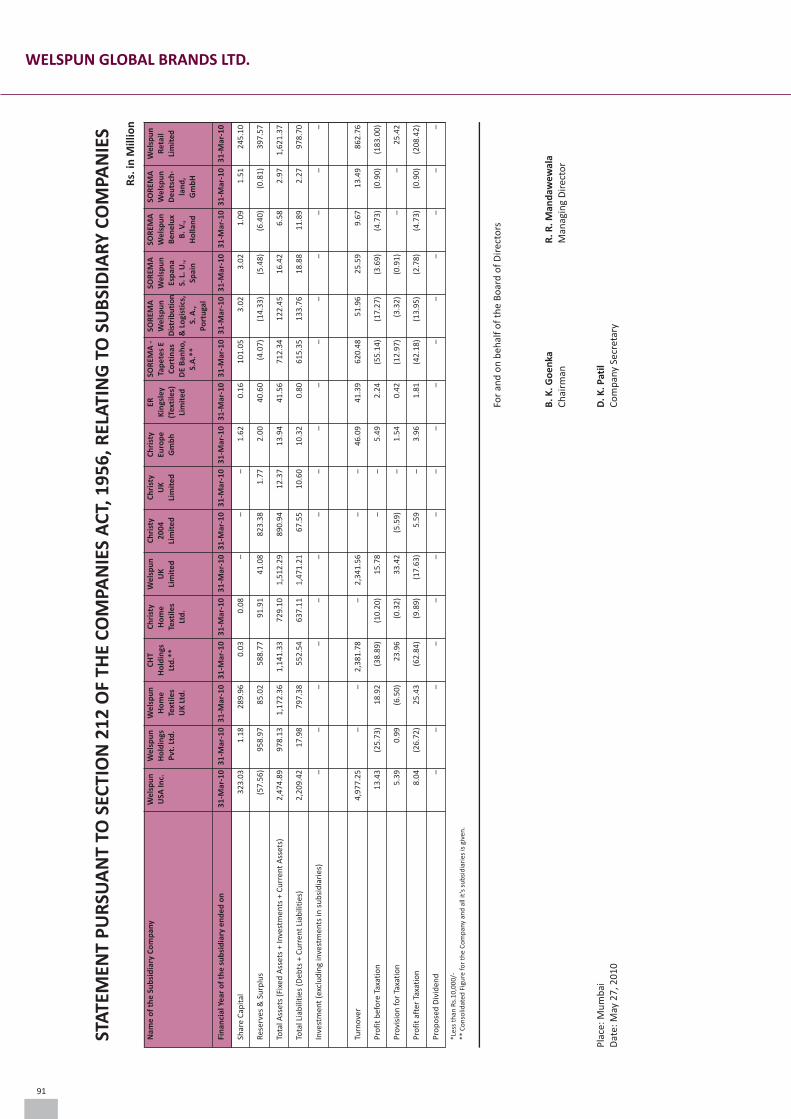

PARTICULARS OF SUBSIDIARIES

The Statement pursuant to Section 212 of the Companies Act, 1956 containing details of subsidiaries of the Company,

forms part of the Annual Report

2009-2010Annual Report

9

The Company has been granted exemption for the year ended March 31, 2010 by the Ministry of Corporate Affairs from

attaching the individual Annual Report of its subsidiary companies to its Balance Sheet. In terms of the approval,

Balance Sheet, Profit and Loss Account, report of Board of Directors and Auditors of the subsidiaries have not been

attached with the Annual Report of the Company. These documents would be made available upon request in writing

by any member of the Company interested in obtaining the same. However, as directed by Central Government, the

financial details of the subsidiaries have been furnished under 'Statement relating Subsidiaries', which forms part of

Annual Report.

DIRECTORS RESPONSIBILITY STATEMENT

The Directors confirm that they had:

a. followed in the preparation of annual accounts, the applicable accounting standards and given proper explanation

relating to material departures, if any;

b. selected such accounting policies and applied them consistently and made judgments and estimates that are

reasonable and prudent so as to give a true and fair view of the state of affairs of the company at the end of the

financial year and of the profit and loss of the company for that period;

c. taken proper and sufficient care for the maintenance of adequate accounting records in accordance with the

provisions of the Act so as to safeguard the assets of the company and to prevent and detect fraud and other

irregularities; and

d. Prepared the accounts on a going concern basis.

ACKNOWLEDGEMENTS

Your directors wish to place on record their appreciation for the valuable support and assistance received by your

Company from Banks, Government and their departments, Regulatory authorities and Stakeholders. The Board also

thanks the employees at all levels for their dedication, commitment and hard work put in by them for the Company's

achievements.

For and on behalf of the Board

May 27, 2010 B. K. Goenka

Mumbai Chairman

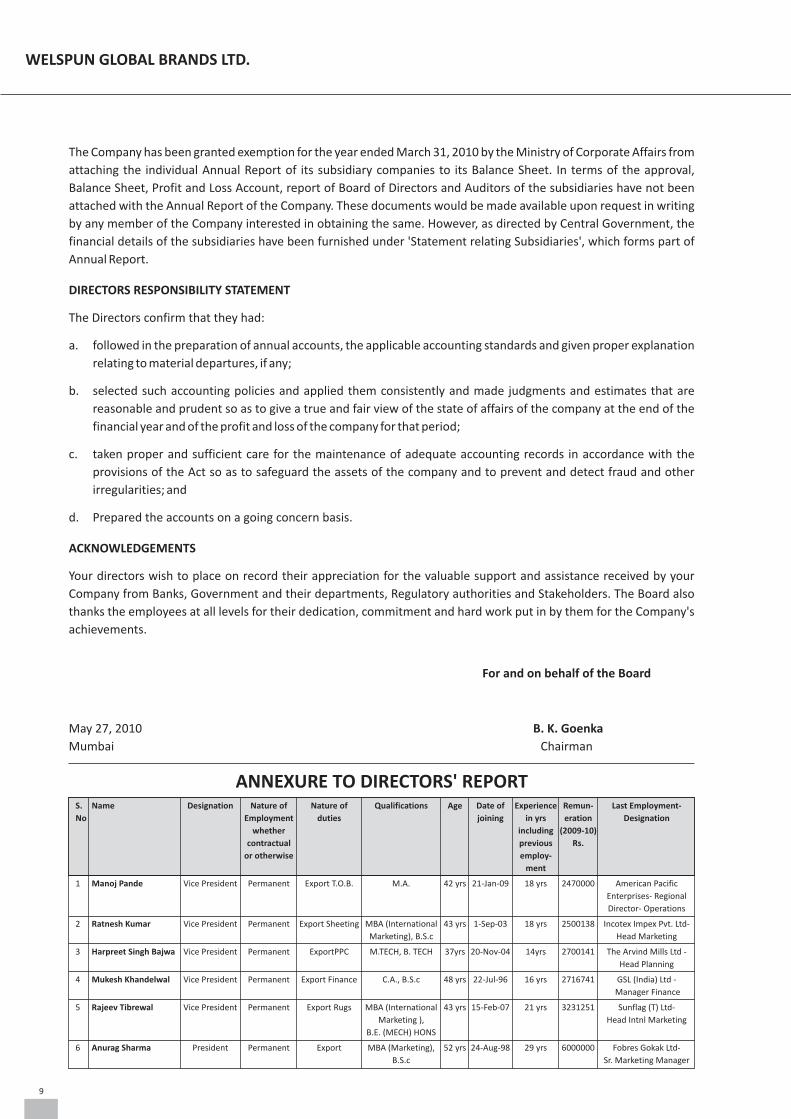

S. Name Designation Nature of Nature of Qualifications Age Date of Experience Remun- Last Employment-

No Employment duties joining in yrs eration Designation

whether including (2009-10)

contractual previous Rs.

or otherwise employ-

ment

1 Manoj Pande Vice President Permanent Export T.O.B. M.A. 42 yrs 21-Jan-09 18 yrs 2470000 American Pacific

Enterprises- Regional

Director- Operations

2 Ratnesh Kumar Vice President Permanent Export Sheeting MBA (International 43 yrs 1-Sep-03 18 yrs 2500138 Incotex Impex Pvt. Ltd-

Marketing), B.S.c Head Marketing

3 Harpreet Singh Bajwa Vice President Permanent ExportPPC M.TECH, B. TECH 37yrs 20-Nov-04 14yrs 2700141 The Arvind Mills Ltd -

Head Planning

4 Mukesh Khandelwal Vice President Permanent Export Finance C.A., B.S.c 48 yrs 22-Jul-96 16 yrs 2716741 GSL (India) Ltd -

Manager Finance

5 Rajeev Tibrewal Vice President Permanent Export Rugs MBA (International 43 yrs 15-Feb-07 21 yrs 3231251 Sunflag (T) Ltd-

Marketing ), Head Intnl Marketing

B.E. (MECH) HONS

6 Anurag Sharma President Permanent Export MBA (Marketing), 52 yrs 24-Aug-98 29 yrs 6000000 Fobres Gokak Ltd-

B.S.c Sr. Marketing Manager

ANNEXURE TO DIRECTORS' REPORT

WELSPUN GLOBAL BRANDS LTD.

CORPORATE GOVERNANCE REPORT

I. Philosophy on Corporate Governance:

Board of Directors of the Company acts as a trustee and assumes fiduciary responsibility of protecting the interests

of the shareholders and other stakeholders of the Company. The Company is committed to good corporate

governance with accountability and transparency in all its dealing, and places emphasis on business ethics to

achieve fairness to all stakeholders. Board supports the broad principles of Corporate Governance. In order to

attain the highest level of good Corporate Governance practice, Board lays strong emphasis on transparency,

accountability and integrity. It is believed that the importance for good Corporate Governance lies not merely in

drafting a code of Corporate Governance but in practising it.

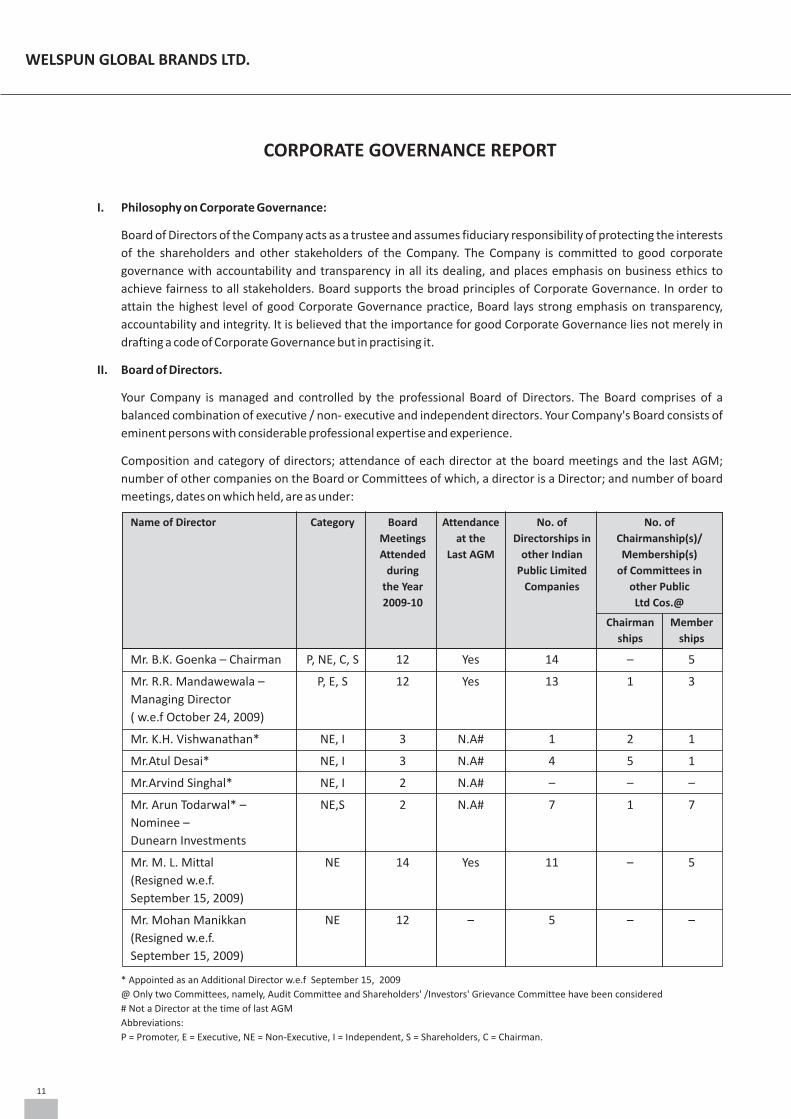

II. Board of Directors.

Your Company is managed and controlled by the professional Board of Directors. The Board comprises of a

balanced combination of executive / non- executive and independent directors. Your Company's Board consists of

eminent persons with considerable professional expertise and experience.

Composition and category of directors; attendance of each director at the board meetings and the last AGM;

number of other companies on the Board or Committees of which, a director is a Director; and number of board

meetings, dates on which held, are as under:

Name of Director Category Board

Meetings at the Directorships in Chairmanship(s)/

Attended Last AGM other Indian Membership(s)

during Public Limited of Committees in

the Year Companies other Public

2009-10 Ltd Cos.@

Chairman Member

ships ships

Mr. B.K. Goenka – Chairman P, NE, C, S 12 Yes 14 – 5

Mr. R.R. Mandawewala – P, E, S 12 Yes 13 1 3

Managing Director

( w.e.f October 24, 2009)

Mr. K.H. Vishwanathan* NE, I 3 N.A# 1 2 1

Mr.Atul Desai* NE, I 3 N.A# 4 5 1

Mr.Arvind Singhal* NE, I 2 N.A# – – –

Mr. Arun Todarwal* – NE,S 2 N.A# 7 1 7

Nominee –

Dunearn Investments

Mr. M. L. Mittal NE 14 Yes 11 – 5

(Resigned w.e.f.

September 15, 2009)

Mr. Mohan Manikkan NE 12 – 5 – –

(Resigned w.e.f.

September 15, 2009)

* Appointed as an Additional Director w.e.f September 15, 2009

@ Only two Committees, namely, Audit Committee and Shareholders' /Investors' Grievance Committee have been considered

# Not a Director at the time of last AGM

Abbreviations:

P = Promoter, E = Executive, NE = Non-Executive, I = Independent, S = Shareholders, C = Chairman.

Attendance No. of No. of

11

WELSPUN GLOBAL BRANDS LTD.

Seventeen meetings of the Board of Directors were held during the financial year 2009-10. Dates of those meetings

were April 7, 2009, April 21, 2009, April 24, 2009, May 27, 2009, May 29, 2009, June 23, 2009,June 29, 2009,June

30, 2009, July 14, 2009,July 30, 2009, August 5, 2009, August 26, 2009, August 27, 2009, September 11, 2009,

September 15, 2009, December 31, 2009 and January 11, 2010.The information as required under Annexure IA to

Clause 49 is being made available to the Board.

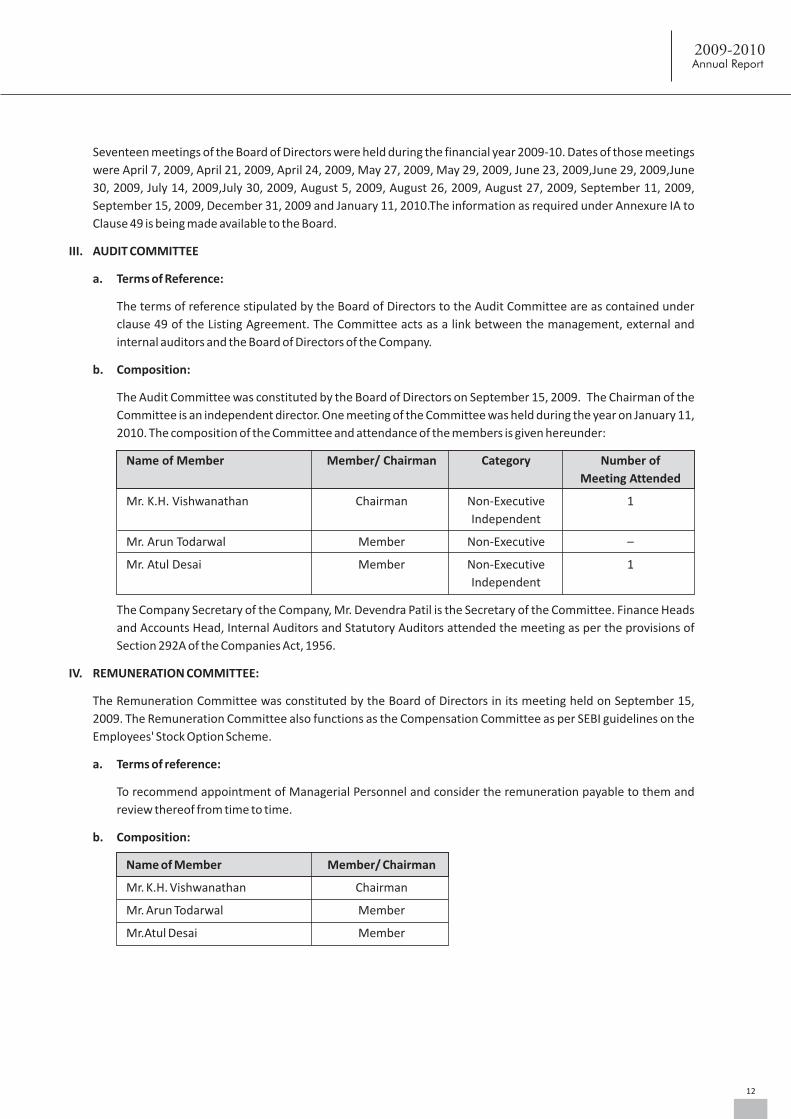

III. AUDIT COMMITTEE

a. Terms of Reference:

The terms of reference stipulated by the Board of Directors to the Audit Committee are as contained under

clause 49 of the Listing Agreement. The Committee acts as a link between the management, external and

internal auditors and the Board of Directors of the Company.

b. Composition:

The Audit Committee was constituted by the Board of Directors on September 15, 2009. The Chairman of the

Committee is an independent director. One meeting of the Committee was held during the year on January 11,

2010. The composition of the Committee and attendance of the members is given hereunder:

Name of Member Member/ Chairman Category Number of

Meeting Attended

Mr. K.H. Vishwanathan Chairman Non-Executive 1

Independent

Mr. Arun Todarwal Member Non-Executive –

Mr. Atul Desai Member Non-Executive 1

Independent

The Company Secretary of the Company, Mr. Devendra Patil is the Secretary of the Committee. Finance Heads

and Accounts Head, Internal Auditors and Statutory Auditors attended the meeting as per the provisions of

Section 292A of the Companies Act, 1956.

IV. REMUNERATION COMMITTEE:

The Remuneration Committee was constituted by the Board of Directors in its meeting held on September 15,

2009. The Remuneration Committee also functions as the Compensation Committee as per SEBI guidelines on the

Employees' Stock Option Scheme.

a. Terms of reference:

To recommend appointment of Managerial Personnel and consider the remuneration payable to them and

review thereof from time to time.

b. Composition:

Name of Member Member/ Chairman

Mr. K.H. Vishwanathan Chairman

Mr. Arun Todarwal Member

Mr.Atul Desai Member

12

2009-2010Annual Report

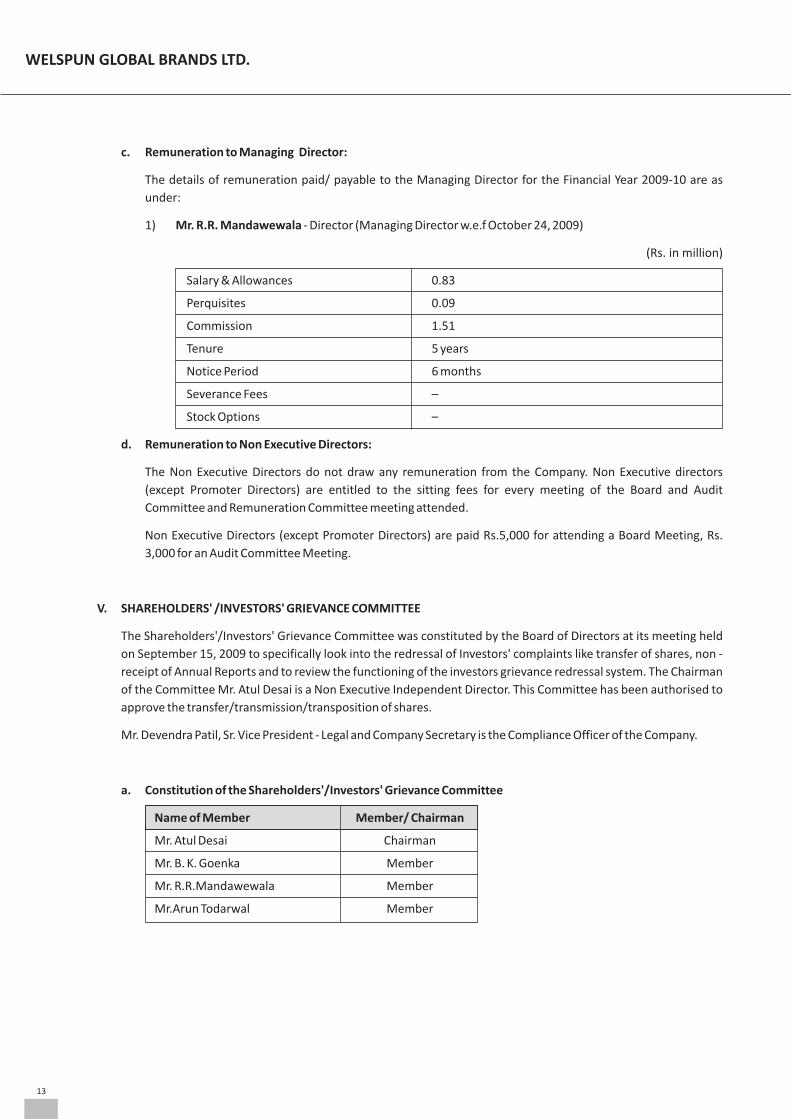

c. Remuneration to Managing Director:

The details of remuneration paid/ payable to the Managing Director for the Financial Year 2009-10 are as

under:

1) Mr. R.R. Mandawewala - Director (Managing Director w.e.f October 24, 2009)

(Rs. in million)

Salary & Allowances 0.83

Perquisites 0.09

Commission 1.51

Tenure 5 years

Notice Period 6 months

Severance Fees –

Stock Options –

d. Remuneration to Non Executive Directors:

The Non Executive Directors do not draw any remuneration from the Company. Non Executive directors

(except Promoter Directors) are entitled to the sitting fees for every meeting of the Board and Audit

Committee and Remuneration Committee meeting attended.

Non Executive Directors (except Promoter Directors) are paid Rs.5,000 for attending a Board Meeting, Rs.

3,000 for an Audit Committee Meeting.

V. SHAREHOLDERS' /INVESTORS' GRIEVANCE COMMITTEE

The Shareholders'/Investors' Grievance Committee was constituted by the Board of Directors at its meeting held

on September 15, 2009 to specifically look into the redressal of Investors' complaints like transfer of shares, non -

receipt of Annual Reports and to review the functioning of the investors grievance redressal system. The Chairman

of the Committee Mr. Atul Desai is a Non Executive Independent Director. This Committee has been authorised to

approve the transfer/transmission/transposition of shares.

Mr. Devendra Patil, Sr. Vice President - Legal and Company Secretary is the Compliance Officer of the Company.

a. Constitution of the Shareholders'/Investors' Grievance Committee

Name of Member Member/ Chairman

Mr. Atul Desai Chairman

Mr. B. K. Goenka Member

Mr. R.R.Mandawewala Member

Mr.Arun Todarwal Member

13

WELSPUN GLOBAL BRANDS LTD.

b. Number of Shareholders complaints received during the year:

During the Year under review, a total of 89 Investor complaints/requests were received and were processed.

All the complaints received during the year under review were processed/solved within the time limit to the

satisfaction of the investors/shareholders and no complaint is pending as at March 31, 2010 for a period over

30 days.

VI. MANAGEMENT

a. Management Discussion and Analysis

Management Discussion and Analysis of various businesses of the Company is separately given in the Annual

Report.

b. Disclosures by Management to the Board

All details relating to financial and commercial transactions where directors may have a pecuniary interest are

provided to the Board, and the interested directors neither participated in the discussion, nor do they vote on

such matters.

VII. GENERAL BODY MEETINGS

(i) The details of Annual General Meetings held in the last three years are given hereunder:

Meeting Day & Date of Meeting Time Place

7th Annual Saturday, September 29, 2007 10.30 a.m. Survey No.76, Village Morai,

General Meeting Vapi, Dist. Valsad, Gujarat - 396191

8th Annual Monday, September 8, 2008 10.30 a.m. Survey No.76, Village Morai, Vapi,

General Meeting Dist. Valsad, Gujarat - 396191

9th Annual Thursday, June 11, 2009 1.00 p.m. Survey No.76, Village Morai, Vapi,

General Meeting Dist. Valsad, Gujarat - 396191

(ii) Special Resolutions passed in the previous Annual General Meeting:

(a) To approve the Employees Stock Option Scheme titled as 'WELSOP 2009' to the permanent employees,

who are in employment of the Company and its present and future subsidiaries.

(b) To alter the Articles of Association by way of substituting with new set of Articles of Association bearing

Articles No. 1 to 220.

(c) To give loans for a sum not exceeding Rs. 20 Crores to Welspun Retail Limited, a Welspun Group Company

(d) To seek approval pursuant to Section 149 (2A) of the Companies Act, 1956 to commence the business

specified in the Clause III (C) 94 of the Memorandum of Association.

VIII. DISCLOSURE

a. Details of related party transactions

Refer Note No. 17(ii) to the Accounts for list of related party transactions.

b. Details of information on appointment of new directors

Name of the director, nature of expertise in specific functional areas, names of companies in which the person

already holds directorship and membership of committees of the Board and his shareholdings in the Company

forms part of the Notice of General Meeting, annexed to this Annual Report.

14

2009-2010Annual Report

c. Details of non-compliance

There was no non compliance by the Company, nor were there any penalty or stricture imposed on the

Company by the Stock Exchange or SEBI or any authority on any matter related to capital market during the last

3 years.

IX. MEANS OF COMMUNICATION

The Company has filed an application for listing of the Equity Shares with Bombay Stock Exchange Limited (BSE) and

National Stock Exchange of India Limited (NSE) and awaiting listing.

Once the Equity Shares gets listed on BSE and NSE, the Company will publish the quarterly/half- yearly /annual

financial results after the same are approved / taken on record by the Board of Directors in newspapers as required

under the Listing Agreements entered into with the Stock Exchanges.

The Financial results will also be placed on the Company's website: www. welspunglobalbrands.com

Management Discussion and Analysis form part of this Annual Report.

X. GENERAL SHAREHOLDER INFORMATION

AGM will be held on Tuesday, September 28, 2010 at 12.30 p.m. at the Registered Office of the Company at

Welspun City, Village Versamedi, Taluka Anjar, District Kutch, Gujarat - 370 100.

Financial Year of the Company is April 1 to March 31.

Date of Book Closure: Tuesday, September 21, 2010 to Tuesday, September 28, 2010 (Both days inclusive)

Dividend payment date: Not applicable.

The Company's Equity Shares are proposed to get listed on Bombay Stock Exchange Limited (BSE) and National

Stock Exchange of India Limited (NSE).

Market Price Data and Performance in comparison BSE Sensex and NSE Nifty is not available as the Company's

shares are not listed.

Registrar and Transfer Agent: The Company has appointed Registrar and Transfer agent to handle the share transfer

work and to solve the complaints of Shareholders. Name, Address and telephone number of Registrar and Transfer

Agent is given hereunder:

M/s. Link Intime India Private Limited

Unit: Welspun Global Brands Limited

C-13, Pannalal Silk Mills Compound,

LBS Marg, Bhandup (West),

Mumbai - 400078

Tel : + 91- 22- 25946970

Email : [email protected]

Contact person: Mr. Joy Verghese/ Mr. Raghunath Poojary

15

WELSPUN GLOBAL BRANDS LTD.

16

2009-2010Annual Report

Share Transfer System:

Share Transfers in physical form can be lodged with Link Intime India Private Limited at the above mentioned

address. The transfer requests are normally processed within 15-20 days of receipt of the documents, if

documents are found in order. Shares under objection are returned within two weeks.

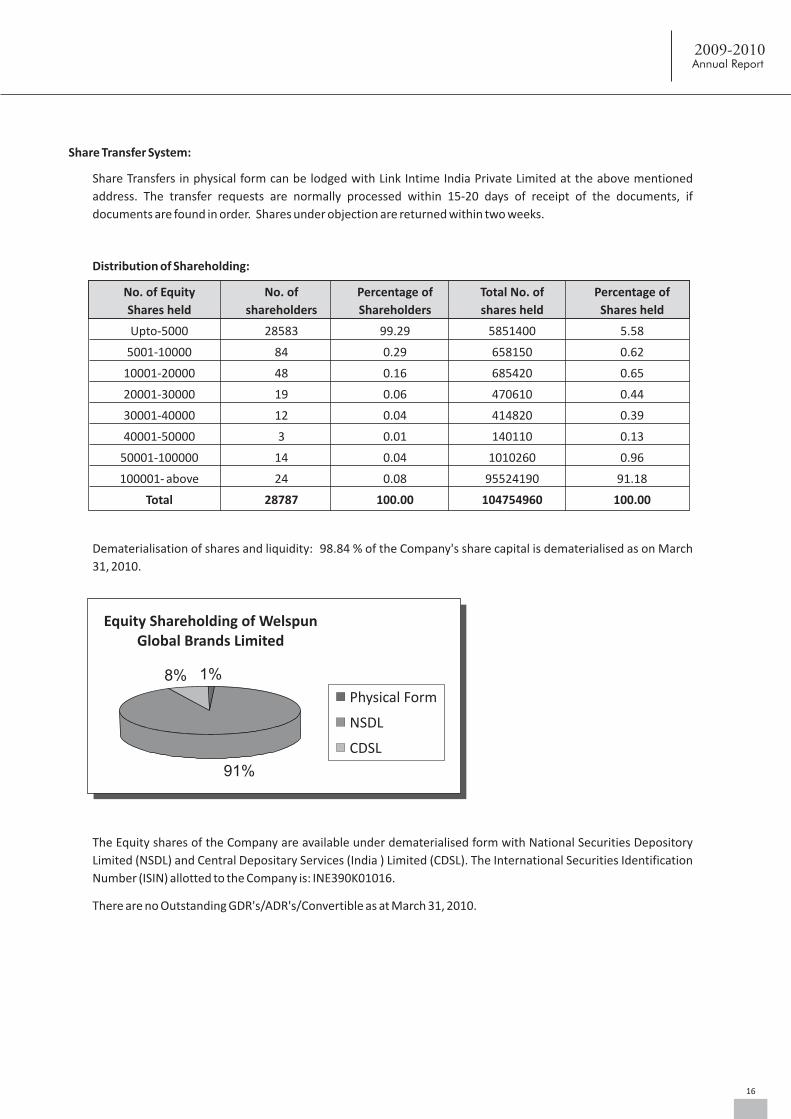

Distribution of Shareholding:

No. of Equity No. of Percentage of Total No. of Percentage of

Shares held shareholders Shareholders shares held Shares held

Upto-5000 28583 99.29 5851400 5.58

5001-10000 84 0.29 658150 0.62

10001-20000 48 0.16 685420 0.65

20001-30000 19 0.06 470610 0.44

30001-40000 12 0.04 414820 0.39

40001-50000 3 0.01 140110 0.13

50001-100000 14 0.04 1010260 0.96

100001- above 24 0.08 95524190 91.18

Total 28787 100.00 104754960 100.00

Dematerialisation of shares and liquidity: 98.84 % of the Company's share capital is dematerialised as on March

31, 2010.

The Equity shares of the Company are available under dematerialised form with National Securities Depository

Limited (NSDL) and Central Depositary Services (India ) Limited (CDSL). The International Securities Identification

Number (ISIN) allotted to the Company is: INE390K01016.

There are no Outstanding GDR's/ADR's/Convertible as at March 31, 2010.

1%

91%

8%

Physical Form

NSDL

CDSL

Equity Shareholding of Welspun Global Brands Limited

17

WELSPUN GLOBAL BRANDS LTD.

Address for correspondence:

Company Secretary

Welspun Global Brands Limited

Welspun House, 6th Floor,

Kamala City, Senapati Bapat Marg,

Lower Parel, Mumbai 400013

Tel: +91-22-24908000, +91-22-66136000

Fax: +91-22-24908020

E-mail : [email protected]

For and on behalf of the Board

May 27, 2010 B. K. Goenka

Mumbai Chairman

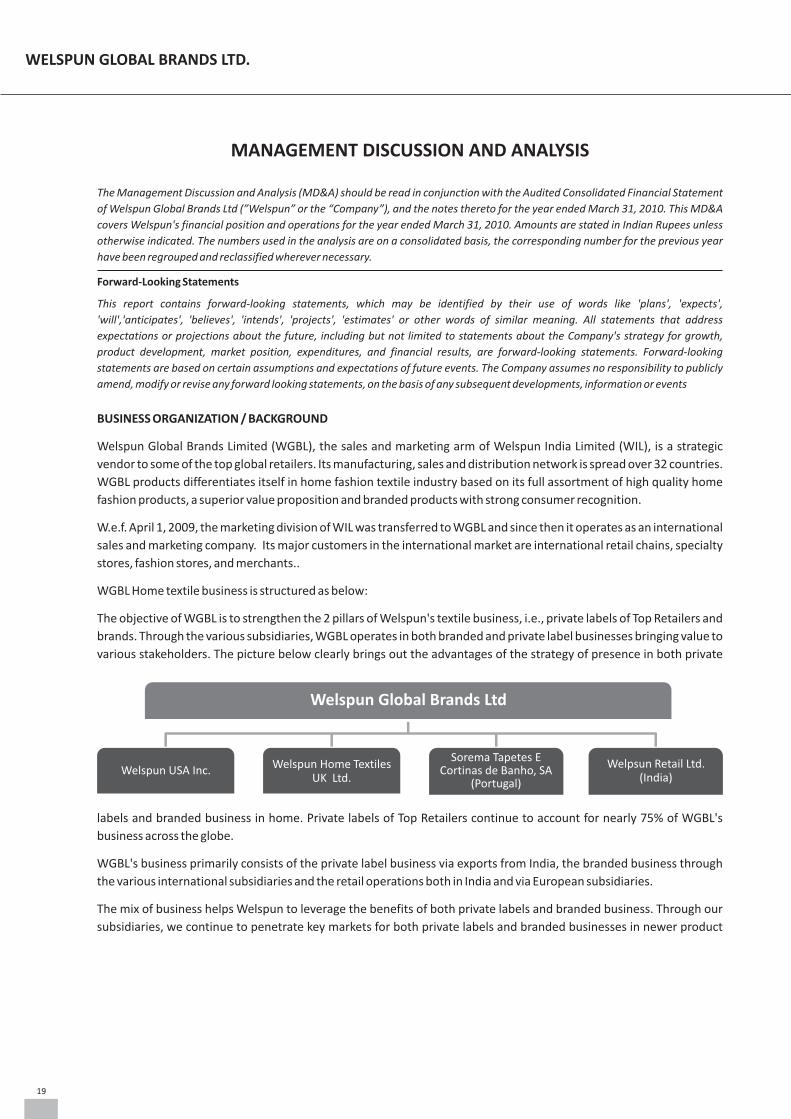

MANAGEMENT DISCUSSION AND ANALYSIS

The Management Discussion and Analysis (MD&A) should be read in conjunction with the Audited Consolidated Financial Statement

of Welspun Global Brands Ltd (”Welspun” or the “Company”), and the notes thereto for the year ended March 31, 2010. This MD&A

covers Welspun's financial position and operations for the year ended March 31, 2010. Amounts are stated in Indian Rupees unless

otherwise indicated. The numbers used in the analysis are on a consolidated basis, the corresponding number for the previous year

have been regrouped and reclassified wherever necessary.

Forward-Looking Statements

This report contains forward-looking statements, which may be identified by their use of words like 'plans', 'expects',

'will','anticipates', 'believes', 'intends', 'projects', 'estimates' or other words of similar meaning. All statements that address

expectations or projections about the future, including but not limited to statements about the Company's strategy for growth,

product development, market position, expenditures, and financial results, are forward-looking statements. Forward-looking

statements are based on certain assumptions and expectations of future events. The Company assumes no responsibility to publicly

amend, modify or revise any forward looking statements, on the basis of any subsequent developments, information or events

BUSINESS ORGANIZATION / BACKGROUND

Welspun Global Brands Limited (WGBL), the sales and marketing arm of Welspun India Limited (WIL), is a strategic

vendor to some of the top global retailers. Its manufacturing, sales and distribution network is spread over 32 countries.

WGBL products differentiates itself in home fashion textile industry based on its full assortment of high quality home

fashion products, a superior value proposition and branded products with strong consumer recognition.

W.e.f. April 1, 2009, the marketing division of WIL was transferred to WGBL and since then it operates as an international

sales and marketing company. Its major customers in the international market are international retail chains, specialty

stores, fashion stores, and merchants..

WGBL Home textile business is structured as below:

The objective of WGBL is to strengthen the 2 pillars of Welspun's textile business, i.e., private labels of Top Retailers and

brands. Through the various subsidiaries, WGBL operates in both branded and private label businesses bringing value to

various stakeholders. The picture below clearly brings out the advantages of the strategy of presence in both private

labels and branded business in home. Private labels of Top Retailers continue to account for nearly 75% of WGBL's

business across the globe.

WGBL's business primarily consists of the private label business via exports from India, the branded business through

the various international subsidiaries and the retail operations both in India and via European subsidiaries.

The mix of business helps Welspun to leverage the benefits of both private labels and branded business. Through our

subsidiaries, we continue to penetrate key markets for both private labels and branded businesses in newer product

Welspun Global Brands Ltd

Welspun USA Inc.Welspun Home Textiles

UK Ltd.

Sorema Tapetes E Cortinas de Banho, SA

(Portugal)

Welpsun Retail Ltd.(India)

19

WELSPUN GLOBAL BRANDS LTD.

categories.

GLOBAL ECONOMIC ENVIRONMENT

Post the economic downturn in 2009, the global economy is showing signs of revival. The various stimuli that were put

in place by governments are yielding results and the global GDP is expected to grow at 3.3% in 2010. This growth is

expected to drive increase in both private and government consumption levels. Consumption is expected to grow at

2.6% world-wide.

The key markets, i.e., the developed economies of USA, UK and Western Europe are expected to grow at 2.1% The US

market is expected to grow at 2.6% and 2.4% in 2010 and 2011 respectively, while the developing markets are expected

to grow at an average rate of 6.2%.What is encouraging is that world trade volume of goods and services is expected to

rise by 5.8% in 2010 after a fall of 12.9% in 2009. As a global company where majority of our revenues come from

international trade, this is a very positive development. These signs are further strengthened by the fact that 11 out of 1the 13 major retailers in the US reported positive like-for-like sales growth in June 2010. Post April 2010, both UK and

the Eurozone have also shown positive growth in like-for-like retail sales.

The overall positive macro-economic trends have resulted in rising per capita income, increased consumerism and

higher consumer spending. A large proportion of this higher consumer spending is towards textiles, apparel and

lifestyle products. The chief reason for this has been India's changing demographic profile. The disposable income in

India is also expected to increase significantly over the next decade. Welspun believes that the above factors strongly

suggest an ongoing structural shift in the demand pattern for textiles within the domestic markets. This indicates that

the textile industry is on the threshold of higher consumer demand and consequently higher growth.

India's economy is on the fulcrum of an ever-increasing growth curve. With positive indicators such as a stable 8-9

percent annual growth, rising foreign exchange reserves and rapidly expanding FDI inflows, India has emerged as the

second fastest growing major economy in the world after China.

GLOBAL TEXTILE MARKET - Demand & Supply scenario

The global economic crisis which began in 2008-09 continued to impact the global textile and apparel trade in 2009-10

as well, leading to lower growth rates. 2008-09 saw a worldwide drop in consumption due to consumers cutting back on 2discretionary spends impacting demand for textiles. In the last quarter of FY10, we have seen increasing demand at the

retail level, both domestically and internationally. This leads us to believe that the textile industry is on a path to

recovery. We expect the industry demand to stabilize and grow in the near future.

3Currently, the global textile and apparel trade is estimated to be over US$ 450 billion. The global market for textile trade

includes yarns, fabrics, apparel, and non-apparel finished products.

Post the expiry of the Agreement on Textiles and Clothing (ATC) in 2005, India's share of textile imports into the

Private Labels of Top Retailers

High volumes, ensurescapacity utilization at plants

Higher Margins

Market Presence

Direct Connect with end-use

Entry into new geographies

Brand Recall andRecognition

Strategic Partner/Preferred Vendor

Increased market shareacross geographies

1Source: Home Textiles Today.2Source: Technopak Perspective, Vol 3/ 2010.3Source: Fibre2fashion.com

20

2009-2010Annual Report

European Union and the United States of America has significantly increased. India is among the top 3 leading suppliers 4of bed and bath linen in the EU. India along with China and Pakistan are the top 3 suppliers of textiles globally.

The largest consumers of home textile products are Europe, the United States of America and Japan. In the last few

years, consumer wallet share of textiles has been declining leading to great demand in the value segment. In the last

quarter of 2009-10, we observed a cautious optimism in the consumer demand.

In 2009, there was severe price competition due to depressed demand. With the cotton and crude oil prices moving up,

we expect an increase in prices of finished goods. We do not expect any negative impact on demand for home textiles.

We are increasingly facing competition from lower cost destinations like Cambodia, Vietnam and Bangladesh, whose

shares in imports have been steadily increasing.

For the first 4 months of 2010, India's share in towels import into US is at 27% and sheets at 35%, making it the largest

supplier of towels and sheets into the US. Overall, China remains the largest supplier of home textiles into the US,

followed by India and Pakistan.

GLOBAL HOME TEXTILE INDUSTRY

The Home Textiles market includes:

1. Household textiles: Which includes rugs, bed linen, table linen, bathroom and kitchen linen

2. Furnishing textiles: Which includes curtains, bedspreads and other furnishing articles for home interiors

The global home textiles industry is estimated at US$ 70 billion (at the retail level) with US and EU together accounting 5for nearly 70% of the overall market. Home textiles are, in large part, a replenishment business. This creates the need

for a retailer to keep the same product in stock consistently, and requires a steady and consistent supply of products.

Earlier, quota restrictions inhibited foreign manufacturers from developing economies of scale and the logistics and

supply chain capabilities required to effectively service overseas replenishment demand. The removal of quotas in

January 2005 has resulted in the elimination of the advantages enjoyed by manufacturers in the United States and

improved the competitive position of overseas manufacturers.

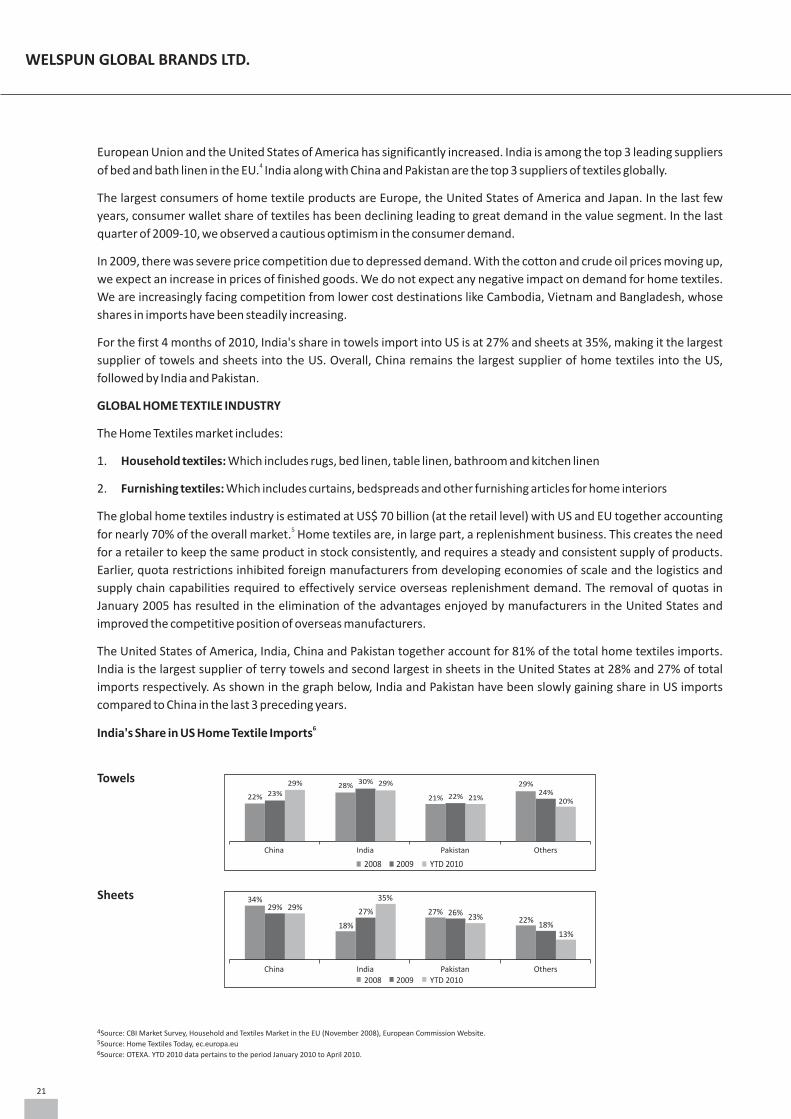

The United States of America, India, China and Pakistan together account for 81% of the total home textiles imports.

India is the largest supplier of terry towels and second largest in sheets in the United States at 28% and 27% of total

imports respectively. As shown in the graph below, India and Pakistan have been slowly gaining share in US imports

compared to China in the last 3 preceding years.

6India's Share in US Home Textile Imports

Towels

Sheets

4Source: CBI Market Survey, Household and Textiles Market in the EU (November 2008), European Commission Website. 5Source: Home Textiles Today, ec.europa.eu6Source: OTEXA. YTD 2010 data pertains to the period January 2010 to April 2010.

China India Pakistan Others

2008 2009 YTD 2010

22% 23%

29% 28%30% 29%

21% 22% 21%

29%24%

20%

China India Pakistan Others

2008 2009 YTD 2010

34%29% 29%

18%

27%

35%

27% 26%23% 22%

18%13%

21

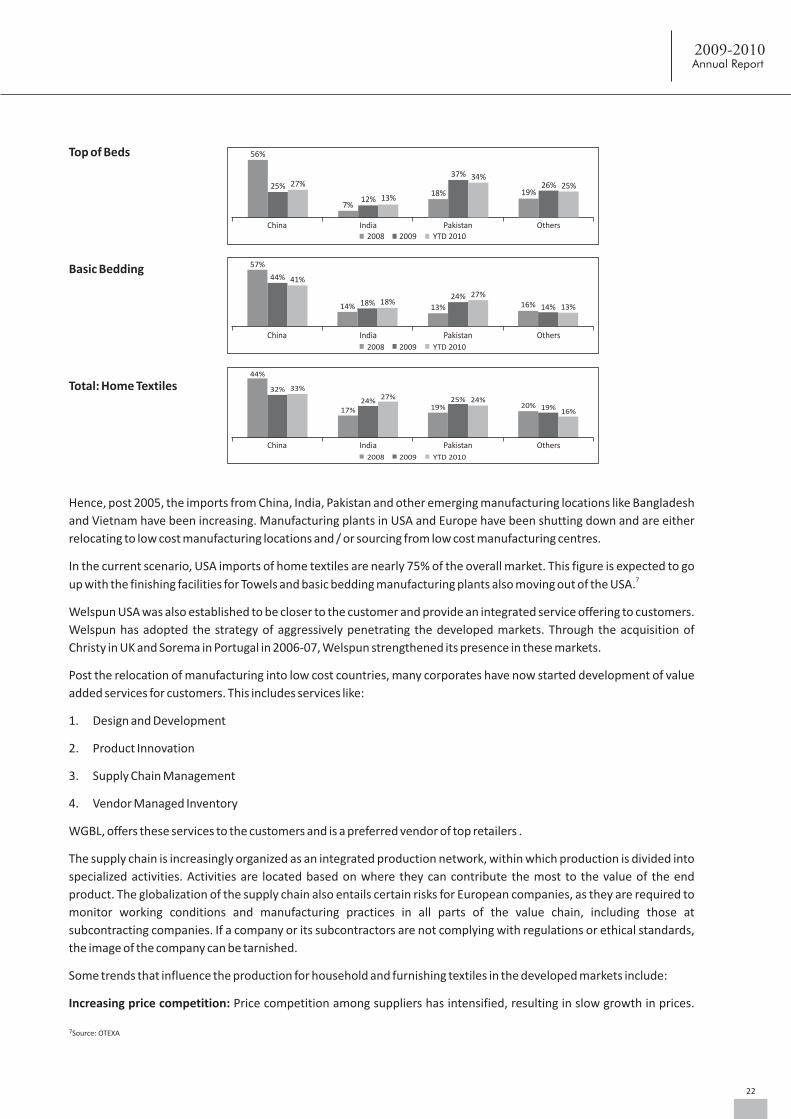

WELSPUN GLOBAL BRANDS LTD.

Top of Beds

Basic Bedding

Total: Home Textiles

Hence, post 2005, the imports from China, India, Pakistan and other emerging manufacturing locations like Bangladesh

and Vietnam have been increasing. Manufacturing plants in USA and Europe have been shutting down and are either

relocating to low cost manufacturing locations and / or sourcing from low cost manufacturing centres.

In the current scenario, USA imports of home textiles are nearly 75% of the overall market. This figure is expected to go 7up with the finishing facilities for Towels and basic bedding manufacturing plants also moving out of the USA.

Welspun USA was also established to be closer to the customer and provide an integrated service offering to customers.

Welspun has adopted the strategy of aggressively penetrating the developed markets. Through the acquisition of

Christy in UK and Sorema in Portugal in 2006-07, Welspun strengthened its presence in these markets.

Post the relocation of manufacturing into low cost countries, many corporates have now started development of value

added services for customers. This includes services like:

1. Design and Development

2. Product Innovation

3. Supply Chain Management

4. Vendor Managed Inventory

WGBL, offers these services to the customers and is a preferred vendor of top retailers .

The supply chain is increasingly organized as an integrated production network, within which production is divided into

specialized activities. Activities are located based on where they can contribute the most to the value of the end

product. The globalization of the supply chain also entails certain risks for European companies, as they are required to

monitor working conditions and manufacturing practices in all parts of the value chain, including those at

subcontracting companies. If a company or its subcontractors are not complying with regulations or ethical standards,

the image of the company can be tarnished.

Some trends that influence the production for household and furnishing textiles in the developed markets include:

Increasing price competition: Price competition among suppliers has intensified, resulting in slow growth in prices.

China India Pakistan Others

2008 2009 YTD 2010

56%

25% 27%

7%12% 13%

18%

37% 34%

19%26% 25%

China India Pakistan Others2008 2009 YTD 2010

57%

44% 41%

14% 18% 18%13%

24% 27%16% 14% 13%

44%

32% 33%

17%24%

27%

19%25% 24%

20% 19%16%

China India Pakistan Others

2008 2009 YTD 2010

7Source: OTEXA

22

2009-2010Annual Report

This is causing concern among producers in developed markets who are finding it increasingly difficult to match low

import prices.

Increasing internationalization: Textile manufacturing and retail companies are expanding their activities on a global

scale at a rapid pace and their products are available in many developed markets resulting in increased competitive

pressures.

High degree value chain integration: Several producers have opened their own chain(s) and many suppliers have

started a close and long-term co-operation with distribution channels, thereby increasing the entry barriers for new

suppliers.

Consolidation: The number of suppliers has decreased and many suppliers have merged or have taken over other

suppliers. This is resulting in greater economies of scale and value chain efficiencies, forcing their less competitive

counterparts out.

Specialization: Several manufacturers of home textiles have specialized in specific functions (such as design) or in

specific markets (such as the contract market), while other manufacturers have shifted from manufacturing for private

labels to introducing their own brands.

THE MARKET STRUCTURE

Consumers

A majority of purchases in the home textiles segment are made for replacement purposes and are discretionary in

nature. The purchase of home textiles, therefore, gets deferred during periods of economic slowdown and a

subsequent economic upturn tends to be steeper than the normal rate of consumption growth. Consumption patterns

of households vary substantially across geographies due to differences in culture, traditions and tastes. In the

household textiles sector, Welspun believes that brand awareness among consumers is limited, as can be derived from

the high market shares for interior department stores, Specialty chains and variety chains operating with their own

private label and textile discounters, while super and hyper markets sell unknown or fancy brand names.

Distribution channels

Importers purchase products from manufacturers abroad and we estimate that they generally add a 30-40% mark-up

to cover commissions, credit risk, after-sales service and the cost of carrying a local inventory to meet small orders. In

contrast to the agent, this importer holds his own stocks at his own risk.

Wholesalers cater to specialist shops as well as to department stores and home shopping companies. The wholesaler

also holds stocks at own risk. This non-importing distributor purchases from domestic manufacturers and importers.

The mark-up of wholesalers, Welspun estimates, is approximately 20-30%. Large retail companies are increasingly

purchasing abroad, thereby bypassing this intermediary.

DC Exporter

DomesticManufacturer/s

Sales Agents /Purchasing Agents

Importers

Wholesalers

RetailersDepartmental Stores, Furnishing Stores,

Speciality Stores, Value Retailers,Hyper/Super Market

23

WELSPUN GLOBAL BRANDS LTD.

Purchasing agents are widely used by retailers and wholesalers due to their wide network of contacts and knowledge of

foreign markets. They do not carry their own stock but purchase solely on the request of their customers.

Domestic manufacturers: The domestic manufacturers either import the raw material required for the finishing

operations or are primarily manufacturing products which are freight unfriendly or difficult to manage with long supply

chains. These manufacturers have the advantage of proximity to the source of raw material as well as the customer.

Sales agents are independent intermediaries between the (foreign) manufacturer and the retailer or retail

organization, receiving a commission from the former. The sales agent does not take title to the merchandise, but is

limited to presenting samples to potential clients, obtaining orders, and forwarding these to the exporter.

Retailers constitute the final stage before products reach the consumer. A criterion for dividing the market is the

composition of the total assortment: wholly or partly specialized in selling home textiles.

Being in the Private Label business of Top retailers also helps us generate value for the customer through our own

innovations. Welspun believes in investing in innovation as a key to remain ahead in business. Today, Welspun's

innovations are being looked at as growth drivers.

THE INDIAN TEXTILES INDUSTRY: An Overview

The textile industry plays a crucial role in the Indian economy. The size of the Indian textile industry is estimated at

approximately USD 60 billion. It contributes about 14 per cent to the industrial production of the country and 4% to the

GDP.

As regards employment, it is the second largest after agriculture, employing nearly 35 million people and accounting 20 8percent of the total workforce of the nation. Its contribution to forex earnings is around 17 per cent. Textiles sector has

been identified as one of the priority sectors having high growth potential and higher multiplier effects for employment

generation.

India occupies a prominent position in the global textile industry. It is the second largest producer of textiles in the

world, with China being the largest. India's competitive advantages are supplemented by the fact that it contributes 923.7% to global cotton production, being the second largest producer in the world. India is also the second largest

producer of man-made fiber, polyester and filament yarns in the world. India produces a large variety of textile products

based on natural fibers (cotton, wool and silk) as well as man-made fibers (polyester, viscose and acrylic). Of the above,

cotton accounts for a majority share of India's overall textile output.

India – A Manufacturing Destination

India has several inherent advantages, which lend it the potential and ability to emerge as a key global outsourcing hub

for textile products:

Self sufficiency of raw materials

9India has a vast pool of raw materials for textiles, both natural and man-made . Cotton textiles and clothing account for

approximately one-third of global textile trade. Three countries, China, India and US, account for approximately two

thirds of global cotton production. Further, India is a country which has surplus cotton production, as a result of its

increased productivity in the last few years. Other Asian countries such as China, Bangladesh, Pakistan, Thailand and

Indonesia are net importers of cotton. India's self sufficiency in cotton provides it with a strong competitive advantage

in global textile and clothing trade.

Labour Cost Advantage

On account of its vast population, India enjoys manufacturing cost competitiveness due to easy availability of low cost

skilled labor across different industries. The textile industry is no such exception whereby India's cost of production

ranks amongst the lowest in the world today.

9Source: USDA.

8Source: Ministry of Textiles, 2009-10 Annual Report.

24

2009-2010Annual Report

Design Skills and Value Addition Capabilities

Welspun believes that India has high value addition skills, which enable it to service niche markets worldwide.

This has been acknowledged by the world's leading global retailers.

Economies of Scale owing to a Huge Domestic Market

India is among the largest textile manufacturers and consumers in the world. The size of the domestic textile industry

has been estimated at USD 40 billion. This gives India a natural advantage of economies of scale, which enables it to

lower manufacturing overheads and improve operational efficiencies.

KEY TRENDS IN THE RETAIL SECTOR

Indian retail market is one of the fastest growing retail markets in the world. According to the BMI India Retail Report for

the third-quarter of 2010, on the back of Strong underlying economic growth, population expansion, the increasing

wealth of individuals and the rapid construction of organised retail infrastructure, total retail sales are expected to grow

from an estimated US$ $353 billion in 2010 to US$ 543.2 billion by 2014. With an ever-expanding middle and upper

class consumer base, there will also be huge opportunities in India's tier II and tier III cities. The greater availability of

personal credit and a growing vehicle population that provides improved mobility will also contribute to a trend

towards annual retail sales growth of approx 11-12%. (Source: BMI India Retail Report)

The growth in the overall retail market will be driven, in large part, by the explosion in the organized retail market.

Currently organized retail have a share of 5-6% (~US$ 21.2bn) of total sales and hence the opportunity for organized

retail in India remains immense. By 2014 the share of organized retail sales is expected to grow to 12-13% of the total

retail sales.

In 2009-10, the apparel sector witnessed a rebound in growth mainly during the last quarter of FY 2010. Improvement

in sales was mainly because of a continued switch to ready-to-wear branded garment and general higher consumer

spending sentiment. In addition, rentals have fallen around 25-30% from their peak in 2007-08. Lower rentals have

given more comfort to the expansion plans of organized retail and this is encouraging the apparel brands' store

expansion in retail operations. A vast majority of India's young population favors branded garments. With the influence

of electronic media, urban consumer trends have spread across the rural areas also. The shopping spree of the young

Indians for clothing, favorable income demographics, increasing population of young people joining the workforce with

considerably higher disposable income, has unleashed new possibilities for retail growth even in the rural areas. Thus,

85% of the retail boom which was focused only in the metros has started to infiltrate towards smaller cities and towns.

Tier-II cities are already receiving focused attention of retailers and the other smaller towns and even villages are likely

to join in the coming years. This is a positive trend, and the contribution of these tier-II cities to total organized retail

sales is expected to grow to 20-25%.

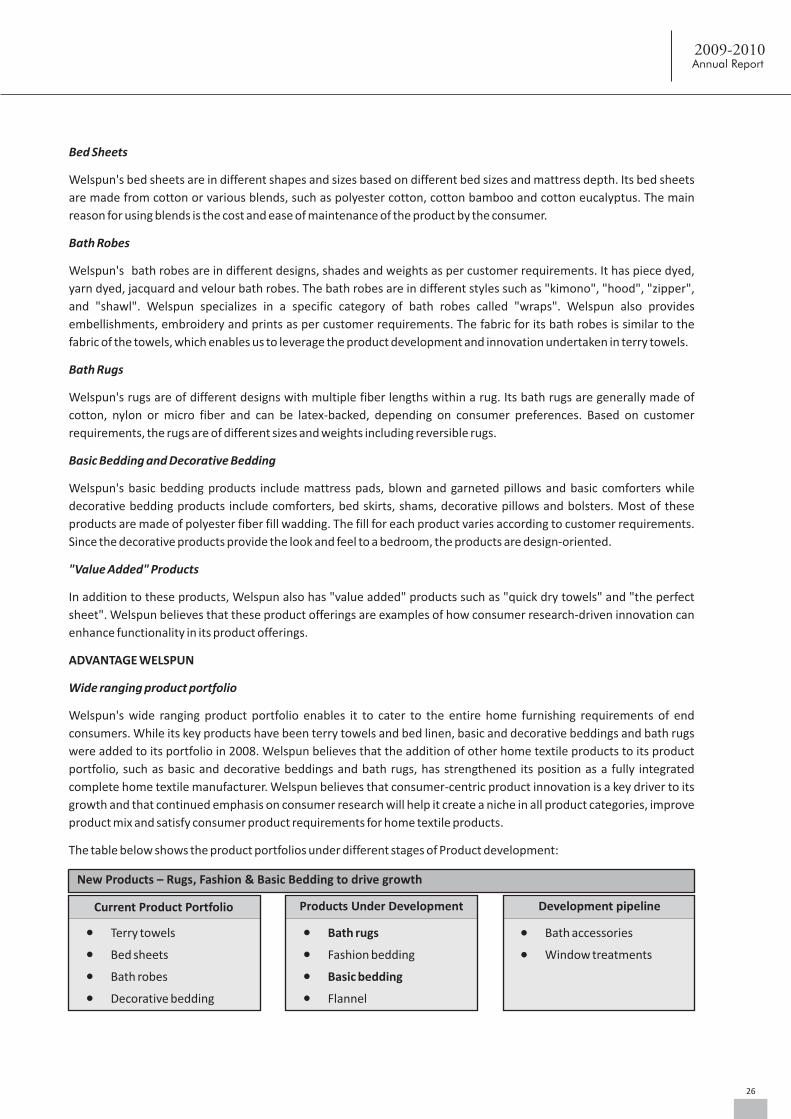

WELSPUN's PRODUCTS:

Welspun has a wide ranging portfolio of home textile products comprising terry towels, bed sheets, bath robes, bath

rugs, basic bedding and decorative bedding.

Terry Towels

Welspun's terry towels are in different shapes and sizes. Some of the towels are intended for use in a particular setting,

such as beach towels, or for a particular purpose, such as kitchen towels and baby hood towels, or in sizes convenient

for a special use, such as hand towels, face towels and bath sheets. Being woven out of 100% cotton yarn, these fabrics

acquire significant hygroscopic property, which is the prime reason for using terry fabrics in home textiles in general and

towels and bath robes in particular.

25

WELSPUN GLOBAL BRANDS LTD.

Bed Sheets

Welspun's bed sheets are in different shapes and sizes based on different bed sizes and mattress depth. Its bed sheets

are made from cotton or various blends, such as polyester cotton, cotton bamboo and cotton eucalyptus. The main

reason for using blends is the cost and ease of maintenance of the product by the consumer.

Bath Robes

Welspun's bath robes are in different designs, shades and weights as per customer requirements. It has piece dyed,

yarn dyed, jacquard and velour bath robes. The bath robes are in different styles such as "kimono", "hood", "zipper",

and "shawl". Welspun specializes in a specific category of bath robes called "wraps". Welspun also provides

embellishments, embroidery and prints as per customer requirements. The fabric for its bath robes is similar to the

fabric of the towels, which enables us to leverage the product development and innovation undertaken in terry towels.

Bath Rugs

Welspun's rugs are of different designs with multiple fiber lengths within a rug. Its bath rugs are generally made of

cotton, nylon or micro fiber and can be latex-backed, depending on consumer preferences. Based on customer

requirements, the rugs are of different sizes and weights including reversible rugs.

Basic Bedding and Decorative Bedding

Welspun's basic bedding products include mattress pads, blown and garneted pillows and basic comforters while

decorative bedding products include comforters, bed skirts, shams, decorative pillows and bolsters. Most of these

products are made of polyester fiber fill wadding. The fill for each product varies according to customer requirements.

Since the decorative products provide the look and feel to a bedroom, the products are design-oriented.

"Value Added" Products

In addition to these products, Welspun also has "value added" products such as "quick dry towels" and "the perfect

sheet". Welspun believes that these product offerings are examples of how consumer research-driven innovation can

enhance functionality in its product offerings.

ADVANTAGE WELSPUN

Wide ranging product portfolio

Welspun's wide ranging product portfolio enables it to cater to the entire home furnishing requirements of end

consumers. While its key products have been terry towels and bed linen, basic and decorative beddings and bath rugs

were added to its portfolio in 2008. Welspun believes that the addition of other home textile products to its product

portfolio, such as basic and decorative beddings and bath rugs, has strengthened its position as a fully integrated

complete home textile manufacturer. Welspun believes that consumer-centric product innovation is a key driver to its

growth and that continued emphasis on consumer research will help it create a niche in all product categories, improve

product mix and satisfy consumer product requirements for home textile products.

The table below shows the product portfolios under different stages of Product development:

Current Product Portfolio

New Products – Rugs, Fashion & Basic Bedding to drive growth

l Terry towels

l Bed sheets

l Bath robes

l Decorative bedding

Products Under Development

l Bath rugs

l Fashion bedding

l Basic bedding

l Flannel

Development pipeline

l Bath accessories

l Window treatments

26

2009-2010Annual Report

Focus on cost reduction

Welspun intends to retain its focus on improving manpower productivity and the synergies of its global operations with

the overall aim of reducing the cost of operations. Welspun also continues to strive to remove bottlenecks from its

operations to ensure smooth distribution of its products in the Home textile market globally.

Focus on quality

Welspun believes that as its products are sold in some of the most competitive markets globally, ensuring quality of

products is important to maintain competitive advantage. Welspun strives to continue to consistently supply high

quality products to meet the standards of its consumers. Welspun believes that its reputation for high quality products

will enable it to attain a leadership position in each of its product segments.

Global recognitions

Welspun USA (WUSA) is ranked 3rd amongst the Top 15 Home Textile Suppliers (Source: Home Textile Today (HTT) Top

15 Supplier Giants) with

Rank # 1: in Bath towels

Rank # 3: in Bed Sheets & Pillow cases

Rank # 5: in Comforters (Decorative Bedding)

Brand Sales providing growth

WGBL has a portfolio of Own Brands and Licensed Brands. While own brands like Hygrocotton, Luxus, Smart and

Eversmooth, Christy, Graccioza by Sorema are finding increasing customer recognition and acceptance, Licensed

Brands like Amy Butler and Waverly provide access to retailers

Retail Presence via 305 doors:

l WELHOME, India: 144

l Christy, U.K.: 71

l Sorema (Across Europe) : 90

New Channels to drive future growth

Geographic diversification

Welspun is increasing its Penetration in New Geographies and also strengthening presence outside USA & UK It has

setup a Sales Network set up in Europe, Dedicated Sales Team for South America, Canada. It is closely working with

Customers in China, Japan & Russia, China with Luolai, Japan with Yoshi for product development, and Russia with

Ecotex.

l Retailers

l Own retail operations

l Internet / websites

l Hospitality

l Small & Boutique

retailers

l Television: Home

shopping network

l Catalogues and

Mail orders

CURRENT CHANNELSCHANNELS UNDER

DEVELOPMENTDEVELOPMENT PIPELINE

27

WELSPUN GLOBAL BRANDS LTD.

Strategic Supply arrangement with WIL provides unique advantages:

l Strategically located manufacturing facilities of WIL

WIL has strategically located manufacturing facilities in Anjar and Vapi in Gujarat, India, close to its source of

cotton, the primary raw material for our products and to seaports on the western coast of India. Locating two of

WIL's manufacturing facilities in Gujarat provides us with a competitive advantage because India is the one of the

largest producers of cotton in the world and Gujarat is one of its major cotton-producing states. With cotton

accounting for the major portion of our cost of goods sold, WIL has been able to establish synergies between raw

material sourcing and its manufacturing facilities that allow it to achieve superior cost control and improved

margins.

l Economies of scale with modern manufacturing facilities of WIL

WIL modern manufacturing facilities also enable us to consistently supply high-quality products that exceed the

demands of our customers and end consumers. WIL manufacturing facilities at Vapi and Anjar operate in strict

accordance with ISO 9001:2008 certifications and our manufacturing facility at Vapi also operates in accordance

with ISO 14001:2004. Both of these certifications are by Intertek Systems Certification.

l Integration across the production chain under WIL

Welspun has integrated manufacturing facilities which allows it to undertake all of the production processes

(Spinning, weaving, processing, cut and sew, packing and logistics) involved in the manufacture of its products. This

helps us to exercise control over and to make profit from the major part of the value chain starting from the

procurement of cotton to the distribution of our products.

WELSPUN's STRATEGY

WGBL's Strategy is to be a “Brand and Marketing Company” for Home Textiles. It will focus on upgraded marketing,

product development and innovation, superior designs, additional distribution channels and its customer

service.Revenue growth by being partners with existing customers (top retailers) and improve profitability by

increasing own / licensed brands sales.

Further to this WGBL Strategy would be as under:

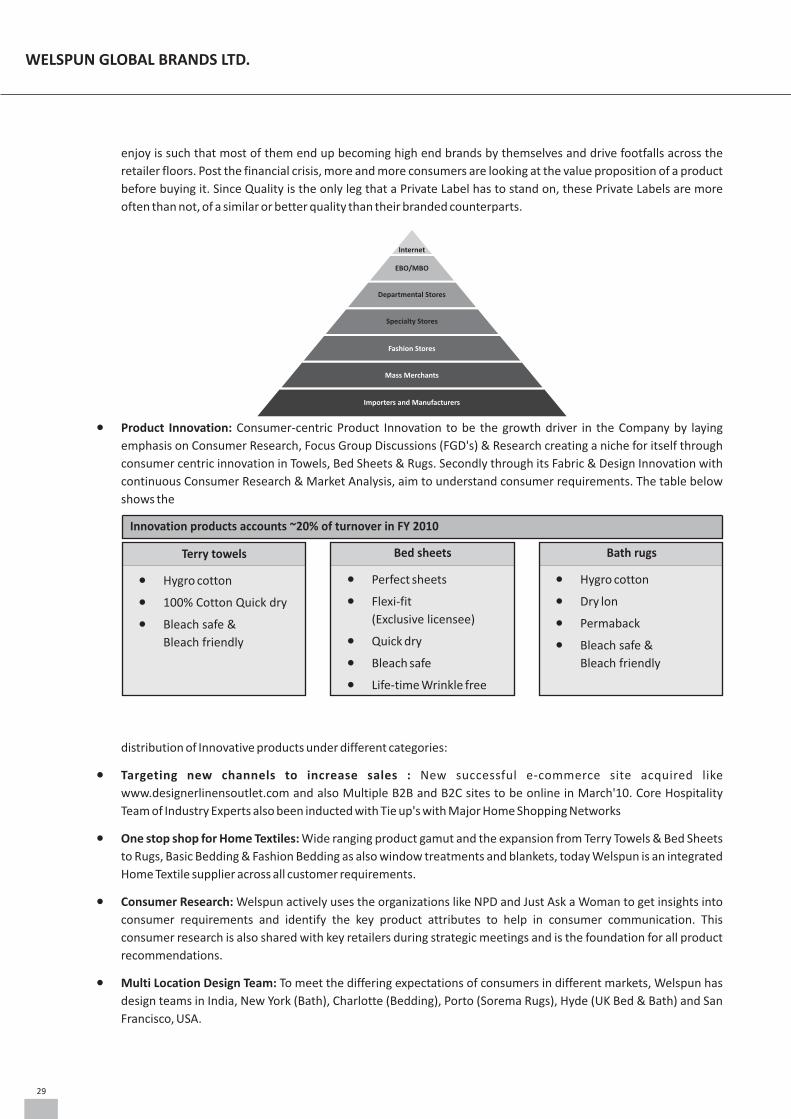

l Customer Centric approach: WGBL directly address its end customers through its owned and licensed brands,

which apart from being available at various top retailers around the world, are also made available through

Exclusive Brand Outlets or Shop-in-shops/ Concessionaires (SIS Format). Other than these channels, Welspun also

addresses its customers through the internet with channels such as the Designer Linens Outlet website. The

pyramid above tells us about the various different types of retailers that we reach our customers through. The top

two layers give us an opportunity to not only reach our end customers, but also get to understand what exactly

their needs are. Welspun aims to become a leader in Home Textiles across the globe, and that is why it believes

that Brands is the way to go. It is this belief that has led Welspun to acquire brands like Christy and Sorema and with

this Welspun continues with its approach towards a happy end customer. Welspun's India operations boast of a

strong network of Company and Franchisee owned outlets for its Home textiles brand like 'Welhome' and a wide

Shop-in-shop presence across the country for premium Home textiles brand 'Spaces'.

Apart from these channels, there are various other Mass merchants, Fashion Stores and Specialty Stores who help

to reach the customers through not only Welspun brands, but also through their own Private Label goods. Private

labels, also known as “store brands” or “house brands”, have long been associated with inexpensive name-brand

knockoffs. In recent years, however, retailers have begun marketing higher-quality products under their private

labels. The result has been a huge increase in the market share of private label brands. Of every $100 spent around

the world, $17 is spent on a private label. The private label industry is worth an estimated one trillion US dollars,

and its growth is outpacing that of manufacturer brands. The quality and loyalty that these Private Label brands

28

2009-2010Annual Report

enjoy is such that most of them end up becoming high end brands by themselves and drive footfalls across the

retailer floors. Post the financial crisis, more and more consumers are looking at the value proposition of a product

before buying it. Since Quality is the only leg that a Private Label has to stand on, these Private Labels are more

often than not, of a similar or better quality than their branded counterparts.

l Product Innovation: Consumer-centric Product Innovation to be the growth driver in the Company by laying

emphasis on Consumer Research, Focus Group Discussions (FGD's) & Research creating a niche for itself through

consumer centric innovation in Towels, Bed Sheets & Rugs. Secondly through its Fabric & Design Innovation with

continuous Consumer Research & Market Analysis, aim to understand consumer requirements. The table below

shows the

distribution of Innovative products under different categories:

l Targeting new channels to increase sales : New successful e-commerce site acquired like

www.designerlinensoutlet.com and also Multiple B2B and B2C sites to be online in March'10. Core Hospitality

Team of Industry Experts also been inducted with Tie up's with Major Home Shopping Networks

l One stop shop for Home Textiles: Wide ranging product gamut and the expansion from Terry Towels & Bed Sheets

to Rugs, Basic Bedding & Fashion Bedding as also window treatments and blankets, today Welspun is an integrated

Home Textile supplier across all customer requirements.

l Consumer Research: Welspun actively uses the organizations like NPD and Just Ask a Woman to get insights into

consumer requirements and identify the key product attributes to help in consumer communication. This

consumer research is also shared with key retailers during strategic meetings and is the foundation for all product

recommendations.

l Multi Location Design Team: To meet the differing expectations of consumers in different markets, Welspun has

design teams in India, New York (Bath), Charlotte (Bedding), Porto (Sorema Rugs), Hyde (UK Bed & Bath) and San

Francisco, USA.

Internet

EBO/MBO

Departmental Stores

Specialty Stores

Fashion Stores

Mass Merchants

Importers and Manufacturers

Terry towels

Innovation products accounts ~20% of turnover in FY 2010

l Hygro cotton

l 100% Cotton Quick dry

l Bleach safe &

Bleach friendly

Bed sheets

l Perfect sheets

l Flexi-fit

(Exclusive licensee)

l Quick dry

l Bleach safe

l Life-time Wrinkle free

Bath rugs

l Hygro cotton

l Dry lon

l Permaback

l Bleach safe &

Bleach friendly

29

WELSPUN GLOBAL BRANDS LTD.

l Product Development and Innovation: Welspun believes that Product Development & Innovation is a key area to

create a sustainable competitive advantage. Using the inputs from the consumer research and through tracking

the new developments, we have added new towel products like nanospun, eco-lite (quick dry), cotton bamboo,

eucalyptus and texture towels to our product basket.

On the Bed Linen front, we have added products like Ever Smooth MXL Wrinkle Free, Quick Dry Sheets, Flexifit

sheets and the Perfect Sheet incorporating all the qualities mentioned.

l Packaging and Point Of Sale: Welspun has a Marketing team in USA at Charlotte and in India which works on

developing the packaging for different products. POS communication is also developed in order to ensure that the

key functional product attributes are communicated to the consumer at the retail floor.

l Extended SCM: Welspun is among the few companies who provide Collaborative Forecasting, Planning and

Replenishment to its customers over more than 30 programs from POS to production at plant level.

l Global Market intelligence: Welspun has presence at multiple locations across the world and uses this presence to

build the market intelligence for different markets. In addition to this, secondary research using published Industry

sources helps to build the market intelligence.

l Technology: Along with WIL, WGBL offers State-of-the art technology, machinery know-how from the best

international suppliers and vertically integrated plants give Welspun a very strong footprint in this particular

industry. Welspun is flexible, change oriented and innovative.

l Reliability: A strong client base and a great track record in terms of client servicing and on time delivery is our key

strength.

l Projected growth of textile industry: The exponential growth anticipated in the textile industry gives a great

futuristic hope for companies like us who have implemented process and technology of global standards and are

ready to meet future demands.

WELSPUN'S EFFORTS TO SHARPEN COMPETITIVE EDGE

In 2010-11, Welspun plans to:

l Grow its market share of Towels in USA and UK

l Improve its market share of Bed Linen in all Markets

l Enhance Product design and development

l Utilize the Sales Network set up in Europe to increase sales across all product categories

l Acquire/ License Brands across the major markets

l Increase revenues in Fashion Bedding, Basic Bedding and Bath Rugs

l Develop new Markets like Mexico, Japan, Russia and China

l Consumer Research and product development

l Innovative products share to further increase total revenue.

l Seamless sourcing relation with WIL to cater to the customers across the globe

l Grow capability for Hospitality sector

Developing a Competitive Advantage

l Offering a Business Proposition

30

2009-2010Annual Report

– Be a strategic partner to Customers

l Sharing of Common Objective with Customer

– Maximize inventory turns

– Optimize ROI for Customer & Welspun

l Integration

– Supply Chain Integration with Client data base

l Quick response through USA distribution

PRINCIPAL FACTORS AFFECTING RESULTS OF OPERATIONS

l General economic conditions;

l Condition and performance of Indian and international textile industry;

l Price and availability of raw materials;

l Demand and supply of products;

l Foreign exchange fluctuations

l Competition.

HUMAN RESOURCES POLICY

Our HR policies cover our objectives, eligibility and coverage, policy and procedures. We review, revise and update our

Human Resource policies from time to time to make them relevant, effective and useful to its employees.

OUTLOOK

Welspun is already a strategic vendor to major retailers in the USA. It has been able to sustain its growth even in the

current economic scenario where the retail sales in its key market of US dropped since Sept'08. As a result of reduced

consumer spending, the retailers also corrected the inventory in the entire supply chain leading to low orders.

In 2008-09, Welspun USA signed a License for a leading brand for North America for Fashion Bedding, Fashion Bath,

Blankets/ Throws and Area Rugs in addition to the earlier license of Bath, Solid Sheets and rugs. The new license has

helped Welspun in becoming a key player in the Fashion Bedding segment.

Welspun today differentiates itself from the other manufacturers by focusing on Consumer Research driven

innovations, use of new technologies, a global manufacturing & sales footprint and ability to offer a comprehensive end

to end solution to the customers. A recent example of a consumer research driven innovation has been the Quick Dry

Towel and the Perfect Sheet.

Welspun occupies a strong market positioning with its customer partnership and brand sales. Going forward we target

to enhance our market share. With Improvement in consumer sentiments in North America and Europe demand

outlook is positive.

31

WELSPUN GLOBAL BRANDS LTD.

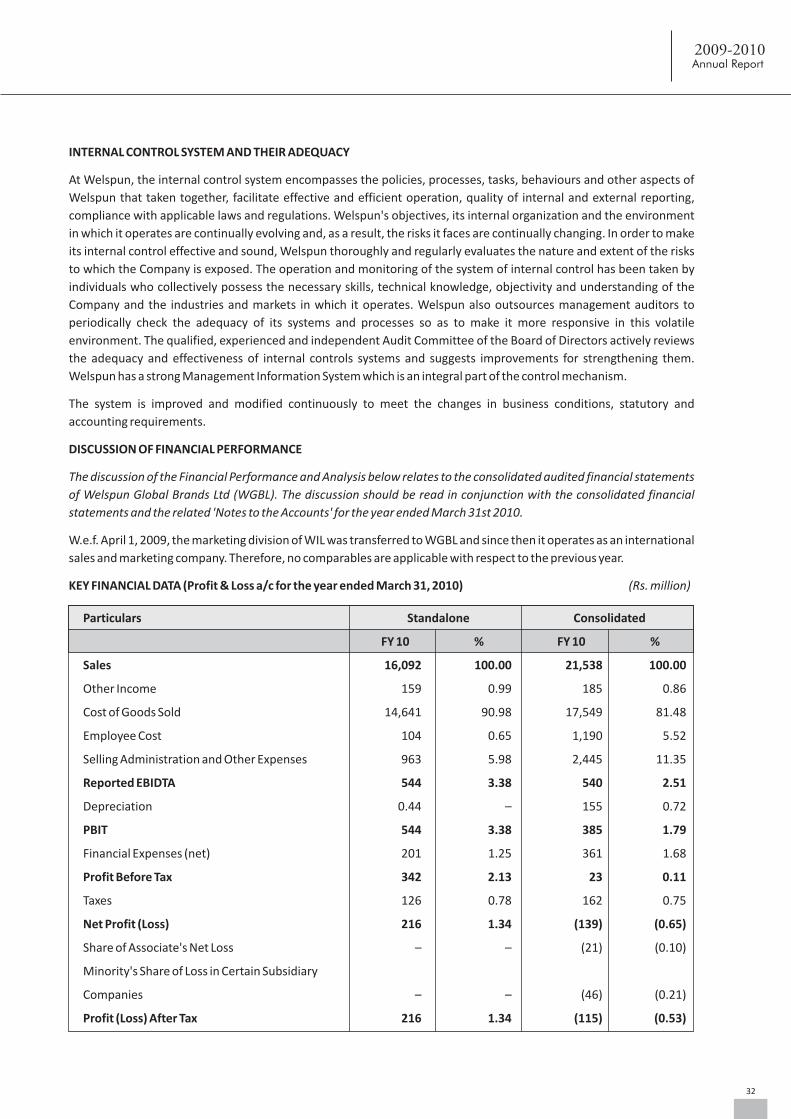

INTERNAL CONTROL SYSTEM AND THEIR ADEQUACY

At Welspun, the internal control system encompasses the policies, processes, tasks, behaviours and other aspects of

Welspun that taken together, facilitate effective and efficient operation, quality of internal and external reporting,

compliance with applicable laws and regulations. Welspun's objectives, its internal organization and the environment

in which it operates are continually evolving and, as a result, the risks it faces are continually changing. In order to make

its internal control effective and sound, Welspun thoroughly and regularly evaluates the nature and extent of the risks

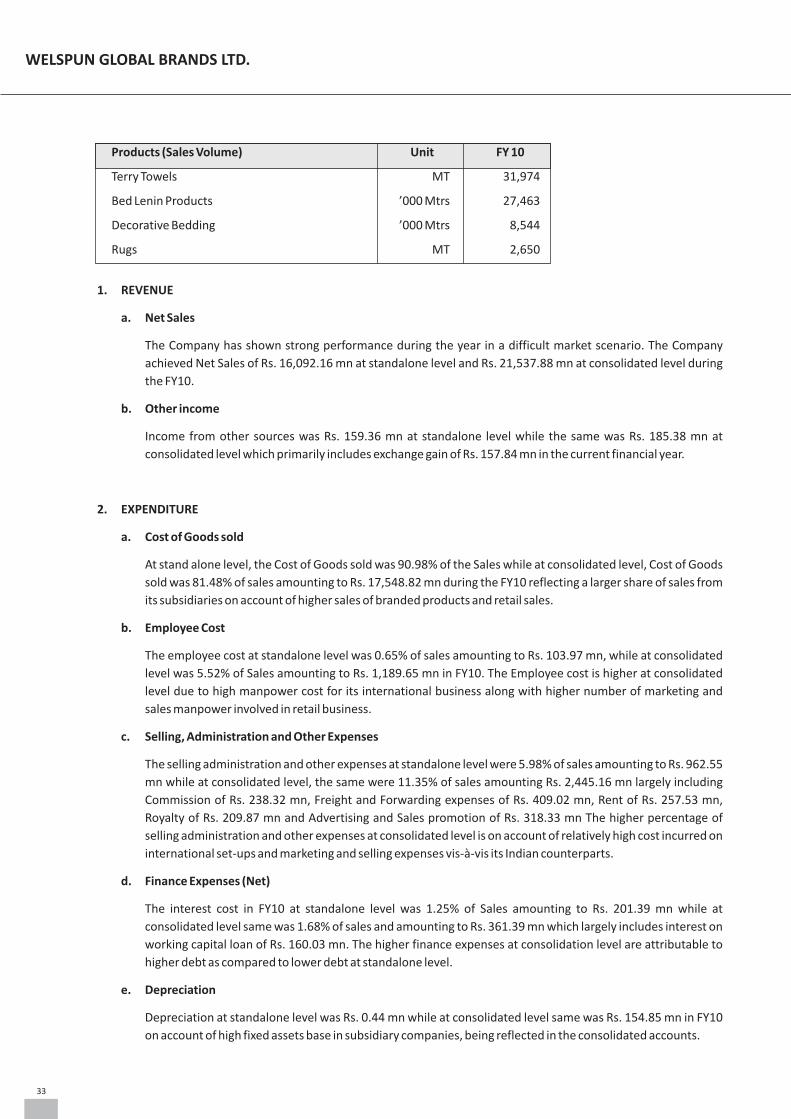

to which the Company is exposed. The operation and monitoring of the system of internal control has been taken by