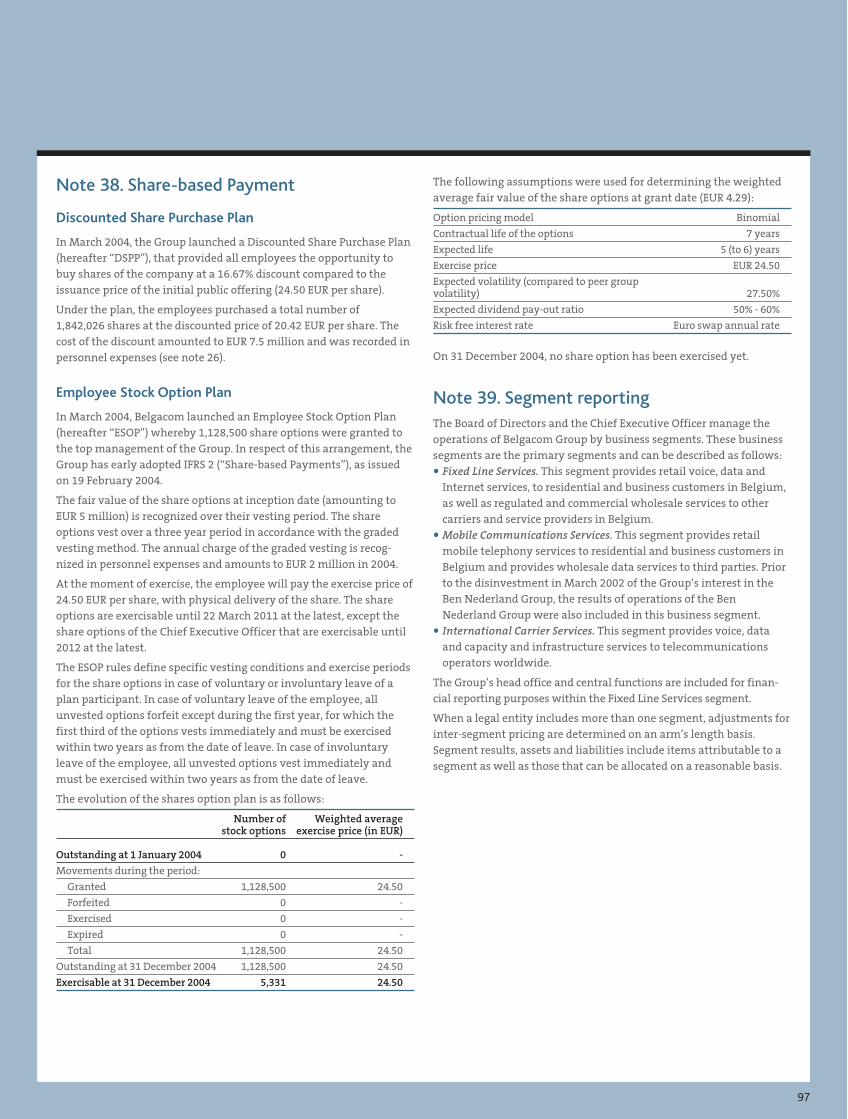

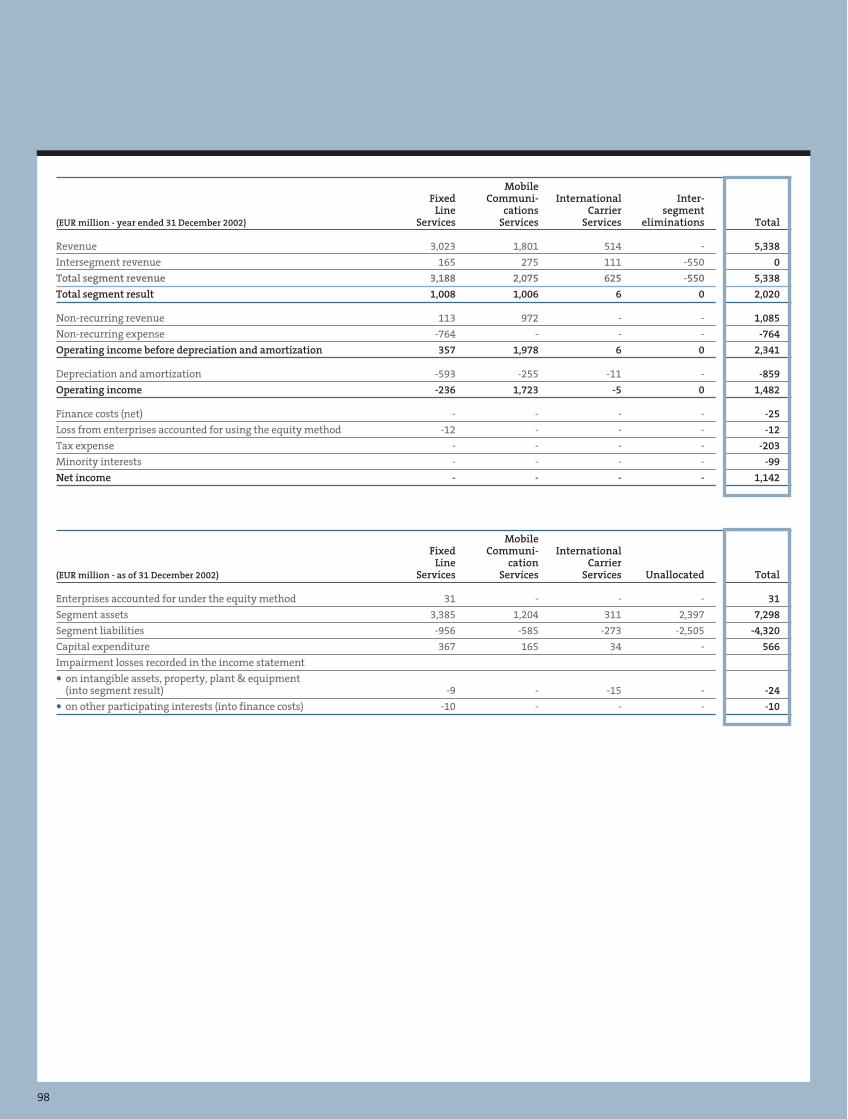

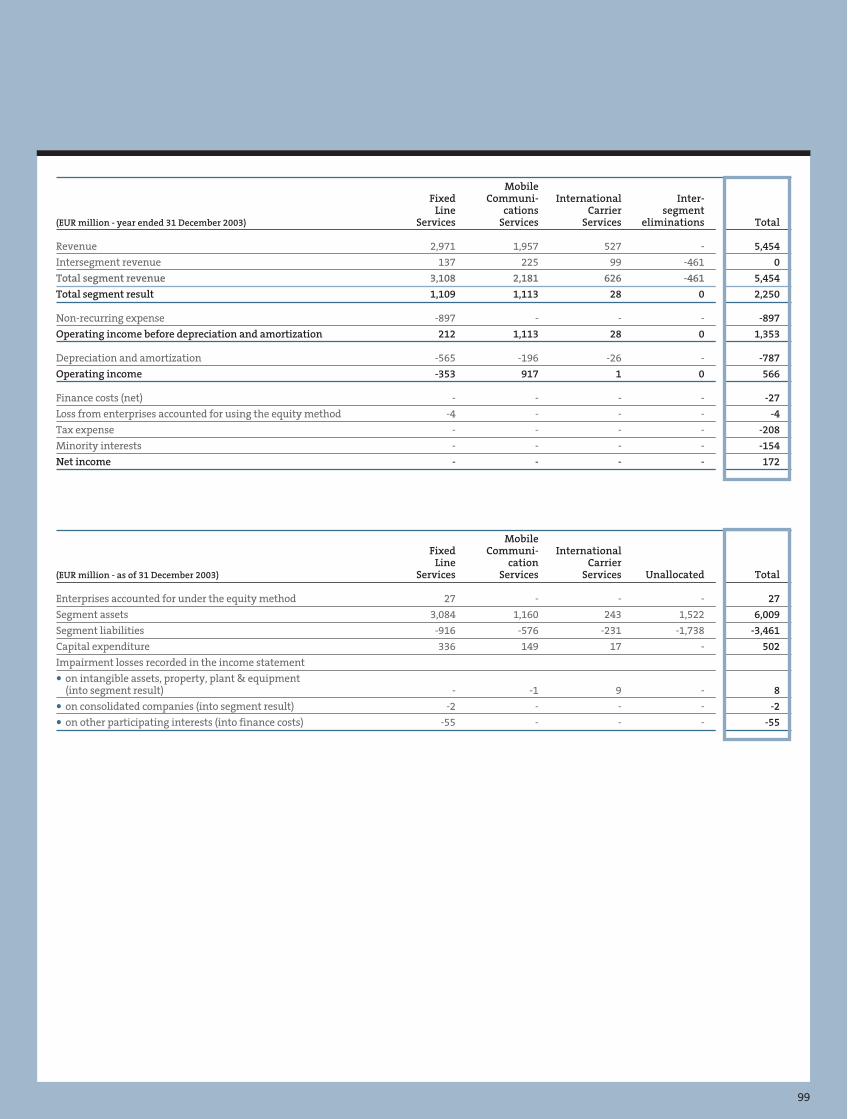

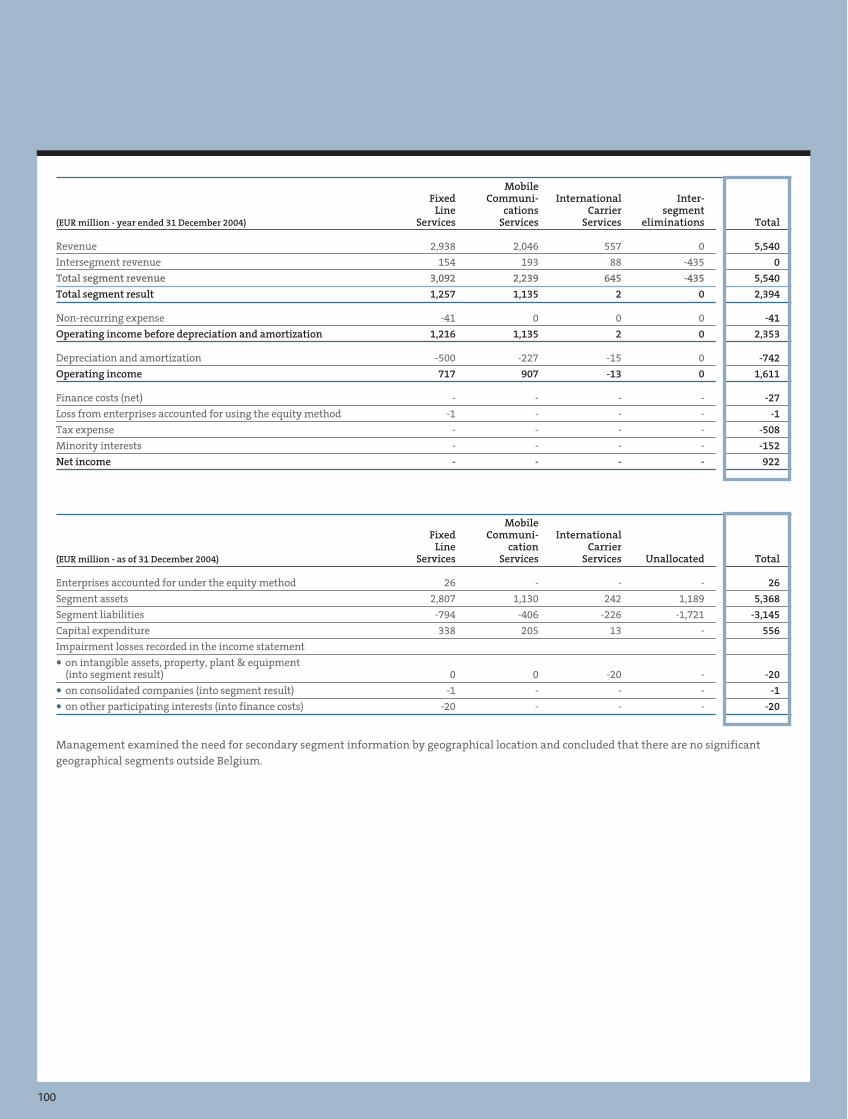

Embed Size (px)

DESCRIPTION

The complete annual report 2004 of the Belgacom Group.

Citation preview

Belg

aco

m

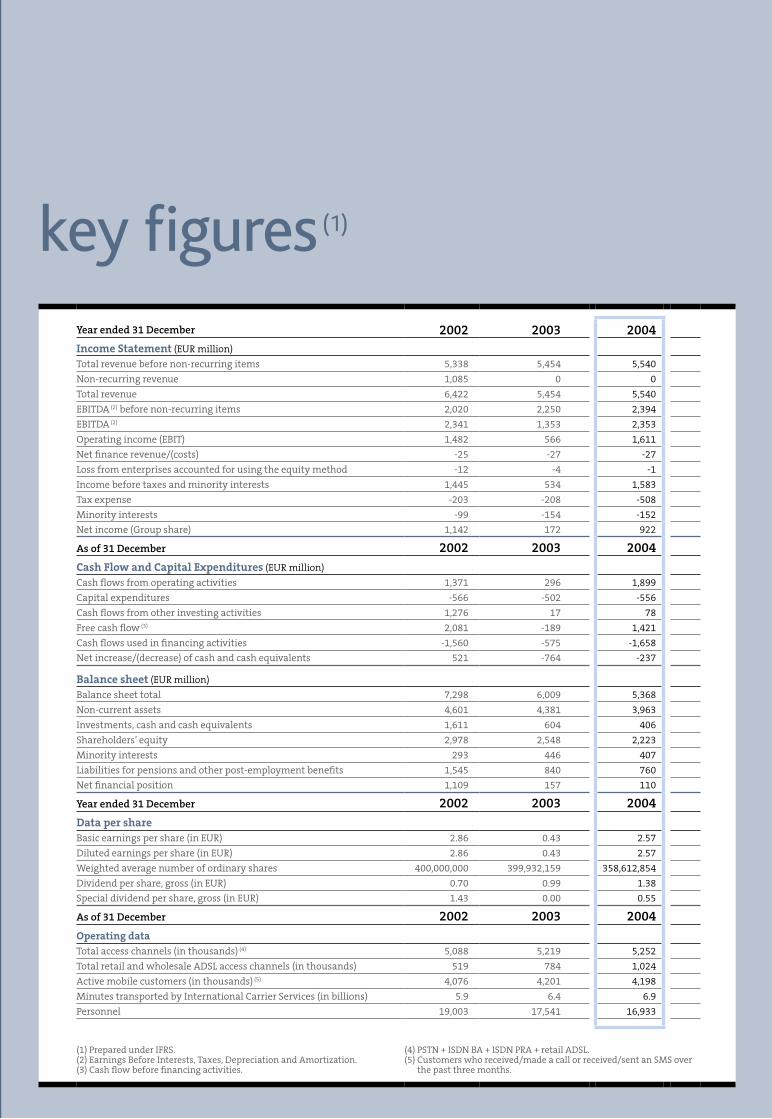

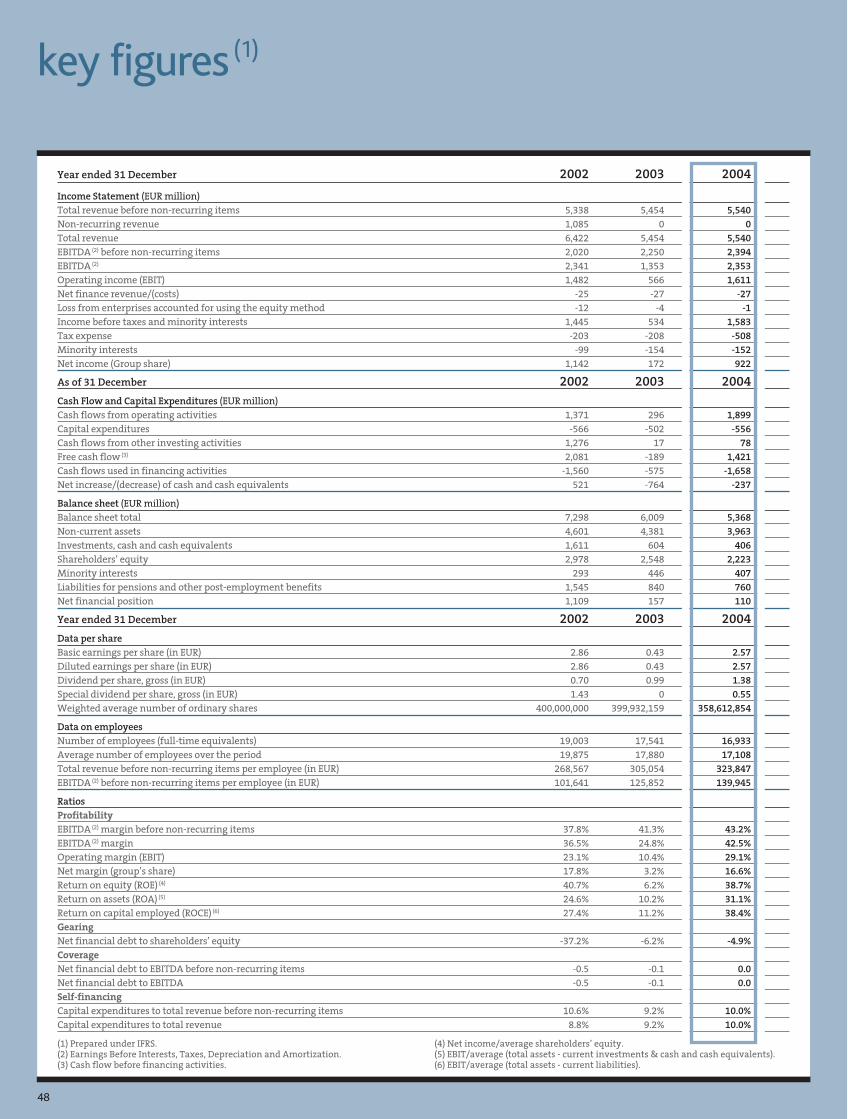

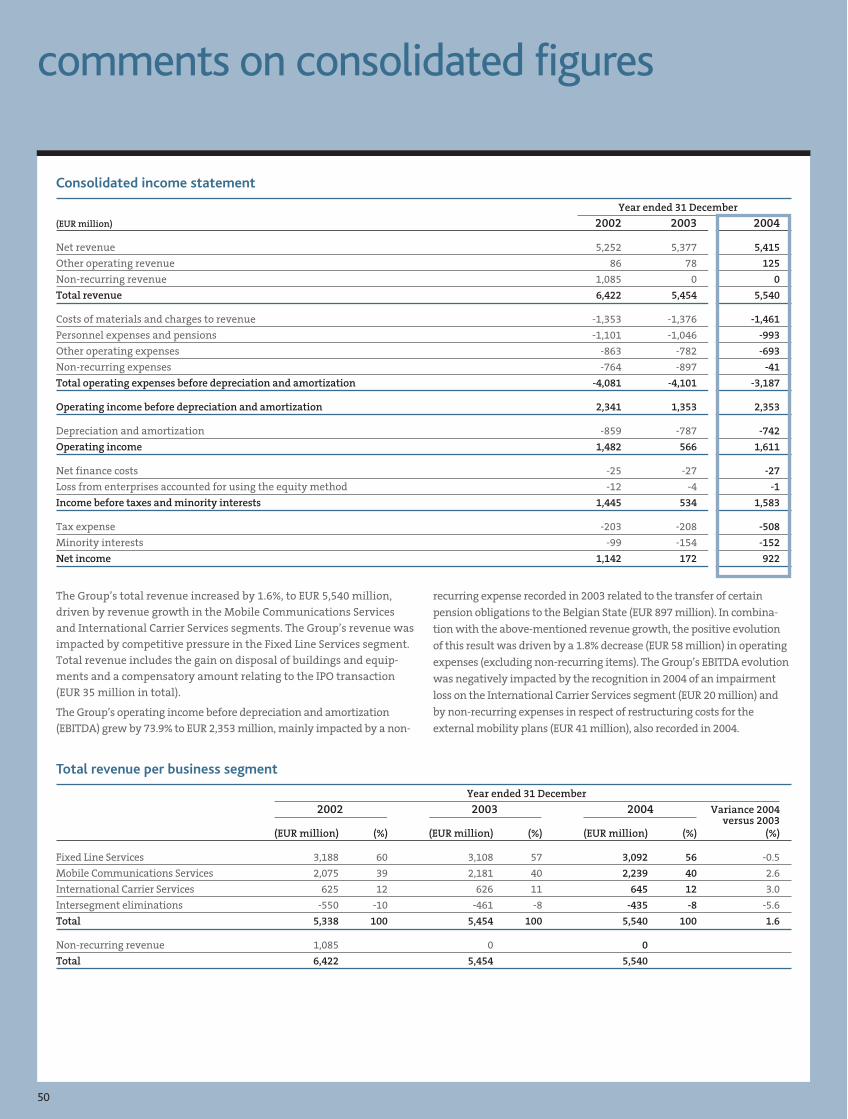

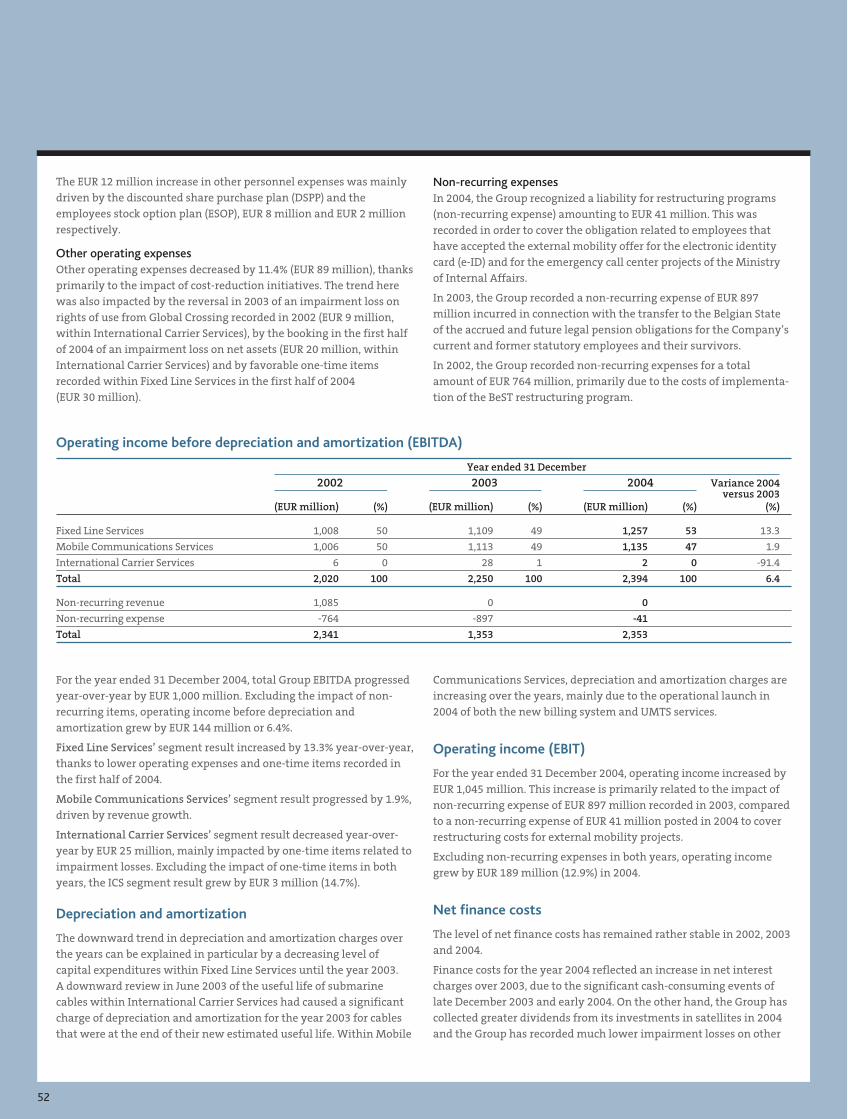

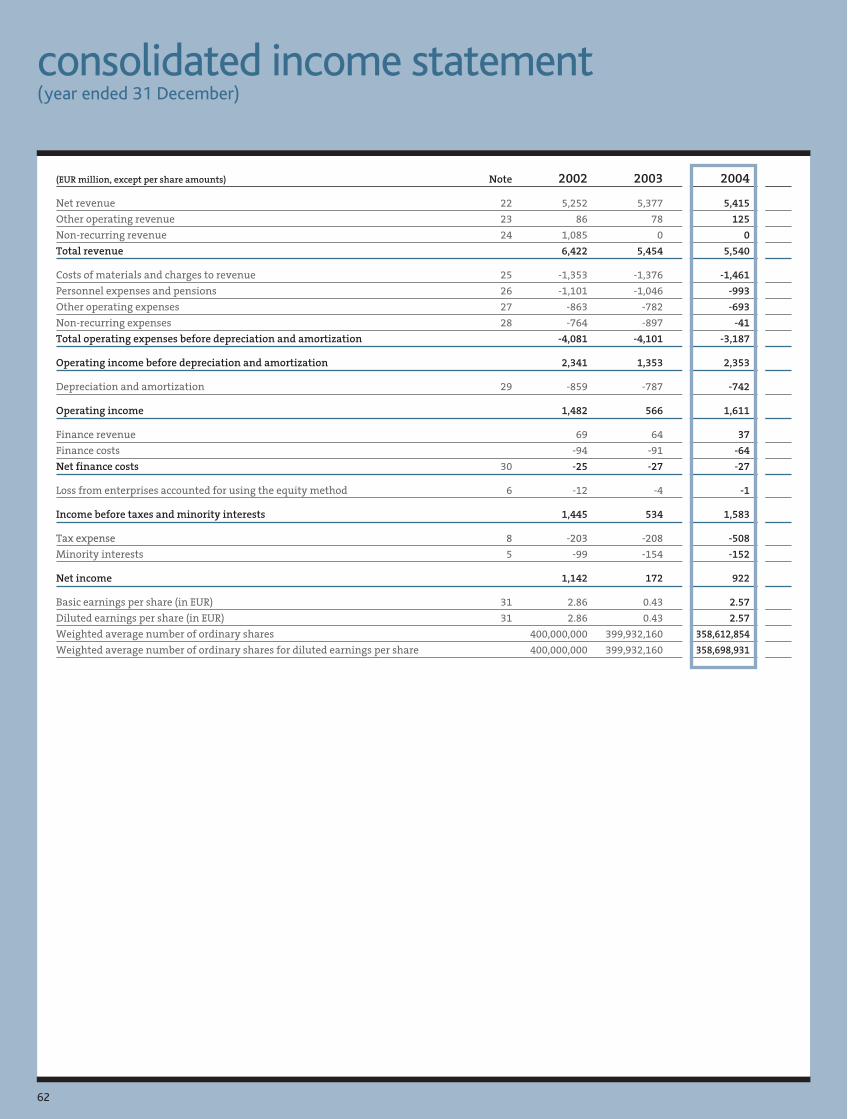

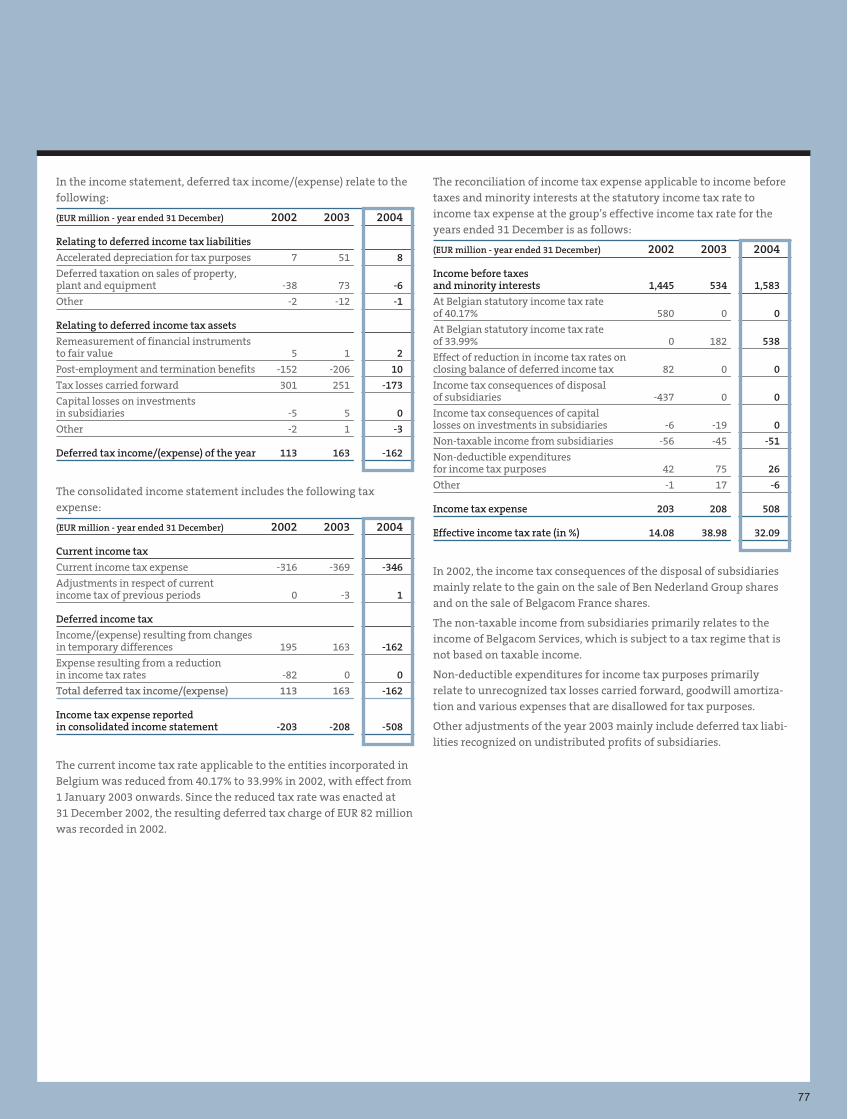

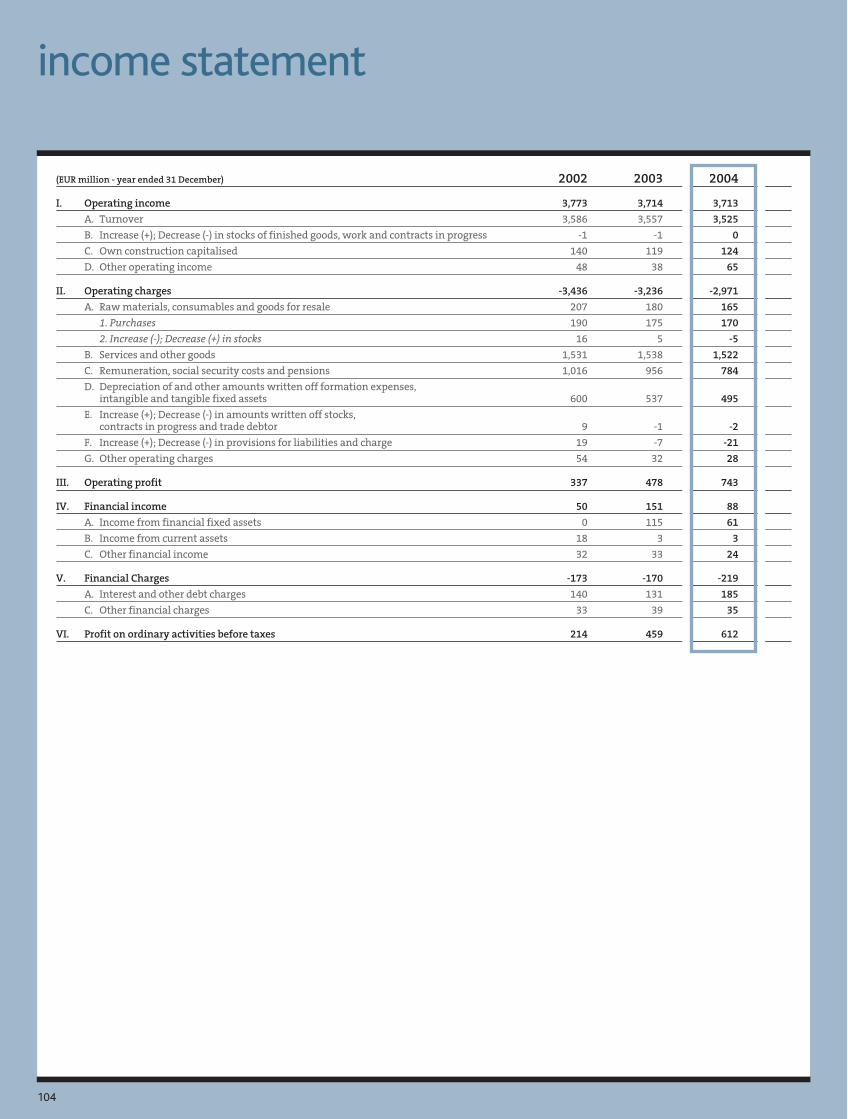

Year ended 31 December 2002 2003 2004Income Statement (EUR million)

Total revenue before non-recurring items 5,338 5,454 5,540

Non-recurring revenue 1,085 0 0

Total revenue 6,422 5,454 5,540

EBITDA (2) before non-recurring items 2,020 2,250 2,394

EBITDA (2) 2,341 1,353 2,353

Operating income (EBIT) 1,482 566 1,611

Net finance revenue/(costs) -25 -27 -27

Loss from enterprises accounted for using the equity method -12 -4 -1

Income before taxes and minority interests 1,445 534 1,583

Tax expense -203 -208 -508

Minority interests -99 -154 -152

Net income (Group share) 1,142 172 922

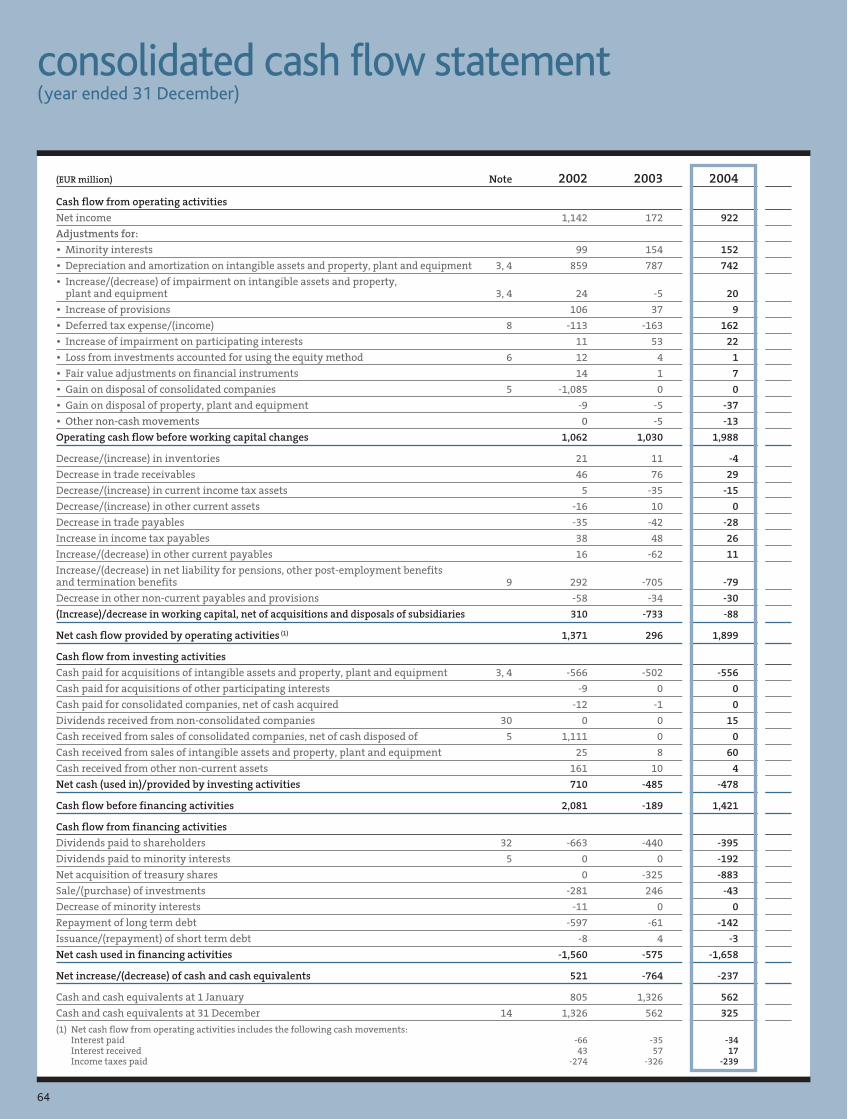

As of 31 December 2002 2003 2004Cash Flow and Capital Expenditures (EUR million)

Cash flows from operating activities 1,371 296 1,899

Capital expenditures -566 -502 -556

Cash flows from other investing activities 1,276 17 78

Free cash flow (3) 2,081 -189 1,421

Cash flows used in financing activities -1,560 -575 -1,658

Net increase/(decrease) of cash and cash equivalents 521 -764 -237

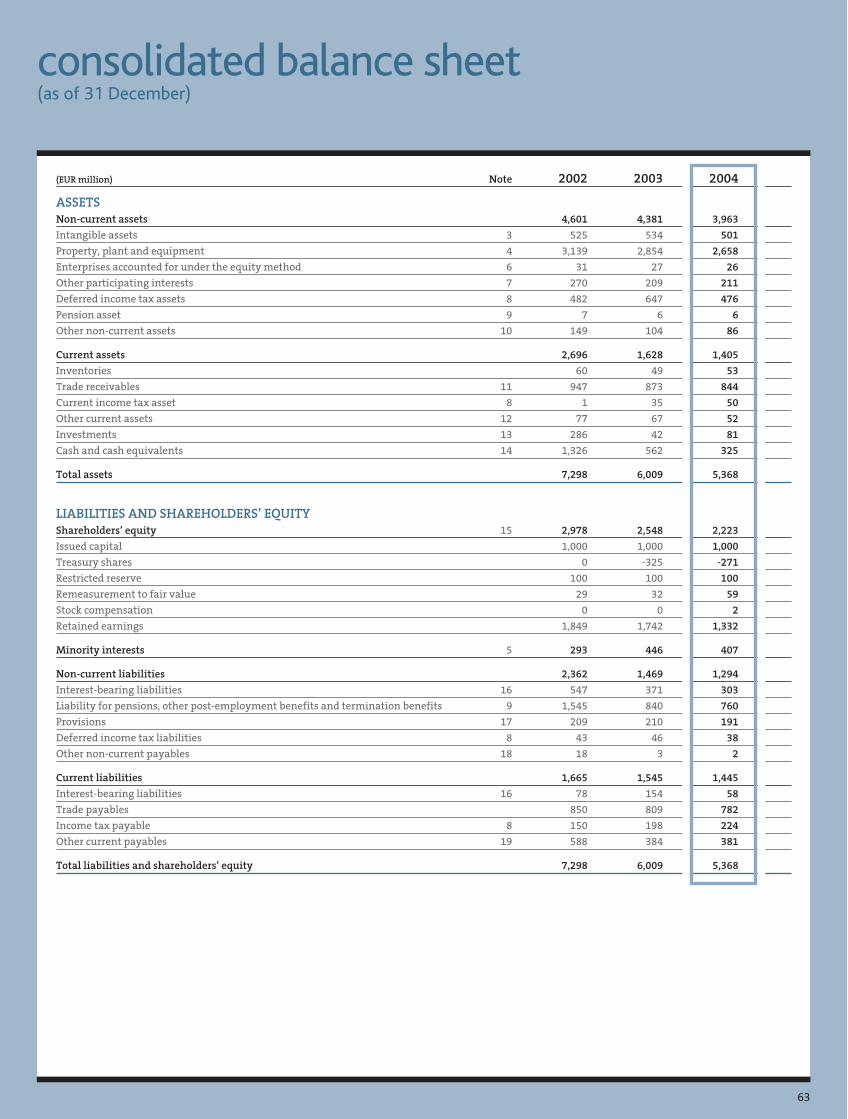

Balance sheet (EUR million)

Balance sheet total 7,298 6,009 5,368

Non-current assets 4,601 4,381 3,963

Investments, cash and cash equivalents 1,611 604 406

Shareholders’ equity 2,978 2,548 2,223

Minority interests 293 446 407

Liabilities for pensions and other post-employment benefits 1,545 840 760

Net financial position 1,109 157 110

Year ended 31 December 2002 2003 2004Data per shareBasic earnings per share (in EUR) 2.86 0.43 2.57

Diluted earnings per share (in EUR) 2.86 0.43 2.57

Weighted average number of ordinary shares 400,000,000 399,932,159 358,612,854

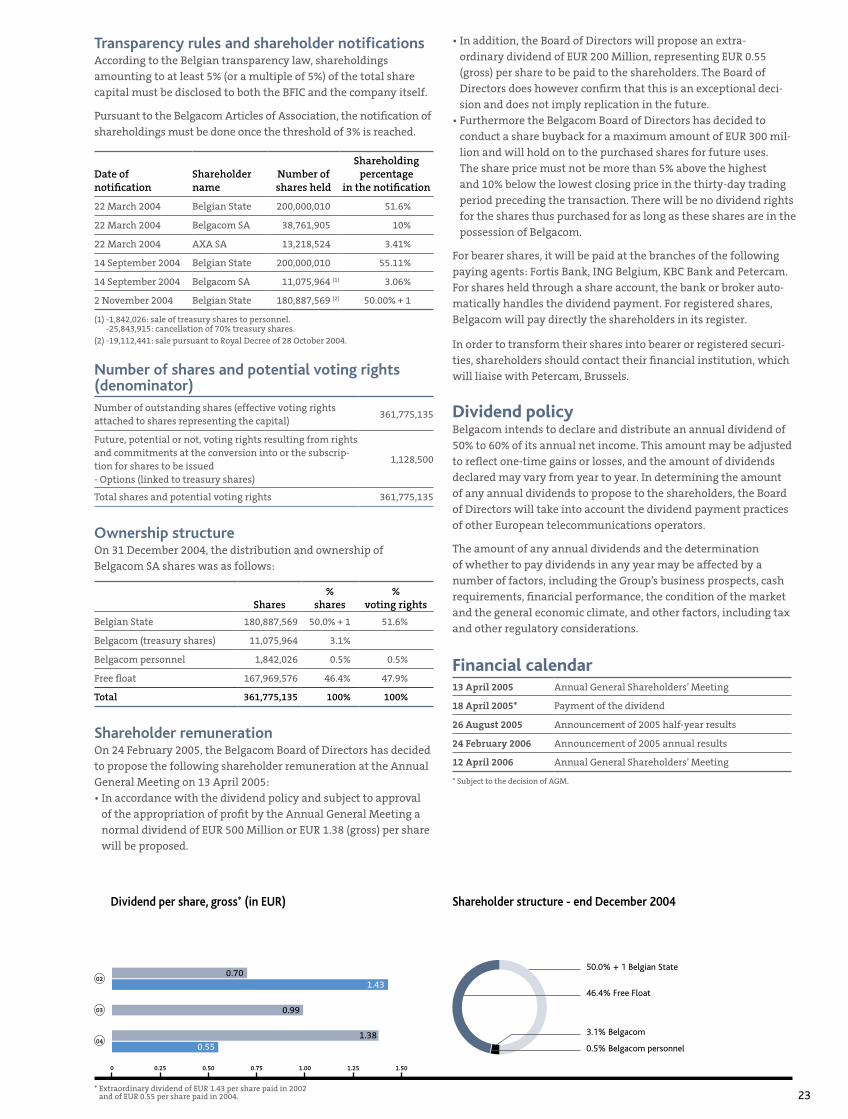

Dividend per share, gross (in EUR) 0.70 0.99 1.38

Special dividend per share, gross (in EUR) 1.43 0.00 0.55

As of 31 December 2002 2003 2004Operating dataTotal access channels (in thousands) (4) 5,088 5,219 5,252

Total retail and wholesale ADSL access channels (in thousands) 519 784 1,024

Active mobile customers (in thousands) (5) 4,076 4,201 4,198

Minutes transported by International Carrier Services (in billions) 5.9 6.4 6.9

Personnel 19,003 17,541 16,933

(1) Prepared under IFRS.(2) Earnings Before Interests, Taxes, Depreciation and Amortization.(3) Cash flow before financing activities.

(4) PSTN + ISDN BA + ISDN PRA + retail ADSL.(5) Customers who received/made a call or received/sent an SMS over

the past three months.a n n u a l r e p o r t • 2 0 0 4

The commitment of a leader. The spirit of a challenger.

key figures (1)

glossary

ADSL (Asymmetric Digital Subscriber Line): technology enabling a one-to-one, high-speed, digital connection (up to eight megabits per second (Mbps) in receive mode and 640 Kilobits per second (Kbps) in send mode) on a single pair of copper wires.

ARPU (Average Revenue Per Unit): Average revenue generated per mobile telephone subscriber.

ATM (Asynchronous Transfer Mode): technique enabling the high-speed transfer of digital data. It consists of dividing information flow (voice, data and image) into fixed-size packets, known as “cells”.

BACKBONE This is a high bandwidth line which acts as the mainstay linking access providers to the world network.

BILAN (Belgacom Interconnection of LAN): a total solution based on the Internet Protocol (IP), Frame Relay and ATM networks.

BIT (Contraction of Binary digIT): the basic unit of information. A bit has two possible values, 1 or 0. Each print character has an eight-bit code. Eight bits make one octet, or byte.

BROADBAND Network capable of high-speed transmission of several Megabits per second (Mbps), generally much faster than on the telephone network. These networks are composed of coaxial cable, optic fiber or wireless media.

CDMA (Code Division Multiple Access): digital technique in which dif-ferent conversations can be transmitted simultaneously and are differentiated by being tagged with a code.

CHAT Type of messaging done over the Internet, involving short text messages and often used by strangers to meet.

DWDM (Dense Wavelength Division Multiplexing): see WDM.

ETHERNET The most common LAN (Local Area Network) technology, devel-oped originally by Xerox, DEC and Intel. Conventionally, the Ethernet LAN uses coaxial cables or high-quality twisted cable. The most widely installed Ethernet network is known as 10BASE-T, which enables transmission at a speed of up to 10 Mbps. With Fast Ethernet, or 100BASE-T, speeds of up to 100 Megabits per second (Mbps) are possible.

EXTRANET Intranet to which a company’s suppliers, customers and partners have access. A network essential for e-business.

FRAME RELAY Data transport protocol that divides a physical communications line into several virtual channels. Technology part-way between X25 packet switching and ATM.

GPRS (General Packet Radio Service): a second-generation mobile telephony standard. It enables direct Internet access and data exchange at speeds 18 times faster than those of the GSM protocol and allows volume-based pricing.

GPS (Global Positioning System): system enabling a vehicle or person to pinpoint their position within approximately 50 meters or so anywhere in the world. It functions thanks to a network of 24 satellites put in place by the US Department of Defense.

GSM (Global System for Mobile Communications): an abbreviation which is often synonymous, in common parlance, with mobile terminal or telephone. In reality, it is a European standard for a common digital cellular telephony system.

INTRANET Application of Internet technologies (e-mail, Web, etc.) to a com-pany’s local area network (LAN).

IP (Internet Protocol): packet data protocol used for routing and car-riage of messages across the Internet.

annu

al r

epor

t 20

04

Belg

aco

m

Year ended 31 December 2002 2003 2004Income Statement (EUR million)

Total revenue before non-recurring items 5,338 5,454 5,540

Non-recurring revenue 1,085 0 0

Total revenue 6,422 5,454 5,540

EBITDA (2) before non-recurring items 2,020 2,250 2,394

EBITDA (2) 2,341 1,353 2,353

Operating income (EBIT) 1,482 566 1,611

Net finance revenue/(costs) -25 -27 -27

Loss from enterprises accounted for using the equity method -12 -4 -1

Income before taxes and minority interests 1,445 534 1,583

Tax expense -203 -208 -508

Minority interests -99 -154 -152

Net income (Group share) 1,142 172 922

As of 31 December 2002 2003 2004Cash Flow and Capital Expenditures (EUR million)

Cash flows from operating activities 1,371 296 1,899

Capital expenditures -566 -502 -556

Cash flows from other investing activities 1,276 17 78

Free cash flow (3) 2,081 -189 1,421

Cash flows used in financing activities -1,560 -575 -1,658

Net increase/(decrease) of cash and cash equivalents 521 -764 -237

Balance sheet (EUR million)

Balance sheet total 7,298 6,009 5,368

Non-current assets 4,601 4,381 3,963

Investments, cash and cash equivalents 1,611 604 406

Shareholders’ equity 2,978 2,548 2,223

Minority interests 293 446 407

Liabilities for pensions and other post-employment benefits 1,545 840 760

Net financial position 1,109 157 110

Year ended 31 December 2002 2003 2004Data per shareBasic earnings per share (in EUR) 2.86 0.43 2.57

Diluted earnings per share (in EUR) 2.86 0.43 2.57

Weighted average number of ordinary shares 400,000,000 399,932,159 358,612,854

Dividend per share, gross (in EUR) 0.70 0.99 1.38

Special dividend per share, gross (in EUR) 1.43 0.00 0.55

As of 31 December 2002 2003 2004Operating dataTotal access channels (in thousands) (4) 5,088 5,219 5,252

Total retail and wholesale ADSL access channels (in thousands) 519 784 1,024

Active mobile customers (in thousands) (5) 4,076 4,201 4,198

Minutes transported by International Carrier Services (in billions) 5.9 6.4 6.9

Personnel 19,003 17,541 16,933

(1) Prepared under IFRS.(2) Earnings Before Interests, Taxes, Depreciation and Amortization.(3) Cash flow before financing activities.

(4) PSTN + ISDN BA + ISDN PRA + retail ADSL.(5) Customers who received/made a call or received/sent an SMS over

the past three months.a n n u a l r e p o r t • 2 0 0 4

The commitment of a leader. The spirit of a challenger.

key figures (1)

glossary

ADSL (Asymmetric Digital Subscriber Line): technology enabling a one-to-one, high-speed, digital connection (up to eight megabits per second (Mbps) in receive mode and 640 Kilobits per second (Kbps) in send mode) on a single pair of copper wires.

ARPU (Average Revenue Per Unit): Average revenue generated per mobile telephone subscriber.

ATM (Asynchronous Transfer Mode): technique enabling the high-speed transfer of digital data. It consists of dividing information flow (voice, data and image) into fixed-size packets, known as “cells”.

BACKBONE This is a high bandwidth line which acts as the mainstay linking access providers to the world network.

BILAN (Belgacom Interconnection of LAN): a total solution based on the Internet Protocol (IP), Frame Relay and ATM networks.

BIT (Contraction of Binary digIT): the basic unit of information. A bit has two possible values, 1 or 0. Each print character has an eight-bit code. Eight bits make one octet, or byte.

BROADBAND Network capable of high-speed transmission of several Megabits per second (Mbps), generally much faster than on the telephone network. These networks are composed of coaxial cable, optic fiber or wireless media.

CDMA (Code Division Multiple Access): digital technique in which dif-ferent conversations can be transmitted simultaneously and are differentiated by being tagged with a code.

CHAT Type of messaging done over the Internet, involving short text messages and often used by strangers to meet.

DWDM (Dense Wavelength Division Multiplexing): see WDM.

ETHERNET The most common LAN (Local Area Network) technology, devel-oped originally by Xerox, DEC and Intel. Conventionally, the Ethernet LAN uses coaxial cables or high-quality twisted cable. The most widely installed Ethernet network is known as 10BASE-T, which enables transmission at a speed of up to 10 Mbps. With Fast Ethernet, or 100BASE-T, speeds of up to 100 Megabits per second (Mbps) are possible.

EXTRANET Intranet to which a company’s suppliers, customers and partners have access. A network essential for e-business.

FRAME RELAY Data transport protocol that divides a physical communications line into several virtual channels. Technology part-way between X25 packet switching and ATM.

GPRS (General Packet Radio Service): a second-generation mobile telephony standard. It enables direct Internet access and data exchange at speeds 18 times faster than those of the GSM protocol and allows volume-based pricing.

GPS (Global Positioning System): system enabling a vehicle or person to pinpoint their position within approximately 50 meters or so anywhere in the world. It functions thanks to a network of 24 satellites put in place by the US Department of Defense.

GSM (Global System for Mobile Communications): an abbreviation which is often synonymous, in common parlance, with mobile terminal or telephone. In reality, it is a European standard for a common digital cellular telephony system.

INTRANET Application of Internet technologies (e-mail, Web, etc.) to a com-pany’s local area network (LAN).

IP (Internet Protocol): packet data protocol used for routing and car-riage of messages across the Internet.

annu

al r

epor

t 20

04

5,200 5,300 5,400 5,500 5,600 1,800 1,900 2,000 2,100 2,200 2,300 2,400

0 200 400 600 800 1,000 1,200 0.0 0.5 1.0 1.5 2.0 2.5 3.0

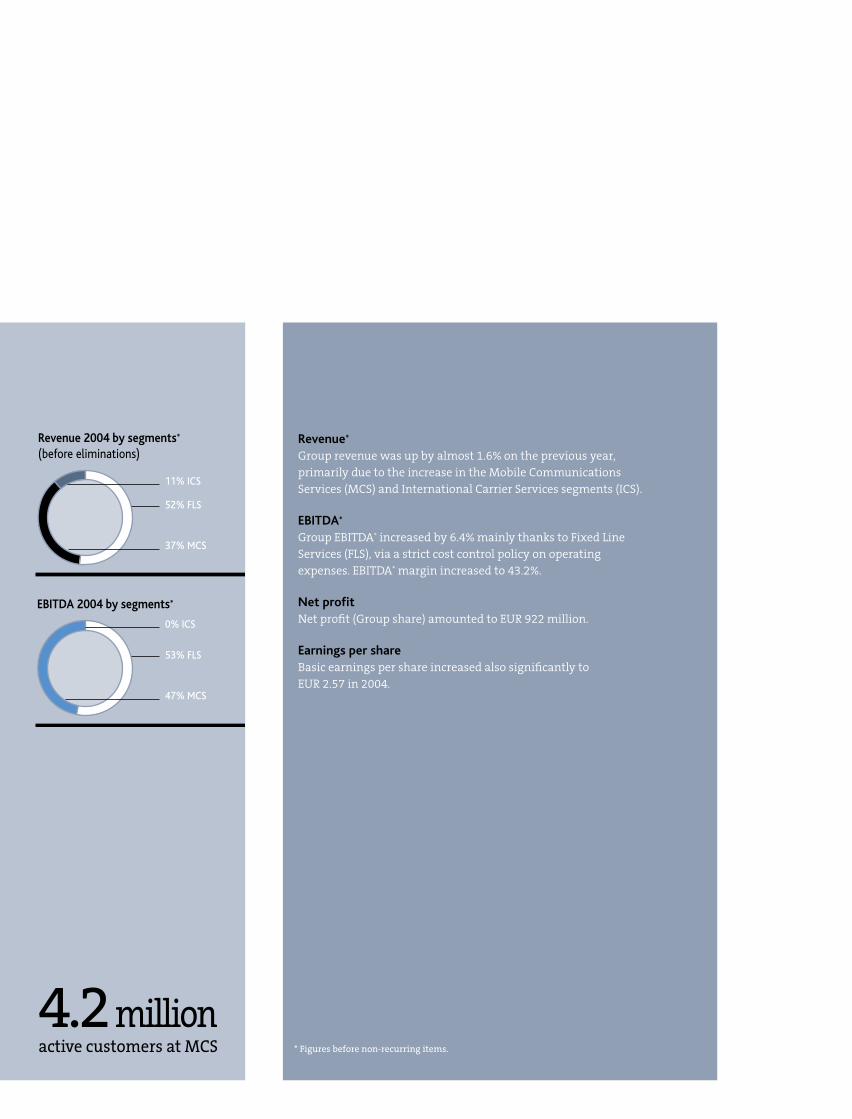

11% ICS

52% FLS

37% MCS

0% ICS

53% FLS

47% MCS

5,33802

5,45403

5,54004

1,14202

17203

92204

2,02002

2,25003

2,39404

2.8602

0.4303

2.5704

Revenue 2004 by segments* (before eliminations)

EBITDA 2004 by segments*

Revenue*

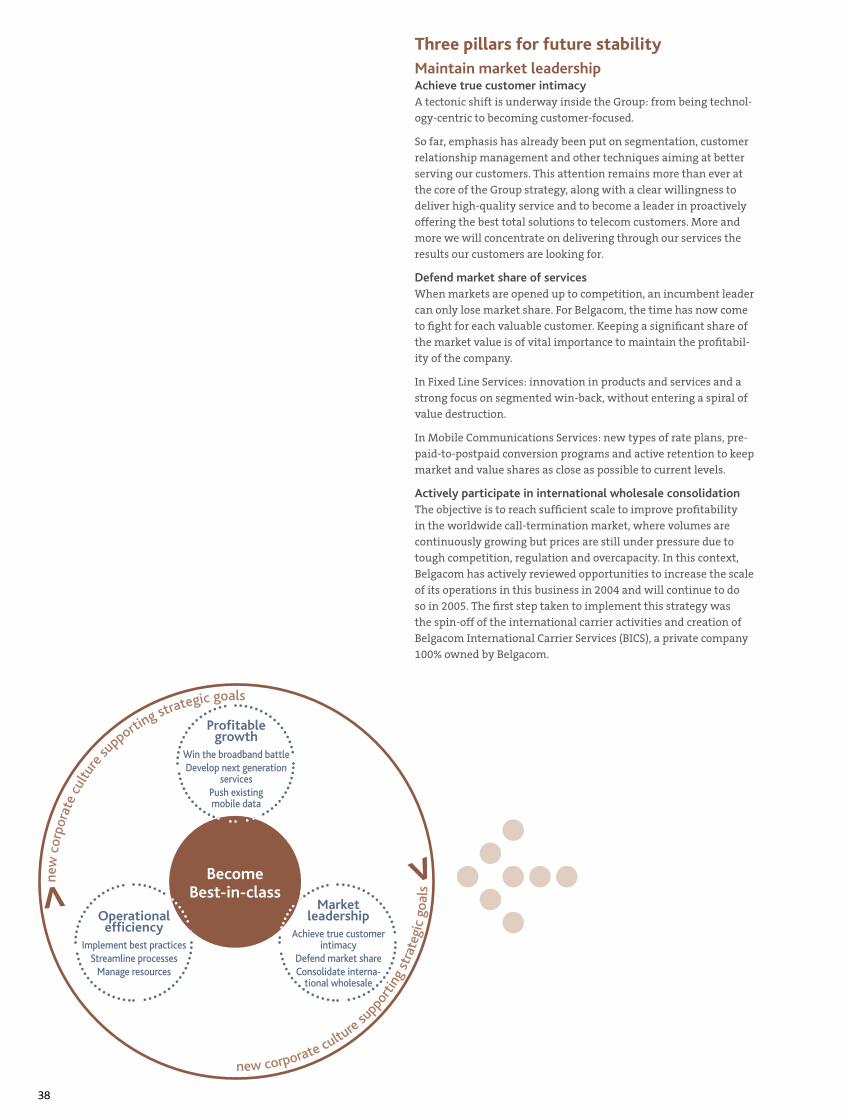

Group revenue was up by almost 1.6% on the previous year, primarily due to the increase in the Mobile Communications Services (MCS) and International Carrier Services segments (ICS).

EBITDA*

Group EBITDA* increased by 6.4% mainly thanks to Fixed Line Services (FLS), via a strict cost control policy on operating expenses. EBITDA* margin increased to 43.2%.

Net profitNet profit (Group share) amounted to EUR 922 million.

Earnings per shareBasic earnings per share increased also significantly to EUR 2.57 in 2004.

4.2 millionactive customers at MCS

group financials

Revenue* (in EUR millions)

142,000customers won back at FLS

more than 1,000,000total retail and wholesale ADSL access channels

Net profit (in EUR millions)

EBITDA* (in EUR millions)

Earnings per share (in EUR)

glossary

IP VPN (Internet Protocol Virtual Private Network): A VPN offers the advantages of a private network (security, etc.) while using the resources of a public switched network. The user thereby saves money on network infrastructure and manage-ment costs.

ISDN (Integrated Services Digital Network): fully digitized network ena-bling simultaneous, high-speed transmission of speech, text, data and images (still or animated). There are two types of ISDN lines: the ISDN-2, equipped with two communication channels, and the ISDN-30, equipped with thirty communication channels.

ISP (Internet Service Provider): a company providing Internet access to its customers and a personal e-mail address.

LARGE BAND See Broadband.

MMS (Multimedia Messaging Service): possibility to illustrate text mes-sages on mobile phones with photographs, images and sound.

PABX (Private Automatic Branch Exchange): company exchange around which the company’s internal telephone network is organized. It also enables data transmission.

PORTAL Site offering to act as a gateway to the World Wide Web (WWW) for a large number of surfers, ideally immediately on connection. Many Internet Access Providers offer portals to their customers (e.g., the Belgacom Skynet portal).

SERVER Machine that assists in providing information and/or resources in a network, be it public or private.

SDSL A technology that transports data at a maximum bit rate of 2.3 Mbits/s in both directions.

SMS (Short Message Service): enables written messages to be received and displayed on a GSM.

STREAMING Technique for downloading multimedia files enabling surfers to read the file in real-time, without waiting for full download. This is the case, for example, with sound or video on the Internet.

TCP-IP (Transmission Control Protocol – Internet Protocol): a protocol used in conjunction with the Internet Protocol (IP) to send data in the form of message units (datagrams, or packets) between com-puters over the Internet. IP handles the actual delivery of the data, while TCP keeps track of the individual units of data for efficient routing through the Internet.

UMTS (Universal Mobile Telecommunications System): a third-genera-tion telecommunications system capable of providing multimedia services at a very-high speed.

VIDEO- Communication in which the callers can be seen as well as heard CONFERENCING (video conference).

VPN (Virtual Private Network): a data network that shares telecommu-nications infrastructure but acts as a secure private network, with an architecture based on the use of the TCP-IP (Time Compression Multiplexing - Internet Protocol).

WAP (Wireless Application Protocol): new protocol enabling GSMs to be transformed into Internet and multimedia terminals.

WDM (Wavelength Division Multiplexing) or DWDM (Dense Wavelength Division Multiplexing): technique enabling several independent flows of digital information to coexist on the same optical fiber.

WIFI Stands for wireless fidelity. Technology makes possible wireless, high-speed surfing from a hotspot.

Despite ever increasing fixed and mobile competitive pressure, the Belgacom Group managed to gen-erate higher revenue and EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) in 2004. The net profit (Group share) also rose significantly as compared with the previous financial year.

* Figures before non-recurring items.

5,200 5,300 5,400 5,500 5,600 1,800 1,900 2,000 2,100 2,200 2,300 2,400

0 200 400 600 800 1,000 1,200 0.0 0.5 1.0 1.5 2.0 2.5 3.0

11% ICS

52% FLS

37% MCS

0% ICS

53% FLS

47% MCS

5,33802

5,45403

5,54004

1,14202

17203

92204

2,02002

2,25003

2,39404

2.8602

0.4303

2.5704

Revenue 2004 by segments* (before eliminations)

EBITDA 2004 by segments*

Revenue*

Group revenue was up by almost 1.6% on the previous year, primarily due to the increase in the Mobile Communications Services (MCS) and International Carrier Services segments (ICS).

EBITDA*

Group EBITDA* increased by 6.4% mainly thanks to Fixed Line Services (FLS), via a strict cost control policy on operating expenses. EBITDA* margin increased to 43.2%.

Net profitNet profit (Group share) amounted to EUR 922 million.

Earnings per shareBasic earnings per share increased also significantly to EUR 2.57 in 2004.

4.2 millionactive customers at MCS

group financials

Revenue* (in EUR millions)

142,000customers won back at FLS

more than 1,000,000total retail and wholesale ADSL access channels

Net profit (in EUR millions)

EBITDA* (in EUR millions)

Earnings per share (in EUR)

glossary

IP VPN (Internet Protocol Virtual Private Network): A VPN offers the advantages of a private network (security, etc.) while using the resources of a public switched network. The user thereby saves money on network infrastructure and manage-ment costs.

ISDN (Integrated Services Digital Network): fully digitized network ena-bling simultaneous, high-speed transmission of speech, text, data and images (still or animated). There are two types of ISDN lines: the ISDN-2, equipped with two communication channels, and the ISDN-30, equipped with thirty communication channels.

ISP (Internet Service Provider): a company providing Internet access to its customers and a personal e-mail address.

LARGE BAND See Broadband.

MMS (Multimedia Messaging Service): possibility to illustrate text mes-sages on mobile phones with photographs, images and sound.

PABX (Private Automatic Branch Exchange): company exchange around which the company’s internal telephone network is organized. It also enables data transmission.

PORTAL Site offering to act as a gateway to the World Wide Web (WWW) for a large number of surfers, ideally immediately on connection. Many Internet Access Providers offer portals to their customers (e.g., the Belgacom Skynet portal).

SERVER Machine that assists in providing information and/or resources in a network, be it public or private.

SDSL A technology that transports data at a maximum bit rate of 2.3 Mbits/s in both directions.

SMS (Short Message Service): enables written messages to be received and displayed on a GSM.

STREAMING Technique for downloading multimedia files enabling surfers to read the file in real-time, without waiting for full download. This is the case, for example, with sound or video on the Internet.

TCP-IP (Transmission Control Protocol – Internet Protocol): a protocol used in conjunction with the Internet Protocol (IP) to send data in the form of message units (datagrams, or packets) between com-puters over the Internet. IP handles the actual delivery of the data, while TCP keeps track of the individual units of data for efficient routing through the Internet.

UMTS (Universal Mobile Telecommunications System): a third-genera-tion telecommunications system capable of providing multimedia services at a very-high speed.

VIDEO- Communication in which the callers can be seen as well as heard CONFERENCING (video conference).

VPN (Virtual Private Network): a data network that shares telecommu-nications infrastructure but acts as a secure private network, with an architecture based on the use of the TCP-IP (Time Compression Multiplexing - Internet Protocol).

WAP (Wireless Application Protocol): new protocol enabling GSMs to be transformed into Internet and multimedia terminals.

WDM (Wavelength Division Multiplexing) or DWDM (Dense Wavelength Division Multiplexing): technique enabling several independent flows of digital information to coexist on the same optical fiber.

WIFI Stands for wireless fidelity. Technology makes possible wireless, high-speed surfing from a hotspot.

Despite ever increasing fixed and mobile competitive pressure, the Belgacom Group managed to gen-erate higher revenue and EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) in 2004. The net profit (Group share) also rose significantly as compared with the previous financial year.

* Figures before non-recurring items.

1

>

02 • The Belgacom Group

04 • Highlights 2004

06 • Message from the Chairman

08 • Message from the CEO

10 • Corporate governance and management

20 • Shareholder information

24 • Business update

26 • Fixed Line Services

30 • Mobile Communications Services

34 • International Carrier Services

36 • Group strategy

40 • Teams that have endurance

44 • Striving for the well-being of all

48 • Financial report

Committed to defend its leadership and beBest-in-class

2

The commitment of a leader.The spirit of a challenger.

3

the Belgacom GroupCorporate profileBelgacom is the leading telecommunications company in Belgium and a market leader in a number of areas, including retail and wholesale fixed-line telephony services, mobile communications services and broadband data and Internet services. For the year ended 31 December 2004, the Group had total revenues of EUR 5,540 million and operating income before depreciation and amortization (excluding non-recur-ring items) of EUR 2,394 million.

VisionWe believe in a world where unlimited communication pos-sibilities will create new unexpected services of uplifting benefit for all.

MissionBy opening up the amazing universe of communication pos-sibilities, we enable and inspire people and organizations to achieve their dreams and goals in their ever changing world.

ValuesSimple – Uplifting – Reliable – Fresh

Our activitiesFixed Line Services (FLS)Belgacom offers a comprehensive range of voice, data and Internet fixed-line services to residential and business custom-ers. At the end of 2004, Belgacom provided approximately 5.3 million fixed connections for residential and business customers, including around 975,000 ISDN access lines and 828,000 ADSL access lines for the retail market. As the leading

ISP in Belgium, Belgacom offered Internet access to more than 1 million narrowband and broadband subscribers at the end of 2004, as well as providing wholesale services to other opera-tors and service providers in Belgium. Belgacom has the widest commercial coverage of all telecom operators in Belgium thanks to its sales outlets, resale network, account managers, call centers and website.

Mobile Communications Services (MCS)Belgacom Mobile is the leading provider of mobile communi-cations services in Belgium through its Proximus and Pay&Go brands, with approximately 4.2 million active customers(1) and an estimated market share of approximately 50%. Belgacom has a 75% stake in Belgacom Mobile while 25% is owned by Vodafone, one of the world’s largest mobile operators. Belgacom Mobile provides a broad range of mobile commu-nications services to residential and business customers in Belgium, including traditional voice, data (SMS and MMS) and international roaming as well as wholesale data services to other companies.

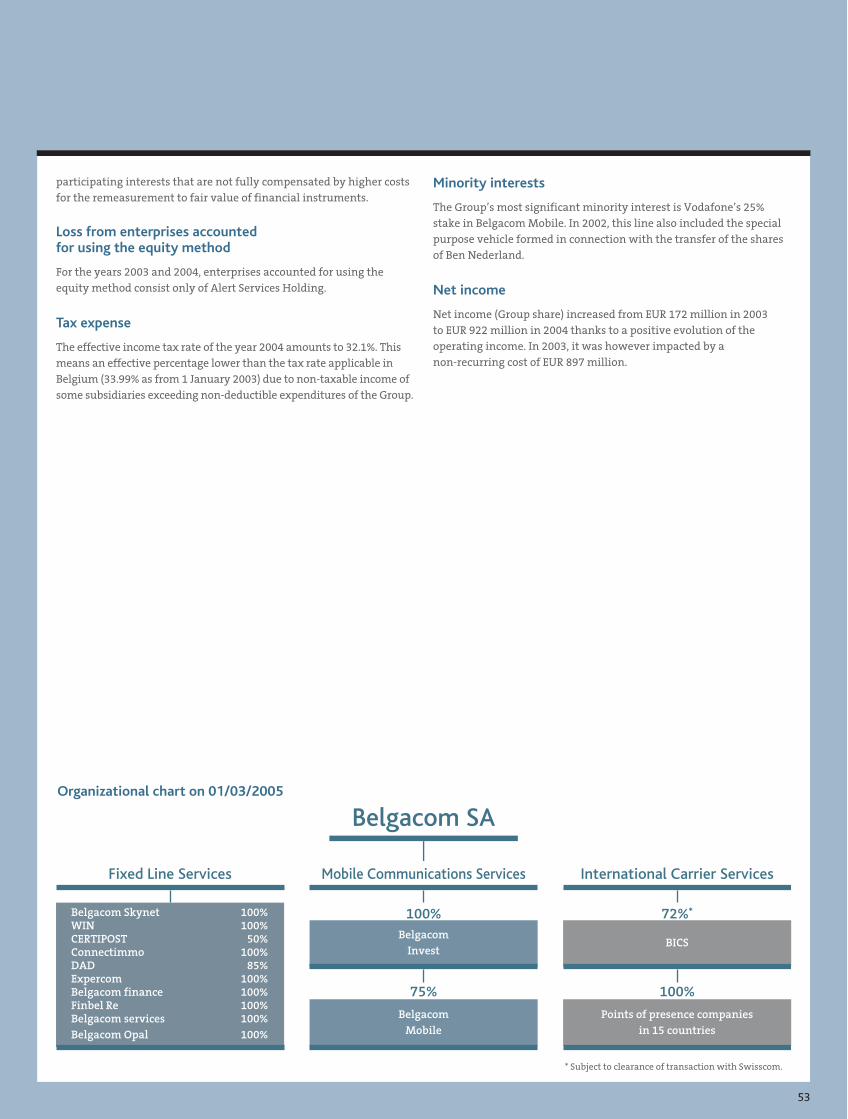

International Carrier Services (ICS)In addition to its activities in Belgium, Belgacom provides voice and data connectivity and capacity services to telecom-munications operators and service providers worldwide. On 22 February 2005, Belgacom signed an agreement to combine its BICS with Swisscom Fixnet into a joint venture in which Belgacom will own 72% of the shares.

A combination of strength and flexibility, in other words. Two approaches that may seem paradoxical, but that both require our attention. The strength of a leader that can invest in future technologies. The flexibility of a challenger that has what it takes to streamline structures, and to adapt them to every market demand. It is our way of listening to our customers. To respond to their needs and to anticipate their desires.

(1) Active customers are customers who have made or received at least one call or sent or received at least one SMS message in the last three months.

4

03/04

May• Launch of external mobility projects “e-ID” and “Call

Center 112.”

• FLS boosts its ADSL offer and introduces ADSL Light.

• Mobile Communications Services (MCS) launches first 3G services for corporate market in Belgium.

• Belgacom makes development of interactive digital television a top priority.

June• MCS brings Vodafone live!, the most integrated multimedia

offer, to the residential market.

• Skynet acquires 100% of Eduline capital.

January• Fixed Line Services (FLS) launches major internal campaign to

win back customers.

February• Belgacom has 1,000,000 active surfers connected to its net-

work. More than two out of every three have opted for ADSL.

March• International Carrier Services (ICS) officially opens its Dubai

office.

• Successful Initial Public Offering of Belgacom on Euronext Brussels Prime Market, with share offer price of EUR 24.50.

• Appointment of new members to the Board of Directors.

April• New independent Board member appointed and new compo-

sition of Board Committees approved.

• Fixed Line Services (FLS) launches “Discovery Line.”

2004 was not just the year in which Belgacom was first listed on the stock exchange, it was also a year of fierce competition. This we experienced every day, at all levels of the Group’s activities. But we did more than just stand our ground: we launched a counter-offensive. Which is apparent in some of the key events of the year: the win-back of 142,000 (fixed-line) customers, the reinforcement of our leadership position in terms of market shares and mobile-sector profitability, and our active participation in the consolidation of European carrier activities.

highlights 2004

June: launch of Vodafone live!

March: listing on the stock market

06/04

5

07/04

July• Belgacom ICS selected by peers as most competitive carrier.

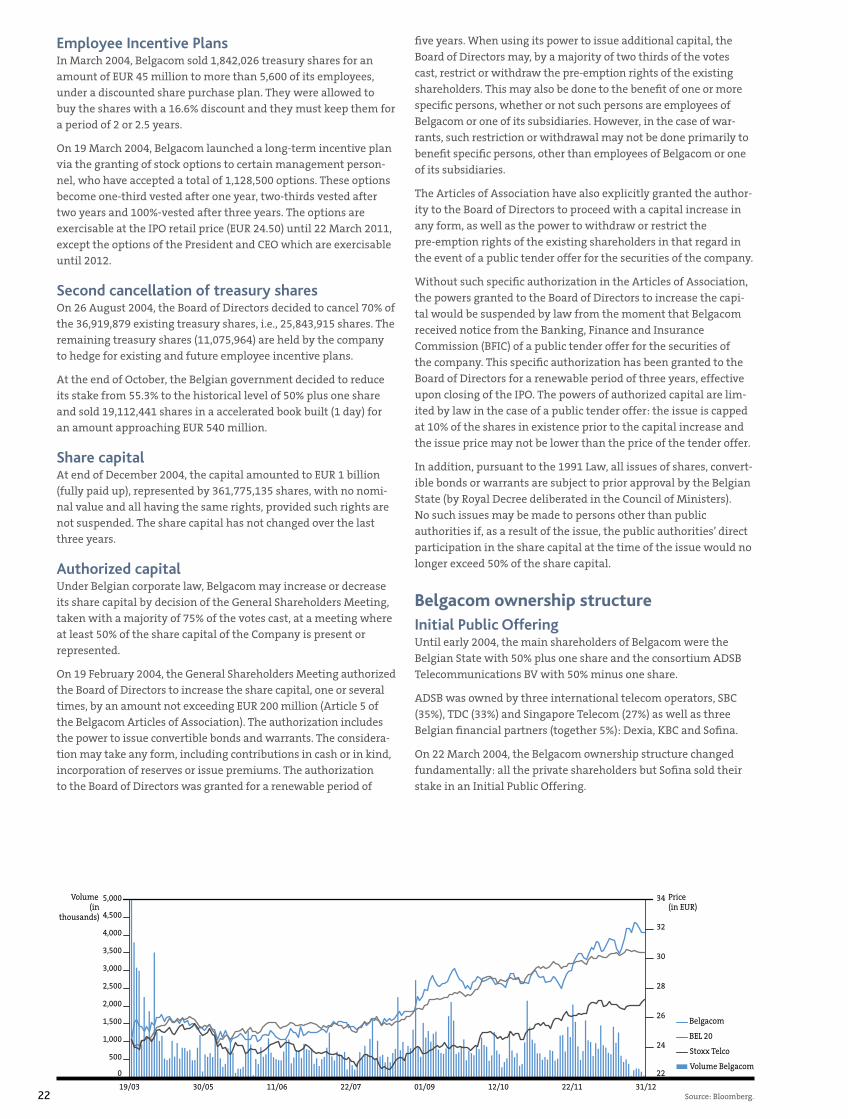

August• Belgacom decides to cancel 70% of its treasury shares.

October• Theo Dilissen appointed as chairman of the Board of

Directors of Belgacom.

• Government sells Belgacom shares, bringing its stake back to 50% + one share.

• FLS launches Belgacom VDSL and automatic Directory Services 1-2-3-4.

• MCS proposes BlackBerry solution to its business customers.

November• Launch of Belgacom TV test, a new service over Belgacom

broadband.

• MCS markets UMTS/GPRS/Wireless LAN Connect card.

• More than one million ADSL connections in Belgium.

• Skynet launches Arena51 gaming portal.

• Belgacom receives “Supplier of Telecommunications Services of the Year” award from Data News.

December• Internal presentation of Belgacom main strategic axes for the

future (Today we build tomorrow).

Highlights early 2005• The International Carrier Services (ICS) segment becomes a subsidiary named BICS (Belgacom International Carrier Services).

• Belgacom sells its stake in Alert Services Holding to Securitas.

• Belgacom sells its stake in BDS (Belgacom Directory Services) to Promedia.

• Agreement to merge ICS business in a joint venture with Swisscom Fixnet.

• Decision to conduct a share buyback for a maximum amount of EUR 300 million.

• Reshaping of MCS Management Committee.

July: ICS most competitive carrier

More than 142,000 customers won back in 2004!

06/04

6

An exciting future is opening up for Belgacom. One that will be

marked by change and progress. We will continue to move further

away from the former monopoly to become more of a service

company, offering not only access and bandwidth but also appli-

cations and content.

Stock market listingFor Belgacom, 2004 was a year marked above all by a fundamental

transition: on 22 March 2004, Belgacom was listed for the first

time on the Euronext Brussels stock market. My thanks and con-

gratulations go to all those who helped prepare the Initial Public

Offering (IPO), the largest ever on the Belgian market! The opera-

tion was flawlessly executed, and the investors who have placed

their trust in the company’s management have ample reason to be

pleased.

The listing on the stock market has created new obligations of

transparency and corporate governance for Belgacom, which the

company has met as a positive challenge. On a practical level, the

IPO brought about changes in the composition of the Board of

Directors: as part of our efforts to apply principles of good corpo-

rate governance, eight new Directors joined the Board.

Committees created to ensure proper management, such as

the Audit and Compliance Committee, the Nomination and

Remuneration Committee and the Strategic and Business

Development Committee, have functioned extremely well. Several

Belgacom Board members were active participants in the work of

the Lippens Commission, which in December 2004 established a

new code of corporate governance. I would like to extend my most

sincere thanks to the Board Members for the excellent work they

Today, Belgacom is a de facto leader in the field of electronic

communications. Belgacom has played, is playing now and will

continue to play a fundamental role in helping individuals and

businesses communicate.

The liberalization of the telecom market is now a well-established

fact. Inevitably, when Belgacom ceased to be a monopoly, it lost

market share. And today Belgacom, like any other company, has to

fight day in and day out to maintain its leadership position and to

attract and keep customers.

Confidence in the futureThanks to its healthy financial situation and absence of debt,

Belgacom is in a position to develop exciting projects, to look to

the future with confidence and ambition.

• We are investing heavily in the construction of very high-speed

broadband networks, thereby laying the foundations for tomor-

row’s information highway, for e-Belgium.

• Belgacom, which remains Belgium’s telecommunications leader,

is now positioning itself to be a challenger in the world of broad-

casting. We are not taking this step simply for the pleasure of

diversifying our activities: Belgacom is bringing to the effort its

expertise, its networks and, thanks to interactivity, an innovative

way of thinking about television.

• Lastly, Belgacom can now look beyond Belgium’s frontiers and

consider opportunities for expansion. Finding a partner for our

international wholesale activities… seizing profitable oppor-

tunities… Belgacom is ready for these new challenges and will

evaluate them with a simple question: do they create value for

our shareholders?

message from the Chairman

Belgacom has come an long way over the last ten years. I myself arrived in October 2004, following my appoint-ment as the Chairman of the Board of Directors. And one of the first things that struck me was how different today’s Belgacom — dynamic, state-of-the-art — is from yesterday’s monopoly operator.

7

carried out in 2004. By sharing their commitment and profession-alism, they have given Belgacom the tools for building its future.

Upon my arrival, I also found a spirit of open, constructive dialog between the representatives of labor and management. It will be essential to preserve this spirit in order to take Belgacom and its employees forward together.

Let me conclude by thanking Didier Bellens, the Management Committee and each of our 17,000 employees for the quality of their work during this crucial year in the life of our company. Together, we will continue working in concert to make Belgacom a company turned towards the future. A company that prides itself on providing for the well-being of its employees, meet-ing the needs of its customers, rewarding the confidence of its shareholders and doing its part to help make Belgian society more harmonious and the knowledge economy a reality.

Theo Dilissen Chairman

“An exciting future is opening up for Belgacom. One that will be marked by change and progress.”>

8

same time, we conducted a large-scale communication campaign

to show that the rates applied by Belgacom are indeed attractive.

Mobile telephonyAs for mobile telephony, we are the Belgian market leader and are

determined to maintain this position. In the business segment,

we are still the biggest, by far. On the other hand, for the first time

since Proximus launched mobile technology ten years earlier, we

noted in 2004 that the market was reaching a high level of matu-

rity. Competition is fierce, which explains why growth was limited.

Here too, we turned to new uses and applications for the future,

such as mobile payment, location-based services and videophony.

Once again Mobile Communications Services demonstrated its

capacity for innovation by being the first operator to deploy a UMTS

network and propose a veritable multimedia portal (Vodafone live!)

to its customers, in anticipation of the services of the future. In

addition, new types of rate plans and targeted customer-retention

campaigns allowed Proximus to make good its promises.

International Carrier ServicesFinally, our international operations (Carrier & Wholesale) also

had a positive year, even though competition is fierce in this sec-

tor too. The results recorded by Belgacom International Carrier

Services (BICS) show that the decision to put greater emphasis on

the mobile segment was a good one. At the end of 2004, this activ-

ity was completely spun off to enable BICS to take full advantage

of the consolidation opportunities that will present themselves.

The objective is to reach sufficient critical size to improve profit-

ability in this global call-termination market, where volumes

continue to increase but rates are constantly under pressure.

There is certainly no shortage of challenges half way through this

first decade of the new century: technologies are developing at

high speed, the landscape is constantly changing through increas-

ingly intensive competition, the regulatory context is complex.

In this extremely complicated environment, 2004 has proved a

highly satisfactory year for Belgacom, despite ever fiercer competi-

tion, both in the mobile and the fixed-line sectors.

For Belgacom, the opening up of the market obviously meant losing

a share of that market. In 2004, we entered into a new phase in

which the emphasis was placed on retaining and winning back cus-

tomers. Today Belgacom is fighting to create value for the company

and its shareholders. Belgacom intends to create this value by being

Best-in-class and by innovating. New uses, new services and new

rates have enabled Belgacom to meet its objectives in 2004.

Fixed-line telephonyWhere fixed-line telephony is concerned, Belgacom decided to

take the offensive with a vigorous program to win back customers

who had left for the competition and a communication campaign

to increase awareness of the attractive rate plans available at

Belgacom. At the very beginning of the year, from January on,

we launched the Winback program, which enabled Belgacom to

recover more than 142,000 customers who had left for the com-

petition. This daily effort manifested itself in great operational

dynamism: new products, new offers, etc. We launched Discovery

Line, a discount program for conventional fixed-line telephony

subscriptions which allowed us to keep and win back a significant

number of customers; we developed our ADSL range of products,

providing ever more users with high-speed Internet access. At the

message from the CEO

Today Belgacom is fighting to create value for the company and its shareholders. Belgacom intends to create this value by being Best-in-class and by innovating. New uses, new services and new rates have enabled Belgacom to meet its objectives in 2004.

9

> “We did it and we made it a success: we’ve done a fantastic job! I’m proud of Belgacom.”(on the IPO of Belgacom, 22 March, 2004)

InfrastructureOf course, voice communications should remain relatively stable; but the principal field of growth in the next few years will be data transmission. One of Belgacom’s major challenges is to develop a very high-capacity data transmission infrastructure capable of meeting this increased demand. To create value for Belgacom and its shareholders was our strategy in 2004 and is still our commit-ment for the the future.

We also decided to launch the Broadway project and invest mas-sively to increase the capacity of our networks, notably through VDSL for fixed-line telephony and UMTS for mobile telephony. This major effort will make it possible to develop applications and services in a number of different fields: e-Health, electronic billing, teleworking, home networks, data storage, online gam-ing, television via PC and interactive digital television, the latter a challenge that Belgacom took up in 2004 under the name “Belgacom TV”. Not to mention e-Government and e-Belgium, social projects in which we aim to play a key role.

It is in this dynamic environment that the Belgacom Group was able to attain its objectives. Revenue increased by 1.6% to reach EUR 5,540 million.

These achievements were only possible with the full support of all the Belgacom employees. Their recognition and development are the key elements in a global strategy developed by the manage-ment, in continuous consultation with its union partners. In 2004, Belgacom has favored clear, transparent consultation between labor and management. This open and continuous dialog fosters a positive management-labor environment.

Stock market listingOf course, 2004 was also the year that Belgacom launched an initial public offering, which was a resounding success for the company as a whole. This was a corporate project that truly united all our forces in a common objective. And I believe that we were successful in attracting and retaining major international inves-tors, who are clearly confident about Belgacom’s future.

All this would not have been possible without a team of brilliant professionals, which successfully managed Belgacom’s transition to a listed company while facing the changes and challenges spe-cific to our sector. Together with all Belgacom staff, and with the support of the Board of Directors, I intend to transform Belgacom, a telecommunications company, into a veritable service company.

Didier Bellens President & CEO

10

>Good corporate governance leads to increased transparency

11

corporate governanceand management

Corporate governance aims to define a set of rules and behaviors according to which companies are properly managed and controlled, the result being increased transparency. Belgacom is preparing itself to conform to the recommendations made by the market authorities and more specifically to best practices of Belgium’s “Lippens Code,” published on 9 December 2004. Additionally it has continued to reinforce its internal compliance program.

The key features of Belgacom’s governance model are:

• a Board of Directors, which defines Belgacom’s general policy

and strategy and supervises operational management;

• the creation by the Board of Directors within its structure

of an Audit and Compliance Committee, a Nomination and

Remuneration Committee and a Strategic and Business

Development Committee;

• a Chief Executive Officer, who takes primary responsibility and

ownership for operational management (including, but not lim-

ited to, day-to-day management); and

• a Management Committee which, apart from a number of spe-

cific responsibilities attributed to it by the 1991 law, assists the

Chief Executive Officer in the exercise of his duties.

Board of DirectorsAs provided for in the 1991 Law, the Board of Directors is com-

posed of:

• Directors appointed by the Belgian State pro rata to its share-

holding; the aggregate number of directors being determined

by the shareholders’ meeting; and

• Directors appointed by a separate vote among the other share-

holders, for the remaining seats.

The Lippens CodeAt the European Commission level, several initiatives have been taken to improve governance and strengthen shareholders’rights. In Belgium, in order to align with international practices and EU recommendations, the Banking, Finance and Insurance Commission, Euronext Brussels and the Federation of Belgian Enterprises established a committee in January 2004 to draft one single code for listed companies.

The goal of the code is to set forth principles of good governance and transparency that will help companies develop and improve their image vis-à-vis investors and the general public. This code of best practices on corporate governance is based on the “comply or explain” system.

Belgacom governance modelAt Belgacom, the Articles of Association are strongly influenced by the specific legal status of the company. As a limited liability company under public law, Belgacom is in first instance governed by the Law of 21 March 1991 on autonomous public-sector enter-prises (“the 1991 Law”). The 1991 Law was not modified on the occasion of the IPO. For matters not explicitly regulated otherwise by the 1991 Law, Belgacom is governed by Belgian corporate law.

12

12 3

4

5

6

7

8

910

11

12 13

14

15

1617

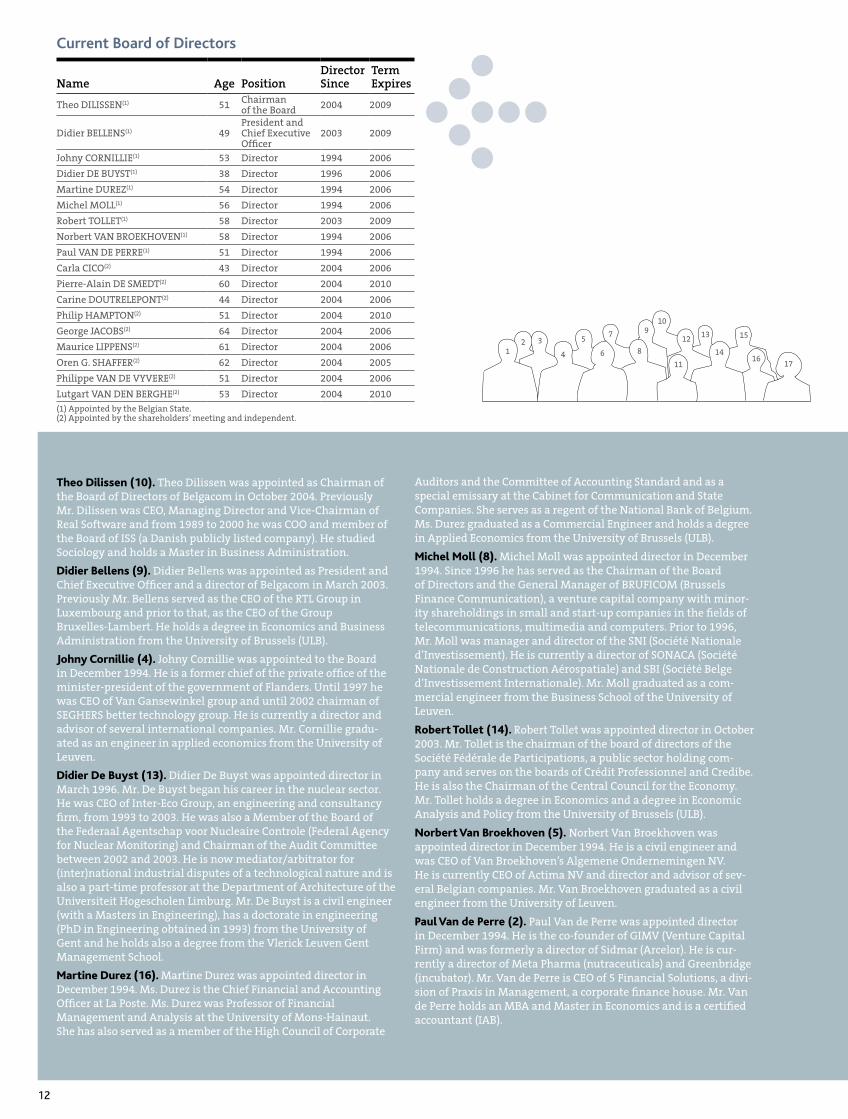

Current Board of Directors

Name Age PositionDirector Since

Term Expires

Theo DILISSEN(1) 51 Chairman of the Board 2004 2009

Didier BELLENS(1) 49President and Chief Executive Officer

2003 2009

Johny CORNILLIE(1) 53 Director 1994 2006

Didier DE BUYST(1) 38 Director 1996 2006

Martine DUREZ(1) 54 Director 1994 2006

Michel MOLL(1) 56 Director 1994 2006

Robert TOLLET(1) 58 Director 2003 2009

Norbert VAN BROEKHOVEN(1) 58 Director 1994 2006

Paul VAN DE PERRE(1) 51 Director 1994 2006

Carla CICO(2) 43 Director 2004 2006

Pierre-Alain DE SMEDT(2) 60 Director 2004 2010

Carine DOUTRELEPONT(2) 44 Director 2004 2006

Philip HAMPTON(2) 51 Director 2004 2010

George JACOBS(2) 64 Director 2004 2006

Maurice LIPPENS(2) 61 Director 2004 2006

Oren G. SHAFFER(2) 62 Director 2004 2005

Philippe VAN DE VYVERE(2) 51 Director 2004 2006

Lutgart VAN DEN BERGHE(2) 53 Director 2004 2010

(1) Appointed by the Belgian State. (2) Appointed by the shareholders’ meeting and independent.

Theo Dilissen (10). Theo Dilissen was appointed as Chairman of the Board of Directors of Belgacom in October 2004. Previously Mr. Dilissen was CEO, Managing Director and Vice-Chairman of Real Software and from 1989 to 2000 he was COO and member of the Board of ISS (a Danish publicly listed company). He studied Sociology and holds a Master in Business Administration.

Didier Bellens (9). Didier Bellens was appointed as President and Chief Executive Officer and a director of Belgacom in March 2003. Previously Mr. Bellens served as the CEO of the RTL Group in Luxembourg and prior to that, as the CEO of the Group Bruxelles-Lambert. He holds a degree in Economics and Business Administration from the University of Brussels (ULB).

Johny Cornillie (4). Johny Cornillie was appointed to the Board in December 1994. He is a former chief of the private office of the minister-president of the government of Flanders. Until 1997 he was CEO of Van Gansewinkel group and until 2002 chairman of SEGHERS better technology group. He is currently a director and advisor of several international companies. Mr. Cornillie gradu-ated as an engineer in applied economics from the University of Leuven.

Didier De Buyst (13). Didier De Buyst was appointed director in March 1996. Mr. De Buyst began his career in the nuclear sector. He was CEO of Inter-Eco Group, an engineering and consultancy firm, from 1993 to 2003. He was also a Member of the Board of the Federaal Agentschap voor Nucleaire Controle (Federal Agency for Nuclear Monitoring) and Chairman of the Audit Committee between 2002 and 2003. He is now mediator/arbitrator for (inter)national industrial disputes of a technological nature and is also a part-time professor at the Department of Architecture of the Universiteit Hogescholen Limburg. Mr. De Buyst is a civil engineer (with a Masters in Engineering), has a doctorate in engineering (PhD in Engineering obtained in 1993) from the University of Gent and he holds also a degree from the Vlerick Leuven Gent Management School.

Martine Durez (16). Martine Durez was appointed director in December 1994. Ms. Durez is the Chief Financial and Accounting Officer at La Poste. Ms. Durez was Professor of Financial Management and Analysis at the University of Mons-Hainaut. She has also served as a member of the High Council of Corporate

Auditors and the Committee of Accounting Standard and as a special emissary at the Cabinet for Communication and State Companies. She serves as a regent of the National Bank of Belgium. Ms. Durez graduated as a Commercial Engineer and holds a degree in Applied Economics from the University of Brussels (ULB).

Michel Moll (8). Michel Moll was appointed director in December 1994. Since 1996 he has served as the Chairman of the Board of Directors and the General Manager of BRUFICOM (Brussels Finance Communication), a venture capital company with minor-ity shareholdings in small and start-up companies in the fields of telecommunications, multimedia and computers. Prior to 1996, Mr. Moll was manager and director of the SNI (Société Nationale d’Investissement). He is currently a director of SONACA (Société Nationale de Construction Aérospatiale) and SBI (Société Belge d’Investissement Internationale). Mr. Moll graduated as a com-mercial engineer from the Business School of the University of Leuven.

Robert Tollet (14). Robert Tollet was appointed director in October 2003. Mr. Tollet is the chairman of the board of directors of the Société Fédérale de Participations, a public sector holding com-pany and serves on the boards of Crédit Professionnel and Credibe. He is also the Chairman of the Central Council for the Economy. Mr. Tollet holds a degree in Economics and a degree in Economic Analysis and Policy from the University of Brussels (ULB).

Norbert Van Broekhoven (5). Norbert Van Broekhoven was appointed director in December 1994. He is a civil engineer and was CEO of Van Broekhoven’s Algemene Ondernemingen NV. He is currently CEO of Actima NV and director and advisor of sev-eral Belgian companies. Mr. Van Broekhoven graduated as a civil engineer from the University of Leuven.

Paul Van de Perre (2). Paul Van de Perre was appointed director in December 1994. He is the co-founder of GIMV (Venture Capital Firm) and was formerly a director of Sidmar (Arcelor). He is cur-rently a director of Meta Pharma (nutraceuticals) and Greenbridge (incubator). Mr. Van de Perre is CEO of 5 Financial Solutions, a divi-sion of Praxis in Management, a corporate finance house. Mr. Van de Perre holds an MBA and Master in Economics and is a certified accountant (IAB).

13

Carla Cico (17). Carla Cico was appointed director in March 2004. Ms. Cico has been CEO of Brasil Telecom since 2001. She has been working in the telecommunications sector for over 19 years, in the areas of strategy, equipment and operations. Ms. Cico is a mem-ber of the London Business School’s Regional Advisory Board. She obtained a MBA from London Business School. In August 2004 Ms. Cico ranked 75th in Forbes Magazine’s “100 Most Powerful Women” and in October was selected by Fortune Magazine as the 25th among the world’s 50 most powerful women in international business.

Pierre-Alain De Smedt (12). Pierre-Alain De Smedt was appointed director in March 2004. Mr. De Smedt was appointed Executive Vice President of Renault in 1999. He was chairman of Autolatina, VAG and Ford’s joint venture subsidiary in Latin America. He served as Chairman of Volkswagen Brazil and Argentina before being appointed as Chairman of Seat. Mr. De Smedt is member of the Board of Deceuninck Plastics Group and also of Compagnie Nationale à Portefeuille. He is a graduate in engineering and eco-nomics from the University of Brussels (ULB).

Carine Doutrelepont (6). Carine Doutrelepont was appointed director in March 2004. Ms. Doutrelepont is a partner at the Belgian law firm of Uyttendaele, Gérard & Doutrelepont and is specialized in information technology, intellectual property, media law and competition matters. She is a member of the Belgian Competition Authority. She holds a PhD in law from the University of Brussels (ULB) where she currently holds tenure as a Professor of Media Law, Intellectual Property Law, Electronic Commerce Law and European Audiovisual Law. She is also Director of the Information and Communication Law Centre of the ULB.

Philip Hampton (3). Philip Hampton was appointed director in March 2004. He spent the first ten years of his career at Lazard Brothers in London, New York and Paris. He then took up the posi-tions of Finance Director for British Steel plc, British Gas plc and British Telecommunications Group plc and for Lloyds TSB Group plc. He is currently Chairman of J. Sainsbury plc. Mr. Hampton is a Chartered Accountant and holds an MBA from INSEAD, Fontainebleau.

Georges Jacobs (15). Baron Georges Jacobs was appointed director in March 2004. Mr. Jacobs is a Chairman of the Board of Directors of UCB. He commenced his career as an economist

at the International Monetary Fund (USA). Later, he joined the UCB Group and was appointed as a Director of UCB in 1987. Furthermore, Baron Jacobs is member and Chairman of the Board of Delhaize, and a member of the Board of Bekaert and SN Brussels Airlines. He holds a law degree and a degree in economics, as well as a Master of Arts in Economics from the University of California, Berkeley.

Maurice Lippens (not on the picture). Count Maurice Lippens was appointed director in March 2004. Mr. Lippens is co-founder of Fortis, created in 1990 and the first European cross-border bank-ing and insurance group. He served as the executive Chairman of Fortis until 2000 and since then he is the non-executive Chairman of the Board of Directors. He is a member of the Board of several companies including Suez-Tractebel, Groupe Bruxelles Lambert and Total. He holds a law degree from the University of Brussels (ULB) as well as an MBA from Harvard Business School.

Oren G. Shaffer (7). Oren G. Shaffer was appointed director in April 2004. He is Vice Chairman and Chief Financial Officer of Qwest Communications International Inc. Formerly Mr. Shaffer was President and Chief Operating Officer of Sorrento Networks and from 1994 to 2000 he was Chief Financial Officer of Ameritech. He holds a Bachelor of Science in business administration from The University of California at Berkeley and a Master of Science in management from The Massachusetts Institute of Technology.

Philippe Van de Vyvere (not on the picture). Philippe Van de Vyvere was appointed director in March 2004. Mr. Van de Vyvere is the founder, CEO and Chairman of Sea-Invest, Europe’s largest bulk and fruit transshipment company. He is currently a non-executive board member for ING Belgium. Mr. Van de Vyvere holds a degree in Economics.

Lutgart Van den Berghe (11). Prof. dr. Lutgart Van den Berghe was appointed director in March 2004. Ms. Van den Berghe holds a PhD in economics from Gent University. As Executive Director, she heads the Competence Centre Entrepreneurship, Governance and Strategy at the Vlerick Leuven Gent Management School as well as the Belgian Directors’ Institute. She is a professor at Gent University, where she lectures on corporate governance and serves as a non-executive director in a number of listed and non-listed multinational companies such as Electrabel, CSM (The Netherlands), SHV Holding (The Netherlands) and Solvay BV (The Netherlands).

Roger De Borger (1). Government Commissioner.

14

Nomination and Remuneration CommitteeThe Nomination and Remuneration Committee (NRC) consists of

four directors. Pursuant to its charter, this committee is chaired by

the Chairman of the Board of Directors, who is an ex-officio mem-

ber. One member is chosen from among the directors appointed

by the Belgian State. Two members must be appointed among the

independent directors.

The Nomination and Remuneration Committee’s role is to assist

and advise the Board of Directors regarding:

• the nomination of candidates for appointment to the Board of

Directors and the Board Committees;

• the appointment of the President and Chief Executive Officer and

appointment by the President and Chief Executive Officer of the

members of the Management Committee;

• the remuneration of the members of the Board of Directors and

the Board Committees (legal duties and others);

• the remuneration of the President and Chief Executive Officer

and members of the Management Committee; the review on

an annual basis of the remuneration philosophy and strategy of

all personnel and specifically the compensation packages of top

senior management; and

• the oversight of the decisions of the President and Chief

Executive Officer with respect to the appointment, the dismissal

and the compensation of management, in order to allow the

Board of Directors, when it chooses to do so, to exercise its overall

supervising duties.

In its session of October 2004, the Board of Directors decided to

extend the role of the Nomination and Remuneration Committee

and requested it to also assist and advise the Board of Directors

regarding Corporate Governance issues.

The Nomination and Remuneration Committee meets at least two

times annually.

Mr. Theo Dilissen (Chairman), Ms. Martine Durez, Mr. Georges

Jacobs and Ms. Lutgart Van den Berghe are the members of the

Nomination and Remuneration Committee.

Strategic and Business Development CommitteeThe Strategic and Business Development Committee (SBDC) consists

of five directors. Pursuant to its charter, the President and Chief

Executive Officer and the Chairman of the Board of Directors are

ex officio members, and the committee is chaired by the Chairman

of the Board of Directors. One additional member is chosen among

the directors appointed by the Belgian State. Two members must be

appointed from among the independent directors.

The Strategic and Business Development Committee’s role is to

assist and advise the Board of Directors on matters concerning the

Company’s general policy and strategy, as well as on major issues

regarding its strategic development.

The Strategic and Business Development Committee meets at

least two times annually.

Functioning of the Board of DirectorsThe Board of Directors meets whenever the interests of the company so require or at the request of at least two directors. In principle, the Board of Directors meets six times a year.

The agenda for each meeting contains items of an informational nature and items on which a decision must be made.

In principle, the Board’s decisions are made by a simple major-ity of the directors present or represented. For certain issues, a qualified majority is required. The Board of Directors has adopted a Board Charter which, together with the charters of the Board Committees, reflects the principles by which the Board of Directors and its Committees operate. The Board Charter provides, among other things, that important decisions should have broad support, understood as a qualitative concept indicating effective decision-making within the Board of Directors following a constructive dialogue between directors. They should be prepared by standing or ad hoc Board Committees having significant representation of non-executive, independent directors within the meaning of Article 524, § 4 of the Belgian Commercial Companies Code.

Committees of the Board of DirectorsThe Board of Directors adopted formal charters for its Committees at its meeting of 19 February 2004. Amendments to key prin-ciples with respect to the composition and core tasks of such Committees, as set out in their respective charters, require broad support within the Board of Directors.

Audit and Compliance CommitteeThe Audit and Compliance Committee (ACC) consists of five non-executive directors, the majority of whom must be independent. Pursuant to its charter, the ACC is chaired by an independent director.

The Audit and Compliance Committee’s role is to assist and advise the Board of Directors in its oversight of:• the quality and integrity of the statutory and the consolidated

annual accounts and the financial statements of the Company;• the relationship with the Company’s statutory auditors;• the Company’s internal audit function;• the Company’s compliance with legal and regulatory require-

ments; and• compliance within the Company with the Company’s Code of

Conduct and its Policies, which must include dealings in finan-cial instruments of the Company, equal opportunity treatment among the sexes and sexual harassment.

The Audit and Compliance Committee meets at least once every quarter.

Mr. Philip Hampton (Chairman), Messrs. Pierre-Alain De Smedt, Michel Moll, Oren G. Shaffer and Paul Van de Perre are the mem-bers of the Audit and Compliance Committee.

The President and CEO is invited to meetings to state the manage-ment’s view on audit findings.

15

Mr. Theo Dilissen (Chairman), Mr. Didier Bellens, Ms. Carla Cico and Messrs. Maurice Lippens and Robert Tollet are the members of the Strategic and Business Development Committee.

At times, the Committee invites other Board members to the meetings.

Changes in the composition of the Board of DirectorsIn addition to the changes in the composition of the Board of Directors that occurred on the occasion of the company’s IPO in March 2004, the following changes occurred at the level of the Board of Directors.

In conformity with his commitment, Mr. Lloyd Kelley resigned in April 2004, since ADSB Telecommunications BV retained less than 7.5% of the voting stocks after the IPO. The Board of Directors has filled the vacancy by appointing Mr. Oren Shaffer as independent director through cooptation, upon the recommendation of the Nomination and Remuneration Committee. The shareholders will be requested to ratify this appointment during their 13 April 2005 meeting.

Mr. Oren Shaffer is considered independent since he meets all the independence conditions of the Belgian Code on Corporate Governance.

In October 2004, Mr. Jan Coene resigned for personal reasons as member and Chairman of the Board of Directors.

The Belgian State appointed Mr. Theo Dilissen as member and Chairman of the Board of Directors.

Directors’ remunerationBy virtue of a decision taken by the General Meeting on 12 April 1995, members of the Board of Directors that were appointed by the Belgian State, with the exception of the President & CEO, have the right to an attendance fee of EUR 619.73 per meeting, up to a ceiling of EUR 9,915.74 a year. They also have the right to directors’ emoluments for an amount equal to the attendance fee.

On 19 February 2004, the General Meeting changed these directors’ remunerations and compensations as follows. An annual fixed com-pensation of EUR 50,000 for the Chairman of the Board of Directors and of EUR 25,000 for the other members of the Board of Directors, with the exception of the President & CEO, is foreseen. All members of the Board of Directors, with the exception of the President & CEO, have the right to an attendance fee of EUR 5,000 per attended meeting of the Board of Directors. Finally attendance fees of EUR 2,500 have been foreseen for each member, with the exception of the President & CEO, of an advising committee to the Board of Directors. For the Chairman these attendance fees are doubled.

For 2004, a total amount of EUR 1,011,000 has been paid out.

As of 2005, individidual compensation will be published in con-formity with the Code Lippens’ recommendations.

Activity report and attendance at Board and Committee meetings

NameBoard (total 6)

ACC (total 4)

NRC (total 10)

SBC (total 3)

Theo DILISSEN 2/2 2/2 1/1

Didier BELLENS 5/6 2/2

Johny CORNILLIE 6/6

Didier DE BUYST 6/6

Martine DUREZ 6/6 10/10

Michel MOLL 6/6 3/3

Robert TOLLET 6/6 3/3

Norbert VAN BROEKHOVEN 6/6

Paul VAN de PERRE 6/6 4/4

Carla CICO 4/5 3/3

Pierre-Alain DE SMEDT 3/5 2/3

Carine DOUTRELEPONT 5/5

Philip HAMPTON 5/5 3/3

Georges JACOBS 5/5 4/4

Maurice LIPPENS 3/5 2/3

Oren G. SHAFFER 5/5 2/3

Philippe VAN de VYVERE 4/5

Lutgart VAN den BERGHE 4/5 4/4

Jan COENE 4/4 1/1 8/8 2/2

James W. CALLAWAY 1/1

Sock Koong CHUA 1/1

Henning DYREMOSE 1/1

Lloyd KELLEY 2/2 5/6

Jonathan P. KLUG 1/1 1/1

Ho Kee LIM 0/1

Hans MUNK NIELSEN 1/1

J. Kenneth RALEY 1/1

Hang Boon SIN 1/1

The IPO resulted in an important change in the composition of the

Board of Directors. Representatives of ADSB Telecommunications

BV resigned at the occasion of the IPO and hence were only invited

to one (or for Mr. Lloyd Kelley two) Board meeting(s) in 2004.

Transactions between the company and its board members and executive managersA general policy on conflicts of interest is applicable within the

company. It prohibits the possession of financial interests that

may affect one’s personal judgment or professional tasks to the

detriment of the Belgacom Group.

In accordance with Article 523 of the Belgian Commercial

Companies Code, President & CEO Didier Bellens declared at the

16

1 2 3

19 February 2004 and 13 December 2004 Board of Directors meetings that he had a conflict of interest in connection with the Employee Incentive Plans item of the agenda of these Board meetings. He is in fact a proposed beneficiary of the Senior Management Long-term Incentive Plans 2004 and 2005 and the Short-term Incentive Plans 2004 and 2005.

Mr. Bellens has also been offered the opportunity to purchase shares at a discount under the Belgacom Discounted Share Purchase Plan 2004 (DSPP). He has informed Belgacom’s auditor of these conflicts of interests and has decided not to participate in the deliberation or voting on such items on the agenda.

Other members of the Belgacom Management Committee (BMC) are also proposed beneficiaries under the Senior Management Long-term Incentive Plans 2004 and 2005 and the Short-term Incentive Plans 2004 and 2005. Additionally, in the context of the 2004 DSPP, the BMC members have been offered the opportunity to purchase shares at a discount, just as any other employee of the Group.

Application of the measures taken by the company in order to comply with existing legislation on insider trading and market manipulation (market abuse)In order to comply with existing legislation on insider dealing and market manipulation, Belgacom adopted a dealing code prior to the IPO. This code aims at creating awareness about possible improper conduct by employees, officers and directors and the pos-sible sanctions attached thereto. This dealing code has been widely communicated and is available to all employees. A list of key per-sons is kept, and all directors and key employees were requested to sign a affidavit that they have read, understand and agree to comply with the dealing code. Closed periods (including prohibited periods) are defined, and any deal must be communicated to and cleared by the Head of Compliance Services before the transaction (see “Compliance” section p. 18).

ManagementPresident and Chief Executive OfficerThe President and Chief Executive Officer is entrusted with the day-to-day management and reports to the Board of Directors.

In addition, pursuant to the 1991 Law and the company’s Articles of Association, the Board of Directors may, deciding by a majority of two thirds of its members present or represented, delegate all or part of its powers to the President and Chief Executive Officer with the exception of:

• the approval of the Management Contract with the Belgian State and changes thereto;

• the establishment of the business plan and general policy of the company;

• the supervision of the President and Chief Executive Officer; and• other powers explicitly reserved by law to the Board of Directors

which include, for example, the establishment of the annual accounts for submission to the General Shareholders Meeting and the preparation of merger proposals.

The Board of Directors has delegated broad powers to the President and Chief Executive Officer.

The composition and, with the exception of certain specific pow-ers entrusted to the Management Committee by the 1991 Law, the powers of the Management Committee are determined by the President and Chief Executive Officer.

The President and Chief Executive Officer is appointed by the Belgian State by Royal Decree deliberated in the Council of Ministers for a renewable six-year term. The President and Chief Executive Officer and the Chairman of the Board of Directors must come from different language groups. The President and Chief Executive Officer may only be removed from office by Royal Decree deliberated in the Council of Ministers. Pursuant to the 1991 Law and the Company’s Articles of Association, the President and Chief Executive Officer is a member of the Board of Directors.

The current President and Chief Executive Officer is Mr. Didier Bellens.

Management CommitteeThe Management Committee’s role, apart from exercising the specific powers entrusted by the 1991 Law to the Management Committee, is to assist the President and Chief Executive Officer in the exercise of his duties. The Management Committee aims to decide by consensus, but in the event of disagreement, the view of the President and Chief Executive Officer will prevail. The Management Committee generally meets on a weekly basis. Pursuant to the 1991 Law and the Articles of Association, the President and Chief Executive Officer serves as a member of the Management Committee, which he chairs. There must be the same number of French-speaking members and Dutch-speaking members on the Management Committee, the President and Chief Executive Officer excepted in case of an uneven number. Members who are neither French-speaking nor Dutch-speaking shall not be taken into account for the calculation of this linguistic parity requirement.

The current members of the Management Committee are as follows:

17

4 5 6

Didier Bellens. Didier Bellens (49) was appointed as President and Chief Executive Officer and a director of Belgacom in March 2003. Previously Mr. Bellens served as the CEO of the RTL Group in Luxembourg and prior to that, as the CEO of the Group Bruxelles-Lambert. He holds a degree in Economics and Business Administration from the University of Brussels (ULB).

Scott Alcott (1). Scott Alcott (38) is Chief Operating Officer of Belgacom’s Fixed Line Services since July 2004. Previously, Mr. Alcott served as Belgacom’s Chief Strategy Officer, Chief Information and Technology Officer, General Manager of Marketing and Product Management, director at Skynet and director at Belgacom’s Multi-Media Venture Capital Fund. In 1995, Mr. Alcott joined Ameritech (now SBC) as Director of Marketing & Product Management – Long Distance Division, and later as Director of New Product Development/Packaging. Mr. Alcott holds a B.S. in Economics from the Wharton School at the University of Pennsylvania.

Bridget P. Cosgrave (2). Bridget Cosgrave (43) has served as the President of the International Carrier Services of Belgacom since 2001, and she joined the Board of Directors of Belgacom Mobile in 2004. From 1993 to 1996, Ms. Cosgrave was a Project Director at British Telecom Plc. In 1996, she was elected and served her full term as the Deputy Director General of the European Telecommunications Standards Institute (ETSI). Ms. Cosgrave has a B.A. (Hons.) from Queen’s University at Kingston, Canada and a MBA from the London Business School.

Astrid De Lathauwer (3). Astrid De Lathauwer (41) has served as Chief Human Resources Officer for Belgacom since 2002. Ms. De Lathauwer joined Belgacom in 2000 and previously held the positions of Top Group Resources & Talent Director and HR Director of Belgacom. Prior to joining Belgacom, Ms. De Lathauwer

worked in marketing and human resources with Monsanto. Ms. De Lathauwer holds a degree in History of Art from the University of Gent and a degree in International Politics and Diplomatic Sciences from the University of Leuven.

William Mosseray (4). William Mosseray (40) was appointed Chief Strategy Officer in July 2004 and has served as Belgacom’s Chief Restructuring and Change Officer since 2002. Mr. Mosseray joined Belgacom in 1993 and has served as Executive Advisor to the CEO, General Manager for the Special Business Division, Head of Corporate Strategy & Development and Chief Human Resources Officer. He obtained a law degree from the University of Leuven and a tax law degree from ICHEC. Mr. Mosseray also holds an MBA from the Vlerick Leuven Gent Management School.

Ray Stewart (5). Ray Stewart (55) has served as the Chief Financial Officer of Belgacom since 1997. Mr. Stewart was employed by SBC, but became an employee of Belgacom on 1 April 2004. From 1994 to 1997, Mr. Stewart was the CFO of Matav, a Hungarian telecom oper-ator in which Ameritech bought a shareholding. Mr. Stewart holds an undergraduate degree in Accounting and an MBA in Finance from Indiana University and is a certified public accountant.

Philippe Vander Putten (6). Philippe Vander Putten (45) has served as the CEO of Belgacom Mobile since 1998 where he is also an executive director, since 1998. Mr. Vander Putten started his professional career at Procter & Gamble, working in the FMCG sector at L’Oréal. In 1986, Mr. Vander Putten joined the Kraft Jacobs Suchard Group (now Kraft Foods) and held several positions in Marketing & Sales before becoming the Managing Director of Kraft General Foods for Benelux in 1991. Mr. Vander Putten holds a bachelor’s degree and a master’s degree in administration and management from the University of Leuven.

Belgacom Management Committee

18

Compensation of the members of the Management CommitteeThe total amount paid to members of the Belgacom Management Committee (BMC) as a whole, including the President & CEO, amounted to EUR 4,897,000 in the year ending 31 December 2004. The members of the Belgacom Management Committee are Ms. B. Cosgrave, Ms. A. De Lathauwer and Messrs. D. Bellens, R. Stewart, Ph. Vander Putten, W. Mosseray and S. Alcott. This total covers the pecuniary benefits, both direct or immediate (basic pay, variable pay) and indirect (insurance, long-term profit-sharing scheme), which are related directly to the office held or which are awarded to members of the BMC.

In addition to these pecuniary benefits, the BMC as a whole, including the President & CEO, participated in the Discounted Share Purchase Plan (510,410 shares bought at an introduction price of EUR 24.50 with a discount of 16, 66 %) and the Employee Stock Option Plan (355,581 stock options acquired at a strike price of EUR 24.50).

As of 2005, compensation details of members of the Management Committee will be published in conformity with the Lippens Code recommendations.

Board of AuditorsThe Board of Auditors of the company is composed of the follow-ing persons:• ERNST & YOUNG Reviseurs d’Entreprises S.C.C.R.L./

Bedrijfsrevisoren B.C.V.B.A., represented by Ludo Swolfs, also Chairman of the Board of Auditors

• Romain LESAGE, Member of the Court of Auditors, Commissaire• Pierre RION, Member of the Court of Auditors, Commissaire• CALLENS, GUEVAR, VAN IMPE & Co S.C.C.R.L./B.C.V.B.A., repre-

sented by Herman VAN IMPE, Commissaire

Ernst & Young is responsible for the audit of the consolidated financial statements of Belgacom and its subsidiaries. The other members of the Board of Auditors are, together with Ernst & Young, entrusted with the audit of the non-consolidated financial statements of the parent company.

Mr. Lesage’s mandate will expire on 30 June 2008, the mandates of Mr. Rion, Ernst & Young, and Callens, Guévar, Van Impe & Co. will expire at the annual General Shareholders Meeting in 2010.

Additional fees paid to the statutory auditorsIn accordance with the provisions of Article 134 § 2 of the Belgian Company Law, Belgacom declares the supplementary fees that it granted during the 2004 financial year to two auditors, mem-

bers of the Joints Auditors: Ernst & Young Reviseurs d’entreprises S.C.C.R.L. and Callens, Guevar, Van Impe & Co. S.C.C.R.L.

The overview of the subject and the remuneration linked to excep-tional assignments executed by the auditors within Belgacom SA under public law or a Belgian enterprise affiliated to Belgacom SA under public law in the sense of article 11 or a foreign affiliate is as follows:• to Ernst & Young Reviseurs d’entreprises: EUR 1,026,330 for

control assignments concerning the initial public offering, EUR 350,218 for other control assignments and EUR 6,250 for other assignments within Belgacom SA under public law and EUR 39,000 for other control assignments in affiliated enterprises in Belgium;

• to other members of the Ernst & Young network: EUR 20,758 for other assignments in foreign affiliates;

• to Callens, Guevar, Van Impe & Co.: EUR 5,750 for other control assignments in Belgacom SA under public law.

Government CommissionerThe State has appointed Mr. Roger De Borger as Government Commissioner in order to supervise, in conformity with the 1991 law, the management of Belgacom from an administrative point of view.

ComplianceTowards more transparencyBelgacom has consistently considered compliance as an important part of sound corporate governance. As early as 1998, it introduced a code of conduct, and today more than 40 policies have been implemented in matters as diverse as competition law, e-mail usage and business continuity management.

Aware that it is operating in an increasingly complex regulatory environment and because of the legitimate high expectations of its customers, shareholders and other stakeholders, Belgacom has decided to integrate these different existing initiatives into one central Compliance Office, as of 1 October 2004.

Furthermore, various public initiatives such as the Sarbanes Oxley Act in the United States and the European Union action plan on enhancing corporate governance have in the meantime further strengthened the case for a coherent compliance approach. In Belgium, this was also the case with the publication of the “Belgian Code on Corporate Governance” (Lippens Code).

19

Belgacom Compliance OfficeSince the IPO of 22 March 2004, compliance is defined at the Belgacom board level, in the Audit & Compliance Committee (ACC).

In the ACC Charter, the ACC has been given the responsibility of regularly reviewing Belgacom’s compliance with legal/regulatory requirements and the Belgacom Group’s codes of conduct and policies.

The Belgacom SA Code of Conduct and a set of 40 policies provide guidelines to employees so as to clarify what is expected from them in given situations. The guidelines cover all fields of the business, including customer and business relations, corporate culture, assets and corporate citizenship. A similar structure is in place at Belgacom Mobile.

The Compliance Office began operations on 1 October 2004, building upon the existing Code and Policies team. The ACC has appointed a senior executive as Head of Compliance Services, with a direct reporting line to the ACC Chairman and to the President and CEO.

A Group Compliance Council has been set up. It meets quar-terly under the presidency of the Head of Compliance Services and is composed of key executives from Internal Audit, Risk Management, Human Resources, Corporate Communications, Internal Services, Belgacom Mobile and BICS.

Rules, tools and consistencyIt is every employee’s personal responsibility to ensure that the company and its employees comply with the internal and external rules and regulations. Belgacom’s compliance office has three responsibilities: to clarify the rules, to provide tools and to ensure consistency.• In the identified compliance areas, the compliance office ensures

that the rules, as set by the area owners and endorsed by man-agement, are clearly defined, properly communicated and easily accessible.