Embed Size (px)

Citation preview

Annual Report 2000.

1

CONTENTS.

Investkredit at a glance. ................................................................................................. 2

Income development of the Investkredit Group 1996 – 2000. .................................... 3

Key figures of the Investkredit Group 1996 – 2000. .................................................... 4

Letter from the Board of Management. ....................................................................... 5

Policy-making bodies. .................................................................................................... 8

Supervisory Board. ..................................................................................................... 8

State Commissioner. .................................................................................................. 9

Board of Management. ............................................................................................. 9

Organizational chart. ................................................................................................... 10

Investkredit shares. ...................................................................................................... 11

Management discussion. ............................................................................................. 13

Investkredit Group. ................................................................................................. 13

Development of earnings. ...................................................................................... 16

Total assets and capital development. ................................................................... 18

Outlook for 2001. .................................................................................................... 19

Segment reporting according to IAS. .......................................................................... 21

Enterprises. .............................................................................................................. 21

Financing and aid. .............................................................................................. 21

Corporate finance, private equity and counselling. ........................................ 26

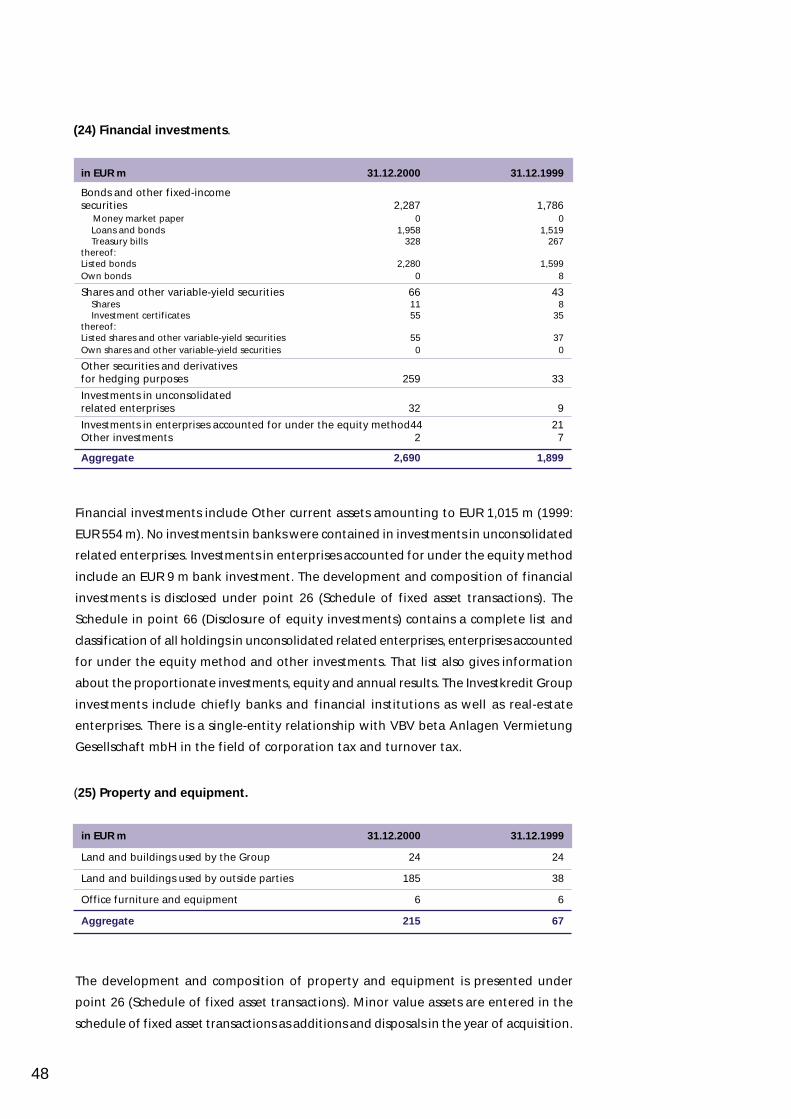

Financial asset management. ............................................................................ 28

Treasury. .............................................................................................................. 30

Local government. ................................................................................................... 32

Real estate. .............................................................................................................. 34

Financial statements of the Investkredit Group for 2000. ......................................... 36

Balance sheet. .......................................................................................................... 36

Income statement. ................................................................................................... 37

Statement of changes in equity. ............................................................................. 38

Cash flow statement. .............................................................................................. 39

Notes to the financial statements of the Investkredit Group. .............................. 40

Accounting principles. ....................................................................................... 40

Information on the balance sheet. ................................................................... 46

Information on the income statement. ............................................................ 55

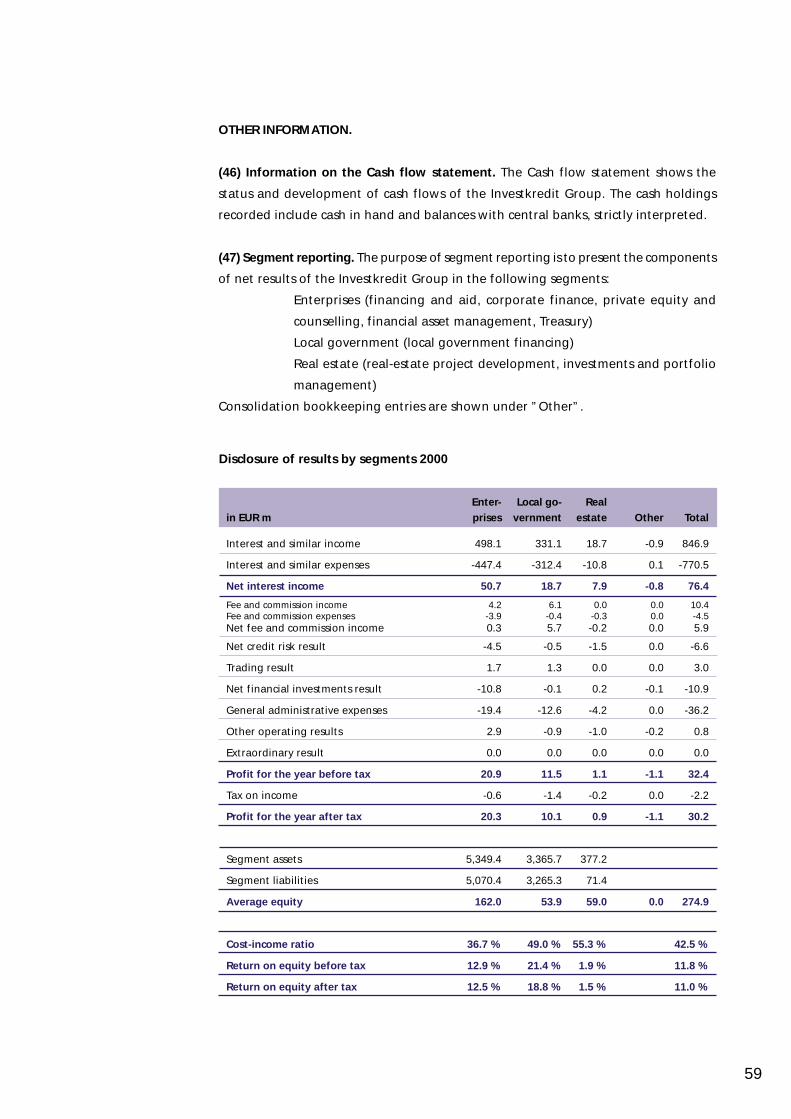

Other information. ............................................................................................ 59

Audit certificates pursuant to § 245a of the Austrian Commercial Code. ........... 73

Report of the Supervisory Board. ................................................................................ 74

Glossary of important technical terms. ....................................................................... 75

Our photographic presentation. .................................................................................. 83

2

Investkredit shares.

2000 1999 Change

Earnings per share (in EUR) 42.28 27.33 +55 %

Dividend per share (in EUR) 8.72 8.72

Year-end price (in EUR) 350.00 325.50 +7 %

High 360.25 331.50

Low 325.50 318.73

Market capitalization (in EUR m) 221.6 206.0 +7 %

Price-earnings ratio 8.3 11.9

Investkredit Group.2)

2000 2000 1999 1999 ChangeEUR ATS3) EUR ATS

m m m m

Net interest income 76.4 1,052 62.1 854 +23 %

Profit for the year before tax 32.4 445 24.3 334 +33 %

Profit for the year after tax 30.2 415 19.5 268 +55 %

Total assets 8,703.4 119,762 6,920.4 95,227 +26 %

Financing4) 7,437.8 102,346 5,896.1 81,183 +26 %Core capital (Tier 1) pursuant tothe Austrian Banking Act 272.0 3,742 247.5 3,406 +10 %

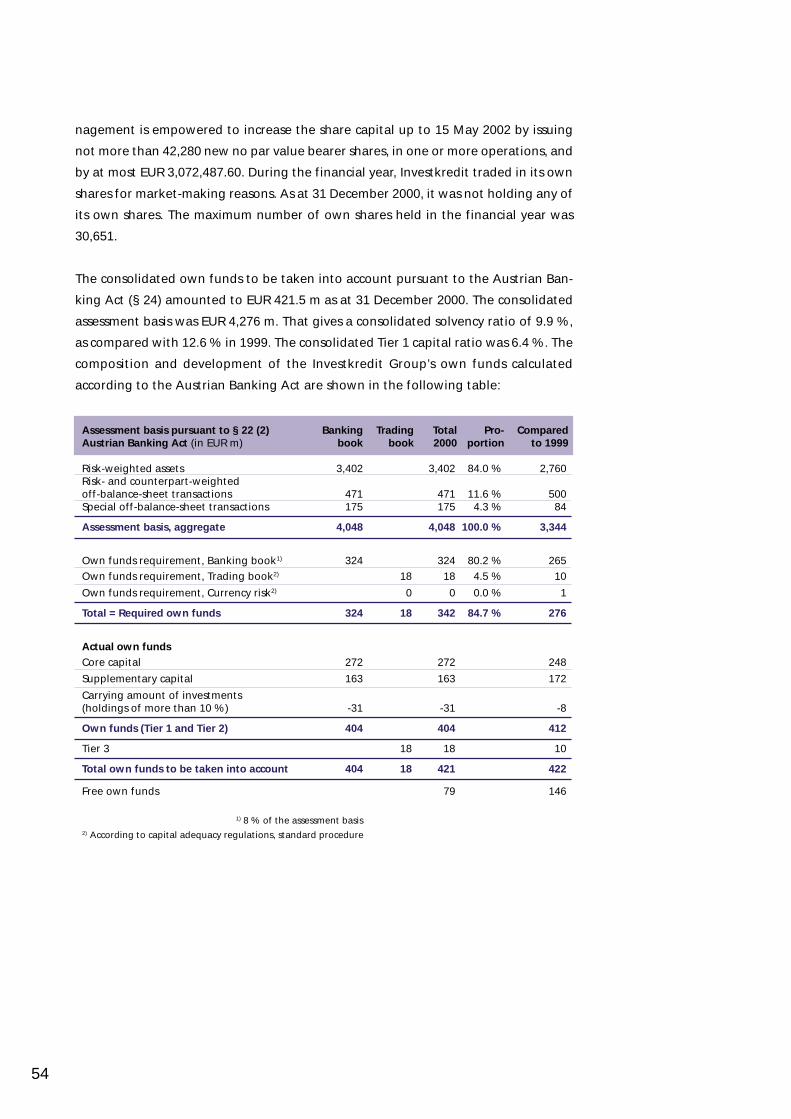

Own funds (Tier 1 + 2 + 3) pursuantto the Austrian Banking Act 421.5 5,800 422.0 5,807 - 0 %

Total capital ratio 9.9 % 12.6 %

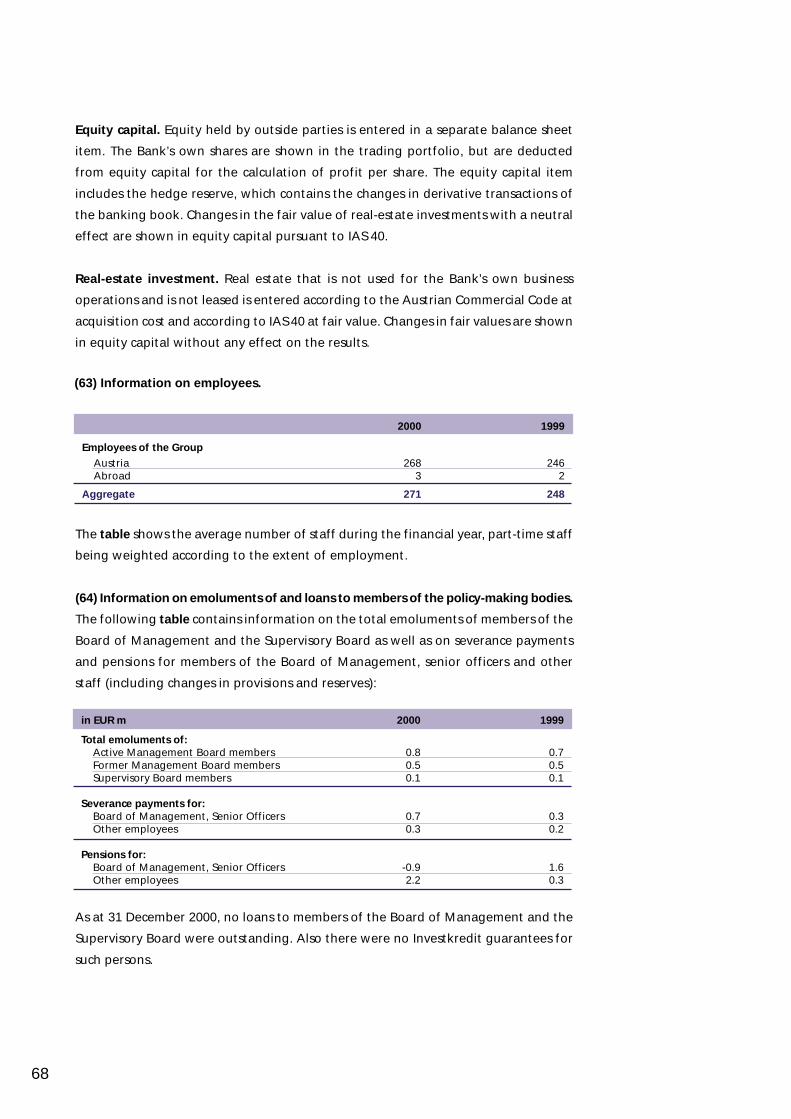

Number of employees (year-end) 290 269 +8 %

2) In this Annual Report, totals may not add precisely because of rounding3) The 2000 Annual Report has been drawn up in EUR. The ATS figures have been converted4) Loans and advances to customers, provision for guarantees and trust loans as well as bonds and

other fixed-interest securities of other non-bank issuers

Rating.

Moody’s Investors Service long-term short-term

Investkredit Bank AG A1 P-1

Kommunalkredit Austria AG A1 P-1

INVESTKREDIT AT A GLANCE.

3

INCOME DEVELOPMENT OF THEINVESTKREDIT GROUP 1996 – 2000.

65 %

60 %

55 %

50 %

45 %

40 %

35 %

30 %

25 %

16 %

12 %

8 %

4 %

0 %1996 1997 1998 1999 2000

Cost-income ratio Return on equity

Cost-income ratio

Return on equity

53.6

1.7 %

11.8 %

14 %

10 %

6 %

2 %

52.6 52.654.0

42.55.9 %6.3 %

9.9 %

40

35

30

25

20

15

10

5

0

1.2 %

0.9 %

0.6 %

0.3 %

0.0 %1996 1997 1998 1999 2000

in EUR m Return on assets

Profit for the year before tax

Profit for the year after tax

Return on assets

2.5

24.3

3.40.14 %

0.85 %

8.9

0.46 %

10.3

13.7

0.51 %

30.2

19.5

0.80 %

32.4

11.9

4

KEY FIGURES OF THE INVESTKREDIT GROUP1996 – 2000.

HGB HGB HGB IAS IAS

1996 1997 1998 1999 2000

Net interest income (in EUR m) 43.9 49.3 51.1 62.1 76.4

Profit for the year before tax (in EUR m) 3.4 11.9 13.7 24.3 32.4

Profit for the year after tax (in EUR m) 2.5 8.9 10.3 19.5 30.2

Core capital (Tier 1) pursuant to theAustrian Banking Act (in EUR m) 194.2 209.0 227.9 247.5 272.0

Own funds (Tier 1 + 2 + 3) pursuant to theAustrian Banking Act (in EUR m) 286.0 330.4 372.2 422.0 421.5

Total assets (in EUR m) 4,209.6 4,750.1 5,298.4 6,920.4 8,703.4

Employees (year-end) 225 232 244 269 290

Market capitalization (in EUR m) 157.2 187.7 204.7 206.0 221.6

Total capital ratio 11.2 % 12.7 % 13.2 % 12.6 % 9.9 %

Core capital ratio 7.6 % 8.1 % 8.1 % 7.4 % 6.4 %

Interest margin1) 1.09 % 1.10 % 1.02 % 1.02 % 0.98 %

Operating income per employee (in EUR m) 0.26 0.26 0.26 0.24 0.29

Cost-income ratio2) 53.6 % 52.6 % 52.6 % 54.0 % 42.5 %

Return on assets3) 0.25 % 0.46 % 0.53 % 0.80 % 0.85 %

Return on equity4) 1.7 % 5.9 % 6.3 % 9.9 % 11.8 %

Return on equity after tax5) 1.3 % 4.4 % 4.7 % 8.0 % 11.0 %

Earnings per share (in EUR) 10.7 13.6 14.2 27.3 42.3

Owing to the application of IAS, the figures for 1996 to 1998 are only partly comparable

1) Ratio of net interest income to average total assets2) Ratio of administrative expenses to income3) Ratio of net income before tax to average risk-weighted assets4) Ratio of net income before tax to average equity5) Ratio of net income after tax to average equity

5

LETTER FROM THE BOARD OFMANAGEMENT.

This financial statement is a “first” in two respects. To begin with, the results of the

Bank for Corporates are expressed in euros and also, for the first time, the IAS (Inter-

national Accounting Standards) rules have been adopted in the balance sheet. The

significance of these two innovations certainly goes beyond the related accounting

and presentation challenges.

Euro and IAS represent a basic transformation of our financing culture. The European

Union currency creates absolutely new possibilities, because it transforms previously

fragmented capital markets into an extremely liquid all-European financial market.

Thereby, instruments that have been in common use for many years in Anglo-Ameri-

can financing business are now also available in continental Europe.

The intensive growth of the markets for corporate bonds and equity instruments –

ranging from venture capital and subordinated financing (mezzanine capital) to stock

exchange placements – reflects this trend.

Long-term lending, for which a pan-European market is also evolving, also faces new

conditions after the elimination of currency frontiers, including the expectation of

new capital requirements for lending banks. This will in future lead to a more marked

differentiation of risk and capital costs according to customer ratings and the matu-

rity period of commitments.

The significance of external and internal ratings is distinctly increasing and is also

becoming more and more significant for medium-sized manufacturing enterprises, if

they wish to enter the capital market with bonds or planned stock exchange listings.

Fears that the financing of medium-sized enterprises is in jeopardy owing to the

reorientation of banks according to rating categories are in our view, however, just as

unjustified as exaggerated euphoria with regard to the newly accessible financing

products.

A decisive factor in applying the new rules on the European financial market is to

ensure that they are implemented for the benefit of corporate customers. In the final

analysis – as is shown not least by the drastic market movements in the so-called new

economy – the new financing world will in essence not be much different from the

old.

In all individual discussions with our customers, we therefore consistently seek solu-

tions that best support the corporate aims of long-term stability and autonomy, de-

pending on the available scope for risk-taking and financing.

6

Alfred Reiter

The year under review has shown

that this approach by Investkredit

as the Bank for Corporates is fully

accepted by our customers and

market partners. Competency

teams of the Bank have success-

fully translated their skills into

concrete results: from the reorgan-

ized Enterprise Financing Depart-

ment to Corporate Finance, the

Mezzanine Fund and the equity

funds, from Treasury with its risk-

hedging instruments to the coun-

selling services of Europa Consult.

In the international area, we have

continued to expand our struc-

tured bond portfolio both in the

USA and Europe. In parallel, the

high-quality Europolis real estate

portfolio was further developed in

EU candidate country capitals.

Our purpose in developing project financing into a separate business segment is to

assist our customers more systematically than before in their international investment

projects. Also, special bank representative offices are to make the entire range of

bank services available in individual target markets.

New media facilities for our customers have also been distinctly expanded. InvestDirekt

(www.investdirekt.at) provides direct access to accounts and deposits. Up-to-date serv-

icing with data on money and foreign currency has been supplemented with a direct

transaction platform (www.investdirektfx.at). Investkredit’s internet presence

(www.investkredit.at) has also been modernized and enlivened. We regard this as a

major step towards intensifying information for investors, which should improve trad-

ing openings for our shares in the specialist market of the Vienna Stock Exchange. At

the moment, the price movements of Investkredit shares do not adequately reflect

the growth in the value of the Bank because of the low liquidity of these securities.

Nevertheless, at the end of the year, the price-earnings ratio of the share stood at 8.3,

which is an attractive value for bank securities. Not only to Investkredit Bank AG itself

but also, and prominently, Kommunalkredit Austria AG and Investkredit International

Bank p.l.c., Malta, as well as to other successful subsidiaries of the Group produced

the positive performance underpinning this Investkredit Group value.

7

Wilfried Stadler

The capital increase in

Kommunalkredit that was carried

out at an attractive valuation by

the Franco-Belgian Dexia Group,

the market leader in European lo-

cal government financing, is grati-

fying confirmation of the

Investkredit Group’s specialist

bank focus. We welcome the deci-

sion of this strategic partner to ex-

pand its activities in Central and

Eastern Europe in full partnership

with Investkredit. The first result

has been the acquisition of the PBK

bank in Slovakia, in which

Investkredit held an overall

31.36 % investment via a holding

company at the end of the year

2000.

In the reporting year, we also

worked consistently to ensure

greater value for money for our

customers by increasing cost-effectiveness. Thus, the cost-income ratio was improved

despite a larger payroll, and the proportion of personnel and administrative expenses

that were necessary to generate income was reduced. With a new boost in return on

equity before tax (ROE) from 9.9 % to 11.8 %, we are further improving capital yield

in the interests of our shareholders.

Precisely in periods of upheaval in financial markets, specialization proves to be the

right way forward for the Investkredit Group. Together with our staff, whom we thank

for their commitment and personal competence, we intend to continue this develop-

ment to the satisfaction of our customers and shareholders.

Alfred Reiter Wilfried Stadler

8

POLICY-MAKING BODIES.

Supervisory Board.

Geiserich E. Tichy

Chairman

Karl Samstag

Vice-Chairman

Vice-Chairman of the Board of Management

Bank Austria AG

Karl Sevelda

Vice-Chairman

Member of the Board of Management

Raiffeisen Zentralbank Österreich

Aktiengesellschaft

Elisabeth Bleyleben-Koren

Vice-Chairperson (to 24 May 2000)

Vice-Chairperson of the Board of Manage-

ment, Erste Bank der oesterreichischen

Sparkassen AG

Helmut Elsner

Chairman of the Board of Management

Bank für Arbeit und Wirtschaft

Aktiengesellschaft

Max Kothbauer

(to 31 December 2000)

Vice Chairman

(from 24 May 2000 to 31 December 2000)

Chairman of the Board of Management

Österreichische Postsparkasse

Aktiengesellschaft

(to 1 December 2000)

Klaus Haberzettl

Head of Division

Commercial Customers 1, Bank Austria AG

Herwig Hutterer

Manager, Finanzierungsgarantie-

Gesellschaft m.b.H.

(to 30 June 2000)

Heinz Kessler

Chairman of the Board of Management

Nettingsdorfer Papierfabrik AG

Kurt Löffler

Manager, ERP Fund

Regina Prehofer

Head of Division, International

Groups, Corporate Finance and

Foreign Trade, Bank Austria AG

Gerhard Tanew-Iliitschew

Head of Division, Raiffeisen Zentralbank

Österreich Aktiengesellschaft

Klaus Thalhammer

Chairman of the Board of Management

Österreichische Volksbanken-AG

Wolfgang Agler

Employees‘ representative

Gabriele Bauer

Employees‘ representative

Regina Frick

Employees‘ representative

Otto Kantner

Employees‘ representative

Peter Wimmer

Employees‘ representative

9

State Commissioner.

Board of Management.

Alexander Gancz Kurt Bayer

State Commissioner Deputy State Commissioner

Director Head of Department

Federal Ministry of Finance Economic Policy and Integration

Federal Ministry of Finance

Alfred Reiter Wilfried Stadler

CEO and Chairman Member of the Board of Management

“invest.outlook panel“

10

ORGANIZATIONAL CHART.

Member of the Board ofManagement

Wilfried StadlerTel. 53 1 35 Ext. [email protected]

Enterprise Financing

Claudia Schmied Ext. [email protected] Riess Ext. [email protected]

International Business andFinancial Asset Management

Walter Anscheringer Ext. [email protected]

International BusinessJohannes Wundsam Ext. [email protected]

International Project Financingand Representative OfficesMichael Smutny Ext. [email protected]

Financial Asset ManagementThomas Heinisch Ext. [email protected]

Business Analysis and Technical Consulting

Klaus Gugglberger Ext. [email protected] Ehringer Ext. [email protected] Mayer Ext. [email protected]

Corporate FinanceGerhard Ehringer Ext. [email protected]

Financial AnalysisBernhard Mayer Ext. [email protected]

Technical Consulting and Real EstateJohann Salzmann Ext. [email protected]

CEO & Chairmanof the Board of Management

Alfred ReiterTel. 53 1 35 [email protected]

Treasury

Peter Tschusch [email protected] Hochgatterer [email protected]

Money and currency market dealingsAlfred Buder [email protected]

Capital marketRita Hochgatterer [email protected]

HandlingFerdinand Dietersdorfer [email protected]

Legal Department

Stefan Süssenbach [email protected] Hanzl [email protected]

Organization and Controlling

Julius Gaugusch Ext. [email protected] Grechenig Ext. [email protected]

User Service andOrganization DevelopmentGottfried Grechenig Ext. [email protected]

ITHeinz Polke Ext. [email protected]

Accounts, Taxation andControllingGerald Stich Ext. [email protected]

Board of Management

Internal Audit

Anton Taubenschuss Ext. [email protected] Angerer Ext. [email protected]

Personnel

Karl Öckher Ext. [email protected] Wimmer DW [email protected]

Corporate Communications

Hannah Rieger Ext. [email protected]

Company Secretary andInternational Relations

Margot Binder Ext. [email protected]

11

Key data per share As at 31 December 2000

Share capital EUR 46,000,110

Shares outstanding 633,000

Securities code number 74810

ISIN Code AT0000748108

Reuters OIKV.VI

Bloomberg OEIKAVEquity

Shareholders

BA/CA Group 24.8 %

BAWAG/P.S.K. Group 21.3 %

RZB 15.6 %

Erste Bank 11.3 %

Wiener Städtische 7.1 %

ÖVAG 3.4 %

Other Banks 3.1 %

Shares widely held, especially 13.4 %by industrial enterprises

100.0 %

INVESTKREDIT SHARES.

Important information on Investkredit shares. The Investkredit shares are listed in the

specialist market of the Vienna Stock Exchange. The share capital remained unchanged

in the reporting year at some EUR 46 m. Conversion of the ordinary capital to euros

was undertaken in 1999. The Annual General Meeting of 24 May 2000 empowered

Investkredit Bank AG to hold own shares for trading purposes up to a level of 5 %.

Earnings per share were increased in

2000 to EUR 42.3, and the price/earn-

ings ratio – 11.9 at the end of 1999 –

was sharply improved to 8.3 by the end

of 2000. The carrying amount per share

at year-end 2000 was EUR 464.72. As a

result of the increased stock exchange

price, market capitalization rose from

EUR 206 m to EUR 222 m.

Stable shareholder structure. The chief

shareholders of Investkredit are all the

major Austrian banking groups. The

special task of the Bank and its broad-

based shareholder structure determine

its neutral sectoral position towards the

universal banks. Some 13 % of the

shares are held by industrial enter-

prises, private shareholders and staff of

the Bank. More shareholders were won

in the year 2000 through a staff sub-

scription drive.

Share markets 2000. The year 2000 was a turbulent period on the international share

markets. After high gains in the first three months for growth and technology stocks,

telecom and media shares, there was a turnaround against the background of persist-

ent losses by Internet enterprises and costs for UMTS licences and telecom takeovers.

Some “new economy” stocks that had earlier been much overvalued fell dramatically.

For the first time in years, the share markets thereby developed less favourably in

many countries in 2000 than the markets for government bonds. With a share index

performance of minus 11 %, the negative experience of other European bourses has

been echoed in Vienna, though it could not build on a comparably profitable past.

The market capitalization of the Vienna Stock Exchange (A-market and specialist mar-

ket), namely, some EUR 27 bn as at 28 December 2000, indicates the bourse’s subordi-

12

1st quarter result 23 May 2001

AnnualGeneral Meeting 23 May 2001

Ex-date 30 May 2001

Dividend payment date 30 May 2001

1st half-year result 3 August 2001

1st -3rd quarter results 23 November 2001

Financial market calendar 2001

Investkredit Bank AG shares (EUR)*

ATX index (EUR)*

112.00

110.00

108.00

106.00

104.00

102.00

100.00

98.00

96.00

94.00

92.00

90.00

88.00

86.00

84.00

1/00 2/00 3/00 4/00 5/00 6/00 7/00 8/00 9/00 10/00 11/00

1.1.2000 - 31.12.2000

* Standardized presentation

12/00

nate importance in the European context. The profit outlook for some financial shares

remained positive, however, even in a difficult environment. With a price increase of

7 %, Investkredit shares performed better in the year 2000 than the overall share

index on the Vienna Stock Exchange.

EUR 5,687,414.54, be used to pay a

dividend of EUR 8.72 per share. The

resulting total distribution is

EUR 5,519,760.00, or some 12 % of

the 2000 dividend-bearing capital

of EUR 46,000,110.00. By reference

to the Investkredit share price of

EUR 350.00 as of 28 December

2000, that gives a 2.5 % dividend

yield.

Proposal for the distribution of the profit. The Board of Management proposes to the

Annual General Meeting of 23 May 2001 that the net annual profit for 2000, namely,

13

MANAGEMENT DISCUSSION.

Investkredit Group.

Enterprises Local GovernmentINVESTKREDIT

Board of ManagementAlfred ReiterWilfried Stadler

INVEST EQUITY

Board of ManagementHelmut BousekMartin Prohazka

INVEST EQUITYEARLY STAGE

Board of ManagementBurkhard FeursteinMartin Prohazka

INVEST MEZZANIN

ManagersGerhard EhringerOliver Grabherr

INVESTKREDITINTERNATIONAL BANK

Board of DirectorsJohn ButtigiegWalter AnscheringerThomas HeinischJoseph Said

VBV AG

Board of ManagementJulius GauguschStefan Süssenbach

VBV HOLDING

ManagersJulius GauguschKlaus GugglbergerStefan Süssenbach

EUROPA CONSULT

ManagersGerhard EhringerKlaus GugglbergerHeike Jandl

EUROTECHMANAGEMENT

ManagersJosef ErnstAndreas Gotwald

KOMMUNALKREDIT

Board of ManagementReinhard PlatzerGerhard Gangl

PRVA KOMUNALNABANKA A.S.

Board of ManagementJozef MihalikGernot DaumanFrancis Teynier

Real EstateEUROPOLISINVEST

ManagersWolfgang LunardonEduard KornfeldBernhard Mayer

EUROPOLIS CEHOLDING

ManagersEduard KornfeldWolfgang LunardonBernhard Mayer

Investkredit Bank AG 53 %

Kommunalkredit Austria AG 37 %

Investkredit International Bank p.l.c. 4 %

VBV AG 1 %

Other 5 %

Shares of the most important companiesin total assets for 2000

The Investkredit Group. Through

the activities of Investkredit and

its subsidiaries in the areas of spe-

cialist banking, equity invest-

ment financing, corporate fi-

nance and consultancy as well as

real estate, the Investkredit

14

Group covers practically all aspects of medium- and long-term enterprise and local

government financing. Investkredit Bank AG holds about 53 % of the Group’s total

assets. The International Accounting Standards (IAS) were adopted in the Investkredit

Group’s accounting in 2000. The relevant figures for the previous year were calculated

and verified. Also, accounts were changed from schillings to euros.

Strategy. Investkredit regards itself as a Bank for Corporates and as an independent

financial services provider. The Group is primarily concerned with Austrian enterprises

and local government bodies, but opportunities in the international financial markets

are also grasped. As a specialist bank, Investkredit combines the functions of a financ-

ing bank, an equity investor, a financial assets management bank, a treasury bank and

a real-estate bank. The Investkredit Group’s strategy is to expand existing business

segments, while retaining its specialization as a Bank for Corporates. Its aim is to

provide continuous high-quality service for existing customers and to enlarge its cus-

“invest.outlook panel“

15

tomer base among enterprises with turnover higher than EUR 8 m. Simultaneously, it

aspires to further refine credit risk control, consistently seeking appropriate combina-

tions of risk and income profiles.

Our customers. The latest regular survey commissioned by Austrian banks in the year

2000, conducted by the independent financial consultant Schwabe, Ley & Greiner

among 1,100 large enterprises with a turnover of more than EUR 40 m, shows that

Investkredit is the second-largest long-term loan financier for this customer group.

The Bank’s services are used not only in long-term financing but also, increasingly, in

asset management and foreign currency dealings. The survey also confirmed the ex-

cellent reputation of Investkredit, whose customers rated it first among the 21 banks

surveyed in the categories of “technical competence”, “flawless conduct of business”

and “action on complaints”. In the overall assessment of all six factors, which also

included “decisiveness”, “openness/partnership” and “price”, Investkredit is first among

all banks. These customer assessments show that Investkredit is awarded top marks

for quality. If one also takes into account the results of the latest TOP 2000 study,

conducted in 1999 and covering enterprises above EUR 7.3 m, Investkredit is the third-

largest source of long-term financing in Austria. The consistent expansion of its fields

of business as a Bank for Corporates thus finds a positive echo in Investkredit’s main

target group.

The market environment. 2000 was a good year for the Austrian economy. Under the

favourable influence of a stable world economy, the development of the euro and a

positive unit wage costs situation, export dynamism was extremely high, at a real

+12 % on the average for the year. Domestic consumption also developed encourag-

ingly and reached +2.7 % owing to the effects of the 1999 tax reform. In parallel with

the vigorous cyclical upswing in the EU, economic growth in Austria attained a real

+3.3 %. The year began on a dynamic note, but the international economy weakened

from mid-2000 and the sharp rise in petroleum prices caused a drift of purchasing

power to the oil-producing countries. As compared with the first half of the year,

economic growth in Austria almost halved. Manufacturing output reflected a spe-

cially favourable business situation. The growth in output almost trebled as compared

with the year before – against the background of a strong improvement in the rela-

tive unit wage costs position and extremely dynamic foreign demand. Total exports

achieved a new record high. Expectations regarding the business situation and pro-

duction development have deteriorated somewhat since the middle of the year. Over-

all, the mood is, however, upbeat following one of the best years in recent history. As

the earnings situation remains favourable, but also taking into account a major mod-

ernization requirement, enterprises are continuing the rapid renewal of their capital

equipment. Capital investment in the economy as a whole rose by some 6 % in the

year 2000. As a result of growing uncertainty as to future cyclical development, capi-

tal investment activity recently lost some of its momentum. Capital spending over the

entire year amounted to some EUR 7 bn in manufacturing and to some EUR 5.5 bn in

16

industry in the narrower sense, so that the investment ratio in industry will have reached

6.7 %, a typical value for boom phases.

Increase in earnings. The Bank’s consistent expansion of business segments in recent

years – while retaining its specialization – also led to improved earnings in the report-

ing year. The Investkredit Group recorded distinct growth in net interest income, the

net trading result and profit for the year as compared with 1999.

Net interest income. Net interest income rose by EUR 14.4 m or 23 % to EUR 76.4 m.

The increase was primarily due to the expansion of business in the year. Income from

lending business in the narrower sense was increased not only through the expansion

of lending business but also through the improvement of margins. Income from vari-

able-yield securities, equity investments and real-estate assets management also rose.

Margit Poglits-Raffetseder Johann Salzmann

Development of earnings.

17

It was not possible to avoid the effect of higher refinancing costs and a decline in

interest contributions caused by the flatter interest curve. The interest margin – i.e.

the ratio of net interest income to average total assets – thus dipped overall from

1.02 % to 0.98 %.

Other operating results. Net fee and commission income at EUR 5.9 m rose slightly

over 1999. The most significant items of income came from environmental aid admin-

istered by Kommunalkredit for the Republic of Austria on a trust basis. The net result

of risk provisions in lending business remained relatively stable in the reporting year

at EUR 6.6 m. Overall, total risk provision for loans in lending business decreased by

some EUR 7.7 m to EUR 64.3 m owing to the more relaxed risk situation. The net

trading result at EUR 3.0 m was distinctly higher than in the previous year, when losses

occurred. Within trading activities, profits were achieved in bonds and shares trading

and in derivatives. Only currency business showed a negative result. In the case of

financial investments, there were write-offs, particularly among securities held as in-

vestments available for sale, whereas sales of equity investments had a positive effect.

On the whole, the net financial investments result at minus EUR 10.9 m was distinctly

below expectations.

General administrative expenses. Personnel expenses fell to EUR 20.9 m, despite the

increase in staff by 21 to 290 (disregarding the Board of Management and maternity

leave). The reason was the reduction in provisions expenses. Other administrative ex-

penses rose 47 % in the year from EUR 9.1 m to EUR 13.4 m – chiefly in connection

with consultancy costs. Depreciation and write-downs of property and equipment re-

mained practically unchanged at EUR 2.5 m. Overall, general administrative expenses

rose 5 % from EUR 34.6 m to EUR 36.2 m, proportionately less than income. Accord-

ingly, the cost-income ratio in the reporting year was sharply reduced from 54 % to

42 %.

Profit for the year. Other operating results amounting to EUR 0.8 m comprised prima-

rily the increase in the value of derivatives that do not serve for trading purposes. The

profit for the year before tax improved by 33 % or EUR 8.1 m to EUR 32.4 m, as

compared with 1999. Taking into account taxes of EUR 2.2 m, the profit for the year

after tax rose 55 % from EUR 19.5 m to EUR 30.2 m. Accordingly, earnings per share

jumped from EUR 27.3 to EUR 42.3.

18

Balance sheet structure. The Investkredit

Group recorded a 26 % expansion in to-

tal assets to some EUR 8.7 bn, its strong-

est growth since 1980. The greatest con-

tributions came from loans and advances

to customers. In particular, local govern-

ment business expanded greatly in rela-

tion with bidding for loans auctioned by

the Republic of Austria. Furthermore, se-

curities financing in financial investments

also rose. Loans and advances to custom-

ers continue to represent the largest share

on the assets side at 57 %. On the liabili-

ties side, debts evidenced by certificates re-

main the largest item at 59 %. Amounts

owed to banks declined to 27 %. Risk-

weighted assets did not rise as distinctly as

total assets, since the Investkredit Group

continues to adopt a low-risk business

policy.

Capital resources. The core capital of the

Investkredit Group rose to EUR 272.0 m

through the formation of reserves. The to-

tal capital resources to be taken into account according to § 23 of the Austrian Bank-

ing Act declined to EUR 421 m owing to higher deductions following new equity

investments in the Group. As at 31 December 2000, the solvency ratio had fallen from

12.6 % of the assessment basis to 9.9 % as a result of the expansion. The Tier 1 capital

ratio also fell, namely, from 7.4 % to 6.4 %.

Rating. Moody’s Investors Service fixed the ratings for Investkredit and Kommunalkredit

in 2000 at A1 in the long-term and Prime 1 in the short-term area. The financial strength

ratings were unchanged at D+ for Investkredit and C for Kommunalkredit.

Kommunalkredit was reviewed for a “possible upgrade” at the beginning of 2001.

Staff. The proportion of female employees is 52 % and that of part-time staff – with

contracts covering between 50 % and 90 % of normal working hours – is 38 persons

or 13 %. In terms of normal working hours, this represents a staff of 278, in compari-

son with 258 the year before. The average age of employees in the Investkredit Group

is just under 39.

Volume in EUR m10,000

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

019991997 200019981996

4,2104,750

5,298

6,920

8,701

2,550 2,5922,812

3,343

4,276

Total assets

Risk-weighted assets

Total assets and capital development.

Loans and advancesto customers 57 %

Financial investments 31 %

Other assets 12 %

Debts evidenced bycertificates 59 %

Amounts owed to banks 27 %

Other liabilites 14 %

19

Latest developments. The capital of Kommunalkredit Austria AG was increased at the

beginning of 2001. The related rise in the share held by Dexia PFB will further inten-

sify the international involvement of Kommunalkredit. Shortly after the publication

of the new shareholder structure, the Moody’s rating was reviewed positively. Up-

grading to the AA segment could take place in the first half of 2001.

Market development. The weakening of the international economy, the consequences

of the oil-price increase and the restrictive effects of the Government’s package will

lead to a slowdown in economic growth this year. The real growth rate of GDP will

still be 2.2 % in 2001, and will be approximately the same in 2002. The situation on the

labour market will continue to develop favourably in 2001. With a declining oil price

and dollar exchange rate, the rate of inflation will again fall to 1.7 %. The slowdown

of the world economy in 2001 will have a negative effect on Austrian exports, which

will rise by a real 6%. Furthermore, the competitive advantages derived from the

euro-dollar relationship will no longer apply, so that relative unit wage costs will rise

slightly as compared with those of trading partners (+0.4 %). This will also retard the

expansion of manufacturing output, which can be expected to achieve a real produc-

tion increase of +3.8 % in 2001. Nevertheless, capital investment by industry will

remain high in 2001. Enterprises recently reported a planned volume of some

EUR 6.1 bn, in nominal terms some 10 % more than in 2000. In that context, expansive

plans are chiefly to be found among enterprises in the basic sector and technical process-

ing, while building sub-con-

tractors and producers of

traditional consumer goods

may perceptibly restrict their

capital investment.

Preview. Continuing its busi-

ness strategy, Investkredit

plans additional increases in

results in 2001. Earnings per

share are planned to rise to

over EUR 45, as against EUR

42.3 in the year 2000. This is

to be achieved by further

growth and the improvement

of margins in business with

domestic enterprises. In the

wake of reorganization of the

European capital markets

through the introduction ofHelmut Hinek Sabine Dungl

Outlook for 2001.

20

the euro, Investkredit plans to utilize its securities competence in the field of corpo-

rate bonds and to develop its market position. In the local government and real estate

areas, investments in Central and Eastern Europe are to be continued. Further aims

are to achieve a sustained increase in the return on equity by broadening and deepen-

ing customer relations. An expansion of the existing business segments, coupled with

the maintenance of specialization is expected to contribute to further improvement

of the cost-income ratio to less than 40 % by the year 2004.

Bedrija Ismaili

21

Enterprises.

SEGMENT REPORTING ACCORDING TO IAS.

FINANCING AND AID.

Core service. Demand for long-term financing was high in Austrian industry, against

the background of excellent cyclical development. Our most important concerns as a

Bank for Corporates in the year 2000 were the structuring of enterprise financing in

the M&A area and project financing in the energy sector. Services to the Austrian SME

sector were also important. Family enterprises are an important customer group of

the Bank for Corporates, since their busi-

ness development and innovative power

make important contributions to the

sustained prosperity of Austria as a busi-

ness location. In the structured financ-

ing, the Investkredit Group’s services

range from the provision of equity capi-

tal to borrowings and consultancy serv-

ices related to aid. Interest rate and cur-

rency risk management instruments are

in increasing demand. In line with in-

ternational capital market develop-

ments, interest in capital market prod-

ucts such as private placements and cor-

porate bonds is also growing in Austria.

Our customer service officers work out

individual solutions for all financing

problems, in collaboration with the en-

terprises and experts. They are reliable

advisers in entrepreneurial matters. Con-

tinuity and dependability in customer

relations contributed to our success in

the year 2000, as before. Investkredit

contracted EUR 553 m of financial loans

in 2000 (see table: Financing transac-

tions with enterprises). An important

area in enterprise financing is capital in-

vestment financing. In the year 2000 a

volume of EUR 2.3 bn of investments

was co-financed by Investkredit (see ta-

ble: Financing transactions with enter-Hannah Rieger Claudia Schmied

22

prises). The average amount of loans in 2000 was EUR 2.9 m, which was considerably

higher than the average for 1999 (EUR 1.9 m). Maturity at 10.1 years has on average

risen from 1999 (8.7 years). The trend towards long-term liquidity provision was thus

continued in the reporting year. Against the background of portfolio control by banks,

syndicated financing is growing in importance. Investkredit was much in demand as a

syndicate partner in the year 2000, primarily by Austrian banks. It also played a lead-

ing role in syndicates for major projects.

The following table shows the regional breakdown of cumulative lending business.

Enterprises with their domicile outside Austria account for an aggregate 10 % of fi-

nancing. This share of financing is concentrated in enterprises in the European Union

and in the countries of Central and Eastern Europe. In terms of cumulative regional

financing, Vienna, Lower Austria and Upper Austria are still in the lead.

In 2000, Vienna had the largest share of financing, partly because many enterprises

have their registered domicile in Vienna. Tyrol came second. 56 % of new financing

transactions concluded in the year 2000 was accounted for by industrial enterprises

(1999: 52 %). This shows the importance of Investkredit as a financier for industry. The

Financing transactions with enterprises

Annual 1996 1997 1998 1999 2000 2000 (cumulative from 1957)

Financing (in EUR m) 337 415 308 500 553 8,943

Investments (in EUR m) 1,048 1,135 1,090 1,323 2,296 32,229

Regional breakdown of financing transactions with enterprises, 1957 – 2000

Regions Financingin EUR m Share

Vienna 2,283 26 %

Lower Austria 1,557 17 %

Upper Austria 1,348 15 %

Styria 830 9 %

Tyrol 749 8 %

Salzburg 462 5 %

Carinthia 416 5 %

Vorarlberg 367 4 %

Burgenland 42 1 %

Total – Austria 8,054 90 %

Europe 830 9 %

Rest of world 59 1 %

Total – international business 889 10 %

Grand total 8,943 100 %

23

branches that received the largest shares of financing in the year 2000 were the

papermaking industry, electrical engineering and the petroleum and chemical engi-

neering industries. In the reporting year, business was considerably expanded in the

energy sector. The liberalization of the markets for electricity and gas ushered in di-

versification projects, among other things in the field of renewable energy.

The total volume of financing outstanding in the Investkredit Group in the year 2000,

including guarantees, trust loans and securities financing, grew by 13 % to some EUR

4.6 bn. The following table shows the structure of financing in the enterprise seg-

ment, broken down into domestic loans with and without aid, and international busi-

ness.

Domestic enterprise financing without aid. Loans and advances to domestic custom-

ers without a public aid component rose 5 % in the reporting year to EUR 1.9 bn. In

the domestic sector, special attention is devoted to margins in risk and earnings policy.

The income margins in domestic business improved in the year 2000, but are below

those in foreign business. Financing without aid also includes guarantee loans, which

declined in the reporting year by 4 % to EUR 381 m. Guarantee loans were mostly

related to the ERP Fund and are thus induced by aid-related business.

Financing with aid. The persistent year-long trend towards financing without aid is

clearly revealed in the declining share of aid-related business in the total volume from

23 % in 1999 to 16 % in 2000. The outstanding volume of loans with aid fell by 21 %

to EUR 749 m. This distinct decline was caused by extraordinary premature public-

sector repayments totalling EUR 160 m. The category of aid-related financing includes

ERP trust loans amounting to EUR 423 m. That shows the position of Investkredit as an

ERP Trust Bank. Disbursements in aid-related lending amounted to EUR 70 m in the

year 2000.

Aid management. Aid management from application to final settlement is a special

task of the Bank. The aim is to reduce enterprises’ financing costs by making use of

interest support, low-interest loans, grants, EU co-financing and guarantees by the

Domestic, without aid Domestic, with aid International business Total

1) Loans and advances to customers, trust loans and provision for guarantees2) Bonds and other fixed-income securities of other non-bank issuers

Financing in the enterprise segment

in EUR m2000 1999 Chan- 2000 1999 Chan- 2000 1999 Chan- 2000 1999 Chan-

ge ge ge ge

Loans1) 1,745 1,680 +4 % 749 950 -21 % 932 755 +24 % 3,426 3,385 +1 %

Securitiesfinancing 2) 196 174 +13 % - - 952 501 +90 % 1,148 676 +70 %

Total finan-cing 1,941 1,854 +5 % 749 950 -21 % 1,884 1,256 +50 % 4,574 4,061 +13 %

24

Federal, Provincial and local authorities. With the advent of the new Structural Fund

period 2000-2006, procedures and European rules for aid to enterprises have funda-

mentally changed. In the reporting year, the relevant objective programmes for EU

co-financing, except for the Objective 1 programme for Burgenland, had not yet been

approved by the European Commission. Application could therefore not yet be made,

so that it was not possible to apply for EU co-financing funds for new Objective 2

projects. The “Handbuch EU-konformer Förderungen” (Handbook of EU-conforming

aid measures), Hannah Rieger and Claudia Schmied, Wirtschaftsverlag Ueberreuter,

5th edition, Vienna, 2000) is a concise presentation of aid regulations. The “EU-

Förderdatenbank” and “EU-konform interaktiv” online services (www.investkredit.at)

support the Bank’s counselling in aid questions. There is a perceptible trend towards

direct grants in Austrian aid instruments. It is to be expected that decisions on aid

with regard to co-financing will shift noticeably towards the Provincial level. Domes-

tic partners in the field of aid are the ERP Fund, the BÜRGES-Förderungsbank, the

Austrian Industrial Research Fund (FFF), the Financing Guarantee Company (FGG), and

Bedrija Ismaili Hans-Michael Schania Johannes Wundsam

25

the aid institutions at Provincial level. Under the Environmental Aid Act,

Kommunalkredit is responsible for Federal environmental aid schemes. Applications

under the Austrian export financing and guarantee system are processed by the

Oesterreichische Kontrollbank AG.

European aid. At European level, cooperation with the European Investment Bank

(EIB), Luxembourg, was continued in the year in the context of the global loan. This

loan covers investments by SMEs as well as environmental protection and energy in-

vestments and is awarded either as an EIB bonus loan or – through close cooperation

with the customer banks of the enterprises – in the context of an EIB Europe loan.

Under that scheme, the partner banks provide guarantees to Investkredit, which makes

the funds available. Investkredit operates as a financial intermediary for the Euro-

pean Commission’s Joint European Venture Initiative (JEV). In the summer of 2000, a

loan agreement for EUR 150 m to refinance investment projects of medium-sized

enterprises in Austria, Slovenia, Hungary, the Slovakian Republic and the Czech Re-

public was concluded with the Kreditanstalt für Wiederaufbau (KfW), Frankfurt – the

largest aid bank in Germany. Investkredit’s counselling subsidiary EuroTech Manage-

ment provides Austrian enterprises with access to EU research and technology promo-

tion programmes, particularly under the EU Framework V Programme. A special Bank

technical team helps enterprises in the evaluation and submission of projects.

International business. As before, the focus of international business in the year un-

der review lay in the area of asset backed securities (ABS). The worldwide issue of this

type of security reached a volume of about USD 370 bn in the year 2000 and European

transactions had a 20 % share, a perceptible increase over the year before. In the

expansion of its ABS portfolio, the Bank concentrated on low-risk and high-rating

tranches. For margin reasons, investment was chiefly made in transactions on the US

market. Overall, the quality of the ABS portfolio was improved over 1999 in terms of

the average weighted rating factor. To control return in international risk business,

transactions with a higher risk profile were concluded in the area of internationally

syndicated loans, in addition to the ABS portfolio – though at a far lower level. The

risk/gains profile in international risk business also improved in the past financial year

with better overall quality owing to repayments but also to positive rating migra-

tions.

Leasing. In the leasing area, movable and real property was held with an aggregate

financing volume of some EUR 74 m. The lessees are Investkredit corporate custom-

ers. In the year 2000, there was a decline in volume and the Investkredit Group con-

centrated on servicing existing projects.

26

CORPORATE FINANCE, PRIVATE EQUITY AND COUNSELLING.

Corporate finance. The corporate finance field continued to develop dynamically in

the year. The growing demand for corporate finance services reflects a change in the

financing culture that is now also increasingly taking hold among Austrian enter-

prises. The Investkredit Group has stimulated the proactive shaping of this change by

means of new structured financing instruments. In the corporate finance field, the

Group now has a comprehensive range of services for enterprises throughout their

lives, from the early phases to pre-IPO financing. Thereby, the Bank for Corporates can

provide instruments suited to all financing situations. The enterprise finance field is

served by Investkredit Bank AG itself and by the subsidiaries INVEST EQUITY, Invest

Mezzanin and Europa Consult.

INVEST EQUITY. INVEST EQUITY Beteiligungs-AG expanded and strengthened its position

in the Austrian private equity and venture capital market. Cooperation with the found-

ing shareholder, Investkredit, the shareholder bank EIB and with shareholders from

the venture capital industry, namely, Parnib Holding BV and Financière Natexis Inter-

national S.A., strengthened its position. Companies in the INVEST EQUITY portfolio were

further developed both in the technology area and in the transaction-oriented sec-

tors of established production enterprises. In December 1999, CyberTron Telekom AG,

Vienna, was the first Austrian telecom enterprise to be listed on the Vienna Stock

Exchange; the second stock market venture from the INVEST EQUITY portfolio,

update.software AG, Vienna, also distributed dividends to INVEST EQUITY. New capital

investments made in 2000 in the technology companies TIANI MEDGRAPH GmbH, Brunn

am Gebirge, Viviance new media AG, St. Gallen and INFONIQA Informationstechnik

GmbH, Wels, strengthened the involvement of INVEST EQUITY in the B2B segment of

“Internet-enabling technology”. The portfolio enterprise Lomographische AG, Vienna,

is active both in the lifestyle branded goods area and the B2C market. These enter-

prises have the qualifications for necessary organic growth as well as for the strategic

development of their position in their respective market segments by means of acqui-

sitions. They can therefore be regarded as potential stock market candidates. Chemson

Polymer-Additive AG, Arnoldstein, was spun off from the Metallgesellschaft Group,

Frankfurt, and was acquired in 2000 by the management jointly with Leman Capital

and INVEST EQUITY. Chemson is the second-largest producer of additives for the PVC

industry world-wide; it also produces additives for the glass industry. At the end of the

year, INVEST EQUITY disposed of its stake in the Salzburg medical technology enter-

prise Anthos Labtec Instruments GmbH. INVEST EQUITY early stage Beteiligungs-AG

also established itself on the market in the year as an early-phase technology investor.

Invest Mezzanin. At the end of 1999, Investkredit established an EUR 40 m mezzanine

capital fund (Invest Mezzanin) in cooperation with FGG, as the first of its kind in Aus-

tria. This innovative financing instrument offers Austrian enterprises access to a form

of financing that has proved itself for many years internationally. It is chiefly regarded

27

as subordinated financing and has

the function of equity mezzanine

capital. Mezzanine capital has a

higher risk than loans but is serv-

iced before equity and thus occu-

pies an intermediate position be-

tween equity and borrowing in

the financing structure. Invest

Mezzanin had a very dynamic start

to the year. An autonomous risk

financing profile was created for

mezzanine capital, and incentives

were created for new and exist-

ing Investkredit customers in market development. In 2000, Invest Mezzanin analysed

and evaluated over 200 projects. Four investments were carried out in Austria in 2000,

for both “old-” and “new-economy” enterprises. With the establishment of Invest

Mezzanine Capital Management GmbH in December 2000, Investkredit laid the foun-

dation for the management of other funds.

Europa Consult. The growing demand among Austrian enterprises for corporate fi-

nance services was also felt by Europa Consult. Europa Consult – a wholly owned sub-

sidiary of Investkredit – concentrates on advisory services to medium-sized enterprises.

The range of services available for consulting on mergers and acquisitions (M&A) was

successfully expanded in the year. Against the background of a rapidly growing M&A

market, the combination of innovative financing instruments and a comprehensive

advisory service is becoming more and more important. Europa Consult assists its cus-

tomers in assembling structured financing packages and also in the acquisition and

disposal of enterprises, management buy-outs (MBOs), management buy-ins (MBIs)

and cooperation arrangements. Consultancy services in 2000 focused specially on the

solution of problems of succession in Austrian family enterprises. Europa Consult also

acted as an adviser on several sales assignments related to the privatization of public-

sector enterprises.

EuroTech Management. This Investkredit consultancy subsidiary, founded in 1996, has

two main fields of activity: EU projects, and technical consultancy on R&D projects.

EuroTech Management had a gratifying increase in orders in the year, 34 Austrian and

EU projects for Austrian enterprises and ministries being successfully processed. In

that context, EuroTech Management concentrates on the preparation, submission and

management of aid projects in research and technology (EU Framework V Programme)

and in EU environmental technology programmes (e.g. the ASIA Urbs programme).

EuroTech Management submitted project proposals to the European Commission jointly

with Austrian and international partners in large and small-scale industry, in research

centres and with the Municipality of Vienna. Through close personal cooperation with

Heike Jandl Oliver Grabherr

28

Investkredit technical experts, EuroTech advises enterprises on access to Austrian aid

programmes focusing on environmental protection and production technology. The

range of services on offer comprises the analysis, structuring and submission of projects

and the coordination of aid when several institutions are involved. In addition to aid

consultancy, EuroTech Management provides enterprises with technological, product

and market analysis and also with ongoing technical project controlling in implement-

ing investment projects and in the assessment of real estate, buildings and plant – if

necessary with the assistance of sworn court experts.

FINANCIAL ASSET MANAGEMENT.

Investkredit investment funds. Financial asset management services in the year con-

tinued to focus on the Investkredit investment funds. These are specially tailored to

the asset management needs of enterprises and institutional investors. With their

very conservative approach (dynamic asset allocation), the Investkredit floor funds

Julius Wallner Christian Doppler Thomas Heinisch

29

(i2F, i2-bond and i2-dollar), managed by UBS AG, are particularly suitable for enter-

prises that have high risk-awareness. By means of its prudential funds (i2V-

Vorsorgefonds, i2V-Euro, i2V-Select and i2V-Protect), the Bank takes into account the

expanded possibilities of corporate provision, among other things for severance

payment and pension commitments. Since October 2000, the Bank Vontobel Öster-

reich AG has taken over from UBS AG as fund manager for i2V-Protect. In the first half

of 2000, the Mercury Europäischer High Yield Anleihefonds – as the first foreign fund

– was included in the Investkredit marketing programme. This fund invests in corpo-

rate bonds from West European countries and is also suitable for corporate provident

schemes.

Performance and development by volume. In the year 2000, the value development

of the funds could not escape the effect of trends on the international securities mar-

kets. While the floor funds were all able to achieve positive returns, thanks to their

hedging approach, some provident funds with share components (i2V-Vorsorgefonds)

ended the year on a negative note. Therefore, the dynamic growth in the funds area

of recent past years could not be continued. Since the Investkredit investment funds

have a mainly short-term orientation, repurchasing of fund holdings exceeded sales.

The two funds chiefly affected were i2F and i2-bond. The total volume of Investkredit

investment funds as at year-end 2000 was EUR 230 m – see chart. Despite this decline

in volume, current income from the financial assets management segment topped

EUR 1.3 m, which was higher than in the year before. That was due to a natural delay-

ing effect in the disbursement of commissions. Accordingly, a decline is to be expected

in the current year.

350

300

250

200

150

100

50

0

12/96

EUR m

06/97 12/97 06/98 12/98 06/99 12/99 06/00 12/00

i2V-Select

i2V-Protect

i2V-Euro

i2V-Vorsorgefonds

i2-dollar

i2-bond

i2F

Investkredit investment funds: development by volume

30

Deposit business. The fi-

nancial asset management

requirements of corporate

customers were chiefly met

in the year 2000 by the use

of Investkredit’s and

Kommunalkredit’s own se-

curities holdings, own bond

issues and by Investkredit

investment funds. Deposit

business rose further in the

year to EUR 3.5 bn (assets

under management).

The InvestDirekt Internet

p r o g r a m m e

(www.investdirekt.at) ,

which was established in

2000, is already being used

by every fourth deposit cus-

tomer. This programme

makes it possible to create

charts presenting price

changes for individual secu-

rities holdings. The charts

also show the development of selected indices, for instance, ATX. With InvestDirekt,

users can individually create the charts that best meet their information needs.

Time deposits. Deposits by corporate customers are accepted via Investkredit Interna-

tional Bank p.l.c., Malta, which was founded in 1996 with an onshore banking licence

from the Maltese central bank and is a wholly owned Investkredit subsidiary. The

volume of time deposits by Austrian corporate customers shot up 23 % from the year

before to EUR 96 m. The total assets of Investkredit International were just under EUR

320 m.

TREASURY.

Refinancing. Bond issues for the refinancing of new business by enterprises in 2000

reached a volume of EUR 921 m. Investkredit launched a total of six issues during the

year. The largest transactions were three EUR floating rate notes (issue volumes: EUR

100 m, EUR 250 m and EUR 300 m). Prominent among the USD issues was the variable

basis USD 200 m transaction. Private placements were also launched to supplement

activity in the USD area. The facility for strengthening the capital resources basis was

Gernot Rux Josef Bernhard

31

used by means of a 20-year subordinated EUR 5 m issue. All new bond issues are listed

on European bourses. In the unsecuritized area, funds were raised chiefly by means of

note loans.

Securities management and derivatives. In the year 2000, securities management fo-

cused mainly on the euro capital market and on the United States economic area.

Trading activities concentrated on liquid bond markets. In addition, the Bank engaged

in trading on selected West European share markets. Even under difficult market con-

ditions, it was possible to achieve positive contributions to results in the year. Demand

by corporate customers for derivative instruments strengthened. The use of treasury

services thus makes a lasting contribution to optimizing the financial structure of en-

terprises. In the foreign exchange field, Investkredit has created a new Internet serv-

ice, InvestDirektFX (www.investdirektfx.at), an online currency trading system that has

been available since the spring of 2001. Its most important features are the availability

of tradable real-time currency cash and futures rates on PC and the possibility of hedg-

ing against currency risks by mouse-click. Derivatives are used in the Investkredit Group

for the fine tuning of interest and currency risk management. Trading with derivatives

also made important contributions to revenue.

32

The business approach. Kommunalkredit Austria AG is the investment bank for local

authorities. It specializes in financing infrastructural investments by public-sector and

similar institutions (local authorities, cities, associations, provinces, regions, States, etc.),

both in Austria and internationally. In the domestic market, 60 % of Austrian local

authorities are Kommunalkredit customers, while the chief international customers

are public-sector entities in Euroland, the other EU States, Switzerland and East Euro-

pean countries carefully selected in the light of risk assessment. A further important

field of business is management on a trust basis (aid processing and consulting serv-

ices for public-sector customers). In the framework of its internationalization strat-

egy, Kommunalkredit seeks investments in Central and East European financial serv-

ices providers that also have a communal/public-sector customer structure. The larg-

est investment so far – in the Slovakian bank Prvá Komunálna Banka, PKB – was car-

ried out in the year 2000.

Financing. 1,364 new loan agreements with an aggregate volume of EUR 893.4 m

were concluded in 2000. The related project costs (investment costs) amounted to

EUR 1.4 bn. Despite a difficult initial situation, Kommunalkredit succeeded in substan-

tially increasing its market share in the financing of local government infrastructural

projects in Austria. That became possible through successful bidding for Environmen-

tal and Water Management Fund loans. In the year, the Austrian Government under-

took its fifth sale of Fund loans (1,461 loans to a nominal amount of EUR 1.3 bn).

Kommunalkredit was awarded 844 loans. Development in the international financing

area is gratifying: overall in the year 2000, 145 projects with a volume of EUR 261.9 m

were financed (just under one-third of the entire volume of loans for the year). The

group of customers comprises local authorities, cities, regions and also States (Euroland,

EU States, East European States selected in the light of risk assessment). Switzerland,

with a share of some 80 % of new international business, became Kommunalkredit’s

second “home market”. In addition, Kommunalkredit financed projects in Greece,

Iceland, Lithuania, Norway, Poland, Slovakia, Spain and Cyprus. The following table

shows the dynamic development of local government financing business:

2000 1999 Chan- 2000 1999 Chan- 2000 1999 Chan-ge ge ge

Loans1) 2,140 1,529 +40 % 416 134 +211 % 2,557 1,663 +54 %

Securitiesfinancing2) 48 42 +13 % 104 56 +86 % 151 98 +55 %

Totalfinancing 2,188 1,571 +39 % 520 190 +174 % 2,708 1,760 +54 %

Austria Abroad Total

1) Loans and advances to customers, trust loans and provision for guarantees2) Bonds and other fixed-income securities of other non-bank issuers

in EUR m

Financing in the local government segment

Local government.

33

Management of Trust Funds. In the year Kommunalkredit carried out projects for the

following institutions: the Federal Ministry of Agriculture and Forestry, Environment

and Water Management, the Province of Upper Austria, the Federal Ministry of For-

eign Affairs, and Oesterreichische Kontrollbank AG, as well as for international part-

ners (such as the World Bank, the European Commission, or the European Bank for

Reconstruction and Development). 2000 was a record year for the management of

Federal and Provincial aid. More than 3,000 applications were filed with

Kommunalkredit. Concrete awards were made for 2,624 projects.

Equity investments. For the purpose of joint strategic action in Central European coun-

tries, Dexia and Kommunalkredit established Dexia Kommunalkredit Holding in the

year 2000. The ownership ratio is 40 % Kommunalkredit and 60 % Dexia. Through this

new holding company, Dexia and Kommunalkredit acquired 78.4 % of the Slovakian

Prvá Komunálna Banka (PKB) – registered office in Zilina – in May 2000. With a staff of

614 and 47 branch offices, PKB has more than 70 % of the Slovakian market. Since

Dexia and Kommunalkredit joined PKB, its strategic approach has been aligned with

that of the parent enterprises and initial action to optimize its organization has been

taken.

Treasury. Kommunalkredit raised some EUR 1.1 bn on the capital market in 2000 for

the financing of local government environmental projects. Twelve issues were launched

in all, and were documented under the debt issuance programme established in 1998.

Six of the twelve were public-sector syndicated environmental bond issues and the

remainder were private placements. In December 2000, the volume of this programme

was increased from EUR 2 bn to EUR 3 bn.

34

Business approach. The Investkredit Group’s activities with regard to commercial real-

estate are concentrated in Europolis Invest, which has specialized in three fields:

real-estate investments, real-estate project development and real-estate portfolio

management. It is company policy in Europolis Invest to focus on office properties,

and the aims are long-term safeguarding of revenue and the expansion of volume.

Accordingly, the main factors in project selection are the quality of buildings, the

credit rating of tenants and the long-term contractual safeguarding of rentals. A nu-

cleus of high-yield properties in Vienna was the starting base for the first activities in

Central Europe. The success achieved since 1997 has now led to concentration on mar-

kets in Central and Eastern Europe, in order to benefit from the extremely advanta-

geous relationship between revenue and risk in those markets. The continuous rev-

enue achievable in this area is 3-4 % higher than in Austria, legal and economic con-

ditions are stable and there are concrete prospects of entry into the EU. Accordingly,

current revenue should be accompanied by an increase in value, which will be antici-

pated by the markets before formal entry takes place. The real-estate segment there-

fore meaningfully supplements the financing business of Investkredit Bank AG.

Real-estate project development. Europolis Invest has so far carried out three real-

estate project developments in Vienna. After the completion of the Akademiehof

Karlsplatz in Vienna, activities were switched in 1997 towards former Eastern-bloc

States in Central and Eastern Europe. The decisive factors in this policy shift were not

only the positive economic developments in some of these countries, with an attend-

ant increase in the interest shown by many international enterprises, but also the

stable legal environment and the availability of first-class advisers. The first target

markets defined were Budapest, Prague and Warsaw. In Prague, Europolis developed

a project with a town-planning component, situated directly on the bank of the Vltava

(www.rivercity.cz). The first project stage of River City Prague will comprise two office

buildings, a hotel and an apartment hotel. The internationally renowned Kohn Petersen

Fox group of architects was commissioned to design the project complex. Planning

and construction of the advanced energy installations are in the hands of a team of

2000 1999 Chan- 2000 1999 Chan- 2000 1999 Chan-ge ge ge

Loans1) 9 13 -34 % 5 19 -73 % 14 32 -57 %

Securitiesfinancing2) 42 8 +417 % - - 42 8 +417 %

Buildings 55 35 +58 % 45 - 100 35 +187 %

Totalfinancing 105 56 +88 % 50 19 +163 % 155 75 +107 %

Austria Abroad Total

1) Loans and advances to customers, trust loans and provision for guarantees2) Bonds and other fixed-income securities of other non-bank issuers

in EUR m

Real estate.

Financing in the real-estate segment

35

leading enterprises in this highly specialized field. In the reporting period, Investkredit

took over all the project companies, in agreement with the previous project partner,

in order to safeguard the entire potential revenue for the Group. Building permission

has already been granted for the first office building (“Danube House”), which will

have a gross floor area of some 30,000 m2. Building work commenced at the turn of

the year. A further landmark project is being started in Budapest. The project is for a

high-rise office building with a floor area of some 30,000 m2 meeting international

technical and architectural standards. The project is being carried out in cooperation

with a developer with years of experience in this market.

Real-estate investments. Investkredit has founded a company, Europolis CE Holding

GmbH with the task of assembling a high-quality real-estate portfolio in Central and

Eastern Europe. The aim is to invest in first-class fully rented properties in top loca-

tions in Warsaw, Prague and Budapest, with amenities that meet Western investment

standards. Four investments have already been carried out, to a volume of some EUR

175 m, for two properties in Budapest (City Gate and Info-Park Research Center), one

in Prague (Hadovka Office Park), and one in Warsaw (Warsaw Towers). Europolis CE

thus has some 70,000 m2 of office space available for rental. A factor of decisive impor-

tance in these dynamic markets is to have a tenant structure that ensures stable long-

term revenue. The long-term value generated through this strategy should give a

distinct boost to growth through the entry of these countries into the European Un-

ion. The projects have already been almost entirely let, enterprises such as Nokia,

Siemens, Sun Microsystems, Ernst & Young, IBM and HP being among the largest ten-

ants. It is our constant concern to sustain and improve services to all our tenants. The

investment focus of Europolis CE has been expanded both regionally and substantively

in a second phase. Investment opportunities are being examined not only in office

properties but also in industrial and logistic parks. Assuming appropriate return and

suitable properties, commitments are possible in Bratislava, Polish regional centres

and in the capitals of the Baltic States.

Real-estate portfolio management. The portfolio so far assembled by Europolis CE is

one of the largest in the region. A locally staffed management company was set up in

the context of expanding activities in Prague.

36

FINANCIAL STATEMENTS OF THEINVESTKREDIT GROUP FOR 2000.

Balance sheet.

Assets Notes 31.12.2000 31.12.1999 Changein EUR 1,000

Cash and balances with central banks 18 4,780 69,367 -93 %

Loans and advances to banks 19 661,866 934,395 -29 %

Loans and advances to customers 20 4,950,232 3,869,844 28 %

Risk provisions for loans and advances 7, 22 -64,310 -71,977 -11 %

Trading assets 8, 23 187,169 118,578 58 %

Financial investments 24 2,689,824 1,898,629 42 %

Property and equipment 25 214,839 66,964 221 %

Other assets 27 59,007 34,602 71 %

Total assets 8,703,408 6,920,402 26 %

Liabilities 31.12.2000 31.12.1999 Changein EUR 1,000

Amounts owed to banks 28 2,357,201 2,419,734 -3 %

Amounts owed to customers 29 328,155 397,597 -17 %

Debts evidenced by certificates 30 5,139,159 3,477,785 48 %

Provisions 31 40,675 43,614 -11 %

Other liabilities 33 324,429 112,971 187 %

Subordinated capital 34 197,087 190,245 4 %

Minority interests 22,532 22,785 -1 %

Equity 35 294,168 255,671 15 %

Total liabilities and equity 8,703,408 6,920,402 26 %

37

Income statement.

Income statement Notes 31.12.2000 31.12.1999 Changein EUR 1,000

Interest and similar income 835,221 500,592 67 %

Interest and similar expenses -758,773 -438,501 73 %

Net interest income 36 76,448 62,091 23 %

Fee and commission income 10,369 9,193 13 %Fee and commission expenses -4,511 -3,523 28 %

Net fee and commission income 37 5,857 5,670 3 %

Net credit risk result 38 -6,586 -7,401 -11 %

Trading result 39 2,968 -3,699 -180 %

Net financial investments result 40 -10,861 14,974 -173 %

General administrative expenses 41 -36,227 -34,605 5 %

Other operating results 42 770 -12,779 -106 %

Extraordinary result 0 0 -

Profit for the year before tax 32,369 24,251 33 %

Tax on income 43 -2,193 -4,758 -54 %

Profit for the year after tax 30,176 19,492 55 %

Minority interests -3,415 -2,191 56 %

Net profit for the year 26,760 17,301 55 %

38

Statement of changes in equity.

Changein EUR 1,000 31.12.2000 31.12.1999 2000

Subscribed capital 46,000 46,000 0

Capital reserve 61,047 61,047 0

Profit reserves in the strict sense 157,038 128,231 28,807

Hedging reserve 8,842 8,611 231

Net profit for the year 26,760 17,301 9,459

Dividend paid by Investkredit Bank AG -5,520 -5,520 0

Aggregate 294,168 255,671 38,498

39

in EUR 1,000 2000 1999

Profit for the year (before minority interests) 30,176 19,492

Non-cash items included in profit for the year, and adjustments to reconcileprofit for the year to cash flows from operating activities

Depreciation/revaluation gains on property and equipment and financial investments 2,002 429 Transfer to/release of provisions and risk provisions for loans and advances -10,606 -3,030

Profit/loss from the disposal/valuation of financial assets, property and equipment 10,861 -14,974

Other adjustments (net) -72,977 -37,638

Changes in assets and liabilities from operating activities after adjustments for non-cash components

Loans and advances to banks 272,529 -134,644 Loans and advances to customers -1,080,389 -345,627 Trading portfolio -68,592 48,694 Currents assets -707,079 -141,576 Other assets from operating activities -24,405 3,079 Amounts owed to banks -62,533 205,658 Amounts owed to customers -69,441 48,625 Debts evidenced by certificates 1,661,373 1,113,438 Other liabilities from operating activities 211,458 -22,459