Embed Size (px)

Citation preview

Northeast Asia Energy FocusNortheast Asia Energy FocusVol.7 No.1 Spring 2010

Inside the KEEI 2Briefs on Northeast Asia 5

Basic Concepts of Cooperation in North-East Asia in the Oil and Gas Sector for the Period 2010-2030 10Alexander N. Gulkov

Apropos Cogeneration Based on the Development of the Small Power Industry Sector in the Far East 16Igor Svetlov / Andrey Zagumynnov

The Turkmenistan-China Pipeline: What Are Its Implications? 25Stephen Blank

The East as the New Priority of the Russian Energy Policy 36Vyacheslav Kulagin

Decline or Re-rise of OPEC: Implications for Northeast Asia 44Hooman Peimani

Energy Security Dilemma Bubble: Cold War Thinking in aWorld Supply Oil Market 52Kevin P. Kane

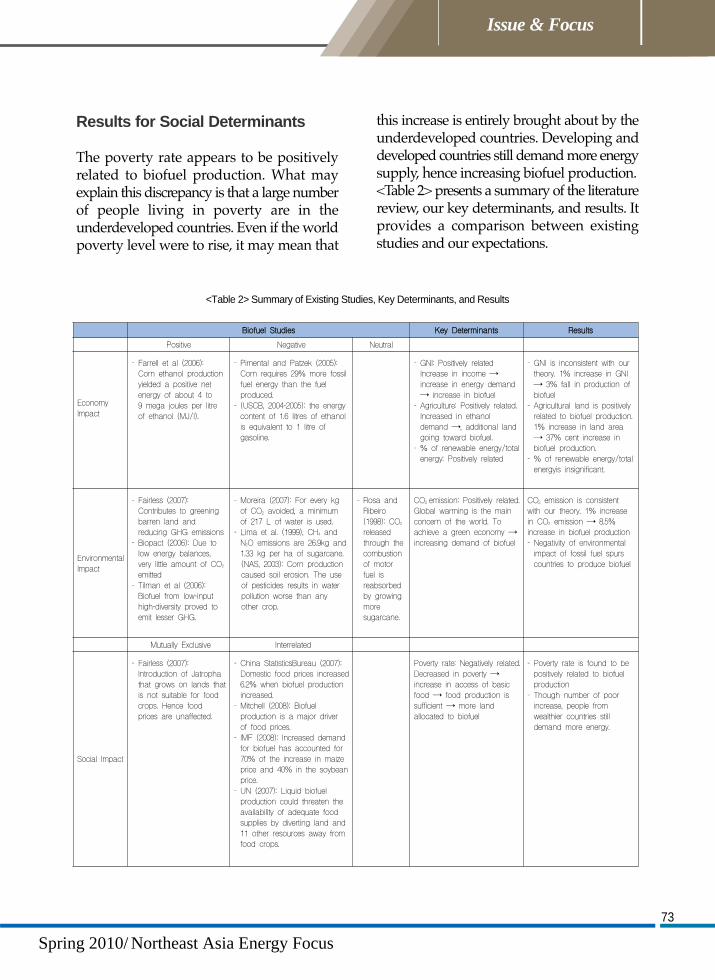

Effect of Biofuel Production on the Global Economy: Economic, Social, and Environmental Perspectives 65Youngho Chang / Sarah Ho / Patricia Seah

Nuclear Share of Total Electricity Generation in 2008 76Total Energy Requirement by Fuel Type in 2008 76

Issue & Focus

News Update

NEA Statistics

ISSN 1738-8562

Spring 2010/ Northeast Asia Energy Focus

Inside the KEEI

The Third Korea-China EnergyWorkshop

The Korea Energy Economics Institute(KEEI) and the Energy Research Institute

(ERI) of China jointly organized a workshopnamed “Energy Security and OverseasInvestment and Green Energy Development,”which was conducted on November 25-26,2009, at the Coex Intercontinental Hotel, Seoul,Korea.The KEEI-ERI” Joint Workshop wasconducted under a performance agreementconcluded between Korea and China in 2002;it has been conducted alternately in Korea andChina since 2007, and the third meeting of thisseries was conducted in 2009.The workshop aimed to exchange informationand opinions regarding energy policy changesand the promotion of joint projects betweenKorea and China and to build the foundationof a close partnership by organizing regularworkshops.At the inaugural session, Dr. Ki-Yual Bang, thepresident of the KEEI, made the openingremarks, and Prof. Han Wenke, DirectorGeneral of the ERI, offered his congratulationsto all the participants.

The program comprised three sessions. Thefirst session addressed “Energy Security andOverseas investment” and was organized bythe chair of this session, Dr. Jin-Woo Kim ofthe KEEI.Dr. Gao Shixian of the ERI made apresentation on “China’s Energy SecurityPolicy for Overseas Oil & Gas Development”under the theme “Overseas Oil & GasDevelopment,” and Dr. Yongduk Pak of theKEEI made a presentation on the “Strategiesand Policies in the Overseas Oil and Gas E&Pof Korea.” Dr. Jiang Xinmin of the ERI madea presentation on “The Recent Expansion ofOil Refinery Facilities in China” under thetheme “Petroleum Products Market,” and Dr.Kim Hyung-Gun of the KEEI made apresentation on “The Oil Industry of Korea.” The second session organized by the chair, Dr.Yu Cong of the ERI, dealt with “Green EnergyDevelopment.” Dr. Zhang Yousheng of theERI made a presentation on “China’s CoalbedMethane Development and Utilization,” whileDr. Ahn, Dal- Hong of KEPCO KEPRI (KoreaElectric Power Corporation, Korea ElectricPower Research Institute) made a presentationtitled “Introduction to Korea IGCCDevelopment Program” under the theme“Clean Coal Technology.” Dr. Feng Shengboof the ERI presented a paper on “China’sCDM Policy and Progress,” and Dr. HwangIn-Chul, of KEMCO (Korea EnergyManagement Corporation) presented a paperon “CDM Implementation in Korea.”The last session involved a round-tablediscussion organized by Dr. Nam-Yll Kim ofthe KEEI and Dr. Gao Sixian of the ERI. Allthe participants interacted enthusiastically onthe subject of effective regional energycooperation and opportunities and visions foreffective energy cooperation between Koreaand China.

2

News Update

News Update

3

SOC (The Senior Officials’ Committee)Conference

The KEEI hosted the Second ExpertWorkshop for the WG-EPP Joint Study

and the Third Meeting of the Ad-hoc TaskForce for Development of the Five YearStrategy on November 26-27 at the Lotte Hotelin Seoul, Korea.

The Second Expert Workshop for theWG-EPP Joint Study

The Second Expert Workshop for the WG-EPP Joint Study was conducted on

November 26 under the theme “EnergyProduction Potential and Development Plansin Northeast Asia, PhaseⅡ.” Approximately20 participants, including officials from theRussian Government and the ESI (EnergySystems Institute), the ERI of China, theMongolian Government and the EA (EnergyAuthority), the UN/ESCAP, and the KEEImembers participated in the workshop.The KEEI was designated a Nodal Institutionfor the 2009-2010 Working Group on EnergyPlanning and Policy (WG-EPP) on Feb 2009in Jeju Island, Korea. This conference wasorganized to inspect the progress of the2009-2010 joint research project on “NortheastAsia Energy Production Potential andDevelopment Planning” and interim findingsof each country and to conduct a debate onrelated matters. Furthermore, Dr. Sokolov ofthe ESI, Dr. Chimeddorj of the EA, Dr. Gaoand Dr. Jiang of the ERI, and Nam-Yll Kimand Dr. Ji Chul Ryu of the KEEI discussed onthe oil fields of China, Korea, Mongol, and

Russia, and they concluded that each of thesecountries would express their positions on theDevelopment of the Five Year Strategy ofNortheast Asian Energy IntergovernmentalAlliance.

Third Meeting of the Ad-hoc Task Forcefor the Development of the Five YearStrategy

The Third Meeting of the Ad-hoc TaskForce for the Development of the Five Year

Strategy was held on November 27 in Seoul,Korea. The KEEI was designated a NodalInstitution of Ad-hoc Task Force on June 2009in Bangkok, Thailand (at the seventh meetingof the Working Group on Energy Planningand Policy). This meeting was conducted toevaluate activities over the past three yearsand reset the future direction of operations. This meeting was attended by Dr. Aliev of theMinistry of Energy and Dr. Sokolov of the ESIfrom Russia, Dr. Chimeddorj of the EA fromMongol, Mr. Gao of the ERI from China, Dr.Maritess Cabrera from UNESCAP, and sixmembers of the KEEI, including Jin-Woo Kim,Nam-Yll Kim and Ji-Chul Ryu.

Presentation Detailing the Resultsof the 2009 Northeast Asia EnergyCooperation Research Projects

Apresentation on the results of the 2009Northeast Asia Energy Cooperation

Research Projects was made on December 22,2009, at the Coex Intercontinental Hotel inSeoul, Korea. The presentation detailed thefinal results of 16 research projects undertaken

News Update

Spring 2010/ Northeast Asia Energy Focus

in 2009. Over 30 people attended thispresentation and provided valuable comments.The 16 research projects were as follows:

Study on the changes in the oil distributionmarket in JapanStudy on energy conservation policies ofmajor northeast Asian countriesStudy on energy welfare policies of themajor northeast Asian countriesStudy on the economic cooperation strategyof South Korea and North Korea throughthe energy system link of northeast AsiaAnalysis of the long-term energy plan ofnortheast AsiaStudy on the economic and social developmentstrategies of Turkmenistan and the energyresource development cooperation betweenKorea and TurkmenistanStudy on the green energy markets ofnortheast Asia and international cooperationsituation and prospectAnalysis of energy markets in northeastAsia; energy taxes and pricesStudy on securing the stability of the supplyof natural gas in RussiaStudy on the energy-related R&D situationof China and the cooperative measuresundertaken by Korea and ChinaStudy on the cooperative measures appliedto uranium resource development innortheast AsiaAnalysis of the energy export structure andtransportation system of RussiaStudy on the revitalization of Korea-Mongolenergy cooperation: energy developmentinfrastructureStudy on making inroads into the Uzbekelectricity marketStudy on the Local Distributed PowerDemand Survey and Resources CooperativePlan Research in Kazakhstan Study on the effect of changes in theinvestment conditions of Russian energycompanies on Korea-Russia energy cooperation

In addition, the international expert of the

KEEI, Dmitry Sokolov, presented a paper titled“Potentialities and Problems of IncreasingRussian Coal Supplies to markets of APRCountries.”

KEEI-IOG Joint Workshop

The KEEI-IOG (Institute of Oil and Gas)Joint Workshop was conducted on

December 4 in Vladivostok, Russia. Dr. Euy-Seok Yang and Dr. Sung-Kyu Lee of KEEIparticipated in the conference as speakers.The session began with opening remarkspresented by Dr. Alexander Gulkov, the Directorof the IOG, followed by a congratulatoryaddress to all the participants by Dr. Jin-Woo Kim, Managing Director of the KEEI.The conference comprised two sessions—presentations and a round-table discussion.In the first session, Dr. Eyu-Seok Yang madea presentation on “The Oil Industry of Korea,”which was followed by a presentation by DrSung-Kyu Lee on “Promotion Status of EnergyCooperation Projects after the 2008-MoscowSummit Meeting between Korea and Russia.”Later, Dr. Alexander Gulkov presented a paperon “The Development of the Oil and GasIndustry of the Far East of Russia.”Thereafter, at the round table discussionsession, all participants had a heated debateon issues related to the presentation. The KEEI and IOG concluded an agreementfor the implementation of the 2009 jointresearch project. The subject of their joint studywas “Contents and Promotion Status ofOngoing and Planned Energy Projects in theFar East Region of Russia.”

4

News Update

Spring 2010/ Northeast Asia Energy Focus

5

News Update

Spring 2010/ Northeast Asia Energy Focus

Briefs on Northeast Asia

New energy to become focus ofChina’s strategic emerging industries

Departments including the Ministry ofIndustry and Information Technology

(MIIT), the National Development andReform Commission (NDRC) and theMinistry of Finance jointly formed acoordination group before the Spring Festival.In a group meeting, it was clearly pointed outthat China would constitute strategic emergingindustries to develop the “12th Five-YearPlan.”The meeting also decided that it wouldestablish a research and coordinationdepartment for accelerating the developmentof strategic emerging industries to coordinatedevelopment research ideas and to deal withimportant issues of constitution work as awhole. The department will consist of theheads of 20 organizations, and Zhang Ping,the director of the NDRC, will be thedepartment leader. The coordination groupwill make important arrangements suchas the main targets and tasks, the keydevelopment areas, the main developmentdirection and the industrial geographicaldistribution of China’s strategic emergingindustries.Reporters learned that of the 7 emerging high-tech realms brought forward by relevantgovernmental departments in November 2009including the information industry andbiotechnology, the new energy realm will mostlikely become the main development directionand obtain more policy support.Up until now, China has established 3important standards to select strategicemerging industries. First, it must have steadyand promising market demand. Second,

it must have excellent economic andtechnological effects and third, it must be ableto promote a group of other industries.Compared to other technological realms, thenew energy realm is most suited to thestandards.An official from the MIIT said that developingnew energy is quite identical to China’s ideaof developing a low-carbon economy. “Afterthe Copenhagen Conference, the MIIT has putthe low-carbon economy’s development in amore important position.”(People’s Daily Online, 2.23)

Russia threatens BP Kovykta assets

Russia’s Natural Environment Inspectorate,RosPrirodNadzor, has recommended that

BP’s joint venture in Russia, TNK-BP, bestripped of the giant Kovykta natural gasproject in eastern Siberia. Located in eastern Siberia’s Irkutsk oblast, theKovykta field holds an estimated 2 trillioncubic meters of gas. RUSIA Petroleum is thelicense-holding company (technically the“mineral resource user”) in the Kovyktaproject. TNK-BP owns a 63% stake in it. TNK-BP is a parity joint venture of British companyBP with the Russian TNK (formerly TyumenNeftegaz company), which is currentlycontrolled by four Russian billionaire tycoons. The Kremlin seems to be moving rapidly totighten the noose around TNK-BP’s asset,using the state’s regulatory apparatus tothreaten with revocation of the license. Inrecent weeks, RosPrirodNadzor has steppedup its inspection of the project. It claims tohave found “continuing violations” of licenseterms, with field development “persistentlylagging”. Officially, the decision regarding the license ismainly up to Russia’s Mineral ResourcesOversight Service (RosNedra). In practice,there is little doubt that the decision will be a

6

News Update

Spring 2010/ Northeast Asia Energy Focus

political one, ultimately to be made at the topof the government and in the Kremlin. State oil company Rosneft has apparentlydeveloped ambitions to enter the natural gasbusiness through a major project. Rosneft’ssubsidiary, Rosneftegaz, is expected to bid fora controlling stake in Kovykta. On February 4, Aleksei Miller, chief executiveof gas monopoly Gazprom, announced thatthe company does not need to includeKovykta’s gas resources in Gazprom’s exportprograms for China or other countries in theEast Asia-Pacific region. On the following day,the natural resources ministry (to whichRosPrirodNadzor is a subordinate agency)announced an “extraordinary” round ofinspection of the Kovykta project. On February12, Natural Resources Minister Yuri Trutnovwarned that a decision to revoke the licensemight ensue within several weeks. In that case,the Kovykta field would be transferred intothe legal category of “unallocated mineralreserves” (unlicensed fields). The dispute dates to 2006-2007, although it laydormant since. RUSIA Petroleum wasplanned to have supplied 9 billion cubicmeters (bcm) per year from 2006 onward forthe needs of Irkutsk oblast. However, thatamount far exceeds the level of demand inIrkutsk oblast, and a local distributioninfrastructure would first have to be created.Project shareholders had considered exportingthe gas to China. However, the idea wasthwarted by the lack, or denial of access toGazprom’s export pipelines. RosNedra threatened to revoke the license in2007 on the pretext that field developmentwas lagging behind schedule and gasproduction was below the levels stipulated inthe license and the contract. Under pressure,TNK-BP agreed to sell its Kovykta stake toGazprom for a sum in the range of US$700million to $900 million, with an option toretain or regain a minority stake, subject to

further negotiations. At that stage, Gazpromwas trying to pressure BP into ceding a stakein BP’s liquefied natural gas (LNG) project onTrinidad and Tobago. That project suppliesthe US market, which Gazprom was trying toenter. The resolution was deferred in 2007-2008 bythe Russian stakeholders’ conflict with BP.Thanks to the Russian authorities’ strong-armmeasures, the TNK side evicted the jointventure’s chief executive, Charles Dudley (anAmerican citizen) from Russia in 2008, andforced changes on the joint venture’s board infavor of the Russian side. Gazprom employeeGerhard Schroeder (formerly the Germanchancellor) was foisted on TNK-BP’s board asan “independent” member. No sooner wasthe board coup accomplished than thefinancial crisis hit, further postponing aresolution of the Kovykta dispute. At this stage, license revocation threatens notonly BP, but also the Russian tycoon ownersof TNK: an offer that TNK-BP cannot refuse.Apparently, Russian authorities are about togive all concerned an option to avoid licenserevocation and investment forfeiture, if theyagree to sell the project to Rosneftegaz, orpossibly another Russian company. Gazprommay well also be waiting in the wings, itsdisclaimer notwithstanding. This time, however, Kovykta stakeholdersmight try to avail themselves of the EnergyCharter Treaty’s provisions on the protectionof foreign investment. In a potentiallylandmark case in December 2009, thePermanent Arbitration Court in The Hagueruled that Russia is bound by the EnergyCharter Treaty’s provisions from the momentof Russia’s signature in 1994. Under the terms of that signature, the treatytook legal effect in Russia through provisionalapplication, ahead of its ratification andirrespective of it. In August 2009, Russiaserved notice that it would not ratify the Treaty

7

News Update

Spring 2010/ Northeast Asia Energy Focus

and that it was not bound by it. The court inthe Hague, however, ruled the opposite, in acase brought to the court by the shareholdersof the expropriated Yukos company. Thismeans that foreign investments made inRussia after 1994 are covered by the treaty’sprotection, apparently for the 20-year periodstipulated at that time. This in turn opens theway for investors to seek internationalarbitration of their disputes with the Russianauthorities in energy projects. (Asia Times, 2.24)

Russian watchdog may revoke TNK-BP’s Kovykta gas field license

Russia’s environmental regulator said onWednesday that the Russian-British joint

oil venture TNK-BP may lose its license todevelop a huge gas field in Siberia over afailure to comply with the terms of theagreement.Rosprirodnadzor has completed anunscheduled audit of TNK-BP’s operations atthe Kovykta gas condensate field, withestimated reserves of over 2 trillion cubicmeters of natural gas, and will recommendthat the Natural Resources Ministry revokethe license, the watchdog said.It was earlier reported that a decision on therevoking of the license for the gas field, whichalso contains 2.3 billion cubic meters of heliumand 115 million metric tons of gas condensate,could be made before March 1, 2010.The gas field is located in East Siberia’s Irkutsk

Region.Under the terms of the license agreement,TNK-BP, a highly lucrative 50-50 joint venturebetween the British major BP and four Russianbillionaires, is required to produce 9 billioncubic meters of gas annually in contrast to itsactual output of several dozen million cubicmeters.Russia’s Natural Resources Ministry carriedout a check of the joint venture’s compliancewith the license agreement in 2007 and gaveRUSIA Petroleum, the Kovykta operatorowned by TNK-BP, twelve months to bringup output to the level stipulated in theagreement.Natural Resources Minister Yury Trutnevearlier announced, however, that “the licenseagreements were not fulfilled in the past andare not being fulfilled at present.”Last week, Viktor Vekselberg, one of the fourRussian partners in the joint venture with BP,said there were difficulties with theimplementation of the Kovykta project, addingthat an unscheduled check by the regulatorwas damaging the investment environmentin the country and would not contribute toefforts to resolve the problem.The regulator’s plans to revoke the licensemay be linked to an unsettled deal betweenenergy giant Gazprom and TNK-BP on thegas field.Under an agreement signed in 2007, Gazpromintended to buy a 62.8% stake in RUSIAPetroleum to take over the Kovykta gas field.The deal, however, has not been closed asGazprom was reported in December 2008 tohave asked TNK-BP to reduce the price forthe purchase of the Kovykta field, originallyestimated at $700-900 million.(RIANOVOSTI, 2.17)

8

News Update

Spring 2010/ Northeast Asia Energy Focus

China-Central Asian Gas Pipeline:Success and Pitfalls

Under a 2007 accord, Turkmenistan agreedto export 30 billion cubic meters (BCM)

of natural gas to China annually for the next30 years. The deal, the first PSA onshoregranted to any foreign country inTurkmenistan, allows CNPC develop naturalgas fields in the Bagtyiarlyk area on the AmuDarya Right Bank in Turkmenistan. Theoutput of natural gas from Bagtyiarlyk wouldamount to 5 BCM by next year.A natural gas pipeline linking Turkmenistanand China’s Xinjiang Uygur autonomousregion started operations earlier this monthas part of the agreement. The project isexpected to boost China’s efforts to increasethe use of natural gas to 5 percent of its totalenergy consumption in 2010, according toanalysts.To secure further gas resources, CNPC andcompanies from South Korea and the UnitedArab Emirates (UAE) have won contractsworth $9.7 billion to develop a large naturalgas field in Turkmenistan. The consortium,comprising of CNPC, South Korea’s LGInternational Corp and Hyundai EngineeringCo, and the UAE’s Gulf Oil & Gas FZE andPetrofac International Corp, will jointlydevelop the South Yolotan gas field,considered to be one of the biggest five naturalgas deposits in the world. According to someestimates, it may hold approximately 6 trillioncubic meters (TCM) of gas.The integrated gas exploration and productionin Turkmenistan and cross bordertransportation through Uzbekistan andKazakhstan into China is not merely acommercial partnership, it also creates apolitical alliance between the four countriesbased on such a single energy cooperationarrangement. It fosters systematic and broader

cooperation. Unfortunately, there are no inter-governmental contractual framework designedto govern the cross border transportationsystem as BOODC International advised.Taking account of the complicated relationsbetween these Central Asian states, CNPCwas advised to ink bilateral governmentalagreements with each of these Central Asiannations and form joint ventures withindividual country separately. However, thelegal regime may be vulnerable to deal withpossible disruption of supply, disputes or otherconflicts that may occur in the future. We areinvited to work out a proposal to assess theseissues from the lens of various stakeholders.(Financial Times, 2.13)

Mongolian Prime Minister: Dual Listingsto Take Time

Initial public offerings of Mongolia’s state-owned mineral assets could take more time,

as the government works on upgrading thestock exchange to facilitate dual listings,Mongolian Prime Minister SukhbaatarBatbold said Tuesday.“We’d prefer to list [companies] in Mongoliafirst, but it may take more time than weexpected to list on the local exchange becausethings are not running properly in terms ofinfrastructure and management and real timefunctions. It’s getting there but needs moreimprovements,” Mr. Batbold said in aninterview.Mr. Batbold would like to see dual listingsof Mongolian assets with companiessimultaneously offering shares on globalexchanges such as Hong Kong, London orNew York as well as on the Mongolian StockExchange. State-owned companies lined upfor listing include Erdenes MGL LLC, whichowns licenses for the Tavan Tolgoi coal mineas well as other mineral deposits, ErdenetMining Corporation and national carrier

9

News Update

Spring 2010/ Northeast Asia Energy Focus

Mongolian Airlines, also known as MIAT.In addition to preparing the assets for duallistings, the government is working on hiringa team of new managers with internationalexperience for the exchange later this year, hesaid. Among the issues that need to beaddressed is establishing regulatory andaccounting standards that are in line withinternational standards.The prime minister said he would also like tosee foreign companies that hold Mongolianassets and are listed abroad to list a 10% stakeon the local exchange.Companies with Mongolian assets that arelisted on overseas stock exchanges includecoal producer SouthGobi Energy ResourcesLtd., which listed on the Hong Kong StockExchange just last week, as well as MongoliaEnergy Corp. Ltd. also listed in Hong Kong.Development of Mongolia’s nascent stockexchange is one of the challenges facing thepoor nation as it tries to capitalize on itsnatural resources to bring wealth into itspopulation of 2.7 million.Mongolia’s stock exchange was established in1991 when the Securities Committee was setup with the goal of privatizing more than 400major state companies. But since then, thestock exchange and securities market havefailed to drive Mongolia’s economy.“There’s a big discrepancy between theMongolian stock exchange, which lists about200 companies with a total marketcapitalization of about US$450 million andcompanies that list abroad,” said Alisher AliSjumanov, chief executive officer of EurasiaCapital.“Even if just a few companies [of those listedabroad] list, this will be a big boost to localcapital,” he said. (The Wall Street Journal, 2.09)

Alaska sees China as energy partner

China has a role to play in the Alaskanplans to develop its oil and natural gas

ambitions, said Alaskan Lt. Gov. CraigCampbell.Alaska’s Republican Gov. Sean Parnell saidhe would invite Chinese investors to the statefollowing a trip to the region by Campbell inDecember.Parnell in his January state of the state addresssaid “gushers” in the Prudhoe Bay and PointThomson regions of the North Slope requirean ambitious effort to exploit.The plans come as international explorationcompanies said they could slow efforts inAlaska and look for economic benefitselsewhere.“As North Slope oil production continuesto decline, we must work diligently tofind additional economic developmentopportunities,” said Campbell in a statementfrom his office. “Now is the time tosignificantly increase our marketing efforts inAsia.”Alaska needs investors to back its plans tobuild a gas pipeline in the state to market thegas potential in the North Slope. TransCanada and Denali, a joint venturebetween BP and ConocoPhillips, arecompeting to develop a natural gas pipelinefrom the Alaskan North Slope to the Lower48 states.“Alaska could become a significant partnerwith China in the development of value-added products from our natural gasresources, produced here in Alaska,” saidCampbell.Exxon Mobil said developing Point Thomsongas fields in Alaska’s North Slope would pushdevelopments of the pipeline.(UPI, 2.15)

10

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

At present, we are witnessing theformation of a new era of civilization. It

is a result of the latest scientific advances thatpeople living on planet Earth today are in aposition to create a comfortable environmentfor themselves. There are, however, majorsystemic problems that remain: limitedterritory and resources, population growth,different levels of technological and politicaldevelopment of nations, etc. The solutions tothese problems are yet to be found, althoughwork in that direction is underway: thecreation of the European Community (EC),the Eurasian Economic Community (EEC),the Shanghai Cooperation Organization(SCO), and several other institutions isexpected to expedite the search for solutions.The decisions that will invariably need to betaken while we look for the aforementionedsolutions should be reached on the principlesof mutual trust and benefit so as to engendera more open society. Models for sustainabledevelopment that are needed by ourcivilization today do not really exist. It is wellknown that the center of global civilization inthe 21st century is increasingly moving towardthe Asia-Pacific region.The growing demand for oil in the industrialized

and developing countries is likely to be adecisive factor in the geopolitical struggle thatwill dominate the period between 2010 and2030. According to the forecasts of manyexperts, worldwide oil production willincrease until 2015, when production will beat its peak; the subsequent years willexperience a slowdown with all of the ensuingconsequences. In this regard, as we arecompelled to come up with the basis for amodel that will allow us to determine theconditions necessary for the development ofa prosperous region, it is imperative that webegin by selecting a region. In the subsequentyears, lessons learned can be extended to otherregions. In our opinion, one of the most appropriateregions to conduct a pilot project in is North-East Asia (NEA). The prerequisites for aproject of this nature are all met by the NEAregion-the presence, no matter how incipient,of different symbols of industrial andeconomic development, of energy and humanresources, of political systems, of the nuclearpotential, of history, of religion, etc.There are few regions in the world that are asacutely contradictory in their constitution,where symptoms of deep and dangerousdeterioration lie hidden only barely beneaththe surface. Many people are of the view thatit would take 15-20 years and if nothing wasdone, the situation could spiral out of controland lead to consequences that are difficult topredict. The basic contradiction lies in theuneven distribution of resources, especiallyenergy, which are indispensable for the future

Basic Concepts of Cooperation in North-East Asia inthe Oil and Gas Sector for the Period 2010-2030

Alexander N. GulkovDirector of the Institute of Gas and OilFar Eastern National TechnicalUniversity, [email protected]

Issue & Focus

11

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

development of the region. The basis for the formation of a long-termdevelopment model for NEA can double upas the core around which co-operativedevelopment of the oil and gas sector of theNEA countries can be planned andimplemented during 2010-2030. As we know, the oil and gas sphere continuesto define the development of the NEA region.In the coming years, the influence of this sectorwill only intensify. Rapid economicdevelopment in NEA in recent years has ledto an increased demand for energy. Accordingto forecasts for the next 10 years, more thanhalf of the energy demand of the planet willbe driven by the NEA region. Already, out ofall the countries of the world, in terms of theirconsumption of petroleum products, China isthe 2nd; Japan, the 3rd; and South Korea, the7th. Further, their dependence on oil importsis 50%, 99%, and 97%, respectively. Nosignificant change in import policy is foreseenfor any of these countries in the coming yearsdespite the introduction of energy-savingtechnologies and the launch of alternativeenergy forms. Today, a large proportion of their energyimports are procured by these countries fromthe Middle East, Australia, and Russia. Russiais the second largest oil producing country inthe world and one of the largest gas producingcountries (generating approximately 13% ofthe global oil production and about 21% ofthe global gas); exports to the countries inNEA account for approximately 3% ofRussia’s exports.What has for so long deterred Russian energyexports from making their way to thecountries of NEA Several reasons could beascribed to explain the matter: first, the lackof transportation hubs-only railroads connectthe Far East with the oil-producing regions ofSiberia; second, there is a crucial lack of oilterminals on the Pacific coast of Russia; third,

the orientation of the oil and gas producers inEurope who are still steeped in the traditionalpatterns of supply and have not undertakenany significant investments in transportationor in the development of new fields; fourth,the lack of exploratory ventures to look fornew reserves of oil and gas and the lack ofcapital investment in this area; fifth, theinstability of markets-China, with the lack oforientation in its north-eastern areas whosereserves of coal are significant, and the bindingof the cost of imported energy to the cost oflocal coal; Japan, with the Northern Territoriesissue and the issue of long-term contracts withother countries for the supply of energy; andKorea, with its stable pool of long-term energysuppliers and the influence of external andinternal factors in the decision-making withinits energy sector. The energy supply to the Democratic People’sRepublic of Korea should be consideredseparately because of the nature of the existingpolitical system that governs it, which servesthe country with certain distinct disadvantagesas well as advantages. One of the positives isthat the specific consumption of naturalresources per inhabitant in that country, withits relatively minimal acceptable livingstandard, allows for an unusual pattern ofplanning and distribution throughout thenation. One of the primary disadvantages isthe largely imaginary threat that is perceivedas coming from that country to the worldcommunity in the form of aggression andnuclear weapons. While the threat does exist,it is largely a political affair, since theDemocratic People’s Republic of Korea isundoubtedly an aberration when the majorityof the nations of the world are committed tothe capitalist path of development. We shall now consider the foundations of theconcept of cooperation among countries inNEA, particularly with respect to their oil andgas sector, in the near future.

12

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

Goals, objectives, and priorities ofthe concept

The main purpose of the concept advocatedin this study is to create a unified approach tothe oil and gas sector of NEA, a region capableof producing not only hydrocarbon oil andfood petrochemistry but also creatingconditions for the sustainable development ofits resources and people. To achieve the goal, key provisions of thedevelopment strategies of Russia, China, SouthKorea, and Japan would need to beimplemented by 2030. The following are themain tasks that need to be accomplished:- Drafting projections of the levels of oil and

gas production in the countries of NEA ona medium- and long-term basis, assumingoil and gas exploration

- Evaluating the prospects of the domesticconsumption of oil and gas in NEA basedon calculations of the optimal energy balancein the region while considering the economicand resource structures of the variousnations Studies delving into the followingareas may have to be conducted:

- On the countries in NEA, focusing on theircommon production, their transportinfrastructure, on the exploration, extraction,and processing of hydrocarbons in order toensure the region’s raw materials and oilproducts are utilized in the best possible way

- On the creation of a unified system of gassupply in the region

- On the creation of transport corridors for thetransfer of oil and gas pipelines forhydrocarbon processing and use

- On the organization of common centers fortraining and retraining and for studyingproblems related to the complex use ofhydrocarbons

- On the creation of conditions necessary toattract foreign investment, in order to

implement a unified approach to the oil andgas sector throughout the NEA

- And on the creation of an internationalconsortium for planning, organizing, andimplementing major projects in the oil andgas sector of the NEA

The key favorable factors toward theestablishment of a unified approach to oil andgas sector of the NEA are outlined as follows:- There is a substantial resource base of oil

and gas in the region. - A high and growing demand for petroleum

products and gas. - A need for improving and optimizing the

regional energy mix of the countries in theregion.

- The unique geographical position of theregion creates ample opportunities forexporting both oil and gas and their by-products.

The main factors hindering the establishmentof a unified approach to the oil and gas sectorof the NEA are listed as follows:■The lack of a comprehensive agreement on

cooperation in the oil and gas sector of theNEA nations stands out prominently. Theprevious agreement did not contain asystematic approach to support cooperationin the oil and gas sector; it was more of anagreement on the intent of the countriesinvolved and focused on theimplementation of local projects only. Allthis makes the formation of a unifiedapproach to the oil and gas sector of theNEA very uncertain, particularly in viewof the complexities involved.

■The lack of a coherent policy in NEA, aseach nation attempts to pursue anindependent policy in its oil and gas sectorwithout taking into account the interests ofother states, is a major deterrent to aunification drive today. Effectivedevelopment in the energy sector isimpossible without a coherent policy, as

13

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

countries may be unequally placed in terms ofthe availability of resources, manpower andtechnological capabilities, levels of economicdevelopment, etc. Only the joint participationof countries in neftegazorazvedke, fieldconstruction, extraction of hydrocarbonsand their transportation, processing, andfinally, in the sale of products, will meet thechallenge of creating a single oil and gascomplex that can function stably andfacilitate solutions to the geopoliticalproblems in NEA without upsetting thebalance of forces in the region.

■The lack of an integrated policy with respectto subsoil use is already acknowledged. Alack of consensus plagues other fields too,most notably in relation to the running ofoil and gas fields and the managementof rights to geological exploration anddevelopment of large deposits. There havebeen difficulties in implementing tasksowing to the lack of clear positions on issuessuch as participation in mining andinfrastructure development in China, Japan,and Korea, particularly among the oil andgas companies in these countries. There isa need for clear and consistent policy inorder to draw potential foreign partners andglobal consumers of oil and gas.

Other inimical factors include the high capitalintensity of exploration, mining, oil andgas transportation, and the establishmentof processing facilities; the lack of owninvestment resources for the developmentof the complex; and the high levels ofenvironmental restriction that demandcompliance. The first step toward the realization ofprofitable cooperation can be the beginningof the construction of major oil and gaspipelines in the Far East of Russia. A majorpipeline from East Siberia to the Pacific Oceanwould greatly deliver on the economic and

geopolitical interests of Russia and those ofNEA as well. The following points are relevant to Russia asa whole: - An increase in the capacity of the Eastern

and Far Eastern regions would trigger theimplementation of important prerequisitesfor sustainable development.

- Strengthening the geopolitical potential ofRussia in the East would lead to the growthof Russia’s geopolitical influence in the Asia-Pacific region.

- The diversification of Russia’s economicsystems is vital.

- The formation of new places of employmentand income growth is important.

- A positive impact on the demographicpotential of the region is long overdue.

- The nation would have to meet its regionalneeds with regard to oil, gas, and energyresources, through its own sources.

For the countries of NEA (Japan, China,Republic of Korea) the following are distinctpossibilities: - Meeting the growing demand for oil and

gas.- Meeting the growing demand for electricity. - Diversifying their oil and gas markets and

energy resources.- Creating a more reliable and stable presencein the global market; the construction of theSakhalin-Khabarovsk-Vladivostok line andthe Yakutia-Khabarovsk channel are essentialboth for the development of the region andthe long-term natural gas supply among thecountries of NEA.

For the successful implementation of a regimeof cooperation between the countries in NEAwith respect to their oil and gas sector duringthe period 2010-2030, all the countries in NEAshould consider the following conditions: ■Stop pursuing questions related to possible

adjustments or revisions of existing stateborders.

14

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

■The cost of oil and gas should bedetermined by prevailing world prices.

■Equal opportunity should be extended toinvolve all the countries of NEA in theexploration and development of oil and gasresources along the Far East of Russia,including the shelves of the northern andFar Eastern seas.

■The main export routes of oil and gas willend on Russia’s Pacific coast, particularlyaround south of the Primorsky Region.

■The main mode of transportation ofhydrocarbons is expected to be sea vessels;each nation should respond flexibly toemerging markets and eliminate thecreeping in of any privileges to any of theparticipants in the cooperative undertaking.

Raw materials and the state of oilexploration

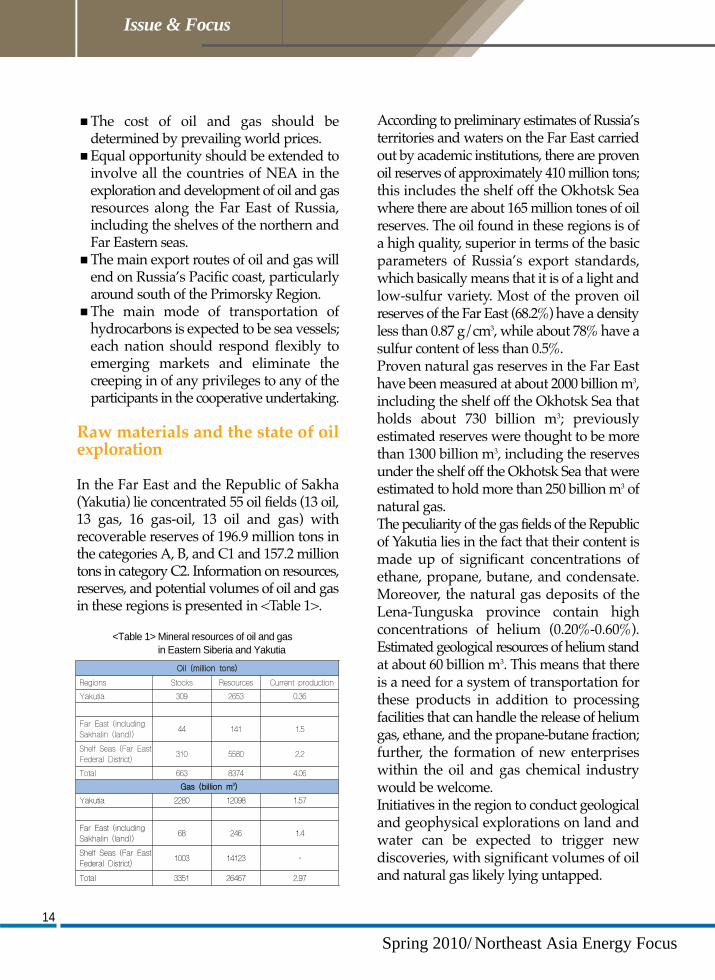

In the Far East and the Republic of Sakha(Yakutia) lie concentrated 55 oil fields (13 oil,13 gas, 16 gas-oil, 13 oil and gas) withrecoverable reserves of 196.9 million tons inthe categories A, B, and C1 and 157.2 milliontons in category C2. Information on resources,reserves, and potential volumes of oil and gasin these regions is presented in <Table 1>.

According to preliminary estimates of Russia’sterritories and waters on the Far East carriedout by academic institutions, there are provenoil reserves of approximately 410 million tons;this includes the shelf off the Okhotsk Seawhere there are about 165 million tones of oilreserves. The oil found in these regions is ofa high quality, superior in terms of the basicparameters of Russia’s export standards,which basically means that it is of a light andlow-sulfur variety. Most of the proven oilreserves of the Far East (68.2%) have a densityless than 0.87 g/cm3, while about 78% have asulfur content of less than 0.5%. Proven natural gas reserves in the Far Easthave been measured at about 2000 billion m3,including the shelf off the Okhotsk Sea thatholds about 730 billion m3; previouslyestimated reserves were thought to be morethan 1300 billion m3, including the reservesunder the shelf off the Okhotsk Sea that wereestimated to hold more than 250 billion m3 ofnatural gas.The peculiarity of the gas fields of the Republicof Yakutia lies in the fact that their content ismade up of significant concentrations ofethane, propane, butane, and condensate.Moreover, the natural gas deposits of theLena-Tunguska province contain highconcentrations of helium (0.20%-0.60%).Estimated geological resources of helium standat about 60 billion m3. This means that thereis a need for a system of transportation forthese products in addition to processingfacilities that can handle the release of heliumgas, ethane, and the propane-butane fraction;further, the formation of new enterpriseswithin the oil and gas chemical industrywould be welcome. Initiatives in the region to conduct geologicaland geophysical explorations on land andwater can be expected to trigger newdiscoveries, with significant volumes of oiland natural gas likely lying untapped.

<Table 1> Mineral resources of oil and gasin Eastern Siberia and Yakutia

OOiill ((mmiilllliioonn ttoonnss))

Regions Stocks Resources Current productionYakutia 309 2653 0.36

Far East (includingSakhalin (land)) 44 141 1.5

Shelf Seas (Far EastFederal District) 310 5580 2.2

Total 663 8374 4.06GGaass ((bbiilllliioonn mm33))

Yakutia 2280 12098 1.57

Far East (includingSakhalin (land)) 68 246 1.4

Shelf Seas (Far EastFederal District) 1003 14123 -

Total 3351 26467 2.97

Proven reserves of oil and gas within theYakutia and the Far East can allow for thecreation of a new center of hydrocarbon rawmaterials, fully satisfying the needs of the FarEastern federal district in the oil and gas sector,as well as ensuring the possibility of EastSiberian oil and gas exports to the Asia-Pacific(notably, Korea, China, Japan, and the USA).Increased export of hydrocarbons to relevantmarkets will largely depend on the detailedexploration of oil and gas in the region. In analyzing the possible export of oil and gasto the NEA, the reserves in Western Siberiaand the shelf off the northern seas should beexamined. Even today, in connection withglobal warming, we should consider thepossibility of oil and gas transport along theNorthern Sea Route, subject to the explorationand development of deposits in the shelf offthe northern seas and the construction of gasliquefaction plants. The successful participation of Russia inthe proposed cooperation in the oil and gassector across NEA would depend on theunderstanding that Russia views itself as anequal strategic partner on the Pacific coast, asa nation that is able to influence thedevelopment of all events taking place in theregion. Moreover, with greater resources,including oil and gas, Russia would be readyto become a guarantor of energy security inthe region, subject to its interests.The main interests of Russia in the Far Eastwould be related to the following: - The economic development of territories

and improvements in living standards - The rational use of natural resources - Strengthening national security in the region - Building promising development and

exploration initiatives along the region,taking into account the geopolitical changesin the 21st century associated with thedepletion of natural resources.

The progression of the concept of cooperationin the oil and gas sector can be divided intothe following stages:■The conclusion of agreements on cooperation

in energy security in the region. ■The development of transnational projects

for the exploration and development of theoil and gas resources of NEA.

■Attracting investments for the implementationof transnational projects, taking into accountthe interests of all countries in NEA.

■Creating the oil and gas markets in NEA.■The gradual replacement of oil and gas as

sources of power with the advent ofhydrogen, nuclear, and alternative energysources.

In conclusion, this paper examined certainobjective prerequisites for the formationand development of energy cooperation,particularly within the oil and gas sector ofNEA. A special structure-forming role isproposed to be assigned to Russia. Theperformance of this role would be possibleonly if the efforts of all countries in NEA wereconcentrated. The adoption of a strategic linethat takes into account all the economic,political, and energy conditions in the regionand their associated global fall-out is necessaryin addition to the political will to implementthe same because only then would it bepossible to realize the proposals made in thispaper.

15

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

The Far Eastern Federal District (FEFD)comprises a total of 6,216 thousand sq. km

(36.4% of the Russian Federation’s territory).FEFD includes nine subjects of the RussianFederation: the Republic of Sakha (Yakutia),the Primorski Territory, the KhabarovskTerritory, the Amur Region, the KamchatkaEdge, the Magadan Region, the SakhalinRegion, the Jewish Autonomous Region, andthe Chukchi Autonomous Region. As ofJanuary 1, 2009, 6,460 thousand people wereliving in the FEFD (4.6% of the totalpopulation of Russia); out of these, 74%comprised the urban population. At thepresent time, 4.6% of the gross volume ofRussia’s total internal product; 3.2% of thecountry’s industrial product volume; and 3.6%of its agricultural production volume isproduced by the FEFD. The Far East basinports provide 17.7 percent of the total cargoturnover of Russian seaports. Over the last few years, the FEFD’s grossregional product has shown a growth levelof 5.1% (Russia showed an average growth of7.2% as regards its real gross internationalproduct for 1998-2005). It is expected thatfor the period extending till 2025, the

development of the Far East will be definedappreciably by the development of itsconsiderable natural resources (fish, wood, oiland gas, coal, ore, and nonmetallic resources)as also by the essential involvement of thedistrict with the countries of the Asian-PacificRim (APR) in connection with goods turnover.The natural climatic conditions of the Far Eastcan be characterized as rather severe, evenextreme. Only in the south of the PrimorskiTerritory does the mid-annual temperatureexceed zero degrees centigrade. In the light ofthese facts, it is clear that the power industryplays a key role in the social and economicdevelopment of the FEFD. Secure and stableenergy and heat supply is a basic necessity forthe citizens and enterprises of the Far Eastduring the winter period and should beprovided at any cost. In other words, thesupply of these resources is mandatory andcannot be subject to the existing marketconditions.

Structure and Condition of theFEFD’s Energy Industry

The power industry in Russia can be divided

16

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

Apropos Cogeneration Based on the Development ofthe Small Power Industry Sector in the Far East

Svetlov I.B. Director of the ANO “CSRD RPC FE” (Autonomous Non-commercial OrganizationThe Center of Strategic ResearchesDevelopment of Resources Power Complex of the Far East)[email protected]

Zagumynnov A.G. Deputy Director of foreign economic relations of theANO “CSRD RPC FE.”

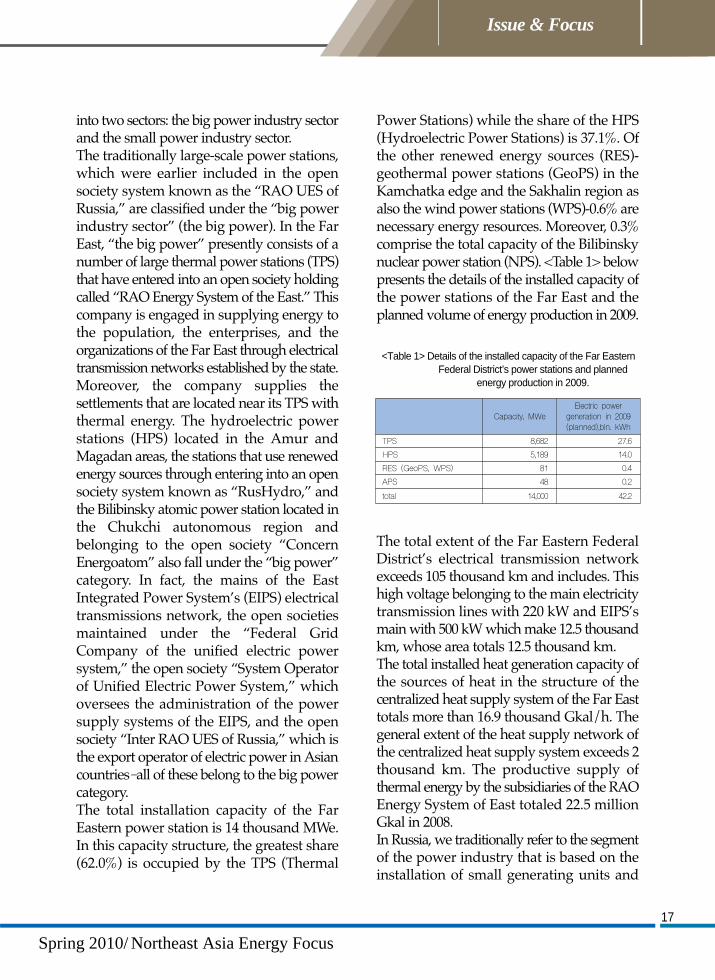

into two sectors: the big power industry sectorand the small power industry sector.The traditionally large-scale power stations,which were earlier included in the opensociety system known as the “RAO UES ofRussia,” are classified under the “big powerindustry sector” (the big power). In the FarEast, “the big power” presently consists of anumber of large thermal power stations (TPS)that have entered into an open society holdingcalled “RAO Energy System of the East.” Thiscompany is engaged in supplying energy tothe population, the enterprises, and theorganizations of the Far East through electricaltransmission networks established by the state.Moreover, the company supplies thesettlements that are located near its TPS withthermal energy. The hydroelectric powerstations (HPS) located in the Amur andMagadan areas, the stations that use renewedenergy sources through entering into an opensociety system known as “RusHydro,” andthe Bilibinsky atomic power station located inthe Chukchi autonomous region andbelonging to the open society “ConcernEnergoatom” also fall under the “big power”category. In fact, the mains of the EastIntegrated Power System’s (EIPS) electricaltransmissions network, the open societiesmaintained under the “Federal GridCompany of the unified electric powersystem,” the open society “System Operatorof Unified Electric Power System,” whichoversees the administration of the powersupply systems of the EIPS, and the opensociety “Inter RAO UES of Russia,” which isthe export operator of electric power in Asiancountries-all of these belong to the big powercategory.The total installation capacity of the FarEastern power station is 14 thousand MWe.In this capacity structure, the greatest share(62.0%) is occupied by the TPS (Thermal

Power Stations) while the share of the HPS(Hydroelectric Power Stations) is 37.1%. Ofthe other renewed energy sources (RES)-geothermal power stations (GeoPS) in theKamchatka edge and the Sakhalin region asalso the wind power stations (WPS)-0.6% arenecessary energy resources. Moreover, 0.3%comprise the total capacity of the Bilibinskynuclear power station (NPS). <Table 1> belowpresents the details of the installed capacity ofthe power stations of the Far East and theplanned volume of energy production in 2009.

The total extent of the Far Eastern FederalDistrict’s electrical transmission networkexceeds 105 thousand km and includes. Thishigh voltage belonging to the main electricitytransmission lines with 220 kW and EIPS’smain with 500 kW which make 12.5 thousandkm, whose area totals 12.5 thousand km.The total installed heat generation capacity ofthe sources of heat in the structure of thecentralized heat supply system of the Far Easttotals more than 16.9 thousand Gkal/h. Thegeneral extent of the heat supply network ofthe centralized heat supply system exceeds 2thousand km. The productive supply ofthermal energy by the subsidiaries of the RAOEnergy System of East totaled 22.5 millionGkal in 2008.In Russia, we traditionally refer to the segmentof the power industry that is based on theinstallation of small generating units and

17

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

<Table 1> Details of the installed capacity of the Far EasternFederal District’s power stations and planned

energy production in 2009.

Capacity, MWeElectric power

generation in 2009(planned),bln. kWh

TPS 8,682 27.6HPS 5,189 14.0RES (GeoPS, WPS) 81 0.4APS 48 0.2total 14,000 42.2

complexes and that functions on traditionalkinds of fuel and renewed energy sources(RES) as the “small power industry sector”(the small power). Some parts constituting thesmall power cannot be connected to thecentralized electrical transmission network. Asmall generating unit alludes to a generatingobject with the installed capacity of up to 25MWe while a small generating complex refersto a generating object having the combinedinstalled capacity to produce electric andthermal energy of up to 25 MWe, includingthe heat generating capacity.The small power has traditionally solvedpower-related problems by increasing thestability and reliability of all the state powersystems. It has been doing this by creatingadditional generating capacity, increasing theefficiency of the power systems at the regionaland municipal levels, bringing downtechnological losses by bringing generatingcapacities nearer to the consumers, and finally,by reducing the cost of transmitting power.The small power also facilitates theimprovement of power safety and aids thestate in balancing fuel and outputted energyby increasing the use of local fuels.Nevertheless, its key mission remains theprovision of power supply to decentralizedconsumers and increasing the reliability andprofitability of the existing power supply inhousing and communal services.The small power of the FEFD comprisesmunicipal and private boiler houses andelectric power stations, along with enterprisesbelonging to the local electrical transmissionnetworks and district central heating systems.Most of the “small power industry sector” iscontrolled and financed by regional andmunicipal authorities, in whom is also vestedthe responsibility for this sector. Owing to thespecific features of the power industry, privateenergy enterprises as a rule cooperate withthe regional and municipal authorities.

Although a substantial part of the FEFDpopulation lives in small towns and villages,the electricity and heat energy generationcenters are concentrated in big cities such asKhabarovsk, Vladivostok, Komsomolsk-on-Amur, Yuzhno-Sakhalinsk, and Petropavlovsk-Kamchatsky. The high concentration of energyfacilities in these cities helps them to producean adequate amount of heat. At the same time,most of the small towns and villages of theFar East are supplied with heat by privateindustrial enterprises and small municipalboiler houses located in housing andcommunal services. At present, there are atotal of 4,710 small municipal boiler houses inthe FEFD’s regions. Most of them use coal andmasout (black mineral oil) as fuel. DuringRussia’s economic development in the sovietperiod, the construction of apartment housessupplied with centralized heating waspreferred. Today, these apartment houses haveno alternative heating system, and therefore,the only sources of heat available to them arethe municipal boiler houses located in everysmall town or village. There are no electricity generation sources inmany small towns and villages of the FEFD,and therefore, electric power needs to betransmitted to these places from where thepower stations are located, which is oftentimes a long distance. As a result, small townsand villages in remote areas-especially nearstate borders and in the areas adjoining thepower systems of other subjects of the RussianFederation-experience shortage of electricpower supply during the peak of the winterseason.In a number of inhabited localities of theFar East, electric power is supplied bydecentralized sources-diesel power stations(DPS) that were constructed over the 60th tothe 80th year of the last century. In particular,in the Republic of Sakha (Yakutia), the localpower industry is equipped with almost 200

18

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

DPS, for the functioning of which it annuallydelivers more than 120 thousand tons of dieselfuel. More than 80 diesel power stationsprovide consumers with electric energy in thedecentralized power supply zone of theKhabarovsk territory while 64 DPS work inthe Primorski territory toward supplyingpower. In the Sakhalin region, there are 22power knots carrying out a decentralizedpower supply function. Among these powerknots, 11 are located on the Kuril Islands.The present technical condition of thecomponents of the power industry andmunicipal services in majority of the regionsof the Far East points to a real threat of increasein breakdowns and compromised powersafety. In the FEFD, about 70% of the powergenerating equipment has been in operationfor terms ranging from 20 to 40 years-and theirdeterioration exceeds the 60% margin-while30% of the equipment has been in use for over40 years. The general share of the effectiveequipment totals only 22.8%. The deteriorationof the fixed capital of the housing andcommunal service enterprises ranges from60% to 100%. The percentage of the financial resources thatthe FEFD allocates from its regional and localbudgets toward power supply is a constantlygrowing number. In a situation of economiccrisis, this fact leads to an increased deficiencyin the budgets of the majority of the FarEastern subjects of the Russian Federation andmunicipal unions. Moreover, these limitedresources suffice only for the maintenance ofthe existing heat production capacity and DPS.The abovementioned chronic deficiency offinancial assets makes the acquiring of newpower equipment difficult and has thus ledto an increasing tendency of continuing to useextremely old power equipment. As a result,the efficiency of the equipment of municipalboiler houses is extremely low. It follows thatdue to the large scale poor quality of thermal

protection accorded to the district heatingsupply system’s pipelines, the loss of thermalenergy is excessively great.The basic fuel resources of Far Eastern subjectsof the Russian Federation are coal and mineraloil products. The cost of fuel and the transportcost of its delivery to consumers have bothbeen showing a constant rise. In the 2005-2006winter, the FEFD’s municipal boiler housesconsumed over 6.2 million tons of firm fuel-totaling the sum of almost 50 billion roubles-and 1.8 million tons of liquid fuel, totaling thatof over 16 billion roubles (taken altogether,about 66 billion roubles). The result of thedeficiency of fuel that arises during theseparate periods of autumn and winter is thatthe maximum power load, as a rule, occursduring periods of sharp cold. Thus, the heatsupply organizations are frequently unable tomaintain an appropriate temperature modeas regards the heat-carrier equipment in theheating systems’ pipelines. As a result, thewater temperature of the heating systemdecreases and owing to the low temperatureoutdoors, the population has no choice but tosupplement the provided warmth by usingelectroheating devices to heat their houses.The direct outcome of this is a considerablegrowth of electrical energy consumption inhousing and communal services, which inturn leads to the electrical supply systemgetting overloaded and compromises itsreliability. The average household powerconsumption in the FEFD territory is high. Itthus follows that in 2008, the share of theelectric power consumed by the FEFDpopulation exceeded the Russian middlinglevel on more than two occasions (by 19.6%and 7.4%).The equipment being used by the DPS todayis so worn out that it is inappropriate for usefrom even the moral point of view. Due to thefact that the cost of the electric powerdeveloped by these DPS is the highest,

19

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

implementing an overestimated blanket tarifffor the electric energy provided to all the otherconsumers becomes necessary-a factor thatconstrains the development of the real sectorof the economy and displeases the population.This problem in especially acute in theRepublic of Sakha (Yakutia), where the cost ofsubsidizing diesel power has already reached4 billion roubles. In the Primorski Territory,the average deterioration of the DPSequipment is estimated to be 72.9%.Thus, the power branch of the FEFD-especiallythe “small power” branch-requires urgentmodernization, which should be carried outin the near future at any cost.

Prospects of Gasification in the FarEast Federal District

Almost 25% of the total gas and 15% of thetotal oil resources of Russia are located in thebowels of Eastern Siberia and the Far East. Theinitial total hydrocarbon resources present hereare estimated to have been equivalent to100-140 billion tons of oil. Within this region,including its sea shelf, 140 oil and gas fieldshave been developed, while the developmentof about 50 major oil fields and over 170 gasfields is predicted to take place in the nearfuture.In Eastern Siberia and the Far East, 15 gas and7 oil deposits containing 1,8 bln. m3 gas stocksand 396.2 million tons of oil have beenprepared for industrial development. Thereconnoitered and preliminary estimated oiland gas stocks of the six major oil and gasfields of the Sakhalin shelf are estimated at 292million oil tons and - 0.9 bln. m3 of free gas.At present, the development of oil gas fieldsis being actively carried out in the Far East.The construction of the main oil pipeline “theEastern Siberia - Pacific ocean” (ESPO) hasresulted in the development of some oildeposits of Yakutia that contain considerable

stocks of passing gas. The realization of the East gas program willallow for the installation of gas almostthroughout the small power of the Far East.Within the framework of this program, newcenters of gas production will be created inthe Yakutia, Kamchatka, and Sakhalin regionsof the FEFD. In the beginning of 2012, theopen society “Gazprom” will construct a main“Sakhalin-Khabarovsk-Vladivostok” gaspipeline, the resource base for which will bethe “Sakhalin-1” gas in the short term and the“Sakhalin-3” gas in the long term. In 2012,Gazprom plans to start the construction of a“Yakutia-Khabarovsk-Vladivostok” gaspipeline (implementation term: the beginningof 2017). The capacity of this gas pipeline willextend to 32-35 billion cubic meters per yearand its length will be about 4.5 thousand km.It will share a uniform corridor with the oilpipeline system ESPO and deliver gas from alarge Chajandinsky deposit and otherYakutian deposits to the Russian consumersof the Far East, besides exporting it to thecountries of the Asian-Pacific Rim. A uniformtransport system will be generated on the basisof these two gas pipelines. Gas supply to theKamchatka Edge is planned to be providedat the expense of infrastructural developmentof the Kshuksky and Under-Kvakchikskydeposits located at the western coast of theKamchatka Peninsula and the constructionof the main gas pipeline “Sobolevo-Petropavlovsk-Kamchatskij,” the operation ofwhich is planned in 2010. The project will alsoprovide the necessary resources for theconstruction of distributive networks in thePetropavlovsk-Kamchatskij area.However, in spite of the abovementionedefforts, the gasification of the Far East withinthe framework of Gazprom open society’sEast program will not result in its plannedresult, that of a sharp reduction of expenseswith regard to housing and communal

20

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

services power supply, if not accompanied byan in-depth modernization of the powerbranch at the levels of both the RussianFederation subjects and the power generatingcompanies. An inspection of the boiler networkcommunications carried out by theAutonomous Non-commercial Organization“The Center of Strategic ResearchesDevelopment of Resources Power Complexof the Far East” (ANO “CSRD RPC FE”) inlocalities of the Far East experiencing shortagesof electrical objects and security energy carriersconfirms the urgent need for installing newpower object equipment. The requiredeconomy of fuel and decrease in the cost priceof electric and thermal energy can only beachieved through the modernization of “thesmall power” on the basis of the newesttechnologies facilitating the combinedgeneration of electric and thermal energy(cogeneration).

Cogeneration in “The Small Power”as means of Solving the PowerProblems of the Far East

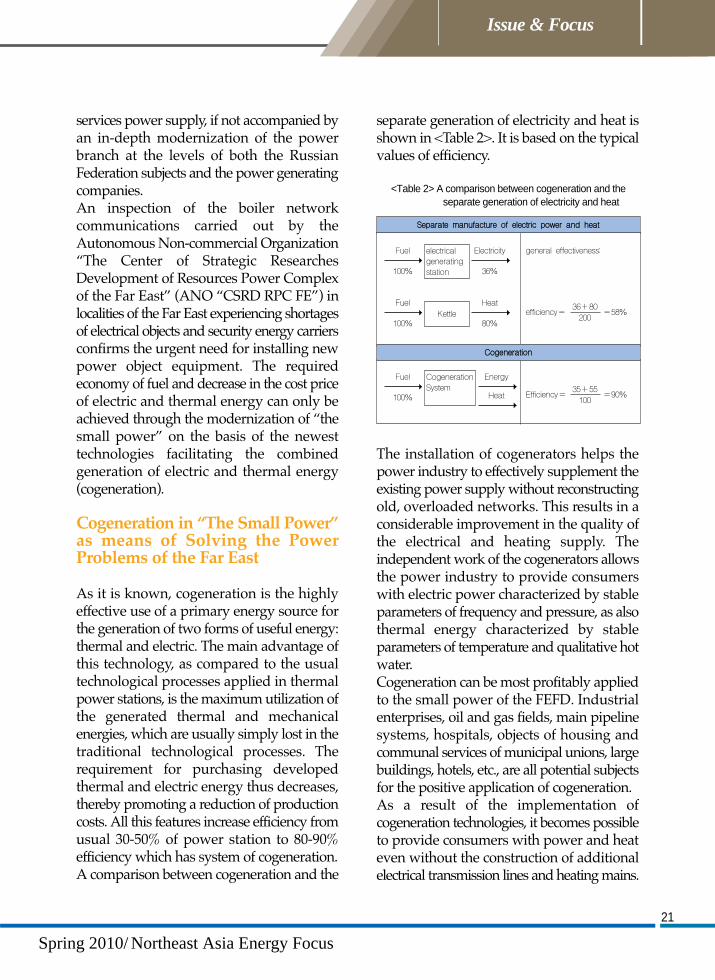

As it is known, cogeneration is the highlyeffective use of a primary energy source forthe generation of two forms of useful energy:thermal and electric. The main advantage ofthis technology, as compared to the usualtechnological processes applied in thermalpower stations, is the maximum utilization ofthe generated thermal and mechanicalenergies, which are usually simply lost in thetraditional technological processes. Therequirement for purchasing developedthermal and electric energy thus decreases,thereby promoting a reduction of productioncosts. All this features increase efficiency fromusual 30-50% of power station to 80-90%efficiency which has system of cogeneration. A comparison between cogeneration and the

separate generation of electricity and heat isshown in <Table 2>. It is based on the typicalvalues of efficiency.

The installation of cogenerators helps thepower industry to effectively supplement theexisting power supply without reconstructingold, overloaded networks. This results in aconsiderable improvement in the quality ofthe electrical and heating supply. Theindependent work of the cogenerators allowsthe power industry to provide consumerswith electric power characterized by stableparameters of frequency and pressure, as alsothermal energy characterized by stableparameters of temperature and qualitative hotwater. Cogeneration can be most profitably appliedto the small power of the FEFD. Industrialenterprises, oil and gas fields, main pipelinesystems, hospitals, objects of housing andcommunal services of municipal unions, largebuildings, hotels, etc., are all potential subjectsfor the positive application of cogeneration. As a result of the implementation ofcogeneration technologies, it becomes possibleto provide consumers with power and heateven without the construction of additionalelectrical transmission lines and heating mains.

21

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

<Table 2> A comparison between cogeneration and the separate generation of electricity and heat

Fuel electrical generatingstation100%

Electricity

36%

FuelKettle

100%

Heat 36+80200

general effectiveness:

efficiency= =58%80%

SSeeppaarraattee mmaannuuffaaccttuurree ooff eelleeccttrriicc ppoowweerr aanndd hheeaatt

Fuel CogenerationSystem

100%

CCooggeenneerraattiioonn

Energy

Heat35+55100Efficiency= =90%

Bringing the power sources nearer to theconsumers allows for the considerablereduction of networks, and therefore, leads tothe saving of the finance resources that areusually needed for the construction andservice of such networks. Moreover, itfacilitates an improvement in the quality ofenergy produced and lowers the lossesincurred during its transmission.The conditions that are put forward by theelectric power and heating suppliers forconnection to the electricity and heatingsupply networks often result in considerableirrevocable expenses and sometimes, even tothe revision of the above connections. Thespecific cost of connection to power networkshas already been reached and as regards anumber of power objects, has even exceededthe specific cost of cogeneration installationswith identical power parameters. The essential difference between the capitalexpenses for power supply from networksand power supply from one’s own source isthat the capital expenses connected withcogeneration acquisition are compensatedwhile the capital expenses incurred duringtaking a connection to the existing networksare irrevocably lost in the transfer of newlyconstructed substations. Therefore, accordingto the economically weak Russian customerswho want to connect to the existing electricitynetworks, the power supply companiesshould construct all the technologicalsubstations (transforming station connectors,etc.) that are needed for this connectionand transfer these substations free of costto the electrical network companies. The synchronized development of “big” and“small” (or local thermal) power is aphenomenon that is seen worldwide. Therehas been a global increase in the installationshare of the small power due to thecogeneration cycle, which allows for theoptimal development of heat and electric

power for the housing-and-municipal sectorand the establishment of a social and industrialinfrastructure, besides facilitating effectivepower saving. Moreover, cogeneration lightensthe load of the main heat and powergenerating networks of the big power. Forexample, in the USA and Great Britain, thesmall power cogeneration share reaches 80%while it reaches 70% and 50% in theNetherlands and Germany, respectively.Outside of Russia, this process is activelysupported by the state through legislativeregulation and budgetary financing. Theexperience of industrially developed countriesshows that the construction of thermal powerstations having a low generating capacityinstead of large power units results in a ten-fold reduction in the total expenses incurredduring the modernization process of thepower industry.

Gas Turbine Technologies as a Basisof Cogeneration in the Small Powerof the Far East

Aiming to create the necessary prerequisitesfor the re-equipment of the FEFD’s “smallenergy,” the ANO “CSRD RPC FE” designeda project concerning the construction of a cityplant in Khabarovsk that would comprise agas turbine and gas turbine cogeneration unit(GTCU) of small and medium generatingcapacity.A GTCU generates electrical power throughthe burning of natural gas, the primary energycarrier inside the turbine, while the thermalenergy and exhaust generated at the sametime are used for heating. A GTCU has aparticular advantage, especially in the caseswhere simultaneous electrical power supplyand large scale heating supply are needed.Better efficiency of fuel use, substantialdecrease in the primary demands for fuel, anddecrease in power and heating supply costs

22

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

are the main advantages of using a GTCU. AGTCU is remarkable for its compact design,operation simplicity, extremely low vibrationrate, comparable ease of noise suppression,and low installation cost.In the Far East, GTCUs are able to efficientlysolve municipal heating supply problems aswell as local power supply problems. In thetowns and villages that are supplied withelectrical power through a transmissionnetwork of “large energy,” the electricitygenerated by a GTCU may be used tosupplement the existing heat supply or tocompete with the open society RAO EnergySystem of East, through which it may aid adecrease in energy tariffs.This project is undoubtedly economicallyviable. As a result of the modernization of4,710 Far Eastern boiler houses through thereplacement of old equipments by GTCUs - ofwhich 80% are to be produced at theKhabarovsk turbine plant - 4.6 million tons ofreference fuel will be saved per year. The totalamount of money saved only through thedecrease in fuel purchasing, even withoutcalculating the money saved in repair andoperation costs, will come to 36-38 billionrubles - perhaps even more. In our opinion, the introduction of advancedtechnologies used in overseas companiesthat are world class leaders of turbinemanufacturing is the most reasonable way ofimplementing the Khabarovsk gas turbineplant project. We have already initiatedcontact with our future partners in Japantoward this objective. We also plan to use thetechnologies developed in Russia during theimplementation of this project.The Limited Liability Company “Khabarovsk’sgas turbine plant (KGTP)” was founded as aproject operator toward the implementationof this project on March 31st, 2009.In April, the Khabarovsk Region’s governmentprovided the KGTP with a 31.6 hectare plot

in the northern industrial area of Khabarovsk.Together with the concerned Khabarovskagencies and organizations, we formulated anelaborate plan of action aimed at the successfulimplementation of the project. This plan alsoincluded such project support measures asthe granting of tax relief and financingof endorsements to the KGTP by thegovernment of the Khabarovsk region.This project was backed in full by therepresentative of the Russian president in theFEFD, Victor Ishaev, and by the RussianFederation’s minister of energy, SergeyShmatko. With their support, we could obtainthe preliminary consent of the Russian“Vnesheconombank” and “Vneshtorgbank”managements toward extending the creditguarantee of the Japan Bank for InternationalCooperation to the KGTP. Moreover, theKhabarovsk gas turbine plant construction isto be included in the priority project list of thepresidential commission for the modernizationand technological development of the Russianeconomy. The Russian government’s decreeconcerning the state’s support to the projectis presently under consideration in the relatedministries and agencies. At the present time, increasing the energyefficiency of its economy and the saving of itsresources are Russia’s national priorities.On June 4, 2008, the president of theRussian Federation-Dmitry Medvedev-signedthe presidential decree No. 889 “on certainmeasures aimed at increasing the energy-related and ecological efficiency of the Russianeconomy.”At the extended session of the state councilheld in June 2009, the measures needed forincreasing the energy efficiency of the Russianeconomy at large was the main subjectof discussion. President Medvedev, whochaired the session, set a target of reducing thepower intensity of the state economy by 40%.The state council took the decision to outline

23

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

some drastic measures concerning themodernization of the thermoelectric powerstations, including switching them over tothe combined heat and power generationmode (cogeneration mode). Medvedev alsorepeatedly brought up the question of energyefficiency at the sessions held by thepresidential commission for the modernizationand technological development of the Russianeconomy. In the session of the commissionheld in September 2009, the President said:“We have a lamentable situation on our handsbecause the energy intensity of our country’sgross internal products outnumbers manifoldthe same of developed countries. Our heatsupplying system loses more than 50% of itsgenerated heat.” The federal law of the Russian Federation No.261-fl dated November 23 (f 2009), whichstates that “energy-saving and increasing ofpower efficiency is also about the introductionof changes into certain legislative acts of theRussian Federation” has already taken effect.This law introduces the concept of energy-saving as well as technologies related toenergy-saving and increasing energy efficiency.It also establishes legal relations in this field.The law gives priority to investment projectsaimed at reducing the consumption of naturalgas, electricity, and useful heat consumption.Companies, organizations, and businessmenimplementing such projects might be grantedpayment subsidies from the federal budgetestablished by the Russian Federation’sgovernment.The law outlines the measures related to theplanning of power saving and increase ofenergy efficiency at the federal, regional, andmunicipal levels. These plans will go on tobecome the base for setting goal-orientedindicators of power saving and increasingenergy efficiency together with the fixing ofthe amount of subsidies granted from thefederal budget to the regional and municipal

budgets toward furthering the aims of energysaving and increased energy efficiency. Probably, in the immediate future, the personalcontribution of the presidential representativesin federal districts and of the state ministers,governors, and other managers towardincreasing energy efficiency and recoursessaving will become the main criteria forestimating the results of their activities.The construction of the Khabarovsk gasturbine plant completely corresponds to thegovernment’s established priorities, leadingus to believe that the project will undoubtedlyreceive governmental support and that theplant’s production in the Russian market willmove forward smoothly.As increasing Russia’s energy efficiency,especially in the country’s housing and publicutilities, is not only an imperative need fromthe point of view of the country’s economybut is also one of the most important politicalchallenges facing the Russian leaders of today,the active participation of Korean businesscircles toward solving this problem will serveto strengthen the friendship and goodwillbetween Korea and Russia. The successfulimplementation of the Khabarovsk gas turbineplant project will not only serve as a perfectexample of such participation but also hasevery chance of fostering large-scalecooperation from Russia, which will provefavorable to Korean firms for exerting powerin Far East Russia. This cooperation,undoubtedly, will positively impact otherspheres of mutual relations between Koreaand Russia.

24

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

25

Spring 2010/ Northeast Asia Energy Focus

Issue & Focus

On December 14 2009 China andTurkmenistan formally opened the gas

pipeline from Turkmenistan through CentralAsia to China. This pipeline, built withChinese capital, is the first gas pipelineconnecting China to Turkmenistan and toCentral Asia, but is unlikely to be the last suchpipeline. Therefore this pipeline has significantconsequences for both Central Asia and China,as well as Russia. But the likely repercussionsof this pipeline do not stop in Central Asia.Instead they also affect the future of energyflows in East Asia as both Central and EastAsia (as this pipeline shows) are becomingincreasingly more integrated in energy andother forms of social infrastructure, e.g.transportation.This pipeline is in fact two pipelines. The firstpipeline, opened on December 14, travels 1833km from Turkmenistan through Uzbekistanand southern Kazakhstan to Xinjiang in China.From there it will connect to China’s domestic