Embed Size (px)

Citation preview

Andrew Cote

PotashCorp.com

Sales Manager, South Region

World Fertilizer Outlook

Forward-Looking Statements

The following presentation contains forward-looking statements. These statements are based on certain factors

and assumptions including foreign exchange rates, expected growth, results of operations, performance,

business prospects and opportunities and effective income tax rates. While the company considers these

factors and assumptions to be reasonable based on information currently available, they may prove to be

incorrect. A number of factors could cause actual results to differ materially from those in the forward-looking

statements, including, but not limited to: fluctuations in supply and demand in fertilizer, sulfur, transportation

and petrochemical markets; changes in competitive pressures, including pricing pressures; timing and amount

of capital expenditures; risks associated with natural gas and other hedging activities; changes in capital

markets and corresponding effects on the company’s investments; changes in currency and exchange rates;

unexpected geological or environmental conditions, including water inflow; strikes and other forms of work

stoppage or slowdowns including the possibility of work stoppages at our Allan, Cory and Patience Lake

facilities; changes in and the effects of, government policy and regulations; and earnings, exchange rates and

the decisions of taxing authorities, all of which could affect our effective tax rates. Additional risks and

uncertainties can be found in our Form 10-K for the fiscal year ended December 31, 2007 under captions

“Forward-Looking Statements” and “Item 1A – Risk Factors” and in our filings with the US Securities and

Exchange Commission and Canadian provincial securities commissions. Forward-looking statements are given

only as at the date of this presentation and the company disclaims any obligation to update or revise the

forward-looking statements, whether as a result of new information, future events or otherwise, except as

required by law.

Fertilizer Demand Drivers

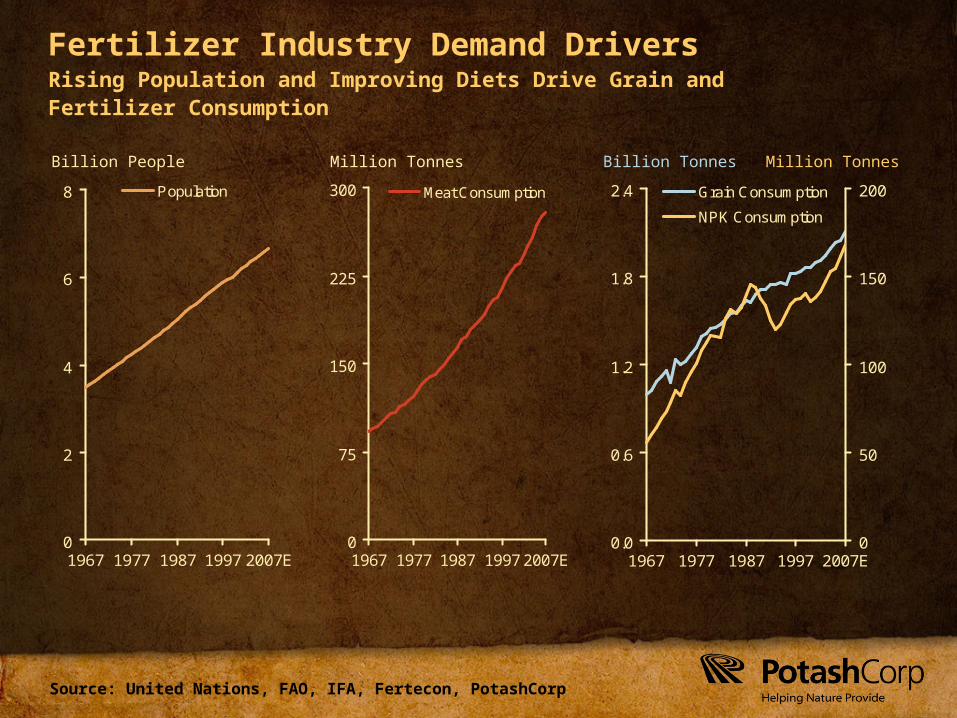

Source: United Nations, FAO, IFA, Fertecon, PotashCorp

Fertilizer Industry Demand Drivers

0

2

4

6

8

1967 1977 1987 1997 2007E

Population

Rising Population and Improving Diets Drive Grain and Fertilizer Consumption

Billion People Million Tonnes Billion Tonnes

0.0

0.6

1.2

1.8

2.4

1967 1977 1987 1997 2007E0

50

100

150

200Grain Consumption

NPK Consumption

Million Tonnes

0

75

150

225

300

1967 1977 1987 1997 2007E

Meat Consumption

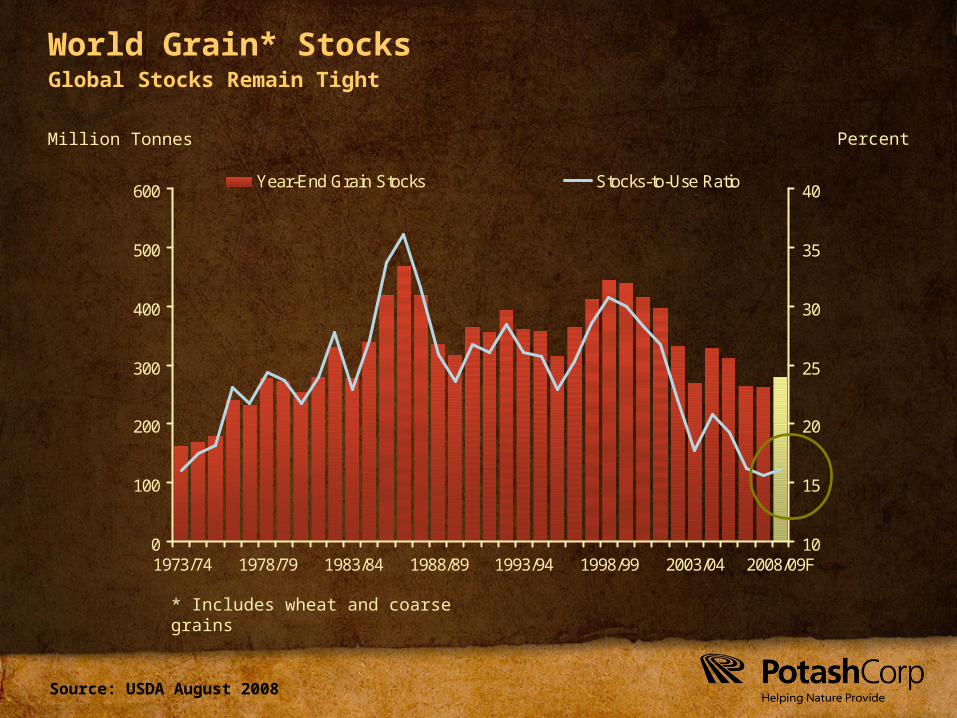

Source: USDA August 2008

World Grain* Stocks

Million Tonnes Percent

Global Stocks Remain Tight

0

100

200

300

400

500

600

1973/74 1978/79 1983/84 1988/89 1993/94 1998/99 2003/04 2008/09F10

15

20

25

30

35

40Year-End Grain Stocks Stocks-to-Use Ratio

* Includes wheat and coarse grains

Source: USDA

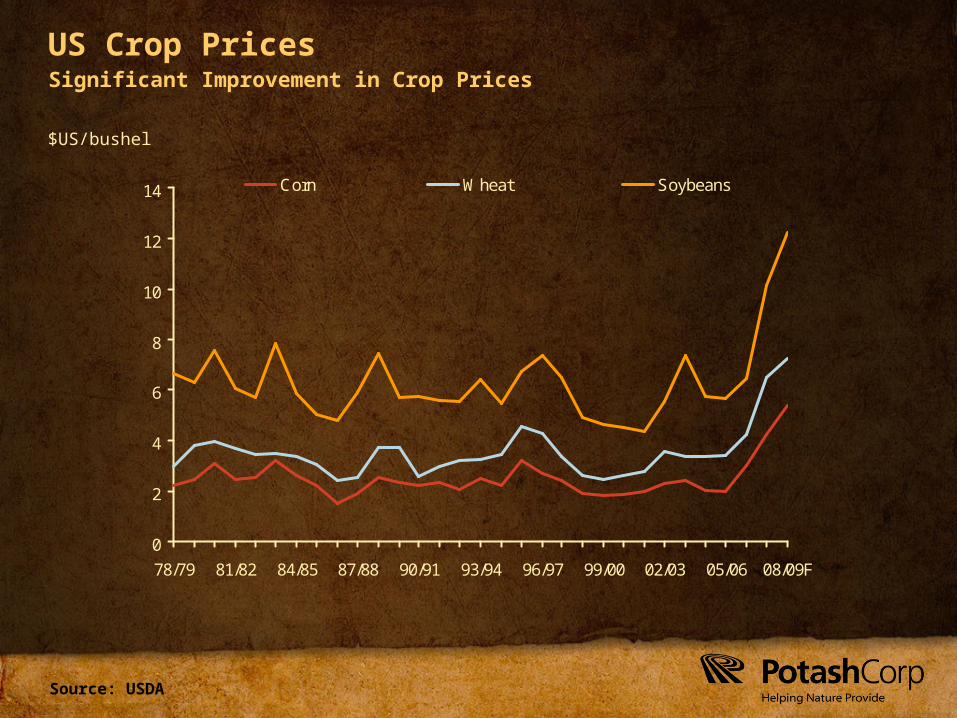

US Crop Prices

$US/bushel

Significant Improvement in Crop Prices

0

2

4

6

8

10

12

14

78/79 81/82 84/85 87/88 90/91 93/94 96/97 99/00 02/03 05/06 08/09F

Corn Wheat Soybeans

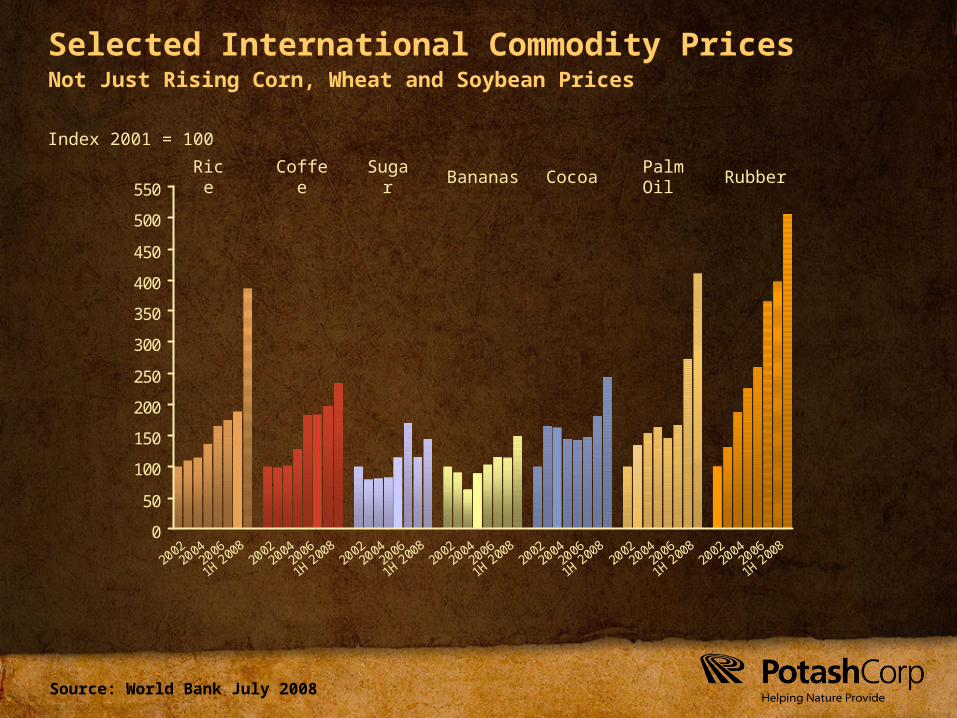

Source: World Bank July 2008

Selected International Commodity Prices

0

50

100

150

200

250

300

350

400

450

500

550

20022004

2006

1H 20082002

20042006

1H 20082002

20042006

1H 20082002

20042006

1H 20082002

20042006

1H 20082002

20042006

1H 20082002

20042006

1H 2008

Index 2001 = 100

Coffee Sugar BananasRice Cocoa RubberPalm Oil

Not Just Rising Corn, Wheat and Soybean Prices

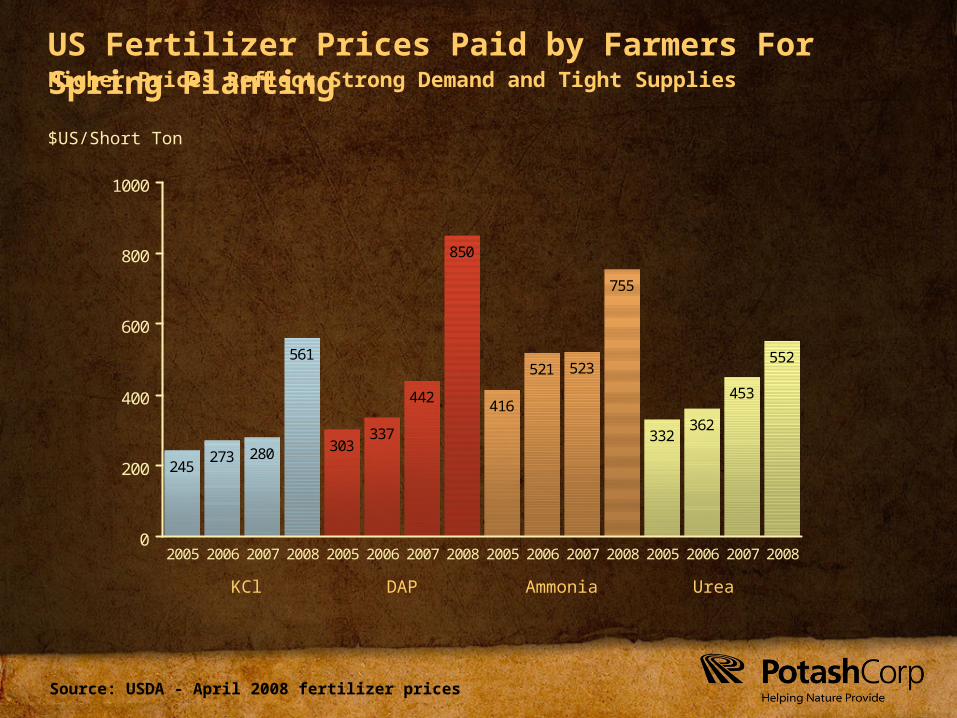

Source: USDA - April 2008 fertilizer prices

US Fertilizer Prices Paid by Farmers For Spring Planting

245273 280

561

303337

442

850

416

521 523

755

332362

453

552

0

200

400

600

800

1000

2005 2006 2007 2008 2005 2006 2007 2008 2005 2006 2007 2008 2005 2006 2007 2008

$US/Short Ton

KCl UreaDAP Ammonia

Higher Prices Reflect Strong Demand and Tight Supplies

Source: USDA, PotashCorp

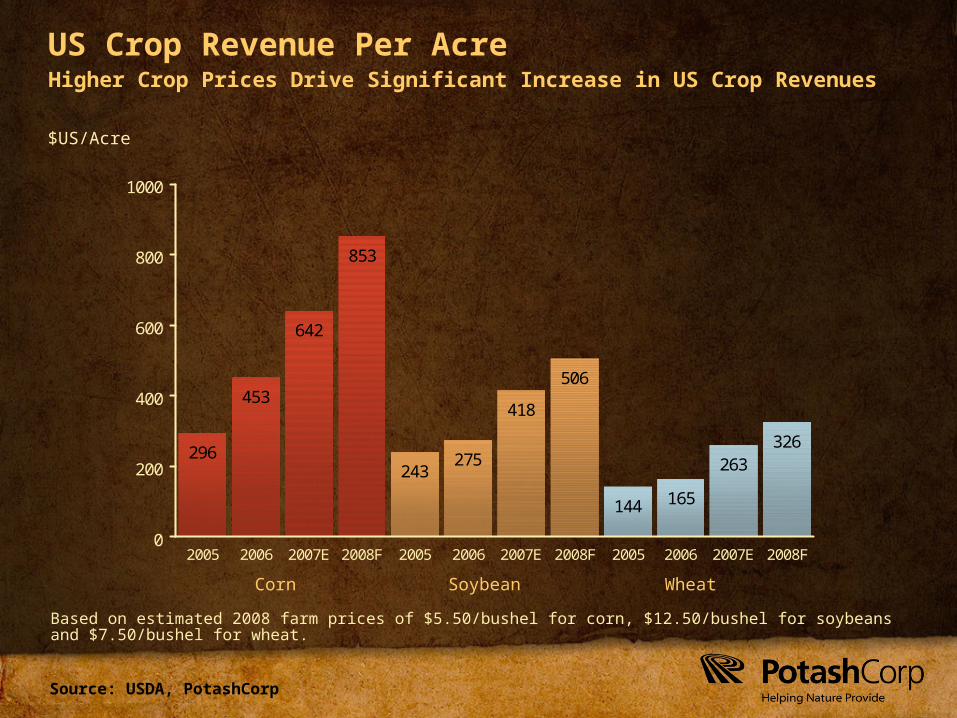

US Crop Revenue Per Acre

296

453

642

853

243275

418

506

144 165

263326

0

200

400

600

800

1000

2005 2006 2007E 2008F 2005 2006 2007E 2008F 2005 2006 2007E 2008F

$US/Acre

Higher Crop Prices Drive Significant Increase in US Crop Revenues

Based on estimated 2008 farm prices of $5.50/bushel for corn, $12.50/bushel for soybeans and $7.50/bushel for wheat.

Corn WheatSoybean

Source: USDA, PotashCorp

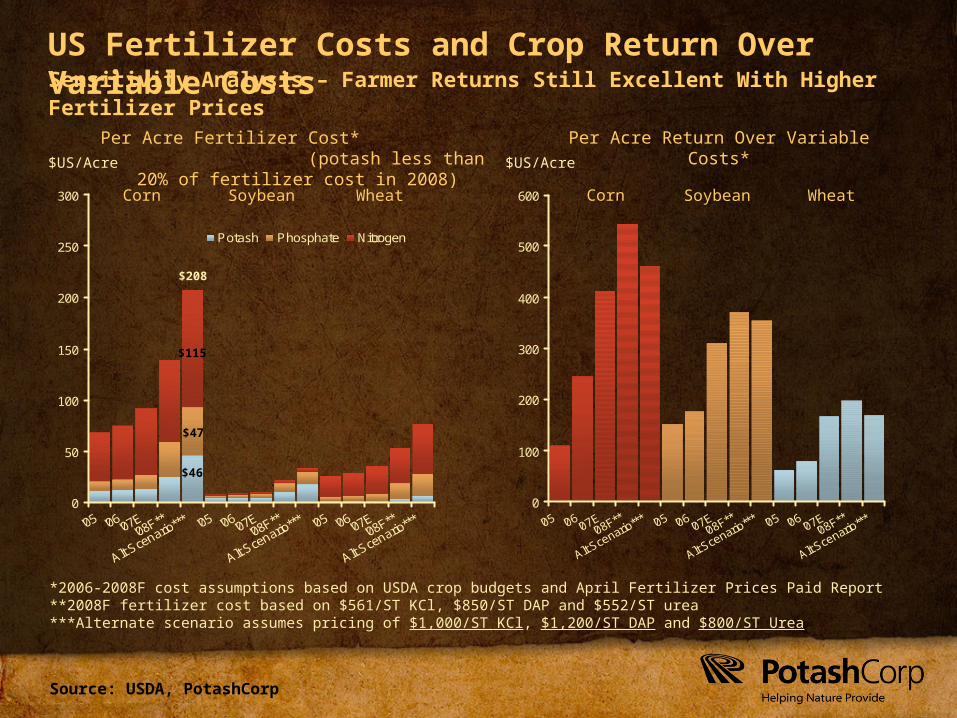

US Fertilizer Costs and Crop Return Over Variable Costs

0

50

100

150

200

250

300

Potash Phosphate Nitrogen

Sensitivity Analysis – Farmer Returns Still Excellent With Higher Fertilizer Prices

0

100

200

300

400

500

600

*2006-2008F cost assumptions based on USDA crop budgets and April Fertilizer Prices Paid Report**2008F fertilizer cost based on $561/ST KCl, $850/ST DAP and $552/ST urea***Alternate scenario assumes pricing of $1,000/ST KCl, $1,200/ST DAP and $800/ST Urea

Per Acre Fertilizer Cost* (potash less than 20% of fertilizer cost in 2008)

Per Acre Return Over Variable Costs*

Soybean WheatCorn

$115

$47

$46

$208

$US/Acre $US/Acre

Soybean WheatCorn

Source: USDA, Doane

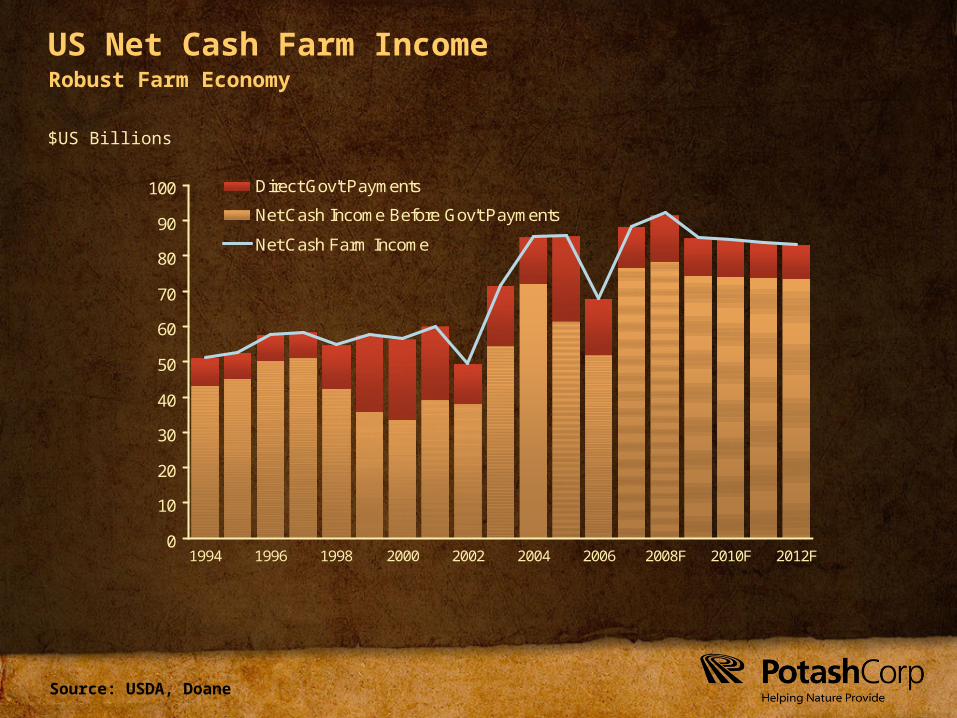

0

10

20

30

40

50

60

70

80

90

100

1994 1996 1998 2000 2002 2004 2006 2008F 2010F 2012F

Direct Gov't Payments

Net Cash Income Before Gov't Payments

Net Cash Farm Income

US Net Cash Farm Income

$US Billions

Robust Farm Economy

Source: Fertecon, PotashCorp

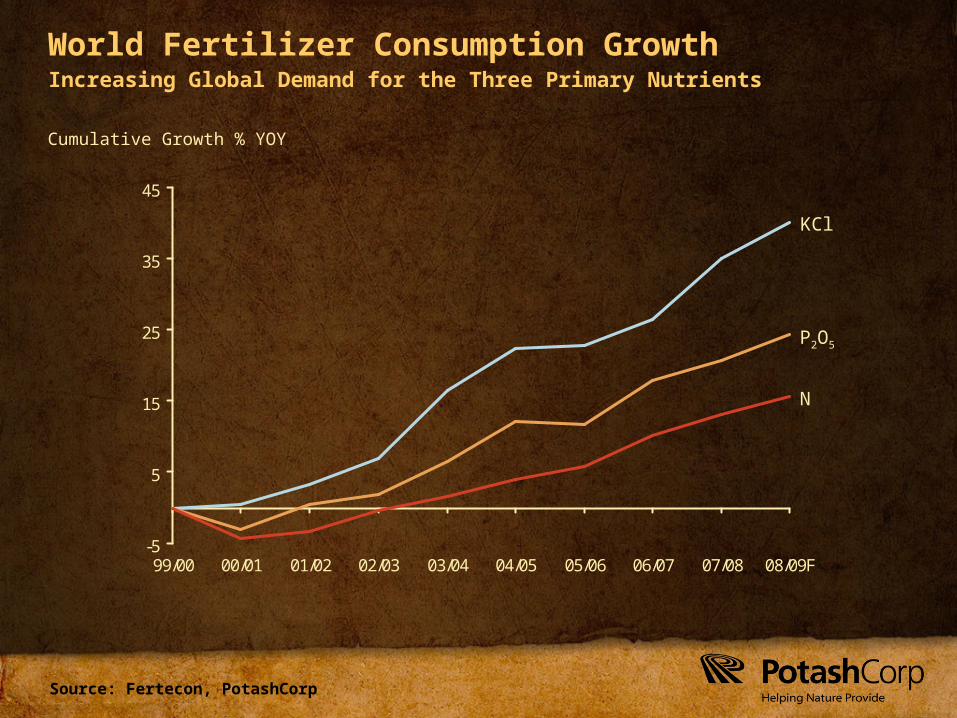

-5

5

15

25

35

45

99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09F

World Fertilizer Consumption Growth

Cumulative Growth % YOY

Increasing Global Demand for the Three Primary Nutrients

KCl

P2O5

N

Source: IFA

World and US Fertilizer Consumption by Crop

17%

15%

15%

5%4%7%

4%

4%

15%

14%Wheat

Rice

Corn

OtherCereals

Cotton

Fruits &Vegetables

Soybeans

All Other Crops All Other CropsWheat

CornSoybeans

Cotton

World US

Other Oilseeds

Sugar

13%

1%

45%3%

4%2%

5%1%

5%

21% Rice

OtherCereals

Other Oilseeds

Sugar

Fruits &Vegetables

Fertilizer Used on a Diverse Set of Crops

Source: IPNI, Fertecon, PotashCorp

Improved Fertilization Can Raise Yields

0

10

20

30

40

50

60

70

80

Current Potential

IndiaChina

Million Tonnes

0

10

20

30

40

50

Current Potential0

5

10

15

20

25

Current Potential

Brazil

N P2O5 KCl

Potential Levels Exceed Current Application Levels

Phosphate Overview

Source: Fertecon, PotashCorp

0

5

10

15

20

25

30

35

2008F 2009F 2010F 2011F 2012F

Capacity Demand

Million Tonnes Rock, Cumulative Growth

New Phosphate Rock Capacity vs Demand Supply/Demand Balance to Remain Tight

Source: Fertecon, PotashCorp

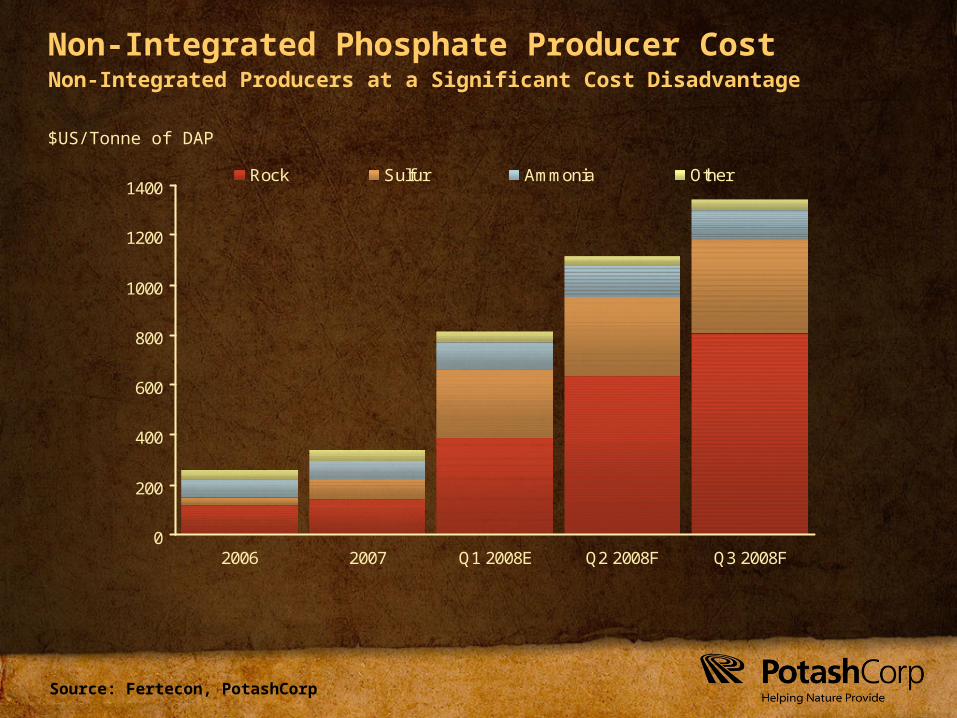

Non-Integrated Phosphate Producer Cost

$US/Tonne of DAP

0

200

400

600

800

1000

1200

1400

2006 2007 Q1 2008E Q2 2008F Q3 2008F

Rock Sulfur Ammonia Other

Non-Integrated Producers at a Significant Cost Disadvantage

Source: British Sulphur, Fertecon, PotashCorp

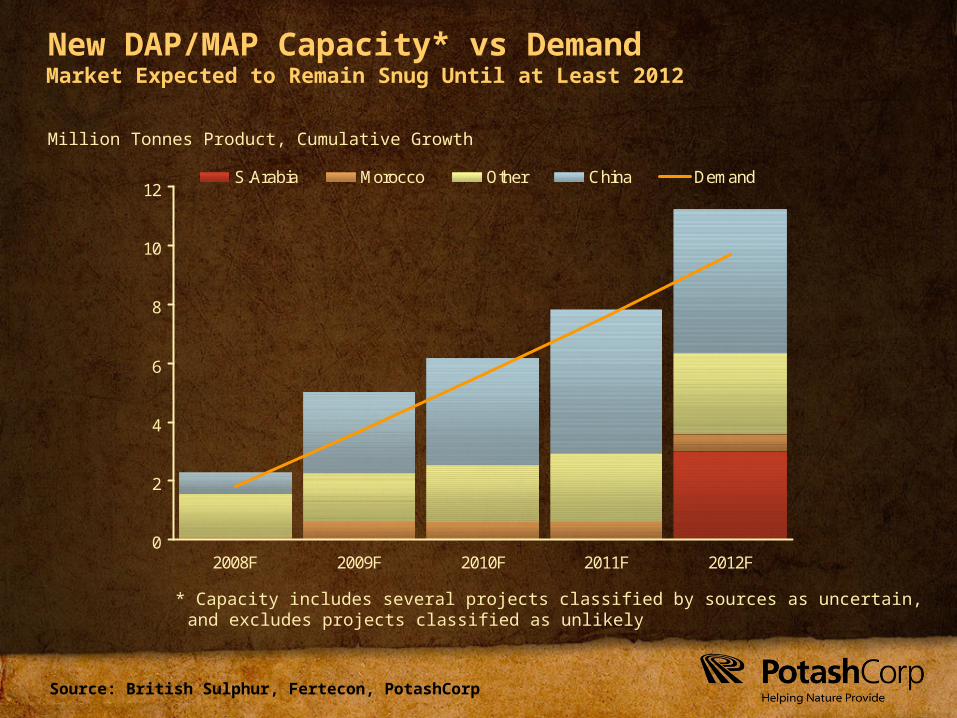

New DAP/MAP Capacity* vs Demand

0

2

4

6

8

10

12

2008F 2009F 2010F 2011F 2012F

S.Arabia Morocco Other China Demand

Million Tonnes Product, Cumulative Growth

* Capacity includes several projects classified by sources as uncertain,and excludes projects classified as unlikely

Market Expected to Remain Snug Until at Least 2012

Source: Fertecon, PotashCorp

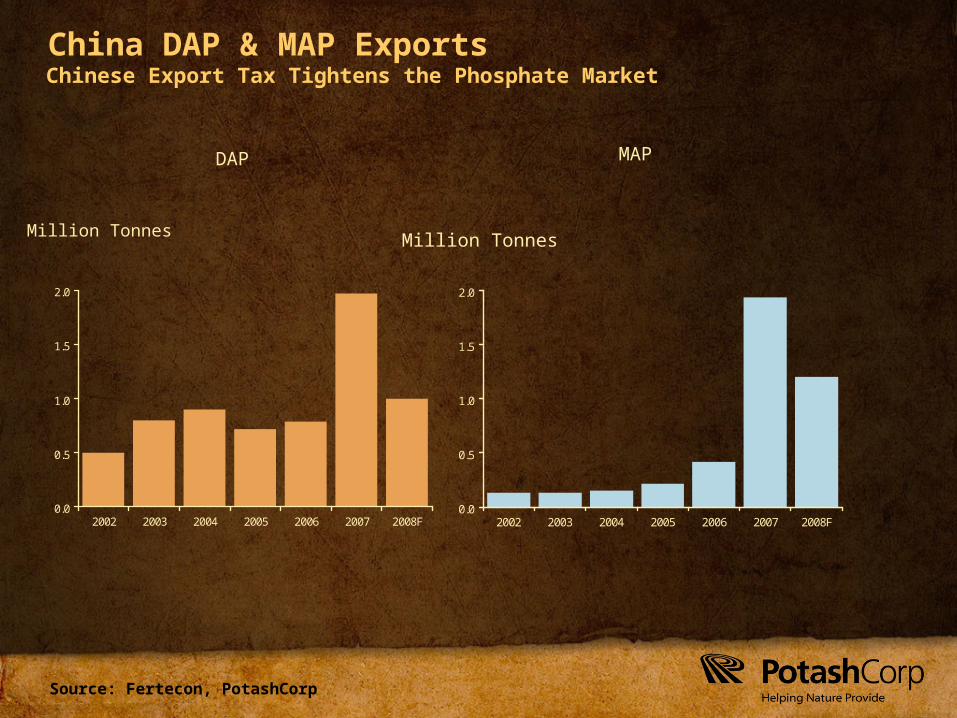

China DAP & MAP Exports

0.0

0.5

1.0

1.5

2.0

2002 2003 2004 2005 2006 2007 2008F

Million Tonnes

0.0

0.5

1.0

1.5

2.0

2002 2003 2004 2005 2006 2007 2008F

Million Tonnes

DAP MAP

Chinese Export Tax Tightens the Phosphate Market

Source: Fertecon, PotashCorp

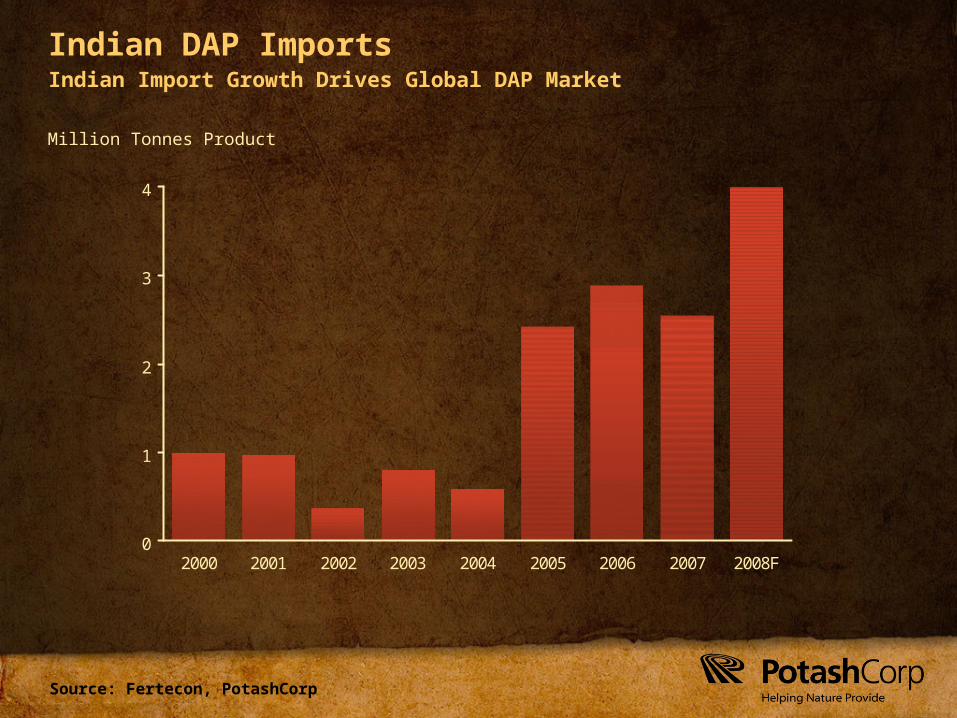

Indian DAP Imports

0

1

2

3

4

2000 2001 2002 2003 2004 2005 2006 2007 2008F

Million Tonnes Product

Indian Import Growth Drives Global DAP Market

Nitrogen Overview

Source: Fertecon, PotashCorp

0

2

4

6

8

10

12

14

2000 2001 2002 2003 2004 2005 2006 2007 2008F

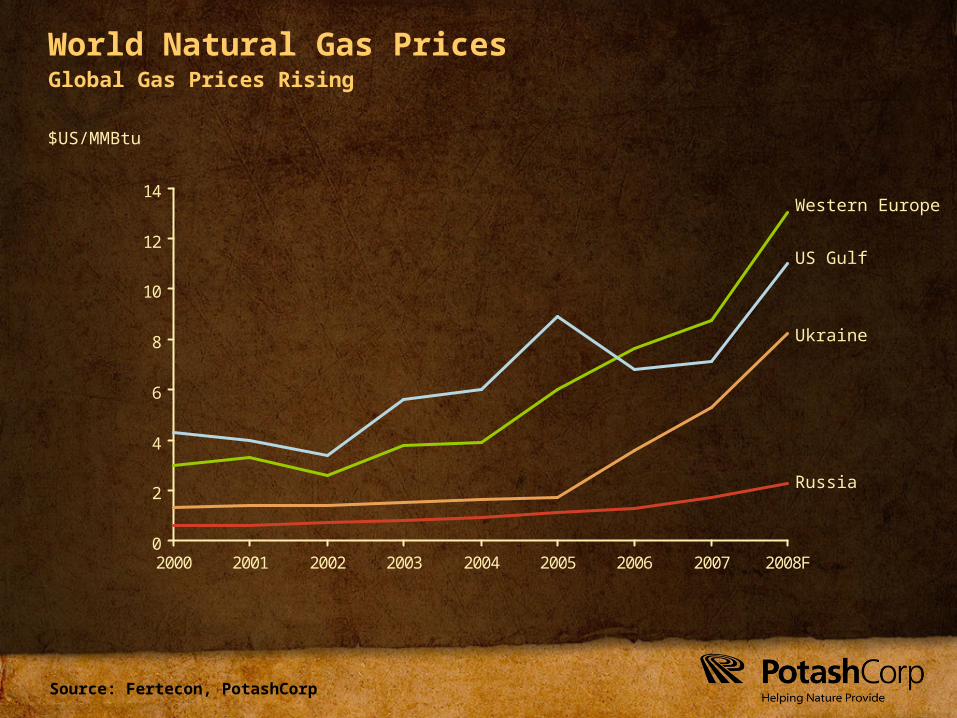

World Natural Gas Prices

$US/MMBtu

Global Gas Prices Rising

Western Europe

US Gulf

Ukraine

Russia

Source: Fertecon, PotashCorp

0

100

200

300

400

500

600

20062007

1H 2008E

2H 2008F2006

2007

1H 2008E

2H 2008F2006

2007

1H 2008E

2H 2008F

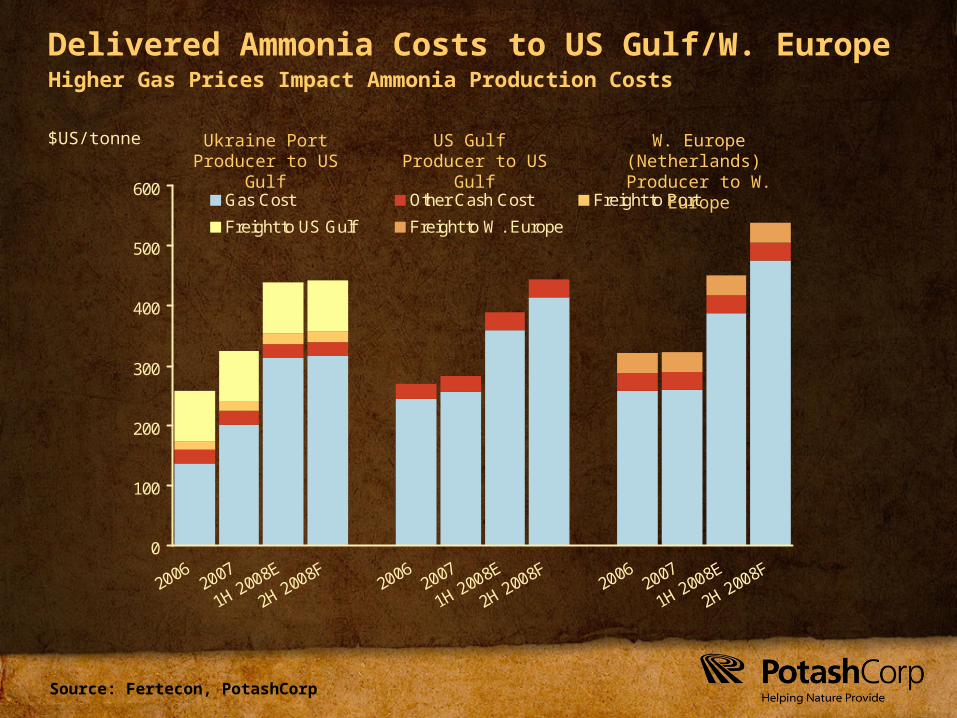

Gas Cost Other Cash Cost Freight to Port

Freight to US Gulf Freight to W. Europe

Delivered Ammonia Costs to US Gulf/W. Europe

$US/tonne Ukraine Port Producer to US Gulf

US Gulf Producer to US Gulf

W. Europe (Netherlands) Producer to W. Europe

Higher Gas Prices Impact Ammonia Production Costs

Source: Fertecon, British Sulphur, Potash Corp

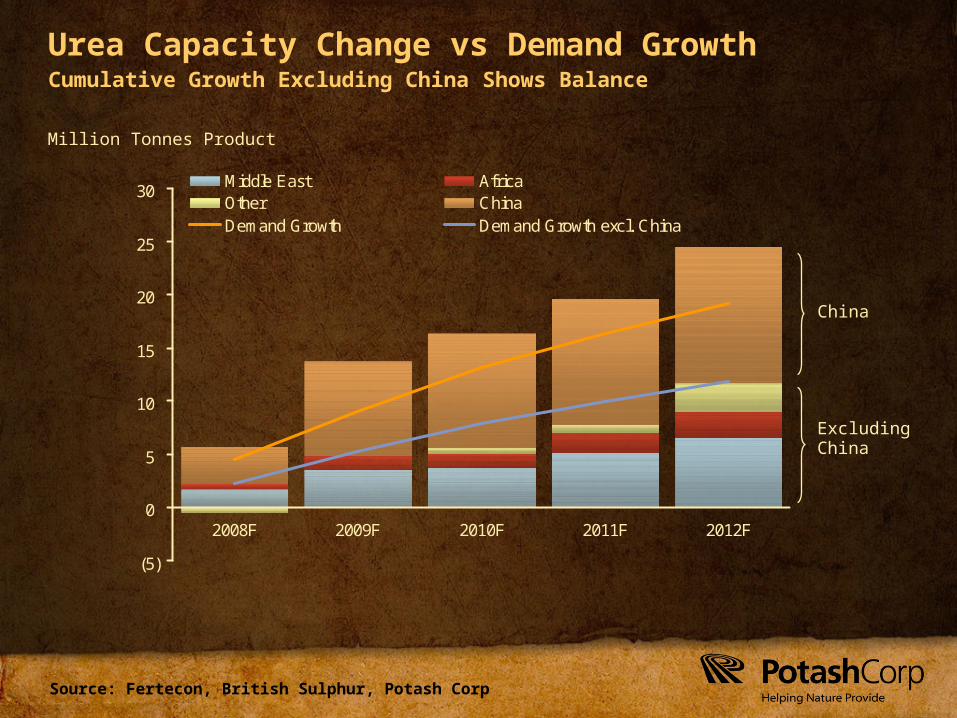

Million Tonnes Product

Urea Capacity Change vs Demand Growth

(5)

0

5

10

15

20

25

30

2008F 2009F 2010F 2011F 2012F

Middle East AfricaOther ChinaDemand Growth Demand Growth excl. China

Cumulative Growth Excluding China Shows Balance

Excluding China

China

Source: Fertecon

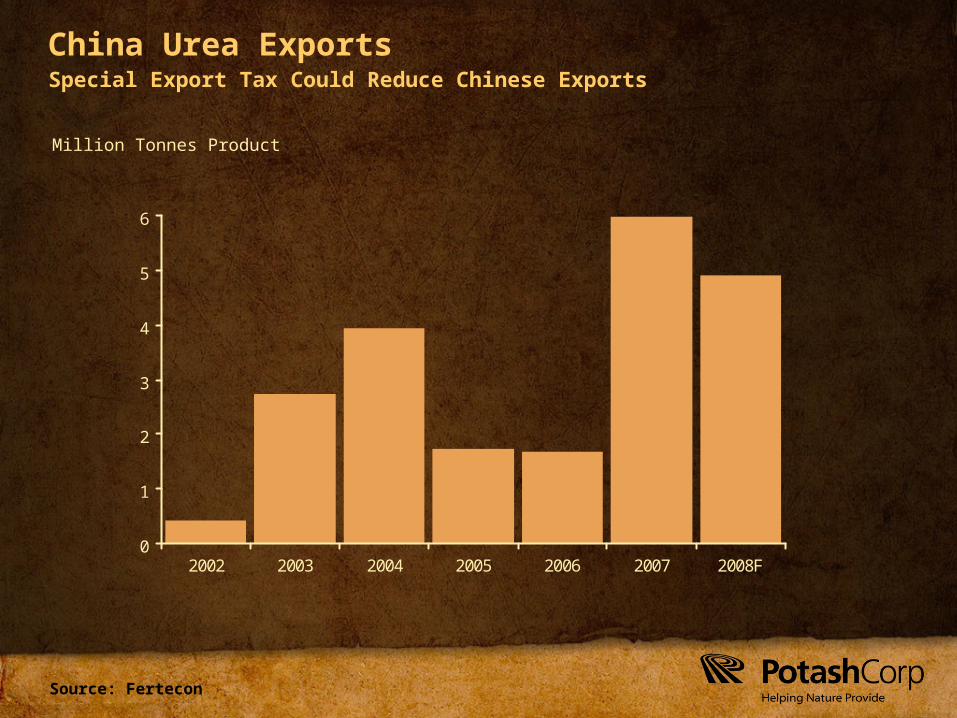

China Urea Exports

0

1

2

3

4

5

6

2002 2003 2004 2005 2006 2007 2008F

Million Tonnes Product

Special Export Tax Could Reduce Chinese Exports

Source: Fertecon, British Sulphur, PotashCorp

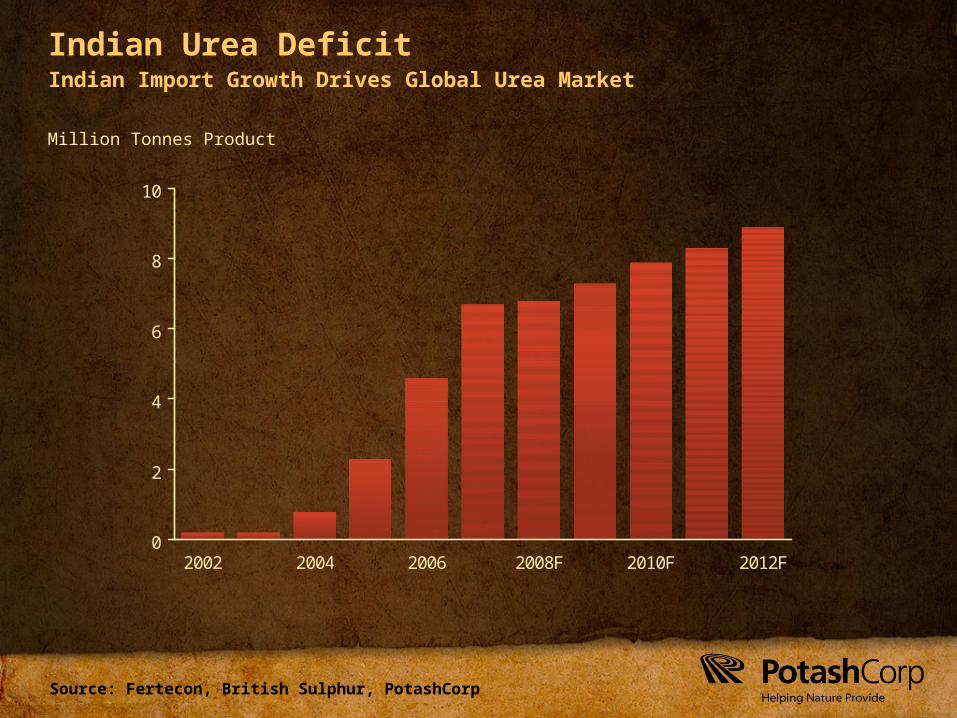

Indian Urea Deficit

0

2

4

6

8

10

2002 2004 2006 2008F 2010F 2012F

Million Tonnes Product

Indian Import Growth Drives Global Urea Market

Potash Overview

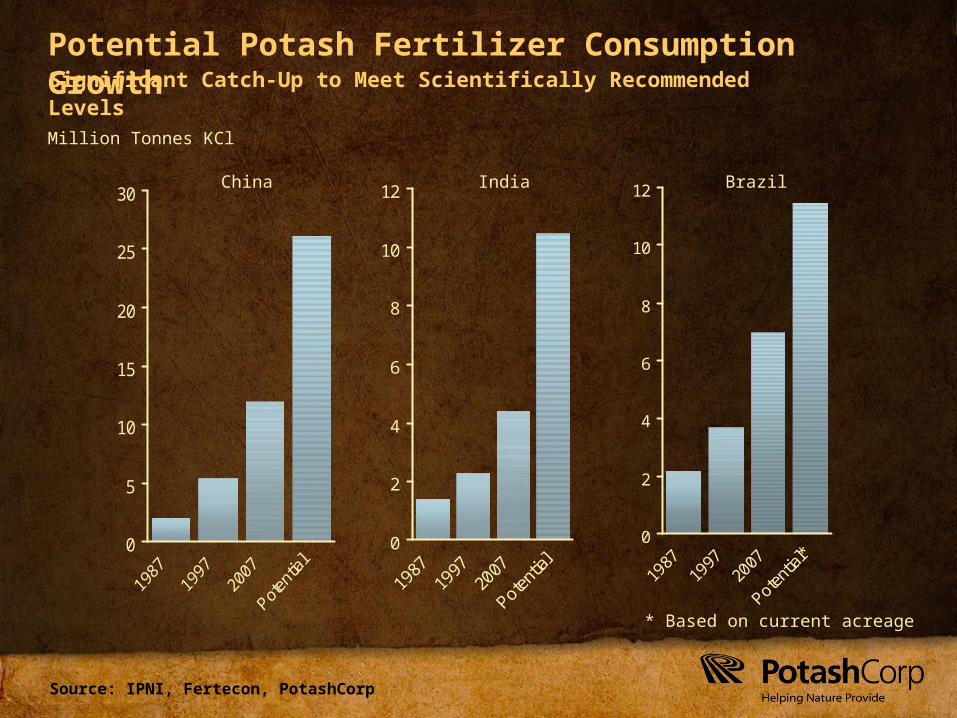

Source: IPNI, Fertecon, PotashCorp

0

5

10

15

20

25

30

0

2

4

6

8

10

12

1987

1997

2007

Potent

ial0

2

4

6

8

10

12

1987

1997

2007

Potent

ial*

Potential Potash Fertilizer Consumption Growth

China India Brazil

Million Tonnes KCl

Significant Catch-Up to Meet Scientifically Recommended Levels

* Based on current acreage

Source: Fertecon

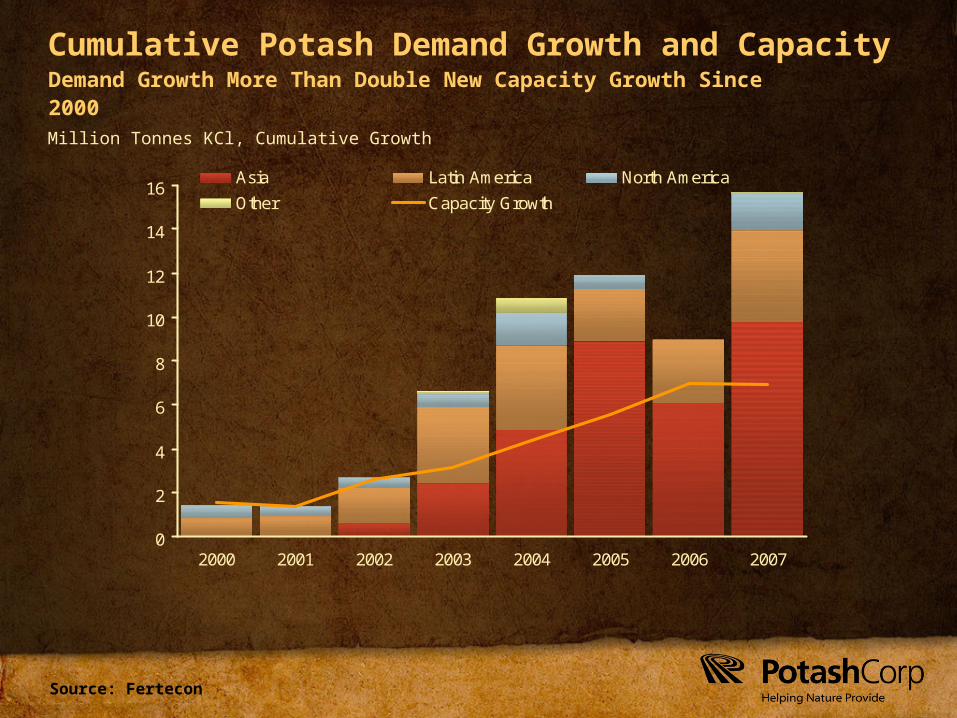

Cumulative Potash Demand Growth and Capacity

Million Tonnes KCl, Cumulative Growth

0

2

4

6

8

10

12

14

16

2000 2001 2002 2003 2004 2005 2006 2007

Asia Latin America North America

Other Capacity Growth

Demand Growth More Than Double New Capacity Growth Since 2000

Source: Fertecon, PotashCorp

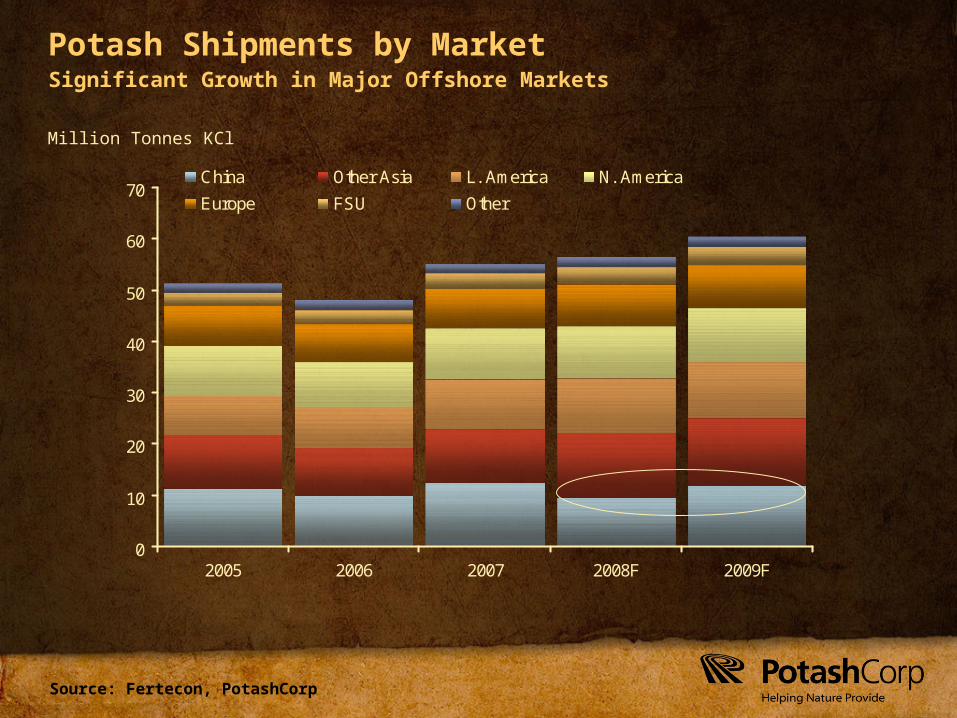

Potash Shipments by Market

Million Tonnes KCl

0

10

20

30

40

50

60

70

2005 2006 2007 2008F 2009F

China Other Asia L. America N. America

Europe FSU Other

Significant Growth in Major Offshore Markets

Source: IPNI

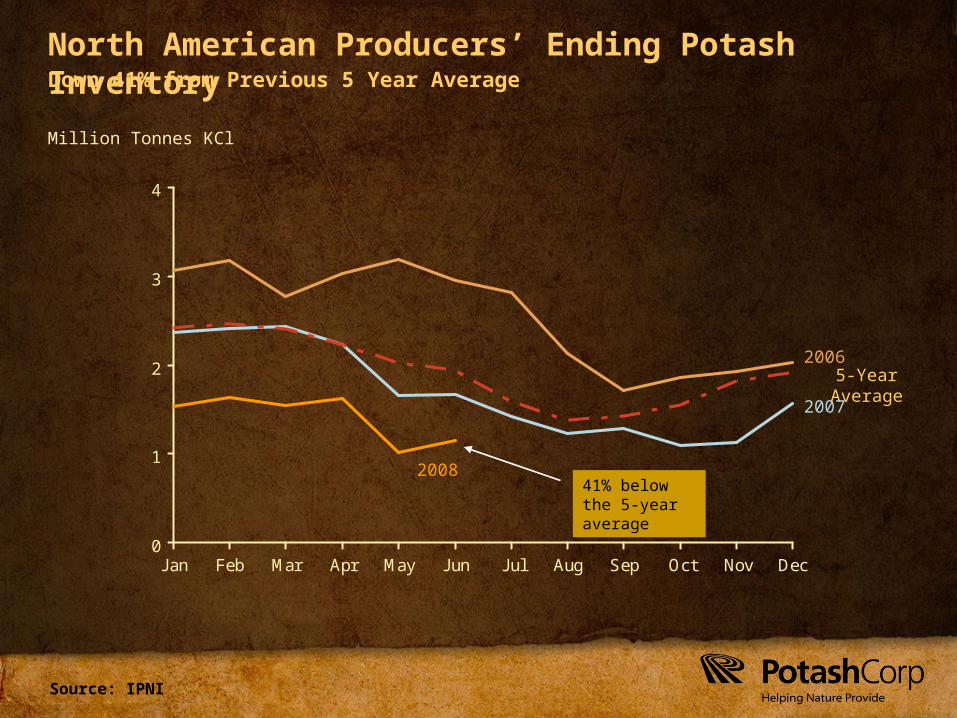

North American Producers’ Ending Potash Inventory

0

1

2

3

4

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Million Tonnes KCl

5-Year Average

41% below the 5-year average

2006

2007

2008

Down 41% from Previous 5 Year Average

Source: PotashCorp

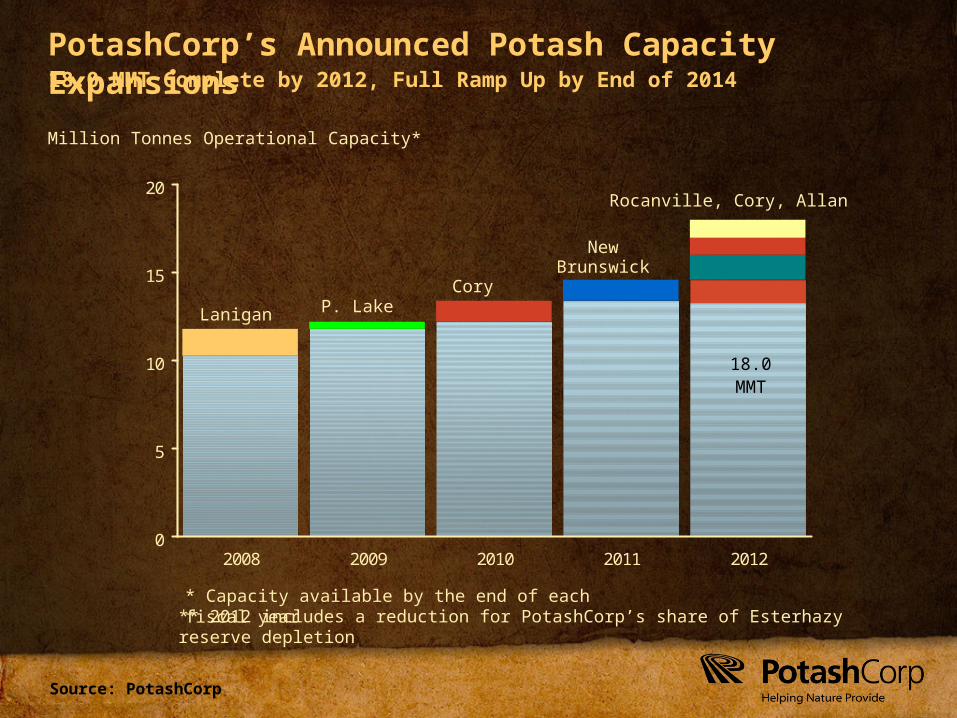

PotashCorp’s Announced Potash Capacity Expansions

0

5

10

15

20

2008 2009 2010 2011 2012

Million Tonnes Operational Capacity*

18.0 MMT Complete by 2012, Full Ramp Up by End of 2014

Lanigan

Cory

Rocanville, Cory, Allan

NewBrunswick

* Capacity available by the end of each fiscal year** 2012 includes a reduction for PotashCorp’s share of Esterhazy reserve depletion

18.0MMT

P. Lake

Thank You

PotashCorp.com