Embed Size (px)

Citation preview

An interaction on

Types of Contracts and the Distinctitive

Approaches and Methodologies in Audit

according to the type of Contracts,

interpretation of Contract Clauses

sharing the experiences

Procurement

What do we buy or sell ?

Some Basics

What we buy or sell? (Goods, Services , etc to meet our needs)

Satisfaction ! (In terms of quality, quantity, rates and convenience)

What is required exactly should be clear to both buyer and

seller? (Often vague in new type of procurements ? Will get better response (go to

him he knows the job?)

Expectations of both the sides should be crystal clear :

DMS (Computerisation case- SRS), IGNOU (ERP), DDA (Bakkarwala)

(Requirements formulation)

Clarity will help better competition , bid evaluation process

and contract execution.

(To understand above clearly by both the sides :Pre bid conference)

Basics

How balancing of Interests/Expectations : by following

rules & procedures (Bidding/tendering Process).

The two sides have conflicting interests/expectations but a

Win- Win situation when satisfaction is there on both the

sides. (In terms of quality, quantity, rates and convenience- creates issues later if any of

these is vague).

CONTRACT : DEFINITION A contract is defined as

• An agreement between two or more parties, with some

• legal binding enforceable in the court of law.

• A contract is a promise or a set of promises :

• for the breach of which, the law gives a remedy or

• the performance of which, the law in some way

recognizes as a duty.

• There are many stages involved in the formation and

acceptance of a legal contract. The basic stages of any

contract includes :

proposal,

offer,

acceptance,

agreement and

consideration.

Types of Contracts

• There may be contracts for procurement of :

• Works,

• Goods,

• Services or

• Consultants/manpower

• PPP, etc

Some of the common types of contracts used in the

engineering and construction Projects are :

• Lump Sum Contract

• Cost Plus Contract

• Unit Price Contract

• Percentage (of Project cost ) or Fee

• Incentive Contracts

Lump Sum Contracts • Percentage (of Project cost ) or Fee

• Incentive Contracts

The contractor agrees to do a described and specified project

for a fixed price.

Often used in engineering contracts.

Also named "Fixed Fee Contract".

It is suitable, if the scope and schedule of the project are so

clear and sufficiently defined as to allow the consulting engineer

to estimate the project costs.

Cost Plus Contract• A contract agreement wherein the purchaser agrees

to pay the cost of all labour and materials plus an

amount for contractor overhead and profit (usually as

a percentage of the labour and material cost).

• The contracts may be specified as :

Cost + Fixed Percentage Contract

Cost + Fixed Fee Contract

Cost + Fixed Fee with Guaranteed Maximum Price

Contract

Cost + Fixed Fee with Bonus Contract

Cost + Fixed Fee with Guaranteed Maximum Price

and Bonus contract

Cost + Fixed Fee with Agreement for Sharing Any

Cost Savings contract

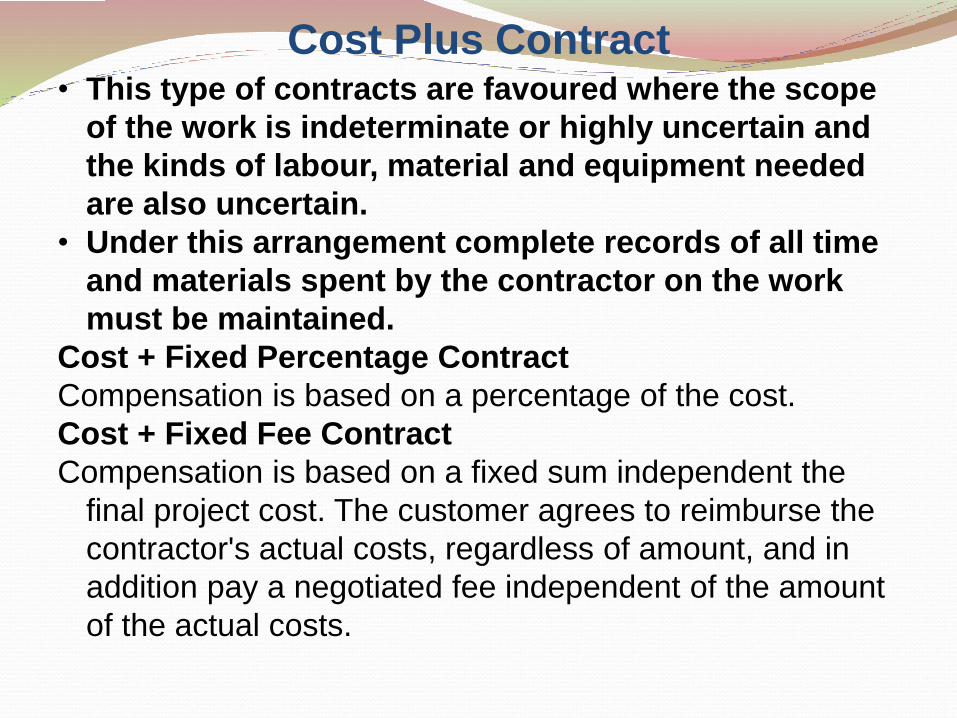

Cost Plus Contract• This type of contracts are favoured where the scope

of the work is indeterminate or highly uncertain and

the kinds of labour, material and equipment needed

are also uncertain.

• Under this arrangement complete records of all time

and materials spent by the contractor on the work

must be maintained.

Cost + Fixed Percentage Contract

Compensation is based on a percentage of the cost.

Cost + Fixed Fee Contract

Compensation is based on a fixed sum independent the

final project cost. The customer agrees to reimburse the

contractor's actual costs, regardless of amount, and in

addition pay a negotiated fee independent of the amount

of the actual costs.

Cost + Fixed Fee with Guaranteed Maximum Price Contract

Compensation is based on a fixed sum of money. The total project cost

will not exceed an agreed upper limit.

Cost + Fixed Fee with Bonus Contract

Compensation is based on a fixed sum of money. A bonus is given if the

project finish below budget, ahead of schedule, etc.

Cost + Fixed Fee with Guaranteed Maximum Price and Bonus

Contract

Compensation is based on a fixed sum of money. The total project cost

will not exceed an agreed upper limit and a bonus is given if the project is

finished below budget, ahead of schedule etc.

Cost + Fixed Fee with Agreement for Sharing Any Cost Savings

Contract

Compensation is based on a fixed sum of money. Any cost savings are

shared with the buyer and the contractor.

Unit Price Contract

This kind of contract is based on estimated quantities of items

included in the project and their unit prices. The final price of the

project is dependent on the quantities needed to carry out the

work.

In general this contract is only suitable for construction and

supplier projects where the different types of items, but not their

numbers, can be accurately identified in the contract documents.

It is not unusual to combine a Unit Price Contract for parts of the

project with a Lump Sum Contract or other types of contracts.

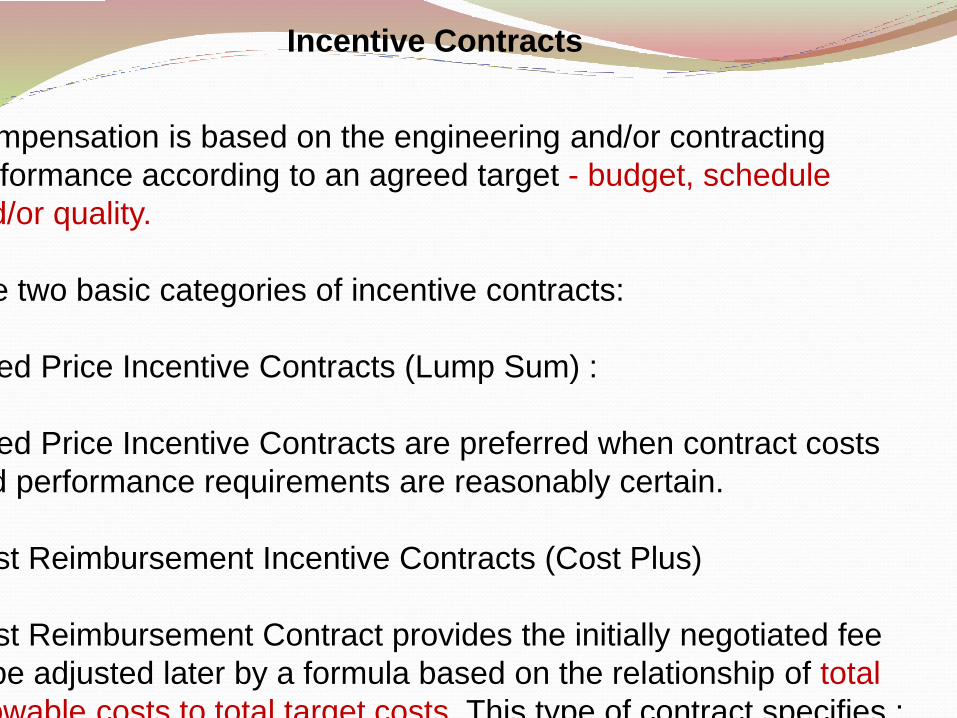

Incentive Contracts

Compensation is based on the engineering and/or contracting

performance according to an agreed target - budget, schedule

and/or quality.

The two basic categories of incentive contracts:

Fixed Price Incentive Contracts (Lump Sum) :

Fixed Price Incentive Contracts are preferred when contract costs

and performance requirements are reasonably certain.

Cost Reimbursement Incentive Contracts (Cost Plus)

Cost Reimbursement Contract provides the initially negotiated fee

to be adjusted later by a formula based on the relationship of total

allowable costs to total target costs. This type of contract specifies :

Percentage of Construction Fee Contracts

Common for engineering contracts. Compensation is

based on a percentage of the construction costs :

Planning & Architectural Works

DPRs preparations

Consultations

Designing & Drawing

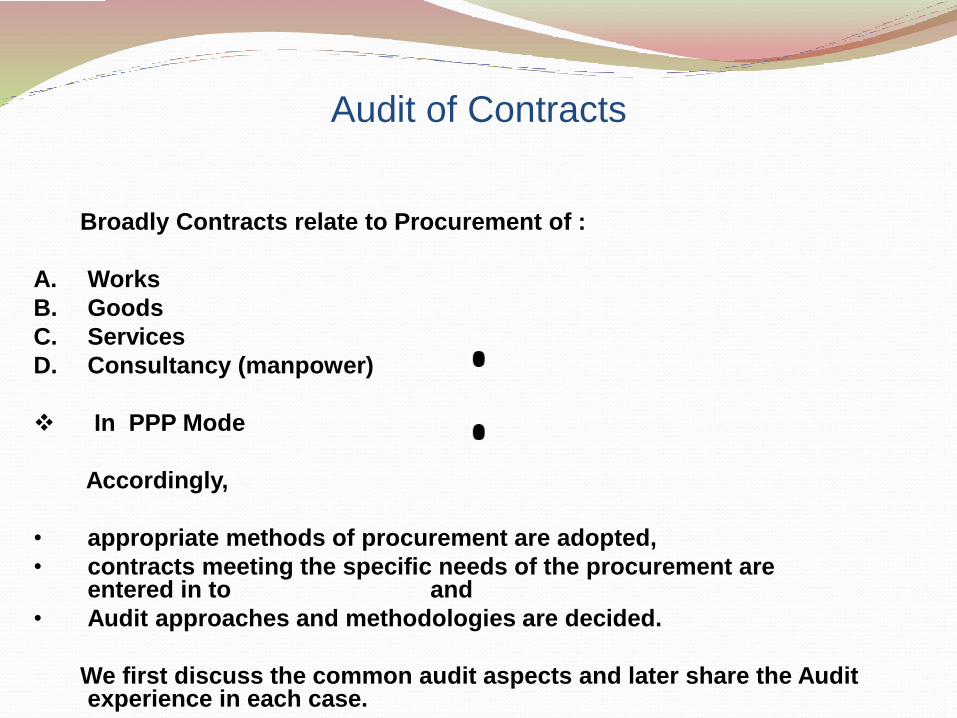

Audit of Contracts

Broadly Contracts relate to Procurement of :

A. Works

B. Goods

C. Services

D. Consultancy (manpower)

In PPP Mode

Accordingly,

• appropriate methods of procurement are adopted,

• contracts meeting the specific needs of the procurement are entered in to and

• Audit approaches and methodologies are decided.

We first discuss the common audit aspects and later share the Audit experience in each case.

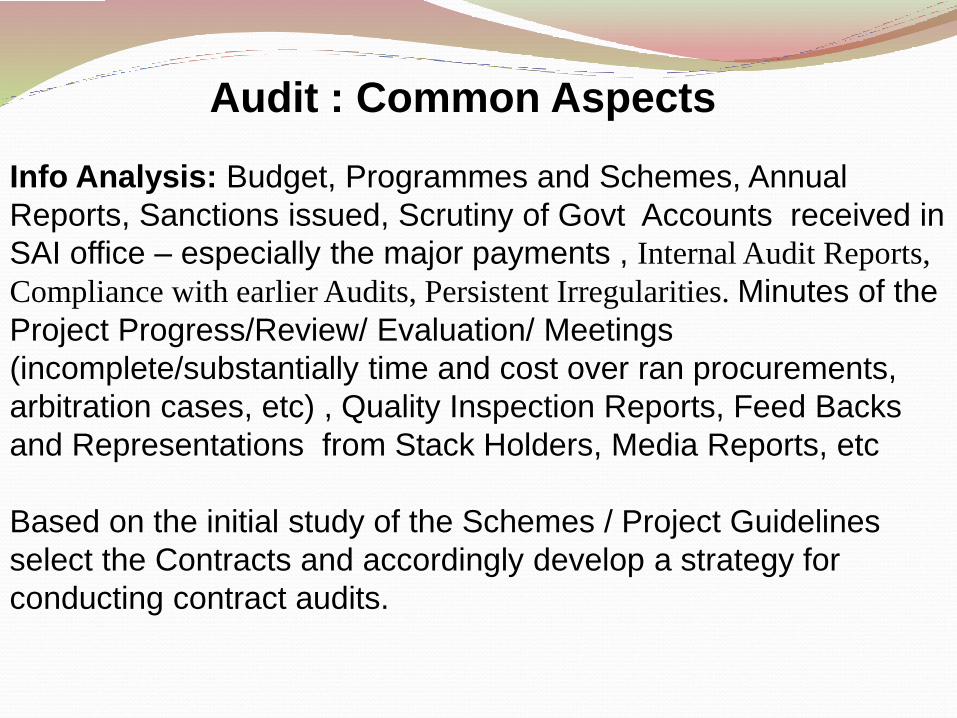

Audit : Common Aspects

Info Analysis: Budget, Programmes and Schemes, Annual

Reports, Sanctions issued, Scrutiny of Govt Accounts received in

SAI office – especially the major payments , Internal Audit Reports,

Compliance with earlier Audits, Persistent Irregularities. Minutes of the

Project Progress/Review/ Evaluation/ Meetings

(incomplete/substantially time and cost over ran procurements,

arbitration cases, etc) , Quality Inspection Reports, Feed Backs

and Representations from Stack Holders, Media Reports, etc

Based on the initial study of the Schemes / Project Guidelines

select the Contracts and accordingly develop a strategy for

conducting contract audits.

Audit : Common Aspects

•Perform risk analysis of contracts to determine which ones

to audit. Contract risks include: Time and cost overruns; frauds; duplicate billing or billing of unrelated costs; compliance with government regulatory agencies; Abondoned/Incomplete procurementsSubstandard quality/benefit projectionsUnder arbitration,etc

Audit : Common Aspects Because of limited resources, it may be impractical or

impossible to audit all contracts. Resources may need to

be concentrated on new contractors and contracts over a

certain amount. Other factors to consider may be the

complexity of the contract, type of project, importance or

sensitivity of the project and regulatory issues.

Decide who will conduct the audits: Assign specific

contracts to specific auditors or audit groups.

Audit : Common Aspects Obtain information to plan specific audits. Auditors

should obtain contract files, budgets, project and/or

engineering plans, accounting records and any other

documents they need to plan the specific audits. These

documents are usually obtained from the organization

commissioning the audit. They should review these

documents and update themselves on the contract and to

develop the audit procedures.

Auditors will need to obtain documentation of direct costs

and indirect costs charged to the contract and records

documenting compliance with contract provisions,

regulatory matters and contract deliverables.

Audit : Common Aspects Auditors will execute the audit procedures.

They will verify billings from the contractor by examining the contract costs

incurred by the contractor.

Auditors will select samples of direct and indirect costs and test those costs

to determine if they are allowable to the contract in accordance with applicable criteria.

Audit of works Contracts

The aim of audit is to see that all works were executed within

the minimum possible cost and in accordance with the

procedure laid down for the purpose.

There are four main Stages connected with a project

clearance – which contain the contract management

problems which surface later:

1. Administrative Approval

2. Financial Sanction

3. Technical Sanction and

4. Appropriation or Re-appropriation of funds

The aim of audit is to see that all works were executed

within the minimum possible cost and in accordance

with the procedure laid down for the purpose.

There are four main Stages connected with a

project clearance – which contain the

contract management problems which

surface later:1. Administrative Approval

2. Financial Sanction

3. Technical Sanction and

4. Appropriation or Re-appropriation of funds

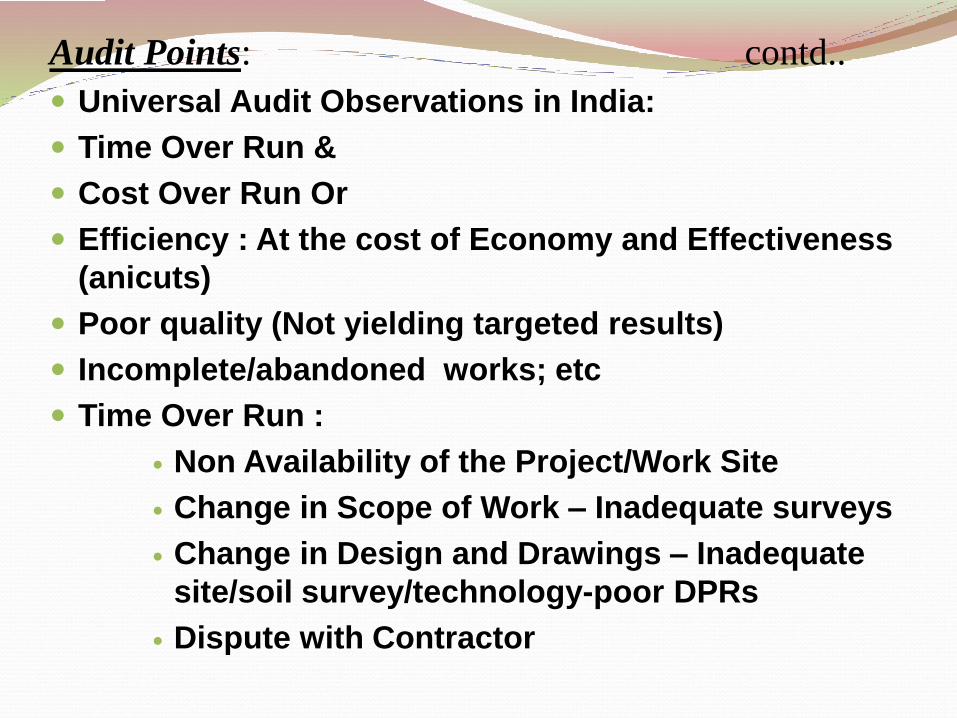

Audit Points: contd..

Universal Audit Observations in India:

Time Over Run &

Cost Over Run Or

Efficiency : At the cost of Economy and Effectiveness

(anicuts)

Poor quality (Not yielding targeted results)

Incomplete/abandoned works; etc

Time Over Run :

Non Availability of the Project/Work Site

Change in Scope of Work – Inadequate surveys

Change in Design and Drawings – Inadequate

site/soil survey/technology-poor DPRs

Dispute with Contractor

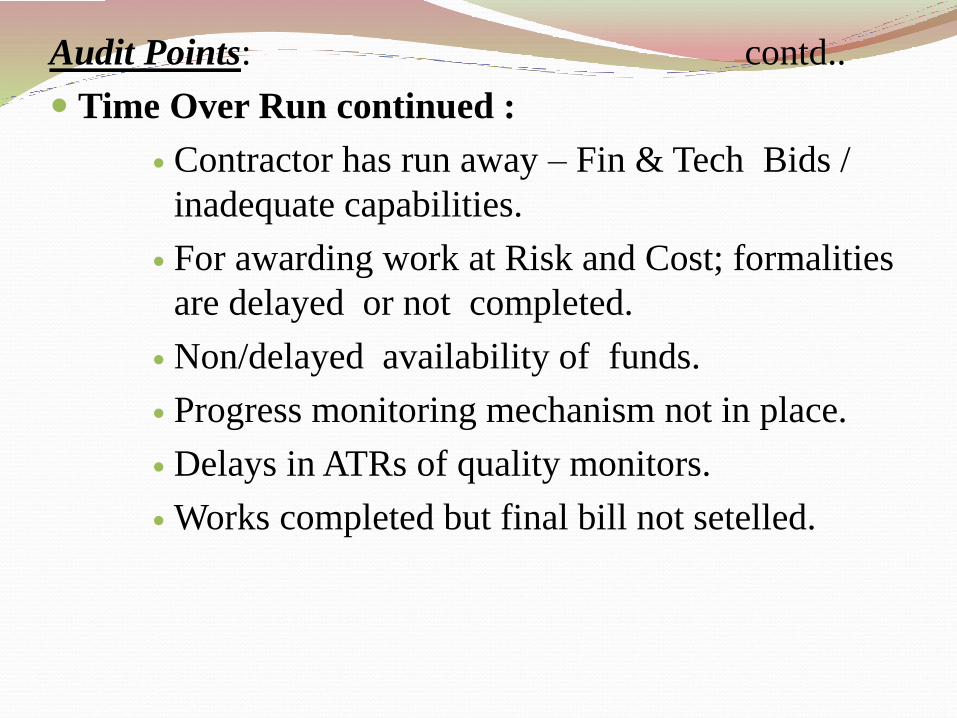

Audit Points: contd..

Time Over Run continued :

Contractor has run away – Fin & Tech Bids /

inadequate capabilities.

For awarding work at Risk and Cost; formalities

are delayed or not completed.

Non/delayed availability of funds.

Progress monitoring mechanism not in place.

Delays in ATRs of quality monitors.

Works completed but final bill not setelled.

Cost Over Run: Adequate contractual capacity not available in the

States. Award at higher rates.

Adequate competition not generated:

e-procurement/tendering

Cost escalation due to time over run

Disputes with Contractor : Arbitration

Turn key Projects: Defective agreements/vague

terms and conditions.

LD charges are levied correctly and recoverd.

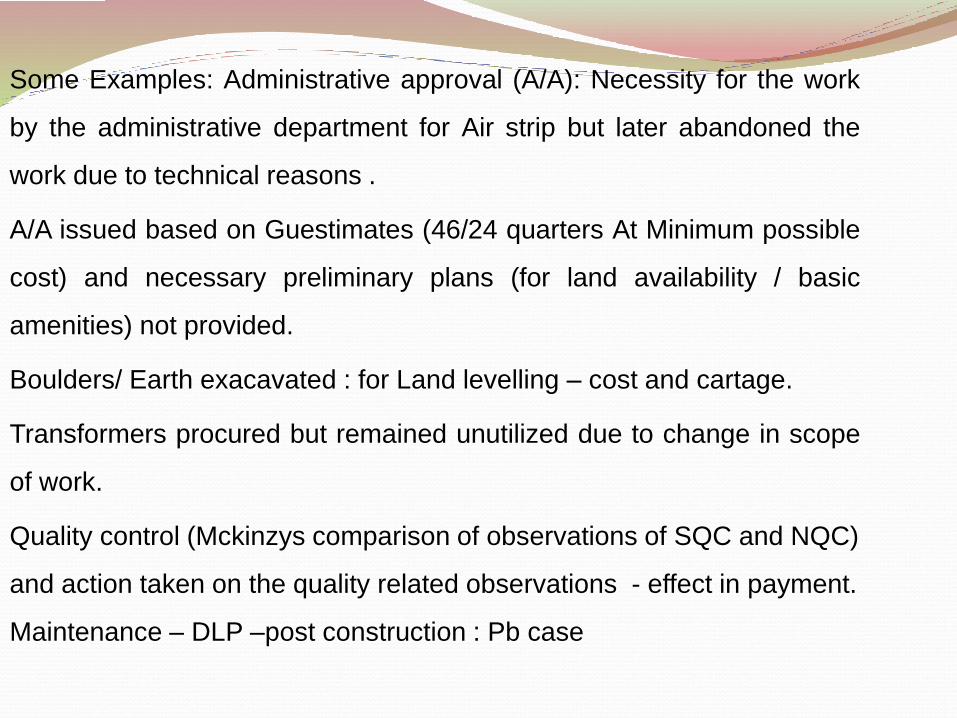

Some Examples: Administrative approval (A/A): Necessity for the work

by the administrative department for Air strip but later abandoned the

work due to technical reasons .

A/A issued based on Guestimates (46/24 quarters At Minimum possible

cost) and necessary preliminary plans (for land availability / basic

amenities) not provided.

Boulders/ Earth exacavated : for Land levelling – cost and cartage.

Transformers procured but remained unutilized due to change in scope

of work.

Quality control (Mckinzys comparison of observations of SQC and NQC)

and action taken on the quality related observations - effect in payment.

Maintenance – DLP –post construction : Pb case

DPRs/ Design and Drawings: To be based on proper field

and site surveys, necessary soil/field investigations

(seldom found/normally noticed at the execution stage in

the form of large deviations/variations in scope of

work/quantities)

Road alignments based on transact walk (normally

dispute with forest department/land owners)

Proper soil surveys in works (building , dams, canals

which do not come up timely or never used or

breached or washed away)

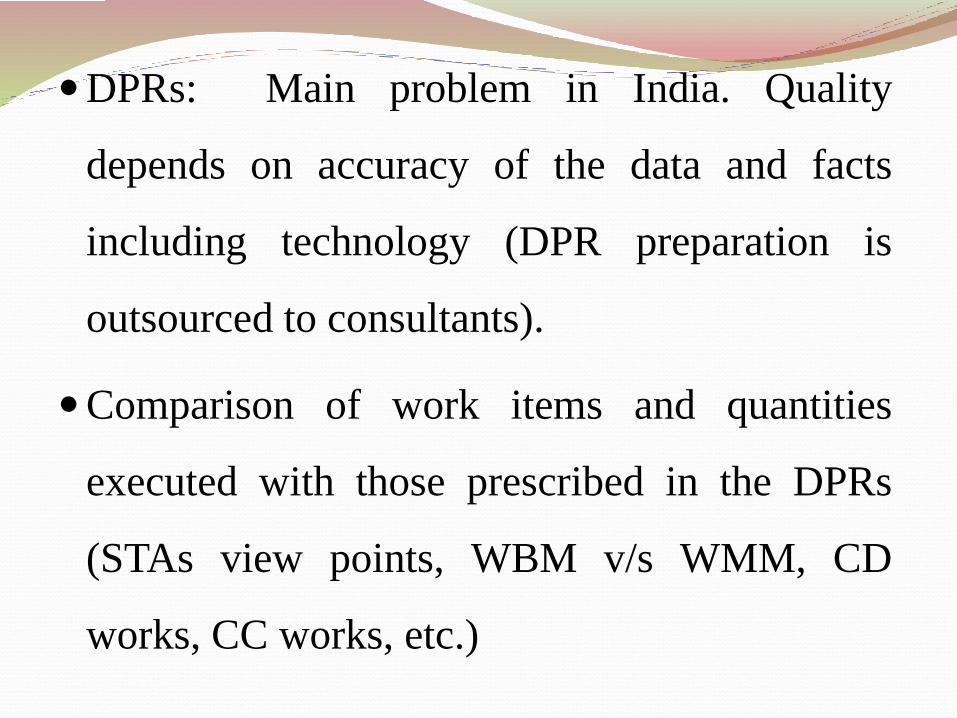

DPRs: Main problem in India. Quality

depends on accuracy of the data and facts

including technology (DPR preparation is

outsourced to consultants).

Comparison of work items and quantities

executed with those prescribed in the DPRs

(STAs view points, WBM v/s WMM, CD

works, CC works, etc.)

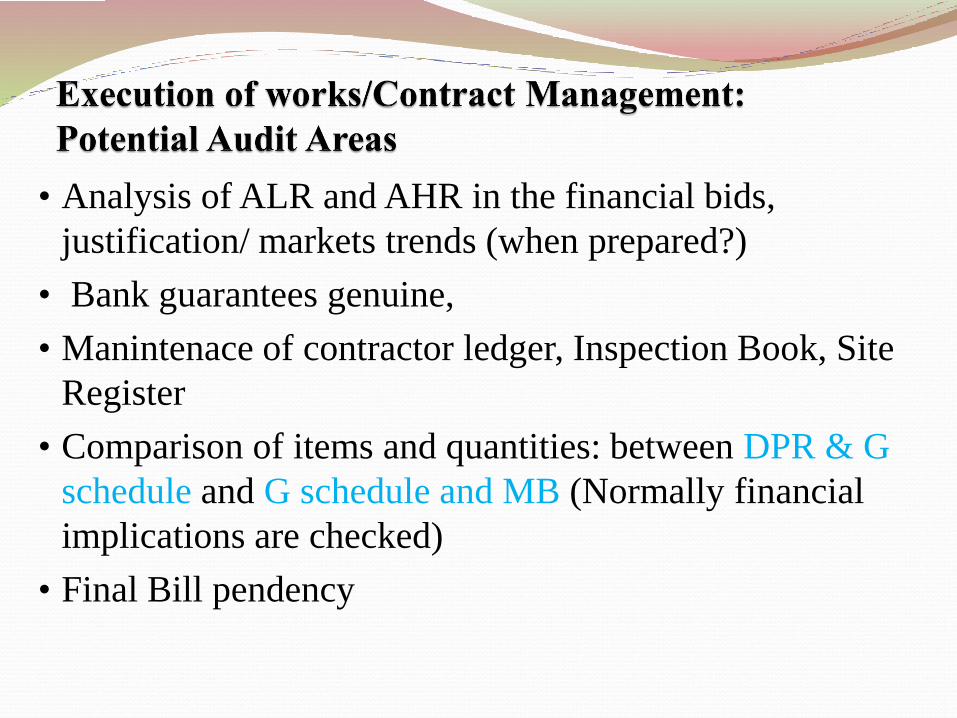

• Analysis of ALR and AHR in the financial bids,

justification/ markets trends (when prepared?)

• Bank guarantees genuine,

• Manintenace of contractor ledger, Inspection Book, Site

Register

• Comparison of items and quantities: between DPR & G

schedule and G schedule and MB (Normally financial

implications are checked)

• Final Bill pendency

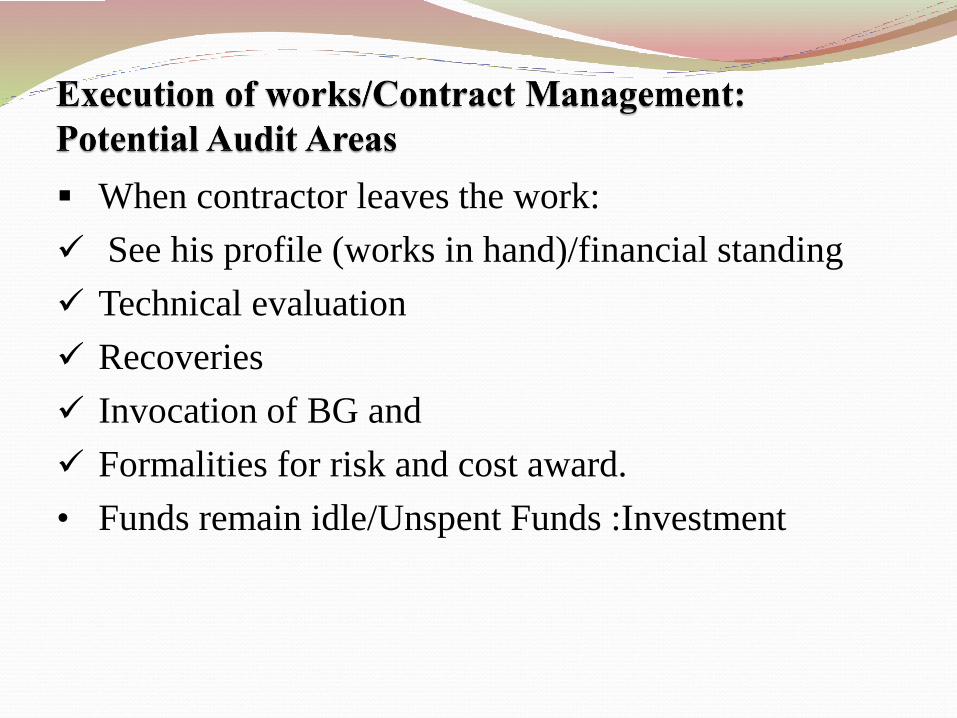

When contractor leaves the work:

See his profile (works in hand)/financial standing

Technical evaluation

Recoveries

Invocation of BG and

Formalities for risk and cost award.

• Funds remain idle/Unspent Funds :Investment

Appropriateness of the action taken on the

observations of quality monitors

Comparison of observations of different quality

monitors

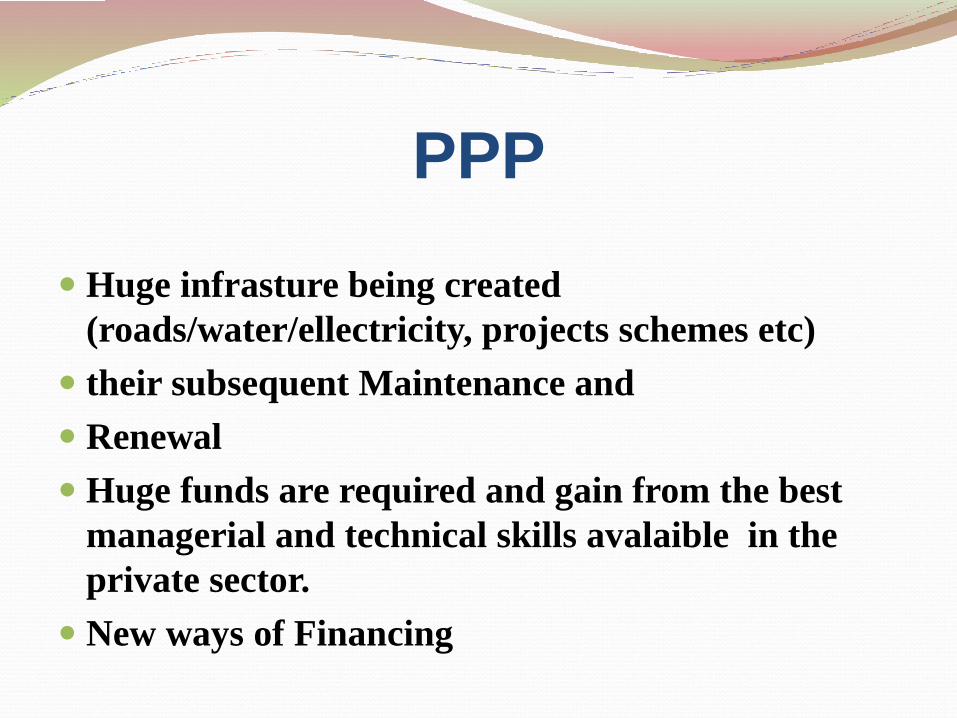

PPP

Huge infrasture being created

(roads/water/ellectricity, projects schemes etc)

their subsequent Maintenance and

Renewal

Huge funds are required and gain from the best

managerial and technical skills avalaible in the

private sector.

New ways of Financing

PPP contd….

Requirement of huge funds:

Tools for meeting funds requirement - Diferrent Models:

PPP - JVs and

Others:

BOLT (Built, Operate, Lease and

Transfer/MCA-TCS)

BOOT (Built, Operate,Own and Transfer)

BOT (Built, Operate and Transfer/TCS-

IGNOU)

SPVs (opens a company for the purpose)

PPP contd…

Financing:

Toll (Estimation of Receipts & Payments/

Cost Benefit Analysis)

Cess on users who can afford (Mining and

other commercial users)

Annuity (Where Toll/Cess not possible):

Bunching to ivite financially and

technically sound big players.

Thank you

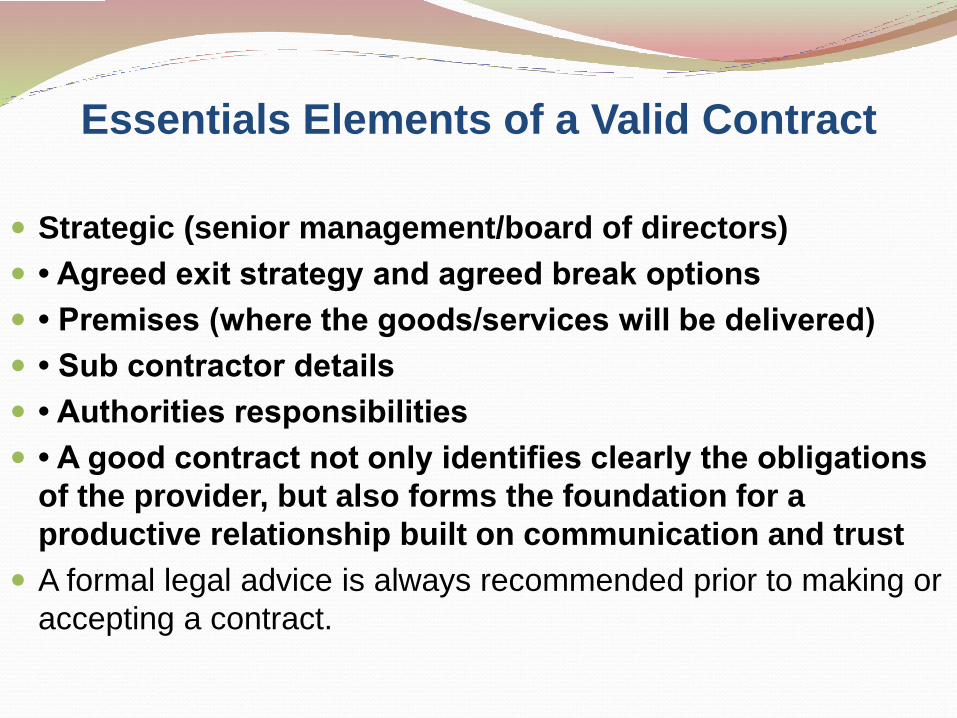

Essentials Elements of a Valid Contract

Strategic (senior management/board of directors)

• Agreed exit strategy and agreed break options

• Premises (where the goods/services will be delivered)

• Sub contractor details

• Authorities responsibilities

• A good contract not only identifies clearly the obligations

of the provider, but also forms the foundation for a

productive relationship built on communication and trust

A formal legal advice is always recommended prior to making or

accepting a contract.

Essentials Elements of a Valid Contract:

acceptance,

agreement and

consideration.

Essentials Elements of a Valid Contract:

1.Proposal and acceptance

2. Consideration -- lawful consideration with a lawful object

3. Capacity of parties to contract -- competent parties

4. Free consent

5.An agreement must not be expressly declared to be void.

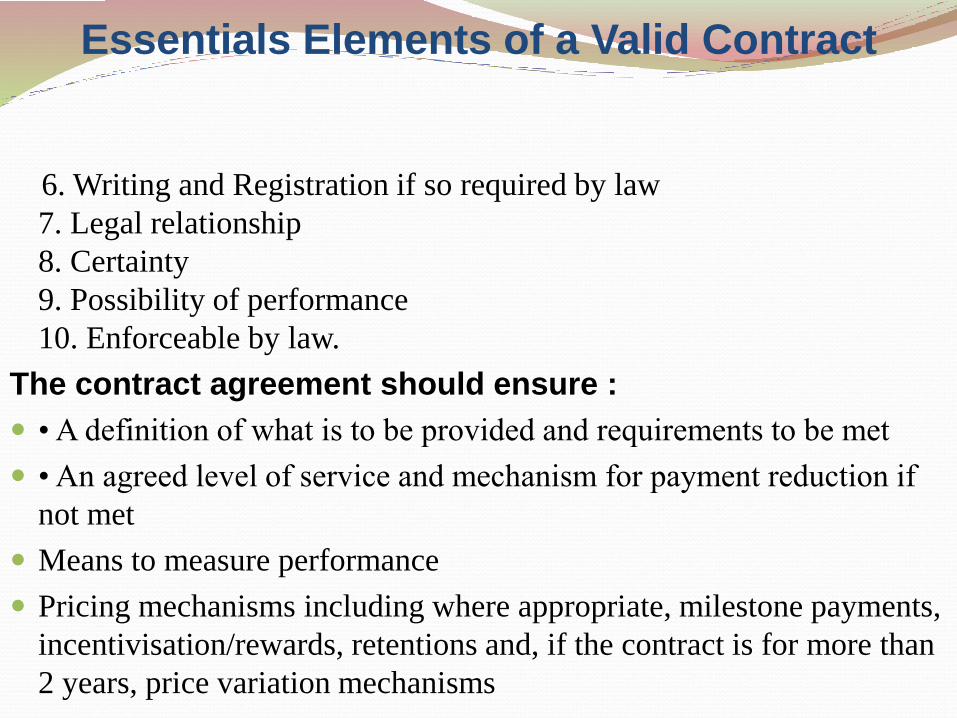

Essentials Elements of a Valid Contract

6. Writing and Registration if so required by law

7. Legal relationship

8. Certainty

9. Possibility of performance

10. Enforceable by law.

The contract agreement should ensure :

• A definition of what is to be provided and requirements to be met

• An agreed level of service and mechanism for payment reduction if

not met

Means to measure performance

Pricing mechanisms including where appropriate, milestone payments,

incentivisation/rewards, retentions and, if the contract is for more than

2 years, price variation mechanisms

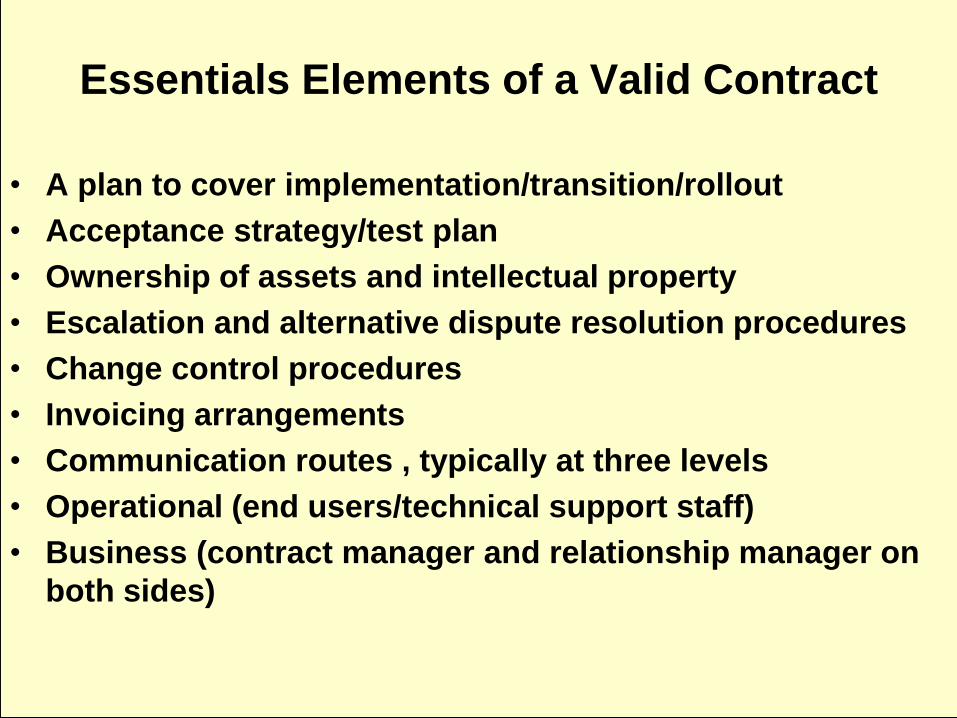

Essentials Elements of a Valid Contract

• A plan to cover implementation/transition/rollout

• Acceptance strategy/test plan

• Ownership of assets and intellectual property

• Escalation and alternative dispute resolution procedures

• Change control procedures

• Invoicing arrangements

• Communication routes , typically at three levels

Operational (end users/technical support staff)

Business (contract manager and relationship manager on

both sides)

Types of the works :

•Petty (not more than ` 50,000),

•Minor works (More than ` 50,000 but not more

than 50 lakh)

•Major works (More than ` 50 lakh)

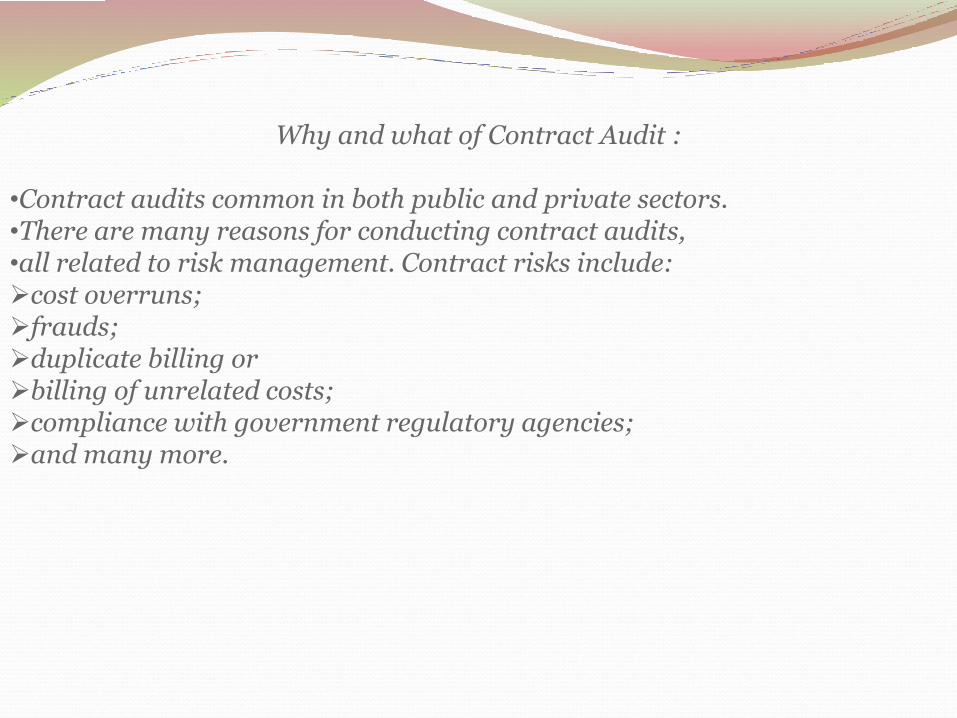

Why and what of Contract Audit :

•Contract audits common in both public and private sectors. •There are many reasons for conducting contract audits, •all related to risk management. Contract risks include: cost overruns; frauds; duplicate billing or billing of unrelated costs; compliance with government regulatory agencies; and many more.

There are two general types of contract audits:

control audits and recovery audits.

Control audits are conducted either prior to the spending period or early in the spending period. The purpose is to gain an understanding of the contractors systems, controls and supporting documentation.

Recovery audits are conducted near the end of the spending period. The purpose is to determine if any costs charged to the contract are not valid and if there are any regulatory or contract noncompliance issues to be resolved.

Strategy Development

Develop a strategy for conducting contract audits.

Decide who will conduct the audits: internal auditors or an outside firm?

Determine criteria for which type of audit to conduct. For example, first-time contractors conduct control audits to learn

their systems, controls and documentation and also conduct a recovery audit.

All other contractors only perform recovery audits.

An interaction on

Essentials of a valid contract

and general principles

sharing the experiences

Essentials Elements of a Valid Contract:

Essentials Elements of a Valid Contract:

1.Proposal and acceptance

2. Consideration -- lawful consideration with a lawful

object

3. Capacity of parties to contract -- competent parties

4. Free consent

5. An agreement must not be expressly declared to be

void

6. Writing and Registration if so required by law.

Essentials Elements of a Valid Contract

7. Legal relationship

8. Certainty

9. Possibility of performance

10. Enforceable by law

The contract-agreement should ensure :

• A definition of what is to be provided and requirements to be

met

• An agreed level of service and mechanism for payment

reduction if not met

• Means to measure performance

• Pricing mechanisms including where appropriate, milestone

payments, incentivisation /rewards, retentions and, if the

contract is for more than 2 years, price variation mechanisms

Essentials Elements of a Valid Contract

• A plan to cover implementation/transition/rollout

• Acceptance strategy/test plan

• Ownership of assets and intellectual property

• Escalation and alternative dispute resolution procedures

• Change control procedures

• Invoicing arrangements

• Communication routes , typically at three levels

• Operational (end users/technical support staff)

• Business (contract manager and relationship manager on

both sides)

Essentials Elements of a Valid Contract

• Strategic (senior management/board of directors)

• • Agreed exit strategy and agreed break options

• • Premises (where the goods/services will be delivered)

• • Sub contractor details

• • Authorities’ responsibilities

• • A good contract not only identifies clearly the obligations

of the provider, but also forms the foundation for a

productive relationship built on communication and trust

• A formal legal advice is always recommended prior to making

or accepting a contract.

GENERAL PRINCIPLES TO BE OBSERVED

Cardinal principle of spending: Spend money as if it is from your ownpocket and document the spending procedure appropriately.

Every officer is expected to exercise the same vigilance in respect ofexpenditure incurred from public moneys as a person of ordinaryprudence would exercise in respect of expenditure of his own money.

The expenditure should not be :

prima facie more than the occasion demands; directly or indirectly to theauthority’s own advantage; for the benefit of a particular person orsection of people (exception:court/public policy and allowances not asource of profit.

Transparency in spending, ensuring equal opportunities to suppliers,maximizing competition

Value for money: Efficiency, Economy, Effectiveness (Ensure all or anoptimal mix of the three)

FUNDAMENTAL PRINCIPLES OF PROCUREMENT

Fundamental principles of public procurement :

Every authority delegated with the financial powers of

procuring goods in public interest shall have the

responsibility and accountability to bring

• efficiency,

• economy,

• transparency and

• for fair and equitable treatment of suppliers

• and promotion of competition in public procurement.

The procedure to be followed in making public procurement must conform to the following yardsticks:-

1. the specifications in terms of quality, type etc., as also quantity of goods to be procured, should be clearly spelt out keeping in view the specific needs of the procuring organisations.

2. the specifications so worked out should meet the basic needs of the organisation without including superfluous and non-essential features, which may result in unwarranted expenditure. Care should also be taken to avoid purchasing quantities in excess of requirement to avoid inventory carrying costs;

3. offers should be invited following a fair, transparent and reasonable procedure;

4. the procuring authority should be satisfied that the selected offer adequately meets the requirement in all respects;

5. the procuring authority should satisfy itself that the price of the selected offer is reasonable and consistent with the quality required;

6. at each stage of procurement the concerned procuring authority must place on record, in precise terms, the considerations which weighed with it while taking the procurement decision.

TRANSPARENCY, COMPETITION, FAIRNESS AND

ELIMINATION OF ARBITRARINESS IN THE

PROCUREMENT PROCESS

Arbitrariness in the procurement process: All government purchases should be made in a transparent, competitive and fair manner, to secure best value for money. This will also enable the prospective bidders to formulate and send their competitive bids with confidence. Some of the measures for ensuring the above are as follows:-

(i) the text of the bidding document should be self-contained and comprehensive without any ambiguities. All essential information, which a bidder needs for sending responsive bid, should be clearly spelt out in the bidding document in simple language. The bidding document should contain, inter alia;

(ii) the criteria for eligibility and qualifications to be met by the bidders such as minimum level of experience, past performance, technical capability, manufacturing facilities and financial position etc.

• eligibility criteria for goods indicating any legal restrictions or conditions about the origin of goods etc which may required to be met by the successful bidder;

• the procedure as well as date, time and place for sending the bids;

• date, time and place of opening of the bid;• terms of delivery;• special terms affecting performance, if any.

(iii) Suitable provision should be kept in the bidding document to enable a bidder to question the bidding conditions, bidding process and/ or rejection of its bid.

(iv) Suitable provision for settlement of disputes, if any, emanating from the resultant contract, should be kept in the bidding document.

(iv)The bidding document should indicate clearly thatthe resultant contract will be interpreted under theLaw of the Land.

(v)The bidders should be given reasonable time tosend their bids.

(vi)The bids should be opened in public andauthorised representatives of the bidders should bepermitted to attend the bid opening.

(vii) The specifications of the required goods shouldbe clearly stated without any ambiguity so that theprospective bidders can send meaningful bids. Inorder to attract sufficient number of bidders, thespecification should be broad based to the extentfeasible. Efforts should also be made to use standardspecifications which are widely known to the industry.

Public procurement procedure is also to ensure efficiency,

economy and accountability in the system. To achieve the

same, the following keys areas should be addressed:

To reduce delay, appropriate time frame for each stage of

procurement should be prescribed by the Department. Such

a time frame will also make the concerned purchase officials

more alert.

To minimise the time needed for decision making and

placement of contract, every Department, with the approval

of the competent authority, may delegate, wherever

necessary, appropriate purchasing powers to the lower

functionaries.

EFFICIENCY, ECONOMY AND ACCOUNTABILITY IN PUBLIC

PROCUREMENT SYSTEM

The Departments should ensure placement of contract within the original validity of the bids. Extension of bid validity must be discouraged and resorted to only in exceptional circumstances.

Bring in the rate contract system more and more common user items which are frequently needed in bulk by various departments. The Central Purchase Organisation should also ensure that the rate contracts remain available without any break

Misconception of buying only the cheapest goods ignoring desired quality

From the above procedure, it is quiteclear that one need not always buythe cheapest articles/equipment.Where quality is an importantconsideration of procurement,substandard goods/undesirablesuppliers can be eliminated at the‘Technical Bid’ stage itself withoutopening their financial bids.

For inviting Bids/Tenders, a detailed document called “Bidding Document” is prepared.

Tendering/Invitation of Bids

Criteria for determining responsiveness of bids, criteria as well as factors to be taken into account for evaluating the bids on a common platform and the criteria for awarding the contract to the responsive lowest bidder should be clearly indicated in the bidding documents.

Bids received should be evaluated in terms of the conditions already incorporated in the bidding documents; no new condition which was not incorporated in the bidding documents should be brought in for evaluation of the bids. Determination of a bid's responsiveness should be based on the contents of the bid itself without recourse to extrinsic evidence.

Bidders should not be permitted to alter or modify their bids after expiry of the deadline for receipt of bids.

Negotiation with bidders after bid opening must be severely discouraged. However, in exceptional circumstances where price negotiation against an ad-hoc procurement is necessary due to some unavoidable circumstances, the same may be resorted to only with the lowest evaluated responsive bidder.

Bid Evaluation

In the rate contract system, where a number of firms are brought on rate contract for the same item, negotiation as well as counter offering of rates are permitted with the bidders. Contract should ordinarily be awarded to the lowest evaluated bidder whose bid has been found to be responsive and who is eligible and qualified to perform the contract satisfactorily as per the terms and conditions incorporated in the corresponding bidding document. However, where the lowest acceptable bidder against ad-hoc requirement is not in a position to supply the full quantity required, the remaining quantity, as far as possible, be ordered from the next higher responsive bidder at the rates offered by the lowest responsive bidder.

The name of the successful bidder awarded the contract should be mentioned in the Departments notice board or bulletin or web site.

Bid Evaluation

WEB PUBLICITY

Necessary in India

Thanks

CONTRACT : DEFINITION

• A contract is defined as

• An agreement between two or more parties, with some

• legal binding enforceable in the court of law.

• A contract is a promise or a set of promises :

• for the breach of which the law gives a remedy or

• the performance of which the law in some way recognizes as a duty.

• There are many stages involved in the formation and acceptance of a legal

contract. The basic stages of any contract includes :

proposal,

offer,

acceptance,

agreement and

consideration.

PROCUREMENT of GOODS

i. These are available in Chapter VI of the General Financial Rules (GFR), brought out by the Ministry of Finance, Department of Expenditure, Government of India, (GFRs 135 to 185). These rules have been adopted by IGNOU with the approval of Finance Committee and Board of Management. These rules have been circulated also by the Administration Division vide…. These rules are also available on the website of the Ministry of Finance , Department of Expenditure ( ….)

RULES GOVERNING PROCUREMENTOF GOODS AND SERVICES

In addition to this, the Department of Expenditure has also brought out a detailed Manual of Policies and Procedures for appointment of consultants which in fact details all the aspects relating to appointment of consultants.

This Manual is also available on the website of the Ministry of Finance, Department of Expenditure ( …).

Estimated Value of

Purchase

Prescribed Method/ Relevant GFR

1. Up to Rs.15,000/- Purchase of goods without quotations Rule 145

2. Above Rs.15,000/- and up

to Rs.1,00,000/-

Purchase of goods by Purchase Committee

Rule 146

3. Above Rs.1,00,000/-

a) Purchase of routine /

non-technical item

b) Special/technical

nature purchases

Purchase of goods by obtaining Sealed Bids:

Rule 149-53

a)Single Bid (Financial Bid)

b) Two Bids (Financial & Technical Bids)

3A. Above Rs.1,00,000/- and

up to Rs.25,00,000/-

Limited Tender Enquiry Rule-151

3B. Above Rs.25,00,000/- Advertised Tender Enquiry Rule 150

3C. Single tender enquiry Procurement from a single source in case of

proprietary articles, emergency necessarily to be

purchased from a particular source spare parts and

compatibility Rule 154

Purchase Rules at a Glance