Embed Size (px)

Citation preview

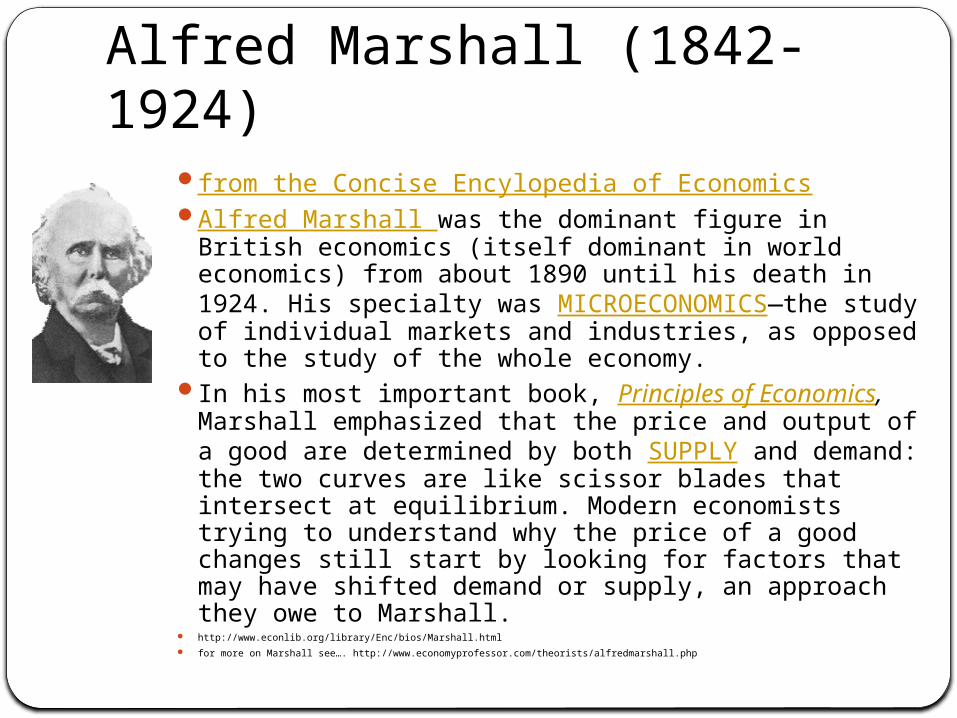

Alfred Marshall (1842-1924)from the Concise Encylopedia of EconomicsAlfred Marshall was the dominant figure in British

economics (itself dominant in world economics) from about 1890 until his death in 1924. His specialty was MICROECONOMICS—the study of individual markets and industries, as opposed to the study of the whole economy.

In his most important book, Principles of Economics, Marshall emphasized that the price and output of a good are determined by both SUPPLY and demand: the two curves are like scissor blades that intersect at equilibrium. Modern economists trying to understand why the price of a good changes still start by looking for factors that may have shifted demand or supply, an approach they owe to Marshall.

http://www.econlib.org/library/Enc/bios/Marshall.html

for more on Marshall see…. http://www.economyprofessor.com/theorists/alfredmarshall.php

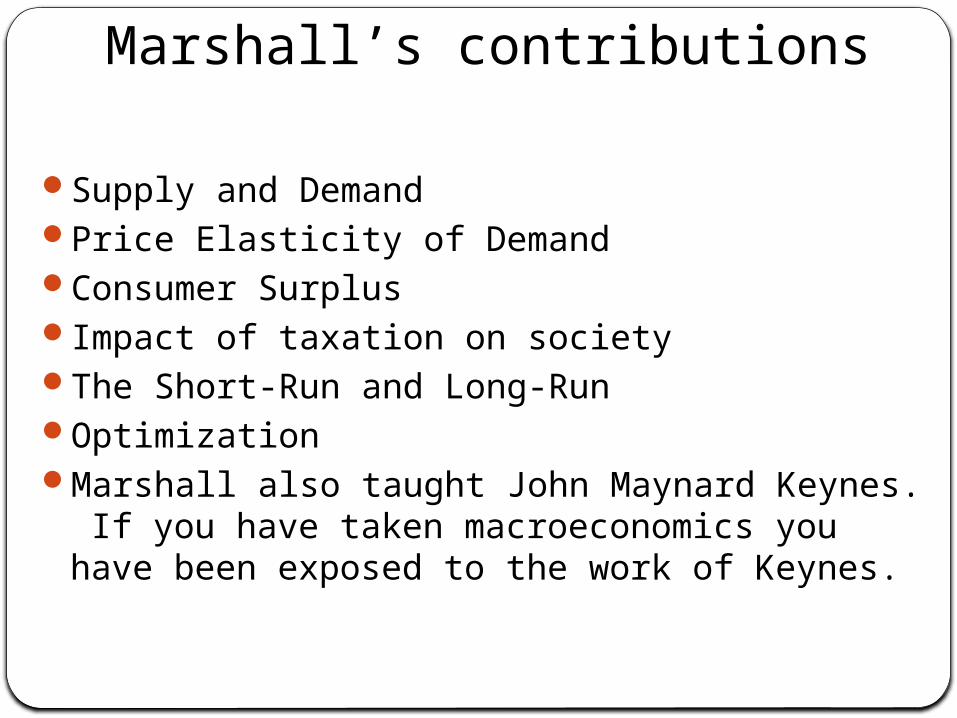

Marshall’s contributionsSupply and DemandPrice Elasticity of DemandConsumer SurplusImpact of taxation on societyThe Short-Run and Long-RunOptimizationMarshall also taught John Maynard Keynes. If

you have taken macroeconomics you have been exposed to the work of Keynes.

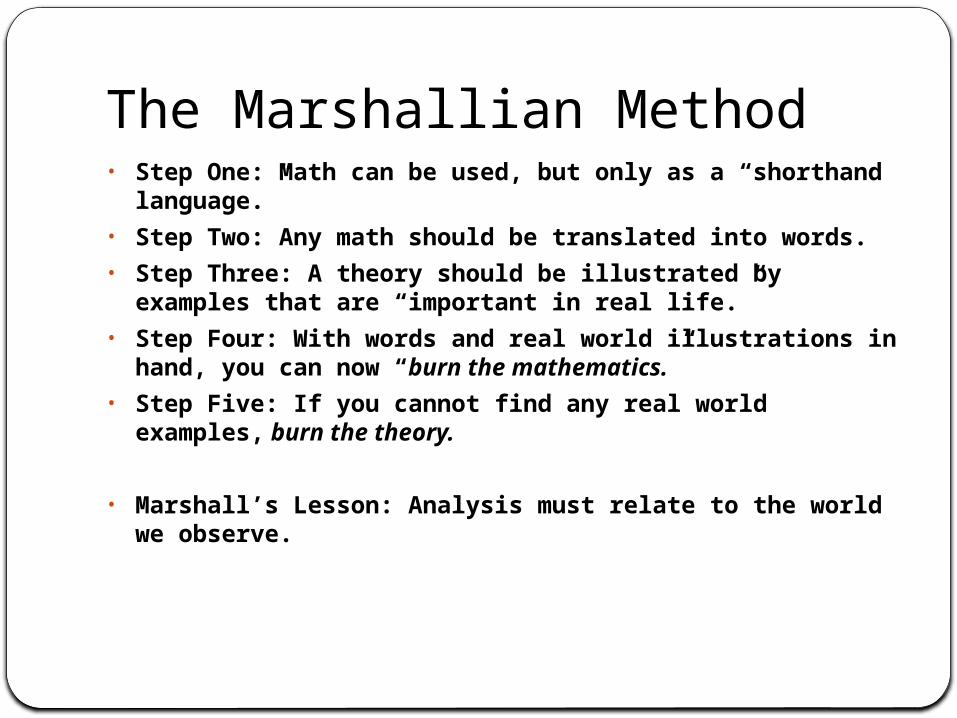

The Marshallian Method• Step One: Math can be used, but only as a “shorthand

language.”• Step Two: Any math should be translated into words.• Step Three: A theory should be illustrated by examples

that are “important in real life.”• Step Four: With words and real world illustrations in

hand, you can now “burn the mathematics.”• Step Five: If you cannot find any real world examples,

burn the theory.

• Marshall’s Lesson: Analysis must relate to the world we observe.

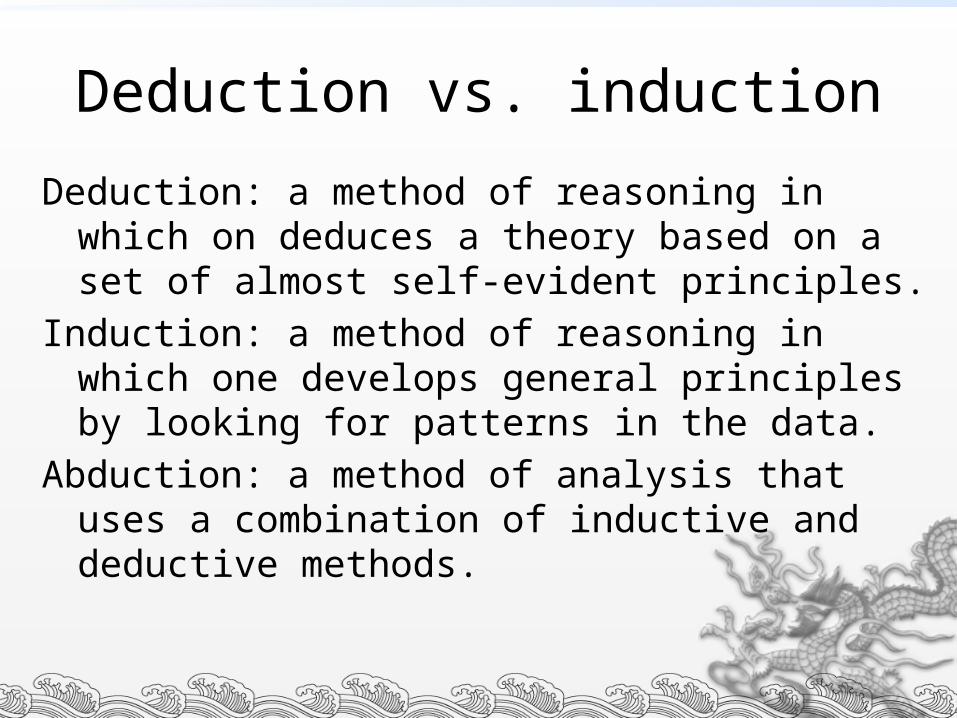

Deduction vs. induction

Deduction: a method of reasoning in which on deduces a theory based on a set of almost self-evident principles.

Induction: a method of reasoning in which one develops general principles by looking for patterns in the data.

Abduction: a method of analysis that uses a combination of inductive and deductive methods.

More on deduction and induction

The basic microeconomic theory of the firm – which we are about to review – is an example of deduction.

Estimating a firm’s demand function is an example of induction.

Interpreting a demand function is an example of abduction – since one needs to understand both data analysis and economic theory to make sense of the empirical results.

Maximizing the Value of the Firm• Profit = Total Revenue – Total Cost• The value of the firm is impacted by ▫Total Revenue.... which is a function of marketing

strategies, pricing and distribution policies, nature of competition....

▫Total Cost .... which is a function of the price and availability of inputs, alternative production methods...

▫The model of the firm is a deductive exercise designed to describe both factors that determine profit.

▫We begin with some basic definitions…

Total, Average, and Marginal RelationsDefinitions•Marginal – change in a dependent

variable caused by a one unit change in an independent variable.A Marginal Change is represented as

ΔY / ΔX•Alternative definitions: ▫Rate of change▫Slope

Graphing Total, Marginal, and Average Relations•Slope – a measure of the steepness of

a line.OR The rate of change

The marginal relation•Tangent – a line that touches but does

not intersect a given curve.▫This is used to find the slope of a

nonlinear curve.•Inflection Point – a point of maximum

slope.

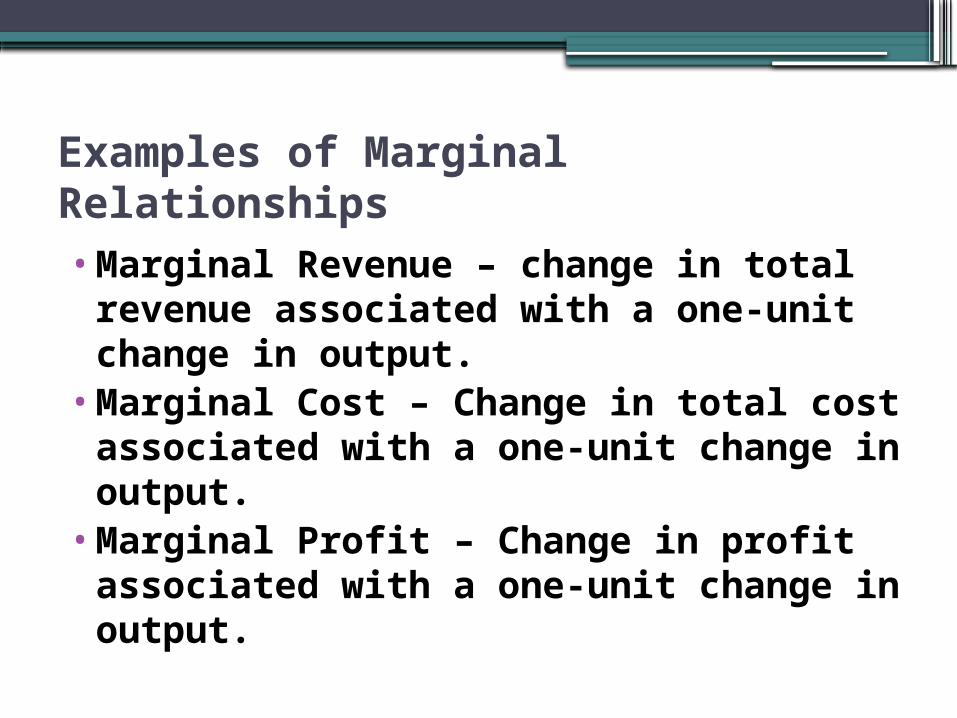

Examples of Marginal Relationships•Marginal Revenue – change in total

revenue associated with a one-unit change in output.

•Marginal Cost – Change in total cost associated with a one-unit change in output.

•Marginal Profit – Change in profit associated with a one-unit change in output.

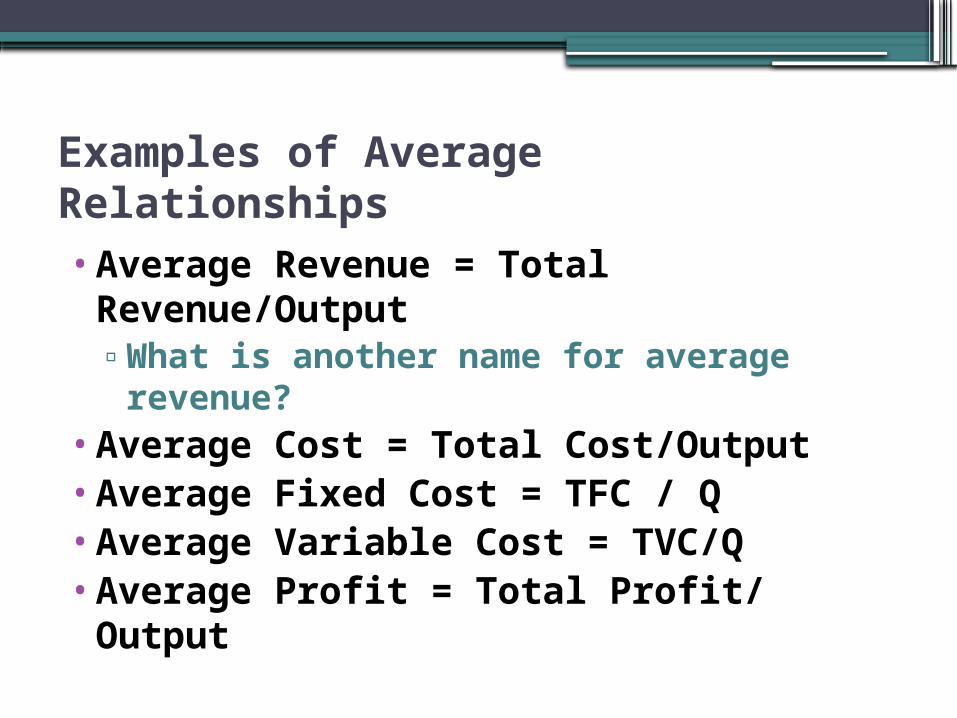

Examples of Average Relationships•Average Revenue = Total

Revenue/Output▫What is another name for average

revenue?•Average Cost = Total Cost/Output•Average Fixed Cost = TFC / Q•Average Variable Cost = TVC/Q•Average Profit = Total Profit/ Output

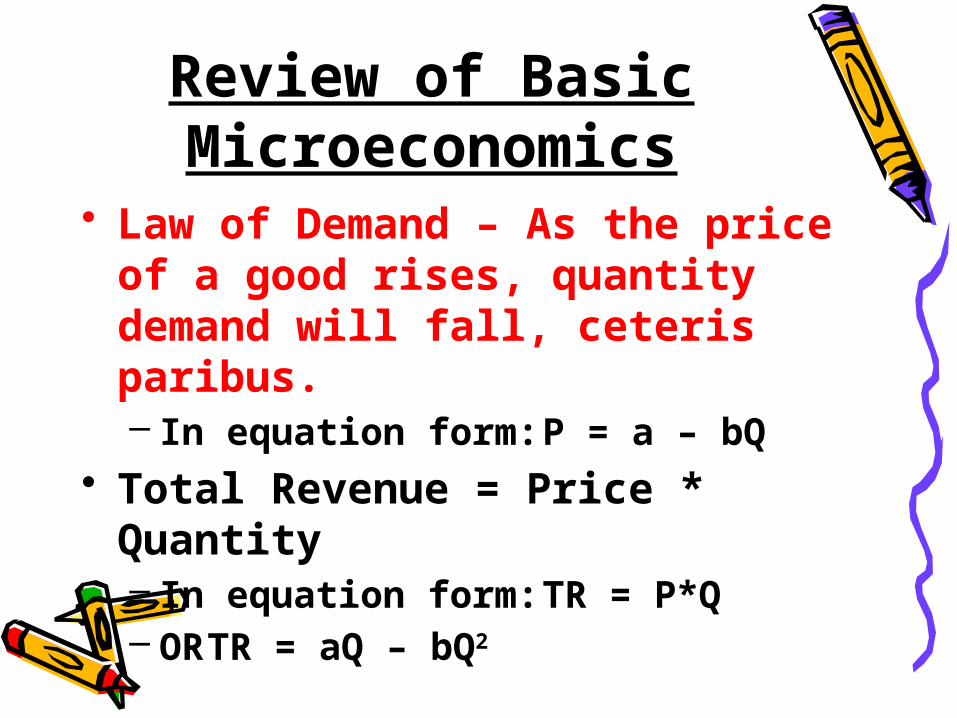

Review of Basic Microeconomics

• Law of Demand – As the price of a good rises, quantity demand will fall, ceteris paribus.– In equation form: P = a – bQ

• Total Revenue = Price * Quantity– In equation form: TR = P*Q– OR TR = aQ – bQ2

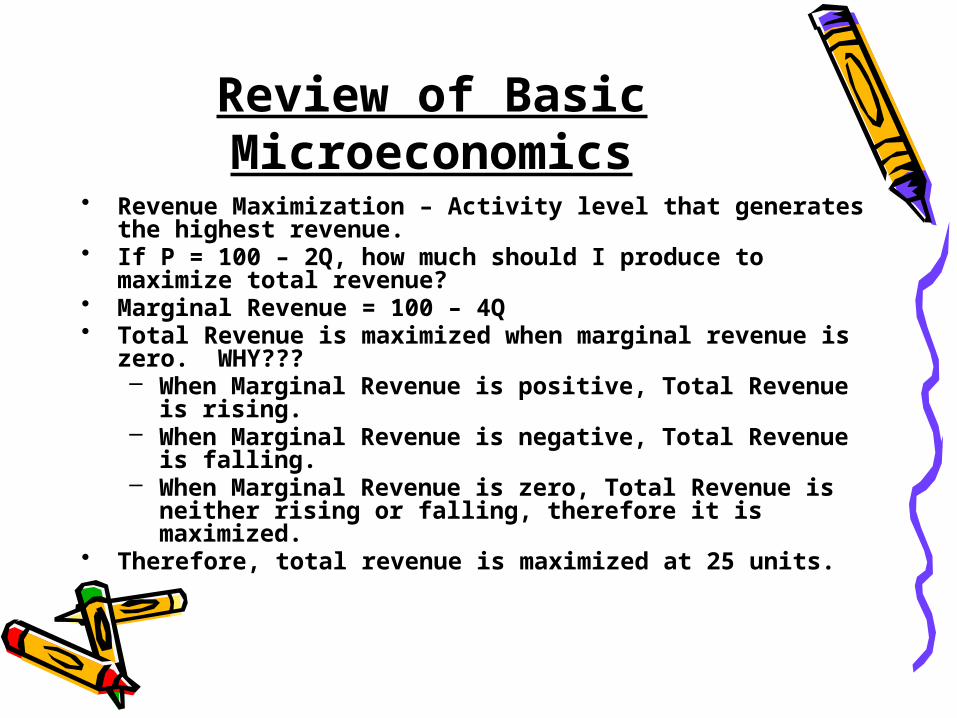

Review of Basic Microeconomics

• Revenue Maximization – Activity level that generates the highest revenue.

• If P = 100 – 2Q, how much should I produce to maximize total revenue?

• Marginal Revenue = 100 – 4Q• Total Revenue is maximized when marginal revenue is

zero. WHY???– When Marginal Revenue is positive, Total Revenue

is rising.– When Marginal Revenue is negative, Total Revenue

is falling.– When Marginal Revenue is zero, Total Revenue is

neither rising or falling, therefore it is maximized.• Therefore, total revenue is maximized at 25 units.

Review of Basic Microeconomics

• What is the objective of the firm? PROFIT MAXIMIZATION

• Profit = Total Revenue – Total Cost• To understand profit, you need to

understand both revenue and cost. Understanding total revenue begins with the Law of Demand. Understanding total cost begins with the Law of Diminishing Returns.

Review of Basic Microeconomics

• The Law of Diminishing Returns – As a variable input increases, holding all else constant, the rate of increase in output will eventually diminish.

• OR..... As a firm increases its employment of labor, holding capital and all other factors constant, the productivity of each worker hired will eventually diminish.

• WHY? Each additional worker has less and less capital to work with.

• The Law of Diminishing Returns is the foundation from which we build the relationship between output and total cost, marginal cost, and average cost.

Review of Basic Microeconomics

• Average Cost Minimization– Why not Total Cost Minimization?

• If Marginal Cost is less than Average Cost, Average Cost will be declining.

• If Marginal Cost is greater than Average Cost, Average Cost will be increasing.

• When MC = AC, Average Cost is Minimized.

• THE MATH OF AC MINIMIZATION

Review of Basic Microeconomics

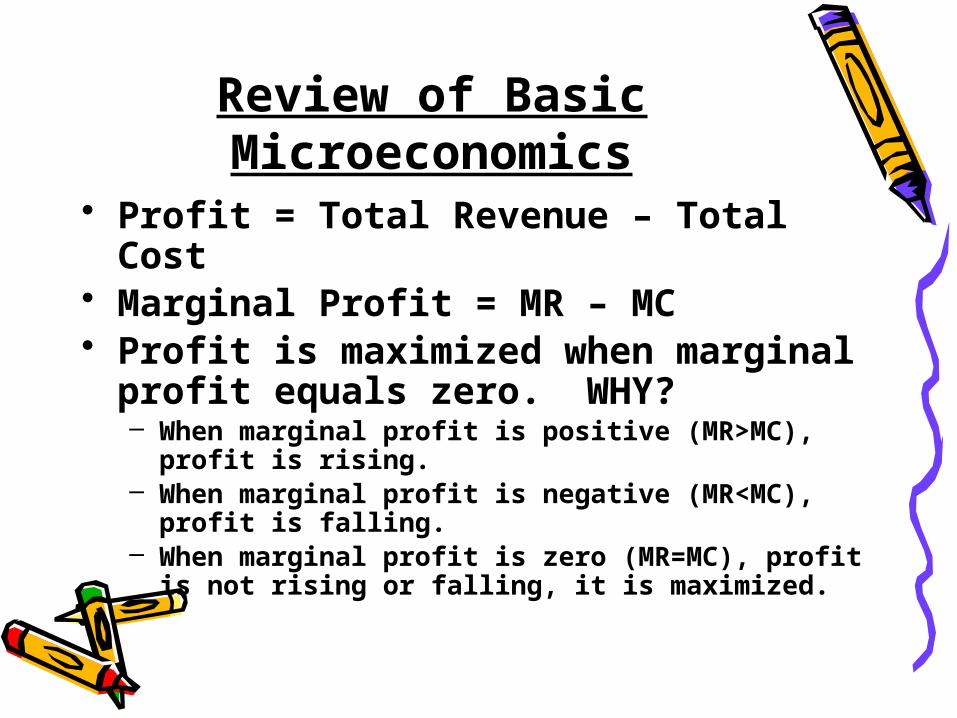

• Profit = Total Revenue – Total Cost• Marginal Profit = MR – MC• Profit is maximized when marginal

profit equals zero. WHY?– When marginal profit is positive (MR>MC),

profit is rising.– When marginal profit is negative (MR<MC),

profit is falling.– When marginal profit is zero (MR=MC), profit

is not rising or falling, it is maximized.

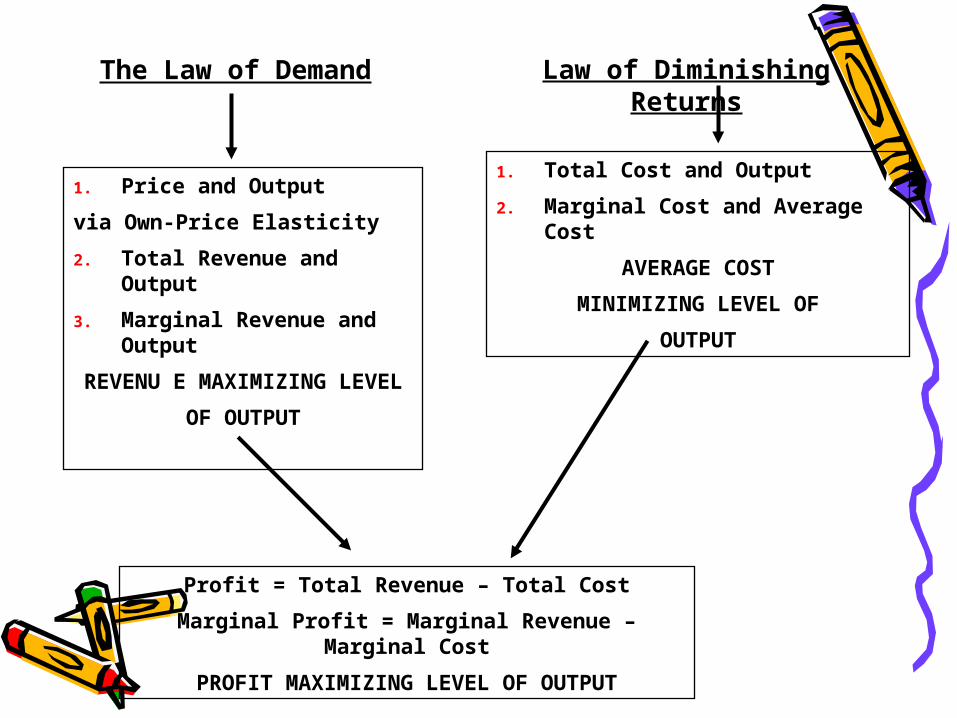

The Law of Demand Law of Diminishing Returns

1. Price and Output

via Own-Price Elasticity

2. Total Revenue and Output

3. Marginal Revenue and Output

REVENU E MAXIMIZING LEVEL

OF OUTPUT

1. Total Cost and Output

2. Marginal Cost and Average Cost

AVERAGE COST

MINIMIZING LEVEL OF

OUTPUT

Profit = Total Revenue – Total Cost

Marginal Profit = Marginal Revenue – Marginal Cost

PROFIT MAXIMIZING LEVEL OF OUTPUT

![Where to house the London poor [1881] - Alfred Marshall](https://img.pdfslide.us/doc/110x75/55cf882655034664618dd84e/where-to-house-the-london-poor-1881-alfred-marshall.jpg)

![Principles of Economics [1890] - Alfred Marshall](https://img.pdfslide.us/doc/110x75/55cf882555034664618dd607/principles-of-economics-1890-alfred-marshall.jpg)