Embed Size (px)

Citation preview

1

Executive Organization and Crisis Economic Policy-Making in the Americas

Alejandro Bonvecchi

Universidad Torcuato Di Tella-CONICET

Paper prepared for delivery at the 7th ECPR General Conference, Bordeaux, 4-7 September, 2013.1

1 The author is grateful to Octavio Amorim Neto, Lucio Renno, Juan Carlos Torre and Javier Zelaznik for their information, comments, and suggestions.

2

How do governments organize and manage responses to economic crises? The literature has typically paid attention to the nature of responses and its determinants rather than to their inception. Responses to crises have usually been analyzed as determined by the type of crisis and the political context in which they are formulated. Political economy models usually distinguish debt- or inflation-ridden crises from those stemming from external shocks; and focus on the status of the government party in the legislature, or on the type of political regime under which crises occur as determinants of both the government’s ability to develop and impose stabilization policies, and the extent to which those policies may solve the crisis (Persson and Tabellini 2000, Drazen 2000, Gourevitch 1986, Rogowski 1989). But these approaches are generally oblivious of the fact that responses to economic crises are generally crafted within the Executive branch, and traverse the same stages through which all public policies are produced – formulation, launching, and implementation.2 Consequently, there is virtually no analysis beyond former officials’ memoirs on how the Executive is organized to generate those responses, and whether the varying decision contexts corresponding to the different phases of public policymaking influence the Executive’s crisis management.

This paper investigates how governments organize and manage responses to economic crises by combining two hitherto unrelated threads of research: the literature on Executive organization and presidential decision styles developed within US presidential studies; and the literature on adjustment politics in emerging economies during the 1980s and 1990s. While the former has shown the linkages between decision settings, organizational arrangements, and managerial styles, the latter has argued the existence of shifts in Executive organization and management across policymaking stages as well as political and economic contexts. This paper brings those theoretical insights together in a comparative analysis of the Executive’s organization and decision-making processes during economic crisis in three federal presidential democracies with varying institutional arrangements and contrasting experiences with economic emergencies: Argentina, Brazil, and the United States. Analysis shows centralized organizational arrangements managed in a hierarchical way are typical of countries with more volatile economies and institutionally stronger executives, while more decentralized arrangements managed in an adversarial or collegial way are usually employed in countries with less volatile economies and institutionally weaker presidents.

To develop this argument, the paper is organized as follows. Section 1 discusses the theoretical combination of the cognitive and organizational variables central to US presidential studies and the institutional factors in the literature on adjustment politics, and explicates the methodology employed in the research. Section 2 describes the general patterns arising from the comparison of government responses to economic crises in Argentina, Brazil, and the United States. Section 3 discusses within-country variations by briefly comparing stabilization programs under different cognitive and institutional settings. The final section concludes and sets the agenda for further research.

2 For exceptions see Hall (1989, 1993).

3

1. Executive Organization and Economic Crisis Policy-making.

Students of the United States presidency have argued that analysis of decision-making should focus on how the Executive is organized and how presidents manage their staff. The organization of the Executive is structured to provide presidents with information and policy alternatives (Burke 2000). Organizational choices range from centralized – when information and policy alternatives are concentrated in a small circle of close advisers who may operate above cabinet jurisdictions – to decentralized – when information and advice is mainly provided by cabinet ministers, permanent bureaucrats, and/or legislators (Rudalevige 2002). Presidential management styles intend to exploit the advantages or compensate for the disadvantages of the Executive’s organization. According to Johnson (1974) presidents use three styles: competitive or adversarial, in which the president stands at the center of decision processes by overlapping jurisdictions, duplicating assignments, and developing rivalries amongst advisers and/or ministers; formalistic or hierarchical, in which the president delegates authority to top advisers who run a hierarchical organization with clearly specified, differentiated functions, and who filter the information and policy alternatives that reach the presidential desk; and collegial, in which the president operates as the hub of a wheel the spokes of which are a group of advisers who collectively discuss and propose alternatives. The competitive style is useful for maximizing presidential control and factoring in considerations of bureaucratic feasibility and political viability, but if the Executive’s organization is not centralized enough it demands an enormous investment of time from the president to manage and solve staff tensions. The hierarchical style is useful for maximizing diversity in information gathering and advice in the face of a moderately to extremely decentralized Executive organization, but it may generate upwards distortions and slowness in crisis situations. The collegial style is useful for maximizing technical optimality and bureaucratic feasibility in either centralized or decentralized Executive organizations, but it requires presidents to be skilled in maintaining a working group dynamics (Burke 2009).

The literature on the politics of economic adjustment in emerging economies claims that the organization of the Executive and the presidential management styles shift according to the stage of the policymaking process and the evolution of the economic crisis (Nelson 1989; Haggard and Kaufman 1992a, 1992b, 1995). The formulation and launching of responses to crises are typically carried out in a hierarchical way through a centralized organization of decision-making: hierarchy and centralization are instrumental to insulate policymakers against the influence and pressures of interest groups seeking to avoid the costs, or increase the benefits, of stabilization policies. The implementation of responses to crises is typically executed using a decentralized organization of decision-making managed through either competitive or collegial styles: competition/collegiality and decentralization are instrumental for opening arenas in which government and interest groups may bargain over the nature and extent to which compensations or benefits may be distributed to offset or enhance the consequences of policies (Haggard and Kaufman 1992b, 1995). These shifts in organization and managerial styles are assessed in this literature as inefficient for the realization of stabilization objectives: by ending the insulation of policymakers and enabling interest groups to influence outcomes, the organization and management of Executive decision-making processes ends up channeling exactly the pressures that would have to be contained for stabilization policies to succeed (ibid.).

4

On the basis of these two literatures, it can be argued that economic crises pose a series of tradeoffs to the organization of the Executive and the styles of presidential decision-making. In the formulation of policy responses to economic crises, the Executive should be isolated from bureaucratic and interest group pressures in order to design optimal policies – but isolation may generate biases in information and policy alternatives that may result in suboptimal policies and/or obstruction by the economic and/or political actors excluded from the formulation process. In the launching of responses to crises, the Executive should be insulated from those same pressures in order to prevent gridlocks that may threaten the intertemporal credibility of policy announcements – but insulation may stop necessary information about the political and bureaucratic viability of policies from reaching the presidential desk, and thus complicate the very initiation of stabilization policies. In the implementation of policy responses to economic crises, the Executive’s previous isolation should be relaxed to enable information about the effects of policies to be factored in and possibly lead to the fine tuning of policy instruments – but increasing access of interest groups to policymakers may give sectoral influences the chance to derail the consistency of policies.

To deal with these tradeoffs, presidents must choose specific combinations of organizational structures and management styles. The argument of this paper is that presidential choices are driven by two factors: the cognitive context of their decision setting, and the institutional capacity of the presidency.

Cognitive contexts shape how presidents perceive situations. As argued in the sociological (Luhmann 1997, 1998), economic (Knight 1921; Kahneman and Tversky 2000) and organizational (Simon 1978, 1997) literatures on decision-making, the cognitive disposition of individuals is marked by uncertainty: the more uncertain they perceive to be about what is happening, the less capable they feel of assessing what is at stake for them, and of deciding what to do about it – and vice versa: the more certain they perceive to be, the more capable they feel of understanding the situation and acting upon it. A situation or context is uncertain for individuals if they perceive to be lacking information to define it or analytical capabilities to process it. In contrast, a context would be one of certainty if individuals feel confident they possess enough information and analytical capabilities to navigate it.

Cognitive contexts matter for crisis decision-making because, following Walcott and Hult (1995: 20), presidents develop staff structures that are “roughly congruent with the prevailing decision setting”. Thus, if presidents perceive they are confronted with uncertainty, they should build competitive or collegial arrangements that foster the search for alternative sources of information and advice, so that new information and options can be introduced, weighed in, and decided on after thorough debate. If presidents perceive certainty about their situation, they should develop hierarchical or collegial-consensual arrangements to enhance control over decision-making, so that policies actually conform to their view of the context and their choices about the issues at stake (ibid: 21-23).

The crafting of responses to economic crises should be no different: presidents should organize decision-making and manage their staff in ways congruent with the main feature of their decision setting. If the nature of the economic crisis is perceived to be novel by policymakers and thus disposes them to act under uncertainty, then a decentralized organization managed in a collegial way – also termed multiple

5

advocacy (George 1972) – should be employed to formulate policy responses: these arrangements maximize the variety of information and policy viewpoints that serves as input to the decision process, and prevents bureaucratic, economic, and political actors from obstructing the launching and implementation of policies by involving them in their preparation (Porter 1988). If, in contrast, the nature of the crisis is perceived by policymakers to be well-known, and thus disposes them to operate in a fairly certain context, then a centralized decision process managed in a hierarchical way would be most efficient to formulate policy responses: these arrangements maximize insulation from pressures, control over policymaking, and the surprise and secrecy typically required for stabilization policies to begin successfully. Centralized organization and hierarchical management styles would be most efficient to launch responses to economic crises: once the policy content of responses is defined, their operation should be set in motion by (an) actor(s) empowered to coordinate stabilization efforts – so that bureaucratic or interest-group pressures do not re-introduce the uncertainty that policy responses intend to terminate. Finally, since the implementation of responses to economic crises is typically marked by controversy in a less-than-uncertain context between the government and the economic actors affected by stabilization policies, the Executive should organize its decision-making processes so that the voice of the affected actors may generate information that enables presidents to adequately weigh in potential problems, contextual changes, and policy alternatives to adjust to emerging challenges: competitive arrangements allow presidents to achieve these aims while preserving power to settle controversies, and thus protect the consistency of responses to crises.

The institutional capacity of the presidency shapes the extent to which presidents can decide unilaterally. This capacity has two dimensions: legislative and organizational. The more the executive is institutionally empowered to legislate unilaterally, the higher the president’s disposition to decide alone: strong legislative powers enable executives to develop quick responses to crisis which may be closer to their preferences and escape the pressures of interest groups – while weak legislative powers force them to seek consensus and compromise at the expense of speed and preference consistency (Amorim Neto 1998; Moe and Howell 1999). The more the executive is institutionally empowered to organize unilaterally its internal policymaking process, the higher the president’s inclination to concentrate decisions: centralized organizational powers enable presidents to maximize their control over the Executive’s bureaucracy by creating and dismantling units and positions, thus expanding or restricting their sources of information and advice, and consequently escaping bureaucratic biases and strife – while decentralized organizational powers force presidents to share policymaking with experts and bureaucrats, thus gaining technical competence and consistency at the expense of political control (Moe and Wilson 1994; Lewis 2008).

The institutional capacity of the presidency matters because it constrains the type of organizational arrangements and managerial styles presidents may employ in crisis situations. If presidents have strong legislative and organizational powers, they would be able to impose a centralized policymaking process managed in a hierarchical way: ministers and bureaucrats would be at the president’s service because they would also be at their mercy – political control by the president and his immediate, most trusted advisers is thus maximized (Moe 1993). If presidents have strong legislative powers but weaker organizational powers, policymaking could still be hierarchically managed but no longer centralized in the president’s office:

6

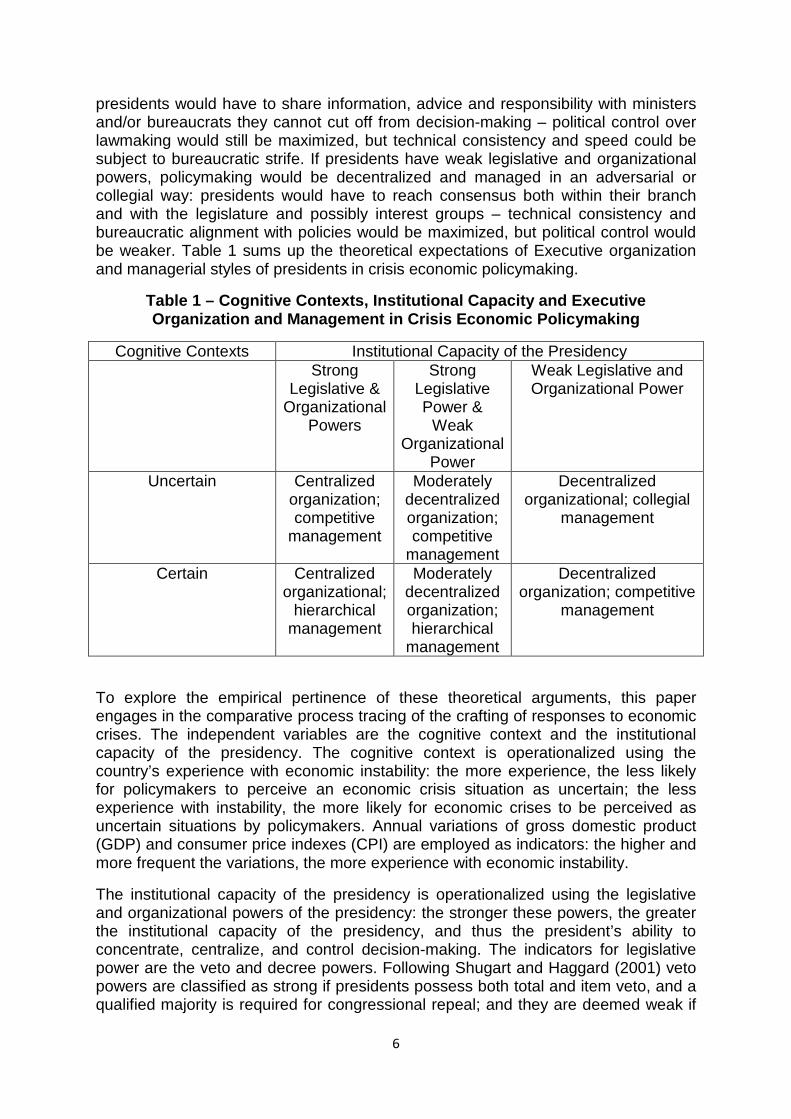

presidents would have to share information, advice and responsibility with ministers and/or bureaucrats they cannot cut off from decision-making – political control over lawmaking would still be maximized, but technical consistency and speed could be subject to bureaucratic strife. If presidents have weak legislative and organizational powers, policymaking would be decentralized and managed in an adversarial or collegial way: presidents would have to reach consensus both within their branch and with the legislature and possibly interest groups – technical consistency and bureaucratic alignment with policies would be maximized, but political control would be weaker. Table 1 sums up the theoretical expectations of Executive organization and managerial styles of presidents in crisis economic policymaking.

Table 1 – Cognitive Contexts, Institutional Capacity and Executive Organization and Management in Crisis Economic Policymaking

Cognitive Contexts Institutional Capacity of the Presidency Strong

Legislative & Organizational

Powers

Strong Legislative Power &

Weak Organizational

Power

Weak Legislative and Organizational Power

Uncertain Centralized organization; competitive

management

Moderately decentralized organization; competitive

management

Decentralized organizational; collegial

management

Certain Centralized organizational;

hierarchical management

Moderately decentralized organization; hierarchical

management

Decentralized organization; competitive

management

To explore the empirical pertinence of these theoretical arguments, this paper engages in the comparative process tracing of the crafting of responses to economic crises. The independent variables are the cognitive context and the institutional capacity of the presidency. The cognitive context is operationalized using the country’s experience with economic instability: the more experience, the less likely for policymakers to perceive an economic crisis situation as uncertain; the less experience with instability, the more likely for economic crises to be perceived as uncertain situations by policymakers. Annual variations of gross domestic product (GDP) and consumer price indexes (CPI) are employed as indicators: the higher and more frequent the variations, the more experience with economic instability.

The institutional capacity of the presidency is operationalized using the legislative and organizational powers of the presidency: the stronger these powers, the greater the institutional capacity of the presidency, and thus the president’s ability to concentrate, centralize, and control decision-making. The indicators for legislative power are the veto and decree powers. Following Shugart and Haggard (2001) veto powers are classified as strong if presidents possess both total and item veto, and a qualified majority is required for congressional repeal; and they are deemed weak if

7

presidents only have total veto power and/or face non-qualified majority requirements for congressional repeal. Decree powers are classified as strong if presidential decrees have immediate force of law and do not require congressional ratification; as intermediate if they have immediate force of law but require congressional ratification; as weak if their validity depends on congressional ratification; and as null if they are not contemplated in the constitution (ibid.; Amorim Neto 1998). The indicators for organizational power are the president’s ability to unilaterally a) issue decrees and bills on Executive organization, b) create and eliminate cabinet positions and administrative agencies, c) appoint leading cabinet members, and d) appoint central bank presidents and/or directors. If presidents have all these capacities, their organizational power is deemed strong; if they can create and eliminate positions and agencies and appoint their staff alone, but cannot issue decrees and bills on their own, their organizational power is classified as intermediate; and it is classified as weak if presidents do not possess any of these capacities.

The dependent variables are the organization of the economic policymaking process and the management style employed to operate this process. Following Rudalevige (2002: 19), an economic policymaking process is defined as centralized if led by centralized staff – i.e. by “staff whose only constituent (whether in stature or in practice) is the president himself, and which is organizationally (and normally, physically) proximate to him”. In contrast, a decentralized economic policymaking process would be led by decentralized staff – i.e. staff with more constituents than the president and less organizational proximity to them. This notion of centralization is hereby operationalized somewhat differently from Rudalevige’s study. Following this author’s lead, the centralized/decentralized nature of staff is identified here by looking into the institutional origin of the administrative units involved in the policymaking process; but whereas Rudalevige uses as indicator the “legislative pre-history” of presidential proposals as registered in the administration’s internal memos, for lack of comparable information for the cases analyzed here, this paper relies on participants’ testimonies and historical accounts. If at least 50% of available testimonies and accounts report one (set of) specific unit(s) as leading the policymaking process, and the unit(s) in question depend for their existence, staffing, and stability only on presidential decisions, the process is classified as centralized. If, in contrast, the existence, staffing, and stability of the unit(s) reported as leading the process depends jointly on presidential and congressional or constitutional decisions, then the policymaking process is classified as decentralized.

The management styles employed to operate the economic policymaking process are defined following Johnson (1974). The process is managed with a hierarchical style when the president delegates authority to top advisers (ministers or personal counselors) who run a hierarchical organization with clearly specified, differentiated functions, and who filter the information and policy alternatives that reach the presidential desk. The process is managed with a competitive style when the president stands at the center of units with overlapping jurisdictions, duplicates assignments, and develops rivalries amongst advisers and/or ministers. The process is managed with a collegial style when the president chairs debates of a group of advisers who collectively discuss and propose alternatives. Management styles are also identified according to participants’ testimonies and historical accounts: if more than 50% of available sources report the employment of one particular style, then the process is classified as managed with that style.

8

The cases selected for comparison are three federal presidential democracies: Argentina, Brazil, and the United States. The case selection is predicated on the variation in the independent variables: the cognitive contexts, indicated by their different historical experiences with economic instability; and the institutional capacity of the president, as indicated by the legislative and organizational powers of each Executive branch. The period under analysis is 1985-2009, when all three countries were continuously democratic. In this period, Argentina’s economy was the most unstable: the variation in its Consumer Price Index ranged from 3,079.5% in 1989 to -1.2% in 1999, back to over 23% since 2007; and the variation in its GDP ranged from -10.9% in 2002 to 9% in 2004. Brazil’s experience with instability was as extreme as Argentina’s in inflation, but not in GDP: the CPI ranged from 2,947.7% in 1990 to 3.2% in 1998, and the GDP varied between -4.4% in 1990 to 5.8% in 1994 and 2007. In contrast, the CPI in the United States varied between 6.1% in 1990 and 0.1% in 2008, and its GDP changed between 7.53% in 1988 and -1.2% in 2008 – making it the most stable of the three economies.3

Argentina also has the presidency with the strongest institutional capacity: its legislative powers are strong, insofar as presidents have both total and item veto power and strong decree power; and its organizational powers are intermediate, insofar as they can create and eliminate cabinet positions and administrative units as well as appoint their staff, but cannot issue decrees or bills alone (Bonvecchi and Zelaznik 2012). The Brazilian presidency has strong legislative powers but weak organizational powers. Presidents have total and item veto power, and are entitled to issue legislative decrees with immediate force – though conditions for their validity have changed since 1985: under the 1967 Constitution, which was in force until 1988, decrees were valid unless Congress rejected them within sixty days of issuance; between 1988 and 2001, decrees were valid for thirty days but could be indefinitely re-issued; since 2001, decrees only remain valid if Congress ratifies them within 30 days and can only be re-issued once (Figueiredo and Limongi 1999; Pereira and Mueller 2002; Santos 2003; Pereira et al. 2005). In the organizational arena, Brazilian presidents cannot issue decree or bills alone, nor create or eliminate cabinet positions and administrative units or appoint central bank staff, but they can unilaterally appoint their ministers and secretaries (Amorim Neto 2012). In contrast, the United States presidency has both weak legislative and organizational powers: in the legislative arena, US presidents only have total veto power and no decree power, though the President’s power to issue executive orders has been acknowledged by the Supreme Court and implicitly accepted by Congress on several occasions (Cooper 2002; Howell 2003); in the organizational arena, presidents have no legislative initiative and contested power of executive order (ibid.), cannot either create or eliminate cabinet positions and administrative units, and are unable to appoint cabinet secretaries or Federal Reserve board members without congressional approval (Lewis 2008).

Consequently, the expectations would be for more centralized organization of crisis economic policymaking managed with a hierarchical style to be found in Argentina; for a more decentralized organization managed with a collegial style to be found in the United States; and for Brazil’s organization of crisis economic policymaking to be moderately decentralized with management styles ranging from competitive to 3 The data for Argentina and Brazil are from ECLAC (CEPALSTAT); the data for the US CPI, from the Bureau of Labor Statistics; the data for its GDP, from the Bureau of Economic Analysis.

9

hierarchical. The next section compares the organization of the Executive and the management styles employed by presidents in all economic stabilization programs launched in these three countries between 1985 and 2009.

2. The General Patterns.

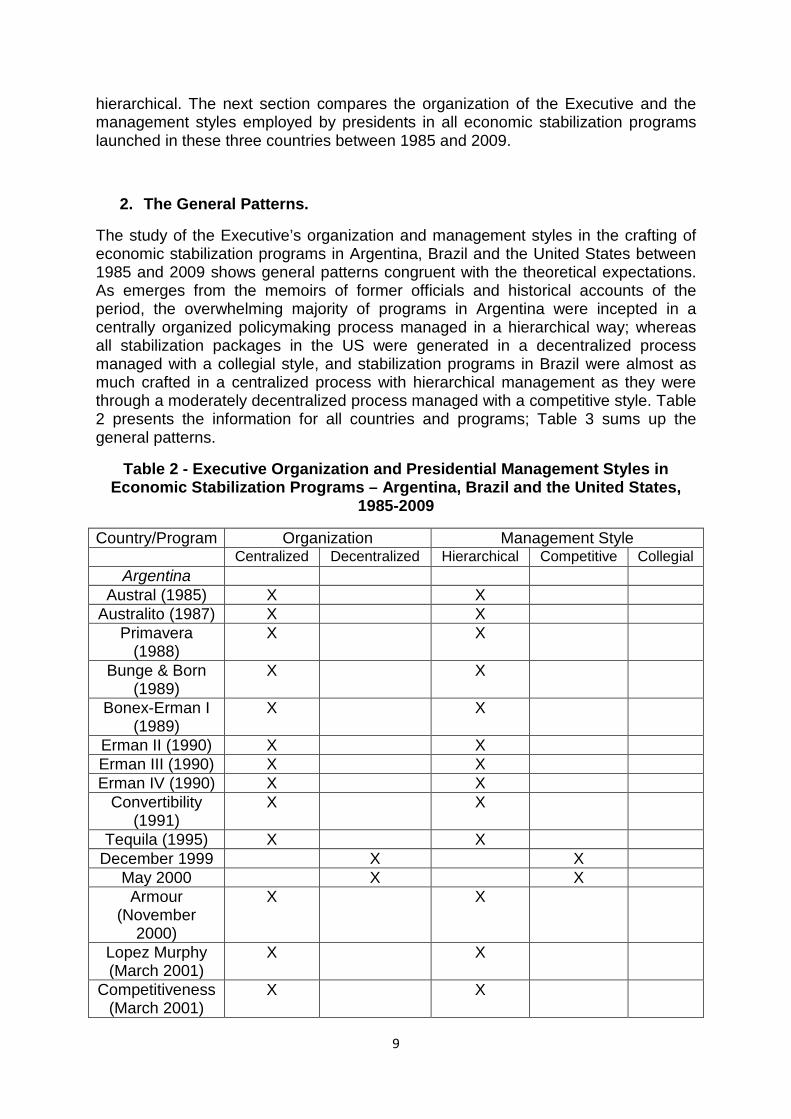

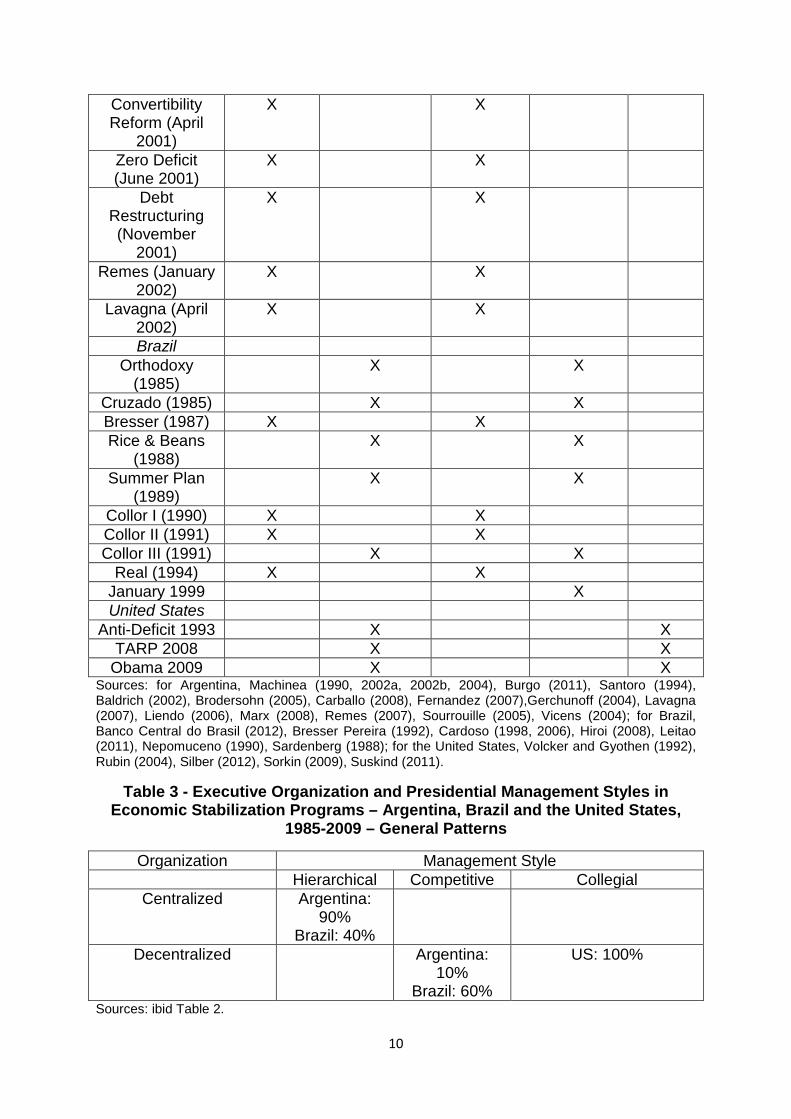

The study of the Executive’s organization and management styles in the crafting of economic stabilization programs in Argentina, Brazil and the United States between 1985 and 2009 shows general patterns congruent with the theoretical expectations. As emerges from the memoirs of former officials and historical accounts of the period, the overwhelming majority of programs in Argentina were incepted in a centrally organized policymaking process managed in a hierarchical way; whereas all stabilization packages in the US were generated in a decentralized process managed with a collegial style, and stabilization programs in Brazil were almost as much crafted in a centralized process with hierarchical management as they were through a moderately decentralized process managed with a competitive style. Table 2 presents the information for all countries and programs; Table 3 sums up the general patterns.

Table 2 - Executive Organization and Presidential Management Styles in Economic Stabilization Programs – Argentina, Brazil and the United States,

1985-2009

Country/Program Organization Management Style Centralized Decentralized Hierarchical Competitive Collegial

Argentina Austral (1985) X X

Australito (1987) X X Primavera

(1988) X X

Bunge & Born (1989)

X X

Bonex-Erman I (1989)

X X

Erman II (1990) X X Erman III (1990) X X Erman IV (1990) X X

Convertibility (1991)

X X

Tequila (1995) X X December 1999 X X

May 2000 X X Armour

(November 2000)

X X

Lopez Murphy (March 2001)

X X

Competitiveness (March 2001)

X X

10

Convertibility Reform (April

2001)

X X

Zero Deficit (June 2001)

X X

Debt Restructuring (November

2001)

X X

Remes (January 2002)

X X

Lavagna (April 2002)

X X

Brazil Orthodoxy

(1985) X X

Cruzado (1985) X X Bresser (1987) X X Rice & Beans

(1988) X X

Summer Plan (1989)

X X

Collor I (1990) X X Collor II (1991) X X Collor III (1991) X X

Real (1994) X X January 1999 X United States

Anti-Deficit 1993 X X TARP 2008 X X

Obama 2009 X X Sources: for Argentina, Machinea (1990, 2002a, 2002b, 2004), Burgo (2011), Santoro (1994), Baldrich (2002), Brodersohn (2005), Carballo (2008), Fernandez (2007),Gerchunoff (2004), Lavagna (2007), Liendo (2006), Marx (2008), Remes (2007), Sourrouille (2005), Vicens (2004); for Brazil, Banco Central do Brasil (2012), Bresser Pereira (1992), Cardoso (1998, 2006), Hiroi (2008), Leitao (2011), Nepomuceno (1990), Sardenberg (1988); for the United States, Volcker and Gyothen (1992), Rubin (2004), Silber (2012), Sorkin (2009), Suskind (2011).

Table 3 - Executive Organization and Presidential Management Styles in Economic Stabilization Programs – Argentina, Brazil and the United States,

1985-2009 – General Patterns

Organization Management Style Hierarchical Competitive Collegial

Centralized Argentina: 90%

Brazil: 40%

Decentralized Argentina: 10%

Brazil: 60%

US: 100%

Sources: ibid Table 2.

11

Twenty stabilization programs were introduced in Argentina between 1985 and 2002. In all but two of these programs, the economic policymaking process was dominated by the Economy Ministry, with the Central Bank playing a secondary but significant role. The formulation and launching of all the stabilization packages delivered by the Executive in this period were delegated by the President to the Economy Ministry – which also played the leading, albeit not exclusive, part in their implementation. The Central Bank was, through its president and/or directors, an important player in the formulation of all stabilization programs until December 1999, when the economic team of the Alliance government, faced with a Central Bank president appointed by the previous administration and whose independence was protected by statute, chose to exclude him from the preparation and launching of its policies – a practice maintained by the Duhalde administration in the 2002 stabilization packages. The two exceptions to this policymaking process centralized in, and hierarchically managed by, the Economy Ministry were the December 1999 and May 2000 packages of the Alliance government – the formulation of which included a large set of political actors: the President, the Vicepresident, the ministers of Defense, Justice, and Education, and the coalition’s parliamentary leaders in the Budget Committees of both houses of Congress (Quintana 2013). The team at the Economy Ministry was the first mover, but all these political actors made significant inputs (Machinea 2002a, 2002b, 2004).

The Argentine patterns are consistent with the theoretical expectations about the effects of cognitive contexts and institutional capacities of the presidency. As already noted, Argentina’s experience with economic instability has been extensive in frequency and content: both inflation and output have varied significantly and frequently in the period under analysis. The Argentine Executive is institutionally empowered to issue legislative decrees on all matters of economic policy (except taxation, but only since the constitutional ban introduced in 1994) and possesses both total and partial veto power – which can only be overturned by a qualified majority of two-thirds of Congress’ membership (Garcia Montero 2009). The presidency can shape the cabinet’s composition and jurisdictions unilaterally – organizational powers which it used to give the Economy Ministry jurisdiction over budgetary policy, as well as the direction of agricultural, industrial, and trade policy until 2002, when the first two were transferred to the Production Ministry and subsequently transformed into ministerial offices. The cognitive disposition and institutional capacity of the presidency in Argentina thus bred an economic policymaking process in times of crisis organized in a centralized way, and managed with a hierarchical style by the Economy Ministry – in which presidents typically delegate responsibility.

Control over Brazil’s economic policymaking process since the beginning of the current democratic period in 1985 has been shared between the Finance Ministry and other Executive agencies. Of the ten stabilization programs put forward between 1985 and 1999, only four were conducted exclusively by the Finance Ministry (Bresser in 1987; Collor I in 1990; Collor II in 1991; and Real in 1994); the six remaining packages were all formulated, launched, and implemented by teams made up not only of Finance Ministry top brass, but also of Planning Ministry officers, Central Bank directors, Treasury secretaries, General Legal Counsel, presidential advisers, and members of the National Monetary Council (Leitao 2011). While the Finance Ministry had the leading role in program launching and implementation, the formulation process also involved other Executive units: the Planning Ministry, in

12

charge of designing the country’s development strategy since the 1950s; the Central Bank – formally independent from government since 1988, though effectively so only since 1995 (Hiroi 2008); and the National Monetary Council, a collective body in charge of determining the size and evolution of the money supply, made up of directors from the Central Bank, the Finance, Planning, Industry, Agriculture, Infrastructure, Interior, Urban Development, Labour, and Social Welfare ministries, the heads of the main public banking institutions (BNDES, Banco do Brasil, Banco da Amazonia, Banco do Nordeste do Brasil, Banco Nacional de Habitacao, Caixa Economica Federal, Instituto de Reaseguros do Brasil, and the Commissao de Valores Mobiliarios), plus representatives of business associations and the union movement (Banco Central do Brasil 2012). However, this pattern of decentralized policymaking crafted by competitive units gradually shifted to greater centralization and hierarchical control by the Finance Ministry since the 1994 Real Plan (Cardoso 1998, 2006).

Brazil’s patterns are also consistent with theoretical expectations. In terms of cognitive contexts for economic decision-making, as noted above, the country’s experience with economic instability has been mixed: highly volatile inflation rates in the 1980s to mid-1990s, but less volatility in output results. The institutional capacity of the presidency is strong in legislative powers but weak in organizational powers. The Brazilian Executive can issue legislative decrees on most aspects of economic policy – except taxation and the annual national budget – but unlike the Argentine Executive’s decrees, the Brazilian president’s Medidas Provisorias are only valid for specific time periods and expire unless explicitly ratified by Congress – which grants legislators bargaining power over the nature and cost distribution of economic policies (Figueiredo and Limongi 1999; Pereira and Mueller 2002; Santos 2003; Pereira et al. 2005). In organizational terms, the Brazilian president can unilaterally appoint and dismiss its cabinet ministers, but not the Central Bank or Monetary Council boards. This resulted in fiscal policy being under jurisdiction of the Finance Ministry since 1986, but monetary policy always being shared with the Central Bank and the National Monetary Council (though under the direction of the Central Bank since 1995), and development planning with the Planning Ministry (Hiroi 2008). The cognitive disposition and institutional powers of the presidency thus bred an economic policymaking process organized in a moderately decentralized way that could be managed either with a competitive style by the president or with a hierarchical style through the Finance Ministry.

The three policy packages set up in response to economic crises in the United States in the past two decades – the 1993 Anti-Deficit program, the 2008 TARP, and the 2009 Obama administration’s response to the crisis – were incepted in a decentralized decision process managed in a collegial style. The economic policymaking process in these cases was a joint enterprise of the Treasury Department, the Federal Reserve Board (FRB), the National Economic Council (NEC), the Council of Economic Advisers (CEA), and the leaderships of the specialized committees in Congress. While the Treasury Department is statutorily the main player in the formulation stage, it was not the leader of the decision process: it shared the formulation stage with the FRB and the NEC, the launching stage with the FRB and Congress, and the implementation stage with the FRB and some of the cabinet departments represented in the NEC (State, Agriculture, Commerce, the Office of Management and Budget, and the United States Trade Representative) (Destler 1996; Morris 2002; Sorkin 2009; Suskind 2011). Presidents

13

– strong and weak, incoming and outgoing – were neither hierarchical nor competitive managers of economic policymaking, but conductors of multiple advocacy debates.

These patterns also correspond to expectations about cognitive contexts and institutional power of the presidency. The country’s experience with economic instability in the period under analysis was scarce: there was little volatility in both inflation and output, so the cognitive contexts in which these policy packages were crafted were contexts of uncertainty. In terms of institutional capacity, the United States presidency is both legislatively and organizationally weak. In the legislative arena, it has no recognized decree power,4 possesses only a total veto power, and lacks the power to initiate legislation, so Congress is the main actor in the legislative process. In the organizational arena, the president lacks the power to unilaterally appoint cabinet or Federal Reserve members, shape their jurisdictions, and so forth, so the powers of all the administrative units in charge of economic policymaking have been defined jointly with Congress. Thus, the Treasury is in charge of general macroeconomic policy, but its formulation process also involves the director of the National Economic Council and the Council of Economic Advisers. The FRB is in charge of monetary policy, but under the supervision of the Banking and Finance Committees of the Senate and the House of Representatives. The CEA is a group of experts who directly advise the White House on economic policy affairs independently of other Executive agencies. The NEC is in charge of coordinating economic policymaking, for which it must bring together the aforementioned departments plus Housing and Urban Development, Labor, Energy, Transportation, and Health, the Environmental Protection Agency, and the President’s Special Assistants for National Security, Domestic Policy, and Science and Technology Policy. This cognitive and institutional setting thus bred an economic policymaking process in times of crisis marked by a decentralized organization managed with a collegial style.

The comparison of these general country patterns indicates support for the theoretical expectations about the effects of cognitive contexts and institutional capacities of the presidency in the organization and management of economic policymaking in times of crisis. However, the country patterns also show the existence of variations in Argentina and Brazil, and stability in the United States. The next section looks into these divergent experiences by comparing the crafting of responses to economic crises within each country.

3. Within-Country Comparisons.

The comparison of the Executive’s organization and management styles in the crafting of responses to economic crises across stabilization programs in Argentina, Brazil, and the United States suggests the weight of cognitive contexts may be greater than that of the institutional variables in each country’s experience. This, as discussed below, would be consistent with the theoretical intersection between the

4 However, the President’s power to issue executive orders has been acknowledged by the Supreme Court and implicitly accepted by Congress on several occasions (Cooper 2002; Howell 2003), which has given the President the institutional advantage to move first to set the agenda and reform policy away from the status quo and closer to his preferences (Moe and Howell 1999; Howell 2003).

14

literature on presidential management styles and the works on decision-making in economic adjustment processes.

3.1. Argentina.

Eighteen out of twenty stabilization programs set in motion in Argentina since 1985 were formulated through a centralized decision-making process managed hierarchically by the Economy Ministry. In contrast, the two policy packages put together by the Alliance government in December 1999 and May 2000 were incepted through a decentralized process managed by the presidency in a competitive way. These exceptions also stand out considering the programs developed by the same administration in subsequent months were crafted in the usual centralized policymaking process managed hierarchically by the Economy Ministry, and no institutional innovation in the capacities of the presidency was introduced in between. The accounts of former officials suggest a cognitive explanation: policymakers viewed crisis situations as certain throughout the period, except in the early months of the Alliance government – when the Convertibility regime was starting to collapse.

The two main anti-inflationary programs in the period were born out of extensive theoretical debates and empirical analyses developed by economists who were academically trained in the study of high inflation and exchange-rate-based stabilization. The Austral Plan, a heterodox anti-inflationary package that significantly curbed inflation from mid-1985 to late-1986, was designed by a team of economists who had hitherto devoted their academic careers to studying the flaws of orthodox stabilization efforts and the mistakes of previous heterodox programs: Minister J. Sourrouille and Treasury Secretary M. Brodersohn had investigated the political problems underpinning the failure of previous stabilization plans (Mallon and Sourrouille 1973; Brodersohn 1972); Central Bank president J.L. Machinea had studied the pitfalls of exchange-rate-based stabilizations (Machinea 1982); senior adviser R. Frenkel had theorized the problems of stabilization under contractually-based inflationary inertia (Frenkel 1978); and senior adviser D. Heymann had investigated the macroeconomic conditions for stabilization in high-inflation economies (Heymann 1983). The Convertibility Plan, which eventually succeeded in ending hyperinflation in 1991, was prepared by three people with extensive study about the problems of high inflation and stabilization: Economy Minister D. Cavallo had investigated the role of interest-rate control and monetary creation in stabilization programs (Cavallo 1977); Economic Programming Secretary J. Llach had written thoroughly on stabilization programs in hyperinflationary economies (Llach 1987, 1990); and senior adviser H. Liendo had developed a treatise on the legal conditions for successful stabilization (Liendo 1990). The testimonies of both teams’ members indicate their academic background was crucial for their perception of the crisis: based upon the studies and debates in which they had engaged within the academic community, these policymakers presented themselves as certain about the nature of the crisis with which they had to deal (Machinea 1990, 2002a, 2002b, 2004; Sourrouille 2005; Brodersohn 2005; Santoro 1994; Dellepiane 2005; Llach 2006; Liendo 2006; Burgo 2011). In other words, these policymakers appeared to know what to do with the economy, and were able to convey their perception of certainty to their presidents to the extent that they gave them hierarchical control over a centralized policymaking process.

15

This perception of certainty seems to be absent from the inception of the first two programs developed by the Alliance government. While senior policymakers such as Economy Ministry Machinea and Chief Adviser P. Gerchunoff had written noteworthy pieces on the challenges of economic policymaking under the Convertibility regime (Machinea and Gerchunoff 1994; Gerchunoff and Canovas 1995), there was comparatively scarcer reflection on how to manage a combination of fiscal and financial crisis under this exchange-rate regime. As Machinea recalled it, a double-edged crisis would simultaneously bankrupt the public and private sectors, the banks and the families, because lack of confidence would trigger a banking crisis, the banking crisis would deplete the Central Bank reserves and force devaluation, and devaluation would bankrupt everyone via the sudden increase in domestic currency of the cost of honoring dollar-denominated debts (Machinea 2002a, 2002b, 2004). No such situation had been experienced in Argentina before, so not only economic policymakers but also President F. de la Rua felt wary of trying any measures that could activate any of these triggers (ibid.; Gerchunoff 2005). This perception of uncertainty about the nature of the situation may explain the president’s decision to set up a decentralized decision-making process in which the Economy Ministry’s proposals were extensively debated by other cabinet members and Congressional leaders both before launching and during implementation (ibid.).

In contrast, the programs launched by the same administration between November 2000 and November 2001 appear to have been crafted in a cognitive context of certainty. The Armour Plan, which attempted in November 2000 to stop the financial crisis of the Convertibility regime through massive aid by the IMF, the World Bank and foreign investors, was set up and hierarchically managed by Economy Minister Machinea after thorough discussions with US Treasury Secretary L. Summers under the Clinton administration’s policy framework of pre-emptive bailouts (Machinea 2004; Marx 2008; Vicens 2004; Gerchunoff 2004; Gadano 2004). Minister Cavallo’s Convertibility Reform Plan of March-April 2001 recycled the idea for a currency basket to deal with competitiveness problems Cavallo himself had devised and proposed to President C. Menem in 1992 (Cavallo 2001, 2004; Liendo 2006; Marx 2008; Burgo 2011). And Cavallo’s Zero Deficit and Debt Restructuring plans of June and November 2001 recast the combination of fiscal adjustment and debt rescheduling with which Cavallo’s team had fought the 1995 financial crisis (ibid.). In all these episodes, just like in the Austral and Convertibility Plans, policymakers seemed certain about the nature of the crisis and were able to successfully convey their certainty to the president so that they obtained authority to hierarchically manage a centralized policymaking process.

3.2. Brazil.

Of the ten stabilization programs incepted in Brazil since 1985, two introduced innovations in the conceptualization and execution of anti-inflationary policy: the Plano Cruzado in 1986, and the Plano Real in 1994. Both programs departed from orthodox approaches to stabilization and addressed the challenges of stopping high inflation in the same manner, but differed significantly in the organization and management of their inception and implementation. While the Cruzado was formulated in a moderately decentralized setting managed in a competitive way, the Real was developed in a more centralized, hierarchically managed decision process.

16

This difference appears as noteworthy considering that the institutional innovations introduced in the 1988 Constitution reduced, rather than increased, the unilateral powers of the presidency. Testimonies and accounts from former officials suggest a cognitive explanation instead: the main policymakers were uncertain about the effects and the practical problems of implementation of heterodox stabilization measures in the Plano Cruzado, but had learnt how to overcome them in the Real.

The Cruzado Plan, announced in February 1986, was developed in a context of uncertainty through a protracted debate which began in academia in late 1984, and continued in government all through 1985 without political supervision from the Presidency until just a few weeks before its launching. The debate started as an intellectual discussion on the feasibility of fighting inflation via monetary reform among a series of economists: academics P. Arida, A. L. Resende, F. Lopes and E. Bacha at the Catholic University in Rio de Janeiro; and L. Gonzaga Belluzo, M. Tavares and J. Cardoso de Mello, economic advisers to the incoming democratic transition president of Brazil, T. Neves. The discussion continued within government, with the aforementioned economists employed as advisers at the Central Bank and the Planning Ministry, and with the added participation of Planning Ministry J. Sayad and Finance Minister D. Funaro, as a practical debate on how the stabilization program could avoid regressive income redistribution. This collective thinking process was finalized in late February 1986 in a series of discussions amongst all participants, plus Central Bank President F. Bracher, held under the supervision of presidential adviser J. Murad, who adjudicated the debate on income redistribution effects by imposing a positive wage adjustment before launching the program (Sardenberg 1988; Nepomuceno 1990). Although Brazil had had, by 1986, a long experience with inflation and stabilization programs (Baer 1995; Da Fonseca 1998), none of the previous packages had been designed as a heterodox shock structured on the basis of a monetary reform oriented to immediately stopping inflation without causing a recession or negative income redistribution (Arida and Resende 1985). Consequently, both economists and politicians treated the economic situation and the ideas informing the Plano Cruzado as sources of uncertainty. In other words, neither the policymakers nor the politicians knew exactly how economic actors would react to the Plano. This cognitive disposition led President J. Sarney to set up a competitive policymaking process within which the advantages, pitfalls, and potential side effects of these novel policy proposals could be extensively discussed.

In contrast, the Real Plan was incepted in a context of certainty, in a considerably shorter period of time, by a considerably smaller group of economists hierarchically managed by Finance Minister F. H. Cardoso. Between late May and August 1, 1993, Cardoso’s team – Bacha, G. Franco, W. Frisch, C. Carvalho, P. Malan, Arida, Lara Resende, and Lopes – discussed in secrecy a new anti-inflationary program based upon monetary reform that would avoid what the team perceived to have been the mistakes in design – previous wage adjustment – and execution – lack of spending and monetary control – made during the Plano Cruzado, all the while Cardoso maneuvered to place his advisers in key positions at the Central Bank, the Planning Ministry, and the foreign debt negotiation team (Cardoso 1998; Leitao 2011). The centralized organization of the policymaking process and the hierarchical management of Minister Cardoso appear to have been the outcomes of learning from the experience of the Plano Cruzado. The policymakers in Cardoso’s team, which included some of the founding fathers of the Plano Cruzado, seemed to have learnt which heterodox policy tools were apt for re-use – namely, monetary reform –

17

and which implementation problems had to be avoided – i.e. lack of control over spending and debt management (Leitao 2011). Cardoso himself, who had been a senator in the Budgetary Committee during the Plano Cruzado, appeared to have learnt that a centralized decision process hierarchically managed by the Finance Minister would be instrumental for maintaining technical consistency and insulating the program’s design from political pressures that could derail it from its very inception (Cardoso 1998, 2006). This conceptual and practical learning constituted a cognitive context of certainty strong enough for Cardoso to convince President I. Franco to appoint members of the economic team to key positions in the Central Bank, the Treasury Secretary, and the foreign debt renegotiation unit – which gave the team authority and opportunity to gather and analyze critical information to help them implement the program and deal with other ministries and Congress (ibid.). In short, learning from past experience enabled policymakers to perceive the crisis context as certain, and to obtain from political leaders the power to organize a centralized policymaking process hierarchically managed by the economic team.

3.3. United States.

The three main policy packages set up in response to economic crises in the US in the past two decades were formulated in a decentralized decision process managed with a collegial style. Testimonies from policymakers and historical accounts depict these patterns of organization and management as responses to situations perceived as uncertain. The weight of uncertainty as an explanatory factor is enhanced by the absence of innovations in the institutional capacity of the presidency during the period.

The 1993 Anti-Deficit program with which the Clinton administration began its tenure was prepared by officials representing the Treasury Department (Secretary L. Bentsen and Undersecretaries R. Altman and L. Summers), the Office of Management and Budget (OMB Director L. Panetta and Deputy Director A. Rivlin), the Council of Economic Advisers (L. D’Andrea Tyson and A. Blinder), and the National Economic Council (chairman R. Rubin and deputy chairman G. Sperling). This council was a brand new unit explicitly created by President Clinton to organize economic policymaking by acting as an honest broker that would bring together before the President the advice of all Executive agencies concerned with economic issues, and would coordinate discussion of the political dimensions of policy proposals with the White House’s political advisers (Rubin 2004: 109-118). The NEC, however, was not an organizational innovation: the Economic Policy Board established during the Ford administration was its functionally equivalent predecessor (Porter 1988). But Clinton’s decision to create the NEC was explicitly shaped by the incoming Democratic administration’s concern that it was facing the dual challenge of closing a significant fiscal gap, and establishing a reputation for sound economic policymaking with economic policymakers mostly inexperienced in government (Rubin 2004). In other words, uncertainty about the effectiveness of proposed measures and the competence of policymakers seems to have induced the president to set up a decentralized process managed collegially in order to thoroughly confront and discuss information and policy advice.

18

Uncertainty also appears to have marked the development of responses to the Great Recession of 2008-2009. In late 2008 and early 2009, the economic teams of the Bush II and Obama administrations were confronted with a crisis the complexity and extent of which was unknown to any contemporary economic policymaker – so much so that not even the seasoned officials in both teams had the experience or the specialized knowledge to resort to (Paulson 2010; Suskind 2011). Consequently, again in these cases the policymaking process was organized in a decentralized manner and managed in a collegial way. The Troubled-Assets Recovery Program (TARP) put together in October 2008 by the outgoing Bush II administration was developed by the joint effort of teams in the Treasury Department, the Federal Reserve Bank of New York, and the chairman of the Federal Reserve Board, coordinated by Treasury Secretary H. Paulson (Sorkin 2009), who kept President Bush informed though without submitting policy alternatives to him (Pfiffner 2011). The Obama administration’s crisis response package, made up of the stimulus bill and the stress tests for banks, was formulated through a protracted process coordinated by NEC chairman L. Summers and White House Chief of Staff R. Emanuel which also involved Treasury Secretary T. Geithner, CEA Director C. Romer, Federal Reserve Board chairman B. Bernanke, and Congressional leaders from specialized committees (Suskind 2011; Pfiffner 2011). In short, US presidents seemed to have perceived economic crisis situations as highly uncertain, to have organized the economic policymaking process in a decentralized way so as to incorporate all relevant Executive agencies in the crafting of each program, and to have managed it a collegial way in order to make sure that all information and policy options available were presented and discussed.

3.4. Discussion.

These within-country comparisons suggest a primacy of cognitive contexts as explanatory factors of the organization and management of policymaking in response to economic crises. When policymakers perceive economic contexts as uncertain, they resort to decentralized arrangements to organize the policymaking process and to collegial or competitive styles to manage it. In contrast, when policymakers perceive economic contexts as certain, they resort to centralized arrangement of policymaking and typically use hierarchical management styles. These choices of organization and management style seem to be independent of the institutional capacities of the presidency: shifts to and from centralized organizational arrangements and hierarchical management styles have occurred in countries with different levels of institutional capacity, some not akin to such organization and management style, and regardless of the stability in presidential capacities.

This primacy of cognitive contexts relative to institutional capacities in the shaping of the Executive’s organization and management of responses to economic crises stands at the intersection of the theoretical contributions of US presidential studies and the literature on decision-making in economic adjustment processes. The works of Burke and Greenstein (1989) about decision-making on Vietnam, Wallcot and Hult (1995) about White House organization, Ponder (2000) about staff management, and Preston (2001) about foreign policy decision-making show presidents adapt the organization of policymaking processes and the style with which they manage their staff according to their perception of contexts. The works of Weyland (1996, 1998,

19

2002) about the politics of market reform in Latin America show that presidents choose both their policies and the tools to enact and implement them according to their perception of risk. These literatures intersect precisely at this point: perceptions of context drive presidential decisions on all aspects of policymaking – organizational arrangements, management styles, and institutional tools. Presidents respond to economic crisis deciding first what the nature and stakes of the context are, and subsequently adapting their government’s organization, management, and institutional capacities to rise to those stakes.

The findings arising from these comparisons therefore have at least two relevant implications for the literature on presidential decision-making. On the one hand, they challenge the institutional argument of Haggard and Kaufman (1992a, 1992b, 1992) that presidential choices for unilateral or consensual decision-making are driven by their constitutional and partisan powers. More akin to Amorim Neto’s (1998) argument, presidential decision-making in response to economic crises appears to be shaped by the nature of context as well – only perception of context seems to have causal precedence to other factors, rather than equal footing. On the other hand, the comparative findings in this paper challenge the cognitive argument of Weyland (1996, 1998, 2002) that risk-taking in the domain of losses takes the form of unilateral, top-down decision-making. This only appears to be the case when policymakers perceive situations as certain and are consequently confident they know what to do about them. All in all, then, these findings suggest the inner workings of presidential decision-making should not be taken as thoroughly determined by institutions or economic incentives: perceptions of context may be driving decisions, and may be marked by cognitive, rather than economic, factors.

4. Towards a Research Agenda.

The patterns of organization and management of economic policymaking in times of crisis identified in this paper suggest that Executives in Argentina, Brazil, and the United States deal differently with the tradeoffs between information processing and political control over policymaking. The US presidents organize their decision processes and manage their staff with the aim of maximizing information processing rather than political control. In contrast, the Argentine and Brazilian Executives organize decision-making and manage their staff with the aim of maximizing political control rather than information processing. These differing patterns appear to be driven by varying cognitive contexts. The more familiar experience with economic instability in Argentina seems to induce presidents to perceive crisis situations as certain and to organize their policymaking process in a centralized, hierarchically managed way. The reverse would be the case in the United States: the infrequent experience with economic instability seems to induce presidents to perceive its occurrence as an uncertain situation, and to respond by organizing their policymaking process in a decentralized, collegially managed way. The case of Brazil, more familiar with economic instability than the United States but less familiar with heterodox stabilization ideas and programs than Argentina, appears to reinforce these points: Brazilian presidents chose decentralized organization and collegial management of policymaking when uncertain about the potential effects of novel policy ideas, and resorted to centralized organization and competitive management when learning from experience made the use of policy instruments more certain.

20

The above conclusions are limited by at least three problems. First, the sample size: the analysis is circumscribed here to three countries with similar institutions, and to crisis economic policymaking. To test the validity of these arguments and findings it would be necessary to extend the study to countries with different institutions, and to ordinary, non-crisis economic policymaking. Are responses to crises in unitary, parliamentary countries crafted using similar organization and management styles according to cognitive contexts? Is ordinary economic policymaking organized and managed equally or different from crisis decision-making? Larger comparisons would be required to answer these questions.

Second, the nature of the evidence: the analysis here relies on testimonies and accounts that may misrepresent the nature of decision processes. To overcome this problem, more objective measures and indicators may be used – such as network data on the intervention of actors and units in decision-making. This would require accessing internal Executive documents on the preparation of stabilization programs, or press information depicting connections during the formulation and implementation stages. To what extent do ministers, secretaries and advisers intervene in policymaking? What is the influence of legislators and pressure groups and how can it be assessed? Network analysis and/or more in-depth case studies would be necessary to tackle these issues.

Finally, the scope of the analysis: this paper focuses on the formulation of stabilization programs, which leaves aside their launching and implementation stages. Do presidents/prime ministers employ different organizational arrangements and management styles in subsequent policymaking stages? Do organization and styles in launching and implementation vary according to cognitive contexts as much as in the formulation stage, or is variation more driven by the capacities of the presidency and/or other institutional factors? More extensive comparison and process-tracing of stabilization cases must be done to sort out these matters.

Bibliography

1. Books and Articles.

Amorim Neto, O. (2006): Presidencialismo e Governabilidade nas Americas, Rio de Janeiro, Konrad Adenauer Stiftung-Fundacao Getulio Vargas.

Arida, P. and Resende, A.L. (1985): “Inertial Inflation and Monetary Reform”, in J. Williamson (ed.): Inflation and Indexation: Argentina, Brazil and Israel, Washington DC, Institute for International Economics.

Baer, W. (1995): The Brazilian Economy: Growth and Development, Westport, Praeger.

Banco Central do Brasil (2012): Histórico da composição do Conselho Monetário Nacional (CMN), in http://www.bcb.gov.br/Pre/CMN/composi%C3%A7%C3%A3o_CMN.pdf

Bonvecchi, A. and J. Zelaznik (2012): “Recursos de Gobierno y Funcionamiento del Presidencialismo en Argentina”, in J. Lanzaro (ed.): Presidencialismo y Parlamentarismo Cara a Cara. Estudios sobre presidencialismo, semi-

21

presidencialismo y parlamentarismo en América Latina y Europa Meridional, Madrid, Centro de Estudios Políticos y Constitucionales: 63-102.

Burgo, E. (2011): 7 Ministros. La Economia Argentina: Historias debajo de la Alfombra. Buenos Aires: Planeta.

Burke, J.P. (2000): The Institutional Presidency. Organizing and Managing the White House from FDR to Clinton - Second Edition. Baltimore, Johns Hopkins University Press.

Burke, J.P. (2009): “Organizational Structure and Presidential Decision Making”, in Edwards, G.C. and Howell, W.G. (eds.): The Oxford Handbook of the American Presidency, Oxford, Oxford University Press: 501-527.

Burke, J.P. and Fred Greenstein (1989): How Presidents Test Reality: Decisions on Vietnam 1954 and 1965, New York, Russell Sage Foundation.

Cardoso, F.H. (1998): O Presidente Segundo O Sociologo: Entrevista de Fernando Henrique Cardoso a Roberto Pompeu de Toledo, Sao Paulo, Companhia das Letras.

Cardoso, F.H. (2006): A Arte da Politica, Rio de Janeiro, Civilizacao Brasileira.

Cavallo, D.F. (1977): “Los efectos recesivos e inflacionarios iniciales de las políticas monetarias de estabilización”. Jornadas de Economia Monetaria y Sector Externo, Banco Central de la Republica Argentina.

Cooper, P.J. (2002): By Order of the President. The Use and Abuse of Executive Direct Action, Lawrence, University Press of Kansas.

Da Fonseca, M.A.R. (1998): “Brazil’s Real Plan”, Journal of Latin American Studies, 30, 3: 619-640.

Dellepiane, S. (2005): The Political Economy of Institutional Credible Commitments: The Case of Argentina’s Convertibility Law (1991-2001), Ph.D. Dissertation, Colchester, University of Essex, Department of Government.

Destler, I.M. (1996): The National Economic Council: A Work in Progress, Washington DC, Institute for International Economics.

Drazen, A. (2000): Political Economy in Macroeconomics, Princeton, Princeton University Press.

Figueiredo, A. and F. Limongi (1999): Executivo e Legislativo na nova ordem constitucional, Rio de Janeiro: Editora FGV.

Garcia Montero, M. (2009): Presidentes y Parlamentos: ¿quién controla la actividad legislativa en América Latina?, Madrid: Centro de Investigaciones Sociologicas.

George, A. (1972): “The Case for Multiple Advocacy in Making Foreign Policy”, American Political Science Review, 66: 751-785.

Haggard, S. and R. Kaufman (1995): “The Challenges of Consolidation”, in Diamond, L. and Plattner, M.F., Economic Reform and Democracy, Baltimore, The Johns Hopkins University Press: 1-12.

22

Haggard, S. and R. Kaufman (1992a): “Institutions and Economic Adjustment”, in Haggard, S. and Kaufman, R. (eds.): The Politics of Economic Adjustment, Princeton, Princeton University Press: 3-37.

Haggard, S. and R. Kaufman (1992b): “The State in the Initiation and Consolidation of Market-Oriented Reform”, in Putterman, L. and Rueschemeyer, D. (eds.): State and Market in Development, London, Lynne Rienner, 1992: 221-240.

Hiroi, T. (2008): “Exchange Rate Regime, Central Bank Independence, and Political Business Cycles in Brazil”, Studies in Comparative International Development, 44: 1-22.

Howell, W.G. (2003): Power without Persuasion. The Politics of Direct Presidential Action. Princeton: Princeton University Press.

Johnson, R.T. (1974): Managing the White House. New York: Harper & Row.

Kahneman, D. and A. Tversky eds. (2000): Choices, Values, and Frames. New York: Russell Sage.

Knight, F. (1921): Risk, Uncertainty, and Profit. Boston, Houghton Mifflin Company.

Leitao, M. (2011): Saga Brasileira: A Longa Luta de Um Povo por Sua Moeda, Rio de Janeiro-Sao Paulo, Editora Record.

Liendo, H. (1990): Emergencia Nacional y Derecho Administrativo, Buenos Aires: Editorial Centro de Unión para la Nueva Mayoría.

Llach, J.J. (1987): Reconstruccion o Estancamiento. Buenos Aires: Tesis.

Llach, J.J. (1990): Las Hiperestabilizaciones sin Mitos. Buenos Aires: ITDT.

Luhmann, N. (1997): “Organización y Decisión”. In N. Luhmann: Organización y Decisión. Autopoiesis, Acción y Entendimiento Comunicativo. Barcelona, Anthropos-Universidad Iberoamericana: 3-98.

Luhmann, N. (1998): Sociología del Riesgo. Mexico, Triana-Universidad Iberoamericana.

Machinea, J.L. (1990): Stabilization under Alfonsin’s Government: A Frustrated Attempt, Buenos Aires, CEDES.

Machinea, J.L. (2002a): “Currency Crises: A Practitioner’s View”. In S. Collins and D. Rodrik (eds.): Brookings Trade Forum 2002. Washington DC, The Brookings Institution: 183-210.

Moe T. and W. Howell (1999): “Unilateral Action and Presidential Power: A Theory”, Presidential Studies Quarterly, Vol. 29, No. 4: 850-872.

Morris, I.L. (2002): Congress, the President, and the Federal Reserve, Ann Arbor, Michigan University Press.

Nelson, J., (1989): “The Politics of Long-Haul Economic Reform”, in Nelson, J. et al. (eds.): Fragile Coalitions: The Politics of Economic Adjustment, Oxford, Overseas Development Council: 3-26.

23

Nepomuceno, E. (1990): O Outro Lado da Moeda. Dilson Funaro: Historias Ocultas do Cruzado e da Moratoria. Sao Paulo: Edicoes Siciliano.

Pereira C. and B. Mueller (2002): “Comportamento Estratégico em Presidencialismo de Coalizão: As Relações entre Executivo e Legislativo na Elaboração doOrçamento Brasileiro”. Dados, vol. 45, 2: 265-301.

Pereira, C. et al. (2005): “Under What Conditions Do Presidents Resort to Decree Power? Theory and Evidence from the Brazilian Case”, Journal of Politics, Volume 67, Issue 1: 178–200.

Persson, T. and G. Tabellini (2000): Political Economics: Explaining Economic Policy. Cambridge, MA: MIT Press

Pfiffner, J.P. (2011): “Decision Making in the Obama White House”, Presidential Studies Quarterly, June 2011: 244-62.

Ponder, D.E. (2000): Good Advice. Information & Policy Making in the White House, College Station, Texas A&M University Press.

Porter, R.B. (1980): Presidential Decision Making: The Economic Policy Board. Cambridge: Cambridge University Press.

Preston, T. (2001): The President and His Inner Circle: Leadership Style and the Advisory Process in Foreign Affairs. New York: Columbia University Press.

Rogowski, R. (1989): Commerce and Coalitions, Princeton, Princeton University Press.

Rubin, R. (2004): In an Uncertain World. Tough Choices from Wall Street to Washington. New York: Random House.

Rudalevige, A. (2002): Managing the President’s Program. Presidential Leadership and Legislative Policy Formulation, Princeton, Princeton University Press.

Santoro, D. (1994): El Hacedor. Una biografía política de Domingo Cavallo, Buenos Aires, Planeta.

Santos, F. (1993): O Poder Legislativo no Presidencialismo de Coalizao. Rio de Janeiro: IUPERJ.

Sardenberg, C.A. (1988): Aventura e Agonia Nos Bastidores do Cruzado, Sao Paulo, Companhia das Letras.

Simon, H.A. (1978). “On how to decide what to do”. The Bell Journal of Economics, 9, 494-507.

Simon, H.A. (1997). Models of Bounded Rationality. Cambridge: The MIT Press.

Shugart, M. and S. Haggard (2001): “Institutions and Public Policy in Presidential Systems”, in S. Haggard and M. McCubbins (eds): Presidents, Parliaments, and Policy. Cambridge: Cambridge University Press: 64-102.

24

Sorkin, A.R. (2009): Too Big to Fail: The Inside Story of How Wall Street and Washington Fought to Save the Financial System---and Themselves, New York, Viking.

Suskind, R. (2011): Confidence Men: Wall Street, Washington, and the Education of a President, New York, Harper.

Walcott C.E. and Hult K.M. (1995): Governing the White House from Hoover to LBJ, Lawrence, University Press of Kansas.

Weyland, K. (2002): The Politics of Market Reform in Fragile Democracies: Argentina, Brazil, Peru, and Venezuela. Princeton: Princeton University Press.

Weyland, K. (1998): “The Political Fate of Market Reform in Latin America, Africa, and Eastern Europe”. International Studies Quarterly, 42, 4: 645-673.

Weyland, K. (1996): “Risk-Taking in Latin American Economic Restructuring”. International Studies Quarterly, 40, 2: 185-207.

2. Interviews.

Baldrich, J. (2002): Interview with author, Buenos Aires, 6/6/2002.

Brodersohn, M. (2005): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 12/8/2005.

Carballo, C. (2008): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 7/7/2008.

Fernandez, R. (2007): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 24/10/2007.

Gadano, N. (2004): Interview with author, Buenos Aires, 7/6/2004.

Gerchunoff, P. (2004): Interview with author, Buenos Aires, 5/6/2004.

Gonzalez Fraga, J. (2008): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 10/7/2008.

Lavagna, R. (2007): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 14/11/2007.

Liendo, H. (2006): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 30/8/2006.

Llach, J.J. (2006): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 11/13/2006.

Machinea J.L. (2002b): Interview with author, Washington DC, 30/12/2002.

Machinea, J.L. (2004): Interview with author, Santiago, 7/8/2004.

25

Marx, D. (2008): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 18/1/2008.

Remes, J. (2007): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 20/12/2007.

Sourrouille, J. V. (2005): Oral History Archive Interview, University of Buenos Aires, Buenos Aires, 14/9/2005.

Vicens, M. (2004): Interview with author, 8/5/2004.