Embed Size (px)

Citation preview

1

ALBA SE

Mid-year Financial Report ofALBA SE and its Affiliated

Subsidiaries (Group)

for the period January 1, 2016, through June 30, 2016

ALBA SE AG – Stollwerckstraße 9a – 51149 Cologne – Phone: +49 2203 9147-0 – Fax: +49 2203 9147-1394E-Mail: [email protected] – Internet: www.alba-se.com

2

Table of Contents

The Share .................................................................................................................................... 3

Interim Group Management Report

A. Basis of the Group ............................................................................................................ 4B. Economic Report .............................................................................................................. 5B.1. Sector-Related Framework Conditions.............................................................................. 5B.2. Changes in the Legal Framework Conditions.................................................................... 6B.3. Course of Business........................................................................................................... 6B.3.1. Steel and Metals Recycling............................................................................................... 6B.3.2. Services............................................................................................................................ 7C. Situation............................................................................................................................ 8C.1. Earnings Situation............................................................................................................. 8C.2. Assets Situation ................................................................................................................ 9C.3. Financial Situation........................................................................................................... 10D. Events after the Balance Sheet Date .............................................................................. 11E. Risks and Opportunities Report ...................................................................................... 11E.1. Opportunities .................................................................................................................. 11E.2. Risks............................................................................................................................... 12F. Additional Disclosures..................................................................................................... 12F.1. Administrative Board....................................................................................................... 12F.2 Employees ...................................................................................................................... 12F.3 Environment and Sustainability ....................................................................................... 13G. Outlook ........................................................................................................................... 13G.1. Segment Development.................................................................................................... 13G.2. Group Development........................................................................................................ 15

Consolidated Interim Financial Statements

Consolidated Balance Sheet ...................................................................................................... 16Consolidated Income Statement................................................................................................. 18Exhibit of Income and Expense Recorded in Group Equity......................................................... 19Consolidated Statement of Changes in Equity............................................................................ 20Consolidated Cash Flow Statement............................................................................................ 22Condensed Notes to the Consolidated Interim Financial Statements.......................................... 23

Contacts..................................................................................................................................... 39

3

The share

ALBA Group plc & Co. KG, as parent of ALBA SE, and its affiliated

subsidiaries comprise the ALBA Group. The ALBA Group belongs to one of

the ten largest environmental services, recycling and secondary resource

trading companies worldwide. The Group’s business activities prevent the

release of 6.6 million tonnes of environmentally harmful carbon emissions

every year.

ALBA Group plc & Co. KG is the largest shareholder of ALBA SE. Voting

rights of ALBA Group plc & Co. KG, Berlin, are to be attributed to Dr. Axel

Schweitzer and Dr. Eric Schweitzer in accordance with Section 22,

paragraph 1, clause 1 (1) of the German Securities Trading Act via ALBA

Finance plc & Co. KGaA, ALBA Finance Holding plc, ALBA Group Europe

plc, Alpsee Ltd. and Eibsee Ltd., each with statutory headquarters in

London, UK, and administrative headquarters in Berlin. As of December 31,

2015, these voting rights were composed of 9,135,777 shares (92.843 %).

The remainder 7.157% are in free float, no holdings exceed the threshold of

3% or more.

The markets started 2016 unexpectedly weak and leading indices suffered

severe losses in the first weeks of trading. Worries about weakness in the

Chinese economy were a problem for stock markets around the world and

created the weakest start for Germany's DAX index since 1988. After the

markets reached a low point in early February, the central banks took steps

to calm the markets. They then experienced a broad recovery. Improved

economic data from China and higher oil prices helped further improve

sentiment. The leading indices expanded significantly on gains in the

second quarter. Investor uncertainty gradually increased as the vote on a

possible UK exit from the European Union loomed on June 23rd, generating

increased fluctuations in share prices. The British vote to leave the EU

shocked global equity markets and they reacted to the news with massive

price drops. Though financial markets were able to recover from their low

points during the final days of trading, the semi-annual results were still

disappointing. The leading German index, the DAX, fell by 9.89%, while the

MDAX dropped 4.48% and the SDAX was 3.48% lower. The German

technology index TecDAX was one of the biggest losers, falling 12.55% in

the first half of 2016.

The ALBA SE shares remained relatively unfazed by the general market

trends. At the start of XETRA trading on January 4, 2016, ALBA SE shares

were valued at EUR 51.98. The highest price in the first half was EUR 53.22

euros; the lowest price was EUR 47.39. At the end of the reporting period

on June 30, 2016, the share ALBA SE share was selling for EUR 48.20.

4

Interim Group Management Report

A. Basis of the Group

ALBA SE and the affiliated subsidiary companies are included in the

consolidated interim financial statement for ALBA Group plc & Co (ALBA

Group KG). At the ALBA Group KG level and those of the affiliated

subsidiary companies (ALBA Group) is the home for treasury, taxes and

corporate communications departments. Their duties and services extend

to ALBA SE and the affiliated subsidiaries.

ALBA SE and ALBA Group KG have a control and profit-and-loss transfer

agreement. Under the agreement ALBA Group KG any external shareholder

of ALBA SE bearer shares with a notional share in capital stock of EUR 2.60

per share for cash compensation of EUR 46.38 for each ALBA SE share

(cash compensation offer) upon said shareholder's request.

Those external ALBA SE shareholders preferring not to accept the cash

compensation are entitled to receive a recurring payment for the duration of

the agreement (equalisation payment). The equalisation payment amounts

to EUR 3.94 gross per ALBA SE share for each full fiscal year minus

corporate taxes plus a solidarity surcharge according to the rate applicable

to these taxes for the relevant fiscal year.

A legal challenge under the German Award Proceedings Act for cash

compensation and equalisation payment is pending at the District Court in

Cologne. On April 20, 2012, the District Court in Cologne heard the plea

from the claimant and the respondent (ALBA Group KG) and on June 15,

2012 decided to order a new expert opinion, which included an independent

calculation of the company capitalization taking into account the

"appropriate consideration of the relevant clarifications provided" by no later

than the middle of 2014. After objections of bias on the part of a claimant

and subsequent dismissal by the court, the expert appointed by the District

Court in Cologne went to work in late 2013. The expert submitted an

assessment to determine the company value of the ALBA SE. The claimant

and respondent raised objections to the assessment. The District Court in

Cologne requested said expert provide a supplemental assessment, which

was submitted in May 2016. The expert came to the conclusion that the

claimant and respondent objections were irrelevant and thus upheld the

original findings of the assessment. The Expert's statement makes it

possible that a first instance decision shall be made in the current fiscal year.

5

Effective as of 1 January 2016 ALBA SE sold all shares in INTERSEROH

Management GmbH to ALBA Group KG. The disposal of the company had

no material impact on the asset, financial and earnings status of the ALBA

SE Group.

B. Economic Report

B.1. Sector-Related Framework Conditions

Steel and Metals Recycling Segment

Global raw steel production fell compared to production in the previous year

by 1.9%. Production in the EU fell by 6.1% and 1.2% in Germany. While

German steel production with iron ore declined by 0.1%, electric furnace

steel production - which primarily uses scrap steel - dropped by 3.1%. China

failed to throttle steel production despite declines in domestic demand in the

first half of 2016. Chinese steel production actually rose to an all-time high

in April of the reporting period according to information the People's

Republic National Statistics Office issued in May. The country then placed

the excess production on the world market. In the first half year, China

shipped more steel than ever. According to the German Steel Federation,

China supports their steel industry with state subsidized raw materials and

energy.

Turkey - the world's largest consumer of steel scrap - generated additional

demand from March to early May causing a price increase in those months

to 96.50 a tonne, German imports of scrap then dropped to zero in the

second week of May and the price for leading scrap type 2 fell to EUR 62.30

a tonne in June.

According to the Bundesvereinigung Deutscher Stahlrecycling- und

Entsorgungsunternehmen e.V. (Federation of German Steel Recycling and

Disposal Companies: BDSV), the average sales price of lead scrap type 2

was EUR 166.60 a tonne in the first six months of the year and was thus 50

euros less than the average for the same period in the previous year of EUR

216.60 a tonne.

The economic situation in the German metal recycling industry and the

German metal trading industry was dominated by huge uncertainty in the

first half of the year according to the Verband Deutscher Metallhändler e.V.

(German Metal Traders Association: VDM).

The prices for non-ferrous metals also fell in the same period. The average

price for aluminium sank by 13% to USD 1,544 per tonne, while the average

price for copper tonne fell 20.7% to USD 4,701 and 36.6% for a tonne of

nickel to USD 8,662.

6

Services segment

Private consumption in the first two quarters of 2016 drove growth.

The transport packaging business remained highly competitive with

enormous pressure on profit margins.

The seventh revision to the German packaging ordinance also had an

impact in the first six months of the current fiscal year. The elimination of the

self-take-back requirement and the significant increase in requirements

placed on industrial solutions helped stabilise licensed volumes in 2015.

The prices for recycles paper in the reporting period increased by 14.5% to

44.7% on average compared to the average prices for the first half of 2015,

while the price for foils fell by 11.3% to 46.4% compared to the median value

for the same period in the previous year. The average price for transparent

PET fell by 45% compared to the same period in the previous year, coloured

PET by 77.8%.

In addition, the service segment saw an impact from increased prices for

thermal processing.

B.2. Changes in the Legal Framework Conditions

No changes in the legal framework were made in the reporting period.

B.3. Course of BusinessB.3.1. Steel and Metals Recycling

The extremely difficult economic conditions presented in B.1 will have an

impact on the steel and metals recycling segment.

Both ferrous and non-ferrous sales volumes in the first two quarters in 2016

were below those for same period for the previous year. 695 thousand

tonnes (previous year: 1,118 thousand tonnes) of ferrous metals were sold,

non-ferrous metals had 123 thousand tonnes changing hands (previous

year: 183 thousand tonnes). When the previous year figures are adjusted

for portfolio changes the ferrous metal sales volume was 935 thousand

tonnes and 177 thousand tonnes for non-ferrous metals.

The price collapse and weak demand caused sales revenues to fall by EUR

304.3 million to EUR 317.1 million (-49.0%).

7

Despite the difficult market situation, we made minimal improvements to the

margins. The fall in sales volumes led to a significant reduction in the gross

margin. In addition, revenue generated from disposals to improve the

portfolio increased over the first half year 2015. The extraordinary costs

were compensated with savings for outgoing freight and transport costs and

storage costs of EUR 7.5 million and personnel costs of EUR 3.9 million.

Overall, EBITDA fell EUR 10.7 million to EUR 2.5 million.

EBT recorded a 7.2 million decline to negative EUR -2.0 million compared

to the same period in the previous year. The effects described above

contrast with lower depreciation and interest expenses compared to the

same period in the previous year.

Investments of EUR 1.6 million were lower than the investments for the first

six months of 2015 (EUR 3.1 million). Investment was particularly modest

for technical equipment and machines and fleet due to the uncertainty

starting in the second half of 2015.

B.3.2. Services

Sales revenue from transport packaging sank only moderately in the first

half of 2016 compared to the same period in the previous year. Due to

severe competitive pressures, the price reductions provided to customers

contrast with new contract and positive developments in the order book.

Income reductions from reduced foil prices were compensated with higher

sale prices in the cardboard/paper segment.

The sales packaging business remained stable in the first half of 2016

compared to the period in the previous year. The market share from the

Interseroh dual system increased slightly.

The income from the Recycling Solution Interseroh (RSI) increased

marginally, which resulted from the higher order volumes from existing

customers.

Overall, sales revenue from the services segment increased in the first two

quarters of 2016 by EUR 174.4 million compared to the turnover for the

same period in the previous year (previous year: EUR 172.1 million).

EBITDA was EUR 13.5 million, EBT was EUR 13.8 million and thus greater

than for the previous year (11.5 million and EUR 10.8 million). The cause

was primarily non-business model based extraordinary income from

operations, which contrast with the somewhat higher commission expenses.

The investment volume in the first half of 2016 was EUR 1.2 million and thus

higher than the same period in the previous year (EUR 0.9 million).

8

C. Situation

In January 2016 ALBA SE was informed that the ALBA Group KG - as the

parent company of ALBA SE - intends issue statements on the companies

in the services segment along with the two companies in the steel and

metals recycling segment exclusive of ALBA SE to the ALBA Group KG or

another company within the ALBA Group. The impact of the steps on the

asset, financial and earnings situation at ALBA SE Group can be found in

the supplementary report in the 2015 annual report. No instructions have

been issued thus far. At the time of issuance, the disposal income and time

remain uncertain. Therefore, the financial impact on the consolidated interim

financial statement cannot be reliably estimated.

C.1. Earnings Situation

In keeping with expectations, sales declined significantly in the first half year

compared to the same period in the previous year by EUR 301.5 million (-

38.0%) to EUR 491.1 million. In the services segment, sales revenue

increased by EUR 2.3 million (+1.4%) to EUR 174.4 million and was thus

higher than in the previous year while the steel and metals recycling

segment suffered a significant drop in revenue. In this segment the sales

revenue fell by EUR 304.3 million (-49.0%) to EUR 317.1 million, specifically

due to the low prices and low quantities compared to the first six months of

2015.

Material expenses sank 41.9% compared to the first half of 2015 in keeping

with sales trends.

Other operating income was down correspondingly by EUR 8.4 million

(32.7%) to EUR 17.4 million. The earnings from the disposal of assets as

part of portfolio improvements, the earnings from IT services for third parties

as well as the earnings from foreign exchange gains fell by a total of EUR

13.8 million. By contrast, earnings increased by EUR 6.5 million from the

settlement of liabilities, which were associated with operational systems and

other factors.

Personnel costs fell by EUR 4.4 million (-10.2%) and thus reflects the 11.0%

fall in the average staffing level.

The other operational expenses fell by EUR 13.1 million (17.2%) to EUR

63.3 million. The primary contribution here came from EUR 7.5 million in

lower outgoing freight, transport and storage costs and EUR 4.6 million in

lower operating expenses. In addition, the foreign exchange losses and IT

service expenses were reduced by a total of EUR 4.6 million. By contrast,

the expenses from the implementation of provisions for accounts receivable

and sales commissions increased by a total of EUR 3.0 million.

9

The EBITDA reduction of EUR 8.7 million (35.2%) to EUR 16.0 million had

EUR 10.7 million from the steel and metals recycling segment. The services

segment saw an EBITDA increase of EUR 2.0 million.

The EBT fell compared to the previous year by EUR 4.3 million (26.6%) to

EUR 11.7 million. A positive impact stemmed from the improved financial

result of EUR 2.7 million and the reduction of depreciation by EUR 1.7

million.

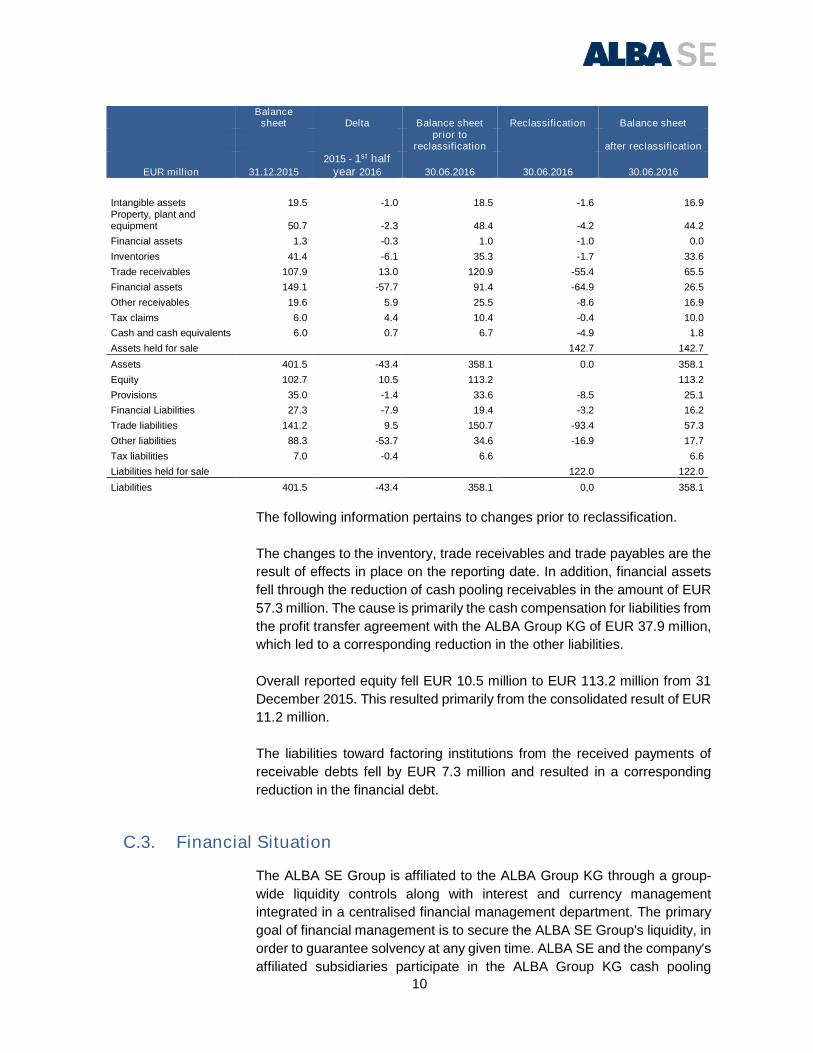

C.2. Assets Situation

Compared to December 31, 2015, total assets had fallen by EUR 43.4

million (-10.8%) to EUR 401.5 million. In tandem with the consolidated

results the equity ratio improved from 25.6% to 31.6%.

EUR 142.7 million in assets from the long-term and short-term assets were

reclassified as "Assets belonging to an assigned disposal group".

Corresponding to the assets, the liabilities saw EUR 122.0 million classified

as "Debt assigned to the disposal group". The assets and debt in this case

are those of the companies in the services segment (ex ALBA SE).

10

Balancesheet Delta Balance sheet Reclassification Balance sheet

prior toreclassification after reclassification

EUR million 31.12.2015

2015 - 1st halfyear 2016 30.06.2016 30.06.2016 30.06.2016

Intangible assets 19.5 -1.0 18.5 -1.6 16.9Property, plant andequipment 50.7 -2.3 48.4 -4.2 44.2

Financial assets 1.3 -0.3 1.0 -1.0 0.0

Inventories 41.4 -6.1 35.3 -1.7 33.6

Trade receivables 107.9 13.0 120.9 -55.4 65.5

Financial assets 149.1 -57.7 91.4 -64.9 26.5

Other receivables 19.6 5.9 25.5 -8.6 16.9

Tax claims 6.0 4.4 10.4 -0.4 10.0

Cash and cash equivalents 6.0 0.7 6.7 -4.9 1.8

Assets held for sale 142.7 142.7

Assets 401.5 -43.4 358.1 0.0 358.1

Equity 102.7 10.5 113.2 113.2

Provisions 35.0 -1.4 33.6 -8.5 25.1

Financial Liabilities 27.3 -7.9 19.4 -3.2 16.2

Trade liabilities 141.2 9.5 150.7 -93.4 57.3

Other liabilities 88.3 -53.7 34.6 -16.9 17.7

Tax liabilities 7.0 -0.4 6.6 6.6

Liabilities held for sale 122.0 122.0

Liabilities 401.5 -43.4 358.1 0,0 358.1

The following information pertains to changes prior to reclassification.

The changes to the inventory, trade receivables and trade payables are the

result of effects in place on the reporting date. In addition, financial assets

fell through the reduction of cash pooling receivables in the amount of EUR

57.3 million. The cause is primarily the cash compensation for liabilities from

the profit transfer agreement with the ALBA Group KG of EUR 37.9 million,

which led to a corresponding reduction in the other liabilities.

Overall reported equity fell EUR 10.5 million to EUR 113.2 million from 31

December 2015. This resulted primarily from the consolidated result of EUR

11.2 million.

The liabilities toward factoring institutions from the received payments of

receivable debts fell by EUR 7.3 million and resulted in a corresponding

reduction in the financial debt.

C.3. Financial Situation

The ALBA SE Group is affiliated to the ALBA Group KG through a group-

wide liquidity controls along with interest and currency management

integrated in a centralised financial management department. The primary

goal of financial management is to secure the ALBA SE Group's liquidity, in

order to guarantee solvency at any given time. ALBA SE and the company's

affiliated subsidiaries participate in the ALBA Group KG cash pooling

11

process. Cash and cash equivalents are compiled, monitored and invested

according to uniform principles throughout the group.

Cash and cash equivalents in the cash flow statement include liquidity in the

amount of EUR 1.8 million (previous year: EUR 6.0 million) along with the

net cash pool balance for the ALBA Group KG of EUR 20.8 million (previous

year: EUR 141.3 million) as well as the net cash and cash equivalent

receivables along with cash pooling receivables for the disposal group of

EUR 68.2 million, making the inventory of cash and cash equivalents at the

end of the reporting period EUR 90.8 million (previous year: EUR 147.3

million). The balances included in the level of cash and cash equivalents are

only subject to minimal fluctuation risks.

Cash flow performance is presented in item 5 of the consolidated notes.

D. Events after the Balance Sheet Date

No material events have occurred since the end of the intermediate

reporting period.

E. Risks and Opportunities Report

Please refer to the information on pages 75 to 88 of the 2015 annual report

for the strategic and operational opportunities and risks which are still

applicable. Under assumption of compliance with the covenants and

assurances in the loan agreement, the risks identified as of June 30, 2016

do not represent a threat to solvency both severally and as a whole. Since

compilation of the consolidated annual report on April 25, 2016, the following

opportunities and risks have arisen or altered.

E.1. Opportunities

Services

The packaging law changes currently under debate and set for passage in

this legislative period may help further stabilise the market for sales

packaging. Such an outcome is dependent on the content of the packaging

law.

12

E.2. RisksSegments

Steel and Metals Recycling

The markets for ferrous and non-ferrous metals are subject to economic

risks arising in the numerous geopolitical problem areas. The recent political

developments in Turkey could have an impact on scrap demand.

Another risk is the scope of steel production in China. Should China receive

the status of a market economy this December, fail to slow steel production

and should a reform of the European anti-dumping law not be passed in

time, attaching tariffs to the steel exported to Europe at dumping prices

could prove difficult. This may have negative consequences for ferrous

scrap prices and demand.

Services

The management sees risks in the market for sales packaging stemming

from the content of included in the drafting the packaging law but generally

sees the potential opportunities having the upper hand.

F. Additional DisclosuresF.1. Administrative Board

The court decision of January 14, 2016 appointed Mr. Dirk Beuth as

Administrative Board member. The term ended at the end of the orderly

General Shareholders’ Meeting on June 7, 2016. The ALBA SE General

Shareholders’ Meeting appointed Dr. Axel Schweitzer, Dirk Beuth and

Robert Nansink once again to the Administrative Board. The appointment

of the Administrative Board members was performed in compliance with §

8 (2) of the company statutes for the period up to the end of the General

Shareholders' Meeting, which passed a resolution regarding approval for

the five fiscal year term in office, but no more than six years. The fiscal year

in which the appointment has been made is not included in such

calculations.

F.2 Employees

In the first half of 2016 the ALBA SE Group employed an average of 1,380

individuals, not including trainees and students (previous year: 1,550). Their

number was thus 11.0% below the level for the previous year.

The steel and metals recycling segment employed an average 814

individuals in the first half (previous year: 986), of which 334 (previous year:

13

409) were clerical employees and 480 (previous year: 577) were

commercial employees.

In the services segment the average number of employees was 566

(previous year: 564). The number of clerical workers was 434 (previous

year: 435), and 132 commercial employees (previous year: 129).

F.3 Environment and Sustainability

On June 14, 2016 Interseroh brought out their new annual sustainability

magazine and thus expanded on their classic sustainability reporting. In the

first edition titled "Solutions with a future", Interseroh presented current best

practices for sustainability - both within the company and for customers. As

part of the sustainability strategy, Interseroh defined quantifiable goals for

sustainable development. In detail, the goals include closing recycling

loops, conserving resources, reducing the company's ecological footprint,

improving attractiveness as an employer and acting as intermediary for

sustainable development. The magazine covers both the services segment

at Interseroh and the sorting of light packing and facility management at the

ALBA Group.

The integrated management system (DIN EN ISO 9001:2008, DIN EN ISO

14001:2009, BS OHSAS 18001:2007) and INTERSEROH Dienstleistungs

GmbH and the company's subsidiaries was confirmed in June 2016 as part

of a monitoring audit on the part of the certifier without any deviation. The

companies were also recertified as a waste disposal operator.

G. OutlookG.1. Segment Development

The estimate of segment development at ALBA SE is based on performance

in the first half of 2016 as well as the current expectations and assumptions

regarding the impact of future events and economic conditions on

operational companies in the second half of the current fiscal year.

Steel and Metals Recycling segment

According to the German Steel Federation prospects for the second half of

2016 remain uncertain in the face of developments in both the global

economy and the global steel market. In 2016 Chinese steel capacity shall

be reduced by 45 million tonnes and by 150 million tonnes by 2020.

According to the Chinese supervisory authority SASAC, provincial

governments failing to make the planned capacity reductions or failing to

meet their targets will be punished. Nevertheless, experts assume China

will still attempt to get rid of 120 million tonnes of steel at fire sale prices, 8%

more than in 2015.

14

Simultaneously the EU Commission is planning to reform European anti-

dumping legislation to protect the domestic industry from state-subsidised

and low-price imports from China. The reform is needed because China will

have discrimination-free access to the European domestic market as of

December 16, 2016. The previous differentiation between market economy

and non-market economy shall no longer apply. Anti-dumping tariffs may no

longer be directed against a government but against a state-subsidised

industry such as the Chinese steel industry.

According to the German metal traders' association, expectations for the

second half of the year are fairly reserved.

As forecast at the start of the reporting year, ALBA SE management expects

strong drops in the demand for ferrous metals in the current fiscal year due

to the difficult situation on the steel market as well as the planned portfolio

adjustments. Due to the unexpectedly difficult situation on the metal

markets, demand for non-ferrous metals is also expected to decline

significantly. Sales volumes and prices will lead to the significant reduction

in sales revenues predicted at the start of the year.

The EBITDA is still expected to improve significantly in 2016. The steps

taken to increase vertical value creation and cut structural costs are the

primary sources of the improvements. The effects and the lack of

extraordinary write downs on intangible assets as in fiscal 2015 have had a

positive impact on the EBT, which is expected to increase extraordinary.

By the end of the year, the necessary replacement investments in the fleet

and holding facilities will be made. In addition, some sites will be renovated

or renewed. Due to the continued volatility on steel and metals markets, little

investment is expected, meaning the 2016 budget will most likely not be

completely deployed.

Services Segment

In deviation from the forecast at the start of fiscal 2016, which assumed

slightly lower sales revenues, the management now expects a marginal

increase is sales revenues through customer loyalty and promotional

campaigns.

Significant declines for the EBITDA and EBT were predicted at the start of

fiscal 2016. Contrary to expectations, income improved in the first half of

2016 due to positive non-periodic business model effects. Nevertheless,

management continues to expect the EBITDA and EBT for fiscal 2016

forecast at the start of the year, which will still be improved when adjusted

for the non-periodic effects. EBITDA and EBT are still expected to be

significantly reduced compared to 2015.

15

The planned investments will be fully implemented by the end of the year.

G.2. Group Development

Management continues to expect significant revenue reductions for fiscal

2016 compared to fiscal 2015. The revenue development in the steel and

metals segment will be dominated by weak demand for steel scrap and low

prices.

In contrast to the predictions at the start of the year, which assumed a

significant decline in EBITDA, the EBITDA compared to 2015 will only be

moderately lower. The supplemental earnings improvements result primarily

from positive non-periodic business model effects from the first half from the

services segment.

When compared to the forecast at the start of the year assuming significant

EBT improvements would continue causing an increase in EBITDA, though

not to the same extent as in the year 2015 due to the extraordinary write

downs offset with an extraordinary increase.

Investments were lower than expected.

The ALBA SE Group is still bound in the financing of the ALBA Group. Doing

so guarantees that ALBA SE Group has sufficient liquidity available.

16

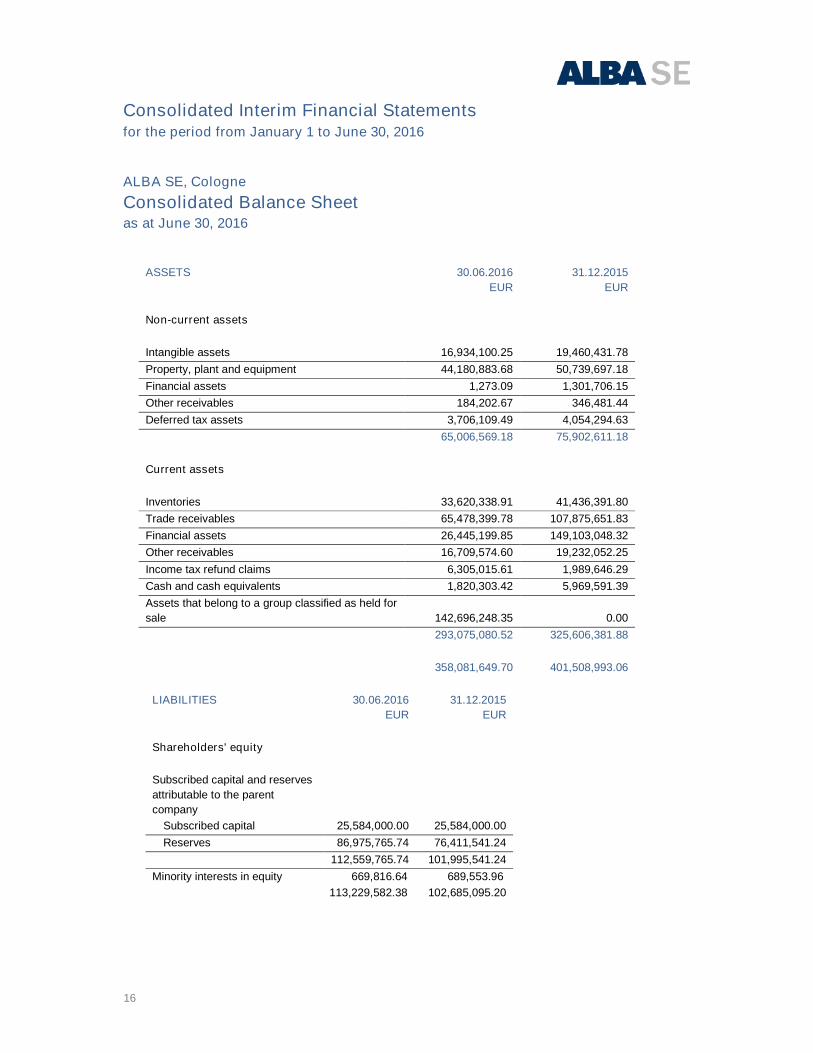

Consolidated Interim Financial Statementsfor the period from January 1 to June 30, 2016

ALBA SE, Cologne

Consolidated Balance Sheetas at June 30, 2016

ASSETS 30.06.2016

EUR

31.12.2015

EUR

Non-current assets

Intangible assets 16,934,100.25 19,460,431.78

Property, plant and equipment 44,180,883.68 50,739,697.18

Financial assets 1,273.09 1,301,706.15

Other receivables 184,202.67 346,481.44

Deferred tax assets 3,706,109.49 4,054,294.63

65,006,569.18 75,902,611.18

Current assets

Inventories 33,620,338.91 41,436,391.80

Trade receivables 65,478,399.78 107,875,651.83

Financial assets 26,445,199.85 149,103,048.32

Other receivables 16,709,574.60 19,232,052.25

Income tax refund claims 6,305,015.61 1,989,646.29

Cash and cash equivalents 1,820,303.42 5,969,591.39

Assets that belong to a group classified as held for

sale 142,696,248.35 0.00

293,075,080.52 325,606,381.88

358,081,649.70 401,508,993.06

LIABILITIES 30.06.2016

EUR

31.12.2015

EUR

Shareholders' equity

Subscribed capital and reserves

attributable to the parent

company

Subscribed capital 25,584,000.00 25,584,000.00

Reserves 86,975,765.74 76,411,541.24

112,559,765.74 101,995,541.24

Minority interests in equity 669,816.64 689,553.96

113,229,582.38 102,685,095.20

17

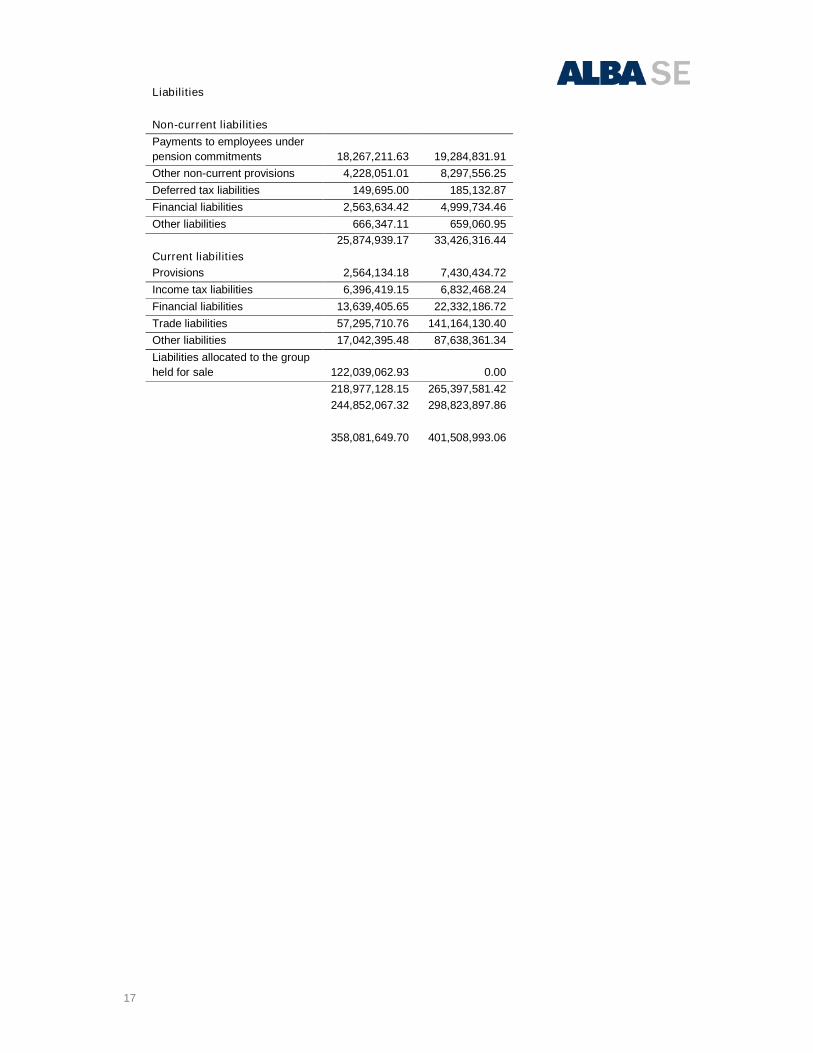

Liabilities

Non-current liabilities

Payments to employees under

pension commitments 18,267,211.63 19,284,831.91

Other non-current provisions 4,228,051.01 8,297,556.25

Deferred tax liabilities 149,695.00 185,132.87

Financial liabilities 2,563,634.42 4,999,734.46

Other liabilities 666,347.11 659,060.95

25,874,939.17 33,426,316.44

Current liabilities

Provisions 2,564,134.18 7,430,434.72

Income tax liabilities 6,396,419.15 6,832,468.24

Financial liabilities 13,639,405.65 22,332,186.72

Trade liabilities 57,295,710.76 141,164,130.40

Other liabilities 17,042,395.48 87,638,361.34

Liabilities allocated to the group

held for sale 122,039,062.93 0.00

218,977,128.15 265,397,581.42

244,852,067.32 298,823,897.86

358,081,649.70 401,508,993.06

18

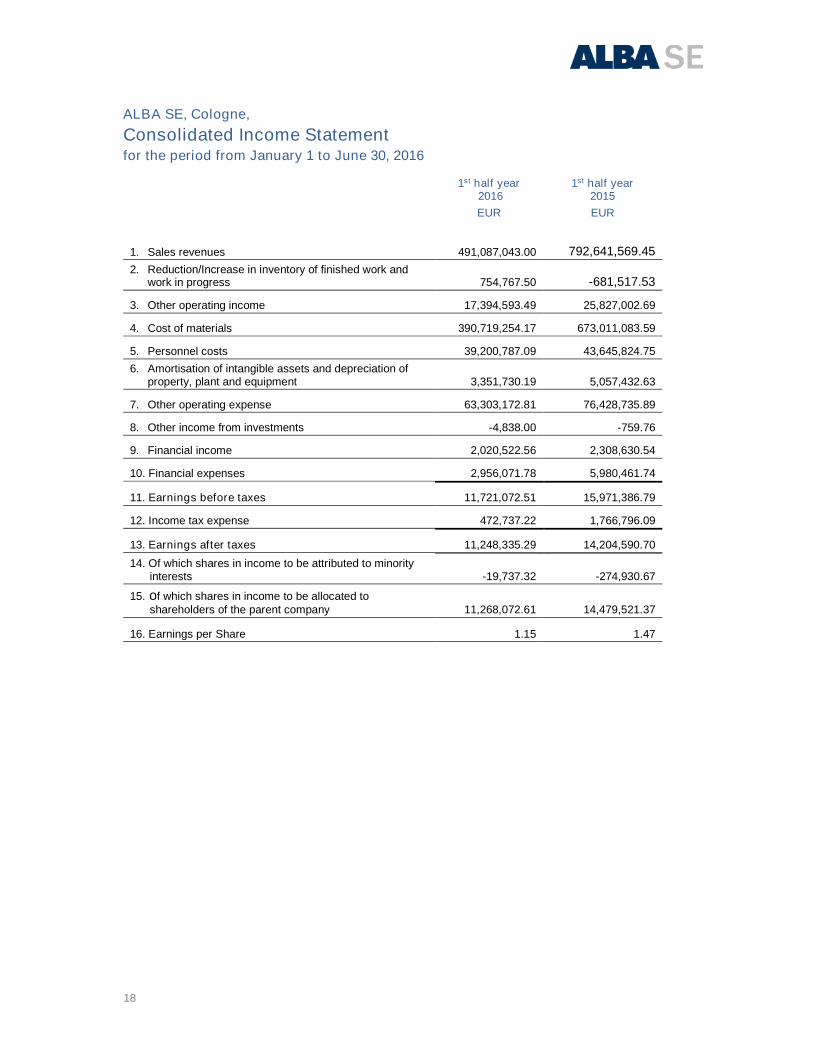

ALBA SE, Cologne,

Consolidated Income Statementfor the period from January 1 to June 30, 2016

1st half year2016

1st half year2015

EUR EUR

1. Sales revenues 491,087,043.00 792,641,569.45

2. Reduction/Increase in inventory of finished work andwork in progress 754,767.50 -681,517.53

3. Other operating income 17,394,593.49 25,827,002.69

4. Cost of materials 390,719,254.17 673,011,083.59

5. Personnel costs 39,200,787.09 43,645,824.75

6. Amortisation of intangible assets and depreciation ofproperty, plant and equipment 3,351,730.19 5,057,432.63

7. Other operating expense 63,303,172.81 76,428,735.89

8. Other income from investments -4,838.00 -759.76

9. Financial income 2,020,522.56 2,308,630.54

10. Financial expenses 2,956,071.78 5,980,461.74

11. Earnings before taxes 11,721,072.51 15,971,386.79

12. Income tax expense 472,737.22 1,766,796.09

13. Earnings after taxes 11,248,335.29 14,204,590.70

14. Of which shares in income to be attributed to minorityinterests -19,737.32 -274,930.67

15. of which shares in income to be allocated toshareholders of the parent company 11,268,072.61 14,479,521.37

16. Earnings per Share 1.15 1.47

19

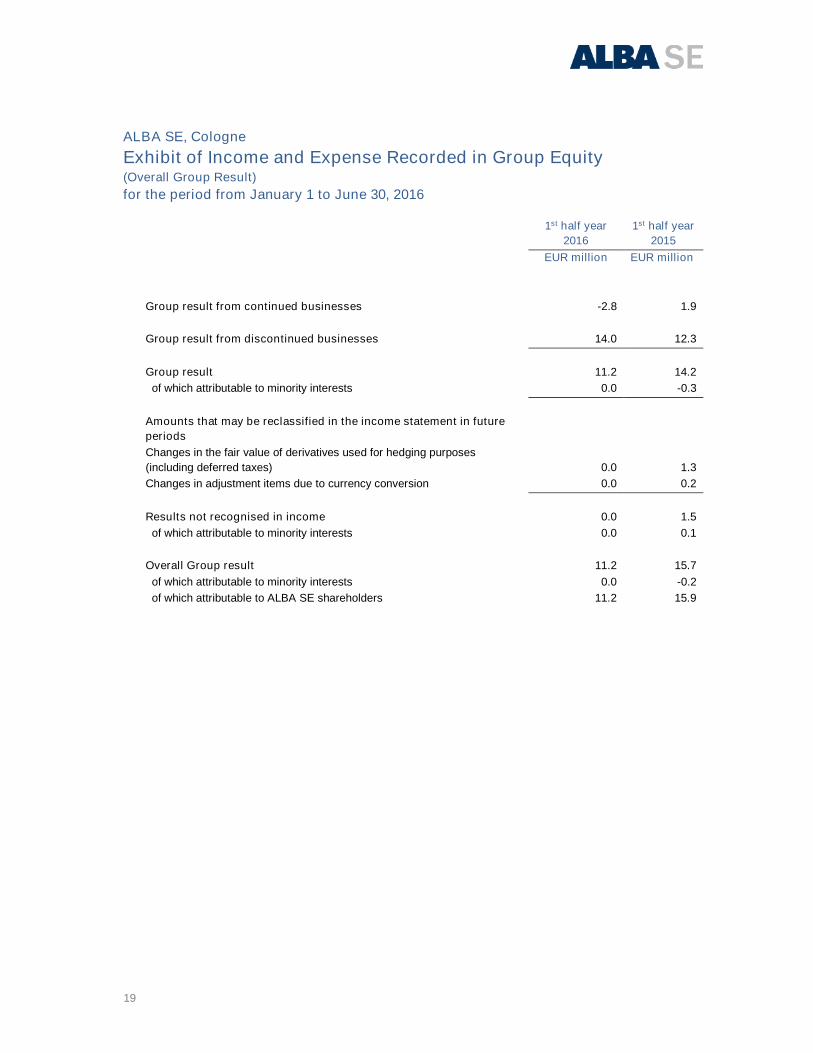

ALBA SE, Cologne

Exhibit of Income and Expense Recorded in Group Equity(Overall Group Result)

for the period from January 1 to June 30, 2016

1st half year

2016

1st half year

2015

EUR million EUR million

Group result from continued businesses -2.8 1.9

Group result from discontinued businesses 14.0 12.3

Group result 11.2 14.2

of which attributable to minority interests 0.0 -0.3

Amounts that may be reclassified in the income statement in future

periods

Changes in the fair value of derivatives used for hedging purposes

(including deferred taxes) 0.0 1.3

Changes in adjustment items due to currency conversion 0.0 0.2

Results not recognised in income 0.0 1.5

of which attributable to minority interests 0.0 0.1

Overall Group result 11.2 15.7

of which attributable to minority interests 0.0 -0.2

of which attributable to ALBA SE shareholders 11.2 15.9

20

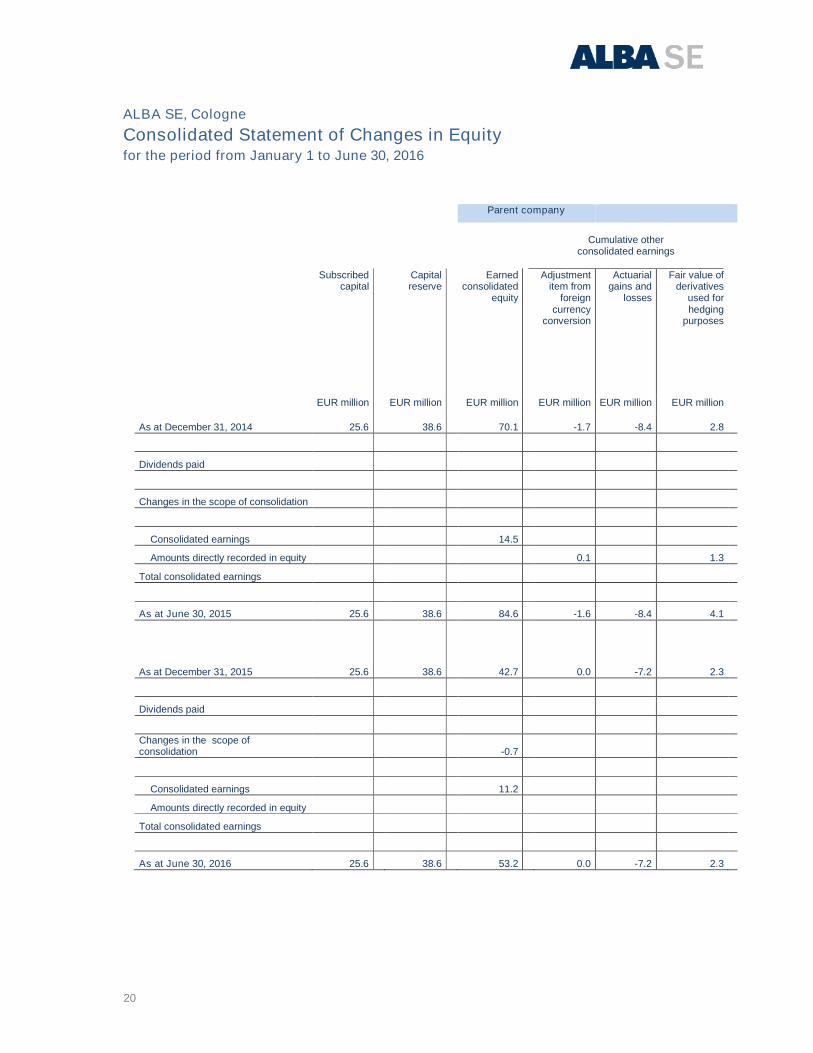

ALBA SE, Cologne

Consolidated Statement of Changes in Equityfor the period from January 1 to June 30, 2016

Parent company

Cumulative otherconsolidated earnings

Subscribedcapital

Capitalreserve

Earnedconsolidated

equity

Adjustmentitem from

foreigncurrency

conversion

Actuarialgains and

losses

Fair value ofderivatives

used forhedging

purposes

EUR million EUR million EUR million EUR million EUR million EUR million

As at December 31, 2014 25.6 38.6 70.1 -1.7 -8.4 2.8

Dividends paid

Changes in the scope of consolidation

Consolidated earnings 14.5

Amounts directly recorded in equity 0.1 1.3

Total consolidated earnings

As at June 30, 2015 25.6 38.6 84.6 -1.6 -8.4 4.1

As at December 31, 2015 25.6 38.6 42.7 0.0 -7.2 2.3

Dividends paid

Changes in the scope ofconsolidation -0.7

Consolidated earnings 11.2

Amounts directly recorded in equity

Total consolidated earnings

As at June 30, 2016 25.6 38.6 53.2 0.0 -7.2 2.3

21

Parent company Minority shareholders Consolidated equity

Equity Minority capital Consolidated equity

EUR million EUR million EUR million

As at December 31, 2014 127.0 6.8 133.8

Dividends paid -0.1 -0.1

Changes in the scope of consolidation

Consolidated earnings 14.5 -0.3 14.2

Amounts directly recorded in equity 1.4 0.1 1.5

Total consolidated earnings 15.9 -0.2 15.7

As at June 30, 2015 142.9 6.5 149.4

As at December 31, 2015

102.0 0.7 102.7

Dividends paid

Changes in the scope ofconsolidation -0.7 -0.7

Consolidated earnings 11.2 11.2

Amounts directly recorded in equity

Total consolidated earnings 11.2 0.0 11.2

As at June 30, 2016 112.5 0.7 113.2

22

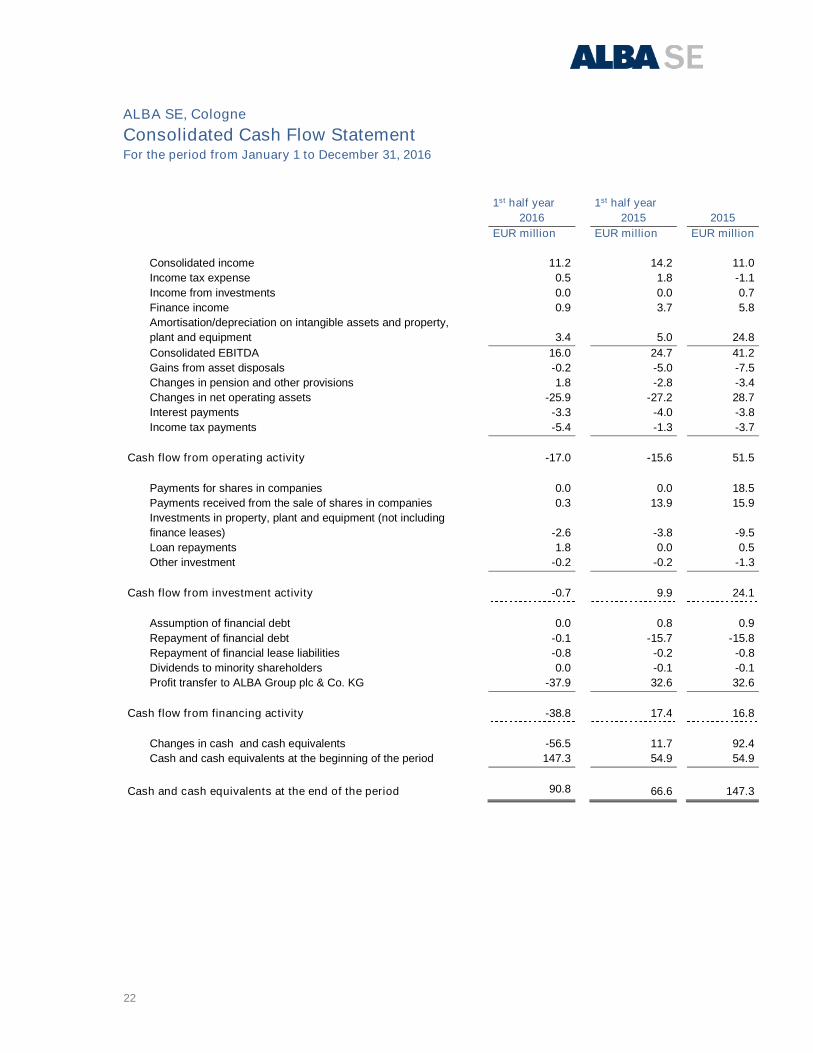

ALBA SE, Cologne

Consolidated Cash Flow StatementFor the period from January 1 to December 31, 2016

1st half year 1st half year

2016 2015 2015

EUR million EUR million EUR million

Consolidated income 11.2 14.2 11.0

Income tax expense 0.5 1.8 -1.1

Income from investments 0.0 0.0 0.7

Finance income 0.9 3.7 5.8

Amortisation/depreciation on intangible assets and property,

plant and equipment 3.4 5.0 24.8

Consolidated EBITDA 16.0 24.7 41.2

Gains from asset disposals -0.2 -5.0 -7.5

Changes in pension and other provisions 1.8 -2.8 -3.4

Changes in net operating assets -25.9 -27.2 28.7

Interest payments -3.3 -4.0 -3.8

Income tax payments -5.4 -1.3 -3.7

Cash flow from operating activity -17.0 -15.6 51.5

Payments for shares in companies 0.0 0.0 18.5

Payments received from the sale of shares in companies 0.3 13.9 15.9

Investments in property, plant and equipment (not including

finance leases) -2.6 -3.8 -9.5

Loan repayments 1.8 0.0 0.5

Other investment -0.2 -0.2 -1.3

Cash flow from investment activity -0.7 9.9 24.1

Assumption of financial debt 0.0 0.8 0.9

Repayment of financial debt -0.1 -15.7 -15.8

Repayment of financial lease liabilities -0.8 -0.2 -0.8

Dividends to minority shareholders 0.0 -0.1 -0.1

Profit transfer to ALBA Group plc & Co. KG -37.9 32.6 32.6

Cash flow from financing activity -38.8 17.4 16.8

Changes in cash and cash equivalents -56.5 11.7 92.4

Cash and cash equivalents at the beginning of the period 147.3 54.9 54.9

Cash and cash equivalents at the end of the period 90.8 66.6 147.3

23

Condensed Notes to the Consolidated Interim Financial Statementsfor the period January 1 to June 30, 2016

ALBA SE, Cologne

1. Information on the Company

ALBA SE is a listed stock corporation domiciled in Cologne, Germany. Its

business address is: Stollwerckstrasse 9a, 51149 Cologne. The

condensed consolidated interim financial statement for the first half of

2016 includes the Company, its subsidiaries and holdings in associated

companies (collectively termed the ALBA SE Group).

The ALBA SE Group is one of the leading environmental services and raw

materials providers in Europe. As service provider, the ALBA SE Group

organises recycling processes and, as supplier to steel works, smelters

and foundries, supplies processing industries. The business activities of

the ALBA SE Group are divided into two segments – steel and metals

recycling and services.

According to the control and profit transfer agreement with ALBA Group

plc & Co. KG (hereinafter: ALBA KG), the latter guarantees external

shareholders of ALBA SE a recurrent payment, a so-called equalisation

payment, for the duration of the agreement, for each full fiscal year in the

gross amount of EUR 3.94 per ALBA SE share, minus corporate taxes

and a solidarity surcharge according to the rate applicable to these taxes

for the relevant fiscal year.

The condensed consolidated interim financial statements covering the

first six months of fiscal 2016 were released for publication upon

resolution of the Administrative Board on August 5, 2016.

2. Accounting Policies

The creation of the condensed consolidated interim financial statements

for the period from January 1 to June 30, 2016 was compiled in

compliance with the International Financial Reporting Standards (IFRS),

IAS 34 "Interim reporting" and the relevant interpretations of the

International Accounting Standards Board (IASB), as these apply in the

European Union. It is a condensed interim financial statement, which does

not contain all information and annex information, which the IFRS requires

for the consolidated notes at the end of fiscal year.

The consolidated interim financial statements are prepared in euros, the

Company's functional currency. Amounts are – with the exception of the

24

consolidated balance sheet and consolidated income statement – shown

in millions of euros rounded to two decimal places. Rounding differences

occur in isolated cases.

Accounting policies applied in preparing the condensed consolidated

interim financial statements reflect the methods used in the consolidated

interim financial statements for the fiscal year ending December 31, 2015.

This also applies to the principles and methods relating to the required

assumptions and estimates in the interim financial statements.

A detailed description of the accounting policies is contained in the Notes

to the consolidated interim financial statements of December 31, 2015,

and published in our 2015 annual report.

Obligatory international financial reporting standards and interpretations

applicable in fiscal 2016 include:

The initial application of amended accounting rules did not have any

material influence on ALBA SE nor influence the presentation of the asset,

financial earnings situation of earnings per share.

Changes to IFRS 11 - Reporting the acquisition of shares in joint

arrangements

The supplement to IFRS 11 governs the reporting the acquisition of

shares in a joint arrangement, which represents an operation as defined

in IFRS 3 "Business Combinations". In such cases, the purchaser shall

apply the principles for reporting business combinations in accordance

with IFRS 3. These amendments are to be applied for the first time to

fiscal years starting on or after January 1, 2016.

Amendments to IAS 1 – Separate Financial Statements

The changes should lead to an improvement of presentation obligations

and relate to various reporting issues. They have an impact on materiality,

aggregation and disaggregation of entries in the balance sheet and

statement of comprehensive income, structure of the notes, the material

accounting methods and the separate reporting of other comprehensive

income (OCI) for companies valued at equity. These amendments are to

be applied for the first time to fiscal years starting on or after January 1,

2016.

25

Amendments to IAS 16 and IFRS 38 – Clarification of the permitted

depreciation methods

The supplements to IAS 16 and IAS 38 clarify that a revenue-based

depreciation of fixed assets and intangible assets is not appropriate and

only permitted in specific exceptional cases. These amendments are to

be applied for the first time to fiscal years starting on or after January 1,

2016.

Amendment to IAS 16 and IAS 41 - Agriculture: Fruit-bearing plants

Amendments to IAS 16 and IAS 41 state that fruit-bearing plants only used

to generate agricultural products need to be reported in compliance with

IAS 16. These amendments are to be applied for the first time to fiscal

years starting on or after January 1, 2016.

Amendments to IAS 27 Equity method in separate financial

statements

The change permits use of equity method as a reporting option for shares

in subsidiaries, joint ventures and associated companies in separate

financial reports for an investor once more. The existing option for

valuation at acquisition costs or in compliance with IAS 39 /IFRS 9

remains in place. These amendments are to be applied for the first time

to fiscal years starting on or after January 1, 2016.

Amendment to IFRS 2012-2014

Amendments to four standards were undertaken as part of the ‘annual

improvement project’. They specify the approach, the valuation and the

presentation of business incidents, uniform terminology and can generally

be seen as editorial corrections to existing standards. They shall apply to

the fiscal year starting on or after January 1, 2016.

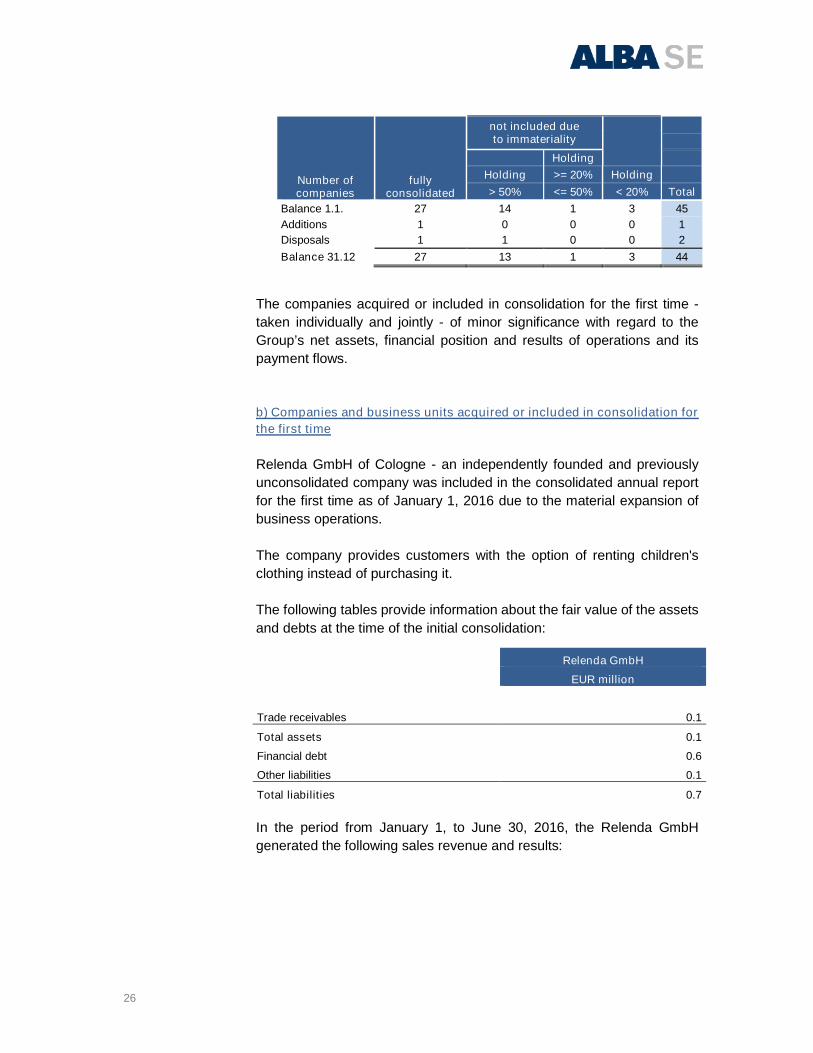

3. Scope of Consolidation

a) Overview

In the first half of 2016 changes were made to the consolidation scope,

which were as follows:

26

The companies acquired or included in consolidation for the first time -

taken individually and jointly - of minor significance with regard to the

Group’s net assets, financial position and results of operations and its

payment flows.

b) Companies and business units acquired or included in consolidation for

the first time

Relenda GmbH of Cologne - an independently founded and previously

unconsolidated company was included in the consolidated annual report

for the first time as of January 1, 2016 due to the material expansion of

business operations.

The company provides customers with the option of renting children's

clothing instead of purchasing it.

The following tables provide information about the fair value of the assets

and debts at the time of the initial consolidation:

In the period from January 1, to June 30, 2016, the Relenda GmbH

generated the following sales revenue and results:

Number ofcompanies

fullyconsolidated

not included dueto immateriality

Holding

Holding >= 20% Holding

> 50% <= 50% < 20% Total

Balance 1.1. 27 14 1 3 45

Additions 1 0 0 0 1

Disposals 1 1 0 0 2

Balance 31.12 27 13 1 3 44

Relenda GmbH

EUR million

Trade receivables 0.1

Total assets 0.1

Financial debt 0.6

Other liabilities 0.1

Total liabilities 0.7

27

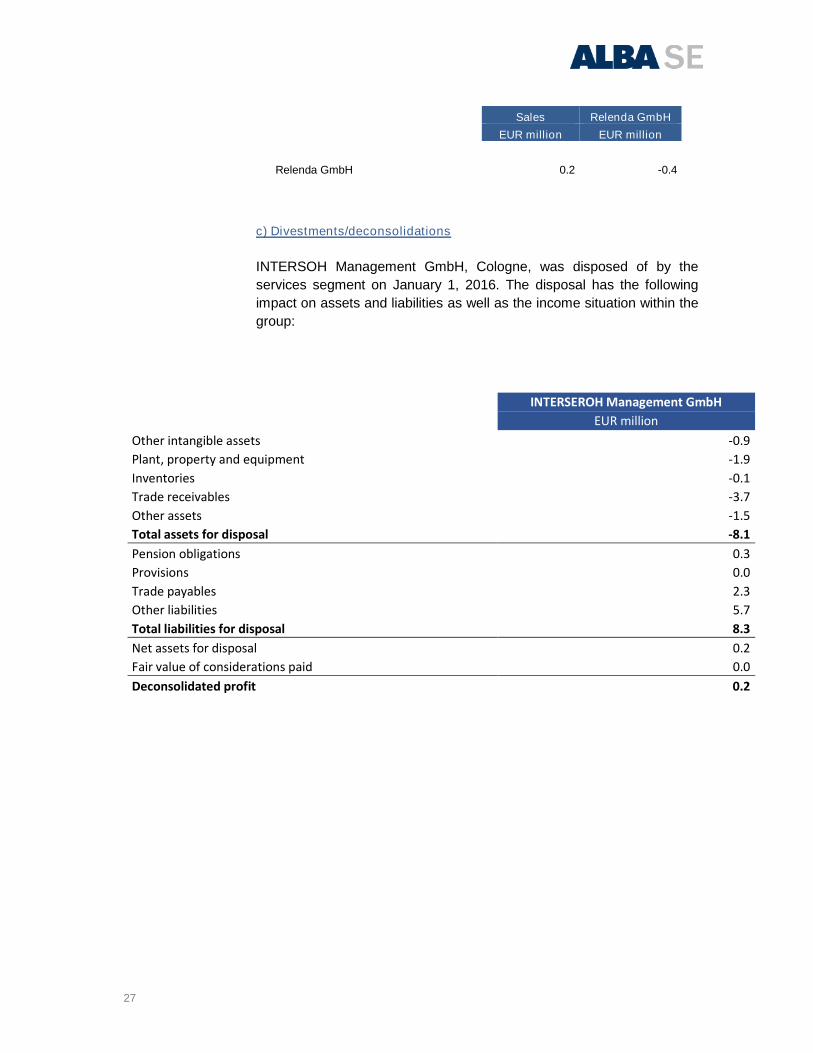

Sales Relenda GmbH

EUR million EUR million

Relenda GmbH 0.2 -0.4

c) Divestments/deconsolidations

INTERSOH Management GmbH, Cologne, was disposed of by the

services segment on January 1, 2016. The disposal has the following

impact on assets and liabilities as well as the income situation within the

group:

INTERSEROH Management GmbH

EUR million

Other intangible assets -0.9

Plant, property and equipment -1.9

Inventories -0.1

Trade receivables -3.7

Other assets -1.5

Total assets for disposal -8.1

Pension obligations 0.3

Provisions 0.0

Trade payables 2.3

Other liabilities 5.7

Total liabilities for disposal 8.3

Net assets for disposal 0.2

Fair value of considerations paid 0.0

Deconsolidated profit 0.2

28

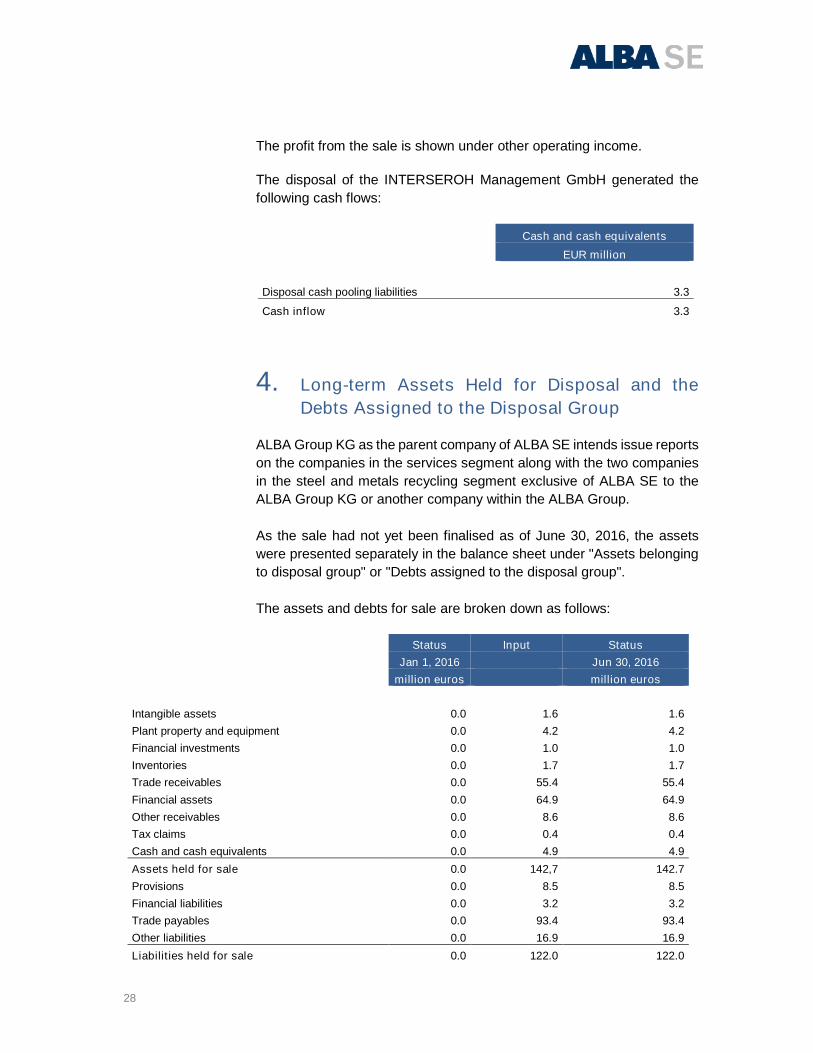

The profit from the sale is shown under other operating income.

The disposal of the INTERSEROH Management GmbH generated the

following cash flows:

Cash and cash equivalents

EUR million

n

Disposal cash pooling liabilities 3.3

Cash inflow 3.3

4. Long-term Assets Held for Disposal and the

Debts Assigned to the Disposal Group

ALBA Group KG as the parent company of ALBA SE intends issue reports

on the companies in the services segment along with the two companies

in the steel and metals recycling segment exclusive of ALBA SE to the

ALBA Group KG or another company within the ALBA Group.

As the sale had not yet been finalised as of June 30, 2016, the assets

were presented separately in the balance sheet under "Assets belonging

to disposal group" or "Debts assigned to the disposal group".

The assets and debts for sale are broken down as follows:

Status Input Status

Jan 1, 2016 Jun 30, 2016

million euros million euros

Intangible assets 0.0 1.6 1.6

Plant property and equipment 0.0 4.2 4.2

Financial investments 0.0 1.0 1.0

Inventories 0.0 1.7 1.7

Trade receivables 0.0 55.4 55.4

Financial assets 0.0 64.9 64.9

Other receivables 0.0 8.6 8.6

Tax claims 0.0 0.4 0.4

Cash and cash equivalents 0.0 4.9 4.9

Assets held for sale 0.0 142,7 142.7

Provisions 0.0 8.5 8.5

Financial liabilities 0.0 3.2 3.2

Trade payables 0.0 93.4 93.4

Other liabilities 0.0 16.9 16.9

Liabilities held for sale 0.0 122.0 122.0

29

The assets and debts classified for disposal have been valued in

compliance with the rules governing long-term assets, disposal groups

and abandoned operations.

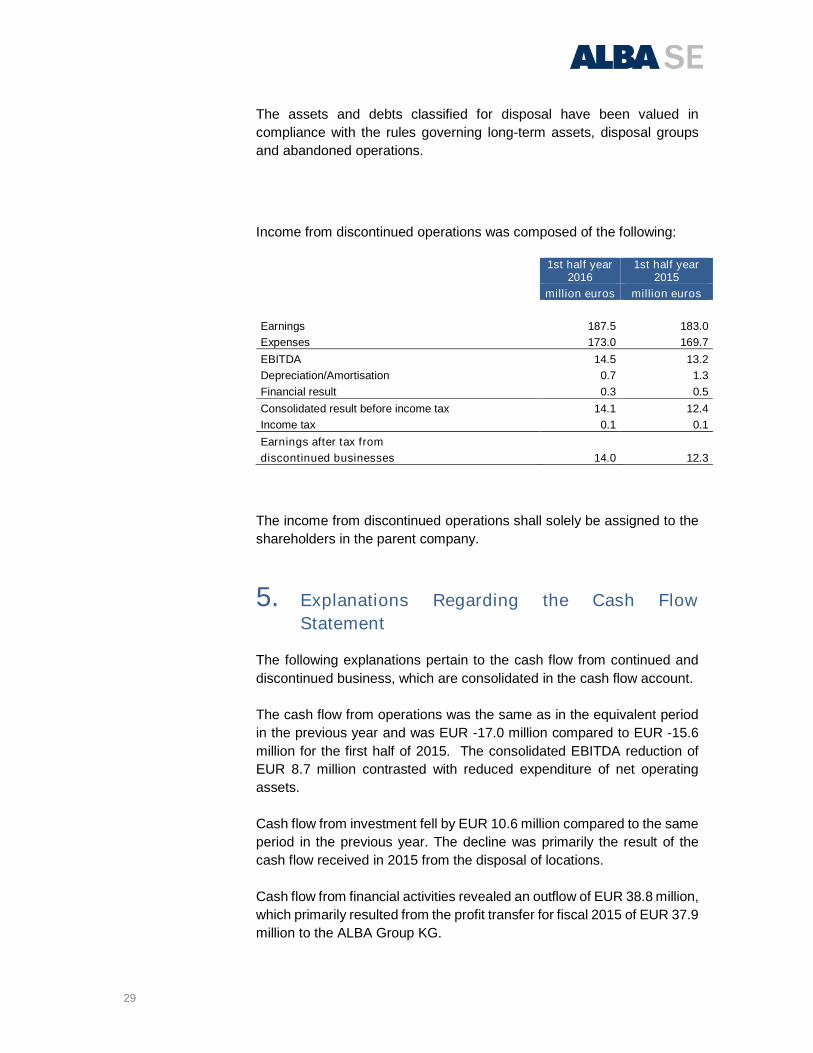

Income from discontinued operations was composed of the following:

1st half year2016

1st half year2015

million euros million euros

Earnings 187.5 183.0

Expenses 173.0 169.7

EBITDA 14.5 13.2

Depreciation/Amortisation 0.7 1.3

Financial result 0.3 0.5

Consolidated result before income tax 14.1 12.4

Income tax 0.1 0.1

Earnings after tax from

discontinued businesses 14.0 12.3

The income from discontinued operations shall solely be assigned to the

shareholders in the parent company.

5. Explanations Regarding the Cash Flow

Statement

The following explanations pertain to the cash flow from continued and

discontinued business, which are consolidated in the cash flow account.

The cash flow from operations was the same as in the equivalent period

in the previous year and was EUR -17.0 million compared to EUR -15.6

million for the first half of 2015. The consolidated EBITDA reduction of

EUR 8.7 million contrasted with reduced expenditure of net operating

assets.

Cash flow from investment fell by EUR 10.6 million compared to the same

period in the previous year. The decline was primarily the result of the

cash flow received in 2015 from the disposal of locations.

Cash flow from financial activities revealed an outflow of EUR 38.8 million,

which primarily resulted from the profit transfer for fiscal 2015 of EUR 37.9

million to the ALBA Group KG.

30

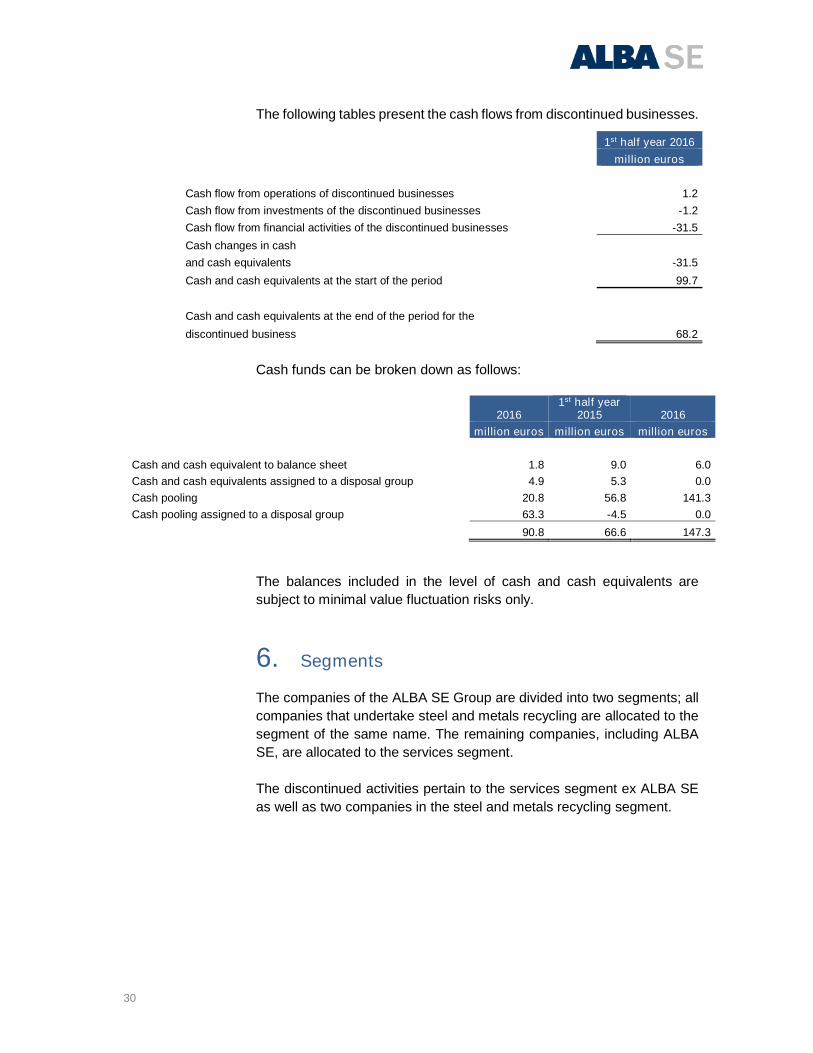

The following tables present the cash flows from discontinued businesses.

Cash funds can be broken down as follows:

20161st half year

2015 2016

million euros million euros million euros

Cash and cash equivalent to balance sheet 1.8 9.0 6.0

Cash and cash equivalents assigned to a disposal group 4.9 5.3 0.0

Cash pooling 20.8 56.8 141.3

Cash pooling assigned to a disposal group 63.3 -4.5 0.0

90.8 66.6 147.3

The balances included in the level of cash and cash equivalents are

subject to minimal value fluctuation risks only.

6. Segments

The companies of the ALBA SE Group are divided into two segments; all

companies that undertake steel and metals recycling are allocated to the

segment of the same name. The remaining companies, including ALBA

SE, are allocated to the services segment.

The discontinued activities pertain to the services segment ex ALBA SE

as well as two companies in the steel and metals recycling segment.

1st half year 2016

million euros

Cash flow from operations of discontinued businesses 1.2

Cash flow from investments of the discontinued businesses -1.2

Cash flow from financial activities of the discontinued businesses -31.5

Cash changes in cash

and cash equivalents -31.5

Cash and cash equivalents at the start of the period 99.7

Cash and cash equivalents at the end of the period for the

discontinued business 68.2

31

Segment revenues and earnings in the interim reported period are

depicted as follows:

Steel andMetals Recycling

Cross-segment

Services consolidations Group

1st halfyear2016

1st halfyear2015

1st halfyear2016

1st halfyear2015

1st halfyear2016

1st halfyear2015

1st halfyear2016

1st halfyear2015

EUR million EUR million EUR million EUR million

Sales revenues 317.0 621.3 174.1 171.3 0.0 0.0 491.1 792.6

External sales 0.1 0.1 0.4 0.8 -0.5 -0.9 0.0 0.0

Sales between the segments 317.1 621.4 174.5 172.1 -0.5 -0.9 491.1 792.6

Steel andmetals recycling

Cross-segment

Services consolidations Group

1st halfyear2016

1st halfyear2015

1st halfyear2016

1st halfyear2015

1st halfyear2016

1st halfyear2015

1st halfyear2016

1st halfyear2015

EUR million EUR million EUR million EUR million

Segment - EBITDA 2.5 13.2 13.5 11.5 0.0 0.0 16.0 24.7

Scheduled amortisation of intangibleassets and depreciation of plantproperty and equipment 2.6 3.5 0.8 1.5 0.0 0.0 3.4 5.0

Investment income0.0 0.0 0.0 0.0 0.0 0.0 0.0. 0.0

Financial income -1.9 -4.5 1.0 0.8 0.0 0.0 -0.9 -3.7

of which interest earnings 0.4 0.9 1.6 1.4 0.0 0.0 2.0 2.3

of which interest expenses 2.3 5.4 0.6 0.6 0.0 0.0 2.9 6.0

Segment - EBT -2.0 5.2 13.7 10.8 0.0 0.0 11.7 16.0

- Tax expenses -0.5 -1.8

Consolidated income according toincome statement

11.2 14.2

32

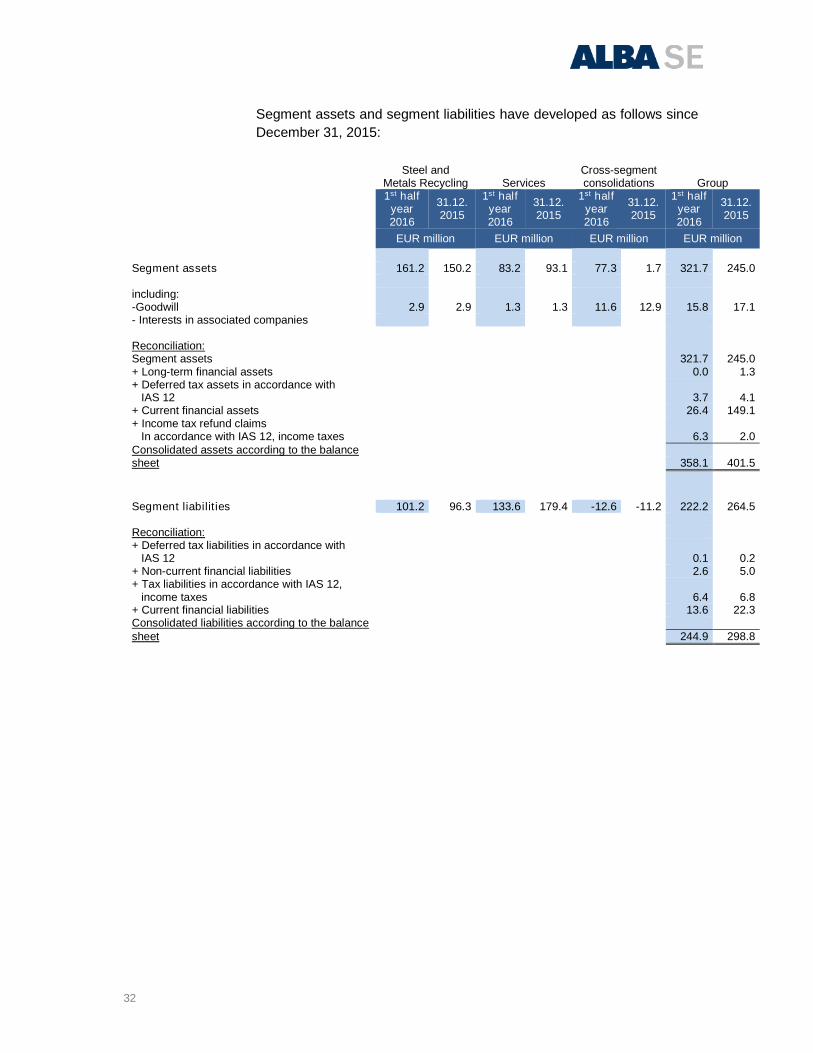

Segment assets and segment liabilities have developed as follows since

December 31, 2015:

Steel and Cross-segmentMetals Recycling Services consolidations Group1st half

year2016

31.12.2015

1st halfyear2016

31.12.2015

1st halfyear2016

31.12.2015

1st halfyear2016

31.12.2015

EUR million EUR million EUR million EUR million

Segment assets 161.2 150.2 83.2 93.1 77.3 1.7 321.7 245.0

including:-Goodwill 2.9 2.9 1.3 1.3 11.6 12.9 15.8 17.1- Interests in associated companies

Reconciliation:Segment assets 321.7 245.0+ Long-term financial assets 0.0 1.3+ Deferred tax assets in accordance with

IAS 12 3.7 4.1+ Current financial assets 26.4 149.1+ Income tax refund claims

In accordance with IAS 12, income taxes 6.3 2.0Consolidated assets according to the balancesheet 358.1 401.5

Segment liabilities 101.2 96.3 133.6 179.4 -12.6 -11.2 222.2 264.5

Reconciliation:+ Deferred tax liabilities in accordance with

IAS 12 0.1 0.2+ Non-current financial liabilities 2.6 5.0+ Tax liabilities in accordance with IAS 12,

income taxes 6.4 6.8+ Current financial liabilities 13.6 22.3Consolidated liabilities according to the balancesheet 244.9 298.8

33

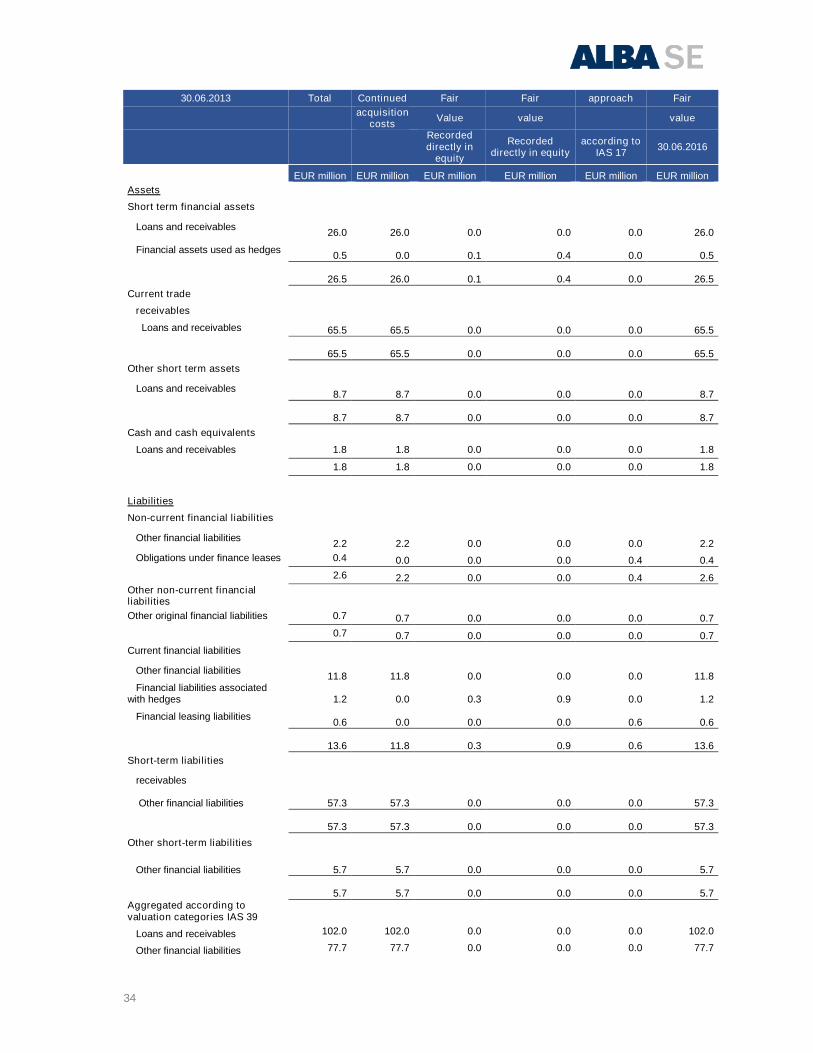

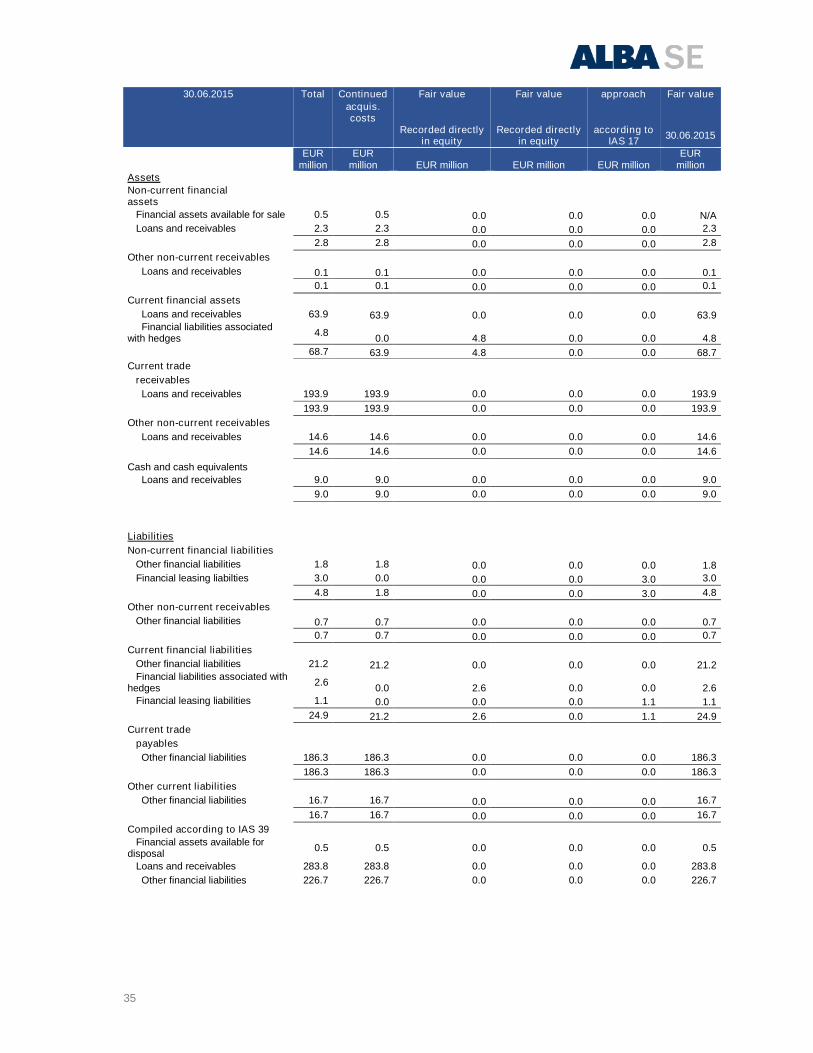

7. Financial Instruments

The following table depicts the financial assets and liabilities based on

valuation categories and classes. In the process, the financial instrument

classes correspond to the balance sheet classification. Liabilities from

financial leasing as well as derivatives with balance sheet hedges shall be

taken into account, even though they do not belong to any IAS 39

valuation category. The following financial instruments are reported in the

consolidated interim financial statements:

34

30.06.2013 Total Continued Fair Fair approach Fair

acquisitioncosts

Value value value

Recordeddirectly in

equity

Recordeddirectly in equity

according toIAS 17

30.06.2016

EUR million EUR million EUR million EUR million EUR million EUR million

Assets

Short term financial assets

Loans and receivables26.0 26.0 0.0 0.0 0.0 26.0

Financial assets used as hedges0.5 0.0 0.1 0.4 0.0 0.5

26.5 26.0 0.1 0.4 0.0 26.5

Current trade

receivables

Loans and receivables 65.5 65.5 0.0 0.0 0.0 65.5

65.5 65.5 0.0 0.0 0.0 65.5

Other short term assets

Loans and receivables8.7 8.7 0.0 0.0 0.0 8.7

8.7 8.7 0.0 0.0 0.0 8.7

Cash and cash equivalents

Loans and receivables 1.8 1.8 0.0 0.0 0.0 1.8

1.8 1.8 0.0 0.0 0.0 1.8

Liabilities

Non-current financial liabilities

Other financial liabilities2.2 2.2 0.0 0.0 0.0 2.2

Obligations under finance leases 0.4 0.0 0.0 0.0 0.4 0.4

2.6 2.2 0.0 0.0 0.4 2.6Other non-current financialliabilities

Other original financial liabilities 0.7 0.7 0.0 0.0 0.0 0.7

0.7 0.7 0.0 0.0 0.0 0.7

Current financial liabilities

Other financial liabilities11.8 11.8 0.0 0.0 0.0 11.8

Financial liabilities associatedwith hedges 1.2 0.0 0.3 0.9 0.0 1.2

Financial leasing liabilities0.6 0.0 0.0 0.0 0.6 0.6

13.6 11.8 0.3 0.9 0.6 13.6

Short-term liabilities

receivables

Other financial liabilities 57.3 57.3 0.0 0.0 0.0 57.3

57.3 57.3 0.0 0.0 0.0 57.3

Other short-term liabilities

Other financial liabilities 5.7 5.7 0.0 0.0 0.0 5.7

5.7 5.7 0.0 0.0 0.0 5.7Aggregated according tovaluation categories IAS 39

Loans and receivables 102.0 102.0 0.0 0.0 0.0 102.0

Other financial liabilities 77.7 77.7 0.0 0.0 0.0 77.7

35

30.06.2015 Total Continued Fair value Fair value approach Fair value

acquis.costs

Recorded directlyin equity

Recorded directlyin equity

according toIAS 17

30.06.2015

EURmillion

EURmillion EUR million EUR million EUR million

EURmillion

Assets

Non-current financialassets

Financial assets available for sale 0.5 0.5 0.0 0.0 0.0 N/A

Loans and receivables 2.3 2.3 0.0 0.0 0.0 2.3

2.8 2.8 0.0 0.0 0.0 2.8

Other non-current receivables

Loans and receivables 0.1 0.1 0.0 0.0 0.0 0.1

0.1 0.1 0.0 0.0 0.0 0.1

Current financial assets

Loans and receivables 63.9 63.9 0.0 0.0 0.0 63.9Financial liabilities associated

with hedges4.8

0.0 4.8 0.0 0.0 4.8

68.7 63.9 4.8 0.0 0.0 68.7

Current trade

receivables

Loans and receivables 193.9 193.9 0.0 0.0 0.0 193.9

193.9 193.9 0.0 0.0 0.0 193.9

Other non-current receivables

Loans and receivables 14.6 14.6 0.0 0.0 0.0 14.6

14.6 14.6 0.0 0.0 0.0 14.6

Cash and cash equivalents

Loans and receivables 9.0 9.0 0.0 0.0 0.0 9.0

9.0 9.0 0.0 0.0 0.0 9.0

Liabilities

Non-current financial liabilities

Other financial liabilities 1.8 1.8 0.0 0.0 0.0 1.8

Financial leasing liabilties 3.0 0.0 0.0 0.0 3.0 3.0

4.8 1.8 0.0 0.0 3.0 4.8

Other non-current receivables

Other financial liabilities 0.7 0.7 0.0 0.0 0.0 0.7

0.7 0.7 0.0 0.0 0.0 0.7

Current financial liabilities

Other financial liabilities 21.2 21.2 0.0 0.0 0.0 21.2Financial liabilities associated with

hedges2.6

0.0 2.6 0.0 0.0 2.6

Financial leasing liabilities 1.1 0.0 0.0 0.0 1.1 1.1

24.9 21.2 2.6 0.0 1.1 24.9

Current trade

payables

Other financial liabilities 186.3 186.3 0.0 0.0 0.0 186.3

186.3 186.3 0.0 0.0 0.0 186.3

Other current liabilities

Other financial liabilities 16.7 16.7 0.0 0.0 0.0 16.7

16.7 16.7 0.0 0.0 0.0 16.7

Compiled according to IAS 39

Financial assets available fordisposal

0.5 0.5 0.0 0.0 0.0 0.5

Loans and receivables 283.8 283.8 0.0 0.0 0.0 283.8

Other financial liabilities 226.7 226.7 0.0 0.0 0.0 226.7

36

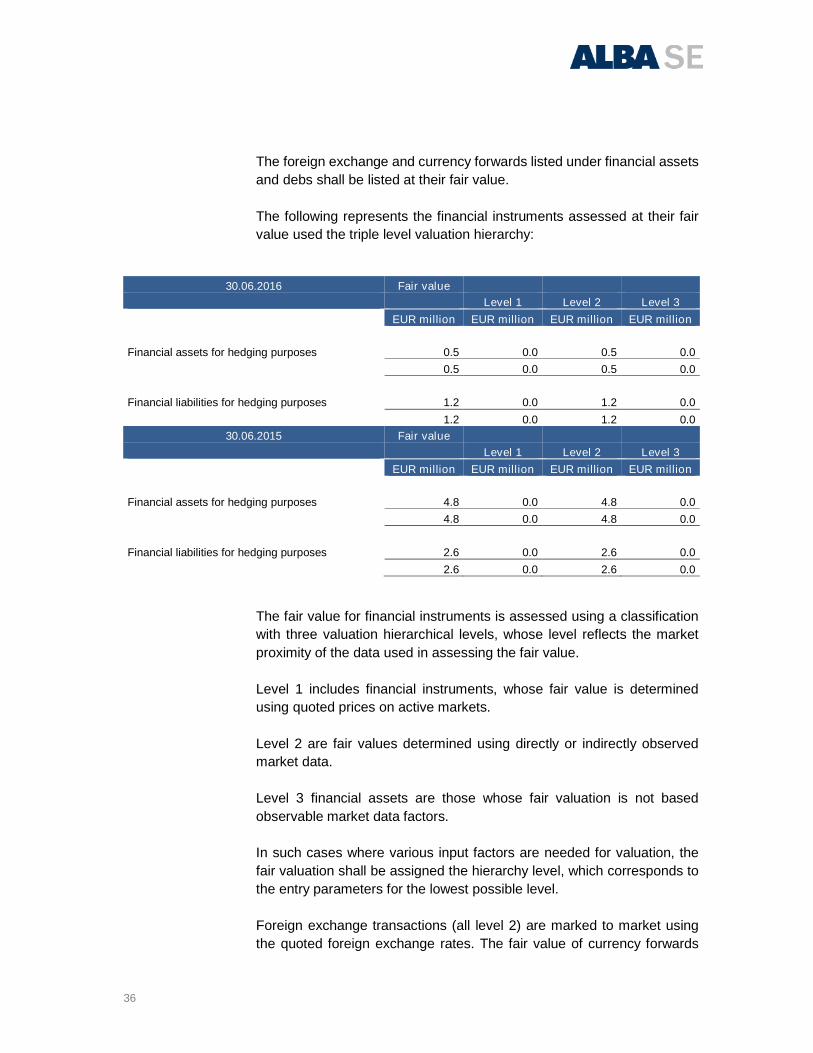

The foreign exchange and currency forwards listed under financial assets

and debs shall be listed at their fair value.

The following represents the financial instruments assessed at their fair

value used the triple level valuation hierarchy:

30.06.2016 Fair value

Level 1 Level 2 Level 3

EUR million EUR million EUR million EUR million

Financial assets for hedging purposes 0.5 0.0 0.5 0.0

0.5 0.0 0.5 0.0

Financial liabilities for hedging purposes 1.2 0.0 1.2 0.0

1.2 0.0 1.2 0.0

30.06.2015 Fair value

Level 1 Level 2 Level 3

EUR million EUR million EUR million EUR million

Financial assets for hedging purposes 4.8 0.0 4.8 0.0

4.8 0.0 4.8 0.0

Financial liabilities for hedging purposes 2.6 0.0 2.6 0.0

2.6 0.0 2.6 0.0

The fair value for financial instruments is assessed using a classification

with three valuation hierarchical levels, whose level reflects the market

proximity of the data used in assessing the fair value.

Level 1 includes financial instruments, whose fair value is determined

using quoted prices on active markets.

Level 2 are fair values determined using directly or indirectly observed

market data.

Level 3 financial assets are those whose fair valuation is not based

observable market data factors.

In such cases where various input factors are needed for valuation, the

fair valuation shall be assigned the hierarchy level, which corresponds to

the entry parameters for the lowest possible level.

Foreign exchange transactions (all level 2) are marked to market using

the quoted foreign exchange rates. The fair value of currency forwards

37

(Level 2) is calculated as the average of the price set by the market for

the previous month.

Financial instruments listed at their acquisition cost in the balance sheet

and whose fair value can first be found in the noted shall also be classified

using the triple level fair value hierarchy.

Trade receivables, short-term financial assets, other short-term

receivables as well as cash and cash equivalents are equal to the carrying

value based on the maturity used to approximate the fair value.

The fair value of all other financial assets and financial liabilities shall be

assessed using their cash value of the payments associated with these

balance sheet items. The calculation shall use the interest structure

curves applicable at the reporting date (Level 2).

8. Related Party Disclosures

The court decision of January 14, 2016 appointed Mr. Dirk Beuth as

Administrative Board member. The term ended at the end of the orderly

General Shareholders' Meeting on June 7, 2016. The ALBA SE general

meeting appointed Dr. Axel Schweitzer, Dirk Beuth and Robert Nansink

once again to the Administrative Board. The appointment of the

Administrative Board members was performed in compliance with § 8 (2)

of the company statutes for the period up to the end of the General

Shareholders' Meeting, which passed a resolution regarding approval for

the five fiscal year term in office, but no more than six years. The fiscal

year in which the appointment has been made is not included in such

calculations.

9. Events After the end of the Interim Reporting

Period

No material events have occurred since the end of the intermediate

reporting period.

10. Audit Review

The consolidated interim financial statements for the period January 1, to

June 30, 2016, and the interim management report as at June 30, 2016,

have neither been subject to audit review nor audited according to § 317

of the German Commercial Code (HGB).

38

11. Assurances of Legal Representatives

To the best of our knowledge we provide assurance that the consolidated

interim financial statements prepared in accordance with applicable

accounting principles for interim financial reporting represent a true and

fair view of the Group’s financial, earnings and liquidity position and that

the interim Group management report presents the course of business,

including business results and the situation of the Group, such that a true

and fair view is conveyed and that significant risks and opportunities

inherent in the anticipated development of the Group during the remaining

fiscal year are described.

Cologne, August 5, 2016

ALBA SE

Executive Director

Rob Nansink

39

Contacts:ALBA SEInvestor RelationsStollwerckstraße 9a51149 Cologne, GermanyPhone: +49 2203 9147-0E-Mail: [email protected]: www.alba-se.de