Embed Size (px)

Citation preview

14 June 2010

Initiating Coverage

AIA Engineering

Overweight Mid Cap

Refer to disclaimer, analyst certification and ratings criteria on the last page prior to making any investment decision.

THE “COMMINUTION” INDIAN EXPERT – READY FOR THE SPURT IN

INTERNATIONAL MINING BUSINESS AIA Engineering is the largest Indian and second largest player globally in the

manufacture of high chrome mill internals which forms an important

ingredient of every cement, iron ore, copper, gold, platinum group metals,

coal, and other mineral processing mines globally.

Penetration into new global mining companies to offer volume growth:

AIA has cleared the trial stage and has entered the regular supply stage with

- Vale, Brazil (CVRD) for their Samarco (iron ore – 50% JV with BHP Billiton)

and Vittoria Mines (for Kaolin) up to 30,000 TPA; Lonmin (South Africa)

~10,000 TPA ; Konkola Copper (Zambia) ~5,000 TPA; Anglo Platinum (South

Africa) ~30,000 TPA; Nkomati (ARM – South Africa) ~1,000 TPA.

Together these mines offer new business in international mining of 60,000-

80,000 tons per annum in the next 24 months to the existing 20,000 tons

per annum in mining and 103,000 TPA overall.

Lack of a large sized quality grinding media supplier in international

markets: AIA will be the only other global player with second largest

manufacturing capacity of ~165,000 TPA after Magotteaux, thereby meeting

the need of mining companies for quality and consistency in supplies.

EBITDA margins to dip: The trial period for supplies is at least 6 months

of grinding media consumption, post which results are analysed. Initial

supplies post approval desire tough negotiations on the pricing front which

will keep margins under pressure. AIA at present will only be supplying

grinding balls while liners will take more time to breakthrough. We expect

EBITDA margins to dip ~150 bps dip in FY11E and ~70 bps in FY12E.

De-risking the business model: Addressing concerns over the

introduction of vertical mills to reduce consumption of grinding media, the

company is expanding capacities by 20,000 TPA for the manufacture and

supply of vertical mill parts. However, vertical mills at present form barely

1% of the global market and hence the ball mill market still offers

tremendous potential for the coming 10 years.

Valuation & Recommendation: We initiate coverage with an Overweight

rating on the stock with a target price of Rs 444 based on average of DCF

value of Rs 425 and PE based price of Rs 462 based on 22x FY11E EPS.

Market Data

Bloomberg code

Sensex

Price

Target Price

Target return

AIAE IN

16,922

Rs 398

Rs 444

12%

Equity shares o/s (mn)

Market Cap ($ mn)

Market Cap (Rs bn)

52 Wk H/L

FII Limit

94.3

814

38.1

434/ 188

24%

Stock performance

(%) Absolute Relative

1 Month (0.5) 0.4

6 Months 16.9 19.7

12 Months 63.6 45.8

Shareholding pattern

Promoter 61.7 FIIs 17.8

Pub & Oth 7.0 DIIs 13.5

Sensex Relative chart

Year end 31 Mar (Rs mn) FY09 FY10 FY11E FY12E CAGR (10-12E)

Net Sales 10,233 9,497 11,817 13,879 20.9

EBITDA 2,467 2,458 2,886 3,285 15.6

PAT 1,712 1,673 1,985 2,223 15.3

EPS (Rs) 18.2 17.7 21.0 23.6 15.3

PE (x) 21.9 22.4 18.9 16.9 -

EV/EBITDA (x) 14.2 13.9 11.8 10.2 -

P/BV (x) 4.8 4.1 3.5 3.0 -

EBITDA % 24.1 25.9 24.4 23.7 -

PAT % 16.7 17.6 16.8 16.0 -

ROE % 24.8 19.9 20.0 19.2 -

ROCE% 33.8 26.7 27.2 26.4 -

Vinay Pandit +91-22-4333 5115 [email protected] Jason Soans +91-22-4333 5133 [email protected]

0

100

200

300

400

500

Jun

-06

Sep

-06

Dec

-06

Ma

r-0

7

Jun

-07

Sep

-07

Dec

-07

Ma

r-0

8

Jun

-08

Sep

-08

Dec

-08

Ma

r-0

9

Jun

-09

Sep

-09

Dec

-09

Ma

r-1

0

SENSEX AIA ENGINEERING LTD

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

2

Contents Page

KEY INVESTMENT CRITERIA 4-13

o Breakthrough in international mining to lend volume growth – but margins to be impacted 4

- International mining breakthroughs and business potential - However, margins to be impacted in initial years of breaking through The key factor here is cost Risk of using new products in the system The 6 month testing criteria Only grinding balls are high chrome; liners are always forged Cost competitiveness to Chinese -Similar composition of Chinese forged players Local manufacturing/ technology based competition from players like Magotteaux o Forged mill internals are here to stay *

- The type of grinding media required for a type of mill *

o Potential for high chrome grinding media in mining *

- Other prominent technologies in grinding (other than ball mills) *

- Established rule of thumb for grinding media in ball mills *

- Market size for grinding media (Source: AIA) o Pricing competitiveness with forged media 8

o Shortage of large scale manufacturers of high chrome grinding media in international markets; AIA dominates domestic market share

9

o Increased capacity to help meet demand from new breakthroughs in international mining 9

o Cement and mining activity uptick in global and domestic markets 10

o Sustainability of business model 13

o POTENTIAL ANALYSIS OF MINING CLIENTS WHERE BREAKTHROUGH ACHIEVED *

- Anglo Platinum, South Africa *

- Konkola Copper Mines, Zambia, Africa *

- Lonmin, South Africa *

- Nkomati – African Rainbow Minerals, South Africa *

KEY INVESTMENT RISK 14-16

o Volatility in currency movements and raw material prices 14

o Upcoming new technologies – Vertical Mills 15

o Increase in market share in international markets will attract competition on account of high margin and healthy return ratios

16

VALUATIONS 17

KEY ASSUMPTIONS 18

SENSITIVITY ANALYSIS 18

FINANCIAL ANALYSIS 19-22

o Debottlenecking to improve sales to capital employed in FY10-11-12; However, further capex for 100,000 TPA to keep ratio <= 1x

19

o Low debt and healthy cash flow position to assist in expansion and acquisition 19

o Return ratio analysis 20

o Stretch in working capital cycle lies ahead 21

o Breakthrough in mining to lead to margin reduction 22

SWOT Analysis 23

Available in the detailed hard copy of report only.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

3

BUSINESS BACKGROUND 24-30

o Background o Settlement deed with Magotteaux – restriction clause for 15 years o Company structure o Products o Technical collaborations o Production capacity o Management team

o Manufacturing facilities o Manufacturing process o Mining process o Cement production process INDUSTRY ANALYSIS *

COMMINUTION – MILL INTERNAL DYNAMICS *

o What is comminution *

o Objectives of comminution *

o Four stages in comminution *

o Different levels of hardness required in grinding media for different rocks/ores *

o Types of comminution *

- Batch comminution *

- Continuous comminution *

Open circuit *

Closed circuit *

o Grinding *

- What is grinding? *

- Materials and particle size desired post grinding *

- AIA target market for grinding media *

o Types of grinding mills *

- Autogenous Grinding (AG) and Semi-Autogenous grinding (SAG) mills *

- Ball mills (tubular) *

Three types of tubular mills: *

-Overflow discharge mills *

-Diaphragm / Grate discharge mills *

-Centre periphery discharge *

o Preferred ore treatment for different kinds of mills *

o RULE OF THUMB FOR DECIDING GRINDING MEDIA AND OTHER MILL INTERNALS *

- Rule of thumb for grinding balls in a BALL mill *

- Rule of thumb for liners and other parts *

- Ore wise abrasion index *

o Factors affecting grinding media wear *

o Growing competitive technologies 31

- High Pressure Grinding Rolls (HPGR) – competition to SAG mills 31

- Vertical Mills – competition for SAG+BALL mills 32

FINANCIAL SUMMARY 33

DISCLAIMER; Other stocks covered by the analyst 34

Available in the detailed hard copy of report only.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

4

Key Investment Criteria

Breakthrough in international mining to lend volume growth – but margins

to be impacted

International mining volume sales for FY10 stood at 20,000 Tons. For FY11E we estimate

~40,000 Tons while for FY12E we estimate ~60,000 Tons in the international mining

business. This will be driven by the following key factors:

A. International mining breakthroughs and business potential:

AIA has been witnessing recent breakthroughs with various mining companies in Africa

in the area of copper, platinum and platinum group metals, and gold. Some of these

visible names are Anglo Platinum (South Africa), Konkola Copper Mines (Zambia),

Lonmin (Aouth Africa) and ARM Group in South Africa (for their Nkomati mines).

We estimate the following potential from these players for AIA:

Estimated potential for grinding media from new mining breakthroughs:

Client BALL Mill grinding media

Vale (Samarco, Vittoria)* 10,000-15,000 TPA to 30,000 TPA

Anglo Platinum 32,000-43,000 TPA

Konkola Copper 4,400-6,600 TPA

Lonmin 9,000-12,000 TPA

ARM Group 12,350-14,200 TPA

-Nkomati 950-1,300 TPA

Source: IFIN Research; * - as indicated by management of AIA

The total potential indicated above is in the area of ball milling, which is the target

market for AIA Engineering in the grinding media space.

In any mining operation globally, the standard milling or grinding or comminution

process includes a SAG mill as well as a BALL mill. The SAG mill (Semi Autogenous

Grinding) is generally large in size and is used to crush large pieces of rock (read: ore)

into smaller manageable pieces. It is the primary grinder in any milling operation. The

BALL mill is then used to further grind these smaller pieces of rock into smaller sizes of

ore. SAG mills are generally huge in size and cannot use high chrome grinding media

since the pressure generated in a SAG mill at times touches 20 bar, under which

circumstances, the high chrome grinding media tends to break. Hence forged iron is

always preferred in SAG mill operations. Our target potential for AIA Engineering

therefore lies in breaking through at the secondary grinding (BALL mill) level in various

mines. This again can hold true only for BALL mills which are smaller than 24 feet in

diameter. SAG mills may be as wide as 40 ft in diameter.

B. However, margins to be impacted in initial years of breaking through:

While AIA engineering may successfully convince its potential customers the benefits of

high chrome grinding media over forged, there are certain factors which are inevitable:

1. The key factor here is cost. In the mining industry, the highest cost component is

crushing and grinding (10-15%), followed by explosives and diesel cost to run mining

equipments. If a supplier is ready to cut margins to 10-15% in the first year of operation,

then only will it give him an initial entry to use the products. The cash cost of operations

is a very important factor globally in the mining industry. Later on, once the products

are approved and come into regular use, then one will always talk about increase in

prices due to rise in raw material prices, labour charges and energy expenses.

International mining to be future growth driver

Target market is ball mills only since forged iron is preferred in SAG mills.

Supplier will have to compromise on margins initially by pricing not more than 10-15% above forged for an initial entry for trials.

Estimate potential of 68,000 – 85,000 TPA (detailed on page 16-20)

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

5

Cost of producing copper in Central Africa:

Process % of total

Mining 46% Concentrating 11% Smelting 6% Leaching 13% Refining 2% Overheads 22%

Total 100%

Fixed Cost 60% Variable Cost 40% Source: IFIN Research

2. Risk of using new products in the system: the plant chief engineer or the plant head

is generally taking a risk on the production front by giving an opportunity to a new

player, against tested and in use products. Hence, he will be all the more interested in

looking at lower costing during initial trials.

3. The 6 months testing criteria: the typical time taken to test the full impact of the

newly introduced charge (grinding media) is 6 months. At any given trial, it is not

possible for the plant manager to shut down the mill and therefore charge has to be

continuously added through the day or once in a day. It generally takes 3 months to

empty the old charge which could be forged iron and another 3 months to allow the ne

charge of high chrome to be present in the mill completely. Hence the first 3 months

will not show the performance of the mill with the completely new charge. It is only

after completion of the first 3 months through refilling of the charge in the mill tested

for performance with a single company’s products. Hence the first one or two supplies

for 6 months will be considered as a trial supply and will have to be provided at very low

margins.

4. Only grinding balls are high chrome; liners are low on chrome: liners used in ball mills

in the world are always of forged material with small traces of chrome.

Source: IFIN Research

Forged High-Chrome

International Players

Magotteaux Belgium 262,751 √ √ √ √ √ √

Christian Pfieffer Italy 15,000 √ √ - √ - √

Estanda Spain Spain 8,000 √ √ - - √ √

Toyo Japan NA - - - √ - -

Anhui China 120,000 - - - √ - -

Aresco Egypt NA n/a n/a n/a √ n/a -

Firth Rickson UK NA n/a n/a n/a n/a √ -

Scaw Metals(Anglo American) S.Africa 700,000 - √ √ √ - √

Local Players

ACC Nihon (Hindustan Udyog) India n/a √ √ - - √ √

Balaji Industrial Products India n/a √ √ √ √ √ √

Balls and Cylpebs India n/a √ √ √ √ -

RN Metals India 18,000 - √ √ √ -

Aqua Alloys India 5,000 √ - - - √ √

Tega Industries India 6,200 - √ - - - √

Competitive scenario LocationCapacity

(Tons)Diaphragms

AIA Engineering India 172,000 √ √

LinersGrinding Media

√

Vertical

Mill Parts

Other Mill

Parts

- √ √

Crushing and grinding are single highest cost forming part of mining and concentrating @ 10-15% followed by explosives and diesel

It takes 3 months to flush out the existing charge (grinding media) and another 3 months to test the full impact of the newly fed charge.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

6

5. Cost competitiveness to Chinese: Chinese players are big players in the manufacture

and sale of grinding media. They are very price competitive in the international markets

on account of following key factors. However they lack in consistency and quality of

supplies, thereby hampering the production.

i. Chinese players import huge quantities of scrap steel from Africa for manufacture of

forged grinding media. Even high chrome grinding media uses scrap steel as a key

material component. AIA Engineering raw material composition primarily comprises

of 75% scrap steel, 23% Ferro chrome and 2-3% others.

ii. The liners, made of forged iron / high chrome, are scrapped and remade into

grinding balls for grinding purposes.

iii. The Chinese players work with small units of even 4000-5000 tons per annum, with a

supplier of steel rods at times carrying 20 rods in a truck and dropping 3-4 rods at

each supplier and hence have quite similar composition to one another (see table

below).

iv. The Chinese manufacturers get export subsidies from their government as well.

Similar composition of Chinese forged players

Forged grinding

media composition

SIMON

CHEN JINAN ZOUPING WE JINAN ZIBO

% Carbon 0.4-0.65 0.52-0.8 0.52-0.65 0.52-0.65 0.52-0.65

% Manganese 0.5-1.2 0.6-1.2 0.6-1.2 0.6-1.2 0.6-1.2

% Chromium 0.25 max - 0.25 max 0.25 max 0.25 max

% Silicon 0.15-0.37 0.15-0.37 0.15-0.37 0.15-0.37 0.15-0.37

% Phospherous <0.04 <0.04 <0.04 <0.04 <0.04

% Sulphur <0.04 <0.04 <0.04 <0.04 <0.04

Rockwell Hardness 50-60 55-65 50-60 50-65 50-63

Source: IFIN Research

Hence, when it comes to pricing, the competition with Chinese players will always be an

important factor.

However, the factor that plays in favour of players like AIA in grinding balls is superior

quality and steadiness of quality through supplies.

6. Local Manufacturing / Technology based competition from players like Magotteaux:

Magotteaux has traditionally on its website indicated mill internal production capacity

of 235,000 tons per annum as of 2007. This capacity, as per our various sources, at

present stands at approximate 300,000 tons per annum with manufacturing facilities

across continents to support the demand in the specific regions and keeping themselves

cost competitive. Magotteaux today has manufacturing facilities in Belgium, Thailand,

South Africa, Australia, China and others. This allows them to buy the scrap steel / scrap

chrome from the respective markets including their mill internal customers and reuse

the same in preparing new mill internals.

AIA has now decided to open a warehouse in Africa to meet the regular demand from

breakthroughs in the region. We have good reason to believe that the warehouse would

have opened closer to the Bushveld complex which is where key mining players are

housed in Africa. Company may also have to consider opening a warehouse in Brazil,

another region where mining players are largely based.

“For any mill internal supplier, liners are the way to go. There is more money to be made

in liners......”......international mining expert.

While the Chinese manufacturers are competitive on the pricing front, they are at times unable to set quality standards and product differentiation.

The similarity in composition of the Chinese manufacturers is quite evident.

Magotteaux focusing on value addition and new technological advancement like “SensoMag”.

AIA will open a warehouse in Africa to meet the demand where breakthroughs received.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

7

Magotteaux on the other hand is focusing on providing very strong technical backup and

support for clients and in return creating a market for their products. They are

developing new technologies such as the “SensoMag”.

What is SensoMag?

SensoMag is a magnetic sensor device which can be bolted onto a BALL mill. It is a

magnetic device and it can now measure the charge and the actual amount of balls in

the mill.

“It is the first time in 25 years I am seeing such an equipment......”.....international

mining expert.

So, they are looking at that aspect. So if one can buy such peripherals, they will feel

committed to buy other mill internals as well though one again needs to be price

competitive. This way they have a complete package and they are more professional

compared to an Indian or a Chinese.

This technology when bolted to the mills, tells you what percentage of the mill is

charged with balls. There is a radio transmitter on the device which communicates with

the outside and sends the signal to your control room so you can tell what levels of the

ball you have in the mill, and you can decide the charge.

This results in optimum utilisation leading to power savings and higher productivity.

Normally a mill operator charges the mill once a day on the day shift which is not the

right thing to do. One should be charging balls right through the day so that the

efficiency does not fall off otherwise day shift is the most efficient, afternoon shift is

lower and night shift is the most inefficient, and then one charges the next day.

However, with this new technology, one can also get a device from them which will add

3 balls per minute so that you have consistent performance in the ball mill.

“Going forward SensoMag will take a lot of pressure off the

operators.......”.......international mining expert

Forged iron mill internals are here to stay; however tremendous scope for

high chrome mill internals in BALL mills up to 20 ft diameter

We feel the need to dispel the thought process that high chrome mill internals can

completely replace forged mill internals and grinding media. THIS IS NOT GOING TO BE

POSSIBLE AT ALL.

Before we explain this, one need to understand that in any mining facility there is a

primary grinding process and then there is a secondary grinding process. The primary

grinding process is generally done using SAG mills (Semi Autogenous Grinding mills),

which grinds the large rocks into smaller pieces that are then let out for grinding into

the secondary grinding mill called the BALL mill.

SAG mills are generally more than 24 ft in diameter and go as large as 40 ft while BALL

mills are generally up to 24 ft in diameter.

Sensomag will help reduce the pressure on operators by directly sensing the optimum ball mill requirement to continuously feed the charge.

Forged media is here to stay

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

8

As per the indications provided by the management of AIA, the indicative market

potential for high chrome grinding media in mining stands as under:

Source: AIA Presentation 2009;

Pricing competitiveness with forged media

The primary difference between high chrome grinding media and forged media is the

extent in raw material terms is the extent of use of scrap steel for the manufacture of

grinding balls. The general trend of Ferro Chrome prices, used in the making of high

chrome grinding media, has been similar to scrap steel and exists to the extent of 20-

25% while the balance 75-80% is scrap steel. In case of forged, the scrap steel forms

100%.

A question that comes to ones’ mind is the how will AIA compete with forged media

players in an event of Ferro chrome prices rising abnormally higher than the scrap steel

prices. The chart below helps signify the same since such scenario was witnessed from

Jun’07-Dec’08. However, until FY08, the company had very little presence in the

international mining market. Going forward, such variation could have an adverse

impact on margins to an extent of 150bps.

Source: IFIN Research

India 25 KTIndia 25 KT

-

20

40

60

80

100

120

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Mar

-05

Jun-

05

Sep-

05

Dec

-05

Mar

-06

Jun-

06

Sep-

06

Dec

-06

Mar

-07

Jun-

07

Sep-

07

Dec

-07

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Rs /

Kg

Inde

xex

pric

es

Voltality in raw material prices causing change in realisation

Scrap (75%) Ferro Chrome (25%) Wt Avg Realisation (RHS)

Global Mining market for grinding media is estimated at 2.4 MTPA while for cement at 0.3 MTPA.

Margin pressure expected as AIA will compete with forged players who have exposure only to steel scrap.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

9

Shortage of large scale manufacturers of high chrome grinding media in

international markets; Company dominates domestic markets

AIA Engineering (AIAE) and Magotteaux are the only two companies in the world with

strong brand visibility and large production capacities to command a lion’s share in the

niche segment of high chrome grinding media, which is a fragmented industry with

several small players operating at various levels. On the domestic front, AIA engineering

enjoys the largest chunk of market shares @ 90% in cement and 70% each in power

utilities and mining. However, the mining market in India yields AIA only 3,000 TPA,

power utilities 14,000 TPA and cement 25,000 TPA. The market size is too small for long

term sustainability and hence the need to foray into international market. Almost all the

major cement companies such as ACC, Gujarat Ambuja, Ultra Tech, Grasim Industries

etc have their expansion plans tied up with the company. The balance is catered to by

conventionally used forged components or other high chrome/forged mill internal

players like ACC Nihon (Hindustan Udyog Ltd), RN Metals, Aqua Alloys and Tega.

In the mining space, AIAE’s client list includes Kudremukh Iron Ore Company, Hy-grade

Pellets, Hindustan Zinc Bharat Aluminium Company. The utilities space consists of

customers such as the OEMs to the thermal power sector and major thermal power

plants. The company also has an 18 year long term contract with BHEL (OEM to the

thermal power segment).

Magotteaux on the other hand is the largest player globally with a total production

capacity(CY07) (excl JV) of 235,000 MT vis-a-vis AIA engineering which has a present

capacity of around 172,000 MT up from 65,000 TPA in FY06 owing to the commissioning

of the Moraiya plant. However, as per our estimated and indicative guidance by industry

experts, Magotteaux may have a capacity of 300,000 MTPA until Dec’09. The company

has a manufacturing facility in Thailand with estimated capacity of ~70,000 MTPA. The

company also has manufacturing facilities in Belgium, China, South Africa, Brazil,

Australia and USA.

Increased capacity to help meet demand from new breakthroughs in

international mining

The company has built its capacity from 65,000 tons in FY06 to about 165,000 tons at

present. The company is in the process of debottlenecking its plant to build up capacity

to 200,000 tons to be available by Q3FY11.The company is debottlenecking its Odhav

plant and also building up a third line at its Changodar facility for the same, both in

Ahmadabad.

The Nagpur unit (Formerly Paramount Centrispun Castings) has also become

operational. The company expects to incur capex of around Rs 400 mn for the same.

Also, with breakthroughs achieved in international mining and increased demand of

40,000-50,000 tons coming in for FY11 the company would need incremental addition

to capacity to meet this demand. For the same the company has planned brownfield

expansion of capacities at existing facilities by another 30,000-40,000 TPA. This facility

will require a funding of around Rs 750 mn-800 mn over FY11 and FY12 and is expected

to be ready by end of FY12.

Magotteaux is the largest player globally with a capacity of ~300K TPA followed by AIA with 172K TPA

Increased demand from international mining to be met through increased production capacities to 200K TPA.

Capex of 40,000 Tons of which 20,000 TPA to be towards Vertical mill parts

Domestic Grinding media sales of AIA: Cement 25,000 tpa Utilities 14,000 tpa Mining 3,000 tpa

TOTAL 42,000 tpa

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

10

Source: IFIN Research

AIA Engineering has in the past increased their production capacities to meet the ever

growing demand for the business, post their IPO in 2005. The current production

capacity of the company stands at 165,000 tons per annum. The company is further

planning to de-bottleneck their capacities up to 200,000 tons per annum.

AIA has been expanding capacities in the past which has led to the sales to capital

employed ratio dipping from ~2.0x levels to ~1.0x. While de-bottlenecking at the current

sites will help improve this marginally, we expect the same to stay at ~1.0x on account

of further capex required in future to scale up capacities by further 100,000 TPA. With a

pick up in the international mining business, we expect significant uptick in volumes for

the coming years.

Source: IFIN Research

Cement and mining activity uptick in global and domestic markets

The outlook for the domestic cement industry is positive on the back of favourable

factors such as revival of the housing sector, speedier project execution of infrastructure

projects and the increase in plan outlay of the Union Budget for rural housing and

infrastructure from Rs 207 bn in FY10 to Rs 299 bn for FY11.

Cement production is expected to grow by 13% in FY11 owing to buoyant demand and

the government impetus on infrastructural growth for the economy.

0

50,000

100,000

150,000

200,000

250,000

FY09 FY10 FY11E FY12E

MT

Total Sales and Mining Volume(MT)

Mining Sales Capacity

1.74

1.20

2.05

1.73

1.98

1.23 1.01

1.08 1.23

0.99 1.00 1.02 1.00

-

0.5

1.0

1.5

2.0

2.5

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

E

FY

11

E

FY

12

E

FY

13

ESales : Capital Employed (x) (capex driving down the ratio)

32,000 MT

115,000 MT

65,000 MT

165,000 MT

debottlenecking

to 200,000 MT

New capacity 100,000 TPA

Debottlenecking capacity from 172K TPA to 200K TPA

Sales:Capital Emp-loyed to hover around 1x

100,000 TPA plant not to be set up in SEZ

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

11

Source: CMIE

As per the Planning Commission estimates, investment in roads and bridges and power

will grow by a CAGR of 13% from FY08, which will pave the way for increased capacity

additions for the cement sector.

Source: Planning Commission

The global cement industry is stabilizing after being depressed in late 2009 due to the

economic downturn in the developed economies. Demand in the key continents of

North America and Europe continues to be low with only a gradual recovery expected.

Emerging markets such as Africa, India and China are to drive the global demand for

cement going forward with companies being aggressive in building up capacities in

these growth regions.

0

2

4

6

8

10

12

14

FY06 FY07 FY08 FY09 FY10E FY11E

Cement Production Growth YOY (%)

0

100

200

300

400

500

600

700

FY08 FY09 FY10 FY11 FY12

Rs

bn

Indian Infrastruture Spend (Rs bn)

Roads & Bridges Electricity

Cement prodn. to grow @13% in FY11E (CMIE)

Spending on infra to grow at CAGR of 13%

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

12

Source: LaFarge

The company derives almost 80% of its revenues from the cement sector which over the

last years has exhibited CAGR of 7%. Even during the 2009 recession the global demand

posted growth with 90% emanating from emerging economies, which holds the

company in good stead as the growth in the cement industry is sustainable.

The domestic mining sector after a year of low growth in FY09 is expected to post

substantial growth in FY10 and FY11 on account of heightened demand from the

construction, automobiles, consumer durables and the power sector. Robust growth in

automobile sales, capital goods and revival in construction & infrastructural activity is

expected to increase steel production and aluminium production. Copper being an

important constituent in cables, wiring and other ancillary equipment, will exhibit

increase in production due to the country’s massive power expansion programme under

the 11th five year plan.

Source: CMIE

Globally the mining sector has witnessed increase in commodity prices primarily driven

by the USD 586 bn stimulus package for infrastructure spending by China. Thus

production also has risen as major mining companies have supplied substantial volumes

to China. With China leading the way, the mining sector has witnessed renewed interest

in mining activity.

Emerging Markets-90%

0

250

500

750

1000

1250

1500

1750

2000

2250

2500

2750

3000

3250

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mill

ion

To

nn

es

Global Cement Demand

Mature Markets-10%

0

2

4

6

8

10

12

FY06 FY07 FY08 FY09 FY10E FY11E

Mining Growth(IIP) YOY (%)

Improving economic scenario lends reasonable growth to domestic cement business.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

13

Sustainability of Business Model

The company’s replacement demand forms ~70-80% of its sales which consists of mainly

the worn out media which need to be replaced over a period of time depending upon

their wear rate and abrasion index of different ores. Hence even in a downturn, when

companies defer or go slow on their capex, the replacement demand will hold the

company in good stead to garner sales which leads to a healthy and sustainable

business model for the company. The company derives almost 80% of its sales from the

cement sector.

Consequently even when the cement markets are depressed internationally (in FY10)

major markets such as North America and Europe, the company maintained its cement

tonnages at substantial levels of the FY09 volume (pre-depression) exhibiting their

robust business model.

Replacement demand analysis Q1 Q2 Q3 Q4

Sales FY09 (Cement+Mining+Utilities)* 21,172 26,900 23,928 23,348

Sales FY10 (Cement + Utilities) 16,400 18,718 23,813 23,880

Percentage Demand Maintained 77% 70% 100% 102% * Total mining sales in FY09 was 8,000 Tons.

AIAE

Replacement

Demand

70%

Continuous replacement of worn

out parts

Annual Replacement of worn out parts

Project

Demand

30%

OEM Greenfield Projects

Replacement demand forms 70% of company sales volume which stands in good stead in low capex phases.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

14

Key Investment Risks

Volatility in currency movements and raw material prices

The company derives about 50-55% of its sales from exports and hence hedging this risk

forms an integral part of the company’s agenda. The company total derivative losses for

9MFY10 stood at Rs 314 mn. Notional Mark to Market loss on outstanding derivative

contracts, maturing in 2012 stood at a much improved Rs 540 mn for 9MFY10 compared

to Rs 1.36 bn as on March 31, 2009, owing to the substantial appreciation of the rupee

from Rs 50 levels to current levels of Rs 44.

Source: Bloomberg

With increased sales coming in from the international mining segment, significant

depreciation of the Indian rupee can have an impact on the profitability of the company

and hence currency fluctuations pose a considerable risk to the bottom-line growth of

the company.

Source: IFIN Research

Realisations are a function of product mix and raw material prices. As the company

follows a pass through policy, the input prices form key drivers for the profitability of

the company. The crash in input prices in FY09 led to fall in realisations for the company

from Rs 113/kg in Q4FY09 to Rs 86/kg in Q3FY10. From the above chart it’s observed

that realisations are moving with a 3-6 months lag effect to the key raw material prices.

40

42

44

46

48

50

52

23/0

3/20

09

13/0

4/20

09

22/0

4/20

09

13/0

5/20

09

21/0

5/20

09

29/0

5/20

09

22/0

6/20

09

30/0

6/20

09

20/0

7/20

09

28/0

7/20

09

17/0

8/20

09

26/0

8/20

09

16/0

9/20

09

25/0

9/20

09

21/1

0/20

09

29/1

0/20

09

19/1

1/20

09

27/1

1/20

09

18/1

2/20

09

30/1

2/20

09

19/0

1/20

10

28/0

1/20

10

19/0

2/20

10

15/0

3/20

10

25/0

3/20

10

15/0

4/20

10

23/0

4/20

10

13/0

5/20

10

21/0

5/20

10

INR

INR/USD

-

20

40

60

80

100

120

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Mar

-05

Jun-

05

Sep-

05

Dec

-05

Mar

-06

Jun-

06

Sep-

06

Dec

-06

Mar

-07

Jun-

07

Sep-

07

Dec

-07

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Rs /

Kg

Inde

xex

pric

es

Voltality in raw material prices causing change in realisation

Scrap (75%) Ferro Chrome (25%) Wt Avg Realisation (RHS)

With increasing share of international mining, AIA will be exposed to two new major risks: 1. Currency

fluctuations 2. Commodity

volatility especially with differential price increase in Ferro Chrome and Scrap.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

15

On an analysis of key raw material prices from March 05, it was observed that the

weighted average cost of the product and scrap cost generally move in tandem barring a

few quarters from September 07- September 08. This majorly reduces the degree of risk

to the company in the mining segment, where the company has to compete with forged

media players.

Source: IFIN Research

However, if Ferro chrome prices (being 25% of the product composition and 40% of the

cost) move in a 10% deviation from steel scrap, the impact on margins can be 100-200

bps. This scenario has not impacted the company till FY09 as the company almost had

NIL sales from the overseas mining segment. But going forward as the international

mining segment volume rises, this phenomenon could pose a sizeable risk to the

company’s overall margins.

Upcoming new technologies - Vertical Mills

Vertical Mills are mills which use the concept of stirring along with attrition for grinding.

Grinding is primarily done with a helix screw which maximises grinding efficiency by

imparting high pressure between the feed material and the grinding media.

In a ball mill, 30% of the energy is spent only in the tumbling action of the mill and as

the vertical mill is based on the concept of stirring it results in energy savings up to 30%-

40%. Also it occupies only half of the area of a ball mill among other advantages such as

lesser noise, downtimes and installation costs. The vertical mill also has better drying

ability and the internal temperature can be controlled to suit the varied temperature

needs of the input feed.

Ceramic or steel grinding media is usually preferred in vertical mills and there is no

scope for high chrome grinding media in the same. Also it uses only 25% of the grinding

media required in a ball mill resulting in purchase and energy cost savings for the mining

company. Owing to all these advantages, vertical mills are steadily gaining popularity all

over the world with OEMs such as Metso, Atox, Polysius etc.

Although it poses a risk in the near future as far as grinding media is concerned, vertical

mills constitute a very small portion today (about 1%-2%) and ball mills continue to

dominate the market. Also, the company is expanding their range of manufacturing

vertical mill parts which will substitute the loss of business in grinding media, if any, and

instead provide better realisations and margins.

75

60

25

40

0

10

20

30

40

50

60

70

80

Proportion of Weight(%) Proportion of Cost(%)

%

Key Raw Material -Weightages

Scrap Ferro Chrome

Deviation of 10% between Ferro Chrome and Melting scrap will have impact of 120bps on margin

Ceramic grinding media is preferred in vertical mills

AIA is expanding their offerings into the manufacture of vertical mill parts to de-risk their business model.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

16

Increase in market share in international markets will attract competition

on account of high margin (+20%) and healthy return ratios (20%)

With the company steadily making inroads into the overseas mining segment

(~2.4million TPA including India), attractive return ratios could induce increased

competition especially from China. China imports cheap scrap from Africa to

manufacture forged grinding media. They have scattered foundries all over the country

which offer forged media at extremely competitive prices although not of the best

quality.

In the case of Chinese manufacturers offering high chrome mill internals to the market

in the long run, the company could face a serious threat on the pricing front for the

same. However the Chinese players will continue to lag on quality, continuity of regular

supplies, total solutions provider capabilities vis-a-vis global quality majors like

Magotteaux and AIA Engineering.

Margin and ROE to dip in the long term

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

17

Valuations DCF Assumptions:

WACC DCF Value

Risk free rate 7.5% Perpetual Growth

4%

Beta 0.8 PV of forecast period i.e. FY25E (Rs bn) 20,931

Risk Premium 5.0% PV of terminal value (Rs bn) 15,859

Cost of Equity 11.5% Firm Value (Rs bn)

36,790

Cost of Debt (post Tax) 6.3% Less: Net Debt (Rs bn) (3,310)

Debt : Equity 0.10 Equity Value (Rs bn) 40,100

WACC 11.2% Per share (Rs.) 425

(Rs mn ) FY10 Wt. After tax

cost WACC

Net worth 9,099 0.95 11.5% 10.9%

Debt 490 0.05 6.3% 0.3%

11.2%

Terminal growth

rate 10.0% 10.5% 11.0% 11.20% 11.5% 12.0% 13.0%

2% 453 424 397 386 374 354 318

3% 480 446 416 403 390 367 328

4% 517 475 440 425 410 383 339

5% 567 515 472 454 435 404 354

PE (x) basis of valuation

At CMP of Rs 398, stock is trading at 19x FY11E and 17x FY12E EPS of Rs 21 and Rs 23.6 respectively.

On a PE basis, even if we value AIA engineering at 22x FY11E EPS, we arrive at a target price of Rs 462. At this

price, the stock would be trading at 19.5xFY12E EPS. We believe that significant breakthroughs in the mining

space could lead to better than expected volumes from international mining, lending upsides to our EPS in

FY12E and re-rating in the stock.

We initiate coverage with an Overweight rating on the stock with a target price of Rs 444 based on an

average of DCF value of Rs 425 per share and PE(x) based value of Rs 462 per share.

0

100

200

300

400

500

600

De

c-2

00

5

Feb

-200

6

Apr

-200

6

Jun-

20

06

Au

g-2

00

6

Oct

-20

06

De

c-2

00

6

Feb

-200

7

Apr

-200

7

Jun-

20

07

Au

g-2

00

7

Oct

-20

07

De

c-2

00

7

Feb

-200

8

Apr

-200

8

Jun-

20

08

Au

g-2

00

8

Oct

-20

08

De

c-2

00

8

Feb

-200

9

Apr

-200

9

Jun-

20

09

Au

g-2

00

9

Oct

-20

09

De

c-2

00

9

Feb

-201

0

Apr

-201

0

AIA Engineering - PER Band Chart - 1 year forward

Adj. Share Price 12x 18x 24x 30x

30x

24x

18x

12x

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

18

Key Assumptions Sales Volume

Tons FY09 FY10 FY11E FY12E

Domestic 41,000 42,000 46,200 50,820

Export 54,348 61,011 85,100 108,708

- Mining 6,000 20,011 40,000 60,000

- Others 48,348 41,000 45,100 48,708

Total 95,348 103,011 131,300 159,528

Average Realisation

Rs mn / Ton FY09 FY10 FY11E FY12E

Average Realisation 0.107 0.092 0.090 0.087

Raw material price and mix assumptions

FY09 FY10 FY11E FY12E

Key raw material prices

Scrap (Rs / Ton)* 24,765 18,104 22,000 25,000

Ferro Chrome (USD/Ton)** 4,400 2,026 2,400 2,700

Raw material mix

Scrap (%) 77.7 77.0 75.0 75.0

Ferro Chrome+Other (%) 22.3 23.0 25.0 25.0 * Scrap - Source: HMS-1, Delhi - CMIE

** Ferro Chrome - Source: Bloomberg - 6-8% C, 60% Cr max 15% SI major EU destination

Sensitivity Analysis Sensitivity to Volume and Average Realisation

FY11E

FY12E

Bear Base Bull

Bear Base Bull

Sales Volume (MT) 125,000 131,300 140,000

150,000 159,528 175,000

Average Realn (Rs mn / MT) 0.085 0.090 0.095

0.084 0.087 0.100

Revenue (Rs mn) 10,625 11,817 13300

12,600 13,879 17500

EBITDA (%) 23.3 24.4 25.5

23.0 23.7 25.0

PAT (Rs mn) 1,686 1,985 2356

1,947 2,223 3014

EPS 17.8 20.9 24.9

20.5 23.5 31.8

PE(x) 22.4 19.0 16.0

19.4 16.9 12.5

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

19

Financial Analysis

Debottlenecking to improve sales to capital employed in FY10-11; However,

further capex for 100,000 TPA to keep ratio <=1x

An analysis of the sales to capital employed ratio shows that whenever the company

increased its capacity, the capital employed to turnover ratio has substantially

decreased in various phases.

This, points to the fact that there was always scope for improving the utilisation of the

additional capacity. Hence the company is now in the process of streamlining and

debottlenecking its operations to take the capacity to 200,000 tons. We expect this to

improve the ratio to a level of 1.07 by FY12. Subsequently after the commissioning of

the 100,000 tons new capacity, we see the ratio hovering around ~1x by FY13.

Source: IFIN Research

Low Debt and Healthy cash position to assist in expansion and acquisition

Source: IFIN Research

The company is generating substantial cash flow from operations owing to steady

growth in profits, healthy margins and effective working capital management in FY09

and we expect the company to generate around 1.05 bn of the same in FY10. Robust

bottom-line and margins coupled with no major capex has also led to free cash flow

generation which is a positive sign for the company.

1.74

1.20

2.05

1.73

1.98

1.23

1.01

1.08

1.23

0.99 1.05 1.05

1.00

-

0.5

1.0

1.5

2.0

2.5

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0E

FY1

1E

FY1

2E

FY1

3E

Sales : Capital Employed (x) (capex driving down the ratio)

32,000 MT

115,000 MT

65,000 MT

165,000 MT

debottlenecking to 200,000 MT

New capacity

100,000 TPA

-1500.0

-1000.0

-500.0

0.0

500.0

1000.0

1500.0

2000.0

2500.0

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0E

FY1

1E

FY1

2E

Rs

mn

Cash Flow from Operations and Free Cash Flow

Cash Flow From Operations Free Cash Flow

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

20

From FY11 onwards, we expect a dip in these on account of following factors:

a. Incremental International Mining order breakthroughs leading to higher volumes.

This will increase the delivery cycle for overseas mines leading to stretch in the

working capital cycle.

b. The company will be investing ~Rs 1.3 bn in FY11 and FY12 for brown field

expansion of capacities.

c. The company is virtually a debt free company and has surplus cash balance of Rs

3.54 bn as on December 31, 2009.This includes around Rs 480 mn of the unutilised

proceeds of the QIP done in December 2006.

Source: IFIN Research

Owing to a healthy cash position, the company is comfortably placed to finance its

planned capex or look at a value accretive acquisition. The company may also look at

foraying into other areas like wind power in the future for captive usage leading to

backward integration for the same.

Return Ratio analysis

Source: IFIN Research

We expect the company to maintain ROE and ROCE around ~20% and ~26% respectively

for FY10-12E. We expect return ratios to dip in FY10 in an event of lower realisations

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

-5000

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

Rs m

n

Cash Position and Net Debt

Cash Position Net Debt Net Debt to Equity Ratio(RHS)

36.1 35.4

31.2 31.5

33.8

26.727.6

26.4

33.0

30.1

25.0 24.4 24.8

19.9 20.319.2

15.0

20.0

25.0

30.0

35.0

40.0

FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

(%)

Return Ratios - ROCE / ROE

Return on Capital Employed (ROCE) Return on Equity (Shareholders funds) (ROE)

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

21

due to correction in key raw material prices and increased contribution of international

mining segment.

Stretch in working capital cycle ahead

From FY05 onwards it is observed that the company has significantly reduced its debtor

days from 120 days to around 65 days in FY09, implying that the company has

implemented an effective receivables policy for the same. However, going forward, with

increased exposure to international mining, we expect receivables and inventory levels

to harden to 90 days and 60 days respectively on account of the typical nature of

working capital involved with the international business.

The breakthrough in international mining will lead to lengthening of the working capital

cycle due to the additional time taken for shipment and delivery. We expect inventory

days and debtor days to be in the range of 90-120 days for FY11 and FY12 respectively.

Source: IFIN Research

The company also has optimised its current ratio levels from FY07 onwards to a

comfortable level of 3:1 and we expect the company to maintain the same in the years

ahead.

Source: IFIN Research

52.1 53.7

68.6 71.8

49.754.3

60.2 62.0

116.9110.3

99.292.3

65.9

79.084.0 87.5

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0E

FY1

1E

FY1

2E

Day

s

Inventory and Debtors turnover (days)

Inventory turnover ratio (days) Debtors turnover ratio (days)

3.9

2.6

2.3

2.62.8

3.13.2 3.1

2.9

2.1

1.71.9

2.42.6 2.6

2.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

FY05

FY06

FY07

FY08

FY09

FY10

E

FY11

E

FY12

E

Current Ratio

Current Ratio Acid Test Ratio / Quick Ratio

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

22

Breakthrough in mining to lead to margin reduction

Source: IFIN Research

The company has maintained healthy EBIDTA margins in the range of 24-25% in the

recent past. Henceforth owing to increase in contribution from international mining

sales, wherein realisations are at a 40% discount to the cement realisations of around Rs

90-100 per kg, we expect a dip of 100-200 bps from FY10 levels in margins.

The realisation is much lower as the company in the initial phases will be only supplying

grinding balls to the mines. Over a period of time, the grinding media will be regularised

and AIA will look to provide the complete solutions to mining companies including their

liners. However, the same will take at least 2-3 years to be implemented.

Source: IFIN Research

13.2

20.0

23.8 23.7 24.125.9

24.5 23.7

9.2

13.4

18.319.4

16.7 17.6 16.9 16.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

FY05

FY06

FY07

FY08

FY09

FY10

FY11

E

FY12

E

%Margins

EBITDA margin(%) Adjusted PAT margin(%)

0.083

0.069

0.079 0.081

0.107

0.092 0.0900.087

0.040

0.050

0.060

0.070

0.080

0.090

0.100

0.110

0.120

FY05

FY06

FY07

FY08

FY09

FY10

FY11

E

FY12

E

%

Average Realisation (Rs mn / MT)

Average Realisation (Rs mn/ MT)

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

23

SWOT Analysis

STRENGHTS WEAKNESS

Largest high chrome grinding media player in India

and second largest globally after Magotteaux.

Technically strong management with ~30 years of

experience in the industry.

Technical expertise obtained from Magotteaux

under Settlement Deed of 2000.

Cannot be bought over by Magotteaux until 15

years, starting 2000, as per Settlement Deed.

Management control has to exist in AIA to continue

using the technology without payment of royalty.

Total solution provider capability for user industry

to optimise cost and output.

Ability to quickly scale up capacity on account of

strong cash flows and ability to service debt.

Low/ nil debt on the books.

Labour cost arbitrage against competitors like

Magotteaux.

Once breakthrough achieved and regularised, AIA

stands to gain from regular business on account of

replacement demand.

Pricing is the key – in the short-medium term

company cannot afford to be >10-15%

expensive than forged media while in the long

term not more than 20%.

AIA’s immediate competitor – Magotteaux –

has developed a reputation for possessing

strong technological capabilities, strong brand

image and a complete solutions provider.

None of AIA’s facilities are in tax free or export

oriented zones thereby losing the price

competitiveness to that extent.

Lower arbitrage in labour cost, export

subsidies, economies of scale versus Chinese

however, better off against global players.

In the initial years of breakthrough, AIA will

have to compromise on margins.

High dependency on global cement and

domestic consumption markets to lead to drop

in volume growth in eventuality of a global

slowdown.

OPPORTUNITIES THREATS

AIA may look at getting into forged grinding balls

since their liners are anyways forged, thereby

competing with Chinese players on pricing, quality

and consistency and also target mill > 20 ft diameter

Huge potential in international mining markets

whose estimated mill internals market size is ~2.4

MTPA against cement which is 0.3 MTPA.

Competing with existing forged / high chrome

players and improving overall cost of operations.

Setting up manufacturing facilities in densely mined

areas such as South Africa, Brazil, Indonesia, etc in

eventuality of company not setting up facilities in

trade free zones or tax free zones.

Aggressive foray into liners in international mining

markets, leading to higher realisation vis-a-vis

grinding balls.

AIA is now foraying into supplying grinding media

for new sectors such as Platinum Group Metals,

Gold and Copper. This will de-risk the model from

sole dependency on cement and power utilities

sector.

Chinese players, supported by export subsidies

and undervalued currency, may further drop

prices of forged products, leading to potential

erosion in margins.

Large scale use of vertical mills for soft ores like

limestone, kaolin and others, will reduce

consumption of grinding media drastically.

With economies of scale gaining significance,

mines are moving towards large mills more

than 20 ft in diameter. The target market for

AIA is only ball mills up to 20 ft in diameter.

Increase in exports will lead to greater

exposure to foreign currency volatility.

Patents and copyrights by other international

competitors in various products in other

regions could hamper foray into such markets.

Increase in labour cost on account of higher

payouts under Minimum Wages Act and

increase in tax outgo on account of New Direct

Tax Code to be introduced in 2011 could

hamper pricing competitiveness.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

24

Business Background

Background

AIA Engineering Ltd (AIAEL) is promoted by Mr Bhadresh Shah, a metallurgical engineer

from IIT Kanpur and began operations in 1978 and is a niche manufacturer of

impact/abrasion/corrosion resistant high chrome castings. The company had a joint

venture with Magotteaux International S A, Belgium from 1991 to 2000. On 16 Feb

2000, Mr Bhadresh Shah bought out the 51% stake of Magotteaux in the erstwhile AIA

Magotteaux Ltd for a sum of Rs 400 mn. Post that, the company was renamed to AIA

Engineering Ltd on 2 May, 2000 and was listed in December 2005.

The company enjoys a virtual monopoly in the high chrome mill internals space in the

domestic sector and operates in a duopoly in the overseas market. The company derives

majority of its revenues from the cement sector.

Company Structure

Business

The company is in the business of manufacturing high chrome mill internals for use in

the cement, power and mining industries through the process of sand casting. The

company categorises their offerings as follows:

AIA Engineering Ltd

Manufacturing Subsidiary

Capacity-42,000 MT

Welcast Steels Ltd

Own Manufacturing

Capacity-130,000 MTMarketing Subsidiaries

Vega Industries( (Middle East) F.Z.E

Vega Industries Ltd U.K

Vega Industries Ltd USA

Product Portfolio

Tube Mill Internals

Grinding Media Liners Diaphragms

Vertical Mill Internals

Roller and Table Liners

HRCS Castings

Dipping Tubes Cooler Grates

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

25

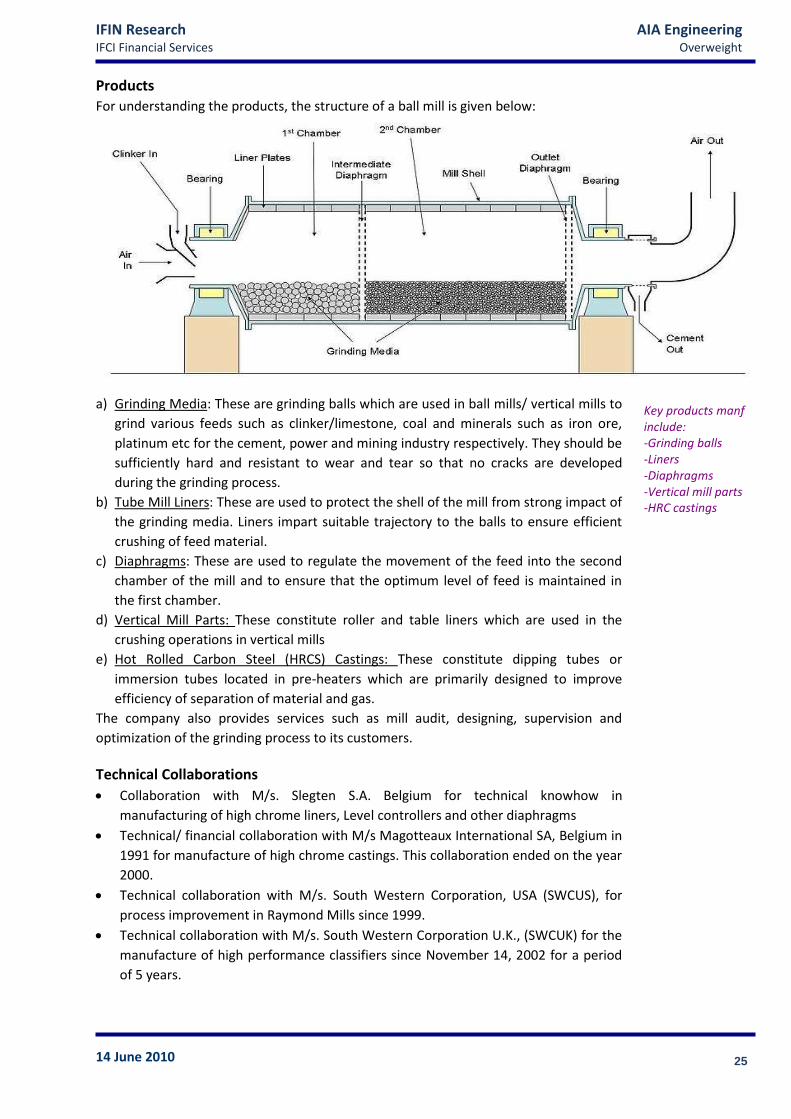

Products

For understanding the products, the structure of a ball mill is given below:

a) Grinding Media: These are grinding balls which are used in ball mills/ vertical mills to

grind various feeds such as clinker/limestone, coal and minerals such as iron ore,

platinum etc for the cement, power and mining industry respectively. They should be

sufficiently hard and resistant to wear and tear so that no cracks are developed

during the grinding process.

b) Tube Mill Liners: These are used to protect the shell of the mill from strong impact of

the grinding media. Liners impart suitable trajectory to the balls to ensure efficient

crushing of feed material.

c) Diaphragms: These are used to regulate the movement of the feed into the second

chamber of the mill and to ensure that the optimum level of feed is maintained in

the first chamber.

d) Vertical Mill Parts: These constitute roller and table liners which are used in the

crushing operations in vertical mills

e) Hot Rolled Carbon Steel (HRCS) Castings: These constitute dipping tubes or

immersion tubes located in pre-heaters which are primarily designed to improve

efficiency of separation of material and gas.

The company also provides services such as mill audit, designing, supervision and

optimization of the grinding process to its customers.

Technical Collaborations

Collaboration with M/s. Slegten S.A. Belgium for technical knowhow in

manufacturing of high chrome liners, Level controllers and other diaphragms

Technical/ financial collaboration with M/s Magotteaux International SA, Belgium in

1991 for manufacture of high chrome castings. This collaboration ended on the year

2000.

Technical collaboration with M/s. South Western Corporation, USA (SWCUS), for

process improvement in Raymond Mills since 1999.

Technical collaboration with M/s. South Western Corporation U.K., (SWCUK) for the

manufacture of high performance classifiers since November 14, 2002 for a period

of 5 years.

Key products manf include: -Grinding balls -Liners -Diaphragms -Vertical mill parts -HRC castings

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

26

Production capacity

The company is looking at enhancing its capacity up to 200,000 MT through de-

bottlenecking and streamlining certain plants to be available by 1QFY11. The Company

has also firmed up plans for setting up another High Chrome Mill Internals unit with the

capacity of additional 1,00,000 TPA at a suitable location, but not in the originally

planned SEZ as before.

Management

The management of the company is majorly independent in nature with only one

Independent Director out of 5 holding interests in AIA or affiliated subsidiaries. This is

Mr Vinod Narain who is also the Chairman of Welcast Steels.

Rajendra Shah

Non Executive Chairman; Independent Non Executive Director – AIA Engineering

Non Executive & Independent Director – Transformer and Rectifier

He is an Ahmadabad-based industrialist, he is a vital member of the AIA think tank and a

key contributor in important policy decision making. He was awarded “Best

Entrepreneur” by Ahmadabad Management Association in 2001.

Bhadresh Shah

MD and Executive Director – AIA Engineering

Director – Welcast Steels (subsidiary of AIA Engineering)

Director – Paramount Centrispun Casting (merged with AIA Engineering)

Former Director – Reclamation Welding (merged with AIA Engineering)

He is a metallurgical engineer from IIT Kanpur, he is the founder of AIA Engineering. His

vision and positioning AIA as a niche metallurgical products Company has placed it

among the top three global Companies in the mill internals space. Mr Shah started Gray

Cast Foundry Works in 1976 to produce small castings in manganese steel, cast steel

and cast iron castings. He founded Ahmadabad Induction Alloys Pvt Ltd (the predecessor

to our Company) in 1978, a company engaged in manufacture and supply of steel, alloy

steel and alloy iron castings used in cement, utility and mining industries. In March

1991, Magotteaux India Pvt Ltd was incorporated to which Ahmadabad Induction Alloys

Pvt Ltd. was merged effective from April 1991 (source: AIA RHP).

Vinod Narain

Independent Non-Executive Director – AIA Engineering

Chairman – WELCAST STEEL

He is the Independent Non-Executive Director of AIA Engineering Ltd. He is an

Industrialist based in Bangalore and the founder of Welcast Steels Ltd. He possesses

National Certificate Course of Mechanical Engineers from .Birmingham, England and is

also a Fellow of the Institution of Valuers and possesses rich and varied experience in

corporate management.

Samakulam Ganesh

Independent Non-Executive Director of AIA Engineering

Served as an Independent Director of Aries Agro

Served as a Consulting Advisor to TCS, Mumbai

Worked as an Advisor to the Essar Group.

Bhadresh Shah - Key person with technological expertise driving this business.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

27

He has B. Tech (IIT), S.M. (Management) Sloan School of Management, MIT, USA, PhD

(Business Studies) London Business School, UK. He is a Management Consultant. He was

a former Senate Member of IIT Bombay; Professor of IIM Ahmadabad; visiting Professor

at various Management Institutes like Andersen Graduate School of Management UCLA,

USA, University of Virginia and S.P. Jain Institute of Management Research, Bombay.

Presently he is a visiting Senior Professor at Narsee Monjee Institute of Management,

Mumbai.

Bhupendra Shah

Independent Non-Executive Director of AIA Engineering Ltd.

He is a Chemical Engineer from IIT, Kanpur with a Masters in Science from the University

of California, Berkeley, USA, his domains of expertise span finance and administration.

Sanjay Majmudar

Independent Non-Executive Director of AIA Engineering Ltd

Independent Non Executive Director – Aarvee Denim

Independent Non Executive Director – Dishman Pharma

He is a practicing Chartered Accountant (S Majmudar and Associates). His financial

acumen facilitates the financial planning for the multiple projects that the Company

undertakes.

S Srikumar

Non Independent Non Executive Director – AIA Engineering

Company Secretary – I Power solutions (e-business IT solutions Provider Company)

He has M. Tech (Industrial Engg.). He has completed his Ph.D in 1988 and holding PGDM

from AIMA. He possesses vast knowledge and experience of Industry, Project

Management, Technical Evaluation, Engineering Coordination and Administration.

Manufacturing facilities

Facility at Ahmadabad for grinding media and small castings

Facility at Ahmadabad for big sized mill internals

Facility at Foundry unit at Nagpur for manufacture of conventional grade industrial

castings having the capacity of 5000 TPA – on account of merger of Paramount.

Welcast Steels Limited-Manufacturing facility for grinding media at Bangalore –

subsidiary of AIA – manufacturing capacity of 40,000 TPA.

Consolidated manufacturing capacity of 172,000 TPA

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

28

Manufacturing Process

Source: AIA Engg - RHP

0

50,000

100,000

150,000

200,000

250,000

FY09 FY10 FY11E FY12E

MT

Total Sales and Mining Volume(MT)

Mining Sales Capacity

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

29

Mining Process

Source: FL Smidth

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

30

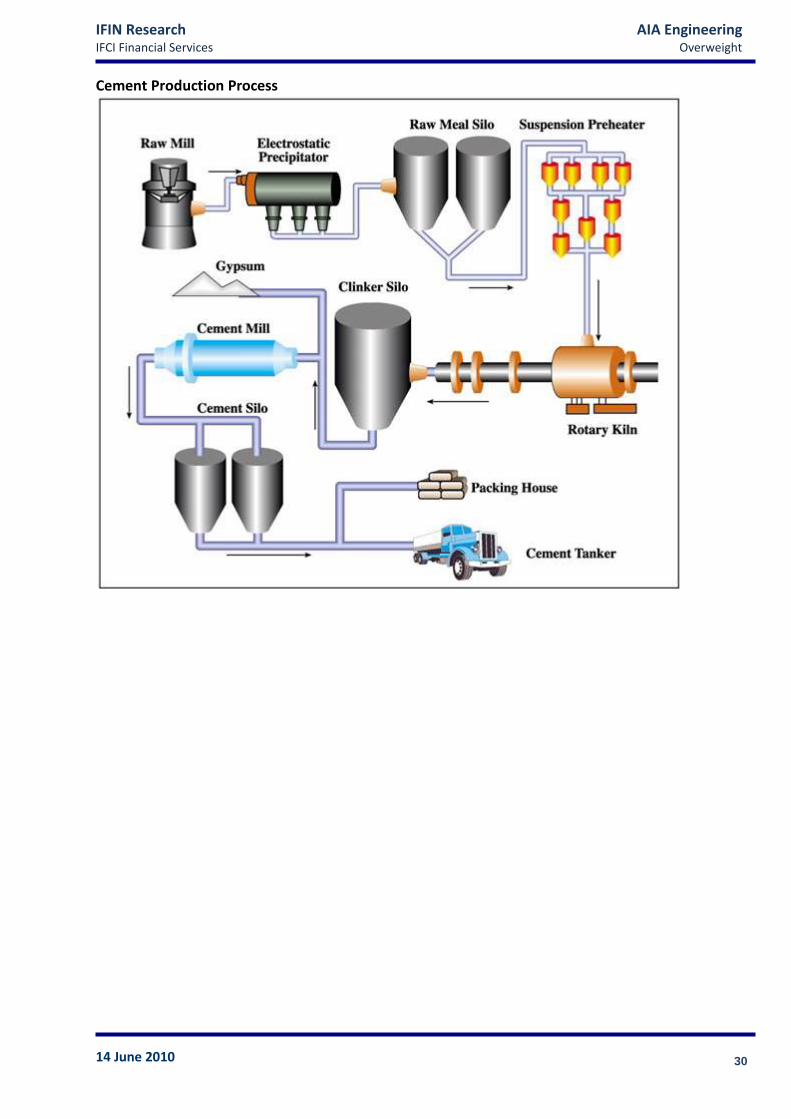

Cement Production Process

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

31

GROWING COMPETITIVE TECHNOLOGIES

HIGH PRESSURE GRINDING ROLLS – competition for SAG mills

Comminution processes account for the largest portion of energy consumption in mining operations. This has

led to new technologies being constantly developed. With increasing economic pressures, the emphasis is now

on reducing unit costs by making equipment larger and through use of technologies with lower operating

costs. This trend can be seen in the increasing size of grinding mills and flotation cells used in recent plant

designs and in the adoption of HPGR crushing as an alternative to SAG milling. The High Pressure Grinding Roll

(HPGR) technology is one such technology which has been growing in the last 10-15 years with key benefits

being better energy efficiency and higher grinding capacity and higher metal recovery in downstream

processes such as leaching and flotation. It can boost milling capacity by 20-40%.

The crushing action occurs in a packed bed between the rolls. As rock is drawn between the rolls they are

forced apart until the inter particle crushing force balances the hydraulic pressure on the rolls. The rock is

compacted into a cake that has a bulk density of between 80-90% of the true rock SG.

Schematic diagram of a HPGR

Difference with a HPGR based grinding circuit and a SAG mill based grinding circuit

Source: IFIN Research

“Fineness is not influenced by Press Force........”....... International mining expert

HPGR Systems are known to save ~30% power compared to SAG mills. Advantages of HPGR: -Better energy efficiency. -Steady high rate throughput. -Finer product. -Low dust and noise. -Compact design – less space. -Low installation cost. -Low operating cost. -More rapid progression from stat to full capacity. -Reduces grinding media consumption. Faster delivery schedule.

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

32

VERTICAL MILLS – competition for SAG+BALL Mills – potential threat in long run for soft ores

Since tumbling mills are not effective in fine grinding due to their relatively low power intensity, the

alternative is a vertical mill. Steel balls or pebbles are placed in a vertical grinding chamber in which an internal

screw flight provides medium agitation. The feed enters at the top with mill water and is reduced in size by

attribution and abrasion as it falls. The finely ground particles are carried upwards by pumped liquid and

overflow into a classifier. Oversized particles are returned to the bottom of the chamber for further grinding.

The idea of vertical mills was initiated way back in 1946 with the Mikro-Atomizer and the Raymond Vertical

mills. However, the idea of vertical mills has recently been taken up in a more serious manner by miners and

manufacturers worldwide with improvements in technology.

These are in direct competition to tubular mills which are generally positioned in horizontal form. They can be

used for wet as well as dry grinding processes. Manufacturers of vertical mills claim the following advantage

over tubular horizontal mills:

1. Higher energy efficient by up to 30-35%.

2. Lower media consumption coinciding with energy savings.

3. Lower maintenance and hence lower operating cost.

4. Lower installation cost and requires less floor space due to its vertical layout.

5. Useful for ultra fine grinding of 100 microns or less.

6. Lesser noise.

7. They can be used

Vertical mills claim to successfully ground virtually all ores namely aluminium oxide, barite, calcite, clay, coal,

coke, copper, copper ore, ferrite, ferro alloy, gold, graphite, iron oxide and sand, kaoline, lead zinc ore,

limestone, etc.

The theory behind vertical mill says

“WHY TUMBLE A MILL WHEN YOU CAN STIR A CHARGE – LESS ENERGY IS REQUIRED” since

ENERGY REQUIRED TO MILL ROCK = INPUT ENERGY – ENERGY REQUIRED TO TUMBEL MILL AND CHARGE

Layout of a vertical mill

Source: Metso

IFIN Research IFCI Financial Services

AIA Engineering Overweight

14 June 2010

33

Financial Summary

Income Statement (Rs mn) Cash Flow Statement (Rs mn)

Year end 31 March FY09 FY10 FY11E FY12E Year end 31 March FY09 FY10E FY11E FY12E

Net Sa les 10,233 9,497 11,817 13,879 Oper.profit before w.cap.changes 2,576 2,488 2,946 3,355

Expenditure 7,766 7,292 9,231 10,944 Change in current assets (888) (514) (1,400) (1,268)

Operating Profit 2,467 2,205 2,586 2,935 Change in current l iabi l i ties 137 57 203 221

Other Operating Income - 253 300 350 Others activi ties (4) (639) (697) (763)

EBITDA 2,467 2,458 2,886 3,285 Cash flow from operation (a) 1,821 1,391 1,052 1,545

Other Income 218 160 210 230 Capita l expenditure (396) (403) (614) (670)

Depreciation 203 219 240 274 Investments 533 (186) (150) (200)

EBIT 2,483 2,399 2,856 3,241 Dividend received 37 60 90 90

Interest 21 25 34 35 Interest received 72 70 60 70

PBT (before non-recurring) 2,462 2,374 2,822 3,206 Others - - - -

Non Recurring - - - - Cash flow from investing (b) 247 (459) (614) (710)

Tax on non recurring - - - - Free cash Flow (a+b) 2,068 932 439 835

PBT (after non-recurring) 2,462 2,374 2,822 3,206 Equity capita l + share premium - - - -

Tota l Tax 750 701 837 983 Debt 306 48 75 100

Reported PAT 1,712 1,673 1,985 2,223 Interest pa id (21) (25) (34) (35)

Adjusted PAT 1,712 1,673 1,985 2,223 Dividend paid (155) (287) (325) (390)

Prior period i tems (31) - - - Others 158 - - -

Minori ty interest (7) - - - Cash flow from financing (c) 254 (320) (284) (325)

Preference dividend - - - - Net change in cash (a+b+c) 2,322 613 154 510

Net Income 1,736 1,673 1,985 2,223 Cash and equivalents at the end 2,588 3,200 3,355 3,865

Key ratios Balance Sheet (Rs mn)

Year end 31 March FY09 FY10 FY11E FY12E Year end 31 March FY09 FY10E FY11E FY12E

Growth rates (%) Share Capita l 188 188 188 188

Net sales 48.0 -7.2 24.4 17.4 Reserves & Surplus 7,538 8,911 10,527 12,306

EBITDA 50.6 -0.4 17.4 13.8 Shareholder's funds 7,726 9,099 10,715 12,494

APAT 27.5 -2.2 18.6 12.0 Minori ties Interest 57 - - -

Margins (%) Short term debt 442 490 565 665

EBITDA 24.1 25.9 24.4 23.7 Long term debt - - - -

EBIT 24.3 25.3 24.2 23.4 Total Debt 442 490 565 665

PBT 24.1 25.0 23.9 23.1 Creditors 521 549 719 887

APAT 16.7 17.6 16.8 16.0 Other current l iab & provn 2,483 2,637 2,855 3,184

Valuation ratios (x) Other non-current l iabi l i ties 100 50 50 50

EPS (Rs ) 18.2 17.7 21.0 23.6 Total Liabilities 11,329 12,825 14,904 17,280

EPS Growth (%) 27.5 -2.6 18.6 12.0

PER (x) 21.9 22.4 18.9 16.9 F.Assets (net) incl . Cap WIP 2,383 2,567 2,942 3,339

Price / Cash EPS (PCEPS) (x) 19.3 19.8 16.9 15.0 Investments 414 600 750 950

Price /Book Value (P/BV) (x) 4.8 4.1 3.5 3.0 Cash & Bank 2,587 3,200 3,355 3,865

EV/Net Sa les (x) 3.4 3.6 2.9 2.4 Inventory 1,393 1,413 1,947 2,357

EV/EBITDA (x) 14.2 13.9 11.8 10.2 Debtors 1,847 2,056 2,720 3,327

DuPont Other current assets 2,705 2,990 3,191 3,443

ROE (%) 24.8 19.9 20.0 19.2 Total current assets 8,532 9,658 11,213 12,991

Net Margin (%) 16.7 17.6 16.8 16.0 Other non-current assets 0 0 0 0

Asset Turnover (x) 1.0 0.8 0.9 0.9 Total Assets 11,328 12,825 14,904 17,279