Embed Size (px)

Citation preview

QUARTERLY UPDATE Q4 2018

AGRICULTURE

Page 2

INDUSTRY OVERVIEWM&A TRANSACTIONS AND INDUSTRY OVERVIEW

-

20

40

60

80

100

120

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Q32016

Q42016

Q12017

Q22017

Q32017

Q42017

Q12018

Q22018

Q32018

Q42018

-

5

10

15

20

25

Tran

sact

ion

Vo

lum

e (

Nu

mb

er o

f Dea

ls)

Tran

sact

ion

Val

ue

($ B

illio

ns)

Transaction Value Transaction Volume

Source 1: Capital IQ. Deals announced, closed or effective. Q4 cut-off of December 31, 2018. Capital IQ report run February 3, 2019.Source 2: https://www.fcc-fac.ca/en/ag-knowledge/ag-economics/top-economic-trends-of-2018-farmland-values.htmlSource 3: Statistics Canada – 2016 Census of AgricultureSource 4: https://www.fcc-fac.ca/en/ag-knowledge/ag-economics/canadian-farm-equipment-market-expected-to-be-softer-in-second-half-of-2018.html

• Intense industry consolidation is still occurring. Large agricultural firms continue to enhancetheir positions in the Canadian market with acquisitions of terminal and processing facilities,and divestitures of non-core assets. There currently exists active competition for deals.

• Increased investment in agricultural infrastructure in the Prairies is energizing transactionactivity. Trade wars are impacting Canadian producers and may drive transaction activity asindustry players look to diversify offerings. Together with government funding through theCanadian Agricultural Partnership, these investments will likely lead to new market activity.

• The decline in independent input providers continues due to industry consolidation.

• Input costs continue to rise while commodity prices have been relatively stable over thefour-year period evaluated, yet many commodities face price pressures as a result ofinstability in the global marketplace2.

• Growth in farm cash receipts is expected to be moderate at 2 percent in 2018, slowing to 1.3percent in 20194. As a leading indicator to consumer spending, slowdowns in farm cashreceipts could be balanced by significant used inventory in the marketplace.

• Continued consolidation and interest of remaining independent dealerships. Buyer poolshrinking may balance out valuation multiples in line with historical averages.

• Increased consolidation in Canadian farming – the number of farms decreased 6 percentbetween 2011 and 2016, with 7 percent growth in the number of large farms over this sameperiod3.

• Succession issues with family farms and large corporate farms have fuelled consolidationamongst primary producers, while demand for quality land has never been higher.

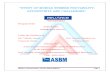

NORTH AMERICAN AGRICULTURE & FOOD PRODUCTSPUBLICLY AVAILABLE MERGERS & ACQUISITIONS1

Number of mergers and acquisitions in Canada in the fourth quarter of 2018 in agriculture and food products.111

Industry & Infrastructure

Inputs & Commodity Markets

Primary Producers

Ag Equipment Manufacturers & Dealerships

Page 3

1 Industry & Infrastructure (Processing, Terminals, Logistics)

Page 4

INDUSTRY & INFRASTRUCTURECURRENT HIGHLIGHTS

The new United States/Mexico/Canada (USMCA) trade deal(commonly referred to as the ‘new NAFTA’ or North American FreeTrade Act) is expected to have widespread impacts on Canada’sagricultural industry and in particular, its dairy producers.

The new deal provides American farmers with tariff-free access to3.6 percent of Canada’s dairy market, sending hundreds of millionsof dollars more in American product into Canada.1 This could putincreased financial pressure on dairy farmers, impacting the valueof production quotas.

Consolidation is expected to continue as producers look toenhance their strategic positioning in an increasingly competitivemarketplace now that there is some certainty over the agreement.

USMCAThe ‘New NAFTA’

USMCA trade deal to have widespread impacts

Crop Research Investment

Growing together

Saskatchewan’s continued crop-research investmentMore than $12 million in funding for 44 crop-related researchprojects was announced through Saskatchewan’s AgricultureDevelopment Fund (ADF) and Strategic Research Initiative (SRI).

The funding is aiming to further crop research that will provideCanadian farmers, producers and agribusiness with knowledge andtechnology to compete globally and improve their bottom lines.3

This continued support for innovation will likely lead to furtherconsolidation, with agricultural-focused companies looking foradditional opportunities to grow in this sector.

Canada’s ProducersAt the forefront

Canadian producers facing challengesThe introduction of USMCA will further increase financial pressureon dairy producers as a pricing model change would impact theprice producers receive for their product. See page 9 for furtherdiscussion on Canada’s dairy industry.

The new Canada Food Guide displays a shift towards more plant-based proteins which also has the potential to impact primaryagricultural producers2.

Increasing market changes could contribute to furtherconsolidation in the agricultural space, and in particular in dairyfarming, as producers aim to diversify their offerings, and seek todivest of non-core assets to strategic buyers.

Source 1: https://www.macleans.ca/economy/the-usmca-explained-winners-and-losers-whats-in-and-whats-out/Source 2: https://www.theglobeandmail.com/canada/article-new-food-guide-shifts-toward-plant-based-foods/Source 3: https://www.saskatchewan.ca/government/news-and-media/2019/january/16/crop-research-investment

Page 5

23%

5%

3%

6%

5%

24%

0% 5% 10% 15% 20% 25% 30%

Nutrien Ltd.

Archer-Daniels-MidlandCompany

Bunge Limited

The Andersons, Inc.

AGT Food and Ingredients Inc.

The Mosaic Company

NTM EBITDA MARGIN

20%

5%

3%

5%

3%

18%

0% 5% 10% 15% 20% 25% 30%

Nutrien Ltd.

Archer-Daniels-MidlandCompany

Bunge Limited

The Andersons, Inc.

AGT Food and Ingredients Inc.

The Mosaic Company

LTM EBITDA MARGIN

25%

5%

1%

5%

10%

7%

0% 5% 10% 15% 20% 25% 30%

Nutrien Ltd.

Archer-Daniels-MidlandCompany

Bunge Limited

The Andersons, Inc.

AGT Food and Ingredients Inc.

The Mosaic Company

NTM REVENUE GROWTH

0%

5%

0%

-15%

-18%

28%

-20% -10% 0% 10% 20% 30%

Nutrien Ltd.

Archer-Daniels-MidlandCompany

Bunge Limited

The Andersons, Inc.

AGT Food and Ingredients Inc.

The Mosaic Company

LTM REVENUE GROWTH*

Source: Capital IQ Note *: Nutrien Ltd. LTM Revenue Growth removed for presentation as growth incorporates recent M&A with Potash Corp. and Agrium merging into Nutrien.Figures above are based on median peer group metrics.

INDUSTRY & INFRASTRUCTUREPUBLIC COMPANY PERFORMANCE

Avg: 0.0% Avg: 8.8%

Avg: 9.2% Avg: 11.0%

Forecasted Improvements in Revenue Growth and EBITDA Margin for Public CompaniesThe median last twelve month (LTM) revenue growth for the highlighted companies was 0.0 percent (-3.5 percent in thethird quarter of 2018) and is forecast to show strong improvements with expected next twelve month (NTM) revenuegrowth of 8.8 percent (15 percent in third quarter 2018).

The median NTM EBITDA margin for these companies is expected to reach 11 percent (10.5 percent in third quarter2018), while the expected enterprise value (EV) over EBITDA multiples are forecast to remain steady at 9.6x (10.5x – Q32018) over the NTM.

Page 6

9.5x

8.9x

10.5x

9.2x

12.0x

7.2x

0.0x 5.0x 10.0x 15.0x 20.0x 25.0x

Nutrien Ltd.

Archer-Daniels-MidlandCompany

Bunge Limited

The Andersons, Inc.

AGT Food and Ingredients Inc.

The Mosaic Company

NTM EV/EBITDA

13.4x

8.6x

9.8x

9.6x

22.7x

8.5x

0.0x 5.0x 10.0x 15.0x 20.0x 25.0x

Nutrien Ltd.

Archer-Daniels-MidlandCompany

Bunge Limited

The Andersons, Inc.

AGT Food and Ingredients Inc.

The Mosaic Company

LTM EV/EBITDA

Source: Capital IQ

INDUSTRY & INFRASTRUCTUREPUBLIC COMPANY PERFORMANCE

Avg: 12.1x Avg: 9.6x

Trading Multiples & Operating Statistics

(Figures In $CAD Millions, except percentages

and ratios)

Company

Market

Capitalization

Enterprise

Value Revenue

Revenue

Growth EBITDA

EBITDA

Margin

Nutrien Ltd. $39,284 $54,103 $20,895 306.8% $4,040 19.3%

Archer-Daniels-Midland Company $31,343 $40,889 $83,330 5.2% $4,484 5.4%

Bunge Limited $10,288 $21,544 $59,210 -0.4% $2,076 3.5%

The Andersons, Inc. $1,152 $2,003 $4,184 -14.7% $198 4.7%

AGT Food and Ingredients Inc. $403 $1,059 $1,590 -17.5% $47 2.9%

The Mosaic Company $15,364 $20,538 $11,839 27.6% $2,280 19.3%

Median $12,826 $21,041 $16,367 2.4% $2,178 5.1%

Mean $16,306 $23,356 $30,175 51.2% $2,187 9.2%

LTM Operating Figures

(Figures In $CAD Millions, except percentages

and ratios)

Company

Revenue

Growth

EBITDA

Margin

NTM

EV/EBITDA

LTM

EV/EBITDA

LTM

EV/REV

Nutrien Ltd. 24.6% 22.9% 9.5x 13.4x 2.6x

Archer-Daniels-Midland (ADM) Company 5.4% 5.4% 8.9x 8.6x .5x

Bunge Limited 0.6% 3.3% 10.5x 9.8x .3x

The Andersons, Inc. 5.2% 5.7% 9.2x 9.6x .5x

AGT Food and Ingredients Inc. 9.7% 5.0% 12.0x 22.7x .7x

The Mosaic Company 7.1% 23.5% 7.2x 8.5x 1.6x

Median 6.3% 5.5% 9.4x 9.7x .6x

Mean 8.8% 11.0% 9.6x 12.1x 1.0x

NTM Consensus Estimates Valuation

Page 7

2 Inputs & Commodity Markets

Page 8

INPUTS & COMMODITY MARKETSPRICE CHANGES

102

104

106

108

110

112

114

116

118

-

200

400

600

800

1,000

1,200

Nov-14 May-15 Nov-15 May-16 Nov-16 May-17 Nov-17 May-18 Nov-18

Farm

Pri

ce I

np

ut I

nd

ex

$/m

etr

ic t

on

ne

Wheat - excl. durum Barley Soybeans Grain corn

Canola Flaxseed Durum Lentils

Dry peas Farm input price index

Chart Source : Farm product prices, crops and livestock – Stats Canada.

Commodity Price Changes and Farm Input Price Index Costs While average commodity prices have seenstability in recent years, a closer look at specificcommodities indicate drastic fluctuations–notably lentils which have faced price pressureresulting from global oversupply and trade wars.The Statistics Canada Farm Input Price Index(FIPI) estimates the change in price that farmerspay for inputs into their farming operationthrough time. The FIPI indicates input costs tofarmers have increased 4.9 percent since thefourth quarter of 2014.

Note: Farm input price index available to Q2 2018.

CROP COMMODITY PRICES

BarleyFlaxseedCanolaSoybeansDry peasDurumLentils

+6.8%+4.5%-2.5%-2.8%

-14.8%-16.7%-32.5%

Largest Price Changes –November 2018

Long-termΔ Since November

2016

Short-termΔ Since November

2017

+19.2%+6.6%-0.9%-6.7%

-20.8%-8.8%

-50.6%

Page 9

INPUTS & COMMODITY MARKETSMARKET PRESSURE, FUTURES & EXPORTS

Source 1: Bloomberg – Ag Futures as of 6:00 PM EST February 1, 2019.Source 2: http://www.agr.gc.ca/eng/industry-markets-and-trade/canadian-agri-food-sector-intelligence/crops/reports-and-statistics-data-for-canadian-principal-field-crops/canada-outlook-for-principal-field-crops-2019-01-25/?id=1548707046784

Dairy Market Update USMCA has placed increasing pressure on Canada’s dairy producers, pressure that may contribute to adairy pricing model change. The recent release of the Canada Food Guide notably included a shift towardsconsumption of plant-based proteins, departing from the previous Canada food guide which included meatand dairy products as significant components of the overall guide. Ongoing market changes suggest theremay be future opportunities for consolidation in the industry.

Canada’s Principal Field Crops Exports2 (kilotonnes)

Total Grains and Oilseeds Total Pulses and Special Crops

2017 – 2018 2018 – 2019(f)

45,303

Updated forecast as at January 25, 2019. Forecast in Q3 update was as at September 17, 2018.

46,408(Up from forecast in Q3

update of 45,453)

Futures – Spring 2019 Contracts1

Canola (January)Wheat (December)Soybean (November)Corn (December)Oats (December)Live Cattle (December)

502.50 CAD/MT514.75 USD/bu.856.75 USD/bu.367.00 USD/bu.295.25 USD/bu. 116.78 USD/lb.

Futures –Winter 2019 Contracts*

Canola (March)Wheat (March)Soybean (March)Corn (March)Oats (March)Live Cattle (April)

482.40 CAD/MT524.25 USD/bu.917.75 USD/bu.378.25 USD/bu.288.50 USD/bu. 126.28 USD/lb.

FUTU

RES

CO

NTR

AC

TS

Note *: As included in MNPCF Quarterly Update –Agriculture – Q3 2018. These quotes on Futures havebeen included for comparison purposes only.Note: Cattle costs are USD per hundredweight.

2019 – 2020(f)

46,555

2017 – 2018 2018 – 2019(f)

5,363 5,101(Down from forecast in

Q3 update of 5,430)

2019 – 2020(f)

5,310

Page 10

3 Primary Producers

Page 11

PRIMARY PRODUCERSLAND VALUE TRENDS

-

500

1,000

1,500

2,000

2,500

3,000

3,500

0%

5%

10%

15%

20%

25%

1980 1985 1990 1995 2000 2005 2010 2015

Val

ue

($/a

cre)

Pri

me

Inte

rest

Rat

e (%

)

FARM VALUES VS. FARM CASH RECEIPTS & INTEREST RATES

Average prime interest rate Value per acre of farm land and buildings (Canada)

Note: Information for value per acre of farm land and buildings (above) has been updated to July 1, 2017. 2018 values expected for 2019 Q1 update.Source 1: https://www.ratehub.ca/prime-mortgage-rate-historySource 2: Stats Canada: Table 002-0003: Value per acre of farm land and buildings, at July 1.Source 3: https://www.discovermoosejaw.com/ag-news/agriculture-news-sk/fcc-optimistic-about-agriculture-sector-in-2019Source 4 https://www.fcc-fac.ca/fcc/about-fcc/reports/2017-farmland-values-report-e.pdf

Key external drivers affecting agricultural industry performance in Canada include: commodity prices, interest rates,consumer preferences, growing season conditions and result and farm land values.

The chart above highlights growth in farm land and building values. Values have increased significantly along with farmcash receipts over the last 15 years while interest rates have displayed a downward trend.

Recent interest rate hikes have widespread impacts within the farming sector due to levels of debt financing. Increases ininterest rates result in larger interest payments on outstanding debt, which may impact farmland valuations. While rateshave increased recently, they remain at near all-time lows. Continued industry consolidation and scarcity of available landmay counteract any decreases in valuation resulting from increasing interest rates.

Farm Credit Canada (FCC) Chief Agricultural Economist JP Gervais expects producers’ margins will be tighter in 2018-2019,with an expectation for farm asset values (particularly farmland) in Saskatchewan to be more stable or grow at a moremoderate pace.3

The 2017 FCC Farmland Values Report published April 23, 2018 indicates strong growth in value for 2017, with an 8.4percent increase for farm land in Canada, with boosts of 10.2 percent in Saskatchewan, 7.3 percent in Alberta, and 5.0percent in Manitoba.4

Since 2000, interest rates have decreased 4%,

while farm values per acre increased 240%*.

*Using Bank of Canada prime interest rate and information in graph above.

Farm Values Continue to Rise

1 2

Farm Cash Receipts (Canada)

-

500

1,000

1,500

2,000

2,500

3,000

0%

5%

10%

15%

20%

25%

1980 1985 1990 1995 2000 2005 2010 2015

Value ($/acre)

Prime Interest Rate (%)

INTEREST RATES AND FARM VALUES

Average prime interest rate Value per acre of farm land and buildings (Canada)

-

10

20

30

40

50

60

70

Farm

Cas

h Re

ceip

tsBi

llion

s

Page 12

4 Agricultural Equipment Manufacturers & Dealerships

Page 13

AGRICULTURAL EQUIPMENT MANUFACTURERS & DEALERSHIPS

Farm cash receipts have levelled in recent years, with 2018 receipts falling below third quarter 2017, yetexceeding receipt totals from third quarter 2016. Farm cash receipts display a defined pattern of drastic annualfluctuations as cash receipts are a lagging indicator of ag equipment sales. Third quarter 2018 results inagriculture implement sales appear to suggest a turnaround as three of the four companies below outperformedtheir two previous years’ third quarter sales totals.

Farm Cash Receipts and Agricultural Implement Sales

Source 1: Capital IQNote: John Deere has a fiscal year-end of October. John Deere quarterly results based on calendar months were used for presentation purposes to align results with other companies.

Data Table – Farm Cash Receipts and Ag Implement SalesFarm Cash Receipts and Ag Implement Sales 2013 2014 2014 2014 2014 2015 2015 2015

(Figures in $CAD Millions) Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Rocky Mountain Equipment (RME) 291 198 242 231 294 220 213 256

Cervus Equipment - Agricultural Equipment (CE) 151 103 164 201 164 140 185 233

John Deere - Ag and Turf (DE) 6,252 8,410 7,608 6,986 5,196 6,997 6,933 6,100

CNH Industrial (New Holland and Case IH) - Ag Equipment (CNHI) 4,400 4,089 4,731 4,091 3,941 3,263 3,787 3,257

Farm Cash Receipts (FCR) 6,989 8,776 7,218 7,594 8,459 9,609 7,176 8,242

2015 2016 2016 2016 2016 2017 2017 2017 2017 2018 2018 2018 2018

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4f

286 189 233 223 286 210 237 239 273 220 303 233 284

154 131 188 240 179 146 235 271 182 159 277 286 N/A

5,077 7,215 6,141 5,950 4,726 7,937 6,657 7,009 5,240 9,084 8,236 7,360 N/A

4,138 2,754 3,645 3,096 3,800 3,126 3,760 3,314 4,063 3,326 4,356 3,408 N/A

8,866 10,440 6,832 7,655 8,744 10,515 7,738 8,134 8,371 9,751 7,821 7,890 N/A

14

16

18

20

1,000

3,000

5,000

7,000

9,000

Q4

2013

Q2

2014

Q4

2014

Q2

2015

Q4

2015

Q2

2016

Q4

2016

Q2

2017

Q4

2017

Q2

2018

Q4f

2018

RESULTS BY QUARTER

John Deere - Ag and Turf (DE) CNH Industrial (New Holland and Case IH) - Ag Equipment (CNHI) #REF!

0

2

4

6

8

10

12

-

100

200

300

400

Q4

2013

Q2

2014

Q4

2014

Q2

2015

Q4

2015

Q2

2016

Q4

2016

Q2

2017

Q4

2017

Q2

2018

Q4f

2018

Farm

Cas

h R

ece

ipts

($ b

illi

on

s)

Re

ven

ue

($ m

illi

on

s)

Rocky Mountain Equipment (RME) Cervus Equipment - Agricultural Equipment (CE)

John Deere - Ag and Turf (DE) CNH Industrial (New Holland and Case IH) - Ag Equipment (CNHI)

Farm Cash Receipts (AB, SK, MB)

Page 14

-80

-30

20

70

120

170

Jan-2014 Jul-2014 Jan-2015 Jul-2015 Jan-2016 Jul-2016 Jan-2017 Jul-2017 Jan-2018 Jul-2018 Jan-2019

Ch

ange

(%

)

SHARE PRICE & S&P/TSX INDEX CHANGES1

S&P/TSX Composite Index (̂ GSPTSE) - Index Value

Rocky Mountain Dealerships Inc. (TSX:RME) - Share Pricing

Cervus Equipment Corporation (TSX:CERV) - Share Pricing

CNH Industrial N.V. (NYSE:CNHI) - Share Pricing

Deere & Company (NYSE:DE) - Share Pricing

AGRICULTURAL EQUIPMENT MANUFACTURERS & DEALERSHIPS

Source 1: Capital IQSource 2: https://www.reuters.com/article/us-deere-results/deere-outlook-for-2019-disappoints-amid-trade-war-slowing-demand-idUSKCN1NQ1CW

Share Price ChangesShare price fluctuations have been increasingly volatile since 2016 with John Deere experiencing the largest fluctuationsin share price increasing over 101 percent since the first quarter of 2014. Cervus and Rocky Mountain share prices havemoved generally in lockstep with one another, Rocky Mountain slightly outperforming Cervus.

“Deere & Co gave an underwhelming earnings forecast… for fiscal2019 after missing quarterly profit estimates amid a U.S. trade battlewith China that has… hurt agriculture equipment demand... (Deere’s)global sales for agriculture and turf equipment are projected to rise 3percent in 2019, significantly slower than a 15 percent year-on-yearjump this year2.”

Reuters on Deere & Co(NYSE: DE)

Notable & Quotable

Page 15

About Us – MNP Corporate Finance Inc.

Page 16

MNPCF – LEADERSHIP TEAM

DUE DILIGENCE LEADERSHIP

TRANSACTION LEADERSHIP

Aleem BandaliManaging Director

Dale AntonsenManaging Director

John CaggianielloManaging Director

[email protected] 416.513.4177

Brett FranklinPresident

Mike ReynoldsManaging Director

Johnny EarlManaging Director

[email protected] 604.637.1514

Dan PorterManaging Director

Stephen ShawManaging Director

Jason BurgessManaging Director

Mark RegehrManaging Director

Craig MaloneyManaging Director

Patrick KhouzamManaging Director

Page 17

MNPCF – RECENT TRANSACTIONS

AGRICULTURE

NATIONAL

Page 18

OTHER RECENT INDUSTRY M&A TRANSACTIONS

Source: Capital IQAll figures are in $CAD unless otherwise indicated.

• MNP Corporate Finance Inc. acted as exclusivefinancial advisor to a Confidential Seller in structuringand negotiating this transaction.

• Bonnefield is Canada’s foremost provider of land-leasefinancing for farmers, dedicated to preserving“farmland for farming” across Canada. Bonnefield andits farmland funds are 100% Canadian owned andcontrolled.

ClosedOctober 30, 2018

Industry Farming

Transaction Value (TV)

Not disclosed

TV/Revenue Not disclosed

• MNP Corporate Finance acted as exclusive financialadvisor to Norsask Farm Equipment Ltd. in structuringand negotiating this transaction.

• Founded in 1948, Redhead is a large andcomprehensive multi-line heavy equipment dealer inSaskatchewan.

• Norsask is a full-service Case IH farm equipmentdealership located near North Battleford,Saskatchewan.

AnnouncedDecember 6, 2018

IndustryAgricultural and Farm Machinery

Transaction Value (TV)

Not disclosed

TV/Revenue Not disclosed

acquired

Acquired land from

• MNP Corporate Finance acted as exclusive financialadvisor to Tri West Agro Ltd. in structuring andnegotiating this transaction with Westview Co-operative Association Ltd.

• Westview Co-op has served its members and guestssince 1933 and has multiple locations in Alberta.

• Founded in 2003, Tri West has become a leadingindependent agricultural retailer in East Central Albertawith a state-of-the-art blending fertilizer plant, anAWSA-approved warehouse for agricultural chemicalsand bulk bin storage.

ClosedSeptember 14, 2018

IndustryProcessing, distribution

Transaction Value (TV)

Not disclosed

TV/Revenue Not disclosed

acquired

• MNP Corporate Finance Inc. acted as exclusivefinancial advisor to Fiskel Farms Transport Ltd. instructuring and negotiating this share transaction.

• Wright Spud Farms Inc. is a large potato and grainfarming company based in the Carberry area and hasbeen named as one of McCain Foods' Top 10 Producers.

• Fiskel Farms is a 3,300-acre potato and grain farm witha McCain Foods grower’s contract located nearCarberry, Manitoba.

Closed April 15, 2018

Industry Farming

Transaction Value (TV)

Not disclosed

TV/Revenue Not disclosed

Wright Spud Farms

Acquired

Fiskel Farms