Embed Size (px)

Citation preview

2

Agenda

• Overview and Corporate Governance model

• Agriculture and Advanced Fuels

• Electricity Generation

• Energy Systems

• Metallic Construction

• Financial overview

3

Overview and Corporate Governance model

4

Martifer carries out its activities through 4 distinct business units

Steel, aluminium and stainless steel solutions

Agriculture activity to produce oil seeds and crops

Vegetable oil producer (future)

Biodiesel production in Portugal and Romania

Petrol station network in Portugal

Wind and solar power plants turnkey supplier

Producer of wind power components

Engineering solutions provider

Power producer from renewable power sources (wind, solar, hydro and in the future waves)

Energy SystemsMetallic Construction Electricity Generation Agriculture & Advanced Fuels (60% owned by Martifer)

5

Shareholder structure

• IPO in June 2007 on Euronext Lisbon:

• Priced at €8,00 per share, top of range

• €199Mn gross proceeds, exclusively to company

• 25% free-float

• MTO 1) and Mota-Engil diluted their stakes from 50% to 37,5%

1) MTO is held in equal parts by Mr. Carlos Martins and Mr. Jorge Martins

N. Shares Outstanding: 100,000,000

Free-float

25%

MTO 1)

37,5%

Mota-Engil

37,5%

6

International presence Martifer currently is present in 18 Countries in 5 Continents

7

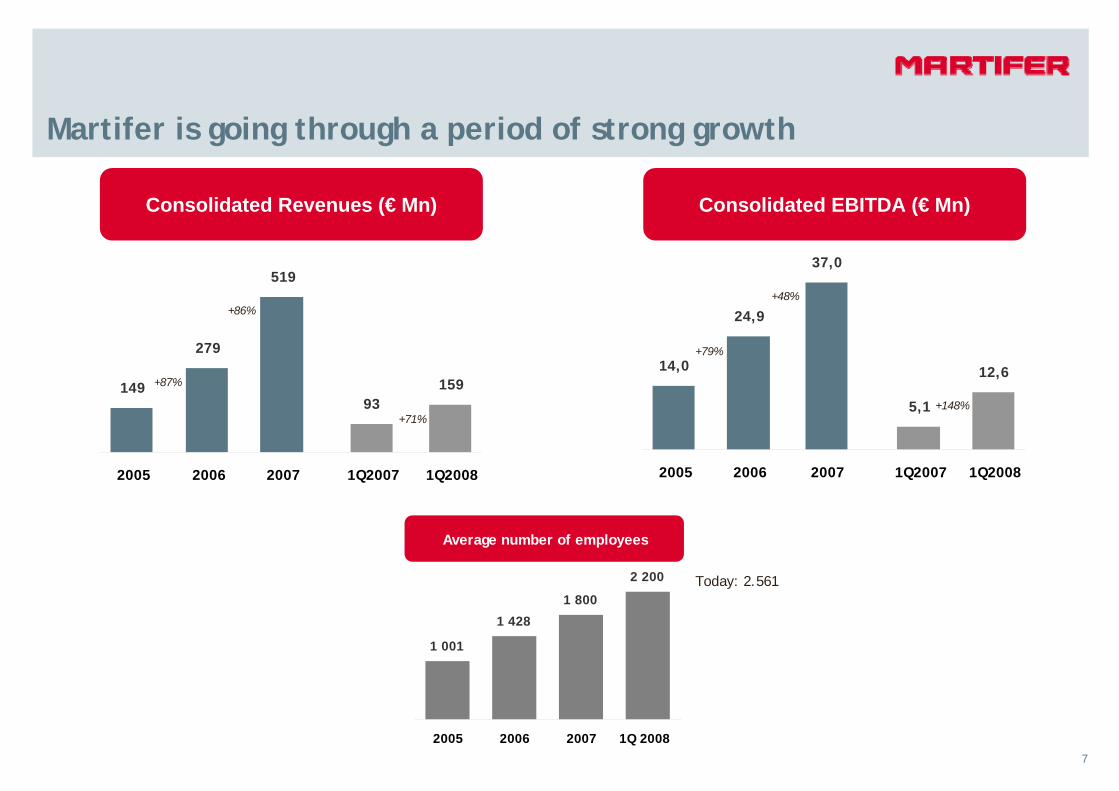

Martifer is going through a period of strong growth

+87%

+86%

+71%

149

279

519

93159

2005 2006 2007 1Q2007 1Q2008

Consolidated Revenues (€ Mn)

+79%

+48%

+148%

14,0

24,9

37,0

5,1

12,6

2005 2006 2007 1Q2007 1Q2008

Consolidated EBITDA (€ Mn)

1 001

1 428

1 800

2 200

2005 2006 2007 1Q 2008

Average number of employees

Today: 2.561

8

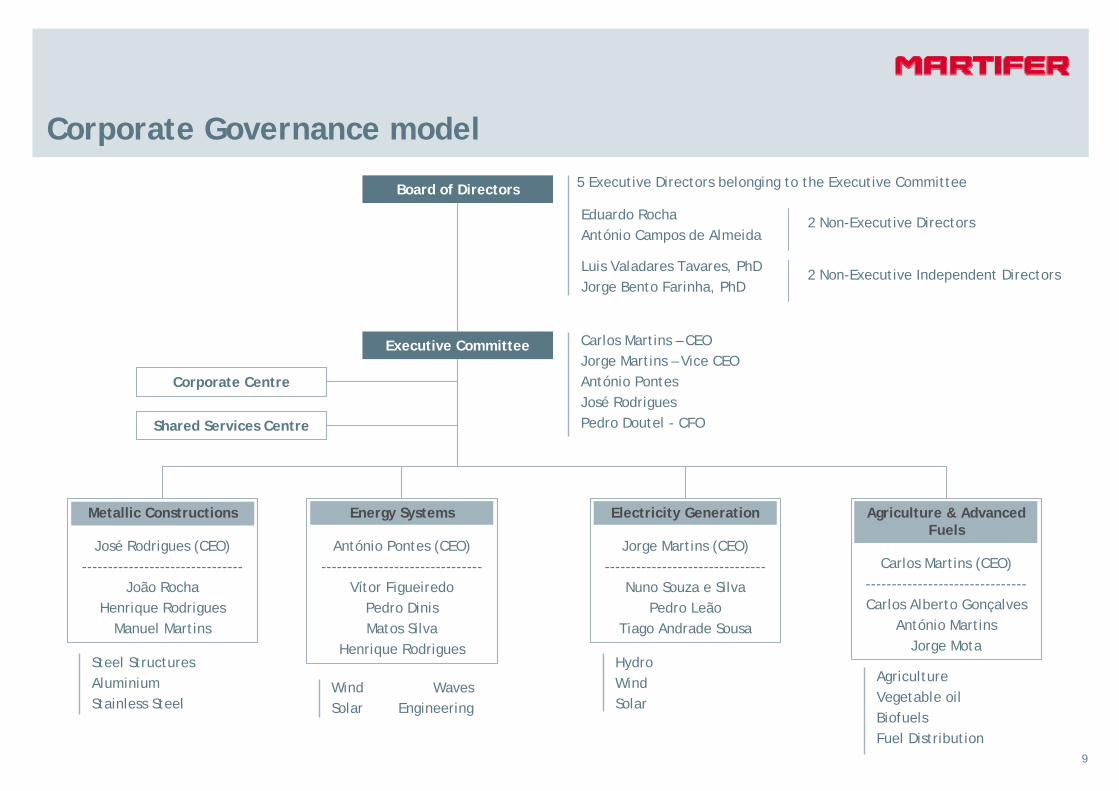

Introduction of a new Corporate Governance model

• Growing size of Group and expansion (new businesses and new regions) leads to higher management complexity

• To address this issue, the Group approved at the end of March a new governance model following detailed work within all the organization and external advisory from Mckinsey & Co.

• Board was enlarged from 5 to 9 Directors, with 5 executive Directors, 2 non-executive Directors and 2 independent Directors

• Martifer SGPS will focus its role on strategy and planning, corporate policies definition, risk management, corporate finance, promoting synergies within the Group and evaluating the performance of the Business Units

• With exception of the CFO, the Executive Directors of Martifer SGPS are also the CEO’s of the business units, creating a strong management with equal responsibility over each business unit

• Each business unit CEO (Metallic Constructions, Energy Systems, Agriculture & Biofuels and Electricity Generation) will lead a fully dedicated team of professionals focused exclusively on that BU

9

Corporate Governance model5 Executive Directors belonging to the Executive Committee

2 Non-Executive Directors

2 Non-Executive Independent Directors

Eduardo RochaAntónio Campos de Almeida

Luis Valadares Tavares, PhDJorge Bento Farinha, PhD

Executive Committee Carlos Martins – CEOJorge Martins – Vice CEOAntónio PontesJosé RodriguesPedro Doutel - CFO

Metallic Constructions

José Rodrigues (CEO)-------------------------------

João RochaHenrique Rodrigues

Manuel Martins

Energy Systems

António Pontes (CEO)-------------------------------

Vítor FigueiredoPedro DinisMatos Silva

Henrique Rodrigues

Electricity Generation

Jorge Martins (CEO)-------------------------------

Nuno Souza e SilvaPedro Leão

Tiago Andrade Sousa

Agriculture & Advanced Fuels

Carlos Martins (CEO)-------------------------------Carlos Alberto Gonçalves

António MartinsJorge Mota

Corporate Centre

Shared Services Centre

Steel StructuresAluminiumStainless Steel

Wind WavesSolar Engineering

HydroWindSolar

AgricultureVegetable oilBiofuelsFuel Distribution

Board of Directors

10

11

Corporate structure

Prio SGPS

Prio Agriculture

E. Europe

Brazil

Mozambique

Extraction Romania Biodiesel Romania

Biodiesel Portugal

Prio AF – Network and tank farm Portugal

Prio Advanced Fuels

Portugal

100%

100%

100%

60%

100% 100%

100%

100%

1212

International presence

1313

Advanced FuelsAgriculture

Board 4 Executive Directors at the Management Committee

Humberto Leite - non-executive Director

Management Committee

Carlos Martins – CEOCarlos Gonçalves – Vice CEOAntónio MartinsJorge Mota – CFOLuis Martins – Fuel MarketingPaulo Carmona – Trading & LogisticsNuno Alegria – QSA and Assets

PortugalEastern EuropeMozambiqueBrazil

Carlos Martins – CEOCarlos Gonçalves – Vice CEOAntónio MartinsJorge Mota – CFO

PortugalRomania

Prio Corporate Governance

Martifer60%

Génisis20%

FinibancoHolding

20%

Prio SGPS shareholder structure

1414

Prio

PRIO

Prio Agriculture Prio Advanced Fuels

Agriculture Agro-Industry

Trading and Logistics

Production of biodiesel and distribution of both fossil fuels and biofuels though retail and wholesale channels

Production of oilseeds, grains, vegetable oil and meal

Logistics and Infrastructure management

• Through its 60% owned subsidiary, Prio, Martifer participates in the Agriculture & Biofuels markets

1515

Trading & Logistics

• Production of seeds and crops: sunflower, soybean, rapeseed, wheat, corn and barley

• Romania & Ukraine: Target of 73.000 ha in 2010, to produce sunflower, rapeseed, wheat, corn and barley

• Brazil: Target of 23.000 ha by 2010 to produce soybean, sunflower and corn

• Mozambique: Target of 9.000 ha by 2010 to produce soybean, sunflower and corn

• Portugal: Buyer of 15.000 ton of sunflower

• Poland: Buyer of 15.000 ton of rapeseed

• Production of vegetable oil and meal from oilseeds:

• Currently investing in a crushing unit in Romania, with capacity to produce 250k tons of oil and 450k tons of meal from 750k tons of oilseeds

• Milling unit in Romania to produce flour from cereals:

• under study

Prio Agriculture

Agriculture Agro - Industry

Agriculture and Agro-Industry

1616

• Responsible for all trading & logistics activities inside Prio Group – transport management; logistics and infrastructures management; warehousing; main responsibility for all contracts; trading

• Search for new market opportunities

• Trading & Logistics main activity in the triangle Costanzia Port – Black Sea – Danube River

Prio Agriculture

Trading & Logistics

Agriculture Agro - Industry

Trading & Logistics

1717

Prio Advanced Fuels

• Distribution network in Portugal:

• Currently: 5 Prio Petrol Stations and 12 under Jerónimo Martins agreement

• Until 2010: 20 Prio Petrol Stations and 50 under Jerónimo Martins agreement

• Goal of achieving sales of 400.000m3/y both fossil and biofuels, in four years

• Two Biodiesel factories (Romania & Portugal) with 100k tons capacity each

• Direct sales for Biodiesel:

• Portugal:

• B 100 – direct sales to BP and GALP

• B 15 – sales through petrol station network (both Prio and Jerónimo Martins)

• B 30 – direct sales to road freight and coach companies

• Romania: B 100 – direct sales to the oil companies like Lukoil, Petrom e Rompetrol

• Biodiesel production expected for 2008:

• Romania: about 85k tons

• Portugal: about 45k tons

• Aveiro Tank Farm:

• Installed capacity: 76.000 m3

• Storage agreement with BP

Prio Advanced Fuels

1818

• Investment at Prio expected to decrease around €78Mn vis-a-vis IPO business plan due to:

• Reduction in the number of petrol stations and the capex per petrol station

• Capacity expansion at biodiesel factories was cancelled

• 2008/2010 capex mostly in Agriculture and Agro-Industry

• All future investments in Prio Advanced Fuels will seek the roll out of the distribution network

Update on the investment plan

2007

2009 - 2010

Total

Prio Advanced Fuels (€ Mn)

66

86

10

Total (€ Mn)

85

250

57

2008 10 108

Prio Agriculture (€ Mn)

19

164

47

98

IPO 164 328164

1919

Guidance

• We maintain our guidance for 2008:

• Revenues: €315Mn

• EBITDA: €16Mn

• We expect to reach this guidance through:

• Good market conditions (yield/prices) in Agriculture lead us to review upwards our expectations

• Sales of about 130k tons of biodiesel for FY2008

• Commercialization of B15 in Portugal with great success from beginning of June – Prio and Jerónimo Martins petrol stations

• Start of activities of Aveiro tank farm in the 2Q2008

20

2121

International presence

22

Strategic positioning

• Martifer Renewables intends to become a major renewable energy developer, leveraging on the competencies of Martifer Energy Systems

Development Turnkey O&MEquipmentsProduction

• Sites identification

• Procurement

• Wind measurement

• Site assessment

• Licensing

• Financing

• WTG assembly• Blades

• Steel towers

• Gearboxes

• Components

• PV modules

• Wave Energy equipments

• Wind farms

• Solar parks• PV

• Thermo

• Operation and maintenance

23

Strategy

Main Strategic Guidelines

• Develop electricity generation projects from renewable resources

• Guarantee a balanced portfolio in what concerns technology and geographical distribution

• Become a pioneer in the exploration of alternative energy resources (e.g. Wave Energy)

• Take advantage of the synergies of the group in the area of energy equipment (Wind and Solar Energy)

Competitive Advantage

• Privileged access to equipments through the partnerships with Repower Portugal, Repower Systems, Suzlon and Martifer Solar

• Onshore and offshore technology

• Equipments output diversity (range from 1MW to 5 MW)

• Strong financial capacity

• Partnerships policy with local developers that add value in their markets (know how and network) and also with larger developers (Galp, Babcock & Brown, EDP)

24

Pipeline

• Pipeline of 2,8 GW from renewable energy sources (RES)

WindRES

Present

Solar Hydro

Future

Wave Geothermal

• Martifer Renewables has a larger pipeline than assets it wants to hold in its portfolio:

• Establish partnerships to share investment

• Assets rotation policy (sale of assets in operation to finance greenfield projects)

25

Electricity Generation portfolio

Capacity Martifer Tariff Tariff 1 Status(MW) stake type (€ / MWh)

Wind

Portugal 400 + 80 2 33% 70-77 Production starting progressively in 2009. Full capacity expected in 2013

Poland 438 100% market 1 109

Romania 618 100% market 1 83

Slovakia 48 100% feed-in 97

Ukraine 200 + 100 50% - -

1 Indicative market price of power + value of green certificates, obtained from various sources, May 2008. Tariff scheme in Ukraine still under Government discussion2 20% of additional capacity may be request to the DGEG

Wind measurement testing or licensing phase

28 MW expected to start construction in 2008

50,4 MW expected to start construction in 2008

Germany 53 100% feed-in 86 In operation, acquired in December 2007

USA(Texas)

816 72% PPA under negotiation - Expected to start construction in 2009

feed-in

Expected to start construction in 2009

26

Electricity Generation portfolio

Capacity Martifer Tariff Tariff Status(MW) stake type (€ / MWh)

SolarSpain (PV) 7.4 100% feed-in 440 Production expected to start in 2H2008

106 80% PPA -- Expected to start construction in 2009

- Portugal 72 45% market 722

Provisional concession granted. Full license expected mid-2008. Construction to be completed in 2012. Total investment of €123Mn.

Romania 1 100% PPA 3 70 by day43 by night in operation

1 Indicative market price of power + value of green certificates, obtained from various sources, December 2007

Hydro

and

Mini

Hydro

Capacity Martifer Tariff Tariff 1 Status(MW) stake type (€ / MWh)

(75 years)

6 45%feed-in

+market

85 (first 23 years)+

79E after

2 Includes an availability factor applicable only to large hydro

3 PPA negotiated with Eon Moldova

USA (CSP)

27

Near term construction schedule

* Year of the beginning of construction

2008* 2009*

Wind 78,4 MW 364 MW

Solar 7,4 MW 106 MW

Total 85,8 MW 470 MW

28

Martifer Renewables PortfolioPortugal

400 MW + 80 MW of wind energy (Ventinvest)

To install between 2009 and 2013

78 MW of hydro energy (partnership with EDP)

Construction to be completed in 2012

Wind

Hydro

29

Martifer Renewables PortfolioPoland

438 MW (15 wind projects)

348 MW with wind measurement

Land for 315 MW

86 MW with grid connection contract

28 MW under construction

Wind

30

Martifer Renewables PortfolioRomania

618 MW (16 wind projects)

609 MW with wind measurement

Land for 176 MW

60,9 MW with grid connection contract

50,4 MW will start the construction in August/08

1 MW of hydro energy in operation

Wind

Mini Hydro

31

Martifer Renewables PortfolioSlovakia

48 MW (2 wind projects)

48 MW with wind measurement

Land for 5 MW

Wind

32

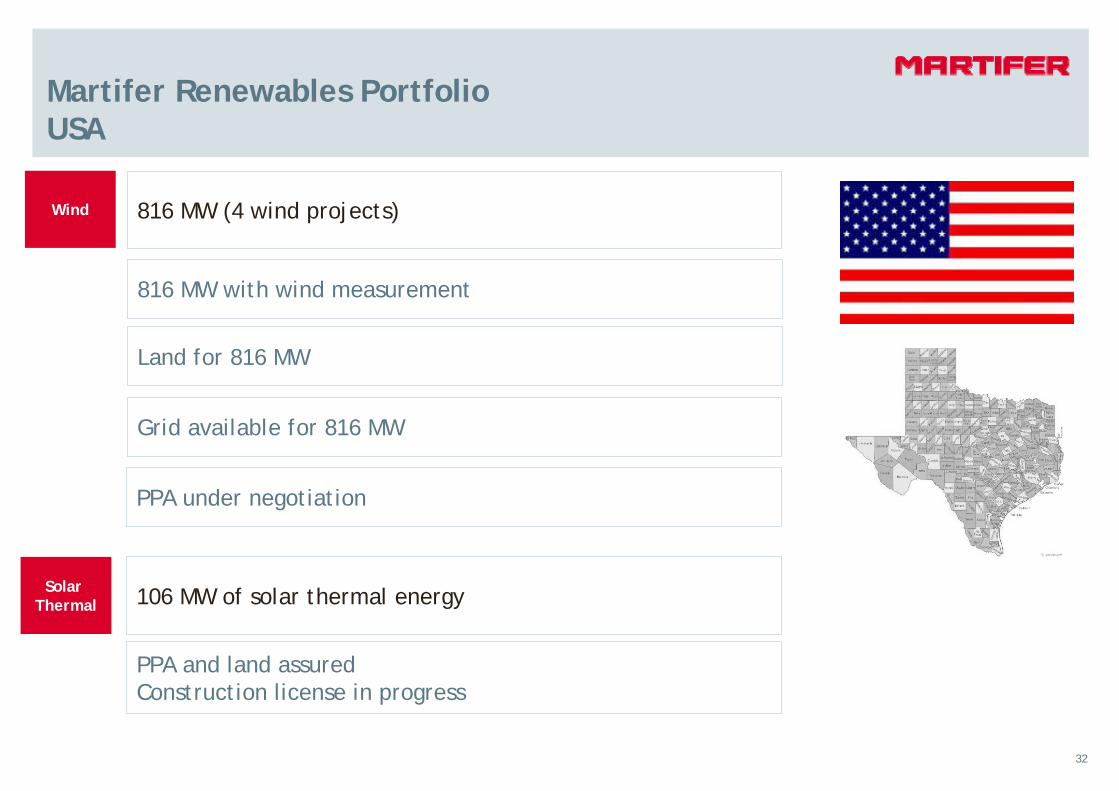

Martifer Renewables Portfolio USA

816 MW (4 wind projects)

816 MW with wind measurement

Land for 816 MW

Grid available for 816 MW

PPA under negotiation

106 MW of solar thermal energy

PPA and land assured Construction license in progress

Wind

Solar Thermal

33

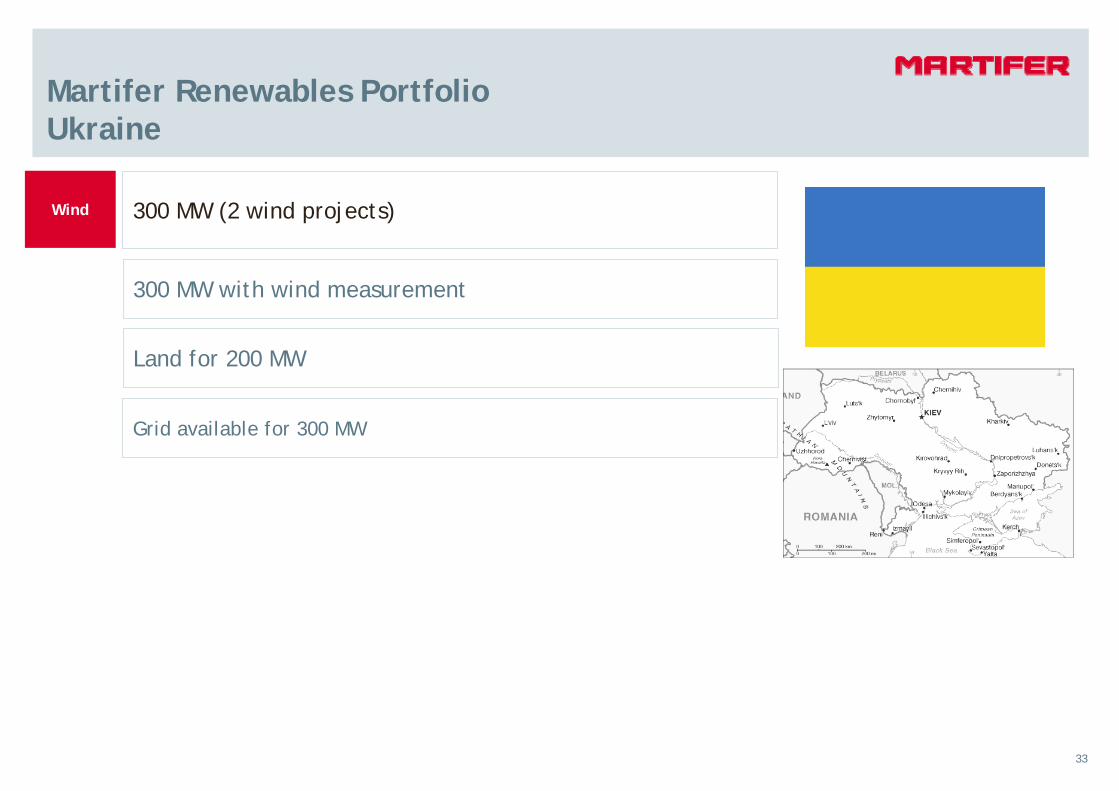

Martifer Renewables PortfolioUkraine

300 MW (2 wind projects)

300 MW with wind measurement

Land for 200 MW

Grid available for 300 MW

Wind

34

Martifer Renewables Portfolio Spain

7,4 MW (6 solar PV projects)

Land for 7,4 MW

7,4 MW in construction

Solar PV

35

36

Corporate structure

Wind Power Industrial Projects Wave Energy Solar Power

Martifer Energia(towers and other

components)

Repower PortugalWind Farms + O&M

(Portugal, Spainand Brazil)

Gebox(Gearboxes)

Reblades(blades factory)

Ventipower(turbines assembey

line)

Martifer EnergiaWind Farms + O&M

(Portugal, Romania, Poland

and USA)

Martifer EnergiaIndustrial Projects

(Portugal, Romenia, USA)

Towers factory USA

Martifer EnergiaR&D wave energy

Navalria(shipyard / wave)

Martifer Solar

Industrial(PV modules)

100%

100%

100%50%

50%

100% 55%

Turnkeysolar parks

(Portugal, Spain,Italy, Greece,

Belgium, France, USA)

Martifer Energy Systems

100%

50%

10%

100%

100%

100%

37

Historical overview

• Start of activity of the tower factory in Portugal with an installed capacity of 100 towers/year

• Initial acquisition of the stake in REpower Systems

• Start of turnkey wind farm business with the construction of the first wind farm in Portugal

• Creation of the R&D centre for wave energy

• Creation of the joint venture Repower Portugal

• Start of the construction of the biodiesel plants in Romania and Portugal for Prio

• Start of the turnkey solar park business with the creation of Martifer Solar

• Martifer and Suzlon agree on partnership for Repower

• Start of activity of gearbox factory

2004

2005

2006

2007

2008

• Martifer consortium awarded Phase B of the portuguese tender for wind power licenses of 400 MW

• Kick-off of the investments in the wind power industrial cluster (turbines, blades, other components, increase capacity of tower and gearbox factories)

• Start of the investments in the PV modules plant

• Acquisition of Navalria shipyard to develop the wave energy project

• Capacity increase of tower factory completed - new capacity of 400 tower/year

• Other wind industrial cluster investments on track

38

Martifer Energy Systems addresses the opportunities in energy systems as a solutions provider

Main Strategic Guidelines

• Become a major solutions provider for renewable energies (wind, solar)

• Position itself as an integrated supplier of turn-key projects with a high degree of technology incorporation, promoting vertical integration and reducing the dependency of outside suppliers

• Take advantage of the market opportunities that arise from the changes in the energy industry

Our Competencies

• A part of Martifer Group with a strong entrepreneurial spirit and financial capacity

• Skilled and experienced work force

• International experience in implementation of large projects

• Ability to establish partnerships to enhance in-house competencies

• Capacity to execute complex projects in short timeframes

• Competence to manage industrial activity

• Capacity to develop and adapt to new technologies

39

Mid term opportunities and threats

Opportunities

• Global need/commitment to increase weight of renewable sources in the energy supply mix

• Rising demand for energy and growing cost competitiveness of renewable energy in a environment of rising energy prices

• Strong pipeline of renewable energy projects within the Group

• Access to technology and growing independence at components level

• Further development of joint ventures and partnerships to access technology and components

• Gain access to new technologies (ex: CSP)

Threats

• Renewable energy is still dependent from Governmental policies

• Instability in raw materials prices

• Critical supply chain management

• Continued technology evolution

• Rising interest rates and macro environment

40

Growth has been strong in this business area

Revenues (€ Mn) EBITDA (€ Mn)

• Increase of activity in the turnkey wind farm business, first activity from solar, growing sales of wind power components and engineering all contributed to a strong top line increase in 2007

16,1

51,8

113,7

17,5

37,2

2005 2006 2007 1Q2007 1Q2008

1,4

3,8

9,9

1,1

3,2

2005 2006 2007 1Q2007 1Q2008

CAGR: 166%CAGR: 166%

41

Wind Power – International presence

42

• Investments in the wind power industrial cluster related to the phase B of the Portuguese tender are progressing on schedule

• The increase capacity of the tower factory has been completed

*Martifer ownership

Turbines Repower Portugal 50% New assembly line 130 turbines – 260 MW

Towers MT Energia 100% Increase industrial capacity 400 towers (+280) - completed

Blades Powerblades 10% New unit 267 sets

Gearboxes Gebox 50% 350 units (+290)

Chassis MT Energia 100% New unit 130 units

Foundation Rings MT Energia 100% New unit 130 units

O & M Repower Portugal 50% Increase capacity

Training Center MT Energia 100% New unit

Other Components MT Energia 100% New units

Investment Company * Description Annual capacity

Increase industrial capacity

Total investment : € 58,3 Mn (ending 3Q 2009) creating 1,129 new jobs

Investments to be made under the terms of the Portuguese tender

Wind power industrial cluster investments

43

2008 will be a landmark year for wind power

• In turnkey wind farms:

• Highest level of wind farms currently under construction in Portugal for third parties (Barão de São João – 25 turbines, Alto da Folgorosa – 9 turbines and Marvila – 6 turbines)

• In Poland, the first wind farm to be delivered outside of Iberia is currently under construction, for Martifer Renewables, with Repower turbines

• In Romania, construction of wind farms for Martifer Renewables is expected to begin in 4Q2008. Turbines have been secured from Suzlon

44

2008 will be a landmark year for wind power

• On the industrial front:

• In May, the tower factory completed the capacity increase

• In the 4Q2008, the first turbines are expected to be assembled in Portugal

• The first production of steel components (chassis) is scheduled for 2H2008

• In the US:

• Martifer Energy Systems plans to invest in a tower factory

• Investment is expected to reach €24Mn

• Construction should be completed in 2009

• Investment location is pending decision

• Turnkey wind farm activity is expected to start in the US also in 2009

45

Martifer is developing its own Wave Energy system

1

2

3

4

Construction of a wave channel to test the models

Conception/Tests/Modelation/Optimization of the 1:40 models

Planning/ Conception of 1:10 prototypes – tests coastwise

Planning/Making 1:1 prototypes – tests coastwise

• Study of patent models and conversion systems

• Confidentiality Agreements

• Partnership protocols

2005 2006 2007 2008

Continuous processes

46

Martifer Solar

PV WafersPV Silicon PV Cells PV Modules Turnkey

Martifer Solar• Supplier of turkey solar PV solutions, both on-grid and building integration

• O&M of PV solar farms

• Producer of own modules from 4Q2008

• Presence in several markets, not dependent on Spanish market

• Building expertise across various technologies (thin-film, concentration, stand alone solutions)

4747

Martifer Solar – International presence

48

Turnkey PV Plants

Spain: Current order book of 20MW

Italy: Letters of engagement covering 90MW in turn-key projects to be delivered over the next 3 years

Greece: Current order book with small installations of 20kW and letter of engagement covering 12MW

Belgium: Framework agreement for 30MW in rooftop installations over the next 3 years, EPC contracts in negotiation

USA: 10 MW for 2008 under negotiation

France: Partnership for 20MW in rooftop installations

Portugal: Roof top installations (microgeração)

49

Module production starting in 2008

• Specifications

• Capacity: 50 MW (1st stage 4Q2008) and 100 MW (2nd stage end 2009)

• Full automated process (reduction of production time and problems with quality of modules)

• Present outline

• Building construction completed

• PV cells supply secured for the next 3 years from several manufactures (contracts to be signed in the next days)

• Other critical raw materials secured (EVA, Tedlar and Ribbon)

• Production in-house of PV glass

50

Energy Systems - Outlook 2008

• Given current backlog and outlook for the remainder of the year, we maintain our guidance for 2008:

• Revenues: €300Mn

• EBITDA: €26Mn

• We expect to reach this guidance through:

• Strong increase in activity in turnkey wind farms

• Increase activity in tower production

• Increase activity from gearbox production

• Initial sales of turbines and components

• First significant revenues from turnkey solar parks

51

Energy Systems - Update on the investment plan

2007

2009 - 2010

Total

Total Wind

(€ Mn)

17

74

27

2008 30

Solar

(€ Mn)

2

34

7

25

Towers US

(€ Mn)

0

24

24

0

Wind Portugal1)

(€ Mn)17

50

3

30

Total Energy Systems

(€ Mn)

19

108

34

55

1) Includes 50% of the investments to be done at Gebox which is held and consolidated at 50%

• Investment at Energy Systems increased from €82Mn (IPO investment plan) to €108Mn due to:

• Increased investment in wind power due to larger commitments related with the Portuguese tender: +€30Mn

• Investment in a tower factory in the US (location still to be decided): +€24Mn

• Investment in the Solar business was reduced with suspension of the PV cells and wafers industrial investments: -€28Mn

52

53

Corporate structure

Martifer Metallic Constructions

Martifer ConstruçõesMetálicas (Portugal)

MC Poland

MC Romania

Marifer Aluminios Martinox

Martinox Angola

MC Angola

MA Spain

MA Angola

MA Poland

Sassal (Australia)

100%

100%

100%

58%

55%

100%

92%

100%

80%

75%

64%

Steel Structures Aluminium Stainless Steel

MC Spain

100%

MC Ireland

100%

54

International presence

55

Martifer addresses the market with a combination of experience and innovation

Main Strategic Guidelines • Consolidate our leadership position and increase profitability in the Iberian market with focus on more complex

and higher added-value projects, through a focus on design and engineering, delivering solutions to our client needs

• Leverage on our expertise, project management experience and know-how that we gained over the last 18 years to expand in some of the fastest growing economies (Eastern Europe and Angola)

• Execute turn-key projects with a significant component of metallic construction

• Enhance competencies through continued training of our workforce in order to be permanently prepared for new projects

Our Competencies• Largest installed capacity base in Iberia

• Ability to execute in-house a multiplicity of projects in our 6 industrial facilities in Europe

• International experience in the execution of large projects (ie, airports, bridges, shopping centres, sport stadiums, etc.)

• Skilled workforce, with a high degree of technical expertise

• Execution of complex projects within tight timeframes

• Use of technology adjusted to our market characteristics

• Strong financial position

56

Mid term opportunities and threats

Opportunities

• Growing opportunities in Central Europe

• Significant infrastructure plans in Portugal and Spain (transport and logistics)

• New bridge over the Tejo river in Lisbon, new Lisbon airport and high speed train are projects which will materialize in the coming years in Portugal

• Inflow of EU funds into Central Europe, namely Poland, Slovakia and Romania

• Euro 2012 co-hosted by Poland and Ukraine

• Agreement to build a series of commercial buildings in Poland for Chamartín

• Indian market in partnership with local player

Threats

• Substitute solutions due to the increasing price of steel and aluminium

• Slowdown in investments due to macro economic conditions

• Higher financial costs due to increase in market interest rates

57

A track record of solid growth

139,5

232,8

295,6

58,4 71,2

2005 2006 2007 1Q2007 1Q2008

12,8

23,4

28,0

5,7 6,9

2005 2006 2007 1Q2007 1Q2008

Revenues (€ Mn) EBITDA (€ Mn) – adjusted for non-recurring items

CAGR: +46% CAGR: +48%

• Strong growth of revenues with stable profitability over the last 3 years

• Growth rates continuing in 1Q2008 +22% versus 1Q2007, with stable profitability

• EBITDA margin is progressing towards the 10% target

+22% +21%

58

Martifer has a comfortable backlog in Metallic Construction

• Metallic Construction usually has an order book of 6 to 8 months work

• Current order book reaches €291Mn

• Current order book gives us a comfortable outlook for the rest of the year and we expect to reach our guidance of €340Mn of revenues and 10% EBITDA margin

Metallic Structures Aluminium Stainless Steel

Rest of the World

Central Europe

Spain

Portugal

Current order book (Total: €291Mn)

• Dublin Airport, Terminal 2 – Ireland - €48,2Mn - 2009

• Office Building – Bucharest, Romania - €8,5Mn – 2008

• Jerónimo Martins Logistics Center – Poland – €14Mn – 2008

• Dolce Vita Tejo Shopping Centre – Lisbon, Portugal -€16Mn – 2008

• Artenius PTA Factory – Sines, Portugal - €22,4Mn - 2009

• Malaga Airport – Spain - €16,2Mn – 2008

• Plod Huambo Logistics Centre – Angola – €14Mn - 2009

Some significant works in progress(Project, Country, Total Value, Conclusion)

101

23

39

6 7

56

28

31

59

Martifer is investing to address growing markets

Romania

• Martifer is currently building a 25.000 m2 industrial facility in Calarasi, Romania

• Installed capacity of 14.000 ton/year

• The plant will employee 85 people

• This investment is a response to the growing demand from the Romanian market

• Investment will reach €8,8Mn and will be completed in 2008

Angola

• The construction of an industrial facility in Angola is still on hold due to delays in obtaining construction license

• The market is being served from Portugal

60

India

• Martifer has been analysing the Indian market since the end of 2007, including several site visits

• PEBs (pre-engineered steel buildings) represent a promising market for newentrants in India, with projected growth rates of 25-30% per year

• Based on the projected infrastructure and construction investments in India, some of the attractive PEB segments for investing in could be warehouses, cold storages, aircraft hangars, cargo buildings and railway stations

• There could be a tremendous opportunity in India

• At this time, Martifer is negotiating with a local entity a partnership for the Indian market

61

FINANCIAL OVERVIEW

6262

Martifer has a track record of growth

€ Mn20071 Chang. 20061 Chang. 2005

Revenues 518,5 86% 278,7 87% 148,9

EBITDA 37,0 49% 24,9 60% 15,6

EBITDA margin 7,1% 8,9% 10,5%

EBIT 21,8 29% 16,9 88% 9,0

EBIT margin 4,2% 6,1% 6,0%

Net financial expenses 4,4 71% 2,5 -4% 2,6

Taxes 4,8 9% 4,4 159% 1,7

Net Earnings 12,6 23% 10,3 119% 4,7

Attributable to min. -0,2 n.s. 1,1 57% 0,7

Attributable to group 12,8 39% 9,2 130% 4,0

Consolidated income statement (IFRS/IAS) for the periods ended December 2007, 2006 and 2005 – excluding non-recurring items

1 These figures exclude some non-recurring items, namely the recording of a capital gain of €3,7Mn in 2006 due to the sale of some REpower systems shares, the recording of a capital gain of €21,1Mn in 2007 resulting from the accounting of the dilution in the share capital of REpower Systems in this period and a non-recurring cost of €7,5Mn related to costs with the bid on REpower Systems.

6363

1Q2008 Consolidated Results

• Consolidated operational revenues reached €159,1Mn, representing a 71% growth when compared to the same period of 2007. All business units contributed to revenues growth.

• EBITDA of €12,6Mn, representing an increase of 148% versus same period last year and an increase of its margin from 5,5% to 7,9%.

• Financial expenses in the quarter were €4,1Mn, of which net interest paid of €3,4Mn, due to the increased net debt position of the Group, and unfavourable currency changes of €0,5Mn.

• Net earnings reached €1,4Mn in the first quarter. Compared to 1Q2007, the decrease is due to the larger level in depreciations, financial expenses and taxes more than offsetting the increase in EBITDA.

€ Mn1Q

2008 Marg. Chang.

1Q2007 Marg.

Revenues 159,1 71% 93,0

EBITDA 12,6 7,9% 148% 5,1 5,5%

EBIT 7,5 4,7% 130% 3,2 3,5%

Net financial expenses 4,1 2,6% 294% 1,0 1,1%

Taxes 1,9 1,2% 169% 0,7 0,8%

Net Earnings 1,4 0,9% -3% 1,5 1,6%

Attributable to min. 0,9 0,6% -467% -0,2 -0,3%

Attributable to group 0,5 0,3% -69% 1,7 1,9%

Consolidated income statement (IFRS/IAS) for the periods ended March 2008 and March 2007 – unaudited

6464

Operational revenues 1Q2008 1Q2007

€ Mn Weight € Mn Weight Change

Martifer Consolidated 159,1 93,0 71%

Metallic Construction 71,2 45% 58,4 63% 22%

Energy Systems 37,2 23% 17,5 19% 112%

Electricity Generation 5,8 4% 0,0 0% n.s.

Agriculture & Biofuels (1) 48,7 31% 22,5 24% 116%

Holding, elim. and adjust. -3,9 -2% -5,4 -6% -29%

EBITDA 1Q2008 1Q2007

€ Mn Margin € Mn Margin Change

Martifer Consolidated 12,6 7,9% 5,1 5,5% 148%

Metallic Construction 6,9 9,7% 5,7 9,8% 21%

Energy Systems 3,2 8,6% 1,1 6,0% 203%

Electricity Generation 1,3 22,8% -0,4 neg. n.s.

Agriculture & Biofuels (1) 1,9 3,8% -1,1 neg. n.s.

Holding, elim. and adjust. -0,7 n.s. -0,2 n.s. 319%

1Q2008 Segmental Overview of Results

(1) Prio, the holding company for the Agriculture & Biofuels business area, is held in 60% by Martifer.

(1) Prio, the holding company for the Agriculture & Biofuels business area, is held in 60% by Martifer.

• Metallic Construction remains the highest contributor but is losing weight to the other business areas.

• Revenues from Agriculture & Biofuels showed the largest growth (increase of €26,1Mn, representing a +116% growth compared to 1Q2007).

• Energy Systems also recorded significant growth, +112% compared to 1Q2007.

• First significant revenues from Electricity Generation in the first quarter, reaching €5,8Mn, of which €3,8Mn from the wind farms in Germany.

• Consolidated EBITDA margin increased from 5,5% to 7,9% as EBITDA improved at Energy Systems and became positive in Electricity Generation and Agriculture & Biofuels. EBITDA margin in Metallic Construction remained stable at 9,7%.

6565

1Q2008 Consolidated Balance Sheet

• Net Debt of €348,2Mn at the end of the period, an increase of €138,7Mn versus YE2007.

• This increase results mainly from investments in working capital (€32Mn), fixed assets (€27Mn) and financial stakes in EDP and Prio (€85 Mn).

• The group presents a solid financial position to pursue its ambitious investment plan.

• Net Debt is residual if we consider the financial stakes of Repower (Put option of 270 M€ exercisable in less than 1 year) and EDP.

• Strong investment program shall continue to impact depreciations and net results in the short term.

• However, we expect significant increase in operational cashflow contribution to the financing of the investment plan.

Mar 2008 Change Dec 2007

Fixed assets (including goodwill) 458,8 26,3% 363,2

Assets available for sale (Repower stake) 67,5 0,0% 67,5

Inventory and receivables 409,9 22,9% 333,5

Derivatives, cash and cash equivalents 46,7 33,9% 34,9

Total assets 982,8 23,0% 799,1

Shareholders equity 270,3 -4,1% 281,8

Minority interests 4,6 25,6% 3,7

Total shareholders equity 274,9 -3,7% 285,5

Non-current liabilities 47,2 0,9% 46,8

Current liabilities 265,8 19,5% 222,5

Debt + Leasings 394,9 61,6% 244,4

Total liabilities 707,9 37,8% 513,6

Consolidated Balance Sheet (IFRS/IAS) at 31 March 2008 – unaudited - and 31 December 2007 – audited

6666

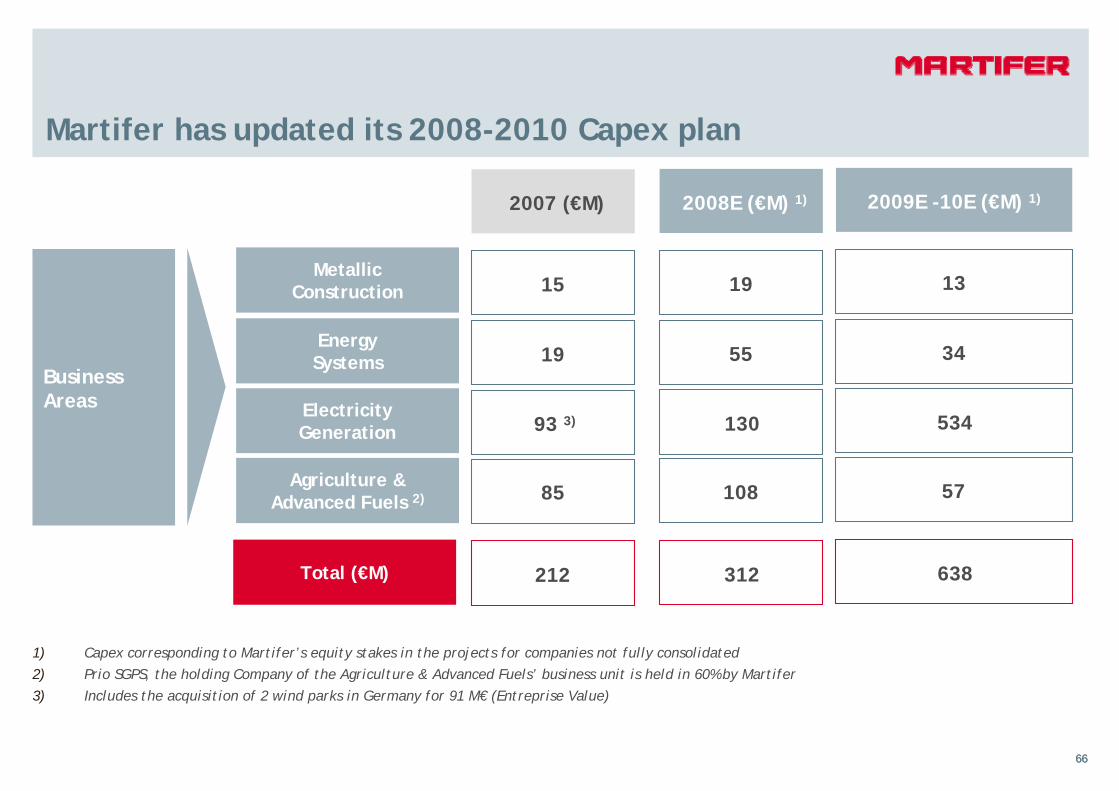

Martifer has updated its 2008-2010 Capex plan

BusinessAreas

15

2007 (€M)

19

93 3)

85

212

13

2009E -10E (€M) 1)

34

534

57

638

Energy Systems

MetallicConstruction

Electricity Generation

Agriculture &Advanced Fuels 2)

Total (€M)

19

2008E (€M) 1)

55

130

108

312

1) Capex corresponding to Martifer’s equity stakes in the projects for companies not fully consolidated2) Prio SGPS, the holding Company of the Agriculture & Advanced Fuels’ business unit is held in 60% by Martifer3) Includes the acquisition of 2 wind parks in Germany for 91 M€ (Entreprise Value)

67

Capex Plan and Outlook for 2008

Despite ambitious targets settled for 2008, Business Units are confident they will be achieved:

Revenues Ebitda Margin

Metallic Constructions 340 M€ 10%

Energy Systems 300 M€ 9%

Electricity Generation 10 M€ 40%

Agriculture & Biofuels 315 M€ 5%

Capex Plan until 2010 was updated :

• Metallic Constructions: + 21 M€, new facility in Romania and investment in Australia

• Energy Systems Wind: + 54 M€, o.w. 30 M€ in Portuguese industrial cluster and 24 M€ in a new tower plant in the US

• Energy Systems Solar: less 28 M€, suspension of industrial investments in PV cells and wafers more than offset capacity increase in PV modules

• Biofuels: less 78 M€, as result of suspending capacity increase in biodiesel plants and size of distribution network

6868

Stock performance since the IPO

0

200.000

400.000

600.000

800.000

1.000.000

1.200.000

Jun-07 Jul-07 Ago-07 Set-07 Out-07 Nov-07 Dez-07 Jan-08 Fev-08 Mar-08 Abr-08 Mai-08 Jun-08

5,50

6,50

7,50

8,50

9,50

10,50

11,50

€Shares

69

70

75

80

85

90

95

100

105

110

115

120

Dez Jan Fev Mar Abr Mai

70

80

90

100

110

120

130

140

150

Jun Jul Ago Set Out Nov Dez Jan Fev Mar Abr Mai

Relative stock performance

Martifer versus PSI20 since IPO Martifer versus PSI20 year to date

-8%

-24%

-10%

-21%

Martifer

PSI 20

Martifer

PSI 20

70