Embed Size (px)

Citation preview

Australian Food and Grocery Councilwww.afgc.org.au

AFGCMARKET INSIGHTS: CHINA

Australian Food and Grocery Council (AFGC)

Address Level 2, Salvation Army Building 2-4 Brisbane Ave Barton ACT Australia 2600

Postal Address Locked Bag 1 Kingston ACT Australia 2604

www.afgc.org.au

ABN 23 068 732 883

This report was prepared by:

Expand into Asia www.trade-worthy.com

This Market Insights report is published for information only. It does not constitute advice or service, and no liability is accepted for negligence, omission or error of any nature. You must obtain your own advice and conduct your own investigations independently from this information.

© Copyright Australian Food and Grocery Council 2014

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

I

CONTENTSTables V

Figures VI

Pictures VI

Message from AFGC VII

Message from Austrade VII

Introduction VIII

Product and Geographic Coverage VIII

Structure of the Report IX

Sources of Further Information X

Defined Terms in this Market Insights report X

Executive Summary XI

PART 1 11. The Big Picture 2

1.1 Demographics 2

1.2 Economic Overview 2

1.3 Food trade with Australia 3

2. Food and Beverage Trends 4

2.1 Broad trends in food and beverage consumption 4

2.2 Attitude to imported food and beverage 5

2.3 Outline of the food and beverage supply chain 6

3. Regulatory and Trading Environments 16

3.1 Trade policy position and approach to trade agreements 16

3.2 Trade Barriers 17

Summary 26

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

II

PART 24. Snackfoods 22

4.1 Chocolates 22

4.2 Sugar Confectionery 26

4.3 Cereal-based Bars 30

5. Beverages 33

5.1 Fruit Juice 33

5.2 Tea 37

5.3 Premium Cold Beverages (non-alcoholic) 40

6. Baked Goods 44

6.1 Biscuits 44

6.2 Baking Mixes 48

7. Condiments 52

7.1 Premium Table Sauces 52

7.2 Jams 56

ANNEXES 60Annex I — Store Checks China 60

Annex II — Key Retailers in the Chinese Premium Retail Market 75

Annex III — Key Distributors in the Chinese Premium Retail Market 77

Annex IV — Key Players in China’s Premium HoReCa Market 79

Annex V — Key Government Bodies 80

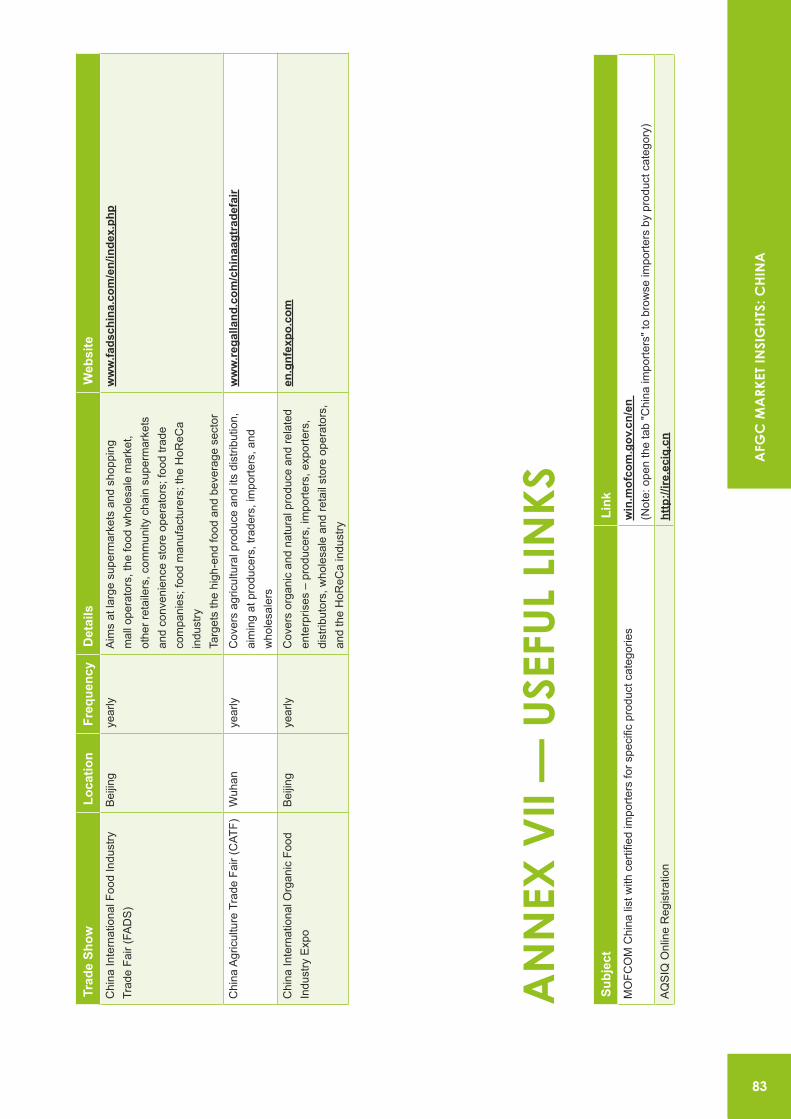

Annex VI — Major Food and Beverage Trade Shows in China 82

Annex VII — Useful Links 83

Annex VIII — Food Regulation and Trade Barriers 84

Annex IX — Sources of Further Information 88

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

III

TABLESTable 1: China GDP and GDP per capita 2

Table 2: Market sizes and anticipated 3 year CAGR for Selected Product Categories 4

Table 3: Top 10 hypermarket and supermarket operators in China 6

Table 4: Top 10 convenience store operators in China 9

Table 5: Top 3 online food and grocery retailers in China 13

Table 6: China's Free Trade Agreements 16

Table 7: Characteristics of surveyed snackfood sub-categories 22

Table 8: Overview of packaging and price point ranges — chocolate 22

Table 9: Overview of packaging and price point ranges — sugar confectionery 26

Table 10: Overview of packaging and price point ranges — cereal-based bars 30

Table 11: Characteristics of surveyed beverage categories 33

Table 12: Overview of packaging and price point ranges — fruit juice 33

Table 13: Tariff rates for selected types of fruit juice 37

Table 14: Overview of packaging and price point ranges — tea 37

Table 15: Overview of packaging and price point ranges — premium cold beverages 41

Table 16: Characteristics of surveyed baked goods categories 44

Table 17: Overview of packaging and price point ranges — biscuits 44

Table 18: Overview of packaging and price point ranges — baking mixes 48

Table 19: Characteristics of surveyed condiments sub-categories 52

Table 20: Overview of packaging and price point ranges — Premium Table Sauce 52

Table 21: Overview of packaging and price point ranges — Jams 56

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

IV

FIGURESFigure 1: Market Share of China's Total Food Imports 3

Figure 2: Routes to the market — Retailers 12

Figure 3: Routes to the market — HoReCa 14

Figure 4: Major chocolate brands in the Chinese Selected Premium Retail Market 23

Figure 5: Major sugar confectionery brands in the Chinese Selected Premium Retail Market 27

Figure 6: Major cereal-based bars brands in the Chinese Selected Premium Retail Market 30

Figure 7: Major fruit juice brands in the Chinese Selected Premium Retail Market 34

Figure 8: Major tea brands in the Chinese Selected Premium Retail Market 38

Figure 9: Major premium cold beverages brands in the Chinese Selected Premium Retail Market 41

Figure 10: Major biscuits brands in the Chinese Selected Premium Retail Market 45

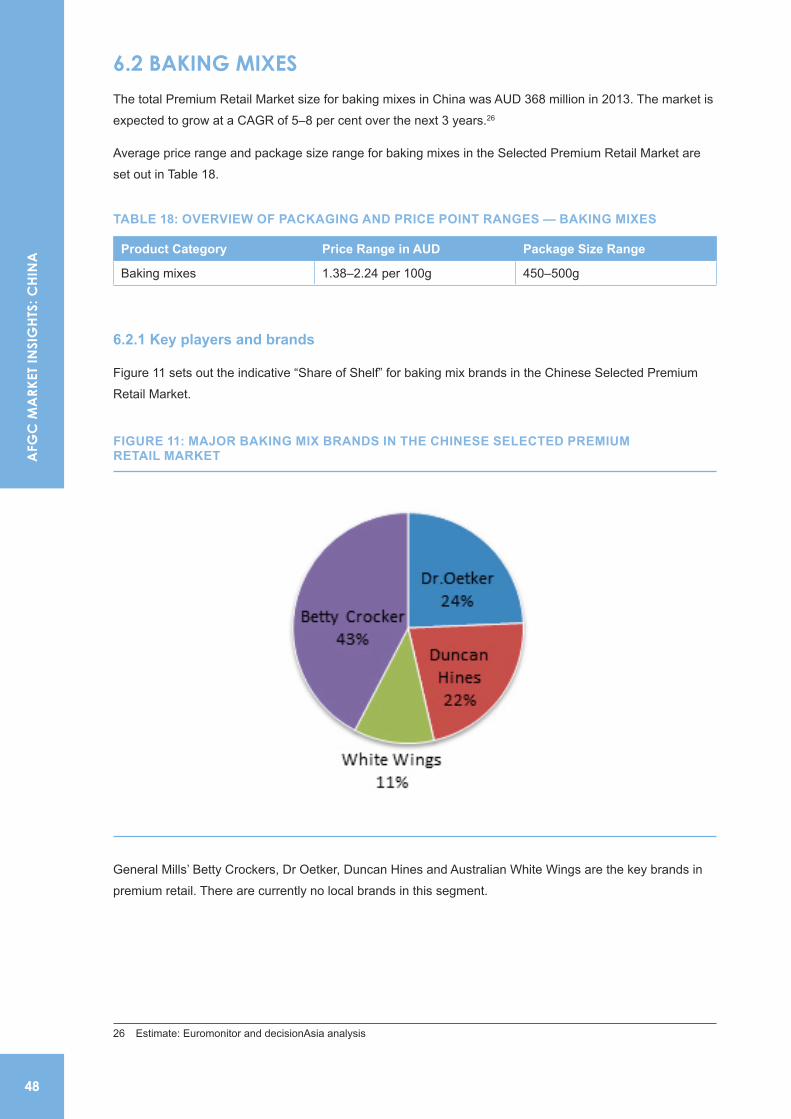

Figure 11: Major baking mix brands in the Chinese Selected Premium Retail Market 48

Figure 12: Major Premium Table Sauce brands in the Chinese Selected Premium Retail Market 53

Figure 13: Major jam brands in the Chinese Selected Premium Retail Market 56

PICTURESPicture 1: Shelf display at Tesco China 7

Picture 2: China – geographical division for supply chain purposes 10

Picture 3: Shelf with chocolate gift boxes at Ole Supermarket 25

Picture 4: Shelf with sugar confectionery at City Shop 28

Picture 5: Cereal-based bars on wangooshop — a Chinese online retailer that caters to expatriates 31

Picture 6: Minute Maid displayed at end of gondola — Lianhua Supermarket 35

Picture 7: Shelf with tea boxes at Tesco China 39

Picture 8: Premium cold beverage shelf at City Super 42

Picture 9: Biscuits shelf at Tesco China 47

Picture 10: Baking mixes shelf display at City Shop 49

Picture 11: Stick on labels for baking mixes - Duncan Hines 50

Picture 12: Premium Table Sauce shelf display at Lianhua 55

Picture 13: Jams shelf display at City Shop 57

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

V

MESSAGE FROM AFGCThe Australian Food and Grocery Council (AFGC) is the leading national organisation representing Australia’s food, drink and grocery manufacturing industry. The membership of AFGC comprises more than 178 companies, subsidiaries and associates which constitutes in the order of 80 per cent of the gross dollar value of the processed food, beverage and grocery products sectors.

The China Market Insight forms part of the AFGC’s renewed engagement on international trade issues. We hope that this information, along with the information on the markets in Malaysia and Thailand, will assist all food industry companies.

www.afgc.org.au

MESSAGE FROM AUSTRADEThe Australian Trade Commission — Austrade — contributes to Australia’s economic prosperity by helping Australian businesses, education institutions, tourism operators, governments and citizens as they:

� develop international markets

� win productive foreign direct investment

� promote international education

� strengthen Australia’s tourism industry

� seek consular and passport services.

We achieve this by generating market information and insight, promoting Australian capabilities, developing policy, making connections through an extensive global network of contacts, leveraging the badge of government offshore and providing quality advice and services. This activity has received funding from Austrade as part of the Asian Century Business Engagement Plan.

www.austrade.gov.au

The views expressed herein are not necessarily the views of the Commonwealth of Australia, and the Commonwealth does not accept any responsibility for any information or advice contained herein.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

VI

INTRODUCTION With rising incomes and increasing consumer demand across Asia presenting export opportunities for Australian based food and beverage manufacturers, the Australian Food and Grocery Council (AFGC) commissioned a series of reports to deepen Australian industry understanding of particular markets.

While Australian and international research has focussed on export opportunities for products such as dairy, meat and wine across Asian markets, there has been little focus on the opportunities for manufactured food products such as snacks, non-alcoholic beverages, and confectionary.

The aim of this project is to provide insights into some of the opportunities that exist for specific manufactured food products in particular markets as a means of contributing to, and supporting the development of, better knowledge of export opportunities of manufactured food into Asia.

PRODUCT AND GEOGRAPHIC COVERAGEWhile there are export opportunities across Asia, the AFGC Market Insights focus on three key markets: Thailand and Malaysia because of improved access under the respective trade agreements; and China due to the long term food consumption forecasts.

This Market Insights series of reports focus on the premium retail and Hotels/Restaurants/Cafes (HoReCa) sector, for the following specific products:

� Snackfoods

– Chocolate

– Sugar Confectionery

– Cereal-based Bars

� Beverages

– Fruit Juice

– Tea

– Premium Cold Beverages

� Baked Goods

– Biscuits

– Baking Mixes

� Condiments

– Premium Table Sauces

– Jams

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

VII

By concentrating on specific products, the Market Insights report is able to bring deeper insights into the key considerations for Australian food & beverage manufacturers. These products have been selected for initial focus for two reasons: (i) each has witnessed significant import growth (between $6m–$219m from 2010–2012 1) into the target markets , and (ii) they are export items supported by capabilities of the Australian food & beverage sector. Together, these products represent opportunities for food & beverage exports from Australia into China.

The Market Insights report offers detailed practical insights into specific product categories, far beyond information which is in the public domain. Manufacturers in the product categories covered (snacks, beverages, baked goods, condiments) — or those with capability to extend into these categories — should find the detailed insights both practical and compelling.

STRUCTURE OF THE REPORT We recommend that you find your own path through this Market Insights report, which may not necessarily be from cover to cover.

Part I of this report contains important information about market size and growth, food & beverage trends, key trade shows and routes to market, as well as regulatory and trading considerations such as labelling standards. This information will be useful for new exporters and for established exporters looking to revisit the underlying market dynamics.

Those with some background and experience in China may wish to skip directly to the content relevant to their specific product lines, which falls in Part II of this Guide. There you will find details — for each covered product category – such as ‘share of shelf’ for key brands, packaging size, price points, tastes and promotional trends, any trade barrier details – and contacts for key retailers and distributors in the market. For those seeking even more detail, the report contains the detailed results of premium retail store surveys across China.

1 Analysis of data from UN Statistical Database ‘Comtrade’ 2014

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

VIII

SOURCES OF FURTHER INFORMATIONCommercial realities, market averages and product trends change frequently. The insights and contact details provided in this Market Insights report are likely to change over time. The Annexes contain a list of organisations, agencies and companies that may assist in providing further information.

DEFINED TERMS IN THIS MARKET INSIGHTS REPORTThere are several defined terms used throughout this Market Insights report, which are critical to understanding the results and implications. These include:

Australian Suppliers Australian food and beverage manufacturers who may seek to export from Australia into China.

Premium HoReCa Market Premium hotel, restaurant and café groups and franchises targeting middle and upper-middle income customers.

Selected Premium HoReCa Market Those Premium HoReCa Market groups and franchises included in the survey underlying this Market Insights report, as set out in Annex IV.

Selected Premium Retail Market Those Premium Retail Market stores included in the survey underlying this Market Insights report, as set out in Annex II.

Selected Product Categories Those product categories included in the survey underlying this Market Insights report (snacks, beverages, baked goods, condiments).

Premium Retail Market Premium retail outlets supplying food and beverage to middle and upper-middle income customers.

Exchange Rates AUD 1 = 5.8 Chinese Renminbi

AUD 1 = 0.95 United States Dollars

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

IX

EXECUTIVE SUMMARYWith rising incomes and increasing consumer demand across Asia presenting export opportunities for Australian based food and beverage manufacturers, the Australian Food and Grocery Council (AFGC) with funding assistance from Austrade, commissioned a series of reports to deepen Australian industry understanding of the opportunities that exist. These reports examine opportunities for specific manufactured food products — snacks, beverages, baked goods and condiments – in Malaysia, Thailand and China.

This report is focussed on China — a market with immense and growing opportunities but a market which requires meticulous planning, a strategic approach to market entry, and patience.

While each manufacturer must uncover their own unique value proposition in the Chinese market — including by comparing their own offering with the prices, packaging, and flavours identified in this report, there are several consistent themes across the market:

� The Chinese processed food and beverage market is very much globalised with competitors from a diverse range of countries including Europe, the United States, and South East Asia through to local Chinese manufacturers.

� Australian food products are generally well regarded and more likely to be competitive at the premium end of the market – given our limited scale of production and global reputation.

� At the premium end, package sizes are shrinking and high quality defined-source ingredients (and verifiable health claims) are of growing importance to the Chinese consumer.

� Each exporter must map out their entry strategy – store format, target cities, direct or through distributors. If starting from scratch, premium food producers should consider targeting emerging premium supermarkets through experienced importer/distributors – some of which are identified in this report.

The challenges of market entry into China – labelling, import taxes and customs – should not cloud the opportunity. These can be deftly handled by experienced importer/distributors if they are convinced of the unique value to their target buyers.

In terms of the specific product categories, there are a wide range of opportunities to be considered as part of an individual company’s approach to the China market. This report highlights a number of opportunities for each category including:

� Chocolates: Gift giving is an important element of Chinese culture. Premium chocolate products with appropriate packaging can be marketed as gifts, particularly for festival celebrations.

� Sugar Confectionery: There is a trend toward sugar confectionery becoming a more regular snack in the market however there is a preference for less sweet products.

� Cereal Bars: Demand for healthy cereal bars is growing but currently in early phases of market development. Opportunity exists for Australian exporters to become established as part of growing market.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

X

� Fruit Juice: Similar to Australia, there is opportunity for premium fruit juice products in coffee shops in China. Opportunity exists for carbonated juice products to be sold as non-alcoholic beverages.

� Tea: There is currently a strong focus on traditional teas and the market for other types of tea, including flavoured tea, is in the early stages of development. There is an opportunity to promote Australian products as clean and safe however it is a very price competitive market.

� Premium Cold Beverages: There is a consumer focus on healthy beverages with fruity flavours and vitamins. A strong opportunity for healthy and natural carbonated beverages exists in the market.

� Biscuits: In a highly competitive market, the opportunity for biscuits is in gift giving, particularly in association with festivals. Products need premium packaging and strong product promotion appropriate for the market.

� Baking mixes: The market for baking mixes is in the early stages of development as ovens are not yet widely available at home. Cake mixes are more popular than bread mixes and a specific demographic is increasingly baking cakes on the weekend.

� Premium Table Sauces: Soy sauce is the first choice for Chinese households, with increasing popularity of chili and black bean sauces given the familiarity of flavours. Of western style sauces, Worcestershire and mayonnaise are increasingly popular however new flavour combinations may have greater appeal in a saturated market.

� Jams: The market for jams is characterised for a preference for less sweet products. Jam products will benefit from heavy promotion, with orange, strawberry, and mixed fruits the current popular flavours.

The AFGC hopes this Market Insights report assists Australian suppliers to understand the characteristics and export opportunities of the Chinese market and to assess whether their products suit the needs of Chinese consumers or require modification for this market.

PART 1

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

2

THE BIG PICTURE

1.1 DEMOGRAPHICSThe demographic picture of China is well known, and simply staggering. China’s growing population (currently 1.35 billion) is expected to reach 1.384 billion in 2020, with a growth rate of 0.5 per cent (2012). The population is growing older, with 15 per cent aged between 15 and 24, 47 per cent aged between 25 and 54, and 20 per cent aged 55 or older.2 The Chinese Government expects that China will become the world’s most aged society in 2030.

The ratio of urban to rural population is about 52:48.3 China has a high population density, with most densely populated areas located in the Yangtze River Valley, the Sichuan Basin, the North China Plain, the Pearl River Delta, and the Shenyang area in the northeast. Geographic income disparities are an entrenched feature, with an immense contrast between poor rural areas and the wealthier urban, coastal areas.

1.2 ECONOMIC OVERVIEWDespite its developing country status, China recently became the second largest economy in the world. From the initiation of the market reforms in the late 1970s, China continues to shift from a centrally planned to a market-based economy and has witnessed rapid economic and social development.

China’s GDP grew by 7.8 per cent in 2012 (AUD 8.66 trillion) and GDP per capita was AUD 6,412.

TABLE 1: CHINA GDP AND GDP PER CAPITA4

2009 2010 2011 2012

GDP (AUD billion) 5,254 6,243 7,707 8,660

Real GDP Growth 9.2% 10.4% 9.3% 7.7%

GDP per capita (AUD) 3,946 4,666 5,734 6,412

Closely linked to China’s GDP growth is rapidly rising disposable income in urban areas, resulting in a middle-income consumer boom in areas such as Shanghai, Guangdong, Beijing and Sichuan. Urban households earning more than USD 5,000 (AUD 5,263) per year are expected to grow by 24 per cent annually — a growing consumer base for high-quality and high-value imported food.

Research by McKinsey suggests that China’s urban incomes will double by 2022, with more than 22 per cent of China’s urban consumers considered middle class, earning USD 9,000 – 16,000, and 54 per cent considered upper middle class, earning USD 16,000 – 34,000.5

2 Worldbank (2014)3 Worldbank (2014)4 Worldbank (2014)5 http://www.mckinsey.com/insights/consumer_and_retail/mapping_chinas_middle_class

1

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

3

1.3 FOOD TRADE WITH AUSTRALIA While China is one of the largest agricultural producers in the world, with production estimated at more than USD 947 billion, China is also a large net importer of food, with annual imports valued at AUD 89.8 billion.6 On current trends, China will import almost a third of all food globally available by 2030.7 Around 5 per cent of Chinese merchandise imports are food and beverage products.8

China is Australia’s 3rd biggest export market for food and beverage and the biggest in terms of groceries. China is also Australia’s 7th biggest export market for fresh produce. Australia’s market share of China’s total food imports has been between 3 per cent–4 per cent over the last decade, though has recently trended downward by comparison to other food export nations such as Indonesia, New Zealand and France (Figure 1 below). Australia’s major food and beverage exports into China are dairy, meat, wine, cereals, oils and fats, baked goods, and beverages. Major growth categories are oilseeds, chocolates, cereals, fruits and nuts, meat and gums.9

FIGURE 1: MARKET SHARE OF CHINA'S TOTAL FOOD IMPORTS (SOURCE: UNITED NATIONS STATISTICAL DIVISION)

6 Austrade (2014)7 Economist Intelligence Unit (2014)8 Worldbank (2014)9 Analysis of data from UN Statistical Database ‘Comtrade’ 2014

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

4

FOOD AND BEVERAGE TRENDS

China is currently Asia’s second largest food and beverage market by value, after Japan. As China’s economy grows and appetite for sophisticated consumer products develops, there are significant and growing opportunities for Australian food and beverage companies seeking to enter the Chinese market — particularly at the premium end.

2.1 BROAD TRENDS IN FOOD AND BEVERAGE CONSUMPTION

In China, the total Premium Retail Market for the Selected Product Categories constitutes a considerable market with growth in the range of 4 per cent to 20 per cent expected over the next three years, as set out in Table 2 below.

TABLE 2: MARKET SIZES AND ANTICIPATED 3 YEAR CAGR FOR SELECTED PRODUCT CATEGORIES

Product Category China Market size in AUD million

Expected CAGR for the next 3 years

Snackfood 7,579 N/A

Chocolate 1,579 10% – 12%

Sugar Confectionery 5,789 7% – 8%

Cereal-based Bars 211 8%

Beverages 19,526 N/A

Fruit Juice 1,842 8% – 10%

Tea 4,000 15% – 17%

Premium Cold Beverages 13,684 14% – 20%

Baked Goods 1,526 N/A

Biscuits 1,158 15% – 20%

Baking Mixes 368 5% – 8%

Condiments 6,632 N/A

Premium Table Sauces 5,789 8% – 9%

Jams 842 4% – 5%

› Specific product trends and insights are included in the relevant product category sections .

2

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

5

A shift in target groups

� Due to the combined effects of an increasing population, longer life expectancy and increasing individual food consumption, China will need to produce or import considerably more food in the future to cover demand.

� A broader middle class – with a higher average age – is increasing interest and consumption of higher quality and imported foods; particularly those with bona fide health claims.

� Single-person households are proliferating, resulting in stronger demand for smaller, “micro” portions in the food and beverage sector.

� With recent relaxation in China’s one child policy, there is expected to be an increase in demand for safe, healthy and organic food and beverages for babies and children.

Food Safety concerns

� Recent food safety incidents– especially related to milk, milk powder and meat – have resulted in food safety being a major concern for the Chinese, and growing demand for brands – particularly imported — that can demonstrate traceability in their supply chains to guarantee safety and authenticity.

Increasing importance of Western style products and health foods

� Western style products are perceived as high quality and more creatively flavoured.

� There is an increasing interest in fresh and better-for-you (BFY) foods, for which consumers pay premium prices. The health food market, which includes food with additional health claims and nutritional supplements, is valued at AUD 103.5 billion and forecast to reach AUD 172.4 billion in 2015.10 A large part of the health food segment is accounted for by organic food - in 2012, the Chinese spent AUD 13.8 billion on organic foods.11

2.2 ATTITUDE TO IMPORTED FOOD AND BEVERAGESince 2009, China has been the world’s third largest importer of goods and services. The key drivers of consumption of imported food and beverage in China are rising incomes and previous domestic food safety incidents. Imported food and beverage is considered good quality, nutritious and — most importantly — safe. Major imported food categories are dairy, meat, wine, snack foods, tree nut products and confectionery.

In response, retailers are increasingly open to imported products in more categories than ever before. The metropolitan areas of Beijing, Shanghai, Guangzhou, Shenzhen, Chongqing and Chengdu offer the largest range of imported foods and beverages, but emerging second tier markets and wealthy coastal cities are growing in appetite for imported food products. The majority of customers are still expatriates and upper-middle income locals.

Suppliers from the US and EU still have a competitive advantage over Australian suppliers in the food & beverage sector, due to deeper experience in the market, and economies of scale creating lower unit costs.

10 HKTDC Research (2013)11 Euromonitor (2013)

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

6

However, Australian products, particularly meat and dairy, are perceived as very safe, providing opportunity to further leverage this reputation to Australian food production more generally. This creates the need for Australian suppliers to position themselves in the premium and gourmet market rather than trying to compete with lower-priced products.

2.3 OUTLINE OF THE FOOD AND BEVERAGE SUPPLY CHAIN China has a very fragmented food and beverage supply chain. Although management across the retail sector has improved recently, most store formats are difficult for foreign manufacturers to penetrate directly. In addition, the distribution generally network lacks consistency and has interrupted transport networks as well as a less sophisticated cold chain.

2.3.1 Retail store formats

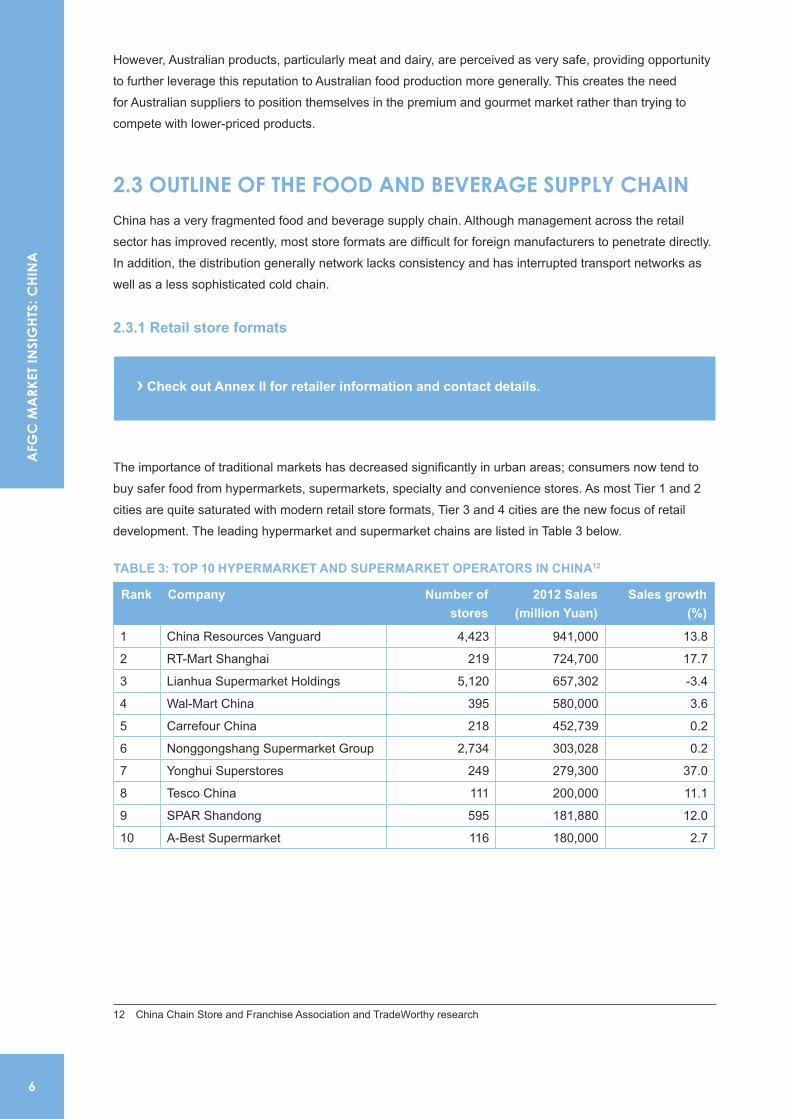

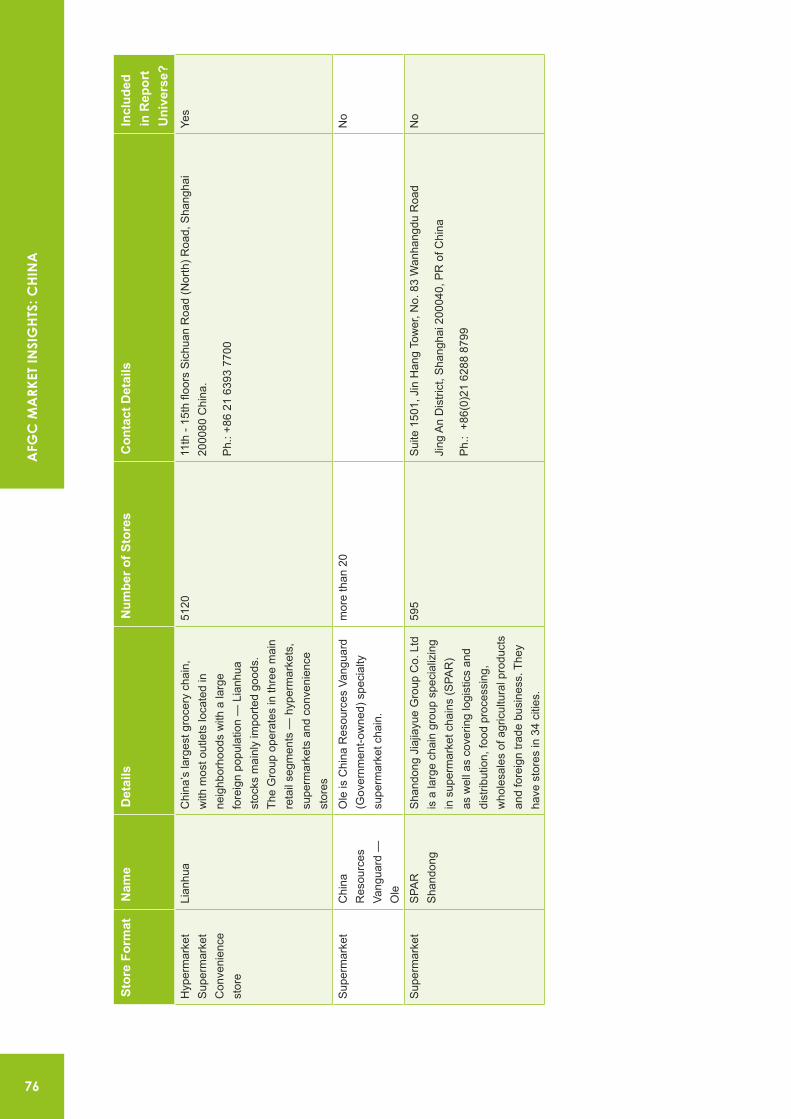

The importance of traditional markets has decreased significantly in urban areas; consumers now tend to buy safer food from hypermarkets, supermarkets, specialty and convenience stores. As most Tier 1 and 2 cities are quite saturated with modern retail store formats, Tier 3 and 4 cities are the new focus of retail development. The leading hypermarket and supermarket chains are listed in Table 3 below.

TABLE 3: TOP 10 HYPERMARKET AND SUPERMARKET OPERATORS IN CHINA12

Rank Company Number of stores

2012 Sales (million Yuan)

Sales growth (%)

1 China Resources Vanguard 4,423 941,000 13.8

2 RT-Mart Shanghai 219 724,700 17.7

3 Lianhua Supermarket Holdings 5,120 657,302 -3.4

4 Wal-Mart China 395 580,000 3.6

5 Carrefour China 218 452,739 0.2

6 Nonggongshang Supermarket Group 2,734 303,028 0.2

7 Yonghui Superstores 249 279,300 37.0

8 Tesco China 111 200,000 11.1

9 SPAR Shandong 595 181,880 12.0

10 A-Best Supermarket 116 180,000 2.7

12 China Chain Store and Franchise Association and TradeWorthy research

› Check out Annex II for retailer information and contact details.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

7

PICTURE 1: SHELF DISPLAY AT TESCO CHINA

Hypermarkets

The Chinese hypermarket format has been largely designed by foreign operators, such as Carrefour Wal-Mart, Tesco, Auchan, Metro and RT-Mart. The proportion of imported food in hypermarkets is increasing with current levels around 60 per cent of total stock. Hypermarkets have a reputation for offering products of superior quality (compared to domestic stores) and greater levels of perceived food safety due, in part, to higher product volumes.

Hypermarkets are a major sales channel for imported products. There is a strong focus on in-store promotion, including free sampling. This trade spend can prove expensive in China, and may include listing fees and agreeing to accept returns of unsold products after promotional campaigns have ended.

Most Australian suppliers will find it difficult to deal directly with hypermarket operators, due to their heavy reliance on a network of favoured distributors. Distributors to hypermarkets tend to be large scale businesses, and may be risk averse when considering entirely new product lines.

Supermarkets

The Chinese supermarket segment is dominated by domestically owned companies with less experience of modern retail practices. The major names are Lianhua with more than 5,000 stores and China Resources Vanguard with almost 4,500 stores. Another player is Suguo with more than 900 stores. The market has a ‘long tail’ of small chain or independent supermarkets. Smaller style stores are the new trend — even for the larger chains. This reflects the desire to shop close to home as most customers do not own their own transport.

The supermarket segment is more price-driven than the hypermarket or convenience store segments, as the target group are lower middle income customers. Import penetration - especially state-owned larger chains – tends to be low. Smaller privately held chains are more likely to look for value in high-margin imports and they typically have better local distribution systems in place.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

8

Premium supermarkets

Several supermarket and hypermarket operators have invested in high-end stores specialising in imported foods. These offer, on balance, the greatest opportunity for Australian suppliers of high-end food and beverage products.

Responding to the growing demand for health foods and organic and fresh produce, China Resources Vanguard launched Ole as their high-end supermarket chain. They operate more than 20 stores in the large cities, with 70 per cent of their products imported. Other popular specialty supermarket chains are City Shop, Pines and City Super in Shanghai, with 12, 5 and 5 branches respectively in the CBD and high-end residential areas. City Shop stock over 80 per cent imported products on their shelves. Additionally, there are boutique retailers such as BHG in Nanjing, Hisense Plaza in Qingdao, and Jin Bou Da in Zhengzhou that sell imported food and beverages. Specialty supermarkets and boutique retailers are often located adjacent to department stores or in business areas and have been multiplying in first and second tier cities.

As hypermarkets have started to attract lower to middle-class income customers with their promotional activities — including offering free shuttle bus services — many high-end customers have moved to specialty supermarkets to avoid the big crowds.

Convenience stores

Convenience store numbers are growing, but with great geographic imbalance across China – in cities such as Guangzhou and Shanghai, competition is fierce, but in Tier 3 and 4 cities this store format is still developing. Like in the supermarket segment, domestic chains lead the convenience store business — e.g. the Sinopec Group with their Easy Joy stores. Despite this, 7-Eleven has become a strong player in Southern China. There have been regulatory initiatives to increase store coverage. For example, Beijing City offers subsidised loans for the establishment of convenience stores and supermarkets. China’s major convenience store chains are listed in Table 4 below.

The convenience store format differs significantly to the other retail types, since it requires smaller package sizes and single servings. To avoid high packaging costs, exporters now commonly use importers to act as “repackers” who can import products in bulk and then repackage them, including Chinese labels and appropriate packaging for the market.

TABLE 4: TOP 10 CONVENIENCE STORE OPERATORS IN CHINA

Rank Company Store Brand Number of stores in 2012

1 Sinopec Group Easy Joy 20,891

2 PetroChina uSmile 13,000

3 Dongguan Sugar & Liquor Group Meiyija 4,650

4 Zhejiang Gongxiao Supermarket Gongxiao; Jialian 2,115

5 Shanghai Lianhua Quik Convenience Stores Quik 2,031

6 Nonggongshang Group Kedi; Alldays 1,780

7 7-Eleven 7-Eleven 1,732

8 China Resource Suguo Suguo 1,694

9 Guangdong Sun-high Convenience Store Sun-high 1,559

10 Chengdu Hongqi Hongqi 1,336

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

9

2.3.2 Premium HoReCa Market

China’s foodservice industry consists of over 6,500,000 food outlets (formal sector), with Yum! Restaurants being the key franchise player in the market, operating KFC, Pizza Hut and Taco Bell outlets. Currently the demand for outlets in non-standalone locations — such as department stores and petrol stations — is increasing. HoReCa chains will grow over the next decade as they build out networks in lower tier cities. HoReCa chains strongly promote their hygiene and food safety credentials, which will see their popularity increase as disposable incomes increase.

2.3.3 Routes to market

China does not have a consistent nationwide network of transport and cold chain, which means distribution channels change constantly. The channels are complex and vary widely throughout China based on geography, product type and retail sector. Geographically, China can be divided into three regions for supply chain purposes:

� North China, with Tianjin, Qingdao, Dalian and Qinhuangdao harbours

� East China, with Shanghai and Ningbo harbours

� South China, with Shenzhen and Xiamen harbours

From these big import hubs, goods are transported to secondary distribution centres like Harbin, Changchun and Shenyang in the northeast, Xi’an and Zhengzhou in the northwest, Wuhan in central China and Chengdu and Chongqing in the southwest. Tier 3 and 4 cities are serviced from there.

Direct import and distribution

Direct relationships between manufacturers (local and foreign) and retailers is increasing, though still the exception.

PICTURE 2: CHINA – GEOGRAPHICAL DIVISION FOR SUPPLY CHAIN PURPOSES

› Check out Annex IV for important Premium HoReCa Market contacts.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

10

Australian suppliers can establish a Foreign Investment Enterprise (FIE)13 in China and distribute products directly without any intermediaries. This gives them direct control over the import process into China and creates a direct link into the market. However, this is very time-consuming — building extensive networks and understanding the complex structures of the Chinese market are typically significant hurdles for small and medium-sized enterprises to take this route to the market.

Importers

Another option is to work with importers who can typically assist with the following:

� Checking for quarantine and sanitary requirements

� Transfer of documents

� Assisting with labelling issues

� Invoicing processes

� Warehousing and transportation

� Customs registration and clearance

� Payment of taxes and other fees

� Foreign exchange control

� Securing import quotas

Importers require a license and need to register with China’s Ministry of Commerce (MOFCOM). They can acquire an automatic import license if the product imported is in the product catalogue for automatic import license management. MOFCOM has published a database with certified importers for different product categories, which is available on their website.

It is typically more efficient to use an importer in China, particularly due to the regulatory and market complexities. Note that importers may or may not also act as distributors. If they are importers only, they will not attend to issues of in-market marketing and promotion.

Distributors

Distributors typically offer after-sales services and can partner with Australian suppliers for in-market marketing and promotional activities. They may also be licensed importers – which offers significant benefits in terms of a clear path to market.

Another option for Australian suppliers is to engage local agents to market products in China. They typically

13 Corporate forms of FIEs in China are Wholly foreign-owned enterprises (WFOE), Equity/Cooperative joint ventures (EJV/CJV), Foreign-invested companies limited by shares (FICLS), and Foreign-invested partnerships.

› The link to the MOFCOM distributor database can be found in Annex VII.

› Check out Annex III for importer/distributor information and contact details.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

11

have extended informal networks and are especially important for niche market products and distribution beyond the bigger cities on the Eastern Seaboard.

Australian suppliers seeking to enter Premium supermarkets should consider identifying distributors who ordinarily service the Premium HoReCa industry, as they are typically highly specialised and well networked in relation to a specific product sub-category.

FIGURE 2: ROUTES TO THE MARKET — RETAILERS

PRACTICAL TIPS

Dealing with Distributors

� Communicate your target market clearly

� Do not relinquish your trademark to a distributor

� Make sure that the distributor has a good record of references and has experience in your product category

� Make sure you agree on an appropriate distribution of costs in advance

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

12

Internet retailing

Having the world’s largest number of internet users at more than 480 million, China has witnessed rapid growth in internet retailing. Most Chinese internet retailers target high-income consumers. The online retail market accounted for 6.2 per cent of total retail sales in 2012.14 In addition to domestic retailers who do not operate physical stores, such as TMall and JD, many international retailers have directly or indirectly entered internet retailing business. Wal-Mart launched an internet retailing site for its Sam‘s Club chain back in 2010, and has invested in the rapid growing domestic online supermarket Yihaodian, in 2012 when they bought a 51 per cent stake in the business. Other large international retailers like Carrefour, Metro and Lotus have introduced online operations likewise.

14 iResearch

AUSTRADE INSIGHTS

How to enter Internet Retailing in China?

Australian suppliers can set up their own stores on online retail platforms, such as Yihaodian, Tmall, and JD. However, they all have different business models and approaches to cooperating with potential overseas suppliers, and typically require a physical presence or importer/ distributor or partner in market.

For example, for TMall, if the Australian company has not established a presence in China, they can only set up their stores on the TMall International Channel.

Another example is Yihaodian (www.yhd.com). For Australian companies with products that already have official distributors in China, Yihaodian can use a sale- on-consignment model with those distributors. In such cases the distributor/supplier will decide the retail price (noting it usually has to be more competitive than the offline retail price). Yihaodian will assume responsibility for storage and distribution of the products via its own Distribution Centre in different cities in China, and will charge a commission on their sales revenue to the distributor.

Australian suppliers need to contact each online retailer individually to discuss opportunities, requirements and pricing expectations.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

13

TABLE 5: TOP 3 ONLINE FOOD AND GROCERY RETAILERS IN CHINA

Internet retailer Details Website

Yihaodian � Biggest food and beverage internet retailer � Wal-Mart bought 51% stake in 2012 � Fresh food delivery service in Shanghai and Beijing (with

expansion plans of this concept)

www.yhd.com

Jd.com � Second largest B2C e-commerce company � Holding stock in their own warehouses

jd.com

Tmall � Owned by Alibaba Group (spun off from Taobao) � Brands can operate their own online stores and manage

distribution themselves � The grocery business line has been introduced recently � A lot of promotional activity for foreign brands and fresh food

from overseas (e.g. seafood from New Zealand or cherries from the US that could be pre-ordered)

tmall.com

Premium HoReCa Market — distribution channels

The Premium HoReCa industry is difficult to penetrate for foreign suppliers, particularly given the sector’s need for rapid product supply and consumption. There are nonetheless significant opportunities in China. Exporters are most likely to enjoy success when they deal through Chinese importer/distributors with strong specialisation and networks among product category managers of the Premium HoReCa chains. These product category managers act as ‘dealers’ by marketing products to individual HoReCa branches.

› Check out Annex IV for information on Premium HoReCa players and their contact details.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

14

FIGURE 3: ROUTES TO THE MARKET — HORECA

2.3.3 Trade shows

To successfully export to the Chinese market, it is crucial to establish good long-term relationships with distributors, importers and agents, who are often exhibiting at industry trade shows. The following are major Chinese trade shows for the food and beverage sector:

SIAL China

� Shanghai, yearly

� Targets retailers, caterers, HoReCa players, food service businesses, importers and exporters and food manufacturers

China International Import Food Exhibition (FCE)

� Beijing, yearly

� Covers high-end food and beverage manufacturing, with a focus on imported food and beverage

› For more information on these major trade shows, refer to Annex VI.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

15

China Food and Drinks Fair

� Chengdu, yearly

� Aimed at producers, distributors and purchasers of alcohol, food, soft beverages, flavorings, food additives, food packages and food machines

International Food Exhibition & Import Food Exhibition

� Guangzhou, yearly

� Covers imported foods, nutritional and health foods, wine & spirits, olive and other edible oils, food additives and ingredients as well as food packaging and processing

Food & Hotel China (FHC)

� Shanghai, yearly

� Targets exporters and importers of food and beverage, wholesalers to the hospitality industry; foodservice equipment manufacturers

China International Food Industry Trade Fair (FADS)

� Beijing, yearly

� Aims at large supermarkets and shopping mall operators, the food wholesale market, other retailers, community chain supermarkets and convenience store operators; food trade companies; food manufacturers; the HoReCa industry

� Targets the high-end food and beverage sector

China Agriculture Trade Fair (CATF)

� Wuhan, yearly

� Covers agricultural produce and its distribution network, aiming at producers, traders, importers, and wholesalers

China International Organic Food Industry Expo

� Beijing, yearly

� Covers organic and natural produce and related enterprises – producers, importers, exporters, distributors, wholesale and retail store operators, and the HoReCa industry

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

16

REGULATORY AND TRADING ENVIRONMENTS

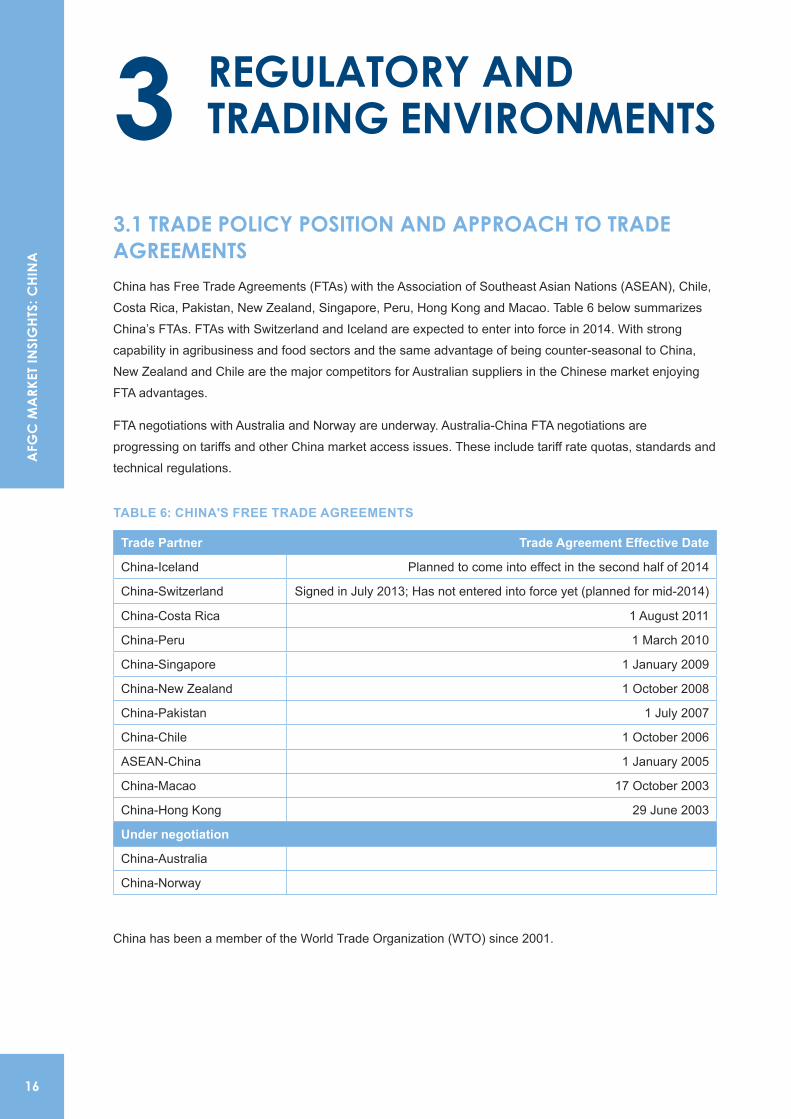

3.1 TRADE POLICY POSITION AND APPROACH TO TRADE AGREEMENTSChina has Free Trade Agreements (FTAs) with the Association of Southeast Asian Nations (ASEAN), Chile, Costa Rica, Pakistan, New Zealand, Singapore, Peru, Hong Kong and Macao. Table 6 below summarizes China’s FTAs. FTAs with Switzerland and Iceland are expected to enter into force in 2014. With strong capability in agribusiness and food sectors and the same advantage of being counter-seasonal to China, New Zealand and Chile are the major competitors for Australian suppliers in the Chinese market enjoying FTA advantages.

FTA negotiations with Australia and Norway are underway. Australia-China FTA negotiations are progressing on tariffs and other China market access issues. These include tariff rate quotas, standards and technical regulations.

TABLE 6: CHINA'S FREE TRADE AGREEMENTS

Trade Partner Trade Agreement Effective Date

China-Iceland Planned to come into effect in the second half of 2014

China-Switzerland Signed in July 2013; Has not entered into force yet (planned for mid-2014)

China-Costa Rica 1 August 2011

China-Peru 1 March 2010

China-Singapore 1 January 2009

China-New Zealand 1 October 2008

China-Pakistan 1 July 2007

China-Chile 1 October 2006

ASEAN-China 1 January 2005

China-Macao 17 October 2003

China-Hong Kong 29 June 2003

Under negotiation

China-Australia

China-Norway

China has been a member of the World Trade Organization (WTO) since 2001.

3

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

17

3.2 TRADE BARRIERS

3.2.1 Tariff Barriers

Since its entry into the WTO in 2001, China has applied tariff rates close to the rates at which it has promised (referred to as “bound” rates). Since accession to the WTO, China has reduced its overall average tariff for agricultural products from 21.2 per cent to 15.3 per cent. However, China still has pockets of high tariff protection — as high as 65 per cent on some key products of interest to Australia.

Tariff classification and reference pricing

A major issue in classifying products is that Chinese customs officers do not follow uniform guidelines and therefore, anticipating border charges has been difficult for exporters. Commonly, delays at customs and excessive fees unrelated to the services received are a major concern.15

3.2.2 Non-Tariff Barriers

China uses various non-tariff border barriers, such as import and export licensing, import quotas and so-called “notice-and-comment” procedures. As import quotas generally do not apply to processed foods in China, the major NTBs experienced by exporters are Notice-and-Comment Procedures.

Notice-and-comment procedures

15 US trade compliance report (2013)

› For individual tariffs applied to the food and beverage categories discussed in this report, please refer to the relevant sections of the report.

› For more details on tariff barriers, please refer to Annex VIII.

PRACTICAL TIPS

� Make sure that you you’re your ingredients lists ready before exporting to China. Customs will make their judgement on product classification based on this.

� Make sure you regularly check bacterial counts - mandatory quarantine checks are carried out during customs clearance, with bacterial counts being the major issue of rejection and subsequent destroying for Australian products.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

18

These are ad-hoc regulations issued by the China Inspection and Quarantine Bureau (CIQ) with little to no notice, e.g. a particular food category suddenly requires to undergo specific inspections or there is a change in requisite documents. Notice-and-comment procedures released by the CIQ are becoming more prevalent in the process of drafting trade laws, regulations, and departmental rules. This means that regulations can change any time and changes in regulations apply immediately. However, not all trade-related information is made available to the public, which can result in challenging situations at the border exporters cannot prepare for.

Although regulations are routinely published, laws are being passed at different levels — central, provincial, municipal – and can often contradict each other and leave a wide margin of discretion when it comes to apply them properly.

Australian products recently affected include meat and dairy. The best countermeasure to these changes is the establishment of strong relationships with Chinese authorities.

3.3 Overview of food regulation and import standards

Food trade into China is, predictably, heavily regulated. Recent legal changes to China’s Food Safety Law have increased focus on food safety through stricter monitoring and supervision – and severe punishment of offenders. In 2013, China streamlined all domestic food safety regulatory agencies into the China Food and Drug Administration (CFDA).

The Food Safety Law includes the following important features:

� All imported foodstuffs and beverages are subject to inspections by the China Inspection and Quarantine Bureau (CIQ). Each ingredient must be registered and permitted for entry. These procedures can be time consuming and costly. For most imported foods, China has strict documentation requirements related to quality, quarantine, origin and import control. Importers must keep detailed records for at least two years.

Food Safety concerns have led to wide-ranging regulatory changes regarding production and distribution of food. A new Food Safety Law is currently under consideration – requiring active attention. In China, laws (in particular those related to food) can change dramatically without notice.

3.3.1 Registration and Certification

The importing process into China requires licenses and certifications — the most important features are explained below.

› More details on food regulation and import standards can be found at Annex VIII.

› For a detailed overview of registration and certification requirements, please refer to Annex VIII.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

19

AQSIQ and CNCA registration

� Foreign producers need to register as “foreign exporter producer” through China's General Administration of Quality Inspection, Supervision and Quarantine (AQSIQ). For specific product groups such as meat, a—hygiene certificate is required by the manufacturer that has to be applied for at the Chinese Certification and Accreditation Administration (CNCA).

� All exporters and importers of food and beverage require a permit for quarantine inspection. Packaged animal products or plant products require veterinary or phytosanitary certification. Local AQSIQ offices will assess product samples to check for quality and labelling as well as hygiene standards.

Chinese Food and Drug Administration

� Food and beverage with added health claims are required to be registered with the State Food and Drug Administration (CFDA).

Documentation and certificate of origin

� The importation of goods into China must be well documented, e.g. name, specification, quantities, date of production, batch numbers, use by date, name and contact details of the exporter, name and contact details of the importer, and delivery time need to be recorded and kept on file for two years minimum.

� For several import products, China requires a certificate of origin to accompany the export consignment, issued by the relevant authority in the exporter’s country (e.g. the NSW Business Chamber, VECCI or AIGroup).

Organic Certification

� The certification body for organic produce is the China Green Food Development Centre (CGFDC). The application process can be time-consuming and costly, with costs of up to AUD 47,000.

3.3.2 Labelling

The Chinese consider food labels the most useful source of information regarding health and nutrition issues. “No food additives”, “no preservatives”, “organic”, “sugar free” and similar wordings have become more popular on packaging.

No pre-packaged foods may be imported into China without appropriate Chinese labels. All imported pre-packaged food must be labelled in both English and Chinese (simplified Chinese as used in mainland China).

While on the face of it, over-stickering may spoil the display of imported products, it is preferred to changing packaging and labelling to Chinese style and language. Upper-middle class consumers look for the original packaging as would be used in the source country, as it assures them of the product’s authenticity.

› A full list of labelling requirements and a listing of relevant Chinese Government agencies can be found at Annexes V and VIII.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

20

SUMMARY — THE OPPORTUNITY IS IN THE DETAIL

The opportunities for Australian food & beverage exports to China are immense and growing fast. But there are no certain paths to achieving success – other than meticulous planning, a strategic approach to entering the market, and patience.

While each manufacturer must uncover their own unique value proposition in the Chinese market — including by comparing their own offering with the prices, packaging, and flavours identified in this report, there are several consistent themes across the products covered in Part II of this report:

� The Chinese processed food and beverage market is very much globalised — your product competition may come from Germany, Russia or a local Chinese manufacturer.

� Australian manufacturers, on the whole, are more likely to be competitive at the premium end of the market – given our limited scale of production and global reputation.

� At the premium end, package sizes are shrinking, and high quality defined-source ingredients (and verifiable health claims) are of growing importance to the Chinese consumer.

� Each exporter must map out their entry strategy – store format, target cities, direct or through distributors. If starting from scratch, premium food producers should target emerging premium supermarkets through experienced importer/distributors – some of which are identified in this report.

The challenges of market entry into China – labelling, import taxes and customs – should not cloud the opportunity. These can be deftly handled by experienced importer/distributors if they are convinced of the unique value to their target buyers.

We hope this report provides the practical insights to bolster confidence about exploring opportunities for your specific products. Part II and the Annexes, in particular, provide deep commercial insights at the specific sub-category level – information which is not available in the public domain.

PART 2

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

22

SNACKFOODS

For the purpose of this report, the category of “Snackfoods” covers chocolate, sugar confectionary and cereal-based bar sub-categories. The total Premium Retail Market size of these snackfood product categories in China was AUD 7.6 billion in 2013.16 Average price range and package size range for the selected sub-categories are set out in Table 7.

TABLE 7: CHARACTERISTICS OF SURVEYED SNACKFOOD SUB-CATEGORIES

Sub-Category HS Code Description of highest current trade growth products

Price Range in AUD

Package Size Range

Chocolates 1806 Filled/unfilled chocolate slabs, bars or specialty chocolates (i.e. boxes)

2.60–6.00 per 100g

75–375g most common: 100g

Sugar Confectionary

1704 Particularly non-cocoa confectionary, such as boiled Sweets, Liquorice, Lollipops, Mints, Pastilles, Gums, Jellies, Chews, Toffees, Caramels, Nougat, but not including chewing gum

Imported: 1.90–2.93 per 100g

Locally produced: 1.20–1.55 per 100g

Imported: 90–365g, most common: 200g

Locally produced: 45–70g

Cereal-based bars

1904 Roasted or unroasted cereal-based snack bars

4.48–4.66 per 6 bars

35g–40g per bar

4.1 CHOCOLATESThe total Premium Retail Market size for chocolate in China was AUD 1.6 billion in 2013 and is forecast to reach AUD 1.8 billion in 2015. The market is expected to grow at a CAGR of 10–12 per cent over the next 3 years.17

Average price range and package size range for chocolate in the Selected Premium Retail Market are set out in Table 8.

TABLE 8: OVERVIEW OF PACKAGING AND PRICE POINT RANGES — CHOCOLATE

Product Category Price Range in AUD Package Size Range

Chocolates 2.60-6.00 per 100g 75-375g, most common: 100g

16 Estimate: Euromonitor and decisionAsia analysis17 Estimate: Euromonitor and decisionAsia analysis

4

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

23

4.1.1 Key players and brands

Figure 4 sets out the indicative “Share of Shelf” for chocolate brands in the Chinese Selected Premium Retail Market, including premium imported as well as local brands.

FIGURE 4: MAJOR CHOCOLATE BRANDS IN THE CHINESE SELECTED PREMIUM RETAIL MARKET

The premium market is dominated by US brands (imported as well as produced locally), with Dove — a Mars product - being the most prominent locally-produced brand. Key imported brands are Hershey from the US, MeiJi (Melty Kiss) from Japan, and Lindt, Ferrero (Rocher and Kinder) and Kraft from Europe. European companies are very successful in this market segment, since they can offer lower prices and have a focus promoting products aggressively, in particular with in-store promotions.

4.1.2 Packaging

The average package size for chocolates in the Selected Premium Retail Market ranges between 75 grams and 375 grams, with 100 gram packages being the most common size. For gift boxes in particular, images of tourist sites or animals on the boxes (e.g. the Great Wall of China or Koalas) appear to work very well in the Chinese market.

› A full list of surveyed package sizes is available at Annex I.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

24

4.1.3 Price points

The average price for chocolate in the Selected Premium Retail Market ranges between RMB 15–35 (AUD 2.60 – AUD 6) per 100 grams. Retailers in the Selected Premium Retail Market enjoy retail margins in the range of 5 per cent–12 per cent.

4.1.4 Product trends

The major flavours used in chocolates and chocolate bars are milk chocolate, almond, hazelnut or mixed nuts. New premium chocolates are increasingly using local flavours such as green tea and red beans or ginger in the winter season. Low sugar versions are also popular. Chinese premium customers prefer chocolates that are less sweet – with a stronger focus on dark chocolates.

Chocolates boxes are a popular gift item. Australian suppliers should target New Year, spring and May holidays to increase sales volumes. During other seasons, chocolate bars dominate the market.

4.1.5 Marketing and promotion

Common promotions for chocolates in the Premium Retail Market consist of price promotions and bonus packs for customers. Trade promotion and in-store promotion are typically required and form part of the retailers’ trading terms. Our survey of the Selected Premium Retail Markets could not identify any promotions (active during the survey period).

› A full list of surveyed retail prices is available at Annex I.

AUSTRADE INSIGHTS

� Small packages are ideal for people who snack at work (75-100g packages) .

� Gift-packaging (in nice tin or boxes) are also preferred in China as chocolates are typically used as gifts, especially during festival times.

� New competition has arisen in the market, including Russian chocolate that has recently entered retail stores in the North East region of China.

� Australian products are typically niche products (superior quality and higher price). Greater competition in chocolate imports is putting downward pressure on imported product prices, and narrowing the price gap with local brands.

� The recommendation on some chocolate products to store below 18 degrees typically cannot be meet by Chinese stores. Some high-end stores in China struggle to meet this recommended storage condition, even with air conditioning for the hot summer months. There is some consumer reluctance to purchase chocolate if the package includes such a warning.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

25

4.1.6 Trade barriers

Import duty is assessed on chocolate (blocks, slabs or bars) at a rate of 10 per cent CIF. Import duty is assessed on chocolate (filled blocks, slabs or bars) at a rate of 8 per cent CIF. Importers of chocolate are also required to pay VAT of 17 per cent.

PICTURE 3: SHELF WITH CHOCOLATE GIFT BOXES AT OLE SUPERMARKET

4.1.7 Routes to market

The typical route to the Premium Retail Market for imported chocolates and global brands that are produced locally is through 3rd party distributors, while local brand chocolate is mainly distributed directly by the manufacturers. A “Routes to Market” overview for China is provided at Section 2.3.3.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

26

Our survey has identified:

� 6 retailers in the Chinese Selected Premium Retail Market with a significant selection of imported chocolates.

� 6 distributors supplying the Chinese Premium Retail Market with a significant selection of imported chocolates.

Our survey has found that the Premium HoReCa channel is not sufficiently developed for the chocolate sub-category.

4.2 SUGAR CONFECTIONERYThe total Premium Retail Market size for sugar confectionery in China was AUD 5.8 billion in 2013. The market is expected to grow at a CAGR of 7–8 per cent over the next 3 years.18

Average price range and package size range for sugar confectionery in the Selected Premium Retail Market are set out in Table 9.

TABLE 9: OVERVIEW OF PACKAGING AND PRICE POINT RANGES — SUGAR CONFECTIONERY

Product Category Price Range in AUD Package Size Range

Sugar Confectionery Imported: 1.90–2.93 per 100gLocally produced: 1.20–1.55 per 100g

Imported: 90–365g, most common: 200gLocally produced: 45–70g

18 Estimate: Euromonitor and decisionAsia analysis

› An overview and contact details for retailers and distributors are available at Annexes II and III.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

27

4.2.1 Key players and brands

Figure 5 sets out the indicative “Share of Shelf” for sugar confectionery brands in the Chinese Selected Premium Retail Market, including premium imported as well as local brands.

FIGURE 5: MAJOR SUGAR CONFECTIONERY BRANDS IN THE CHINESE SELECTED PREMIUM RETAIL MARKET

The Premium Retail Market is dominated by European brands such as Katjes, Haribo and Perfetti van Melle (e.g. Mentos, Chupa Chups) and local brands like Four Seas and Fujiya.

4.2.2 Packaging

The average package size for imported sugar confectionery in the Selected Premium Retail Market ranges between 90 grams and 365 grams, with 200 gram packages being the most popular size. For locally produced sugar confectionery, the average package size ranges between 45 grams and 70 grams.

› A full list of surveyed package sizes is available in Annex I.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

28

4.2.3 Price points

The average price for sugar confectionery in the Selected Premium Retail Market ranges between RMB 11–17 (AUD 1.90 – AUD 2.93) per 100 grams for imported brands. Locally produced sugar confectionery in the Selected Premium Retail Market has an average price between RMB 7–9 (AUD 1.20 – AUD 1.55) per 100 grams. Retailers in the Selected Premium Retail Market enjoy retail margins in the range of 5 per cent–12 per cent.

PICTURE 4: SHELF WITH SUGAR CONFECTIONERY AT CITY SHOP

› A full list of surveyed retail prices is available at Annex I.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

29

4.2.4 Product trends

The major flavours used in sugar confectionery are fruit mixes, watermelon, strawberry, mint and milky flavours. New product trends in the high-end sugar confectionery category are milk candies and chewy candies as well as low sugar content options. The Chinese prefer sugar confectionery that is less sweet than the typical sugar confectionery sold in Australia — this applies specifically for the Northern Chinese. Liquorice is not very popular in the Chinese confectionery market.

Manufacturers are currently seeing a major opportunity in transforming candies and other sugar confectionery into snackfood to be consumed more regularly, e.g. at work. To implement this strategy, it is expected that they will tend to offering less sweet options in this market segment.

4.2.5 Marketing and promotion

Common promotions for sugar confectionery in the Premium Retail Market consist of individual “end aisle gondola displays”, separate from similar products. Trade promotion and in-store promotion are typically required and form part of the retailers’ trading terms. Our survey of the Selected Premium Retail Markets has identified 4 promotions (active during the survey period).

4.2.6 Trade barriers

Import duty is assessed on sugar confectionery (not containing cocoa) at a rate of 10 per cent CIF. Importers of sugar confectionery are also required to pay VAT of 17 per cent.

4.2.7 Routes to market

The typical route to the Premium Retail Market for imported sugar confectionery and global brands that are produced locally is through 3rd party distributors, while local brand sugar confectionery is mainly distributed directly by the manufacturers. A “Routes to Market” overview for China is provided at Section 2.3.3.

Our survey has identified:

� 6 retailers in the Chinese Selected Premium Retail Market with a significant selection of imported sugar confectionery.

� 6 distributors supplying the Chinese Premium Retail Market with a significant selection of imported sugar confectionery.

› The details of promotions identified during the survey period are available at Annex I.

Austrade Insights

Make sure you focus on premium ingredients for sugar confectionery as this is essential to be successful in the Chinese Premium Retail Market. Chinese consumers tend to prefer very “smooth” types of confectionery such as milk candy.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

30

Our survey has found that the Premium HoReCa channel is not sufficiently developed for the sugar confectionery sub-category.

4.3 CEREAL-BASED BARSThe total Premium Retail Market size for cereal-based bars in China was AUD 21 million in 2013. The market is expected to grow at a CAGR of 6–7 per cent over the next 3 years.19

Average price range and package size range for cereal-based bars in the Selected Premium Retail Market are set out in Table 10.

TABLE 10: OVERVIEW OF PACKAGING AND PRICE POINT RANGES — CEREAL-BASED BARS

Product Category Price Range in AUD Package Size Range

Cereal-based Bars 1.83–2.83 per 100g 25–50g per bar (4 or 6 bars per package)

4.3.1 Key players and brands

Figure 6 sets out the indicative “Share of Shelf” for cereal-based bars brands in the Chinese Selected Premium Retail Market, including premium imported as well as local brands.

FIGURE 6: MAJOR CEREAL-BASED BARS BRANDS IN THE CHINESE SELECTED PREMIUM RETAIL MARKET

19 Estimate: Euromonitor and decisionAsia analysis

› An overview and contact details for retailers and distributors are available at Annexes II and III.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

31

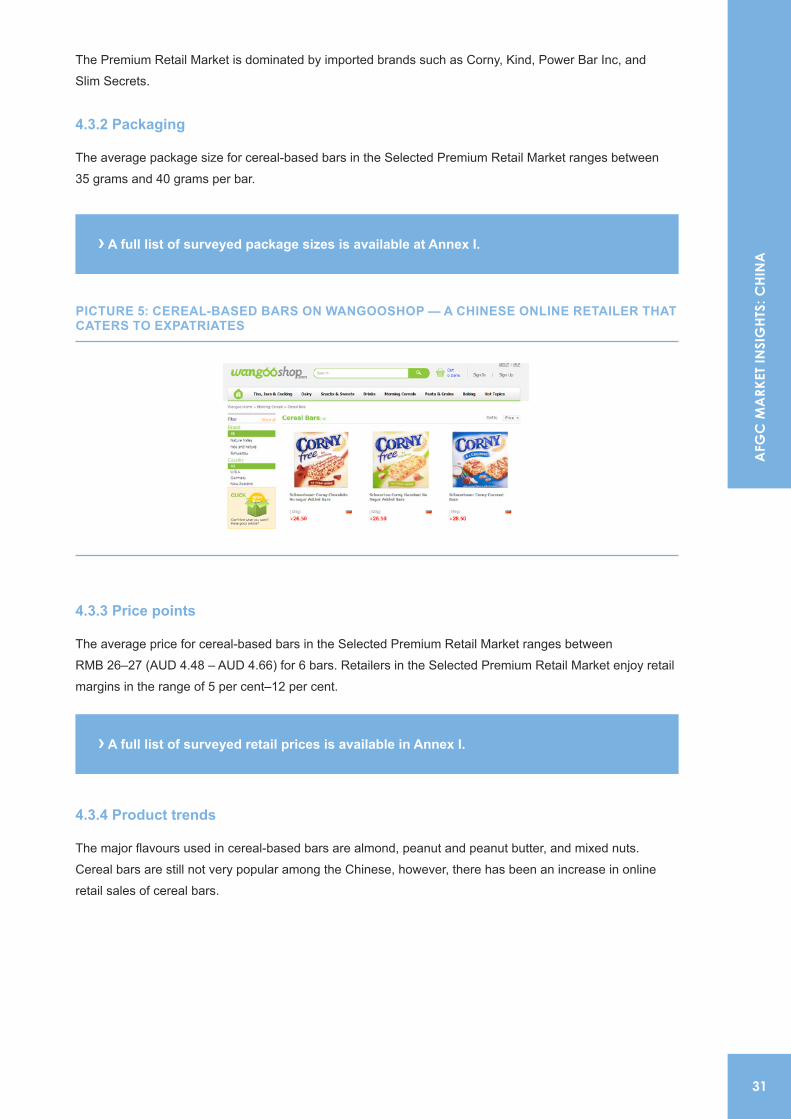

The Premium Retail Market is dominated by imported brands such as Corny, Kind, Power Bar Inc, and Slim Secrets.

4.3.2 Packaging

The average package size for cereal-based bars in the Selected Premium Retail Market ranges between 35 grams and 40 grams per bar.

PICTURE 5: CEREAL-BASED BARS ON WANGOOSHOP — A CHINESE ONLINE RETAILER THAT CATERS TO EXPATRIATES

4.3.3 Price points

The average price for cereal-based bars in the Selected Premium Retail Market ranges between RMB 26–27 (AUD 4.48 – AUD 4.66) for 6 bars. Retailers in the Selected Premium Retail Market enjoy retail margins in the range of 5 per cent–12 per cent.

4.3.4 Product trends

The major flavours used in cereal-based bars are almond, peanut and peanut butter, and mixed nuts. Cereal bars are still not very popular among the Chinese, however, there has been an increase in online retail sales of cereal bars.

› A full list of surveyed package sizes is available at Annex I.

› A full list of surveyed retail prices is available in Annex I.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

32

Only two supermarkets – City Shop and Ole – in the Selected Premium Retail Market currently carry cereal-based bars, which are exclusively imported products. Major demand is highest in expatriate residential areas and Chinese who have returned from overseas are also more likely to be interested in buying cereal bars.

4.3.5 Marketing and promotion

Cereal-based bars are not heavily promoted in the Chinese Premium Retail Market. Our survey of the Selected Premium Retail Markets could not identify any promotions (active during the survey period).

4.3.6 Trade barriers

Import duty is assessed on cereal-based bars at a rate of 25 per cent CIF for foods obtained by the swelling or roasting of cereals or cereal products. Import duty is assessed on cereal-based bars at a rate of 30 per cent CIF for foods obtained from unroasted or mixed of unroasted and roast cereals. Importers of cereal-based bars are also required to pay VAT of 17 per cent.

4.3.7 Routes to market

The typical route to the Premium Retail Market for imported cereal-based bars and through 3rd party distributors. A “Routes to Market” overview for China is provided at Section 2.3.3.

Our survey has identified

� 2 retailers in the Chinese Selected Premium Retail Market carrying cereal-based bars with a significant selection of imported cereal-based bars.

� 6 distributors supplying the Chinese Premium Retail Market with a significant selection of imported cereal-based bars.

Our survey has found that the Premium HoReCa channel is not sufficiently developed for the cereal-based bars sub-category.

Austrade Insights

� Current cereal bars on the market are often considered “too sweet” by Chinese consumers.

� Manufacturers have tried to highlight the “instant energy” benefit of cereal-based bars, but this has not been a successful strategy in the Chinese market.

� Make sure you highlight that your product is less sweet, or contains no fat and less sugar than similar products.

› An overview and contact details for retailers and distributors are available at Annexes II and III.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

33

BEVERAGES

For the purpose of this report, the category of “Beverages” covers fruit juice, tea and premium cold beverage sub-categories. The total Premium Retail Market size of these beverage product categories in China was AUD 19.5 billion in 2013.20 Average price range and package size range for the selected sub-categories are set out in Table 11.

TABLE 11: CHARACTERISTICS OF SURVEYED BEVERAGE CATEGORIES

Sub-Category HS Code Description of highest current trade growth products

Price Range in AUD Package Size Range

Fruit Juice 2009 Specific product types that represent local trends. For example, this done by examining shelf space allocation at major premium retailers.

Imported: 3.28–4.83 per litre Locally produced: 2.76–3.45 per litre

1-2 litres, most common: 1 litre

Tea 0902 Tea for consumption as warm beverage

Imported: 7.76–8.62 per 100gLocally produced: 1.20–1.72 per 100g

Imported: 50–100gLocally produced: 100–180g

Premium Cold Beverages

2202 Energy Drinks, Ready-to-drink tea (e.g. iced tea), premium non-cola carbonated drinks

6.90–10.35 per litre Energy-type drinks: 100–200mlOther: 250–450ml

5.1 FRUIT JUICEThe total Premium Retail Market size for fruit juice in China was AUD 1.84 billion in 2013 and is forecast to reach AUD 2.1 billion in 2015. The market is expected to grow at a CAGR of 8–10 per cent over the next 3 years.21 Average price range and package size range for fruit juice in the Selected Premium Retail Market are set out in Table 12.

TABLE 12: OVERVIEW OF PACKAGING AND PRICE POINT RANGES — FRUIT JUICE

Product Category Price Range in AUD Package Size Range

Fruit Juice Imported: 3.28–4.83 per litre Locally produced: 2.76–3.45 per litre

1–2 litres most common: 1 litre

20 Estimate: Euromonitor and decisionAsia analysis21 Estimate: Euromonitor and decisionAsia analysis

5

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

34

5.1.1 Key players and brands

Figure 7 sets out the indicative “Share of Shelf” for fruit juice brands in the Chinese Selected Premium Retail Market, including premium imported as well as local brands.

FIGURE 7: MAJOR FRUIT JUICE BRANDS IN THE CHINESE SELECTED PREMIUM RETAIL MARKET

The Premium Retail and HoReCa Markets are dominated by local brands like Hui Yuan and Dahu. However, several import brands have established a strong presence in this segment, with Dole, Coca Cola, Tropicana, Santal and Ringo being the major players.

Australian juice such as Berri, Just Juice and Golden Circle Juice has entered the market in major cities such as Beijing, Shanghai and Guangzhou.

5.1.2 Packaging

The average package size for fruit juice in the Selected Premium Retail Market ranges between 1 litre and 2 litres. Fresh juice is commonly available in 1 litre packages, whereas juice concentrate is mostly available in 1.25 litre packages.

Juice packaging in China requires more colourful designs and brighter colours to be successful. Manufacturers are currently moving from cartons to plastic bottles. Small packages (e.g. 250 ml packs) are getting more popular for people who take juice to work or school.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

35

PICTURE 6: MINUTE MAID DISPLAYED AT END OF GONDOLA — LIANHUA SUPERMARKET

5.1.3 Price points

The average price for imported fruit juice in the Selected Premium Retail Market ranges between RMB 19–28 (AUD 3.28 – AUD 4.83) per litre. Locally produced fruit juice in the Selected Premium Retail Market has an average price between RMB 16–20 (AUD 2.76 – AUD 3.45) per litre. Retailers in the Selected Premium Retail Market enjoy retail margins in the range of 5 per cent–12 per cent. HoReCa players in the Selected Premium HoReCa Market have a 5 per cent–10 per cent margin.

› A full list of surveyed package sizes is available at Annex I.

› A full list of surveyed retail prices is available in Annex I.

AFG

C M

ARK

ET IN

SIG

HTS:

CHI

NA

36

5.1.4 Product trends

The major flavours used in fruit juice are apple, orange, tropical mixes and peach, with tropical juice mixes being the major growth category. Orange juice still has a 40–50 per cent market share, which is expected to decrease in the next few years. New trends in the Premium Retail Market, however, are local flavours such as crystal sugar pear, honeysuckle pear and longan red jujube. The leading players that have picked up these new flavour trends successfully are Uni-President Enterprises (crystal sugar pear) and Suntory Holdings (honeysuckle pear and longan red jujube). Those beverages with traditional Chinese tastes are labelled as natural and with health benefits.

Fresh juices are still perceived as being too expensive, even for many customers in the Premium Retail Market.

5.1.5 Marketing and promotion

Common promotions for fruit juice in the Premium Retail Market consist of end gondola displays and product sampling in the form of free small juice packs (e.g. 33ml) attached to a carton or bottle to introduce new flavours. Trade promotion and in-store promotion are typically required and form part of the retailers’ trading terms. Our survey of the Selected Premium Retail Markets has identified 3 promotions (active during the survey period).

5.1.6 Trade barriers

Import duty is assessed on fruit juice at rates between 7.5 per cent–30 per cent CIF. Importers of fruit juice are also required to pay VAT of 17 per cent.

Austrade Insights

� Chinese retailers as well as distributors prefer a longer shelf-life for fruit juice (9 months and over).

� Imported Thai and Malaysian fruit juices are becoming increasingly popular as they offer lower priced options.

� For the HoReCa industry, Australian suppliers should target coffee shops. Most of them now sell bottled fruit juices and they typically prefer 500ml glass bottles.