Embed Size (px)

Citation preview

David L FarrellRegional Sales Director

Paycor Inc

Affordable Care Act Reporting

∗ Who is Paycor

∗ Review of the Affordable Care Act∗ Individual vs. employer mandate

∗ Required IRS filings for employers

∗ Best Practices

∗ Bonus DOL Changes discussion!

Agenda

∗ Founded in 1990 by Bob Coughlan∗ Owner led employee owned∗ 28,000 clients nationwide∗ We serve 1-5,000 employee companies

∗ Suite of services∗ Payroll, HRIS, Time, Onboarding, ATS, some W/C

∗ What we DON’T SELL∗ Health Insurance or 401k (or much W/C)

∗ We’re known for∗ Award winning technology and customer service∗ Helping our clients reduce cost, engage employees, improved

analytics, and improved compliance

3

Paycor

∗ Paycor is not engaged in providing legal advice, or tax advice. Consult a legal or accounting professional to ensure you understand your client’s risk with regards to ACA reporting

∗ This information is subject to change as the IRS changes it’s ACA regulations

4

Consult a Professional

Review of the Affordable Care Act

• ACA was designed to ensure that Americans have health insurance

• Individuals can obtain insurance two ways:1. Through the Marketplace (tax credits are available for those

who can’t afford it)

2. Through their employer if they work 30 hours or more weekly.

Review of the Affordable Care Act

• IRS needs accountability from employers that they are complying with the law

• They want to know…• Who has coverage

• What kind of coverage they have

• Where did they get it

• IRS wants to make sure employers who are supposed to be providing coverage are doing so—if not, they can be penalized.

∗ ACA added two new

reporting and filing

requirements related to

health insurance coverage∗ Section 6055 deals with the

individual mandate

∗ Section 6056 deals with the

employer mandate.

Required IRS filings

∗ Beginning in 2014, PPACA requires all non-exempt

individuals to either maintain minimum essential coverage

(“MEC”) or pay a penalty as part of their income tax returns

for every month they go without MEC

∗ Section 6055 reporting is necessary to determine whether

individuals are maintaining MEC

∗ Returns must be filed with the IRS and statements

furnished to covered individuals.

Section 6055 & the Individual Mandate

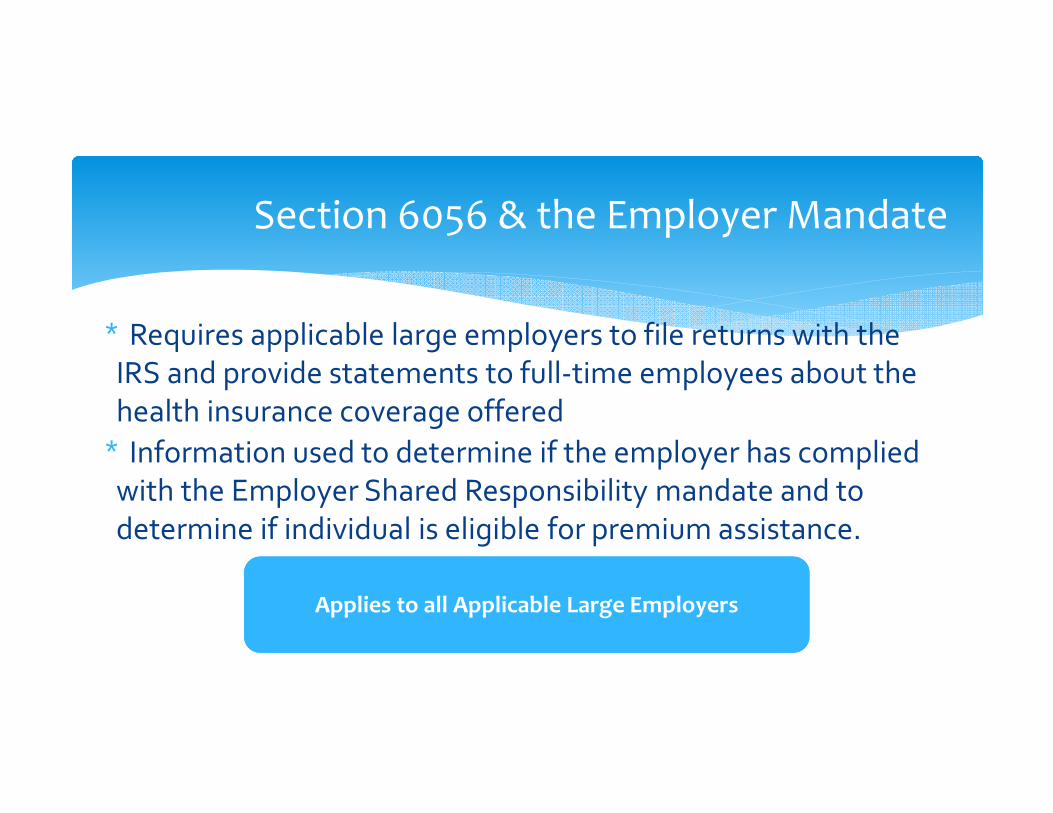

∗ Requires applicable large employers to file returns with the

IRS and provide statements to full-time employees about the

health insurance coverage offered

∗ Information used to determine if the employer has complied

with the Employer Shared Responsibility mandate and to

determine if individual is eligible for premium assistance.

Section 6056 & the Employer Mandate

Applies to all Applicable Large Employers

Reporting Who Reports Transmittal Form IRS Deadline Paycor Filing?

6055 Small Employer with Self-Insured Plan

1094-B 1095-B 1/31 of each year (2/1/16)

No

6055 Insurer 1094-B 1095-B 1/31 of each year (2/1/16)

No

6056 Large Employer with FullyInsured Plan

1094-C 1095-C 2/28 (or 3/31 if filed electronically*)

Yes

6055/6056 Large Employer with Self-Insured Plan

1094-C 1095-C 2/28 (or 3/31 if filed electronically*)

Yes

Required IRS filings overview

*Must file electronically if providing 250 or more *Must file electronically if providing 250 or more

∗ Penalties increased in late July to $250 per return

∗ Up to maximum of $3 million under Sections 6721 and

6722

∗ If the failure relates to both an information return and a

payee statement, penalties are doubled to $500 and $6

million

∗ Special relief for 2015: no penalties will be imposed as

long as the filing entity makes a good faith effort to

comply (clients 50-99 FTE)

∗ However, you don’t want to invite the IRS into your

business.

Penalties for not filing

WHAT INFORMATION IS REQUIRED FOR

THE 1095-C AND 1094-C?

Form 1095-C: Part I

Information about both the employee and employer

Static payroll/benefit admin data

Lines 7-13: Employer information

Comes from client.

Lines 1-6: Employee information including SSN

Line 10: Contact telephone number who the

recipient may call about the information reported

Static payroll/benefit admin data

Form 1095-C: Part II

Client/benefit admin

Client/benefit admin

Client/benefit admin

Line 15: Report the amount of the employee’s share of the

lowest cost monthly premium for self-only coverage

Line 14: Offer of Coverage, for each month enter a “Series 1”

code from the instructions

Line 16: Safe Harbor Codes, for each month enter a “Series 2”

code from the instructions.

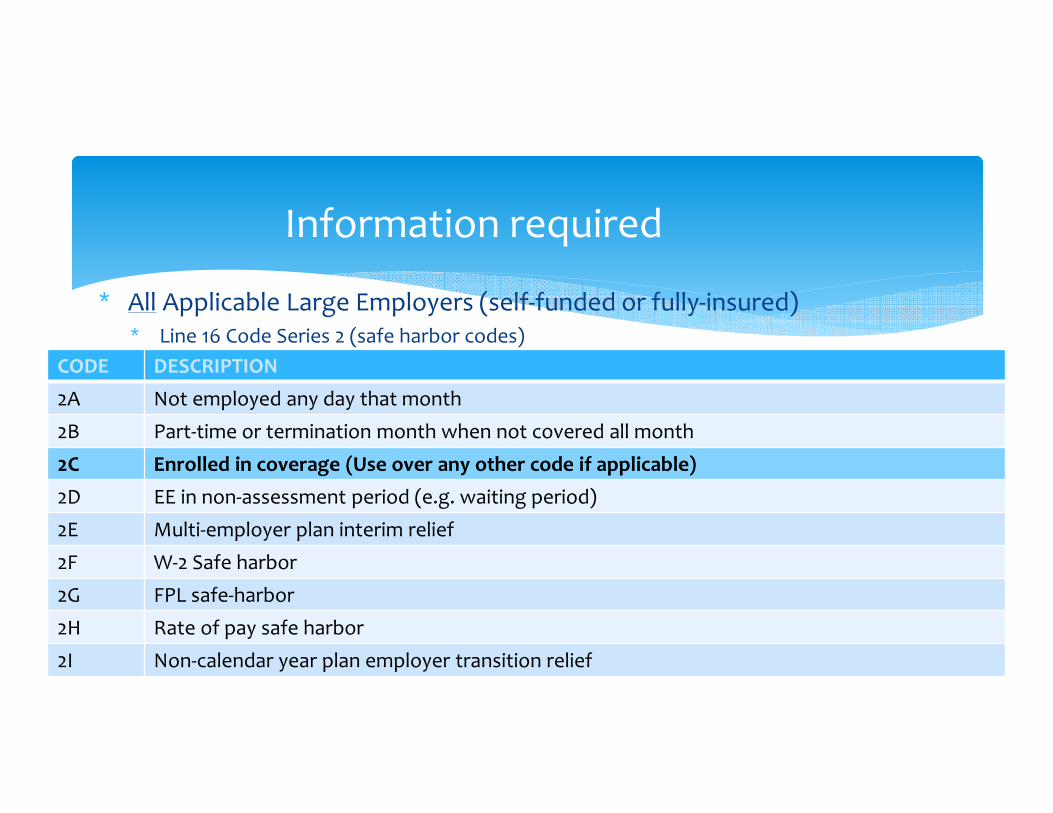

∗ All Applicable Large Employers (self-funded or fully-insured)

∗ Line 14 Code Series 1 (Offer of coverage codes)

Information required

CODE DESCRIPTION HOW COMMON

1A MV offered at less than 9.5% of FPL ($93.18/mo) Common

1B Offer to EE only Rare

1C Offer to EE + Dependent (not spouse) Rare

1D Offer to EE + Spouse (non dependent) Rare

1E MV offered to EE, at least MEC offered to spouse & deps Common

1F MEC that is not MV offered to employee Some

1G Self-funded offered to part-time EE Rare

1H No offer of coverage to full-time employee Common

1I No offer to employee but employer using qualifying offer relief ?

∗ All Applicable Large Employers (self-funded or fully-insured)∗ Line 16 Code Series 2 (safe harbor codes)

Information required

CODE DESCRIPTION

2A Not employed any day that month

2B Part-time or termination month when not covered all month

2C Enrolled in coverage (Use over any other code if applicable)

2D EE in non-assessment period (e.g. waiting period)

2E Multi-employer plan interim relief

2F W-2 Safe harbor

2G FPL safe-harbor

2H Rate of pay safe harbor

2I Non-calendar year plan employer transition relief

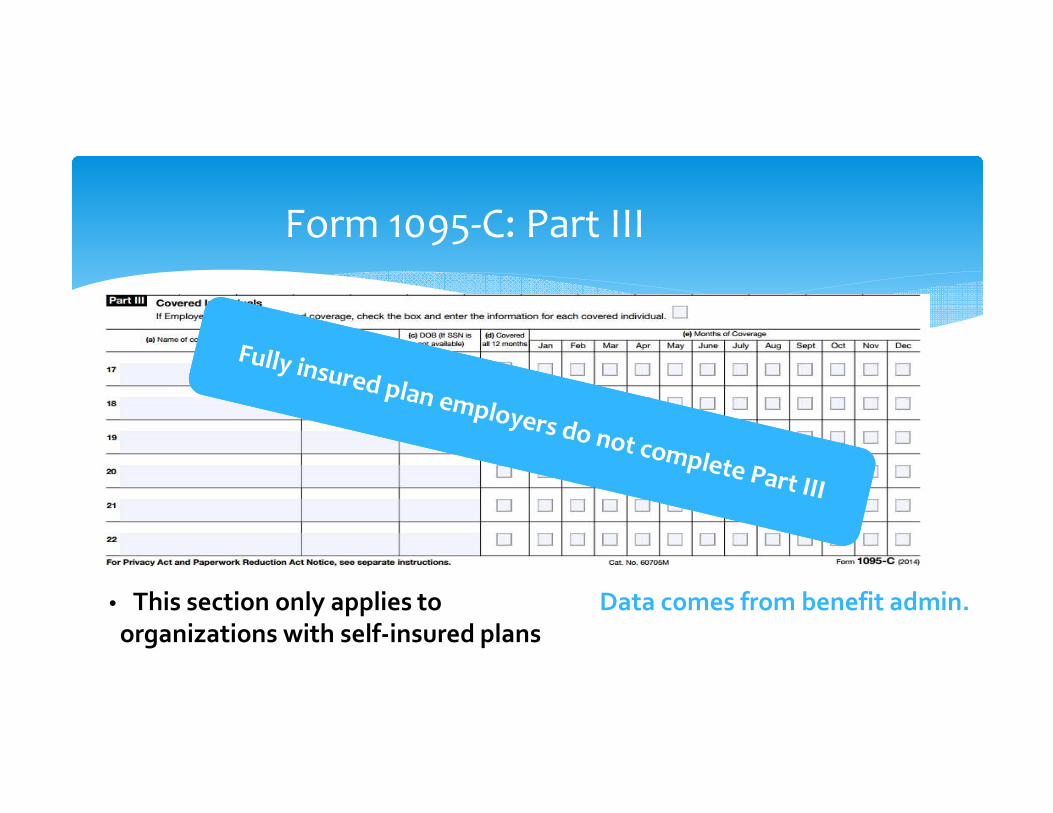

Form 1095-C: Part III

• This section only applies to

organizations with self-insured plans

Data comes from benefit admin.

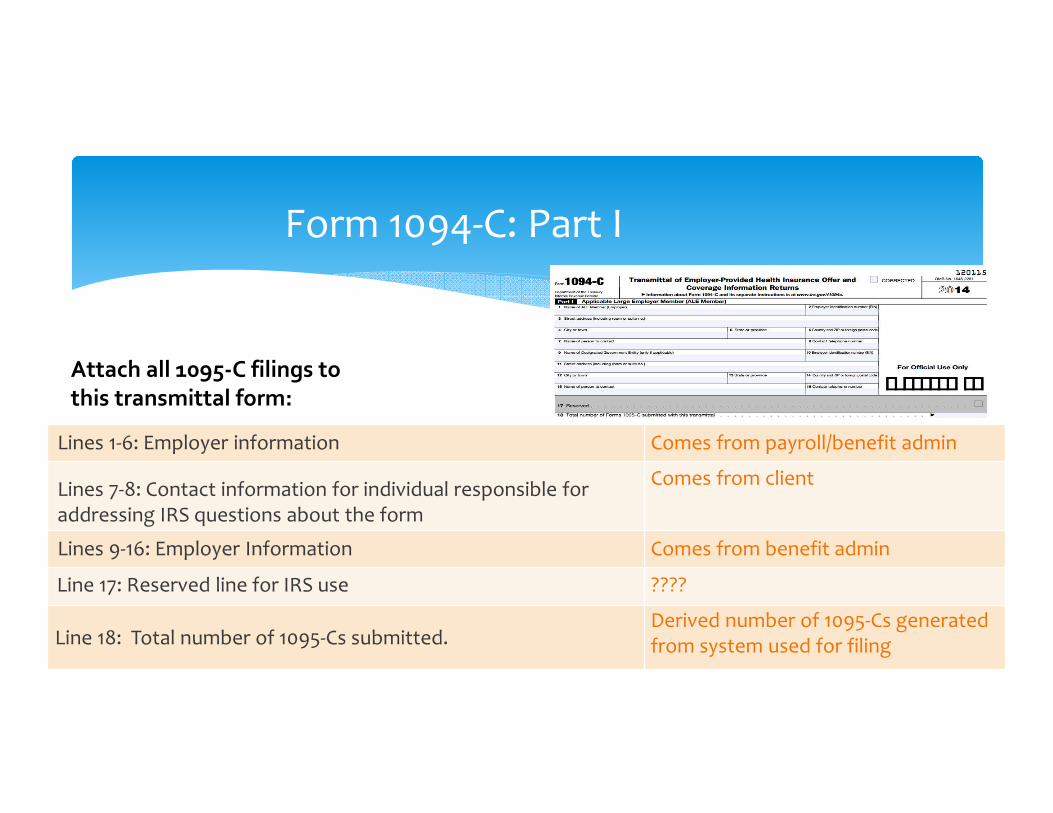

Form 1094-C: Part I

Attach all 1095-C filings to

this transmittal form:

Lines 1-6: Employer information

Lines 7-8: Contact information for individual responsible for addressing IRS questions about the form

Lines 9-16: Employer Information

Line 17: Reserved line for IRS use

Line 18: Total number of 1095-Cs submitted.

Comes from payroll/benefit admin

Comes from client

Comes from benefit admin

????

Derived number of 1095-Cs generated from system used for filing

Form 1094-C: Part II

Lines 19-21: For filings where there are related employers and where each is filing for their own group

Line 22: If an employer files under one of the four optional filing methods, the filer discloses which method they are using

Comes from client

Comes from client/benefit admin.

Qualifying Offer

∗ Employer offers MV coverage with employee cost less than 9.5% of FPL ($93.18 in 2015)

∗ Benefits to employer:∗ Enter code 1A in line 14 of 1095 and employer does not have to provide cost of

lowest cost plan on line 15∗ Can provide a simplified statement to employees instead of a copy of the 1095∗ Problem with the simplified statement approach

∗ Employer still has to provide a 1095 to the IRS…why not just give the employees a copy

∗ Self-funded employers cannot use the simplified statement for anyone who has elected coverage

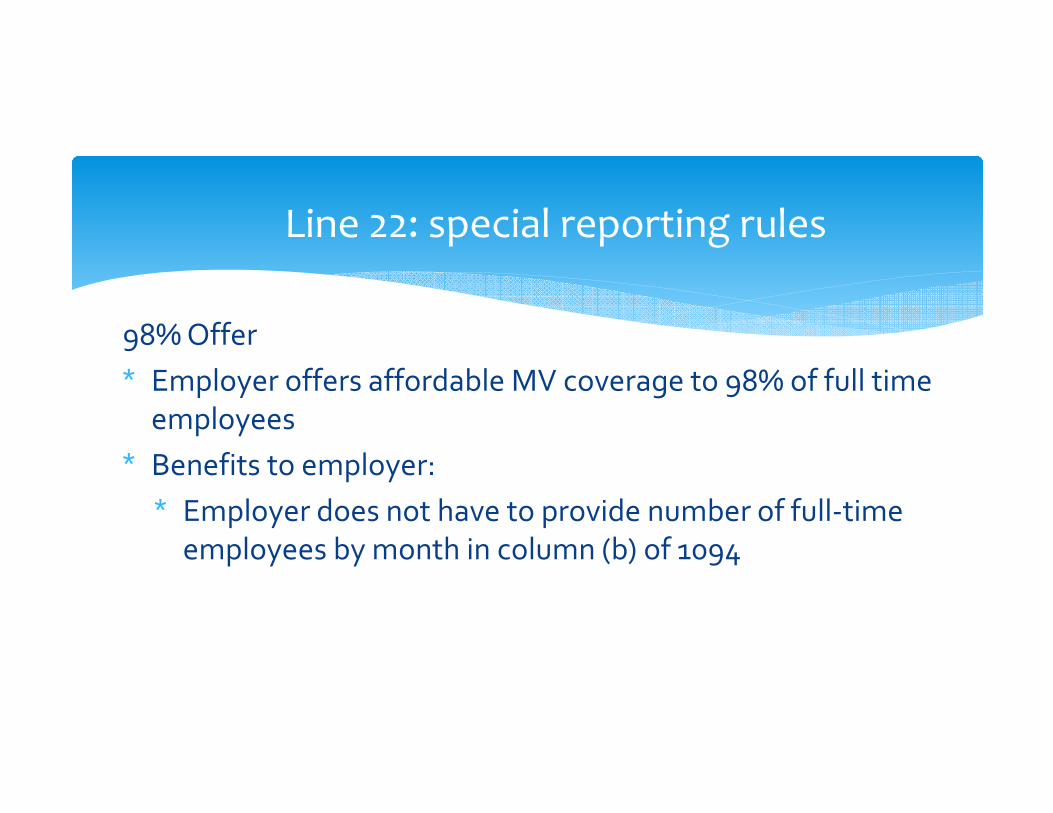

Line 22: special reporting rules

98% Offer

∗ Employer offers affordable MV coverage to 98% of full time

employees

∗ Benefits to employer:

∗ Employer does not have to provide number of full-time

employees by month in column (b) of 1094

Line 22: special reporting rules

Form 1094-C: Parts III and IV

Comes from insurer

Comes from payroll (ALE report)

Comes from payroll (ALE report)

Comes from benefit admin/client.

Comes from benefit admin/client

Comes from benefit admin/client

Column (a): Did employer offer coverage to 95% of full-time?

Column (b): Number of full-time employees

Column (c): Total number of employees

Column (d): Is employer part of a controlled group?

Column (e): Transition relief code•Code A for 50-99 FTE relief•Code B for all other 100+ transition relief

Lines 36-65: Names and EINS of other ALE Members of the

Aggregated ALE Group (if applicable)

What is Paycor doing to help?

• Products that can help • Benefits administration tool

• Time and attendance tracking

• Reporting & Analytics: ACA reporting to help you determine ALE status, employee eligibility and plan affordability

• Filing assistance for 1095-C and 1094-C• We will aggregate information from our systems

• Clients that are not using Paycor’s benefit administration or time and attendance system can import or enter information through a client portal for an additional fee

• We will file the 1094-C and 1095-C forms on the client’s behalf.

ACACompliance

Payroll Data

Open Enrollment/Ben Admin

Time & Attendance

Data

1095 - C

EE info including SSNEE Depending info

including dependent SSNER infoContact numberOffer of CoverageAmount of EE shareSafe Harbor Codes

1094 - C

ER Info - FEINContact NameTotal number of 1095-CsRelated EINsFiling Method SelectedNumber of FTEs

Static Payroll DataEE SSNNumber of FTEs

Offer of CoverageAmount of EE share for Self only CoverageSafe Harbor CodesER InfoTransition Code Relief

Client Data

Name and Contact Number of responsible Person

Control Group Y/NRelated Company EINsOptional Filing Method selection

Reporting

Am I a Large Employer?Which of my Ees are eligible?Are my Benefits Affordable?Measurement, Stability, and

Admin Periods tracking1094-C1095- Cs

PPACA HoursMeasurement, Administrative & Stability Periods

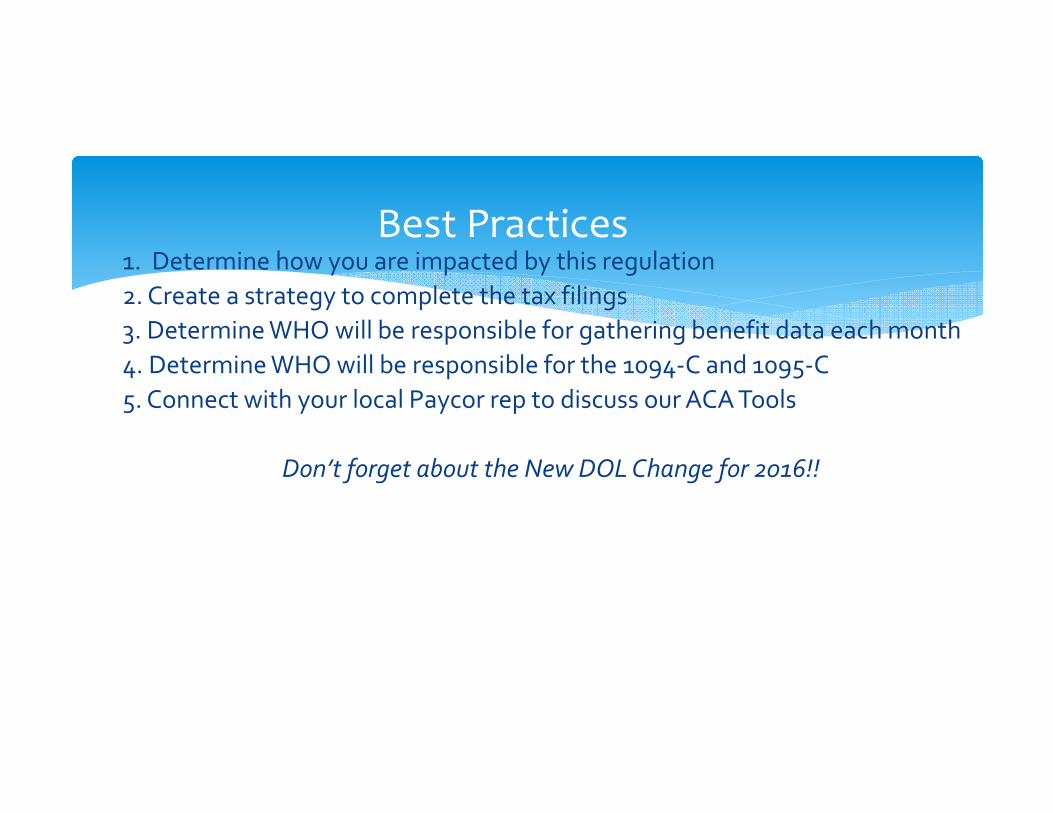

1. Determine how you are impacted by this regulation

2. Create a strategy to complete the tax filings

3. Determine WHO will be responsible for gathering benefit data each month

4. Determine WHO will be responsible for the 1094-C and 1095-C

5. Connect with your local Paycor rep to discuss our ACA Tools

Don’t forget about the New DOL Change for 2016!!

Best Practices

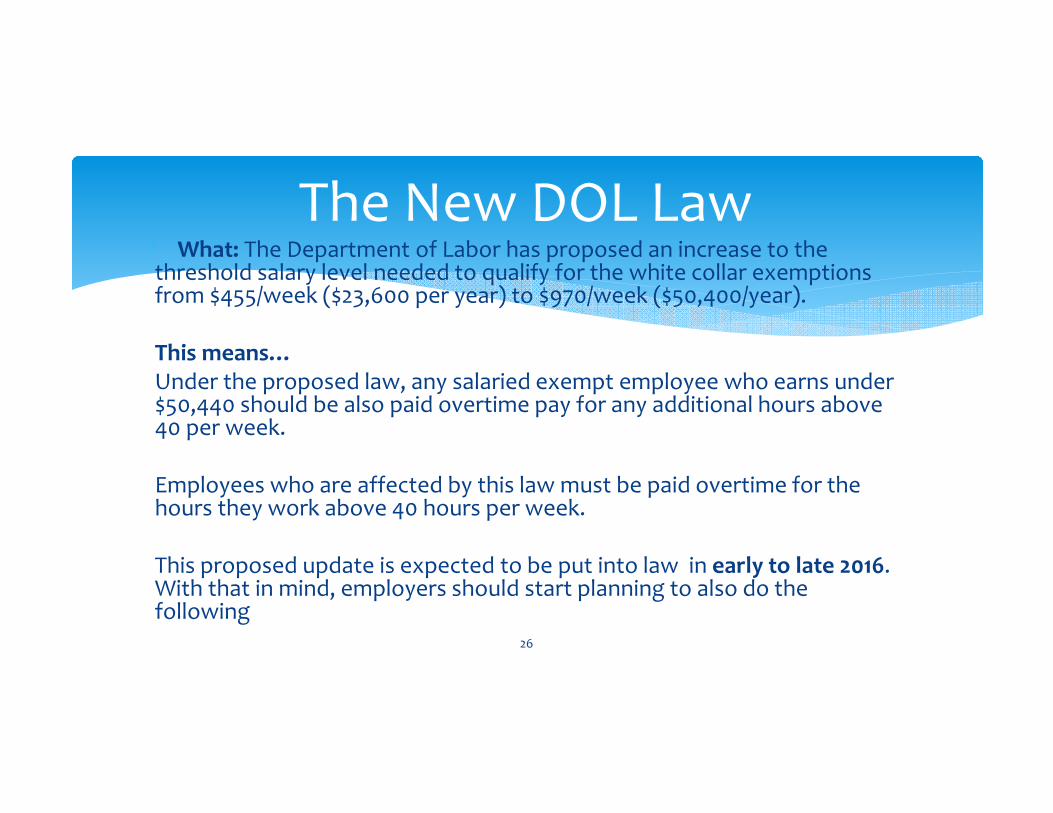

∗ What: The Department of Labor has proposed an increase to the threshold salary level needed to qualify for the white collar exemptions from $455/week ($23,600 per year) to $970/week ($50,400/year).

This means…Under the proposed law, any salaried exempt employee who earns under $50,440 should be also paid overtime pay for any additional hours above 40 per week.

Employees who are affected by this law must be paid overtime for the hours they work above 40 hours per week.

This proposed update is expected to be put into law in early to late 2016. With that in mind, employers should start planning to also do the following

26

The New DOL Law

We expect employers to pick between four options.

Do nothing and watch an employee’s annual pay grow.

Adjust employees to an hourly rate. Then adjust the hourly rate based on hours the employee typically works.

Bump up affected employee’s salaries to $50,440.

Mandate no overtime. Manage it profusely.

27

Consider your options in 2016

∗ Paycor data shows that 65% of employers have one employee or more who are affected by the threshold increase.

To Do Today

∗ Determine if you are affected

∗ Understand which employees are affected

∗ Determine the hours they work…and start tracking your salaried employees hours now!

28

You Need a Plan