Embed Size (px)

Citation preview

Aegis Group

Aegis Group plc is the global media communications and market research group employing approximately 8,000 staff in over 60 countries. Headquartered in London and listed on the London Stock Exchange (AGS.L) the Group is structured around

two core business areas: Aegis Media, which includes Carat, Vizeum, MMA, Isobar and Posterscope and a range of communications businesses; and Synovate, which

is a leading global market research company

Global access to local insights

Offices Countries Staff Revenue

108 60 8,000+ $574m

Synovate in Hungary

A hub for Hungary, Czech Republic and Slovakia

Office established in 1991

Around 40 full-time staff, 15 researchers

58,140 interviews, 395 focus groups and in-depth interviews in 2005

Regional coordinating centre for Central Europe

Business Climate Barometer

Joint Survey of The BCCH & Synovate

Form

online and self administered survey

single interview lasted approx. 15-20 min.

Respondents

senior management of foreign companies investing in Hungary industries like agriculture, tobacco, construction, business services, education, food & beverages, automotive, trade, real estate, communications, finance and hotels

Timing

Interviews were conducted between September 25 – October 16, 2006

Methodology

Investors are rather negative towards the prevailing business environment in Hungary in the near future.

56

-39

16

-100

-80

-60

-40

-20

0

20

40

60

80

100

2003. Oct 2004. May 2006. Oct

* Average score on the scale -100 ..+100, where -100 means definitely less favourable, 0 means the same as today, and +100 means definitely more favourable

Q1

2006. Oct

Definitely less favourable

Definitely more favourable

Expectations towards business environment

The negative sentiment is widespread, but particularly strong amongst large enterprises.

33 16 16

10

56 57 5363

-48-31-38-39

-100

-80

-60

-40

-20

0

20

40

60

80

100

2003. Oct 2004. May 2006. Oct

Q1

Definitely less favourable

Definitely more favourable

Total Small Business Mid-size Business Large Business

* Average score on the scale -100 ..+100, where -100 means definitely less favourable, 0 means the same as today, and +100 means definitely more favourable

Expectations towards business environment

Expectations towards business environment

The construction/real estate and manufacturing/trade sectors were the most pessimistic sectors in the economy.

26 20

7259

0 3 16

27

56

28

9280

-29-33-42-50-58-39

-100

-80

-60

-40

-20

0

20

40

60

80

100

2003. Oct 2004. May 2006. Oct

Q1

Definitely less favourable

Definitely more favourable

Total Manufacturing, Trade

Construction, Real Estate

OtherFinancial services

Professional Services

* Average score on the scale -100 ..+100, where -100 means definitely less favourable, 0 means the same as today, and +100 means definitely more favourable

24

1

-30

-100

-80

-60

-40

-20

0

20

40

60

80

100

2003. Oct 2004. May 2006. Oct

Government’s performance in supporting investors

Q2

* Average score on the scale -100 ..+100, where -100 means making things much worse, 0 means neither better nor worse and 100 means making things much better

The Government is not seen as taking positive steps to improve the business environment. In fact, opinion is that it is making

things worse!

Making things much worse

Making things much better

2006. Oct

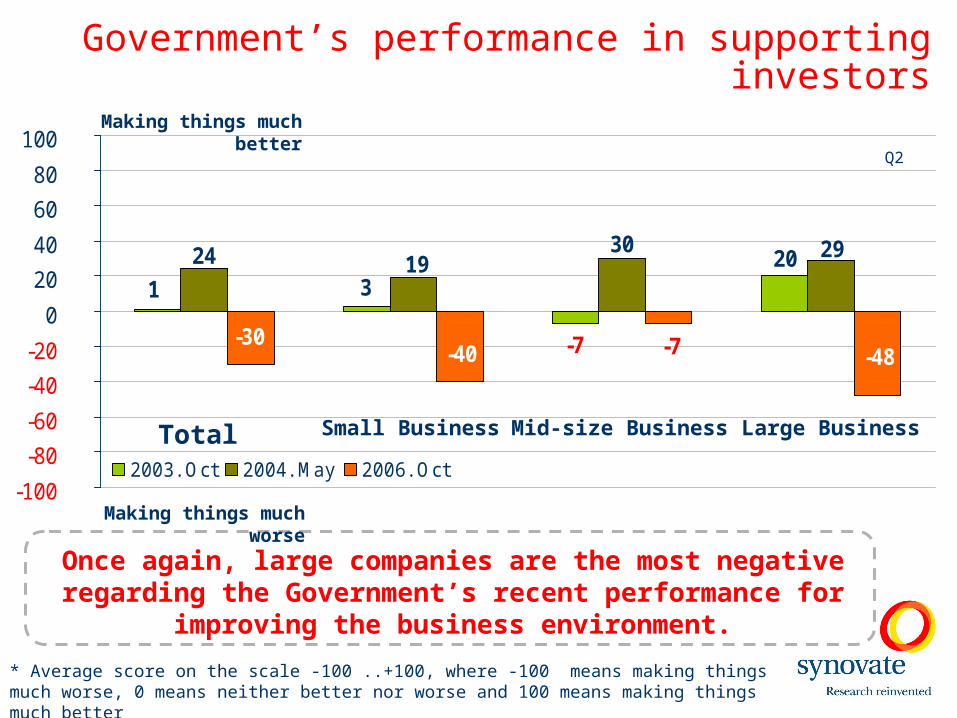

Government’s performance in supporting investors

Once again, large companies are the most negative regarding the Government’s recent performance for improving the

business environment.

20 3 1

-7

24 1930 29

-48-7-40-30

-100

-80

-60

-40

-20

0

20

40

60

80

100

2003. Oct 2004. May 2006. Oct

Q2

Making things much better

Total Small Business Mid-size Business Large Business

Making things much worse

* Average score on the scale -100 ..+100, where -100 means making things much worse, 0 means neither better nor worse and 100 means making things much better

Government’s performance in supporting investors

Although the manufacturing/trade firms had shown pessimism about the business environment, its clear that they don’t blame the

Government for it. However, the construction/real estate sectors strongly believe that the Government is making things worse.

-5

47

162

-8

0 1

27 24 30 25

7

-29-33-25-50

8

-30

-100

-80

-60

-40

-20

0

20

40

60

80

100

2003. Oct 2004. May 2006. Oct

Q2

Total Manufacturing, Trade

Construction, Real Estate

OtherFinancial services

Professional Services

Making things much better

Making things much worse

* Average score on the scale -100 ..+100, where -100 means making things much worse, 0 means neither better nor worse and 100 means making things much better

Impact of Gyurcsány restrictive package

Investors formed the same opinion about Hungary’s competitiveness in terms of the Gyurcsány restrictive package as for the government's performance, with large companies being the

most negative.

-22 -33 -25

0

-100

-80

-60

-40

-20

0

20

40

60

80

100

Total Small Business Mid-size Business Large Business

* Average score on the scale -100 ..+100, where -100 means much less competitive, 0 means neither better nor worse and 100 means much more competitive

Q3

Much less competitive

Much more competitive

Average Small Business Mid-size Business Large Business

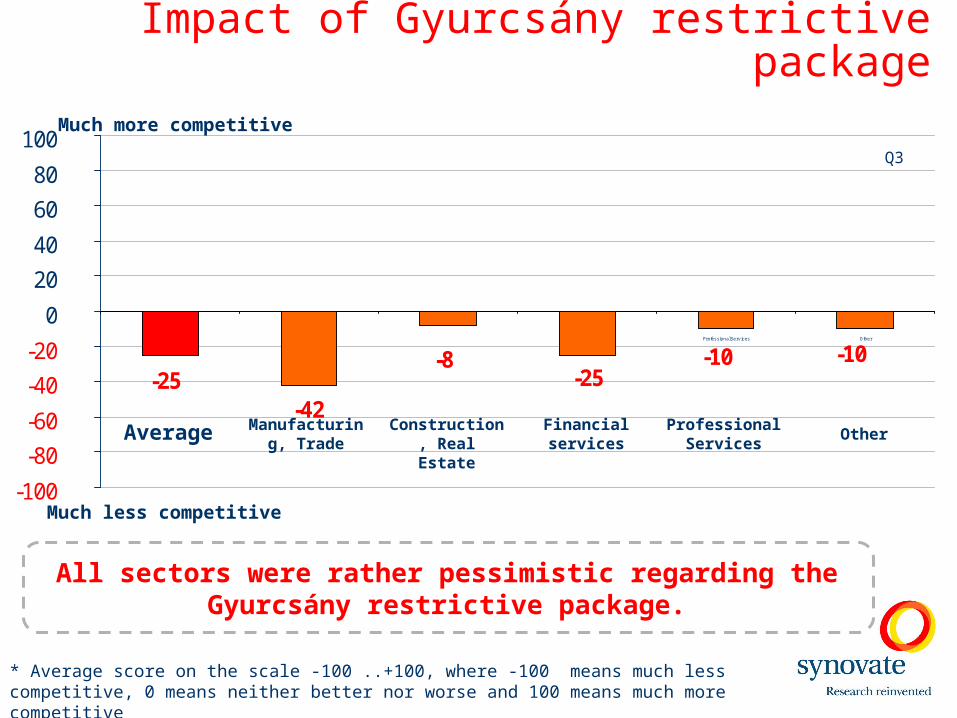

Impact of Gyurcsány restrictive package

All sectors were rather pessimistic regarding the Gyurcsány restrictive package.

-10 -10 -25

-42 -25

-8

-100

-80

-60

-40

-20

0

20

40

60

80

100

TOTAL Manufacturing, Trade Construction, Real Estate Financial serv ices Profess ional Serv ices Other

Q3

Average Manufacturing, Trade

Construction, Real Estate

OtherFinancial services

Professional Services

Much less competitive

Much more competitive

* Average score on the scale -100 ..+100, where -100 means much less competitive, 0 means neither better nor worse and 100 means much more competitive

Yes21%

No66%

DK/NA13%

Q4

Impact of Gyurcsány restrictive package

Yes37%

No48%

DK/NA15%

Plan any reduction in staff work force

Plan to revise staff benefit package

It is clear that the Gyurcsány restrictive package will definitely have an impact on both staff levels as well as on staff benefit

packages. In fact, 1 in 5 companies will reduce their number of staff, whilst almost 2 in 5 will revise staff benefits. There is also a sizeable number of companies that have not yet made a decision.

Q5

Operating sector’s dynamism

Over the next 2-3 years, most companies do not see any change in the dynamism of the sector that they are operating in. However, in

line with other perceptions, large companies are the most pessimistic.

11

-14

9 14

-100

-80

-60

-40

-20

0

20

40

60

80

100

Total Small Business Mid-size Business Large Business

Q7

Average Small Business Mid-size Business Large Business

Much less dynamic

Much more dynamic

* Average score on the scale -100 ..+100, where -100 means much less dynamic, 0 means neither better nor worse and 100 means much more dynamic

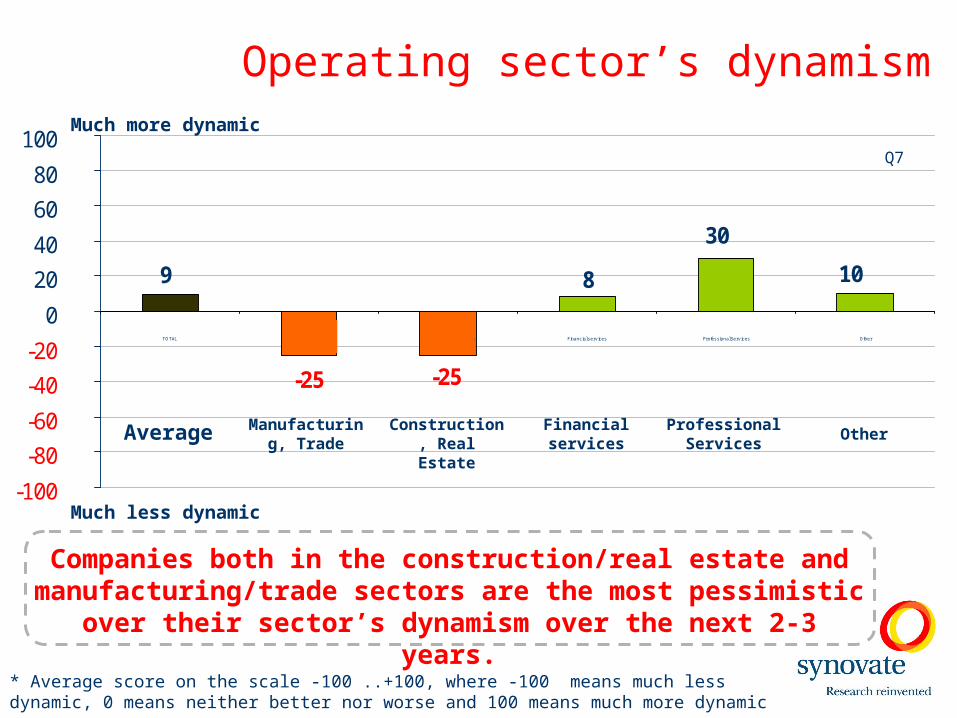

Operating sector’s dynamism

Companies both in the construction/real estate and manufacturing/trade sectors are the most pessimistic over their

sector’s dynamism over the next 2-3 years.

10

30

8

-25

9

-25

-100

-80

-60

-40

-20

0

20

40

60

80

100

TOTAL Manufacturing, Trade Construction, Real Estate Financial serv ices Profess ional Serv ices Other

Q7

Average Manufacturing, Trade

Construction, Real Estate

OtherFinancial services

Professional Services

Much less dynamic

Much more dynamic

* Average score on the scale -100 ..+100, where -100 means much less dynamic, 0 means neither better nor worse and 100 means much more dynamic

3,7

3,2

3,0

2,9

1,6

3,3

2,6

4,2

0 1 2 3 4 5

Bureaucracyand red tape

Corruption

High cost offinance

Slow internaldemand

Quality ofmanagement

Poorinfrastructure

Shortage ofskilled staff

Militant tradeunions

3,7

3,3

3,0

3,0

1,8

3,7

2,9

3,4

0 1 2 3 4 5

Shortage ofskilled staff

Bureaucracyand red tape

High cost offinance

Corruption

Quality ofmanagement

Poorinfrastructure

Slow internaldemand

Militant tradeunions

Barriers to business growthQ8

Average

May 2004 October 2006

Over the past 2 years, bureaucracy and corruption have become bigger threats to business activity in Hungary.

Interestingly, shortage of skilled staff is less of an issue! However, the size of the internal market has become a more decisive point.

In relative scores:

1 = totally insignificant

3 = significant

5 = extremely significant

Q12

%

18%

11%

9%

9%

21%

15%

17%

0% 5% 10% 15% 20% 25% 30%

Economicenvironment

Skilled labour

Low Cost/taxes

Profit

Growth

Infrastructure

Other

Average

Most frequently mentioned points when making a decision on new / further investments

Q12

%

21%

14%

7%

7%

24%

10%

17%

0% 5% 10% 15% 20% 25% 30%

Profit

Growth

Low Cost/taxes

Skilled labour

Economicenvironment

Infrastructure

Other

Average

Most important points when making a decision on new / further investments

Anticipation of any unexpected change

3%

36%

18%

33%

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Definitely yes (2)Rather yes (1)No idea (0)Rather not (-1)Definitely not (-2)

Q19

43% of those interviewed believe that there will be some unexpected changes in the next 6 months regarding the

economy or its legal regulations.

Neither significant nor insignificant

Extremely significant

Totally insignificant

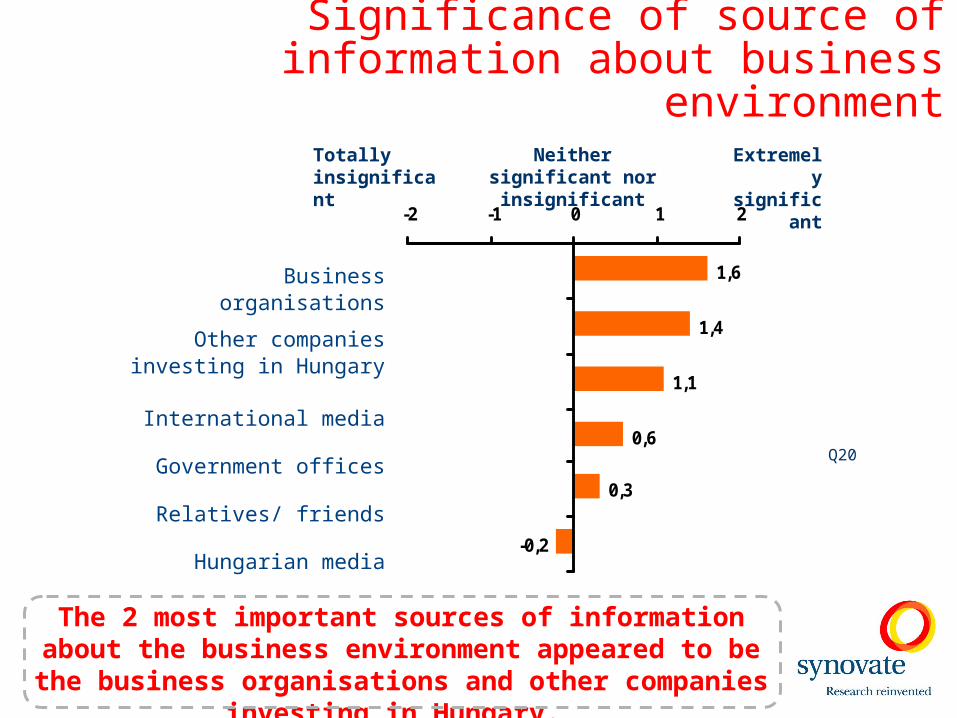

Significance of source of information about business environment

1,1

0,3

-0,2

0,6

1,4

1,6

-2 -1 0 1 2

Business organisations

International media

Relatives/ friends

Business organisations

Other companies investing in Hungary

International media

Government offices

Relatives/ friends

Hungarian media

The 2 most important sources of information about the business environment appeared to be the business

organisations and other companies investing in Hungary.

Q20

0,6

0,3

0,3

0,3

0,3

0,3

0,1

-0,2

-0,4

-0,7

0,4

0,8

0,9

-2 -1 0 1 2

Financing options

EU Overall

Employment policies

Return on Investment

Corruption

Competition

Taxation

Much worse Much better

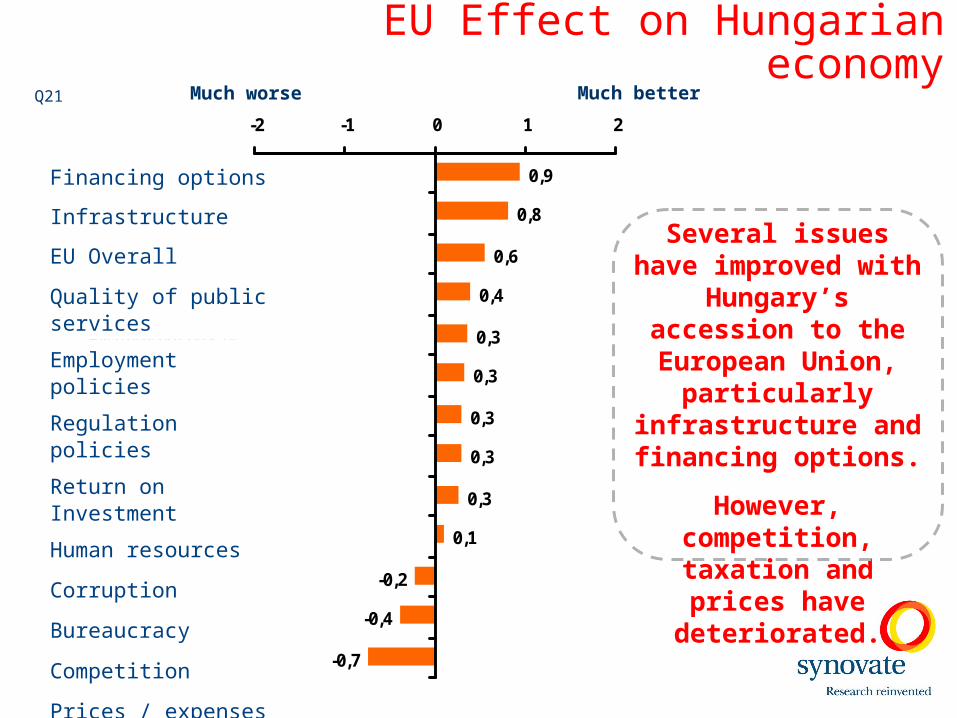

EU Effect on Hungarian economy

Financing options

Infrastructure

EU Overall

Quality of public services

Employment policies

Regulation policies

Return on Investment

Human resources

Corruption

Bureaucracy

Competition

Prices / expenses

Taxation

Several issues have improved with

Hungary’s accession to the European Union,

particularly infrastructure and financing options.

However, competition, taxation and prices have deteriorated.

Q21

Analysis of Critical Business Drivers

Preferred Countries for Investment in Central/ Eastern European

Q16

10%

7%

4%

4%

31%

27%

6%

9%

0% 5% 10% 15% 20% 25% 30% 35%

Czech Republic

Romania

Hungary

Slovakia

Poland

Baltic Countries

None of these

DK/NA

LEGAL ENVIRONMENT

Efficient administrationSimple procedures/ no bureaucracy

Just/impartial judicial systemNo corruption

ECONOMIC ENVIRONMENTHigh internal demand

Transparent information on the business environment

High quality of managementWell developed infrastructureWell developed financial sector

Low costs of finance

Business Drivers

ATTITUDE TO FOREIGNERS

Foreigners are treated equallyBenefits for foreign investors

Business Drivers in Order of Importance

Mostimportant

Leastimportant

54

51

8

1

100

88

87

84

77

32

93

87

0 20 40 60 80 100

Well developed financial sector

Benefits for foreign investors

High internal demand

Foreigners are treated equally

Transparent information on the business environment

Well developed infrastructure

High quality of management

Just/impartial judicial system

Efficient administration

Low costs of finance

Simple procedures/ no bureaucracy

No corruption

Hig

hM

ediu

mL

ow

STANDARDISED PERFORMANCE

Weak Average Strong

DIS

CR

IMIN

AT

OR

S

Low costs of finance

High internal demand

High quality of management

Well developed infrastructure

Well developed financial sector

Transparent information on the

business environment

Just/impartial judicial system

No corruption

Simple procedures/ no bureaucracy

Efficient administration

Benefits for foreign investors Foreigners are

treated equally

Strategic Matrix – Hungary

Key findings (1)• Expectations towards the business environment appear to be fairly

pessimistic and there is quite a decrease versus sentiments expressed when the survey was first launched 2 years ago.

• Opinion on the government's policies toward improving the business environment has also become more pessimistic compared to the previous waves.

• Opinion on the Gyurcsány restrictive package is also negative.

• The most important barrier to business growth is „ Bureaucracy and red tape” followed by „Corruption”. The third biggest factor is “High cost of finance”.

• Taxation rules, unpredictable political steps and lack of purchasing power are mentioned as other important factors hindering business growth.

Key findings (2)• Political predictability, fair taxation rules and lower bureaucracy are

mentioned as top priorities in improving the attractiveness of Hungary for investment.

• Participants agree that EU membership had positive effects on the Hungarian economy especially in terms of financing options, infrastructure and quality of public services.

• EU membership had less positive effect as expected in terms of EU regulations, higher prices/expenses and new competition.

• Hungary is perceived strong in terms of having a well developed financial sector but week in terms of offering benefits for foreign investors and having high internal demand. There is room for improvement in terms of transparency of the business environment and equal treatment of foreigners which are also important drivers for future investment.

Questions