Embed Size (px)

Citation preview

9/12/2017

1

ACUA Annual ConferenceSeptember 27, 2017

Presenter

Amy Block Joy - Faculty Emeritus University of California - Davis

Collusion at the University: A Case Study on Detecting Suspicious Activity Before Funds are Lost

and Reputations are TarnishedPresenter

Amy Block Joy - Faculty Emeritus University of California - Davis

9/12/2017

2

DISCLAIMERS

• Information summarized in this presentations includes published research, documents, articles, interviews, and recollections.

• The presenter would like to acknowledge the many professionals who worked on this case, including: university internal auditors, investigators, campus police, and federal agents.

• Viewpoints expressed in the presentation do not necessarily represent any official position of the University of California.

Presentation

1. Collusion Case Study2. Collusion Research 3. Collusion Indicators4. Reducing the Risk

9/12/2017

3

Collusion Case Study: Part 1

Discovery of Fraud

This Photo by Unknown Author is licensed under CC BY

Background

University of California

Faculty member

Director of USDA program

33 year employee

$150 million secured in grants

9/12/2017

4

Collusion Case Study

How was fraud detected?

This Photo by Unknown Author is licensed under CC BY‐SA

Collusion Case Study

How: Discovered questionable purchase order ($1400)When: March 2006 What happened: I met with accused and supervisorResult? Nothing

9/12/2017

5

Collusion Case Study

Blowing the Whistle*on wrongdoing

*Source: AB Joy, Whistleblower, 2010, ISBN: 9780981957746

This Photo by Unknown Author is licensed under CC BY

Collusion Case Study

2006-2007: Multiple investigations* Internal auditing Campus investigators Campus police OIG

*Source: AB Joy, Whistleblower, 2010, ISBN: 9780981957746

This Photo by Unknown Author is licensed under CC BY‐NC‐SA

9/12/2017

6

Collusion Case Study

Internal Auditing Investigation Identified

Collusion!

*Source: AB Joy, Blowback: The Unintended Consequences of Exposing a Fraud, 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐NC‐SA

Definition of Collusion

A secret agreement or cooperation between two or more individuals for a dishonest, deceitful, or illegal purpose.

This Photo by Unknown Author is licensed under CC BY‐NC‐SA

9/12/2017

7

Definition of Collusion

Is collusion a crime?

Collusion is a course of conduct that’s adverse to someone else’s interest or benefit

This Photo by Unknown Author is licensed under CC BY‐NC

Collusion Case Study

Collusion allowed the criminal activity to continue for six years!

This Photo by Unknown Author is licensed under CC BY‐NC

9/12/2017

8

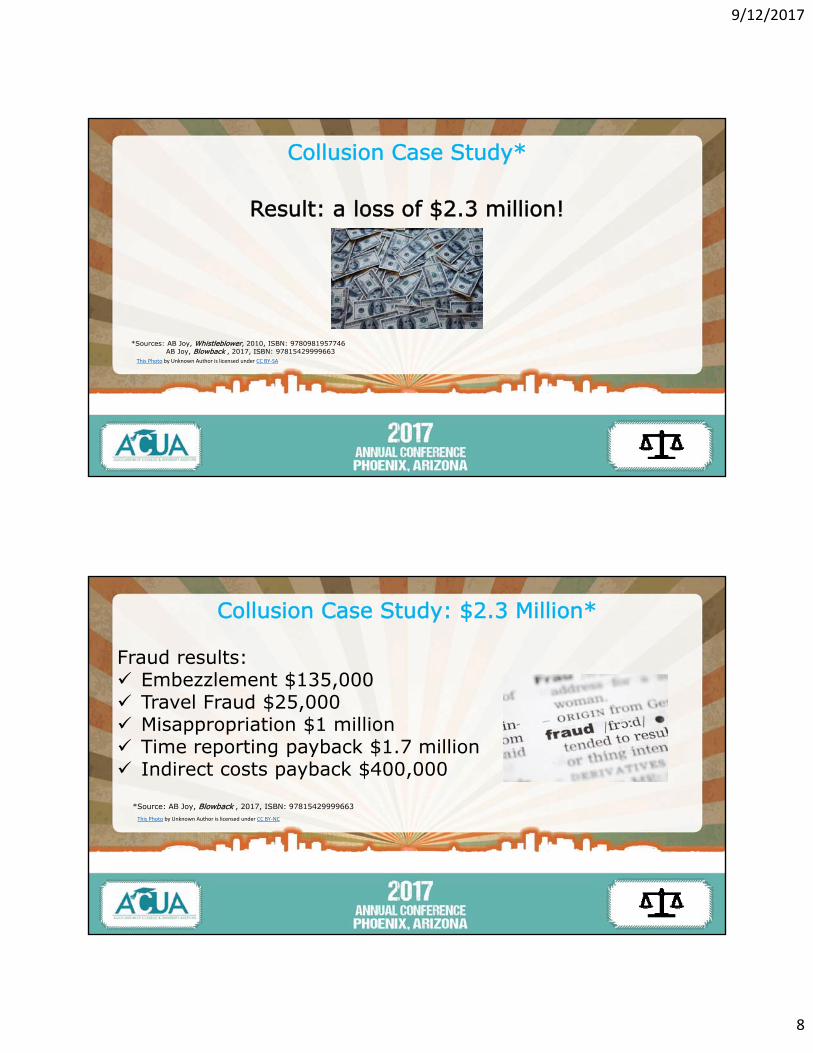

Collusion Case Study*

Result: a loss of $2.3 million!

*Sources: AB Joy, Whistleblower, 2010, ISBN: 9780981957746AB Joy, Blowback , 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐SA

Collusion Case Study: $2.3 Million*

Fraud results: Embezzlement $135,000 Travel Fraud $25,000 Misappropriation $1 million Time reporting payback $1.7 million Indirect costs payback $400,000

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐NC

9/12/2017

9

Collusion Case Study

Timing Questions*

When did the embezzlement begin?When did the travel fraud begin?When did the misappropriation begin?

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐SA

Collusion Case Study: Embezzlement*

When did the wrongdoing begin?

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐NC‐SA

9/12/2017

10

Collusion Case Study*

Fraud Spreadsheet Activity (embezzlement) Loss ($) Timing (dates)

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY‐SA

Collusion Case Study*

Why is the first incident significant?

Testing the financial environment High risk of getting caught

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

9/12/2017

11

Collusion Case Study*

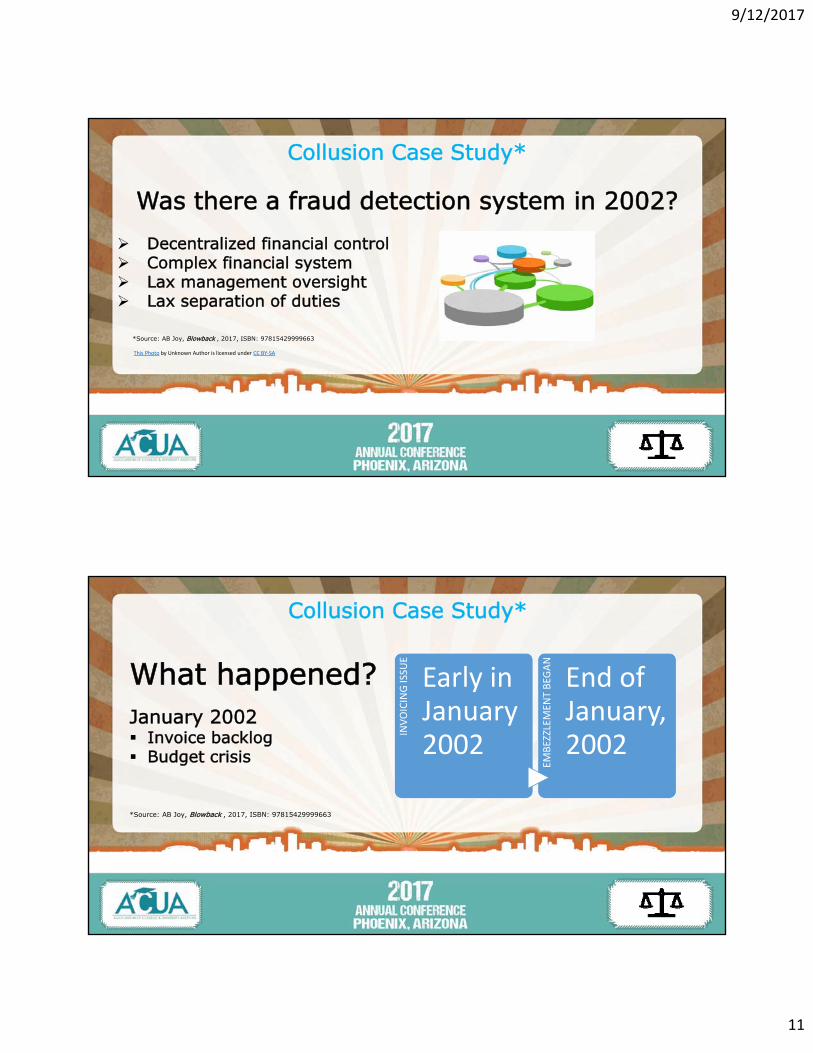

Was there a fraud detection system in 2002?

Decentralized financial control Complex financial system Lax management oversight Lax separation of duties

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐SA

Collusion Case Study*

What happened?January 2002 Invoice backlog Budget crisis

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

INVOICING ISSU

E

Early in January 2002

EMBEZZLEM

ENT BEG

AN

End of January, 2002

9/12/2017

12

Collusion Case Study: Embezzlement*An Embezzlement Scheme

(2002 – 2006)

Invoicing backlog is corrected by employee Employee begins embezzling while “fixing” Employee has chair approve purchases Employee then routinely has chair approve Employee then self-approves

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

Collusion Case Study*

Is a budget crisis a good time to commit fraud?

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY

9/12/2017

13

Collusion Case Study: Misappropriation*What was misappropriated?

Expensive purchases Office renovations Research staff time Effort reporting

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

*

This Photo by Unknown Author is licensed under CC BY

Collusion Case Study: Misappropriation*Employee facilitates purchases/payroll for department

(2004-2006)

Purchase of departmental servers ($101,300) Upgrade conference room with video equipment ($11,500) Research for chair ($80,500) Effort reporting ($378,000)

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐NC‐SA

9/12/2017

14

Collusion Case Study*

Is retaliation anindicator of collusion?

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663AB Joy, Retaliation, 2013, ISBN: 9781482651331This Photo by Unknown Author is licensed under CC BY‐SA

Collusion Case Study: Travel Fraud*Travel Fraud Results: $26,000

(2003 – 2006)

Employee can’t get rid of “stolen property” Employee needs cash Chair approves employee’s fictitious travel 254 fraudulent trips ($22,700) 22 out-of-state unallowable trips ($2,300)*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

9/12/2017

15

Collusion Case Study*Question:

When is the best time to commit fraud?

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY‐SA

Collusion Case Study*Answer:After passing an audit!

In 2003, the travel fraud began right afterextensive audit by the USDA. Findingsfrom the federal audit were mostly positive.

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY‐ND

9/12/2017

16

Collusion Case Study*

EXCEPT …

For an audit finding that required an explanation which was ultimately found acceptable by the government.

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

Collusion Research: Part 2

Can collusive activities be detected?

9/12/2017

17

Collusion Research

Employee Fraud Collusion* Collusion imposes a large economic loss Coordinating efforts so employees can work together More opportunities to circumvent anti-fraud controls Harder to detect so fraud continues for years

*Schaffer, Hagai. “Employee fraud collusion puts companies at high risk.” Corporate Compliance Insights, May 2015.

Collusion - Research

Study of Social Ties: Results from Co-Offender Interviews*

Most research on fraud is the individual fraudster Findings are usually: Increase controls to decrease fraud Increasing controls may not deter/stop collusion Research on collusion is sparse Enron, WorldCom, Tyco, HealthSouth fraud involved groups

* Free, C and PR Murphy. “The Ties that Bind: The Decision to Co-Offend in Fraud.” Contemporary Accounting Research 32(1):18-54, Spring 2015.

9/12/2017

18

Collusion - Research

Study of Social Ties: Results from Co-Offender Interviews*

Willingness of individuals to pool resources Pursuit of shared (and illegal) goals Risk is greater than an individual offender Co-Offenders are vulnerable to one another Loyalty, group culture, and distrust of others cement social bond

* Free, C and PR Murphy. “The Ties that Bind: The Decision to Co-Offend in Fraud.” Contemporary Accounting Research 32(1):18-54, Spring 2015.

Collusion - ResearchStudy of Social Ties: Results from Co-Offender Interviews*

Questions: Is it a decision? “… offenders choose to co-act; though intimidation may have been

used to recruit the offender, s/he participates voluntarily … “

Are people unwittingly involved? Once involved – can’t leave because of group influence, loyalty, fear of prosecution, etc.

How does it begin? “ … starts with a messy situation and pre-existing relationships … impulsive and serendipitous action … opportunity amplifies group bonds …”

* Free, C and PR Murphy. “The Ties that Bind: The Decision to Co-Offend in Fraud.” Contemporary Accounting Research 32(1):18-54, Spring 2015.

9/12/2017

19

Collusion - ResearchStudy of Social Ties: Results from Co-Offender Interviews*

Rationalizations:

Believe widespread corruption in the institutionBelieve government is cheating THEM!Have contempt for government, rules, regulations, and monitoringTake advantage of chaos in the organizationSocietal sanctions fraud because no one’s monitoring or stopping it

* Free, C and PR Murphy. “The Ties that Bind: The Decision to Co-Offend in Fraud.” Contemporary Accounting Research 32(1):18-54, Spring 2015.

Collusion - ResearchStudy of Social Ties: Results from Co-Offender Interviews*

Rationalizations:Denial that there’s a victim “I want to keep the institution/stockholders/etc. happy.”Believe others are incompetent – no one will notice “Everyone does it” “Too good to pass up” “If anyone squealed, we’ll all going down together”* Free, C and PR Murphy. “The Ties that Bind: The Decision to Co-Offend in Fraud.” Contemporary Accounting Research 32(1):18-54, Spring 2015.

9/12/2017

20

Collusion Indicators – Part 3

Identification of Collusive Activities

This Photo by Unknown Author is licensed under CC BY‐NC

Collusion Indicators Campus Internal Auditing Identified Collusive

Activities*

Former chair failed to establish an “internal control system” Former chair created a negative environment to exclude program director Former chair purchased servers without the program director’s approval Former chair consistently excluded program director from reviewing purchases

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

9/12/2017

21

Collusion IndicatorsCollusion Identification By Internal Auditing*

Former chair hired researchers for his research without securing approval Former chair added his employees to program payroll Fraudster initiated and approved payroll and purchases with former chair Former chair approved fraudster’s embezzlement and fictitious travel

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY‐NC‐SA

Collusion Indicators*Financial Control Risks

Lax oversight in department/unit Lax inventory control Missing documentation, poor record-keeping Documents altered (use of photocopies) Last minute adjustments (handwriting) No separation of duties Extra accounts, work-arounds, expense swapping Payroll transfers, end-of-year corrections/transactions, etc.*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY

9/12/2017

22

Collusion Indicators*Policy Risks

Out-dated policies Exceptions to policy allowed No audits or reviews conducted Ignorance of regulations, policies, rules Lack of regular performance evaluations Poor attitude toward government and auditors*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐SA

Collusion IndicatorsSuspicious behaviors*

Mistrust in the workplace No background checks Promotions rare Use of temp employees Lax oversight and supervision

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY

9/12/2017

23

Collusion IndicatorsSuspicious behaviors*

“This is how things are done here” “It’s not illegal” “No big deal” “Everyone does it” “No one’s monitoring”

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663

This Photo by Unknown Author is licensed under CC BY‐NC‐ND

Collusion IndicatorsSuspicious behaviors*

Gossip and rumors “Bond” between supervisor/employee Pressure (debts, gambling, etc.) Lavish lifestyle Angry outbursts Strained relationships

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY

9/12/2017

24

Collusion Indicators*Increase in Employee Complaints/Grievances

Employees: Receive special treatment, assignments Allowed to work at home Receive stipends, bonus, extra-pay, overtime Relatives are hired

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY‐ND

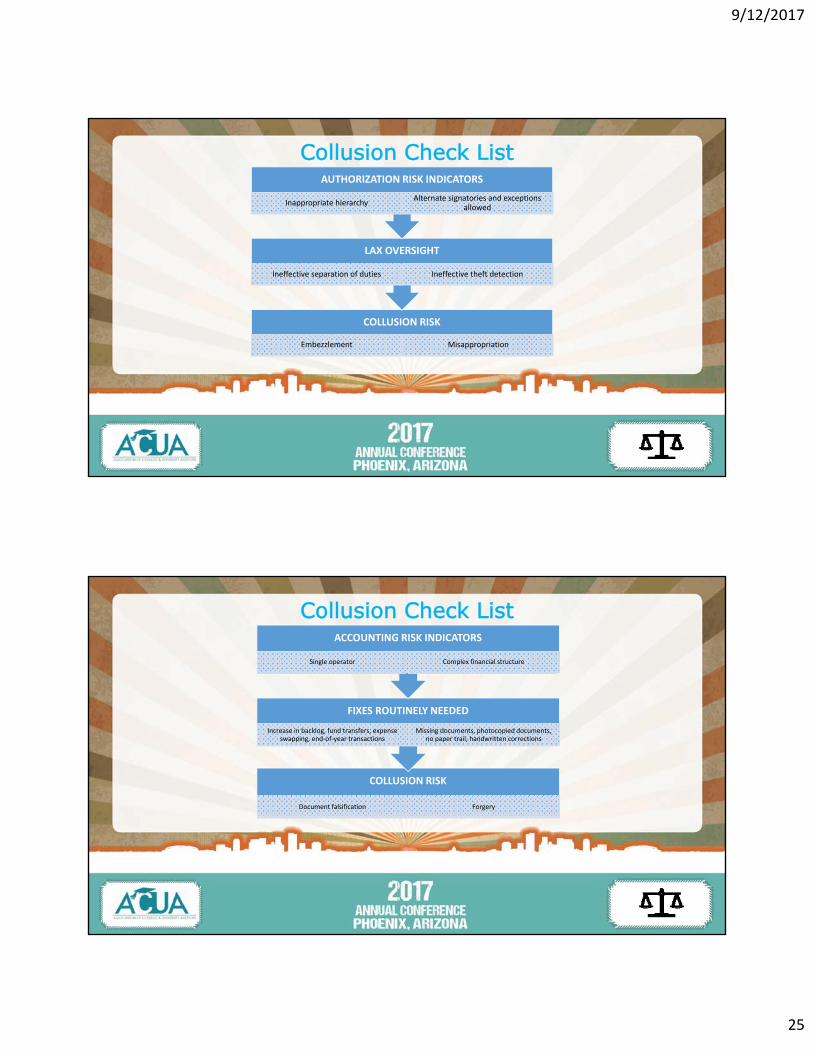

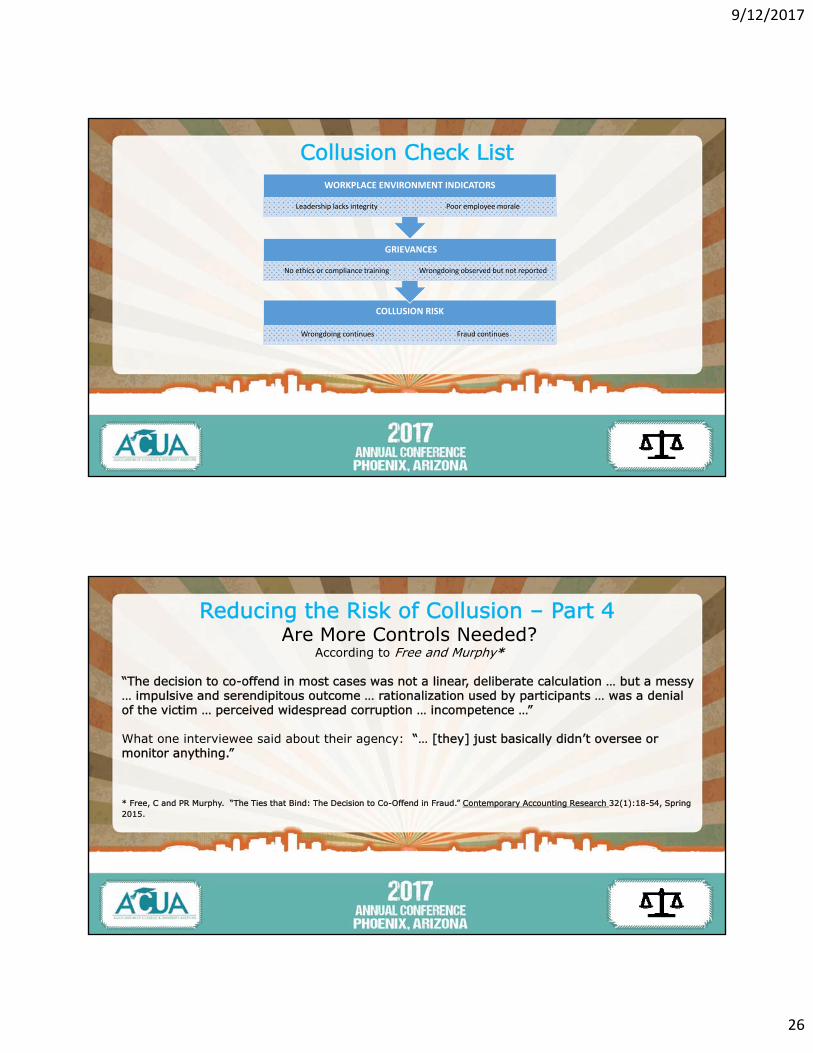

Collusion Check List

COLLUSION RISK

Favoritism Nepotism

INCREASE IN COMPLAINTS/GRIEVANCES

Increase in staff turnover Strained workplace relationships

COMPENSATION RISK INDICATORS

Bonus, Stipends, Overtime Hiring of relatives, friends

9/12/2017

25

Collusion Check List

COLLUSION RISK

Embezzlement Misappropriation

LAX OVERSIGHT

Ineffective separation of duties Ineffective theft detection

AUTHORIZATION RISK INDICATORS

Inappropriate hierarchy Alternate signatories and exceptions

allowed

Collusion Check List

COLLUSION RISK

Document falsification Forgery

FIXES ROUTINELY NEEDED

Increase in backlog, fund transfers, expense swapping, end‐of‐year transactions

Missing documents, photocopied documents, no paper trail, handwritten corrections

ACCOUNTING RISK INDICATORS

Single operator Complex financial structure

9/12/2017

26

Collusion Check List

COLLUSION RISK

Wrongdoing continues Fraud continues

GRIEVANCES

No ethics or compliance training Wrongdoing observed but not reported

WORKPLACE ENVIRONMENT INDICATORS

Leadership lacks integrity Poor employee morale

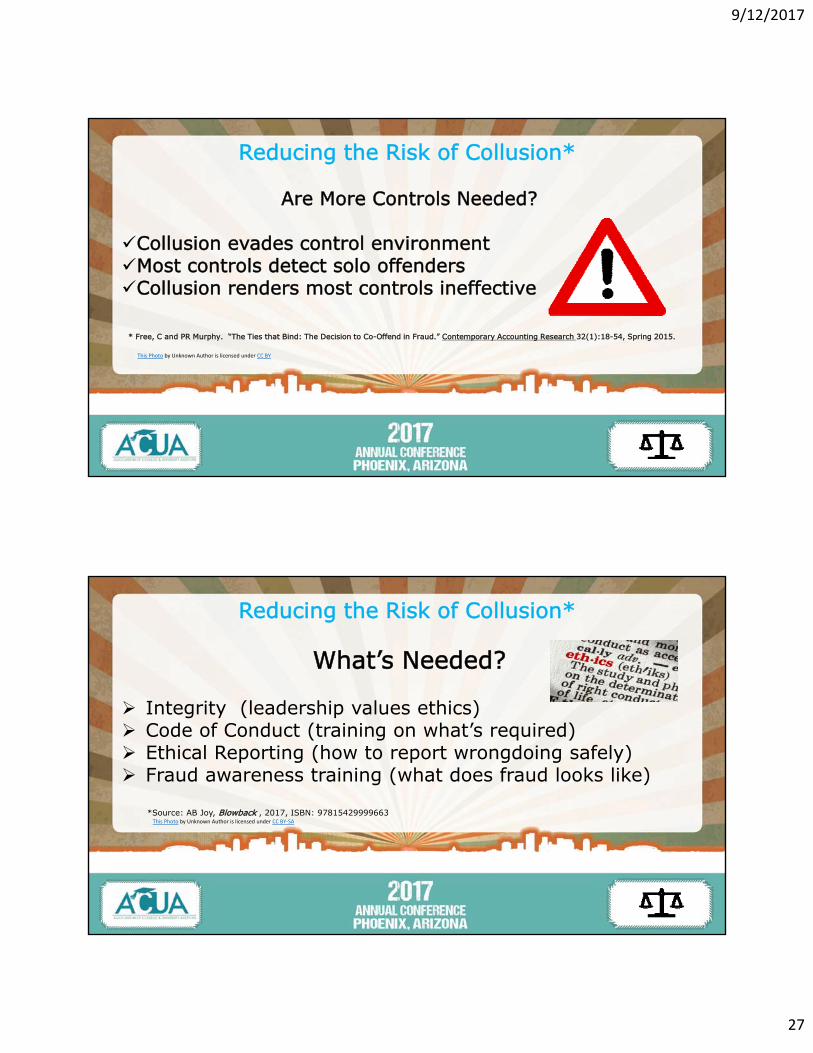

Reducing the Risk of Collusion – Part 4Are More Controls Needed?

According to Free and Murphy*

“The decision to co-offend in most cases was not a linear, deliberate calculation … but a messy … impulsive and serendipitous outcome … rationalization used by participants … was a denial of the victim … perceived widespread corruption … incompetence …”

What one interviewee said about their agency: “… [they] just basically didn’t oversee or monitor anything.”

* Free, C and PR Murphy. “The Ties that Bind: The Decision to Co-Offend in Fraud.” Contemporary Accounting Research 32(1):18-54, Spring 2015.

9/12/2017

27

Reducing the Risk of Collusion*

Are More Controls Needed?

Collusion evades control environmentMost controls detect solo offendersCollusion renders most controls ineffective

* Free, C and PR Murphy. “The Ties that Bind: The Decision to Co-Offend in Fraud.” Contemporary Accounting Research 32(1):18-54, Spring 2015.

This Photo by Unknown Author is licensed under CC BY

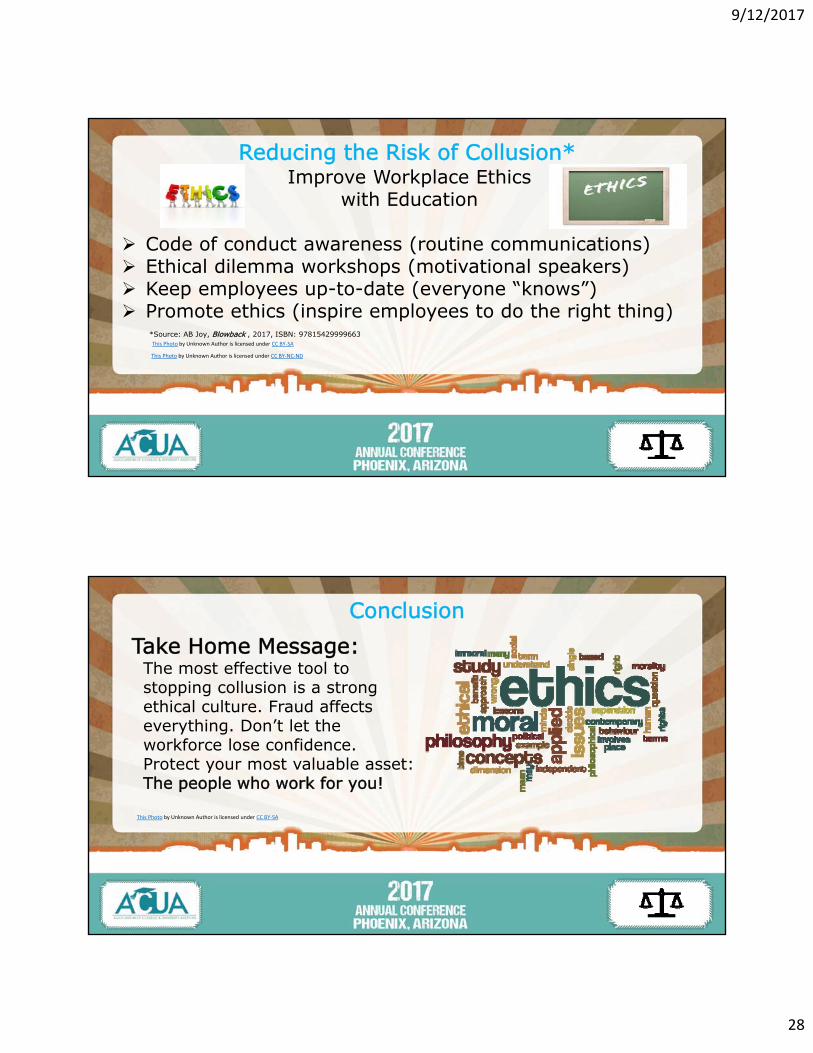

Reducing the Risk of Collusion*

What’s Needed?

Integrity (leadership values ethics) Code of Conduct (training on what’s required) Ethical Reporting (how to report wrongdoing safely) Fraud awareness training (what does fraud looks like)

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY‐SA

9/12/2017

28

Reducing the Risk of Collusion*Improve Workplace Ethics

with Education

Code of conduct awareness (routine communications) Ethical dilemma workshops (motivational speakers) Keep employees up-to-date (everyone “knows”) Promote ethics (inspire employees to do the right thing)

*Source: AB Joy, Blowback , 2017, ISBN: 97815429999663This Photo by Unknown Author is licensed under CC BY‐SA

This Photo by Unknown Author is licensed under CC BY‐NC‐ND

Conclusion

Take Home Message:The most effective tool to stopping collusion is a strong ethical culture. Fraud affects everything. Don’t let the workforce lose confidence. Protect your most valuable asset: The people who work for you!

This Photo by Unknown Author is licensed under CC BY‐SA