Embed Size (px)

Citation preview

9/12/2017

1

Capital Project Cost Management - Implementing a PreConstruction Contract Review and an Ongoing

Monitoring ProgramPresenters

Martin Howell, CCA Principal Fort Hill Associates, LLCJim McCoy, PE, CCA Senior Construction Auditor Fort Hill Associates, LLCCurt Plyler, CFA, CCA Principal Fort Hill Associates, LLC

Introduction – Fort Hill Associates, LLC• Consultancy specializing in construction contract auditing

• Founded in 2006

• Significant focus on higher education projects• Clemson University University of Richmond• Duke University University of Wyoming• Emory University Oregon State University• Portland State University Virginia Tech• University of Houston Wake Forest University• Univ. of North Carolina System West Virginia University

• Audit philosophy of identifying issues prior to contract execution

9/12/2017

2

Introduction – Speakers• Curt Plyler

• Founding member of firm in 2006• Certified Construction Auditor & a CFA charterholder• Engagement Manager at Duke University & University of Richmond

• Jim McCoy• Joined firm in 2016 after 30 years in Facilities Management at Virginia Tech• Certified Construction Auditor & Licensed Professional Engineer• Audit Manager at University of Wyoming & West Virginia University

• Martin Howell• Founding member of firm in 2006• Certified Construction Auditor• Engagement Manager at Emory University & Clemson University

Introduction – Session Objective #1Understand the need for a transactional audit of Contractor/Construction Manager (CM) project billings to complement existing procedural audits

• Procedural audits often are used to detect & eliminate fraud, but the transactional construction audit goes a step further to ensure the project owner has been billed correctly

• A transactional construction audit is designed to validate that the Contractor/CM billings to the Institution are compliant with the construction contract

• The complexity of a construction contract lends itself to using estimates of actual costs (requiring reconciliations)

• The Contractor/CM may attempt to include non-reimbursable overhead costs in their billing

• Effective auditing requires an understanding of how the various components of a construction project are billed to the project owner

9/12/2017

3

Introduction – Session Objective #2Understand why changes in the construction contracting environment are dictating an increased level of oversight by project owners

• Facilities staff are often more familiar w/ the ‘hard bid’ contract• Frequently used on public projects in the past• Project owner pays the agreed-upon amount, regardless of actual

costs• Institutional Resources and skill sets needed for proper analysis of costs

incurred may be limited, if they exist• Larger, more complex projects are increasingly being constructed under

open-book reimbursable contracts• Costs must be substantiated• If the contract amount is not reached, the Institution pays less

Introduction – Session Objective #3

Understand why significant focus should be placed on reconciling rates & methods used to approximate actual costs incurred

• Estimates are routinely used to develop rates for labor costs, leased equipment, project insurance, and IT needs

• These rates are proposed by the Contractor/CM and therefore, they tend to be conservative

• These rates are typically included in the Contractor/CM proposal which is often incorporated into the construction contract

• A best practice is to analyze all proposed rates prior to contract execution, but if that can’t be done, language allowing an audit-to-actual cost should be included in the construction contract

9/12/2017

4

Presentation Outline

1) Overview of Construction Processes and Contract Typesa) Understand the impact of the evolution of construction delivery methodsb) Basic Contract Typesc) Components of a Cost Plus Contract

2) Construction Audit Processa) Standard Construction Audits – what needs to be reviewed and whyb) Challenges to the Institution’s Project Management Staffc) The benefits of a PreConstruction Contract Review

Introduction – Key Takeaway #1

Construction auditing will identify overpayments and opportunities for cost avoidance on most large construction projects

• A detailed analysis is typically not performed by most facilities staff • The incentive to reconcile rates and other project costs lies with the

Institution• Billings for a construction project with a well-written contract will often

have overcharges of 1-2% if not properly monitored

9/12/2017

5

Introduction – Key Takeaway #2

A PreConstruction Contract Review to establish effective controls at project inception is essential

• Mitigates problems & issues before they occur• Reconcile differing contract interpretations, clarifying the intent of

‘actual cost incurred’ and what is/is not an overhead cost• Establish expectations for proper support for payment

• Enables a more efficient audit at project conclusion• Proposed rates and other costs have been reviewed and approved at

project inception• At project conclusion, the focus shifts to the proper application of the

rates & previous cost representations• Cost savings are realized over the entire project, eliminating the need

for a settlement of disagreements at the conclusion of the project

Introduction – Key Takeaway #3

Construction Audits can effectively supplement the Project Management services currently being performed by the Institution.

• A typical Institution’s Project Management staff may not have the capacity to effectively monitor Contractor/CM billings at a transactional level.

9/12/2017

6

• A basic understanding of construction contracting methodology is essential for assessing Institutional risk, identifying project financial controls, and developing an effective audit plan.

• A Construction Audit effectively measures the Contractor’s compliance with the billing requirements set forth in the contract.

Construction Contracting 101

• Design-Bid-Build (Lump Sum/Fixed Price Contract)• Traditional “hard bid” or “low bid” contract

• Multi-Prime (Lump Sum/Fixed Price Contract)• Institution contracts separately with a General Contractor, Mechanical Contractor,

Electrical Contractor, etc. to construct a single project• Design-Build (Lump Sum/Fixed Price or Cost Plus Contract)

• Institution executes one contract with a single entity to both design and construct a facility

• Construction Manager @ Risk (Cost Plus Contract)• Competitive negotiation contract that typically includes a Guaranteed Maximum Price

Construction Delivery and Typical Contracting Methodology

9/12/2017

7

Construction Contract Types

Lump Sum/Fixed Price (Design-Bid-Build)

• Typical contracting method for small (<$10M) projects with a clearly defined scope and with minimal schedule constraints

• Contract awarded to a “General Contractor” based on lowest responsive bid from a responsible bidder

• Building design completed prior to bidding and construction• Contract price is fixed (adjusted by Change Orders)• Limited scope for a Construction Audit– Contractor increases

profit through cost reductions

Construction Contract Types

Cost Plus (Construction Manager @ Risk)• Typical contracting method for “large” projects (>$10M) that are

complex and/or have aggressive completion schedules• Contract awarded to “Construction Manager (CM)” early in the

design process based on best value (weighted combination of contractor qualifications and price)

• CM initially contracted to provide PreConstruction services while the project is still being designed

• Construction contract negotiated during PreCon phase • Construction start typically prior to design completion

9/12/2017

8

Construction Contract Types

Cost Plus (Construction Manager @ Risk) - Continued

• Institution reimburses the CM for their direct construction Costsas allowed by the contract Plus the Institution pays an additional amount for overhead and profit

• Open-Book contract provision allows the Institution to have full access to the CM’s cost records

• Contract price is not fixed but typically capped at some amount (Guaranteed Maximum Price – GMP, GMAX)

• Actual cost to the Institution may be less than GMP amount

Components of a Cost Plus Construction Contract

1) Construction Manager’s Fee

2) Cost of the Work

9/12/2017

9

Components of a Cost Plus Construction Contract

Construction Manager’s Fee

• The “plus” component of a Cost Plus construction contract• CM’s Overhead and Profit• Typically paid as a lump sum or % of the Cost of Work

Components of a Cost Plus Construction Contract

Cost of Work (Direct Costs)

• General Conditions – CM’s on site project management/supervisory labor, equipment and materials • Project Manager(s), Superintendent(s), Admin/Fiscal Support, etc.• Trailer Rental, Vehicles, IT, etc.• Often treated as a separate contract component• Sometimes paid by Owner as a lump sum amount

• General Requirements – CM’s construction labor, equipment and materials• Layout, weather protection, daily clean up, etc.

9/12/2017

10

Components of a Cost Plus Construction Contract

Cost of Work (Direct Costs) - Continued

• Subcontracts and Self-Performed Work• By far the largest component of the construction contract

• CM Performance/Payment Bonds, GL Insurance, Builder’s Risk, etc.• May be included in General Conditions or CM Fee

• Allowances• Elements of work that are known, but not fully defined

• Construction Contingency• Unknown elements of work

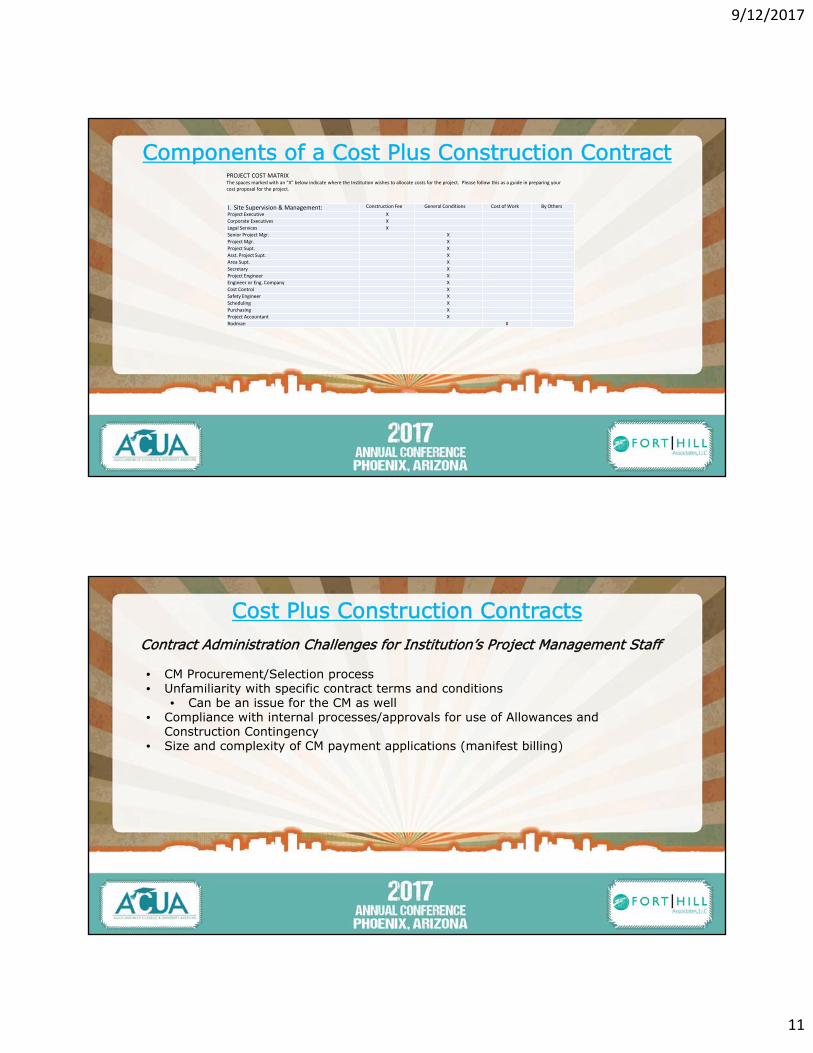

Components of a Cost Plus Construction Contract

9/12/2017

11

Components of a Cost Plus Construction ContractPROJECT COST MATRIX The spaces marked with an "X" below indicate where the Institution wishes to allocate costs for the project. Please follow this as a guide in preparing your cost proposal for the project.

I. Site Supervision & Management: Construction Fee General Conditions Cost of Work By Others

Project Executive X

Corporate Executives X

Legal Services X

Senior Project Mgr. X

Project Mgr. X

Project Supt. X

Asst. Project Supt. X

Area Supt. X

Secretary X

Project Engineer X

Engineer or Eng. Company X

Cost Control X

Safety Engineer X

Scheduling X

Purchasing X

Project Accountant X

Rodman X

Cost Plus Construction Contracts Contract Administration Challenges for Institution’s Project Management Staff

• CM Procurement/Selection process• Unfamiliarity with specific contract terms and conditions

• Can be an issue for the CM as well • Compliance with internal processes/approvals for use of Allowances and

Construction Contingency• Size and complexity of CM payment applications (manifest billing)

9/12/2017

12

Standard Construction Audit - General Conditions

General Conditions are the tools, resources and equipment needed to build a project, but not directly related to the physical construction activities

• Management Labor

• CM-owned Leased Equipment

• Information Technology

• Insurance and Bonds

9/12/2017

13

General Conditions – Management Labor

Management labor typically includes the Project Manager, Project Engineer, Superintendent, Project Accountant and others.

• On-site support is reimbursable

• Home office support is normally considered overhead

• Reimbursable labor can be charged at actual cost, actual cost plus agreed labor burden, or billable labor rates – the Contract specifies which methodology

Home Office Labor

Click to add text

Project Executive

Dir. of Safety

Human Resources Director

9/12/2017

14

Excessive Staff

General Conditions – Leased Equipment

Many Contractors/CMs own their own equipment and lease it to the job in excess of market lease rates. This can be a significant profit center to the Contractor/CM.

• Institution should never be charged more than purchase price of equipment charged

• Contract may cap lease rates or aggregate lease payments at some pre-defined index (i.e., AED Green Book)

9/12/2017

15

General Conditions – Information Technology

Information Technology (IT) can be a significant profit center for the Contractor/CM.

• GMP contracts normally allow project-specific IT as a reimbursable project cost• Laptops• Software• Connectivity

• IT typically charged at a monthly rate or percentage of Contract value• The monthly rate or percentage should be analyzed to ensure non-reimbursable

overhead costs are excluded from the calculation• IT staff• Home office servers

• If a rate or percentage is employed, project cost transactions should be scrutinized to ensure duplicate IT costs have been excluded

General Conditions – Insurance and Bonds

Insurance and Bonds represent one of the greatest opportunities to gain additional profit above and beyond the CM Fee for the Contractor/CM

• General Liability• Subcontractor Default Insurance• Builder’s Risk• Performance and Payment Bond• OCIP/CCIP (wrap-up)• Contractor/CM subsidiary often procures the policy

9/12/2017

16

Insurance – General Liability

• Contract normally specifies charge as a percentage

• If not specified, project-specific GL insurance is reimbursable at cost

• Contractors/CMs will often include overhead and coverages not required by the Institution

• Professional Liability – often the responsibility of the A/E firm• Directors and Officers – no benefit to the Institution

• Transparency is often lacking from the Contractor/CM when trying to ascertain actual cost

Insurance – Subcontractor Default (Subguard)

Subcontractor Default Insurance is a specific insurance product takes the place of Subcontractors procuring their own performance and payment bonds. • Provides for immediate restitution in the event a Subcontractor goes into default • Contract almost always specifies charge as a percentage

• Audit is then to ensure proper application of the rate• The RFP for Contractor/CM services should specify a cap for this rate

• The rate for this coverage includes:• Premium• Subcontractor Qualification• Claims

• Subcontract bids should be reviewed to ensure bond costs have been removed

9/12/2017

17

Insurance – Builder’s Risk

Builder’s Risk Insurance protects the Institution’s insurable interest in materials, fixtures and/or equipment being used in the construction or renovation of a building or structure should those items sustain physical loss or damage from a covered cause.

• Project specific policies are routinely purchased & converted to a percentage

• Before requiring this coverage, an Institution should determine whether their own existing coverage is sufficient

Bonds – Performance and Payment

A performance bond guarantees satisfactory performance of all duties specified in the contract. Payment bonds guarantee all participants (suppliers, subcontractors, and laborers) will be paid should the Contractor/CM default.

• Most projects require these bonds as part of the Contract

• Some Contractors/CMs will mark-up the bond for administration costs

• The Institution should pay no more than the premium cost only

9/12/2017

18

Insurance – OCIP/CCIP

Owner (OCIP) or Contractor (CCIP) Controlled Insurance Programs are sometimes utilized on a project in lieu of GL insurance and Workers’ Compensation Insurance for both the Contractor/CM and the Subcontractor.

• Contract almost always specifies charge as a percentage• Audit is then to ensure proper application of the rate• These rates typically range from 1.6 – 2.9% of the Contract value

• Subcontract bids should be reviewed to ensure GL & workers’ compensation costs have been removed

Standard Construction Audit – Cost of Work

• Subcontracts represent the largest cost on a project. Most Subcontract agreements are awarded on a lump sum basis.

• Self-performed work is another potential profit center. If the Contractor/CM is self-performing any aspect of the project, a clear delineation of costs should be provided.

• Materials purchased directly by a Contractor/CM or Subcontractors working under reimbursable arrangements should require proof of purchase.

9/12/2017

19

Cost of Work - Subcontracts

Subcontracts represent the largest cost on a project. Most Subcontract agreements are awarded by the Contractor/CM on a lump sum basis.

• Ensure the Institution does not pay more than the Contract amount • Ensure partial and final liens are received from each Subcontractor with the

submission of their payment application• Utilize third-party software (similar to Textura) for verification of amounts, approvals,

etc.

Cost of Work – Self Performance

Self-performed work is another potential profit center. If the Contractor/CM is self-performing any aspect of the project, a clear delineation of costs should be provided.

• The Contractor/CM must provide a clear delineation of costs incurred to prevent the duplication of costs charged elsewhere on the project

• The Contractor/CM should provide a separate billing each month for the self-performed work

• The contract should be amended to provide the ability to audit costs for the self-performed work

• The self-performed work should be compensated in the same manner as the base contract

9/12/2017

20

Cost of Work - Materials

Materials purchased directly by a Contractor/CM (or Subcontractors working under a reimbursable subcontract) should require proof of purchase.

• Most materials are procured by the Subcontractors (Trades) working on the project and reside inside of the Subcontract agreements.

• Subcontractors working under reimbursable Contract arrangements need to provide support for the material purchases

• Some materials procured directly by the Contractor/CM should require proof of purchase in the form of invoices, receipts, etc.

Standard Construction Audit – Change Orders

Audits of Change Orders should focus on the following:

• Ensuring appropriate backup support has been provided

• The scope of the change is not an obvious duplication of the base work

• Appropriate approvals have been obtained

• Contract-allowed markups have been calculated correctly

9/12/2017

21

Standard Construction Audit - Project Closeout

The final contract value should be determined at the end of the project after the following items have been completed:

• Reconcile Allowances and Contingency funds

• Reconcile the Contractor’s/CM’s actual costs to the current contract value

• Calculate shared savings (if stipulated by contract)

Project Closeout – Allowances and Contingency

• Allowances and contingency funds need to be reconciled at project closeout

• The Contractor/CM should be able to provide a log identifying usage amount and purpose

• Unused funds, if any, should revert to the Institution unless otherwise specified

9/12/2017

22

Project Closeout – Cost System Reconciliation

• Obtain aggregate cost system report

• Contractor/CM should confirm if any transactions were excluded from the Institution’s billing

• Remove any transactions deemed non-reimbursable during audit

• Add insurance and Contractor’s/CM’s Fee if excluded from cost report

• Compare to the current contract amount

• Calculate shared savings (if stipulated by contract)

Construction Audits Can Effectively Supplement Existing Owner Project Management Services

A typical Institution’s Project Management staff may not have the capacity to effectively monitor Contractor/CM billings at a transactional level. • Limited staff resources • Skill set and personal focus of project management staff • Higher profile issues to address (construction schedule, contract

disputes, facility completion and building occupancy, etc.)• Reluctance to expose what may be perceived as mismanagement and/or

poor performance• Facilities/CM relationship may create an awkward audit environment

9/12/2017

23

PreConstruction Contract Review

A timely and thorough PreConstruction Contract Review can preemptively mitigate many billing issues that might occur during the construction period as well as facilitate the Construction Audit process.

PreConstruction Contract Review

“It’s good to be in something from the ground floor.”

-George Costanza (working on the Penske file)

Insert Logo Here

9/12/2017

24

PreConstruction Contract Review – What is it?

• Overall contract review and mutual understanding with the Contractor/CM regarding Contract interpretation and administration

• Proactive review of a Contractor/CM’s billing methodologies with a specific focus on issues typically arising in a traditional audit at project closeout

• Review and modification of Contract language to ensure the Institution’s interests are not compromised

• Preferably conducted prior to Contract execution, but still beneficial early in the project

PreConstruction Contract Review – Who is Involved?

Facilities • Construction contract administrators ultimately charged with managing the

project• Good understanding of the way the Institution conducts business

Internal/External Audit• Provides the skill set to accurately assess the Contractor/CM’s billing

methodologies in relation to the Institution’s expectations• Identify Contract language at odds with the Institution’s intent for both

reimbursable & non-reimbursable project costs• Able to identify process deficiencies and offer suggestions for mitigation

9/12/2017

25

PreConstruction Contract Review – Who is Involved?

Internal/External Legal Counsel• Review of Contract documents with a specific focus on minimizing the

Institution’s liability• Work is often complementary to the Contract review undertaken by Audit

Contractor/CM• Document desired billing methodologies• Promotes transparency

PreConstruction Contract Review – What is Reviewed?

All documentation comprising the construction contract• Identify inconsistencies, ambiguities and conflicts within the documents• Confirm the financial controls associated with various contract costs

Establish the basis for reimbursable costs• Hourly labor• Equipment owned by the Contractor/CM and leased to the project• Project insurance• Information Technology

9/12/2017

26

PreConstruction Contract Review – What is Reviewed?

Payment Application Support• What does the Contractor/CM intend to provide?• What does the Institution expect to receive?

• Schedule of Values• Periodic Cost Report• Subcontractor Payment Applications

Determine the methodology for pricing Change Orders• Agree on extent of cost itemization necessary for Institution approval• Agree on acceptable mark-ups• Agree on aggregate mark-up

PreConstruction Contract Review – What is Agreed?

• The document should address the Institution’s requirements for payment application support

• Schedule of Values• Periodic Cost Report• Subcontractor Payment Applications• Summary Schedules to aid in Monthly Reviews

• Labor• Leased Equipment • Subcontracts

• Change Order back-up• The understanding should be documented in an audit report or memorandum of

understanding and incorporated into the Contract

9/12/2017

27

PreConstruction Contract Review – What are the Benefits?

• Ensures transparency and fairness to both the Institution and the Contractor/CM on how the contract will be administered

• The Institution gets the full benefit of any Contract clarifications and/or modifications – in a traditional closeout audit, the findings are often negotiated at project closeout for less than full value

• Mitigates the potential for the Contractor/CM to utilize hidden profit centers to realize profit in excess of their stated Fee

Presentation Summary – Key Takeaways (Revisited)

• Construction auditing will identify overpayments on most large construction projects

• A PreConstruction Contract Review to establish effective controls at project inception is essential

• Construction Audits Can Effectively Supplement Existing Owner Project Management Services

9/12/2017

28

“Auditing isn’t painful. Getting shot is painful. Getting stabbed in the rib is painful.”

-Tony Soprano

Questions?

![Republic Act No. 8042. Implementing Rules. Omnibus Implementing Rules[1]](https://img.pdfslide.us/doc/110x75/550257514a7959362a8b47d7/republic-act-no-8042-implementing-rules-omnibus-implementing-rules1.jpg)