Embed Size (px)

Citation preview

Accounts Receivable and

Accounts Payable

Module 5

SAP 2007 / SAP University Alliances Introductory Accounting

Learning Objectives

SAP 2007 / SAP University Alliances Introductory Accounting

Accounts Receivable

SAP 2007 / SAP University Alliances Introductory Accounting

Accounts Receivable

SAP 2007 / SAP University Alliances Introductory Accounting

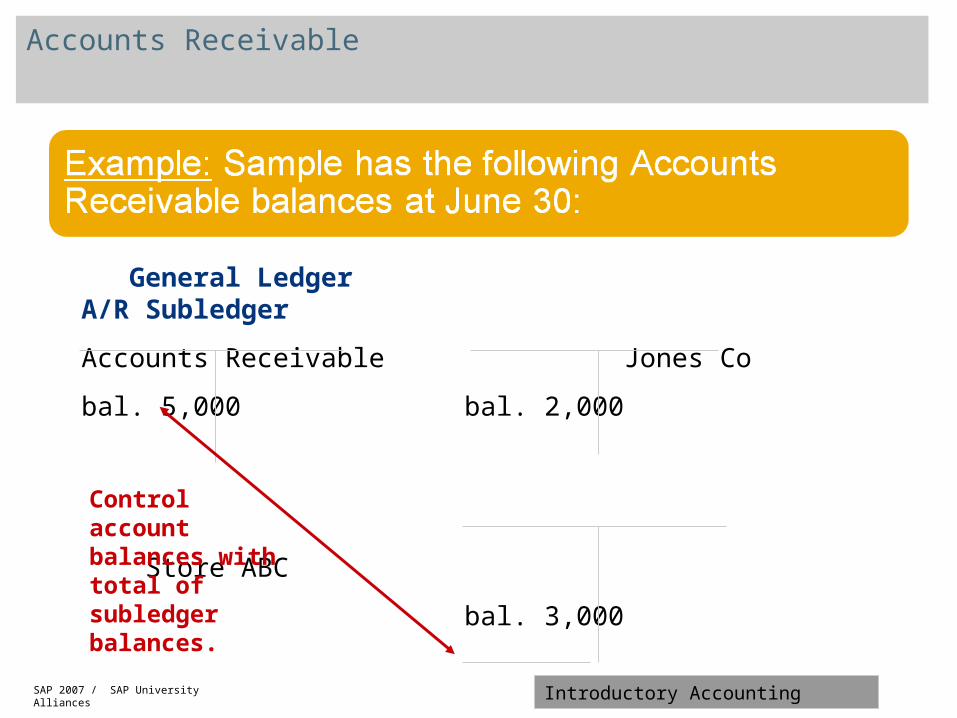

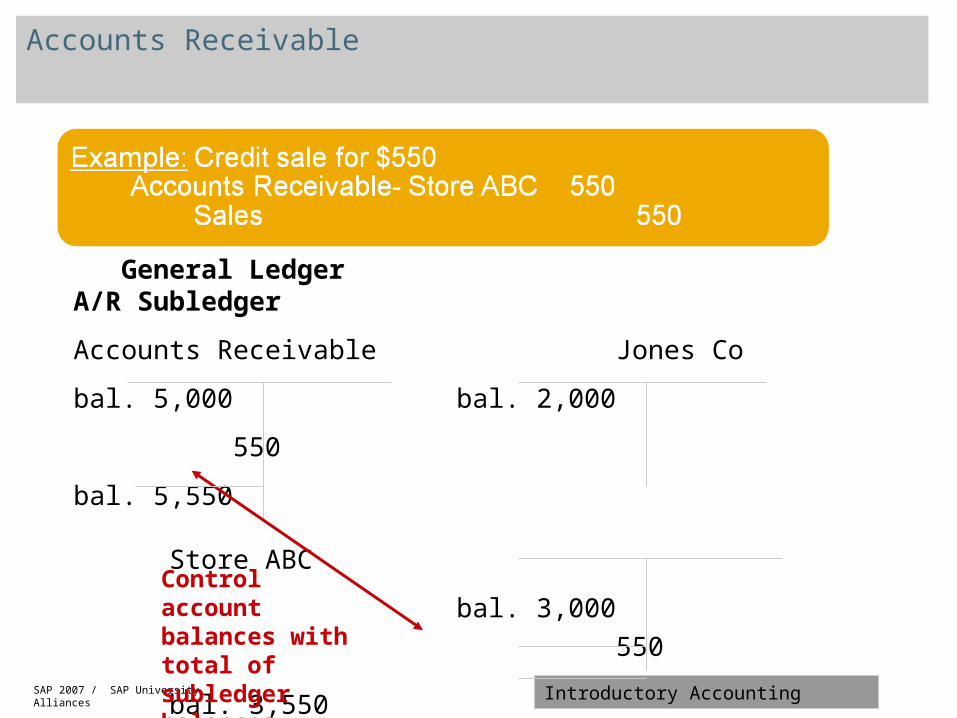

Accounts Receivable

General Ledger A/R Subledger

Accounts Receivable Jones Co

bal. 5,000 bal. 2,000

Store ABC

bal. 3,000

Total 5,000

Control account balances with total of subledger balances.

SAP 2007 / SAP University Alliances Introductory Accounting

Accounts Receivable

General Ledger A/R Subledger

Accounts Receivable Jones Co

bal. 5,000 bal. 2,000

550

bal. 5,550 Store ABC

bal. 3,000

550

bal. 3,550 Total 5,550

Control account balances with total of subledger balances.

SAP 2007 / SAP University Alliances Introductory Accounting

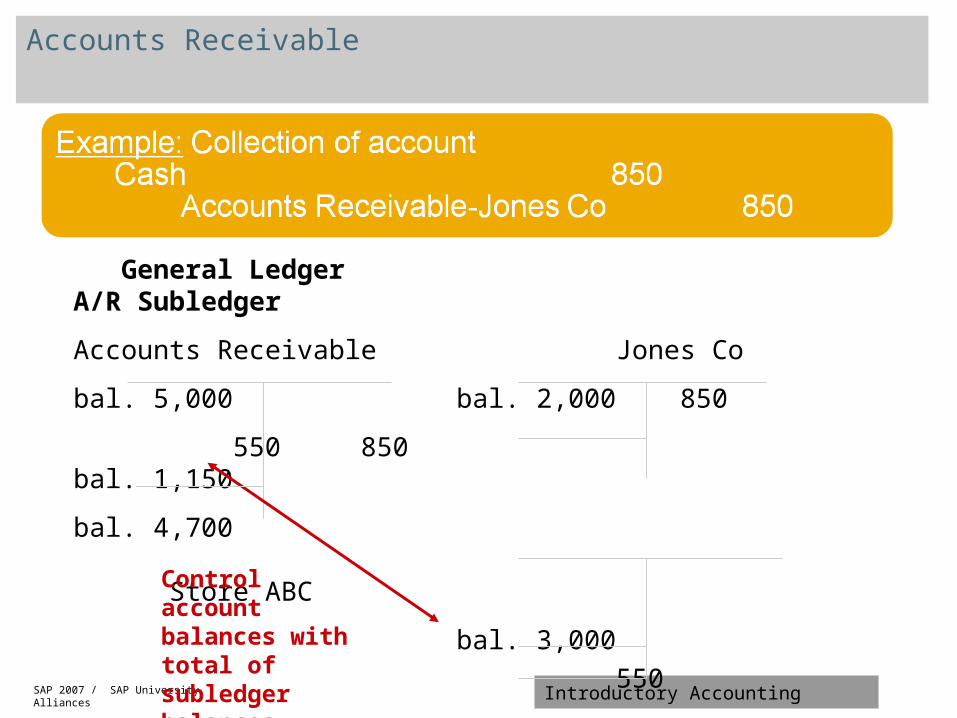

Accounts Receivable

General Ledger A/R Subledger

Accounts Receivable Jones Co

bal. 5,000 bal. 2,000 850

550 850 bal. 1,150

bal. 4,700 Store ABC

bal. 3,000

550

bal. 3,550 Total 4,700

Control account balances with total of subledger balances.

SAP 2007 / SAP University Alliances Introductory Accounting

Non-Bank Credit Cards

SAP 2007 / SAP University Alliances Introductory Accounting

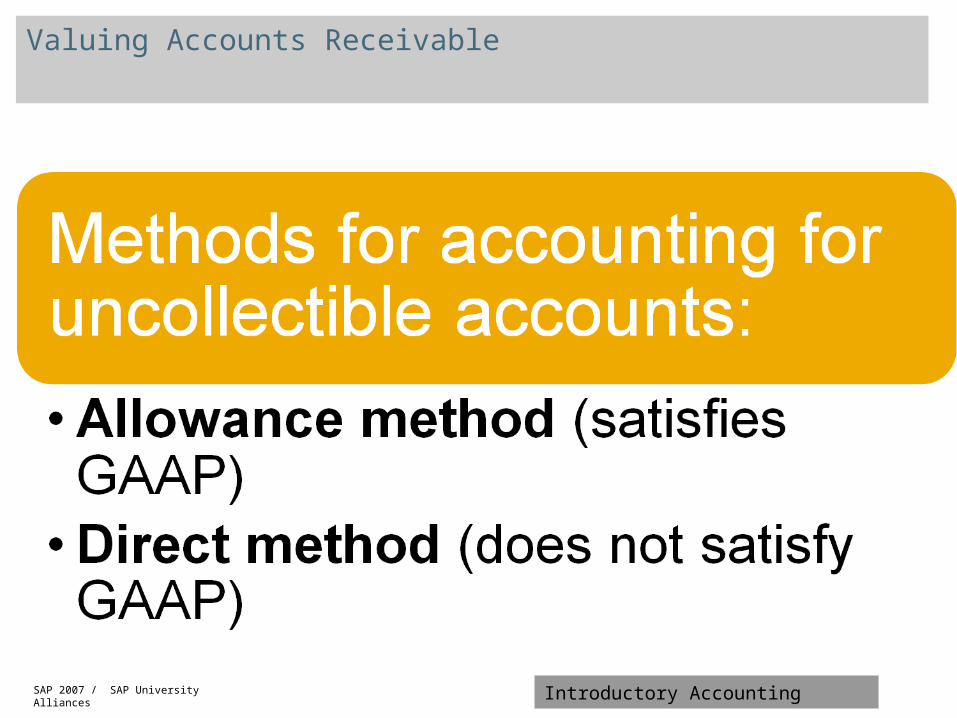

Valuing Accounts Receivable

SAP 2007 / SAP University Alliances Introductory Accounting

Valuing Accounts Receivable

SAP 2007 / SAP University Alliances Introductory Accounting

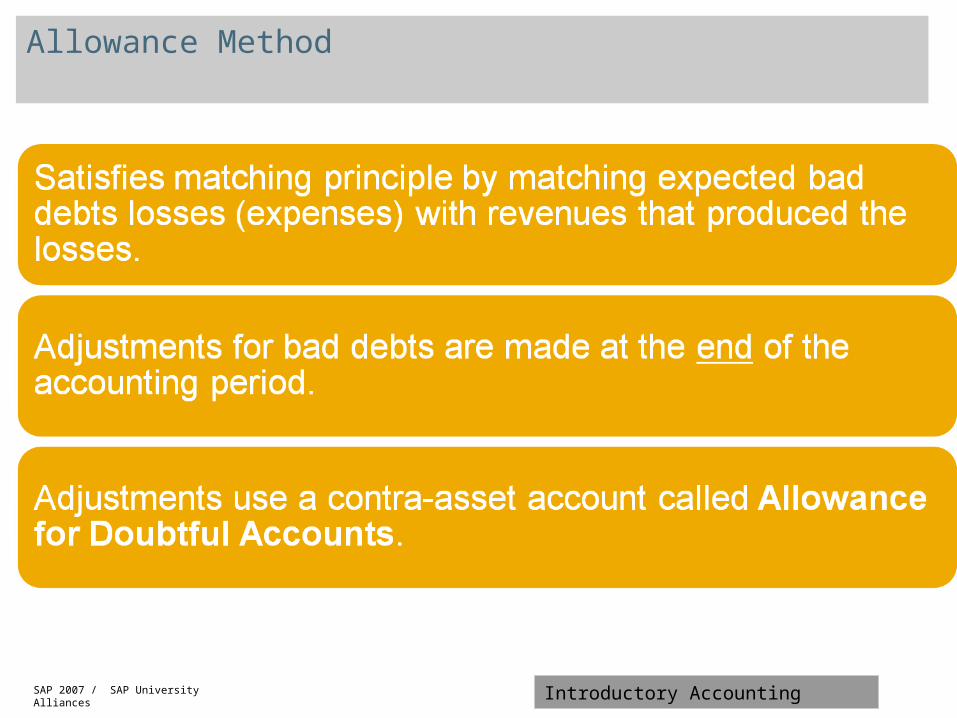

Allowance Method

SAP 2007 / SAP University Alliances Introductory Accounting

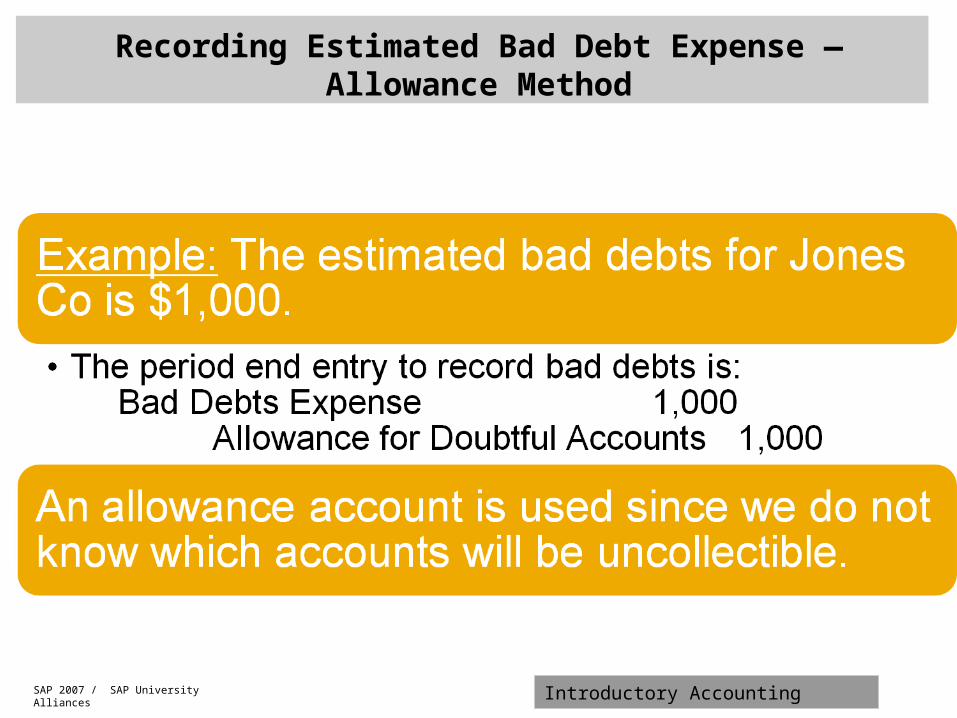

Recording Estimated Bad Debt Expense — Allowance Method

SAP 2007 / SAP University Alliances Introductory Accounting

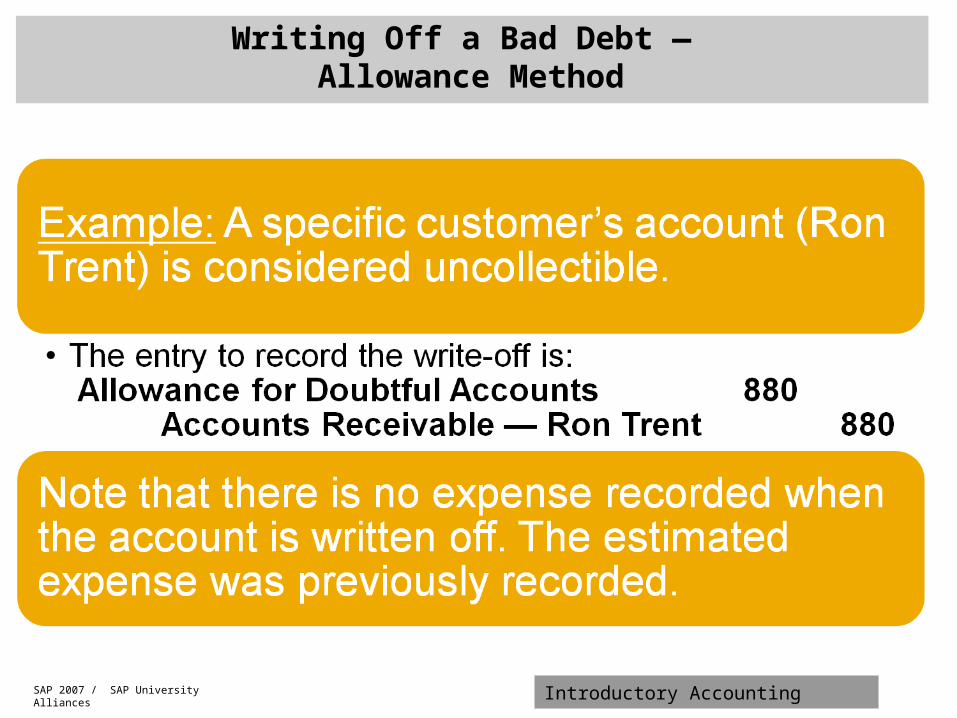

Writing Off a Bad Debt — Allowance Method

SAP 2007 / SAP University Alliances Introductory Accounting

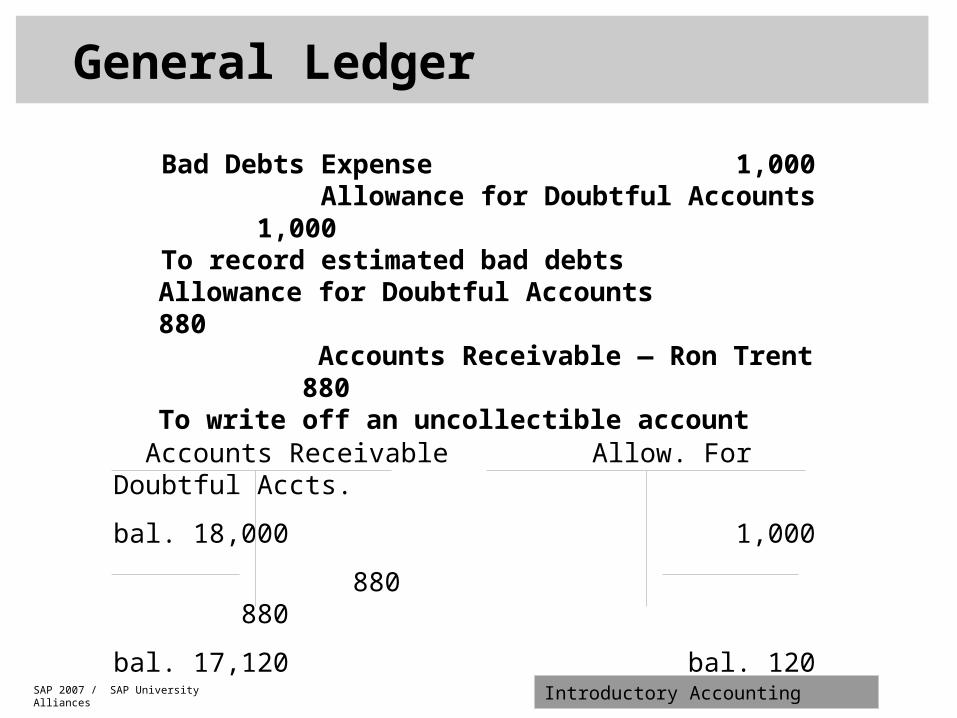

General Ledger Balances

Bad Debts Expense 1,000 Allowance for Doubtful Accounts 1,000To record estimated bad debts

Allowance for Doubtful Accounts 880 Accounts Receivable — Ron Trent 880To write off an uncollectible account

Accounts Receivable Allow. For Doubtful Accts.

bal. 18,000 1,000

880 880

bal. 17,120 bal. 120

SAP 2007 / SAP University Alliances Introductory Accounting

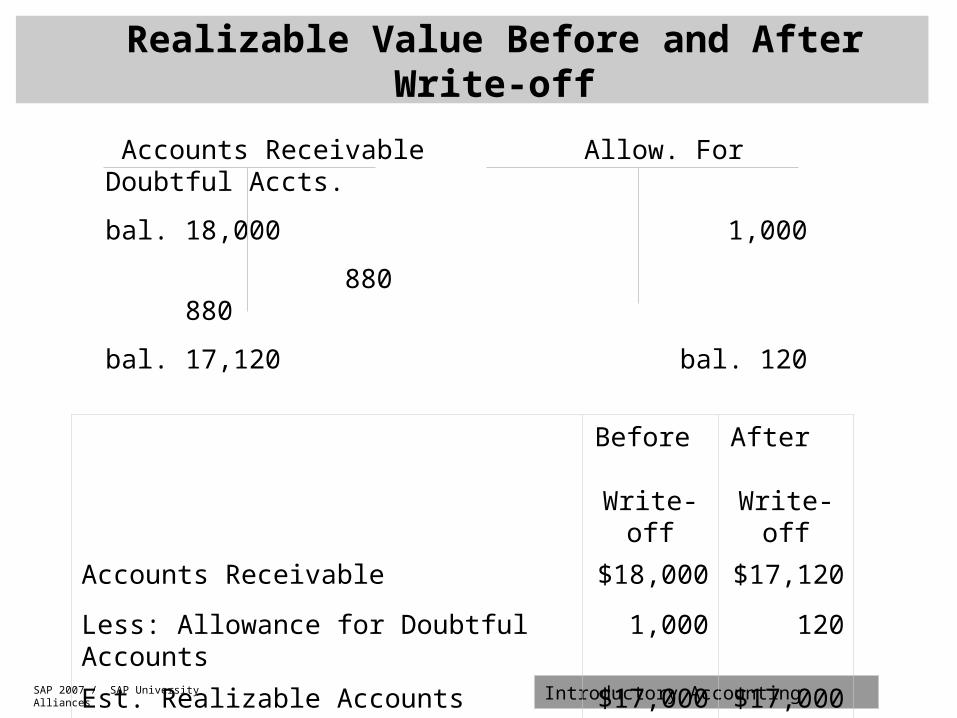

Realizable Value Before and After Write-off

Before Write-off

After Write-off

Accounts Receivable $18,000 $17,120

Less: Allowance for Doubtful Accounts 1,000 120

Est. Realizable Accounts Receivable $17,000 $17,000

Accounts Receivable Allow. For Doubtful Accts.

bal. 18,000 1,000

880 880

bal. 17,120 bal. 120

SAP 2007 / SAP University Alliances Introductory Accounting

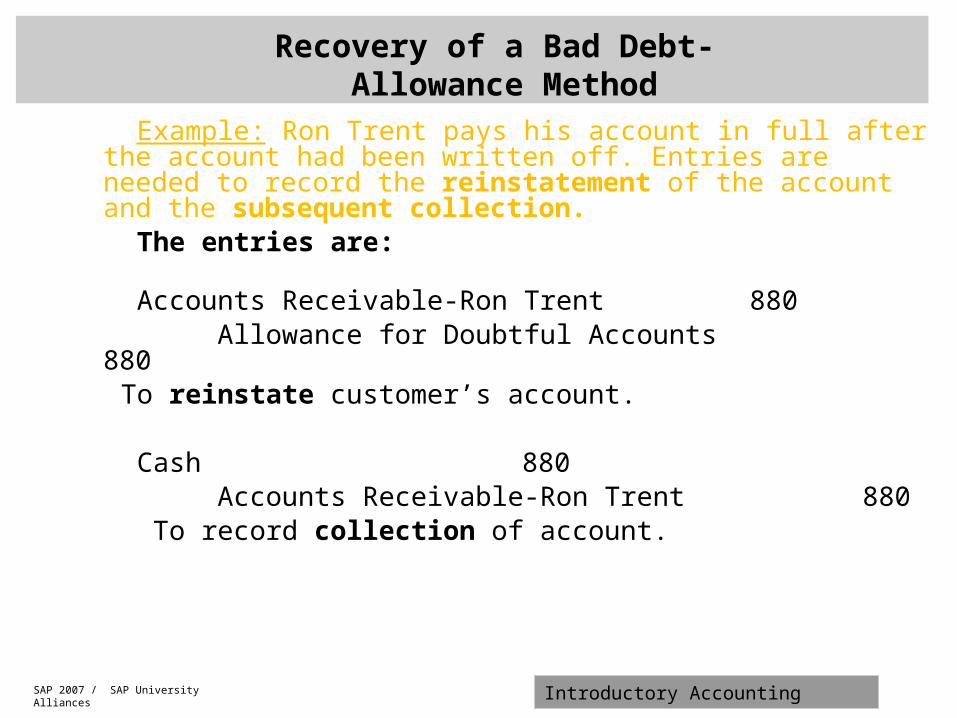

Example: Ron Trent pays his account in full after the account had been written off. Entries are needed to record the reinstatement of the account and the subsequent collection.

The entries are:

Accounts Receivable-Ron Trent 880 Allowance for Doubtful Accounts 880 To reinstate customer’s account.

Cash 880 Accounts Receivable-Ron Trent 880 To record collection of account.

Recovery of a Bad Debt- Allowance Method

SAP 2007 / SAP University Alliances Introductory Accounting

Estimating Bad Debt Expense

SAP 2007 / SAP University Alliances Introductory Accounting

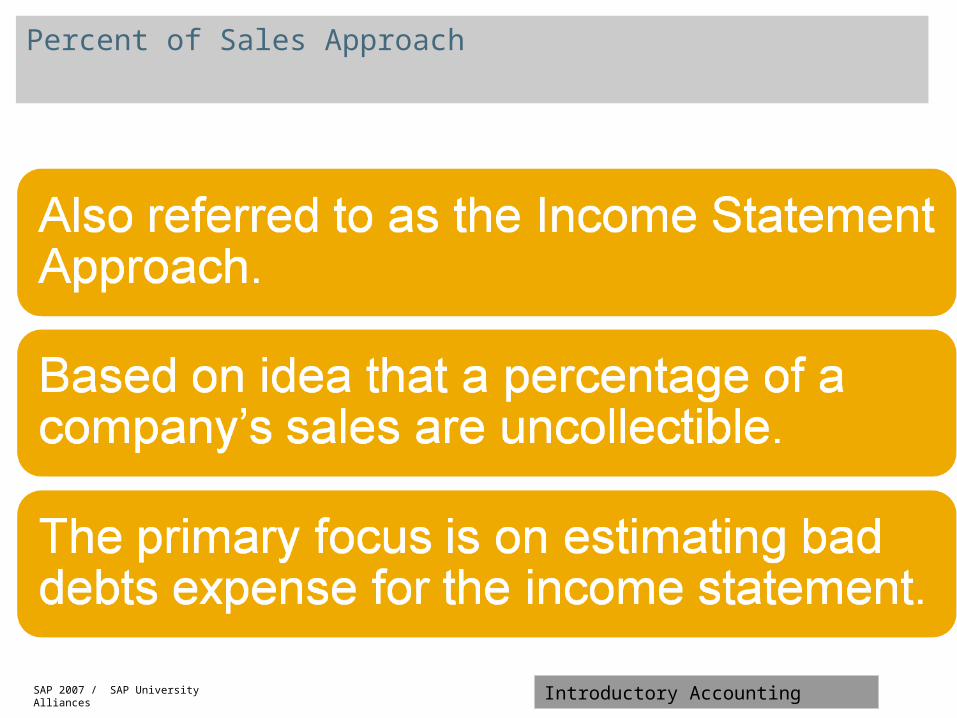

Percent of Sales Approach

SAP 2007 / SAP University Alliances Introductory Accounting

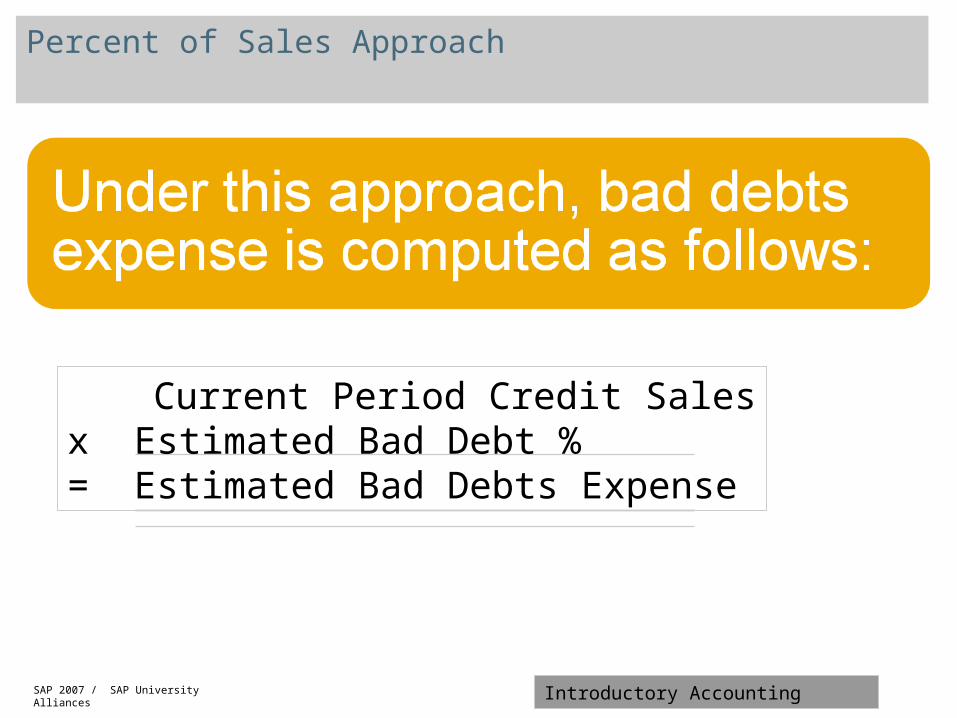

Percent of Sales Approach

Current Period Credit Salesx Estimated Bad Debt %= Estimated Bad Debts Expense

SAP 2007 / SAP University Alliances Introductory Accounting

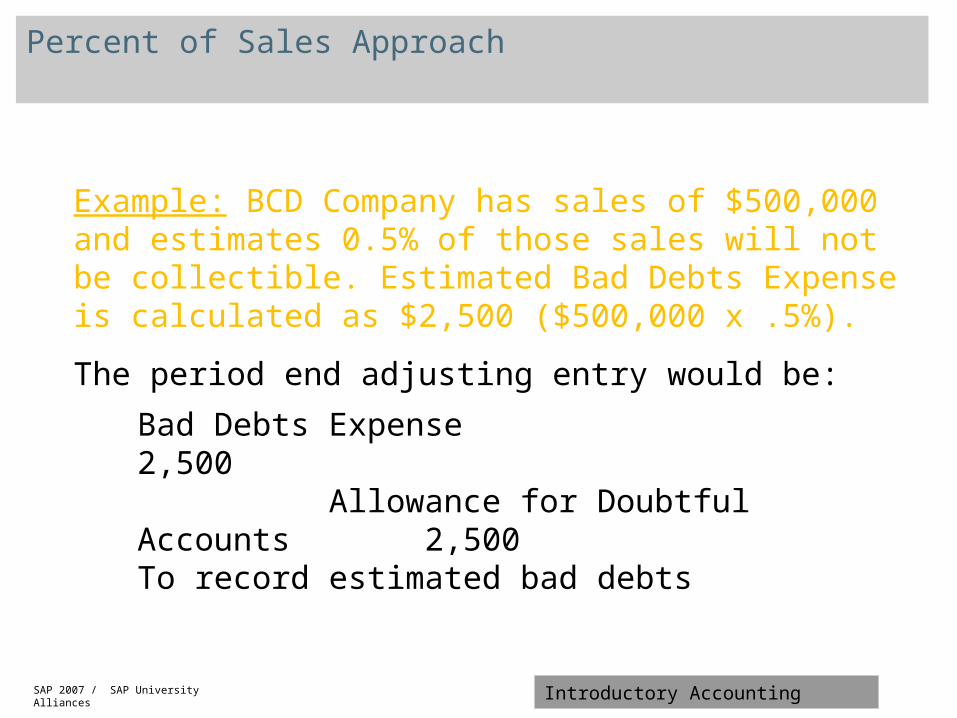

Example: BCD Company has sales of $500,000 and estimates 0.5% of those sales will not be collectible. Estimated Bad Debts Expense is calculated as $2,500 ($500,000 x .5%).

The period end adjusting entry would be:

Percent of Sales Approach

Bad Debts Expense 2,500 Allowance for Doubtful Accounts 2,500To record estimated bad debts

SAP 2007 / SAP University Alliances Introductory Accounting

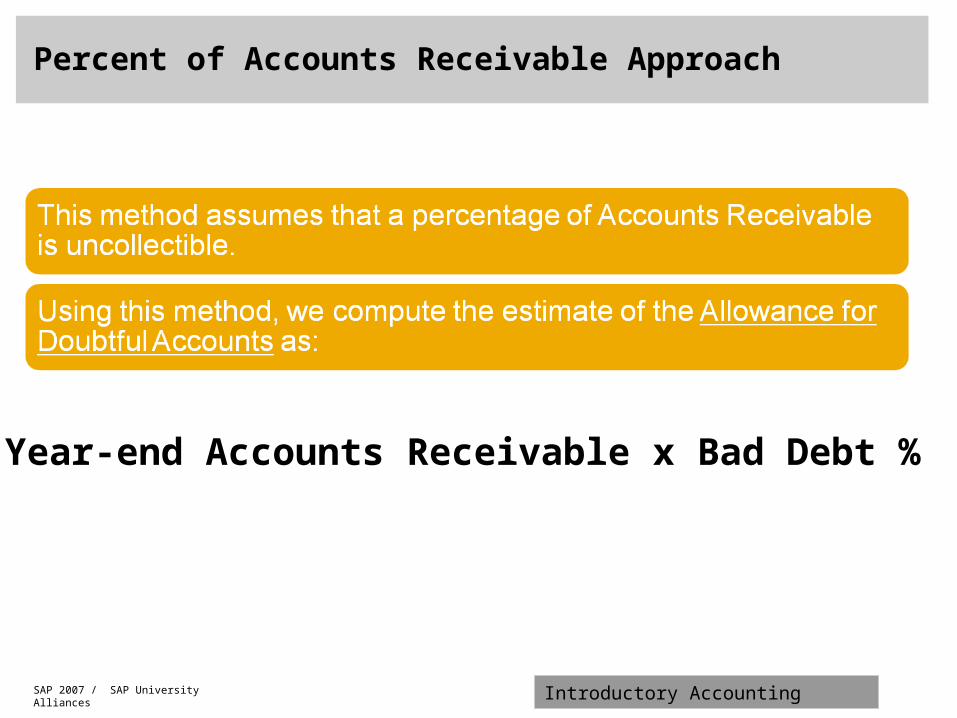

Year-end Accounts Receivable x Bad Debt %

Percent of Accounts Receivable Approach

SAP 2007 / SAP University Alliances Introductory Accounting

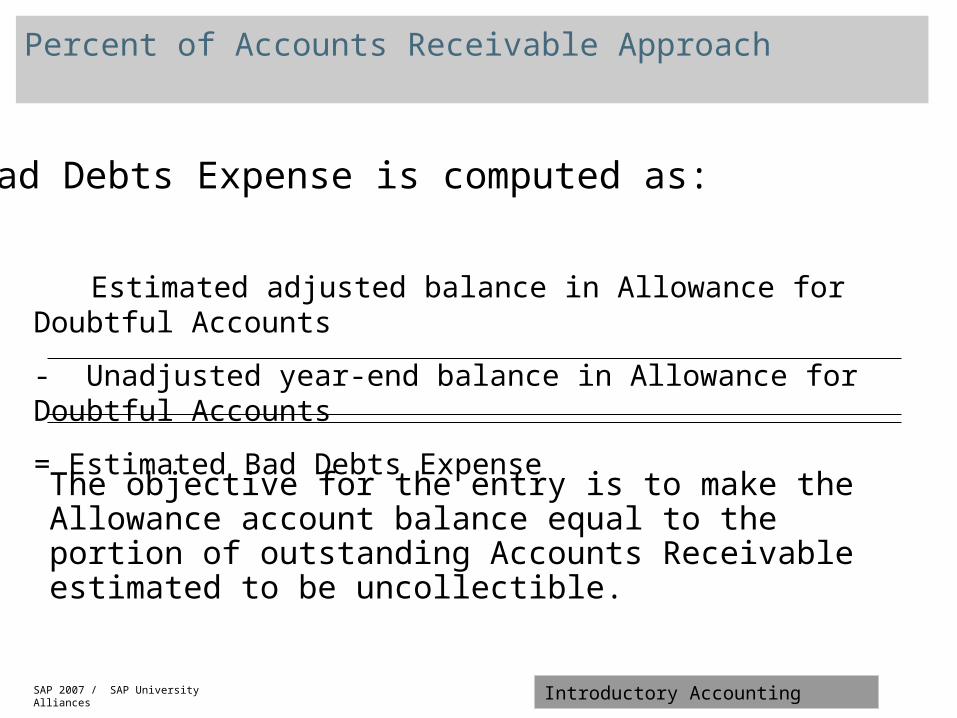

Percent of Accounts Receivable Approach

Bad Debts Expense is computed as:

Estimated adjusted balance in Allowance for Doubtful Accounts

- Unadjusted year-end balance in Allowance for Doubtful Accounts

= Estimated Bad Debts Expense

The objective for the entry is to make the Allowance account balance equal to the portion of outstanding Accounts Receivable estimated to be uncollectible.

SAP 2007 / SAP University Alliances Introductory Accounting

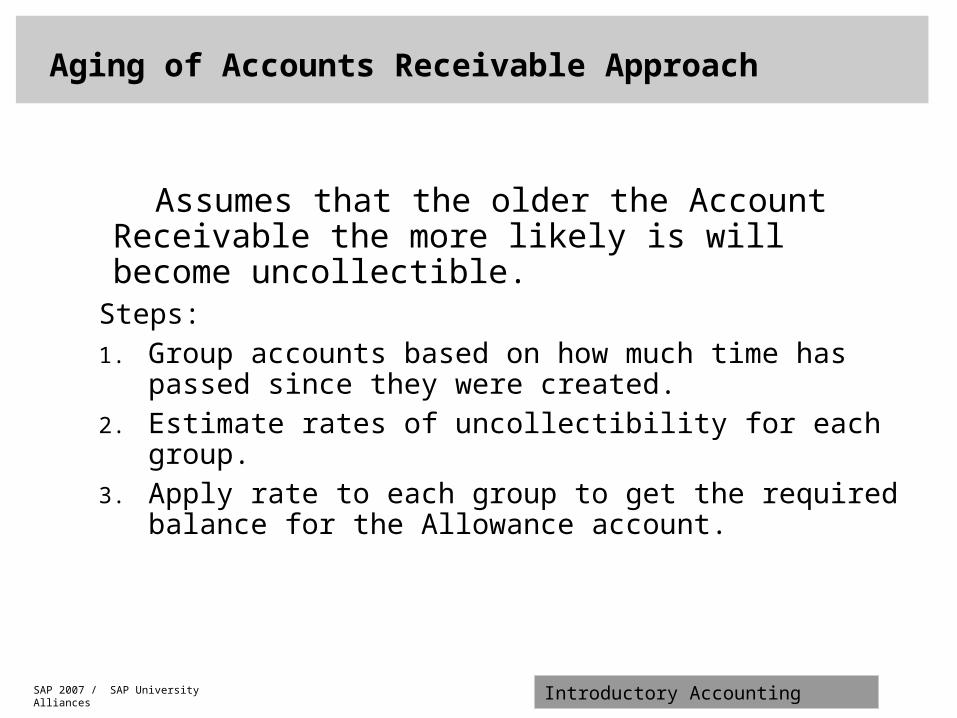

Assumes that the older the Account Receivable the more likely is will become uncollectible.

Steps:1. Group accounts based on how much time has

passed since they were created.2. Estimate rates of uncollectibility for each group.3. Apply rate to each group to get the required balance

for the Allowance account.

Aging of Accounts Receivable Approach

SAP 2007 / SAP University Alliances Introductory Accounting

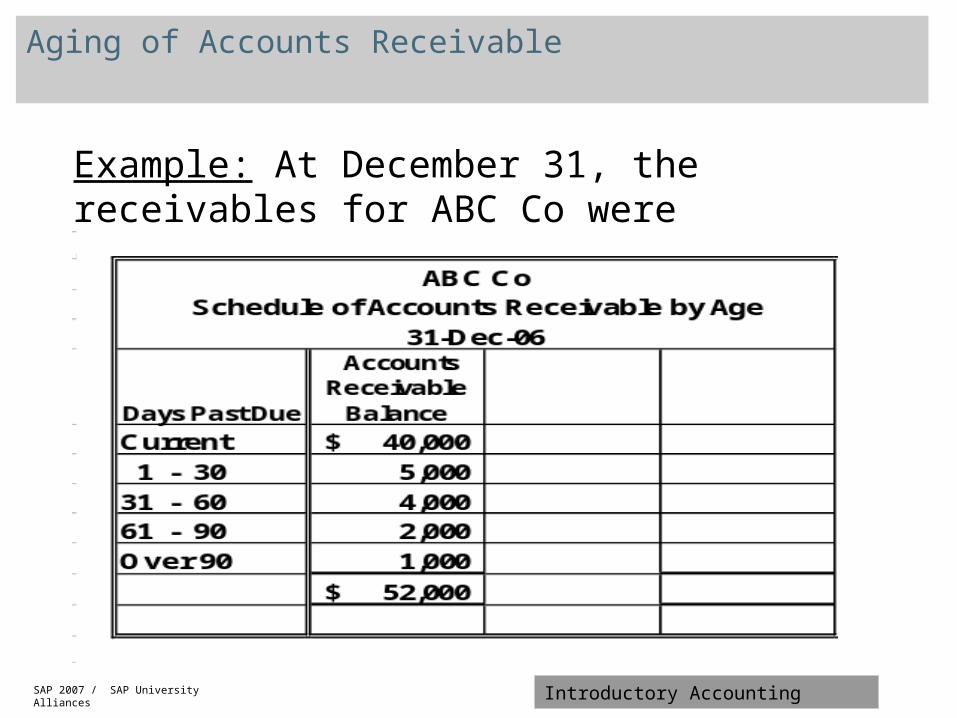

Example: At December 31, the receivables for ABC Co were classified as follows:

Aging of Accounts Receivable

SAP 2007 / SAP University Alliances Introductory Accounting

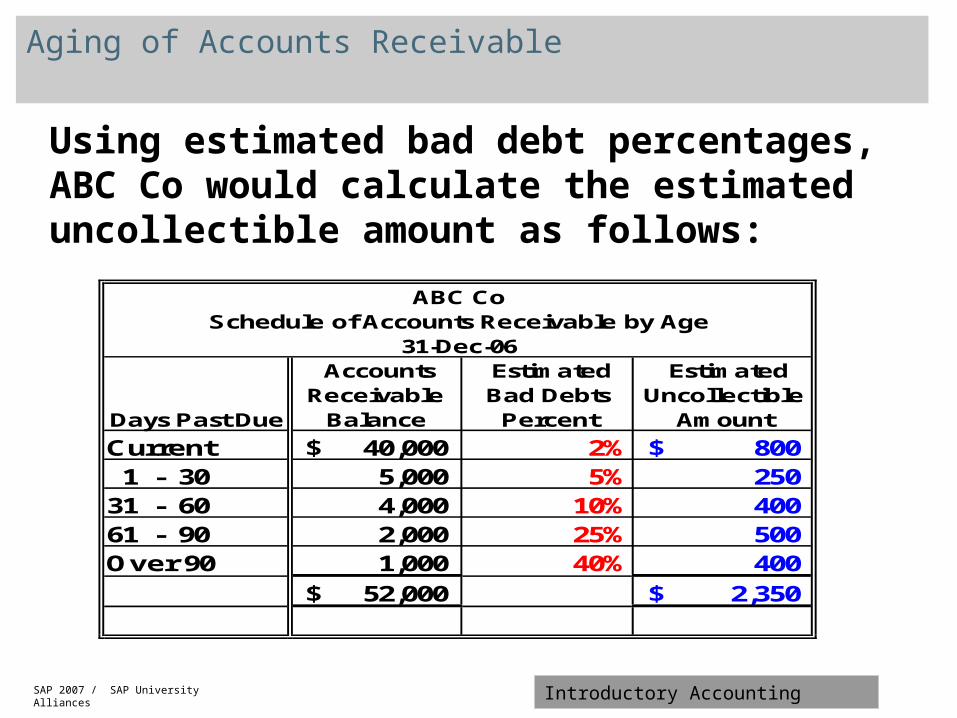

Using estimated bad debt percentages, ABC Co would calculate the estimated uncollectible amount as follows:

Aging of Accounts Receivable

ABC CoSchedule of Accounts Receivable by Age

31-Dec-06

Days Past Due

Accounts Receivable

Balance

Estimated Bad Debts

Percent

Estimated Uncollectible

Amount

Current 40,000$ 2% 800$ 1 - 30 5,000 5% 250 31 - 60 4,000 10% 400 61 - 90 2,000 25% 500 Over 90 1,000 40% 400

52,000$ 2,350$

SAP 2007 / SAP University Alliances Introductory Accounting

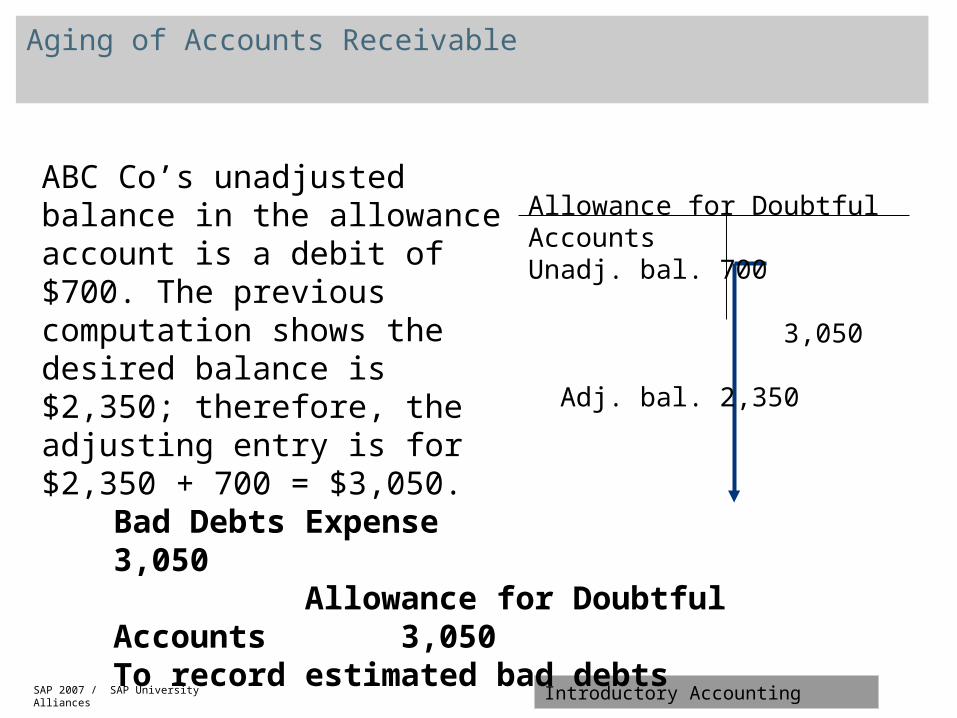

ABC Co’s unadjusted balance in the allowance account is a debit of $700. The previous computation shows the desired balance is $2,350; therefore, the adjusting entry is for $2,350 + 700 = $3,050.

Aging of Accounts Receivable

Bad Debts Expense 3,050 Allowance for Doubtful Accounts 3,050To record estimated bad debts

Allowance for Doubtful AccountsUnadj. bal. 700 3,050 Adj. bal. 2,350

SAP 2007 / SAP University Alliances Introductory Accounting

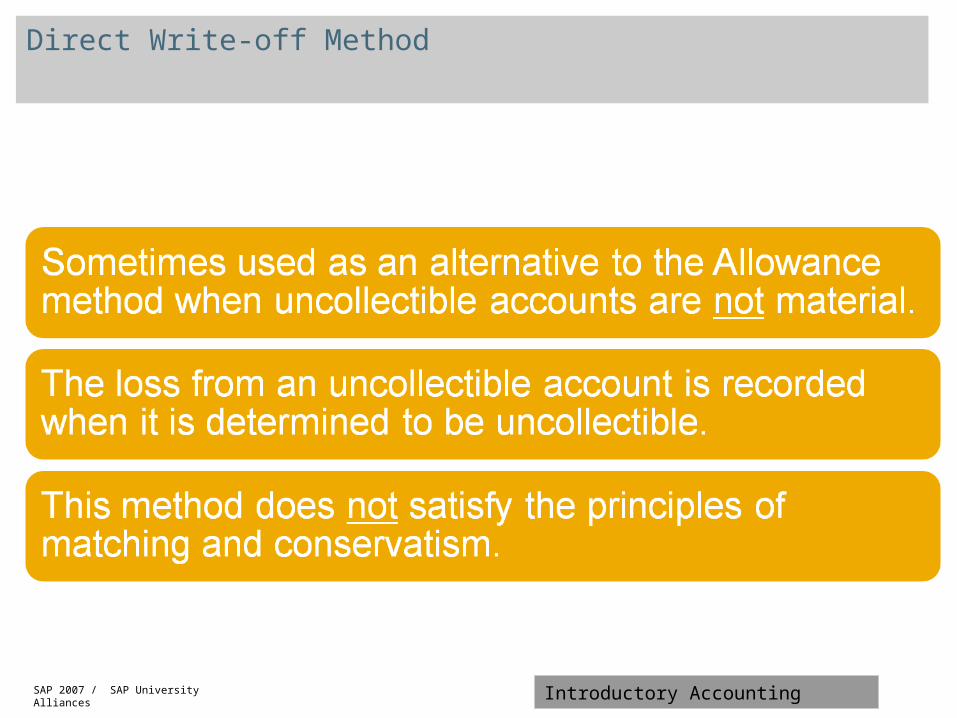

Direct Write-off Method

SAP 2007 / SAP University Alliances Introductory Accounting

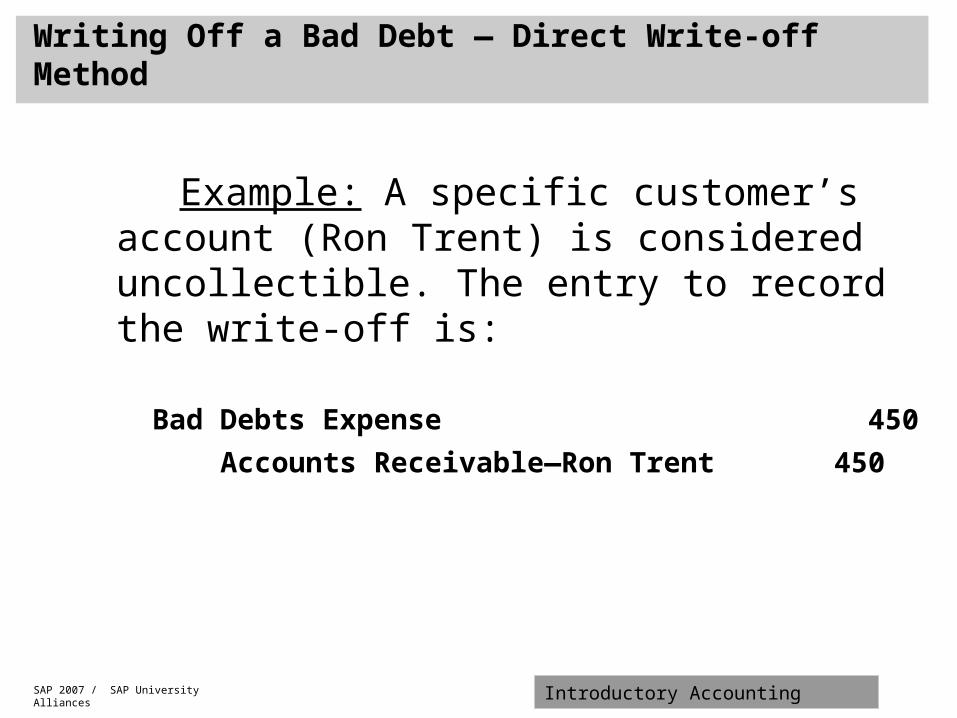

Example: A specific customer’s account (Ron Trent) is considered uncollectible. The entry to record the write-off is:

Bad Debts Expense 450

Accounts Receivable—Ron Trent 450

Writing Off a Bad Debt — Direct Write-off Method

SAP 2007 / SAP University Alliances Introductory Accounting

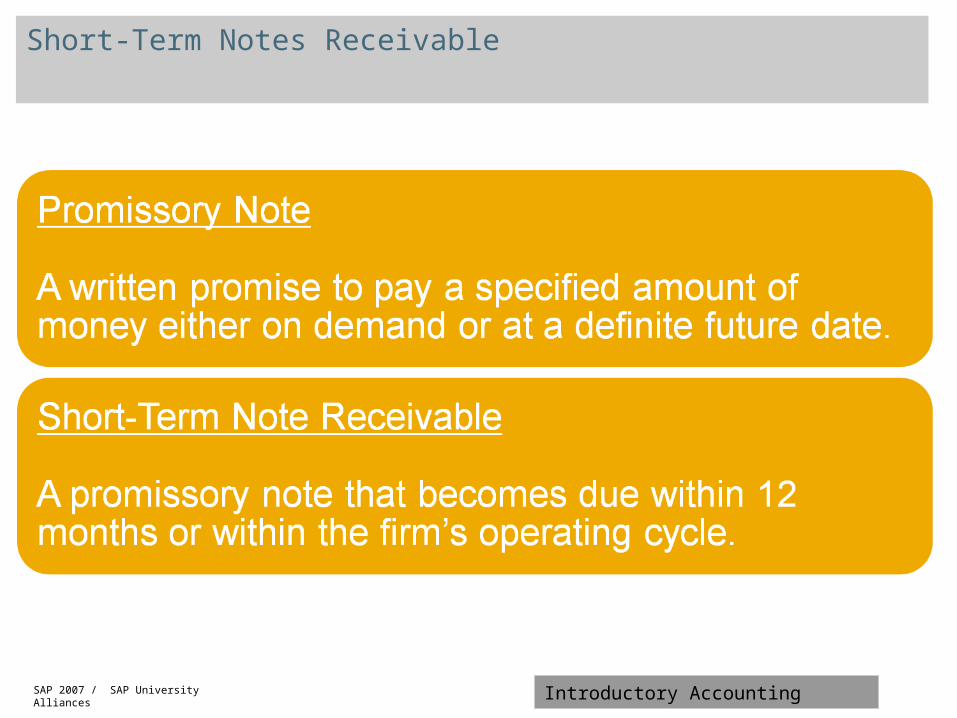

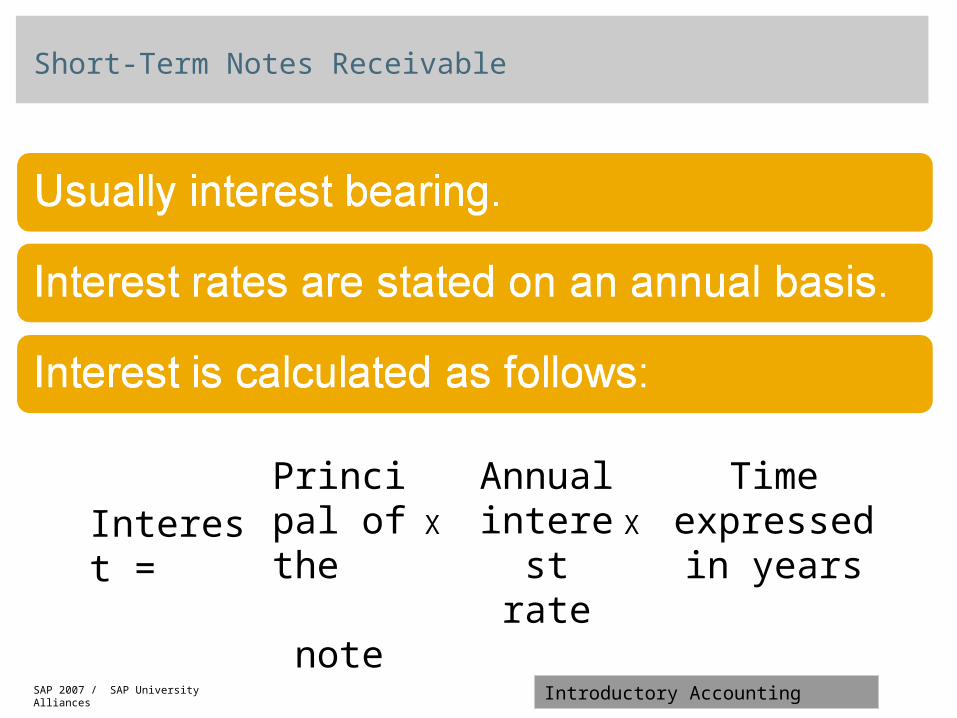

Short-Term Notes Receivable

SAP 2007 / SAP University Alliances Introductory Accounting

Interest =Principal of the note

Annual interest

rate

Time expressed

in yearsX X

Short-Term Notes Receivable

SAP 2007 / SAP University Alliances Introductory Accounting

Short-Term Notes Receivable

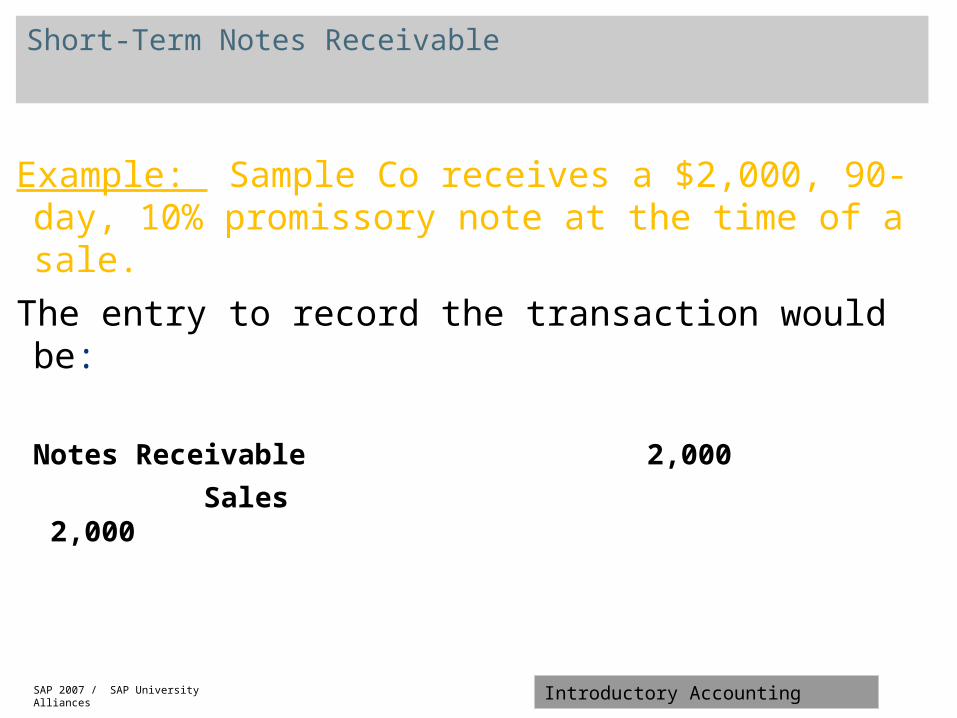

Example: Sample Co receives a $2,000, 90-day, 10% promissory note at the time of a sale.

The entry to record the transaction would be:

Notes Receivable 2,000

Sales 2,000

SAP 2007 / SAP University Alliances Introductory Accounting

Short-Term Notes Receivable

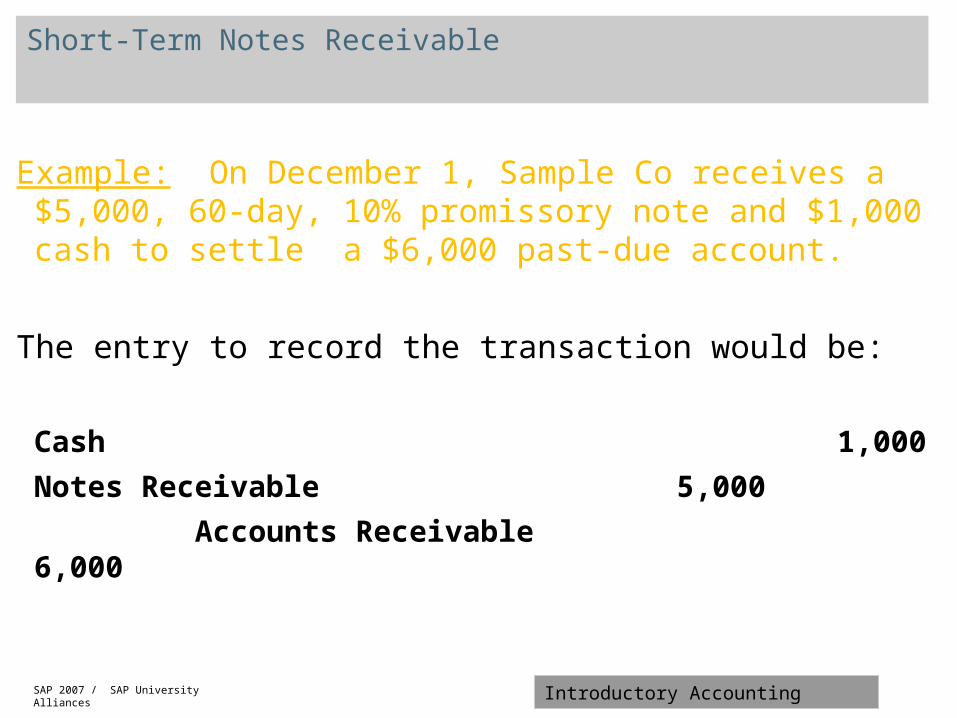

Example: On December 1, Sample Co receives a $5,000, 60-day, 10% promissory note and $1,000 cash to settle a $6,000 past-due account.

The entry to record the transaction would be:

Cash 1,000

Notes Receivable 5,000

Accounts Receivable 6,000

SAP 2007 / SAP University Alliances Introductory Accounting

Short-Term Notes Receivable

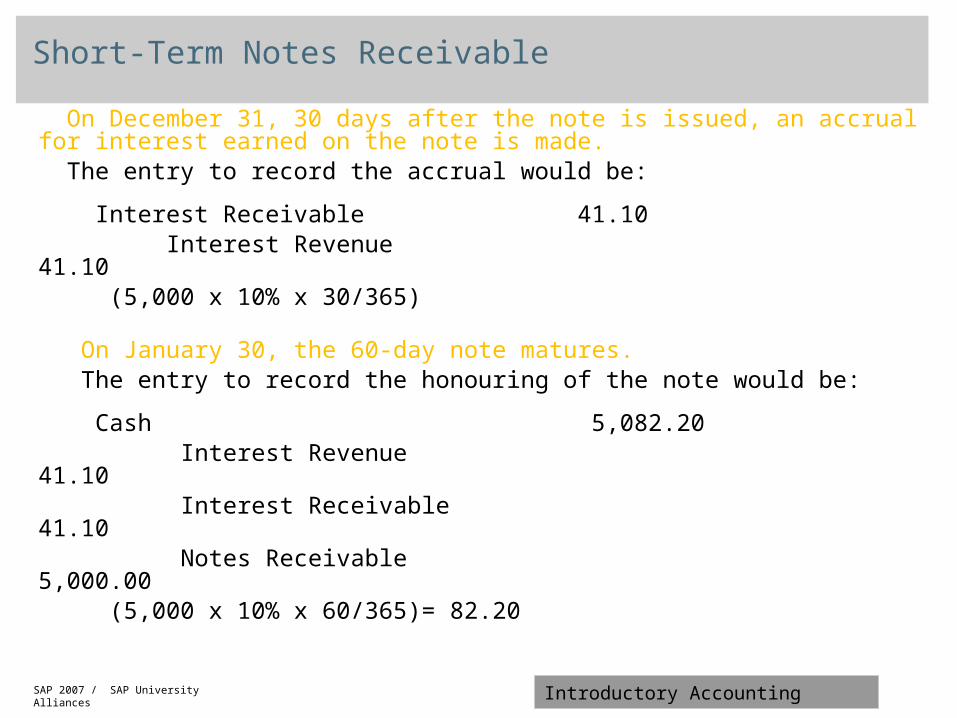

On December 31, 30 days after the note is issued, an accrual for interest earned on the note is made.

The entry to record the accrual would be:

Interest Receivable 41.10 Interest Revenue 41.10 (5,000 x 10% x 30/365) On January 30, the 60-day note matures. The entry to record the honouring of the note would be:

Cash 5,082.20 Interest Revenue 41.10 Interest Receivable 41.10 Notes Receivable 5,000.00 (5,000 x 10% x 60/365)= 82.20

SAP 2007 / SAP University Alliances Introductory Accounting

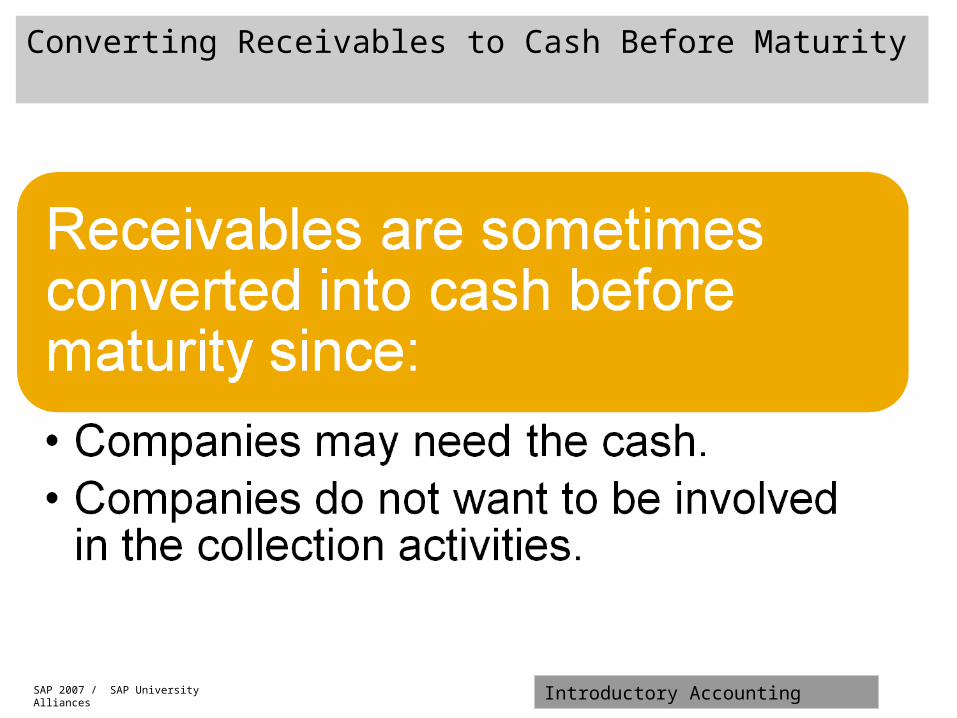

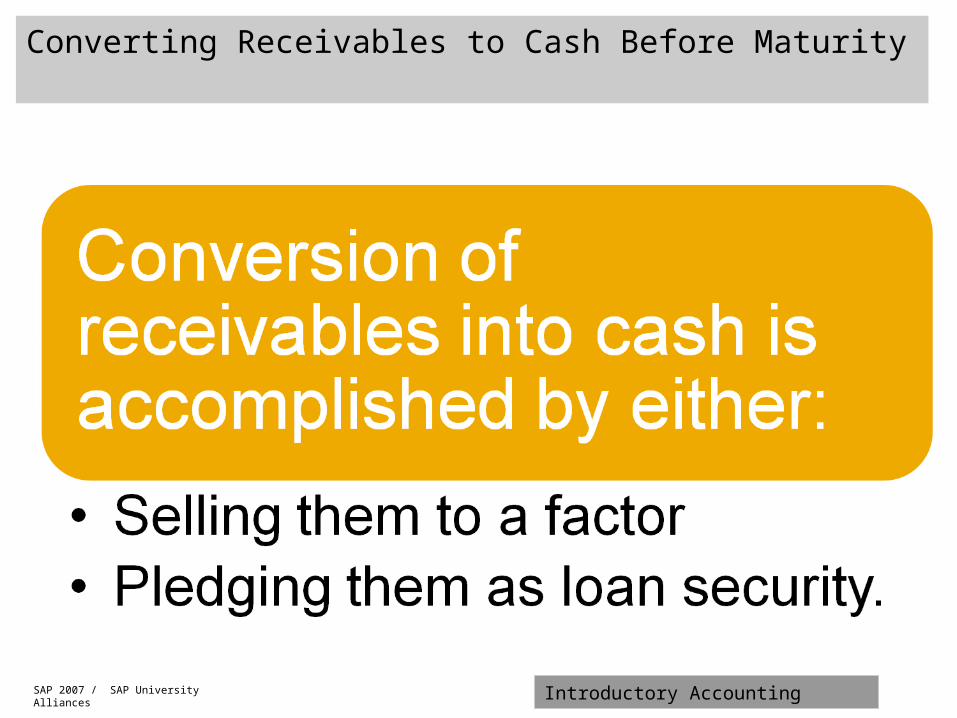

Converting Receivables to Cash Before Maturity

SAP 2007 / SAP University Alliances Introductory Accounting

Converting Receivables to Cash Before Maturity

SAP 2007 / SAP University Alliances Introductory Accounting

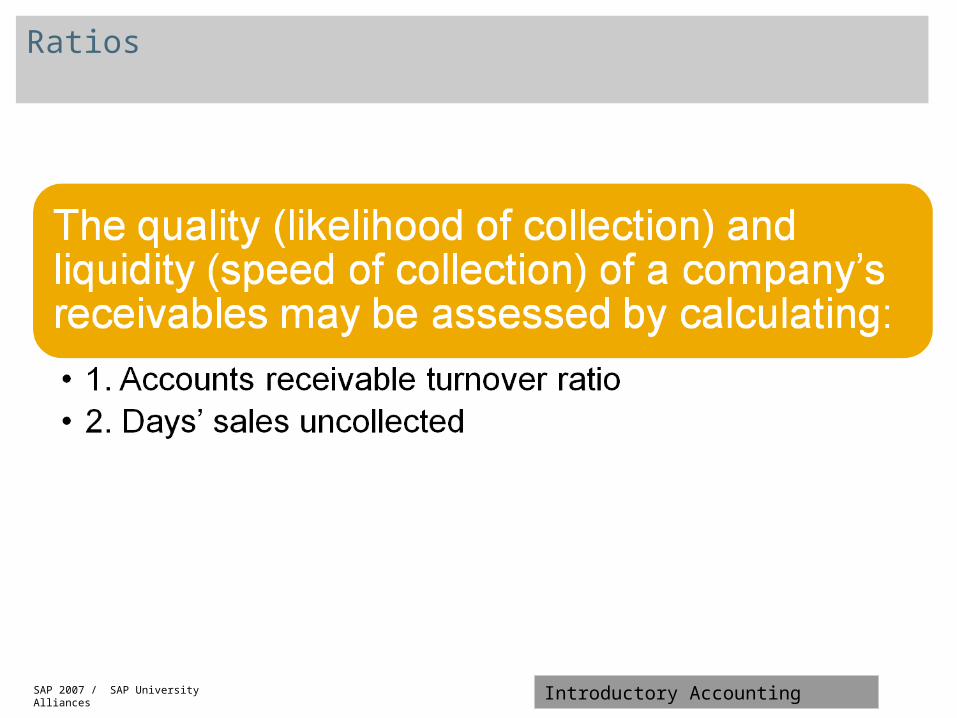

Ratios

SAP 2007 / SAP University Alliances Introductory Accounting

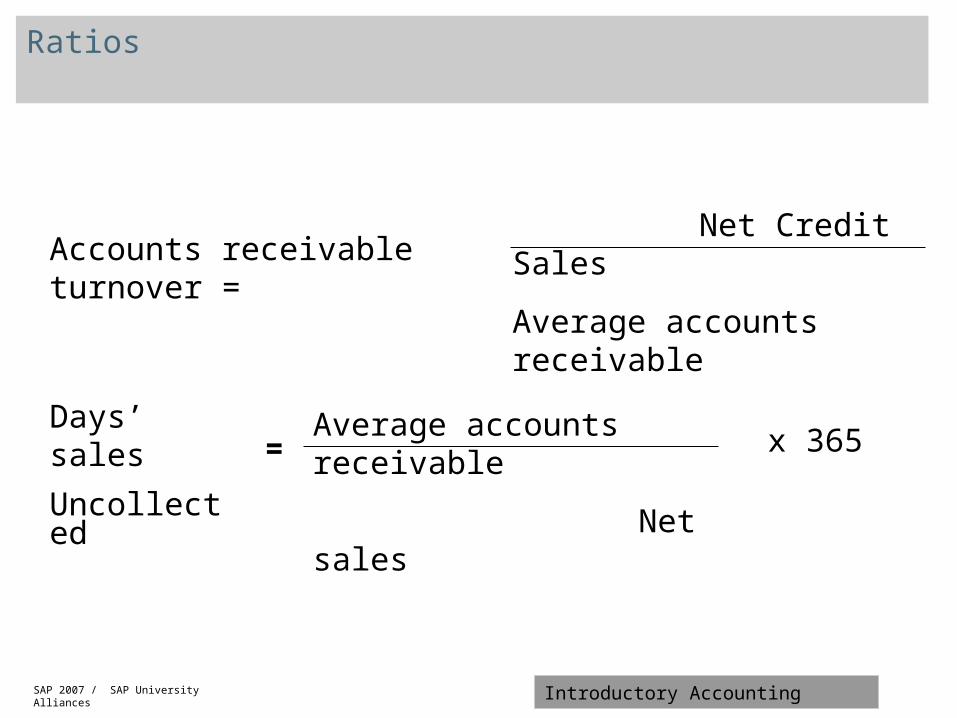

Ratios

Accounts receivable turnover = Net Credit Sales

Average accounts receivable

Days’ sales

Uncollected =Average accounts receivable

Net salesx 365

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

Accounts Payable

SAP 2007 / SAP University Alliances Introductory Accounting

Accounts Payable

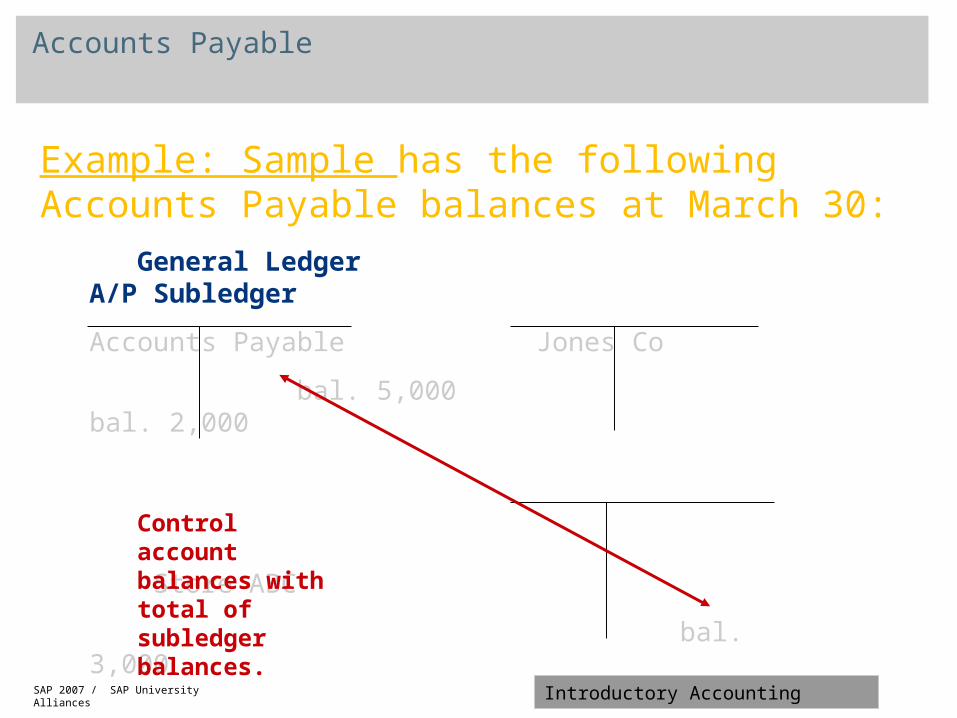

Example: Sample has the following Accounts Payable balances at March 30:

General Ledger A/P Subledger

Accounts Payable Jones Co

bal. 5,000 bal. 2,000

Store ABC

bal. 3,000

Total 5,000

Control account balances with total of subledger balances.

SAP 2007 / SAP University Alliances Introductory Accounting

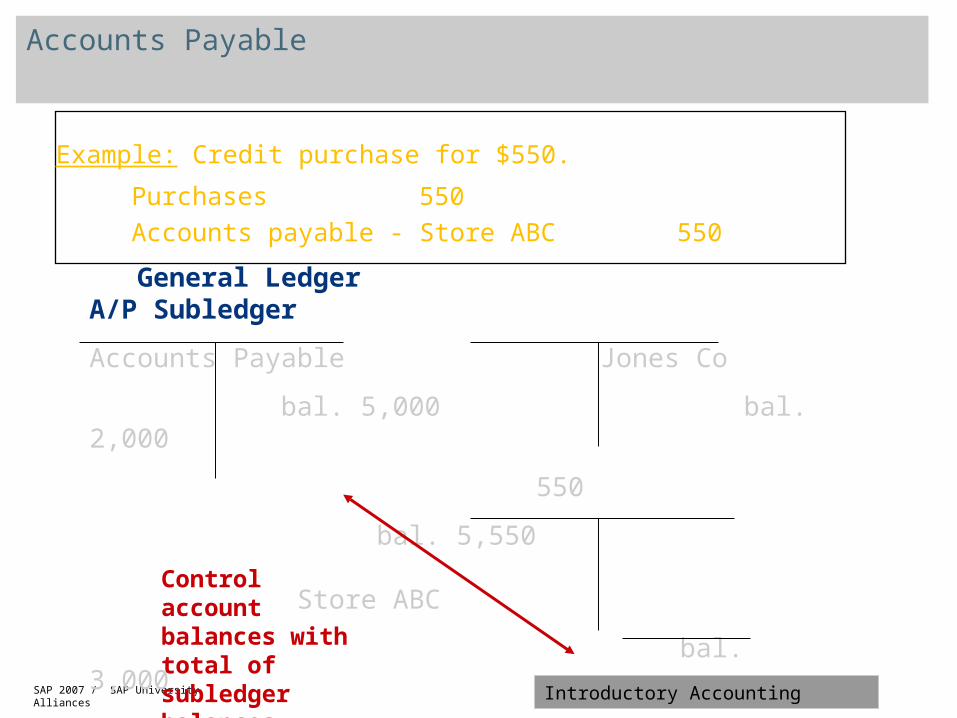

Accounts Payable

Example: Credit purchase for $550.

Purchases 550

Accounts payable - Store ABC 550

General Ledger A/P Subledger

Accounts Payable Jones Co

bal. 5,000 bal. 2,000

550

bal. 5,550 Store ABC

bal. 3,000

550

bal. 3,550 Total 5,550

Control account balances with total of subledger balances.

SAP 2007 / SAP University Alliances Introductory Accounting

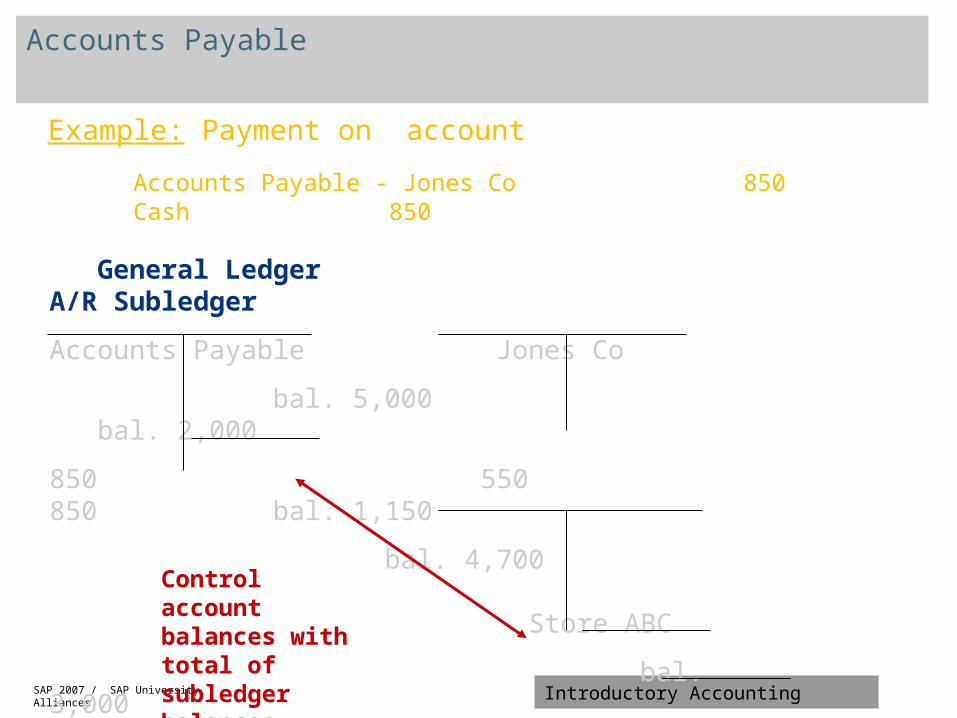

Accounts Payable

Example: Payment on account

Accounts Payable - Jones Co 850Cash 850

General Ledger A/R Subledger

Accounts Payable Jones Co

bal. 5,000 bal. 2,000

850 550 850 bal. 1,150

bal. 4,700 Store ABC

bal. 3,000

550

bal. 3,550 Total 4,700

Control account balances with total of subledger balances.

SAP 2007 / SAP University Alliances Introductory Accounting

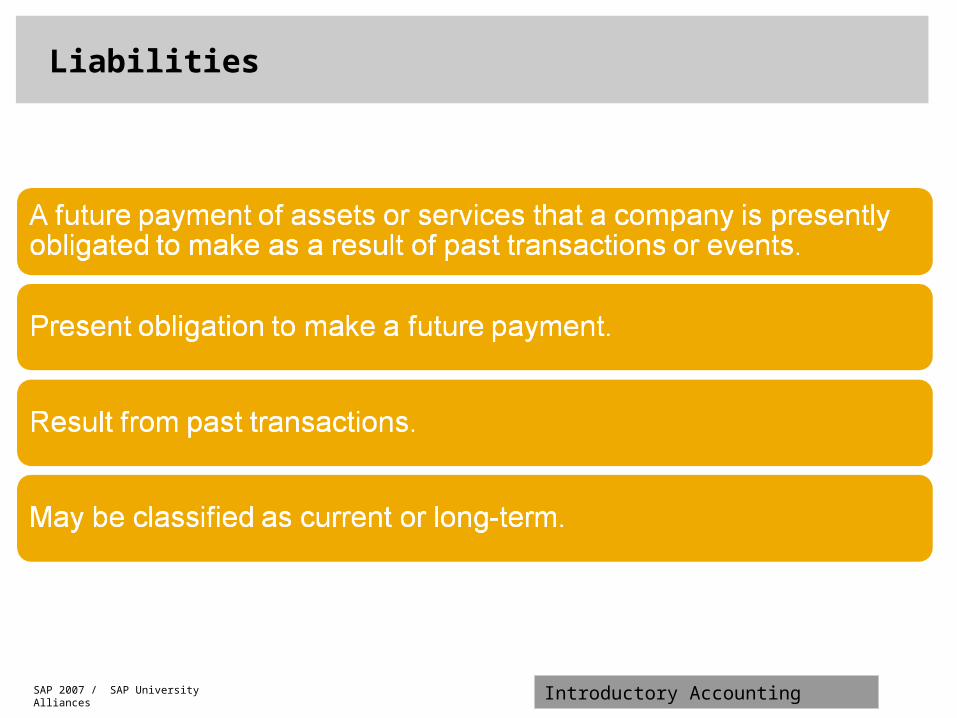

Liabilities

SAP 2007 / SAP University Alliances Introductory Accounting

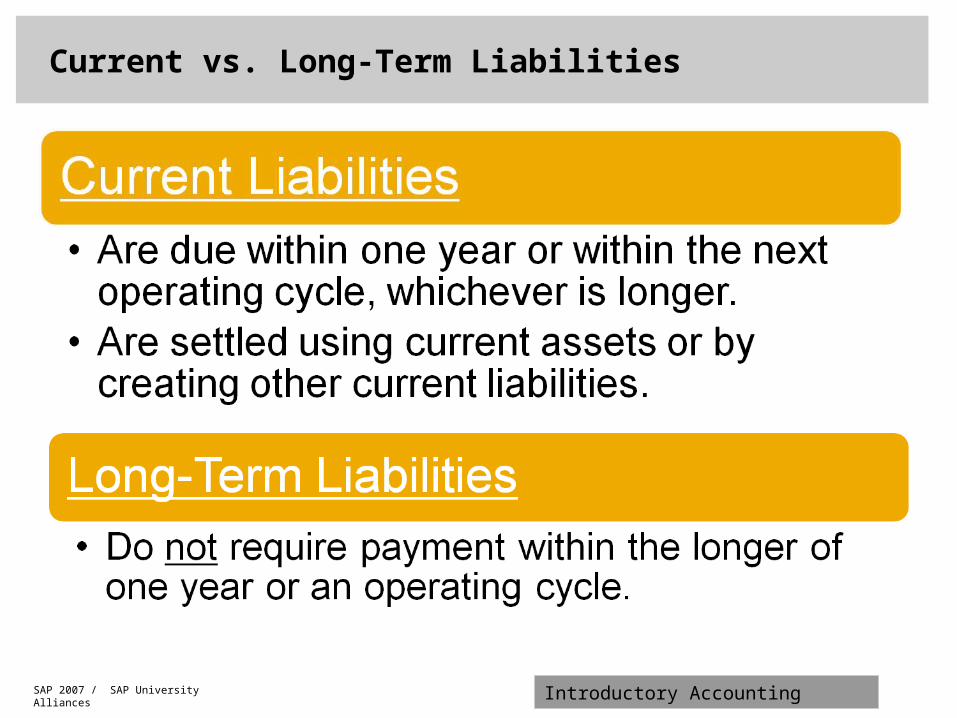

Current vs. Long-Term Liabilities

SAP 2007 / SAP University Alliances Introductory Accounting

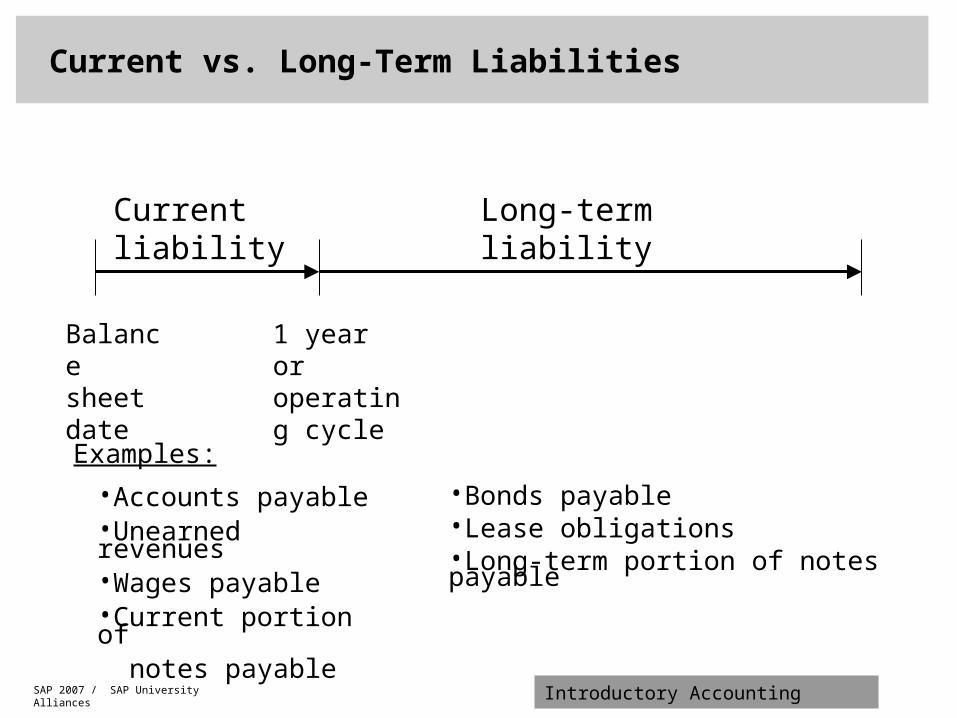

Current vs. Long-Term Liabilities

1 year or operating cycle

Balance sheet date

Current liability Long-term liability

•Accounts payable•Unearned revenues•Wages payable•Current portion of notes payable

•Bonds payable•Lease obligations•Long-term portion of notes payable

Examples:

SAP 2007 / SAP University Alliances Introductory Accounting

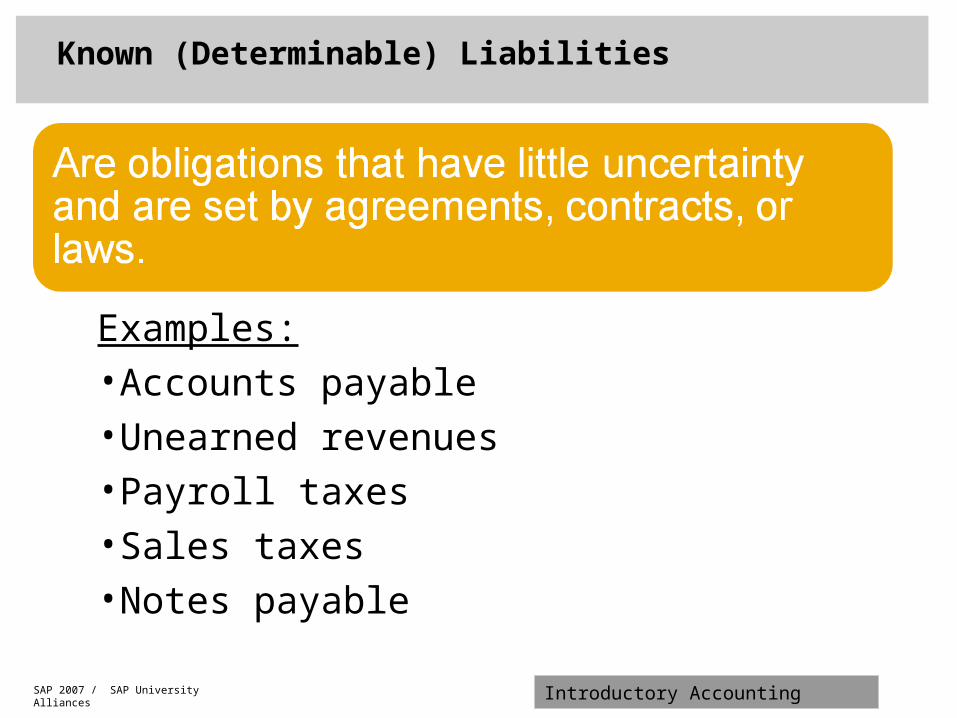

Known (Determinable) Liabilities

Examples:•Accounts payable•Unearned revenues•Payroll taxes•Sales taxes•Notes payable

SAP 2007 / SAP University Alliances Introductory Accounting

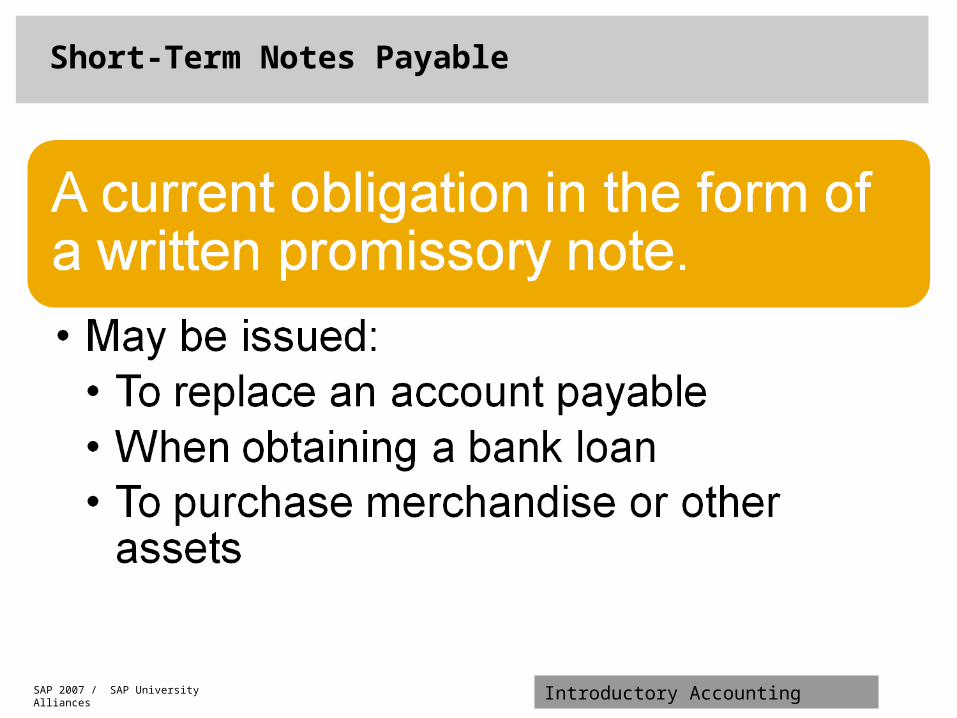

Short-Term Notes Payable

SAP 2007 / SAP University Alliances Introductory Accounting

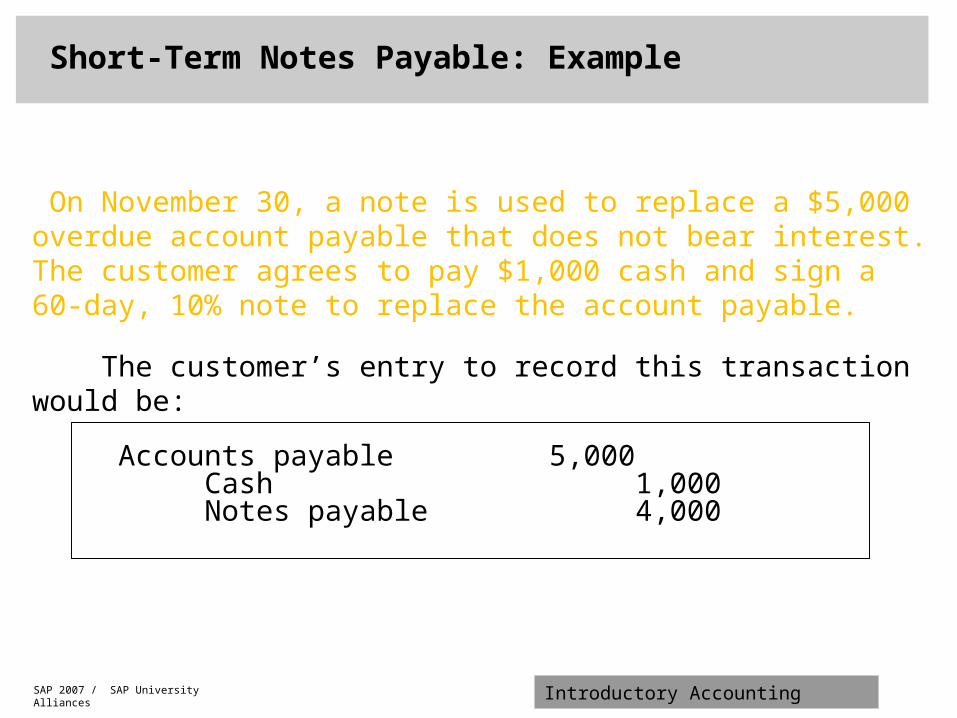

On November 30, a note is used to replace a $5,000 overdue account payable that does not bear interest. The customer agrees to pay $1,000 cash and sign a 60-day, 10% note to replace the account payable.

The customer’s entry to record this transaction would be:

Accounts payable 5,000Cash 1,000Notes payable 4,000

Short-Term Notes Payable: Example

SAP 2007 / SAP University Alliances Introductory Accounting

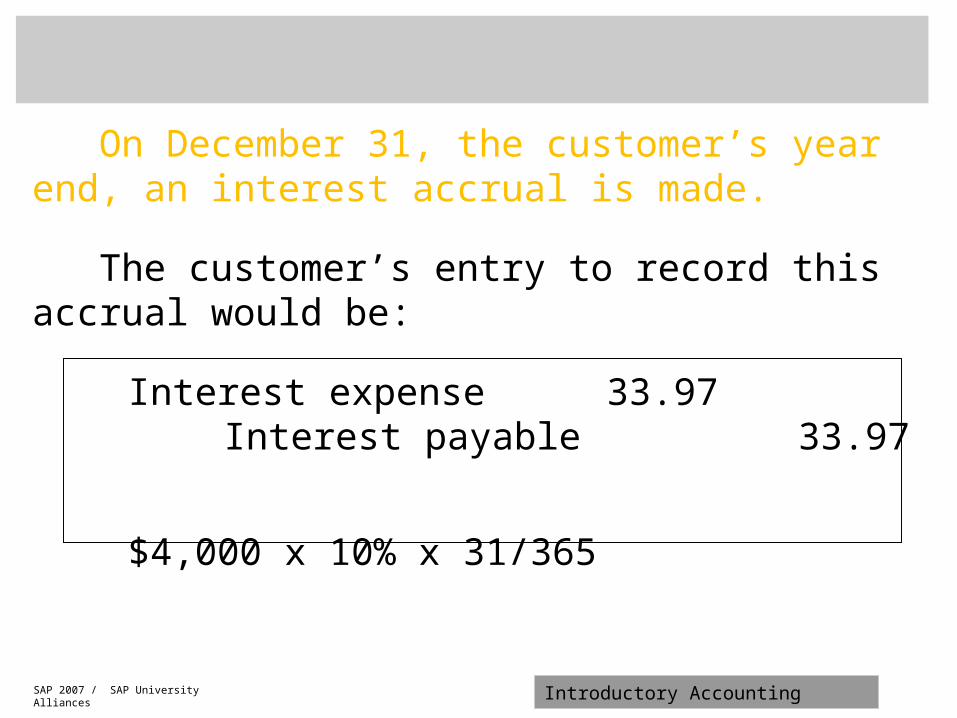

On December 31, the customer’s year end, an interest accrual is made.

The customer’s entry to record this accrual would be:

Interest expense 33.97Interest payable 33.97

$4,000 x 10% x 31/365

SAP 2007 / SAP University Alliances Introductory Accounting

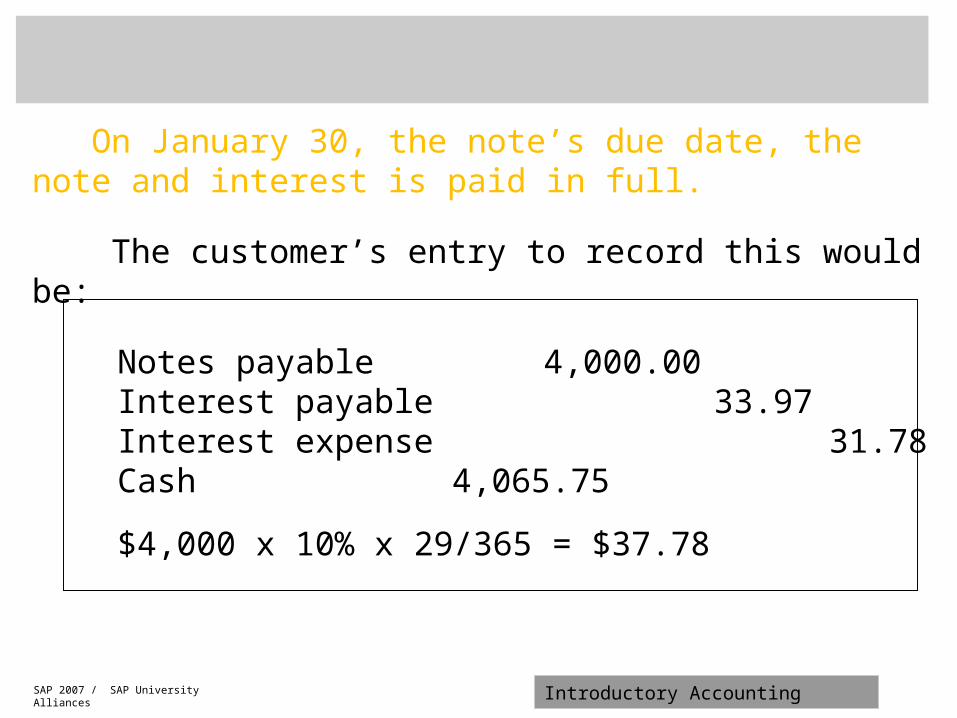

On January 30, the note’s due date, the note and interest is paid in full.

The customer’s entry to record this would be:

Notes payable 4,000.00Interest payable 33.97Interest expense 31.78

Cash 4,065.75

$4,000 x 10% x 29/365 = $37.78