Embed Size (px)

Citation preview

ACCOUNTINGACCOUNTING PRINCIPLESPRINCIPLES

Third Canadian EditionThird Canadian Edition

Prepared by: Prepared by: Keri Norrie, Camosun CollegeKeri Norrie, Camosun College

BUDGETARY PLANNINGBUDGETARY PLANNING

CHAPTER 21CHAPTER 21

BUDGETINGBUDGETING BASICSBASICS BUDGETINGBUDGETING BASICSBASICS

AA budgetbudget is a formal written statement of is a formal written statement of management’s plans, expressed in financial terms, for management’s plans, expressed in financial terms, for a specified future time period. The main benefits of a specified future time period. The main benefits of budgeting include:budgeting include:• all levels of management mustall levels of management must planplan ahead and ahead and

formalize future goals on a recurring basisformalize future goals on a recurring basis• providesprovides definite objectivesdefinite objectives for evaluating performance for evaluating performance • creates ancreates an early warning systemearly warning system for potential problemsfor potential problems• easier toeasier to coordinatecoordinate activities within the businessactivities within the business• greater managementgreater management awarenessawareness of the company’s of the company’s

overall operations andoverall operations and motivatesmotivates personnel to meet personnel to meet planned objectivesplanned objectives

BUDGETING BASICS BUDGETING BASICS Essentials of Effective BudgetingEssentials of Effective Budgeting

BUDGETING BASICS BUDGETING BASICS Essentials of Effective BudgetingEssentials of Effective Budgeting

1.1. Budgeting processBudgeting process

• Collect past data from each organizational Collect past data from each organizational unit of the company as a starting point for unit of the company as a starting point for developing future budget goals.developing future budget goals.

• Develop the budget based on a Develop the budget based on a sales sales forecastforecast that reflects expected industry and that reflects expected industry and economic conditions, with input from sales economic conditions, with input from sales personnel and top management. personnel and top management.

• Assign responsibility for coordinating the Assign responsibility for coordinating the budget preparation, usually to abudget preparation, usually to a budget budget committeecommittee..

BUDGETING BASICS BUDGETING BASICS Essentials of Effective BudgetingEssentials of Effective Budgeting

BUDGETING BASICS BUDGETING BASICS Essentials of Effective BudgetingEssentials of Effective Budgeting

2.2. Budgeting and Human Behaviour Budgeting and Human Behaviour • Each level of management should be invited Each level of management should be invited

to participate in developing the budget.to participate in developing the budget.• Agreement should be reached on a budget Agreement should be reached on a budget

that management considers that management considers fair and fair and achievableachievable..

• The budget should provide the management The budget should provide the management tool for tool for performance evaluationperformance evaluation. .

3.3. Length of the Budget PeriodLength of the Budget Period

• The budget period should be long enough to The budget period should be long enough to provide an attainable goal under normal provide an attainable goal under normal business conditions, usually one year.business conditions, usually one year.

BUDGETING BASICS BUDGETING BASICS Essentials of Effective BudgetingEssentials of Effective Budgeting

BUDGETING BASICS BUDGETING BASICS Essentials of Effective BudgetingEssentials of Effective Budgeting

4.4. Budgeting and Long-Range Planning Budgeting and Long-Range Planning • Budgeting and long-range planning are not the Budgeting and long-range planning are not the

same. Important differences include: same. Important differences include: Time period involved.Time period involved. Budgets are usually Budgets are usually

prepared for an one year or shorter period prepared for an one year or shorter period while long-range plans cover a period of at while long-range plans cover a period of at least five years.least five years.

Emphasis.Emphasis. Achieving specific short-term Achieving specific short-term goals for budgeting compared to developing goals for budgeting compared to developing long-term goals and strategies.long-term goals and strategies.

Amount of detail presented.Amount of detail presented. Budgets are very Budgets are very detailed in order to provide a basis for control detailed in order to provide a basis for control while long-range plans are considerably less while long-range plans are considerably less detailed.detailed.

THE MASTER BUDGET THE MASTER BUDGET THE MASTER BUDGET THE MASTER BUDGET

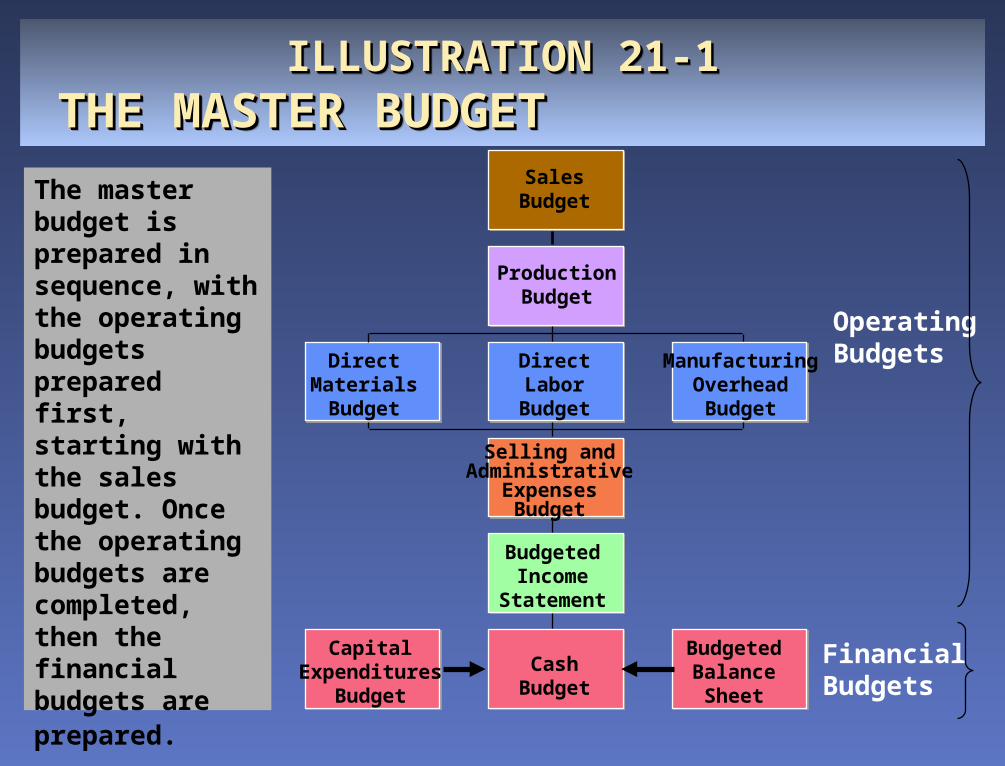

TheThe master budgetmaster budget is a set of interrelated budgets is a set of interrelated budgets that constitute a plan of action for a specified that constitute a plan of action for a specified time period. The master budget contains two time period. The master budget contains two classes of budgets:classes of budgets:

• Operating budgetsOperating budgets are the individual budgets are the individual budgets (sales budget, production budget, direct materials (sales budget, production budget, direct materials budget, direct labour budget, manufacturing budget, direct labour budget, manufacturing overhead budget, and selling and administrative overhead budget, and selling and administrative expenses budget) that result in the preparation of expenses budget) that result in the preparation of thethe budgeted income statementbudgeted income statement. .

• Financial budgetsFinancial budgets include the capital include the capital expenditures budget, the cash budget, and the expenditures budget, the cash budget, and the budgeted balance sheet. These budgets focus budgeted balance sheet. These budgets focus primarily on theprimarily on the cash resources needed to fund cash resources needed to fund expected operations and capital expendituresexpected operations and capital expenditures..

ILLUSTRATION 21-1ILLUSTRATION 21-1THE MASTER BUDGETTHE MASTER BUDGET

ILLUSTRATION 21-1ILLUSTRATION 21-1THE MASTER BUDGETTHE MASTER BUDGET

SalesBudget

ProductionBudget

DirectMaterialsBudget

DirectLabor

Budget

ManufacturingOverhead

Budget

Selling andAdministrative

ExpensesBudget

BudgetedIncome

Statement

CapitalExpenditures

Budget

CashBudget

BudgetedBalance

Sheet

Operating Budgets

Financial Budgets

The master budget is prepared in sequence, with the operating budgets prepared first, starting with the sales budget. Once the operating budgets are completed, then the financial budgets are prepared.

ILLUSTRATION 21-2ILLUSTRATION 21-2PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETS

Sales BudgetSales Budget

ILLUSTRATION 21-2ILLUSTRATION 21-2PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETS

Sales BudgetSales Budget

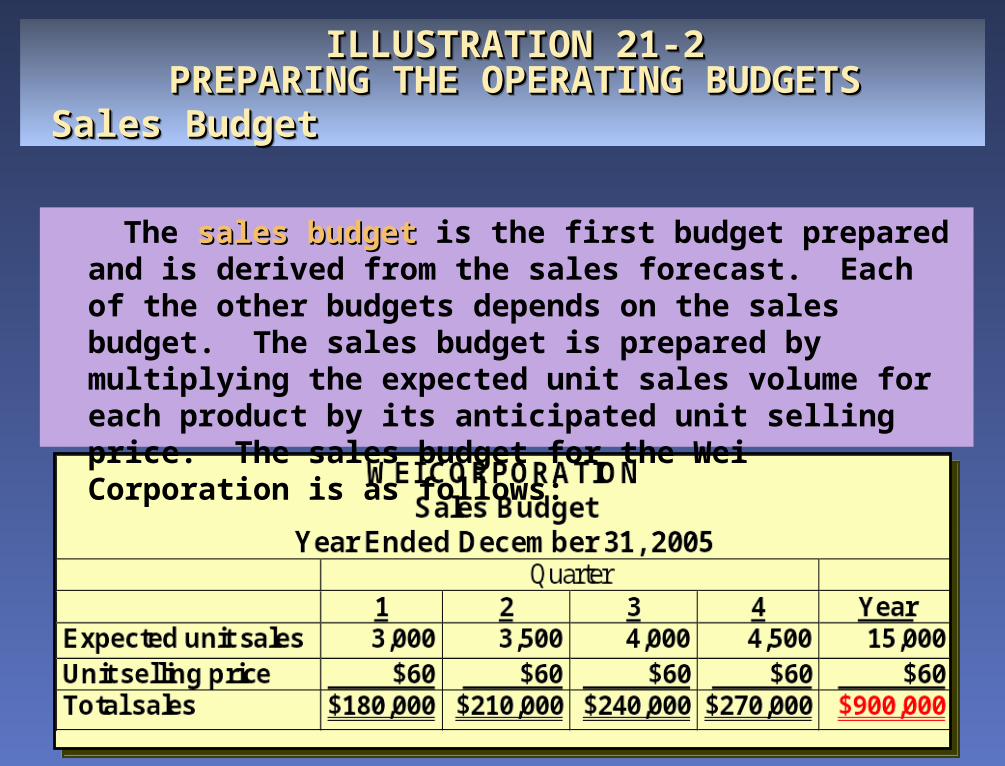

The sales budgetsales budget is the first budget prepared and is derived from the sales forecast. Each of the other budgets depends on the sales budget. The sales budget is prepared by multiplying the expected unit sales volume for each product by its anticipated unit selling price. The sales budget for the Wei Corporation is as follows:

Per sales budget

ILLUSTRATION 21-4ILLUSTRATION 21-4PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETS

Production BudgetProduction Budget

ILLUSTRATION 21-4ILLUSTRATION 21-4PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETS

Production BudgetProduction Budget

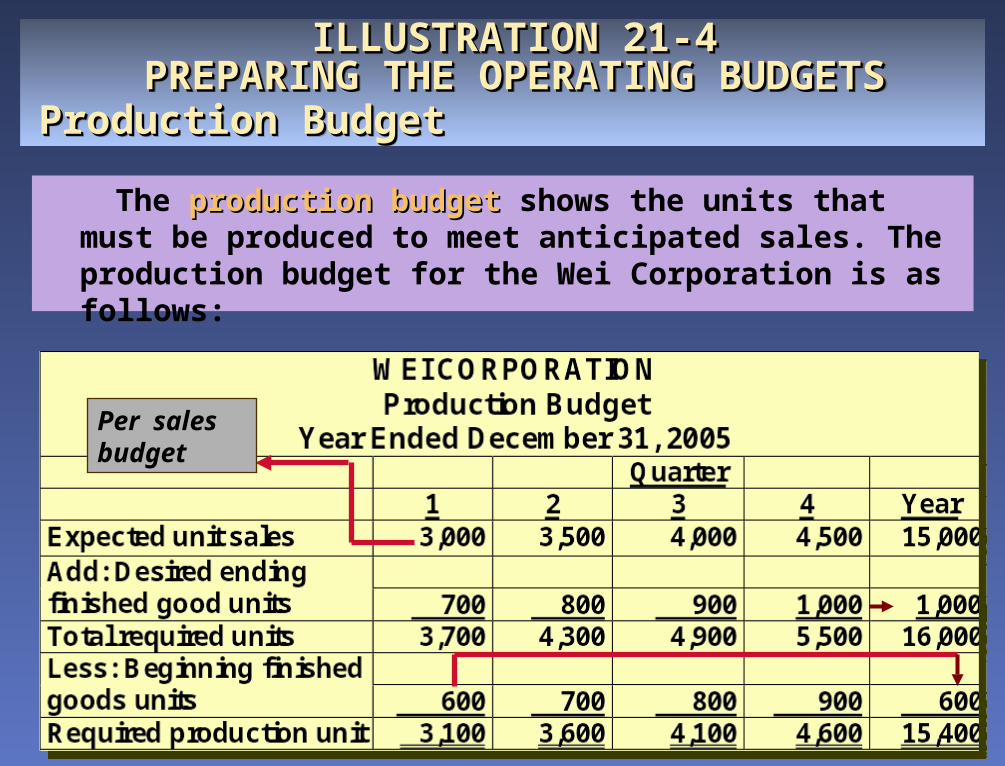

The production budgetproduction budget shows the units that must be produced to meet anticipated sales. The production budget for the Wei Corporation is as follows:

from production budget

ILLUSTRATION 21-6ILLUSTRATION 21-6PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETSDirect Materials BudgetDirect Materials Budget

ILLUSTRATION 21-6ILLUSTRATION 21-6PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETSDirect Materials BudgetDirect Materials Budget

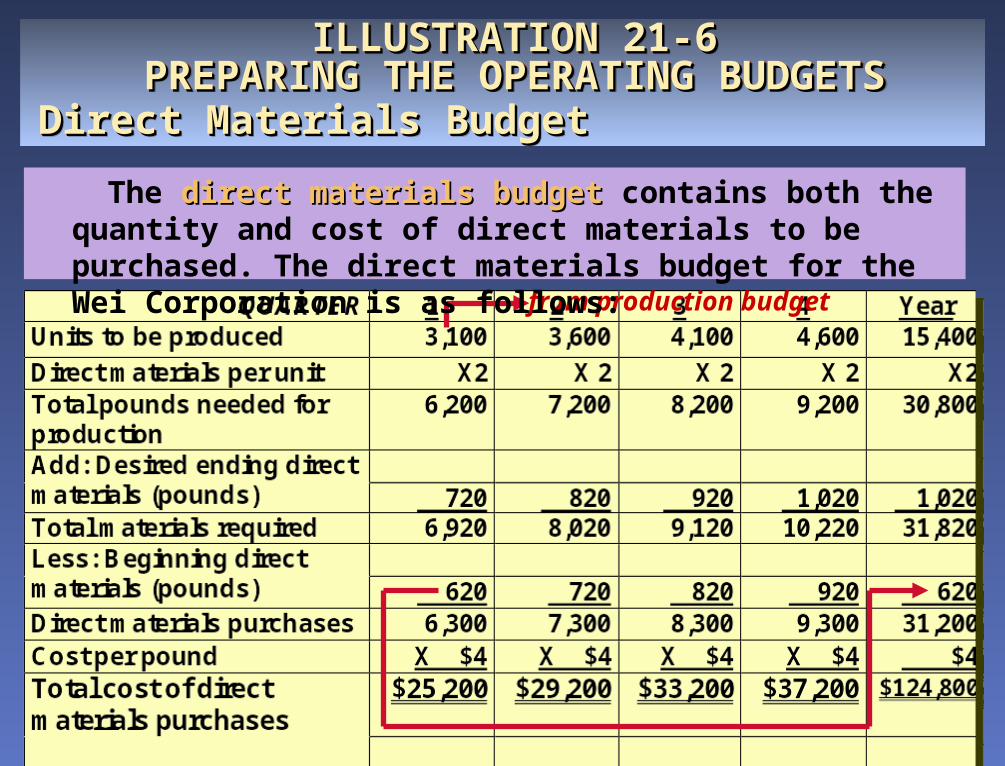

The direct materials budgetdirect materials budget contains both the quantity and cost of direct materials to be purchased. The direct materials budget for the Wei Corporation is as follows:

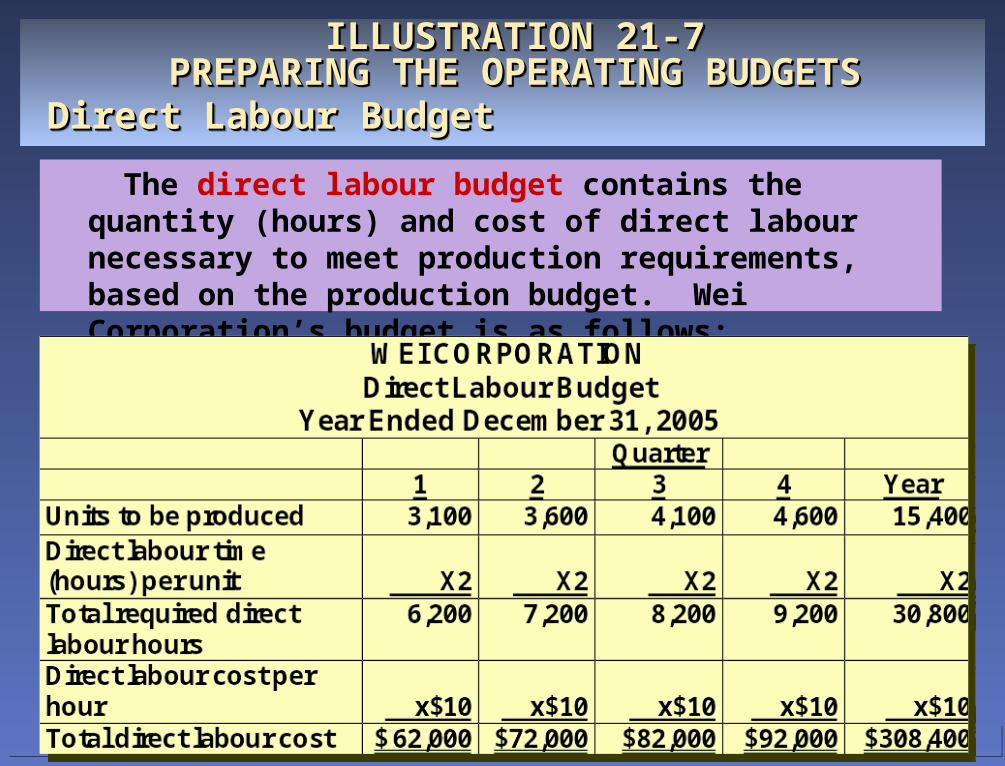

ILLUSTRATION 21-7ILLUSTRATION 21-7PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETS

Direct Labour BudgetDirect Labour Budget

ILLUSTRATION 21-7ILLUSTRATION 21-7PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETS

Direct Labour BudgetDirect Labour Budget The direct labour budget contains the quantity (hours)

and cost of direct labour necessary to meet production requirements, based on the production budget. Wei Corporation’s budget is as follows:

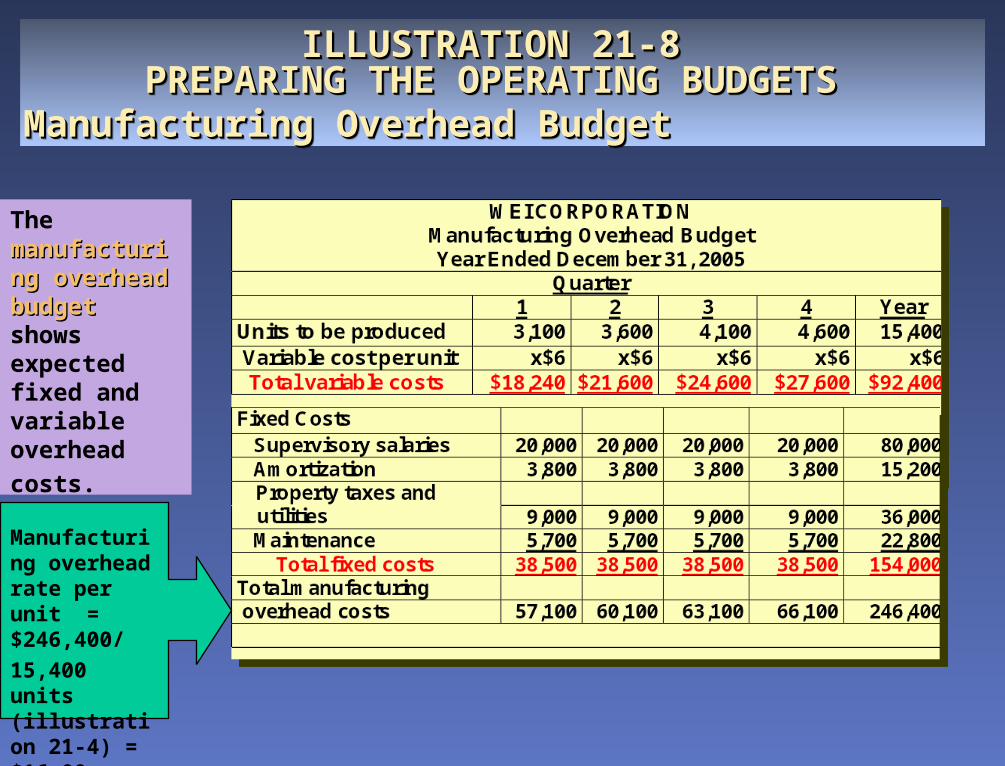

ILLUSTRATION 21-8ILLUSTRATION 21-8PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETS

Manufacturing Overhead BudgetManufacturing Overhead Budget

ILLUSTRATION 21-8ILLUSTRATION 21-8PREPARING THE OPERATING BUDGETSPREPARING THE OPERATING BUDGETS

Manufacturing Overhead BudgetManufacturing Overhead Budget

The manufacturing manufacturing overhead overhead budgetbudget shows expected fixed and variable overhead

costs.

Manufacturing overhead rate per unit = $246,400/

15,400 units (illustration 21-4) = $16.00

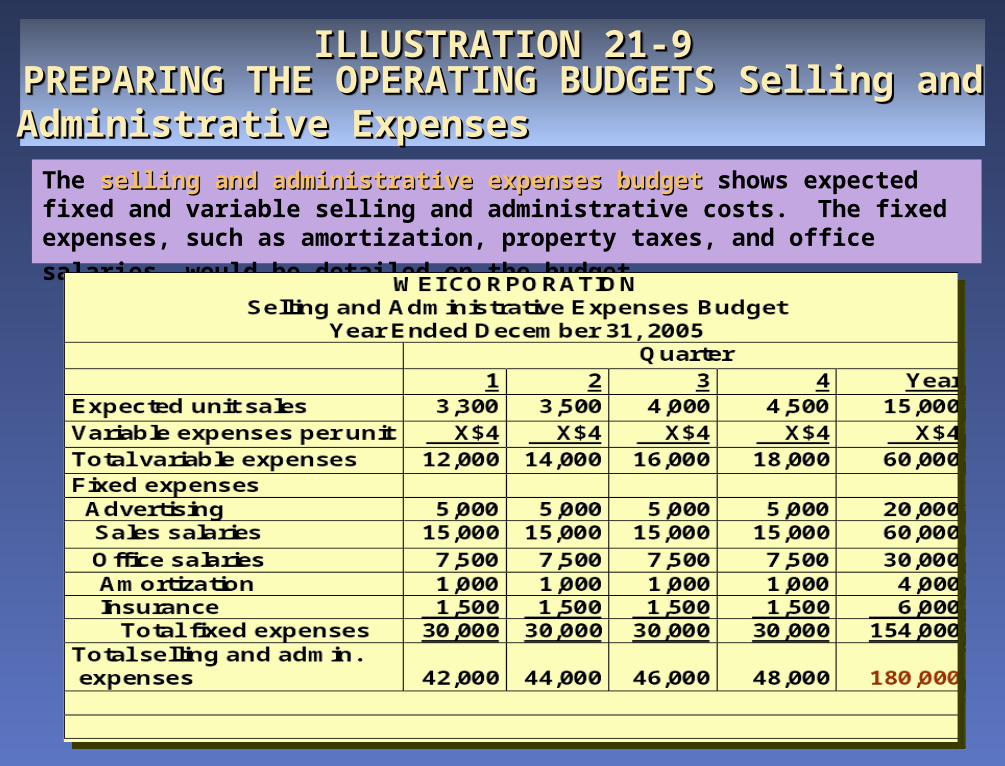

ILLUSTRATION 21-9ILLUSTRATION 21-9PREPARING THE OPERATING BUDGETS Selling and PREPARING THE OPERATING BUDGETS Selling and

Administrative ExpensesAdministrative Expenses

ILLUSTRATION 21-9ILLUSTRATION 21-9PREPARING THE OPERATING BUDGETS Selling and PREPARING THE OPERATING BUDGETS Selling and

Administrative ExpensesAdministrative Expenses The selling and administrative expenses budgetselling and administrative expenses budget shows expected fixed and variable selling and administrative costs. The fixed expenses, such as amortization, property taxes, and office salaries, would be detailed on the

budget.

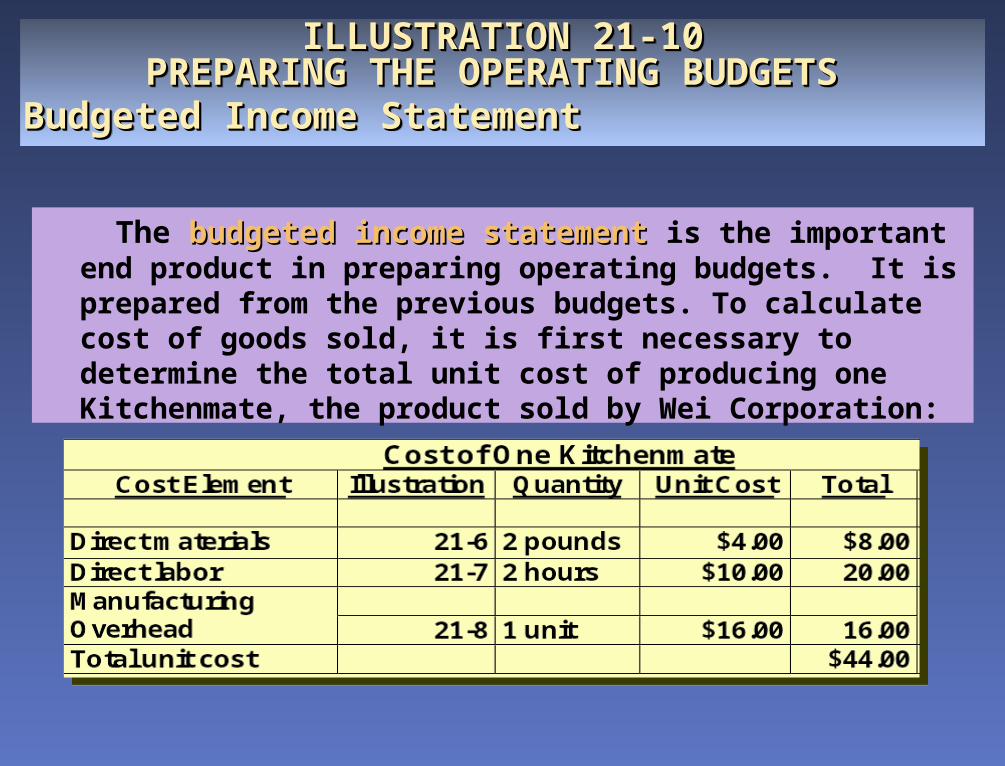

ILLUSTRATION 21-10ILLUSTRATION 21-10PREPARING THE OPERATING BUDGETS PREPARING THE OPERATING BUDGETS

Budgeted Income StatementBudgeted Income Statement

ILLUSTRATION 21-10ILLUSTRATION 21-10PREPARING THE OPERATING BUDGETS PREPARING THE OPERATING BUDGETS

Budgeted Income StatementBudgeted Income Statement

The budgeted income statementbudgeted income statement is the important end product in preparing operating budgets. It is prepared from the previous budgets. To calculate cost of goods sold, it is first necessary to determine the total unit cost of producing one Kitchenmate, the product sold by Wei Corporation:

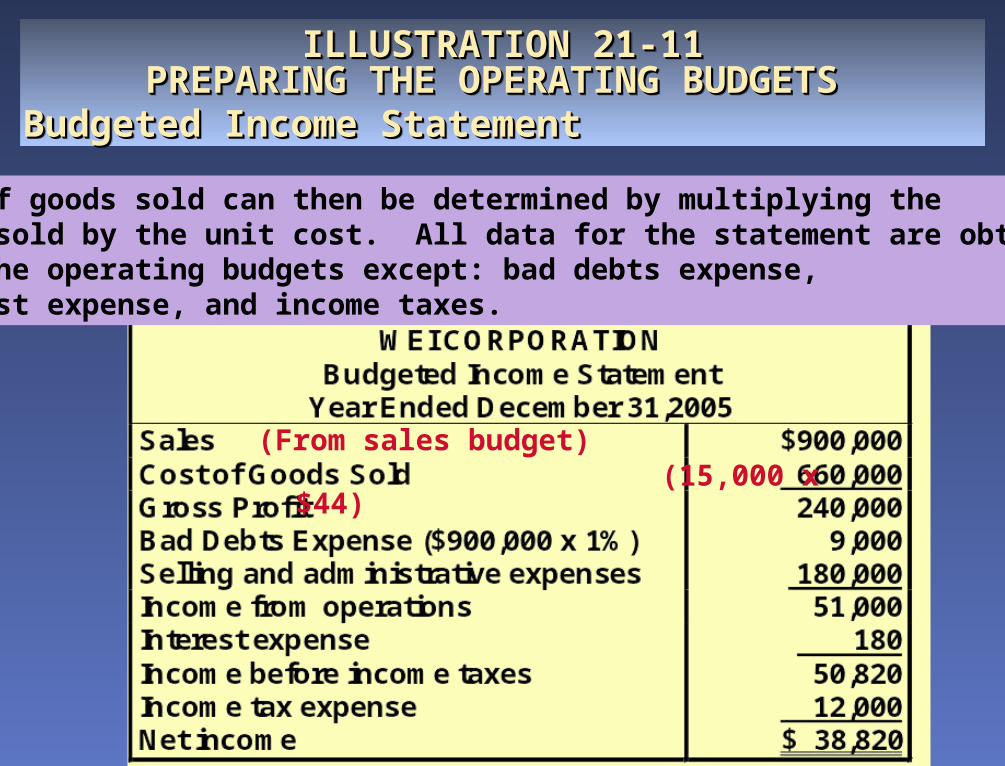

ILLUSTRATION 21-11ILLUSTRATION 21-11PREPARING THE OPERATING BUDGETS PREPARING THE OPERATING BUDGETS

Budgeted Income StatementBudgeted Income Statement

ILLUSTRATION 21-11ILLUSTRATION 21-11PREPARING THE OPERATING BUDGETS PREPARING THE OPERATING BUDGETS

Budgeted Income StatementBudgeted Income Statement

Cost of goods sold can then be determined by multiplying theunits sold by the unit cost. All data for the statement are obtainedfrom the operating budgets except: bad debts expense, interest expense, and income taxes.

(From sales budget) (15,000 x $44)

ILLUSTRATION 21-12ILLUSTRATION 21-12PREPARING THE FINANCIAL BUDGETS PREPARING THE FINANCIAL BUDGETS

Capital Expenditures BudgetCapital Expenditures Budget

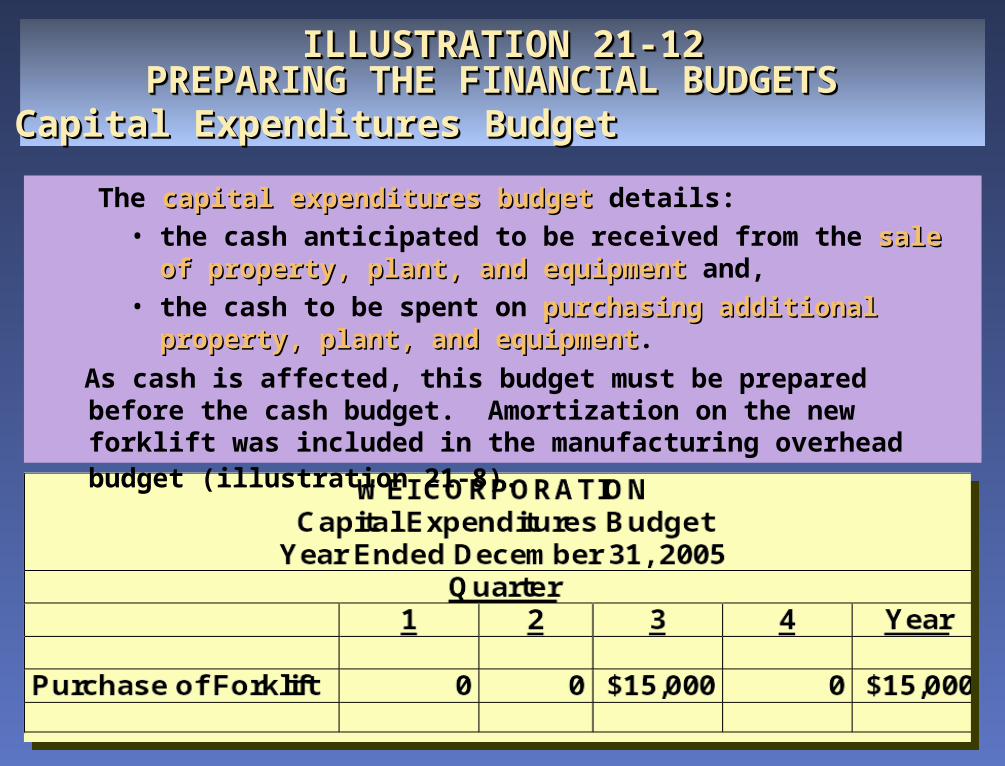

ILLUSTRATION 21-12ILLUSTRATION 21-12PREPARING THE FINANCIAL BUDGETS PREPARING THE FINANCIAL BUDGETS

Capital Expenditures BudgetCapital Expenditures Budget

The capital expenditures budgetcapital expenditures budget details:• the cash anticipated to be received from the sale of property, sale of property,

plant, and equipmentplant, and equipment and,• the cash to be spent on purchasing additional property, plant, purchasing additional property, plant,

and equipmentand equipment.

As cash is affected, this budget must be prepared before the cash budget. Amortization on the new forklift was included in the manufacturing overhead budget (illustration 21-8).

ILLUSTRATION 21-13ILLUSTRATION 21-13PREPARING THE FINANCIAL BUDGETS PREPARING THE FINANCIAL BUDGETS

Cash BudgetCash Budget

ILLUSTRATION 21-13ILLUSTRATION 21-13PREPARING THE FINANCIAL BUDGETS PREPARING THE FINANCIAL BUDGETS

Cash BudgetCash Budget

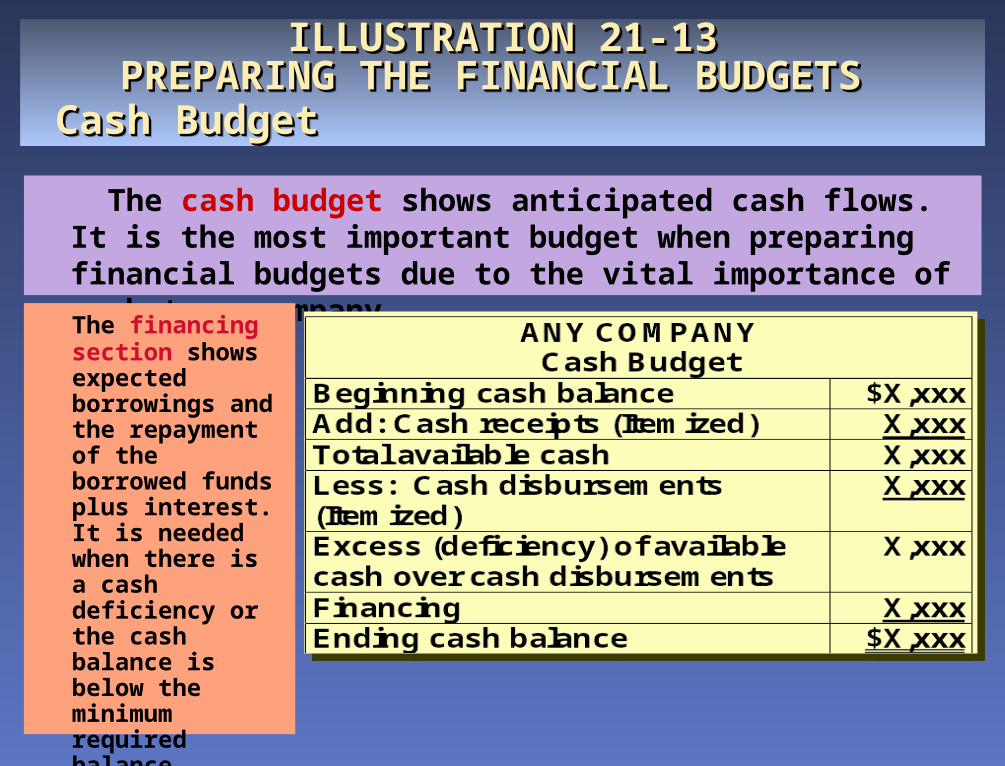

The cash budget shows anticipated cash flows. It is the most important budget when preparing financial budgets due to the vital importance of cash to a company.

The financing section shows expected borrowings and the repayment of the borrowed funds plus interest.It is needed when there is a cash deficiency or the cash balance is below the minimum required balance.

ILLUSTRATION 21-17ILLUSTRATION 21-17PREPARING THE FINANCIAL BUDGETS PREPARING THE FINANCIAL BUDGETS Budgeted Balance SheetBudgeted Balance Sheet

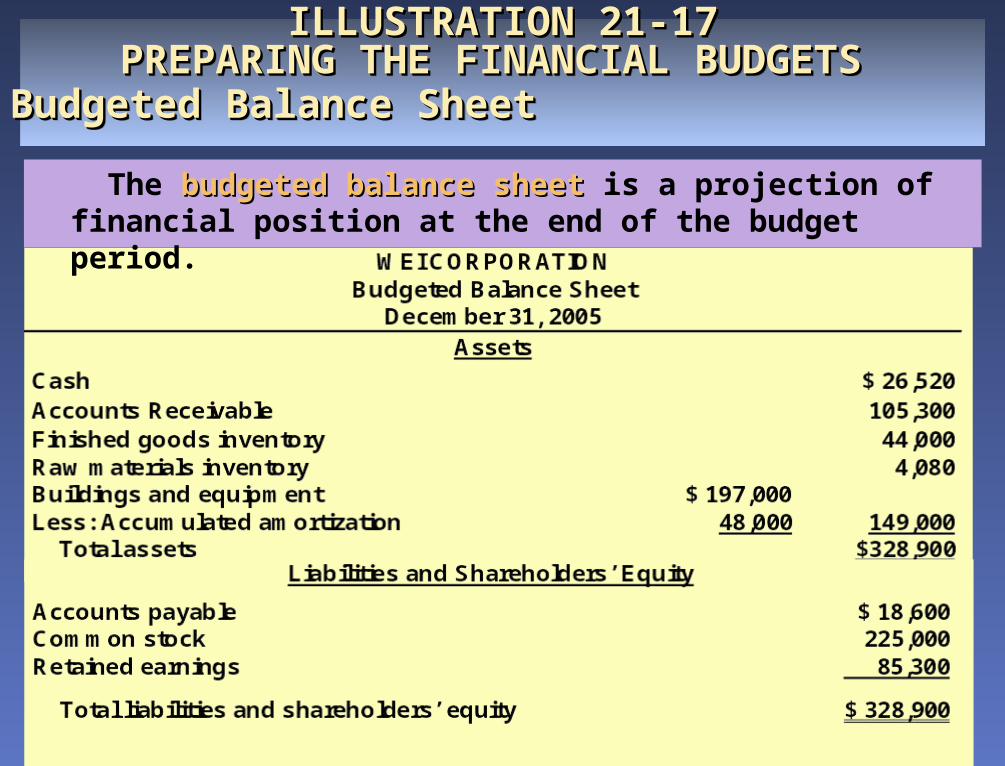

ILLUSTRATION 21-17ILLUSTRATION 21-17PREPARING THE FINANCIAL BUDGETS PREPARING THE FINANCIAL BUDGETS Budgeted Balance SheetBudgeted Balance Sheet

The budgeted balance sheetbudgeted balance sheet is a projection of financial position at the end of the budget period.

BUDGETING IN NONMANUFACTURING BUDGETING IN NONMANUFACTURING COMPANIESCOMPANIES

BUDGETING IN NONMANUFACTURING BUDGETING IN NONMANUFACTURING COMPANIESCOMPANIES

As in manufacturing operations, the sales As in manufacturing operations, the sales budget is the starting point in the budget is the starting point in the development of the master budget for adevelopment of the master budget for a merchandising companymerchandising company. The major . The major differences between the two companies’ differences between the two companies’ master budgets are that a merchandiser:master budgets are that a merchandiser:

• uses auses a merchandise purchases budgetmerchandise purchases budget instead of a production budget and,instead of a production budget and,

• does not use the manufacturing budgetsdoes not use the manufacturing budgets (direct materials, direct labour, and (direct materials, direct labour, and manufacturing overhead).manufacturing overhead).

BUDGETING IN NONMANUFACTURING BUDGETING IN NONMANUFACTURING COMPANIESCOMPANIES

BUDGETING IN NONMANUFACTURING BUDGETING IN NONMANUFACTURING COMPANIESCOMPANIES

• InIn service companiesservice companies such as a public accounting such as a public accounting firm, a law office, or a medical practice, the firm, a law office, or a medical practice, the critical factor in budgeting iscritical factor in budgeting is coordinating coordinating professional staff needs with anticipated professional staff needs with anticipated servicesservices. The goal is to be neither overstaffed . The goal is to be neither overstaffed nor understaffed.nor understaffed.

• Budgeting is important forBudgeting is important for not-for-profitnot-for-profit organizations but the budget process is organizations but the budget process is significantly different. Usually they budget on thesignificantly different. Usually they budget on the basis of cash flowsbasis of cash flows (expenditures and receipts) (expenditures and receipts)

rather than on a revenue and expense basis.rather than on a revenue and expense basis.

COPYRIGHTCOPYRIGHT

Copyright © 2004 John Wiley & Sons Canada, Ltd. All rights reserved. Copyright © 2004 John Wiley & Sons Canada, Ltd. All rights reserved. Reproduction or translation of this work beyond that permitted by Reproduction or translation of this work beyond that permitted by Access Copyright (The Canadian Copyright Licensing Agency) is Access Copyright (The Canadian Copyright Licensing Agency) is unlawful. Requests for further information should be addressed to the unlawful. Requests for further information should be addressed to the Permissions Department, John Wiley & Sons Canada, Ltd. The Permissions Department, John Wiley & Sons Canada, Ltd. The purchaser may make back-up copies for his or her own use only and purchaser may make back-up copies for his or her own use only and not for distribution or resale. The author and the publisher assume no not for distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages caused by the use of responsibility for errors, omissions, or damages caused by the use of these programs or from the use of the information contained herein.these programs or from the use of the information contained herein.