Embed Size (px)

Citation preview

1 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

A Study on Performance Evaluation of Mutual Funds Based on Investors

preference

Bratati Gupta*

Abstract

Financial markets are offering more promising solutions & becoming more exhaustive with

financial products requiring new innovations. As a part of financial markets mutual funds

industry is responding very fast by understanding the dynamics of investor’s perception towards

rewards, they are continuously trying to differentiate their products and this is also visible in

designing mutual funds portfolio but these changes should met the investor’s expectations. With

the decline in the bank interest rates, frequent fluctuations in the secondary market and the

inherent attitude of Indian small investors to avoid risk, it is important on the part of fund

managers and mutual fund product designers to combine various elements of liquidity, return

and security in making mutual fund products the best possible alternative for the small investors

in Indian market. Thus, it is high time to understand the key factors that rules the investor’s

mind, their expectations, and unveil some extremely valuable information to support financial

decision making of mutual funds.The present study aims to analyse the factors which play a key

role in investors mind while taking investment decision. as well as to measure the performance of

selected mutual fund based on investors preference.

Keywords: Mutual fund, Risk-return, Sharp ratio, Beta

* Bratati Gupta, Assistant Professor, Institute of Business Management, Affiliated to Jadavpur

University, India, email : [email protected], M : +91(0) 9830503930.

2 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Introduction

A Mutual Fund is a trust that pools the savings of a number of investors who share a common

financial goal or in other words we can say that it is a mechanism of pooling together the

investment of unsophisticated investors and turn in the hands of professionally managed fund

managers for consistent return along-with capital appreciation. The money collected& invested

by the fund manager in different types of securities depending upon the objective of the scheme.

These could range from shares to debentures to money market instruments collected in this

process are then invested in capital market instrument such as shares, debentures and other

securities. The income earned through these investments and its unit holders in proportion to the

number of units owned by them (pro rata) shares the capital appreciation realized by the scheme.

Mutual funds put forward a way out to investors to approach most schemes and get well-

diversified portfolio because investors with small savings neither have sufficient expertise nor

have access to required diversification. Anybody with an investible surplus of as little as a few

thousand rupees can invest in Mutual Funds. Each Mutual Fund scheme has a defined investment

objective and strategy.

Intensified competition and involvement of private players in the race of mutual funds have

forced professional managers to bring innovation in mutual funds. It has already entered into a

world of exciting innovative products. These products are now tailor made to suit specific needs

of investors. Thus, mutual funds industry has moved from offering a handful of schemes like

equity, debt or balanced funds to liquid, money market, sector specific funds, index funds and

giltedged funds. Beside this recently mutual funds have also introduced some special specific

funds like children plans, education plans, insurance linked plans, and exchange traded funds.

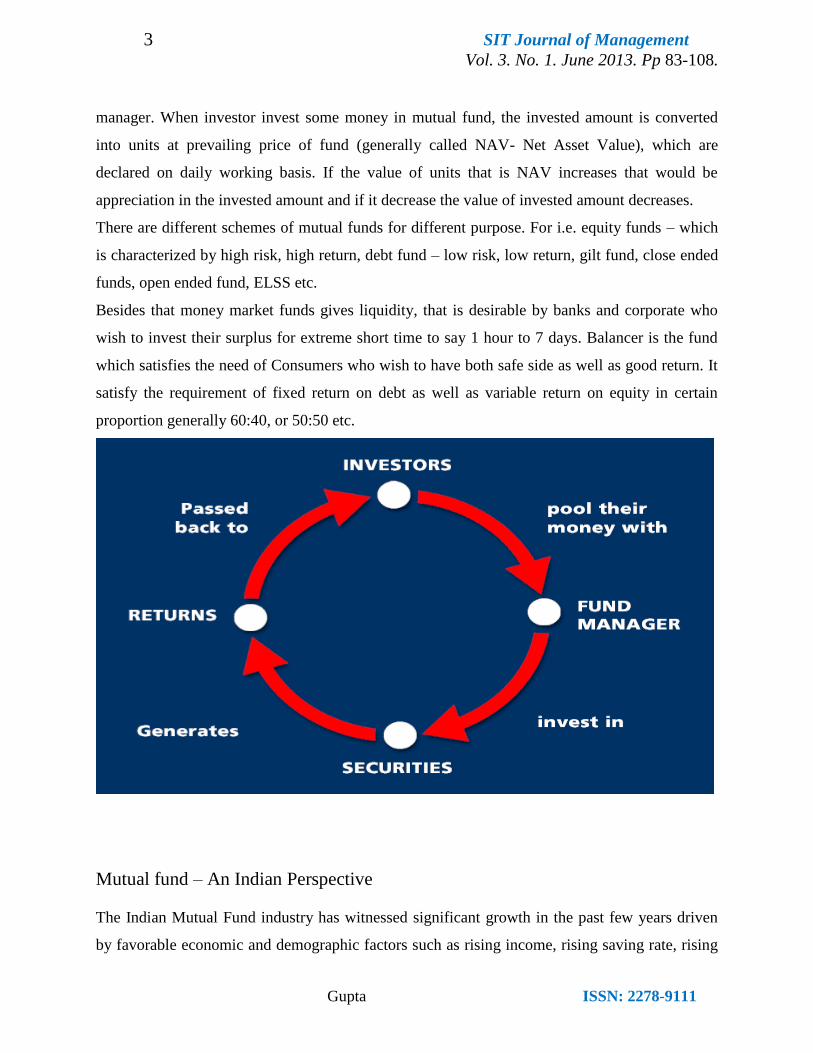

How mutual fund works – A Brief Idea

Mutual fund works on the concept “Small drops of water make a big ocean” i.e., Small investors

can also invest in mutual fund and earned a fair rate of return with less risk compare to shares..

Consumers invest their money into mutual fund through Asset Management Company (AMC).

There are experts available in the market, which are in constant touch with micro and macro

aggregates of the economy viz. share market, consumer preference; trend, fashion etc. act as fund

3 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

manager. When investor invest some money in mutual fund, the invested amount is converted

into units at prevailing price of fund (generally called NAV- Net Asset Value), which are

declared on daily working basis. If the value of units that is NAV increases that would be

appreciation in the invested amount and if it decrease the value of invested amount decreases.

There are different schemes of mutual funds for different purpose. For i.e. equity funds – which

is characterized by high risk, high return, debt fund – low risk, low return, gilt fund, close ended

funds, open ended fund, ELSS etc.

Besides that money market funds gives liquidity, that is desirable by banks and corporate who

wish to invest their surplus for extreme short time to say 1 hour to 7 days. Balancer is the fund

which satisfies the need of Consumers who wish to have both safe side as well as good return. It

satisfy the requirement of fixed return on debt as well as variable return on equity in certain

proportion generally 60:40, or 50:50 etc.

Mutual fund – An Indian Perspective

The Indian Mutual Fund industry has witnessed significant growth in the past few years driven

by favorable economic and demographic factors such as rising income, rising saving rate, rising

4 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

income earning-spending activity etc. Mutual funds in India was firstly launched in July 1964 by

UTI, with the objective of employment of individual savings into gigantic capital formation by

investing it in capital market, besides that there was strong need for channelizing household

savings for circulation and making it available for corporate for their productive use. At the same

time it was felt that UTI could be an effective option to bridge the gap between individual saving

and capital formation. UTI enjoyed the monopoly for almost two decades. In early nineties the

following players entered into the market. They are SBI (1987), Can Bank (1987), LIC (1989),

Indian Bank (1990), Bank of India (1990), PNB (1990), GIC (1991) etc. Presently the concept of

mutual fund has become very familiar to almost all retail Consumers.

Benefits

Diversification

One rule of investing, for both large and small investors, is asset diversification. Diversification

involves the mixing of investments within a portfolio and is used to manage risk By purchasing

mutual funds, investors are provided with the immediate benefit of instant diversification and

asset allocation without the large amounts of cash needed to create individual portfolios.

Economies of Scale

Mutual funds are able to take advantage of their buying and selling size and thereby reduce

transaction costs for investors. When you buy a mutual fund, you are able to diversify without

the numerous commission charges. With mutual funds, you can make transactions on a much

larger scale for less money.

Divisibility

Smaller denominations of mutual funds provide mutual fund investors the ability to make

periodic investments through monthly purchase plans. So, rather than having to wait until you

have enough money to buy higher-cost investments, investor can get in right away with mutual

funds. This provides an additional advantage - liquidity.

5 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Liquidity

Another advantage of mutual funds is the ability to get in and out with relative ease. In general,

investors are able to sell mutual funds in a short period of time without there being much

difference between the sale price and the most current market value. However, it is important to

watch out for any fees associated with selling, including back-end load fees. Also, unlike stocks

and exchange-traded funds (ETFs), which trade any time during market hours, mutual funds

transact only once per day after the fund's net asset value (NAV) is calculated.

Professional Management

When an investor buys a mutual fund, they are also choosing a professional money manager.

This manager will invest the money where he or she has carefully researched. Therefore, rather

than having to thoroughly research every investment before investing , a mutual fund's money

manager is there to handle it for investors.

Potential of Returns

Returns in the mutual funds are generally better than any other option in any other avenue over a

reasonable period. People can pick their investment horizon and stay put in the chosen fund for

the duration. Equity funds can outperform most other investments over long periods by placing

long-term calls on fundamentally good stocks (2). The debt funds too will outperform other

options such as banks, though they are affected by the interest rate risk in general.

The Bottom Line

As with any investment, there are risks involved in buying mutual funds. These investment

vehicles can experience market fluctuations and sometimes provide returns below the overall

market. Also, the advantages gained from mutual funds are not free: many of them carry loads,

annual expense fees and penalties for early withdrawal.

6 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Literature Review

A large number of studies on the growth and financial performance of mutual funds have been

carried out during the past, in the developed and developing countries.The pioneering work on

the mutual funds in U.S.A. was done by Friend, et al., (1962) made an extensive and systematic

study of 52 mutual funds found that mutual fund schemes earned an average annual return

Overall results did not suggest widespread inefficiency in the industry. Comparison of fund

returns with turnover and expense categories did not reveal a strong relationship.

Treynor (1965) coined a fund performance measure taking investment risk into account. Further,

to deal with a portfolio, „portfolio-possibility line‟ was used torelate expected return to the

portfolio owner‟s risk preference. The most prominent study by Sharpe, William F (1966)

developed a composite measure of return and risk. He evaluated 34 open-end mutual funds for

the period 1944-63. The results depicted that good performance was associated with low expense

ratio and not with the size. Sample schemes showed consistency in risk measure.

Treynor and Mazuy (1966) evaluated the performance of 57 fund managers in terms of their

market timing abilities and for the study adopted Treynor‟s (1965) methodology for reviewing

the performance of mutual funds.Jensen (1968) developed a composite portfolio evaluation

technique concerning risk-adjusted returns. He evaluated the ability of 115 fund managers in

selecting securities during the period 1945-66.Jensen concluded that, there was very little

evidence that funds were able to perform significantly better than expected as fund managers

were not able to forecast securities price movements.

McDonald and John (1974) examined 123 mutual funds and identified the existence of positive

relationship between objectives and risk. The study identified the existence of positive

relationship between return and risk. Gupta (1974) evaluated the performance of mutual fund

industry for the period 1962-71 using Sharpe, Treynor, and Jensen models. All the funds covered

under the study outperformed the market irrespective of the choice of market index. The results

indicated that all the three models provided identical results. Return per unit of risk varied with

7 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

the level of volatility assumed and he concluded that, funds with higher volatility exhibited

superior performance.

Meyer‟s (1977) findings based on stochastic dominance model revalidated Sharpe‟s findings

with the caution that it was relevant for mutual funds in the designated past rather than for the

future period.Gupta Ramesh (1989) evaluated fund performance in India comparing the returns

earned by schemes of similar risk and similar constraints. Mutual fund return due to selectivity

was decomposed into return due to selection of securities and timing of Investment in a

particular class of securities. Sarkar A K (1991) critically examined mutual fund evaluation

methodology and pointed out that Sharpe and Treynor performance measures ranked mutual

funds alike inspite of their differences in terms. Sahu R K (1992) identified mutual funds as a

suitable investment vehicle to strengthen capital market, as the total assets were around

Rs.30,000 crores while the total resources in equity was less than 15 percent of market

capitalization.

Objectives of the Study

The buying intent of a mutual fund product by a investor can be of multiple reasons depending

upon the investors risk return trade off.. Due to the constant reduction in bank FD rates &

extreme volatility in stock market investors are looking for a safe avenue for their small time

investment, which will provide them a higher return. So Mutual fund offers the best alternative

to the Indian investors. So the study attempts to achieve the following objectives.

• To analyse factors that influence most while investing in mutual funds.

• To evaluate performance of mutual fund schemes preferred by investors on the basis of return

parameters.

Research Methodology

Research is divided into two different studies:

Research 1:

Primary Research to know the Factors which play a key role while investing in mutual funds.

The survey is conducted with the help of a structured questionnaire based on different parameter

8 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

of investors preference on a sample of 80 respondents. Out of which 57 completed responses are

considered for the purpose of the study Apart from the primary survey on the different

parameters a chi-square test is conducted on the respondent to judge the key factors & to find

their preferences.

Research 2:

Secondary Research to evaluate the performance of Mutual funds which are preferred by most of

the investors .Three mutual fund sectors viz. tax funds, equity diversified funds and balanced

funds are selected and top 5 schemes based on their performance from each segment is selected

for further analysis.

Demographic profile of the Respondents

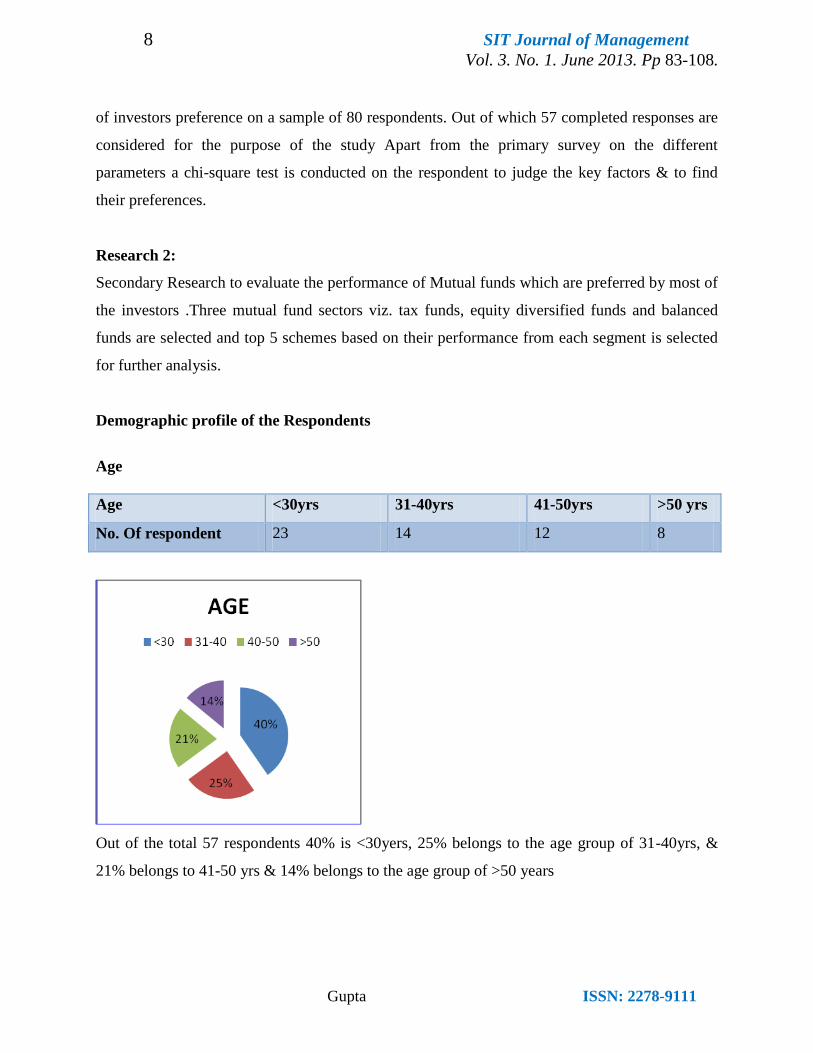

Age

Age <30yrs 31-40yrs 41-50yrs >50 yrs

No. Of respondent 23 14 12 8

Out of the total 57 respondents 40% is <30yers, 25% belongs to the age group of 31-40yrs, &

21% belongs to 41-50 yrs & 14% belongs to the age group of >50 years

9 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

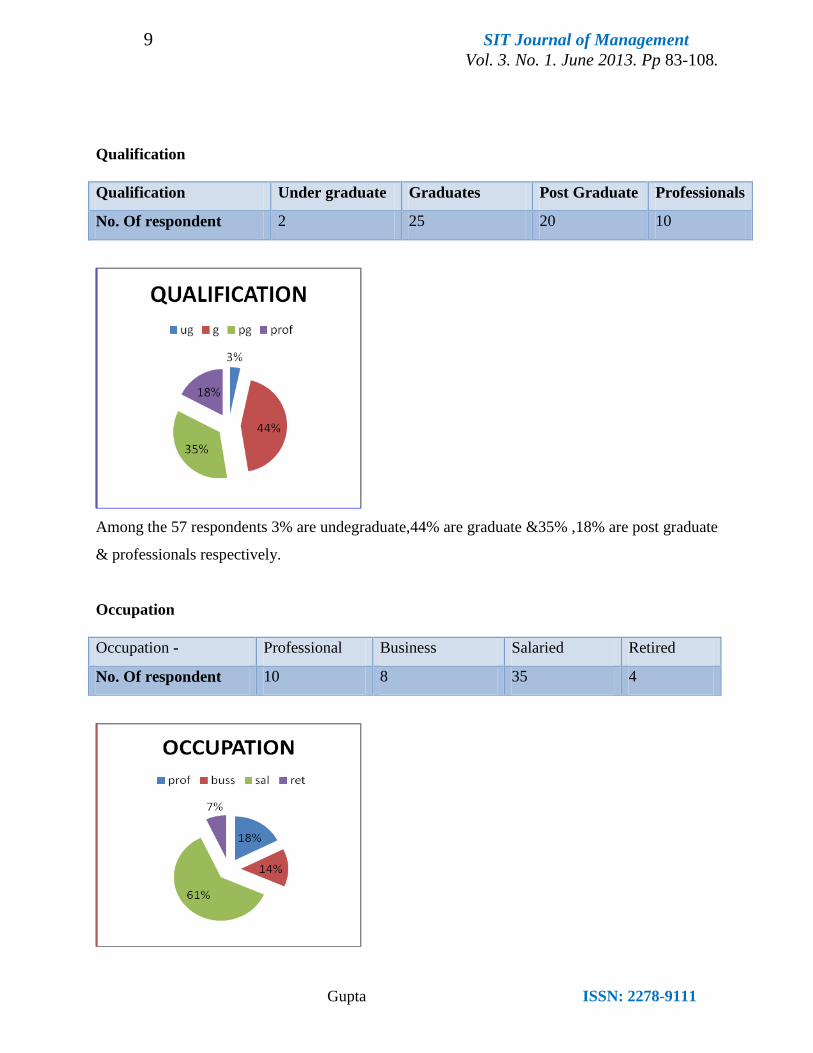

Qualification

Qualification Under graduate Graduates Post Graduate Professionals

No. Of respondent 2 25 20 10

Among the 57 respondents 3% are undegraduate,44% are graduate &35% ,18% are post graduate

& professionals respectively.

Occupation

Occupation - Professional Business Salaried Retired

No. Of respondent 10 8 35 4

10 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

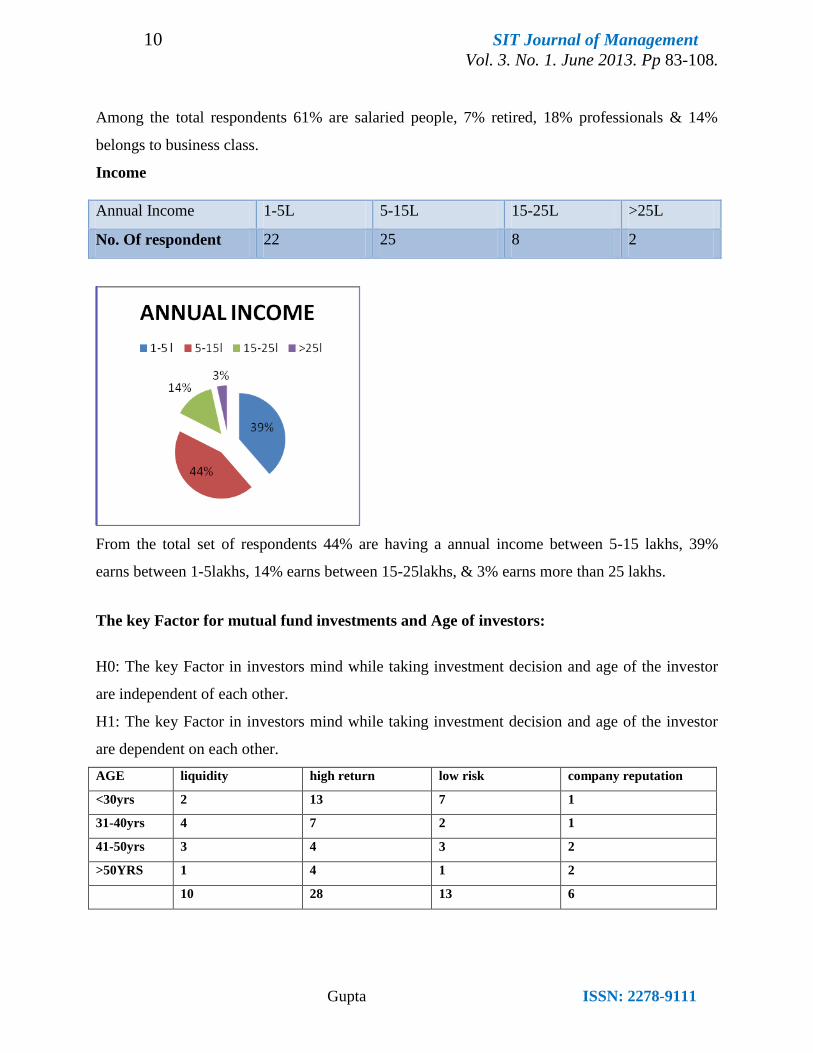

Among the total respondents 61% are salaried people, 7% retired, 18% professionals & 14%

belongs to business class.

Income

Annual Income 1-5L 5-15L 15-25L >25L

No. Of respondent 22 25 8 2

From the total set of respondents 44% are having a annual income between 5-15 lakhs, 39%

earns between 1-5lakhs, 14% earns between 15-25lakhs, & 3% earns more than 25 lakhs.

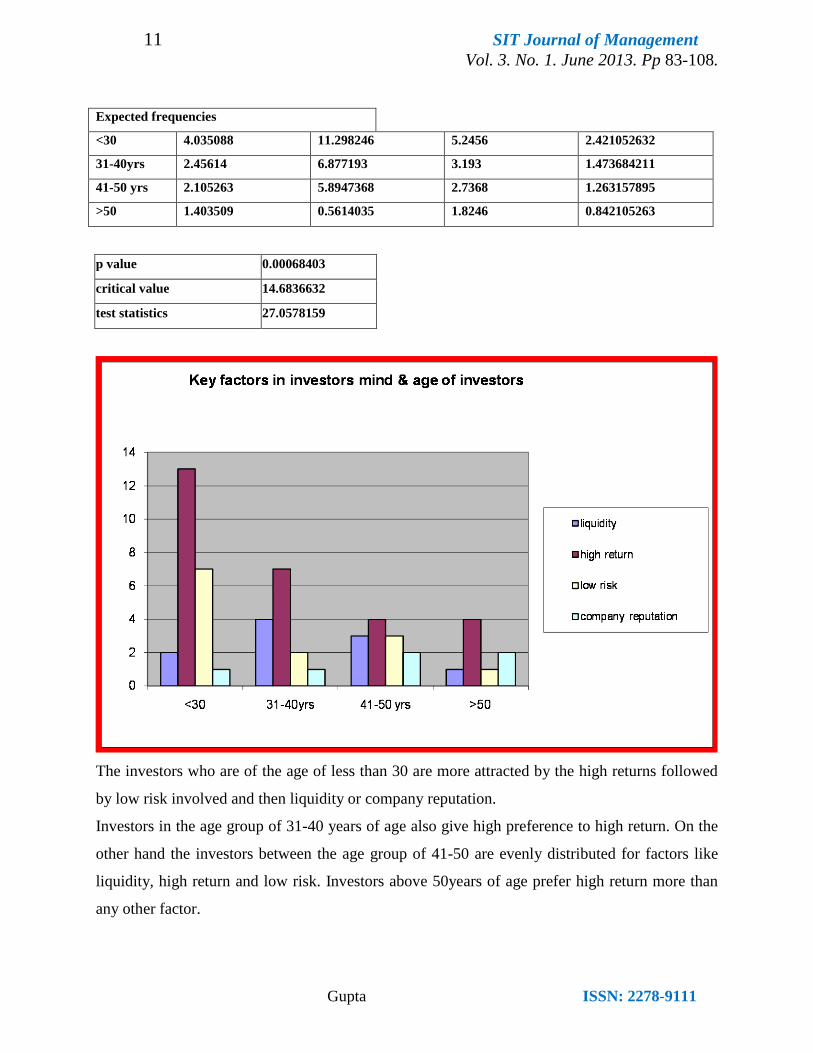

The key Factor for mutual fund investments and Age of investors:

H0: The key Factor in investors mind while taking investment decision and age of the investor

are independent of each other.

H1: The key Factor in investors mind while taking investment decision and age of the investor

are dependent on each other.

AGE liquidity high return low risk company reputation

<30yrs 2 13 7 1

31-40yrs 4 7 2 1

41-50yrs 3 4 3 2

>50YRS 1 4 1 2

10 28 13 6

11 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Expected frequencies

<30 4.035088 11.298246 5.2456 2.421052632

31-40yrs 2.45614 6.877193 3.193 1.473684211

41-50 yrs 2.105263 5.8947368 2.7368 1.263157895

>50 1.403509 0.5614035 1.8246 0.842105263

p value 0.00068403

critical value 14.6836632

test statistics 27.0578159

The investors who are of the age of less than 30 are more attracted by the high returns followed

by low risk involved and then liquidity or company reputation.

Investors in the age group of 31-40 years of age also give high preference to high return. On the

other hand the investors between the age group of 41-50 are evenly distributed for factors like

liquidity, high return and low risk. Investors above 50years of age prefer high return more than

any other factor.

12 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Chi square calculated value is 27.0578 and critical value for the same at 10% level of significance is

14.68. as calculated value is more than tabulated value Ho is rejected. thus there is significant

relationship between two variables.) .This means that age of the investor and the key factors in

investors while taking investment decisions are dependent on each other.

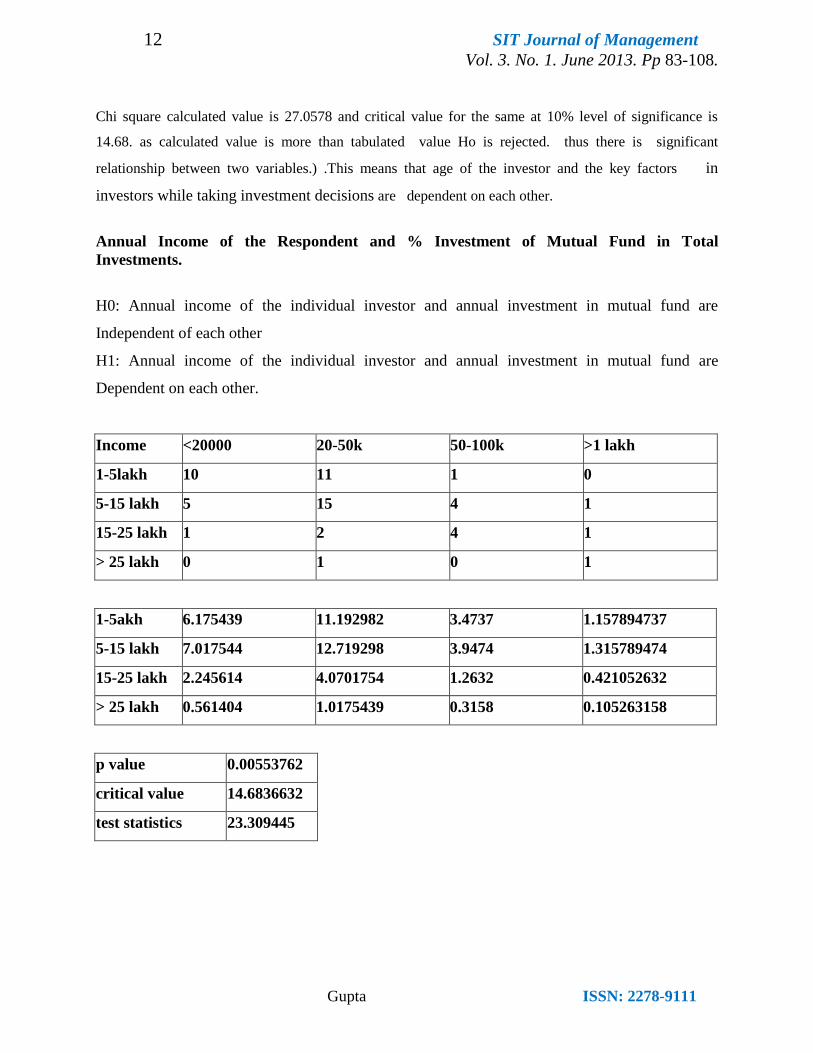

Annual Income of the Respondent and % Investment of Mutual Fund in Total

Investments.

H0: Annual income of the individual investor and annual investment in mutual fund are

Independent of each other

H1: Annual income of the individual investor and annual investment in mutual fund are

Dependent on each other.

Income <20000 20-50k 50-100k >1 lakh

1-5lakh 10 11 1 0

5-15 lakh 5 15 4 1

15-25 lakh 1 2 4 1

> 25 lakh 0 1 0 1

1-5akh 6.175439 11.192982 3.4737 1.157894737

5-15 lakh 7.017544 12.719298 3.9474 1.315789474

15-25 lakh 2.245614 4.0701754 1.2632 0.421052632

> 25 lakh 0.561404 1.0175439 0.3158 0.105263158

p value 0.00553762

critical value 14.6836632

test statistics 23.309445

13 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

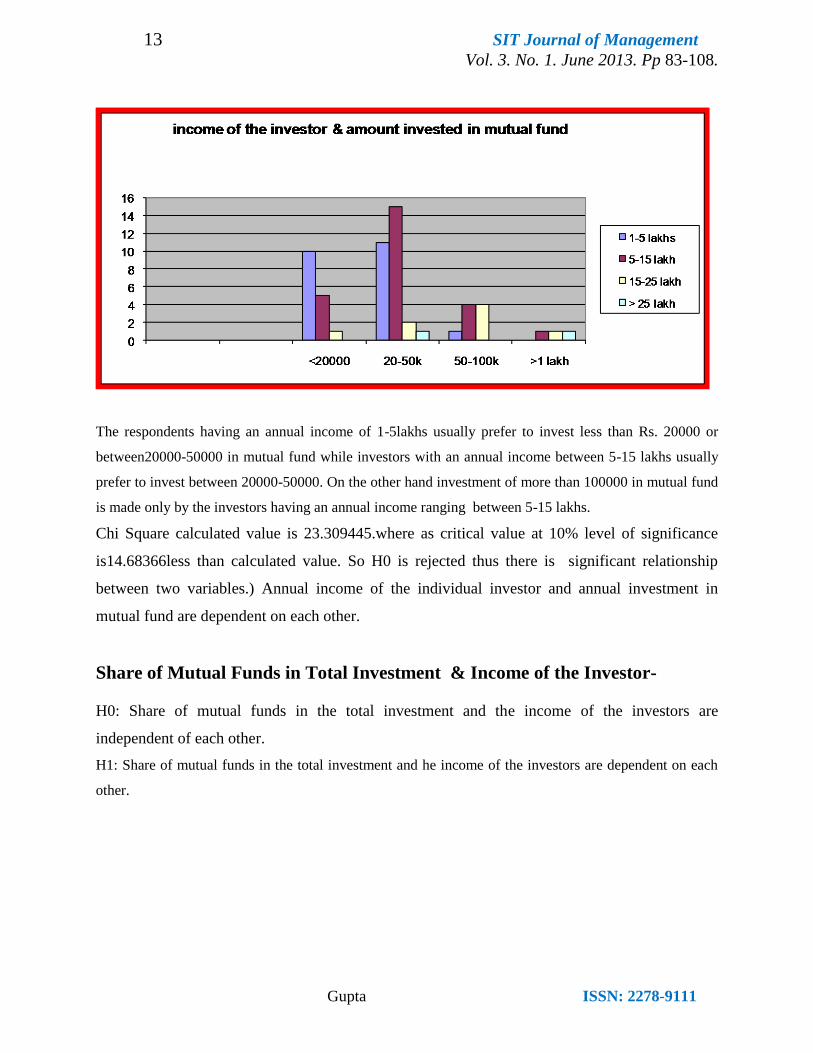

The respondents having an annual income of 1-5lakhs usually prefer to invest less than Rs. 20000 or

between20000-50000 in mutual fund while investors with an annual income between 5-15 lakhs usually

prefer to invest between 20000-50000. On the other hand investment of more than 100000 in mutual fund

is made only by the investors having an annual income ranging between 5-15 lakhs.

Chi Square calculated value is 23.309445.where as critical value at 10% level of significance

is14.68366less than calculated value. So H0 is rejected thus there is significant relationship

between two variables.) Annual income of the individual investor and annual investment in

mutual fund are dependent on each other.

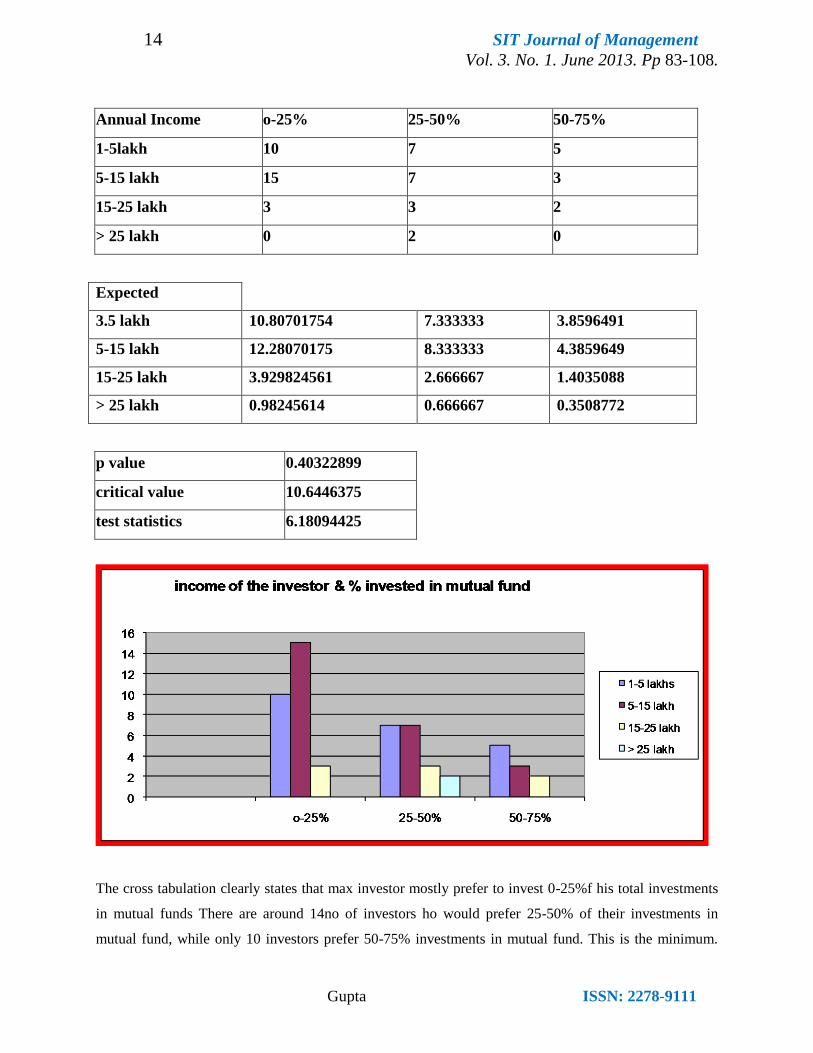

Share of Mutual Funds in Total Investment & Income of the Investor-

H0: Share of mutual funds in the total investment and the income of the investors are

independent of each other.

H1: Share of mutual funds in the total investment and he income of the investors are dependent on each

other.

14 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Annual Income o-25% 25-50% 50-75%

1-5lakh 10 7 5

5-15 lakh 15 7 3

15-25 lakh 3 3 2

> 25 lakh 0 2 0

Expected

3.5 lakh 10.80701754 7.333333 3.8596491

5-15 lakh 12.28070175 8.333333 4.3859649

15-25 lakh 3.929824561 2.666667 1.4035088

> 25 lakh 0.98245614 0.666667 0.3508772

p value 0.40322899

critical value 10.6446375

test statistics 6.18094425

The cross tabulation clearly states that max investor mostly prefer to invest 0-25%f his total investments

in mutual funds There are around 14no of investors ho would prefer 25-50% of their investments in

mutual fund, while only 10 investors prefer 50-75% investments in mutual fund. This is the minimum.

15 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Moreover the above table also states that annual income does not have any impact on % investment of

mutual fund out of total investment and a high income does not mean that his investment in mutual fund

would also be high.

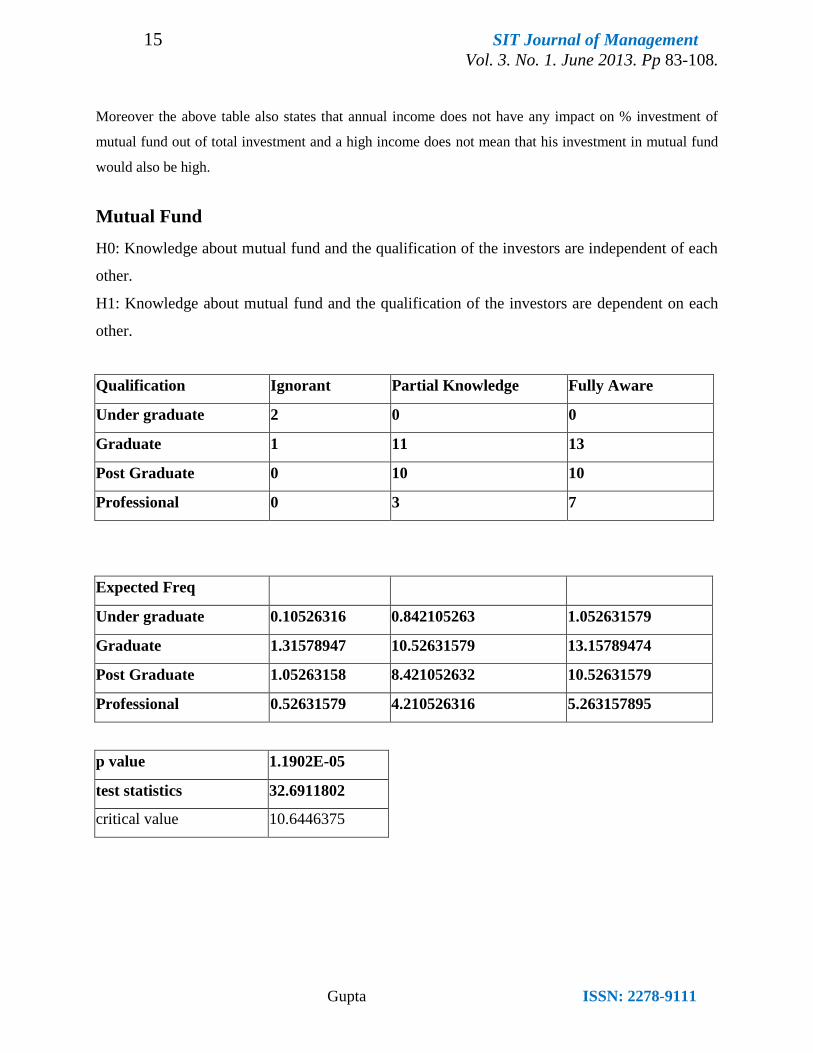

Mutual Fund

H0: Knowledge about mutual fund and the qualification of the investors are independent of each

other.

H1: Knowledge about mutual fund and the qualification of the investors are dependent on each

other.

Qualification Ignorant Partial Knowledge Fully Aware

Under graduate 2 0 0

Graduate 1 11 13

Post Graduate 0 10 10

Professional 0 3 7

Expected Freq

Under graduate 0.10526316 0.842105263 1.052631579

Graduate 1.31578947 10.52631579 13.15789474

Post Graduate 1.05263158 8.421052632 10.52631579

Professional 0.52631579 4.210526316 5.263157895

p value 1.1902E-05

test statistics 32.6911802

critical value 10.6446375

16 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

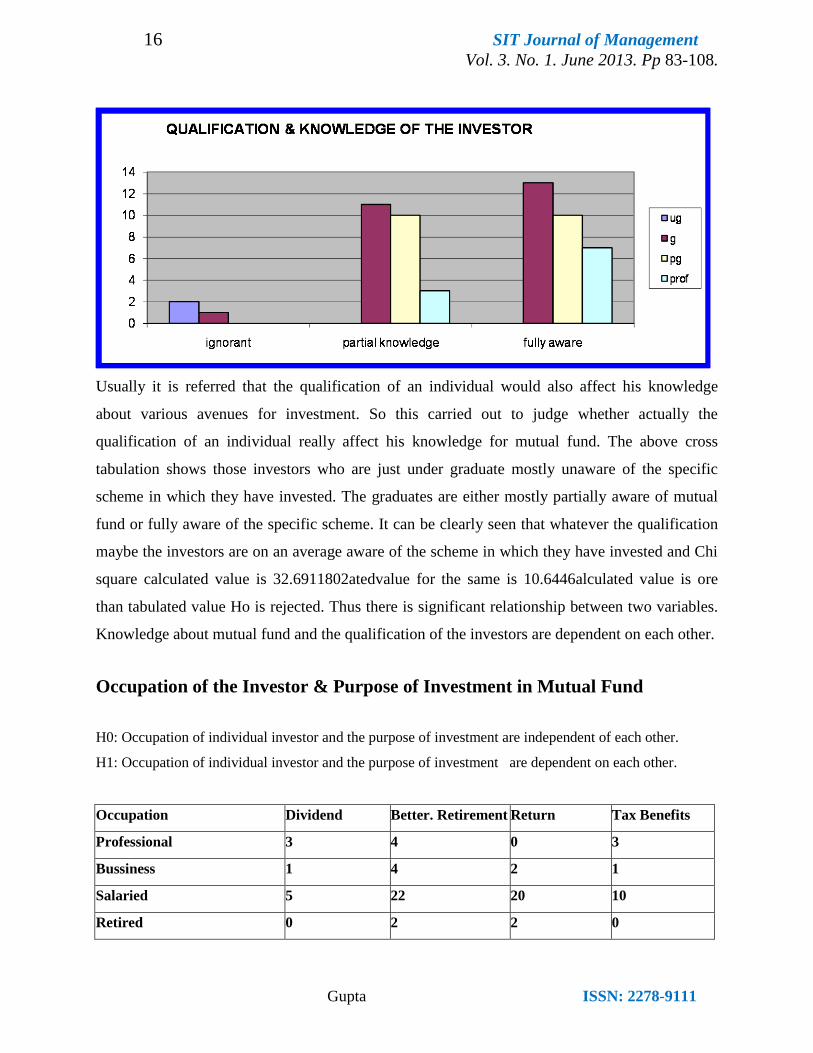

Usually it is referred that the qualification of an individual would also affect his knowledge

about various avenues for investment. So this carried out to judge whether actually the

qualification of an individual really affect his knowledge for mutual fund. The above cross

tabulation shows those investors who are just under graduate mostly unaware of the specific

scheme in which they have invested. The graduates are either mostly partially aware of mutual

fund or fully aware of the specific scheme. It can be clearly seen that whatever the qualification

maybe the investors are on an average aware of the scheme in which they have invested and Chi

square calculated value is 32.6911802atedvalue for the same is 10.6446alculated value is ore

than tabulated value Ho is rejected. Thus there is significant relationship between two variables.

Knowledge about mutual fund and the qualification of the investors are dependent on each other.

Occupation of the Investor & Purpose of Investment in Mutual Fund

H0: Occupation of individual investor and the purpose of investment are independent of each other.

H1: Occupation of individual investor and the purpose of investment are dependent on each other.

Occupation Dividend Better. Retirement Return Tax Benefits

Professional 3 4 0 3

Bussiness 1 4 2 1

Salaried 5 22 20 10

Retired 0 2 2 0

17 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

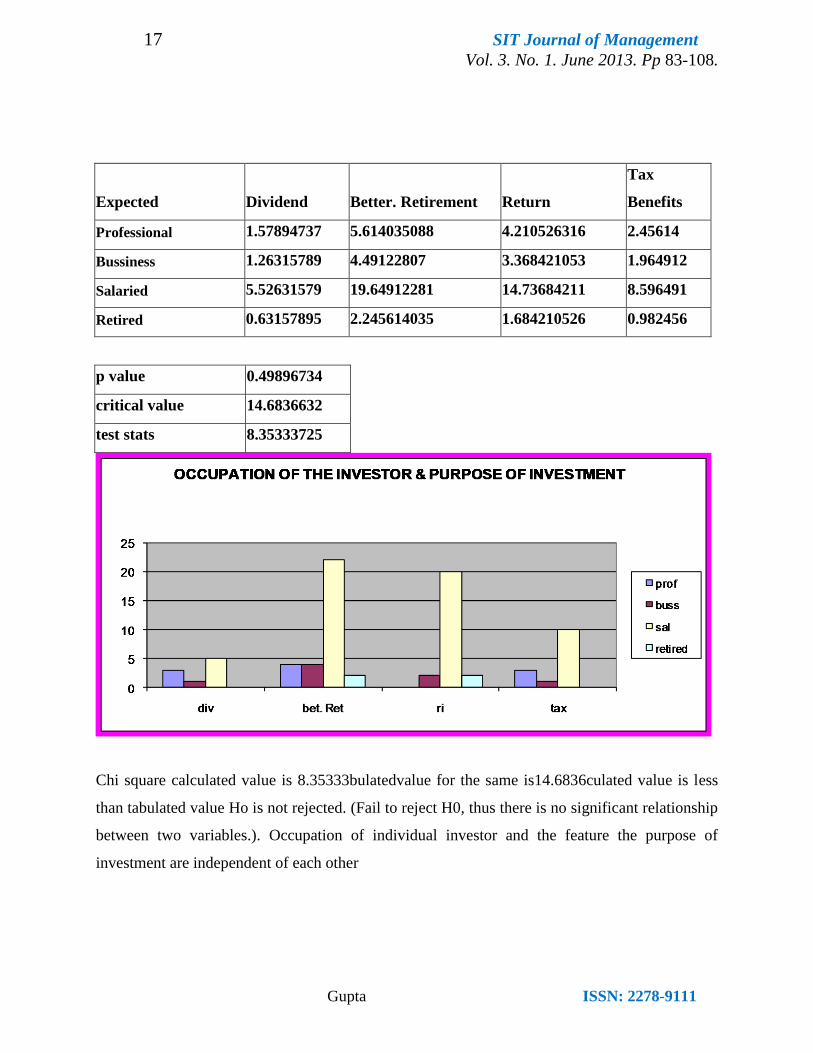

Expected Dividend Better. Retirement Return

Tax

Benefits

Professional 1.57894737 5.614035088 4.210526316 2.45614

Bussiness 1.26315789 4.49122807 3.368421053 1.964912

Salaried 5.52631579 19.64912281 14.73684211 8.596491

Retired 0.63157895 2.245614035 1.684210526 0.982456

p value 0.49896734

critical value 14.6836632

test stats 8.35333725

Chi square calculated value is 8.35333bulatedvalue for the same is14.6836culated value is less

than tabulated value Ho is not rejected. (Fail to reject H0, thus there is no significant relationship

between two variables.). Occupation of individual investor and the feature the purpose of

investment are independent of each other

18 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

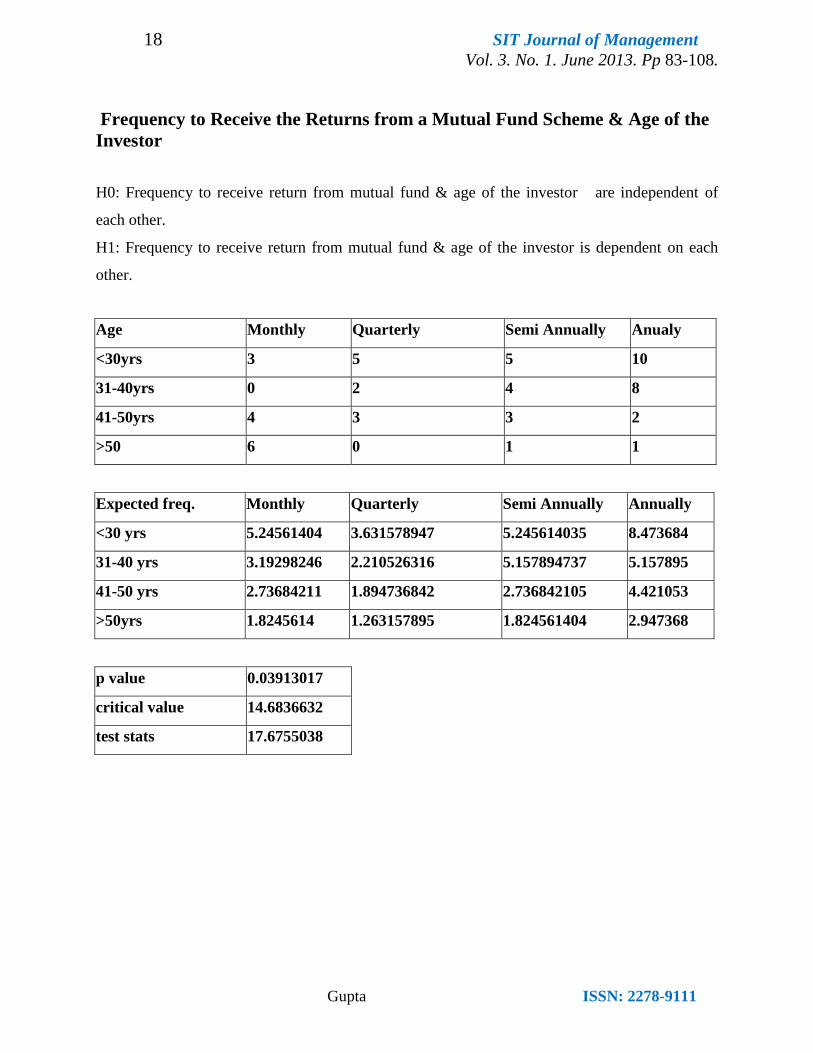

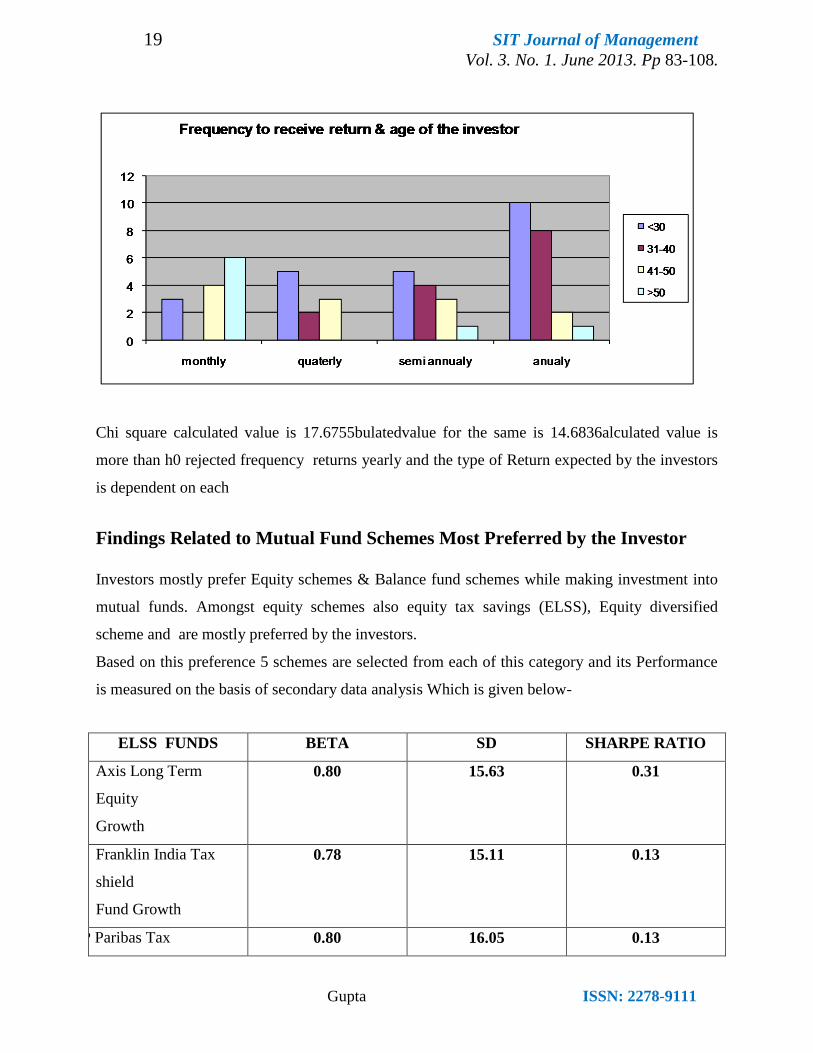

Frequency to Receive the Returns from a Mutual Fund Scheme & Age of the

Investor

H0: Frequency to receive return from mutual fund & age of the investor are independent of

each other.

H1: Frequency to receive return from mutual fund & age of the investor is dependent on each

other.

Age Monthly Quarterly Semi Annually Anualy

<30yrs 3 5 5 10

31-40yrs 0 2 4 8

41-50yrs 4 3 3 2

>50 6 0 1 1

Expected freq. Monthly Quarterly Semi Annually Annually

<30 yrs 5.24561404 3.631578947 5.245614035 8.473684

31-40 yrs 3.19298246 2.210526316 5.157894737 5.157895

41-50 yrs 2.73684211 1.894736842 2.736842105 4.421053

>50yrs 1.8245614 1.263157895 1.824561404 2.947368

p value 0.03913017

critical value 14.6836632

test stats 17.6755038

19 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Chi square calculated value is 17.6755bulatedvalue for the same is 14.6836alculated value is

more than h0 rejected frequency returns yearly and the type of Return expected by the investors

is dependent on each

Findings Related to Mutual Fund Schemes Most Preferred by the Investor

Investors mostly prefer Equity schemes & Balance fund schemes while making investment into

mutual funds. Amongst equity schemes also equity tax savings (ELSS), Equity diversified

scheme and are mostly preferred by the investors.

Based on this preference 5 schemes are selected from each of this category and its Performance

is measured on the basis of secondary data analysis Which is given below-

ELSS FUNDS BETA SD SHARPE RATIO

Axis Long Term

Equity

Growth

0.80 15.63 0.31

Franklin India Tax

shield

Fund Growth

0.78 15.11 0.13

BNP Paribas Tax 0.80 16.05 0.13

20 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Advantage

Plan Growth

Canara Robeco Equity

Tax saver

0.81 16.65 -0.15

HDFC Long Term

Advantage

Fund Dividend

0.87 17.02 0.07

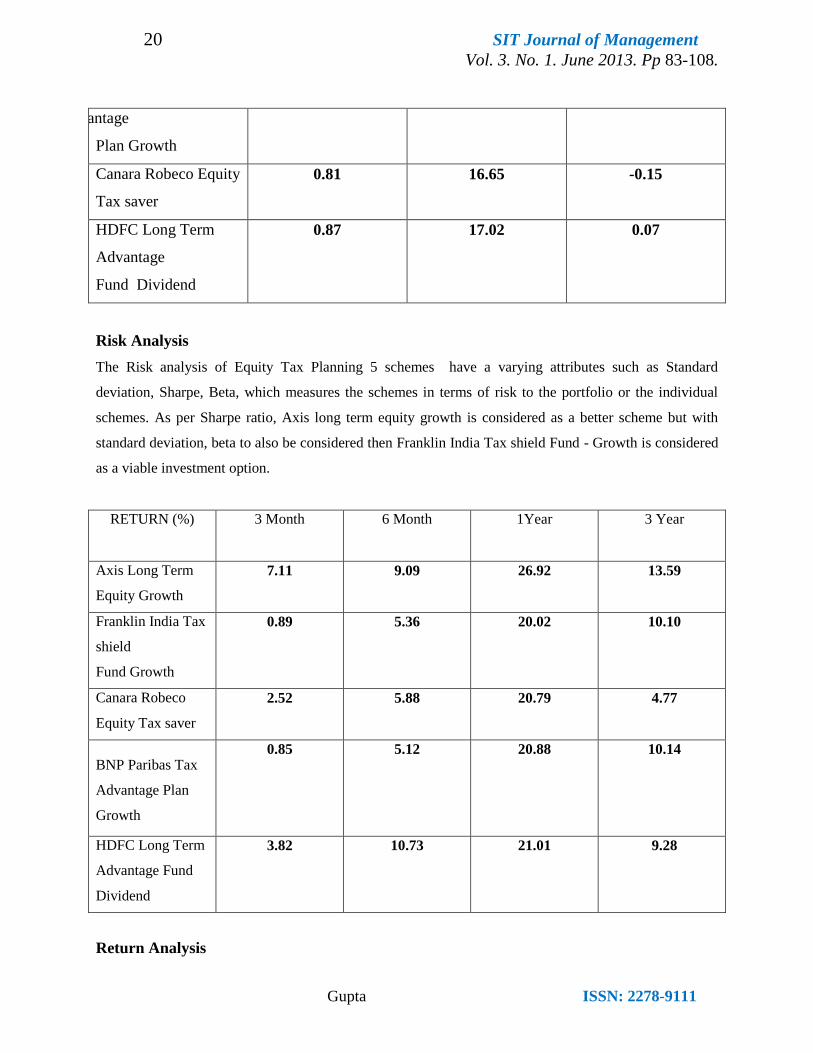

Risk Analysis

The Risk analysis of Equity Tax Planning 5 schemes have a varying attributes such as Standard

deviation, Sharpe, Beta, which measures the schemes in terms of risk to the portfolio or the individual

schemes. As per Sharpe ratio, Axis long term equity growth is considered as a better scheme but with

standard deviation, beta to also be considered then Franklin India Tax shield Fund - Growth is considered

as a viable investment option.

RETURN (%) 3 Month 6 Month 1Year 3 Year

Axis Long Term

Equity Growth

7.11 9.09 26.92 13.59

Franklin India Tax

shield

Fund Growth

0.89 5.36 20.02 10.10

Canara Robeco

Equity Tax saver

2.52 5.88 20.79 4.77

BNP Paribas Tax

Advantage Plan

Growth

0.85 5.12 20.88 10.14

HDFC Long Term

Advantage Fund

Dividend

3.82 10.73 21.01 9.28

Return Analysis

21 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

For the return analysis of Equity Tax Planning 5 schemes it can be seen that all the returns of all the

schemes is maximized in 1 year rather than 3 year returns so here investor should have to invest for a

year. As per 1 year return Axis long term equity growth shows the highest return of 26.92% followed by

HDFC long Term Fund advantage dividend giving a return of 21.01%. while the schemes such as BNP

Paribas Tax Advantage Plan – Franklin India tax shield fund growth Canara Robeco Equity Tax saver

gave a average return of 20.88% to 20.02%. So considering both the risk & return aspect Axis Long

Term Equity Growth found to be a viable option for the investors.

EQUITY DIV. FUND BETA SD SHARPE RATIO

Reliance Equity Fund

Growth

1.02 20.32 -0.24

Birla Sun Life Frontline

Equity Fund Growth

0.90 17.38 0.09

SBI Emerging

Businesses Fund

0.71 18.77 0.47

UTI Equity Fund

Dividend

0.85 16.45 0.18

Axis Equity Dividend 0.86 16.76 0.08

Risk analysis

Amongst the 5 schemes of Equity Diversified funds, it can be said that UTI Equity Fund

Dividend is said to be the most advisable one for the investors as per the Sharpe ratio, standard

deviation & beta similarly Reliance Equity Fund Growth is said to be the least advisable to the

investors which is showing a negative Sharpe ratio & higher standard deviation and beta.

Whereas SBI Emerging Businesses Fund although having a high Sharpe ratio but

simultaneously having a high standard deviation. Schemes like Birla Sun Life frontline equity

fund growth, Axis equity dividend showing a high SD, beta & low Sharpe ratio. so these

schemes seems to be risky than the earlier ones.

22 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

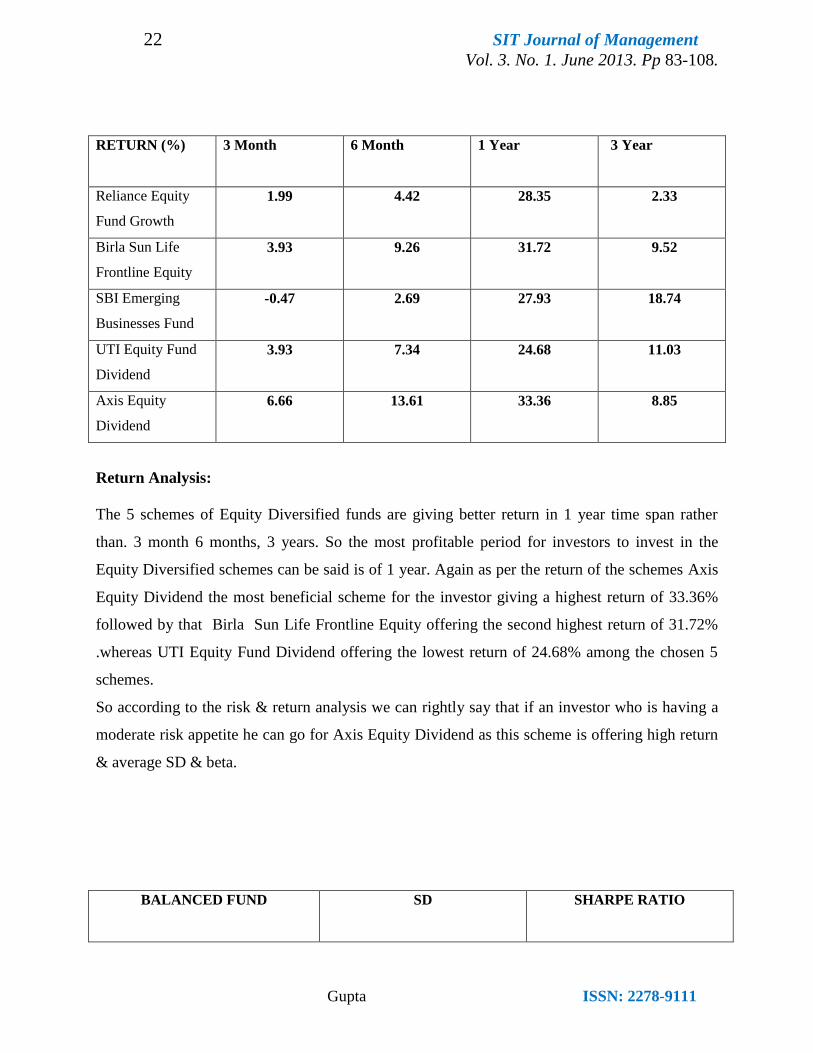

RETURN (%) 3 Month 6 Month 1 Year 3 Year

Reliance Equity

Fund Growth

1.99 4.42 28.35 2.33

Birla Sun Life

Frontline Equity

3.93 9.26 31.72 9.52

SBI Emerging

Businesses Fund

-0.47 2.69 27.93 18.74

UTI Equity Fund

Dividend

3.93 7.34 24.68 11.03

Axis Equity

Dividend

6.66 13.61 33.36 8.85

Return Analysis:

The 5 schemes of Equity Diversified funds are giving better return in 1 year time span rather

than. 3 month 6 months, 3 years. So the most profitable period for investors to invest in the

Equity Diversified schemes can be said is of 1 year. Again as per the return of the schemes Axis

Equity Dividend the most beneficial scheme for the investor giving a highest return of 33.36%

followed by that Birla Sun Life Frontline Equity offering the second highest return of 31.72%

.whereas UTI Equity Fund Dividend offering the lowest return of 24.68% among the chosen 5

schemes.

So according to the risk & return analysis we can rightly say that if an investor who is having a

moderate risk appetite he can go for Axis Equity Dividend as this scheme is offering high return

& average SD & beta.

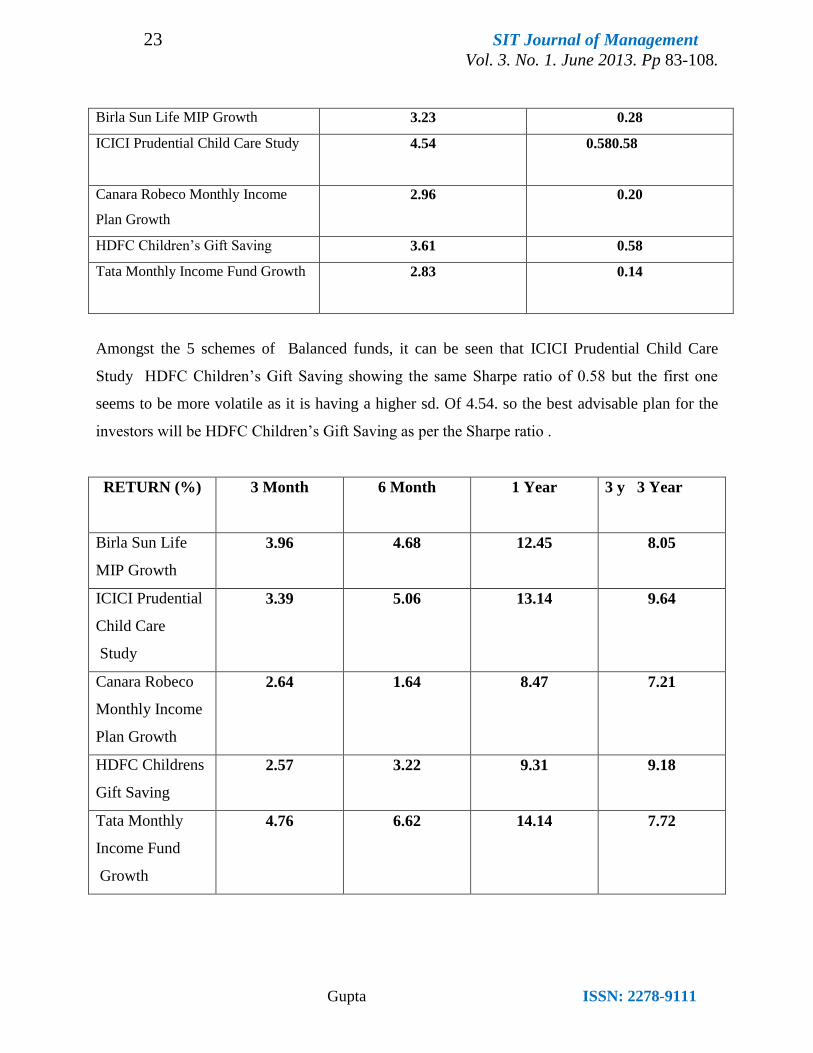

BALANCED FUND SD SHARPE RATIO

23 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Birla Sun Life MIP Growth 3.23 0.28

ICICI Prudential Child Care Study 4.54 0.580.58

Canara Robeco Monthly Income

Plan Growth

2.96 0.20

HDFC Children‟s Gift Saving 3.61 0.58

Tata Monthly Income Fund Growth 2.83 0.14

Amongst the 5 schemes of Balanced funds, it can be seen that ICICI Prudential Child Care

Study HDFC Children‟s Gift Saving showing the same Sharpe ratio of 0.58 but the first one

seems to be more volatile as it is having a higher sd. Of 4.54. so the best advisable plan for the

investors will be HDFC Children‟s Gift Saving as per the Sharpe ratio .

RETURN (%) 3 Month 6 Month 1 Year 3 y 3 Year

Birla Sun Life

MIP Growth

3.96 4.68 12.45 8.05

ICICI Prudential

Child Care

Study

3.39 5.06 13.14 9.64

Canara Robeco

Monthly Income

Plan Growth

2.64 1.64 8.47 7.21

HDFC Childrens

Gift Saving

2.57 3.22 9.31 9.18

Tata Monthly

Income Fund

Growth

4.76 6.62 14.14 7.72

24 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Return Analysis

The 5 schemes of Balanced funds also giving better return in 1 year time span rather than 3

month. 6month, or 3 years. So the most profitable period for investors to invest in this type of

schemes can be said is of 1 year. Again as per the return of the schemes Tata Monthly Income

Fund Growth is giving the maximum return of 14.14% followed by ICICI Prudential Child Care

Study offering a return of 13.14% in 1 year.

So from the risk & return analysis we can see that for a investor who is having low risk appetite

can rightly invest in HDFC Children‟s Gift Saving which is having low risk as well as low

return. On the other hand investors expecting a higher return can invest in Tata Monthly Income

Fund offering a high return & bit risky.

Conclusion

Mutual Fund is offering more lucrative solutions to suit investor‟s expectations. The active

involvement of mutual fund in economic development can be witnessed from dominant presence

of mutual funds in worldwide capital and money market.

Over the time Indian investors have started shifting towards mutual funds instead of traditional

financial avenues. Diversification in mutual funds is coming up with many new faces and as a

result Indian mutual fund industry has been growing exceptionally well on the back of country‟s

booming economy . Findings of this study have got significant managerial implications that can

be used by AMCs in restructuring their existing practices and finally innovating new ways of

service delivery.

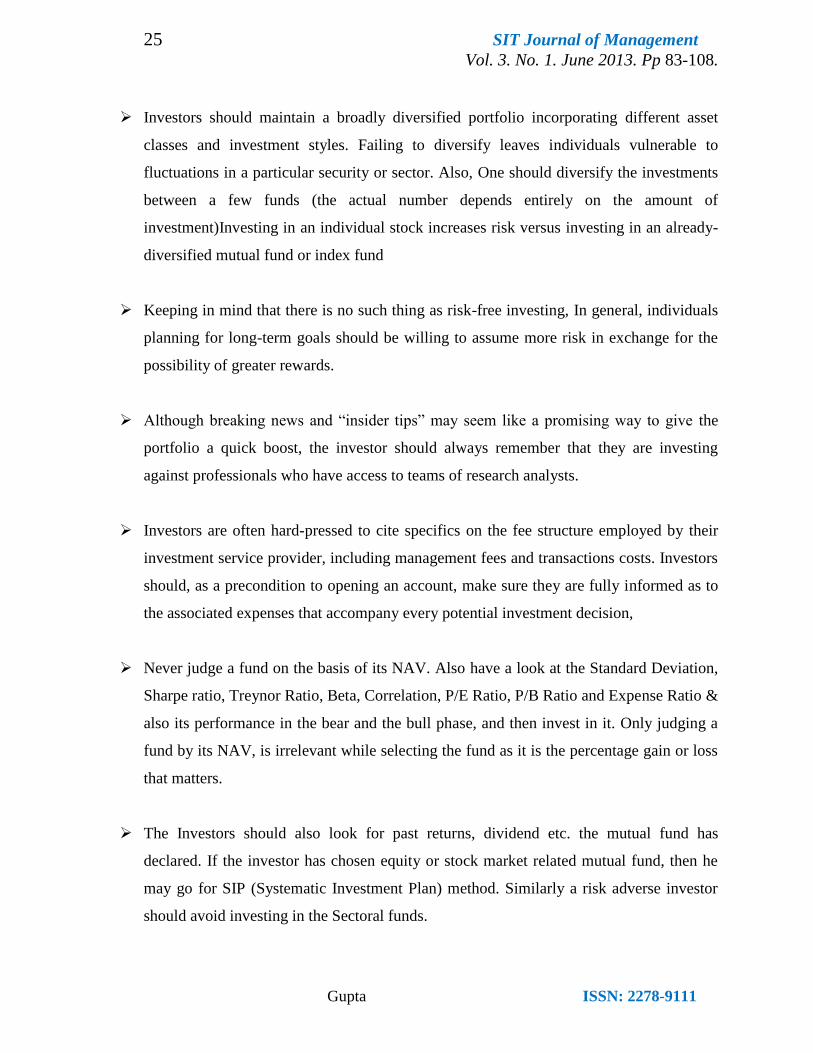

Suggestions

Every investor should form an investment strategy that serves as a framework to guide

future decisions. A well-planned strategy takes into account several important factors,

including time horizon, tolerance for risk, amount of investable assets, and planned future

contributions.

25 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

Investors should maintain a broadly diversified portfolio incorporating different asset

classes and investment styles. Failing to diversify leaves individuals vulnerable to

fluctuations in a particular security or sector. Also, One should diversify the investments

between a few funds (the actual number depends entirely on the amount of

investment)Investing in an individual stock increases risk versus investing in an already-

diversified mutual fund or index fund

Keeping in mind that there is no such thing as risk-free investing, In general, individuals

planning for long-term goals should be willing to assume more risk in exchange for the

possibility of greater rewards.

Although breaking news and “insider tips” may seem like a promising way to give the

portfolio a quick boost, the investor should always remember that they are investing

against professionals who have access to teams of research analysts.

Investors are often hard-pressed to cite specifics on the fee structure employed by their

investment service provider, including management fees and transactions costs. Investors

should, as a precondition to opening an account, make sure they are fully informed as to

the associated expenses that accompany every potential investment decision,

Never judge a fund on the basis of its NAV. Also have a look at the Standard Deviation,

Sharpe ratio, Treynor Ratio, Beta, Correlation, P/E Ratio, P/B Ratio and Expense Ratio &

also its performance in the bear and the bull phase, and then invest in it. Only judging a

fund by its NAV, is irrelevant while selecting the fund as it is the percentage gain or loss

that matters.

The Investors should also look for past returns, dividend etc. the mutual fund has

declared. If the investor has chosen equity or stock market related mutual fund, then he

may go for SIP (Systematic Investment Plan) method. Similarly a risk adverse investor

should avoid investing in the Sectoral funds.

26 SIT Journal of Management

Vol. 3. No. 1. June 2013. Pp 83-108.

Gupta ISSN: 2278-9111

AMC's use NFOs to create excitement and push their funds. These schemes are launched

because they are easy avenues to capture management fees and increase the fund house's

asset base. These schemes are usually just clones of existing schemes, but with new

peppy names flaunted to attract investors.It is important for investors to understand that

NFOs are merely marketing devices. Rather they should opt for such funds which have a

proven track record.

References

Grinblatt, Mark and Sheridan Titman, 1989. "Mutual Fund Performance: An Analysis of Quarterly

Portfolio Holdings." Journal of Business, Vol. 62, No. 3, pp. 393-416

Anjan Chakrabarti and Harsh Rungta, 2000, "Mutual Funds Industry in India : An in depth look into the

problems of credibility, Risk and Brand", The ICFAI Journal of Applied Finance, Vol.6, No.2, April,

27-45

Dr S Narayan Rao, M Ravindran, Manager (2003), Performance Evaluation of Indian Mutual Funds,

SSRNsearch library.

Sharad Panwar and R. Madhumathi ,(2006), Characteristics and Performance Evaluation of

Selected Mutual Funds in India , Indian Institute of Capital Markets 9th Capital Markets Conferenc

Vidya Shankar, S., "Mutual Funds - Emerging Trends in India", Chartered Secretary, Vol.20, No.8, 1990,

639-640.

Soumya Guha Deb , Ashok Banerjee and B. B. Chakrabarti (2007), Indian Institute of Management,

Kolkata, Performance of Indian Equity Mutual Funds vis-a vis Their Style