Embed Size (px)

Citation preview

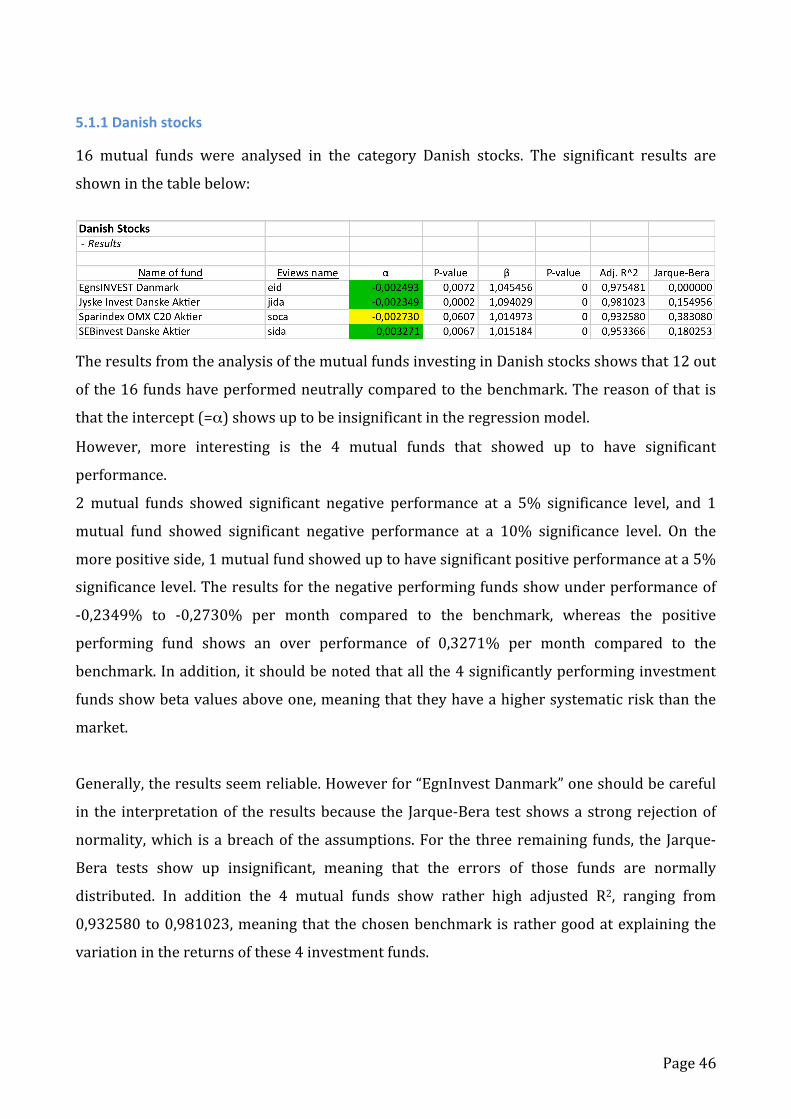

S U P E R V I S O R : M I C H A E L C H R I S T E N S E N P ERFORMANCE EVALUAT ION O F 6 0 DAN I SH

MUTUAL FUNDS

MICHAELVILLADSEN(286274)

U13BSC

AarhusSchoolofBusinessandSocialSciences

Spring11

AbstractIn2011themarketvalueoftheDanishmutualfundsexceededDKK1200billion,investedby

more than 835.000 people. Therefore, the performance by the mutual funds is of great

interest toa largeproportionof theDanishpopulation, andalongwith thehugeamountof

moneymanagedbytheDanishmutualfunds,itisveryimportanttoshedlightonthereturns

thatthemutualfundsareabletoobtain.

Thepurposeofthisthesisisthereforetoprovideaperformanceanalysisof60Danishmutual

funds in the period from 2001‐2009. The analysis will cover three investment categories:

Danishstocks,Europeanstocks,andGlobalstocks.

Thetheoreticalframeworkofthethesisisbuildaroundthetheoryofefficientmarketsandthe

Capital Asset Pricing Model. Consequently, the performance measurements used in the

analysiswillfollowthesetheoriesaswell.Inordertoanalysetheperformanceofthemutual

funds,relevantbenchmarkshavebeenchosen,andthepurposeofthethesisistoseewhether

themutual funds are able to outperform those benchmarks or not. The analysiswill begin

withtheJensenindex,howeverthisisasingleindexmodel,andthereforeitmightnotbeable

toexplainallofthevariationinthereturnsofthemutualfunds.Therefore,theJensenindexis

followedbyamulti‐indexmodel,where4 to7benchmarksare included,dependenton the

investment category of the mutual funds. However, the Jensen index and the multi‐index

modelonlyfocusesontheselectionabilityofthefunds,andthereforeitisdesiredtoseparate

theselectionandtimingabilitiesofthemutualfundsusingtheTreynor&Mazuymodel.

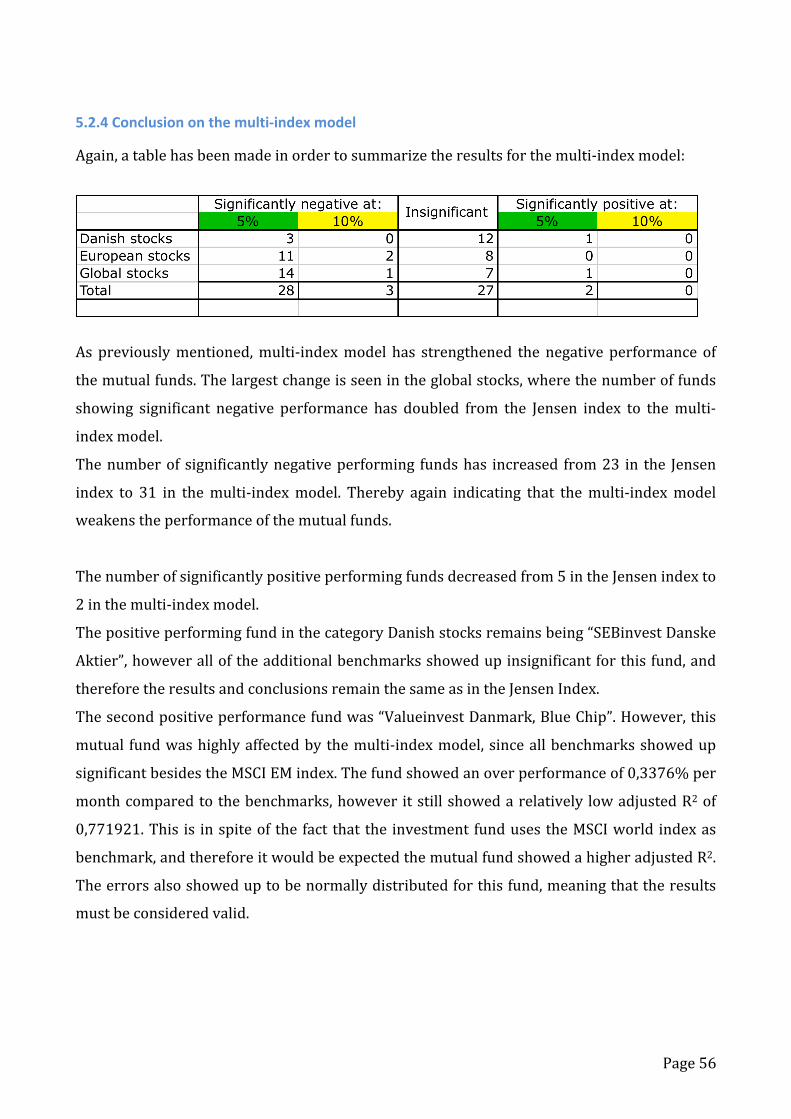

The results from the analysiswere that in the Jensen index, 23 funds underperformed the

index,31fundsperformedneutrally,and6fundsoutperformedtheindex.Inthemulti‐index

model,thesenumberschangedto31,27,and2,respectively,therebyshowinganevenweaker

performancebythemutualfunds.

Takinganaverageofthesetwoanalyseswouldrevealthatclosetohalfof themutual funds

haveperformedsobadthattheyarenotabletocovertheirownexpenses.Thisshouldraise

someconcernregardingtheworkdonebytheDanishmutualfunds.

However,positiveaspectswerealsofoundintheanalysis,sincetwofundsshowedsignificant

positiveperformanceinbothofthemodels.Thosefundsbeing“SEBinvestDanskeaktier”and

“Valueinvest Danmark, Blue Chip” showing a monthly over performance of 0,3271% and

0,3376%, respectively. Itmust thereforebe concluded that these fundshavedone their job

reallywell.

Finally,theTreynorandMazuymodelwasusedtoseparatetheselectionandtimingabilities

ofthemutualfunds.Surprisingly,itwasdiscovedupthat8mutualfundsinvestinginDanish

stocks showed significant timingabilities.However, for the remainingmutual funds, timing

abilities were not present. None of the funds showing timing abilities showed significant

positive selection abilities, and the result of that was that the α values where decreased

comparedtotheJensenindex. Itshouldfinallybenoted,thatnoneofthetwopreviousbest

performingfundsshowedsignificanttimingabilities.

The overall conclusion on the thesis is that one should be careful when selecting mutual

funds. The reason of that is that the returns obtained by the mutual funds compared to

relevantbenchmarksdifferalot,andonewouldthereforeearnsignificantlymoremoneyby

choosingthebestfunds.Finally,itshouldbementionedthathighreturnsofamutualfundin

one period does not guarantee high returns in the following period, and therefore the

selectionofmutualfundsshouldnotsolelybebasedonpreviousreturns.

Tableofcontents

1.INTRODUCTION 1

1.1.PROBLEMSTATEMENT 21.2.DELIMITATION 31.3.THEORETICALFRAMEWORK 3

2.INVESTMENTFUNDSINDENMARK 4

2.1GENERALLYABOUTTHEINVESTMENTFUNDS 42.2LEGISLATION 52.3COSTS 6

3.THEORY 8

3.1EFFICIENTMARKETS 83.2CAPITALASSETSPRICINGMODEL(CAPM) 103.2.1CRITIQUEOFTHECAPITALASSETPRICINGMODEL(CAPM) 123.3RISKMEASUREMENTS 143.3.1SYSTEMATICRISK 143.3.2UNSYSTEMATICRISK 153.4PERFORMANCEMEASUREMENTS 163.4.1JENSEN’SALPHA 183.4.2CRITIQUEOFJENSEN’SALPHA 193.4.3MULTI‐INDEXMODEL 213.4.5MARKETTIMING 23

4.DATA 28

4.1CHOICEOFMUTUALFUNDS 284.2CHOICEOFBENCHMARKS 294.2.1INDEXMETHODOLOGY 304.2.2BENCHMARKFORTHEJENSENINDEX 314.2.3BENCHMARKFORTHEMULTI‐INDEXMODEL 344.3CHOICEOFRISKFREERATE 374.4SURVIVORSHIPBIAS 374.5ASSUMPTIONSFORTHETESTS 39

5.PERFORMANCEANALYSIS 45

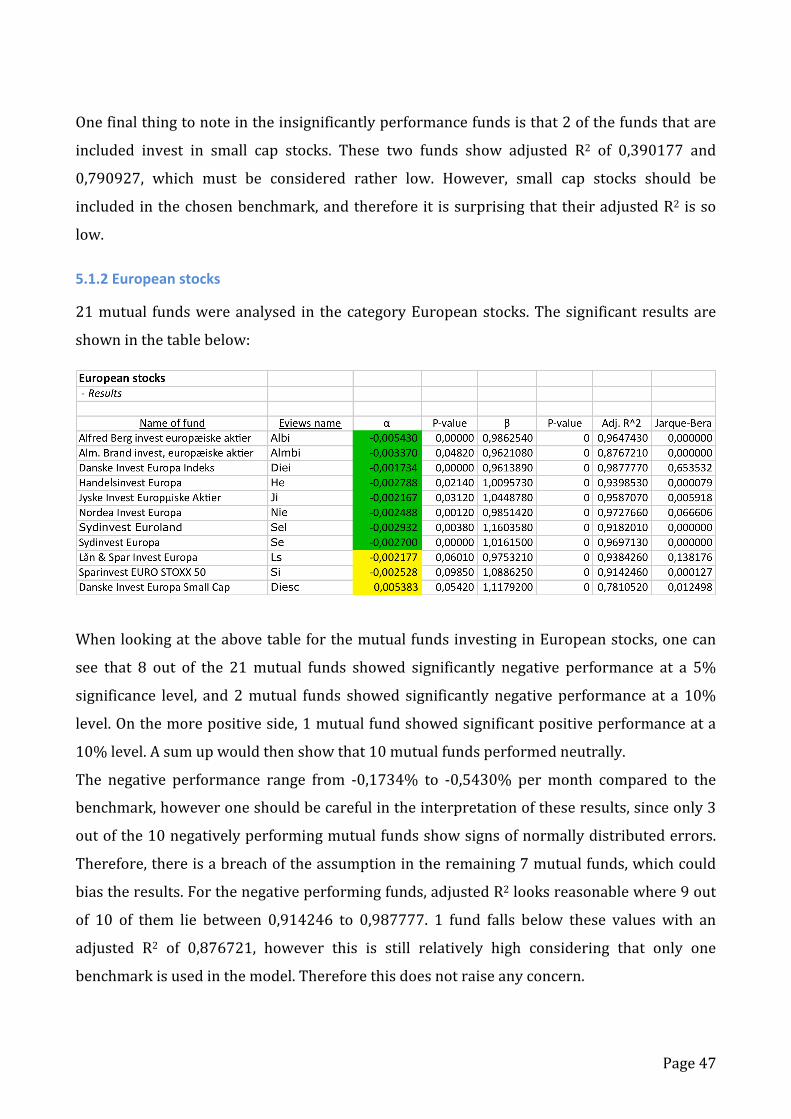

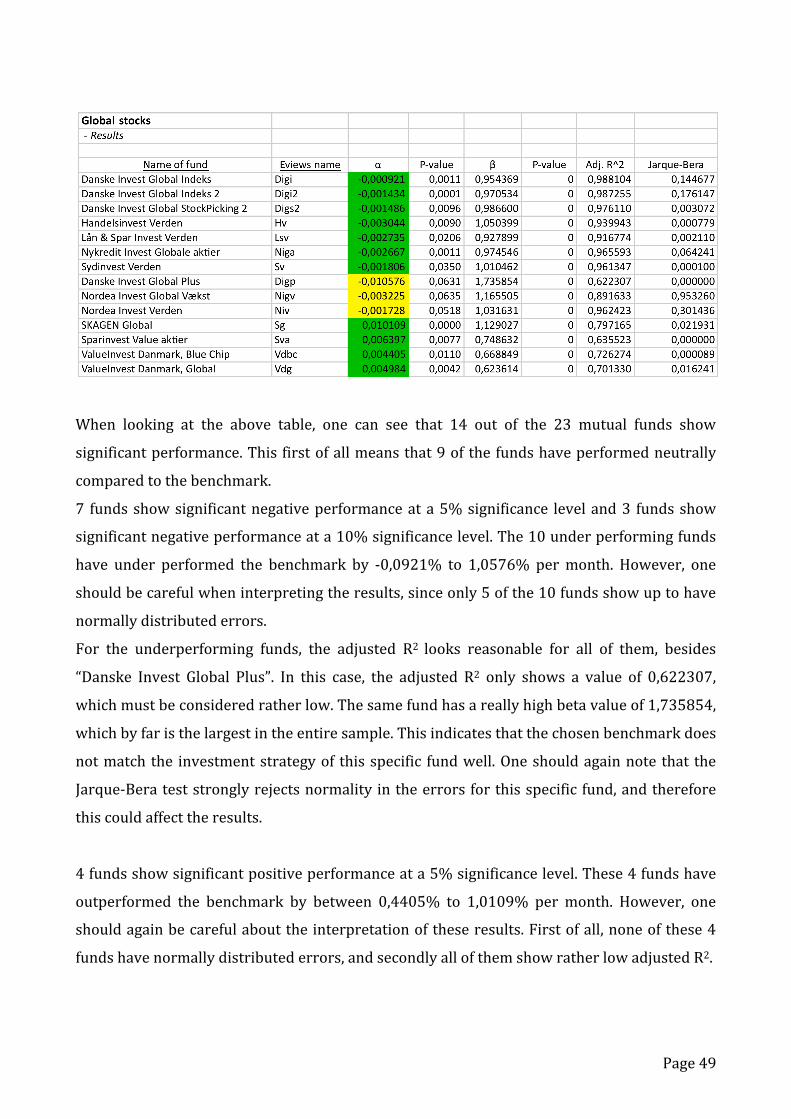

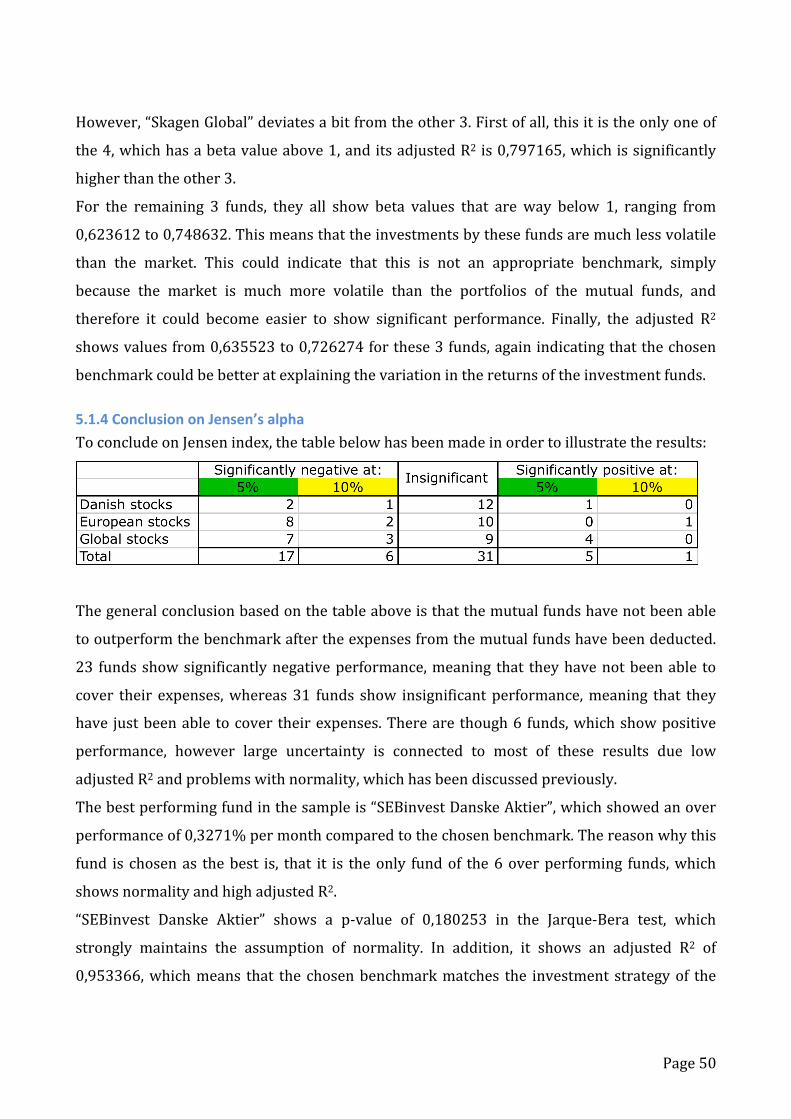

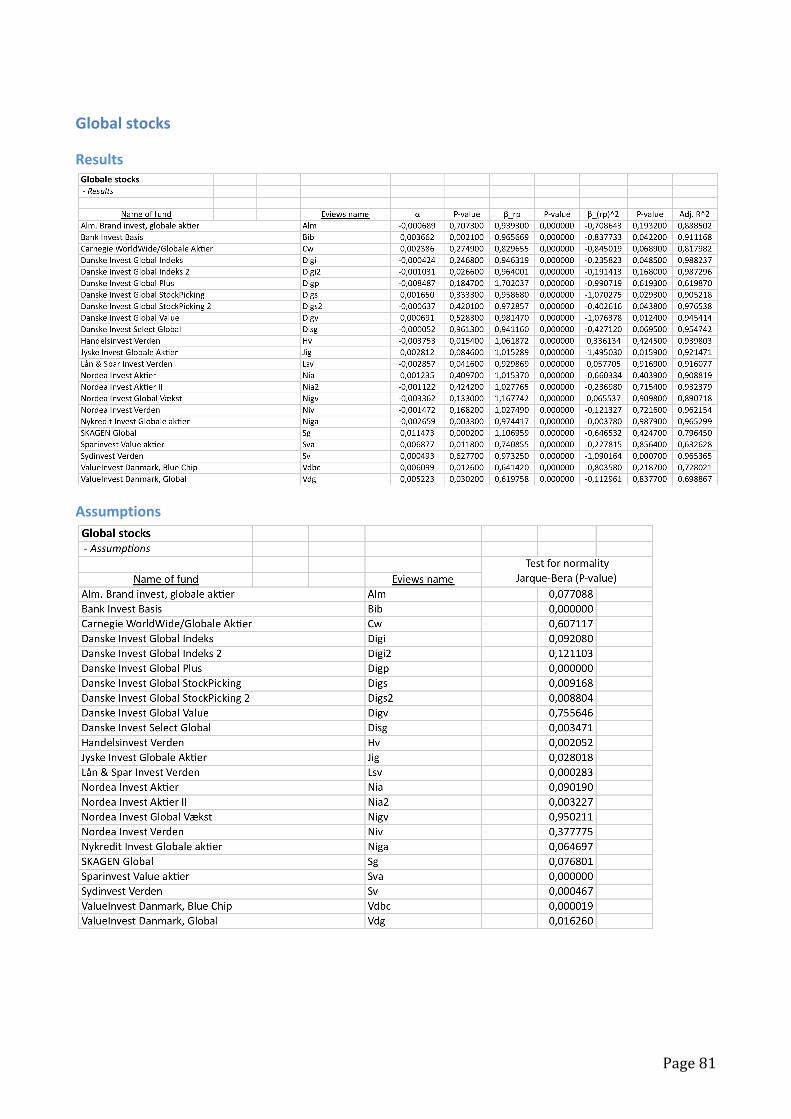

5.1JENSEN’SALPHA 455.1.1DANISHSTOCKS 465.1.2EUROPEANSTOCKS 475.1.3GLOBALSTOCKS 485.1.4CONCLUSIONONJENSEN’SALPHA 505.2MULTIINDEXMODEL 515.2.1DANISHSTOCKS 515.2.2EUROPEANSTOCKS 525.2.3GLOBALSTOCKS 545.2.4CONCLUSIONONTHEMULTI‐INDEXMODEL 565.3MARKETTIMING 575.3.1DANISHSTOCKS 575.3.2EUROPEANANDGLOBALSTOCKS 585.3.2CONCLUSIONONTHETREYNORANDMAZUYMODEL 595.4CONCLUSIONONTHEPERFORMANCEANALYSIS 60

6.DISCUSSIONANDREFLECTIONS 61

7.CONCLUSION 66

8.BIBLIOGRAPHY 68

APPENDIX1:JENSEN’SALPHA 70

DANISHSTOCKS 70RESULTS 70ASSUMPTIONS 70EUROPEANSTOCKS 71RESULTS 71ASSUMPTIONS 71GLOBALSTOCKS 72RESULTS 72ASSUMPTIONS 72

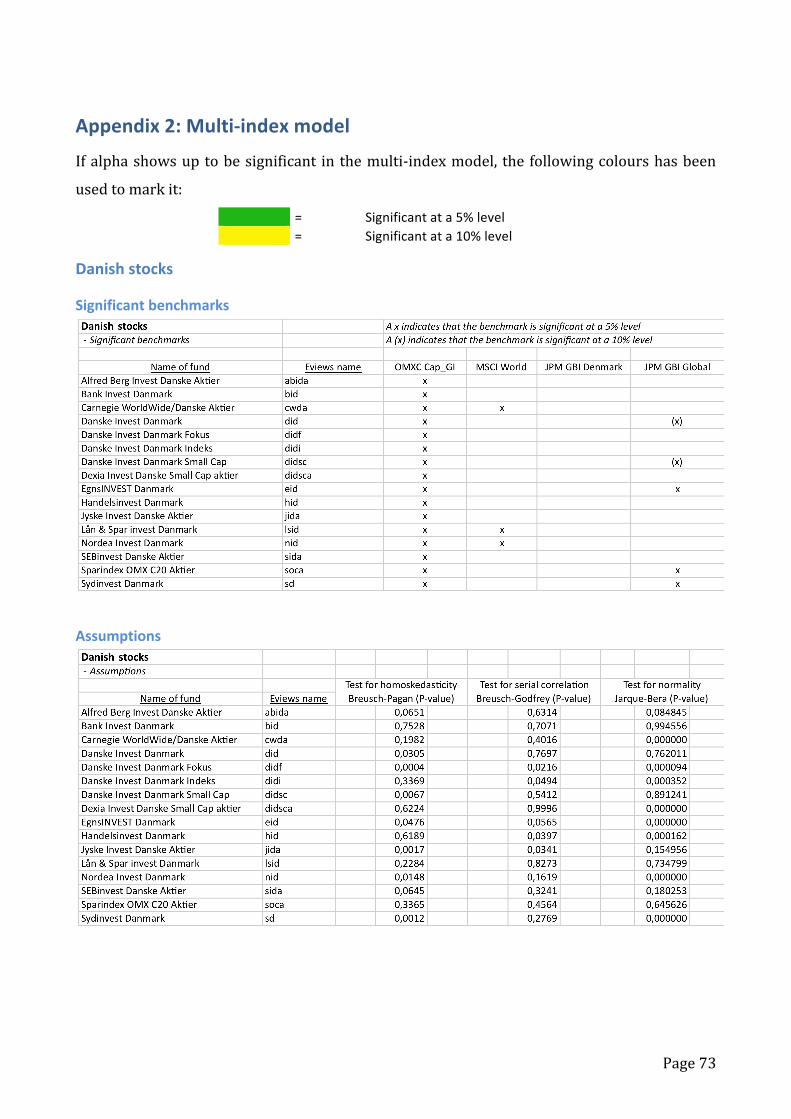

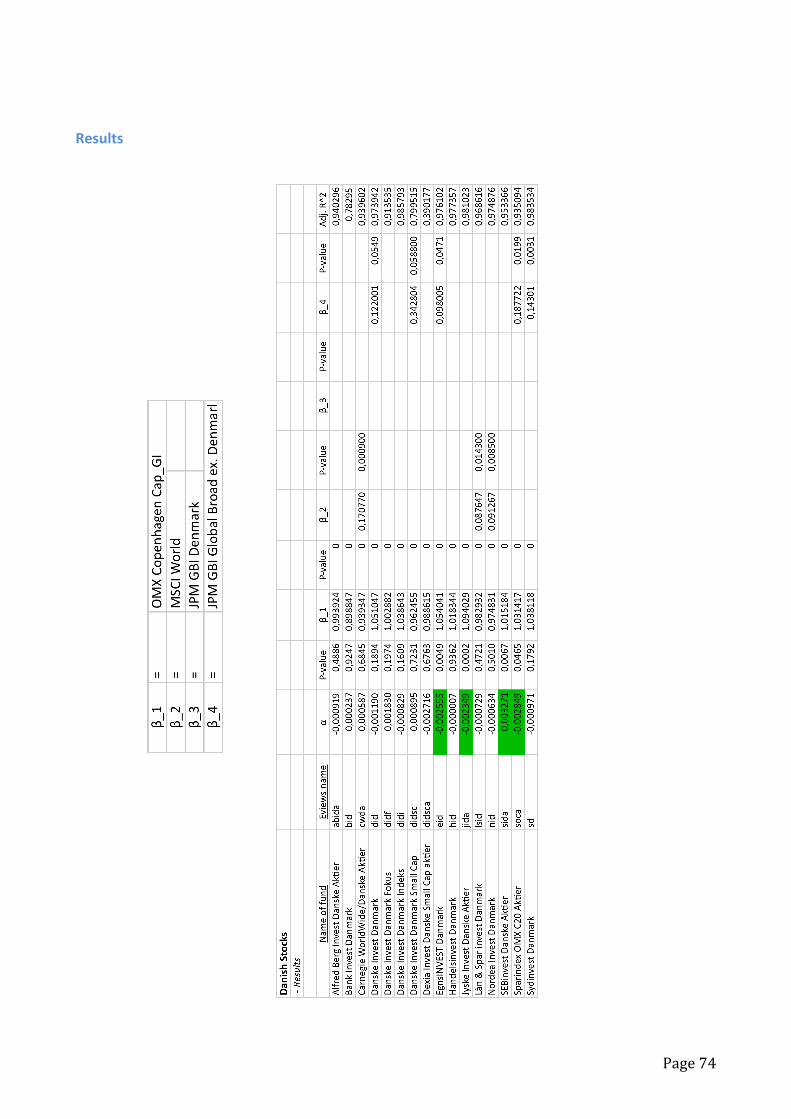

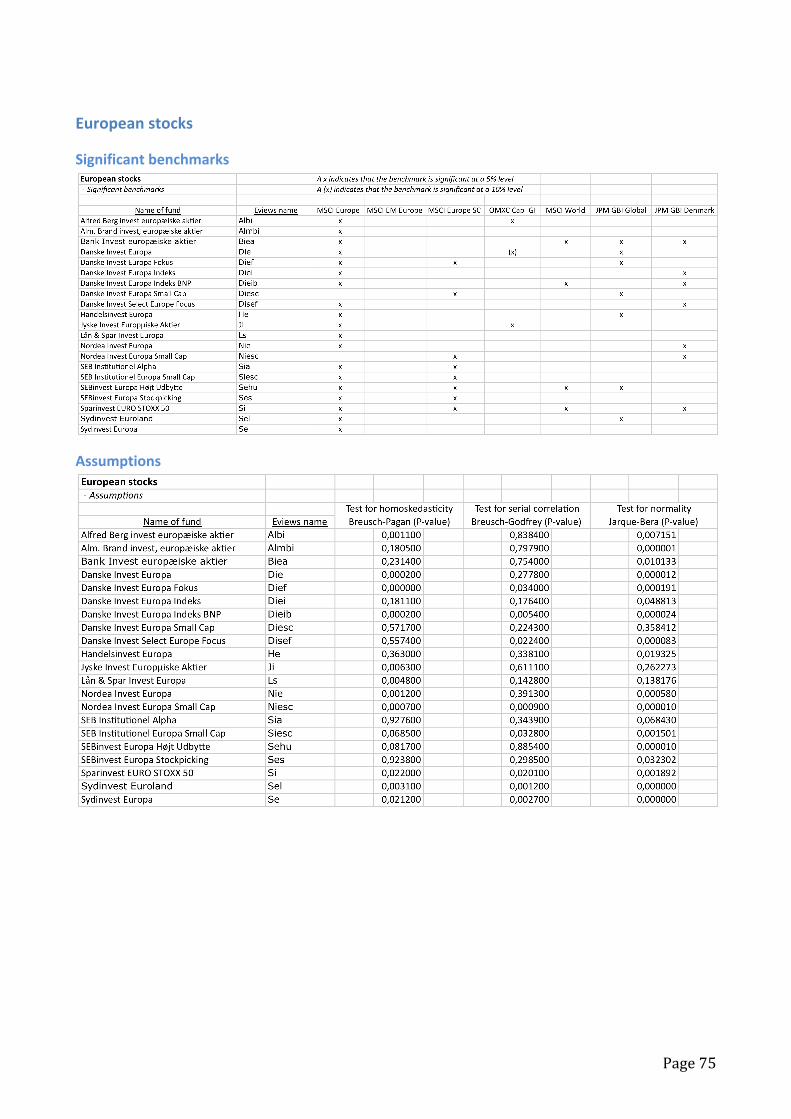

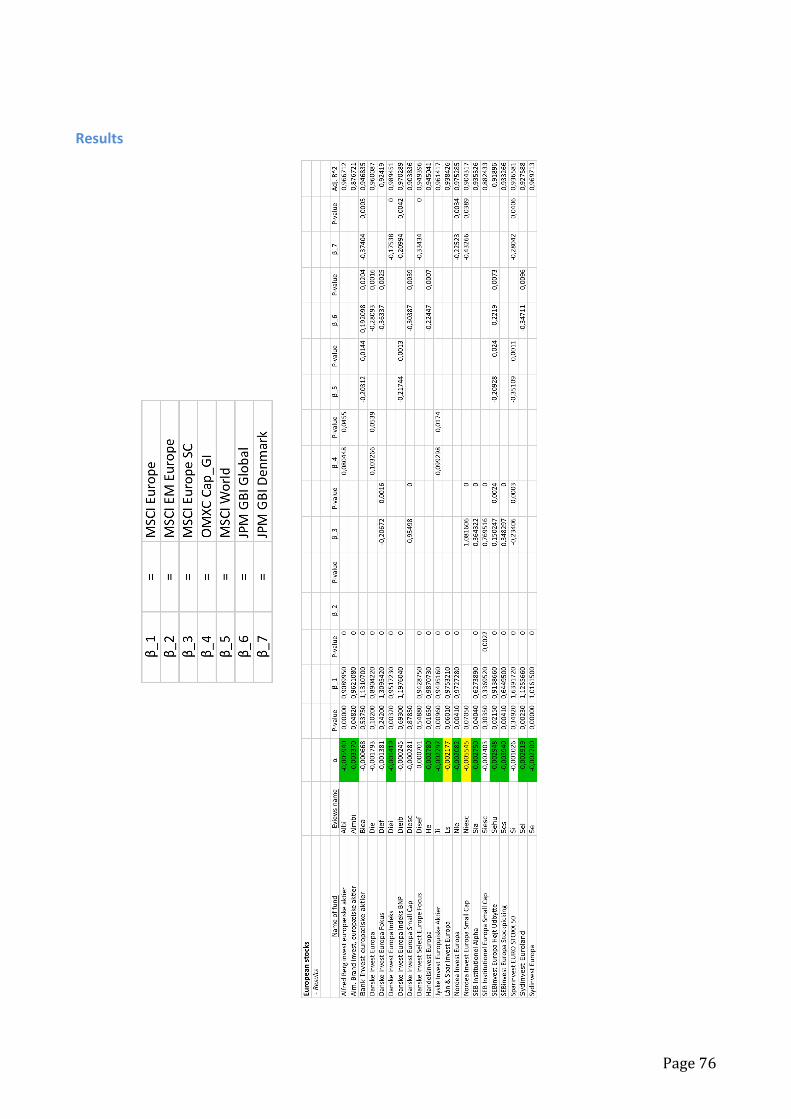

APPENDIX2:MULTIINDEXMODEL 73

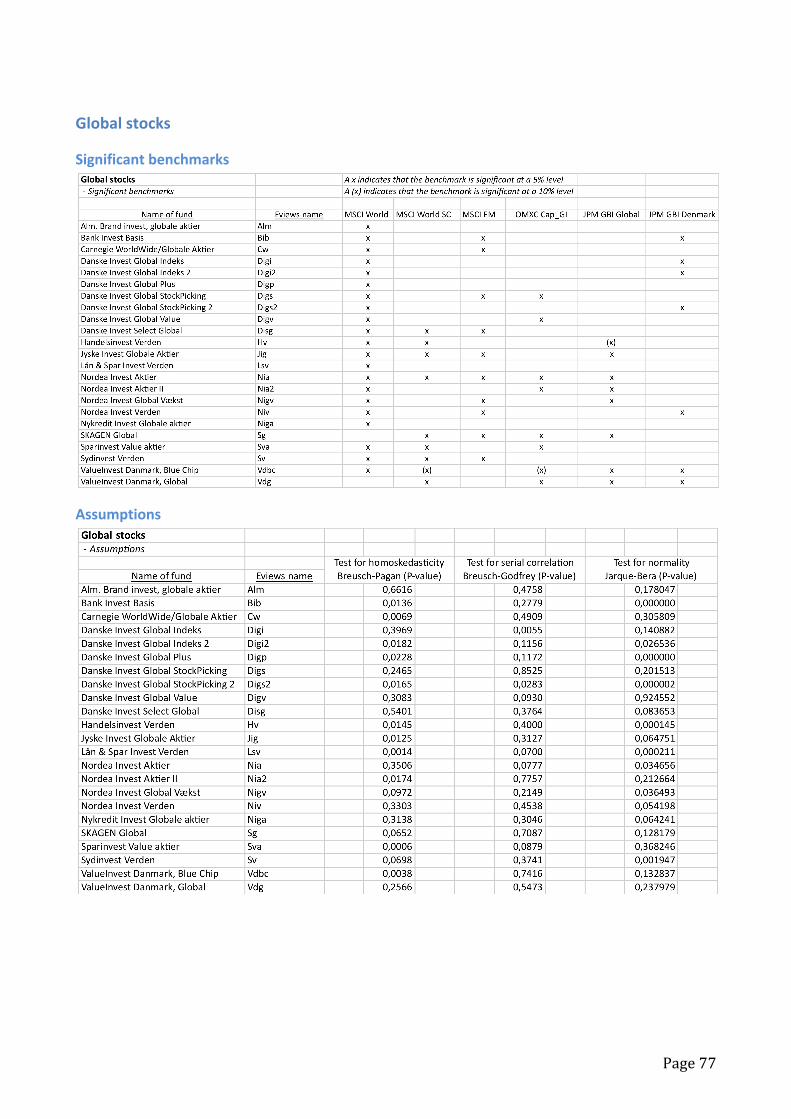

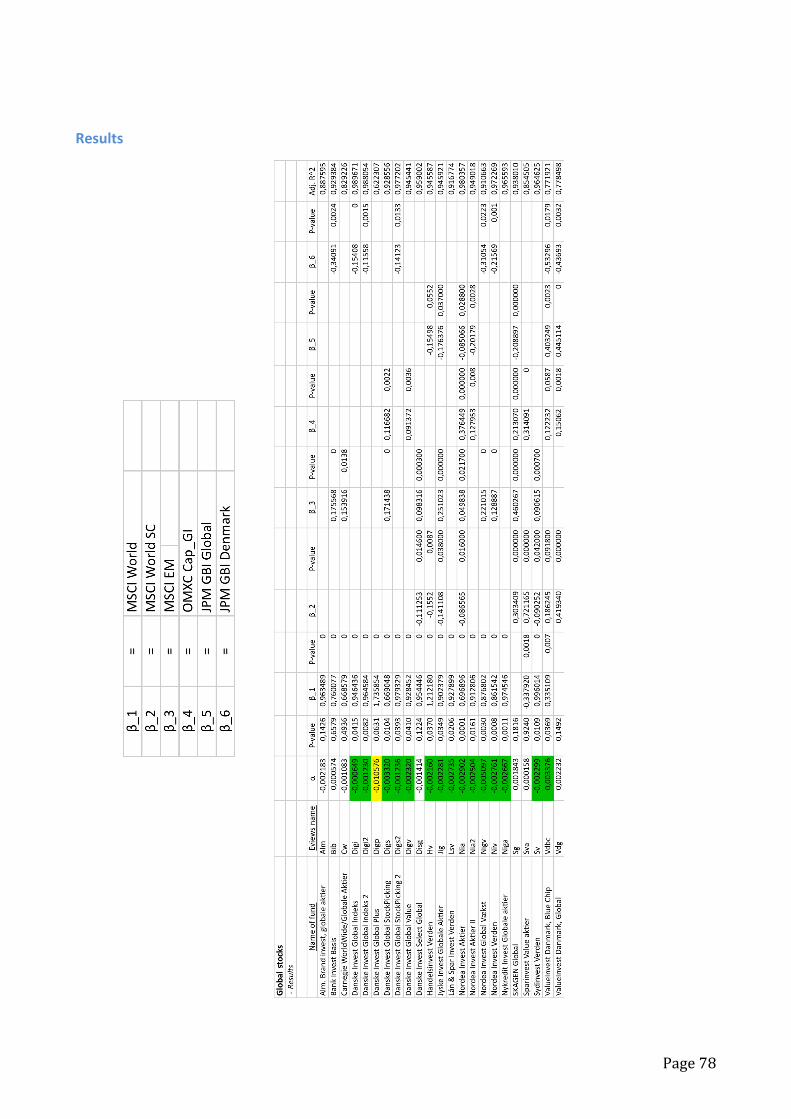

DANISHSTOCKS 73

SIGNIFICANTBENCHMARKS 73ASSUMPTIONS 73RESULTS 74EUROPEANSTOCKS 75SIGNIFICANTBENCHMARKS 75ASSUMPTIONS 75RESULTS 76GLOBALSTOCKS 77SIGNIFICANTBENCHMARKS 77ASSUMPTIONS 77RESULTS 78

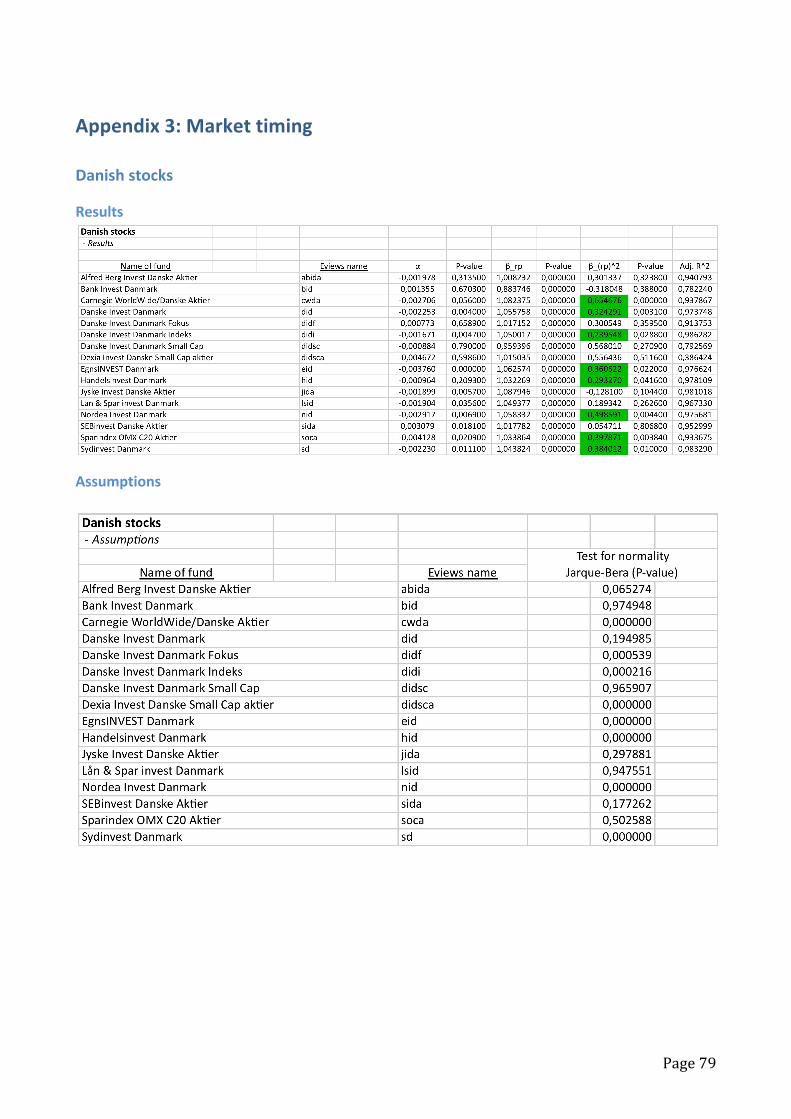

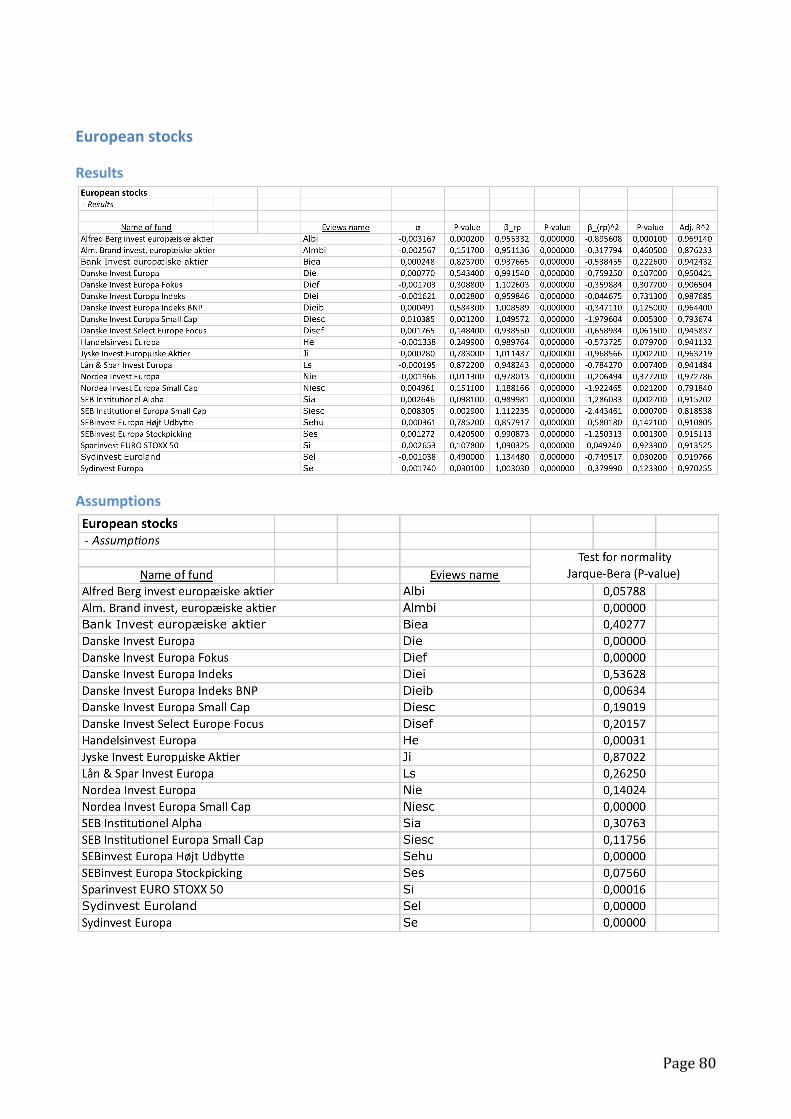

APPENDIX3:MARKETTIMING 79

DANISHSTOCKS 79RESULTS 79ASSUMPTIONS 79EUROPEANSTOCKS 80RESULTS 80ASSUMPTIONS 80GLOBALSTOCKS 81RESULTS 81ASSUMPTIONS 81

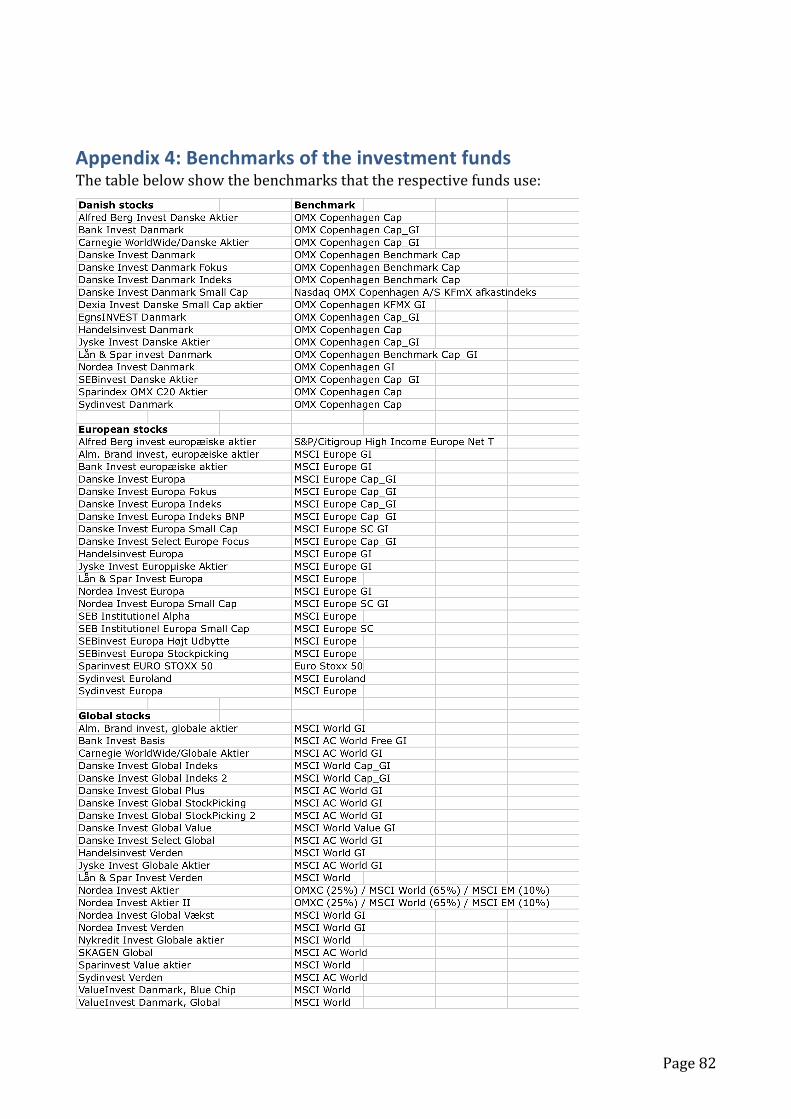

APPENDIX4:BENCHMARKSOFTHEINVESTMENTFUNDS 82

Page1

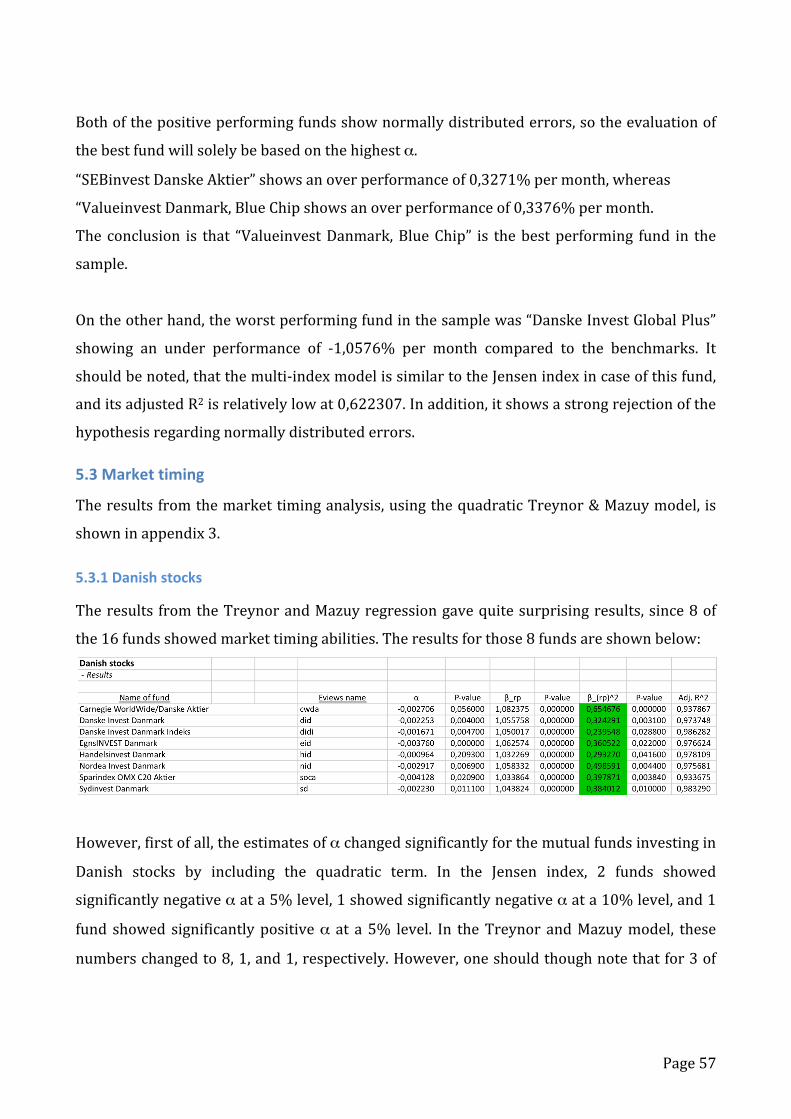

1.IntroductionTheamountofmoneyinvestedintheDanishmutualfundshasexperiencedalargeincreasein

the period from 2001 to 2010, increasing fromDKK 250 billion to DKK 1.200 billion. The

majordevelopmentintheamountofmoneyinvestedputsalargefocusonthereturnsthatthe

mutualfundsareabletoobtain.

Asawiseinvestor,oneshouldbeinterestedinselectingthebestmutualfundstotakecareof

one’smoney.However,thenumberofmutualfundshasalsoincreasedalongwiththeamount

ofmoneyinvested,causingittobecomeevenmoredifficultforaninvestortodecidewhereto

placehismoney.Inordertohelpdecideuponwhichmutualfundstochoosemanydifferent

performance analyses of the mutual funds have been made, some more valid than other.

However, as a general rule proper performance evaluation ofmutual funds should rest on

risk‐adjusted returns, as the investorsmust be considered risk‐averse, therebywanting to

obtainthelargestpossiblereturnwiththesmallestamountofrisk.Inaddition,investorsmust

alsobeinterestedinthereturnthemutualfundhasobtainedcomparedtoarelevantmarket

indexfollowingthereasoning,thatoneshouldnotbesatisfiedwithobtaininga10%returnin

amutualfundifthereturnofthemarketwithasimilarriskhasbeen20%.

Nevertheless, the mutual funds are facing a hard time, following the efficient market

hypothesisbyFama(1970).Theefficientmarkethypothesisstatesthatifamarketisefficient

in it strongest form, then the stock prices would follow a random walk, thereby making

predictionsof futurestockpricesworthless. Ifmarketsareefficient, thetheorystatesthata

passive investment strategy would be the best choice. Still, most mutual funds choose an

activeinvestmentstrategyinthebeliefthattheyareabletomakevaluablepredictionsabout

futurestockpricesenablingthemtooutperformtheirbenchmark.

However, Christensen (2001) argues thatmutual funds can use different strategies, which

maketheirinvestmentslookbettercomparedtotheirbenchmarks.Oneofthembeingthatthe

mutual fund uses a benchmark where dividends are excluded and afterwards including

dividendsinthecalculationoftheirownreturn.AccordingtoChristensen(2001)thiswould

givethemutualfundsaheadstartof2‐3%comparedtotheirbenchmark.

Page2

Another interesting aspects in performance analysis of mutual funds is performance

persistency. Christensen (2004) analysed whether performance persistency exists on the

market forDanishmutual funds.Hereachedtheconclusionthatperformancepersistencyis

non‐existentontheDanishmarket,meaningthatonecannotpredictwhichmutualfundswill

perform thebest in the followingperiodbasedonhow themutual fundsperformed in the

previousperiod.

Consequently, it could be argued that the previous returns are of no relevance to new

investors,sincetheonlyonesbenefitingfromthosearetheinvestorsofthattime.However,

many private investors are still interested in the how mutual funds have performed

previously,sincegoodpreviousperformancecangiveinvestorssomekindof“false”security,

even though this is conflicting with the results reached in the literature regarding

performancepersistency.

Thepurposeofthisthesisistofindthebestperformingmutualfundsintheperiod2001to

2010inthethreemostcommoninvestmentcategoriesfortheDanishmutualfunds,namely

Danish stocks, European stocks, and Global stocks. The evaluation will be based on risk

adjustedreturnsandrelevantbenchmarksincludingdividends.

Thethesiswillshowaninformativepictureoftheperformanceofthemutualfunds,whichcan

beusedinevaluationofwhethertheirobtainedresultsaresatisfactoryornot.Ifonebeliefs

that the performance ofDanishmutual funds is persistent one can also use the analysis to

choosewheretoplaceyourfutureinvestment.

1.1.Problemstatement

Basedontheintroduction,theaimofthethesisistoanalyse60Danishequitymutualfunds

investing in Danish stocks, European stocks, or Global stocks. The period of analysis is 10

yearsrangingfrom2001‐2010.

Thespecificquestions,whichareanalysed,areasfollows:

‐ HowhastheDanishmutualfundsperformedcomparedtorelevantpassivebenchmarks?

‐ DoestheDanishmutualfundspossesstimingabilities?

Page3

1.2.Delimitation

Inordertogetamorethoroughanalysis,certainlimitationshavebeenmadeintheselection

ofthemutualfundsfortheanalysis.

Firstofall,ithasbeendecidedtokeepthefocusinthisthesisonDanishequitymutualfunds.

Thereasonforthischoiceis,thatismustbeexpectedthatthestockmarketsaremorevolatile

compared to the bonds market, and therefore it is found more interesting to analyse the

mutualfundsinvestinginstocks.

Inaddition,ithasbeendecidedtolimittheinvestmentcategoriestoonlythree;thosebeing;

Danishstocks,Europeanstocks,andGlobalstocks.Thereasonforthesespecificchoicesisthat

these three investment categories are themost common for the Danishmutual funds, and

thereforerelativelylargesamplesofmutualfundscanbegatheredineachofthecategories.

The classification of the mutual funds in the three categories will follow the classification

madebytheFederationofDanishInvestmentAssociates(IFR).

Intermsoftheselectionofthemutualfundsforthethesis,ithasbeendecidedonlytoanalyse

mutualfunds,whichhavebeenrunningfortheentireperiodofanalysisfrom2001to2010.

However, this raises the problemof survivorship bias,whichwill be discussed later in the

thesis.Thoughitshouldbenoted,thatthethesishasbeenlimited,sothatsurvivorshipbiasis

notdealtwithintheanalysis.

1.3.Theoreticalframework

The theoriesandanalyses chosen for the thesisareallbuildupon theCapitalAssetPricing

Model (CAPM). Inorder toanalyse theperformanceof theDanishmutual funds, the Jensen

index will be used as a single index model, followed by a multi index model. In order to

separate the selection and timing abilities of themutual funds, the quadratic Treynor and

Mazuymodelwillbeusedaswell.A thoroughdiscussionandargumentation for theuseof

eachofthemodelswillbeincludedinthetheorysection.

Finally, the results thatwill be reached in the analysiswill be compared to similar results

obtainedintheliterature.

Page4

2.InvestmentfundsinDenmark

Thissectionisadescriptivesection,whichwillgiveabriefintroductiontotheDanishmutual

funds. It therefore serves the purpose of providing the reader with some very basic

knowledgeabouttheDanishmutualfunds.

2.1Generallyabouttheinvestmentfunds

TheFederationofDanishInvestmentAssociates(IFR)has30mutualfundsthataremembers

ofthefederation.InbroadtermthismeansthattheDanishinvestorhas30differentmutual

fundstochooseamong.Allofthesemutualfundsthenhavenumerousofdifferentinvestment

portfolios,whichaninvestorcouldchoosetoplacehis/hermoneyin.

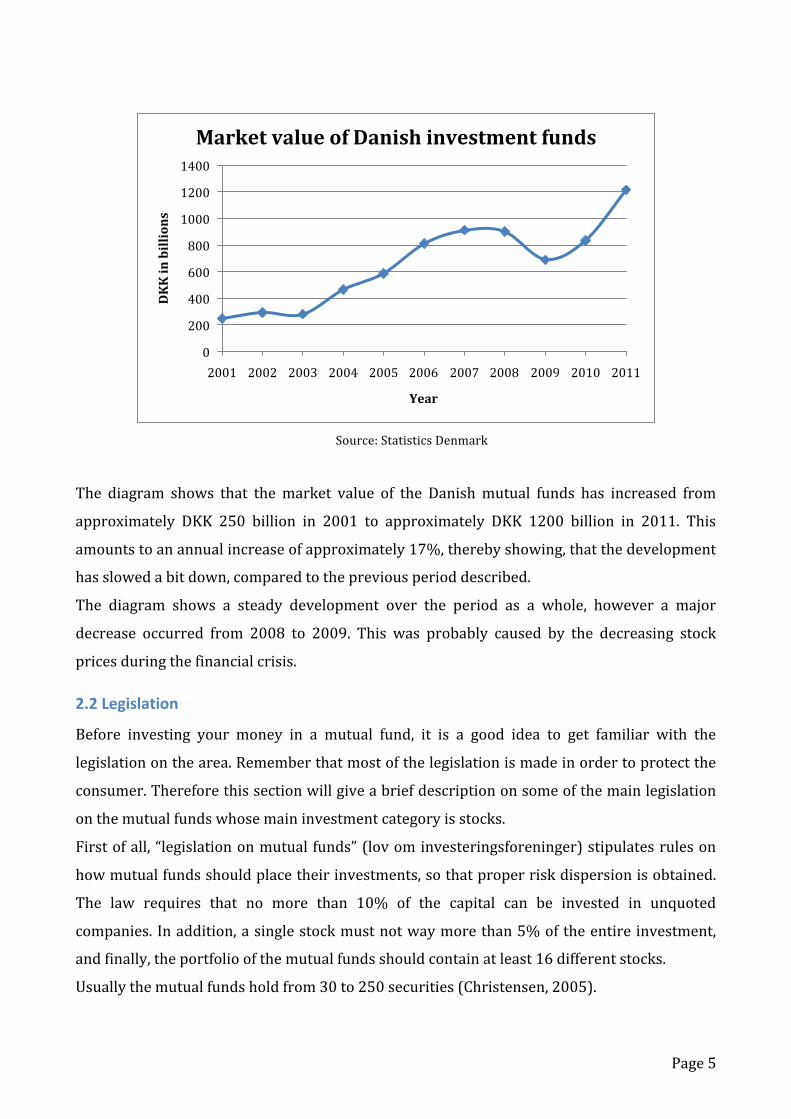

TheamountofmoneyinvestedintheDanishmutualfundsisalsoofinterest.

Christensen(2005)concludesthattherehasbeenatremendousincreaseinthemarketvalue

ofthemutualfundsworldwide,butforDenmarkthedevelopmenthasbeenmuchbiggerthan

fortheEuropeanUnionasawhole.Heconcludes,thatthemarketvalueoftheDanishmutual

funds increased fromUSD3 billion in 1992 toUSD57 billion in 2002. This amounts to an

annual increase of 34%, which can be compared to an annual increase of 18% for the

EuropeanUnion.

However,thesenumbersareratherold,andthereforethebelowdiagramhasbeenmadeto

show how themarket value of the Danishmutual funds has developed over the period of

analysisfrom2001to2010.

Page5

Source:StatisticsDenmark

The diagram shows that themarket value of the Danishmutual funds has increased from

approximately DKK 250 billion in 2001 to approximately DKK 1200 billion in 2011. This

amountstoanannualincreaseofapproximately17%,therebyshowing,thatthedevelopment

hasslowedabitdown,comparedtothepreviousperioddescribed.

The diagram shows a steady development over the period as a whole, however a major

decrease occurred from 2008 to 2009. This was probably caused by the decreasing stock

pricesduringthefinancialcrisis.

2.2Legislation

Before investing your money in a mutual fund, it is a good idea to get familiar with the

legislationonthearea.Rememberthatmostofthelegislationismadeinordertoprotectthe

consumer.Thereforethissectionwillgiveabriefdescriptiononsomeofthemainlegislation

onthemutualfundswhosemaininvestmentcategoryisstocks.

Firstofall, “legislationonmutual funds”(lovominvesteringsforeninger)stipulatesruleson

howmutualfundsshouldplacetheirinvestments,sothatproperriskdispersionisobtained.

The law requires that no more than 10% of the capital can be invested in unquoted

companies.Inaddition,asinglestockmustnotwaymorethan5%oftheentireinvestment,

andfinally,theportfolioofthemutualfundsshouldcontainatleast16differentstocks.

Usuallythemutualfundsholdfrom30to250securities(Christensen,2005).

0

200

400

600

800

1000

1200

1400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

DKKinbillions

Year

MarketvalueofDanishinvestmentfunds

Page6

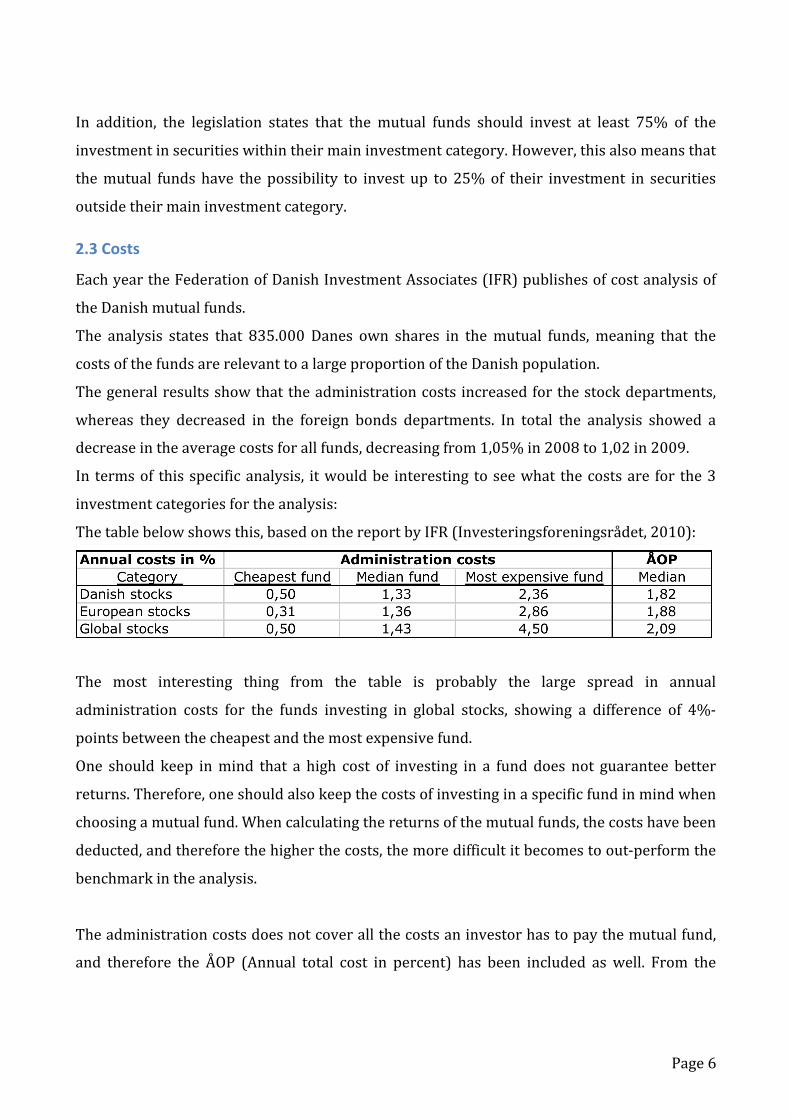

In addition, the legislation states that the mutual funds should invest at least 75% of the

investmentinsecuritieswithintheirmaininvestmentcategory.However,thisalsomeansthat

themutual funds have the possibility to invest up to 25%of their investment in securities

outsidetheirmaininvestmentcategory.

2.3Costs

EachyeartheFederationofDanishInvestmentAssociates(IFR)publishesofcostanalysisof

theDanishmutualfunds.

The analysis states that 835.000 Danes own shares in themutual funds,meaning that the

costsofthefundsarerelevanttoalargeproportionoftheDanishpopulation.

Thegeneralresultsshowthattheadministrationcosts increasedforthestockdepartments,

whereas they decreased in the foreign bonds departments. In total the analysis showed a

decreaseintheaveragecostsforallfunds,decreasingfrom1,05%in2008to1,02in2009.

In termsof thisspecificanalysis, itwouldbe interesting toseewhat thecostsare for the3

investmentcategoriesfortheanalysis:

Thetablebelowshowsthis,basedonthereportbyIFR(Investeringsforeningsrådet,2010):

The most interesting thing from the table is probably the large spread in annual

administration costs for the funds investing in global stocks, showing a difference of 4%‐

pointsbetweenthecheapestandthemostexpensivefund.

One should keep inmind that a high cost of investing in a fund does not guarantee better

returns.Therefore,oneshouldalsokeepthecostsofinvestinginaspecificfundinmindwhen

choosingamutualfund.Whencalculatingthereturnsofthemutualfunds,thecostshavebeen

deducted,andthereforethehigherthecosts,themoredifficultitbecomestoout‐performthe

benchmarkintheanalysis.

Theadministrationcostsdoesnotcoverallthecostsaninvestorhastopaythemutualfund,

and therefore the ÅOP (Annual total cost in percent) has been included as well. From the

Page7

numbers it is seen that among the three, investments in Danish stocks are the cheapest,

whereasinvestmentsinglobalstocksarethemostexpensive.

It therefore implies that if one decides to invest in a category,which has higher costs, one

shouldalsoexpectthatthesewillgiveahigherreturn(Investeringsforeningsrådet,2010)

Page8

3.TheoryThis section will cover the theory, which will be used in the analysis. It is therefore an

extensionofthetheoreticalframework,explainingdifferenttheoriesandwhytheyhavebeen

chosen. The theory will start by going into the theory of the efficient market hypothesis

followed by a discussion of the Capital Asset PricingModel. The reason of that is that the

performancemeasurementsused intheanalysis isbuilduponthosetheories,andtherefore

theylaythefoundationforthelaterexplanationofthetheoriesusedintheanalysis.

3.1Efficientmarkets

Anefficientmarket isdefinedasamarketwhereall information iscontained inthecurrent

stock price. Therefore, if a market is efficient, it would not be possible to find misvalued

stocks. The reasoning behind this is supply and demand. If a stock is overvalued, then

investorswillsellthestock,whereasinvestorswillpurchaseundervaluedstocks.Therefore,

supply and demandwill quickly adjust the price to a correct level, thereby eliminating the

opportunityofearningsuperiorprofitsoveralongperiodoftime.Inotherwordsthiswould

alsomean,thatnotevenareallyhardworkingmanwouldbeabletoearnsuperiorprofits.If

thisisthecase,thentheefficientmarkethypothesisissaidtobefulfilled(Brealeyetal.,2007).

In1970EugeneF.Famafoundtheneedtofurtherdeveloptheefficientmarkethypothesis.

Hearguedthatwhenanefficientmarketisdefinedasamarketthatfullyreflectallavailable

information, then the null hypothesis would be rather extreme, and therefore one cannot

expectittobeliterallytrue.Therefore,hedividedtheefficientmarkethypothesisintothree

subcategories,whichcouldindividuallybetested.

Weakformefficiency:Thistypeofefficiencyischaracterizedbythefactthatpricesreflectall

theinformation,whichiscontainedinthehistoricprices.Changesinthestockpricesaresaid

to follow a random walk, and therefore analysis of patterns in previous stock prices are

valuelesswhentryingtopredictfuturestockprices.

Semistrong form efficiency: This type of efficiency is similar to the weak form efficiency,

however this also includes all public available information. This means, that one simply

Page9

cannotearnsuperiorprofitsjustbyreadingthefinancialpress,studyingfinancialstatements,

etc. In other words this implies, that in the moment new information about a company

becomespublic,thenthestockpricewillimmediatelyadjusttothat.

Strong formefficiency:The last formofefficiency is thestrong formefficiency,whereprices

includeallavailableinformation.Thismeansthatinformationsuchas“insider”informationis

alsocontainedinthestockprice,andtherefore,itisabsolutelyimpossibleforaninvestorto

earnsuperiorprofits.

The advantageof dividing the efficientmarkethypothesis into threewas, that if itwasnot

fulfilled, then one would be able to pinpoint exactly at which level of information the

hypothesisbreaksdown.

In Fama’s analysis he found that there was no important evidence against the weak and

semistrongformefficiency,andthattherewasonlylimitedevidenceagainstthestrongform

efficiency.Whenrelating this to theperformanceofmutual funds, thiswouldmeanthathis

analysispoints inthedirection, thatmutual fundsshouldnotbeabletooutperformpassive

marketindexes.Thesimplereasoningbehindthatis,thatifthestockmarketisfullyefficient,

noanalysisofanykindcouldhelppredictthefuturestockprices,therebyenablingthespecific

fundtoearnsuperiorprofitsoveralongerperiodoftime(Fama,1970).

In1991EugeneF. Famaconducteda similar analysisofmarket efficiency,however, in this

analysishenamedthethreetypesofmarketefficiencydifferently.Theywerecalled:

1.Testforreturnpredictability

2.Eventstudies

3.Testsforprivateinformation

Thesecondandthethirdcategoryhavethesamecoverageaspreviously,but justwithnew

names. Themain difference lies in the first category, which besides the forecasting power

basedonpastreturnsnowalso includethingsas forecastsbasedonvariables likedividend

yields,interestrates,seasonality,etc.

TheresultfromFama’sanalysiswas,thatheconcludedthatreturnswerepredictablebased

uponpastreturns,dividendyields,etc(Fama,1991).

Page10

Toconcludeonthemarketefficiency,onecansaythatifyoubelieveinmarketefficiencyinit

strongest form, then your best choice would simply be to choose a passive investment

strategy. The reasonof that is, that if themarket is efficient in its strongest form, then the

stockpriceswill followarandomwalk.Therefore, thebest thingyoucandoasan investor

wouldbetominimizeyourtradingcostsandinformationseekingcosts.

However,itdoesnotseemasifmutualfundsbelieveinmarketefficiencyinitsstrongestform,

since many of them choose an active investment strategy. Hence, they must believe that

through different kinds of analysis, they would be able to outperform the market. This is

identical totheresultsFamareached inhissecondanalysisofmarketefficiencyfrom1991,

whereheconcludesthatitwaspossibletopredictfuturestockreturns.

Inrelationtothisthesis,thisindicatesthatthereisapossibilitythatthemutualfundsareable

tooutperformthemarket.

3.2CapitalAssetsPricingModel(CAPM)

CAPM was among others developed by William F. Sharpe in 1964, and together with the

efficientmarkethypothesis,thecapitalassetpricingmodelformsthetheoreticalframework

formanyfinancialanalyses.

Asthenamesuggests,itisamodel,whichisusedtodeterminethepriceofcapitalassets.

Basically,themodelisbuildupontwothings;firstly,ariskpremiumbaseduponbetaandthe

marketriskpremiumandsecondly,therisk‐freerate(Brealeyetal.,2007).

CAPMisbaseduponthesecuritymarketline(SML),shownbelow:

SML: Riskpremiumoninvestment=beta*expectedmarketriskpremium.

Thismeans that according to SML the risk premium youwould earn on our investment is

equaltotheexpectedmarketriskpremiummultipliedbythesystematicriskyouarewilling

totake.

Page11

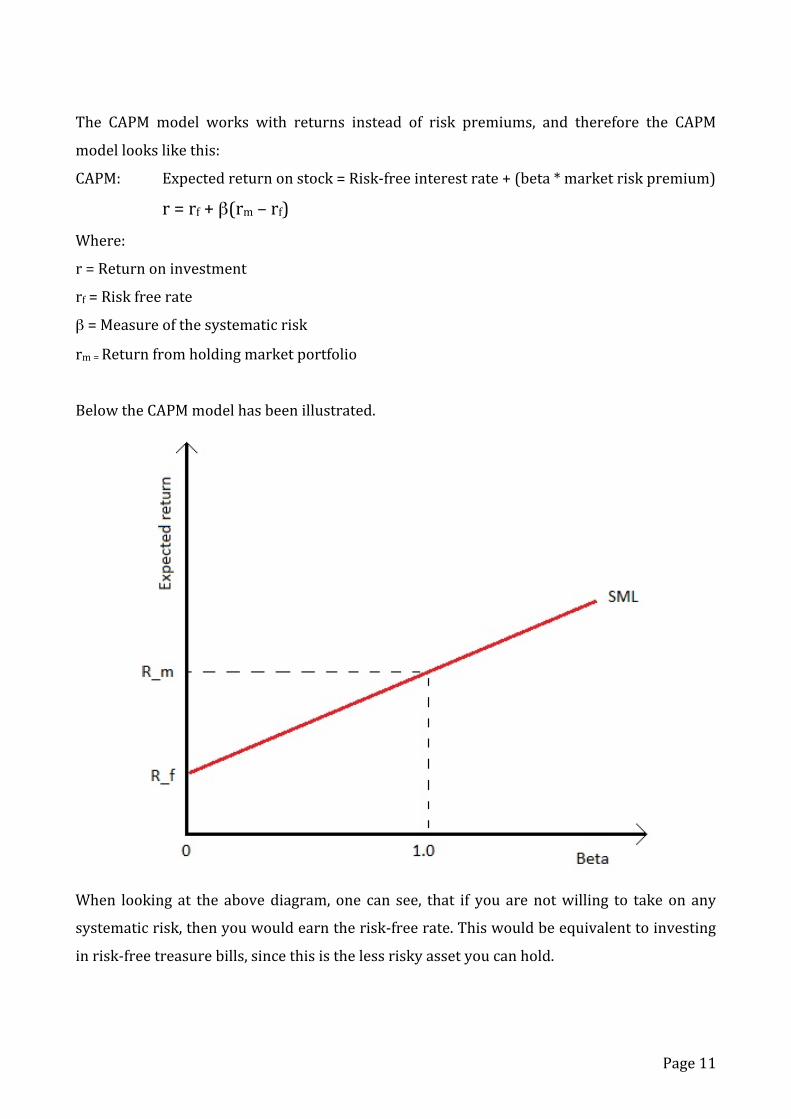

The CAPM model works with returns instead of risk premiums, and therefore the CAPM

modellookslikethis:

CAPM: Expectedreturnonstock=Risk‐freeinterestrate+(beta*marketriskpremium)

r=rf+β(rm–rf)

Where:

r=Returnoninvestment

rf=Riskfreerate

β=Measureofthesystematicrisk

rm=Returnfromholdingmarketportfolio

BelowtheCAPMmodelhasbeenillustrated.

When looking at the abovediagram,one can see, that if you arenotwilling to takeon any

systematicrisk,thenyouwouldearntherisk‐freerate.Thiswouldbeequivalenttoinvesting

inrisk‐freetreasurebills,sincethisisthelessriskyassetyoucanhold.

Page12

Ontheotherhand,ifaninvestorinvestedeverythinginthemarketportfolio,thenhewould

haveabetaof1.AccordingtotheCAPMmodel,hewouldthenearnthemarketreturn.

TheessenceoftheCAPMisthatyouarerewardedbyareturnontheSMLlinedependonthe

risk(β)youarewillingtotake(Brealeyetal.,2007).

3.2.1CritiqueoftheCapitalAssetPricingModel(CAPM)

The CAPM has received a lot of critique for being based upon assumptions, which are so

theoretical,thattheyareunrealisticinapracticalsense.

TheCAPMassumptionsareasfollows(Mullins,1982)and(Jensen,1967):

1. Thesecuritymarketiscompetitiveandefficient.

2. Investorsarerationalandrisk‐averse,andthereforewanttomaximizereturnsbasedon

therisktheyaretaking.

3. Themarketisfrictionless,andthereforeitdoesnotincludetransactioncosts,taxes,and

restrictionsonborrowingandshortselling.

4. Allinvestorscanborrowandlendunlimitedamountsattheriskfreerate.

5. Investors agree on common expectations about performance and risk of all securities

(thereforeallinvestorshavethesameprobabilityofgettingcertainfuturereturns).

6. Allinvestorshavethesametimehorizonfortheirinvestments.

7. Thepriceofsecuritiesisnotaffectedbysalesandpurchasesofindividualinvestors.

8. Allinvestorshavethesameopportunitiesofinvestingindifferentstock.Inotherswords,

allinvestorshavethepossibilitytopurchaseeachandeverysecurityinthemarket.This

wouldalsorequirethesecuritiestobe infinitelydivisible,sothatsothatevery investor

hasthesameinvestmentopportunitiesindependentoftheparticularinvestor’sfortune.

When reading through theseassumptionsofCAPM,one caneasily see, that theyare rather

theoretical, and therefore, it is impossible to fully fulfil theseassumptions in reality. Just to

discuss a few, one can mention that it is doubtful whether all investors have the same

investmentopportunitiesindependentlyoffortune.Thereasonofthatis,thatsomesecurities

areveryexpensiveandnotdividable,meaningthatitrequiresaratherlargefortunetoinvest

in those securities. Thiswill limit the opportunities for the lesswealthy investors. If a less

wealthy investorwantstheopportunityof investing inallsecurities,hewouldhavetodo it

Page13

throughamutual fund.Therebyhewouldhavetopaysomecosts for investingthroughthe

fund.

Even foran investornotusingamutual fund, it isverydoubtful thathehasno transaction

costs. The reason of that is, that for private investors there is some sort of brokerage on

literallyeverytransaction.

InspiteofthecritiqueanddoubtfulassumptionsregardingCAPM,onemightwonderwhether

themodel isworthanything inreal life.Thesimpleanswer isyes. It isnotaperfectmodel,

howeveritisveryuseful.

In1982DavidW.Mullins,Jr.conductedananalysisofwhethertheCAPMworks.Theresults

fromhisanalysiswerethatCAPMwasnotperfect,however itwasaveryusefuladditionto

otheranalytical toolkits.He furtherargued thateven though theassumptionsofCAPMare

very theoretical and unrealistic, it is often necessary to simplify reality in that manner in

ordertodevelopusefulmodels.Inadditionhearguesthattheunderlyingassumptionsofthe

modelarenotnecessarilythemostimportantthings,andthatimportanceshouldbeattached

tothevalidityandusefulnessofthemodel’sprescription.

ResultsfromdifferentanalysesofCAPMhaveshownthatasameasureofrisk,betaseemsto

be related to past returns. In addition, the relationship between past returns and beta has

shown to be linear, and that the relationship between the two is positively sloped. Finally

research has shown, that CAPM overestimates returns for low beta securities and

underestimatereturns forhighbetasecurities.Thiswill cause that theempiricalSML tobe

lesssteeplyslopedthanthetheoreticalSML(Mullins,1982).

To briefly sumup on the empirical tests of CAPM, one can say that they do not absolutely

validatethemodel,howevertheysupportsomeofthemainimplicationsofCAPM.Firstofall,

theysaythatthesystematicrisk(beta)appearstoberelatedtopastreturns,secondly, that

thereisapositiverelationsbetweenriskandreturn,andfinally,thattherelationshipbetween

riskandreturnappearstobelinear.

Theperformancemeasurements thatwill beused in this thesis arebaseduponCAPM, and

thereforethevalidityofCAPMofimportanceforthisthesis.

Page14

3.3Riskmeasurements

Infinanceyouoftendistinguishbetweentwodifferenttypesofrisk,andthereforethesewill

brieflybeexplainedinordertoavoidconfusion.Theperformancemeasurementsusedinthis

analysis only focuses on the systematic risk, and therefore thedistinctionbetween them is

important.

3.3.1Systematicrisk

Thesystematicriskistherisk,whichliesinthemarket.Therefore,thisriskcannotbeavoided

regardless of how diversified your portfolio is. In other words it can be said that the

systematicriskisamacroeconomicrisk,simplybecausethatitisariskwhichtosomeextent

will affect the entire market. An example of this systematic risk, which affects the entire

market, could be the latest financial crisis, or simply just fluctuations of the market. The

degreetohowmuchasecurityisaffectedbythesystematicriskdependsonitsbeta(whichis

thenotationforsystematicrisk)(Brealey,2007).

Securitieswithlowbetaswillbelessaffectedbymacroeconomicchangesthansecuritieswith

highbetas.

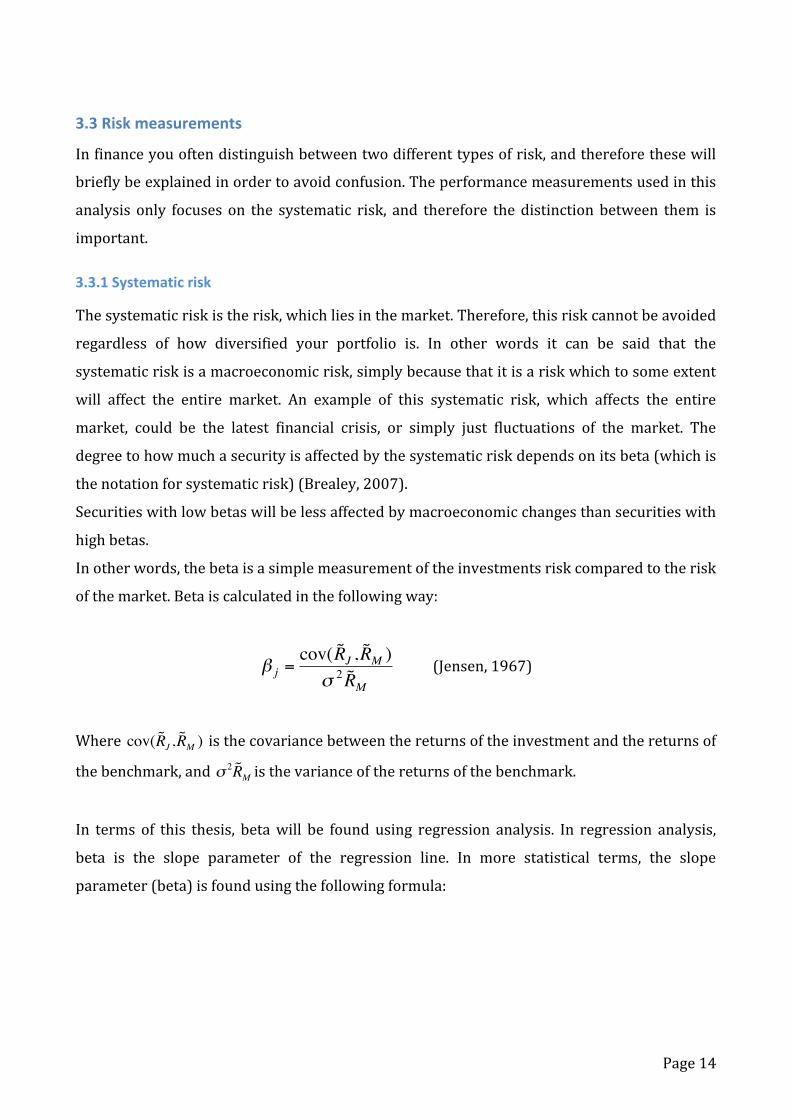

Inotherwords,thebetaisasimplemeasurementoftheinvestmentsriskcomparedtotherisk

ofthemarket.Betaiscalculatedinthefollowingway:

€

β j =cov( ˜ R J , ˜ R M )σ 2 ˜ R M

(Jensen,1967)

Where

€

cov( ˜ R J , ˜ R M ) isthecovariancebetweenthereturnsoftheinvestmentandthereturnsof

thebenchmark,and

€

σ 2 ˜ R M isthevarianceofthereturnsofthebenchmark.

In terms of this thesis, betawill be found using regression analysis. In regression analysis,

beta is the slope parameter of the regression line. In more statistical terms, the slope

parameter(beta)isfoundusingthefollowingformula:

Page15

€

ˆ β =(xi − x

i=1

n

∑ )(yi − y )

(xi − x )2

i=1

n

∑ (Wooldridge,2008)

Whenthinkingaboutthecalculationmethodsofbetashownabove,onewillalsorealisethat

theyarebuilduponpastreturns.Whetherthisisvalidornotcanbediscussed,howeverIwill

juststicktotheconclusionreachedbyDavidW.Mullins,Jr.Thiswasdiscussedintheprevious

section,andtheconclusionwasthatbetaseemedtoberelatedtopastreturns.

3.3.2Unsystematicrisk

Where the systematic risk couldbeexplainedas themacroeconomic risk, theunsystematic

riskcanbeexplainedasamicroeconomicrisk.

Thismeansthattheunsystematicriskisarisk,whichisparticulartoacertaincompanyand

perhaps its closest competitors. Therefore, the unsystematic risk is a risk, which can be

avoidedbyholdingadiversifiedportfolio.Thefirstreasonofthatis,thatifyouhavealarge

portfolio of stock, the total return of your portfolio will only be slightly affected by

fluctuationsinthereturnofasinglestock.Inotherwords,onestockonlyhasalittleeffecton

theentireportfolio.Itisalsorequiredthatyourportfolioshouldbediversified,meaningthat

youholdsecurities inmanydifferent industries, countries, etc. If youwant toeliminate the

unsystematic risk of your portfolio you are not necessarily looking for securities with the

lowestunsystematicrisk.Theimportantthinginordertoeliminatesystematicriskisthatyou

hold securities in your portfolio that has unsystematic risk that outweighs each other

(Brealey,2007).Anexampleofthiscouldbetwostockswhosestockpricesarehighlyaffected

bythegasolineprices.Ifoneofthesecompanieshighlybenefitfromhighgasolineprices,and

theotherloosesonhighgasolineprices,thentheymustindividuallyhavehighunsystematic

risk,howeverbyholdingbothof thestocks inyourportfolio,mostof theunsystematicrisk

willoutweigheachother.

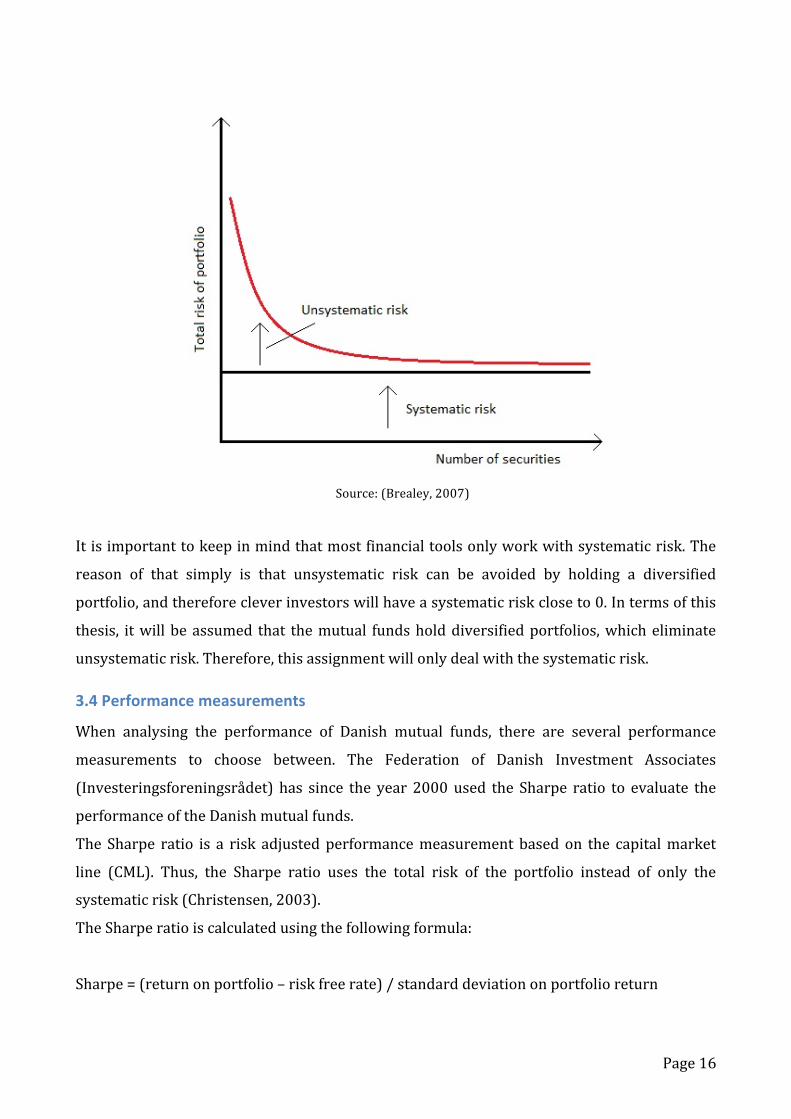

Thediagrambelowshowstherelationshipbetweensystematicriskandunsystematicriskina

portfolio.

Page16

Source:(Brealey,2007)

Itisimportanttokeepinmindthatmostfinancialtoolsonlyworkwithsystematicrisk.The

reason of that simply is that unsystematic risk can be avoided by holding a diversified

portfolio,andthereforecleverinvestorswillhaveasystematicriskcloseto0.Intermsofthis

thesis, itwillbeassumed that themutual fundsholddiversifiedportfolios,whicheliminate

unsystematicrisk.Therefore,thisassignmentwillonlydealwiththesystematicrisk.

3.4Performancemeasurements

When analysing the performance of Danish mutual funds, there are several performance

measurements to choose between. The Federation of Danish Investment Associates

(Investeringsforeningsrådet) has since the year 2000used the Sharpe ratio to evaluate the

performanceoftheDanishmutualfunds.

The Sharpe ratio is a risk adjustedperformancemeasurement basedon the capitalmarket

line (CML). Thus, the Sharpe ratio uses the total risk of the portfolio instead of only the

systematicrisk(Christensen,2003).

TheSharperatioiscalculatedusingthefollowingformula:

Sharpe=(returnonportfolio–riskfreerate)/standarddeviationonportfolioreturn

Page17

As discussed previously, it must be assumed that mutual funds hold diversified portfolio,

which eliminates the unsystematic risk, and therefore the Sharpe ratio is not the best

performancemeasurementinthiscase.

Instead, thisanalysiswilluse the Jensen index/Jensen’sAlpha tocalculate therisk‐adjusted

returnsofthemutualfunds,andthereareseveralreasonsofthat.

Firstofall,theinterpretationofJensen’salphaiseasier,asitshowsthepercentageexcessrisk

premiumthatamutualfundhasearnedcomparedtoitsbenchmark.HenceaJensenindexof

0,15%simplyjustmeansthatthemutualfundhasearnedanexcessreturnof0,15%pertime

unitcomparedtoitsbenchmark.Ontheotherhand,theSharperatiogivesyouriskpremium

per risk unit, and therefore it can be difficult for private investors to interpret whether a

Sharperatioof0,5isgoodorbad.

Secondly,Jensen’salphaiscalculatedusingregressionanalysis,meaningthatitcandirectlybe

seen from the output whether the results are statistically significant or not. If we again

compare to theSharperatio,wecannotdirectly interpretwhetheraSharperatioof0,25 is

significantlybetterthanoneof0,3withoutdoingadditionalcalculations.

Thirdly, Jensen’s alphamakesa relative comparison to abenchmarkwithin the calculation.

UsingtheSharperatio,onewouldhavetocalculatetheSharperatioforthebenchmark,and

thencompareittothatofthemutualfund.

Finally,Jensen’salphacanbeusedonbothefficientandinefficientportfolios,sinceitisbased

onthesecuritymarketline.Inotherwords,itcanbeusedforportfoliosthatlieonthesecurity

market line(theefficientones)andforportfoliosthatdonot lieonthesecuritymarket line

(theinefficientones).IfweagaincomparetotheSharperatio,thenthisisbasedonthecapital

marketline,andthereforeitcanonlybeusedforefficientportfolios(Christensen,2003).

In the analysis by Christensen (2003), he further concludes that the tradition in academic

literatureistouseJensen’salphaandthatmorethan100Americanresearchstudiesarebuild

uponthismethod.

Basedon theabove‐mentionedarguments, Jensen’sAlphawillbeused for theperformance

evaluationinthisthesis.

Page18

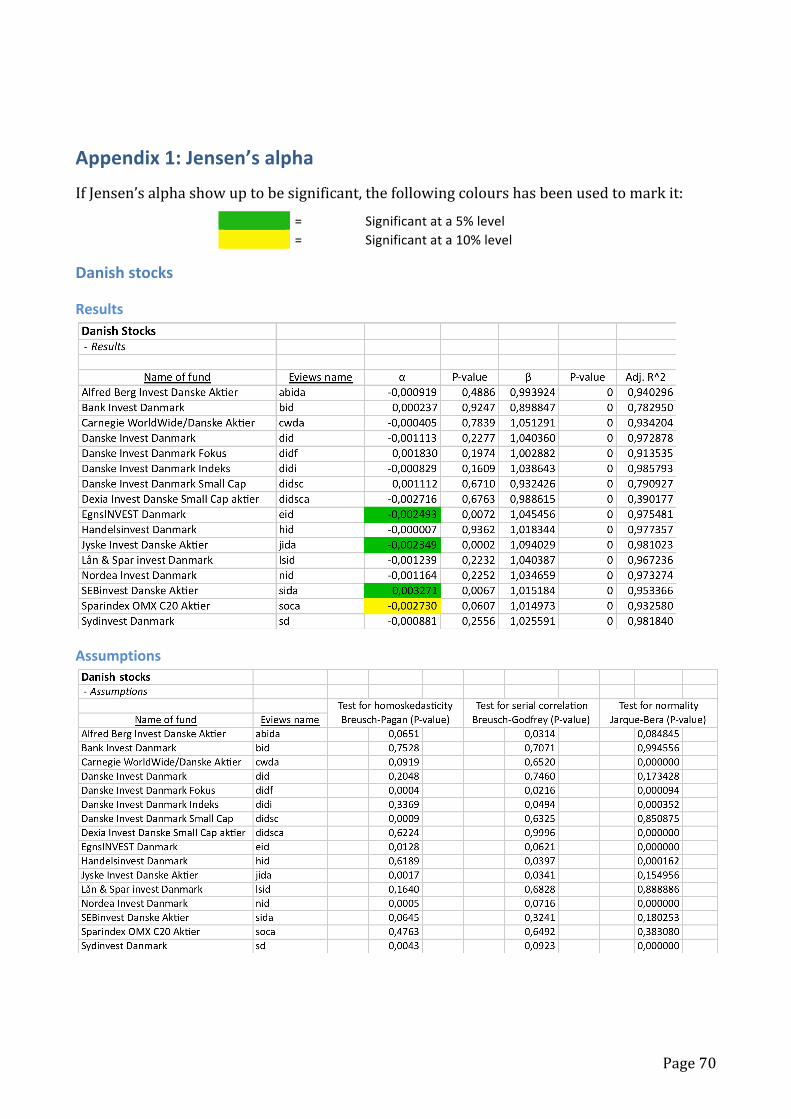

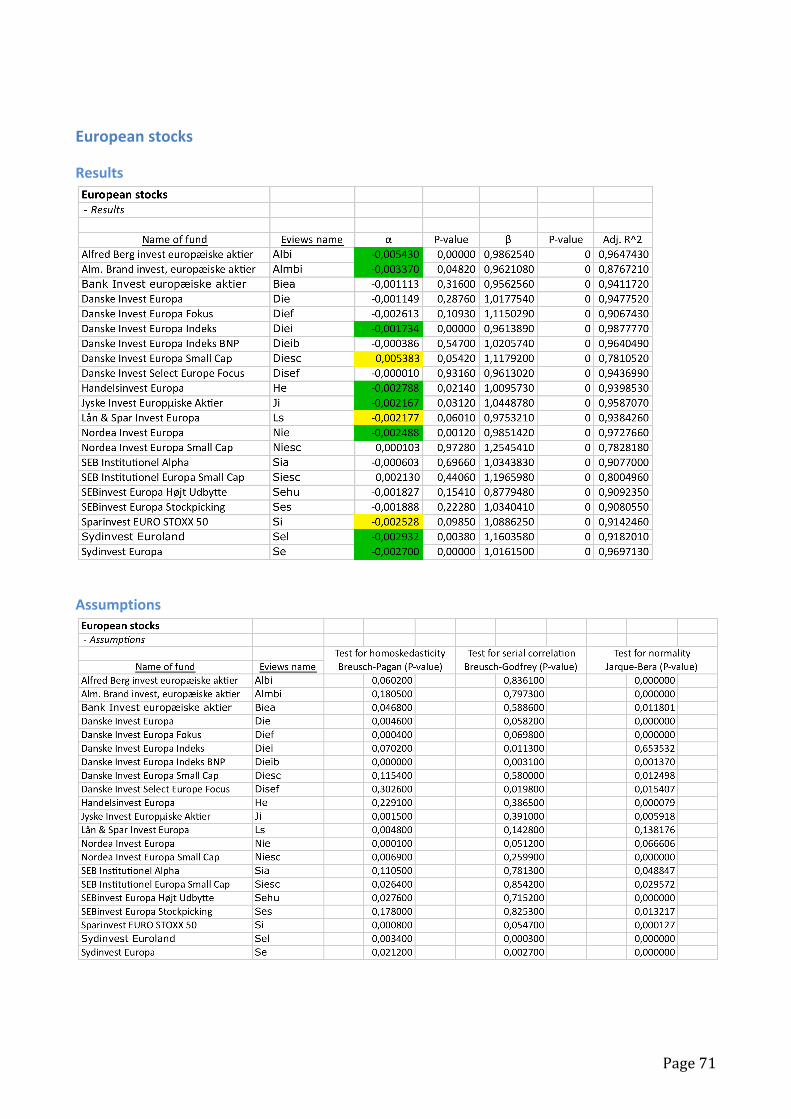

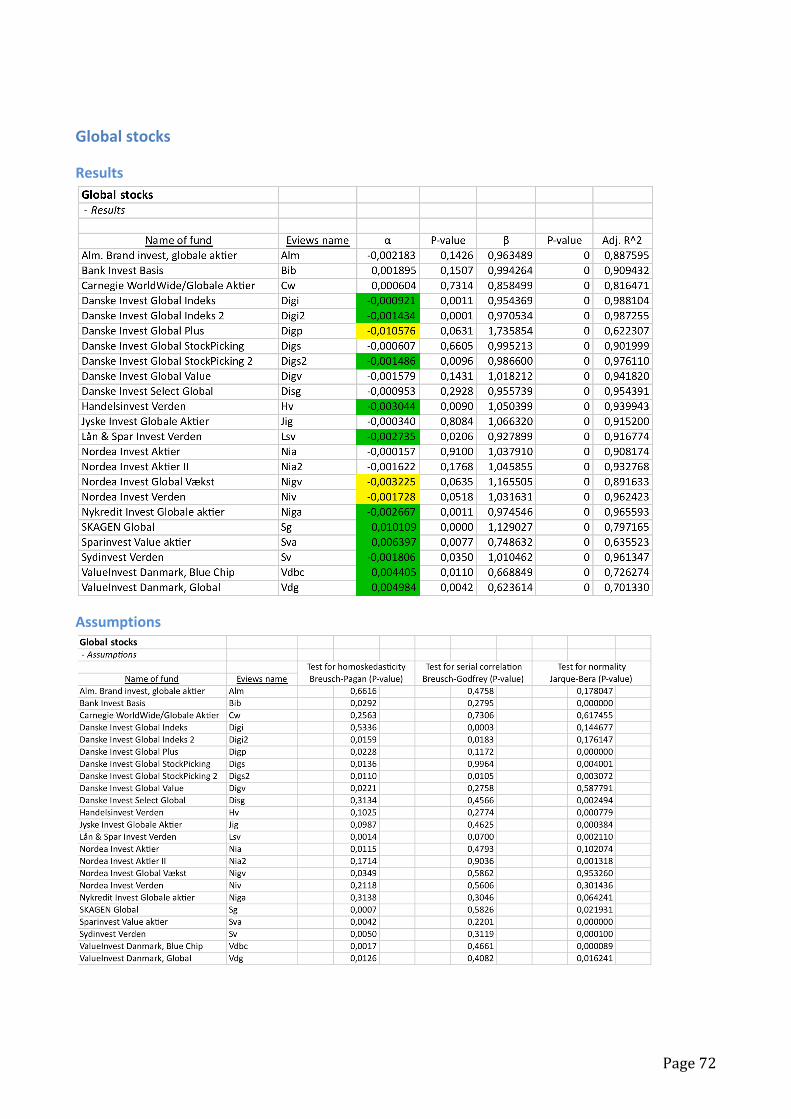

3.4.1Jensen’sAlpha

Jensen’s alphaor Jensen’s index is a riskadjustedperformancemeasurementdevelopedby

MichaelC.Jensenin1967.

ThemodelisbuilduponCAPM,andthereforeitassumesthatportfoliosarewelldiversified,

so that unsystematic risk is eliminated. Since the model is based upon CAPM, the same

assumptionsapplyforJensen’salphaasforCAPM(Jensen,1967).

Jensen’s alpha is calculated as the constant in the following regressionmodel (Christensen,

2003):

€

rpt − rft =α + β(rmt − rft ) + et

Isolatingalpha,weobtain:

€

α = (rpt − rft ) − β(rmt − rft ) + et

Where:

€

rpt :Returnoftheportfolioofthemutualfundinperiodt

€

rmt :Returnofthebenchmarkinperiodt

€

rft :Riskfreerateinperiodt

€

β :Estimateofthesystematicriskofthemutualfund

€

et :Errorterminperiodt

€

α :Performancemeasurementforthemutualfund.

In more technical terms, Jensen’s alpha is estimated using regression analysis in Eviews,

holdingtheriskpremiumofthemutualfundasthedependentvariableandtheriskpremium

of the benchmark as the independent variable. Jensen’s alpha shows up as the constant or

interceptinthemodel.

IftheestimateofJensen’salphashowsuptobepositiveandsignificantlydifferentfrom0,itis

concluded that the mutual fund has outperformed the benchmark. Oppositely, if it is

significantly negative, the benchmark has outperformed themutual fund. If Jensen’s alpha

shows up to be insignificant, it is concluded that themutual fund has performed neutrally

comparedtotheirbenchmark.

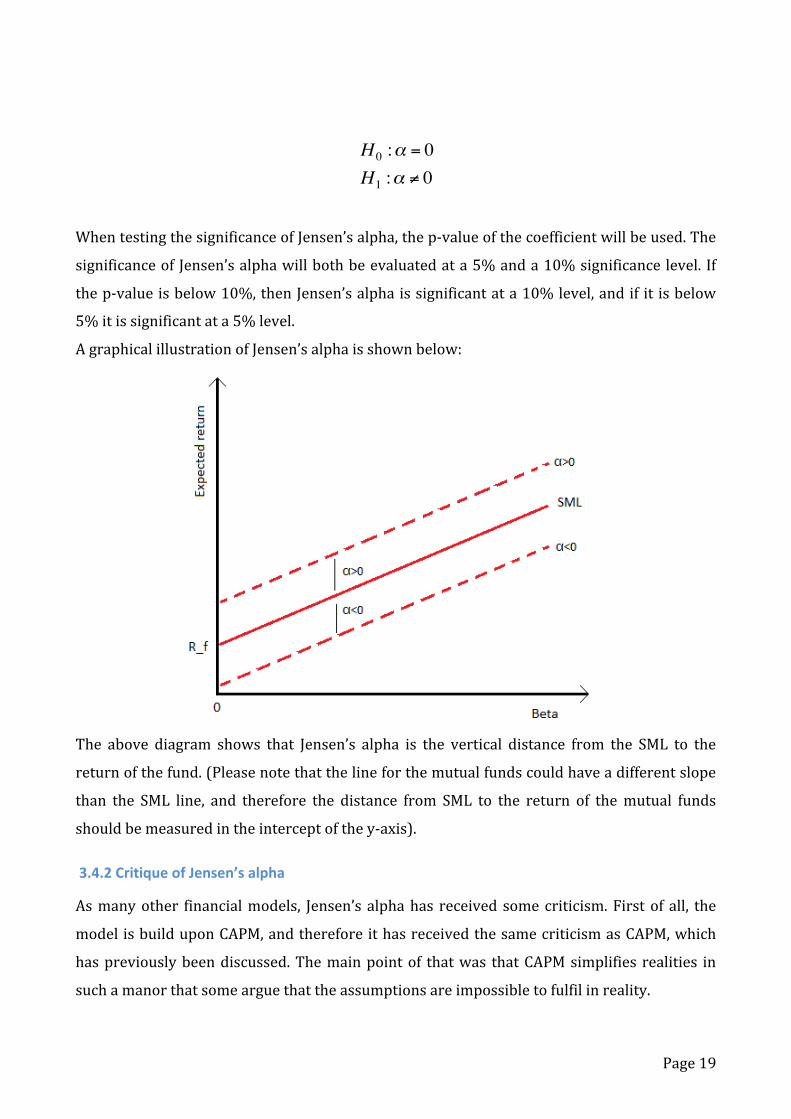

Instatisticalterms,thehypothesesthatarebeingtestedlookslikethis:

Page19

€

H 0 :α = 0H1 :α ≠ 0

WhentestingthesignificanceofJensen’salpha,thep‐valueofthecoefficientwillbeused.The

significanceofJensen’salphawillbothbeevaluatedata5%anda10%significancelevel. If

thep‐valueisbelow10%,thenJensen’salphaissignificantata10%level,andif it isbelow

5%itissignificantata5%level.

AgraphicalillustrationofJensen’salphaisshownbelow:

The above diagram shows that Jensen’s alpha is the vertical distance from the SML to the

returnofthefund.(Pleasenotethatthelineforthemutualfundscouldhaveadifferentslope

than the SML line, and therefore the distance from SML to the return of themutual funds

shouldbemeasuredintheinterceptofthey‐axis).

3.4.2CritiqueofJensen’salpha

Asmanyother financialmodels, Jensen’s alphahas received somecriticism.Firstof all, the

modelisbuilduponCAPM,andthereforeithasreceivedthesamecriticismasCAPM,which

haspreviouslybeendiscussed.Themainpointof thatwas thatCAPMsimplifies realities in

suchamanorthatsomearguethattheassumptionsareimpossibletofulfilinreality.

Page20

Roll (1977) further discusses the CAPM and the implications it has on performance

measurementsusingmodelsbuilduponCAPM.Mostofhisargumentationisconnectedtothe

choiceofbenchmark.

Firstofall,hearguesthatthechoiceofbenchmarkaffectsthesizeofthebetafortheportfolio.

In otherwords, thismeans that aportfoliowill havedifferent valuesof betadependenton

which benchmark is used as proxy for themarket portfolio. The reason of that is, that the

varianceofthemarkedportfolioisusedinthecalculationofthebetaofamutualfund.This

also implies that two investorswithexactly thesameriskprofilecanhavedifferentbetas if

theyusedifferentproxiesforthemarkedportfolio.

Thisthereforeimpliesthatbetaisnotanunambiguousmeasurementofthesystematicriskof

theportfolio.

Roll(1977)alsodiscussesthattherearetwodifficultieswhenusingaproxyforthemarked

portfolio.Firstofall, theproxycouldbeefficienteventhoughthe truemarket is inefficient,

therebyshowingan incorrectpictureof the truemarket.Secondly,heargues that it isvery

likely that there will be a high correlation between reasonable proxies for the marked

portfolio, and therefore it could seem as if the choice of either one of them is of less

importance.However, this is not the case according tohis analysis, becausehe argues that

eventhoughtheproxieshavehighcorrelation,theycanresultinquitedifferentinferencesin

theactualperformanceanalysis.

Theconclusiontothismustthereforebethatthechoiceofbenchmarkisofcrucialimportance

fortheresultsoftheperformanceanalysis.

TheimportanceofcorrectuseofbenchmarkswasshownbyIppolito(1989).Inthisanalysis,

Ippolito reached the opposite conclusion of most other analyses, namely that the mutual

funds had been able to outperform themarket. However, Elton et al. (1993) reviewed the

analysis, and reached the conclusion that Ippolito’s resultswere causedby incorrectuseof

benchmarks. Itshowedup,thatmanyofthemutual fundsIppolitohadanalysedinvestedin

“small” American stocks,whichwere not included in the S&P 500‐indexwhich he used as

benchmark.The“small”stockshadperformedbetterthantheS&P500‐indexintheperiodof

analysis,andthereforetheanalysisbyIppolitoshowedsuperiorperformancebythemutual

Page21

funds. However Elton et al. (1993) redid the analysis using appropriate benchmarks and

reached the same conclusionasother analysis, namely that themutual fundshadnotbeen

abletooutperformthemarket.

The example above shows, that reasonable use of benchmarks is crucial in order to reach

valid conclusions in the analysis. Therefore one should act carefully when choosing the

benchmarksforananalysis.

Inthediscussionofmarketefficiency,Roll(1977)alsodiscussesthatiftheproxyusedforthe

market portfolio is efficient, then none of the estimated Jensen’s alpha can be significantly

positive. The simple argumentation behind this is that if the marked is efficient, then all

informationisreflectedinthestockprice.Thus,itwouldbeimpossibleforamutualfundto

outperformtheindex,andthereforetheyshouldshowuptohaveinsignificantJensen’salpha.

As previously discussed, Fama (1991) showed that the stockmarkets where not perfectly

efficient,sothereforeitshould,atleastaccordingtoFama,bepossibleforthemutualfundsto

outperformthebenchmarks. Inrelationto this,Roll (1977)discusses that if theproxyused

forthemarketportfolioisnotefficient,thenhowcanitbejustifiedtouseitasabenchmarkin

aperformanceanalysis,whentheperformanceanalysis isbuilduponCAPMwhichrequires

efficientmarkets.

Itshouldfinallybenoted,thatthemulti‐indexmodelisbasedontheexactsametheoryasthe

Jensenindex,andthereforethecritiqueappliesforthemulti‐indexmodelaswell.

3.4.3Multi‐indexmodel

OnedrawbackofusingtheJensenindex,asdescribedabove,isthatitisasingleindexmodel.

It therefore requires that the investment objective of the mutual funds is well‐defined,

meaningthatitcanbeexplainedbasedononlyonebenchmark.

DanishlegislationrequiresthatDanishmutualfundsinvestatleast75%oftheirinvestment

withintheirmaininvestmentcategory.Thismeans,thattheDanishmutualfundsareallowed

toinvestupto25%ofitsvalueinanyotherinvestment.These25%canbeinvestedinboth

stocksaswellasbonds,howevermostmutualfundschoosetoinvestsolelyineitherstocksor

bonds.Thereasonofthatis,thatiftheychooseacombination,thefundwillbeclassifiedasa

mixedfund,whichchangesthetaxationofthefund(Christensen,2003).

Page22

The 25%‐rule could indicate that the performance of Danish mutual funds cannot be

evaluatedbasedononebenchmarkonly,andthereforeamulti‐indexmodelwillbeincluded

inordertoseewhetherthisisbetteratexplainingthereturnsofthemutualfunds.

Themulti‐indexmodelwillboth includestock indexesaswellasbonds indexes inorder to

coverallthepossibilitiesthemutualfundshave.

Differentmulti‐indexmodelswillbeuseddependentonwhatthemaininvestmentcategoryof

the investment funds. Therefore, the specificmodelswill be show in the section “choice of

benchmark”.

The purpose of using a multi‐index model is to increase the amount of variation in the

dependent variables explainedby independent variables in themodel. In order to evaluate

uponwhetherithasthedesiredeffect,oneshouldlookatadj.R2.Iftheadj.R2increaseswhen

includingotherbenchmarks,thismeans,thatthenewbenchmarkscapturesomething,which

thesinglebenchmarkwasnotabletocapturebefore.Thereasonofusingtheadj.R2insteadof

just the regular R2 simply is that the adj. R2 allows for comparisons betweenmodelswith

different numbers of independent variables. Adj. R2 has been corrected to allow this

comparison.

However, it is a requirement that the other benchmarks included in themulti‐indexmodel

havebeta‐coefficientsthataresignificantlydifferentfromzero.Ifthisisnotthecase,thenit

means that theyare insignificant, and therefore theydonothavea significanteffecton the

model,andshouldberemovedfromthemodel.

Thus,thereisachancethatthemulti‐indexmodelwillshowupwithexactlythesameresult

as thesingle index‐model.Thiswouldoccur ifall theadditionalbenchmarksshowup tobe

insignificant. If benchmarks show up to be insignificant, they should be removed from the

model onebyone, startingwith theonewith thehighestp‐value.Each timea variablehas

beenremoved,anewregressionmodelshouldbeestimated,andexactlythesameevaluation

shouldtakeplaceuntilthemodelconsistsofonlysignificantvariables.

Themulti‐indexmodelwillbeestimatedusingregressionanalysis,similarlytotheestimation

ofJensen’salphainthesingleindexmodel.Itwillbedonebyregressingtheriskpremiumof

the fundas thedependentvariableholdingtheriskpremiumof thedifferentbenchmarkas

theindependentvariables.

Page23

3.4.5Markettiming

TheJensenindexandthemulti‐indexmodelisonlyconcernedwiththeselectionabilityofthe

mutual funds to earn superior return. However, superior returns can also be obtained by

timingthemarket,andthereforeTreynor&Mazuy(1966)developedamodel,whichcanbe

used toanalyseboth theselectionand timingabilitiesofamutual fund. Inotherwords the

performanceanalysisisdividedintotwopieces,oneanalysingthemutualfundsabilitytofind

undervalued stocks (selectivity) and one analysing the mutual funds ability to predict the

directionthemarketwillbemovingin(timing).Thiswouldallowonetoseespecificallywhich

ofthesetwothingscausesagivenperformancebyaninvestmentfund.

Themodelwritesasfollows:

€

rpt − rft =α + β(rmt − rft ) + γ(rmt − rft )2 + et

Themodel is similar to the Jensen index, however in this themodel by Treynor &Mazuy

(1966)aquadratictermhasbeenincluded.

Inthemodel,αrepresentstheselectionabilityofthefund,whereasγrepresentsthetiming

abilityofthefund.TreynorandMazuy(1966)arguethatifγshowsupsignificantandpositive

intheregressionmodel,thisindicatesthatthemutualfundpossessedtheabilitytotimethe

market.

Thereasoningbehindthemodelisasfollows:

Ifmutual funds posses the ability to time themarket, they should adjust the beta of their

portfolio upwardswhen themarket is rising,whereas they should adjust the beta of their

portfolio downwards when the market is falling. The thoughts behind this is that mutual

funds should maximize their returns by having high betas when the market is moving

upwards,whereastheyshouldminimizetheirloosesbyhavinglowbetaswhenthemarketis

moving downwards. This would therefore also require the mutual funds to adjust their

systematicrisk,correspondingtotheirexpectationsaboutthemarket.

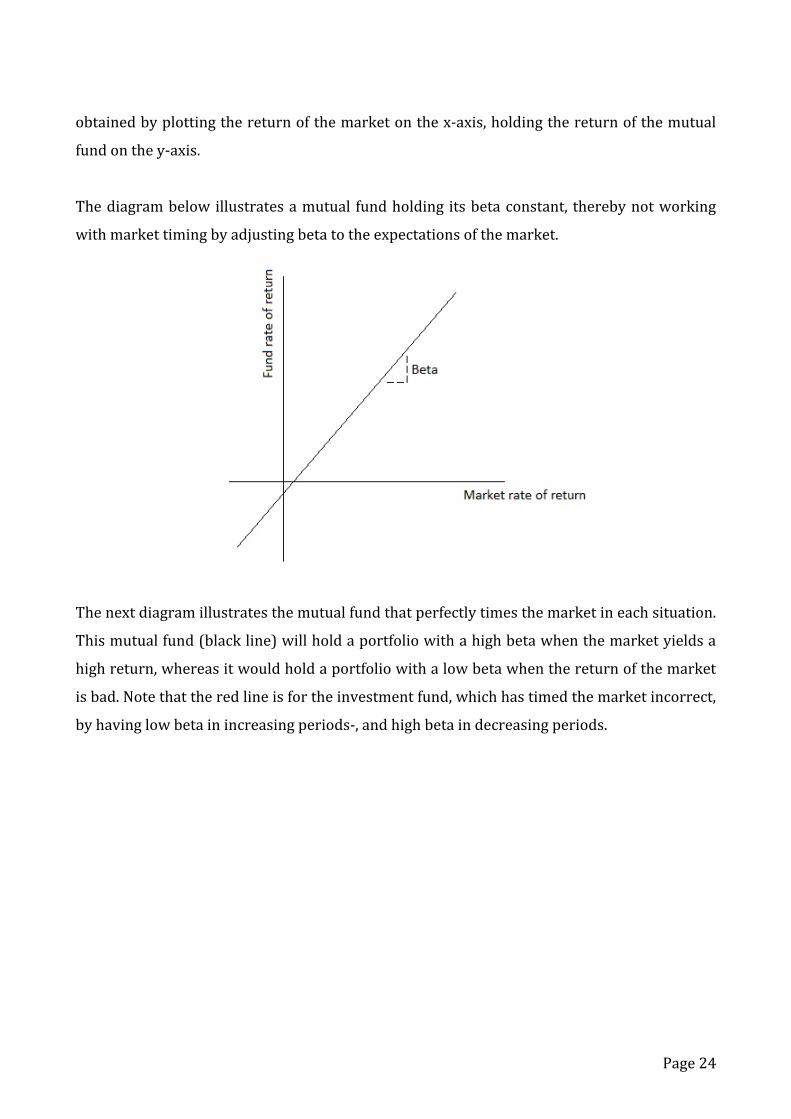

TreynorandMazuy(1966)usedthefollowingthreefigurestoexplainthedifferentscenarios

in the market timing analysis. The models are based on a “characteristic line”, which is

Page24

obtainedbyplottingthereturnofthemarketonthex‐axis,holdingthereturnofthemutual

fundonthey‐axis.

Thediagrambelowillustratesamutual fundholding itsbetaconstant, therebynotworking

withmarkettimingbyadjustingbetatotheexpectationsofthemarket.

Thenextdiagramillustratesthemutualfundthatperfectlytimesthemarketineachsituation.

Thismutualfund(blackline)willholdaportfoliowithahighbetawhenthemarketyieldsa

highreturn,whereasitwouldholdaportfoliowithalowbetawhenthereturnofthemarket

isbad.Notethattheredlineisfortheinvestmentfund,whichhastimedthemarketincorrect,

byhavinglowbetainincreasingperiods‐,andhighbetaindecreasingperiods.

Page25

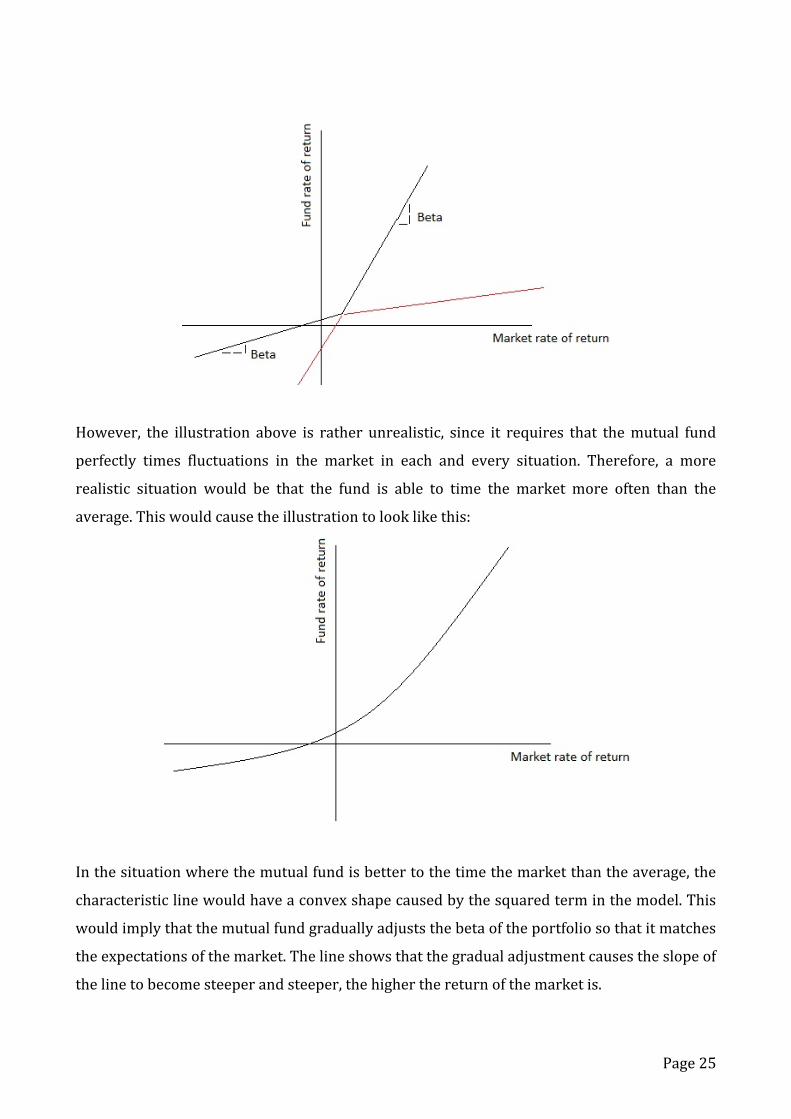

However, the illustration above is rather unrealistic, since it requires that themutual fund

perfectly times fluctuations in the market in each and every situation. Therefore, a more

realistic situation would be that the fund is able to time the market more often than the

average.Thiswouldcausetheillustrationtolooklikethis:

Inthesituationwherethemutualfundisbettertothetimethemarketthantheaverage,the

characteristiclinewouldhaveaconvexshapecausedbythesquaredterminthemodel.This

wouldimplythatthemutualfundgraduallyadjuststhebetaoftheportfoliosothatitmatches

theexpectationsofthemarket.Thelineshowsthatthegradualadjustmentcausestheslopeof

thelinetobecomesteeperandsteeper,thehigherthereturnofthemarketis.

Page26

Basedonthemodelabove,italsomakessensethatthequadratictermisusedtocapturethe

effectofmarkettiming.

Wooldridge(2008)arguesabout theeffectsofusingaquadratic terminamodel.Themain

point is that a quadratic term can be used to capture decreasing or increasing marginal

effects, and in this case, market timing of the mutual funds must be characterised as an

increasingmarginaleffect.

Inotherwordsthismeans,thattheregularregressionmodelassumeslinearity,andtherefore,

ifitshowsupthatthemodelisnotlinear,thelinearregressionwillnotbeabletoexplainthat.

This iswhere thequadratic termcomes inhandy,because it allows themodel to takeona

shape, which is not linear, and thereby the model with the quadratic term might help in

explainingsomething,whichtheregularmodelwasnotabletoexplain.

In termsofmarket timing for themutual funds, thiswouldalso imply, that if thequadratic

termshowsup tobepositiveand significant, theremustbeamarginal effect in themodel,

whichmeansthatthemutualfundhasadjustedthebetaoftheportfoliocorrespondingtothe

developmentinthemarket.

TheestimationoftheregressionmodelwillbedoneinEviews,usingthesamedatasetasfor

the Jensen index. However, for the estimation of the model, the Newey West

heteroskedasticityandautocorrelationconsistent (HAC)standarderrorswillbeusedonall

regressions,followingChristensen(2003),wherehearguesthatthequadratictermimposesa

heteroscedasticitytypeofproblemintothemodel,andthereforeit isparticularlyimportant

tousetheheteroscedasticityconsistentstandarderrors.

Thus, the only assumption that will be discussed for this model is the assumption about

normalityintheerrors.

Grant(1977)arguedthatthepresenceofmarkettimingwouldcausetheestimateofJensen’s

alpha to be downward biased, meaning that the estimate of Jensen’s alpha would be

underestimatedcomparedtotheactualperformanceofthemutualfund.

In other words, this means that in the presence of market timing, the value of α will be

underestimatedcomparedtotheJensenregressionbecauseJensenalphadoesnotaccountfor

themutual funds’abilitiestotimethemarket.Thecharacteristic linewouldbe linear inthe

Page27

Jensenindex,whereasinthepresenceofmarkettimingitwouldbeconcavelyshapedinthe

TreynorandMazuyregression,therebypushingtheinterceptfurtherdowntheY‐axisinthe

TreynorandMazuyregressioncomparedtotheJensenindex.

Finally, itshouldbenoted,thatit is likelythattheestimateofαwillchangewhenincluding

the quadratic term in the model, independently of whether the quadratic term shows up

significantornot.Itshouldthereforebementioned,thataccordingtoregularregressionrules,

thequadratic termshouldbe removed fromthemodel, if it showsup insignificant, thereby

leavingbehindtheJensenregression.

Thereasonofthatis,thatifavariableshowsupinsignificant,itdoesnothaveanysignificant

effectonthemodel.Therefore, itwouldonlycausedisturbanceoftheothervariablesinthe

model,ifthequadratictermisleftinthemodel.

Page28

4.DataThechoiceofdataisofgreatimportancefortheanalysis.Ifwrongchoicesaremade,itisvery

likely that the analysis will be biased, and therefore the results and conclusions will be

misleading.Thus,thissectionwillcoverthethoughtsbehindthechoicesthathavebeenmade

whenchoosingthedatafortheanalysis.Inaddition,certainassumptionsarerequiredtobe

fulfilled in order for the results of the analysis to be valid. Therefore, this sectionwill also

coveratheoreticaldiscussionoftheassumptionsandhowtheywillbetestedintheanalysis.

4.1Choiceofmutualfunds

IthasbeendecidedthatthisanalysisshouldcoverDanishmutualfundsinvestinginstocksin

thefollowingthreeareas:

1. Danishstocks

2. Europeanstocks

3. Globalstocks

Thesethreeareasofinvestmenthavebeenchosen,sincetheyarethemostcommonareasof

investmentfortheDanishmutualfunds.Inotherwords,thesethreecategoriesaretheones

thatcangatherthelargestsamplesizes.

Whenselectingthespecificfundsfortheanalysis,certaincriteriahastobemet:

• Themutualfundshouldexistfortheentireperiodfrom2001‐2010

• Themutualfundshouldonlyinvestinstocks

• Themutualfundshouldfitintooneofthethreecategories(inordertodecide

upon that, the categorization made by IFR has been used, as well as

descriptionsonthehomepagesoftheindividualfunds).

Intotal,60mutualfundshavebeenabletomeettherequirementsforthisanalysis.Theyare

dividedintothethreecategoriesasfollows:

1. Danishstocks(16mutualfunds)

2. Europeanstocks(21mutualfunds)

3. Globalstocks(23mutualfunds)

Page29

Thereturnsof themutual fundsaredeterminedas logreturnsusingmonthlyobservations,

whichtotallyamountsto120observationsforeachfund.

4.2Choiceofbenchmarks

The purpose of a benchmark is to show the general development in specific area of

investment. A benchmark should therefore be an expression of “best practice”. In other

words,thismeansthatthebenchmarkyouchooseshouldbeconsistentwithyourinvestment

strategy.This is themost important criterion for choosingabenchmark,however thingsas

investmenthorizon,restrictions,etc.,shouldalsobetakenintoconsideration.Inotherwords,

thismeans that the perfect benchmark should perfectlymatch your investment criteria. In

realityit isoftendifficulttofindabenchmarkthatperfectlymatchesyourinvestmentonall

criteria.Therefore,apublicindexisoftenchosenasbenchmark,becauseitiseasytoaccess,

stilloneshould thoughkeep inmindthat thiswillonlybeanapproximation to theoptimal

benchmark(Christensen,2001)

Whenchoosingabenchmarktherearecertainpitfallsoneshouldbeawareof.

Firstofall,itisimportantthatyouhaveconsistencybetweenwhetherdividendsareincluded

in your calculations or not. The reason of that is that when calculating the returns of the

mutualfundsyoucorrectfordividend.Ifyouthenchooseabenchmarkwheredividendshave

been excluded, your investment portfolio will already have a head start of 2‐3%‐point

(Christensen,2001).

Somemutual fundsstill chooseabenchmarkwheredividendsarenot included.Thereason

fordoingsoisthatitbecomeseasierforthemutualfundtooutperformtheirbenchmark.One

shouldkeepinmind,thatwhencalculatingthereturnofthemutualfund,costsofrunningthe

mutualfundhasbeendeductedfromthereturn,andthereforeitisdifficultforamutualfund

tooutperformabenchmark,whichiscost less.Stilloneshouldbeawareofthefactthatthe

correctcomparisonistoincludedividendsinboththecalculationofthereturnofthefund,as

wellasforthereturnofthebenchmark(Christensen,2001).

Whencalculatingthereturnsofthemutualfundsforthisanalysis,correctionsfordividends

havebeenmade.Therefore,thebenchmarksfortheanalysisshouldincludedividendsaswell.

Page30

Therearedifferentsuppliersofthesebenchmarks,andoneofthemajoronesisMSCIBarra,

which is a company owned by Morgan Stanley. They supply many different relevant

benchmarks,whicharecommonlyusedamongtheDanishmutualfunds.However,beforeone

isabletochooseappropriatebenchmarks,oneshouldbefamiliarwiththemethodologyused

intheindexes.

4.2.1Indexmethodology

Inordertochoosethemostappropriatebenchmark,oneshouldbeawareofthemethodology

usedintheindexes.Therefore,thissectionwillgiveabriefdescriptionofthat.

TheNASDAQOMXgrouppublishesindexes,whicharerelevanttothisanalysis,andtherefore

abriefdescriptionoftheirmethodologywillbegivenhere.

Firstofall,theyhavethreedifferent“measurement”typesusedfortheindexes,whichcanbe

combinedinanyway.

Grossindex(GI):Asthenamesuggest,thisisagrossindex,andthereforedividendshavebeen

includedintheindex.Theindexassumesthatthedividendsarereinvestedthedayafterthey

havebeenpaidout.

Price index (PI): This index is a price index, and therefore the index does not include

dividends. The index only focuses on movements in the stock prices, and therefore the

differencebetweenthegrossindexandthepriceindexsimplyisattributabletothedividends.

Cappedindex(Cap):Acappedindexmeansthattheindexhasbeencorrected,sotheweightof

asinglestockhasanupperlimitintheindex.Incaseastockexceedsthemaximumweight,the

stockisweightedbythemaximumweight.

Toconcludeontheabovedescriptions,itisfirstofalldesiredthatdividendsareincludedin

thebenchmarks,basedonthepreviousdiscussion.Therefore,thechosenbenchmarkshould

beagrossindex(GI).Inadditionitisalsodesiredthattheindexiscapped,sothatnosingle

stockhastolargeaneffect.Thisisinaccordancewiththelegislationregardingtheinvestment

funds,whichrequiresthatasinglestockcannotwaymorethan5%intheportfolio.Therefore,

acappedindexismorelikelytoshow“bestpractice”.

Page31

Themainconclusionisthereforethatthechosenbenchmarksshouldbeacappedgrossindex.

Onefinalthingthatwouldbedesirableisthattheindexisadjustedforfreeflow.Afreeflow

adjustment means that index has been corrected, so that only the share capital, which is

availableonthemarket,isincludedintheindex.

4.2.2BenchmarkfortheJensenindex

This section will cover a discussion of why certain benchmarks have been chosen. When

choosingthebenchmarkforthemutualfundsinvestinginDanishstocks,severalothergood

alternativesexist.Therefore, adiscussionof thealternativebenchmarkwill be included for

theDanishstocks.However, fortheotherinvestmentcategoriesthemaindiscussionwillbe

regardingthebenchmark,whichhasbeenchosen.

The discussion of the benchmarks will be based upon what the different funds use as

benchmarks.Appendix4showsanoverviewofthebenchmarksusedbythedifferentmutual

funds.

Thedescriptionof thedifferent indexes isbasedonexplanationsfoundonthehomepageof

thesuppliersoftherespectiveindexes.

Danishstocks

Choice:

OMXCopenhagenCap_GI

This index is a total index, which includes all of the stocks that are registered on the

Copenhagen Stock Exchange, and therefore the purpose of the index is to show the actual

conditionaswellaschangesofthemarket.Theindexisbothagrossindexaswellasacapped

indexhowever it hasnot been adjusted for free flow.Despite this fact, this indexhasbeen

chosenasbestpracticefollowingthediscussionofthealternativesbelow.

ThedatafortheindexhasbeencollectedfromCopenhagenStockExchange,andthereforethe

indexismeasuredinDKK.

Alternatives:

OMXCopenhagen20

This index includes the 20 most traded stocks on the Copenhagen Stock Exchange. The

advantage of this index is that the stocks that are included are the most liquid stocks.

Page32

However,itonlyincludes20differentstocks(TheOMXC20stocks),andthereforeithasbeen

concluded that this is not enough to cover the possible investments made by the mutual

funds.Inaddition,theindexisapriceindex,meaningthatdividendshavenotbeenincluded

intheindex.Finally,theindexisneithercapped,meaningthatcompanieslikeNovoNordisk

andA.P.MøllerMærskwillhavealargeweightintheindex.Basedonthis,theindexhasbeen

foundinappropriatefortheanalysis.

OMXCopenhagenBenchmarkCap_GI

This index includes between 50 and 80 of the largest and most frequently traded stocks

representingmost of the different sectors on theDanish stockmarket. The index is both a

cappedindexaswellasagrossindex,andinadditionithasalsobeenadjustedforfreeflow.

Therefore, this would be themost appropriate benchmark to use for the analysis, since it

fulfilsalltherequirementspreviouslystated.However,itonlydatesbacktoOctober242005,

andthereforeitcannotbeusedforthisanalysis.Finally,itshouldbenoted,thatmanyofthe

mutualfundsincludedintheanalysisusesthisindexasbenchmarkontheirportfolios.

MSCIDenmark

ThefinalalternativecouldbetousetheMSCIDenmarkindex.Theadvantageofthisindexis

thatitcanbechosenasbothcapped,grossindexandfreeflowadjusted.Therefore,theindex

couldfulfiltherequirements,whichwerepreviouslystatedforthebenchmarks.However,the

disadvantageisthattheindexismeasureinUSD,sothereforeitshouldbetransformedinto

DKKusing the correspondingexchange rates foreachof theobservations in thedataset. In

addition,noneofthechosenmutualfundsusethisindexasabenchmark,whereasthechosen

oneshowsupasmuchmorefrequent.

However, this index is probably the best possible alternative to the chosen index, and

thereforeitisalsoverylikelythattheywillhavepositivecorrelationscloseto1.

Europeanstocks

Again,therearedifferentbenchmarkstochooseamongforthisinvestmentcategory,however

themain concern for this analysis is theMSCIBarra indexes.Here thereare three relevant

onestochoosebetween.

Page33

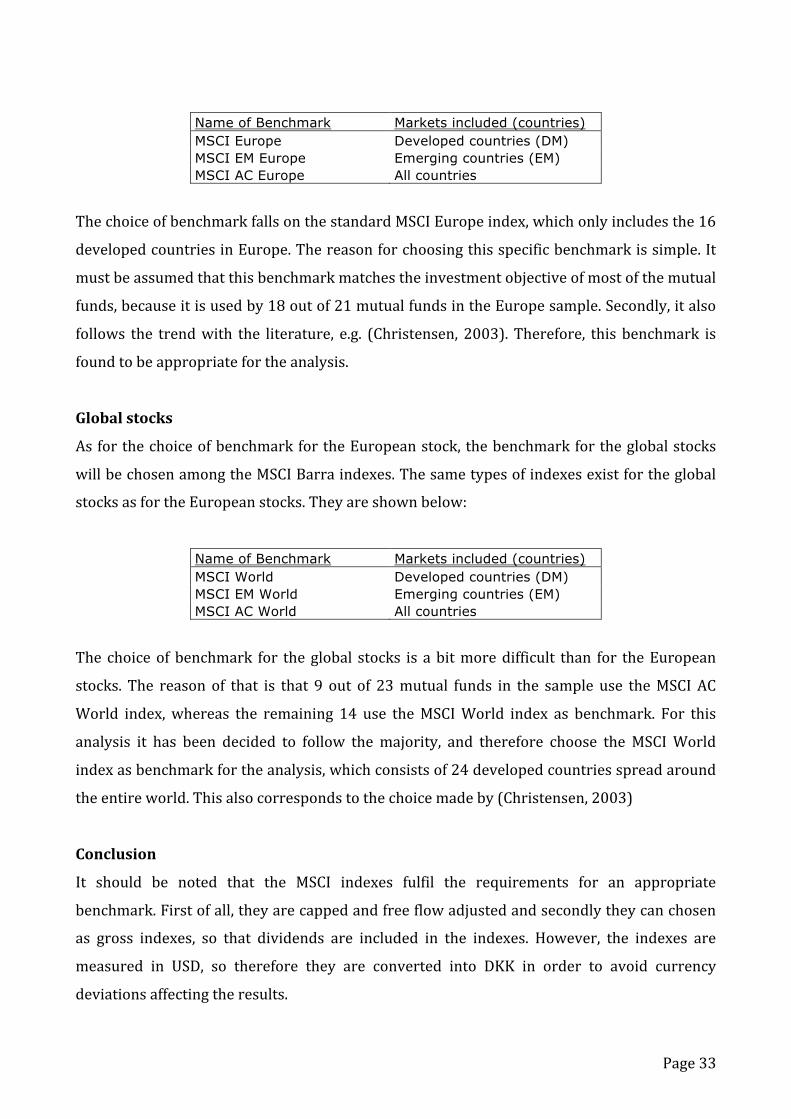

Name of Benchmark Markets included (countries) MSCI Europe Developed countries (DM) MSCI EM Europe Emerging countries (EM) MSCI AC Europe All countries

ThechoiceofbenchmarkfallsonthestandardMSCIEuropeindex,whichonlyincludesthe16

developedcountriesinEurope.Thereasonforchoosingthisspecificbenchmarkissimple.It

mustbeassumedthatthisbenchmarkmatchestheinvestmentobjectiveofmostofthemutual

funds,becauseitisusedby18outof21mutualfundsintheEuropesample.Secondly,italso

follows the trendwith the literature, e.g. (Christensen, 2003).Therefore, this benchmark is

foundtobeappropriatefortheanalysis.

Globalstocks

AsforthechoiceofbenchmarkfortheEuropeanstock,thebenchmarkfortheglobalstocks

willbechosenamongtheMSCIBarraindexes.Thesametypesofindexesexistfortheglobal

stocksasfortheEuropeanstocks.Theyareshownbelow:

Name of Benchmark Markets included (countries) MSCI World Developed countries (DM) MSCI EM World Emerging countries (EM) MSCI AC World All countries

The choiceofbenchmark for theglobal stocks is abitmoredifficult than for theEuropean

stocks. The reason of that is that 9 out of 23mutual funds in the sample use theMSCIAC

World index,whereas the remaining 14 use theMSCIWorld index as benchmark. For this

analysis it has been decided to follow themajority, and therefore choose the MSCIWorld

indexasbenchmarkfortheanalysis,whichconsistsof24developedcountriesspreadaround

theentireworld.Thisalsocorrespondstothechoicemadeby(Christensen,2003)

Conclusion

It should be noted that the MSCI indexes fulfil the requirements for an appropriate

benchmark.Firstofall,theyarecappedandfreeflowadjustedandsecondlytheycanchosen

as gross indexes, so that dividends are included in the indexes. However, the indexes are

measured in USD, so therefore they are converted into DKK in order to avoid currency

deviationsaffectingtheresults.

Page34

TheMSCI indexesareobtained fromMSCIBarra,andthechosen indexesaregross indexes,

followingthediscussionfromprevious.

Onefinalthingtonoteisthatthesamebenchmarkhasbeenchosenforallthemutualfundsin

eachcategory.However, itcanbeabitmisleading,sincesomemutual fundsholdportfolios

only investing in small cap stocks. Therefore, it could be discussed that it would bemore

appropriatetouseabenchmarkthattakesthisintoaccountforthesespecificfunds.Though,

the purpose of the analysis is to divide the mutual funds into these three investment

categories,andseeifanyofthemareabletooutperformthepassivebenchmarks.However,if

mutual funds show up to have significant Jensen’s index, an evaluation about appropriate

benchmarkwillbedone,inordertoavoidmakingthesamemistakeasIppolito(1989).

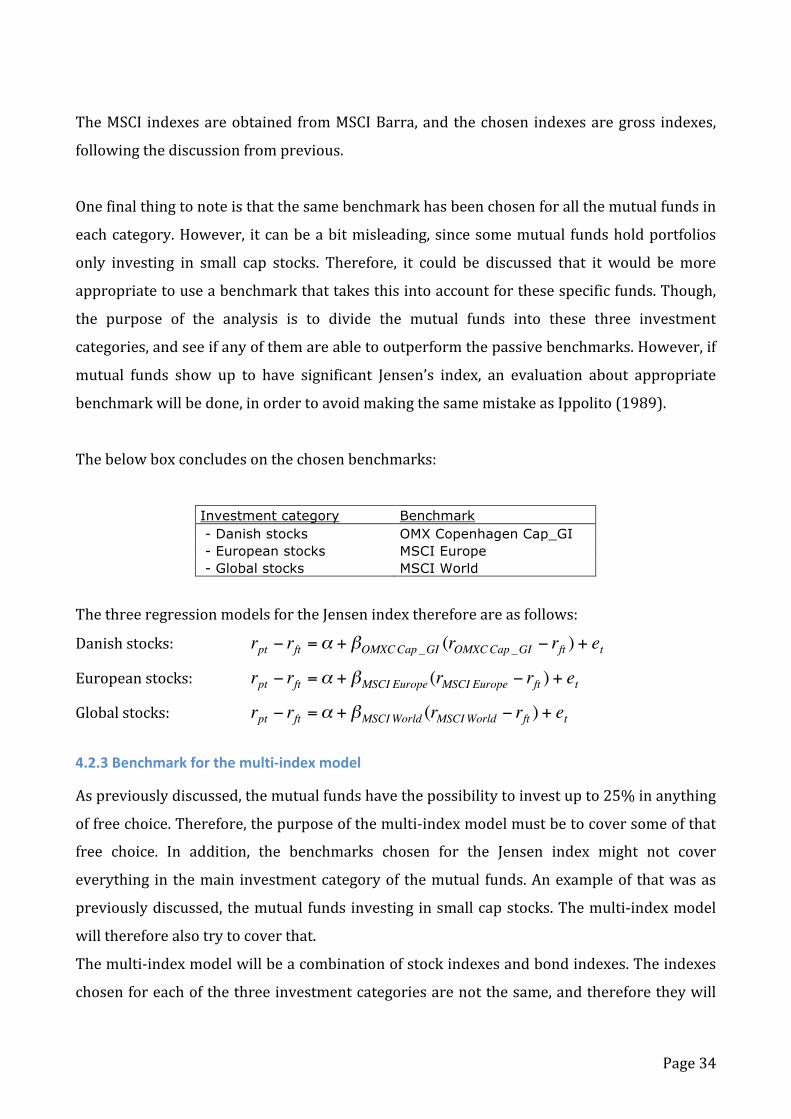

Thebelowboxconcludesonthechosenbenchmarks:

Investment category Benchmark - Danish stocks OMX Copenhagen Cap_GI - European stocks MSCI Europe - Global stocks MSCI World

ThethreeregressionmodelsfortheJensenindexthereforeareasfollows:

Danishstocks:

€

rpt − rft =α + βOMXCCap _GI (rOMXCCap _GI − rft ) + et

Europeanstocks:

€

rpt − rft =α + βMSCI Europe (rMSCI Europe − rft ) + et

Globalstocks:

€

rpt − rft =α + βMSCIWorld (rMSCIWorld − rft ) + et

4.2.3Benchmarkforthemulti‐indexmodel

Aspreviouslydiscussed,themutualfundshavethepossibilitytoinvestupto25%inanything

offreechoice.Therefore,thepurposeofthemulti‐indexmodelmustbetocoversomeofthat

free choice. In addition, the benchmarks chosen for the Jensen index might not cover

everything in themain investmentcategoryof themutual funds.Anexampleof thatwasas

previouslydiscussed,themutualfundsinvestinginsmallcapstocks.Themulti‐indexmodel

willthereforealsotrytocoverthat.

Themulti‐indexmodelwillbeacombinationofstockindexesandbondindexes.Theindexes

chosenforeachofthethreeinvestmentcategoriesarenotthesame,andthereforetheywill

Page35

bediscussedindividually.However,thebondindexeswillbethesameforallthreeinvestment

categories.

Thebondindexesareasfollow:

• J.PMorganDenmarkGovernmentBondIndex(JPMGBIDenmark)

• J.P.MorganGlobalBroadex.Denmarkindex(JPMGBIGlobal)

ThedataforthosetwoindexesareobtainedthroughDatastream.

The choice of bond indices follows Christensen (2003). He concludes that the EFFAS bond

indexes could just as well be chosen, however it has been decided to use the J.P: Morgan

indexesinthisthesisaswell.

Danishstocks

ThebenchmarkchosenfortheJensenindexwas“OMXCopenhagenCap_GI”,andaspreviously

discussed,thisindexincludesallstocks,whicharelistedontheCopenhagenstockexchange.

Thiswould therefore also imply that the index includes small cap stocks aswell. Thus, no

need is foundto includeasmallcap index in themulti‐indexmodel forDanishstockssince

“OMXCopenhagenCap_GI”shouldbeabletocoverthat.

AnotherindexthatwillbeincludedistheMSCIWorldindex,sinceitisbelievedthatthiscould

berelevantforthemutualfundsinvestinginDanishstocks.However,oneshouldthoughkeep

inmindthatthisindexonlyincludesmidandlargecapstocksonthedevelopedmarkets.

Finally,thetwobondindexeswillbeincluded,andthereforetheregressionreadasfollows:

€

rpt − rft =α + βOMXCCap _GI (rOMXCCap _GI − rft )+βMSCIWorld (rMSCIWorld − rft ) + βJPMGBIGlobal (rJPM GBIGlobal − rft )+ βJPM GBI Denmark (rJPM GBI Denmark − rft ) + et

Europeanstocks

In the single index model for European stocks, the MSCI Europe was used as benchmark.

However, this index only includes mid and large cap stocks for the developed markets in

Europe.Therefore, itwouldbe interesting to includean indexon theemergingmarkets. In

ordertocoverthat,theMSCIEMEuropeindexhasbeenincludedinthemodel.Inaddition,it

Page36

wouldalsobeinterestingtocoverthedevelopmentinthesmallcapstocks,andthereforeit

hasbeendecidedtoincludetheMSCIEuropeSCaswell.

Finally,themulti‐indexmodelfortheEuropeanstockswill includetheMSCIWorldindexto

coverthedevelopmentontheworldmarketaswellastheOMXCopenhagenCap_GItocover

the development on the Danish market. In order to cover the development on the bond

markets,thetwopreviouslydiscussedbondindexeswillbeincluded.

Therefore,themulti‐indexmodelforEuropeanstocksreadsasfollows:

€

rpt − rft =α + βMSCI Europe (rMSCI Europe − rft )+ βMSCI EM Europe (rMSCI EM Europe − rft ) + βMSCI EuropeSC (rMSCI EuropeSC − rft )+ βMSCIWorld (rMSCIWorld − rft ) + βOMXCCap _GI (rOMXCCap _GI − rft )+ βJPM GBIGlobal (rJPMGBIGlobal − rft )+ βJPM GBI Denmark (rJPM GBI Denmark − rft ) + et

Globalstocks

For themutual funds investing in global funds, the regressionmodel will follow the same

patternastheonefortheEuropeanstocks.

It isfirstofalldesiredtocoverthedevelopmentinboththeemergingmarketsaswellasin

the small cap markets, since those two things are not included in the MSCI World index,

followingthesamediscussionasfortheMSCIEuropeindex.

Therefore,besides theMSCIworld index, theMSCIWorldSC indexaswell as theMSCIEM

index will be included. These two indexes should cover the development in the small cap

stocksaswellasintheemergingmarkets,respectively.

Finally, OMX Copenhagen Cap_GI index will be included along with the two previously

discussed bond indexes. Therefore, the multi‐index model for the global stocks read as

follows:

€

rpt − rft =α + βMSCIWorld (rMSCIWorld − rft )+ βMSCIWorld SC (rMSCIWorld SC − rft ) + βMSCI EM (rMSCI EM − rft )+ βOMXCCap _GI (rOMXCCap _GI − rft ) + βJPMGBIGlobal (rJPM GBIGlobal − rft )+ βJPM GBI Denmark (rJPM GBI Denmark − rft ) + et

Page37

4.3Choiceofriskfreerate

Therisk freerateshouldrepresent the interest ratean investorcouldobtain in themarket

withouttakinganyriskatall.Intheliteraturedifferentproxiesoftheriskfreerateareused,

suchas“1‐monthT‐bill”,“1‐monthCIBOR”,etc.

This analysis will follow the analysis by Christensen (2003),where he uses the 1‐month

CIBORasaproxyfortheriskfreerate.

The CIBOR (Copenhagen Interbank Offered Rate) is the interest rate, which the Danish

NationalBankdeterminesonadailybasis,basedonreportsfromseveralDanishbanks.

In practical terms, the CIBOR rate is the reference interest rate, which is used for lending

moneyontheinterbankmarket.TheCIBORratesdifferdependentontheperiod,whichgoes

fromoneweekupto12months.

Another argument for using the1‐monthCIBOR rate is, that it is a good representative for

whatthemutualfundscouldhaveearnedontheinterbankmarketinthespecificmonthofan

investment. It shouldalsobenoted, that it isveryunlikely thatother reasonablechoicesof

proxyfortheriskfreeratewouldchangetheconclusionsoftheanalysis.Thereasonofthatis,

thattheriskfreerateisdeductedfromboththereturnofthemutualfunds,aswellasfrom

thereturnofthebenchmark.

Thedataforthe1‐monthCIBORhasbeenobtainedfromthehomepageoftheDanishNational

Bank.Theinterestratesaremeasuredonanannualbasis,andthereforethefollowingformula

hasbeenusedinordertoobtaincontinuousinterestrates:

Monthlyinterestrate=

€

(1+ annual int erest rate)1/12 −1

4.4Survivorshipbias

Survivorshipbiasisdefinedasthebiasthatoccursinyourdatasetifnon‐survivingfundsare

systematicallyignoredintheperformanceanalysis.Theresultofthatwilloftenbethatyour

analysiswouldsignificantlyoverstatethereturns,simplybecausethattheworstperforming

funds(andthereforenon‐surviving)areleftoutoftheanalysis(Christensen,2005)

Eltonet al. (1996) argues that thedisappearanceofmutual fundsoccur eitherdue topoor

performanceorduetoasufficientlysmallmarketvalueofthefund.Inaddition,theyconclude

that lowmarketvaluesareoftencausedbypoorperformance. Theyfurtherarguethat it is

Page38

rarethatfundstotallydisappear,butinsteadtheyareoftenmergedintofundsthatoftenfall

intothesamefamilyoffundsandhaveperformedbetter.Theadvantageforthemutualfunds

ofdoingsois,thattheycontinuetoearnfeesontheinvestmentintheoriginalfund,whilethe

recordofthefund’spoorperformancebecomesdifficulttotrack.

Malkiel (1995) furtheradds to thediscussionofsurvivorshipbias thatmutual funds,which

acceptveryhighriskhaveveryhighprobabilitiesoffailureaswell.Therefore,survivingfunds

doingsoarecomparedtotakingalargebetandhavingwon.Thisclearlyshows,thatifonly

survivingfundsareincluded,thentheywillpositivelybiastheaveragereturnofthemutual

funds.

Asimplified,yetextremeexamplecouldbe10mutual fundsthatallhave invested inhighly

risky securities in a specific area over a 10‐year period. One of these funds has earned a

returnof200%overtheperiod,whereastheother9fundshavenotsurvivedtheperioddue

to poor performance. If a performance analysis was carried out at the end of the 10‐year

period, only including the surviving funds, then the conclusion would be that the average

return within this specific area of investment had been 20%. However, this result is very

misleading,sincetheother9fundsearningnegativereturnwherenotincludedduetolackof

datafortheentireperiod.Theactualaveragereturnwithinthisareaofinvestmentislikelyto

behighlynegative.Thisistheessenceofsurvivorshipbias.

Malkiel (1995) also analysed the effect of survivorship bias. The conclusion was, that the

largertheperiodofanalysis,thelargertheeffectofsurvivorshipbiaswouldbe.Theanalysis

showed that over a 10‐year period, the average annual return of only surviving fundswas

1,5%‐points higher than the average annual return for all funds including non‐surviving

funds.Theanalysiswasalsoconductedona15‐yearperiod,andtheresultswereevenmore

surprising here. The results were that the average annual return of surviving funds was

18,7%, while it was only 14,5% including the non‐surviving funds. This amounts to a

differenceof4,2%‐points,whichmustbeconsideredquitealot.

However, most of the analyses regarding survivorship bias has been conducted on the

Americanmarket.IntheanalysisbyChristensen(2005),heconcludesthattheDanishmutual

fundsarealmostfreeofsurvivorshipbias,becausenofundshavedefaultedduringhisperiod

Page39

ofanalysis.Itshouldthoughbenoted,thattheperiodofhisanalysiswas1996‐2003,whereas

theperiodofthisthesisis2001‐2010.

Itshouldfinallybenoted,thatthisthesisonlydealswithfundsthathaveexistedfortheentire

periodofanalysis.Therefore,fundsthathavedefaultedormergedintheperiodarenottaken

into consideration. In other words, survivorship bias is ignored, and therefore one should

keepthatinmind,wheninterpretingtheresultsoftheanalysis.

4.5Assumptionsforthetests

Thedataused for theanalysis isclassifiedas timeseriesdata, since theanalysisdealswith

observationsovertime.Timeseriesdataisoftenmoredifficulttoanalysethanregularcross‐

sectionaldata, as it is rare that timeseriesdata is independentacross time.Therefore,one

shouldstronglyconsideranddiscusstheassumptionsrequiredforthetesttobevalidbefore

onedraws conclusionsupon them. In case the assumptions arenot fulfilled, one shouldbe

carefullywheninterpretingtheresults.Ifassumptionsshowupnottobefulfilled,comments

willbemadeintheanalysis.

The discussion of assumptions for time series regression will follow the Gauss‐Markov

assumptionsfromWooldridge(2008).

1.Linearinparameters

The assumption states that there should be a linear relationship between the dependent

variable and the independent variables in the model. Eviews will therefore estimate the

modelasifitwaslinear,whetherornotthisisactuallythecaseornot.However,aspreviously

discussed,researchuponCAPMhasshownthat itseemsas if therelationshipbetweenpast

return and beta is linear. This analysiswill also estimate beta based on past returns, and

thereforeitisexpectedthattherelationshipwillbelinearinthiscaseaswell.Inaddition,the

performance measurements used in this analysis are built upon CAPM, which requires

linearity.Therefore,itisassumedthatthisassumptionisfulfilled.

2.Noperfectcollinearity

This assumption states that none of the independent variables can be constant or a linear

combination of the others. If two independent variables show up to be a perfect linear

Page40

combinationofeachother,itissaidthattheyareperfectlycorrelatedwitheachother.Thisis

aproblem,becauseonecannotestimateamodel,whichhasperfectlycorrelatedvariables.If

onefacestheproblemofperfectcollinearity,oneshouldeitherreformulatetheentiremodel,

orleaveoneofthevariablesoutofthemodel.

Itisimportanttokeepinmindthattheassumptionallowsforhighcorrelationsbetweenthe

variables,howevertheyarejustnotallowedtobeperfectlycorrelated.

Intermsofthisanalysis, itmustbeexpectedthatindependentvariables(benchmarks)have

ratherhighcorrelations,astheytosomeextentsufferfromthesamesystematicrisk.Stillitis

notexpectedthatanyofthemsufferfromperfectcollinearity.

Thereisnoreasontotestforthisassumption,asEviewscannotestimateregressions,which

sufferfromperfectcollinearity.Inotherwords,Eviewsautomaticallydoesthetestforyou.If

opposedtoallexpectations,somemodelsshowuptobesufferfromperfectcollinearity,the

modelwillbereformulated,andcommentsregardingthatwillbemade.

3.Zeroconditionalmean

Thisassumptionrequiresthattheexpectedvalueoftheerrortermiszerogivenanyperiodof

theexplanatoryvariable.

Instatisticalterms,theassumptionrequiresthatE(u)=0.Iftheerrortermisindependentof

theobservationsoftheexplanatoryvariablesinthemodel,thisassumptionwillhold.

Tobemorespecific,theassumptiondoesnotputanyrestrictiononthecorrelationbetween

theindependentvariablesinthemodelorintheerrortermacrosstime.Theassumptiononly

states, that the average value of the error term should be unrelated to the independent

variablesinalltimeperiods.

The two most common causes of breaches of this assumption are omitted variables and

measurementerrorsinsomeoftheregressors.

Thisassumption ismuchrelated to the lastassumptionaboutnormality, so the test for the

assumptionwillberelatedtothat.

4.Homoskedasticity

The assumption abouthomoskedasticity requires that the varianceof the error term is the

sameforallvaluesintheperiod.Ifhomoskedasticityisnotpresent,itissaidthatthemodel

suffers for heteroskadasticity. A more graphical illustration would show that if

Page41

heteroskadasticity is present in themodel, a scatterplot with the residuals (errors) would

showa funnel shapecompared to theactual regression line.The funnel shapewouldcause

thatthevarianceiseitherincreasedordecreasedovertime,whichisaproblemforthemodel.

Theassumptionabouthomoskedasticityplaysnoroleinshowingthatthemodelisunbiased,

howevertheassumptionisstillimportant.Ifamodelsuffersfromheteroskadasticityitisvery

likelythattheestimatesofthestandarderrorsarewrong.Thisisofgreatimportanceforthe

conclusionof themodel, as the standarderrorsareused in the calculationsofwhether the

variablesinthemodelaresignificantornot.

Thetestonbetacoefficientslooksasfollows:

€

H 0 :β = 0H1 :β ≠ 0

€

ˆ β x − β x 0

se( ˆ β x )Tn−k−1

The illustration above shows that the standard error of the beta coefficient is used in

calculatingtheteststatisticinthetestonthesignificanceofthebetacoefficient.Aspreviously

discussed,ifheteroskedasticityispresent,theestimateofthestandarderrorsareunreliable,

andtherefore thesignificanceof thecoefficientswillbeunreliableaswell.This isofcrucial