Embed Size (px)

Citation preview

1

RESEARCH SEMINAR SESSION 1, 2003.

A QUALITATIVE EXAMINATION OF MANAGEMENT CONTROL

SYSTEMS IN LARGE AUDIT FIRMS

presented by

Breda Sweeney

National University of Ireland, Galway Date: Friday 7th March

Time: 2:00 p.m. to 3:30

Where: Quad 3005 (Early start due to Vernon Smith presentation.)

The University of NSW School of Accounting

2

A QUALITATIVE EXAMINATION OF MANAGEMENT CONTROL SYSTEMS IN LARGE AUDIT FIRMS

Breda Sweeney and Bernard Pierce

National University of Ireland, Galway and Dublin City University Abstract Audit firms face a constant conflict between the business of auditing and the profession of auditing, characterised in the literature as a cost-quality conflict. This conflict is manifested at trainee levels in the pressure to perform quality work within specified time limits. Prior studies have reported high levels of quality threatening behaviour (QTB) at trainee levels and the importance of examining contributory factors has been highlighted. Multivariate models, based on large-scale surveys have identified some important variables, but calls have been made for in-depth studies to develop a more complete understanding and help refine previous models of auditor behaviour. The objective of this study, the first of its kind, is to conduct a qualitative investigation of how control system variables operate in audit firms and the perceived impact of those variables on QTB. Based on a framework constructed from the management control literature, the study adopted a qualitative approach using 25 semi-structured interviews of audit seniors in four of the (then) Big Five firms in Ireland. The findings suggest that key variables (time pressure, participative target setting, style of performance evaluation and audit review process) have been inadequately operationalised in previous studies. Time pressure emanates not from a single source as suggested previously but from a triad of sources, the balance of which varies over time and is influenced by a range of factors. Participation is heavily influenced by the source of pressure but there is also evidence of a strong interaction between the opportunity for participation and reporting structures. Flatter reporting structures are now in place, promoting asymmetry in the direction of the manager, who is likely to develop more detailed knowledge of all audit areas, and away from the senior who is less likely to be exposed to areas covered by more junior staff. Regarding style of performance evaluation, informal evaluations were reported to be of greater importance than formal evaluations. The shift in performance evaluation approach is not only related to the external economic conditions, but is also facilitated by more regular contact with staff at all levels. The style of audit review has changed to a ‘review by interview’ in audit firms, facilitating more interaction between the manager and the audit team. All of these changes are consistent with the concept of interactive control and a movement away from a diagnostic control system. There is evidence however, that the effectiveness of these interactive controls has been reduced due to understaffing in audit firms at the time of the study. Overall, the study has provided important insights into the nature of the specified variables and their association with QTB. Contributions to the management control literature and areas for future research are outlined.

3

A QUALITATIVE EXAMINATION OF MANAGEMENT CONTROL SYSTEMS IN LARGE AUDIT FIRMS

Breda Sweeney and Bernard Pierce National University of Ireland, Galway and Dublin City University

INTRODUCTION

Previous studies have shown that staff auditors engage in a wide variety of behaviours that threaten audit

quality (Alderman and Deitrick, 1982; Otley and Pierce, 1996a; Malone and Roberts, 1996), collectively

referred to as quality threatening behaviour, or QTB (Pierce and Sweeney, 2002). QTB is defined as any

behaviour by auditors which has the potential to adversely affect audit quality and includes such behaviours

as prematurely signing off tests without completing all the work, biasing sample selection and making

unauthorised reductions in sample sizes. The majority of prior studies have been carried out in the US and

almost all have used either survey questionnaires or experiments to collect data, some of which have sought

to explain the occurrence of QTB using multivariate models. Pierce and Sweeney (2002) adopted the latter

approach and in common with prior research, although their regression model was significant, its

explanatory power was low. They suggested that a likely reason for the low explanatory power is the

changes that have taken place in the audit environment resulting in inadequate operationalisation of variables

and that there is, therefore, a need for research of a more in-depth nature to refine previous models of

dysfunctional behaviour. However, there are major challenges involved in using in-depth methods of

research on sensitive topics and this has been highlighted by a severe shortage of field studies on areas which

could be perceived as threatening for the audit (Gendron and Bedard, 2001) 1.

The purpose of this study is to apply a qualitative research approach to the development of a deeper

understanding of control system variables previously shown to be related to the incidence of QTB, and to

inductively develop some tentative propositions relating to those variables. The study contributes to the

overall contingency literature by demonstrating the contribution of qualitative studies in further developing

contingent models of control systems. The study also represents a response to calls made in the literature for

more in-depth studies of management control issues (e.g. Chapman, 1997; Otley, 1994).

The paper is organised as follows. Firstly, background literature which draws on contingency theory

literature and previous empirical studies of management control in the audit environment is summarised. The

variables examined in the study are then identified and the research method is described. The findings are

then presented and the final section provides a discussion of these findings along with implications of the

findings and possible areas for future research.

This paper is in the early stages of development. Please do not quote without written permission from the authors.

4

CONTINGENCY THEORY OF MANAGEMENT CONTROL

Different theories adopting economic and behavioural views of organisations are used in the management

control literature to gain a better understanding of control issues in organisations. This study is set in the

behavioural management control literature and a contingent view of control systems is adopted.

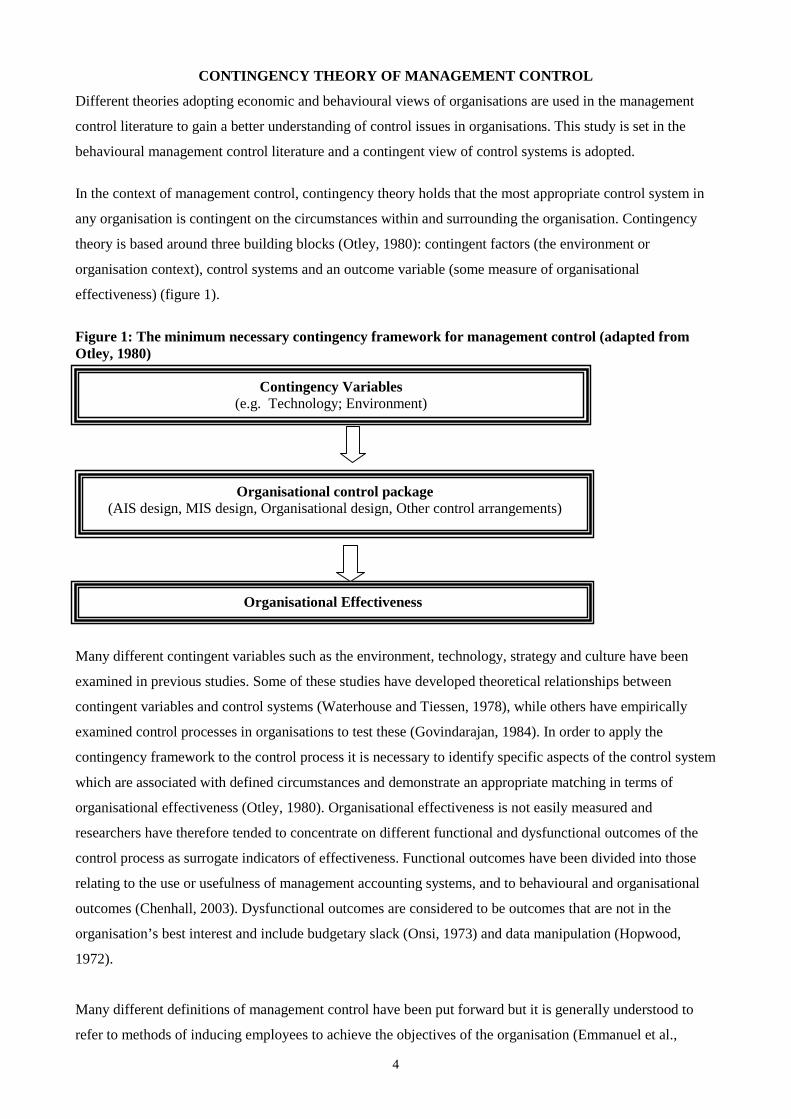

In the context of management control, contingency theory holds that the most appropriate control system in

any organisation is contingent on the circumstances within and surrounding the organisation. Contingency

theory is based around three building blocks (Otley, 1980): contingent factors (the environment or

organisation context), control systems and an outcome variable (some measure of organisational

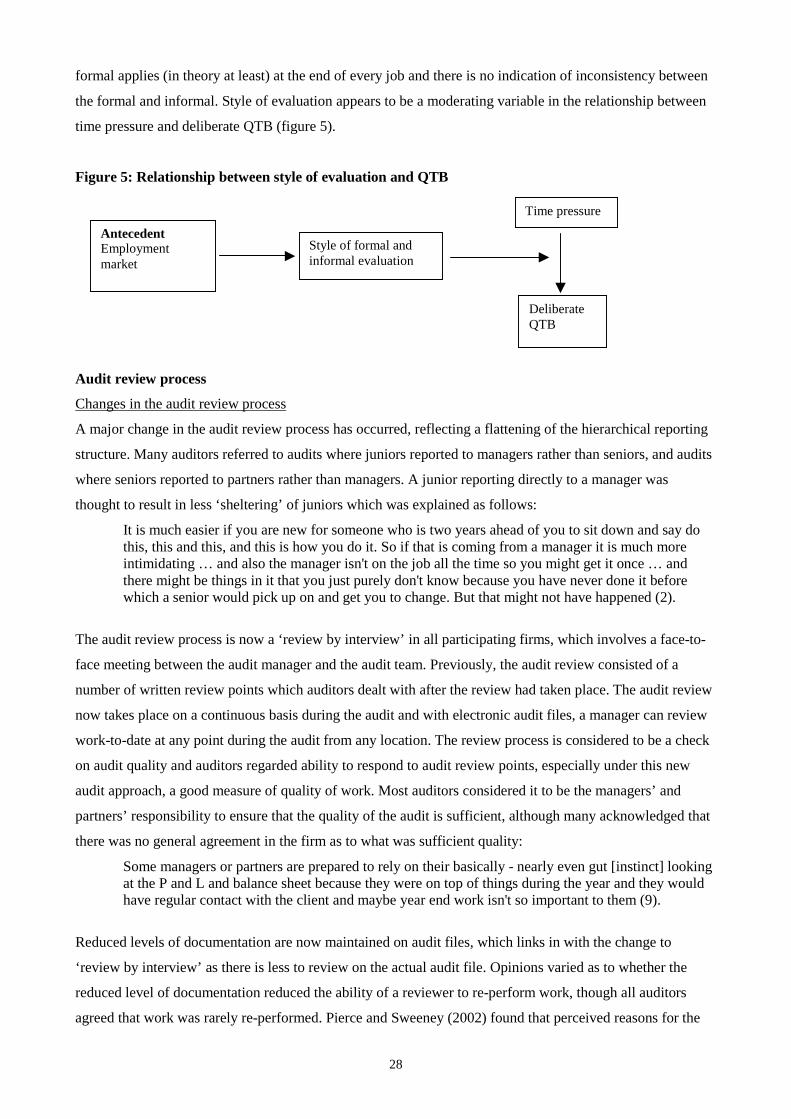

effectiveness) (figure 1).

Figure 1: The minimum necessary contingency framework for management control (adapted from Otley, 1980)

Many different contingent variables such as the environment, technology, strategy and culture have been

examined in previous studies. Some of these studies have developed theoretical relationships between

contingent variables and control systems (Waterhouse and Tiessen, 1978), while others have empirically

examined control processes in organisations to test these (Govindarajan, 1984). In order to apply the

contingency framework to the control process it is necessary to identify specific aspects of the control system

which are associated with defined circumstances and demonstrate an appropriate matching in terms of

organisational effectiveness (Otley, 1980). Organisational effectiveness is not easily measured and

researchers have therefore tended to concentrate on different functional and dysfunctional outcomes of the

control process as surrogate indicators of effectiveness. Functional outcomes have been divided into those

relating to the use or usefulness of management accounting systems, and to behavioural and organisational

outcomes (Chenhall, 2003). Dysfunctional outcomes are considered to be outcomes that are not in the

organisation’s best interest and include budgetary slack (Onsi, 1973) and data manipulation (Hopwood,

1972).

Many different definitions of management control have been put forward but it is generally understood to

refer to methods of inducing employees to achieve the objectives of the organisation (Emmanuel et al.,

Contingency Variables (e.g. Technology; Environment)

Organisational control package (AIS design, MIS design, Organisational design, Other control arrangements)

Organisational Effectiveness

5

1990). Different types of controls are available to an organisation to achieve control and the categorisation of

controls has been performed in a number of ways by different researchers. Hopwood (1974a) categorised

controls into administrative, social, and self-control. Ouchi (1979) divided controls into three fundamentally

different mechanisms: market, bureaucracy, and clan. Emmanuel et al. (1990) presented five categories of

controls: personnel, behaviour, input, output and social. Simons (2000) referred to diagnostic and interactive

control systems, a distinction that relates to how the information is used by managers rather than the actual

content of the control information. He defined diagnostic control systems as ‘formal information systems that

managers use to monitor organizational outcomes and correct deviations from preset standards of

performance’ (p. 209) and interactive control systems as ‘formal information systems that managers use to

personally involve themselves in the decision activities of subordinates’ (p. 216). With diagnostic control

systems, the performance of lower level employees is controlled by monitoring deviations from target on a

number of defined criteria. With interactive control systems however, face-to-face meetings with

subordinates are used to ‘probe subordinates to explain any unforeseen changes in their business and offer

suggested action plans’ (p. 218). The same accounting information can be used in a diagnostic or interactive

manner to control an organisation. Management control literature has consistently emphasised the

importance of understanding the limitations of accounting controls and the role of other forms of control,

particularly in relatively unprogrammed situations (Emmanuel et al., 1990).

Accounting controls

Accounting information is provided within organisations as a means of assisting managers to adapt their

activities so that they can continue to achieve the organisation’s objectives in the face of environmental and

internal changes, and therefore it should have a considerable role to play in the control process (Emmanuel et

al., 1990). Despite heavy criticisms (Bunce et al., 1995) budgets are the most widely used management

accounting control tool (Horngren et al., 2003). Argyris (1952) was the first published study to report the

effects of using budgets on the behaviour of employees and more recently, a substantial body of literature

has developed on budgeting and its behavioural implications in various work settings (Birnberg and Sadhu,

1986). They suggested that a model of the process by which accounting budgets and reports are utilised in

organisations is emerging from these studies. Three issues of critical importance to this process are the

degree of difficulty of budget targets (Emmanuel et al., 1990; Hofstede, 1968), the level of participation in

setting those targets (Shields and Shields, 1998; Brownell, 1982), and the extent of reliance on the targets for

performance evaluation (Hopwood, 1972; Otley, 1978). Research studies on each of these areas are reviewed

in the following sections.

Budget targets

The specificity and level of attainability of budget goals have received considerable attention in the literature

(Hirst, 1987). Two dominant frameworks (expectancy theory and goal setting theory) have emerged to

explain the performance effects of setting performance goals and to guide decisions on specificity and

difficulty of budgets (Kren and Liao, 1988). Both of these theories suggest that performance will increase up

to a certain level of budget difficulty but will decrease beyond that, consistent with an inverted U-shaped

6

relationship between budget tightness and performance (Emmanuel et al., 1990). Empirical findings

regarding the motivational impact of setting budget goals have not, however, been consistent. Hirst (1987)

cautioned against relying too heavily on the psychological literature as little attention has been given to why

goal setting works and to the moderating variables that can limit its effectiveness. He suggested that where

task uncertainty is high, setting budget goals is less effective in promoting task performance than where task

uncertainty is low.

Participation

The accounting literature generally defines participative budgeting as a process in which an individual is

involved with, and has influence on, the determination of his or her budget (Shields and Shields, 1998). A

distinction is made between involvement and influence and for participation to exist, both are considered

necessary. Pseudo-participation, a term coined by Argyris (1952), is defined as involvement and the promise

of influence but after the event the subordinate believes that he or she had no real influence.

The benefits of participation are held to be vertical information sharing, co-ordinating interdependence and

improving motivation and attitudes (Shields and Shields, 1998). Shields and Shields (1998) identified the

antecedents of these benefits/reasons for participation to be information asymmetry along with task and

environmental uncertainty, and task interdependence. Brownell (1982) demonstrated how specific variables

from four major classes (cultural, organisational, interpersonal, and individual) influence the relationship

between participation and its consequences, classifying the first two of these categories as antecedent

moderators and the latter two as consequent moderators. If participation is implemented in situations where

it is not considered appropriate such as where the antecedent conditions do not exist, it can result in

budgetary slack (Hopwood, 1974; Schiff and Lewin, 1970). Schiff and Lewin (1970) conducted an extensive

analysis of the budget and control process in different divisions of three very large firms, and reported that

during the budget formulation stage, divisional managers deliberately build slack into their budgets. They

concluded that the traditional participative budgeting process does not necessarily result in the optimal use of

resources. Not alone has participation been linked to budget slack, it has also been linked to excessively tight

budgets (Otley, 1978), where managers were generally optimistic in setting their budget estimates and

submitted figures that were only infrequently attained.

Overall, the literature highlights a need for a better understanding of the reasons why participative budgeting

exists (Shields and Shields, 1998) and of the antecedents and outcomes of participative budgeting (Brownell,

1982).

Style of performance evaluation

The degree of reliance on accounting performance measures as a measure of supervisory style of evaluation

and behaviours associated with this style has been the focus of much research in the area of management

control (Hartmann, 2000; Brownell and Dunk, 1991). Argyris (1952) was the first to distinguish between the

technical features of an accounting control system and the style of use of accounting information, and the

7

topic commanded strong research interest following publication of apparently contradictory findings by

Hopwood (1972) and Otley (1978).

Hopwood (1972) provided evidence that where accounting information is an imperfect means of measuring

true performance, the use of a rigid style of evaluation (budget-constrained style) is inappropriate, and leads

to dysfunctional consequences such as high degrees of job-related tension, and poor relationships with both

colleagues and subordinates. Hopwood argued that accounting measurements are by their nature imperfect

and that it is important to understand how accounting information can be used to mitigate the observed

dysfunctional effects of a budget-constrained style of performance evaluation. He suggested that the profit-

conscious style, which is a more flexible style of budget use, promotes co-operation and reduces negative

consequences, and also that the way in which managers use budgets is a key determinant of the budget’s

effectiveness.

Otley (1978) replicated some of Hopwood’s work using independent profit centres where budgets were more

technically suited and found little impact of style of budget use on job-related tension or on information

manipulation. He found that a budget-constrained style was related with meeting the budget and did not

result in the negative consequences found by Hopwood. Otley (1978) concluded that his results point toward

the need to develop a more contingent theory of budgetary control and subsequent studies examined the

impact of various contingent variables (Hirst, 1981; Imoisili, 1989; Govindarajan, 1984).

Criticisms of contingency theory

Contingency theory is logically appealing but has been subjected to much criticism on a number of fronts.

These criticisms, however, are generally based on certain aspects of the theory as embodied in studies rather

than with the idea of contingency theory itself (Hopwood, 1989). One of the main criticisms relates to the

methodology used in previous studies, as contingency studies have been mainly ‘ … large scale, cross-

sectional postal questionnaire-based’ (Chapman, 1997, p. 189). Chapman pointed out that these studies

sacrifice accuracy for generality but that many of the subsequent studies have failed to acknowledge this. He

suggested that a greater linkage is needed between qualitative and quantitative studies:

The results of qualitative studies can clearly be seen as providing the starting point of a large body of quantitative literature. But having gained their initial impetus, subsequent studies seemed content to refine existing models, and were at best hesitant to adapt their working assumption in the light of qualitative research on an ongoing basis (p. 203).

More in-depth, qualitative studies of contingency variables is therefore essential, given the rapid pace of

change in the environment. The definition of management control developed in the 1960s is based on large,

hierarchically structured organisations, which are now being replaced by other organisational forms in an

environment characterised by changes in the level of uncertainty and size, outsourcing of services, and

decline of manufacturing activities (Otley, 1994):

Adaptation to change will require the active involvement of many more people than had been traditional and the mechanisms for control of such activities will necessarily involve increased levels of self-control and group accountability (Otley, 1994, p. 292).

8

Contingency studies have had a strong focus on manufacturing settings where tasks and organisation

structures have been more amenable to the successful use of accounting-based controls, and attention now

needs to be directed towards the use of accounting controls in other settings (Abernethy and Brownell,

1997). Using both a survey questionnaire and in-depth interviews, Abernethy and Brownell investigated the

research and development division of an organisation where accounting controls were less suitable because

there was less routine in the task. They used Perrow’s model to explain the relationship between technology

and controls, and found that accounting controls were less suitable where there were high numbers of

exceptions (non-routine items) in performing tasks. The control of time has been highlighted by Otley (1994)

as a key factor in the control of knowledge-based workers (and others), but one that has been almost totally

neglected in the control literature.

Other criticisms of contingency theory relate to piecemeal theoretical development (Briers and Hirst, 1990),

proliferation of antecedent variables (Fisher, 1995), and confusion over definition and measurement of

elements of the contingency model (Chenhall et al., 1981). Fisher (1995) maintained that the relationships

between general control mechanisms and formal control systems have not been explored thoroughly, and that

examining those relationships should provide a clearer understanding of how firms use control systems to

achieve organisational goals.

MANAGEMENT CONTROL IN AUDIT FIRMS

Audit firms are concerned with controlling the cost and quality of an audit. Regarding quality control, the

audit review has been shown to be an important form of quality control as it results in accountability pressure

(DeZoort and Lord, 1997). Auditors are accountable to their superior for the work they have performed and

will have to answer any queries on the work. Changes are taking place in the audit review procedure and the

‘ … emerging trend is the elimination of mandatory, multiple-layered, detail review’ (Rich et al., 1997, p.

88). Audit firms are moving away from a sequential, hierarchical, and iterative audit review to one involving

more verbal interaction (Bedard and Maroney, 1999; Rich et al., 1997). This suggests a move from the use of

the audit review as a diagnostic control to a more interactive one. Regular contact is now maintained

between the preparer and the reviewer, resulting in the audit review taking place on a real time basis (Rich et

al., 1997), often referred to as a review by interview (Bedard and Maroney, 1999). It has also been described

as a process that ‘ … encourages “building in quality” rather than “inspecting in quality” after the fact’

(Winograd et al., 2000, p. 180). This has been suggested to result in a greater ability to detect acts of

omission but a lower ability to detect acts of commission (Rich et al., 1997). The greatest difficulty in

controlling audit quality is the ambiguity of outputs resulting in uncertainty for auditors as to whether they

have conducted a ‘good’ audit (Power, 2003).

Regarding audit cost, control of time has been found to be the dominant form of cost control in audit firms

(Rhode, 1978) and evidence suggests that deviations from time budgets are used in a diagnostic manner to

control time (McNair, 1991). Empirical studies in audit firms have drawn on contingency theory to develop a

9

better understanding of the suitability of time budgets in audit firms (Otley and Pierce, 1996a; Malone and

Roberts, 1996; Pierce and Sweeney, 2002). These studies were based on large samples and identified high

levels of dysfunctional behaviour in Big Four audit firms which were statistically associated with time

budget pressure. Other variables associated with dysfunctional behaviour have also been examined and

multivariate models have been constructed using multiple regression analysis (Pierce and Sweeney, 2002;

Malone and Roberts, 1996), but the explanatory power of these models has been low.

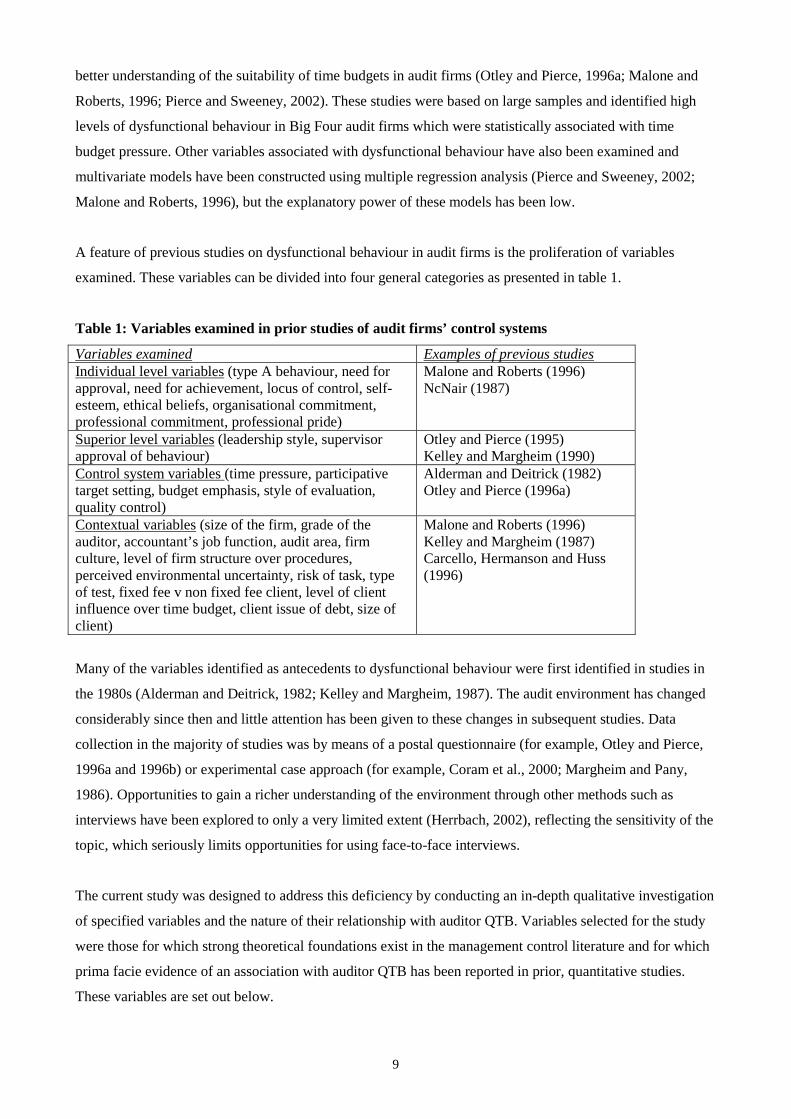

A feature of previous studies on dysfunctional behaviour in audit firms is the proliferation of variables

examined. These variables can be divided into four general categories as presented in table 1.

Table 1: Variables examined in prior studies of audit firms’ control systems

Variables examined Examples of previous studies Individual level variables (type A behaviour, need for approval, need for achievement, locus of control, self-esteem, ethical beliefs, organisational commitment, professional commitment, professional pride)

Malone and Roberts (1996) NcNair (1987)

Superior level variables (leadership style, supervisor approval of behaviour)

Otley and Pierce (1995) Kelley and Margheim (1990)

Control system variables (time pressure, participative target setting, budget emphasis, style of evaluation, quality control)

Alderman and Deitrick (1982) Otley and Pierce (1996a)

Contextual variables (size of the firm, grade of the auditor, accountant’s job function, audit area, firm culture, level of firm structure over procedures, perceived environmental uncertainty, risk of task, type of test, fixed fee v non fixed fee client, level of client influence over time budget, client issue of debt, size of client)

Malone and Roberts (1996) Kelley and Margheim (1987) Carcello, Hermanson and Huss (1996)

Many of the variables identified as antecedents to dysfunctional behaviour were first identified in studies in

the 1980s (Alderman and Deitrick, 1982; Kelley and Margheim, 1987). The audit environment has changed

considerably since then and little attention has been given to these changes in subsequent studies. Data

collection in the majority of studies was by means of a postal questionnaire (for example, Otley and Pierce,

1996a and 1996b) or experimental case approach (for example, Coram et al., 2000; Margheim and Pany,

1986). Opportunities to gain a richer understanding of the environment through other methods such as

interviews have been explored to only a very limited extent (Herrbach, 2002), reflecting the sensitivity of the

topic, which seriously limits opportunities for using face-to-face interviews.

The current study was designed to address this deficiency by conducting an in-depth qualitative investigation

of specified variables and the nature of their relationship with auditor QTB. Variables selected for the study

were those for which strong theoretical foundations exist in the management control literature and for which

prima facie evidence of an association with auditor QTB has been reported in prior, quantitative studies.

These variables are set out below.

10

Time pressure

Most previous studies have equated time pressure with time budget attainability and conflicting evidence has

been found in previous studies on the type of relationship between time budget attainability and QTB. Kelley

and Margheim (1990) found evidence of an inverted U shaped one, though other studies reported evidence of

a positive linear relationship (Otley and Pierce, 1996b; Pierce and Sweeney, 2002). DeZoort and Lord (1997)

identified time deadline pressure as a form of time pressure and Pierce and Sweeney (2002) found both time

deadline pressure and time budget attainability to be significant variables in explaining QTB. Time deadline

pressure was operationalised as adequacy of time booking to job, pressure to work on another assignment

and client imposed deadline. Prior findings provide some insights into the complexity of time pressure but

characteristics other than level and type (deadline or budget) have not been previously addressed.

Participative target setting

Participative target setting has been given little attention in previous studies and where examined, it has been

simply expressed as participation in setting budgets (Otley and Pierce, 1996a; Pierce and Sweeney, 2002).

Conflicting findings have been reported regarding a possible relationship with QTB and no evidence was

found in support of a relationship between time budget attainability and budget participation (Pierce and

Sweeney, 2002), suggesting that even where auditors report that they participate in setting the budget they

have no real influence. The nature and impact of auditor participation in setting targets therefore warrants

further investigation.

Style of performance evaluation

Given that audit firms are labour intensive and audit quality is difficult to measure, pressure for performance

has been found to result from the use of time budgets to control audit cost (McNair, 1991). Previous studies

have found that ability to meet time budgets is a primary criterion for favourable performance evaluations in

audit firms (Kelley and Seiler, 1982) and that the majority of auditors are unable to meet their budgets

without engaging in some form of dysfunctional behaviour (Otley and Pierce, 1996a). Pierce and Sweeney

(2002) found that non-accounting style of evaluation and frequency of written evaluations were significant

variables in explaining QTB. Their findings revealed that the importance of meeting time budgets is now

balanced with other less objective criteria for performance evaluation such as effort put into the job. Style of

evaluation is an important factor in determining how this balance is portrayed to auditors and may impact

upon individual auditor behaviour.

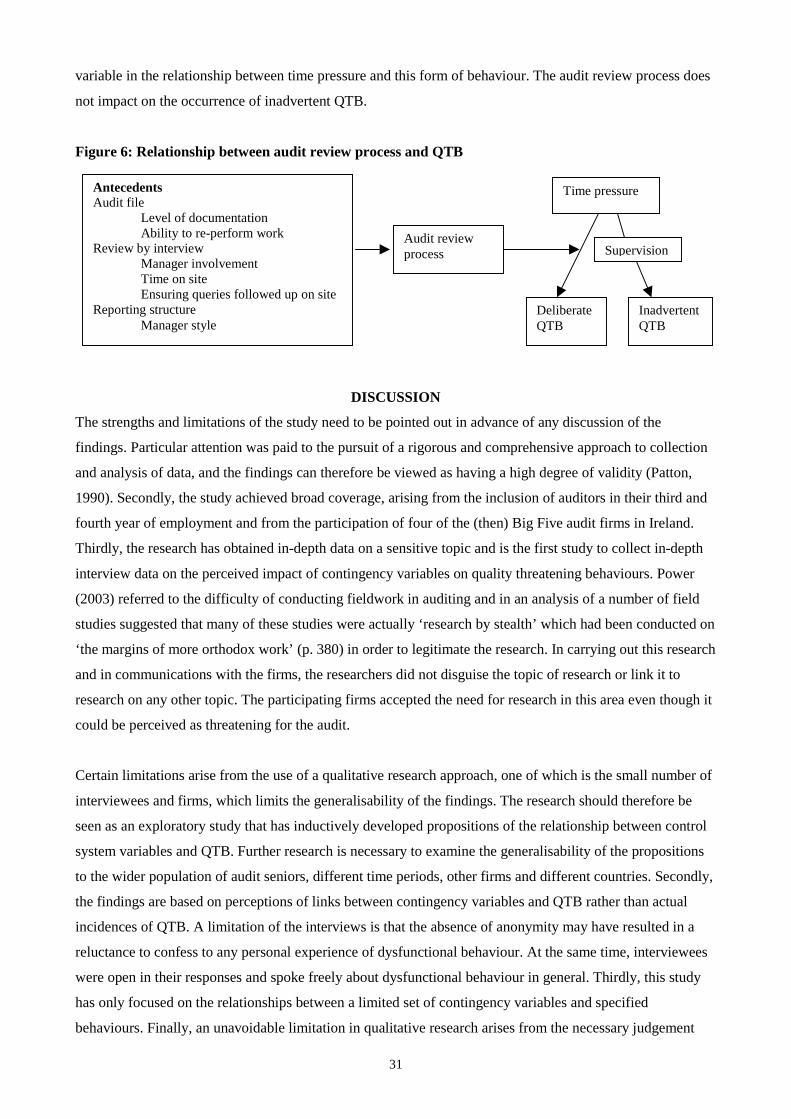

Audit review process

The main control over quality is the audit review which in the case of the ‘review by interview’ approach

takes place during the audit (Rich et al., 1997). Conflicting findings have been reported on the impact of

quality controls on QTB. Otley and Pierce (1996a) reported that perception of the effectiveness of the audit

review was significantly related to QTB, but Malone and Roberts (1996) found that whether a firm had

explicit quality control standards which prohibit QTB was not significantly related to QTB. The changed

audit review process, involving a ‘review by interview’ may impact on the level of QTB and this has not

11

been previously investigated. In light of previous contradictory findings and the revised audit review

approach, further examination of the relationship between the audit review and QTB is warranted.

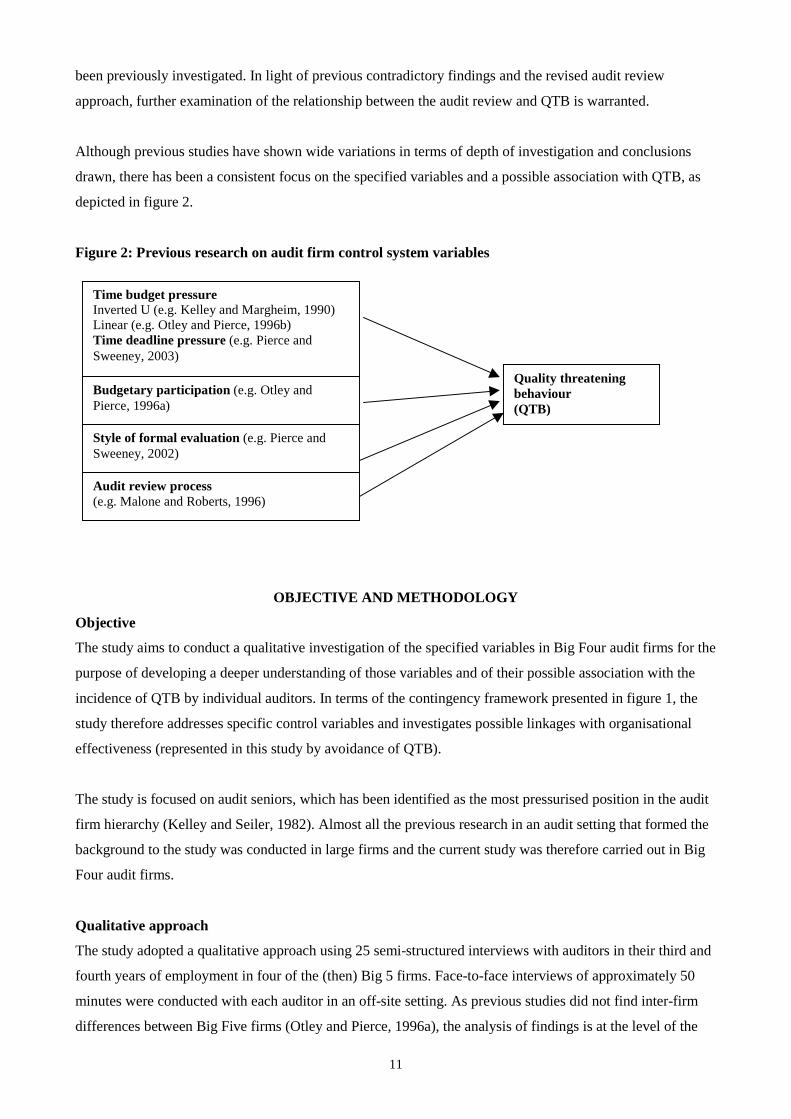

Although previous studies have shown wide variations in terms of depth of investigation and conclusions

drawn, there has been a consistent focus on the specified variables and a possible association with QTB, as

depicted in figure 2.

Figure 2: Previous research on audit firm control system variables

OBJECTIVE AND METHODOLOGY

Objective

The study aims to conduct a qualitative investigation of the specified variables in Big Four audit firms for the

purpose of developing a deeper understanding of those variables and of their possible association with the

incidence of QTB by individual auditors. In terms of the contingency framework presented in figure 1, the

study therefore addresses specific control variables and investigates possible linkages with organisational

effectiveness (represented in this study by avoidance of QTB).

The study is focused on audit seniors, which has been identified as the most pressurised position in the audit

firm hierarchy (Kelley and Seiler, 1982). Almost all the previous research in an audit setting that formed the

background to the study was conducted in large firms and the current study was therefore carried out in Big

Four audit firms.

Qualitative approach

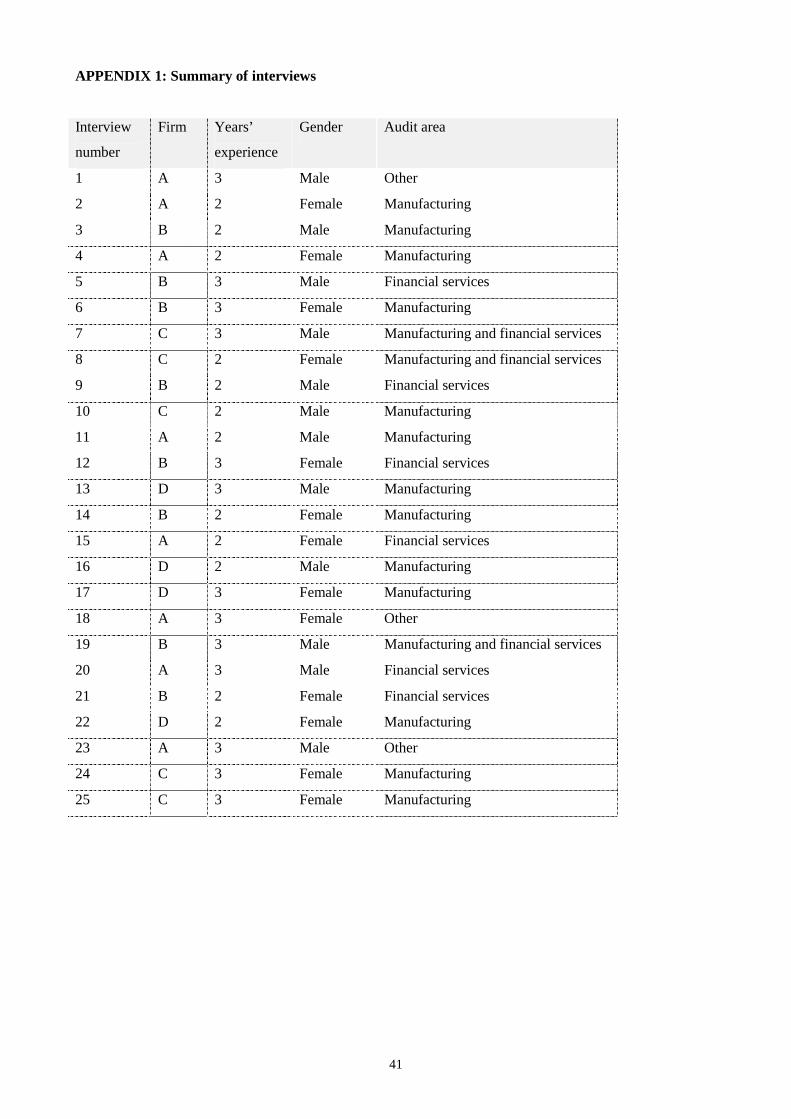

The study adopted a qualitative approach using 25 semi-structured interviews with auditors in their third and

fourth years of employment in four of the (then) Big 5 firms. Face-to-face interviews of approximately 50

minutes were conducted with each auditor in an off-site setting. As previous studies did not find inter-firm

differences between Big Five firms (Otley and Pierce, 1996a), the analysis of findings is at the level of the

Time budget pressure Inverted U (e.g. Kelley and Margheim, 1990) Linear (e.g. Otley and Pierce, 1996b) Time deadline pressure (e.g. Pierce and Sweeney, 2003)

Budgetary participation (e.g. Otley and Pierce, 1996a)

Style of formal evaluation (e.g. Pierce and Sweeney, 2002)

Audit review process (e.g. Malone and Roberts, 1996)

Quality threatening behaviour (QTB)

12

individual and no comparison is made between firms. Qualitative approaches allow issues to be studied in

depth and detail without predetermining categories of responses, and ‘approaching fieldwork without being

constrained by predetermined categories of analysis contributes to the depth, openness, and detail of

qualitative inquiry’ (Patton, 1990, p. 13).

Approximately equal numbers of third and fourth year auditors were selected at random from staff listings

for interview, reflecting a relatively even gender balance. An effort was also made to ensure that auditors

from each of the main audit specialisms (manufacturing, financial services and small companies) were

selected. Appendix 1 sets out the characteristics of each of the interviewees selected. Permission was

obtained from the firms to contact by phone any auditors selected. The firms were not made aware of the

names of the individuals selected and each individual was guaranteed anonymity.

Semi-structured interviews using an interview guide were conducted. The guide was divided into a number

of sections, each section containing general questions and potential probes, and was based on examples of

interview guides in the literature (e.g. Lillis, 1999; Patton, 1990). The interview guide approach enables the

interviewer to have a list of areas for questioning but at the same time allows probing of questions in more

depth depending on the answers provided by the interviewee. Smith (1972) described this approach as ‘ … a

process in which the interviewer focuses her questions on some limited number of points. She may range

quite widely around a point, but this would be done only as a means of getting the required information on

that particular point’ (p. 119). The interview guide approach ‘ … helps minimise bias through the

prespecification of non-directive questions and probes’ (Lillis, 1999, p. 87) and the preconditioning reduces

the tendency to resort to unplanned, non-neutral probes during the interview (McCracken, 1988). Patton

recommended that ‘ … good questions should, at a minimum, be open-ended, neutral, singular, and clear’ (p.

295). These principles were used in the design of questions.

Before commencing, each interviewee was assured of the confidentiality of the study and their permission

obtained to record the interview. Because of the sensitivity of some of the interview questions, it was

emphasised that no other individual would have access to the tapes and that the anonymity of participants

would be fully respected. All interviewees gave permission to tape the interview and no interviewee asked

for the tape to be turned off at any stage. Throughout the interviews, the researcher found no evidence of the

questions being perceived as overly confrontational in any way and interviewees seemed relaxed and willing

to answer questions honestly.

While recognising that no one research method can be truly objective, it is important to document all the

steps taken to increase objectivity as far as possible and to be constantly alert for subjectivity at data

collection and analysis stages (Patton, 1990). Previous field research has been criticised for failing to attend

to such research criteria as validity and reliability (McKinnon, 1988). It is important in obtaining the trust of

readers to disclose fully decisions made in the design of a study and ‘ … at least part of the difficulty in

13

publishing field research lies in convincing reviewers that the study is not only relevant and interesting, but

also trustworthy’ (Lillis, 1999, p. 80).

Several steps were taken to limit bias and increase objectivity both during the interview and in analysing the

interview data. Firstly, the interview guide was used to ensure consistent and complete coverage of all the

themes in each interview. Secondly, as well as taping the interviews, notes were also taken during the

interview to keep a record of important points that needed clarification or that appeared to conflict with other

points. Following each interview, notes were made by the researcher (as recommended by Patton) on such

issues as the level of rapport built up, interviewee’s reaction to questions, initial impressions, and any other

points about the context of the interview which the researcher considered should be noted. Thirdly,

transcripts of the first two interviews were reviewed by a colleague with particular emphasis on objectivity

and freedom from bias in questions. Fourthly, to limit bias in data analysis a structured analytical method

was used and this is described below.

Analysing the data

The importance of a disciplined approach to data analysis is well documented in the qualitative research

literature (for example, Patton, 1990; Miles and Huberman, 1994). Lillis suggested that ‘ … the credibility

and veracity of [any] work relies on the attention to the rigorous, complete and impartial analysis of the

available data’ (p. 81).

The first step in data analysis after transcribing the tapes and saving each of the transcripts in separate

Microsoft Word documents consisted of preparing contact summary sheets for each interview as

recommended by Miles and Huberman (1994). Brief answers to each of the questions on the interview

schedule were included in the contact summary sheets and the transcripts were then coded. This involved

importing the Word document containing the transcript into the software qualitative analysis package NUD-

IST (Non-numerical Unstructured Data – Indexing, Searching and Theorising) and assigning codes to each

sentence. As each interview was coded, codes were refined, which was a straightforward process using

NUD-IST, as any transcripts already coded were easily adjusted. Miles and Huberman suggested that ‘ …

those codes that survive the onslaught of several passes at the site, and several attempts to disqualify them,

will turn out to be the conceptual hooks on which the analyst hangs the meatiest parts of the analysis’ (p. 70).

An initial set of descriptive codes was created before the fieldwork as recommended by Patton (1990) and

these were refined as the interviews progressed. Following each interview, the interview was transcribed, a

contact summary sheet prepared, and the transcript coded before the next interview. This helped to ensure

that the researcher focused attention on key themes and learned from the previous interview.

In analysing the data, the researcher read fully through each of the coded transcripts three times.

Consideration was given to the appropriateness of the coding for each sentence and a report was then printed

on NUD-IST of all the sentences relevant to each code. Each of these sentences was reviewed to determine

the appropriateness of the coding. For presentation of findings, sentences which appeared to represent a

14

particular code/theme were used to present the ‘thick description’ (Denzin, 1994, p. 505) in the findings

section. Patton suggested that ‘ … sufficient description and quotations should be included to allow the

reader to enter into the situation and thoughts of the people represented’ (p. 429-430).

Miles and Huberman (1994) recommended a number of ways of drawing and verifying conclusions, one of

which is pattern analysis. Pattern analysis commenced during data collection. Adding evidence to confirm a

pattern and being open to any evidence that disconfirms it, is important in forming conclusions as it helps to

protect against presenting unreliable evidence (Miles, 1979). Regarding the quality of the findings presented,

the researcher checked to ensure there were no contradictory statements made by the same interviewee and

that the evidence presented to back up each finding appeared to be reliable. Following the first draft of the

‘thick description’ prepared from the individual reports of each code, each of the transcripts was fully read

again to ensure that each of the quotations selected was considered in context and further revisions were

made in the presentation of findings.

Findings are presented in the next section, grouped under the specific variables examined in the study. The

number in brackets after each quotation refers to the interviewee number as set out in Appendix 1.

FINDINGS

Time pressure

Sources and causes of time pressure

Time budget attainability (as a source of time pressure) was the main focus of previous studies on

dysfunctional behaviour (e.g. Otley and Pierce 1996a). However, findings in this study suggest that auditors

are faced with a number of time targets and that time pressure can result from one or a combination of the

following: external time deadlines, internal time deadlines, and time budgets. There was general agreement

among auditors that overall, time pressure had increased in audit firms in the three years prior to the study.

The basic distinction in forms of time pressure was between pressure to have the work completed by a

certain date (deadline pressure) and pressure to control the number of hours charged to a job (budget

pressure). The distinction in forms of time pressure constitutes an important finding, given that most

previous studies of auditor time pressure concentrated entirely on budget pressure. Deadline pressure was

perceived by most interviewees to be more acute than budget pressure when audit firms are operating at full

capacity:

Budgets have never been the main goal … you only have two weeks to do this job so you have to get in and out, so it is more the deadline (15). Yes if you do blow your budget you will have to go and explain it, actually ironically it’s very rare that you blow your budget … you actually physically can’t because you don’t have enough hours to blow it (2).

The findings indicate that audit firms place reduced emphasis on budgets, and on some jobs budgets are not

even set, consistent with the current emphasis in the budgeting literature on a movement away from budgets

(Hope and Fraser, 1997; 1999). The evidence indicates that this decreased focus on budgets is due to the

15

booming economy and staff shortages which have resulted in a time deadline form of cost control, rather

than it being a change of policy by management on the use of time budgets:

They will try and restrict your hours but they understand that we are all working as hard as we can, so if we do go over we have no desire to work overtime. However, it seems to be inevitable at the moment given the amount of jobs versus the amount of staff and I think they know that (25).

The reduction in importance of meeting the budget may explain the positive attitude that many auditors now

have towards budgets:

It helps having a budget definitely because you have an idea, I mean it depends on how many jobs you have in-charged or if you have been on it before … but there are some jobs and there is no budget and it is quite difficult to know (14).

Many interviewees commented on the substantial increase in the volume of work compared to a much

smaller increase in the number of staff (an example was an increase of 27 per cent in the volume of business

over the previous three years compared to an increase of only 10 per cent in the level of staffing over the

same period). Audit firms are now operating at full capacity and resources are perceived to be stretched to

the limit as all staff work to extremely tight internal deadlines to complete their audit work. Further

increasing time pressure is high staff turnover and the recruitment of inexperienced staff. The improved

employment market has led to staff shortages and the increased time pressure resulting from staff shortages

has led to higher auditor turnover. This has become a vicious circle with further staff shortages and further

increases in turnover:

People are just tired and really annoyed … there is a strong atmosphere of you can only do it for three, three and a half years. You don't want to do it for any longer. You know it's not a [question of] people find[ing] auditing boring. It's … I don't really want to work every weekend of my life (2).

Increased time pressure has also arisen from a reduction in the quality and attitude of staff recruited, which

was believed to be a consequence of the improved job market:

The quality of staff they have taken in mightn't be as good as it should be purely because it is being driven by the market ... It is more difficult to recruit to as high a standard as it used to be and that's desperate measures… the attitude as well … of new staff they know they don't have to be there (15).

This reduction in quality of staff was perceived to lead to further time pressure for seniors as it takes longer

to explain the audit work to juniors, and also increased time pressure for juniors as they are slower doing

their work. The supply/demand of staff/audits was seen as mainly impacting on internal deadline pressure.

A source of external time deadline pressure which did not impact on the other time pressures was perceived

to result from international auditors imposing group reporting deadlines on local auditors.

One of two jobs that I have done recently, there were deadlines in relation to a foreign parent company by other auditors, ridicuously hard deadlines to be honest (1).

A further influence on the level of all forms of time pressure was perceived to emanate from the client as the

audit firm very often had to accept fee reductions, changes in timing of the audit, and lack of client

preparation, given the competitiveness of the current environment. The reluctance of clients to accept

16

increases in audit fees was frequently compared to their acceptance of increases in taxation or consultancy

fees. The audit fee was also perceived to impact on even a manager’s ability to influence the time budget.

I suppose they [managers] are getting it from partners, if they can feed it up along the line and say here is a realistic budget, this is what the fee should be, go out and get that fee or else we don't do the job. That is realistically the way it should be done. Instead it comes down to here is the fee, here is the budget and work around that (5).

The level of client preparation for the audit was thought to depend on the timing of the audit and its

proximity to the year-end. Many interviewees accepted time pressure as a fact of life in business and

acknowledged that because clients are under time pressure themselves, they ‘ … don’t have time for

attending to questions from auditors so they are keen to have the jobs done quicker’ (3). Difficulty in

obtaining information from the client and the timing of receipt of information were perceived to lead to

additional time pressure.

Audit specific influences such as the complexity of the client’s business environment, the client’s computer

system, and size of the audit were also perceived to impact on the level of time pressure. The complexity of

the business environment and the sophistication of clients’ computer systems have increased considerably in

the last decade, with consequent implications for the time needed for audit work. The increasing complexity

of clients’ businesses was perceived to have increased the overall time needed for audit work. In some cases,

complexity was perceived to be related to particular industries as some industries such as financial services

were more complex, and that in the manufacturing area:

… they are putting in the long hours for about two months of the year and then that’s it, but in financial services it seems to keep going on and on (15).

Alleviating time pressure was improvements in clients’ systems as ‘the information that is available, if you

know how to ask for it and they [the client] know how to use it or use it to its best ability, can reduce the

amount of work you will have to do’ (4).

The size of the audit was considered significant in determining whether the audit team had to operate under

time budget pressure or time deadline pressure. For example, smaller audits with lower fees were controlled

more tightly by budgets than larger audits. This was perceived to be due to a greater need to make a profit on

the small audit as there is less potential for other profitable work.

Further increasing time pressure is the new risk-based audit approach which was introduced shortly before

the study and auditors were still on a learning curve at the time of the study. It was acknowledged that ‘…

down the line they feel the controls approach will yield savings in terms of budgets’ (10). In addition to these

factors, the increased volume of regulations and standards issued by the profession was thought to have

increased the risk of technical mistakes and increased the time needed on jobs:

The accounting standards aren’t getting any clearer so each time an accounting standard is brought in there is additional work that you didn’t have to do last year. So again that brings it back to the whole budgetary process. Is that built in? (19).

17

In summary therefore, the findings suggest that time pressure arises from three sources: internal deadlines,

external deadlines, and budgets. The level of time pressure from any of these sources is perceived to be

influenced by a number of factors such as client induced pressure, audit specific characteristics (size of audit,

complexity of business environment, and client’s computer system), changes in the audit approach and

volume of regulations. These can be labelled antecedents to time pressure. In addition, staffing issues and the

volume of audit work are antecedents to internal deadlines and pressure from international auditors is an

antecedent to external deadlines.

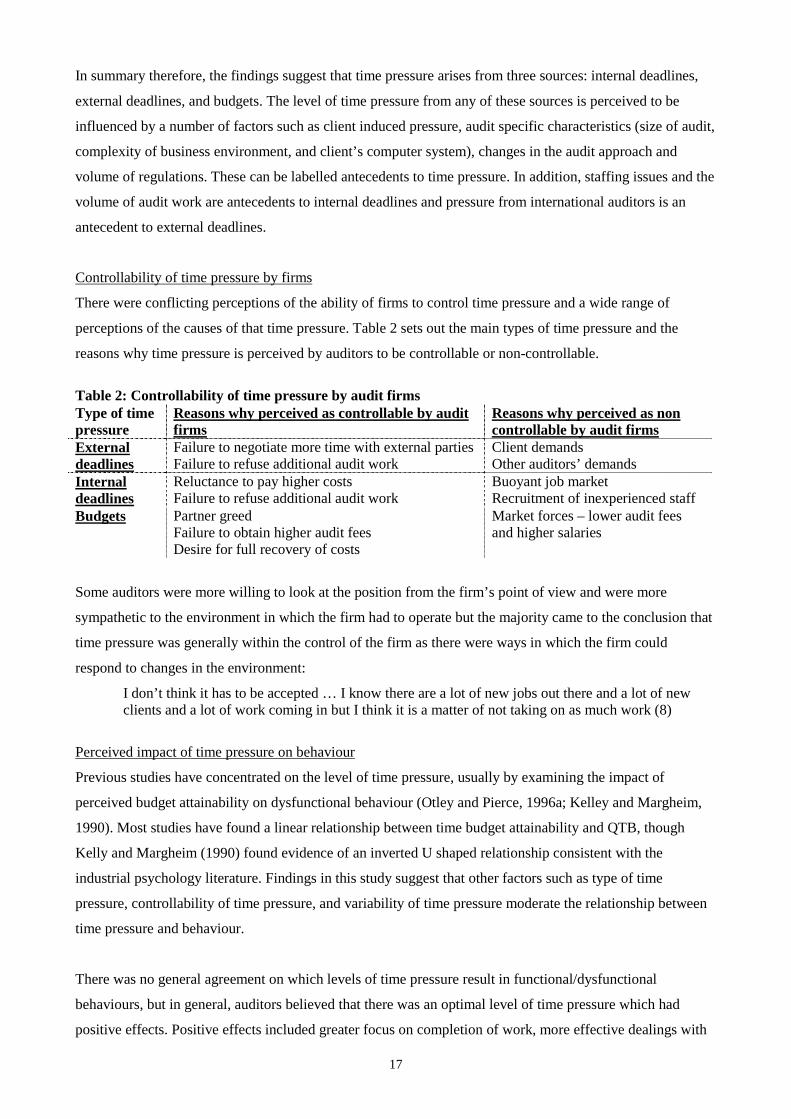

Controllability of time pressure by firms

There were conflicting perceptions of the ability of firms to control time pressure and a wide range of

perceptions of the causes of that time pressure. Table 2 sets out the main types of time pressure and the

reasons why time pressure is perceived by auditors to be controllable or non-controllable.

Table 2: Controllability of time pressure by audit firms Type of time pressure

Reasons why perceived as controllable by audit firms

Reasons why perceived as non controllable by audit firms

External deadlines

Failure to negotiate more time with external parties Failure to refuse additional audit work

Client demands Other auditors’ demands

Internal deadlines

Reluctance to pay higher costs Failure to refuse additional audit work

Buoyant job market Recruitment of inexperienced staff

Budgets Partner greed Failure to obtain higher audit fees Desire for full recovery of costs

Market forces – lower audit fees and higher salaries

Some auditors were more willing to look at the position from the firm’s point of view and were more

sympathetic to the environment in which the firm had to operate but the majority came to the conclusion that

time pressure was generally within the control of the firm as there were ways in which the firm could

respond to changes in the environment:

I don’t think it has to be accepted … I know there are a lot of new jobs out there and a lot of new clients and a lot of work coming in but I think it is a matter of not taking on as much work (8)

Perceived impact of time pressure on behaviour

Previous studies have concentrated on the level of time pressure, usually by examining the impact of

perceived budget attainability on dysfunctional behaviour (Otley and Pierce, 1996a; Kelley and Margheim,

1990). Most studies have found a linear relationship between time budget attainability and QTB, though

Kelly and Margheim (1990) found evidence of an inverted U shaped relationship consistent with the

industrial psychology literature. Findings in this study suggest that other factors such as type of time

pressure, controllability of time pressure, and variability of time pressure moderate the relationship between

time pressure and behaviour.

There was no general agreement on which levels of time pressure result in functional/dysfunctional

behaviours, but in general, auditors believed that there was an optimal level of time pressure which had

positive effects. Positive effects included greater focus on completion of work, more effective dealings with

18

clients, greater attention to relevant information, elimination of unnecessary work and better communication

with superiors:

It will motivate you when you have an achievable target, it will motivate you to work harder and work better. If you have a target and you say there is no way I am ever going to meet that, your work won't be as good even if you do get it eventually done on time. But again if you have weeks to do it it's not going to, there is a level in between (4).

The majority of auditors regarded the current level of time pressure as far higher than optimal, though a

minority of interviewees commented that it was around the optimal level. One auditor believed that what

would be perceived as an optimal level is psychological and that it would vary from person to person, while

others suggested a guideline of working no later than eight o’clock. One auditor expressed the view that,

given the low morale of staff at the present time in accounting firms, the only level of time pressure that

would be optimal was a nine to five day, which would not be considered reasonable by the firms.

In general as time pressure increased, it was perceived that there was a greater likelihood of a dysfunctional

response:

Well I suppose if somebody is under reasonable time pressure they will cope well and when it hits the pot obviously something is going to give. Obviously the work is not going to be to a very high standard but I would say that is going to be in very extreme cases (3). If you have an awful lot of jobs to do and you don't have sufficient time to do them, something is going to suffer … you end up just tying up the figures and you know, you don't get a chance to consider the big picture, the issues or environmental factors or anything like that (21).

The dysfunctional response was thought to occur at the end of the job by many auditors where time pressure

arose from client factors:

The client has given you some kind of reconciliation and you have been asking for the reconciliation for four weeks and you are doing something else and this is like your job that you have to finish up, it is looming over you all the time and he faxes you in a bit of paper, like there is something there and you know you should ask for more backup but you go - ah I will just put it on the file and reference it in, like the director or manager will have a query anyway and if they ask for the backup fair enough you will get the backup, but if you can get away with not doing the work (18).

Other consequences of increased levels of time pressure were perceived to be a lower level of training and

increased responsibility. In general it was felt that there is now less time for on the job training and increased

responsibility due to time pressure:

I don't think they [juniors] are being given the required training (this better be confidential)… and even at a senior level, I have been in there three years and this is my first year as a senior, and you are being given ridiculous stuff to do because it is being pushed all the way down. And managers are not doing their job so they are relying on you to basically manage the job yourself, and you know have a file ready to go to a partner review (15). In my second year, I would have noticed that I would have being doing work that a person a year above me would have done the year before. You are just literally moved up along the ladder (5).

Training courses were not generally seen as effective as ‘ … the tendency at these things is to see them

almost as a week’s holiday’ (11) because of the time pressure auditors are under for the rest of the year.

19

Furthermore, interviewees claimed that training courses are often held during holiday periods and no effort is

made to ensure that the people who need training in a particular area are available. Reduced training and

increased specialisation were seen by auditors as restricting the learning experience during the training

contract. Inadvertent QTB due to lack of training and increased responsibility at junior level was referred to

by interviewees but it was believed that this would be detected by the senior. However, audit seniors

interviewed showed a reluctance to report this behaviour:

I know a number of instances where juniors were caught by my level [senior] and they might have been warned. People would be very hesitant to go straight away to a manager and say “you know they are signing-off tests and they haven't done anything”. I mean because it is such a big thing they mightn't realise just coming in new (21).

Regarding the existence of a linear or an inverted U-shaped relationship between time pressure and

dysfunctional behaviour, in this study different viewpoints were given on whether dysfunctional behaviour

would start to decrease once the time pressure reached a certain point. Most auditors maintained that time

pressure above a certain level resulted in low motivation to meet either the deadline or the budget:

If the time budget was totally unrealistic last year you are not going to even try to achieve it (7). Obviously then if work becomes unrealistic, it is obvious to see you might have a two week job and there is no way it will be done in three weeks in which case people will work a certain amount of overtime, but they are not going to kill themselves because they know it is totally unrealistic (5).

These comments suggest that at a certain level of time pressure, auditors stop trying to meet the time target

whether it is a budget or a deadline. This would support the existence of an inverted U-shaped relationship.

Given, however, the low level of morale and motivation that would be experienced at this point, auditors

may still reduce quality but for different reasons and thus the relationship would appear linear. Not all

interviewees agreed that auditors would stop trying to meet unrealistic time constraints, and a minority

suggested that even for unrealistic time deadlines:

It will just be a case of whoever is on the job will muck in and get it done. Obviously it may not be to the most perfect of audits but it will probably still be up to a high enough standard to pass file review (3).

A certain level of budget overrun was perceived to be acceptable but above that an auditor will have to

explain any overruns and therefore even for impossible to achieve budgets, an auditor would still be

motivated to reduce time. This supports the existence of a linear relationship between budget pressure and

dysfunctional behaviour.

There was no general agreement on what levels of time pressure are likely to result in QTB and moderating

factors such as type of time pressure, perceived controllability of time pressure and variability of time

pressure were thought to be important in determining its impact. Type of time pressure was considered

important in explaining the relationship between time pressure and dysfunctional behaviour as in general,

auditors found external deadlines tighter than internal targets or budgets and were more likely to cut corners

as a result of external deadlines, as these deadlines were perceived to be non-negotiable:

20

If it is the case where the 16th of March you have to have whole loads of accounts sent off to the UK for a plc definitely you have to have that done come hell or high water. And where corners have to be cut they will be if you have to get the accounts off. So maybe quality will suffer if that is the case, if it is just an internal thing you know you can push them off (13).

A minority maintained that it made no difference whether the pressure was due to internal or external factors:

Pressure is pressure. It all leads to one thing, get things done quicker you know, no matter what way you look at it I think you will react the same way because it always comes back through the partner. Either the partner is telling you to hurry up or the client is telling the partner to tell you to hurry up, either way he will tell you and you are going to want to keep him happy (13).

Regarding budgets, one auditor believed that ‘ … budgets have bigger implications for quality than

deadlines’ (1) as partners and managers are more aware of the pressures from deadlines and take this into

account in the audit review, and also if the budget is tight, the manager will be reluctant to spend much time

on review as his/her charge-out rate is high. Though this represents the view of only one auditor it gives

insights into a perceived relationship between quality controls (audit review) and time pressure.

Regarding the perceived reason for time pressure, there was no general agreement on whether the

implications of time pressure differed depending on auditors’ perceptions of the controllability of time

pressure by audit firms. Some believed that time pressure perceived as uncontrollable by the firm had a more

positive effect on motivation and behaviour, as pressure from outside sources affected all levels and it was

not a ‘them and us’ scenario between management and staff:

I would think that morale would be affected more by internal pressure than by external. You know generally if people are working towards an external deadline, okay this is something that is outside of everyone's control and they would work to that ... Whereas internal pressure, I think people resent the fact that there wasn't more staff put on it ... If a manager is cutting budgets there might be a resentment that the manager might be caring more about the budget than about the staff (9).

Others maintained that time pressure emanating from the client made audit work easier as the client would

ensure complete information was available but for internal time pressure, the client would not necessarily be

as well prepared.

Regarding the effect of the level of variability of time pressure, two aspects were considered important in

moderating the relationship between time pressure and QTB. Firstly, a low level of uniformity between

auditors was perceived to lead to low morale:

If everybody isn’t as busy it has got a very bad effect, if you sort of see some people leaving at 5.30 … and then you have other people in until 10.30 and if you are the person in until 10.30 it is very demoralising (10).

Secondly, the constancy of the time pressure from one job to another could have adverse effects. In general,

interviewees believed that time pressure varied far less between jobs than when they commenced working in

the firms. Also, the busy season was seen to be continuous and year-long in the current environment:

I think that is probably the difference in the last few years is that it used to vary much more. There used to be maybe jobs that you would do for a month where you would have serious time pressure and then the next month you would be doing more relaxing jobs or at least you would be working

21

normal hours, whereas now you are going from a really stressful job to another really stressful job to another really stressful job. So they don't have a time in between, and that creates a really bad atmosphere (2).

A minority of auditors thought that time pressure varied considerably between jobs. This was attributed to

several factors such as (1) client pressure, (2) the bargaining power of the manager in getting staff for the

job, (3) the employee grading system where auditors from the same intake can have different charge-out

rates depending on their educational background, and (4) the amount of time spent by the manager on

review. These represent perceived antecedent variables of time pressure, some of which were identified in

the previous section. Regarding the effect of the time spent by the manager on review:

You have a lot more time than you are budgeted for because you know the manager isn’t going to spend much time on the job. Say you have a £20,000 budget, fifteen of it is yours and five is the manager’s, if you know he is not going to use his five you can use more on yours (13).

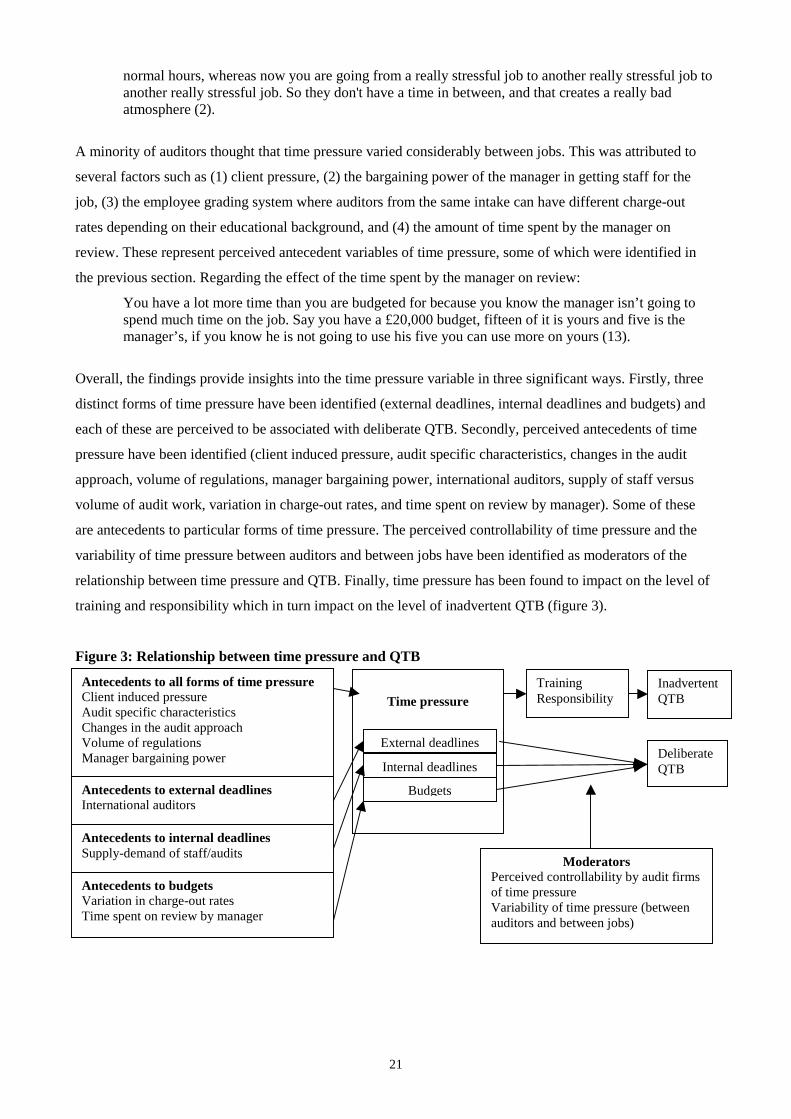

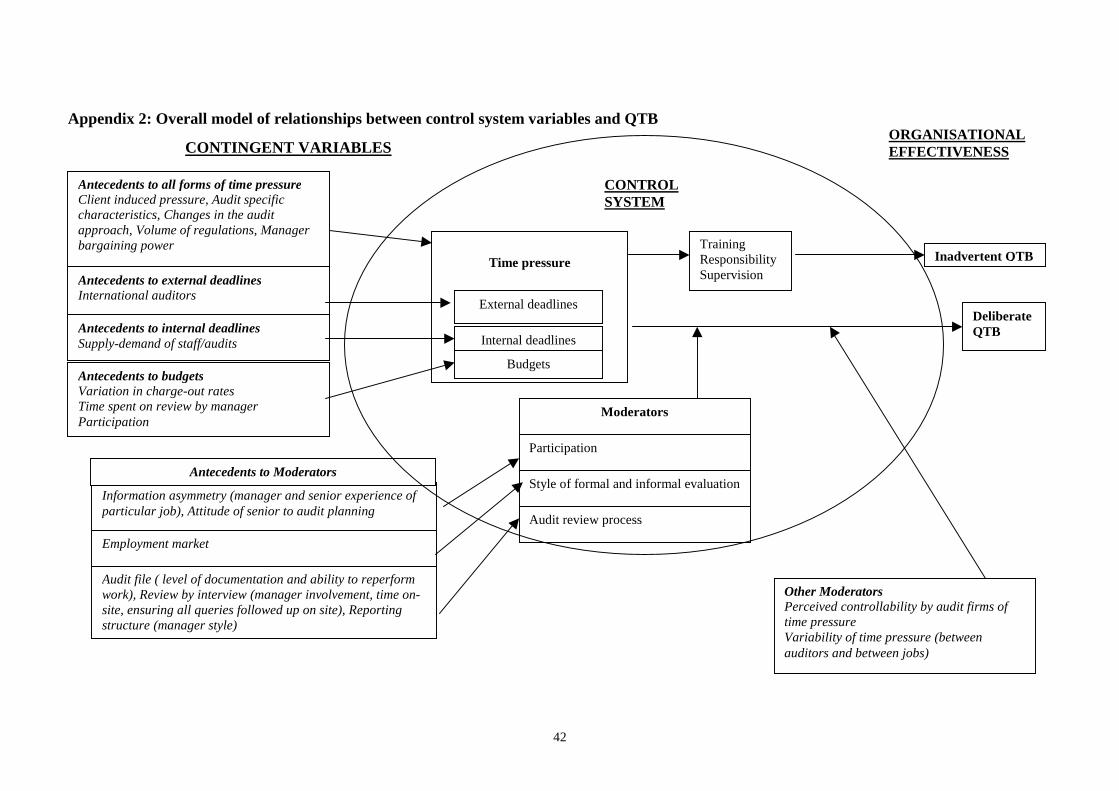

Overall, the findings provide insights into the time pressure variable in three significant ways. Firstly, three

distinct forms of time pressure have been identified (external deadlines, internal deadlines and budgets) and

each of these are perceived to be associated with deliberate QTB. Secondly, perceived antecedents of time

pressure have been identified (client induced pressure, audit specific characteristics, changes in the audit

approach, volume of regulations, manager bargaining power, international auditors, supply of staff versus

volume of audit work, variation in charge-out rates, and time spent on review by manager). Some of these

are antecedents to particular forms of time pressure. The perceived controllability of time pressure and the

variability of time pressure between auditors and between jobs have been identified as moderators of the

relationship between time pressure and QTB. Finally, time pressure has been found to impact on the level of

training and responsibility which in turn impact on the level of inadvertent QTB (figure 3).

Figure 3: Relationship between time pressure and QTB

Antecedents to budgets Variation in charge-out rates Time spent on review by manager

Time pressure

Deliberate QTB

Moderators Perceived controllability by audit firms of time pressure Variability of time pressure (between auditors and between jobs)

External deadlines

Internal deadlines

Budgets Antecedents to external deadlines International auditors Antecedents to internal deadlines Supply-demand of staff/audits

Antecedents to all forms of time pressure Client induced pressure Audit specific characteristics Changes in the audit approach Volume of regulations Manager bargaining power

Training Responsibility

Inadvertent QTB

22

Participation

Participation in setting both budgets and deadlines (internal and external) was examined and interviewees

considered the distinction between budgets and deadlines important in determining the degree of influence

possible over the setting of time targets. In general, both internal and external deadlines were perceived to be

impossible to influence by seniors as they were subject to such constraints as client pressure, pressure from

international auditors, low fees and staff shortages:

The trouble with it is if you are given too short a time for a job, they’ll listen to you and say “yea, yea we know it should take two weeks but you only have a week, and the reason you only have a week is because you are doing something else the following week” (2).

Regarding participation in setting budgets, the findings indicate that the level of audit senior participation

varies significantly between audit seniors even within the same audit firm. The following two respondents

were at the extremes in firm C:

The budget really seems to me to be set in stone and you are going to have to try to build your work around it (10). On some jobs I would set the budget … you would be looking at what sort of time-frame you need on the job and what sort of staff you have (7).

Antecedent variables

Interviewees were questioned on what they perceived to be antecedents of participation and what impact, if

any, they perceived participation has on individual auditor behaviour. The findings indicate that it is difficult

to implement participative budget-setting because the conditions suggested in the literature for successful

adoption of a participative approach are rarely present in the audit environment.

Information asymmetry between the manager and the senior where the senior has more information than the

manager only exists in very specific circumstances where, for example, the senior has worked on the audit in

previous years:

If you were a junior the year before and you are a senior the following year, and as a junior you knew you were under pressure the year before and it was a seven day job and this year it is a six day job so you might say “hang on here we were under pressure last year”, so it wouldn't be like we would be putting in the detail on the budget like this section should be another hour (3).

Where this is not the case, the manager is regarded as being in a better position to provide a more accurate

assessment of the time needed. Information asymmetry may also exist where a manager on a job has no

experience of a particular client. One auditor reasoned that he was given more influence in setting the time

this year because he was working for directors who were new in the firm and that it was not due to any

policy change on participation. Information sharing by the subordinate with the superior is rarely necessary

as the superior generally has more information than the subordinate. Auditors referred to situations where

they were involved in planning jobs that they were not going to work on because they were available at the

time when planning was taking place and that it was just a case of following managers’ instructions as to

what changes to put through from last year. Even though these auditors were involved in setting the time,

they had no influence, nor had they a stake in the budget-setting process as they were not assigned to these

23

jobs. Where time is reduced from the previous year and the senior was not on the job before, the senior can

try to negotiate extra time if he/she knows the time charged the year before:

It is the senior’s responsibility to go to the manager and say “well they had this amount of time last year and this is what we will need this year, what is the difference, show me where there is less work” (9).

This amounts to forced participation and the senior is at a disadvantage in that he/she has no knowledge of

the accuracy of the time charged the previous year. The view was expressed that it would be a waste of time

telling the manager that the time recorded last year might not have been accurate if that manager was on the

job last year as:

If you have the same manager on a few years in a row he is going to know and if he knows then he is the one pushing it. So it is kind of a year on year thing, and you often find if the manager changes on a job then the budget changes as well (2).

Also, it was pointed out that the degree of uncertainty in the audit environment makes it difficult to predict

the amount of time needed on a job and the senior would not be in a position to reduce this uncertainty

before the job commences:

25 per cent of the time would be spent on stuff that was never even foreseen and it just came to light within the course of the audit (19).

The previous year’s senior was perceived to have a role in reducing information asymmetry and to be in a

position to influence the current year's time target by accurately recording time the year before. Setting a

budget often amounts to ‘ … just a case of looking at last year’s and adding on a bit or taking off a bit’ (3).

This view was expressed by many interviewees and typified by the following quote:

In a lot of the jobs you wouldn't have any influence, a manager just sets it and rolls it forward from previous years. I know one or two managers who would make a conscious effort of kind of saying “just record your time on the different sections you are working on, be realistic about it because it helps next year's audit”. That's the way it should be done but in most cases it is just roll it forward from last year (5).

Other auditors referred to ‘old school managers’ (21) who could plan their jobs in 10 minutes and saw

participation as a delay. These experienced managers, however, were seen as more approachable if there

were problems:

I generally find that more experienced managers would be more approachable, because I think new managers sometimes feel themselves under pressure and out of their depth, and they feel that if they have to get someone else for a week it is going to look bad on them, you know. They are a lot more lacking in confidence or you know not as used to the whole system (21).

Because of the particular characteristics of the audit environment (rotating audit team, high staff turnover

and nature of audit work) the opportunities for genuine participation by audit staff in preparing time targets

are limited and the degree of participation is generally perceived to be low.

Perceived impact of participation on behaviour

Participation was linked to improved motivation to meet the time target by some interviewees but it was

thought that this improved motivation could result in either functional or dysfunctional behaviour. By

24

adopting a participative budget-setting approach, managers are ensuring that seniors take more responsibility

for the budget. On the dysfunctional side, it was thought that participation ‘could create pressure not to blow

the budget’ (7) because the senior would have been responsible for setting it. The management control

literature suggests that the use of budget participation in conditions where it is not suitable can result in

budgetary slack (Schiff and Lewin, 1970) or excessively tight budgets (Otley, 1978). Evidence in this study

suggests that participation could actually result in higher QTB if excessively tight budgets have been set to

impress a manager. On the functional side, however, participation was linked with more realistic time

pressure, which was considered a motivating factor in trying to meet targets:

I don’t think it is a case of - I have set the budget so that is a motivating factor. But indirectly if the time budget was totally unrealistic last year you are not going to even try to achieve it, whereas if this year you have an extra staff person on board then … it is a bit of a motivating factor (11).

In order for participation to result in improved motivation however, interviewees maintained that audit

seniors need to regard planning as equally important to other audit work, which was not perceived to be the

case at present. Auditors are perceived to be so overworked that if they are given time to plan a job ‘ … they

are going to take their foot off the gas and relax’ (9). Because of this, it was perceived that managers were

reluctant to assign auditors to planning. The attitude of the senior to planning is an additional antedecent to

participation.

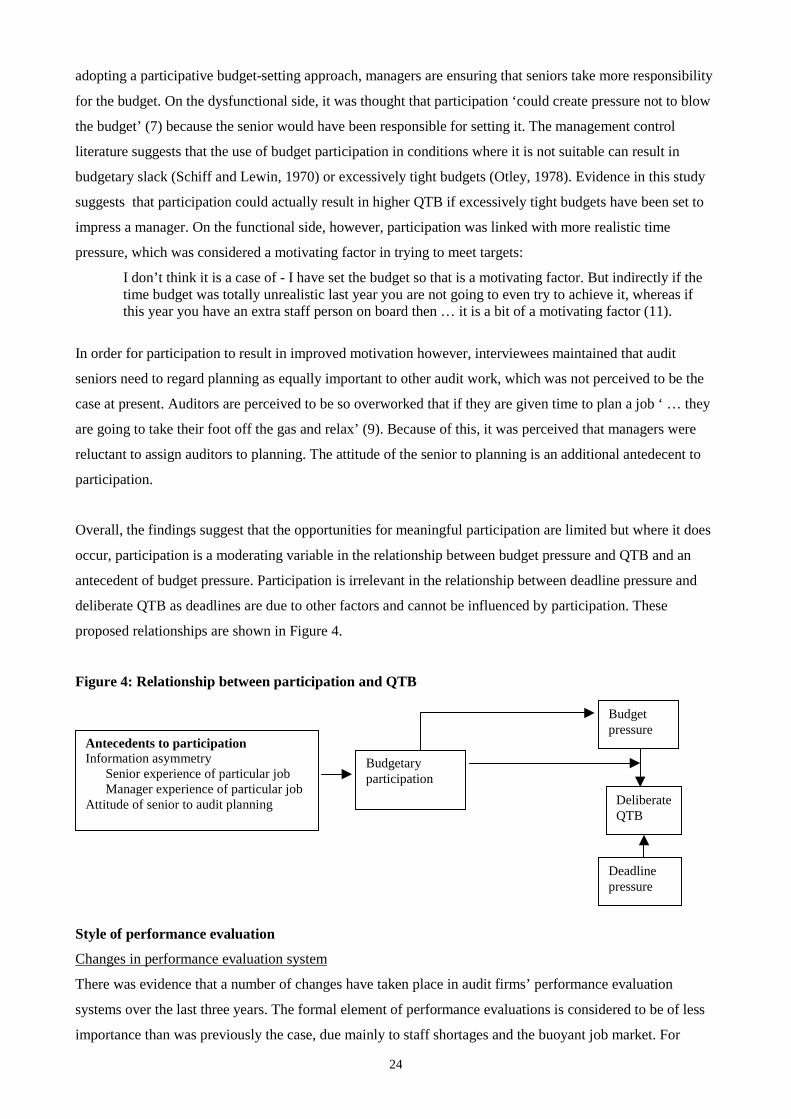

Overall, the findings suggest that the opportunities for meaningful participation are limited but where it does

occur, participation is a moderating variable in the relationship between budget pressure and QTB and an

antecedent of budget pressure. Participation is irrelevant in the relationship between deadline pressure and

deliberate QTB as deadlines are due to other factors and cannot be influenced by participation. These

proposed relationships are shown in Figure 4.

Figure 4: Relationship between participation and QTB

Style of performance evaluation

Changes in performance evaluation system

There was evidence that a number of changes have taken place in audit firms’ performance evaluation

systems over the last three years. The formal element of performance evaluations is considered to be of less

importance than was previously the case, due mainly to staff shortages and the buoyant job market. For

Antecedents to participation Information asymmetry Senior experience of particular job Manager experience of particular job Attitude of senior to audit planning

Budgetary participation

Budget pressure

Deliberate QTB

Deadline pressure

25

promotion to manager, one auditor described the situation in audit firms as being ‘ … more sticking it out

and putting in your time kind of civil service type’ (8):

I think everyone has to keep everyone happy all the time otherwise they will just leave because they will be fed up. There are so many jobs out there, promotion is more if you are there you will get promoted at this stage (17).

Previous studies have referred to the ‘up or out’ promotion system in audit firms which results in strong

internal competition, particularly in periods of overstaffing (McNair, 1991). Findings in this study suggest

that in the current period of understaffing, promotion is more automatic for auditors who remain with the