Embed Size (px)

Citation preview

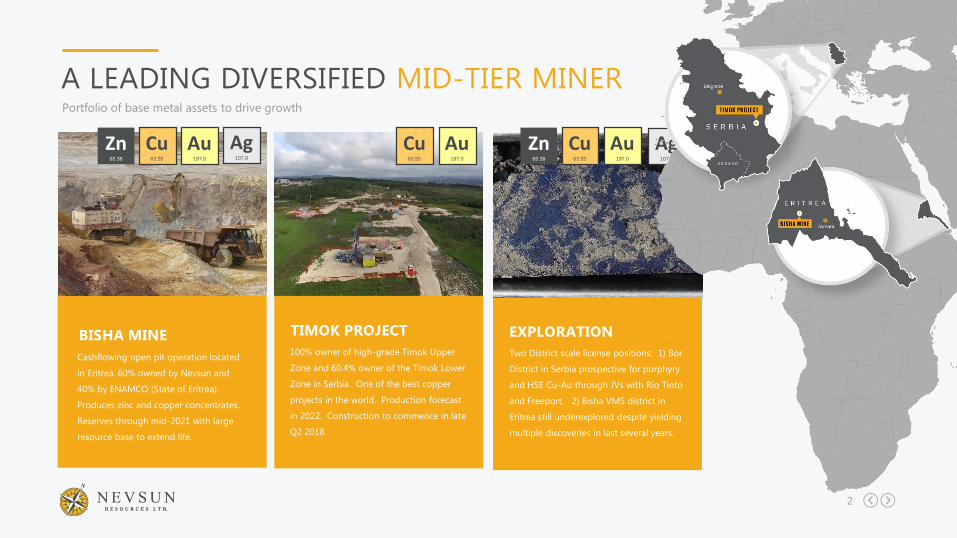

A LEADING DIVERSIFIED

MID-TIER MINER

CORPORATE PRESENTATION

Q2 2018

TSX & NYSE AMERICAN NSU

2

A LEADING DIVERSIFIED MID-TIER MINERPortfolio of base metal assets to drive growth

Cashflowing open pit operation located

in Eritrea. 60% owned by Nevsun and

40% by ENAMCO (State of Eritrea).

Produces zinc and copper concentrates.

Reserves through mid-2021 with large

resource base to extend life.

BISHA MINE100% owner of high-grade Timok Upper

Zone and 60.4% owner of the Timok Lower

Zone in Serbia. One of the best copper

projects in the world. Production forecast

in 2022. Construction to commence in late

Q2 2018.

TIMOK PROJECT

Two District scale license positions; 1) Bor

District in Serbia prospective for porphyry

and HSE Cu-Au through JVs with Rio Tinto

and Freeport. 2) Bisha VMS district in

Eritrea still underexplored despite yielding

multiple discoveries in last several years.

EXPLORATION

Zn65.38

Au197.0

Ag107.9

Cu63.55

Au197.0

Cu63.55

Zn65.38

Au197.0

Cu63.55

Ag107.9

3

INVESTMENT HIGHLIGHTSA leading diversified mid-tier miner with a strong debt free balance sheet to fund growth

Upper Zone PFS $US1.8B NPV and

80% IRR (after tax)*. Follow up FS in

H1’19. Exploration decline to start in

Q2’18 with production in 2022.

Exploration for more UZ deposits

underway.

HIGH GRADE CU-AU

PROJECT IN TIMOK

LOW RISK ZN-CU CASH

FLOW FROM BISHA

210 to 240 million lbs of zinc at C1

cash cost of $0.70 to 0.90/lb in

2018. Upside from large resource

base and regional greenfield

exploration for near surface

deposits.

STRONG BALANCE SHEET

TO FUND GROWTH

~US$150 million in cash and no

debt at March 31, 2018.

TRACK RECORD OF

SUCCESS

Nevsun and management have a

track record of successful mine

building and delivering value to all

stakeholders

*Note: $US1.8B NPV and 80% IRR excludes pre-construction capital of $114M

4

EXPERIENCED MANAGEMENT & BOARDNevsun management and Board has a strong history in successful mine building and operating

Peter Kukielski, CEO

Joe Giuffre, CLO

Ryan MacWilliam, CFO

Scott Trebilcock, CDO

Jerzy Orzechowski, VP & Project Director, Timok

Adam Wright, Heads of Operations

Cara Allaway, VP Group Controller

Marc Blythe, VP Corp Dev

Peter Manojlovic, VP Exploration

Todd Romaine, VP CSR

MANAGEMENT

Ian Pearce, Chairman

Ian Ashby

Geoff Chater

Anne Giardini

Peter Kukielski

Stephen Scott

David Smith

DIRECTORS

PETER KUKIELSKI

CEO

“

”

In 2017 we made

a number of strategic decisions

to position Nevsun for long –

term success. Collectively, our

new Management Team and

Board has decades of

development experience

through the building of

multiple projects and deployed

tens of billions in capital.

5

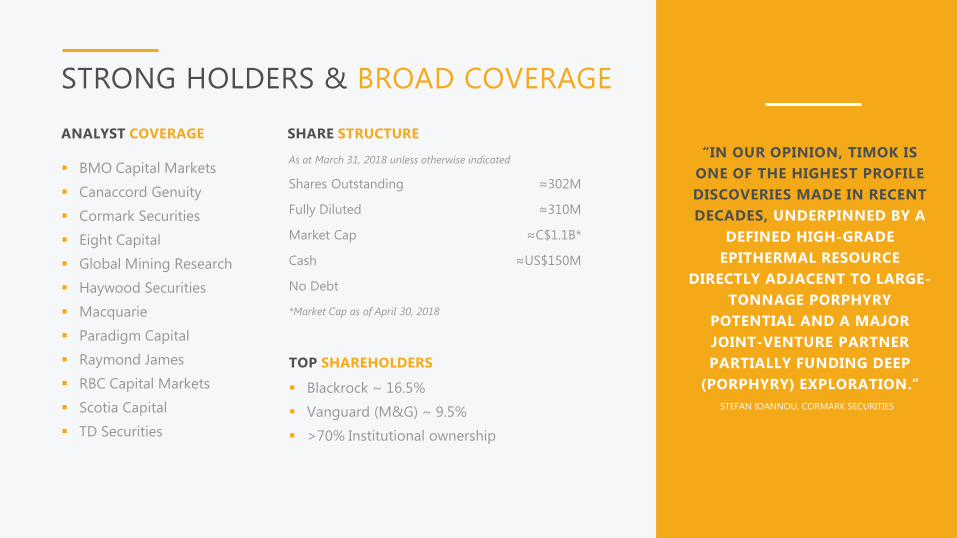

STRONG HOLDERS & BROAD COVERAGE

▪ BMO Capital Markets

▪ Canaccord Genuity

▪ Cormark Securities

▪ Eight Capital

▪ Global Mining Research

▪ Haywood Securities

▪ Macquarie

▪ Paradigm Capital

▪ Raymond James

▪ RBC Capital Markets

▪ Scotia Capital

▪ TD Securities

ANALYST COVERAGE

▪ Blackrock ~ 16.5%

▪ Vanguard (M&G) ~ 9.5%

▪ >70% Institutional ownership

TOP SHAREHOLDERS

As at March 31, 2018 unless otherwise indicated

Shares Outstanding ≈302M

Fully Diluted ≈310M

Market Cap ≈C$1.1B*

Cash ≈US$150M

No Debt

SHARE STRUCTURE

“IN OUR OPINION, TIMOK IS

ONE OF THE HIGHEST PROFILE

DISCOVERIES MADE IN RECENT

DECADES, UNDERPINNED BY A

DEFINED HIGH-GRADE

EPITHERMAL RESOURCE

DIRECTLY ADJACENT TO LARGE-

TONNAGE PORPHYRY

POTENTIAL AND A MAJOR

JOINT-VENTURE PARTNER

PARTIALLY FUNDING DEEP

(PORPHYRY) EXPLORATION.”

STEFAN IOANNOU, CORMARK SECURITIES

*Market Cap as of April 30, 2018

TIMOKPROJECTOne of the best copper projects in the world, is located in the historic Bor

mining district in Serbia within close proximity to existing mining infrastructure.

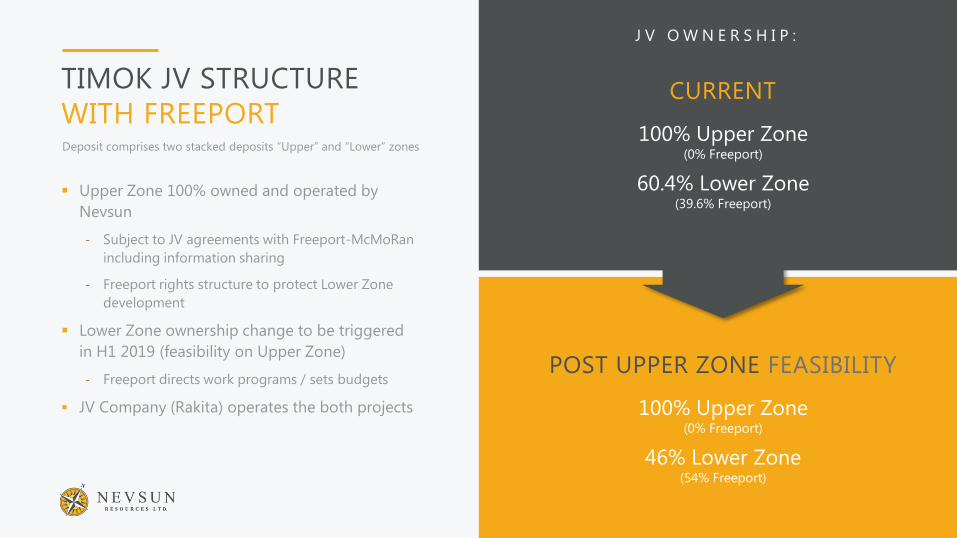

TIMOK JV STRUCTURE

WITH FREEPORTDeposit comprises two stacked deposits “Upper” and “Lower” zones

POST UPPER ZONE FEASIBILITY

100% Upper Zone (0% Freeport)

46% Lower Zone(54% Freeport)

▪ Upper Zone 100% owned and operated by

Nevsun

- Subject to JV agreements with Freeport-McMoRan

including information sharing

- Freeport rights structure to protect Lower Zone

development

▪ Lower Zone ownership change to be triggered

in H1 2019 (feasibility on Upper Zone)

- Freeport directs work programs / sets budgets

▪ JV Company (Rakita) operates the both projects

J V O W N E R S H I P :

CURRENT

100% Upper Zone (0% Freeport)

60.4% Lower Zone(39.6% Freeport)

8

SERBIA: GREAT PLACE TO BUILD A MINESupportive government, fiscal and regulatory environment conducive of foreign investment

• Committed publicly to increase mining GDP from ~2% to 5% by 2020

• No restrictions on foreign ownership

• 5% NSR royalty with 40% going to local community

• 10-year tax holiday enshrined in law

• Dec 2015 updated mining code

• Aspiring EU member country

STRONG FEDERAL GOVERNMENT SUPPORT01

Copper mining as early as 5500 BC. The state-owned copper/gold RTB

Bor mine and smelter has been in operation since the early 1900’s. There

are currently eight other operating mines in Serbia, not including the rich

coal mining district.

EXPERIENCED MINING JURISDICTION02

Other miners operating/exploring in Serbia include Rio Tinto, Freeport-

McMoRan, Dundee Precious Metals and Mundoro.

OTHER MINERS IN SERBIA03Government system Parliamentary democracy

Population / GDP 7.1 million (est) / USD 43 billion

Capital Belgrade

Major ethnic groups 83% Serbian, 4% Hungarian, 2% Roma

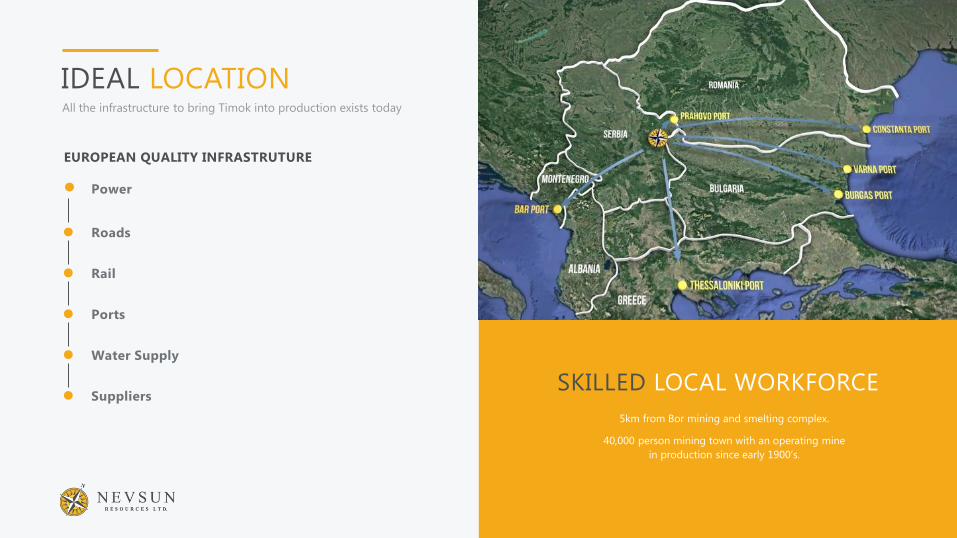

IDEAL LOCATIONAll the infrastructure to bring Timok into production exists today

SKILLED LOCAL WORKFORCE

5km from Bor mining and smelting complex.

40,000 person mining town with an operating mine

in production since early 1900’s.

Power

Roads

Ports

Water Supply

Suppliers

Rail

EUROPEAN QUALITY INFRASTRUTURE

10

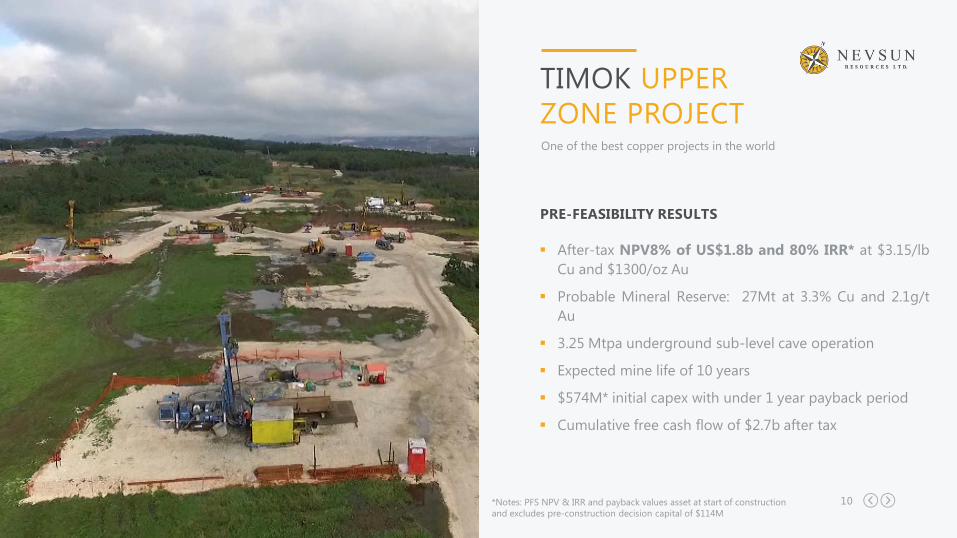

▪ After-tax NPV8% of US$1.8b and 80% IRR* at $3.15/lb

Cu and $1300/oz Au

▪ Probable Mineral Reserve: 27Mt at 3.3% Cu and 2.1g/t

Au

▪ 3.25 Mtpa underground sub-level cave operation

▪ Expected mine life of 10 years

▪ $574M* initial capex with under 1 year payback period

▪ Cumulative free cash flow of $2.7b after tax

TIMOK UPPER

ZONE PROJECTOne of the best copper projects in the world

PRE-FEASIBILITY RESULTS

*Notes: PFS NPV & IRR and payback values asset at start of construction

and excludes pre-construction decision capital of $114M

11

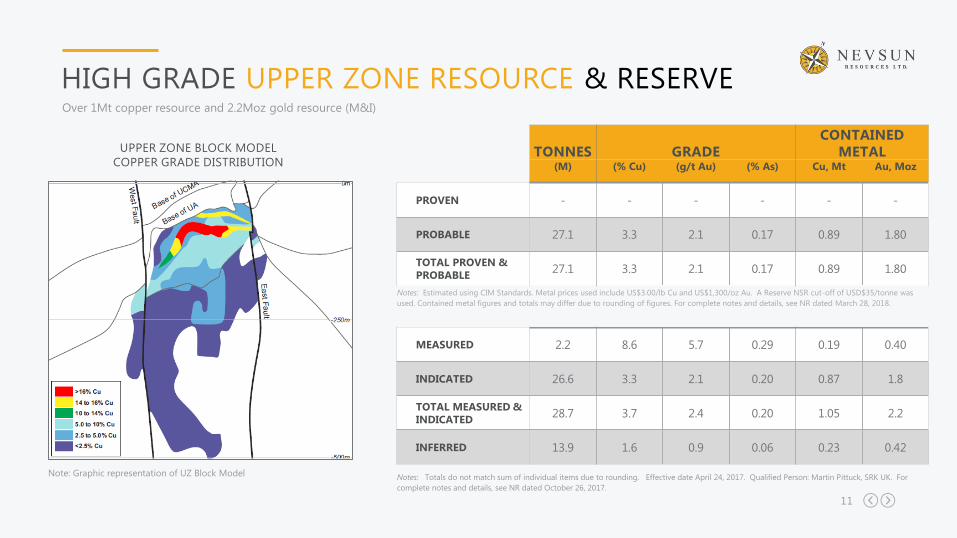

HIGH GRADE UPPER ZONE RESOURCE & RESERVEOver 1Mt copper resource and 2.2Moz gold resource (M&I)

TONNES GRADE

CONTAINED

METAL(M) (% Cu) (g/t Au) (% As) Cu, Mt Au, Moz

PROVEN - - - - - -

PROBABLE 27.1 3.3 2.1 0.17 0.89 1.80

TOTAL PROVEN &

PROBABLE27.1 3.3 2.1 0.17 0.89 1.80

Notes: Totals do not match sum of individual items due to rounding. Effective date April 24, 2017. Qualified Person: Martin Pittuck, SRK UK. For

complete notes and details, see NR dated October 26, 2017.

Note: Graphic representation of UZ Block Model

UPPER ZONE BLOCK MODEL

COPPER GRADE DISTRIBUTION

MEASURED 2.2 8.6 5.7 0.29 0.19 0.40

INDICATED 26.6 3.3 2.1 0.20 0.87 1.8

TOTAL MEASURED &

INDICATED28.7 3.7 2.4 0.20 1.05 2.2

INFERRED 13.9 1.6 0.9 0.06 0.23 0.42

Notes: Estimated using CIM Standards. Metal prices used include US$3.00/lb Cu and US$1,300/oz Au. A Reserve NSR cut-off of USD$35/tonne was

used. Contained metal figures and totals may differ due to rounding of figures. For complete notes and details, see NR dated March 28, 2018.

12

TIMOK UPPER ZONE MINE METHODPFS based on Sub-Level Caving “SLC” mining method

TYPICAL SUB-LEVEL CAVE▪ Proven low cost, bulk tonnage mining method

▪ Applicable to massive, steeply-dipping orebodies and a wide

range of geotechnical conditions

▪ Variable high grades smoothed through cave blending

▪ Mill capable of handling feed variability

<$20/t Mined

SUB LEVEL CAVE MINES

▪ Ernest Henry, Glencore, QLD, Australia

▪ Ridgeway, Newcrest Mining Ltd, NSW Australia

▪ Telfer, Newcrest Mining Ltd., WA, Australia

▪ Perseverance, WMC Resources, WA, Australia

▪ Mt Marion, Harmony Gold, WA, Australia

▪ Kiirunavaara, LKAB, Sweden

▪ Malberget, LKAB, Sweden

13

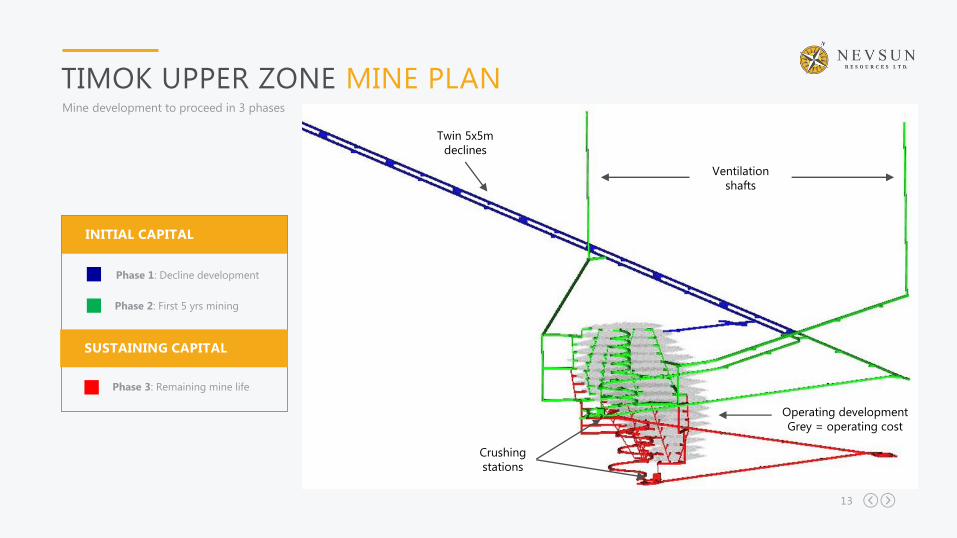

TIMOK UPPER ZONE MINE PLANMine development to proceed in 3 phases

INITIAL CAPITAL

Phase 1: Decline development

Phase 2: First 5 yrs mining

SUSTAINING CAPITAL

Phase 3: Remaining mine life

Ventilation

shafts

Twin 5x5m

declines

Operating development

Grey = operating cost

Crushing

stations

14

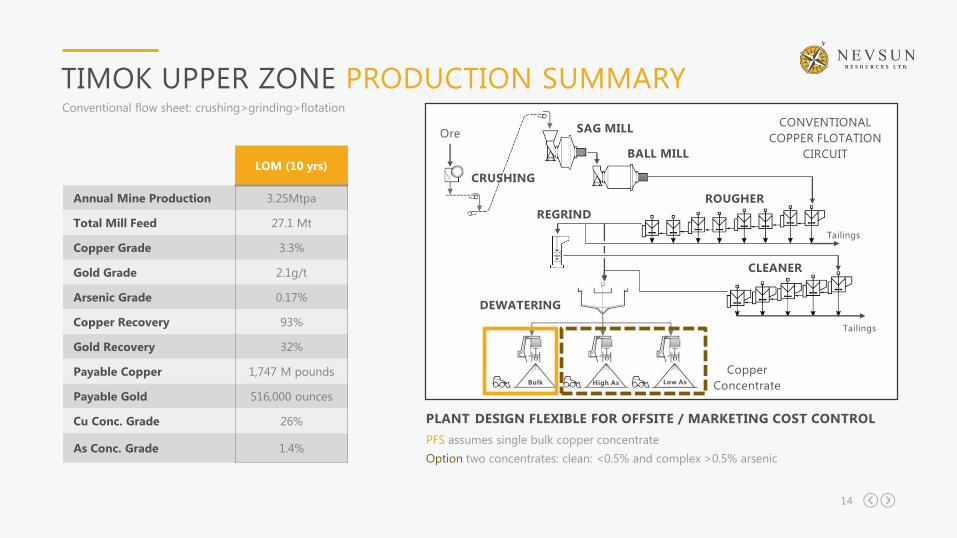

TIMOK UPPER ZONE PRODUCTION SUMMARYConventional flow sheet: crushing>grinding>flotation

PLANT DESIGN FLEXIBLE FOR OFFSITE / MARKETING COST CONTROL

PFS assumes single bulk copper concentrate

Option two concentrates: clean: <0.5% and complex >0.5% arsenic

LOM (10 yrs)

Annual Mine Production 3.25Mtpa

Total Mill Feed 27.1 Mt

Copper Grade 3.3%

Gold Grade 2.1g/t

Arsenic Grade 0.17%

Copper Recovery 93%

Gold Recovery 32%

Payable Copper 1,747 M pounds

Payable Gold 516,000 ounces

Cu Conc. Grade 26%

As Conc. Grade 1.4%

ROUGHER

CLEANER

DEWATERING

REGRIND

CRUSHING

SAG MILL

BALL MILL

CONVENTIONAL

COPPER FLOTATION

CIRCUIT

Bulk High As Low As

Copper

Concentrate

Tailings

Ore

Tailings

15

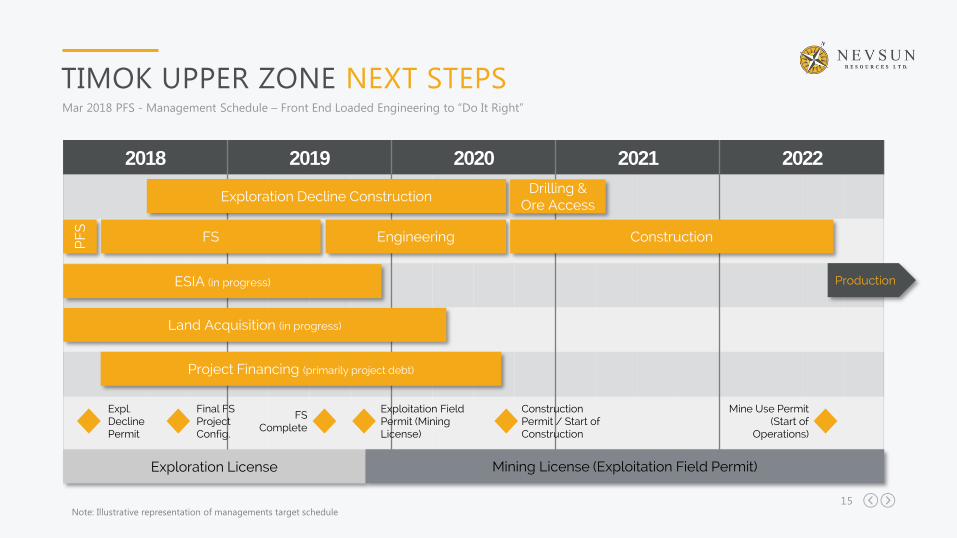

TIMOK UPPER ZONE NEXT STEPSMar 2018 PFS - Management Schedule – Front End Loaded Engineering to “Do It Right”

2018 2019 2020 2021 2022

Exploration Decline Construction

EngineeringPFS

ESIA (in progress)

FS

Production

Land Acquisition (in progress)

Expl. Decline Permit

Exploitation Field Permit (Mining License)

Construction Permit / Start of Construction

Mine Use Permit(Start of

Operations)

Exploration License Mining License (Exploitation Field Permit)

Construction

Drilling & Ore Access

Final FS Project Config.

FS Complete

Project Financing (primarily project debt)

Note: Illustrative representation of managements target schedule

16

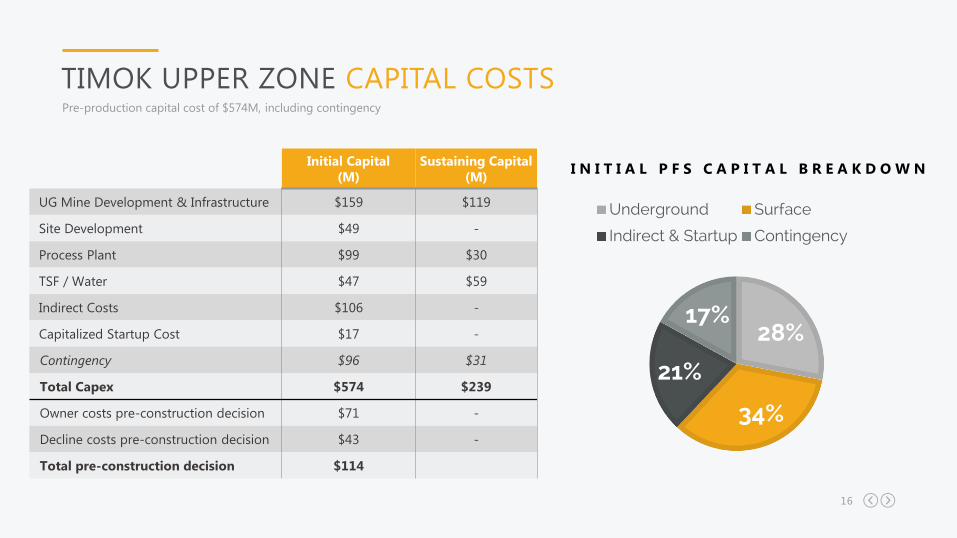

Pre-production capital cost of $574M, including contingency

28%

34%

21%

17%

Underground Surface

Indirect & Startup Contingency

I N I T I A L P F S C A P I T A L B R E A K D O W N

TIMOK UPPER ZONE CAPITAL COSTS

Initial Capital

(M)

Sustaining Capital

(M)

UG Mine Development & Infrastructure $159 $119

Site Development $49 -

Process Plant $99 $30

TSF / Water $47 $59

Indirect Costs $106 -

Capitalized Startup Cost $17 -

Contingency $96 $31

Total Capex $574 $239

Owner costs pre-construction decision $71 -

Decline costs pre-construction decision $43 -

Total pre-construction decision $114

17

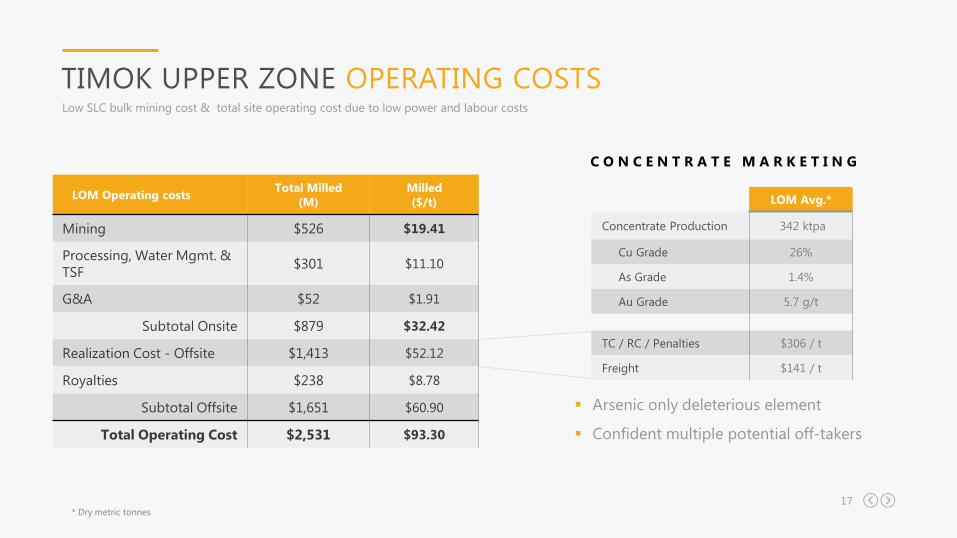

Low SLC bulk mining cost & total site operating cost due to low power and labour costs

TIMOK UPPER ZONE OPERATING COSTS

LOM Operating costsTotal Milled

(M)

Milled

($/t)

Mining $526 $19.41

Processing, Water Mgmt. &

TSF$301 $11.10

G&A $52 $1.91

Subtotal Onsite $879 $32.42

Realization Cost - Offsite $1,413 $52.12

Royalties $238 $8.78

Subtotal Offsite $1,651 $60.90

Total Operating Cost $2,531 $93.30

C O N C E N T R A T E M A R K E T I N G

▪ Arsenic only deleterious element

▪ Confident multiple potential off-takers

LOM Avg.*

Concentrate Production 342 ktpa

Cu Grade 26%

As Grade 1.4%

Au Grade 5.7 g/t

TC / RC / Penalties $306 / t

Freight $141 / t

* Dry metric tonnes

18

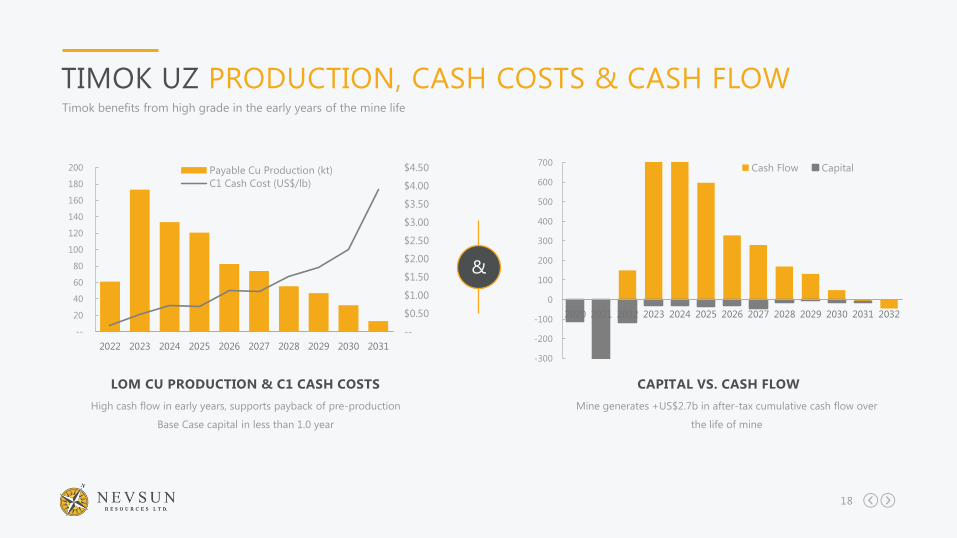

TIMOK UZ PRODUCTION, CASH COSTS & CASH FLOWTimok benefits from high grade in the early years of the mine life

--

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

--

20

40

60

80

100

120

140

160

180

200

2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

Payable Cu Production (kt)

C1 Cash Cost (US$/lb)

High cash flow in early years, supports payback of pre-production

Base Case capital in less than 1.0 year

LOM CU PRODUCTION & C1 CASH COSTS

Mine generates +US$2.7b in after-tax cumulative cash flow over

the life of mine

CAPITAL VS. CASH FLOW

-300

-200

-100

0

100

200

300

400

500

600

700

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032

Cash Flow Capital

&

19

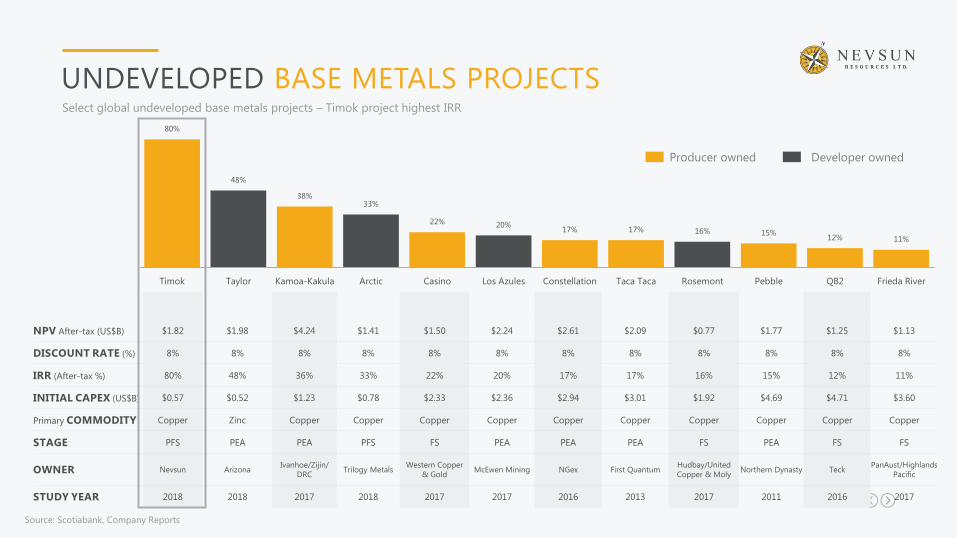

UNDEVELOPED BASE METALS PROJECTSSelect global undeveloped base metals projects – Timok project highest IRR

80%

48%

38%33%

22% 20%17% 17% 16% 15%

12% 11%

Timok Taylor Kamoa-Kakula Arctic Casino Los Azules Constellation Taca Taca Rosemont Pebble QB2 Frieda River

Producer owned Developer owned

Source: Scotiabank, Company Reports

NPV After-tax (US$B) $1.82 $1.98 $4.24 $1.41 $1.50 $2.24 $2.61 $2.09 $0.77 $1.77 $1.25 $1.13

DISCOUNT RATE (%) 8% 8% 8% 8% 8% 8% 8% 8% 8% 8% 8% 8%

IRR (After-tax %) 80% 48% 36% 33% 22% 20% 17% 17% 16% 15% 12% 11%

INITIAL CAPEX (US$B) $0.57 $0.52 $1.23 $0.78 $2.33 $2.36 $2.94 $3.01 $1.92 $4.69 $4.71 $3.60

Primary COMMODITY Copper Zinc Copper Copper Copper Copper Copper Copper Copper Copper Copper Copper

STAGE PFS PEA PEA PFS FS PEA PEA PEA FS PEA FS FS

OWNER Nevsun ArizonaIvanhoe/Zijin/

DRCTrilogy Metals

Western Copper

& GoldMcEwen Mining NGex First Quantum

Hudbay/United

Copper & MolyNorthern Dynasty Teck

PanAust/Highlands

Pacific

STUDY YEAR 2018 2018 2017 2018 2017 2017 2016 2013 2017 2011 2016 2017

20

TIMOK PROJECT NEXT STEPSFront end loading to “do it right”

UPPER ZONE NEXT STEPS

Updated PEA in October 2017

Pre-feasibility study in Q1 2018z

Lower Zone resource – mid-2018z

Feasibility study in mid-2019z

Production anticipated in 2022z

Ongoing drilling to find more Upper Zone style depositsz

Begin decline development Q2 2018z

21

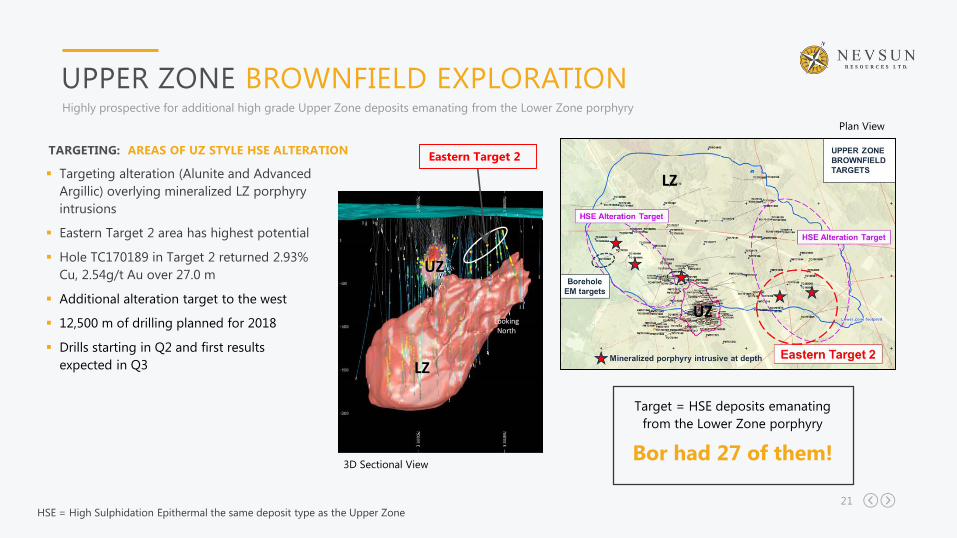

UPPER ZONE BROWNFIELD EXPLORATIONHighly prospective for additional high grade Upper Zone deposits emanating from the Lower Zone porphyry

TARGETING: AREAS OF UZ STYLE HSE ALTERATION

▪ Targeting alteration (Alunite and Advanced

Argillic) overlying mineralized LZ porphyry

intrusions

▪ Eastern Target 2 area has highest potential

▪ Hole TC170189 in Target 2 returned 2.93%

Cu, 2.54g/t Au over 27.0 m

▪ Additional alteration target to the west

▪ 12,500 m of drilling planned for 2018

▪ Drills starting in Q2 and first results

expected in Q3 LZ

UZ

Looking North

Eastern Target 2

Target = HSE deposits emanating

from the Lower Zone porphyry

Bor had 27 of them!

Plan View

3D Sectional View

HSE = High Sulphidation Epithermal the same deposit type as the Upper Zone

LZ

UZ

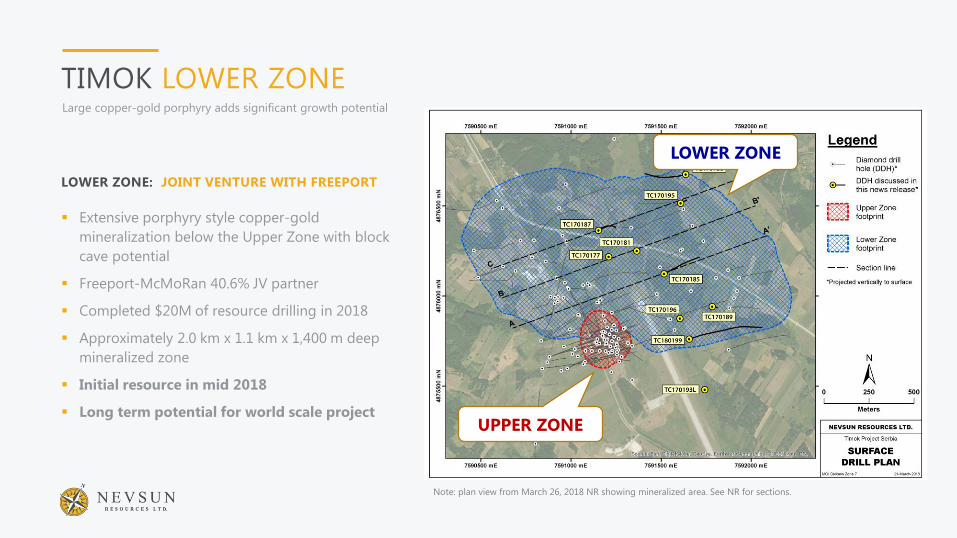

TIMOK LOWER ZONELarge copper-gold porphyry adds significant growth potential

LOWER ZONE: JOINT VENTURE WITH FREEPORT

▪ Extensive porphyry style copper-gold

mineralization below the Upper Zone with block

cave potential

▪ Freeport-McMoRan 40.6% JV partner

▪ Completed $20M of resource drilling in 2018

▪ Approximately 2.0 km x 1.1 km x 1,400 m deep

mineralized zone

▪ Initial resource in mid 2018

▪ Long term potential for world scale project

LOWER ZONE

UPPER ZONE

Note: plan view from March 26, 2018 NR showing mineralized area. See NR for sections.

23

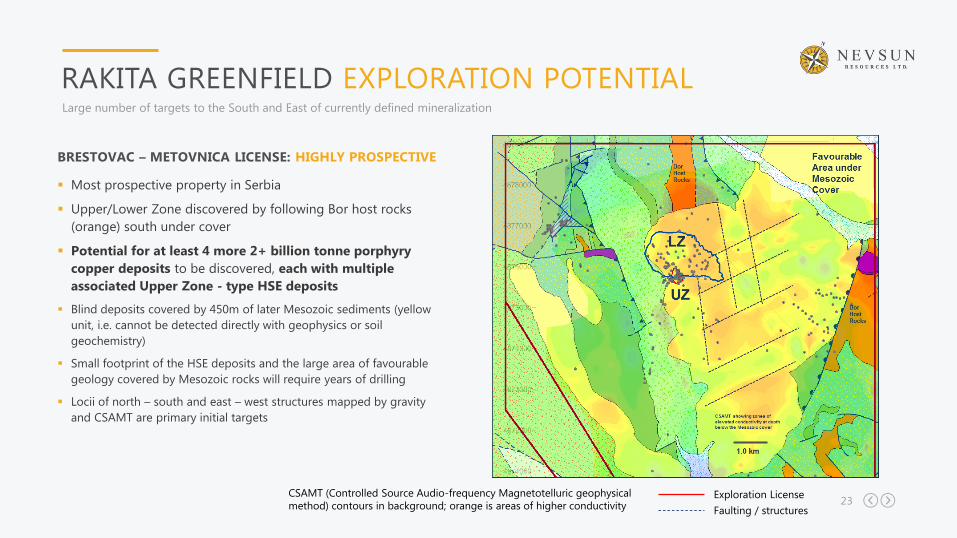

RAKITA GREENFIELD EXPLORATION POTENTIALLarge number of targets to the South and East of currently defined mineralization

BRESTOVAC – METOVNICA LICENSE: HIGHLY PROSPECTIVE

▪ Most prospective property in Serbia

▪ Upper/Lower Zone discovered by following Bor host rocks

(orange) south under cover

▪ Potential for at least 4 more 2+ billion tonne porphyry

copper deposits to be discovered, each with multiple

associated Upper Zone - type HSE deposits

▪ Blind deposits covered by 450m of later Mesozoic sediments (yellow

unit, i.e. cannot be detected directly with geophysics or soil

geochemistry)

▪ Small footprint of the HSE deposits and the large area of favourable

geology covered by Mesozoic rocks will require years of drilling

▪ Locii of north – south and east – west structures mapped by gravity

and CSAMT are primary initial targets

Exploration LicenseCSAMT (Controlled Source Audio-frequency Magnetotelluric geophysical

method) contours in background; orange is areas of higher conductivity Faulting / structures

BISHAMINEBisha is an open pit mine generating revenue from both copper and zinc

concentrates containing gold and silver by-products.

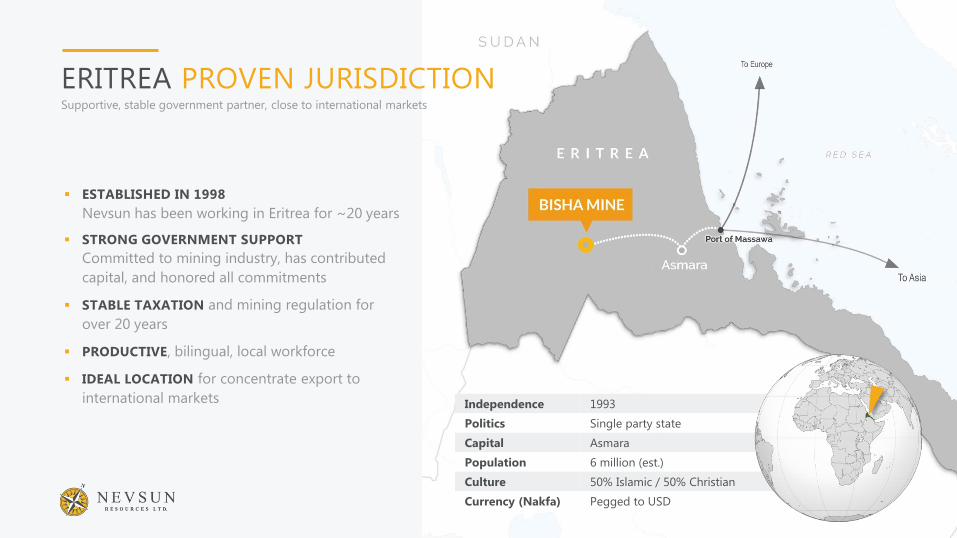

ERITREA PROVEN JURISDICTIONSupportive, stable government partner, close to international markets

Independence 1993

Politics Single party state

Capital Asmara

Population 6 million (est.)

Culture 50% Islamic / 50% Christian

Currency (Nakfa) Pegged to USD

▪ ESTABLISHED IN 1998

Nevsun has been working in Eritrea for ~20 years

▪ STRONG GOVERNMENT SUPPORT

Committed to mining industry, has contributed

capital, and honored all commitments

▪ STABLE TAXATION and mining regulation for

over 20 years

▪ PRODUCTIVE, bilingual, local workforce

▪ IDEAL LOCATION for concentrate export to

international markets

26

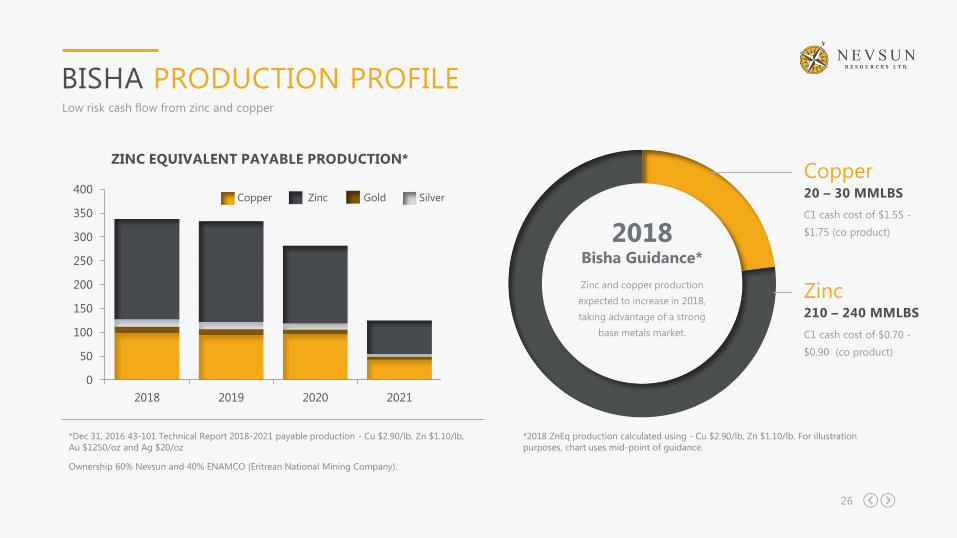

BISHA PRODUCTION PROFILELow risk cash flow from zinc and copper

0

50

100

150

200

250

300

350

400

2018 2019 2020 2021

Copper Zinc Gold Silver

ZINC EQUIVALENT PAYABLE PRODUCTION*

*Dec 31, 2016 43-101 Technical Report 2018-2021 payable production - Cu $2.90/lb, Zn $1.10/lb,

Au $1250/oz and Ag $20/oz

Ownership 60% Nevsun and 40% ENAMCO (Eritrean National Mining Company).

C1 cash cost of $1.55 -

$1.75 (co product)

20 – 30 MMLBS

Copper

C1 cash cost of $0.70 -

$0.90 (co product)

210 – 240 MMLBS

ZincZinc and copper production

expected to increase in 2018,

taking advantage of a strong

base metals market.

2018 Bisha Guidance*

*2018 ZnEq production calculated using - Cu $2.90/lb, Zn $1.10/lb. For illustration

purposes, chart uses mid-point of guidance.

27

OPPORTUNITY TO GROW RESERVESCombined Bisha, Harena, Asheli, Hambok and Northwest Resources

◼ Large resource compared to reserve (8.5Mt) and mill size (primary

mill throughput 2.4Mtpa)

◼ Ongoing study of potential open pit or underground extension of

Bisha Main mine life

◼ High grade Asheli underground potential; study ongoing in 2018

◼ Working with State of Eritrea to improve risk-adjusted economics

and add reserves

TONNAGE COPPER ZINC GOLD SILVER

TOTAL M&I 35.8 Mt 1.0% 4.3 % 0.5 g/t 32 g/t

TOTAL INFERRED 31.4 Mt 1.0% 5.2 % 0.5 g/t 26 g/t

Bisha, Harena and Asheli based on $3.30/lb Copper, $1.50/lb Zinc, $1350/oz Gold and $19.00/oz Silver and Northwest and Hambok based on $3.35/lb Copper, $1.05/lb Zinc, $1350/oz

Gold and $23.00/oz Silver

Notes

1. Effective December 31, 2017 for all deposits except Hambok and

Northwest which have effective date of December 31, 2014

2. Qualified person for mineral resource is Phil Jankowski of BMSC.

3. See 2017 AIF and the Dec 31, 2016 Technical Report for details

4. Resources inclusive of reserves

28

Gap Area

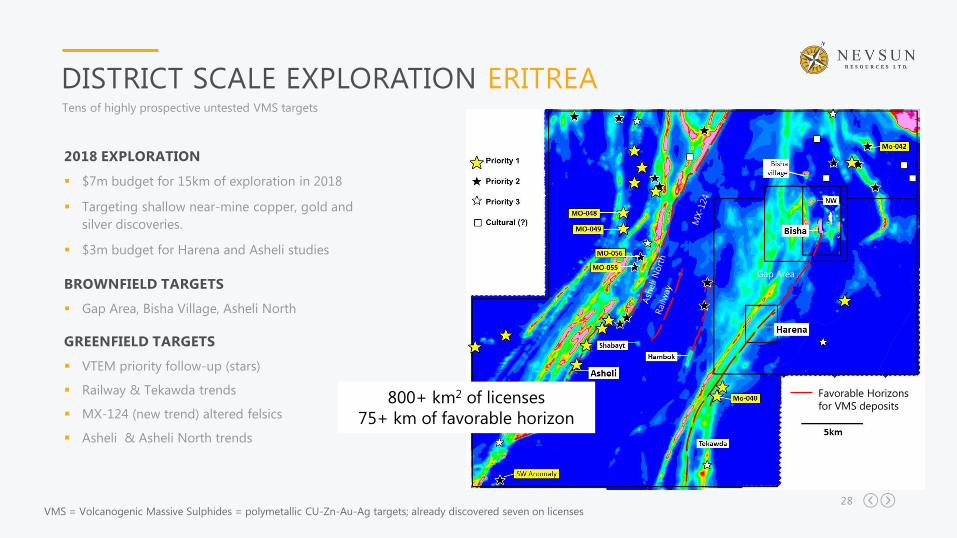

DISTRICT SCALE EXPLORATION ERITREATens of highly prospective untested VMS targets

2018 EXPLORATION

▪ $7m budget for 15km of exploration in 2018

▪ Targeting shallow near-mine copper, gold and

silver discoveries.

▪ $3m budget for Harena and Asheli studies

BROWNFIELD TARGETS

▪ Gap Area, Bisha Village, Asheli North

GREENFIELD TARGETS

▪ VTEM priority follow-up (stars)

▪ Railway & Tekawda trends

▪ MX-124 (new trend) altered felsics

▪ Asheli & Asheli North trends

VMS = Volcanogenic Massive Sulphides = polymetallic CU-Zn-Au-Ag targets; already discovered seven on licenses

Favorable Horizons

for VMS deposits800+ km2 of licenses

75+ km of favorable horizon

29

DISTRICT EXPLORATION SERBIAHighly prospective land packages throughout Serbia along the Timok Magmatic

Complex

RAKITA JV WITH FREEPORT-MCMORAN

4 exploration permits in the Bor region, including the Timok project

TILVA JV WITH RIO TINTO

4 exploration permits in close proximity to the Timok project

(100% funded by Rio Tinto)

100% OWNED PROJECTS (7 exploration permits)

4 permits: copper targets

3 permits: zinc, lead, gold, silver sulphide targets Timok

Project

Bor Mine

Bor Region

12.5KM OF FOLLOW UP

DRILLING ON HIGHLY

PROSPECTIVE UPPER

ZONE TARGETS

30

These risks, uncertainties and factors include general business, economic, competitive, political,

regulatory and social uncertainties; actual results of exploration activities and economic

evaluations; fluctuations in currency exchange rates; changes in project parameters; changes in

costs, including labour, infrastructure, operating and production costs; future prices of copper,

gold, zinc, silver and other minerals; resource estimates and variations of mineral grade or

recovery rates; metallurgical challenges; operating or technical difficulties in connection with

exploration; land acquisition; mining method, production profile and mine plan; other

development or mining activities, including the failure of plant, equipment or processes to

operate as anticipated; delays in exploration, development and construction activities; changes

in government legislation and regulation; the ability to maintain and renew existing licenses

and permits and the ability to obtain other required licences and permits in a timely manner or

at all; the ability to obtain financing on acceptable terms and in a timely manner or at all;

contests over title to properties; employee relations and shortages of skilled personnel and

contractors; the speculative nature of, and the risks involved in, the exploration, development

and mining business; and other factors and risks discussed in the Company’s AIF and MD&A.

The Company’s forward-looking statements are based on the beliefs, expectations and

opinions of management on the date the statements are made and the Company assumes no

obligation to update such forward-looking statements in the future, except as required by law.

For the reasons set forth above, investors should not place undue reliance on the Company’s

forward-looking statements.

Further information concerning risks and uncertainties associated with these forward-looking

statements and our business can be found in our AIF for the year ended December 31, 2016,

which is available on the Company’s website (www.nevsun.com), filed under our profile on

SEDAR (www.sedar.com) and on EDGAR (www.sec.gov) under cover of Form 40-F.

FORWARD LOOKING STATEMENT

This Presentation contains forward-looking statements or forward-looking information within

the meaning of the United States Private Securities Litigation Reform Act of 1995, and

applicable Canadian securities laws. All statements, other than statements of historical facts, are

forward looking statements including statements with respect to the Company’s continuing

and future operations in Eritrea, Serbia and elsewhere that the Company has operations or

business interests.

Forward-looking statements are frequently, but not always, identified by words such as

“expects”, “anticipates”, “believes”, “hopes”, “intends”, “estimated”, “potential”, “possible” and

similar expressions, or statements that events, conditions or results “will”, “may”, “could” or

“should” occur or be achieved. Forward-looking statements are statements concerning the

Company’s current beliefs, plans and expectations about the future, including but not limited

to statements and information made concerning: statements relating to the business, prospects

and future activities of, and development plans related to the Company, anticipated dividends,

goals, strategies, future growth, exploration activities, the adequacy of financial resources and

other events or conditions that may occur in the future.

These forward-looking statements are based on a number of assumptions which, while

considered reasonable by the Company, are subject to risks and uncertainties. In addition to

the assumptions contained herein, these assumptions include the assumptions described in the

Company’s Annual Information Form (“AIF”) and the Company’s management's discussion and

analysis for the year ended December 31, 2017 ("MD&A"). The Company cautions readers that

forward-looking statements involve and are subject to known and unknown risks, uncertainties

and other factors which may cause actual results, performance or achievements to differ

materially from those expressed in or implied by such forward-looking statements and forward-

looking statements are not guarantees of future results, performance or achievement.

THANK YOU

Please feel free to contact us! We’d love to hear from you.

Heather Taylor

604-623-4712 / [email protected]

Investor Relations

www.nevsun.com

@NevsunNSU

nevsun-resources

Follow us on: