Embed Size (px)

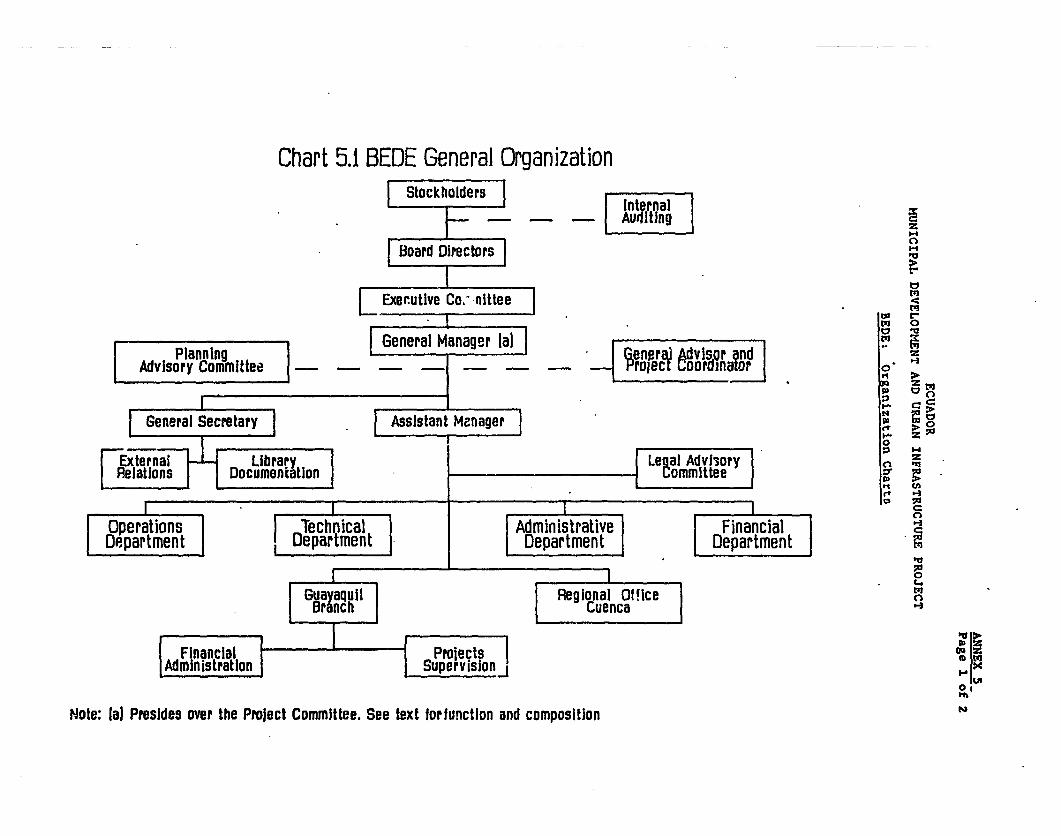

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

A-A/ 3 Z2gS- EcReport No. 9082-EC

STAFF APPRAISAL REPORT

ECUADOR

MUNICIPAL DEVELOPMENT AND URBAN INFRASTRUCTURE PROJECT

NOVEMBER 29, 1990

Infrastructure and Energy DivisionCountry Department IVLatin America and the Cai.$bbean Regional Office

This document has a resticted distribution and may be used by recipienis only In the performance oftheir official dutfes. Its contents may not otherwise be disclosed without World Bank athorization

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY AND EQUrVALENT UNITS

Currency Units Sucre (8/.)

U8$l - 8/* 655.19 (December 1989)

WEIGHTS AND MEASURES

Metric Syste

FISCAL YEAR

January 1 to December 31

ABBREVIATIONS AND ACRONYMS

AME - Asociacion de Municipalidades Ecuatorianas (Association ofEcuadoran municipalities)

BEDE - Banco de Desarrollo del Fcuador S.A. (Development Bankof Ecuador)

CONADZ - Consejo Nacional de Desarrollo (National DevelopmentCouncil)

FODESEC - Fondo de nesarrollo Seccional (Local GovernmentDevelopment Fund)

FONAPAR - Fondo Nacional de Participacion (National RevenueSharing Fund)

FONAPRE - Fondo Nacional de Pre-inversion (National Pre-Lnvestment Fund)

FONEN - Fondo de Emergencia Nacional (National Emergency Fund)GTZ - Gesellschaft fur Technische Zusammenarbeit (German Technical

Assistance Organization)IDB - Inter-American Development BankINEC - Instituto Nacional de Estadistica y Censos (National

Institute of Statistics and Censuses)IEOe - Instituto Bcuatoriano de Obras Sanitarias (Institute of

Sanitary Works of Ecuador)INBCBL - Instituto Nacional de Electrificacion del Ecuador (National

Institute of Electrification)LGDL Local Government Development LawMIF - Municipal Investment FundMDUI - Municipal Development and Urban Infrastructure [program

or project)BENDA Secretaria Nacional de Desarrollo Administrativo (National

Secretariat of Administrative Development)

FOR OFFICIAL USE ONLYECUADOR

MUNICIPAL DEVELOPMENT AND URBAN INFRASTRUCTURE PROJECT

STAFF APPRAISAL REPORT

TABLB OF CONTENTS

Page No.

LOAN AND PROECT SUMMARY ... . . . . . . . . . . . . . . . . . . . . iii

I. THE SECTOR...1A. Background: Rapidly Rising Demands; and Declining Capacity . 1B. Government Structure and the Provision of Public Services . . . 2C. Government's Request for Assistance and the Sector Policy

Letter . .. .. .. ..... .......... 2D. Institutional and Legal Constraints for Provision of Pi'b3ic

Services .*. . . . . . . . .* 3E. Reform of Intergovernmental Fiscal Relations . . 6F. Strengthening BEDE as a Lender and Provider of Technical

Assistance . . . . . . . . . . . . . . . . . . . . . . . . . 8G. Sector Development Issues, Objectives, and Bank Lending

Strategy .... . . . . . . . . . . ... 10H. Prior Bank Experience ............... .... 11I. Rationale for Bank Involvement ......... ...... 11

II. TIE PROJECT.. .. .12A. Project Origin . . . . . . . . . . . . . . . . . . . . . .. . 12B. Project Objectives ... . . . . . . ..... . . . . . . . . . 12C. Project Description ... . .13D. Project Costs and Financing Plan .. .14E. Eligibility Criteria . . . . . . . . . . . . . . . . . . . . . . 16F. Borrower and Executing Agency ... . . . . . .. . . . . . . . 19G. Cost Recovery Policy and Grants to Compensate Lifeline Rates . . 19

II. PROJECT IMPLEMENTATION . .. . . . .. ... ...... . . . 20A. Implementation Arrangements ........ ....... . . 20B. Strengthening Implementing Institutions ... ..... . . . . 21C. Procurement ... . .22D. Disbursement.. . . . .... ......... 24E. Accounts and Audits .... ... 26F. Project Reporting and Monitoring . .. .26

This report was prepared by D. Vetter (LA4IE) based on the findings of amission which visited Ecuador during April/May 1990. The mission comprisedMessrs/Mmes M. Art&za-Rouxel (Mission Leader, LA4IE), J. Carvalho (LEGLA), M.Linder (LACVP), L. Pisani (LATHR), D. Vetter (LA4IE), E. Wessels (LATDR), L.Ficinski, H. Garzon and S. Miquel (Consultants). A. Aza, A. Ezcurra, and W.Malik (Consultants) assisted in the production of this report. The financialprojections were done by B. Von Rabenau (Consultant).

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

IV. PROJUCT JUSTI1MICATION AND RISKS . ...... . . . . . . . . .. . 27

A. Financial Benefit . . . . . . . . . . . . . . .. . . . . .. 27

B. Economic Benefits . . . . . . . . . . . . . . . . . . . . . . 27C. Poverty Impact . . . . . . . . ...... . . . 28D. Environmental Impact . . . . . . . . . . . . . . 28

E. Risks and Safeguards... .. . . . . . . . . 29

V. AGRMANTS REACHED AND RBCOIMNDATIONS . . . . . . . . . . . . . . . 29

ANNBXES

ANNEX 1: Population Trends and Access to Urban Infrastructure

ANNEX 2: Policy Letter and MatrixANNEX 3: Reform of the Transfer SystemANNEX 4s BEDE: Financial Statements and Projections

ANNEX 5: BEDE: Organization ChartsANNEX 6: Institutional Development and Training Component

ANNEX 7: Infrastructure Component

ANNEX 8: Methodology for Economic and Financial Evaluation of Projects

ANNEX 9: Cost Recovery PolicyANNEX 10: Estimated Schedule of Bank Disbursements

ANNEX 11: Monitoring IndicatorsANNEX 12: Selected Documents in the Project File

MAP

IBRD 18179 ECUADOR

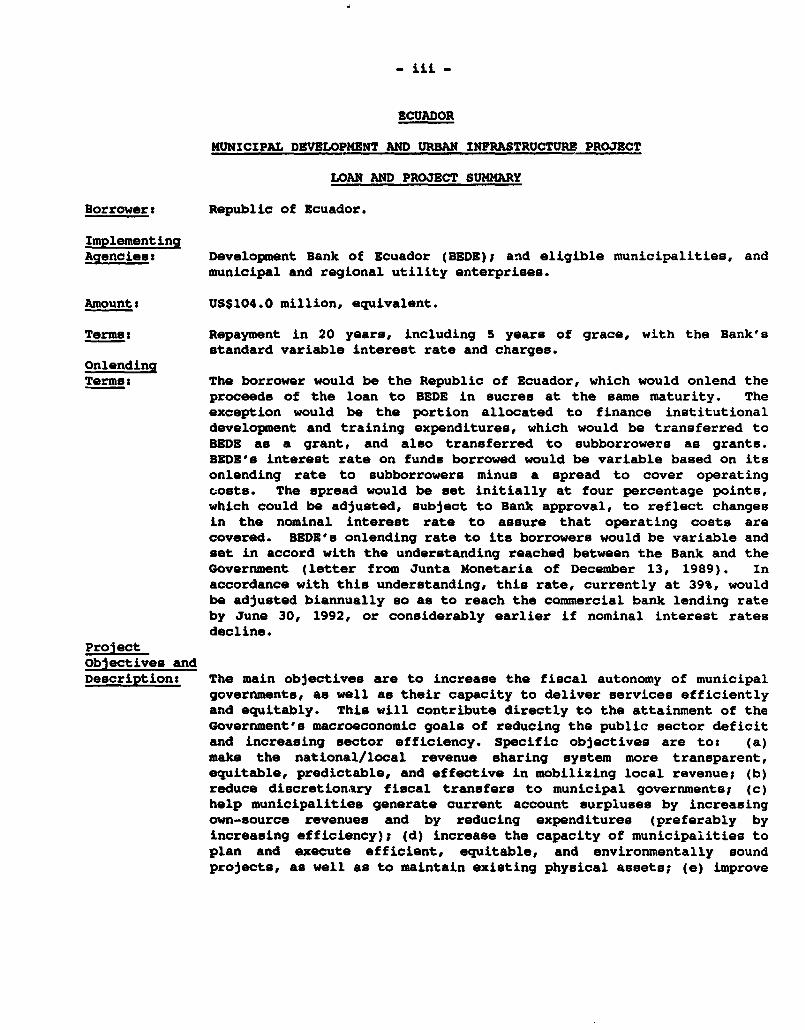

-iii -

ECUADOR

MUNICIPAL DEVELOPMENT AND URBAN INFRASTRUCTURE PROJECT

LOAN AND PROJECT SUMMARY

Borrower: Republic of Ecuador.

ImplementingAgencies: Development Bank of Ecuador (BEDE)I and eligible municipalities, and

municipal and regional utility enterprises.

Amount: US$104.0 million, equivalent.

Terms: Repayment in 20 years, including 5 years of grace, with the Bank'sstandard variable interest rate and charges.

OnlendingTerms: The borrower would be the Republic of Ecuador, which would onlend the

proceeds of the loan to BEDE in sucres at the same maturity. Theexception would be the portion allocated to finance institutionaldevelopment and training expenditures, which would be transferred toBEDE as a grant, and also transferred to subborrowers as grants.BEDE's interest rate on funds borrowed would be variable based on itsonlending rate to subborrowers minus a spread to cover operatingCosts. The spread would be set initially at four percentage points,which could be adjusted, subject to Bank approval, to reflect changesin the nominal interest rate to assure that operating costs arecovered. BEDE's onlending rate to its borrowers would be variable andset in accord with the understanding reached between the Bank and theGovernment (letter from Junta Monetaria of December 13, 1989). Inaccordance with this understanding, this rate, currently at 39%, wouldbe adjusted biannually so as to reach the commercial bank lending rateby June 30, 1992, or considerably earlier if nominal interest ratesdecline.

Projectobjectives andDescription: The main objectives are to increase the fiscal autonomy of municipal

governments, as well as their capacity to deliver services efficientlyand equitably. This will contribute directly to the attainment of theGovernment's macroeconomic goals of reducing the public sector deficitand increasing sector efficiency. Specific objectives are to: (a)make the national/local revenue sharing system more transparent,equitable, predictable, and effective in mobilizing local revenue; (b)reduce discretionary fiscal transfers to municipal governments; (c)help municipalities generate current account surpluses by increasingown-source revenues and by reducing expenditures (preferably byincreasing efficiency); (d) increase the capacity of municipalities toplan and execute efficient, equitable, and environmentally soundprojects, as well as to maintain existing physical assets; (e) improve

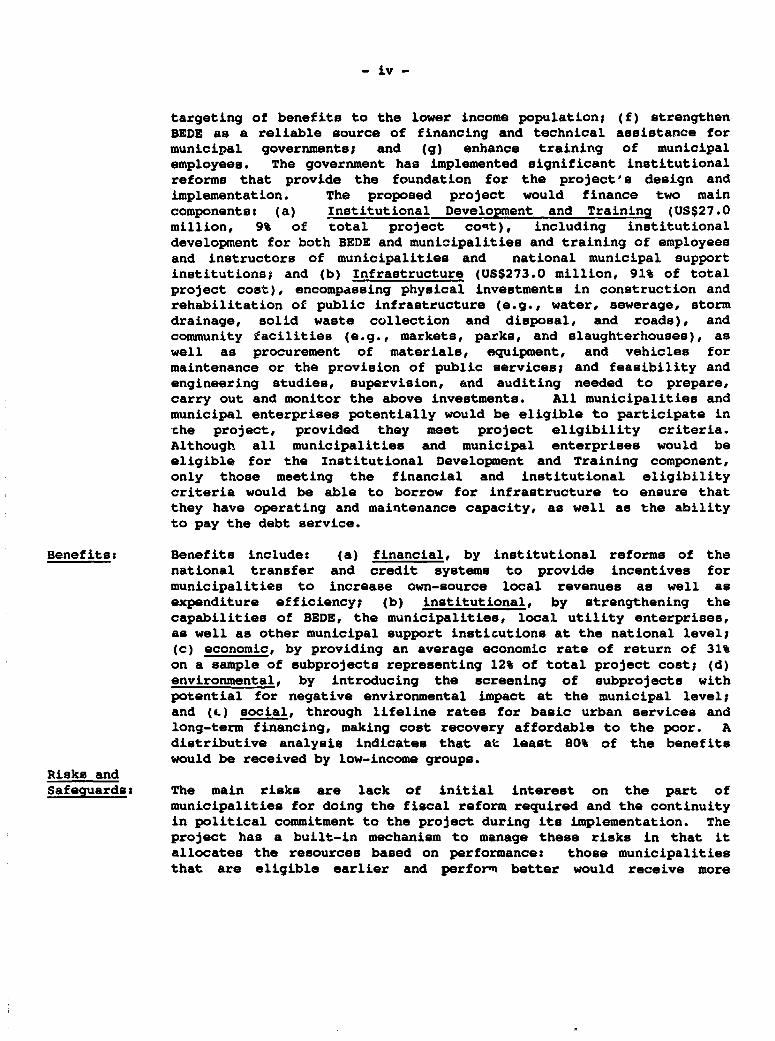

- iv -

targeting of benefits to the lower income population; (f) strengthenBEDE as a reliable source of financing and technical assistance formunicipal governments; and (g) enhance training of municipalemployees. The government has implemented significant institutionalreforms that provide the foundation for the project's design andimplementation. The proposed project would finance two maincomponentes (a) Institutional Development and Traininq (US$27.0million, 9% of total project covt), including institutionaldevelopment for both BEDE and municipalities and training of employeesand instructors of municipalities and national municipal supportinstitutions; and (b) Infrastructure (US$273.0 million, 91% of totalproject cost), encompassing physical investments in construction andrehabilitation of public infrastructure (e.g., water, sewerage, stormdrainage, solid waste collection and disposal, and roads), andcommunity facilities (e.g., markets, parks, and slaughterhouses), aswell as procurement of materials, equipment, and vehicles formaintenance or the provision of public services; and feasibility andengineering studies, supervision, and auditing needed to prepare,carry out and monitor the above investments. All municipalities andmunicipal enterprises potentially would be eligible to participate inche project, provided they meet project eligibility criteria.Although all municipalities and municipal enterprises would beeligible for the Institutional Development and Training component,only those meeting the financial and institutional eligibilitycriteria would be able to borrow for infrastructure to ensure thatthey have operating and maintenance capacity, as well as the abilityto pay the debt service.

Benefits: Benefits include: (a) financial, by institutional reforms of thenational transfer and credit systems to provide incentives formunicipalities to increase own-source local revenues as well asexpenditure efficiency; (b) institutional, by strengthening thecapabilities of BEDE, the municipalities, local utility enterprises,as well as other municipal support insticutions at the national level;(c) economic, by providing an average economic rate of return of 31%on a sample of subprojects representing 12% of total project cost; (d)environmental, by introducing the screening of subprojects withpotential for negative environmental impact at the municipal level;and (e.) social, through lifeline rates for basic urban services andlong-term financing, making cost recovery affordable to the poor. Adistributive analysis indicates that at least 80% of the benefitswould be received by low-income groups.

Risks andSafeguards: The main risks are lack of initial interest on the part of

municipalities for doing the fiscal reform required and the continuityin political commitment to the project during its implementation. Theproject has a built-in mechanism to manage these risks in that itallocates the resources based on performance: those municipalitiesthat are eligible earlier and perform better would receive more

resources. The incentives built into the reformed transfer systemshould also stimulate the transfer of innovations from the lesssuccessful municipalities to the more succeseful ones. In addition tothese general risks, there is the possibility of inefficient projectmanagement by BEDS and the municipalities. This risk has beendiminished through technical assistance and training during projectpreparation, as well as the institutional development requirements inthe eligibility criteria. There ia also the risk of lack ofcontinuity in project management by municipallties due to staffturnover. This would be reduced by technical assistance in thepreparation of legielation to grant civil service status to municipalemployees. Finally, reforms already implemented might be abandoned.While real, this risk has been reduced through the embodiment nf thereforms in legislation as well as by specific related loan conditlons.

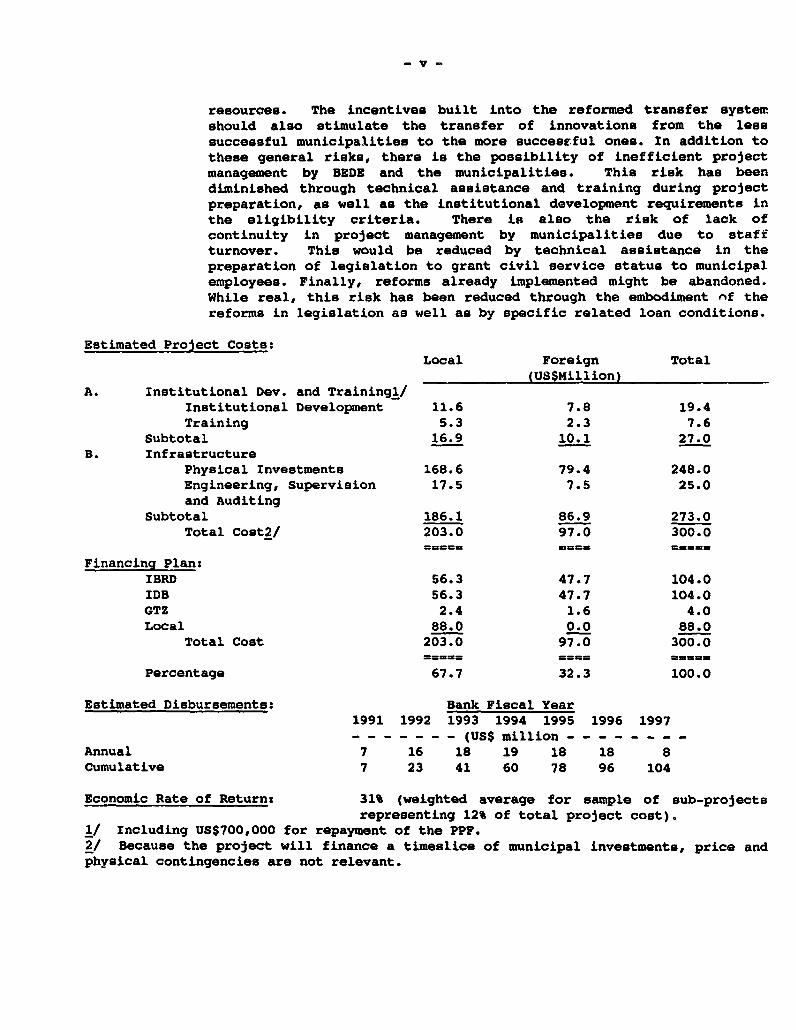

Estimated Project Costs:Local Foreign Total

(US$Million)A. Institutional Dev. and Trainingl/

Institutional Development 11.6 7.8 19.4Training 5.3 2.3 7.6

Subtotal 16.9 10.1 27.0B. Infrastructure

Physical Investments 168.6 79.4 248.0Engineering, Supervlsion 17.5 7.5 25.0and Auditing

Subtotal 186.1 86.9 273.0Total Cost2/ 203.0 97.0 300.0

Financing Plan:IBRD 56.3 47.7 104.0IDB 56.3 47.7 104.0GTZ 2.4 1.6 4.0Local 88.0 0.0 88.0

Total Cost 203.0 97.0 300.0

Percentage 67.7 32.3 100.0

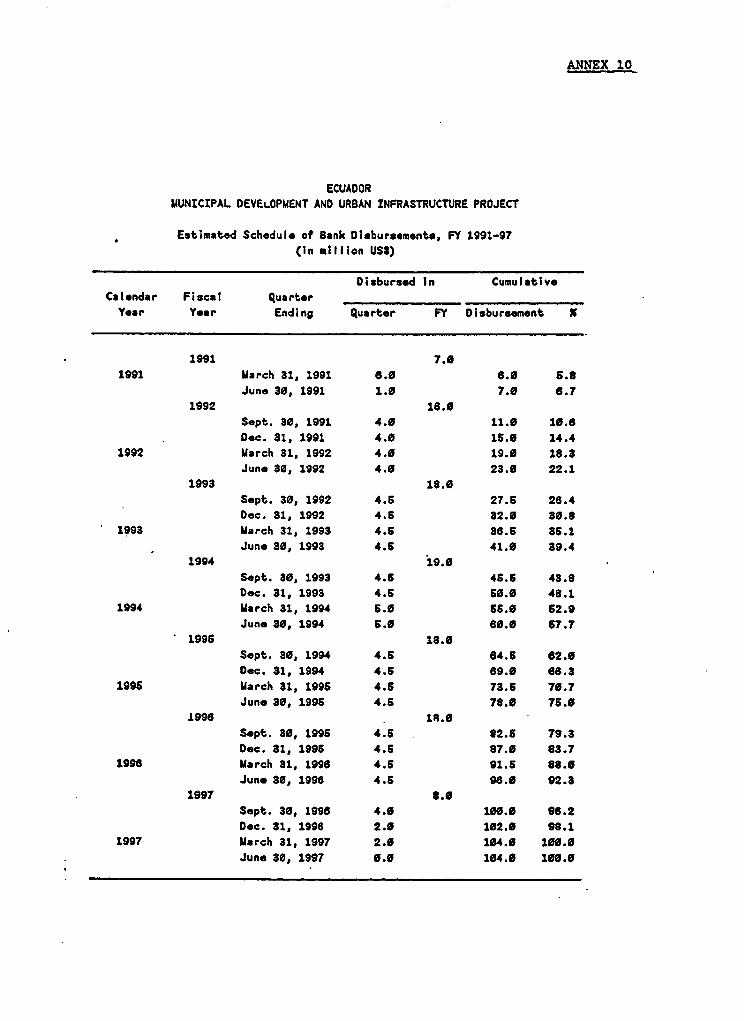

Estimated Disbursements: Bank Fiscal Year1991 1992 1993 1994 1995 1996 1997- - … - - - - (US$ million

Annual 7 16 18 19 18 18 8Cumulative 7 23 41 60 78 96 104

Economic Rate of Return: 31% (weighted average for sample of sub-projectsrepresenting 12% of total project cost).

1/ Including US$700,000 for repayment of the PPF.2/ Because the project will finance a timeslice of municipal investments, price andphysical contingencies are not relevant.

ECUADOR

MUNICIPAL DEVELOPMENT AND URBAN INFRASTRUCTURE PROJECT

I. THE SECTOR

A. Backgrounds Rapidly Rising Demands and Declining Capacitv

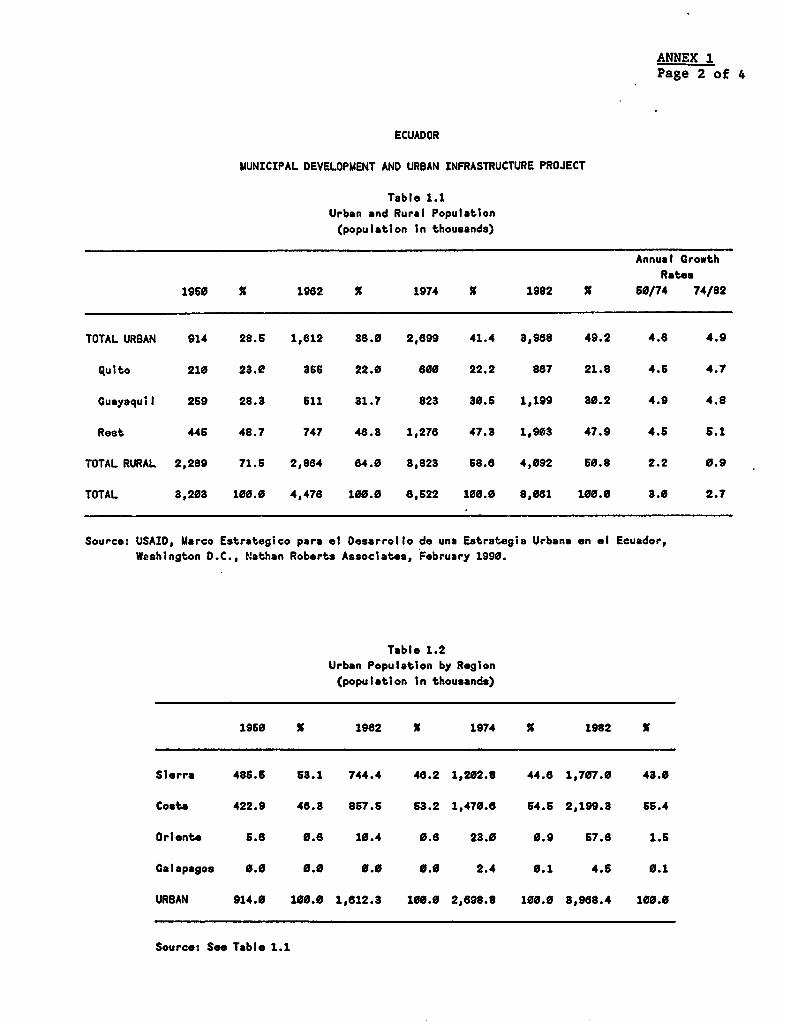

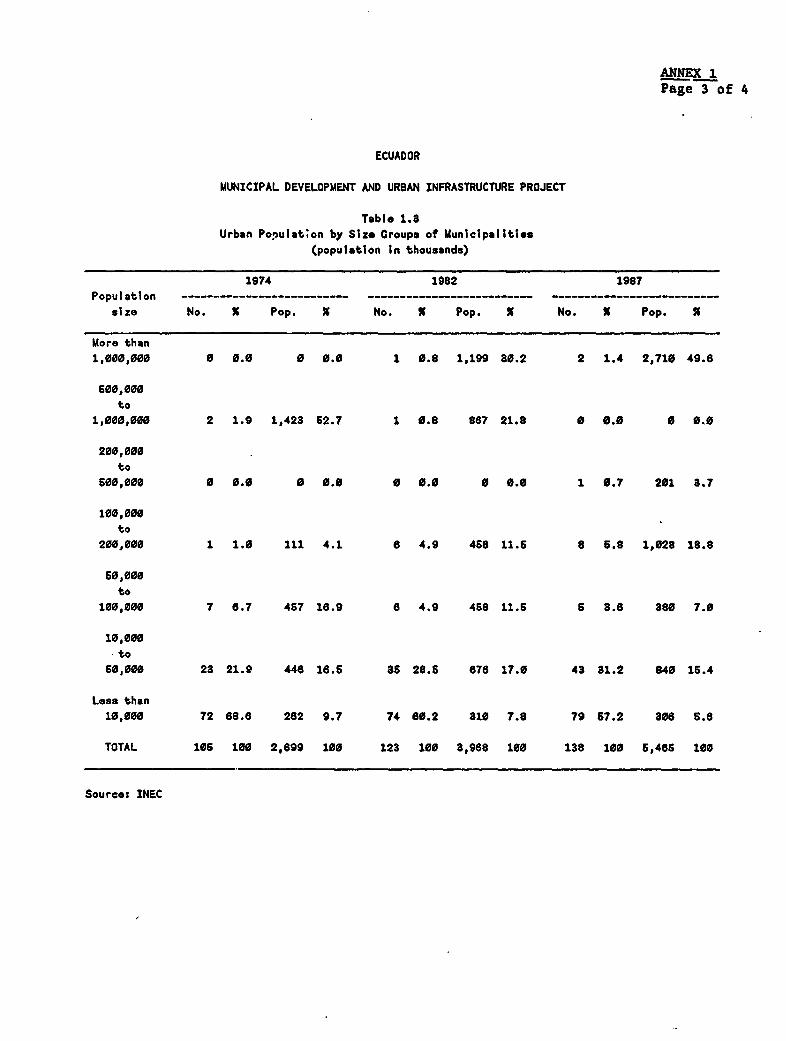

1.01 In Ecuador, deficient infrastructure, weak municipal. institutions,and inadequate regulation constrain the productivity of the urban economy and itsability to generate income, employment, and services for its rapidly growingpopulation, especially the urban poor. Ecuador's urban population more thandoubled between 1962 and 1982 to 4 million. In 1987, 55% of Ecuador's 9.9million inhabitants lived in urban areas. The country's urban economy accountsfor 70% of GDP. Urban agglomerations in the 100,000 to 200,000 range grew mostrapidly, with their participation in the total urban population rising from 4% in1974 to 19% in 1987. The population of the two largest cities, Quito andGuayaquil, is estimated to have more than doubled between 1974 and 1989 to 1.2million and 1.7 million inhabitants, respectively. However, the percentage oftotal urban population living in these two centers declined slightly from 53% in1974 to 50% in 1987, partly due to the faster growth of the medium-size cities.

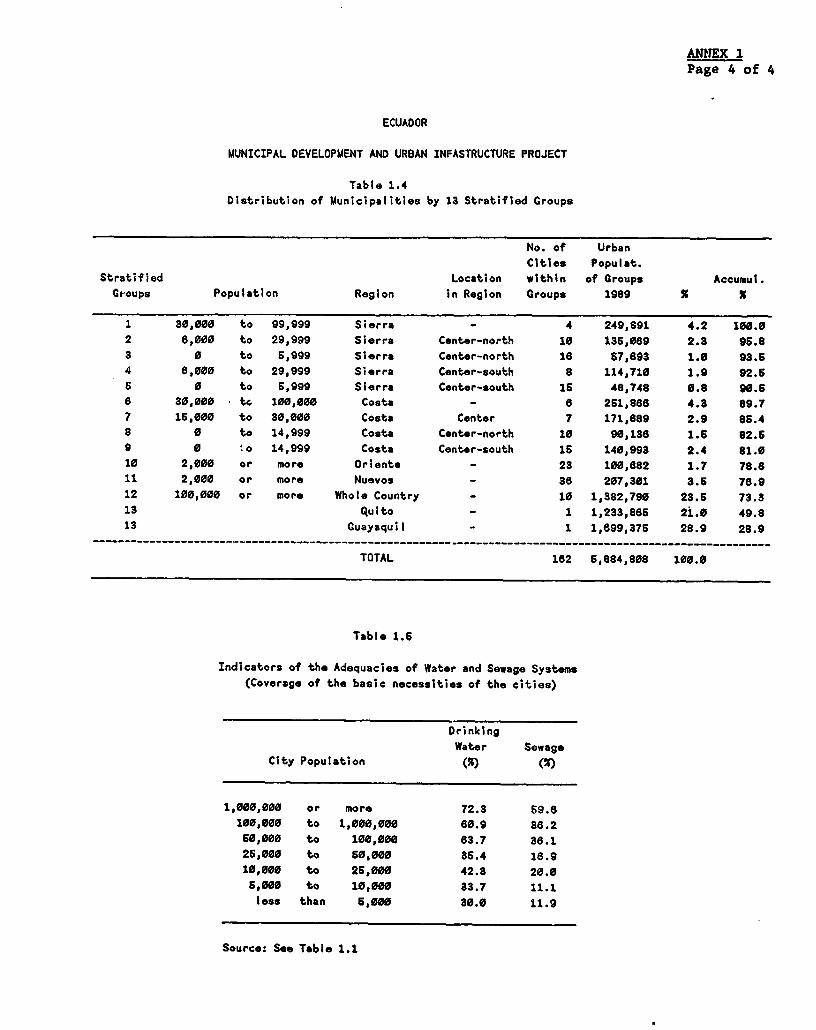

1.02 Urban growth has outstripped the ability of municipalities to keeppace with the overwhelming increase in demand for services and infrastructure.For example, 69% of the total urban population had access to drinking water intheir houses in 1987, down from 75% in 1982; and only 53% had access to adequatesewage facilities in 1987, down from 62% in 1982. These unmet infrastructureneeds tend to be significantly higher outside of Quito and Guayaquil. Forexample, the percentage of families without potable drinking water was over twiceas high in municipalities with 25,000 to 50,000 inhabitants than in Quito andGuayaquil. A study done as part of project preparation (see Annex 7) estimated atotal cost of US$600 million to eliminate urmet urban infrastructure needs(including water, sanitary and storm sewers, streetlighting, and solid wastecollection and disposal) for all municipalities, not including Quito andGuayaquil.

1.03 The following sections will discuss the constraints that haveinhibited municipalities from providing these services and infrastructure forwhich they are legally responsible (paras. 1.08-1.35). The inability ofmunicipalities to meet their critical infrastructure needs is serious, becausethe resulting shortages represent:

(a) an important constraint on the productivity of the urban economyl andtherefore on its ability to increase the incomes of urban workers;

(b) an additional burden on the poor who are most likely to lack accessto these services; and

1 The World Bank, Structural Adjustment and Sustainable Growth: The UrbanAgenda for the 1990., Urban Development Division, Infrastructure and UrbanDevelopment Department, Washington, D.C., August 15, 1990.

2-

(c) environmental degradation, because sewage and solid waste are notbaing disposed of properly due to lack of the necessaryinfrastructure or failure to design and operate the systems properly.

B. Government Structure and the Provision of Public Services

1.04 Local governments in Ecuador include: 20 provinces, 162 cantones %ithconstituted municipalities, and about 1,000 other cantones withoutmunicipalities, mostly in rural areas. Municipalities are the primary politicaland administrative units of government and are headed by mayors (Alcaldes) whogovern together with a Municipal Councils both are elected for four years and areineligible for reelection. The number of municipalities increased from 105 in1974 to 162 today, an increase of 56% in 16 years. Unfortunately, the greatmajority of these are very small (many with less than 2,000 inhabitants),sometimes not large enough to provide efficiently even basic services.

1.05 Under the current Municipal Law, municipalities are responsible forplanning and delivery of various urban services including water supply andsewerage, drainage, solid waste, construction and maintenance of streets, parksand other green spaces, streetlighting, and construction and operation ofslaughterhouses and markets. Provincial Councils provide most of the services inrural areas, especially construction of rural roads. Article III of theMunicipal Law grants full autonomy to municipal governments to: (a) set andcollect property taxes, as well as user fees and tariffs for basic urbanservices; (b) plan, finance and implement investments; and (c) operate andmaintain basic services.

C. Government's Request for Assistance and the Sector Policy Letter

1.06 In December 1988, the Government of Ecuador, through a letter fromthe Minister of Finance, requested assistance from the Bank and IDB for a project"to change the concept of financing works and expenditures, to modify therelationship of dependence on Central Government funds, and to increase thegeneration of local resources, thus providing greater autonomy to localgovernments." Early in project identification, IDB and the Bank agreed tocooperate in the development of a Municipal Development and Urban InfrastructureProject that could be cofinanced by both banks. The GTZ (German TechninalAssistance Organization) soon joined this cooperative effort to provide technicalassistance in the preparation of this Project. The extraordinarily high level ofcooperation and integration of the Bank, IDB, and GTZ teams in projectpreparation made it possible to attain full agreement on project objectives,procedures, evaluation criteria, and on procurement guidelines for local bidding.These agreements are precedents that should greatly facilitate cofinancing withIDB and GTZ in future operations.

1.07 The ensuing dialogue of the Government with IDB, GTZ, and the Bankresulted in an agreement with the Government for a two-stage strategy, involving:(a) a program of significant institutional reforms; and (b) a project that wouldbuild on these reforms to increase further the autonomy of municipal governments.

-3-

Through this dialogue and the reports done to develop an overall sector

strategy, a far-reaching program of rfforms was developed and included in a

policy letter of the Government to the Bank (see Annex 2). This letter addressedthree main problem areas: (a) general institutional and legal constraints to

municipal development; (b) the system of intergovernmental national/local

transfers; and (c) lending to local governments. As will be discussed in the

following sections, the most important of these reforms were embodied in the

Local Goverr4,ient Development Law (LGDL) of May 1990.3

D. Institutional and Legal Co:sstraints for Provii.on of Public Services

1.08 There are numerous institutional and legal constraints that make it

difficult for municipalities to exercise their legal responsibilities for

providing urban services. The following sections will review these constrairnts

and the program of institutional reforms adopted to resolve them.

The Constraints

1.09 Legal Constraint for Full Cost Recovery. Municipalities were allowed

under the previous Municipal Law to recover only operation and maintenance costs

of water and sewer systems through user charges, but not the cost of investment.

Existing water tariffs are exceedingly low in most municipalities. Average

tariffs are well below the marginal cost of new suppliea. For one large new

project in Quito, the average tariff was less than a tenth of the marginal cost.

On average, municipalities currently recover only about 30% of operating and

maintenance costs for sewer and water; and many municipalities recover far less.

Recent studies show willingness to pay more for water to avoid the high costs of

purchasing it from tank cars.

1.10 Lack of Coordination of Central Government Entities Working in Urban

Areas. Several agencies of the Central Government oversee or are responsible for

providing administrative, technical, and financial support to the municipalities.

The Ministry of Government regulates the creation of new municipalities. The

Ministry of Finance and Public Credit administers transfers to the local

governments through the National Revenue Sharing Fund (previously FONAPAR, now

FODESEC, the Local Government Development Fund). The National Development

Council (CONADE) approves the municipal annual budgets and determines tha

priority of the municipal projects presented for domestic and foreign financing,

2The World Bank, "Local Governments," Ecuador: Public Sector Finances:

Reforms to Foster Growth in the Era of Declining Oil Output, Country

Department IV, Latin American and the Caribbean Region, August 22, 1990.

3Ecuador, "Ley de Desarrollo Seccional y de Reformas a las Leyes de Regimen

Municipal, Regimen Tributario Interno, Arancelaria, Organica de

Administracion Financiera y Control y 006 de Control Tributario y

Financiero," May 1990.

-4-

thc latter mainly through credits of the Development Bank of Ecuador (BEDE). TheNait3.onal Pre-investment Fund (FONAPRE) lends and provides 4-echnical assistancefor preinvestment studies for public and private entities. The NationalSueretariat for Administrative Development (SENDA) was created in 1989 to developplolicy for improvement of management in public and private entities by upgradingiiyntor,, and developing integrated national training programs. The Ministries of1;ilAu Work,s, Education ard Health as well as the Iretitutes of Sanitary Works'.;)- arui Electrification of Ecuador (INECEL) execute works or provide servicesto mtAUcipal jurisdictions. There is a. considerable ambiguity on the role androuponeibilities of these institutions and a lack of coordination of theiractivities. The result is bureaucratic conflict and delay with very lowo2fctivenoss in fulfillment of these roles and responsibilities.

Lack of Qualified Staff. The scarcity of qualified staff is one ofi:tio ohi.f constraints to the development of municipalities, causing: reducedmobil)zation of local financial resources, inefficient investment plans, andinioff,ctive operation and maintenance of basic municipal services. Although theiatiibx o- municipal workers is more than adequate (about 1.2 municipal employeesior every 1,000 inhabitants), most are unskilled. Only the largest cities haveotaff with the technical capacity to prepare multiyear investment programs anddesign new projects. Municipalities have a total staff of about 35,000, and thenational support institutions (BEDE, CONADE, AME, etc.) employ about 700.Ettimates of the percentage of municipal personnel by employment category are asfullowss 7% managers and professionals; 31% technical and administrative; and62% manual workers. In general, the levels of education and qualification varywidely by location and size of municipality. For example, while in Machala(Costa) and Puyo (Oriente) only 6.7% and 14.3%, respectively, have completedprimary education, in Ibarra (Sierra), this percentage rises to 24.5%. Theevidence indicates that at the management and professional levels the two majorproblems are: (a) the incompatibility between staff qualification and jobrequirements; and (b) high turnover due to the change of mayor every four years.

1012 Inadequate and Poorly Coordinated Training Programs. Problemsaffecting the municipalities and municipal support institutions are amplified andoften the direct result of insufficient training. During the last 7 years onlyabout 2,000 persons (representing roughly 5% of the potential total) received anytraining at all. Furthermore, the training programs that exist lack: (a)eotablished iolicy, strategy, and objectives; (b) mechanisms for thecoordinatior planning and implementation of the training programs; (c) soundtraining need assessment; (d) managerial knowledge of personnel administvationand training; and (e) human and financial resources to carry out the trainingactivities.

lo 11 Insufficient Controls on Increases in Municipal Payrolls. MunicipalLaw (Chapter III, Article 40) allows municipalities to establish their own systemof personnel administration (including sala&.ies, promotion, and careerdevelopment). Howeve;., until recent reforms, municipalities normally preferredto follow the civil service of the Central Government, including its salary laws.It was common practice to raise salaries in accord with the national laws even if

- 5 -

no municipal budgetary resources were available--and then to go to the CentralGovernment for a transfer to cover the resulting deficit. Municipalities alsooften hired new employees with no budget to pay them, expectinc discretionarytransfers to cover the cost.

Reforms to Reduce the Institutional and Legal Constraints

1.14 These constraints have been addressed in the following legal oradministrative reformsa

1.15 Enactment of Legislation to Permit Full Cost Recover$r for Sewer andWater Systems. The LGDL of May 1990 permits full cost recovery for water andsewer projects.

1.16 Improved Coordination of Central Government Agencies inMunicipalities. A "Project Committee" will be established in BEDE and will bechaired by its General Manager. All Government organizations with a role inurban development would be represented on this Committee, including the Ministryof Finance, BEDE, IEOS, CONADE, FONAPRE, and SENDA. The role of this Committeeis to: (a) determine the priocity of the projects presented for financing; (b)determine the type of studies required for each project; (c) suggest to theGovernment future policies and possible legal reforms regarding municipalitiesand municipal support institutions; and (d) periodically review progress onproject completion. In other words, this Committee would seek to assureconsistency among municipal investment, institutional development, and trainingprograms. As a condition of effectiveness for the proposed project, the membersof the BEDE Pro3ect Committee would have been appointed and such Committee wouldhave begun to exercise its duties in a manner satisfactory to the Bank.

1.17 Passage of Legislation Controlling Increases in the MunicipalPayroll. Under clauses of the LGDL, municipalities cannot raise wages orcontract new employees unleas they have sufficient resources in their budgets topay them. The proposed project will build on this by assisting municipalities todevelop more effective personnel policies. At negotiations, it was agreed thatBEDE, with the assistance of SENDA, will develop a model career development planfor municipal civil servants designed to ensure their greater employmentstability. Taking into account the Bank's comments, BEDE will requiremunicipalities to adopt, as part of their subloan agreement, a career developmentplan for its employees consistent with the model plan, The terms of referencefor the plan itself will be presented to the Bank as a condition of effectivenessand the plan will be completed within the first six months after loaneffectiveness.

1.18 Improvement of the Coordination and Quality of Municipal TrainingPrograms. The Government selected SENDA to coordinate municipal trainingprograms and to form the nucleus of the central national coordination unit.Expanded training under the proposed project will be provided largely by theAssociation of the Municipalities of Ecuador (AhE) through the National Institutefor Municipal Development (INFODEM). AMR is a non-governmental entity with

- 6 -

representatives from all municipalities that was created in 1978 to safeguardmunicipal autonomy, provide technical assistance and training to municipalities,and coordinate municipal investment plans with those of the Central Government.

1.19 A Steering Committee headed by SENDA's secretary and composed ofsenior officials of BEDE, FONAPRE, AME, CONADE would be established to provideadvice in policy, coordination, implementation, evaluation, and financing of thetraining programs within three months after loan effectiveness. The coordinationof training programs for BEDE, FONAPRE, and INFODEM staff will be consolidated bySENDA to avoid overlapping activities and to facilitate participation of staff inprograma of common interest.

1.20 Training programs for about 580 staff of the municipal supportinstitutions (mainly BEDE and FONAPRE) and for about 460 staff of the first groupof municipalities selected to participate in the project were partially financedby the PPFs from IBRD and IDB. These efforts proved useful in improving thedesigri of the project's training programs, as well as providing training forthose who wiLl participate during its first year.

B. Reform of Intergovernmental Fiscal Relations

1.21 Lack of transparency, predictability, sustainability and equity inthe transfer system. Before the reforms, there were significant incentives inthe national/local transfer system for municipalities to run fiscal deficits andfor expenditure inefficiency. Municipalities would run up high fiscal deficitsas a way to pressure the Central Government for more discretionary grants. Thesegrants were often awarded to municipalities in direct proportion to their fiscalirresponsibility (see Annex 3), as in the case of transfers to cover payrollincreases (para. 1.13). As discretionary grants were readily available duringthe oil boom years in the 1970s, municipalities used them in lieu of raisingtheir own taxes and user charges. FONAPAR was set up in 1971 to make revenuesharing more predictable and transparent; however, by 1988 its automatic revenuesharing component constituted only about 30% of total transfers. FONAPAR'stransfers for investments (about 20% of total transfers in 1988) were not madebased on transparent and predictable criteria. In addition to the transfers,investment projects were often carried out in the municipalities by CentralGovernment agencies with only minimal participation by local governments inplanning. Furthermore, there was litt'le analysis of the capacity of thesegovernments to maintain adequately, operate, and recover costs for the completedprojects, or of their commitment for so doing. Technical, economic,environmental and financial evaluation of projects was very weak or nonexistent,

1.22 In summary, the transfer system provided incentives for fiscalbehavior that ran counter to objectives of lower deficits and greater efficiencyin the public sector. After the decline of oil revenues and total transfers, theunsustainability and counterproductive aspects of this transfer system becameincreasingly evident. However, the disincentives for local fiscal effort (para.1.21) kept local own-source revenues at about the same levels. For this reason,total municipal revenues from both own and national sources dropped from 2.5% of

-7

GDP in 1982 to only 1.5% in 1988, creating a serious decline in revenueBnocessary to meet the burgeoning demographic demand for municipal services (para.1.01).

1.23 The removal of the disincentives for local fiscal effort shouldencourage local governments to take advantage of the wide margin for increasedmobilization of resources and improved expenditure efficiency. About 55% ofmunicipal revenues derive from taxes on real estate, transfers of ownership, andprofits from sales. The reBt come from taxes on business activities andvehicles, and user fees, including tariffs and betterment levies. cadastres areout of date, billing and collection procedures inefficient, and cost recoveryfrom services quite low. There is also much room for improvement in expenditureefficiency.

1.24 Per capita transfers from the Central to local governments have notbeen highly correlated with poverty indicators or unsatisfied basic needs which,in turn, are "proxies" for lack of fiscal capacity. Thus, municipalities withrelatively high fiscal capacity often received higher per capita transfers, thanthose with low capacity (see Chart 3.1 in Annex 3). This perceived lack offairness of the system makes it difficult for the Central Government to resistthe demands of municipalities for discretionary grants.

1.25 Reform of the Transfer System. The reform cf the LGDL made thetransfer system more transparent, predictable, sustainable, and equitable (seeAnnex 3). Under the new law, FODESEC (Fondo de Desarrollo Seccional) replacesFONAPR and will receive i ;ut the same share of national fiscal resources (seeAnnex 3). The total amount to be distributed annually by FODESEC should exceedUS$87.1 million in 1991 versus total transfers from all sources to municipalitiesof US$90 million in 1988 of which less than a third came from the automatictransfers from FONAPAR.

1.26 Of this total, the 2% from the non-earmarked current revenues of theNational budget goes to provincial capitals; the remainder is div'ded as follows:75% for municipalities, 20% for provinces, and 5% for the emergency fund. Forthe municipal share, 60% would go to automatic revenue sharing and 40% to theMunicipal Investment Fund (MIF). Given the budget estimates for 1991, this wouldmean US$23.9 million for revenue sharing and US$15.9 million for the MIF. Thefollowing three criteria will be used in automatic distribution: (a) 60% bypopulation; (b) 30% by poverty; and (c) 10% by fiscal effort in relation tofiscal capacity. Chart 3.2 in Annex 3 shows the distribution of the total amountof FODESEC in accord with these different criteria. This automatic revenuesharing will reduce the incentives for fiscal irresponsibility and also make thesystem more equitable, in that municipalities with higher poverty and thereforeless fiscal capacity, will get higher per capita shares. As a condition ofeffoctiveness, the Ministry of Economy and Finance would have established all ofthe operational procedures for automatic revenue sharing, including theoperational definition and calculation of all indicators to be used in theallocation.

1.27 The LGDL specifies that the 40% going to the MIF will be transferredto BEDE and serve as counterpart fo.: the proposed project. The MIF will thenserve as a predictable, transparent, and sustainable source of counterpartfunding for eligible subborrowers. Moreover, all eubprojects to be supportedunder this project must meet the rigorous economic, financial, environmental andtechnical evaluations of BEDE. Eligible subborrowers (para. 2.10-2.16) willhave access to the MIF in three different ways: (a) onlending from BEDE; (b)grants to compensate subborrowers for the lose of revenue from lifeline ratescharged to the lower income families unable to pay the full cost of the followingbasic services: water, sanitary and storm sewers, solid waste and neighborhoodimprovement (see para. 2.20 for method of calculation); and (c) grants asincentives for current account saving. The grants for current account surpluswill serve as an added incentive for municipalities to increase their fiscalautonomy.

1.28 It was agreed by BEDE at negotiations that transfers from the MIF forthe first year will be as follows: (a) a minimum of 10% for onlending; (b) amaximum of 40% for grants for lifeline rates; and (c) a maximum of 50% for theincentives for current account surplus. During the first year, BEDE will onlendto the eligible subborrowers wishing to receive this incentive, then deduct themarginal increase in current account surplus from the principal of the loan atthe end of the year. At negotiations, BEDE agreed to put into effect amethodology, satisfactory to the Bank, for allocation by each of these threecriteria foL the remaining years of project implementation based on the analysisof the municipal financial and institutional action plans within the first 10months of loan effectiveness (para. 5.02). To the extent shown viable in thisanalysis, the grants for lifeline rates should decline and incentives to currentaccount surplus increase to augment the fiscal autonomy of the municipalities.This methodology should also monitor the distributive impact of the criteria usedin revenue sharing. For example, it will be important to know if the transferfrom revenue sharing would enable municipalities with a "reasonable" fiscaleffort and expenditure levels to balance their current accounts. If not, thecriteria might be altered or other steps taken (e.g., combine municipalities thatare too small to be fiscally viable).

1.29 In summary, the LGDL sets up a more predictable, transparent,equitable and sustainable transfer system. At negotiations, the Governmentagreed that the LGDL will not be modified in any way that would reduce itseffective contribution to project objectives.

F. Strengthening BDUE as a Lender and Provider of Technical Assistance

1.30 BEDE and Its Previous Policies. BEDE was established in 1976 as anautonomous financial institution to provide financing for public sector projectsand programs related to the socioeconomic development of Ecuador. BEDE's boardis chaired by the Minister of Finance; its operations are under a GeneralManager; and it is regulated by the Superintendencia de Bancos. BEDEIs mainsource of capital is from Government transfere.

-9-

1.31 BEDE's policy of lending at fixed interest rates of about 12% causedrapid decapitalization in real terms when the annual inflation rates jumped from27% in 1986 to 86% in 1988 causing annual markst interest rates for 90-day CDs toescalate from 23% in the first quarter of 1986 to 65.3% in May 1990. Theresulting highly negative interest rates caused the real value of BEDE's loanportfolio to fall from US$979.7 million in 1986 to only US$133.2 million in 1989,an annual rate of 39.3%. Net real earnings plummeted by an annual rate of 42.1%and real interest revenues dropped from US$148.6 million in 1986 to only US$18.5million in 1989. BEDE's net worth dropped from US$1.4 billion in 1986 to onlyUS$134 million in 1989 for two main reasons: (a) the drop in net earnings; and(b) the decline in capital transfers from oil due to the drop in theinternational price of oil and the sharp reduction of output after the 1987earthquake. The current rise in oil prices will be counteracted in part by theexpected decline of oil output due to the exhaustion of reserves.

1.32 Institutional Reform and Capitalization of BEDE. Reform of BEDE'sinterest rate policy is essential to assure its financial health. The Governmentand BEDE have agreed to an interest rate reform under which BEDE would graduallyincrease its interest charges to market levels on loans to local governmento andother governmental entities in accord with the interest rate agreement betweenthe Government and the Bank (para. 2.18). To capitalize BEDE, it would retain upto 25% of the amount borrowed from the Government as an equity contribution fromthe '^overnment, subject to review by the Government which could increase thepercentage repayment in accord with its overall macroeconomic objectives and theevolution of BEDE's capital base. In light of legislation passed after appraisalsetting up the Provincial Development Fund, which significantly increased thetotal transfers of the Government to BEDE, it was agreed at negotiations thatBEDE willt (a) commission a study with terms of reference and consultantacceptable to the Bank to: (i) develop a methodology for determining the"adequate" level of capitalization to meet its objectives as the primary lenderto the public sector; (ii) revise the estimates of the total amount of capitalassistance to BEDE under current and pending legislation; (iii) recommendappropriate corrective actions if necessary to correct any imbalance between suchcapital requirements and the availability of funds; (b) submit such study to theBank for comments promptly upon its completion; and (c) take into account theBank's comments and take all steps necessary to adopt such recommendations. Thestudy will be done within six months after loan effectiveness. BEDE's financialperformance would be monitored under the project (para. 2.19).

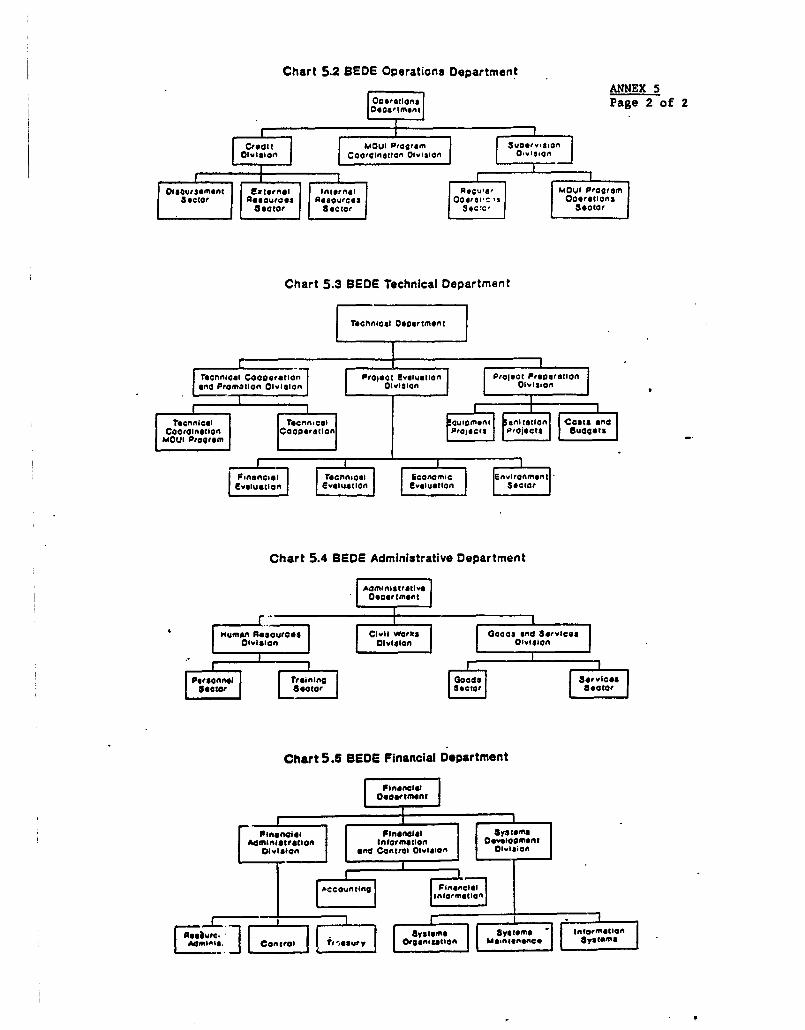

1.33 During project preparation, BEDE commissioned a comprehensivemanagement study (financed in part by the PPF) to determine how it could bestincrease its institutional capacity for the implementation of the proposedproject. Following the recommendations of this study, BEDE completelyreorganized its administrative structure (see organization charts in Annex 5) todeal more effectively with its expanded lending program and increased role as aprovider of technical assistance to municipalities. To improve projectevaluation (a major weakness in the past), a separate Project Evaluation Divisionwas created within the Technical Department with four separate sectors devoted toenvironmental, technical, financial and economic evaluation. To avoid the

- 10 _

implementation problems suffered by other Bank projects in Ecuador due to thehigh turnover of key project staff, BEDE agreed at negotiations to: (a) maintaina person with qualifications and experience satisfactory to the Bank who would beresponsible for the coordination of the Project (Project Coordinator); (b)establish the Project Coordinator as a department management-level position(under BEDE's internal rules, hiring or removal at the departmental levelrequires the permission of the Board of Directors); (c) make appointment orremoval of high-level staff assigned to work under the supervision of the ProjectCoordinator for purposes of the Project *:o be the sole responsibility of BEDE'sBoard of Directors, such appointment or removal to be made on the basis ofrecommendations of the Project Coordinator. As a condition of effectiveness,BEDE's Board of Directors would have issued a directive to establish thesestaffing procedures.

1.34 During project preparation, BEDE contracted with GTZ to producefinancial simulation models for its own use and for developing financial actionplans for municipalities (see Annex 4). To use these models, BEDE formed a newteam of professionals. Financial and institutional action plans for the 18municipalities given technical assistance under the pilot project (partiallyfinanced by the PPF) have been completed (para. 3.08).

0. Sector Development Issues, Objectives, and Bank Lending Strategy

1.35 The sector lending strategy is twofold, in that it aims tot

(a) Induce institutional reforms that:

i) encourage reforms to the current transfer and credit systems toprovide strong incentives for increased fiscal responsibilityand expenditure efficiency at the local level (see paras. 1.21-1.24); and

(ii) strengthen the institutional capacity of municipalities torespond to these new incentives.

(b) Based on this program of reforms, the proposed project would assistmunicipalities in increasing their fiscal autonomy and in reducingtheir shortfalls of urban services and infrastructure in an efficientmanner.

1.36 Although the recent events in the Middle East and the resulting risein oil prices make neceesary constant updating of the country's macroeconomicstrategy, the basic elements relevant to this project remain valid. To exploitfully its productive potential and to alleviate pervasive poverty, the countrywill have to replace the exhausted growth model of the 1970s with medium-termpolicies aimed at accomplishing two fundamental changes in the economy: (a)redefinition of the role of the public sector, and (b) elimination of theexisting protectionist trade regime and constraining labor market policies. Thepublic sector should use most of its oil revenues to finance puk.-lic and private

- 11 -

investment rather than consumption. Within this strategy, the local publicsector should: (a) rely less on subsidies from the Central Government and moreon its own revenues, and (b) increase its expenditure efficiency.

H. Prior Bank M!2erience

1.37 The Bank has financed a number of operations related to the urbansector since 1980. Bank assistance to the urban seotor in Ecuador began with theGuayaquil Urban Development Project (Loan 1776-EC) that became effective in 1980.This US$31 million loan was designed to demonstrate alternative low-costapproaches to providing services to poor beneficiaries with minimum subsidies.Its PCR concluded that this project had a positive impact on the implementinginstitutions at the national level, but was not succeesful in improvingmanagerial and financial capability at the municipal level. Following thisproject, there have been two housing loans to Ecuador. The first loan (Loan2135-EC) in the amount of US$35.7 million closed in 1988. Its PCR indicates thatit succeeded in demonstrating the feasibility of low-cost sheter alternativesand introducing concepts of affordable standards, coet recovery, andreplicability criteria into government housing programs. The follow-up housingloan (Loan 2898-EC) sought to build on the achievements of this first loan byintroducing new interest rate policies and a new mortgage instrument designed toimprove housing affordability. Unfortunately, loan performance has been poor dueto the rapidly rising rates of inflation and the weakness of the implementinginstitution. The Bank is supervising this project closely. FONAPRE received atechnical assistance loan (S-006-EC) of US$11 million in 1977. The PCR showsthat after a very slow start due to bureaucratic delays, the pace of projectexecution improved, resulting in the following achievements: completion of majorpreinvestment studies, good progress in its own institutional development, andthe preparation of a proposal for improving the legislation governing consultingactivities. The Second Guayaquil and Guayas Province Water Supply Project (Loan2135-EC) is currently suspended. The reason for this was that the implementingagency was abolished and responsibility for the sector transferred to a newentity after a serious deciine in the financial and institutional capacity of theoriginal entity. Recent efforts made to improve project performance have beeneffective, and the suspension is expected to be lifted soon with the new entitytaking over as borrower. In 1988, the Bank discussed the results of its UrbanWater Supply and Sewerage Sector Study with the Government and its mainrecommendations were adopted in the design of this project. The Public SectorManagement loan (2516-EC) financed consultants who contributed to the design ofthe reform of the revenue sharing system.

I. Rationale for Bank Involvement

1.38 The rationale for the Bank's involvement to date has been to helpdevelop the overall macroeconomic strategy in which the individual localgovernment reforms (e.g., revenue sharing, municipal legislation, and BEDE) are

- 12 -

integral parts.4 The Bank's continued involvement through the proposed projectwill help the Government to implement this strategy to maximum benefit at boththe national and local levels. Furthermore, the Bank can facilitate themobilization of cofinancing when appropriate and strengthen institutions throughthe introduction of new technologies in such areas as budgeting, informationsystems, and environmental assessment.

II. THE PROJECT

A. Project Origin

2.01 This project evolved from the Government's initial request forassistance in the design of a program of institutional reforms that form thisproject's institutional foundation (paras. 1.06-1.07). The project also draws onthe experience in municipal development and finance gained in similar projects inBrazil (Loan Nos. 2343-BR and 2623-BR) and in Argentina (Loan 2920-AR), whichalso seek to increase the fiscal autonomy of local governments by increasing boththeir capacity to mobilize resources and to spend efficiently.

B. Proiect Obiectives

2.02 The objectives of both the program of institutional reforms alreadydiscussed and the proposed project are essentially the same. The main objectivesare to increase the fiscal autonomy of municipal governments, as well as theircapacity to efficiently and equitably deliver services. This will contributedirectly to the attainment of the Government's overall macroeconomic goals ofreducing the public sector deficit and increasing its efficiency and equity.Specific objectives are to support governmental initiatives to:

(a) modify the national/local revenue sharing system to make it moretransparent, equitable, predictable, and effective in mobilizinglocal revenue;

(b) reduce discretionary fiscal transfers to municipal governments;

(c) help municipalities generate current account surpluses by increasingown-source revenues (especially user charges) and by reducingexpenditures (preferably by increasing efficiency);

(d) increase the capacity of municipalities to plan and executeefficient, equitable, and environmentally sound projects, as well asto maintain existing physical assets;

(e) improve the targeting of benefits to the lower income population;

4The World Bank, "Local Goverrments", op. cit.

- 13 -

(f) strengthen BEDE as a reliable source of financing and technicalassistance for municipal governments; and

(g) enhance the training activities in municipalities and of themunicipal support institutions at the national level.

C. Project DescriDtian

2.03 The proposed project (1991-1997, US$300 million) would financetechnical assistance and training and also onlending from BEDE for civil worksand equipment to eligible subborrowers: municipalities, and municipal andregional utility enterprises (hereafter municipal enterprises). The proposedBank project would finance about 35% of total project cost. BEDE's ProjectOperation Manuals would provide key implementation arrangements to assure projectobjectives would be attained.

2.04 The Project would finance two main componentos

(a) Institutional Development and Training (US$27.0 million, 9% of totalproject cost) including:

(i) institutional development (US$19.4 million, 6.5% of total cost)for both BEDE and municipalities; and

(ii) training (US$7.6 million, 2.5% of total cost) of about 1,100employees of national municipal support institutions (e.g.,BEDE, FONAPRE, SENDA and AME) and about 6,000 municipalemployees and instructors (i.e., training of trainers); and thecoordination of training activities.

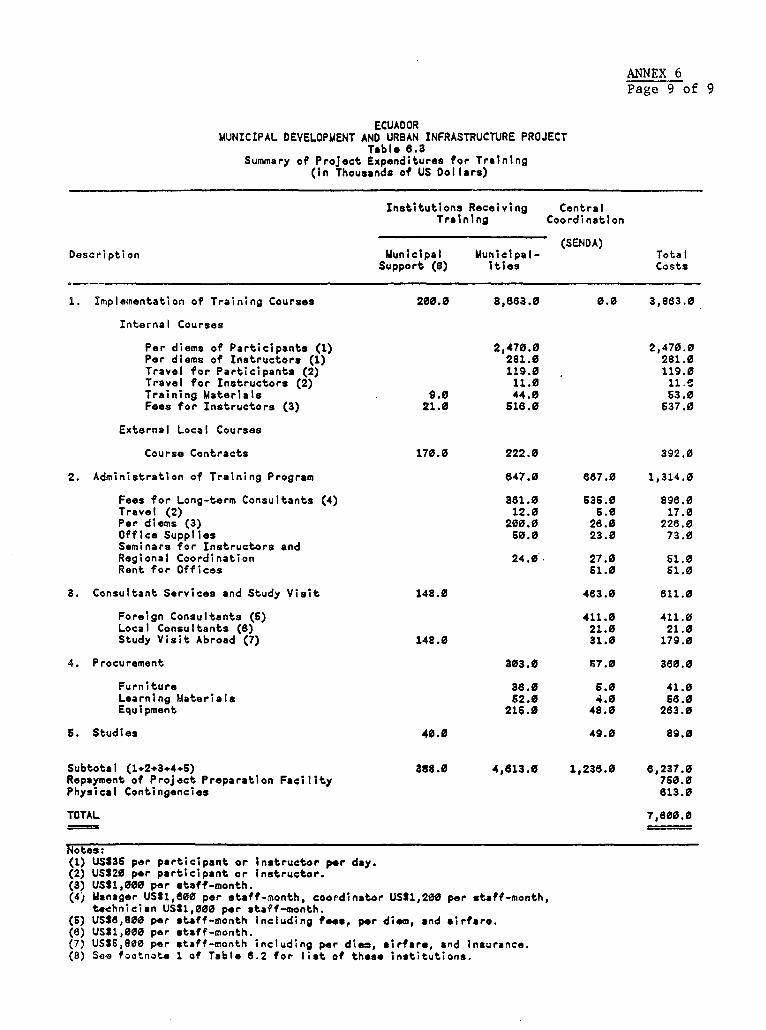

Both institutional development and training would focus on such areasas the creation or improvement of: planning and budgeting systems;cadastres; general organization and management; personnel policy; taxadministration; and project preparation and evaluation, includinganalysis of environmental impacts. This component would finance thefollowing, related to the above areas: fees for consultants andinstructors, courses, travel and subsistence, teaching materials,office supplies and equipment (e.g., vehicles, computers,audiovisuals and furniture). No civil works construction would befinanced under this component. See Annex 6 for details.

(b) Infrastructure (US$273.0 rillion, 91% of total cost) encompassing:

(i) physical investments (US$273 million, 83% of total cost) inconstruction and rehabilitation of public infrastructure (e.g.,water, sewerage, storm drainage, solid waste collection anddisposal, and roads), and community facilities (e.g., markets,parks, and slaughterhouses), as well as procurement of

- 14 -

materials, equipment and vehicles for maintenance or theprovision of public services; and

(ii) feasibility and engineering studies, auditing and supervision(US$25.0 million, 8% of total cost) needed to prepare, carryout and monitor the above investments. For further details,see Annex 7.

D. Proiect Costs and Financina Plan

2.05 The project cost estimates (see Table 1) are based on sample projectsprepared by the municipalities and BEDE and reviewed during appraisal. Generaland unitary specifications and dimensions of typical subprojects were reviewedand found acceptable to the Bank. Manuals for ex ante review and for supervisingexecution were prepared by BEDE and found acceptable to the Bank.

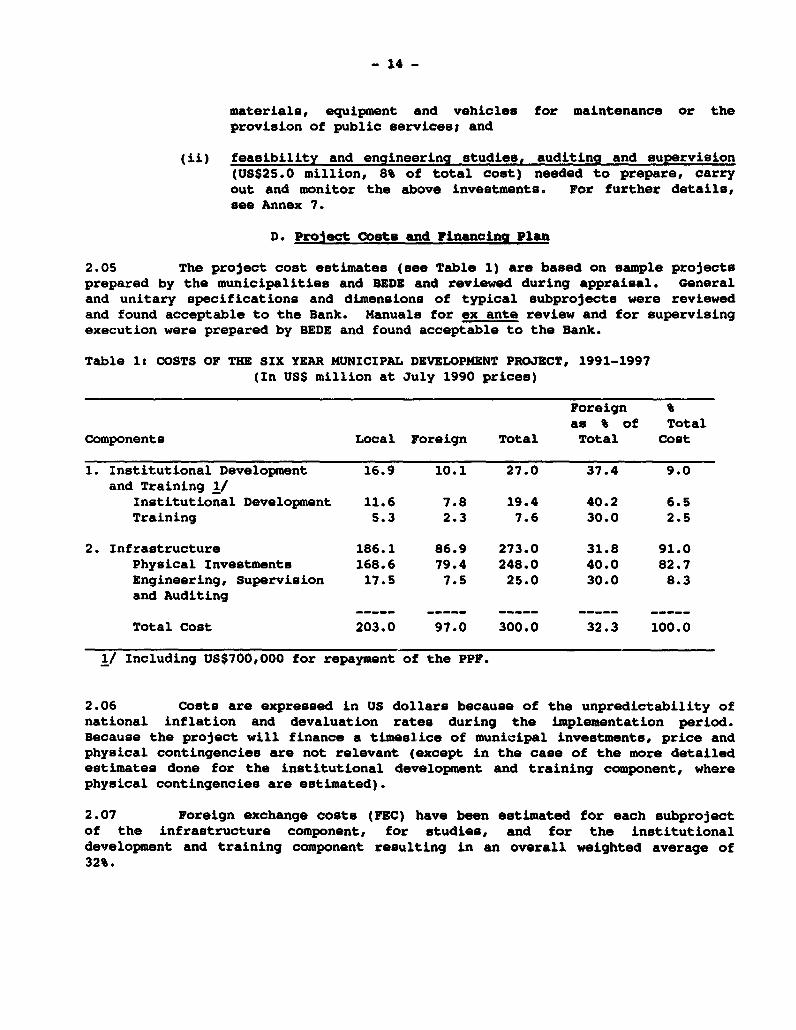

Table 1: COSTS OF THE SIX YEAR MUNICIPAL DEVELOPMENT PROJECT, 1991-1997(In US$ million at July 1990 prices)

Foreign as % of Total

Components Local Foreign Total Total Cost

1. Institutional Development 16.9 10.1 27.0 37.4 9.0and Training 1/

Institutional Development 11.6 7.8 19.4 40.2 6.5Training 5.3 2.3 7.6 30.0 2.5

2. Infrastructure 186.1 86.9 273.0 31.8 91.0Physical Investments 168.6 79.4 248.0 40.0 82.7Engineering, Supervision 17.5 7.5 25.0 30.0 8.3and Auditing

Total Cost 203.0 97.0 300.0 32.3 100.0

1/ Including US$700,000 for repayment of the PPF.

2.06 Costs are expressed in US dollars because of the unpredictability ofnational inflation and devaluation rates during the implementation period.Because the project will finance a timeslice of municipal investments, price andphysical contingencies are not relevant (except in the case of the more detailedestimate. done for the institutional development and training component, wherephysical contingencies are estimated).

2.07 Foreign exchange costs (FEC) have been estimated for each subprojectof the infrastructure component, for studies, and for the institutionaldevelopment and training component resulting in an overall weighted average of32%.

- 15 -

2.08 The total project cost of US$300 million would be financed (see Table2) by foreign sources (71%) and local sources (29%). The foreign sources ares

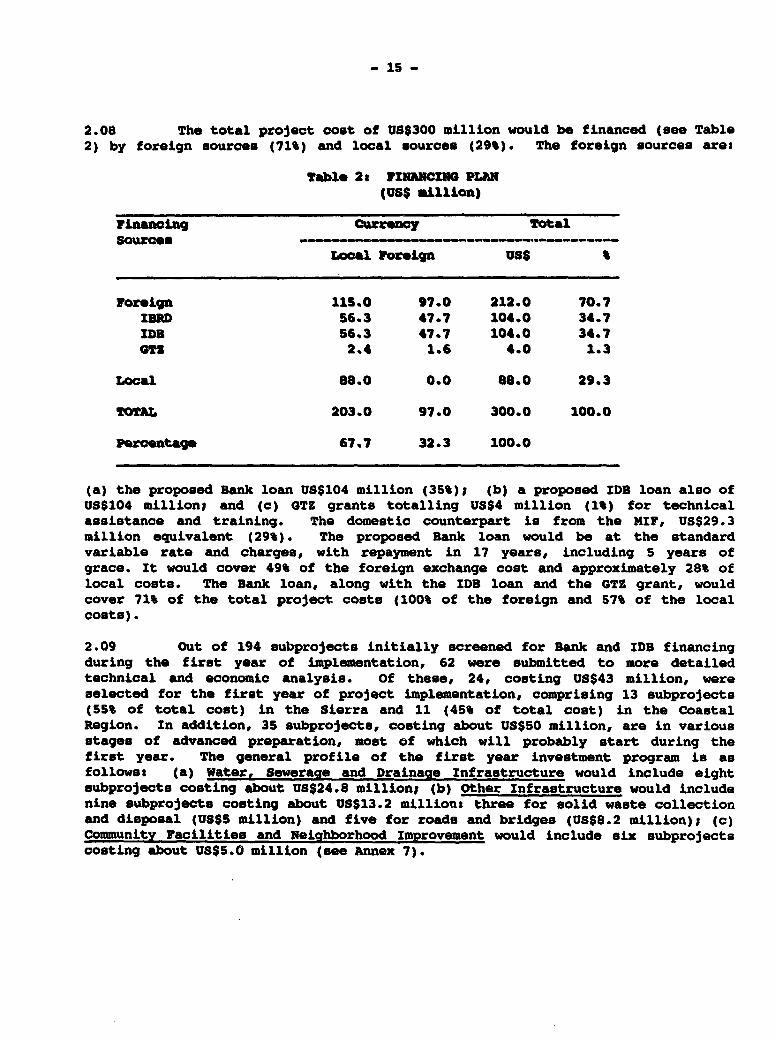

Table 28 P1NANCING PLAN(US$ mlllon)

Financing Currency TotalSources__

Local Poreign US$

Forelgn 115.0 97.0 212.0 70.7IBRD 56.3 47.7 104.0 34.7IDB 56.3 47.7 104.0 34.7GTS 2.4 1.6 4.0 1.3

Local 88.0 0.0 88.0 29.3

TOTAL 203.0 97.0 300.0 100.0

percentage 67.7 32.3 100.0

(a) the proposed Bank loan US$104 million (35%)l (b) a proposed IDB loan also ofUS$104 million; and (c) GTZ grants totalllng US$4 mlllion (1%) for technicalaseistance and tralnlng. The domestic counterpart li from the NIr, US$29.3million equivalent (29%). The proposed Bank loan would be at the standardvarlable rate and charges, with repayment in 17 years, including 5 years ofgrace. It would cover 49% of the foreign exchange cost and approximately 28% oflocal costs. The Bank loan, along with the IDB loan and the GTZ grant, wouldcover 71% of the total project costs (100% of the foreign and 57% of the localcosts).

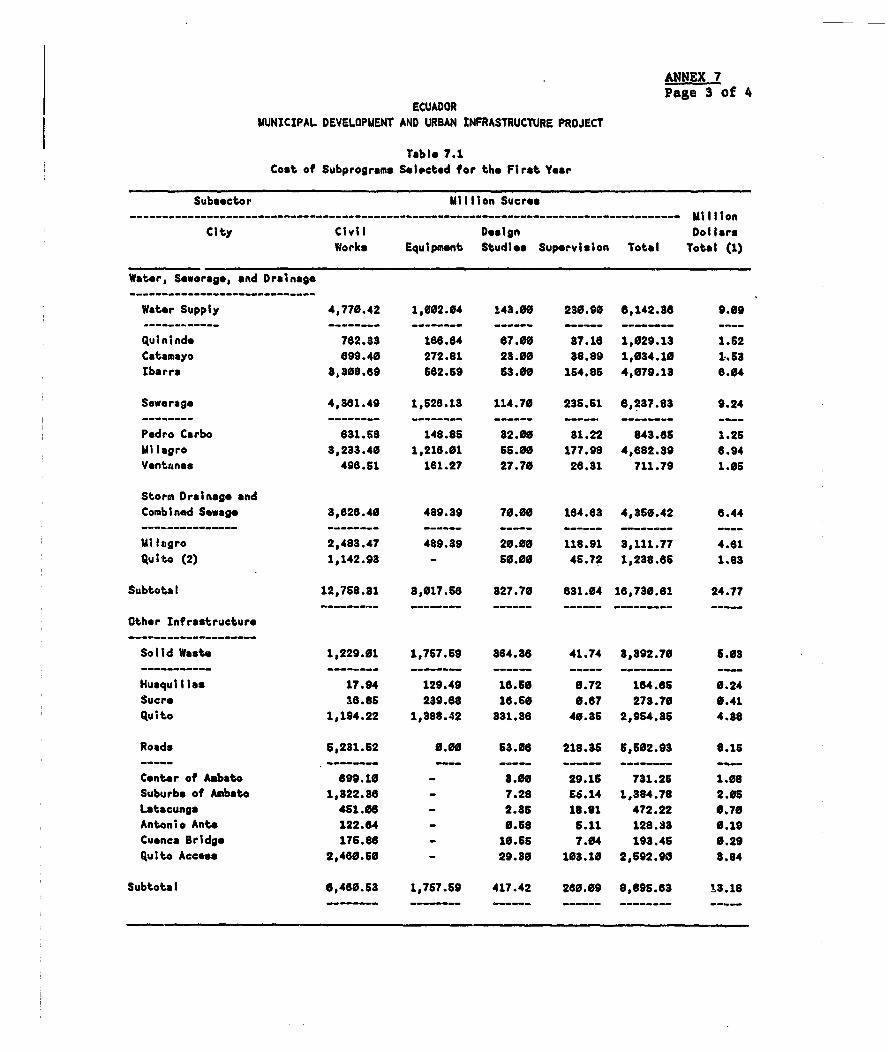

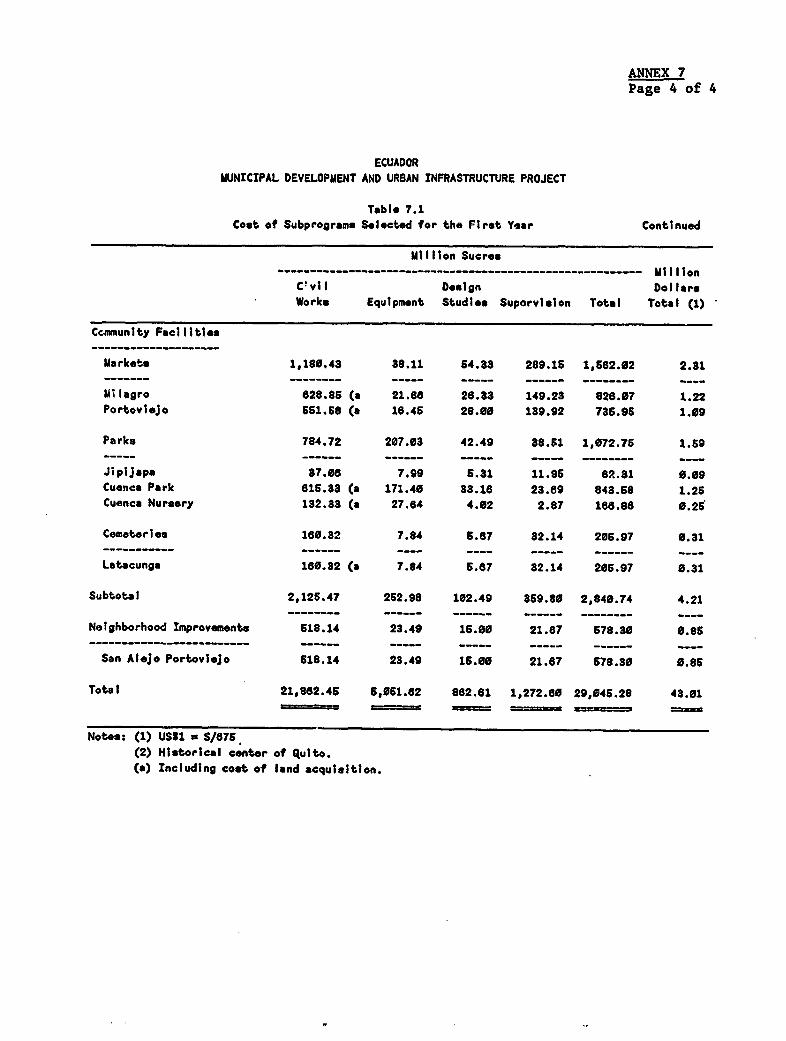

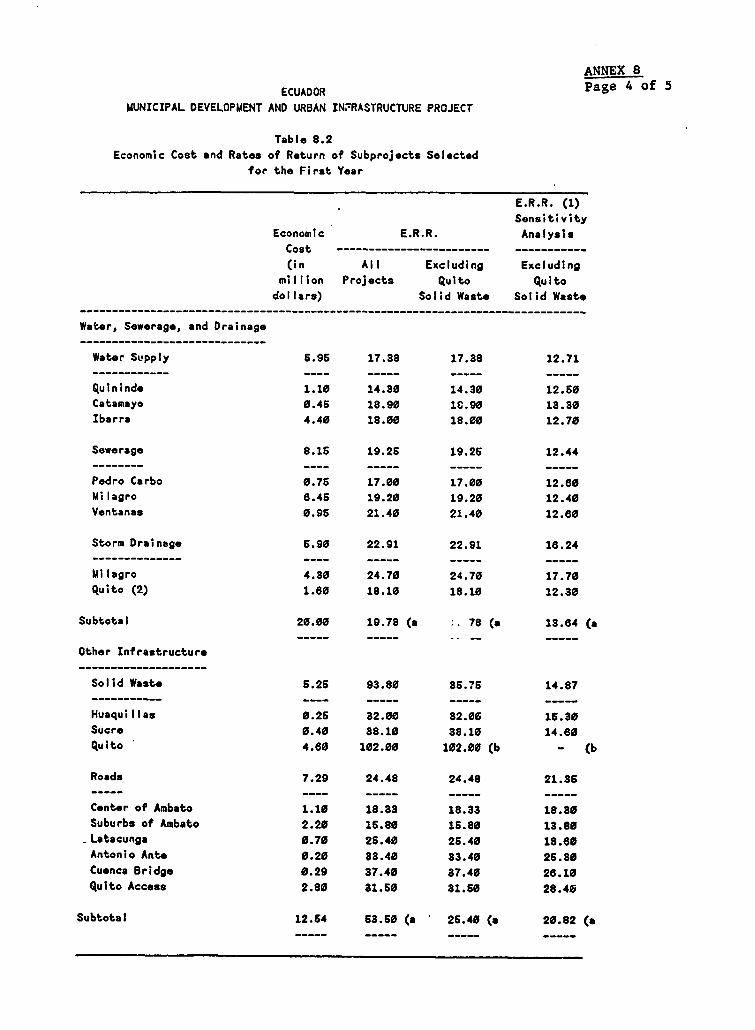

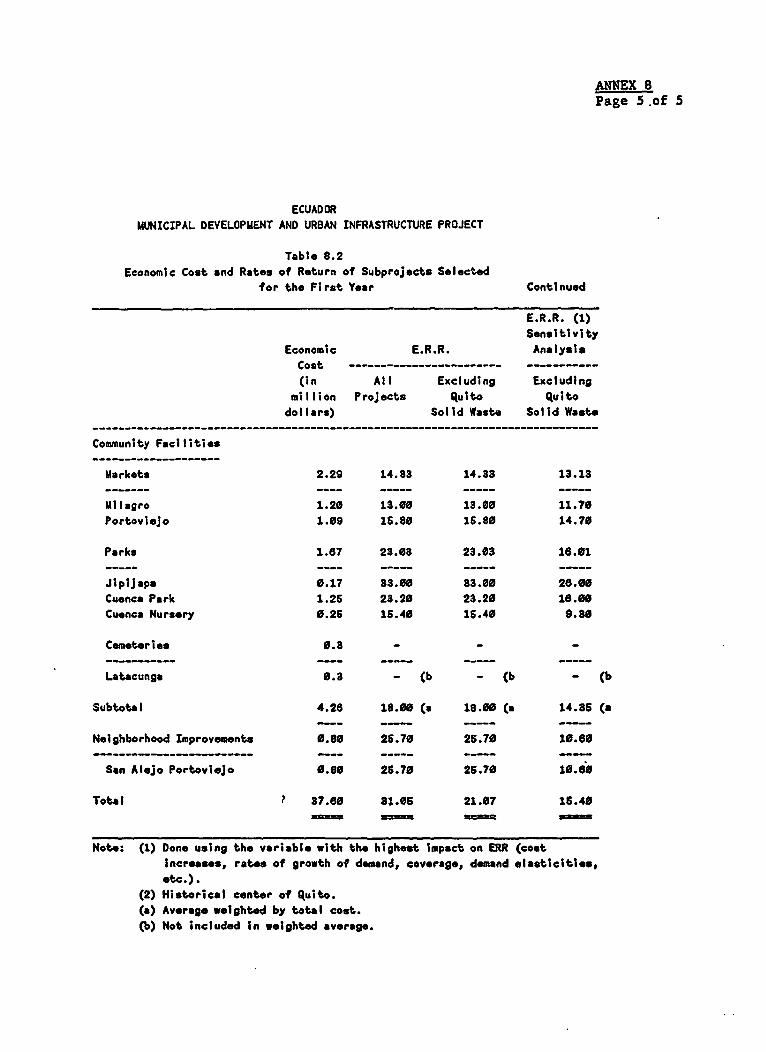

2.09 Out of 194 subprojects inltlally screened for Bank and IDB flnanclngdurlng the first year of implementatlon, 62 were submltted to more detalledtechnical and economlc analysis. Of these, 24, costing US$43 million, wereselected for the flrst year of project implementation, comprlslng 13 subprojects(55% of total cost) ln the Sierra and 11 (45% of total cost) in the CoastalReglon. In addltlon, 35 subprojects, costlng about US$50 milllon, are ln variousstages of advanced preparation, most of which will probably start during theflrst year. The general profile of the flrst year lnvestment program is asfollows: (a) Water, Sewerage and Drainage Infrastructure would include eightsubprojects costing about US$24.8 million; (b) Other Infrastructure would includenine subprojects costing about US$13.2 millions three for solid waste collectlonand disposal (US$S million) and flve for roads and brldges (US$8.2 milllon); (c)Communlty Facliltles and Neiqhborhood Improvement would include six subprojectscostlng about US$5.0 million (see Annex 7).

16

E. Eligibility Criteria

2.10 All municipalities and municipal enterprises potentially would beeligible to participate in the project, provided they meet project eligibilitycriteria. However, to assure sufficient funds for Quito and Guayaquil, while notdepriving the smaller municipalities of much needed resources, no subborrowercould receive more than 15% of the total project resources, unless otherwiseagreed with the Bank. Although all municipalities and municipal enterpriseswould be eligible for the Institutional Development and Training component(subject to the priorities listed balow), only those meeting the financial andinstitutional eligibility criteria would be eligible to borrow for infrastructureto assure that they will have the capacity to maintain and operate theinfrastructure, as well as to pay the debt service. In addition to theserequirements for municipal governments in general, there are specificrequirements for municipal and regional enterprises (para. 2.14). Regionalenterprises will be subject to the same criteria as municipal enterprises.

2.11 Institutional and Financial Action Plan (IFAP). To participate inthe Infrastructure Component, each municipality must present an institutional andfinancial action plan (IFAP) for developing adequate capacity for projectimplementation. This IFAP, which is described in the Project ImplementationManuals, will show how revenues will be raised and expenditure efficiencyincreased for both current and capital expenditures, as well as managementchanges necessary for project implementation. Municipalities that have notupdated their cadastres within the last five years would have to do so in lessthan two years in accordance with the implementation manuals. The goal would beto increase the collection efficiency to 80% of total potential urban land taxthrough such measures as: increasing cadastre coverage, reassessing land values,improving procedures for continual updating (e.g., improving registration of realestate transactions), and strengthening billing and collection procedures,including the indexing of tax bills.

2.12 Specific Requirements for the Sewer and Water Subcomponent. Inaccord with the Bank's sector study on urban water and sewerage, municipalitieswishing to invest in water and sewer systems must:

(a) have a sufficiently autonomous entity for project implementationMunicipalities with populations of 100,000 or more must create anindependent water company to construct, operate and maintain thesystem, and smaller municipalities that do not have an independentcompany must have a decentralized entity within the municipalgovernment for these ends that is acceptable to the Bank;

(b) develop a financial and institutional development plan acceptable tothe Bank as described in the operations manual. This plan wouldcontain strategies for: (i) increasing of metering at points ofproduction, distribution and consumption to augment the percentage ofwater billed to 75% of total water produced; (ii) design and

- 17 -

implementation of a tariff system with lifeline rates for the poorl(iii) improving billing and collection systems; (iv) establishing aseparate and efficient accounting system; and (v) bettering operationand maintenance practices.

2.13 Financial Criteria for municipal eligibility covers (a) currentaccount surplus and (b) debt capacity. In terms of current account surplus, onlymunicipalities with ratios of 1.0 or more between current revenues/currentexpenditures would be eligible to borrow for infrastructure, provided they alsomeet the requirements for improved financial planning discussed above. Incalculating this ratio, automatic revenue aharing is considered as a revenue, butdiscretionary grants are not. However, municipalities entering the program forthe first time with a current account ratio of 0.9 would be eligible to receivesubloans for infrastructure projects subject to the following conditionss (a)presentation of an action plan for reaching a current account ratio of 1.0 withina period compatible with the project's objective of full cost recovery; (b) abalanced current account will be a condition of disbursement for any subloan toassure compliance with the action plan; hcwever, in the case of a current ratioof less than 1.0, proof that the municipality has taken all actions deemed byBEDE necessary to reach this ratio (e.g., has updated the cadastre, raisedtariffs, etc.) based on agreed financial projections would be considered incompliance. In terms of debt capacity. the total service of the debt (includingboth interest and amortization) should not exceed 15% of the total revenues (netof discretionary grants and borrowing) of the preceding year, duly adjusted forinflation; and total short- and long-term debt should not exceed 60% of totalrevenues, as defined above. One of the objectives of the institutionaldevelopment and training component is to improve accounting systems so thatmunicipalities consistently use a cash basis and follow other accepted accountirgprocedures.

2.14 The financial criteria for municipal and regional enterprises arethat: (a) revenues from tariffs must cover all costs of operation, maintenanceand e.ministration, as well as the cost of investment not covered by grants tocompensate lifeline rates when the new works enter into operation (see para. 2.20for a discussion of the grants); (b) the averaga time of bill payment must beless than 90 days--if not, an action plan to reach this goal must be included;and (c) those enterprises with poor project execution or debt paymentperformance must present a plan for improving future performance, as well as forpaying outstanding debts.

2.15 Priorities for Institutional Development and Training Component. Allmunicipalities will be eligible to participate in the Training Sub-component, bu.priorities will be set for participation in the Institutional DevelopmentSubcomponent to assure the most efficient allocation of this more costlyassistance involving intensive on-site work by teams of consultants. For thosesubborrowers not initially eligible for the institutional developmentsubcomponent, BEDE would make recommendations for reforms and a financial actionplan to enable each municipality to meet the financial eligibility criteria.Furthermore, these municipalities would have access to the training programs

- s1 -

(e.g., regular courses, seminars, workshops and on-the-job training) oriented todeveloping its capacity to the point where it could more effectively participatein the institutional development subcomponent and the infrastructure component.The sequential priorities for this institutional subcomponent are as follows:(a) first priority would go to those municipalities that have balanced currentaccounts and are therefore ellgible to borrow for investments or that have amunicipal enterprise that might borrow; (b) second priority would go to thosethat have: (i) a ratio of current revenues/expenditures of 0.9 or more, (ii)institutional potential to achieve current account equilibrium wlthin areasonably short perlod, and (lii) a project that might potentially be financed;and (c) last oriority would go to the remaining municipalities. These criteriaassure that the resources for the institutlonal development subcomporant will beawarded to those municipalities that can best use them.

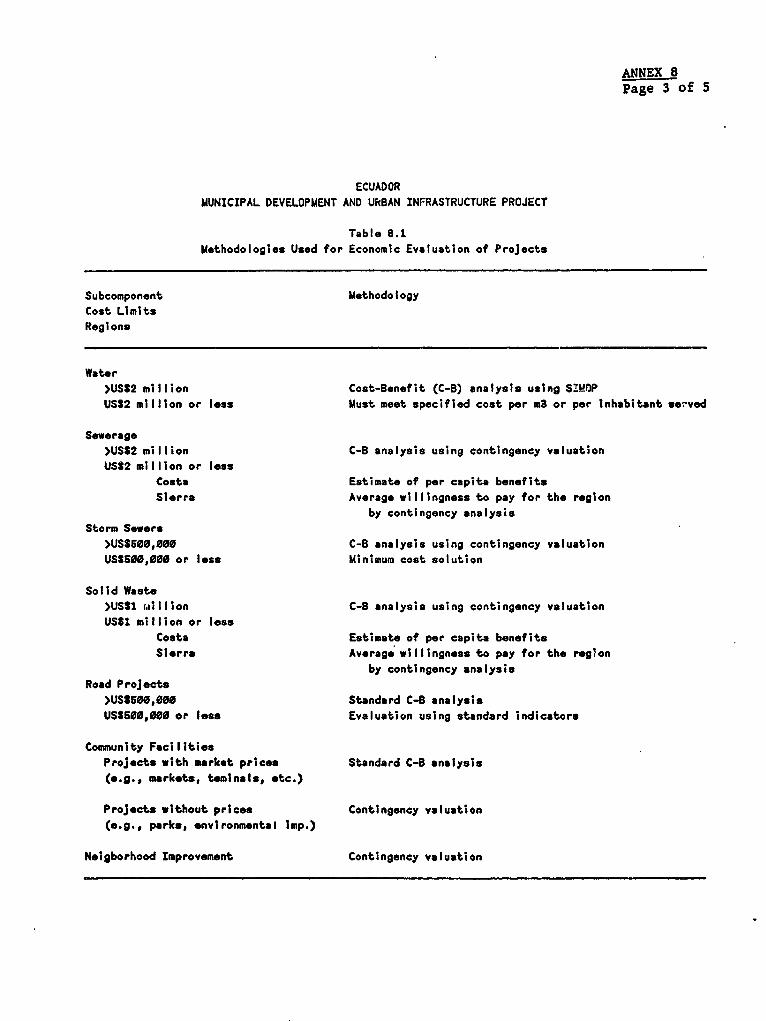

2.16 Criteria for EvaluatJon of Subprojects. Subprojects will be preparedat the municipal level and evaluated by BEDE according to the economic,environmental, technical, financial and institutional criteria set out in theProject Implementation Manuals (see Annex 8 for criteria for economicevaluation).

F. Borrower and ExecutLng Agency

2.17 The Borrower would be the Republic of Ecuador. The proceeds of theBank and IDB loans would be onlent in sucres to BEDE at the same maturity as theBank loan (20 years with five of grace). The exception would be the portionsallocated to finance institutional development and trining expenditures, whichwould be transferred to BEDE and to subborrowers as grants (with the exception ofupdating cadastres, which would be financed by onlending). Grants are used as anadded incentive to participate fully in the institutional development andtraining component. The Central Government would assume the cross-currency anddollar exchange rate risks and will also pay the commitment charge. The signingof agreements between the Government and BEDE for the transfer of the Bank loanwould be a condition of effectiveness.

2.18 BEDE's interest rate on funds borrowed will be variable based on itsonlending rate minus a spread to cover operating costs, set initially at 4percentage points. However, this spread could be adjusted, subject to Bankapproval, in accord with changes in the nominal interest rate to assure thatoperating costs are covered. The spread should be estimated as the totaloperating costs divided by the sum of llabilities and net worth, plus areasonable margin for profit and risk. The first revlew of the spread should bein the first quarter of 1991 to assure that it is adequate given the manymacroeconomic changes that have occurred since appralsal. BEDE's onlending ratetVo all of its subborrowers (not just the subborrower under thls project) would bevariable and set in accord with the understanding reached between the Bank andthe Govern.!ent (Letter of the President of the Junta MonetarLa of December 13,1989). In accordance w.th this understanding, the rate on July 1, 1990 was setac 3S%. This rate would be adjusted biannually in line with the scheduleindicated Ln the above mentioned understanding, reaching the commercial bank

- 19 -

lending rate (Tasa de Libre Contratacion) by June 30, 1992 or considerablyearlier if nominal interest rates decline (see Annex 4, para. 20). The onlendingterms would be included in the agreements between BEDE and each of its borrowers.Municipal repayment of loans would be guaranteed by its revenue-sharing receipts.The repayment period of the loans to municipalities will vary in accord withpotential for cost recovery, ranging from 5 years for cadastres to 20 years forwater and eewer eystems. The local cuunterpart will come from the MIF inaccordance with the criteria established by BEDE (para. 1.28).

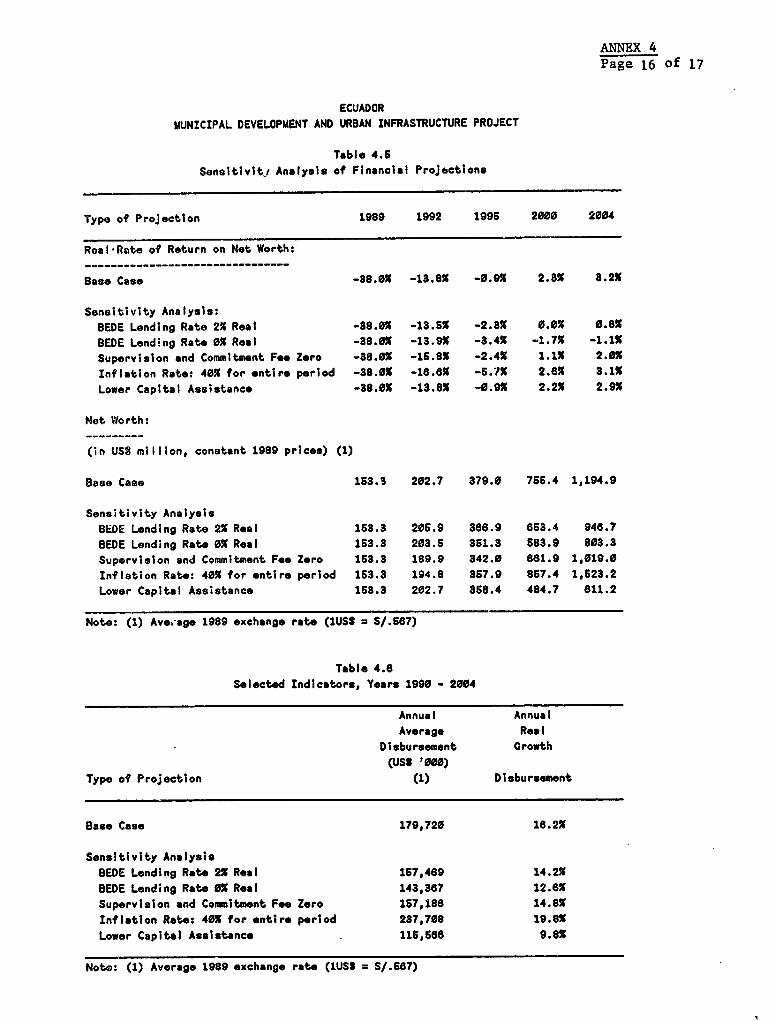

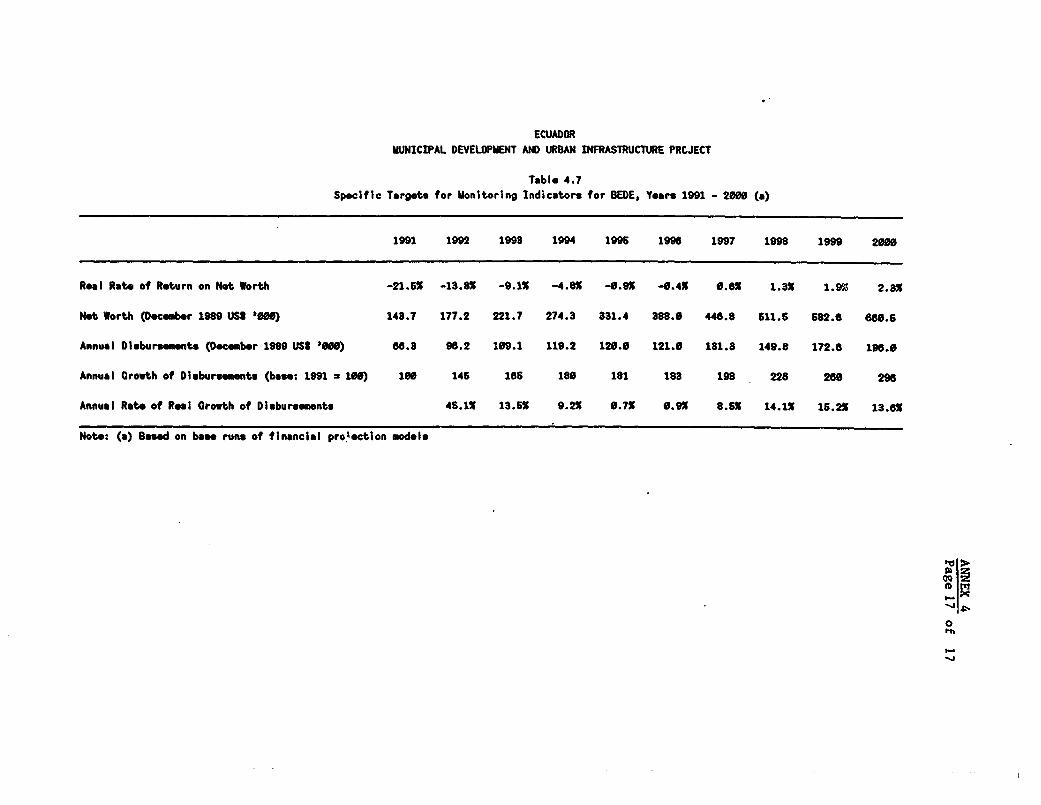

2.19 At negotiations, agreement was reached on a set of specific financialtargets, including real rates of return on net assets, real net worth, realdisbursements and real growth of disbursements. In addition, BEDE agreed toprepare an annual financial management plan acceptable to the Bank, to bediscussed during the annual review, which would include: (a) a review ofprogress in meeting its financial targets; and (b) a atrategy for the coming yearto contribute to the attainment of project and overall macroeconomic objectiveswith emphasis on (i) the volume of capital assistance from the Central Governmontand (ii) capacity to use it effectively. This plan should also analyze po -ac"overcapitalization" of BEDE due to new legislation (e.g., the ProvincialDevelopment Fund) using the methodology discussed previously (para. 1.32). TheBEDE financial simulation would be used to adjust specific targets for monitoringindicators from the base case scenario (see Table 4.7, Annex 4) established atnegotiations in accord with macroeconomic shifts, such as changes in theinternational price of oil.

G. Cost Recovery Policy and Grants to Ccomensate Lifeline Rates

2.20 Normally, all costs of operation, administration, maintenance, andinvestment would be recovered either directly from user charges (e.g., tariffs,fees and betterment levies) or indirectly from increased general tax revenues(see Annex 9 for details by subcomponent). However, in the cases of water,sanitary and storm sewers, solid waste, and neighborhood improvement, the generalrule of total cost recovery would be relaxed to provide lifeline rates. Alifeline rate is a below-marginal-cost price for a minimum quantity of a basicservice for lower-income families unable to pay marginal cost prices. Forexamtple, the municipal water entity could charge a lifeline rate to lower-incomefamilies for a specified minimum amount of water (e.g., 10 to 15 cubic meters permonth), for which families could not be charged more than 3% of the averagemonthly income for '.he municipality (if available) or the region. To compensatefor the revenue lost due to these lifeline rates that cannot be recovered withinthe municipality via cross-subsidies in the form of higher rates to higher-incomefamilies, a transparent and up-front grant from the HIF would be allowed. Thecalculation of the amount of this grant would require only estimates of the totalfamilies paying lifeline rates, in addition to the other data required forproject evaluation. The amount of the grant could never be greater than totalinvestment cost and the other data used for project evaluation. In moretechnical terms, the grant to compensate lifeline rates would be calculated asthe present value of the revenue stream necessary to cover total project costs(including maintenance, administration, operating, and investment costs) minus

- 20 -

the present value of the actual stream of revenue from the project (which doesnot cover all costs due to the lower lifeline rates for poor families). Therules for cost recovery and methodology for calculating the grants are defined indetail in the project implementation manuals.

III. PROJECT IMPLEMENTATION

A. Implementation Arrangements

3.01 Overall responsibility for project implementation would rest withBEDE, which would administer the MIF and the resources from the Bank, IDB loans,and the GTZ grants. During project preparation, a number of efforts weredirected at strengthening BEDE to fulfill adequately its key role in projectimplementation through its expanded lending program and increased role as aprovider of technical assistance, including a complete a'ministrativereorganiization and training of employees (paras. 1.33-1.34). BEDE respondedefficiently to the many demands of project preparation and appears ready toaesume its increased responsibilities. During project implementation, anextensive program of institutional development a-.d training will continue tostrengthen this capacity (para. 3.06 and Annex 6~,

3.02 The Project Implementation Manuals, acceptable to the Bank--includingspecific manuals for Eligibility, Operations, Sapervision and Monitoring,Economic and Financial Appraisal of Projects and Bor,-owers, Technical Evaluation,Environmental Impact, and Institutional Developmen'. --would cover all regulationsconcerning the relationships between the municipal.). ies and other subborrowerswith BEDE, FONAPRE, SENDA, and AME. At negotiation*, BEDE agreed to administerthe project in accordance with these manuals, and not to amend them without priorBank consent. A condition of effectiveness would e that project operatingmanuals acceptable to the Bank have been issued, These regulations woulddescribe in detail the role of participating entities and the internal proceduresof BEDE that municipalities and other subborrowers should be aware of for theirefficient participation in the project, includinS;: (a) the criteria foreligibility (para. 2.13); (b) the preparation of feasibility studies; (c)subproject selection criteria; (d) mechanisms for approval of projects by BEDE,including conditionality on local resource mobilization (tariffs, property taxes,user charges, etc.) and others re.ated to cost recovery and operation andmaintenance of the projects to be financed; (e) a model of the Loan Agreementbetween BEDE and its subborrowers; (f) procurement procedures for goods, worksand services; (g) accounts and auditing; and (h) specific regulations onenvironmental protection to be followed during preparation, implementation, andoperation of each project. BEDE would determine the eligibility of subborrowers(i.e., municipalities and municipal enterprises) according to the EligibilityManual (for criteria see paras. 2.09-2.15) acceptable to the Bank. BEDE alsowould carry out the technical, economic, financial, and environmental evaluationof the subprojects and would approve the respective subloans. The ProjectCommittee will continue to coordinate all Government organizations with a role inurban development (para. 1.16). BEDE would supervise subproject implementationin accordance with procedures determined in the Supervision and Monitoring

- 21 -

Manual, acceptable to the Bank. This Manual would include: (a) a description ofthe rights and obligations of all subborrowers; (b) the financial mechanisms forproject implementation (disbursement, retention, and accounting); (c) monitoringand supervision mechanisms, defining the areas of responsibility of thesubborrowers and BEDE; (d) cross-references with the Project ImplementationManuals on the interrelation between the project advance reports anddisbursements; (e) a mechanism for disbursements for monthly payments; (f) asAnnexes, the models of standard bidding documents for civil works, goods, andservices to be utilized by municipalities and other subborrowers. Auditing wouldbe cai-ried out as described in para. 3.18. BEDE would approve the procurementcontracts of the subborrowers (see para. 3.10) and would provide the Bank with abiannual progress report (para. 3.19).

3.03 BEDE will establish subsidiary agreements with FONAPRE and SENDA toperform specific functions for the project. FONAPRE would be responsible forhiring consultants and supervising the preinvestment studies requested by BEDE'ssubborrowers (prefeasibility, feasibility, and final engineering design) inaccordance with an agreement signed between BEDE and FONAPRE, acceptable to theBank. BEDE would finance these studies with proceeds from the proposed loan, butwould recover these costs from its subborrowers. SENDA will coordinate themunicipal training program, but the actual training programs will be provided byAME and other entities. As a condition of effectiveness, subsidiary agreementsacceptable to the Bank would be signed between BEDE and (i) FONAPRE and (ii)SENDA.

3.04 Adequate Bank supervision would be an especially '.mportant element ofsuccessful project implementation, especially during the first years. BEDEagreed during negotiations to submit all requests for subproject financing withvalues over established limits (e.g., US$4 million for sewer and water projectsand US$1 million for other projects) for prior approval of the Bank.

B. Strenqthening Implementing Institutions

3.05 The institutional development and training programs will encompassall of the institutions involved in the project (see Annex 6).

3.06 BEDE will be strengthened so that it can meet its increasedresponsibilities for providing technical assistance to its subborrowers, as wellas doing the economic, environmental, technical, and financial analyses of theprojects and of the borrowing entities themselves (see Annex 6).

3.07 Since institutional development is a key objective of the project andfinancial and Institutional action plans by municipalities and municipalenterprises are prerequisites for project participation (paras. 2.09-2.15),special emphasis has been given to it. BEDE will establish a technicalcooperation agreement with GTZ that will create a specialized unit staffed byhigh-level professionals to carry out this program. This unit will beinstitutionally located in the Technical Department of BEDE in the Technical

- 22 -

Cooperation and Promotion Division (see Annex 5). The signing of an agreementbetween BEDE and GTZ for execution of the institutional development componentwould be a condition of effectiveness. In addition, at negotiations, BEDE agreedthat it will hire consultants necessary to implement effectively theinstitutional development and training component.

3.08 As part of the project preparation effort, GTZ applied and tested acomprehensive methodology and an institutional development model in themunicipalities of Tulcan, Riobamba, and Babahoyo. In addition, GTZ organizedseveral courses and seminars in coordination with BEDE, AME, FONAPRE and a numberof international entities. Training was provided for about 100 officials fromthe 18 municipalities selected to be the first group of project participants,including the preparation of administrative manuals for improving institutionaland financial management (see Annex 6). This effort facilitated the testing andfine tuning of the institutional development program for the municipalities(para. 1.34). Training programs for about 580 staff of the municipal supportinstitutions (mainly BEDE and FONAPRE) and for about 460 staff of the first groupof municipalities selected to participate in the project were partially financedby the PPFe from IBRD and IDB (see Annex 6). These efforts proved useful inimproving the design of the training programs to be implemented during projectimplementation, as well as providing training for those who will participateduring its first year.

C. Procurement