Embed Size (px)

Citation preview

JP Morgan Basics & Industrials Conference

June 2006

AGCO CorporationAGCO Corporation

A World of Solutions for Your Growing Needs

2

Forward Looking Statements

Statements that are not historical facts, including projections of future sales, net income, earnings, operating income, cash flow, cost reduction, production levels, capitalization, coverage ratio forecasts, industry demand outlook, and our goals and objectives for margins, asset management, revenue and productivity improvements, are forward looking and are subject to risks which could cause actual results to differ materially from those suggested by the statements. These statements are based on current information and beliefs and, accordingly, the Company can give no assurance that the statements will be achieved. The Company bases its outlook on key operating, economic and agricultural data which are subject to change including, but not limited to: farm cash income, worldwide demand for agricultural products, commodity prices, grain stock levels, weather, crop production, farmer debt levels, existing government programs and farm-related legislation. Additionally, the Company’s financial results are sensitive to movement in interest rates and foreign currencies, as well as general economic conditions, pricing and product actions taken by competitors, customer acceptance of product introductions, the success of its facility rationalization process and other cost cutting measures, availability of governmental subsidized financing programs, production disruptions and changes in environmental, international trade and other laws which impact the way in which it conducts its business. Further information concerning these and other factors that could significantly affect the Company’s results is included in our Form 10K for the year ended December 31, 2005 as filed with the Securities and Exchange Commission. The Company disclaims any responsibility to update any forward looking statements.

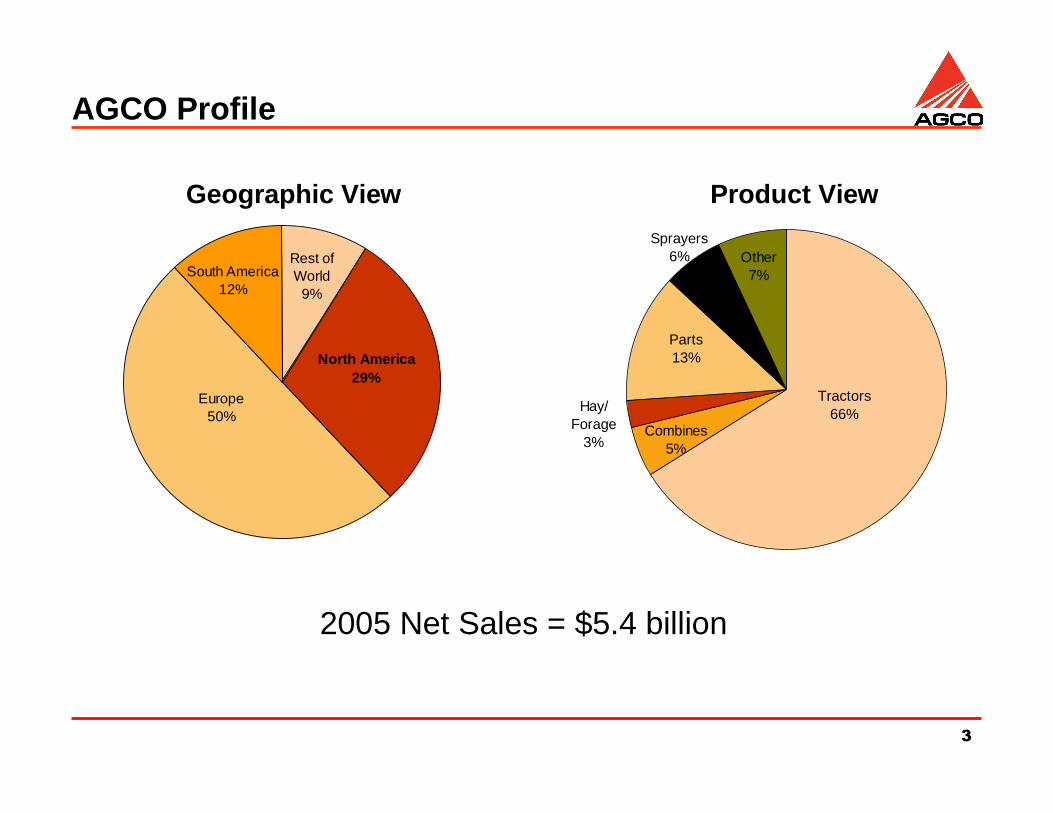

3

Europe50%

South America12%

North America29%

Rest of World

9%

2005 Net Sales = $5.4 billion

AGCO Profile

Parts13%

Sprayers6% Other

7%

Combines5%

Hay/ Forage

3%

Tractors66%

Geographic View Product View

4

Leading Brands - Tractors

5

Combines, Hay, Forage, Sprayers & Other AG. Equip

6

Award Winning Technology

� Fendt 936 Vario – 2005 Agritechnica Show – Machine of the Year award for high-horsepower tractors

� Valtra C150 – 2005 Italian EIMA Agricultural Show Golden Tractor of the Year Award

� Massey Ferguson 6400 – Dyna-6 2005 Royal Show New Equipment Award/Technical Innovation Award

7

Market Overview

North America ’04 ’05 Q106>40 HP Tractors +19% + 5% + 5%

Combines +41% + 1% +13%

Western EuropeTractors + 2% (5%) 0%

Combines (11%) +5% ( 3%)

South America (Brazil+Argentina )Tractors +8% (31%) ( 1%)Combines +8% (58%) (29%)

8

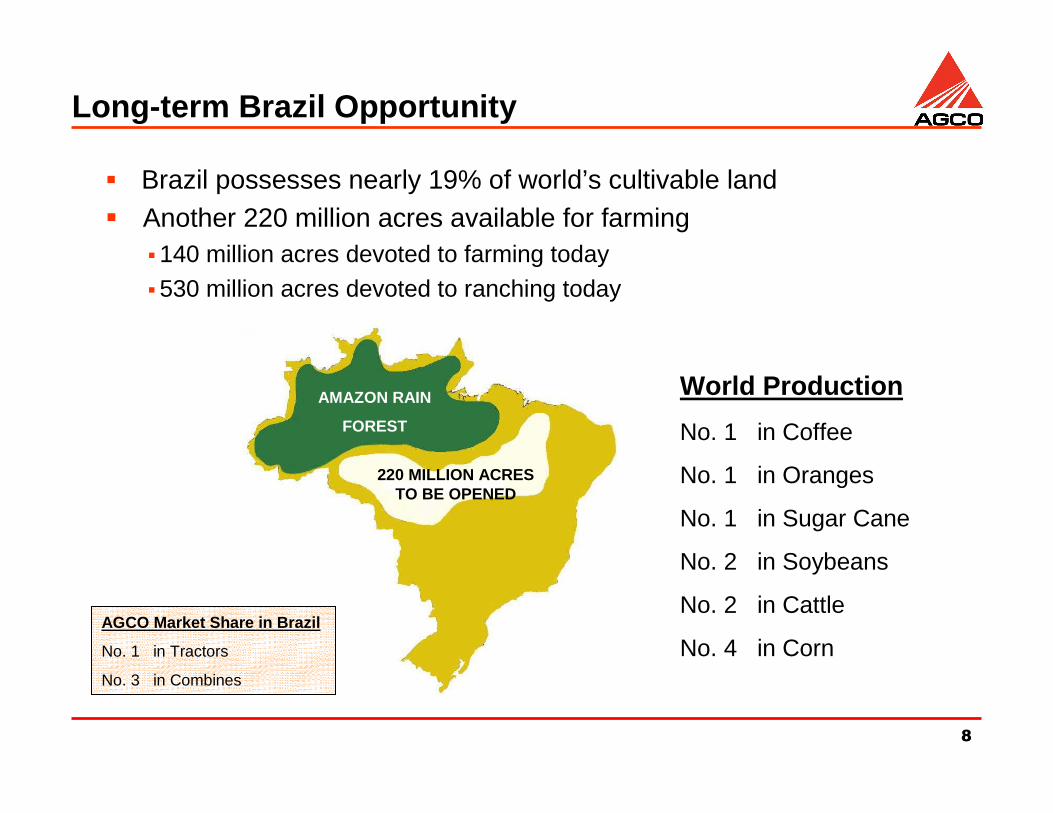

� Brazil possesses nearly 19% of world’s cultivable land� Another 220 million acres available for farming

�140 million acres devoted to farming today

�530 million acres devoted to ranching today

AMAZON RAIN

FOREST

220 MILLION ACRES TO BE OPENED

AGCO Market Share in Brazil

No. 1 in Tractors

No. 3 in Combines

World Production

No. 1 in Coffee

No. 1 in Oranges

No. 1 in Sugar Cane

No. 2 in Soybeans

No. 2 in Cattle

No. 4 in Corn

Long-term Brazil Opportunity

9

Key Strategies – New Products

425 HP Class 8 Combine

� High Capacity

� MF / Challenger / Gleaner brands

� Fastest Unloading Rate

Fendt 900X

� Up to 360 hp

� 60 KPH

� Tier III Engines� Advanced Electronics

10

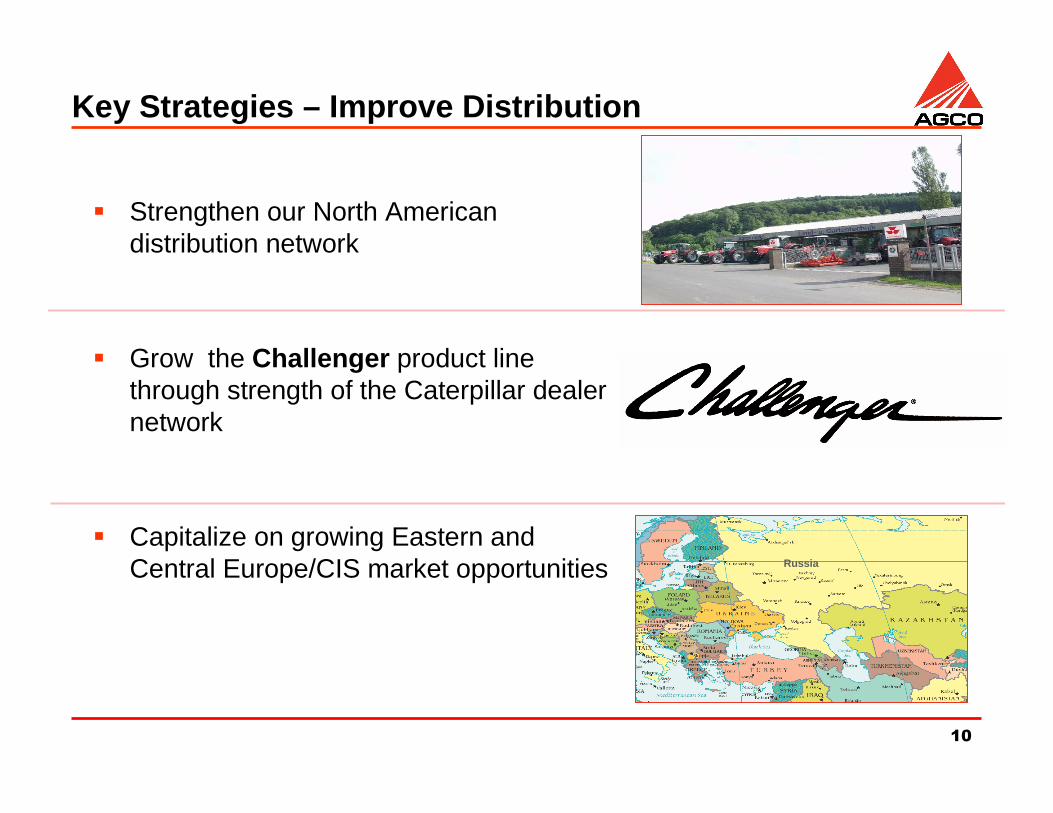

Key Strategies – Improve Distribution

� Strengthen our North American distribution network

� Grow the Challenger product line through strength of the Caterpillar dealer network

� Capitalize on growing Eastern and Central Europe/CIS market opportunities Russia

11

Strategy� Distribute Challenger branded farm machinery through CAT dealers

� Focus on North America & developing markets� Leverage relationship with finest equipment distribution network in the world

� Encourage CAT dealer investment in AG equipment, sales people and new store

locations

Challenger Product Line Initiative

12

Key Strategies – Common Product Platforms

Common Components� Cabs

� Engines

� Drivelines

Common Designs� Combines

� Balers� Sprayers

13

Key Strategies – Expand Engine Production

� 2005 volume: ~24,000 units

� Target: 45,000 to 55,000 units

� $15M to $20M annual savings

14

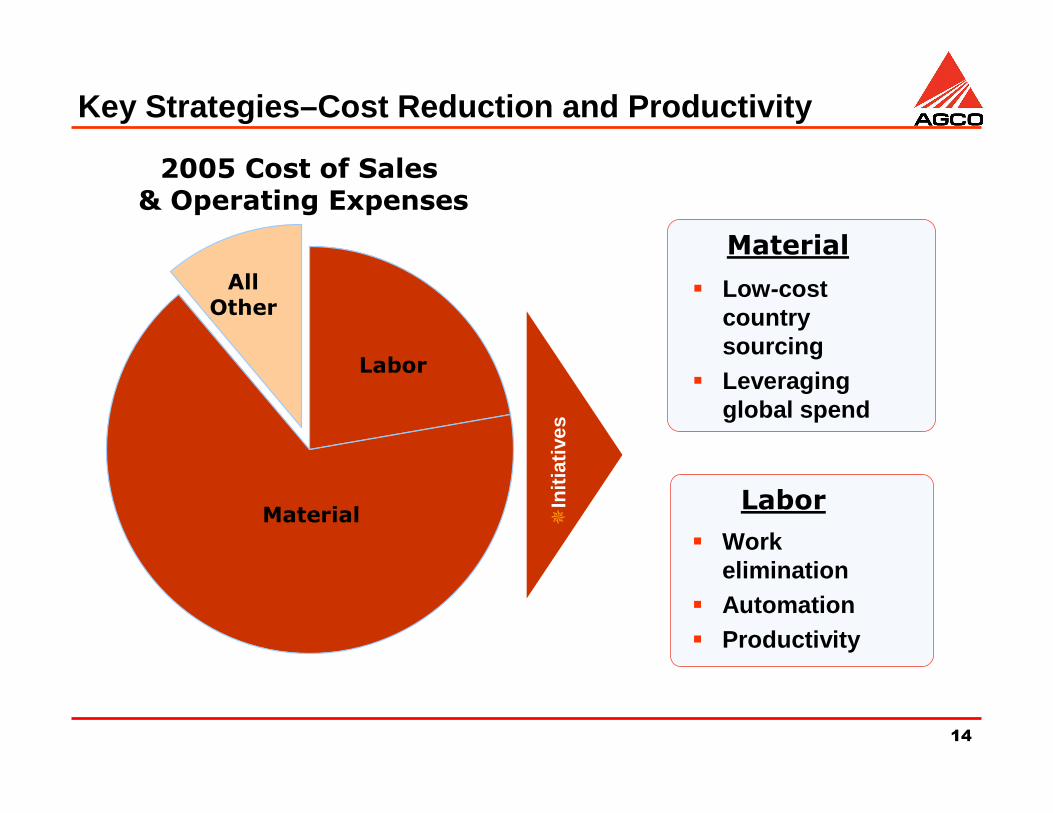

Key Strategies–Cost Reduction and Productivity

Labor

� Work elimination

� Automation� Productivity

2005 Cost of Sales & Operating Expenses

Material

� Low-cost country sourcing

� Leveraging global spend

All Other

�In

itiat

ives

Labor

Material

15

� Total AGCO Gross Margins improved slightly despite 6.9% decrease in net sales

� European sales up 13.6% vs Q105 (Excluding currency translation)

� Q1 NA focus on working capital–reduced build of dealer inventories, improved cashflow, and contributed to 18% reduction in NA Sales

� SA market continued to decline and currency impacts resulted in lower sales and margins

Q106 Results

$1,257 $1,170

Q105 Q106

17.5%17.6%

Q105 Q106

Free Cash Flow (in millions)Net Sales (in millions) Gross Margin %

Q105

Q106

Q105 Q106

($320) ($197)

16

Long Term View

Extended Global Farming Outlook

� Growing demand for larger, more productive farm equipment

� Mechanization to increase in developing countries

� Expanding demand for bio-fuels supports increased requirements for farm products

� Brazil to continue to expand global agricultural leadership

AGCO is well positioned to take advantage of long-t erm trends