Embed Size (px)

Citation preview

Ahmedabad Chartered Accountants Journal December, 2014 501

Volume : 38 Par t : 09 December, 2014E-mail : [email protected] Website : www.caa-ahm.org

Ahmedabad Chartered Accountants Journal

C O N T E N T S To Begin with

MananamHappiness........................................................................................... CA. Arvind Gaudana.................503

Editor ialSwachh Mann, Swachh Bharat!..........................................................CA. Ashok Kataria .................... 504

From the President............................................................................CA. Shailesh C. Shah.................505

Ar ticles

Exemption under the head Capital Gains - Few Beneficial Issues........CA. Manthan Khokhani &CA. Jainee Shah.........................506

Direct Taxes

Glimpses of Supreme Court Rulings................................................... Adv. Samir N. Divatia................512

From the Courts..................................................................................CA. C.R. Sharedalal &CA. Jayesh Sharedalal............... 513

Tribunal News.....................................................................................CA. Yogesh G. Shah &CA. Aparna Parelkar.................. 516

Unreported Judgements......................................................................CA. Sanjay R. Shah....................521Controversies......................................................................................CA. Kaushik D. Shah................. 523Judicial Analysis..................................................................................Adv. Tushar P. Hemani................529

FEMA & International Taxation

T.P. Implications on issue of shares to Associated Enterprise.............CA. Dhinal A. Shah.....................535

Returnee NRI - FEMA & Tax...............................................................CA. Rajesh H. Dhruva................540

FEMA Updates................................................................................... CA. Savan A. Godiawala............547

Indirect Taxes

Service Tax

Service Tax Decoded..........................................................................CA. Punit R. Prajapati................548Recent Judgements............................................................................. CA. Ashwin H. Shah...................551

Value Added TaxRecent Judgements and Updates........................................................ CA. Bihari B. Shah.....................553

Corporate Law & Others

Business Valuation..............................................................................CA. Hozefa Natawala.................555Corporate Law Update.......................................................................CA. Naveen Mandovara.............557

From Published Accounts ................................................................ CA. Pamil H. Shah..................... 559

From the Government ......................................................................CA. Kunal A. Shah..................... 561

Association News.............................................................................. CA. Abhishek J. Jain &CA. Nirav R. Choksi...................563

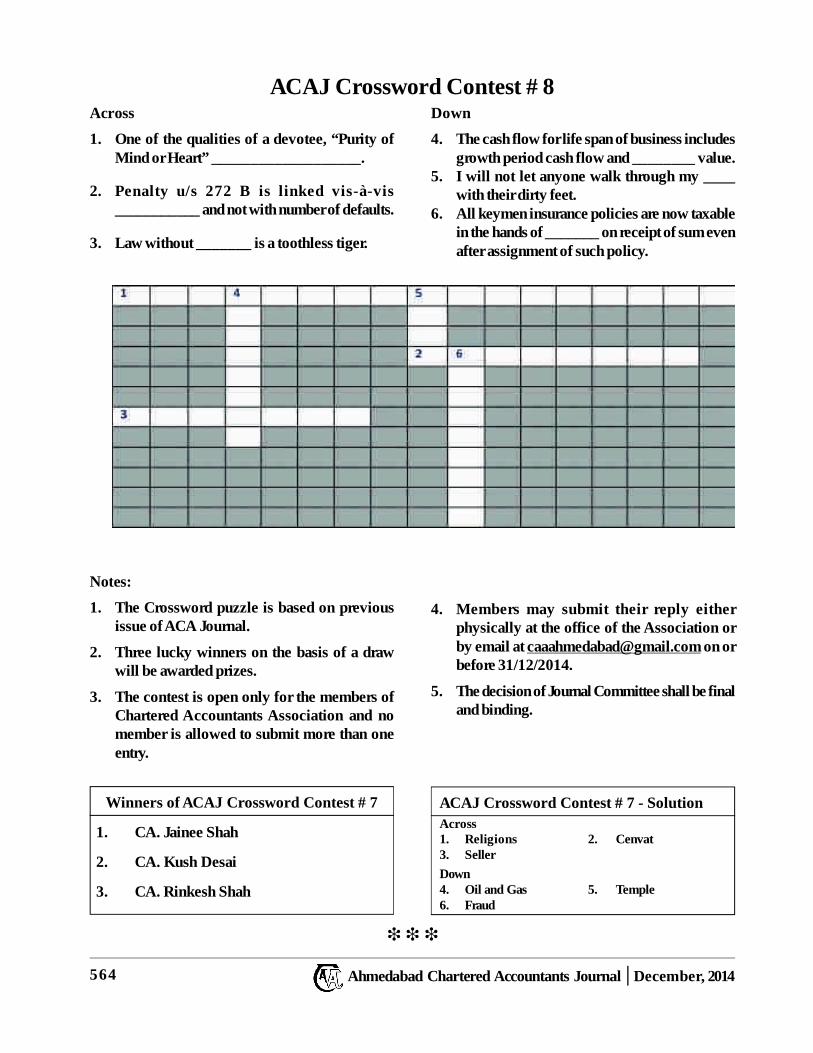

ACAJ Crossword Contest....................................................................................................................564

Ahmedabad Chartered Accountants Journal December, 2014502

AttentionMembers / Subscr ibers / Authors / Contr ibutors1. Journals are carefully posted. If not received, you are requested to write to the Association's

Office within one month. A copy of the Journal would be sent, if extra copies are available.2. You are requested to intimate change of address to the Association's Office.3. Subscription for the Financial Year 2014-15 is ` 400/-. Single Copy (if avai lable) ` 40/-.4. Please mention your membership number/journal subscription number in all your correspondence.5. While sending Articles for this Journal, please confirm that the same are not published / not

even meant for publishing elsewhere. No correspondence wil l be made in respect of Articlesnot accepted for publication, nor will they be sent back.

6. The opinions, views, statements, results published in this Journal are of the respective authors/ contributors and Chartered Accountants Association, Ahmedabad is neither responsible for thesame nor does i t necessarily concur with the authors / contributors.

7. Membership Fees (For ICAI Members)Life Membership ` 7500/-Entrance Fees ` 500/-Ordinary Membership Fees for the year 2014-15 ` 600/- / ` 750/-Financial Year : April to March

Published ByCA. Ashok Katar ia,on behalf of Chartered Accountants Association, Ahmedabad, 1st Floor, C. U. Shah Chambers, NearGujarat Vidhyapith, Ashram Road, Ahmedabad - 380 014.Phone: 91 79 27544232Fax : 91 79 27545442No part of this Publication shall be reproduced or transmitted in any form or by any meanswithout the permission in writing from the Chartered Accountants Association, Ahmedabad.While every effort has been made to ensure accuracy of information contained in this Journal,the Publisher is not responsible for any error that may have arisen.

Professional AwardsThe best articles published in this Journal in the categories of 'Direct Taxes', 'Company Law andAuditing' and 'Allied Laws and Others' will be awarded the Trophies/ Certi ficates of Appreciationafter being vetted by experts in the profession.

Articles and reading literatures are invited from members as well as from other professional colleagues.

Printed : Pratiksha Pr interM-2 Hasubhai Chambers, Near Town Hall, Ellisbridge, Ahmedabad - 380 006.

Mobile : 98252 62512 E-mail : [email protected]

Journal CommitteeCA. Ashok Kataria CA. Pitamber Jagyasi

Chairman ConvenorMembers

CA. Gaurang Choksi CA. Jayesh Sharedalal CA. Mukesh KhandwalaCA. Naveen Mandovara CA. Rajni Shah CA. T. J. Advani

Ex-officioCA. Shailesh Shah CA. Abhishek Jain

Ahmedabad Chartered Accountants Journal December, 2014 503

The ultimate goal of a human being is to be happy.Each one of us wants to be happy and try in hisown way to find happiness. Some thoughtful peoplesay leave “sansar” and “ family” and you wouldbe happy, on the other side a strong argument ismade that happiness can be achieved even whilebeing part of this “sansar” and “family”. One thingis sure that happiness is a feeling, a state of mind.We general ly are happy when we get what wedesire, and are able to keep away from what we donot desire. A simple question whether a desire ismotivator or destroyer? It depends, on the qualityof the desire and by what means you fulfil l yourdesire. Hitler had a noble desire of uniting Europebut the instrument or method used was wrong andultimately there was 2nd world war.

Let us see an illustration:

A mother is happy because she nur tures her childwithout any expectation and her love is selfless,so one can say that happiness is in “sel f lessgiving”.

Against this, if you ‘get’ whatever you want, youare happy. For example, a small chi ld wants hermother and cries… (one who cries… for God likea li ttle chi ld, he definitely feels the “sparsh” of God)and when that child realizes her mother is around,the child is happy. Likewise, a student wants goodmarks and wants admission in MBBS and with hardwork he gets i t, he is happy. A person wants tobecome Prime Minister and he becomes the PrimeMinister, he is happy. The list can be of anything orobject but in nutshell , i f desire of “getting” issatisfied, one is happy. Thus, “Happiness” is inreceiving and also as seen above, in selfless giving.However, the basic difference is that the happinessachieved on fulfil lment of desires is dependent onexternal factors on which one does not have anycontrol . Happiness achieved on ful f i l lment ofdesires is a conditioned happiness. In fact, the Lordin verse 62 and 63 of Chapter 2 of Bhagwad Gitahas warned that desires are the root cause of thedownfal l of a human being.

MananaM

Happiness Thinking about sense objects br ings an attachmenttowar ds them. Attachment breeds desire, anddesi re leads to anger, which in turn leads todelusion. When you are deluded, you lose yourmemory and with the loss of memory, the poweror di scr iminat i on i s dest r oyed; wi th thedestruction of discr imination, your Self itself islost.

How to curtai l or leave these desires or improveupon the quali ty of desires requires a very deepstudy and a powerful determination. Are there anyprinciples for being happy? Yes,

In Bhagwat Gita it is said that:

Practising Yoga will vanquish the troubles of onewho per forms his duties di l igently, and who isdiscipl ined and balanced in his eating, sleepingand working hours. (Verse 17, Chapter 6)

One can be happy if he is regular and balanced inhis food, enjoyment, working habit and sleep Withdaily abhyas (study ) one can curtai l ‘kaam’,‘krodh’, ‘Trushna’ ‘Moh’ and Maad.

Let us do our work with our best efforts, completeplanning and confidence, respect everyone, respectour society and respect our nation. Whatever taskis performed should be judged with the standardsof scriptures, have faith in Almighty and surelysuccess and happiness will be at our doorsteps.

Hard work, self discipline and helping others arethe keys for gaining success. As far as hard work isconcerned, there is no shortcut, one has to workhard, be disciplined and get rid of temptations.

Emerson said” I t is one of the most beauti fulcompensations of l ife that no man can sincerely tryto help another without helping himself. Happinessis a perfume you cannot pour on others withoutgetting a few drops on yourself”.

“One is happy as a result of one’s own efforts, onceone knows the necessary ingredients of happiness—simple tastes, a certain degree of courage, sel f-denial to a point, love of work. And above al l, aclear conscience”.

-George Sand

CA. Arvind [email protected]

Ahmedabad Chartered Accountants Journal December, 2014504

Swachh Mann, Swachh Bharat!The nation today, collectively, is trying hardto come out of the clutches of clutter, filth andmuck spread all around. The Prime Ministerof the country has initiated the campaign‘Swachh Bharat’ which was not just essentialbut in fact was long due, considering the stateof cleanliness in India. The probability of thesuccess of the initiative appears to be veryhigh for the simple reason that it is started bya person who has a great impact over themasses, especially the youth where his fanfollowing is more than anybody else in thecountry.

Di f ferent people are looking di f ferentlytowards the campaign. There are pessimistswho believe it is next to impossible to makeIndia a clean nation, and then are critics whoare busy concentrating more on persons ratherthan the idea. Third is the category of peoplewho appreciate the campaign but expect‘achhe din’ to happen on its own and lastly itis the people who are optimistic, taking onthemselves to do thei r bi t for theaccomplishment of the collective objective of‘Swachh Bharat’. The basic di f ferencebetween the last category of persons and restof the three is the mindset, their thoughts.

Generally, i t is the manner in which weapproach towards a thing makes it good orbad. To be positive it is necessary to have suchpositive attitude towards everything includingthe nation or profession. Better we have acheck on the quali ty of our thoughts weentertain or else we shall always be in thebracket of the first three categories of people.It is said that it is the quality of thoughts thatdetermine our resul t and not the action,

Editor ial [email protected]

because action is followed after a thought.The mission ‘Clean India’ is possible whenwe have a ‘Clean Mind’. It is only when wehave trained our mind, to be posi ti ve,constructive, appreciative, supportive, we canthink of having a clean India.

As a chartered accountant, to begin with, the‘Swachh Bharat’ campaign can be startedfrom our offices. Quite often we find, moreso at the time tax audits that our offices are ina state of complete mess. Why should anoffice of a professional be in such a state?Even at the times other than audits, our tablesare loaded with files and loose papers as iflying since ages. We don’t even bother to clearthe journals and mails received. It is not justabout the physical clearance of the files butthe problem is in setting our priorities in order.If we are able to set things right in throughplanning and execution, it gets reflectedphysical ly as wel l . As a benef i t, cleansurroundings always resul t in improvedefficiency.

Without a doubt, the Clean India campaign isa big task and would not be possible until allcontribute in it. It is very easy to turn a blindeye and move away but then a question arises,are we doing enough as a responsible and aneducated citizen of this great nation. It maynot be necessary to do great things but we candef i ni tely start in our own smal l way.Beginning with our home, offices and then tosurroundings, all can be achieved once weensure that we shall be living with a cleanmind!

Namaste,CA. Ashok Kataria

Ahmedabad Chartered Accountants Journal December, 2014 505

Dear Esteemed Readers

On the Independence Day, Prime Minister NarendraModi gave the slogan ‘Make in India’. The newconcept initiated by the Government of India is aprogram to promote India as a global manufacturingdestination, facili tate investment, foster innovation,and build best-in-class manufacturing infrastructure.India has already marked i ts presence as one of thefastest growing economies. Today India is rankedamong the top 3 attractive destinations for inboundinvestments and the manner in which the presentGovernment i s going about i ts foreign pol icy,investors al l round the globe seem to find a newinterest and a better opportunity.

The industrial output figures suggested that Indianmanufacturing sector is lagging behind for a longtime and thus the campaign has been perfectlytimed. The time when many global companies arelooking for an alternative to China in view of theri si ng producti ons costs, “Make i n India” i sappearing more luring to the investors. There is nodoubt that the ini tiative seeks to make India amanufacturi ng superpower and wi th thi s thegovernment is set to roll out a red carpet to globalcompanies and i nvi ti ng them to set upmanufacturing bases in India.A question arises in the minds of many people aboutthe success of the ‘Make in India’ campaign. Ireckon the probability of success is higher becauseof various and val id reasons. First of al l, India isfull of natural resources; secondly we are a countryof the youth having a large working population thatcan f i t wi th the producti ve cycle i n themanufacturi ng industry. Thi rdl y, the demandgenerated by the population of more than 1 bill ion.Lastly, the government’s willingness to support themanufacturing sector is a big strength that canchange the approach and atti tude of theindustrialists. If this sector develops it can cater tothe demand of various i tems that are importedimproving balance of foreign currency inflow andoutflow and can also boost e-commerce that is fasttaking over f rom the tradi ti onal methods ofbusiness. The biggest advantage that e-commerce

From the PresidentCA. Shailesh C. Shah

offers, is that it has a lot of variety to offer to theconsumer as compared to a physical store, since itdoes not have any constraints of physical space.

Make in India campaign of the Government wouldresult in increase in inbound investment, which inturn wi l l i ncrease the demand of CharteredAccountants. Assuming the success of the Make inIndia campaign I hope it will open up new avenuesfor the Chartered Accountants. With the openingup of new manufacturing industries the CharteredAccountants wi l l have new j ob opportuni ties.Similarly those who are in practice will have newavenues as advisor in the field of investment ,valuati ons, mergers and acquisi tion , transferprici ng, corporate law, securi ti es law, foreignexchange , management consultancy etc. Time willtell whether the India wil l become a super power inthe coming years as imagined by many includingour Prime Minister Narendra Modi or not but theprofession of chartered accountancy, for sure, wouldbe the largest beneficiary.

At the Association, with a view to have in depthstudy and proper understanding of how to submitdetai ls before the assessing officer, an intensivestudy program on the topi c of Income TaxAssessment Proceedings was organised, spreadingover 4 sessions. Al l the participants thoroughlyenjoyed, appreciated and actively participated inthe course. The detai ls of the forthcoming eventsare given in the Association news. This year’s sloganof the Association is ‘nurturing knowledge –fostering fellowship.’ Various educational programshave been organized till now to nurture knowledge.Now it’s time to foster fellowship. The Associationhas for the first time organized cricket tournamentwith tennis bal l so as to enable senior membersparticipate, apart from the regular cricket matchesthat are held over the years. All members are invitedto take part in the activities of the Association.

With regardsCA. Shailesh C. ShahPresident

Ahmedabad Chartered Accountants Journal December, 2014506

1. Introduction

This article encompassing current issues inCapital Gains has been drafted consideringvarious pronouncements of Courts and IncomeTax Appellate Tribunals delivered recently. Theauthors have tried to meticulously analyze theprovisions and explain the relevant issueshoping that this would help the readers inmaking proper representation in the ongoingassessment proceedings. This article would beof great help and assistance to the practicingprofessionals and readers.

2. Issues ar ising under Section 54

2.1 Whether Exchange of old flat for a new flatunder a development agreement amountsto construction and thus extended time limitof 3 years is applicable?

Redevelopment of properties has become quitecommon off late. In such a situation, theassessee exchanges his old flat for a new flat inthe redevelopment scheme. In such a situation,the exchange amounts to transfer within themeaning of section 2(47) of the Act.

The issue that emerges for consideration is thatwhether the new flat acquired by the assesseequalifies as investment for the purpose ofclaiming exemption u/s. 54 of the Act?

The department has in several cases taken astand that acquisi ti on of f lat under thedevelopment agreement does not amount topurchase or construction within the meaningof section 54.

It is pertinent to note that whenever an assesseepurchases a flat from a builder as a part ofconstruction project, it amounts to construction

and not purchase. Similarly what happensunder a redevelopment agreement is that theassessee exchanges the old flat for a new flatto be constructed by the builder. Thus, such atransaction would amount to construction onlyand time limit of 3 years would be applicable.

Similar view has also been adopted In the caseof Jatinder Kumar Madan v/s ITO (I .T.A.No. 6921/Mum/2010) and Smt. Veena GopeShroff Vs. ITO [2013] 33 taxmann.com 344(Mum- Tr ib

Further, for the benefit of readers, it is herebyclarified that in such circumstances the FairMarket Value of the new house shal l beconsidered as the full value of considerationfor the sale of old house.

2.2 Can Capital Gain ar ising out of sale ofmultiple flats be invested in multiple flats toavail exemption u/s. 54?

Section 54 differs from the provisions of section54F on a point that under Section 54F, theexemption will not be available when theassessee owns more than one residential houseother than the new asset on the date of transferof the original asset.

However, Section 54 of the Act provides nosuch condition. There is no restriction placedanywhere in the Section 54 that exemption isavai lable only in relation to sale of oneresidential house. Therefore, in case theassessee has sold two residential houses, beinglong-term assets, the capital gain arising fromthe second residential house is also a capitalgain arising from the transfer of a long-termasset being a residential house. The provisionof Section 54 therefore will also be applicable

CA. Manthan [email protected]

Exemption under thehead Capital Gains –Few Beneficial Issues

CA. Jainee [email protected]

Ahmedabad Chartered Accountants Journal December, 2014 507

Exemption under the head Capital Gains – Few Beneficial I ssues

to the sale of second residential house andsimilarly to a third residential house and so on.Whenever the exemption available is restrictedto one asset, a suitable provision is incorporatedin the relevant section itself.

Thus in a case, there is sale of more than oneresidential house, the exemption wi l l beavailable in relation to each set of sale andcorresponding investment in the residentialhouses.

However, the exemption is not available onan aggregate basis but has to be computedconsidering each sale and the correspondingpurchase adopting a combination beneficial tothe assessee.

The said view also finds support from thedecision rendered in the case of Rajesh KeshavPillai V. ITO (ITA No 6661/M/2009) (Mum-Tr ib)

Note:

At present, when one house is sold andproceeds are invested in multiple houses whichare adjacent to each other, the exemption u/s.54 is available, having regard to the decisionrendered in the case of Ananda Basappa.However, after the amendment brought out byFinance Act 2014, such exemption is notavailable. Now, exemption is available inrespect of investment in one house only.However, i t is clarified that the decisionrendered in the case of Rajesh Pillai (Supra)would still hold good in a case when multipleflats are sold and consideration is invested inmultiple flats. What is proposed to be coveredby the amendment is a situation when a singleflat is sold and investment is made in multipleflats.

3. Issues ar ising u/s. 54EC

3.1 Whether fict ion created by Section 50extends to Section 54EC?

The issue that arises many times is that whetherthe exemption available under Section 54ECof the Income Tax Act is also available inrespect of short term capital gain arising fromthe transfer of ‘long term capital asset’ in wakeof deeming fiction created under Section 50 ofthe Act?

For the purpose of claiming exemption undersection 54EC there should be a transfer of longterm capital asset. Now, what is contemplatedby section 50 is that the gain on transfer oflong term capital asset being a depreciable assetshall be shor t term in nature. The fiction ofSection 50 by no means converts the long termcapital asset into a short term capital asset.

The Gujarat High Court has in the case of CITVs. Adi tya M edisales L td. (2013) 38taxmann.com 244 (Gujarat) held that thereis nothing in Section 50 to suggest that thefiction created in Section 50 is not onlyrestricted to Sections 48 and 49 but also appliesto other provisions. On the contrary, Section50 makes it explicitly clear that the deemedfiction created in sub-sections (1) and (2) ofSection 50 is restricted only to the mode ofcomputation of capital gains contained inSections 48 and 49. Secondly, i t is well-established in law that a fiction created by theLegislature has to be confined to the purposefor which it is created.

Thus, Section 54EC being an independentsection will not be bound by the provisions ofSection 50. The depreciable asset, if held formore than 36 months, shall be a long termcapital asset as per the provisions of section2(29A). Therefore, the exemption u/s. 54ECcannot be denied on account of fiction createdby section 50

3.2 Remedy to the Assessee if NHAI/REC bondsare not available at any point of time duringthe per iod of six months fr om date ofTransfer.

Ahmedabad Chartered Accountants Journal December, 2014508

Section 54EC provides exemption from longterm capital gain arising from transfer of a longterm capital asset, provided investment is madein the specified bonds within 6 months fromthe date of transfer.

There may arise a si tuation wherein theassessee wishes to invest in the specified bondsi.e. NHAI and REC but subscription to thosebonds might not be open at the time when theassessee chooses so. In such a situation, thedelay in investment is not due to fault ofassessee but for the fact that the bonds are notavailable.

The High Court of Bombay has in the case ofCIT Vs. Cello Plast (ITA Nos. 3731 of 2010)(Bom.) held that the assessee is entitled to waittill the last date to invest in the bonds. Even ifthe bonds are available for a part of periodduring the 6 months from the date of transfer,but not as on the expiry of 6 months’ period itmakes no di f fer ence because theassessee�s r ight to buy the bonds upto thelast date cannot be prejudiced.

I t i s observed that Lex not cogi timpossibila (law does not compel a man to dothat which he cannot possibly perform)and impossibilum nulla oblignto est (law doesnot expect a party to do the impossible) are wellknown maxims in law.

The High Court has held that in such a case,an assessee would be entitled to a reasonableextension which must then be decided,depending upon the facts of each case. Further,the assessee cannot be forced to purchasealternative bonds if a particular bond is notavailable since 54EC confers a choice investingeither in the REC bonds or the NHAI bonds.

3.3 Definition of ‘month’ for the purpose ofSection 54EC

Sections 54E, 54EA, 54EB & 54EC requirethe investment to be made “within a period ofsix months after the date of such transfer”. The

subtle question is that whether the word“month” refers in this section a period of 30days or it refers to the month only. This phrasehas otherwise not been used by the legislatorin any other provisions of IT Act, 1961 or ITRule, 1982

The term ‘month’ is not defined in The IncomeTax Act. According to Section 3(35) of theGeneral Clauses Act, 1897 month means amonth reckoned according to the Br itishcalendar .

The question that emerges is whether “month”means a “lunar month” or a “calendar month”.The meaning would depend on intention forthe usage of the term “month”. In BritishCalendar a month is a unit of period used in aCalendar. It may not be out of context tomention that this system was invented byMesopotamia.

An average length of a month is 29.53 days;but in a calendar year there are 7 months with31 days, 4 months having 30 days and onemonth has 28/29 days. It can be possible thatunder common parlance probably it meant alunar month but in calculating the specifiednumber of months that had elapsed afteroccurrence of a specified event then a GeneralRule is that the period of a month ends on thelast day. Therefore, a month ends by the lastdate of that month. .

The Special Bench of Ahmedabad ITAT hasin the case of Alkaben P. Patel (ITA Nos.1973/Ahd/2012) held that in the absence ofany definition of the word ‘month’ in the Act,the definition of General Clauses Act 1897 shallbe appl icable and hence the period ofinvestment of six months for the purpose ofSection 54EC should be reckoned from the endof the month in which transfer of capital assettakes place. Similar view has been taken in thecase of Yahya E. Dhar iwala, 49 SOT 458(Mum) and Aquatech Engineers, 36 CCH167 (Mum Tr ib.),

Exemption under the head Capital Gains – Few Beneficial I ssues

Ahmedabad Chartered Accountants Journal December, 2014 509

3.4 Whether the time per iod of six months is tobe reckoned from date of transfer or receiptof consideration?

Section 54EC requires the assessee to investthe consideration received on transfer of capitalasset in specified bonds in order to availexemption from the capital gains earned.

However, there may arise a situation when theconsideration for sale of capital asset is receivedsubsequently, after the sale of capital asset. Insuch a case, a question arises as to whether theperiod of 6 months for the purpose ofinvestment u/s. 54EC is to be reckoned fromthe date of transfer of the asset or from the receiptof consideration.

Section 54EC requires the assessee to makethe investment within 6 months from the dateof transfer. Thus, if the language of the sectionis strictly construed, the assessee is required toinvest the consideration within 6 months fromdate of transfer even if the consideration isreceived several months after the date of transfer.

However, if the period of 6 months is reckonedfrom the date of transfer, then it would lead toan impossible situation by asking assessee toinvest money in specified asset before actualreceipt of the same.

This view also finds place in various judicialpronouncements. The Hon’ble Andhra PradeshHigh Court has in the case of S. Gopal ReddyVs. CIT (1990) 181 ITR 378 (AP) observedthat under the provisions of section 54E of theAct, what is to be invested in specified assets is“the consideration or any part thereof” andunless the consideration is received, or accrues,there is no question of investing it.

Few supporting decisions for the aforesaidproposition are CIT Vs. Janardhan Dass (latethrough legal heir Shyam Sunder) (2008) 299ITR 210 (All) and Chanchal Kumar SircarV. ITO (2012) 50 SOT 289 (Kol.)

3.5 Whether the exemption u/s. 54EC is to beconsider ed befor e claiming set off ofbrought forward capital loss or after?

The basic issue under consideration is whetherexercise of setting off of brought forward long-term capital loss is to be done before claimingdeduction under Section 54EC or post set offof such loss.

A joint reading of the provisions of section54EC and Section 74 would demonstrate thatthe exercise of setting off of the carried forwardcapital loss u/s. 74 is to be undertaken once theincome under the head capi tal gains iscomputed. Now in order to compute the incomeunder the head capital gains, exemption u/s.54EC ought to have been provided.

Hence, exemption u/s. 54EC is to beconsidered before claiming set off of broughtforward capital loss.

The decisions of courts and tribunals adoptingthe above view are Tata Power Co. L td V.Addl CIT (2011) 47 SOT 470 (Mum.) andCIT Vs. Vijay M. Mahataney (2013) 92 DTR180 (Mad.).

4. Issues ar ising u/s. 54F

4.1 Whether exemption u/s. 54F is available ifconstruction is not fully completed within 3years or sale deed is not executed within thestipulated period?

There may arise a si tuation wherein theassessee starts the construction of the house butthe construction could not be completed withinthe stipulated time period of 3 years. In such acase, the department normally takes a stand thatassessee shall not be entitled to a deductionu/s. 54F since the construction is not complete.

However, one has to bear in mind that S. 54Fis a beneficial provision for promoting theconstruction of residential house & requires tobe construed l iberally for achieving thatpurpose. The intention of the Legislature was

Exemption under the head Capital Gains – Few Beneficial I ssues

Ahmedabad Chartered Accountants Journal December, 2014510

to encourage investments in the acquisition/construction of a residential houseand completion of construction or occupationis not the requirement of law.

The words used in the section are ‘purchased’or ‘constructed’. The condition precedent forclaiming benefit u/s 54F is that the capital gainshould be parted by the assessee and investedeither in purchasing a residential house or inconstructing a residential house.

If after making the entire payment, merelybecause a registered sale deed had not beenexecuted and registered in favour of the assesseebefore the period stipulated, he cannot bedenied the benefit of section 54F of the Act.Similarly, if he has invested the money inconstruction of a residential house, merelybecause the construction was not complete inall respects and it was not in a fit condition tobe occupied within the period stipulated, thatwould not disentitle the assessee from claimingthe benefit under section 54F of the Act

The above issue has also directly been coveredin favour of assessee by the following decisionof the Madras High Court in the case of CITv. Sardarmal Kothar i [2008] 302 ITR 286and of the the Karnataka High Court in thecase of CIT V. Sambandam Udaykumar(2012) 251 CTR 317 (Kar.).

4.2 Deduction u/s. 54F in case of joint names indeed of purchase

As a matter of common practice in our country,property is generally purchased in joint namesof family members. In such a situation, an issuearises as to whether only proportionatededuction i s avai lable to the assesseeparticularly when the co owner is merely aname lender and the payment is fully made bythe assessee under section 54F.

It is pertinent to note here that Section 54Fmandates that the house should be purchasedby the assessee. However it does not stipulate

that the house needs to be purchased in the nameof the assessee.

Such view has been affirmed in the decisionsrendered in the case of CIT Vs. Gurnam Singh(2010) 327 ITR 278 (P& H), Jt. CIT vs. Smt.Armeda K. Bhaya (2006) 99 TTJ 358, ITAT,Mumbai Bench and CIT vs. Kamal Wahal(2013) 351 ITR 4 (Del.),

Thus based on the above decisions, it seemsclear that mere inclusion of family member’sname in the purchase deed does not disentitlethe assessee from claiming exemption u/s. 54F.Exemption would be available to the assesseewhose funds have been used for the purposeof investment.

4.3 Can consideration ar ising out of sale ofmultiple assets be invested in a single assetfor the purpose of Section 54F?

Kindly consider the following situation. Mr. Xhas earned Long Term Capital Gains of Rs. 2cr., 3Cr. And 1 cr. For the AY 2010-11, 2011-12 and 2012-13 respectively. However, heinvests a sum of Rs. 8 crore for purchase a singleflat in AY 2011-12 and claims exemption fromthe Capital Gains earned for all three AY i.e.2010-11, 2011-12 and 2012-13. Can he do so?

Section 54F allows the assessee exemptionfrom long term capital gains provided hepurchases a residential house one year beforeor two years after the date of transfer of theasset.

The Mumbai Bench of ITAT has in the case ofSmt. Anagha Aj it Patnekar V. ITO (2006) 9SOT 685 (Mum.) held that from the languageof this section, legislature has provided leverageto the assessee for claiming deduction underSection 54F in the sense that assessee can buythe property first and claim deduction later oni.e., within one year or can have capital gainfirst and can claim deduction within two yearsby purchasing the residential flat.

Exemption under the head Capital Gains – Few Beneficial I ssues

Ahmedabad Chartered Accountants Journal December, 2014 511

Therefore, in respect of residential proper tytill cost of purchase of flat is exhausted bythe claim of the capital gain deductioncannot be denied. Sub-section (4) has beeninserted with a view to facilitate the assessee toclaim the capital gain exemption when assesseeopts for purchase of flat after arising of thecapital gain and deposit the sale considerationin the bank account till such appropriation.

The assessee cannot be expected to appropriatethe sale consideration in respect of the alreadypurchased flat. If such interpretation is accepted,it will frustrate the object of the provisions of s.54F and lead to absurdity.

Thus, from the aforesaid judgment of theMumbai ITAT it can be stated that there is nobar in Section 54F for claiming deductionsecond or third time for the same property, ifthe capital gain which has arisen in the case oftaxpayer is within the cost of the property.

5. Capital Gain on Retirement of Par tners

5.1 Whether cash received by par tners onretirement is taxable u/s. 45(4) par ticular lywhen par tners had brought cash at the timeof admission, which is used by the Firm topurchase a proper ty?

There may arise a situation when at the time ofretirement, the retiring partner is paid cashequivalent of his share in the partnership firm.The question that arises is whether in such asituation, section 45(4) can be invoked or not?

It has now been well settled that section 45(4)would be applicable in case of dissolution ofthe firm as well as at the time of retirement ofthe partner from the firm.

Following conditions are required to attractSection 45(4)

o There should be a distribution of capitalassets of a firm

o Such distribution should result in transferof a capital asset by firm in favour of thepartner

o on account of the transfer there should bea profit or gain derived by the firm

o such distribution should be on dissolutionof the firm or otherwise

When the firm gives money equivalent of hisshare to the partner on retirement, the firm doesnot transfer any property. Thus section 45(4) isnot attracted at all. This has been held in thecase of CIT V. Riyaz A. Sheikh (ITA No.1969 of 2011) (Bom.)

Further, there may be a situation in which theold partner who had brought property at thetime of admission to the firm retires afterintroduction of new partners and takes themoney value of his share in the firm. In such acase it cannot be said that the said transactionis a device adopted to transfer the immovableproperty to the new partners. The propertybelongs to the partnership firm and not to thepartners. The partners only have a share in thepartnership asset. When they retire they arenot relinquishing their interest in the immovableproperty of the firm. What they relinquish istheir share in the partnership. Therefore, thereis no transfer of a capital asset and no capitalgains or profit arises. The said view also findssupport from the decisions rendered in the caseof ITO Vs. M/s. Dynamic Enterpr ises, (ITANo. 1414/2006 Kar. HC)

6. Conclusion

The subject of Capital Gains is never endingand illimitable. The authors hope that the viewsdiscussed above shall help the readers inhandling the problems and issues arising duringthe course of assessment.

❉ ❉ ❉

Exemption under the head Capital Gains – Few Beneficial I ssues

Ahmedabad Chartered Accountants Journal December, 2014512

Glimpses of SupremeCourt Rulings

Advocate Samir N. [email protected].

Negotiable I nst r uments Act, 1981-Offence of cheque dishonor

Section 138 of NI Act r.w.s. 177 of CrPC leavesno manner of doubt that the return of the chequeunpaid by the drawee bank alone constitutes thecommission of the offence of cheque dishonor andindicates the place where the offence is committed.The Parliament in its wisdom considered it just andproper to give to the drawer of a dishonouredcheque an opportunity to pay up the amount beforepermitting his prosecution, no matter the offence iscomplete the moment the cheque was dishonoured.

A coordinate Bench is bound to fol low thepreviously published view; it is certainly competentto add to the precedent to make it logically anddialectically compelling. However, once a decisionof a larger Bench has been delivered it is thatdecision which mandatorily has to be applied;whereas a coordinate Bench,, in the event that itfinds itself unable to agree with an existing ratio, iscompetent to recommend the precedent forreconsideration by referring the case to the ChiefJustice for constitution of a larger Bench.

Dashrath Rupsingh Rathod vs. ST. OfMaharashtra (2014) (9 SCC 129)

ESI Act , 1948- M eaning of Shop,establishment

The term “shop”, again, has not been defined inthe ESI Act. Therefore, the meaning assigned tothis word in dictionaries may be noticed. It can besaid that a “shop” is a business establishment wherea systematic or organized commercial activity takesplace with regard to the sale or purchase of goodsor services, and includes an establishment thatfacilitates the above transaction as well.

“Entertainment” is an activity that provides withamusement or gratification. Further, i t wouldinclude public performances, including games and

sports. Therefore, it can be said that horse racing isindeed a form of entertainment.

Every word of a language is flexible to connotedifferent meanings when used in different contexts.That is why it is said that words are not static, butdynamic and the court should adopt the dynamicmeaning which upholds the validity or scheme ofany legislation.

Bangalore Turf Club Limited vs. Regional Dir.ESIC (2014) (9 SCC 657)

Cour ts, Tr ibunals and Judiciar y-Judicial Process-Recusal by Judge.

A Judge is to decide every dispute in consonancewith law. If one is not free to decide in consonancewith his will, but must decide in consonance withlaw, the concept of a Judge being individualpossessing power and authority is but a delusion.

Correction of a wrong order would never putanyone to shame. Recognition of a mistake, and itsrectification, would certainly not put the presentBench to shame. The embarrassment would onlyarise when the order assailed is actuated by personaland/or extraneous considerations, and the pleadingsrecord such an accusation.

The oath of office of the Supreme Court requiresthe Bench to discharge its obligations, without fearor favour. The Supreme Court therefore alsocommends to all courts, to similarly repulse allbaseless an unfounded insinuations [of bias], unlessof course, they should not be hearing a particularmatter, for reasons of their direct or indirectinvolvement. The benchmark that justice must notonly be done but should also appear to be done,has to be preserved at all costs.

What is a Judge is taught during his arduous andonerous journey to the Supreme Court is, that hiscalling is based on the faith and confidence reposed

27

28

29

contd. on page no. 520

Ahmedabad Chartered Accountants Journal December, 2014 513

CBDT Ci r cular s : T ime l imi t forselecting cases for Scrutiny assessment.Amal kumar Ghosh v/s. Asst. C.I .T.(2014) 361 ITR 458(Cal).

Issue:

Whether circulars are binding to Department?

Held:

CBDT issued circulars No.9 and 10, i .e. forCorporate/Non Corporate assesses for scrutinyselection.

Circular No. 9 reads as under :-

“The process of selection of cases for scrutiny ofreturns fi led up to March 31, 2004 must becompleted by October 15, 2004. For returns filedduring the current financial year 2004-2005, theselection of cases for scrutiny will have to becompleted within three months of the date of filingof the Return.”

When Return was filed on October 29, 2004 andthe case was selected for scrutiny on July 6, 2005,on challenge by the assessee, High Court has heldas under:

(i) Even assuming that the intention of the CBDTwas to restrict the time for selection of the casefor scrutiny to a period of three months, it couldnot be said that the selection in the case of theassessee was made within the period. Thereturn was filed on October 29, 2004 and thecase was selected for scrutiny on July 6, 2005.By any process of reasoning, it was not opento Tribunal to come to a finding that theDepartment acted within the four corners ofCircular No.9 & 10 issued by the CBDT. Thecirculars were evidently violated. The circularswere binding upon the Department u/s. 119.

CA. C. R. [email protected]

(ii) That even assuming that the circulars were notmeant for the purpose of permi tti ngunscrupulous assessees from evading tax, itcould not be said that the Department which isa State, can be permitted to selectively applystandards set by itself for its own conduct. Whenthe Department has set down a standard foritself the Department is bound by that standardand cannot act with discrimination. If it doesthen the act of the Department is bound to bestruck under Article 14 of the Constitution. Inthe facts of the case, it was not necessary todecide whether the intention of the CBDT wasto restrict the period of issuance of notice fromthe date of filing the return laid down u/s.143(2). Thus, the notice u/s. 143(2) was not inlegal exercise of jurisdiction.

Section 271 (1) (c) Explanation 1 :Requirements - CIT v/s. ManjunathaCotton & Ginning Factory (2013) 263CTR 153 ( Kar ): (2013) 359 ITR 565(Karn)

Issue:

What are the requirements for levy of penalty u/s.271 (1) (c)?

Held :

After insertion of Explanation 1 to Section 271(1)(c), the law on concealment and penalty has becomestiffer. The explanation as it stands now is acomplete code having the following features:

(1) Every dif ference between reported andassessed income needs an explanation.

(2) If no explanation is offered, levy of penaltymay be justified.

From the Courts

CA. Jayesh C. [email protected]

57

58

Ahmedabad Chartered Accountants Journal December, 2014514

(3) If explanation is offered but is found to be false,penalty will be exigible.

(4) If explanation is offered and it is not found tobe false, penalty may not be leviable. - if

(a) Such explanation is bonafide,

(b) The assessee has made available to theA.O. al l the facts and material snecessary in computation of income.

Therefore the Explanation I, understood in theproper context in particular, Clause (c) of Sub. Sec.(1) of Sec. 271 makes the intention of the legislaturemanifest. It clearly sets out when penalty is leviableand when penalty is not leviable. The conditionprecedent for levying the penalty is the satisfactionof the authority that there is concealment ofparticulars of the income or inaccurate particularsare furnished to avoid payment of tax.

Bur den on assessee and burden onDepar tment: Income Tax Act. Sec.68 -C.I .T. v/s. Smt. Sanghamitra Bharali(2014) 361 ITR 481 (Gauhati) [Thisdecision does not appear in CTR DVD]

Issue :

In Income-tax Act, for taxing Income what is theburden on Assessee and on Department?

Held :

In all cases in which receipt is sought to the taxedas income, the burden lies on the Revenue to provethat it is within the taxing provision; but once thatburden is discharged, the burden of proving that itis not taxable, because it falls within exemptionprovision under the I.T. Act. 1961, lies on theassessee. If the explanation offered by the assesseeabout the nature and source thereof, is, in theopinion of the A.O. not satisfactory and there areevidences and circumstances pointing out to theeffect that what has been shown was not real and ifthe assessee fails to contradict such facts andcircumstances, then such acts and circumstancescan certainly be used against the assessee to holdthat the receipt was in the nature of income.

In order to establish the receipt of cash credit asrequired u/s. 68, the assessee must satisfy threeimportant conditions:

(i) The identity of the creditor;

(ii) The genuineness of the transaction and,

(iii) The financial capability of the person givingthe cash credi t to the assessee i .e. thecreditworthiness of the creditor.

However, the onus of the assessee is limited to theextent of proving the source from which hereceived the cash credit. The creditworthiness ofthe creditor is to be judged vis-à-vis the transactionwhich had taken place between the assessee andthe creditor, and it is not the burden of the assesseeto find out the source or creditworthy capacity inorder to prove genuineness of transaction.

Capital Gain of depreciable assets andSection 54 EC. - C.I .T. v/s. Adi tyaMedisales L td. (2014) 266 CTR 98 (Guj)[This decision does not appear in CTRDVD]

Issue :

Whether relief of investment u/s. 54 EC is availablefor short term capital gain of long term depreciablecapital asset?

Held :

Capital gain of depreciable capital asset ifinvested in specified asset, exemption u/s. 54 ECcannot be denied only on account of the fact thatdeeming fiction is created u/s. 50 of the I.T. Act.Legal fiction created under u/s. 50 is thoughrestricted to computation of capital gains, suchdeeming fiction cannot restrict application of Sec.54 EC which allows exemption of capital gain, ifassessee makes investment in specified assets. Thus,the assessee cannot be charged to capital gains whenshort term gain of long term capital assets getinvested, in the assets specified under the law.

From the Cour ts

59 60

Ahmedabad Chartered Accountants Journal December, 2014 515

Waiver of loan amount by Bank: Section41(1) does not apply - C.I.T. v/s. Dholgir iIndustr ies Pvt. L td. (2014) 266 CTR111 (MP)

Issue :

When Bank has waived loan taken, whetherprovision of Sec. 41(1) would apply for taxing thatamount?

Held :

The A.O. has committed error in treating the amountwaived by the bank to be amount earned by theassessee. The principle amount of loan being neverclaimed by the assessee as its expenditure, itswaiver will not amount to income of the assesseeand as such there is no infirmity in the orders passedby CIT (A) and I.T. A.T. in considering the amountas non-taxable and hence addition is not proper.

Section 14 A and availability of interestfree funds - C.I.T. v/s. Gujarat NarmadaValley Fer ti lizer Co. L td. (2014) 221Taxman 479 (Guj)

Issue :

Whether when interest free funds are available forinvestment in shares and UTI from which dividendis received, application of Sec. 14 A is proper?

Held :

The A.O. disallowed the interest expenditure onthe ground that as per the provisions of Sec. 14Athe expenditure in terms of investment whichpertained to the exempt income from interestbearing funds was not allowable.

On appeal the CIT (Appeals) held that the dividendincome was earned out of the investment made inthe earlier years. The assessee company had hugeshare capital and reserves and surplus, which didnot carry any interest. No disallowance was madeon the interest expenditure made in past and theA.O. could not establish any nexus between interestbearing borrowing and investment from whichexempt income was earned. He, therefore, deletedthe disallowance made by the A. O.

From the Cour ts

On second appeal the Tribunal held that no freshinvestment was made by the assessee during theyear under consideration. As per the Balance Sheetof the assessee huge interest free funds in the formof capital, reserves and surplus to the tune ofRs.84.45 Lakhs were available. Whereas investmentwas made only to the extent of Rs.22.70 Lakhs. Ittherefore, upheld order of CIT (Appeal).

High Court held that both the authorities below hadcorrectly approached the issue by setting aside theorder of disallowance under Sec. 14A of the Act,in respect of interest expenditure. When the verybasis for employing Sec. 14-A of the Act. on factualmatrix is lacking, the disallowance to the extent of10% of dividend income was not permissible.

Taxabi l i ty: Lack of taxable event -Chimanlal and Sons v/s. C.I.T. (2013) 353ITR 344 (Guj) : (2014) 221 Taxman 174(Guj .) (Mag.)

Issue:

Subsidy received long back by the firm, which istransferred to partners accounts can be taxable?

Held :

Assessee received subsidy from State Governmentin the year 1995. Since then such subsidy had beenreflected in firm’s Balance Sheet in subsidyaccount. During I.T.A.Y. 2004-05 such amount wastransferred to partners’ capital accounts makingreserve and subsidy nil and correspondingly,partners’ capital was increased by such amount.Consequently, assessment was sought to bereopened to examine taxability of such receipt. Sinceno taxable event did arise during the year underconsideration, mainly because assessee changednature of treatment for accounting purpose, it wouldnot permit revenue to examine taxability of suchreceipt in I.T. A.Y. 2004-05 and thus reassessmentlacked validity.

❉ ❉ ❉

62

63

61

Ahmedabad Chartered Accountants Journal December, 2014516

M.Dinshaw & Co. (P.) L td. v. DCIT 150ITD 342 (Mum.) Assessment year : 2004-05 Order Dated: 14th July, 2014

Basic Facts

The assessee paid vehicle tax on purchase ofvehicle under Bombay Motor Vehicles Tax Act,1958. Vide an amendment to the said act, effective1995, the annual tax was converted into a one-timetax, so that it was required to be paid once duringthe life time of a vehicle, at the time of its purchase.The assessee’s contention was that the amendmentwould, however, not alter its character. The vehicletax under the pre-amended Act was beingcontinuously and undisputedly allowed as revenueexpenditure. The same would continue to be so in-as-much as a lump sum levy, for administrativereasons, would not change the nature of theexpenditure from revenue to capital. The revenueauthorities rejected assessee’s explanation andconcluded that payment is a part of cost of thevehicle to the assessee, a capital asset in its hands,and would accordingly form part of its cost.

Issue

Whether one time vehicle tax paid by assesseeis capital expenditure exigible to depreciationas against being revenue expenditure deductibleu/s 37?

Held

The matter that the motor car on which theimpugned tax stands paid are capital assets inassessee’s hands intended for primary use if notwholly, in Maharashtra, is not in dispute. It is amplyclear that the tax is under law applicable on motorcars or omnibuses registered in the State ofMaharashtra, as one time tax for the life of vehicle.Further, the tax is for user, active or passive of themotor vehicle in the territory to which the jurisdictionof the said Act extends i.e. the state of Maharashtra.

The Tribunal held that Section 43(1) which definesthe term ‘actual cost’, does not define it negatively,i.e., emphasizing the elements which would notform a part thereof, so that the principles ofcommercial accounting shall apply in determiningthe actual cost. The same is even otherwise tritelaw, so that in the absence of a statutory definitionor mandate, the accounting prescription shallprevail. It is only where the law specifically providesfor a particular course of action, inconsistent withthe accounting mandate, that the same shall prevailand override the latter, viz., section 43B. TheAccounting Standard (AS) in respect of accountingfor fixed assets, i.e., AS-10, issued by the Instituteof Chartered Accountants of India, defines ‘fixedasset’, also laying down the principles for itsvaluation (cost) or determining its cost. Therefore,the payment of tax which enables the vehicle beingput to its intended use represents a condition thereofand accordingly shall form a part of its cost. Themisconception arises as the assessee, in its mind,and without basis, links the provisions of the saidAct as it stood prior to the amendment of 1995 withthat as amended. There is nothing in law, as itstands, to suggest that the levy is in lieu of a seriesof annual payments. In fact, the amendment/s hasthe effect of altering the nature of the levy in-as-much as the pre-amended tax could be regarded asan annual charge for the user of the vehicle for oneyear at a time.In view of the above the tribunal heldthat the tax levied by the said act would form partof actual cost of the motor cars.

JSW Energy L td. v. ACIT 140 I TD406(M um) Assessment Year : 2005-06Order dated: 30th Apr il, 2013

Basic Facts

In the instant case, the assessee had set aside out ofthe profits Debenture Redemption Reserve andclaimed the same as deduction while computing

CA. Yogesh G. [email protected]

Tribunal News

CA. Aparna [email protected]

49

50

Ahmedabad Chartered Accountants Journal December, 2014 517

profits u/s 115JB of the Act. The revenue held thesame to be reserve as appropriation of profits andnot ‘provision’ for meeting liability while computingthe profits u/s 115JB.

Issue

Whether amount set aside as ‘Debentur eRedemption Reser ve’ is deductible whi lecomputing book profits under MAT?

Held

Debenture is a loan liability i.e. borrowed capitalof the entity raising funds through the issue ofdebentures. The said liability is classified as asecured loan in the balance-sheet prepared underPart I of Schedule VI to the Companies Act, 1956.As the debenture funds form part of the capitalstructure of the enterprise, the relevant provisionsof the Companies Act provide that its profits are tothat extent, and over the period of its currency, setaside for the purpose. This ensures, simultaneously,two things. Firstly, that the debentures are redeemedout of the profits of the enterprise and, two, that theprofits are capitalized to that extent. The Companies(Acceptance of Deposit) Rules, 1975, as prescribedunder section 58A of the Companies Act, alsoprovide, similarly, for a set aside, over a period oftime, i.e., the tenure of the public deposits, of theprofits of the depositee-company, investing a partthereof in liquid government securities each year.This ensures that the terms of the redemption aremet in a timely manner (out of the fund so created),and there are no defaul ts by the deposi tee-companies, as where the company invests its profitson expansion or in business or otherwise dissipatesthem, as by way of dividends, so that the liquidfunds are not available for discharge of the loanliabili ty at the relevant time, i.e., the time ofredemption, but at hand through the sale/realizationof the liquid securities. This can also be consideredas a measure to protect investor’s confidence as wellas to promote investment climate and corporatediscipline. The set aside of profits is, therefore, onlya sinking fund to fund a capital liability (out of theprofits).The set aside of profits, though for meetinga liability, is of one on capital account so that neitherthe assumption thereof (the l iabil i ty) nor i ts

liquidation (discharge) would impact the operatingstatement of the enterprises, i.e., the company’sprofit and loss account prepared /to be preparedunder Parts I I and III of Schedule VI to theCompanies Act. The adjustments to the book profitunder section 115JB are also consistent with thepreparation of the profit and loss account under theCompanies Act. The set side of the profits is not tomeet a trading liability or a liability on revenueaccount, so as to form part of or get incorporatedtherein, i.e., the profit and loss account. As such aliability would itself be charged to the operatingstatement, reducing the profit to that extent. Thatis, even if not actually discharged out of the profits,as where the same stand locked up in an asset/s,the profits have been deemed to have been absorbedto that extent, so as to become the source of itsdischarge. Therefore, the revenue was not incorrectin stating that the said set aside of the profits is onlyan appropriation of profits, and would not amountto a provision, so as to qualify for deduction in thecomputation of the profit of the assessee-company.The issue, in fact, is not if it is a ‘provision’ againstan ascertained liability or a ‘reserve’ per se, butwhether it could be considered as deductible incomputing the profit of the enterprise. In short, theliability, for the discharge of which the profits arebeing set aside, is in the capital field, so that neitherthe liability (on its assumption) nor the profit setaside (for its discharge) could be considered as acharge against the profits. This is precisely thereason that the same is not either claimed or allowedas deduction in the computation of income underthe regular provisions of the Act.Accordingly, theadjustment made by the assessee in the computationof book profit under section 115JB gets validated.

ACI T v. H i tachi Home and L i feSolut ions (I ndia) L td. 150 ITD 454(Ahd). - Assessment Year: 2000-01, 2001-02, 2003-04 and 2004-05 Order dated:24th September, 2013

Basic Facts

In the case, additions had been made by the TPO,after comparing the rate of royalty paid by otherassociate enterprises with the rate paid by the

Tr ibunal News

51

Ahmedabad Chartered Accountants Journal December, 2014518

assessee, using internal comparable uncontrolledtransaction (CUP) method. In the TP analysis, theassessee did not benchmark this transaction andsubmitted that the royalty rate is comparable to theroyalty payments in international market. It wasfurther submitted that the payment is approved bythe RBI. These arguments were rejected by theTPO.CIT(A)deleted the addition after observingthat on the basis of the chart submitted by theassessee, the royalty paid by it was less than thepayment made by the other associate enterprises.

Issue

Whether where it is proved that effective rateof royalty was paid by assessee was less thanroyalty paid by other AEs would addition bejustified?

Held

The Tribunal held that only stated rate is notdecisive and effective rate has to be considered andwhen the amount of royalty paid by the assessee isconsidered with ex-factory sale value, withoutdeducting various expenses, such as dealercommission, special commission, warranty etc.,then the effective rate worked out is only 2.3% onsale, as against 3% paid by other group entities.This f inding given by the CIT(A) was notcontroverted by Department. Hence based on thisaspect, the Tribunal upheld the order of the CIT(A).

Deraj Agrotech L td. Vs. ITO 164 TTJ495(Mum) Assessment Year : 2007-08Order dated: 29thJanuary, 2014

Basic Facts

The assessee company filed its return of income atNIL after set off of brought forward losses. The AOfinalized the assessment determining the income ofthe assessee at Rs.15.37 lakhs. During the assessmentproceedings AO found that the assessee companyhad not disallowed the deferred tax, fringe benefittax and prior year adjustment amounts debited to theProfit & Loss account. The AO disallowed the sameand initiated penalty proceedings. In penaltyproceedings the assessee stated that these amountswere not offered for tax through an inadvertent error.The AO held that the plea of the assessee that the

default was committed through an inadvertent errorwas too general to be accepted as a reasonable andaccordingly levied penalty under section 271(1)(c).On appeal, CIT(A) held that assessee had given alame excuse for the mistakes committed by it. Takingof a wrong base could not be termed as an inadvertentmistake. Further, assessee had considered those verysums for calculation to be made under section 115JB,hence there was no reason why same was not donefor computing taxable income. The wrong claim, sobasic and fundamental, was not acceptable as areasonable cause while deciding the cases ofconcealment penalty. Accordingly he upheld theorder of the AO.

Issue

Whether income not offered for tax through aninadver tent er ror would result in evasion oftaxes and the provisions of section 271(1) (c) beattracted?

Held

There is fundamental difference in a debatable claimand a patently wrong or false claim. There have tobe diverse opinions of courts about the claims madeunder the first category and where assessee can adoptone of the views. In such circumstances, one cansay that issue has not reached finality and if assesseehas opted for one of the possible views, he shouldnot be visited by penal provisions. But, the claimsmade under the second category have no legs of theirown to stand. Clearly, such claims are not tenablelegally or factually. If a claim of deduction putforward by the assessee is not legally valid and resultsin evasion of taxes, provisions of section 271(1)(c)comes in picture. So, it can be safely said thatwhenever any material fact for correct computationof incomeis not filed or if filed is inaccurate, thenpenalty has to be imposed. Further, it can be observedthat while computing the tax liability under section115JB the assessee had rel ied upon variousjudgments of the Tribunal and arrived at theconclusion that certain amounts were not to beconsidered while computing income under MATprovisions. It clearly shows and proves that theassessee company is well versed with the provisionsand procedure of law. It is not a case of an assessee

Tr ibunal News

52

Ahmedabad Chartered Accountants Journal December, 2014 519

who is a small time player and is ignorant of tax laws.A knowledgeable corporate-assessee cannot beal lowed to take shel ter of inadvertentmistake.Henceforth, the claim of deductions madeby the assessee with regard to FBT and prior periodexpenses was not justified and claims fall in thecategory of false claim. However amount of deferredtaxes was a deductible item at the time of assessmentwhich became disallowable because of retrospectiveamendment and therefore the claim for deductionthereof made by the assessee was not a false claimand no penalty is leviable in respect of said claim.

GFA Anlagenbau GM BH vs. DDI T(International Taxation) 165 TTJ 126(Hyd) Assessment Year : 2005-06 TO2009-10 Order dated: 27thJune, 2014

Basic Facts

The assessee was a foreign company incorporatedin Germany. It was engaged in the activity ofsupervision, erection, commissioning of plant andmachinery for steel and allied plants in India. Duringthe year under consideration, the assessee hadreceived contractual receipts from an Indiancompany for rendering technical and supervisionservices. The assessee had rendered services to theabove mentioned resident company by engagingforeign technicians at the work sites in India andthe total stay of technicians deputed by the assesseecompany on the projects exceeded 183 days .i.e.220 days. On the basis of these particulars of stay,Assessing Officer concluded that the assessee washaving Permanent Establ ishment within themeaning of article 5 of DTAA between India andGermany. The DRP held that the provisions ofrelevant contract agreement as well as the provisionsof article 5 of DTAA between India and Germanyclearly established that the assessee was havingPermanent Establishment in India during therelevant period. Further with regard to the deductionof expenditure DRP held that the assessee wasentitled to deduction of 50 per cent of gross receiptsfrom all projects towards expenditure.

Issue

Since technicians deployed by assessee merelyrendered supervisory services at project sites of

its clients and assessee did not by itself own oroperates such sites independently, whether it canbe concluded that assessee’s supervisory servicesconstituted a PE in India under article 5 of IndiaGermany DTAA?

Held

The term ‘Permanent Establishment’ is defined insection 92F (iiia) which includes a fixed place ofbusiness through which the business of the enterpriseis wholly or partly carried on’. The supervisoryactivities do not constitute a fixed place of businessin as much as the assessee rendered its services atthe project sites of its clients and does not by itselfown or operate such sites independently but ratherprovided under contract terms by its clients. In theinstant case, assessee is clearly doing the supervisionof project of the Indian company and has no fixedplace of business. Only its technicians deputed toIndia in one project stayed in India for more than180 days.Nothing was brought on record that thetechnicians are operating from a fixed place in thecustody of assessee. As per the terms the stay andtransportation are undertaken by Indian company.Applying the rationale of the Special Bench in caseof Motorola Inc. v. Dy. CIT it cannot be said thatthe assessee has a fixed place of business for itssupervisory activities.Further, Article 5(2) (i) talksabout supervisory activities and in the instant case asassessee do not have any building site or constructionsite of its own. The activities being of a technicalnature clearly fall under the Fees for Technical Service(FTS) i.e., Article 12 of the India-German DTAAand is taxable at the rates specified therein.

Aditi Technologies (P.) L td. V ITO 149ITD 515 (Bang) Order dated 14th March2014, Assessment Year 2008-09.

For the relevant assessment year, the assessee filedits return claiming deduction under section 10A inrespect of profits derived from the business ofmanufacture and export of computer software. TheCIT passed order under section 263 holding that theorder of the AO was erroneous and prejudicial to theinterest of the revenue, for the reasons that u/s 10Adeduction was al lowed for ten consecutiveassessment years beginning from the assessment year

Tr ibunal News

53

54

Ahmedabad Chartered Accountants Journal December, 2014520

in which the assessee began to manufacture an articleor thing. According to the CIT, the assessee beganto manufacture article or thing from the assessmentyear 1995-96 and the period of ten years wouldexpire in Assessment year 2004-05 and in such asituation the assessee was not entitled to claimexemption u/s 10A in the assessment year in question.

Issue

Whether the assessee would be entitled todeduction u/s 10A and how to reckon the periodof 10 consecutive assessment years in the caseof the assessee?

Held

The fact that the assessee began manufacturing inAY 1995-96 was not disputed. Accordingly theassessee was entitled to deduction u/s 10A fromAY 1995-96. As per the law as it existed prior tosubstitution of section 10A by Finance Act 2001,the period was 5 consecutive assessment yearsfalling within a period of 8 years from the assessmentyear in which the undertaking began tomanufacture. As per the amended section thededuction was al lowed for a period of 10

consecutive years from the year of manufacture. Inthis case, the assessee had not claimed deductionfor AY 1995-96 to 1997-98. But the assesseeclaimed deduction u/s 10A for AY 1998-99 to2001-02. The assessee opted out of the provisionsof section 10A by virtue of the provisions of section10A(8) which gives such opting out to an assesseefor AY 2002-03 to 2004-05. In the case of theassessee the band of 10 years as per the amendedlaw would be 1995-96 to 2004-05 only. Opting outof the provisions of section 10A will not have theeffect of extending the band period of 10 years.The assessee could get the benefit of the amendedlaw applicable from assessment year 2001-02 onlyfor 2 more years viz., AY 2003-04 & 2004-05. Theprovision for opting out of the provisions of section10A is intended to facilitate an assessee who canget more benefits under any other provisions ofdeduction under Chapter VIA. That provisioncannot extend the period of benefit beyond 10 yearsfrom the previous year relevant to assessment yearin which the assessee begins to manufacture orproduce articles or things.

❉ ❉ ❉

Tr ibunal News

in him to serve his country, its institutions andcitizens. Each one of the above (the country, itsinstitutions and citizens), needs to be preserved.Each of them grows to prosper, with the others’support. Each of them has duties, obligations andresponsibi l i ties and also rights, benefi ts andadvantages. Their harmonious glory emerges fromwhat is commonly understood as “the Rule ofLaw”. The judiciary as an institution has extremelysacrosanct duties, obligations and responsibilities”.

Subrata Roy Sahara vs. UOI (2014) (8 SCC 470)

Recovery of tax-Membership card ofStock Exchange.

A reading of rules 5 and 9 of the Rules, By-Lawsand Regulations of BSE leads to the conclusionthat a membership card is only a personalpermission from the stock exchange to exercise therights and privileges that may be given to subject

to Rules. The moment a member is declareddefaulter, his right of nomination seizes and vestsin the exchange.

Government debts have precedents over unsecuredcreditors. The Income Tax Act, 1961 does notprovide for any paramountcy of dues by way ofincome tax. The moment the stock exchange has alien over the member’s securities; it would haveprecedence over income tax dues. The l ienpossessed by SE makes it a secured creditor andwhether it is a statutory lien arise out of agreement,does not make much of the difference as SE beinga secured credi tor would have priori ty overGovernment dues.

Stock Exchange, Bomaby vs. Y.S.Khandalgaonkar (2014) (368 ITR 296)

❉ ❉ ❉

contd. from page 512 Glimpses of Supreme Cour t Rulings

30

Ahmedabad Chartered Accountants Journal December, 2014 521

In this issue we are giving gist of an importantdecision of Hon’ble Ahmedabad Tribunal in thecase of Shri K ishore R. Pithva, wherein an issueon which the appellant did not press his groundsbefore CIT(A) came to be agitated by assesseebefore Hon’ble Tribunal and the same was allowedby the Hon’ble Tribunal as the legal position wasin favour of the assessee.The Hon’ble Tribunal while deciding the matterreiterated old principle that there cannot be estoppleagainst the law and that there cannot be concessionin the matter of law. If the legal position is in favourof the assessee, the department has to grant relief tothe assessee irrespective of the fact that the assesseemay have waived his entitlement of the same.Present day, many a times, an assessee may beunder certain compulsions made to withdraw hisgrounds as not pressed even if the legal position isin favour of the assessee. In that situation suchdecision could be helpful.

In the Income Tax Appellate Tr ibunal atAhmedabad“D” Bench

Before S/Shr i G.C. Gupta, Vice-President andN.S. Saini, Accountant Member

ITA No. 2931/Ahd/2010[Asstt. Year : 2007-2008]

Shr i K ishore R. Pithva v/s ITO, Ward-12(2)Mathur Master Estate AhmedabadOpp: Babulal Zafarani PattiNagarwel Hanuman RoadAmraiwadi, Ahmedabad – 380 006PAN : ACRPP 9292 L

(Appellant) (Respondent)Assessee by ; Shr i M.K. PatelRevenue by : Smt. Sonia Kumar, Sr. DRDate of Hear ing : 8th September, 2014Date of Pronouncement : 17/10/2014

GistFacts :

CA. Sanjay R. [email protected]

Unreported Judgements

The relevant grounds before Hon’ble Tribunal wereas under :“2. The ground No.1 and 2 of the assessee are as

under :

“1. The ld. CIT(A) has erred in deciding theground of appeal ‘a’ as not pressed inrespect of non deduction of TDS u/s 194Cof the Act on expenses of Rs.7,97,850/-and Rs.1,75,000/- as not allowable u/s40(a)(ia) when the provisions of deductionof TDS for an individual assessee weremade applicable w.e.f. 01/06/2007 andalso brought to the notice of CIT(A) videsubmission dated 25/03/2010 that it werenot applicable during previous year 2006-07. The learned CIT(A) ought to havedeleted the expenses disallowance as notconsistent with legal provisions.

2. The ld. CIT(A) has erred in rejecting theground number ‘a’ of the ground of appealbefore him as not pressed vide order sheetentry dated 06/09/2010 in as much as theAR was not empowered to do so but asexplained to appellant he was forced to doso to avoid adverse consequences thereof.The acceptance of the AR for not pressingthe ground number ‘a’ be held to be illegaland bad in law and also as not in conformitywith the authority granted to AR.”

Rival Contentions :The Counsel for the assessee submitted that issueof disal lowance of expenses amounting toRs.7,97,850/- and Rs.1,75,000/- u/s 40(a)(ia) of theAct was not pressed by the Chartered Accountantof the assessee before CIT(A). It is submitted thatprovisions of TDS u/s 194C for an individualassessee were made applicable w.e.f. 01/06/2007and therefore were not applicable for the relevantassessment year 2007-08 and therefore theconcession made by C.A. of the assessee was under

Ahmedabad Chartered Accountants Journal December, 2014522

misconception of the law. He submitted that issuebeing legal in nature, Revenue authorities shouldhave decided the same in accordance with the law.He relied on the decisions of Hon’ble Apex Courtin CIT v/s Shelly Products and Another, 261 ITR367 (SC) and the decisions of the Hon’ble GujaratHigh Court in P.V. Doshi v/s CIT, 113 ITR 22(Guj.) and S.R. Koshti v/s CIT, 276 ITR 165 (Guj.).On the other hand DR opposed the submission ofthe assessee and submitted that since the C.A. ofthe assessee had conceded the issue before CIT(A),the assessee should not be allowed to re-agitate thesame now before the Tribunal.

HeldThe Hon’ble Tribunal on consideration of the factsand legal position held as under:“5. We have considered rival submissions and have

perused the orders of theAO and the CIT(A), andalso decisions of various courts relied upon onbehalfof the assessee. We find that the assesseehas admitted that its Chartered Accountant has“not pressed” the issue before the CIT(A).However, we findthat there could not legally beno estoppel against the law. The disallowancewasmade for non-deduction of tax on expenses undersection 40(a)(ia) of theAct, although, the TDSprovision under section 194C on an individualassesseewas not applicable during the relevantperiod to the case of the assessee, beinganindividual, as this provision of TDS was madeapplicable w.e.f. 1-6-2007 incase of an individual.We find that there could not be any validagreement ofthe assessee with the department incontravention of the statute. It is not thecase ofthe department that the TDS provisionundersection 194C were in factapplicable to the factsof the case of the assessee during the relevantperiod.The only reasoning of the Revenueauthori ties was that since theassessee’srepresentative has conceded the issuebefore the CIT(A), the addition should beupheld.Such an interpretation of law, in our consideredopinion, shall lead toanomalies and also notsustainable in law. We are of the view that it istheresponsibility of the Revenue authorities tocompute the taxable income of theassesseecorrectly in accordance with the provision of law