Embed Size (px)

Citation preview

2018 Insurance Market Briefing -Germany

Hotel Pullman, Cologne – 27 September 2018

2018 Insurance Market Briefing - Germany

Welcome

Nick Charteris-BlackManaging Director, Market Development – EMEA

William MillsDirector, Market Development

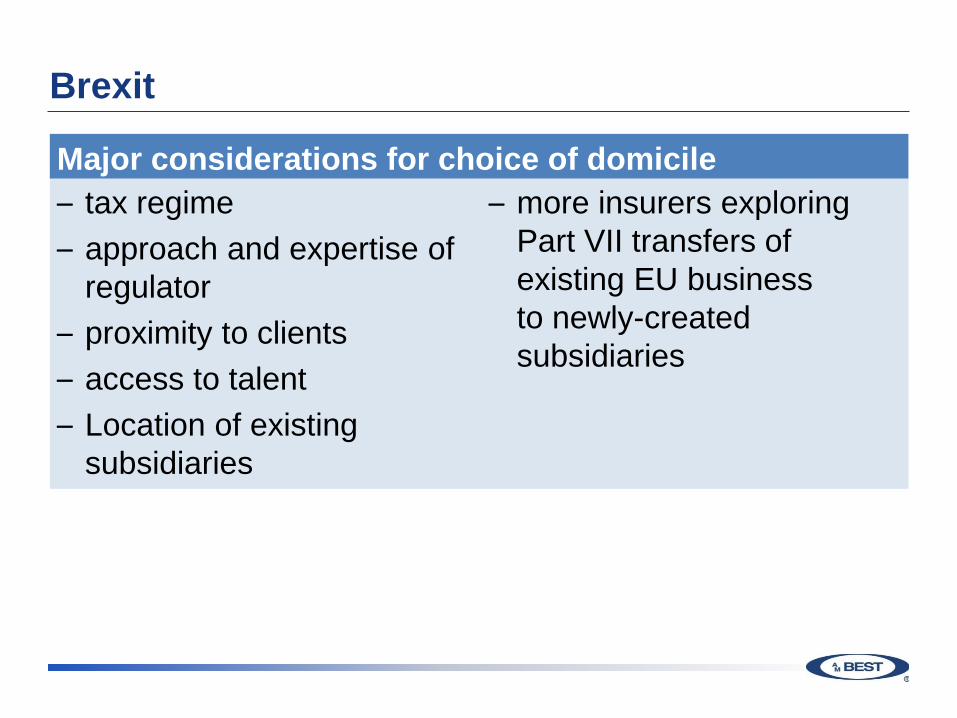

Brexit

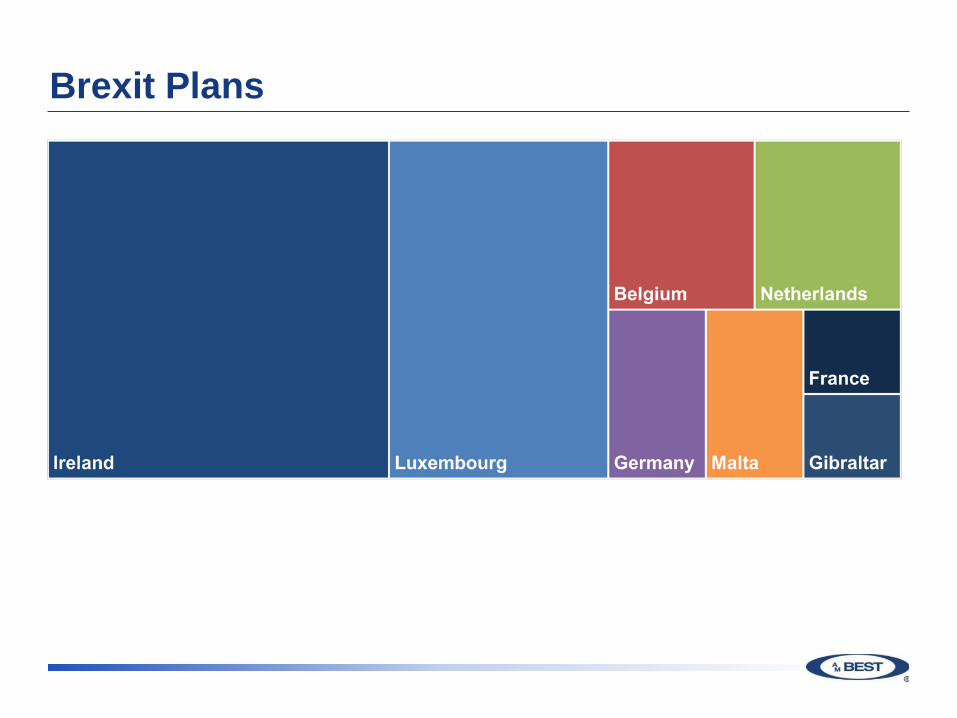

Brexit Plans

Brexit

Major considerations for choice of domicile– tax regime– approach and expertise of

regulator– proximity to clients– access to talent– Location of existing

subsidiaries

– more insurers exploring Part VII transfers of existing EU businessto newly-created subsidiaries

A.M. Best - Preparing for Brexit…

• A.M. Best currently registered with European Securities and Markets Authority (ESMA)

• Allows market access across the current EU 28 to provide rating services

• New registered EU subsidiary being established in Amsterdam to maintain EU 27 access

• Operational by 29 March 2019

Agenda14:10 Guest Presentation: Allianz

ESG Integration into InvestmentsLeyla Javadova, Senior Analyst, ESG at Allianz Investment Management (AIM SE)

14:50 Thematic Session: Reinsurance Market HighlightsDr Angela Yeo, Senior Director, Analytics

15:20

15:40 European (Re)Insurance Market Overview

Charlotte Vigier, Senior Financial AnalystKonstantin Langowski, Financial Analyst

16:15 A.M. Best's Revised Rating Methodology in Action: A Case Study

Catherine Thomas, Senior Director, AnalyticsMichael Dunckley, Associate Director, Analytics,Dr Angela Yeo, Senior Director, AnalyticsCharlotte Vigier, Senior Financial AnalystKonstantin Langowski, Financial Analyst

17:00

Disclaimer © AM Best Company (AMB) and/or its licensors and affiliates. All rights reserved. ALL INFORMATION CONTAINED HEREIN ISPROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISEREPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED ORRESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM ORMANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT AMB’s PRIOR WRITTEN CONSENT. Allinformation contained herein is obtained by AMB from sources believed by it to be accurate and reliable. Because of thepossibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS”without warranty of any kind. Under no circumstances shall AMB have any liability to any person or entity for (a) any loss ordamage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance orcontingency within or outside the control of AMB or any of its directors, officers, employees or agents in connection with theprocurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or(b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lostprofits), even if AMB is advised in advance of the possibility of such damages, resulting from the use of or inability to use, anysuch information. The credit ratings, financial reporting analysis, projections, and other observations, if any, constituting part ofthe information contained herein are, and must be construed solely as, statements of opinion and not statements of fact orrecommendations to purchase, sell or hold any securities, insurance policies, contracts or any other financial obligations, nordoes it address the suitability of any particular financial obligation for a specific purpose or purchaser. Credit risk is the risk thatan entity may not meet its contractual, financial obligations as they come due. Credit ratings do not address any other risk,including but not limited to, liquidity risk, market value risk or price volatility of rated securities. NO WARRANTY, EXPRESS ORIMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANYPARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY AMB INANY FORM OR MANNER WHATSOEVER. Each credit rating or other opinion must be weighed solely as one factor in anyinvestment or purchasing decision made by or on behalf of any user of the information contained herein, and each such usermust accordingly make its own study and evaluation of each security or other financial obligation and of each issuer andguarantor of, and each provider of credit support for, each security or other financial obligation that it may consider purchasing,holding or selling.

Disclaimer US Securities Laws explicitly prohibit the issuance or maintenance of a credit rating where a person involvedin the sales or marketing of a product or service of the CRA also participates in determining or monitoring thecredit rating, or developing or approving procedures or methodologies used for determining the credit rating.

No part of this presentation amounts to sales / marketing activity and A.M. Best’s Rating Divisionemployees are prohibited from participating in commercial discussions.

Any queries of a commercial nature should be directed to A.M. Best’s Market Development function.

© Copyright Allianz SE

Allianz Investment Management SE

Leyla Javadova

September 2018

ALLIANZ ESGINTEGRATION INTOINVESTMENTS

© Copyright Allianz SE

CONTENT

11

ALLIANZ CORPORATE RESPONSIBILITY AT A GLANCE

ABOUT AIM SE

AIM ESG APPROACH

© Copyright Allianz SE 12

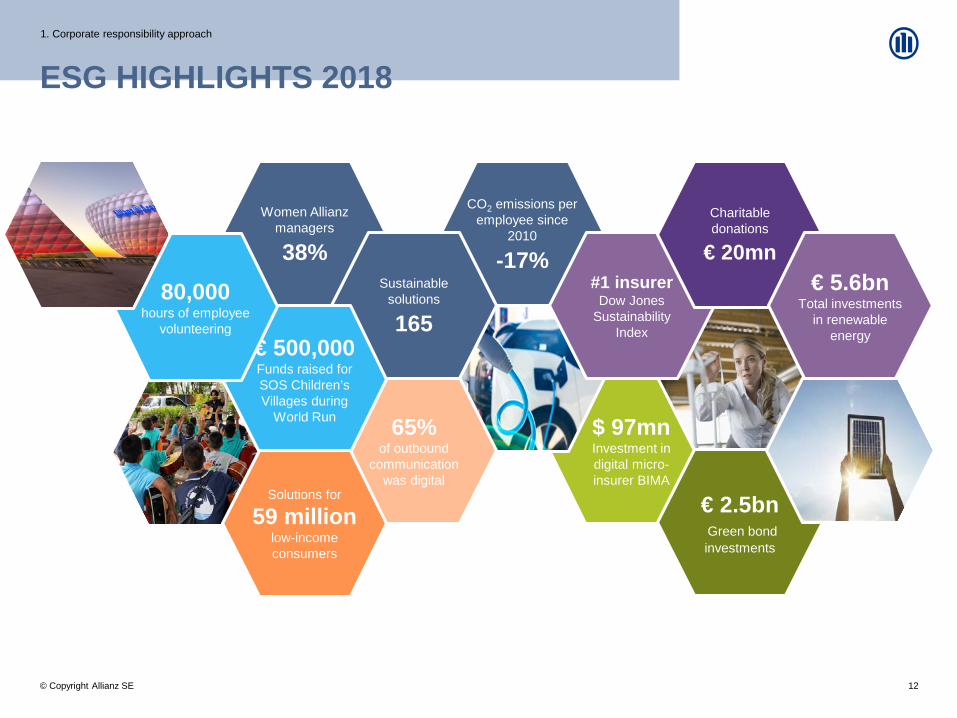

Women Allianz managers

38%

$ 97mnInvestment in digital micro-insurer BIMA

CO2 emissions per employee since

2010

-17%

65%of outbound

communication was digital

Sustainable solutions

165€ 500,000Funds raised for SOS Children’s Villages during

World Run

#1 insurerDow Jones

Sustainability Index

€ 2.5bnGreen bond investments

Solutions for

59 million low-income consumers

80,000hours of employee

volunteering

Charitable donations

€ 20mn€ 5.6bn

Total investments in renewable

energy

ESG HIGHLIGHTS 20181. Corporate responsibility approach

© Copyright Allianz SE 13

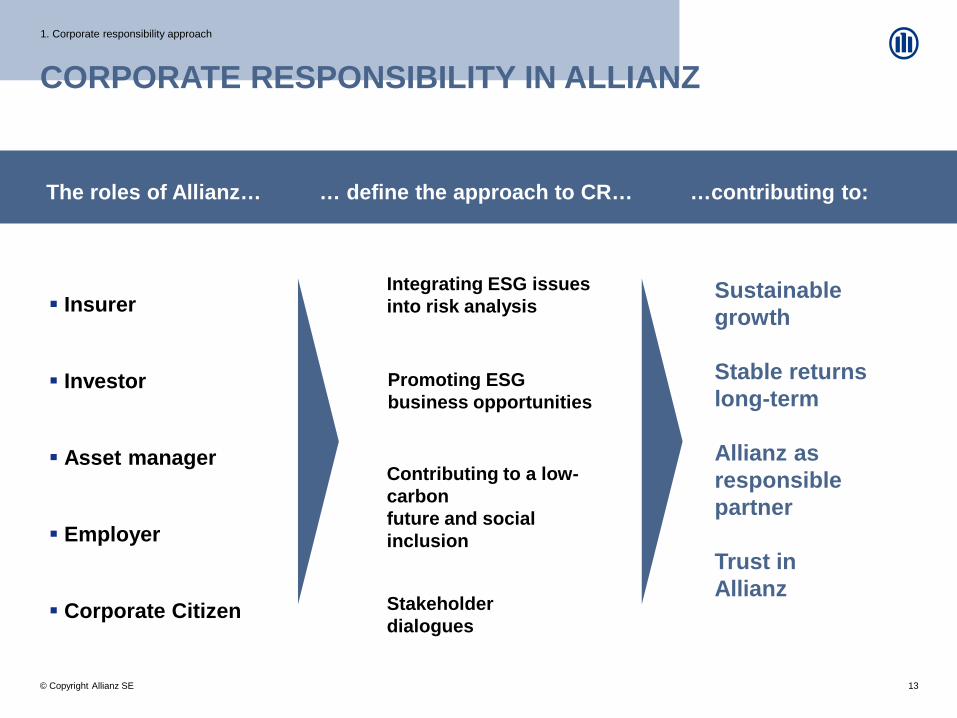

CORPORATE RESPONSIBILITY IN ALLIANZ1. Corporate responsibility approach

Integrating ESG issuesinto risk analysis

Promoting ESG business opportunities

Contributing to a low-carbonfuture and social inclusion

Stakeholder dialogues

Insurer

Investor

Asset manager

Employer

Corporate Citizen

The roles of Allianz… … define the approach to CR… …contributing to:

Sustainable growth

Stable returns long-term

Allianz as responsible partner

Trust in Allianz

© Copyright Allianz SE 14

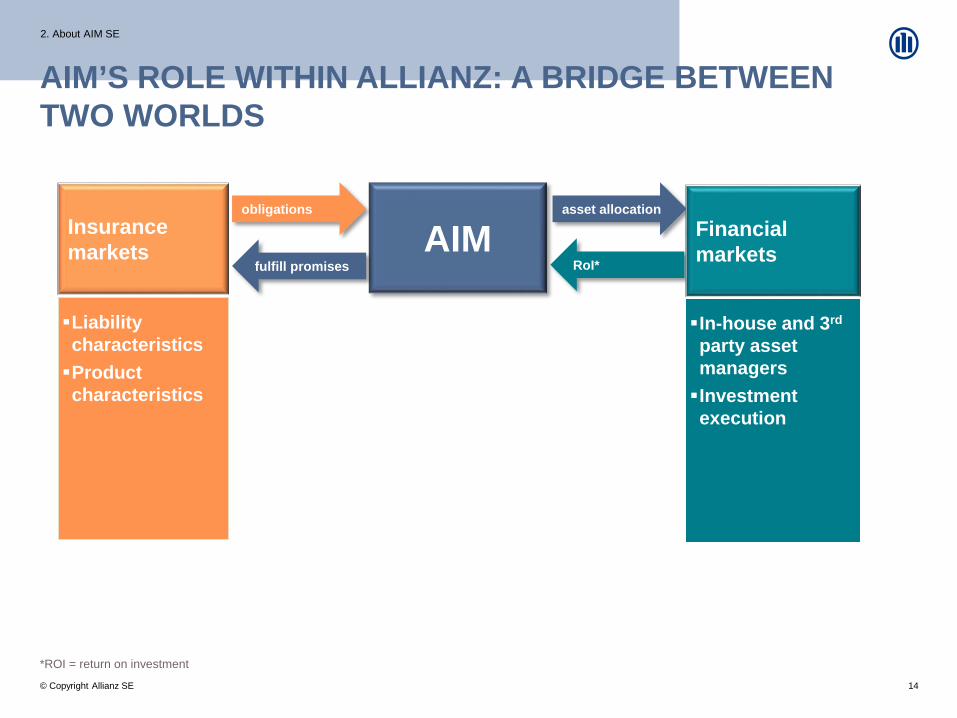

AIM’S ROLE WITHIN ALLIANZ: A BRIDGE BETWEEN TWO WORLDS

2. About AIM SE

AIM

In-house and 3rd

party asset managersInvestment execution

Liability characteristicsProduct characteristics

obligations asset allocation

fulfill promises RoI*

Insurancemarkets

Financialmarkets

*ROI = return on investment

© Copyright Allianz SE 15

MILESTONES OF ESG INTEGRATION3. AIM ESG approach

Organization

2011Allianz SE signs

Exclusion of controversial

weapons1

2013Roll-out of ESG

guidelines for non-listed assets

2016ESG scoring

Allianz Group ESG Board

2012

Exclusion of coal-based business

models

2015

First Investments in Africa

2017

¹Cluster Munitions, Anti-Personnel Mines, Chemical & Biological Weapons

© Copyright Allianz SE 16

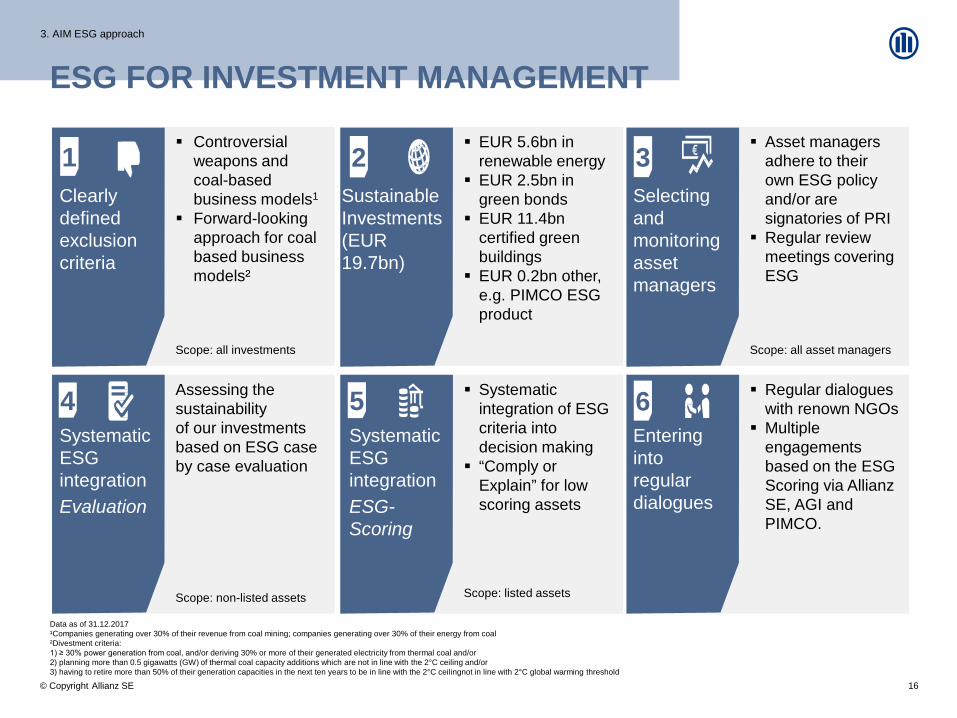

ESG FOR INVESTMENT MANAGEMENT3. AIM ESG approach

Controversial weapons and coal-based business models1

Forward-looking approach for coal based business models²

Scope: all investments

Assessing the sustainabilityof our investments based on ESG case by case evaluation

Scope: non-listed assets

Asset managers adhere to their own ESG policy and/or are signatories of PRI

Regular review meetings covering ESG

Scope: all asset managers

Regular dialogues with renown NGOs

Multiple engagements based on the ESG Scoring via Allianz SE, AGI and PIMCO.

Systematic integration of ESG criteria into decision making

“Comply or Explain” for low scoring assets

Scope: listed assets

Systematic ESG integrationEvaluation

Selecting and monitoring asset managers

3Clearly defined exclusion criteria

1

Entering into regular dialogues

64

EUR 5.6bn in renewable energy

EUR 2.5bn in green bonds

EUR 11.4bn certified green buildings

EUR 0.2bn other, e.g. PIMCO ESG product

Sustainable Investments(EUR 19.7bn)

2

Systematic ESG integrationESG-Scoring

5

Data as of 31.12.2017¹Companies generating over 30% of their revenue from coal mining; companies generating over 30% of their energy from coal²Divestment criteria:1) ≥ 30% power generation from coal, and/or deriving 30% or more of their generated electricity from thermal coal and/or2) planning more than 0.5 gigawatts (GW) of thermal coal capacity additions which are not in line with the 2°C ceiling and/or3) having to retire more than 50% of their generation capacities in the next ten years to be in line with the 2°C ceilingnot in line with 2°C global warming threshold

© Copyright Allianz SE 17

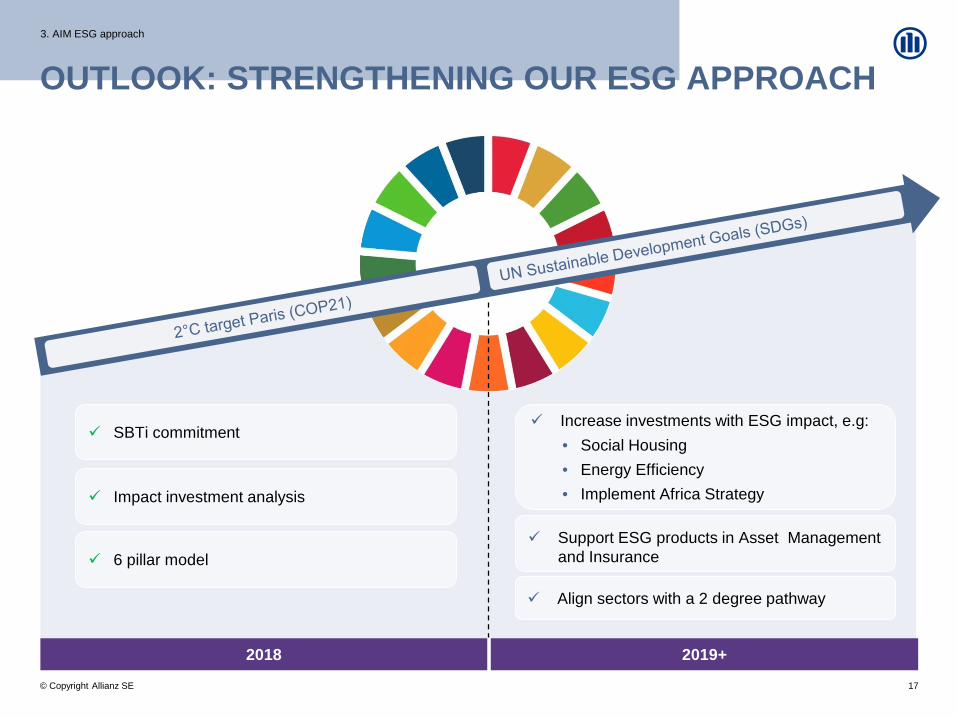

OUTLOOK: STRENGTHENING OUR ESG APPROACH

SBTi commitment

2018 2019 +

3. AIM ESG approach

2019+

Impact investment analysis

6 pillar model

Increase investments with ESG impact, e.g:• Social Housing• Energy Efficiency• Implement Africa Strategy

Support ESG products in Asset Management and Insurance

Align sectors with a 2 degree pathway

© Copyright Allianz SE 18

THANK YOU!4. Thank you

QUESTIONS?

2018 Insurance Market Briefing - Germany

Thematic Session: Reinsurance Market Highlights

Dr Angela YeoSenior Director, Analytics

2018 Insurance Market Briefing - Germany

2018 Überblick über den globalen Rückversicherungsmarkt

Dr. Angela YeoSenior Director, Analytics

Discussion Outline

Global Reinsurance Results and Trends

Global Reinsurance Market Capacity

Global Reinsurance Market Evolution

Global Reinsurance Sector Outlook

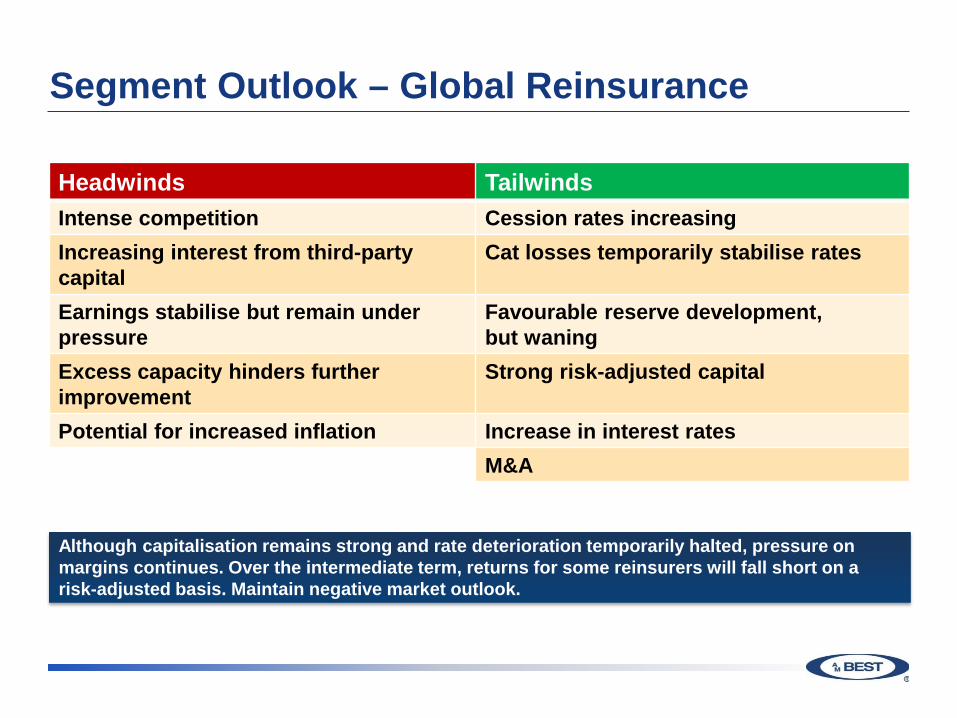

Segment Outlook – Global Reinsurance

Headwinds TailwindsIntense competition Cession rates increasingIncreasing interest from third-party capital

Cat losses temporarily stabilise rates

Earnings stabilise but remain under pressure

Favourable reserve development,but waning

Excess capacity hinders further improvement

Strong risk-adjusted capital

Potential for increased inflation Increase in interest ratesM&A

Although capitalisation remains strong and rate deterioration temporarily halted, pressure on margins continues. Over the intermediate term, returns for some reinsurers will fall short on a risk-adjusted basis. Maintain negative market outlook.

Global ReinsuranceResults and Trends

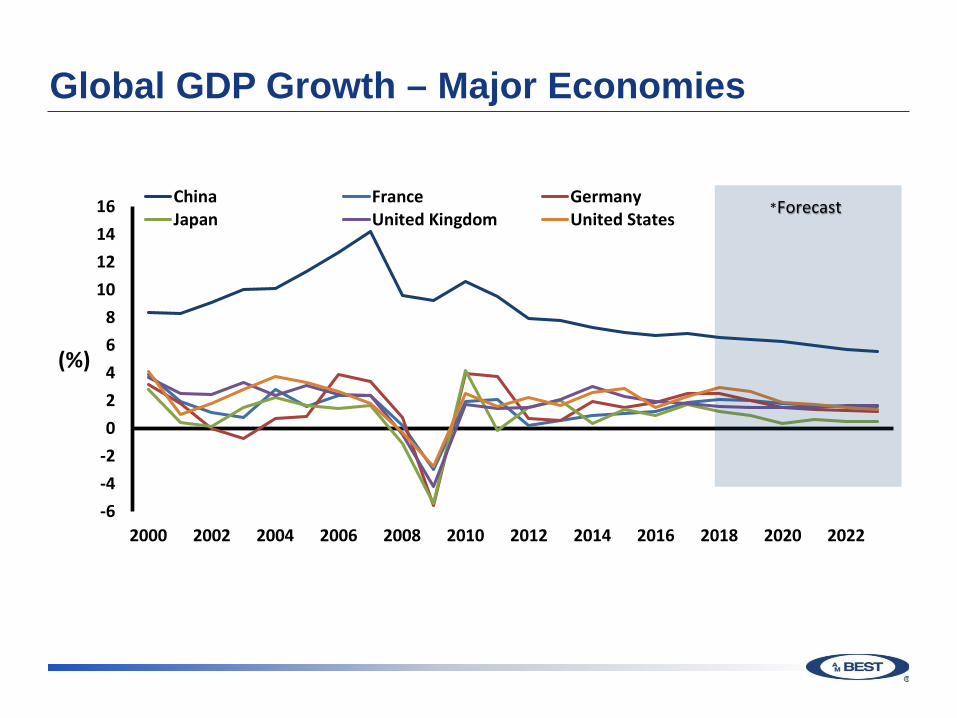

Global GDP Growth – Major Economies

-6-4-202468

10121416

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

(%)

China France GermanyJapan United Kingdom United States

*Forecast

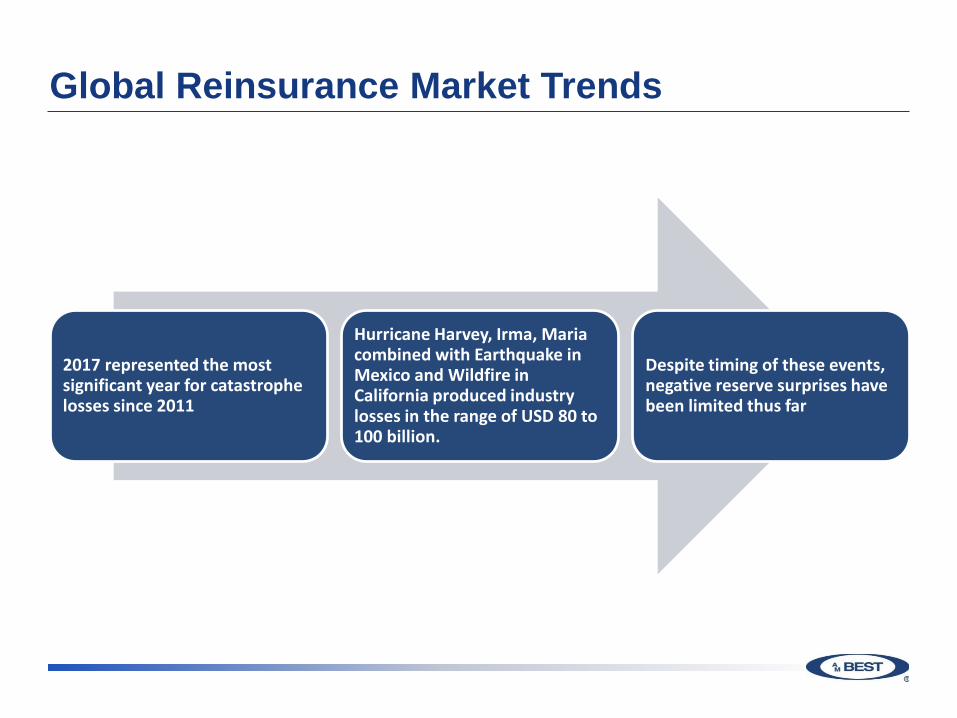

Global Reinsurance Market Trends

2017 represented the most significant year for catastrophe losses since 2011

Hurricane Harvey, Irma, Maria combined with Earthquake in Mexico and Wildfire in California produced industry losses in the range of USD 80 to 100 billion.

Despite timing of these events, negative reserve surprises have been limited thus far

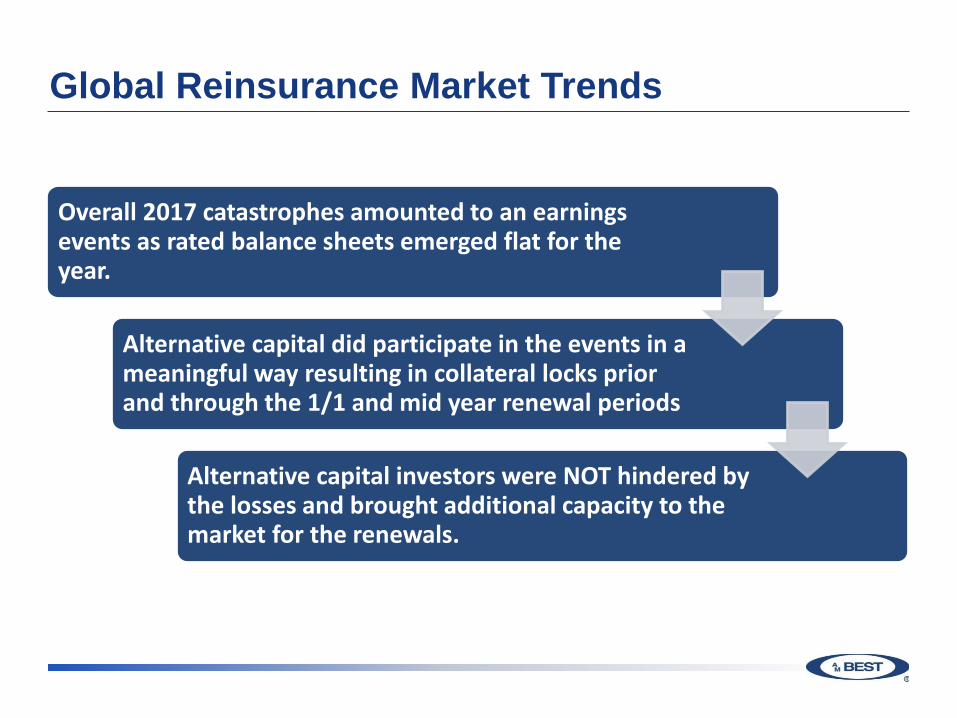

Global Reinsurance Market Trends

Overall 2017 catastrophes amounted to an earnings events as rated balance sheets emerged flat for the year.

Alternative capital did participate in the events in a meaningful way resulting in collateral locks prior and through the 1/1 and mid year renewal periods

Alternative capital investors were NOT hindered by the losses and brought additional capacity to the market for the renewals.

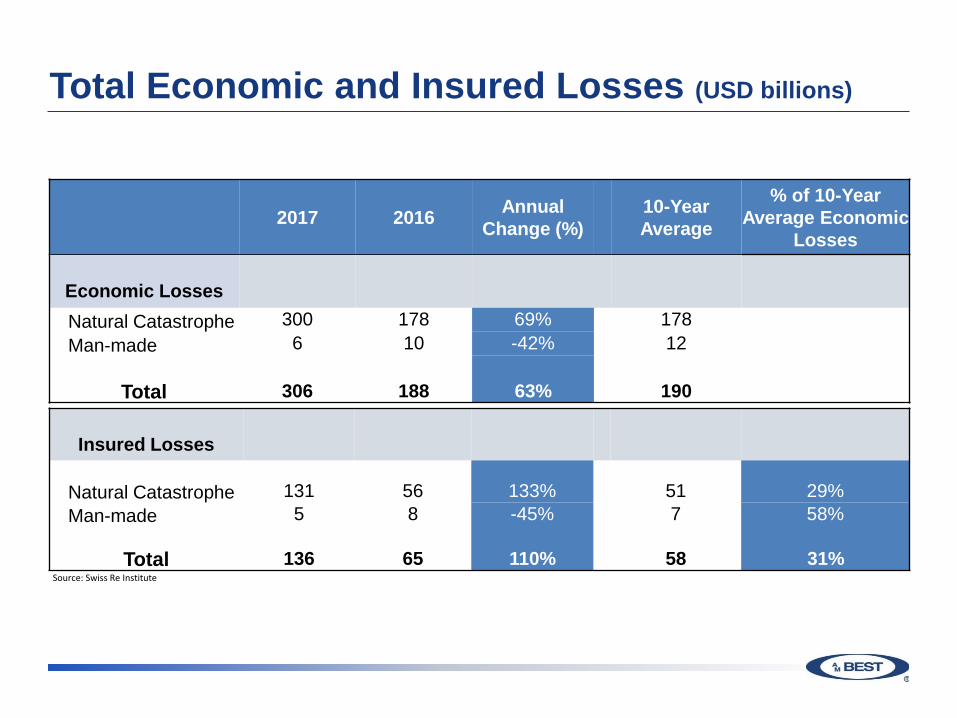

Total Economic and Insured Losses (USD billions)

Source: Swiss Re Institute

2017 2016 Annual Change (%)

10-YearAverage

% of 10-Year Average Economic

Losses

Economic LossesNatural Catastrophe 300 178 69% 178Man-made 6 10 -42% 12

Total 306 188 63% 190

Insured Losses

Natural Catastrophe 131 56 133% 51 29%Man-made 5 8 -45% 7 58%

Total 136 65 110% 58 31%

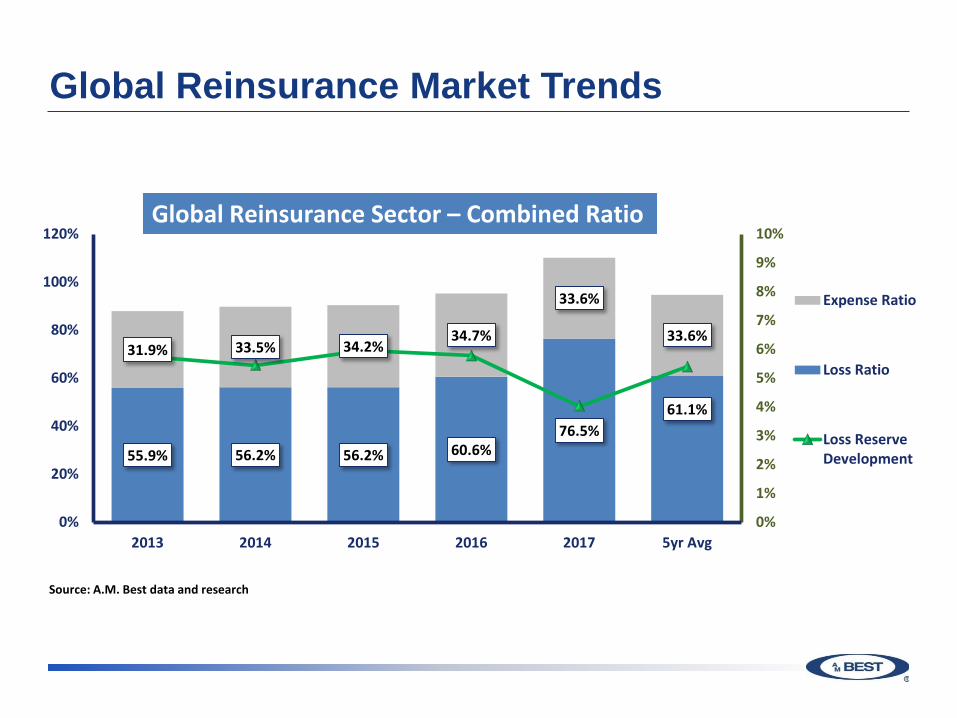

Global Reinsurance Market Trends

55.9% 56.2% 56.2% 60.6%76.5%

61.1%

31.9% 33.5% 34.2%34.7%

33.6%

33.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0%

20%

40%

60%

80%

100%

120%

2013 2014 2015 2016 2017 5yr Avg

Expense Ratio

Loss Ratio

Loss ReserveDevelopment

Source: A.M. Best data and research

Global Reinsurance Sector – Combined Ratio

Global Reinsurance Market Trends

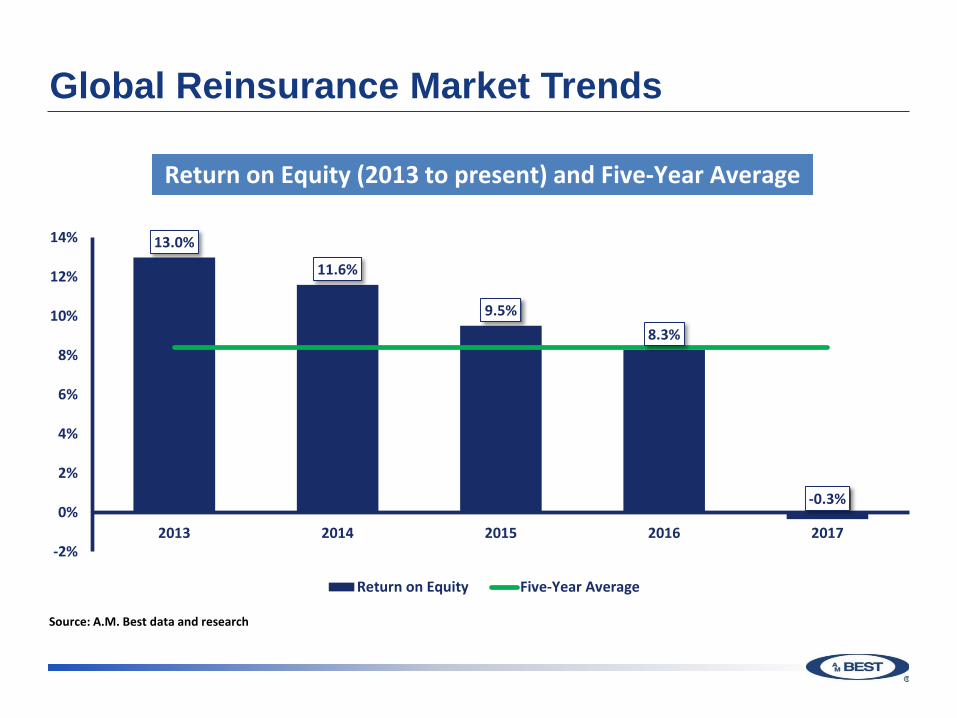

13.0%

11.6%

9.5%8.3%

-0.3%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2013 2014 2015 2016 2017

Return on Equity Five-Year Average

Source: A.M. Best data and research

Return on Equity (2013 to present) and Five-Year Average

Global Reinsurance Market Trends

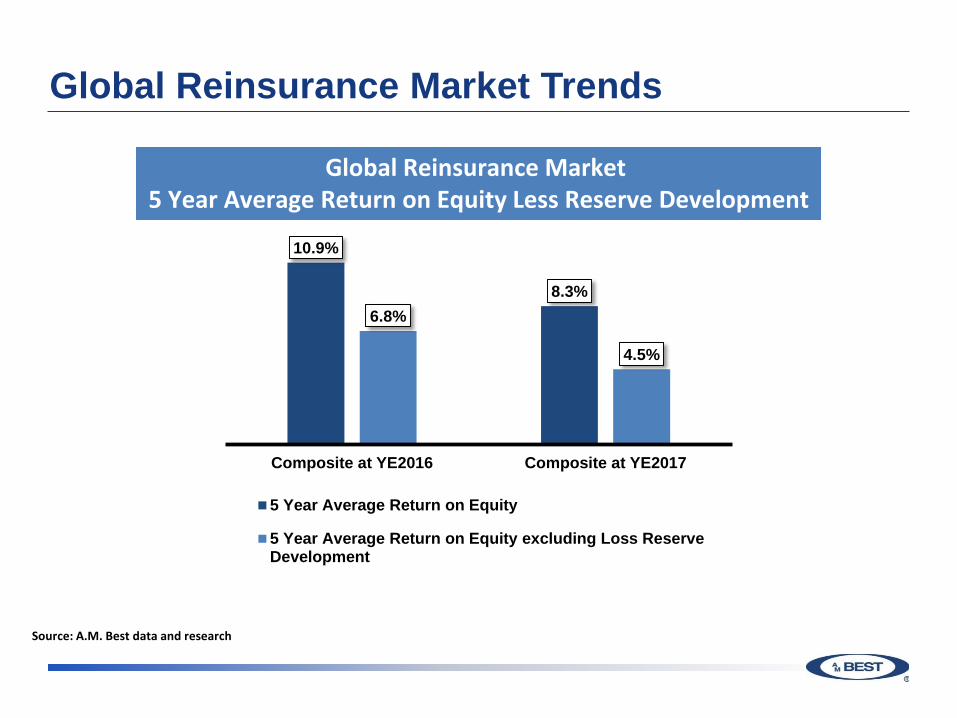

Global Reinsurance Market 5 Year Average Return on Equity Less Reserve Development

Source: A.M. Best data and research

10.9%

8.3%6.8%

4.5%

Composite at YE2016 Composite at YE2017

5 Year Average Return on Equity

5 Year Average Return on Equity excluding Loss ReserveDevelopment

Global ReinsuranceMarket Capacity

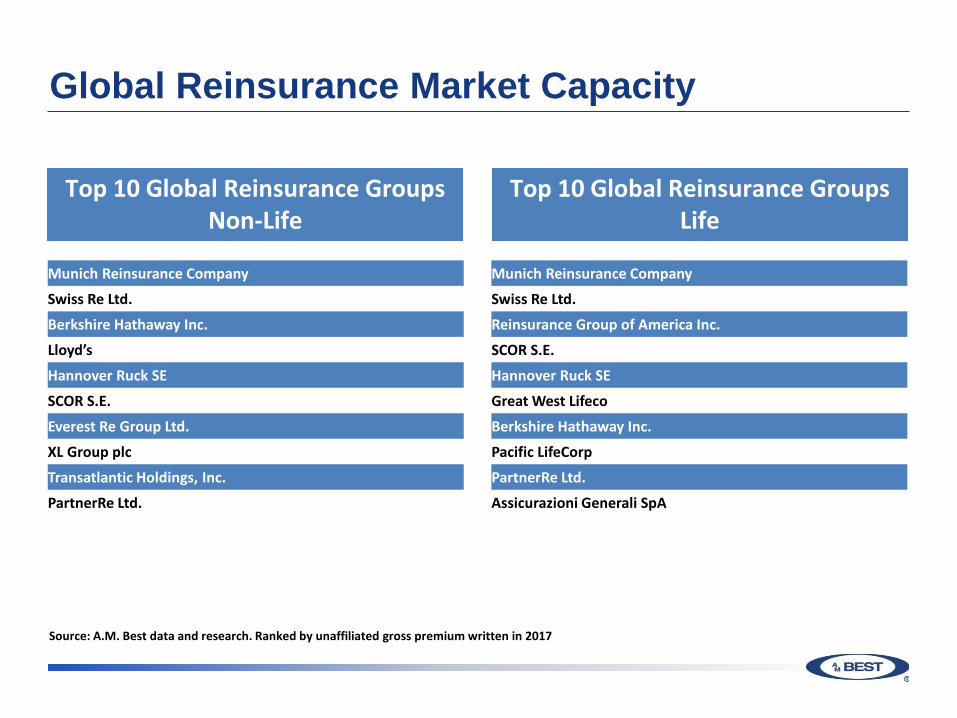

Global Reinsurance Market Capacity

Top 10 Global Reinsurance Groups Non-Life

Top 10 Global Reinsurance Groups Life

Munich Reinsurance Company

Swiss Re Ltd.

Berkshire Hathaway Inc.

Lloyd’s

Hannover Ruck SE

SCOR S.E.

Everest Re Group Ltd.

XL Group plc

Transatlantic Holdings, Inc.

PartnerRe Ltd.

Munich Reinsurance Company

Swiss Re Ltd.

Reinsurance Group of America Inc.

SCOR S.E.

Hannover Ruck SE

Great West Lifeco

Berkshire Hathaway Inc.

Pacific LifeCorp

PartnerRe Ltd.

Assicurazioni Generali SpA

Source: A.M. Best data and research. Ranked by unaffiliated gross premium written in 2017

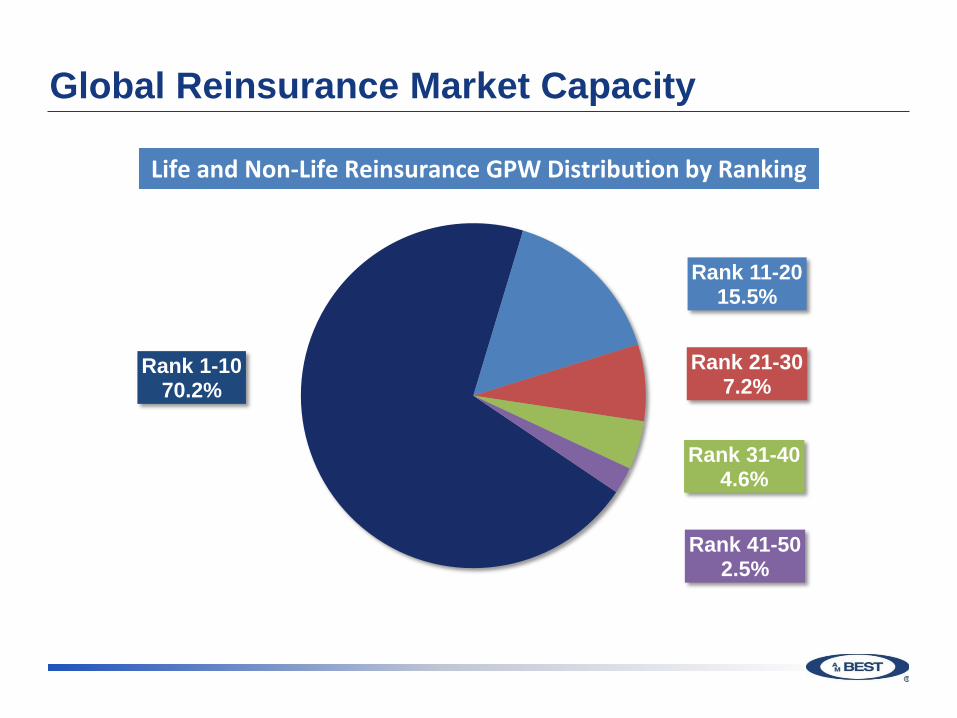

Global Reinsurance Market Capacity

Life and Non-Life Reinsurance GPW Distribution by Ranking

Rank 1-1070.2%

Rank 11-2015.5%

Rank 21-307.2%

Rank 31-404.6%

Rank 41-502.5%

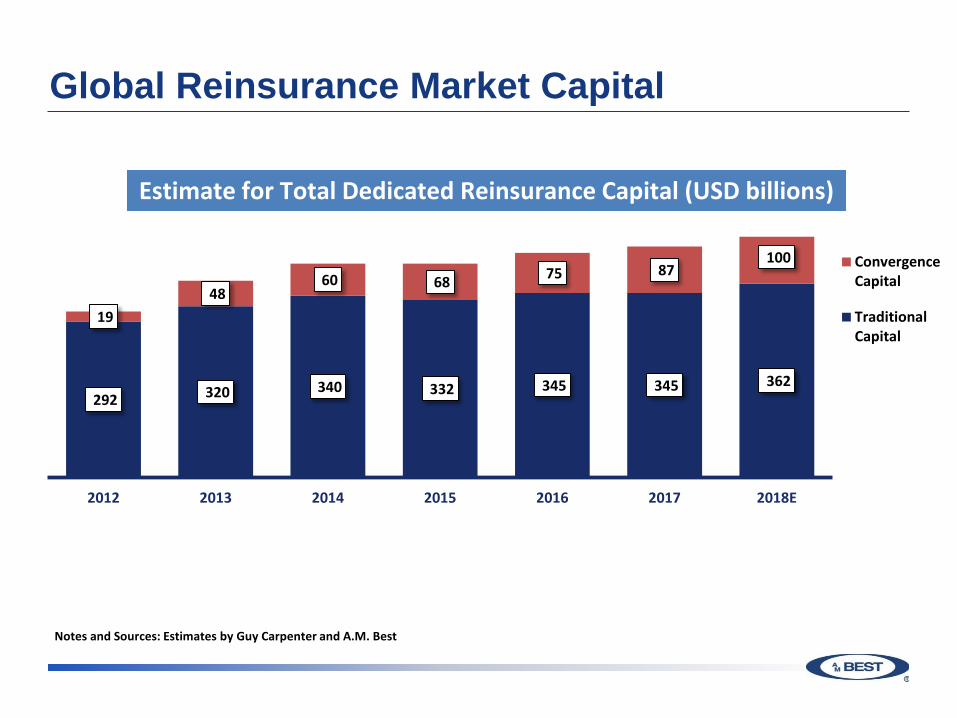

Global Reinsurance Market Capital

292 320 340 332 345 345 362

19 48

60 68 75 87 100

2012 2013 2014 2015 2016 2017 2018E

ConvergenceCapital

TraditionalCapital

Estimate for Total Dedicated Reinsurance Capital (USD billions)

Notes and Sources: Estimates by Guy Carpenter and A.M. Best

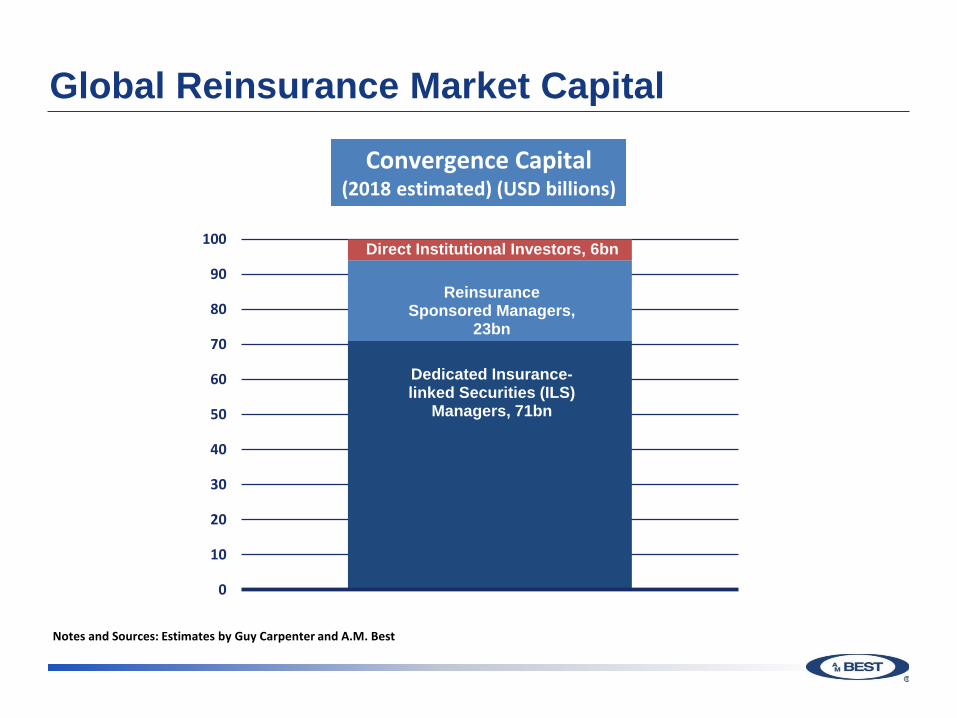

Global Reinsurance Market Capital

Dedicated Insurance-linked Securities (ILS)

Managers, 71bn

Reinsurance Sponsored Managers,

23bn

Direct Institutional Investors, 6bn

0

10

20

30

40

50

60

70

80

90

100

Convergence Capital(2018 estimated) (USD billions)

Notes and Sources: Estimates by Guy Carpenter and A.M. Best

Global Market Evolution

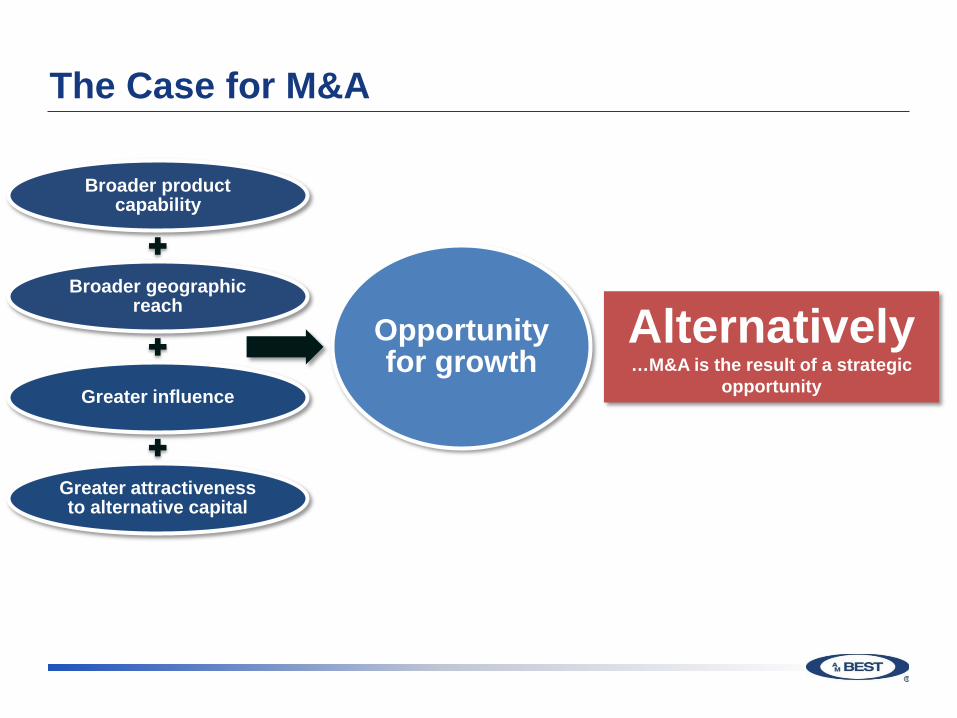

The Case for M&A

Broader product capability

Broader geographic reach

Greater influence

Greater attractiveness to alternative capital

Opportunity for growth

Alternatively…M&A is the result of a strategic

opportunity

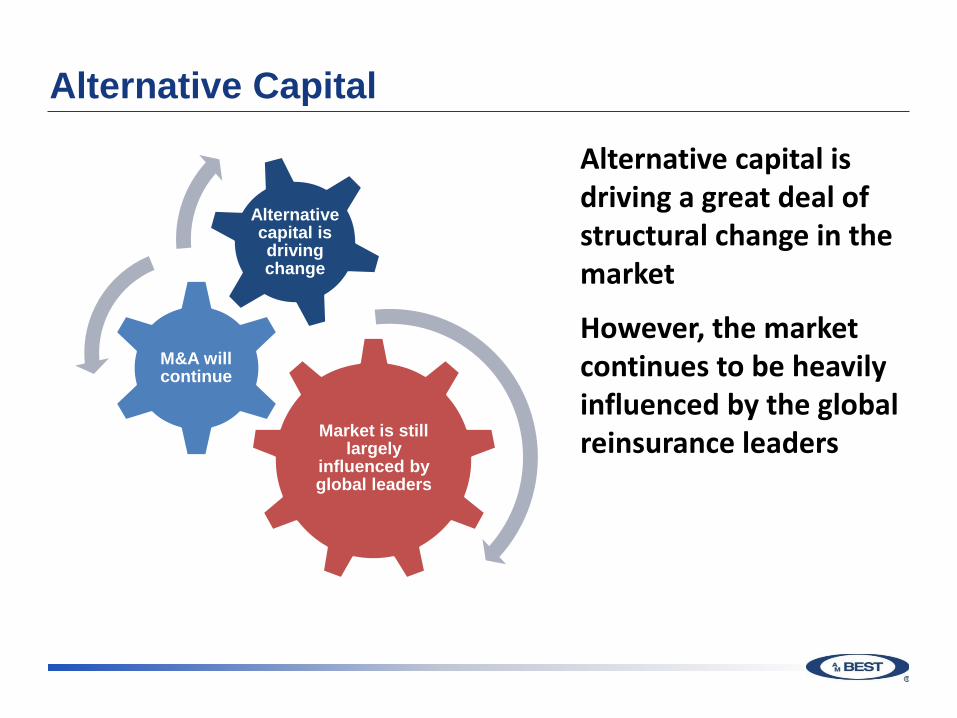

Alternative Capital

Market is still largely

influenced by global leaders

M&A will continue

Alternative capital is driving change

Alternative capital is driving a great deal of structural change in the market

However, the market continues to be heavily influenced by the global reinsurance leaders

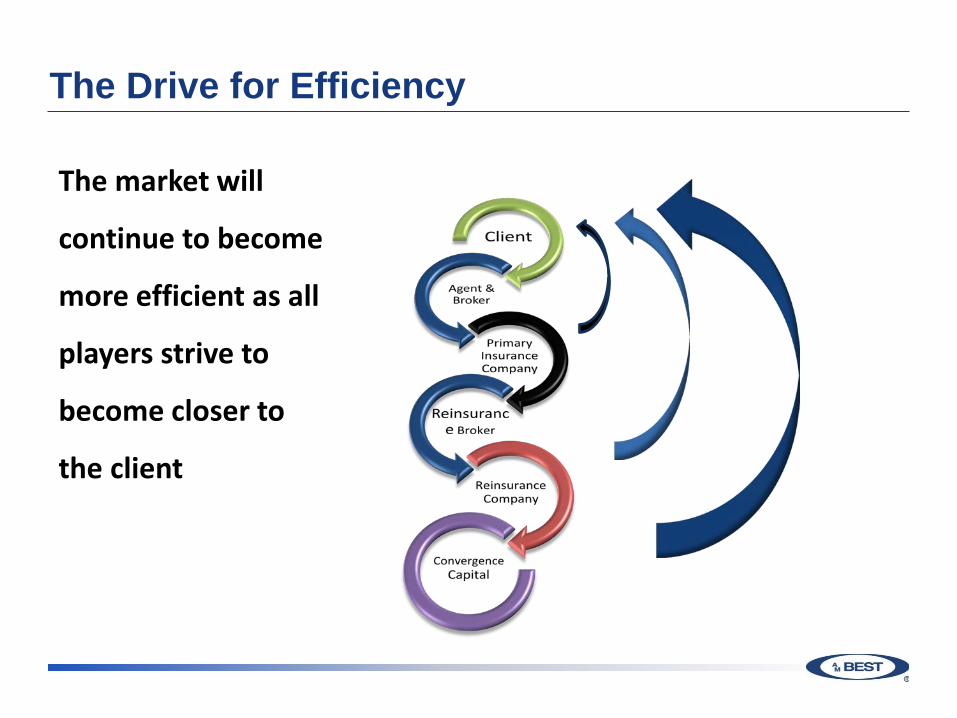

The Drive for Efficiency

The market will

continue to become

more efficient as all

players strive to

become closer to

the client

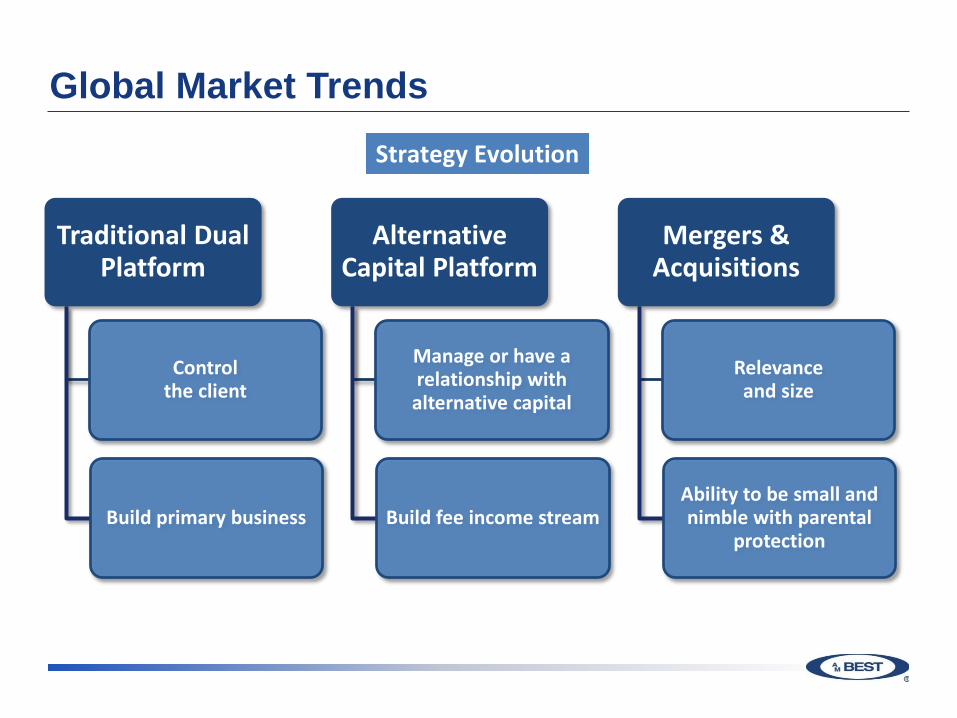

Global Market Trends

Traditional Dual Platform

Controlthe client

Build primary business

Alternative Capital Platform

Manage or have a relationship with

alternative capital

Build fee income stream

Mergers &Acquisitions

Relevanceand size

Ability to be small and nimble with parental

protection

Strategy Evolution

Global Market Trends

Potential Opportunities

Cyber Insurance Flood Mortgage Terrorism InsurTech US Tax

Reform

2018 Insurance Market Briefing - Germany

European (Re)Insurance Market Overview

Charlotte VigierSenior Financial Analyst

Konstantin LangowskiFinancial Analyst

Market Segment Outlooks

Examine the current trends in particular segments of the insurance industry over the next 12 months

Typical factors considered include current and forecast economic conditions; the regulatory environment and potential changes; emerging product developments; and competitive issues that could impact the success of the companies operating in the segment

A Best’s Market Segment Outlook, like a Best’s Credit Rating Outlook for a company, can be positive, negative, or stable

Many segments covered internationally

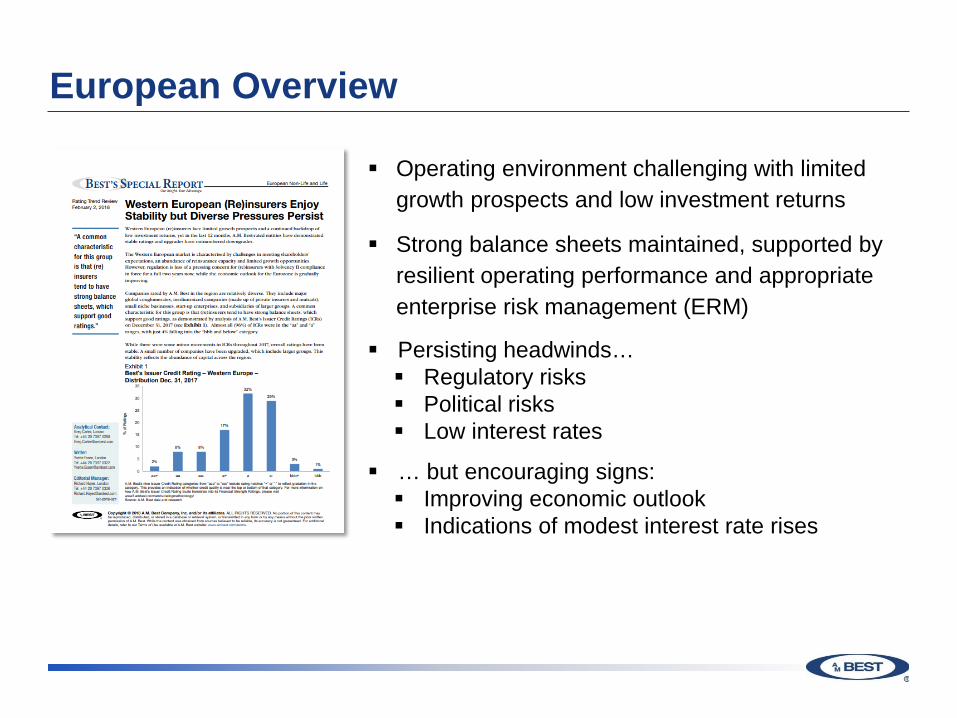

European Overview

Operating environment challenging with limited growth prospects and low investment returns

Strong balance sheets maintained, supported by resilient operating performance and appropriate enterprise risk management (ERM)

Persisting headwinds… Regulatory risks Political risks Low interest rates

… but encouraging signs: Improving economic outlook Indications of modest interest rate rises

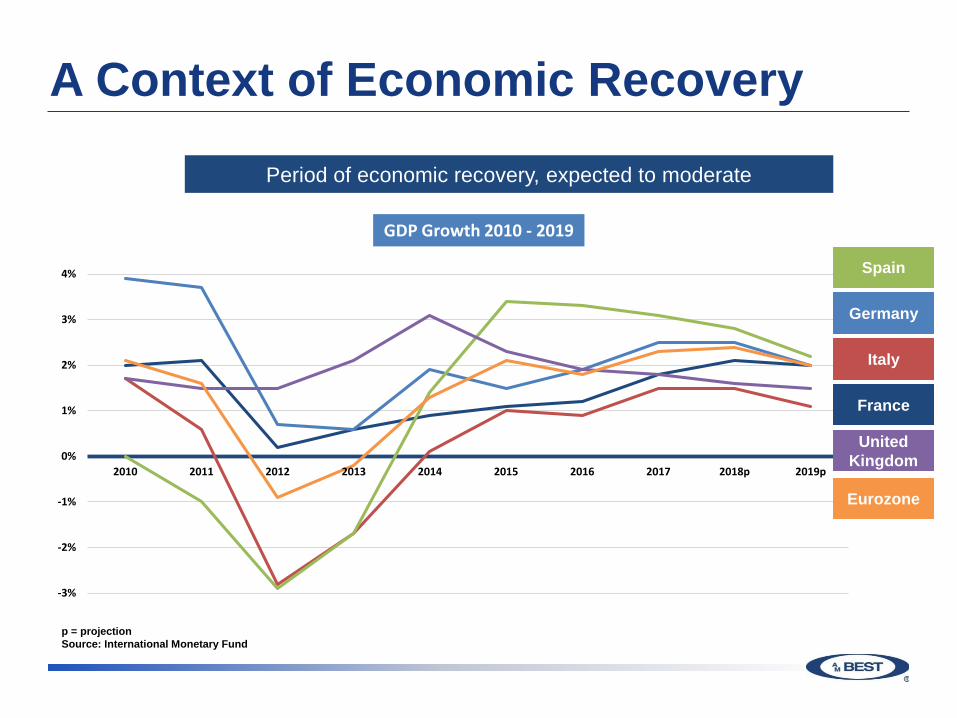

A Context of Economic Recovery

p = projectionSource: International Monetary Fund

Period of economic recovery, expected to moderate

GDP Growth 2010 - 2019

-3%

-2%

-1%

0%

1%

2%

3%

4%

2010 2011 2012 2013 2014 2015 2016 2017 2018p 2019p

Spain

Italy

France

United Kingdom

Germany

Eurozone

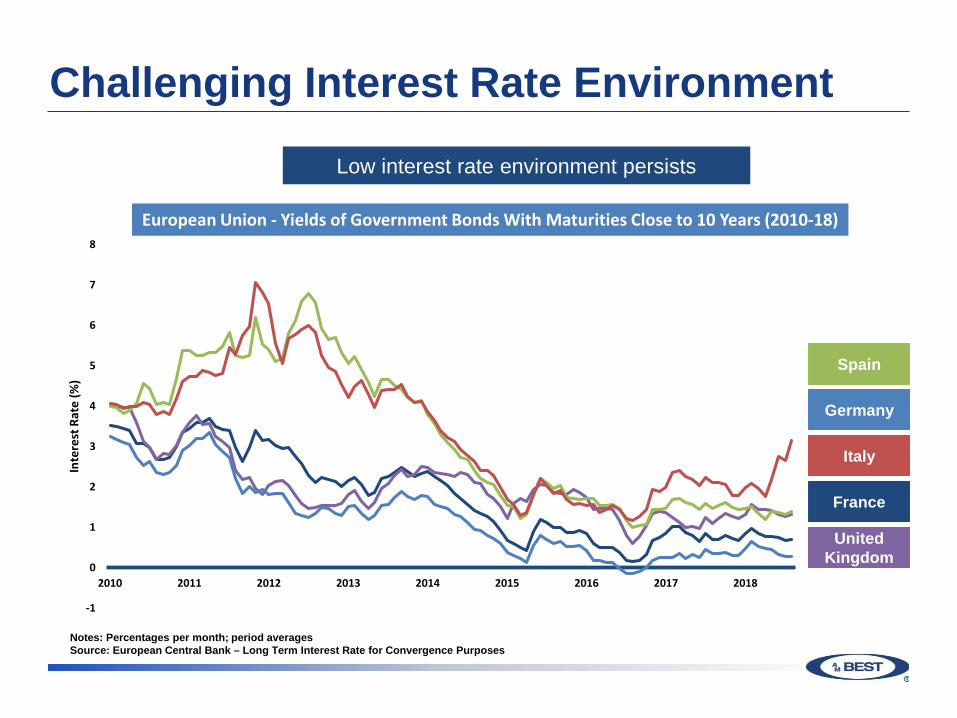

Challenging Interest Rate Environment

Low interest rate environment persists

European Union - Yields of Government Bonds With Maturities Close to 10 Years (2010-18)

-1

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015 2016 2017 2018

Inte

rest

Rat

e (%

)

Spain

Italy

France

United Kingdom

Germany

Notes: Percentages per month; period averagesSource: European Central Bank – Long Term Interest Rate for Convergence Purposes

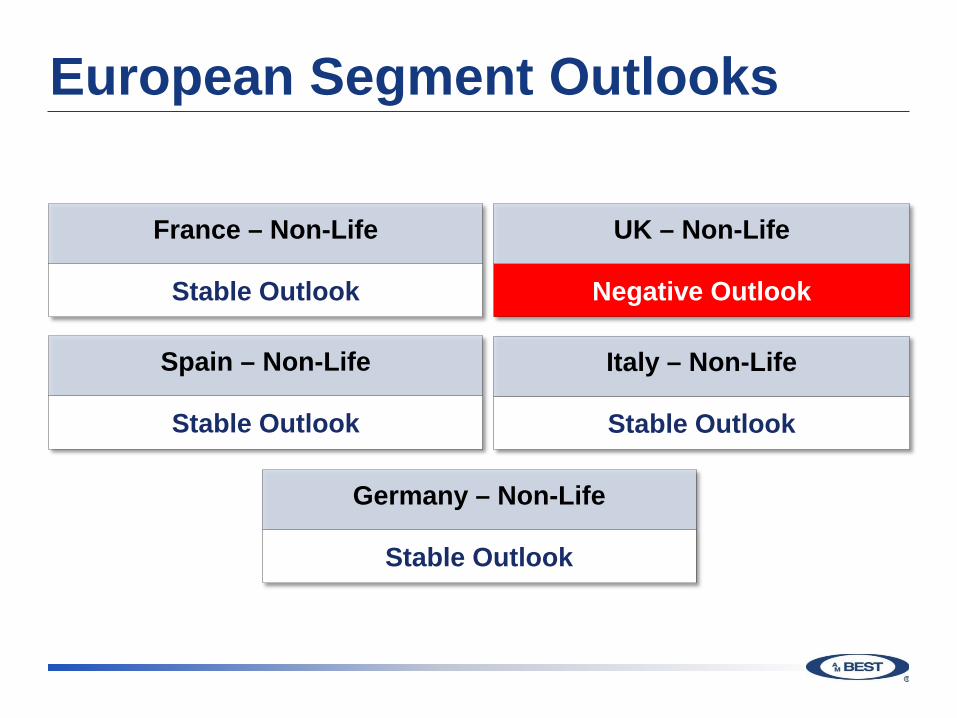

European Segment Outlooks

European Segment Outlooks

Stable Outlook

France – Non-Life

Stable Outlook

Spain – Non-Life

Negative Outlook

UK – Non-Life

Stable Outlook

Italy – Non-Life

Stable Outlook

Germany – Non-Life

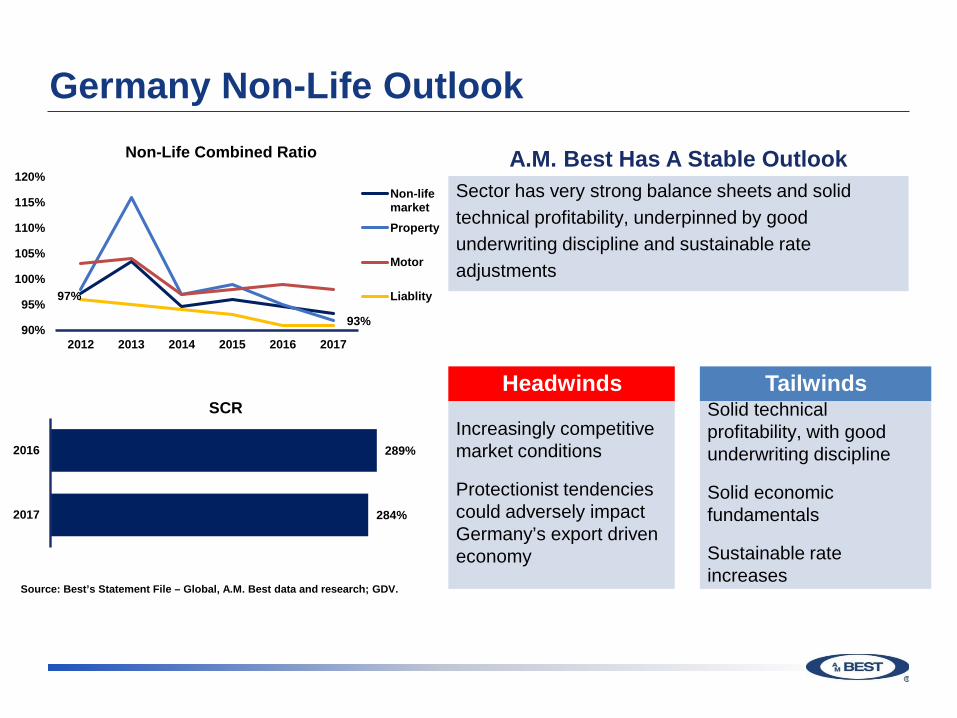

Germany Non-Life Outlook

A.M. Best Has A Stable OutlookSector has very strong balance sheets and solid technical profitability, underpinned by good underwriting discipline and sustainable rate adjustments

Headwinds

Increasingly competitive market conditions

Protectionist tendencies could adversely impact Germany’s export driven economy

TailwindsSolid technical profitability, with good underwriting discipline

Solid economic fundamentals

Sustainable rate increases

Source: Best’s Statement File – Global, A.M. Best data and research; GDV.

97%

93%90%

95%

100%

105%

110%

115%

120%

2012 2013 2014 2015 2016 2017

Non-Life Combined Ratio

Non-lifemarketProperty

Motor

Liablity

284%

289%

2017

2016

SCR

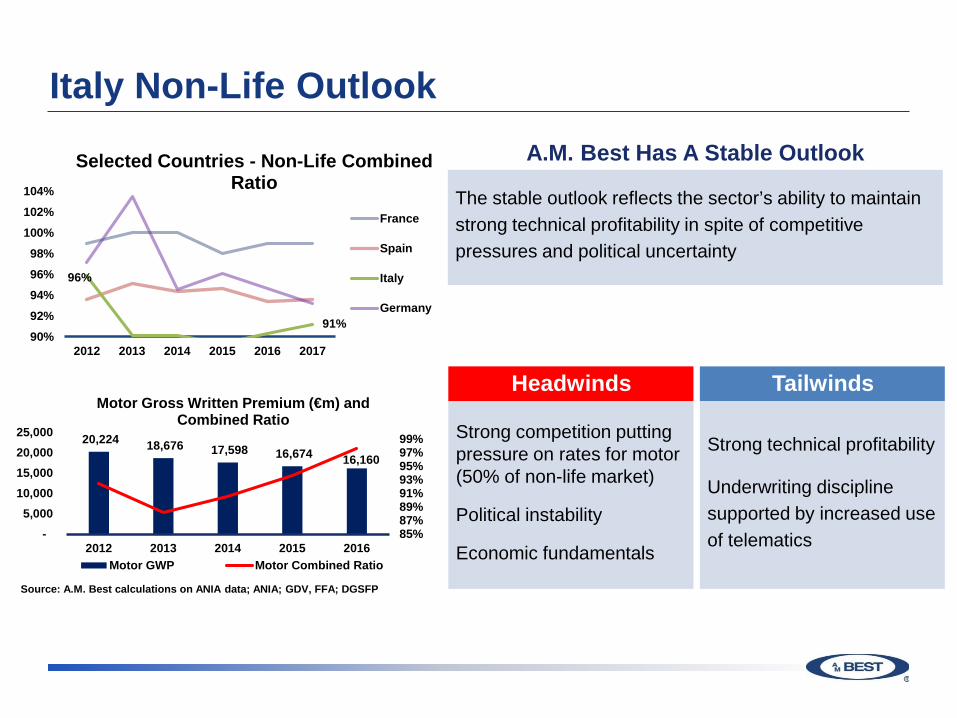

Italy Non-Life OutlookA.M. Best Has A Stable Outlook

The stable outlook reflects the sector’s ability to maintain strong technical profitability in spite of competitive pressures and political uncertainty

Headwinds

Strong competition putting pressure on rates for motor (50% of non-life market)

Political instability

Economic fundamentals

Tailwinds

Strong technical profitability

Underwriting discipline supported by increased use of telematics

Source: A.M. Best calculations on ANIA data; ANIA; GDV, FFA; DGSFP

20,224 18,676 17,598 16,674 16,160

85%87%89%91%93%95%97%99%

- 5,000

10,000 15,000 20,000 25,000

2012 2013 2014 2015 2016

Motor Gross Written Premium (€m) and Combined Ratio

Motor GWP Motor Combined Ratio

96%

91%90%92%94%96%98%

100%102%104%

2012 2013 2014 2015 2016 2017

Selected Countries - Non-Life Combined Ratio

France

Spain

Italy

Germany

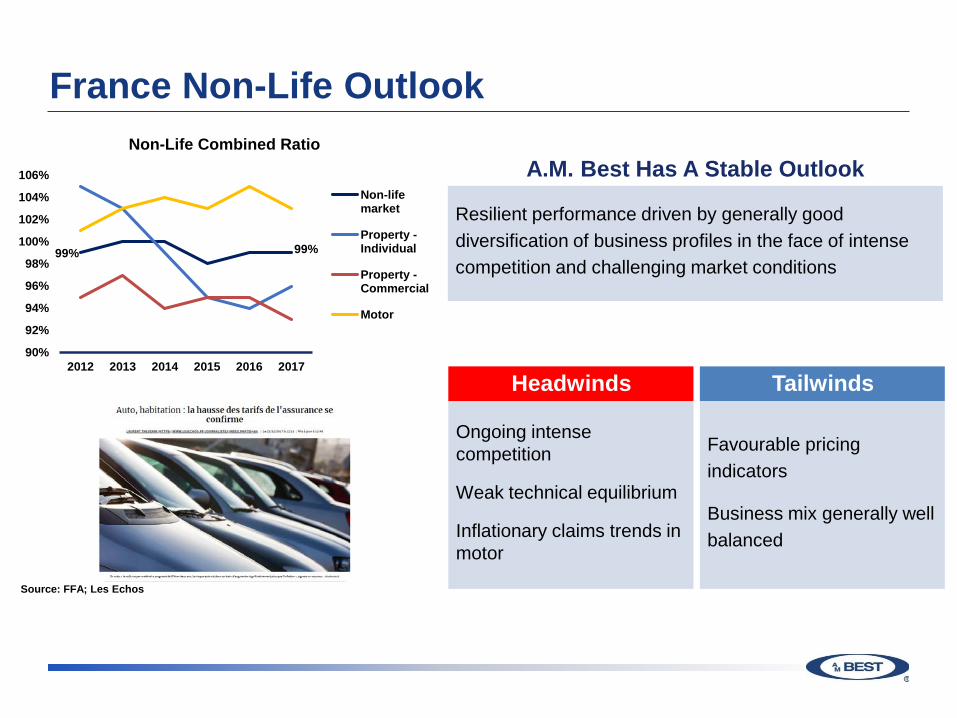

France Non-Life Outlook

A.M. Best Has A Stable Outlook

Resilient performance driven by generally good diversification of business profiles in the face of intense competition and challenging market conditions

Headwinds

Ongoing intense competition

Weak technical equilibrium

Inflationary claims trends in motor

Tailwinds

Favourable pricing indicators

Business mix generally well balanced

Source: FFA; Les Echos

99% 99%

90%

92%

94%

96%

98%

100%

102%

104%

106%

2012 2013 2014 2015 2016 2017

Non-Life Combined Ratio

Non-lifemarket

Property -Individual

Property -Commercial

Motor

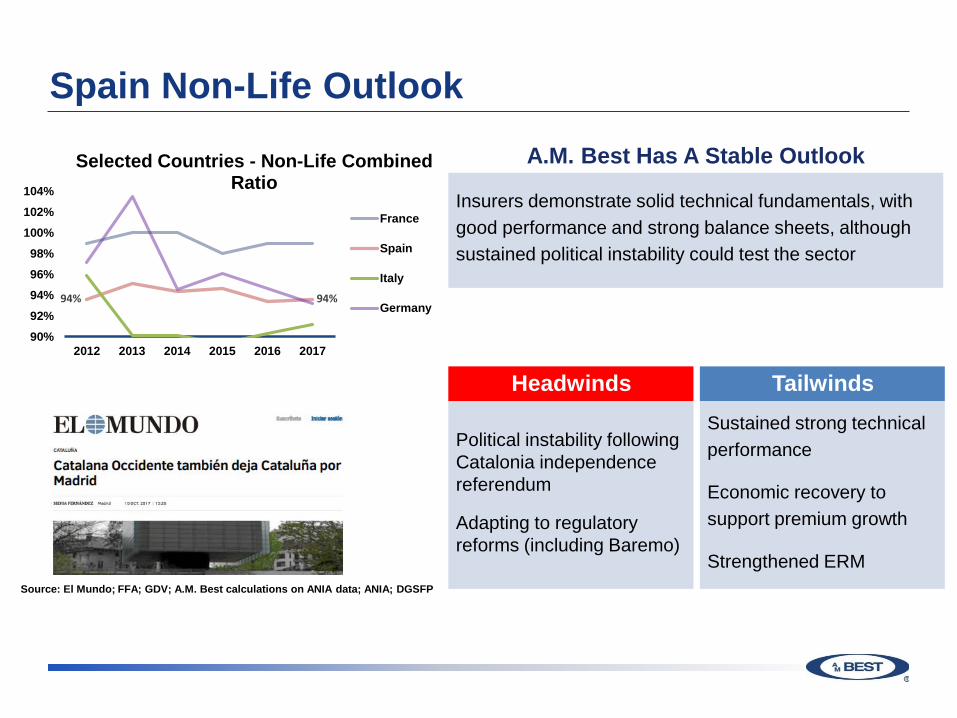

Spain Non-Life OutlookA.M. Best Has A Stable Outlook

Insurers demonstrate solid technical fundamentals, with good performance and strong balance sheets, although sustained political instability could test the sector

Headwinds

Political instability following Catalonia independence referendum

Adapting to regulatory reforms (including Baremo)

TailwindsSustained strong technical performance

Economic recovery to support premium growth

Strengthened ERMSource: El Mundo; FFA; GDV; A.M. Best calculations on ANIA data; ANIA; DGSFP

94% 94%

90%92%94%96%98%

100%102%104%

2012 2013 2014 2015 2016 2017

Selected Countries - Non-Life Combined Ratio

France

Spain

Italy

Germany

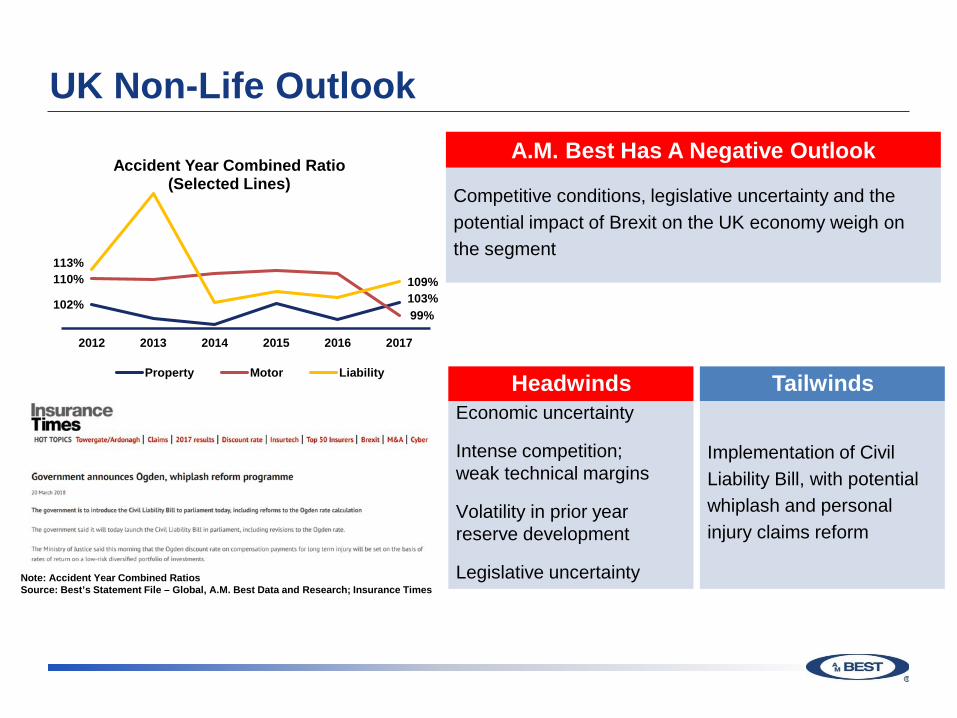

UK Non-Life OutlookA.M. Best Has A Negative Outlook

Competitive conditions, legislative uncertainty and the potential impact of Brexit on the UK economy weigh on the segment

HeadwindsEconomic uncertainty

Intense competition; weak technical margins

Volatility in prior year reserve development

Legislative uncertainty

Tailwinds

Implementation of Civil Liability Bill, with potential whiplash and personal injury claims reform

Note: Accident Year Combined RatiosSource: Best’s Statement File – Global, A.M. Best Data and Research; Insurance Times

102% 103%110%

99%

113%109%

2012 2013 2014 2015 2016 2017

Accident Year Combined Ratio (Selected Lines)

Property Motor Liability

Looking Forward

Key things to watch…

Competition continues to put technical margins under pressure

Ongoing focus on cost management, as insurers aim to preserve profitability in a highly competitive market and low investment return environment

Economic environment to present some opportunities for insurers, although dramatic growth not expected

Key things to watch…

Increasing focus on, and investment in, innovation and customer experience

Key things to watch…

Political Uncertainty

GDPR

IFRS17Legislative Reforms

Distribution Directive

External challenges persist

Brexit

2018 Insurance Market Briefing - Germany

A.M. Best's Revised Rating Methodology in Action:

A Case Study

Michael DunckleyAssociate Director,

Analytics

Catherine ThomasSenior Director,

Analytics

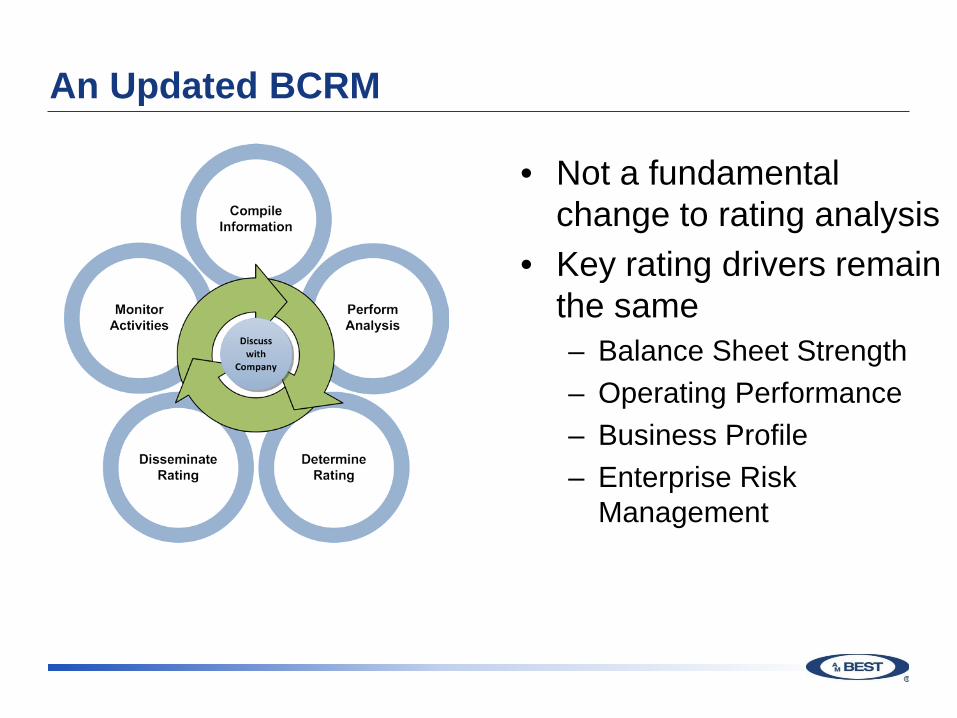

An Updated BCRM

• Not a fundamental change to rating analysis

• Key rating drivers remain the same– Balance Sheet Strength– Operating Performance– Business Profile– Enterprise Risk

Management

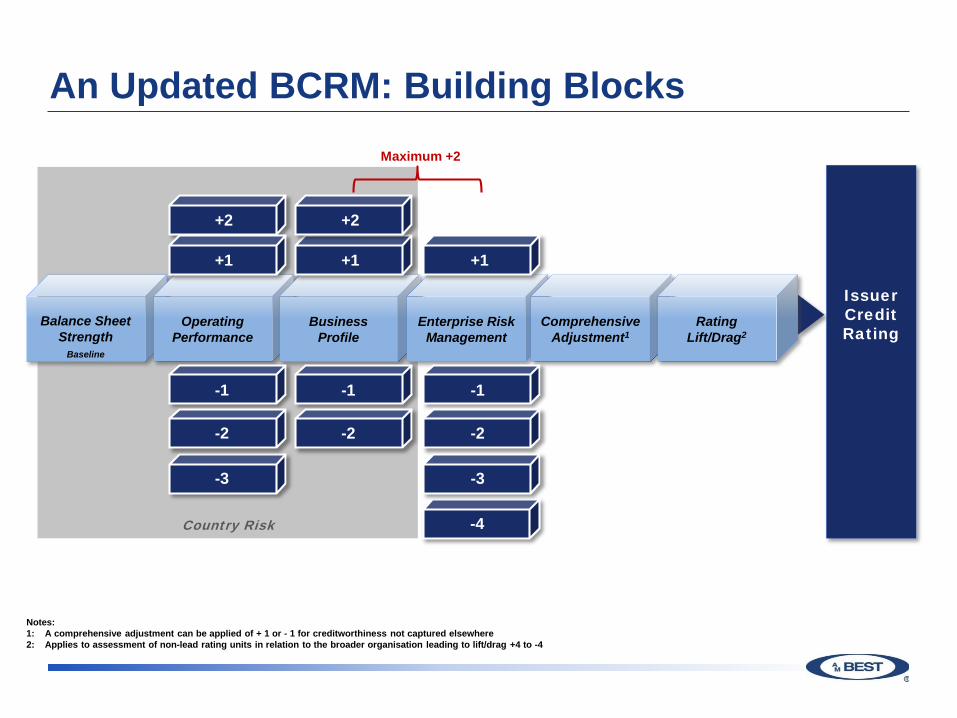

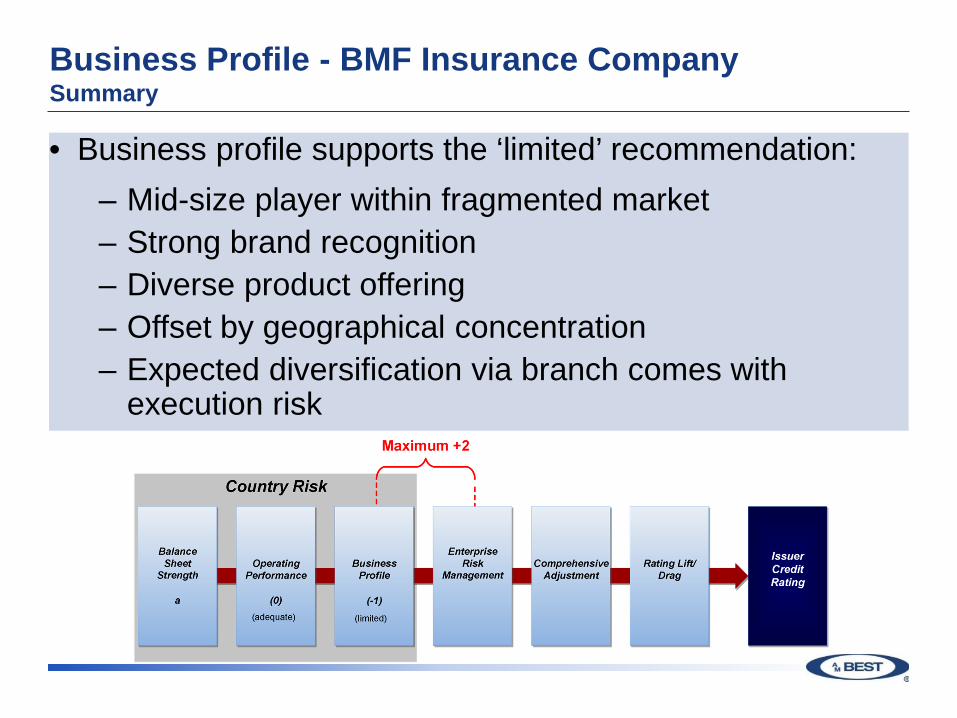

An Updated BCRM: Building Blocks

Balance Sheet Strength

Baseline

Operating Performance

BusinessProfile

Enterprise Risk Management

Comprehensive Adjustment1

RatingLift/Drag2

Issuer Credit Rating

Country Risk

+2

+1 +1 +1

-1

-2

-3

-1

-2

-3

-1

-2

+2

Maximum +2

-4

Notes:1: A comprehensive adjustment can be applied of + 1 or - 1 for creditworthiness not captured elsewhere2: Applies to assessment of non-lead rating units in relation to the broader organisation leading to lift/drag +4 to -4

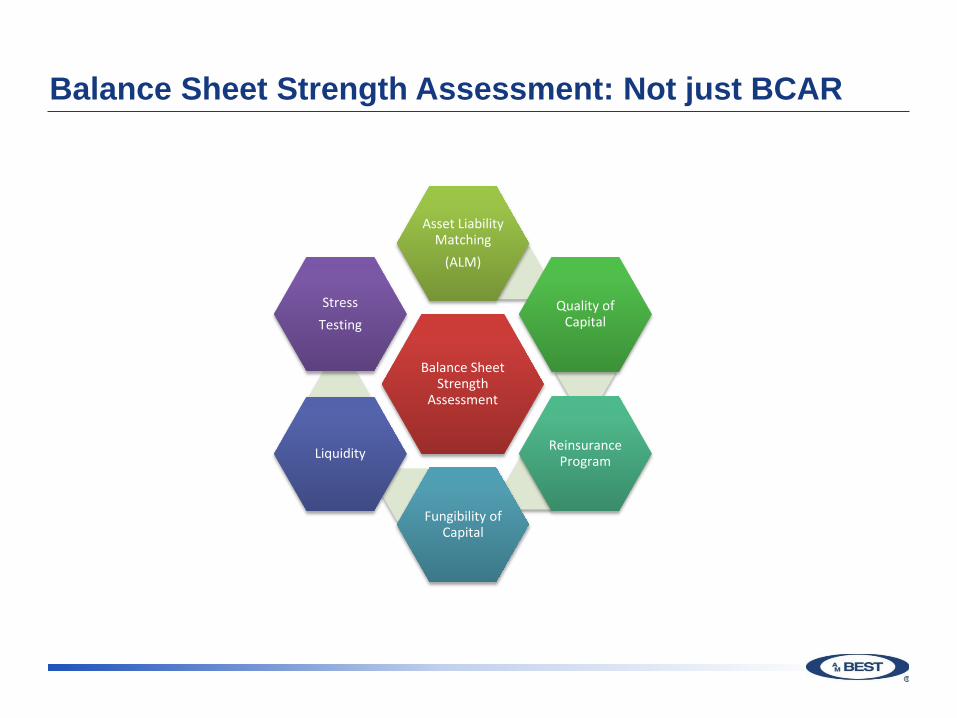

Balance Sheet Strength Assessment: Not just BCAR

A.M. Best - An Introduction 20 March 2018

Balance Sheet Strength

Assessment

Asset Liability Matching

(ALM)

Quality of Capital

Reinsurance Program

Fungibility of Capital

Liquidity

StressTesting

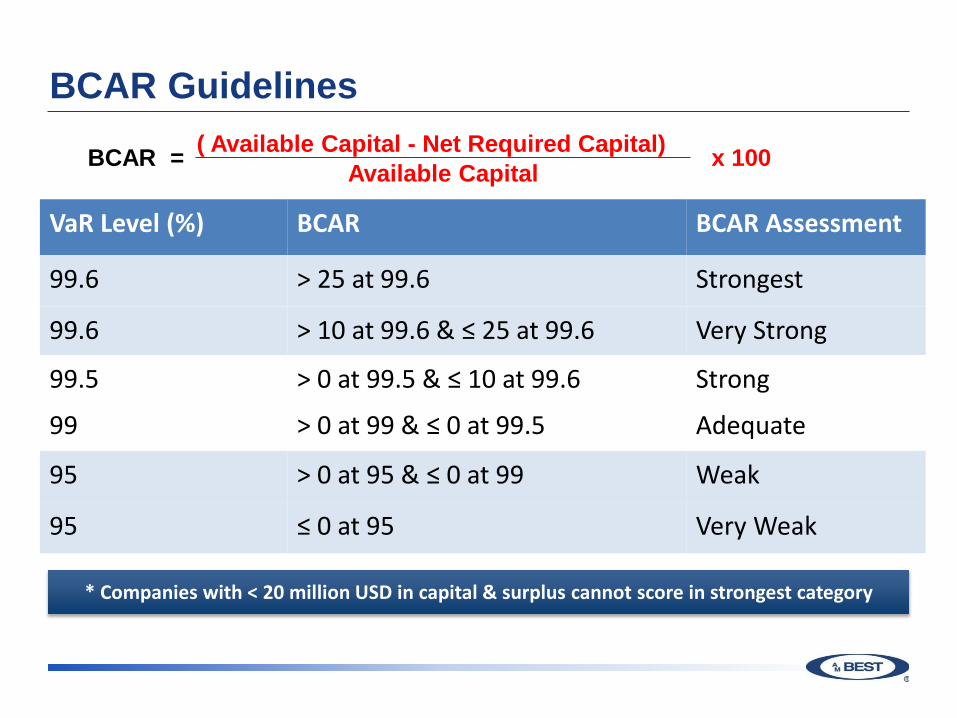

BCAR Guidelines

VaR Level (%) BCAR BCAR Assessment

99.6 > 25 at 99.6 Strongest

99.6 > 10 at 99.6 & ≤ 25 at 99.6 Very Strong

99.5 > 0 at 99.5 & ≤ 10 at 99.6 Strong

99 > 0 at 99 & ≤ 0 at 99.5 Adequate

95 > 0 at 95 & ≤ 0 at 99 Weak

95 ≤ 0 at 95 Very Weak

* Companies with < 20 million USD in capital & surplus cannot score in strongest category

BCAR = ( Available Capital - Net Required Capital) x 100Available Capital

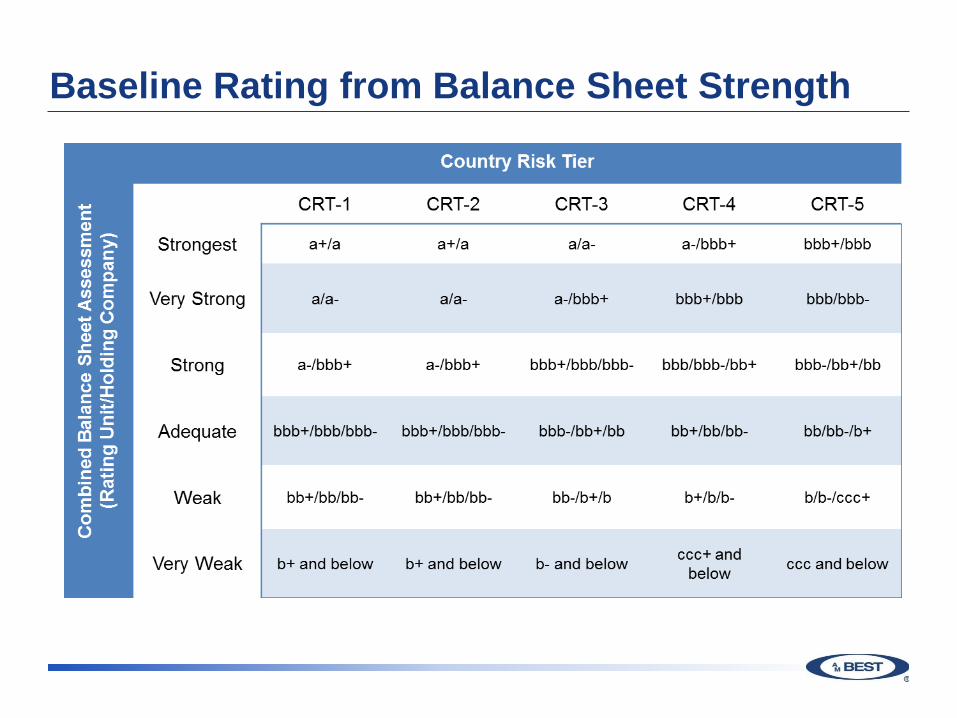

Baseline Rating from Balance Sheet Strength

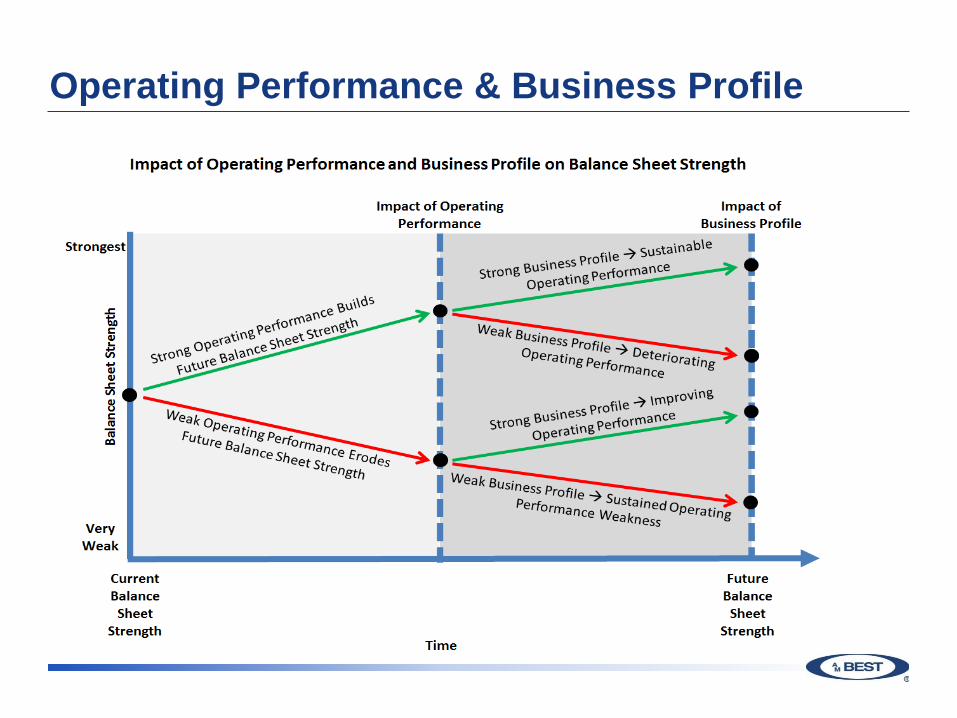

Operating Performance & Business Profile

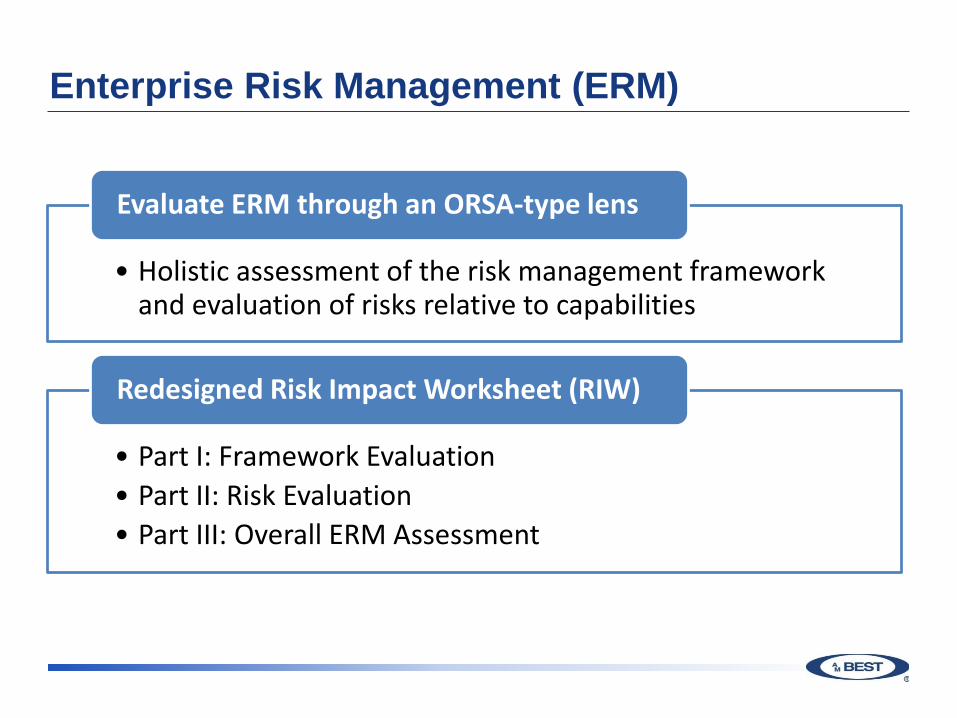

Enterprise Risk Management (ERM)

• Holistic assessment of the risk management framework and evaluation of risks relative to capabilities

Evaluate ERM through an ORSA-type lens

• Part I: Framework Evaluation• Part II: Risk Evaluation• Part III: Overall ERM Assessment

Redesigned Risk Impact Worksheet (RIW)

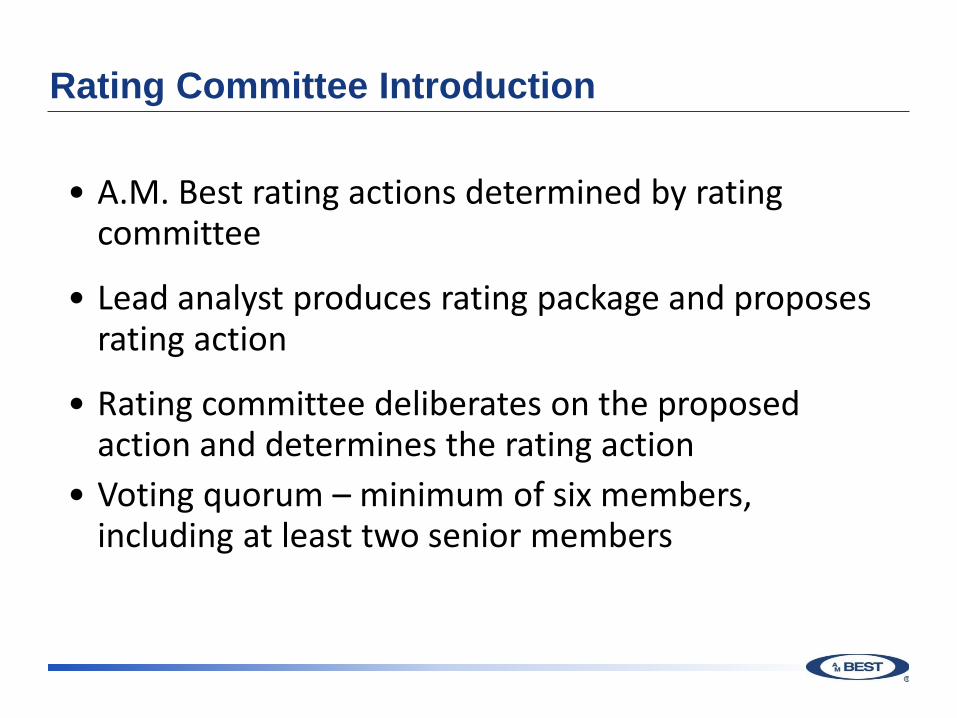

Rating Committee Introduction

• A.M. Best rating actions determined by rating committee

• Lead analyst produces rating package and proposes rating action

• Rating committee deliberates on the proposed action and determines the rating action

• Voting quorum – minimum of six members, including at least two senior members

Rating Committee Members

• Michael Dunckley, Associate Director (lead analyst)

• Angela Yeo, Senior Director (reviewer)

• Catherine Thomas, Senior Director (chair)

• Charlotte Vigier, Senior Financial Analyst

• Konstantin Langowski, Financial Analyst

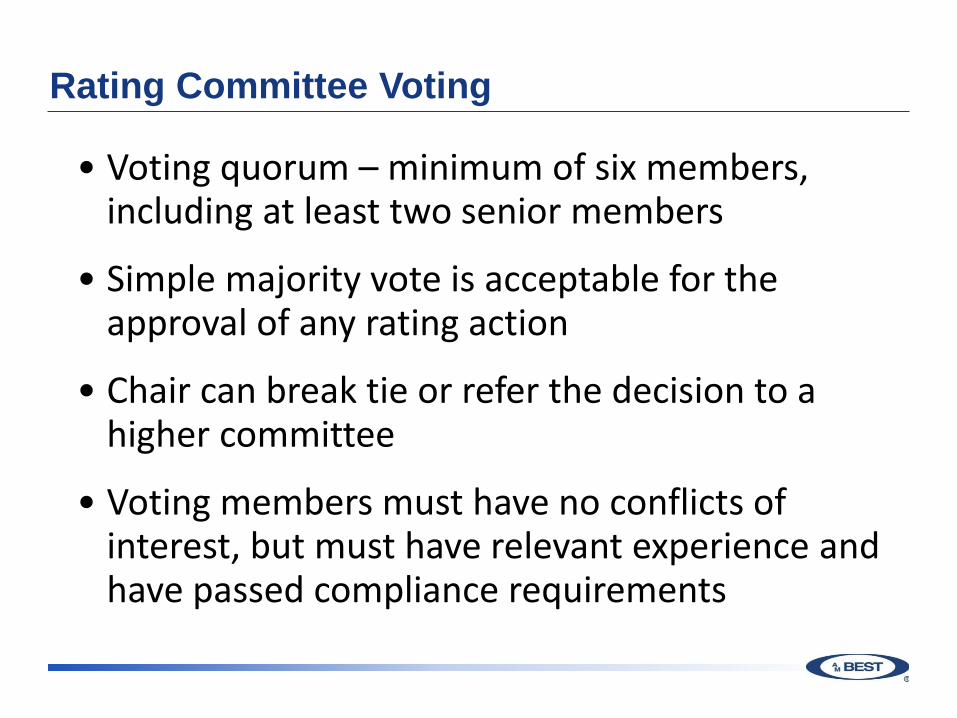

Rating Committee Voting

• Voting quorum – minimum of six members, including at least two senior members

• Simple majority vote is acceptable for the approval of any rating action

• Chair can break tie or refer the decision to a higher committee

• Voting members must have no conflicts of interest, but must have relevant experience and have passed compliance requirements

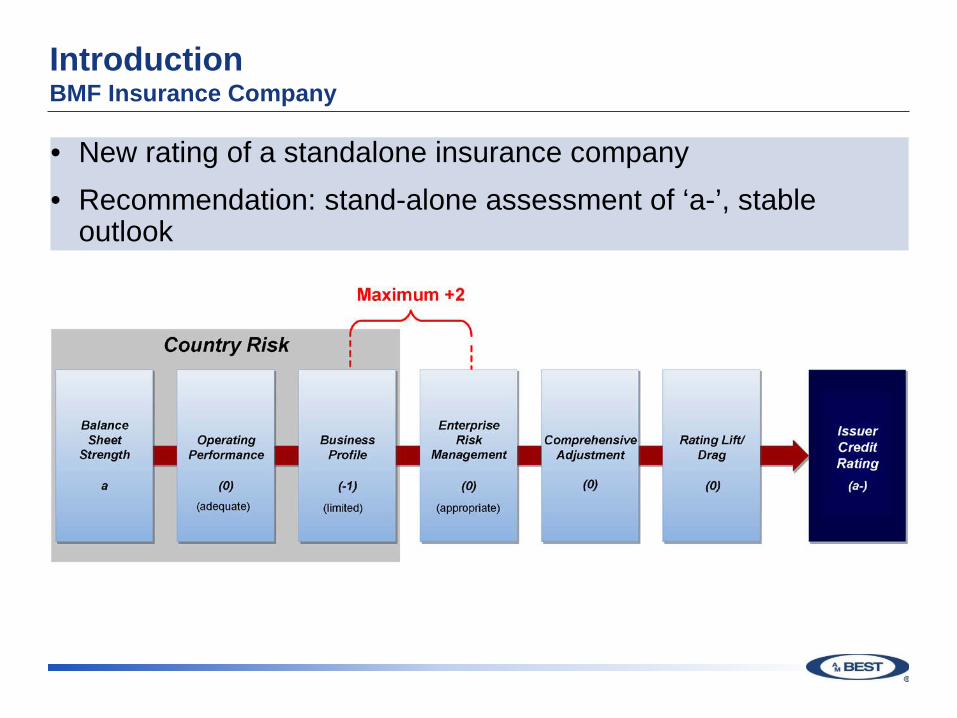

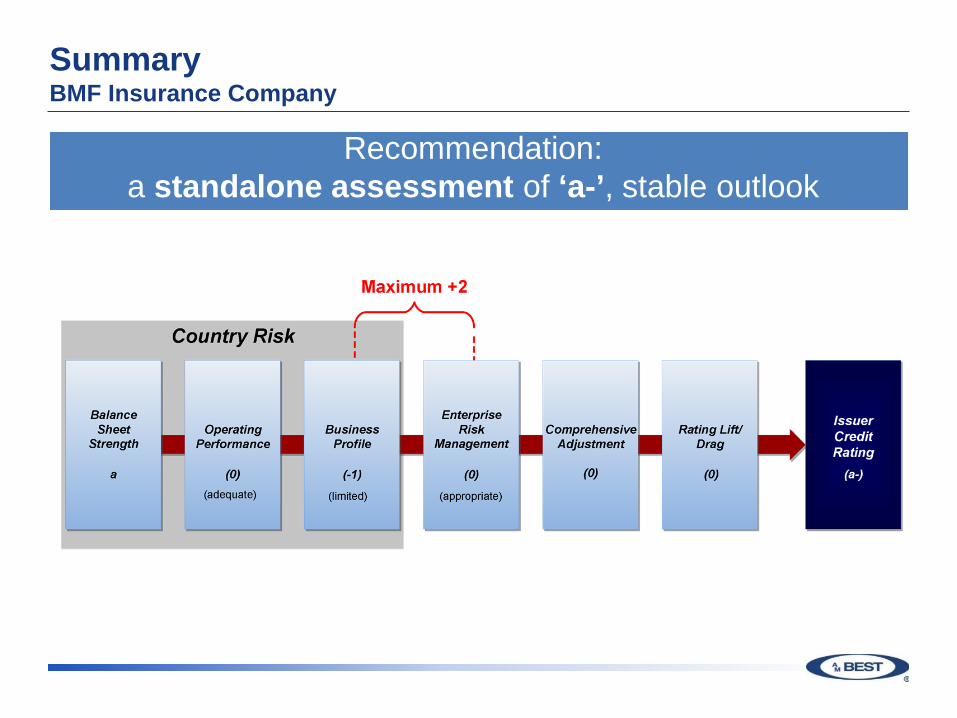

IntroductionBMF Insurance Company

• New rating of a standalone insurance company• Recommendation: stand-alone assessment of ‘a-’, stable

outlook

Overview - BMF Insurance CompanyOverview

• Domiciled in a small European country• Country Risk Tier 2 – stable operating environment• BMF Insurance Company (BMF) established 70 years

ago and is a private company• Fifth-largest insurer in its country of domicile • Management have in-depth knowledge and experience

of the local market

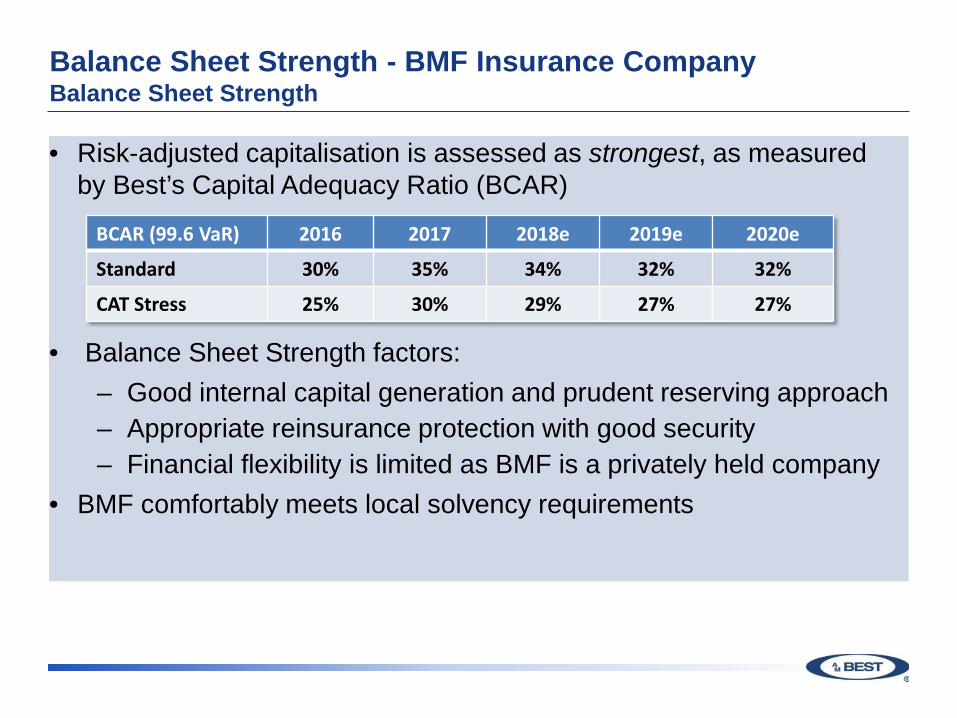

Balance Sheet Strength - BMF Insurance CompanyBalance Sheet Strength

• Risk-adjusted capitalisation is assessed as strongest, as measured by Best’s Capital Adequacy Ratio (BCAR)

• Balance Sheet Strength factors:– Good internal capital generation and prudent reserving approach– Appropriate reinsurance protection with good security– Financial flexibility is limited as BMF is a privately held company

• BMF comfortably meets local solvency requirements

BCAR (99.6 VaR) 2016 2017 2018e 2019e 2020e

Standard 30% 35% 34% 32% 32%

CAT Stress 25% 30% 29% 27% 27%

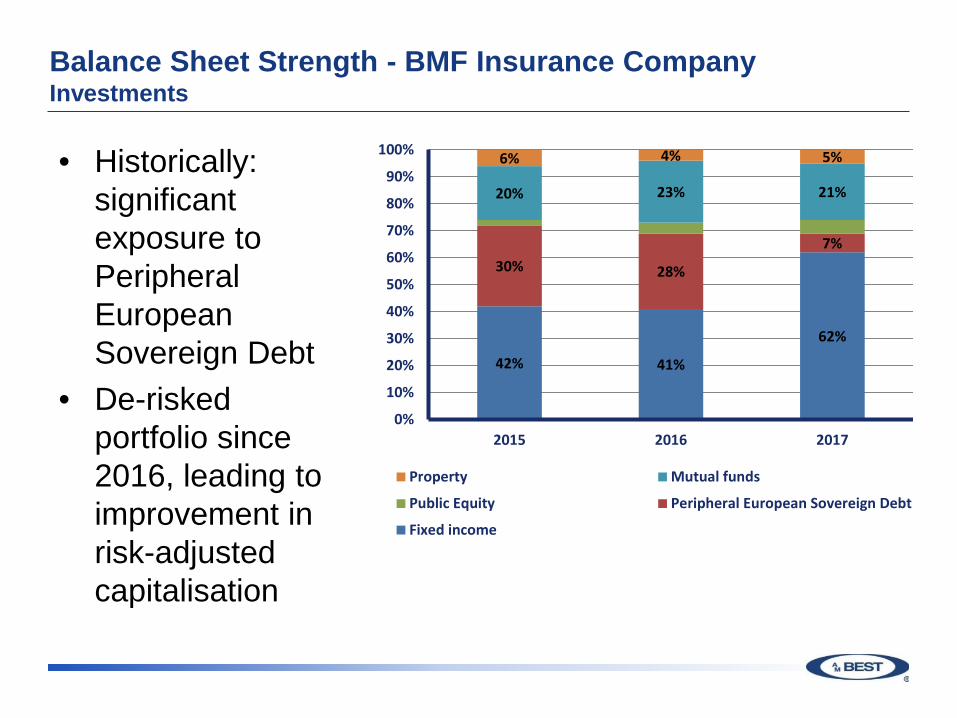

Balance Sheet Strength - BMF Insurance CompanyInvestments

• Historically: significant exposure to Peripheral European Sovereign Debt

• De-risked portfolio since 2016, leading to improvement in risk-adjusted capitalisation

42% 41%

62%

30% 28%

7%

20% 23% 21%

6% 4% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017

Property Mutual funds

Public Equity Peripheral European Sovereign Debt

Fixed income

Balance Sheet Strength - BMF Insurance CompanyReserving

• Reserves are reviewed by an internal actuary quarterly and by an external actuary annually

• Small margin in held reserves over external actuaries best estimate

• Loss triangles for the past 10 years indicate stability

• Modest reserve releases in each of the past three years

Balance Sheet Strength - BMF Insurance CompanyReinsurance

• Reinsurance includes both proportional and non-proportional arrangements

• 92% of reinsurers are rated “A-” or above• Limited cat risk in local market, earthquake risk is

borne by state reinsurer

Balance Sheet Strength - BMF Insurance CompanyKey factors

• BCAR scores in the ‘strongest’ range

• Good internal capital generation to support planned growth

• Stable reserve development

• Limited CAT risk

• Comprehensive reinsurance with high quality panel

• Limited financial flexibility• Sovereign risk exposure

has reduced• CRT-2 domicile

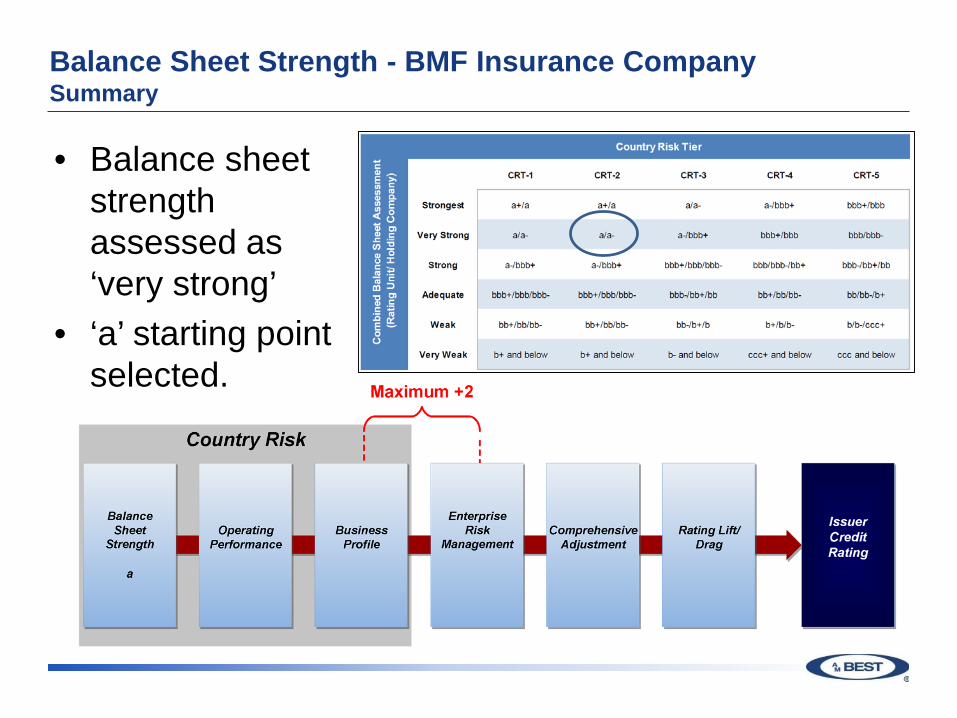

Balance Sheet Strength - BMF Insurance CompanySummary

• Balance sheet strength assessed as ‘very strong’

• ‘a’ starting point selected.

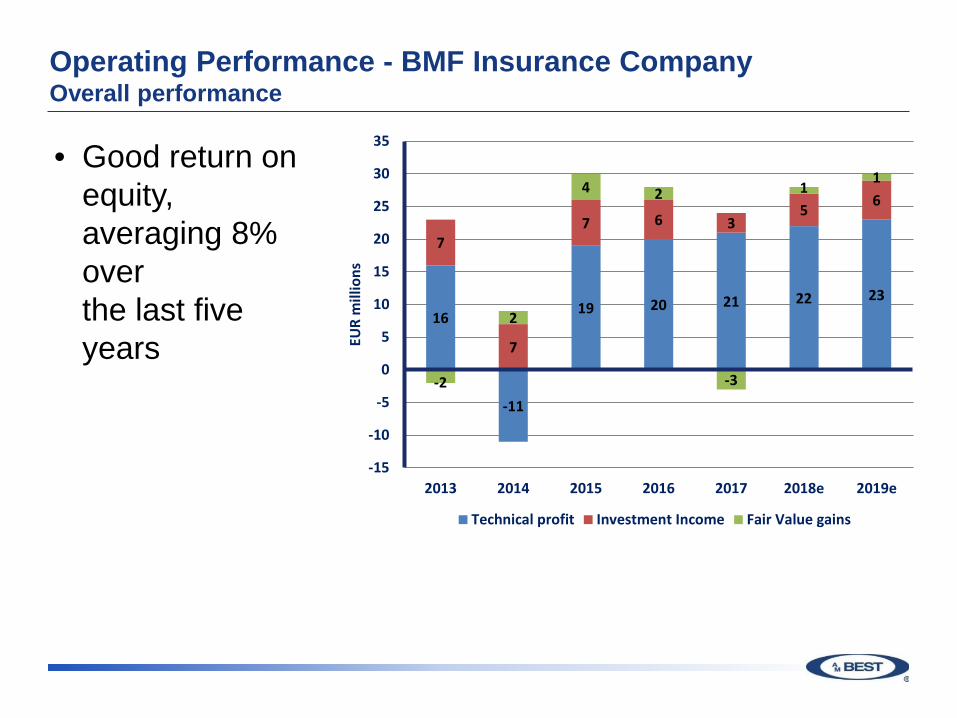

Operating Performance - BMF Insurance CompanyOverall performance

• Good return on equity, averaging 8% over the last five years

16

-11

19 20 21 22 23

7

7

7 6 35 6

-2

2

4 2

-3

11

-15

-10

-5

0

5

10

15

20

25

30

35

2013 2014 2015 2016 2017 2018e 2019e

EUR

mill

ions

Technical profit Investment Income Fair Value gains

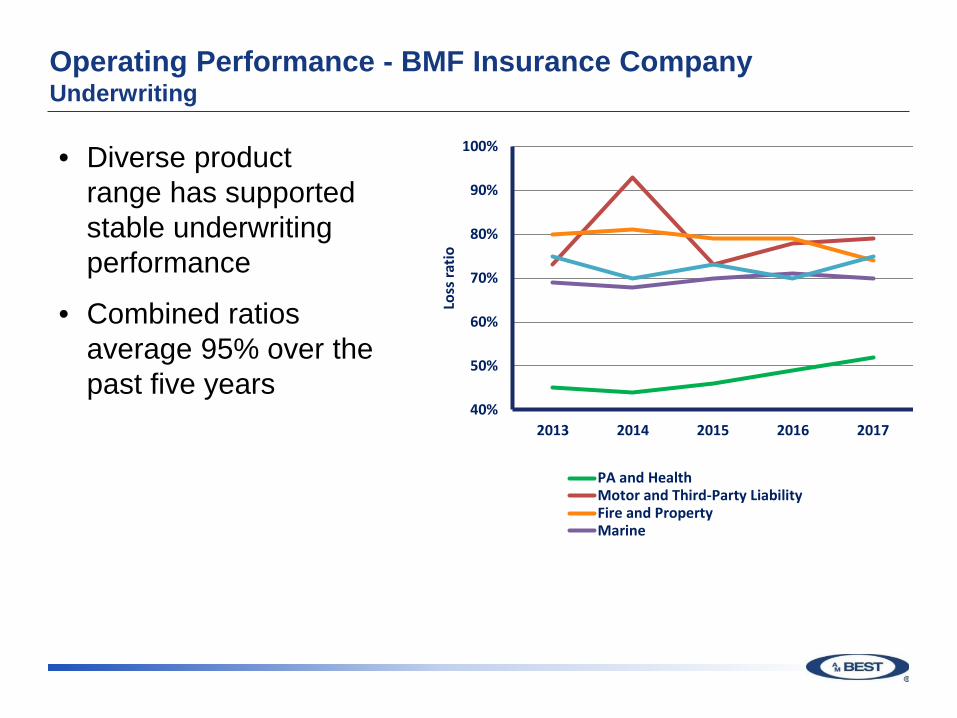

Operating Performance - BMF Insurance CompanyUnderwriting

• Diverse product range has supported stable underwriting performance

• Combined ratios average 95% over the past five years

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015 2016 2017Lo

ss ra

tio

PA and HealthMotor and Third-Party LiabilityFire and PropertyMarine

Operating Performance - BMF Insurance CompanyUnderwriting

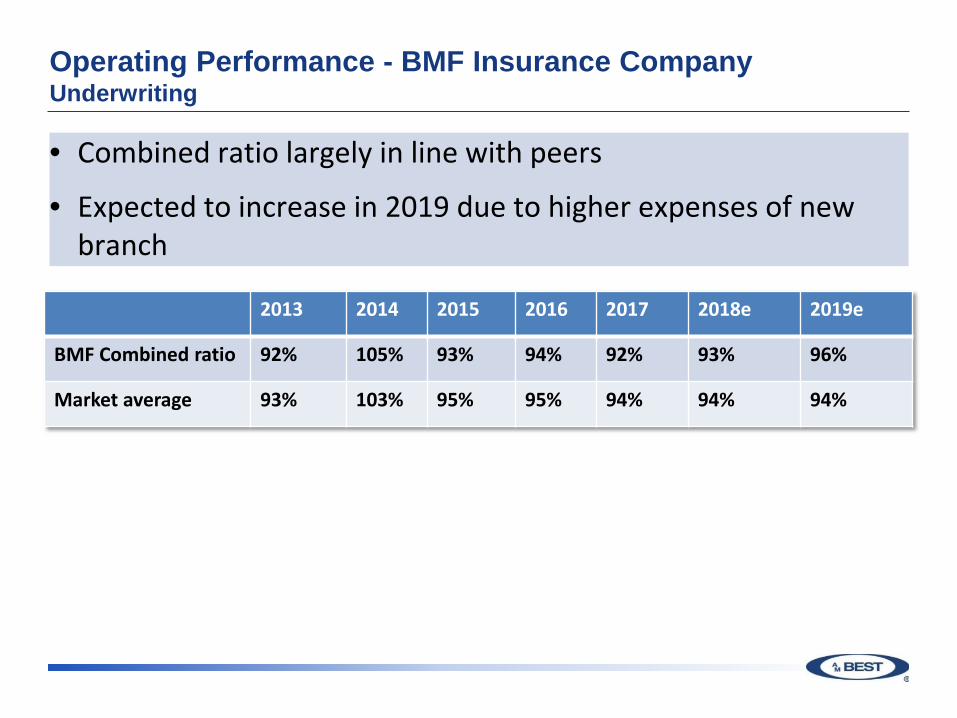

2013 2014 2015 2016 2017 2018e 2019e

BMF Combined ratio 92% 105% 93% 94% 92% 93% 96%

Market average 93% 103% 95% 95% 94% 94% 94%

• Combined ratio largely in line with peers

• Expected to increase in 2019 due to higher expenses of new branch

Operating Performance - BMF Insurance CompanyInvestment income

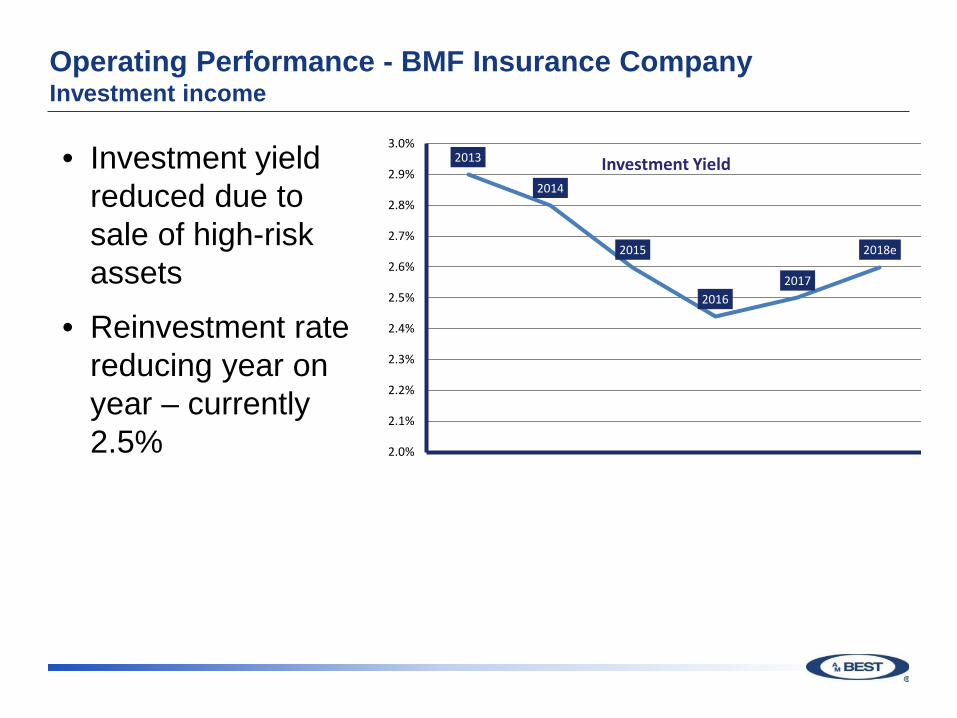

• Investment yield reduced due to sale of high-risk assets

• Reinvestment rate reducing year on year – currently 2.5%

2013

2014

2015

20162017

2018e

2.0%

2.1%

2.2%

2.3%

2.4%

2.5%

2.6%

2.7%

2.8%

2.9%

3.0%

Investment Yield

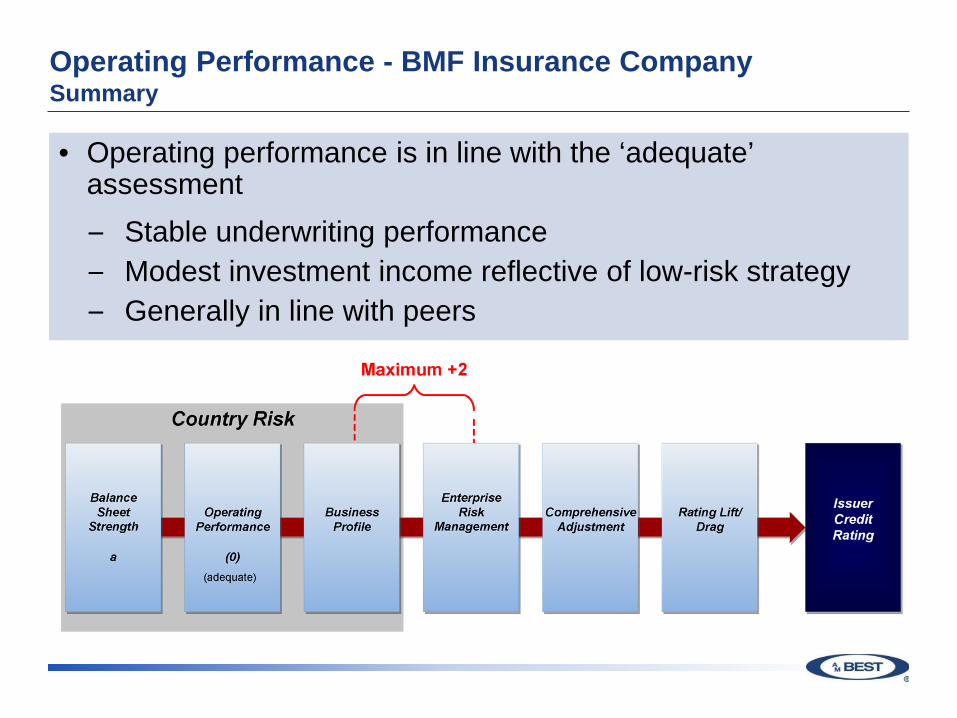

Operating Performance - BMF Insurance CompanySummary

• Operating performance is in line with the ‘adequate’ assessment– Stable underwriting performance– Modest investment income reflective of low-risk strategy– Generally in line with peers

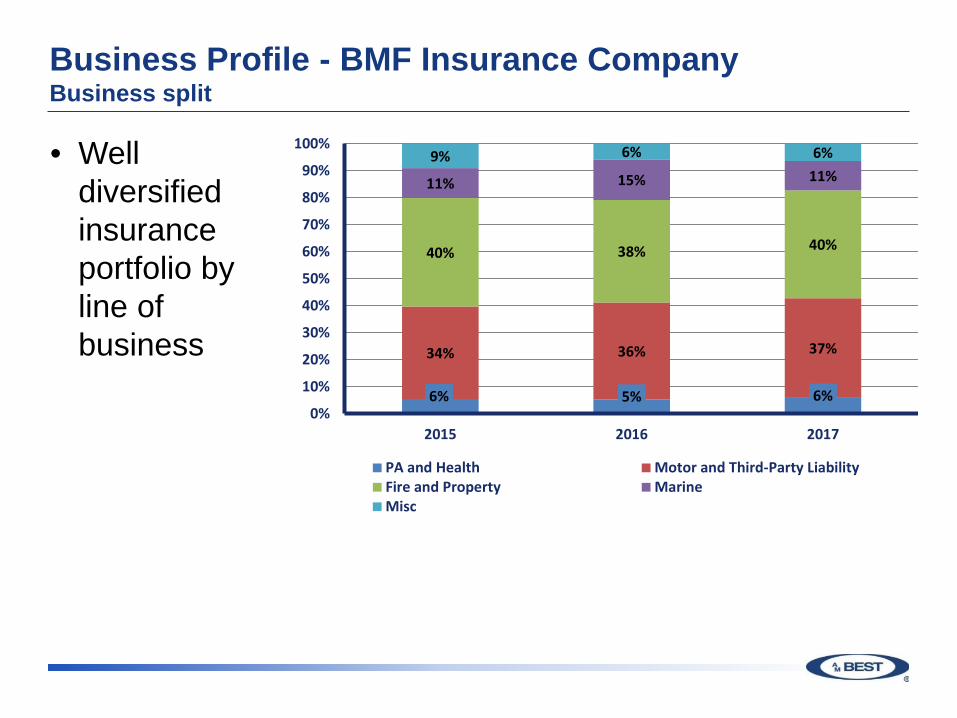

Business Profile - BMF Insurance CompanyBusiness split

• Well diversified insurance portfolio by line of business

6% 5% 6%

34% 36% 37%

40% 38% 40%

11% 15% 11%9% 6% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017

PA and Health Motor and Third-Party LiabilityFire and Property MarineMisc

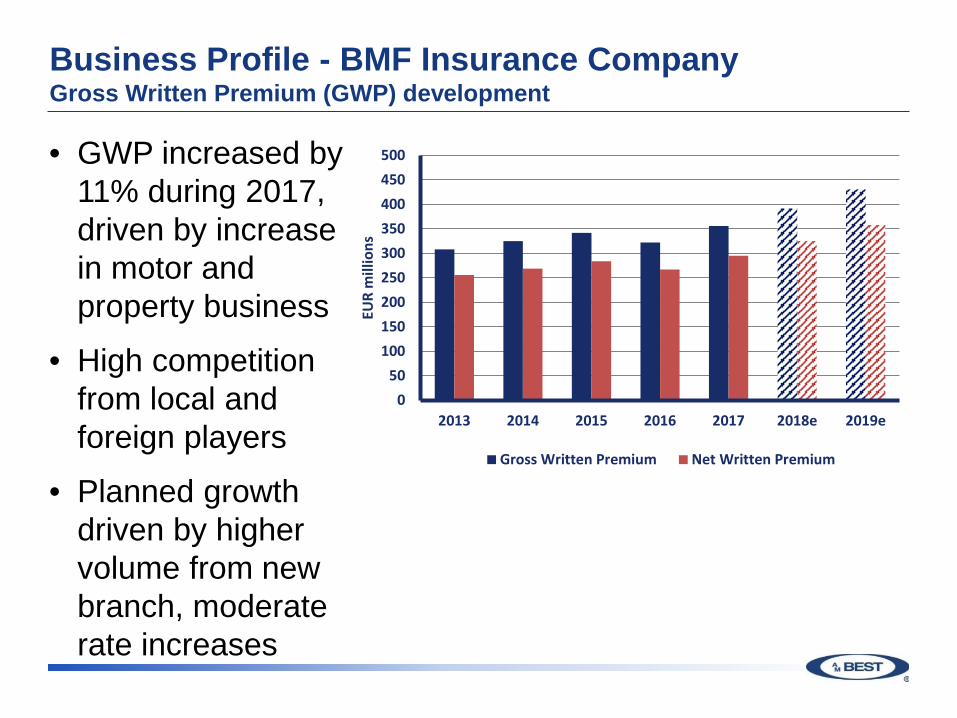

Business Profile - BMF Insurance CompanyGross Written Premium (GWP) development

• GWP increased by 11% during 2017, driven by increase in motor and property business

• High competition from local and foreign players

• Planned growth driven by higher volume from new branch, moderate rate increases

050

100150200250300350400450500

2013 2014 2015 2016 2017 2018e 2019e

EUR

mill

ions

Gross Written Premium Net Written Premium

Business Profile - BMF Insurance CompanyBusiness plans

• Geographically concentrated, only writing local business

• Plans to open a branch in a neighbouring country in 2019 to diversify geographically

• Growth of 10 - 15% expected over each of the next three years, includes growth via new branch

• New branch represents execution risk

Business Profile - BMF Insurance CompanySummary

• Business profile supports the ‘limited’ recommendation: – Mid-size player within fragmented market– Strong brand recognition– Diverse product offering– Offset by geographical concentration– Expected diversification via branch comes with

execution risk

Enterprise Risk ManagementBMF Insurance Company

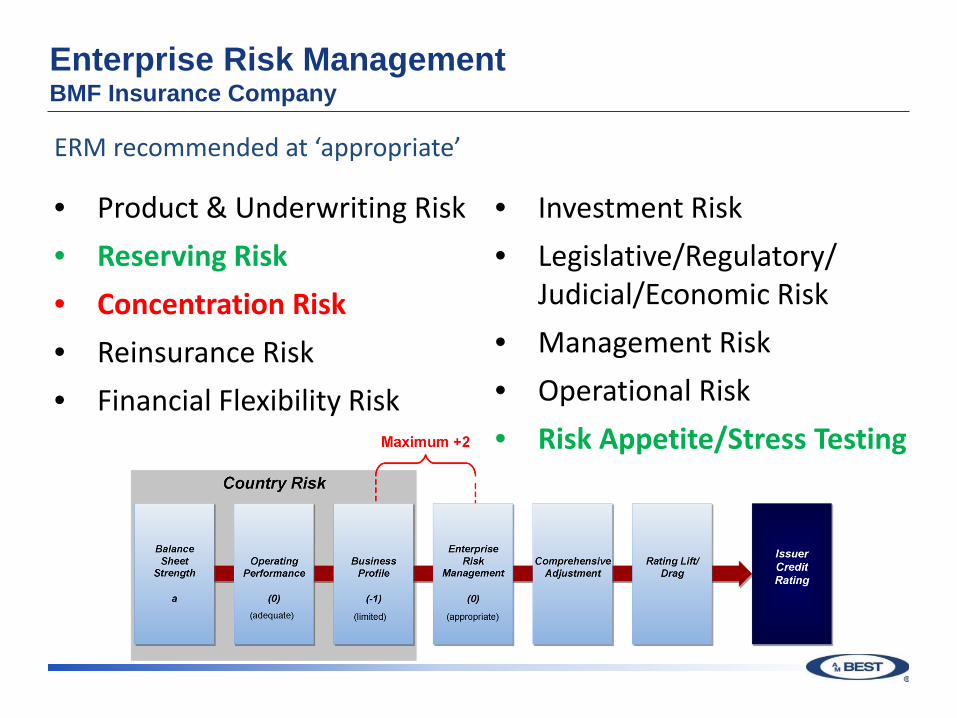

Principal areas of focus – Risk Categories

• Product & Underwriting Risk• Reserving Risk• Concentration Risk• Reinsurance Risk• Financial Flexibility Risk

• Investment Risk• Legislative/Regulatory/

Judicial/Economic Risk• Management Risk• Operational Risk• Risk Appetite/Stress Testing

Enterprise Risk ManagementBMF Insurance Company

• Product & Underwriting Risk• Reserving Risk• Concentration Risk• Reinsurance Risk• Financial Flexibility Risk

• Investment Risk• Legislative/Regulatory/

Judicial/Economic Risk• Management Risk• Operational Risk• Risk Appetite/Stress Testing

ERM recommended at ‘appropriate’

SummaryBMF Insurance Company

Recommendation: a standalone assessment of ‘a-’, stable outlook

Q&A

2018 Insurance Market Briefing – Europe& Methodology Review Seminar

Tuesday 6 November, 2018:2018 Insurance Market Briefing – Europe08:30 – 13:00 GMT, followed by lunchMethodology Review Seminar14:00 – 16:00 GMT

etc. venues St Paul's, London200 Aldersgate, London, EC1A 4HD

EMEA Market Overview ● Reinsurance ●Environmental, Social, and Governance ●Technology in Insurance Panel

Notable Developments since last year’s Best's Credit Rating Methodology Update ● BCRM –Key Changes, Impacts and Expectations ● Mock Rating Committee

There is no cost to attend the Briefing or Seminar, but registration is required as space is limited.

2018 Insurance Market Briefing -Germany

Hotel Pullman, Cologne – 27 September 2018