Embed Size (px)

Citation preview

Federal Reserve Challenge

Agenda

● Current Economic Conditions● Risks to the Economy● Forecast● Policy Recommendation

2

Current Economic Conditions

Financial markets support economic growth.

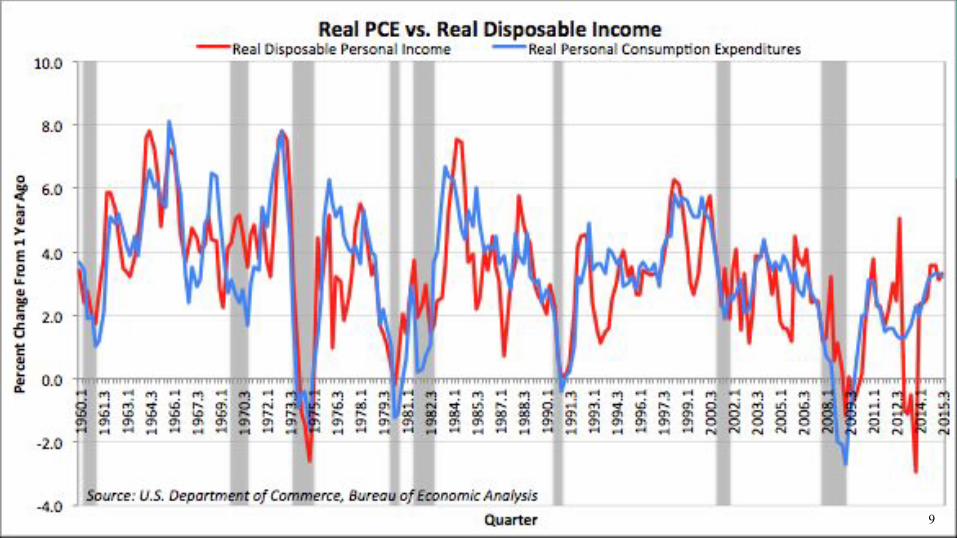

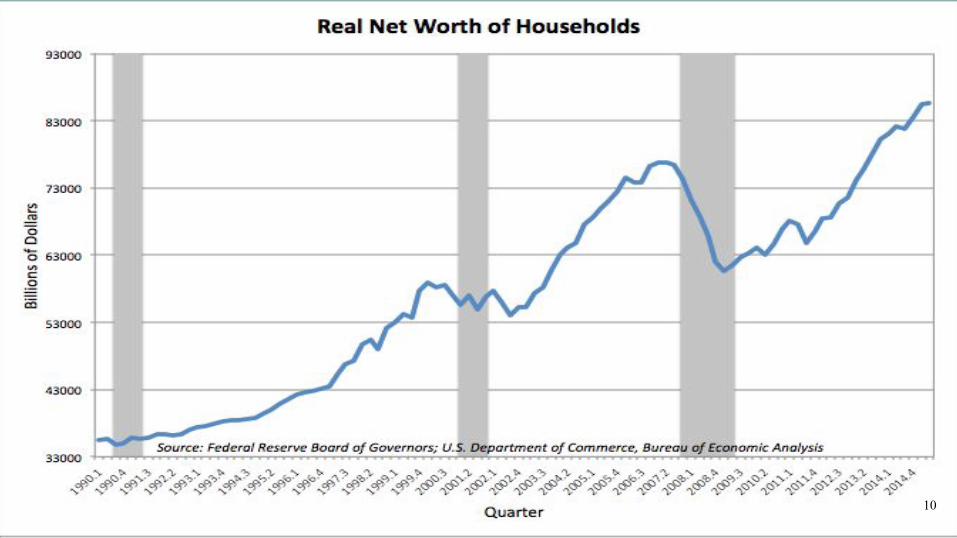

Aggregate demand is strengthening due to stronger consumption, investment, and government purchases; only net exports are weak.

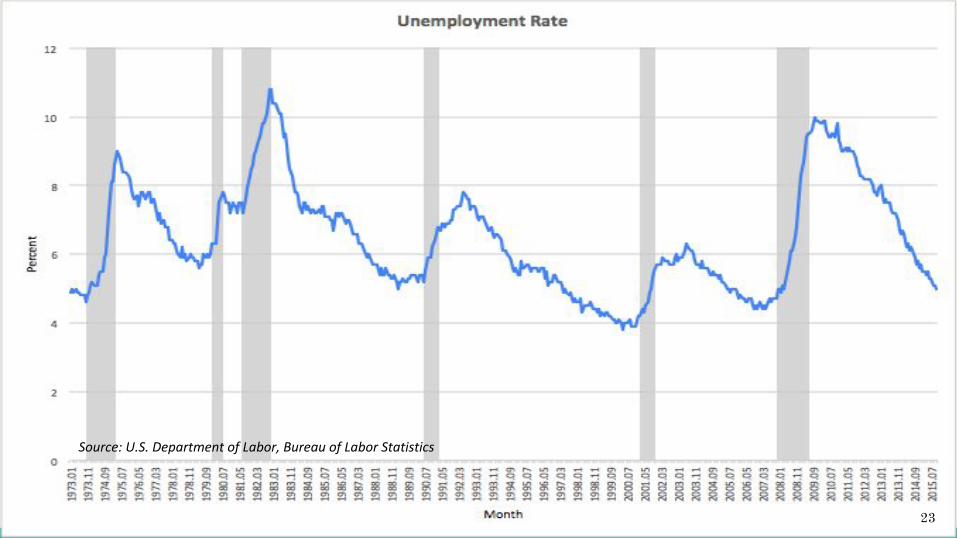

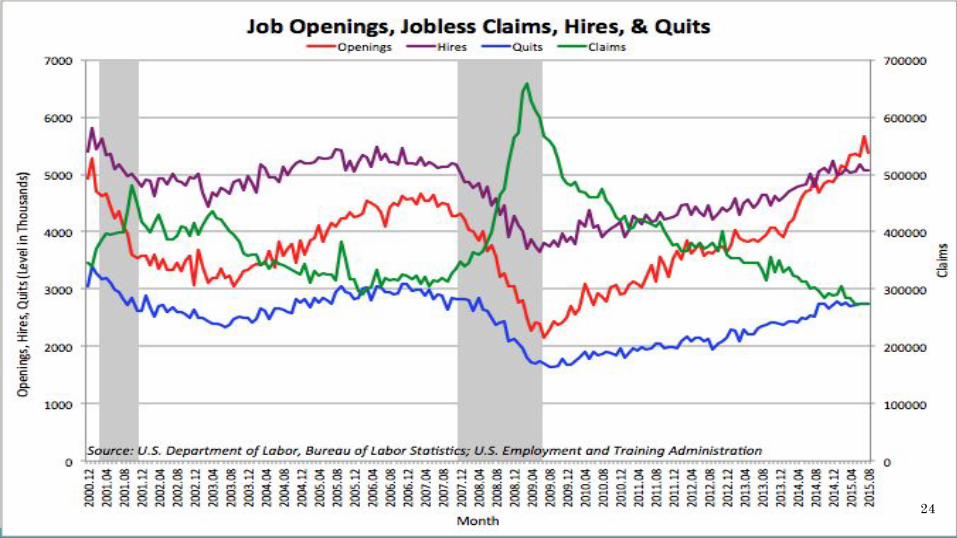

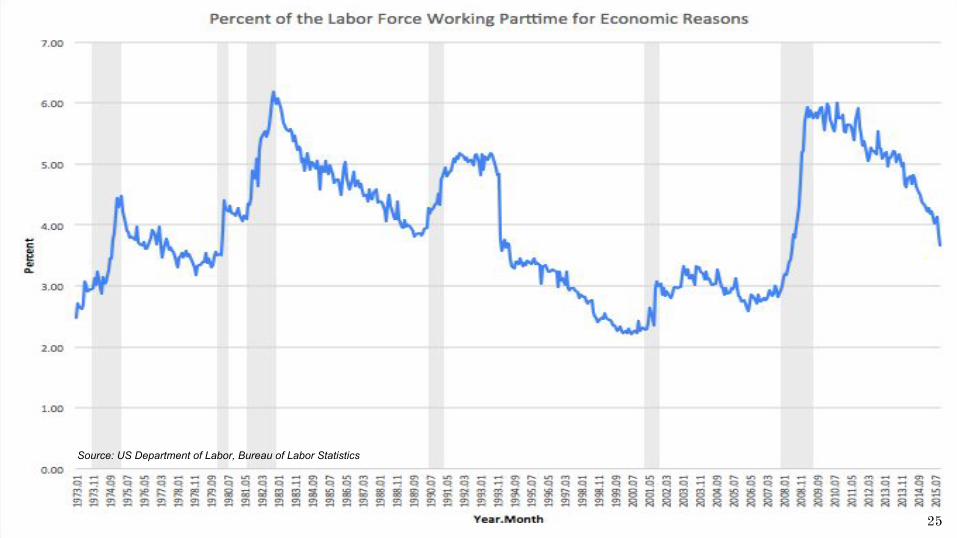

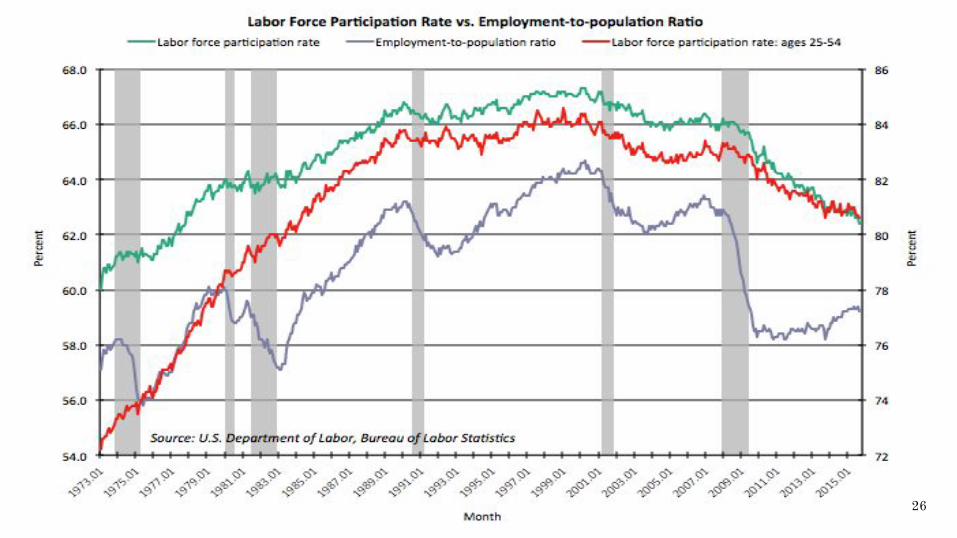

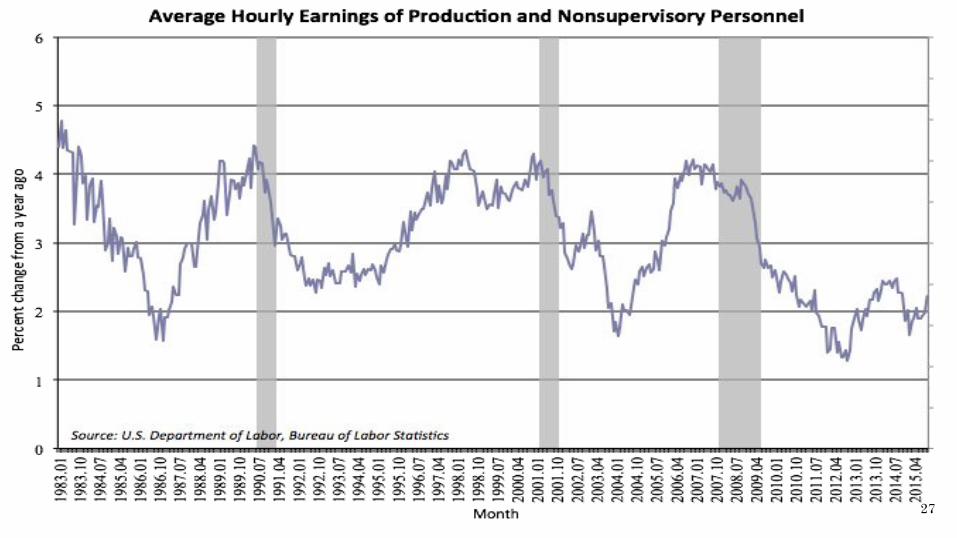

Labor markets are improving but evidence of slack still remains.

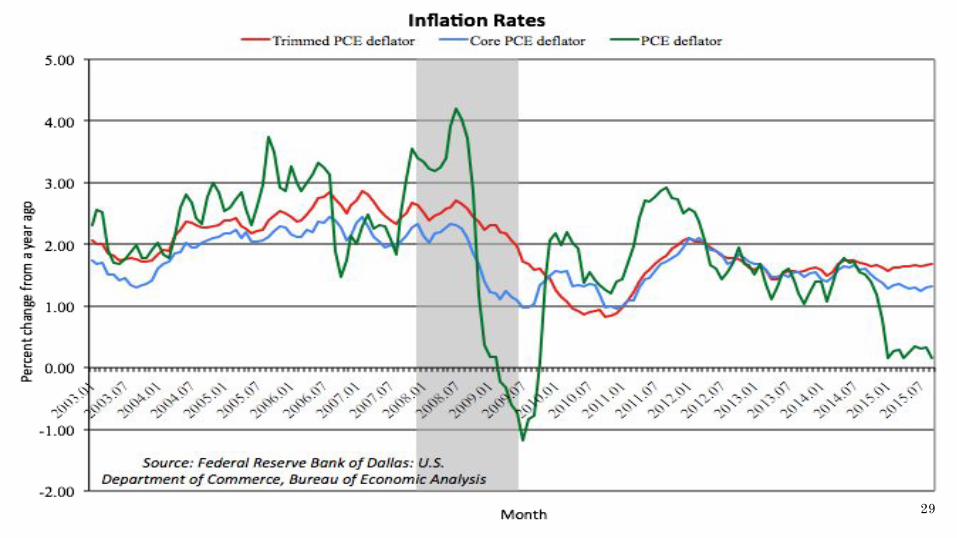

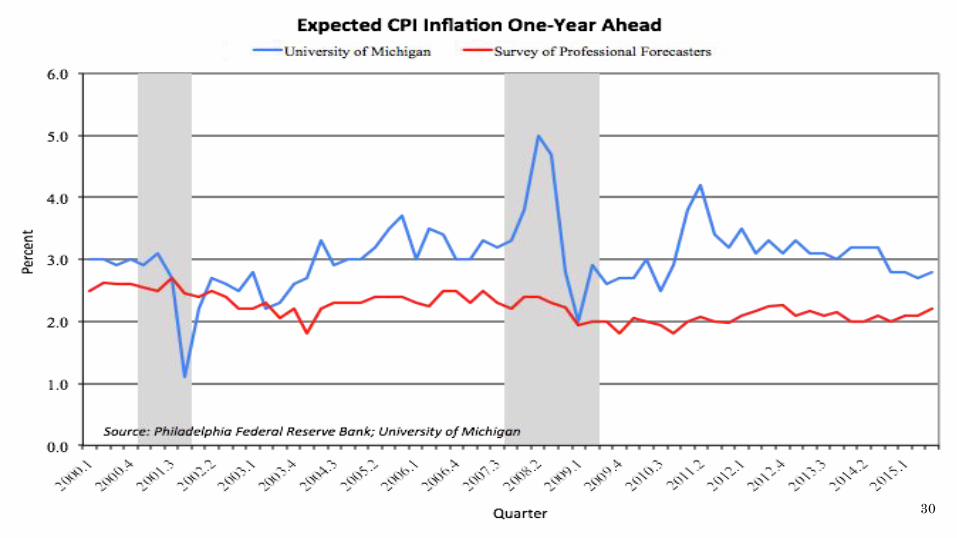

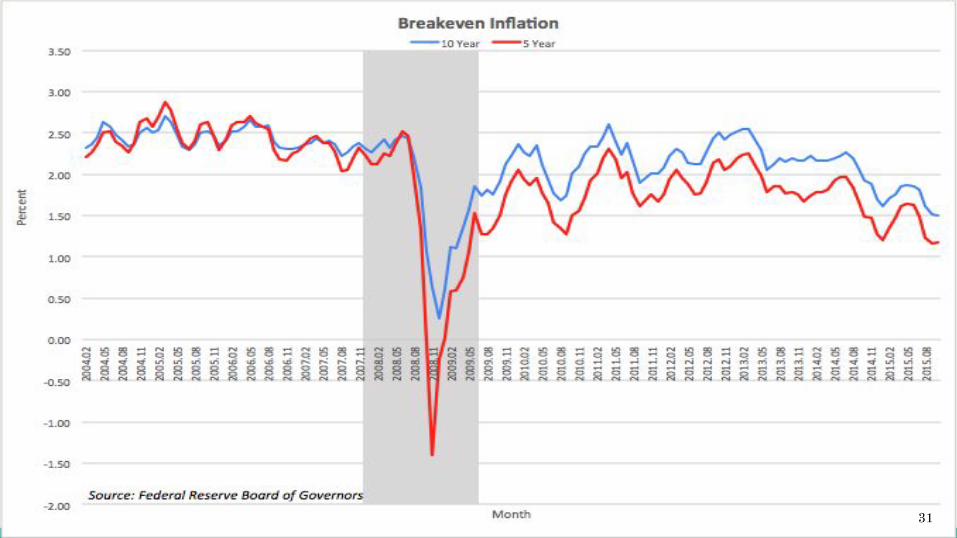

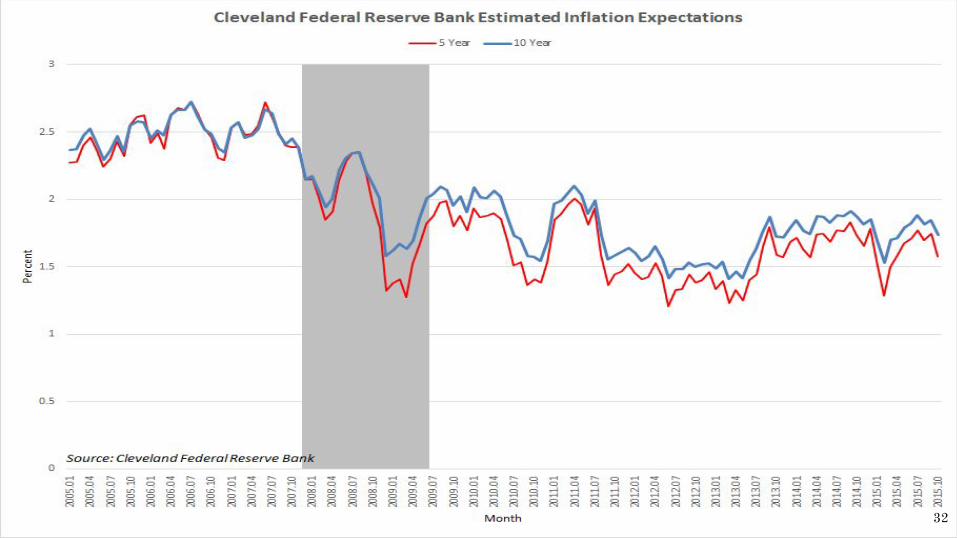

Inflation remains below target and inflation expectations remain stable.

3

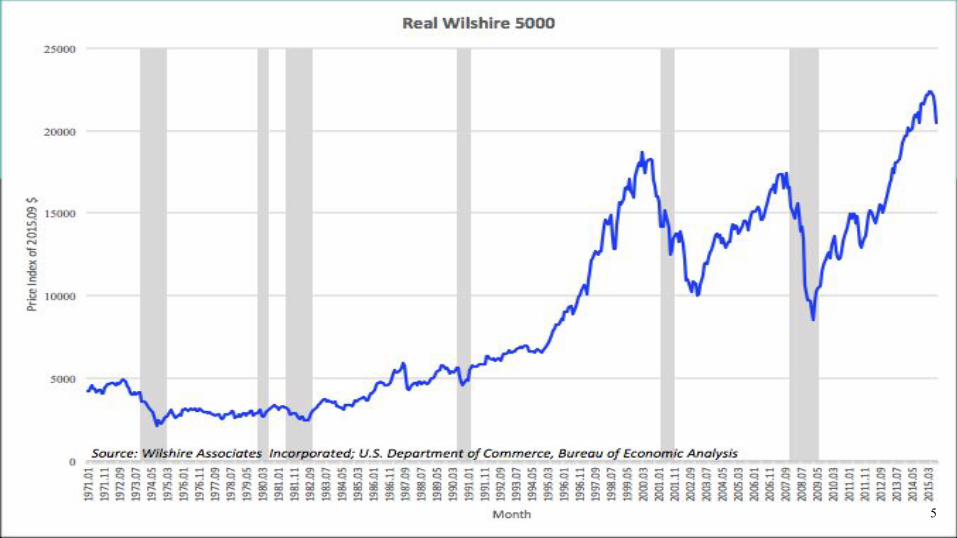

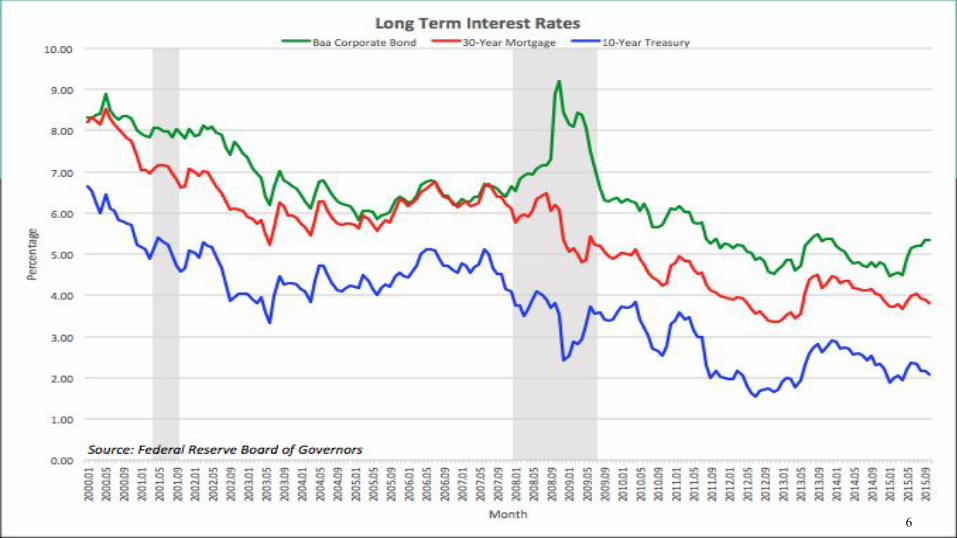

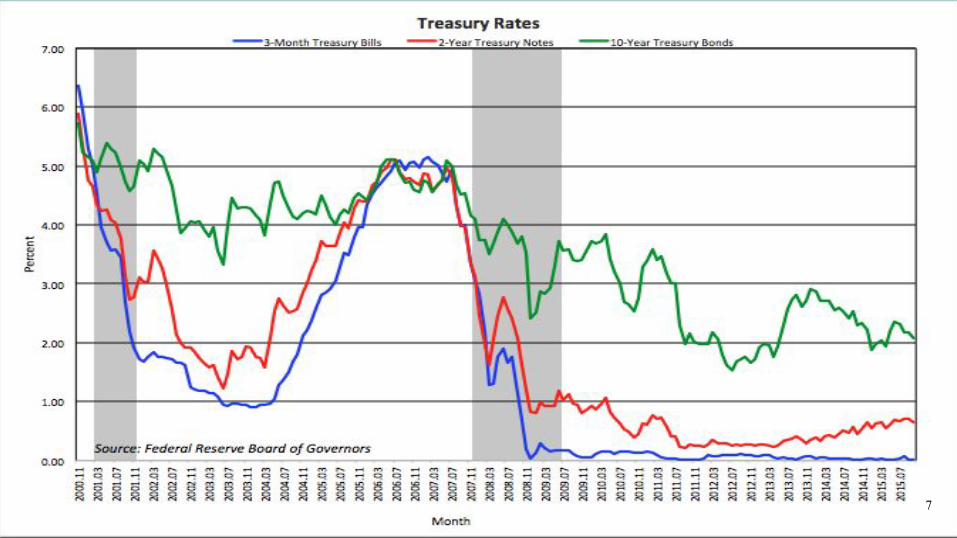

Financial Markets

4

5

66

7

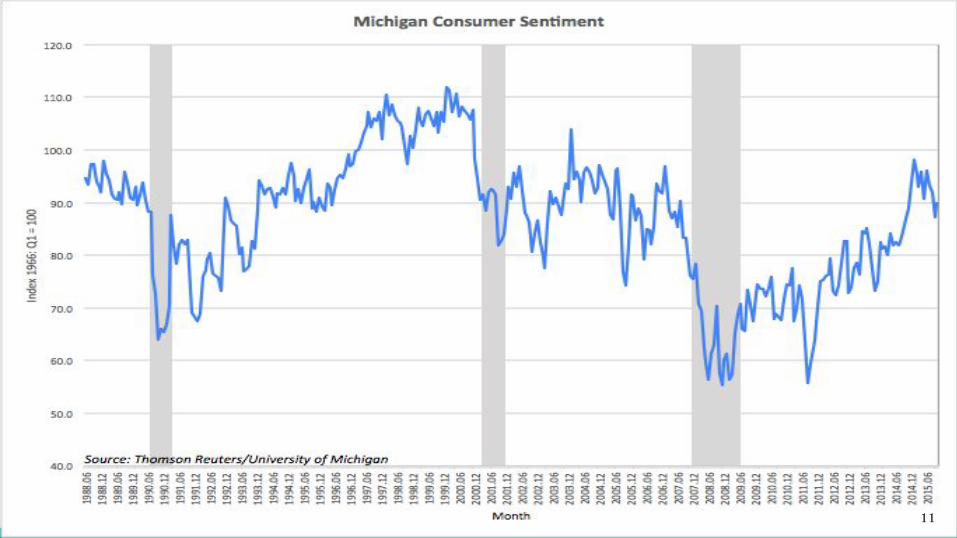

Components of Demand

8

Source:U.S Department of Commerce, Bureau of Economic Analysis

9

10

11

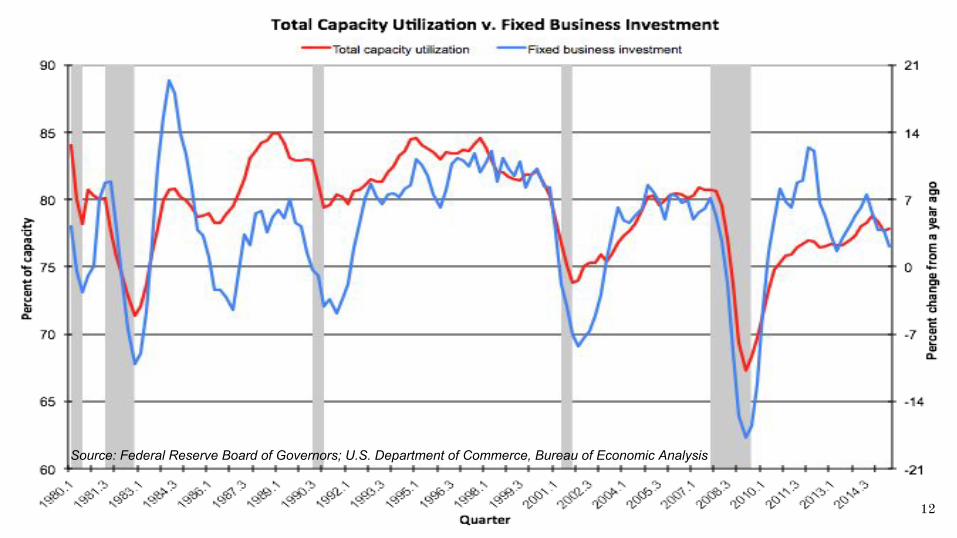

12

Source: Federal Reserve Board of Governors; U.S. Department of Commerce, Bureau of Economic Analysis

13

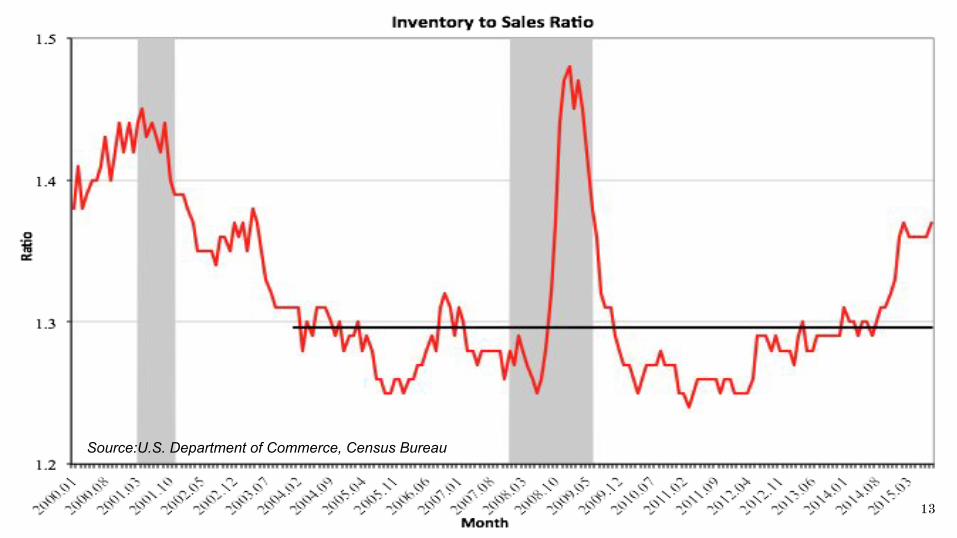

Source:U.S. Department of Commerce, Census Bureau

Source: U.S. Department of Commerce, Census Bureau

14

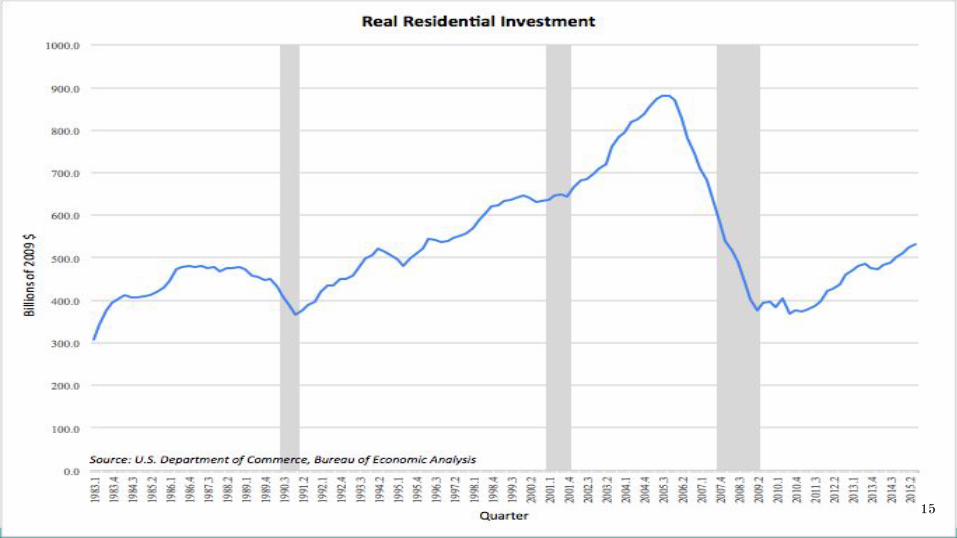

15

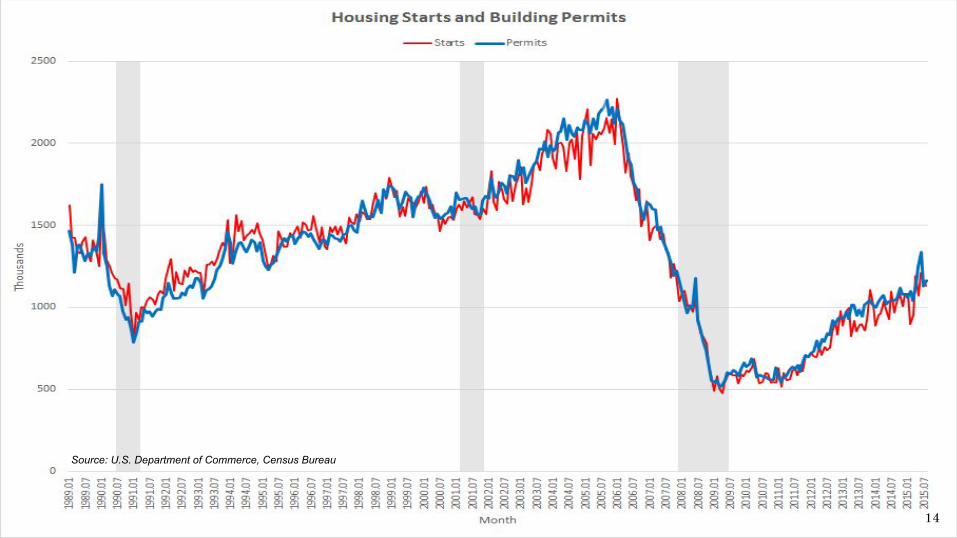

Source: U.S. Department of Commerce, Bureau of Economic Analysis

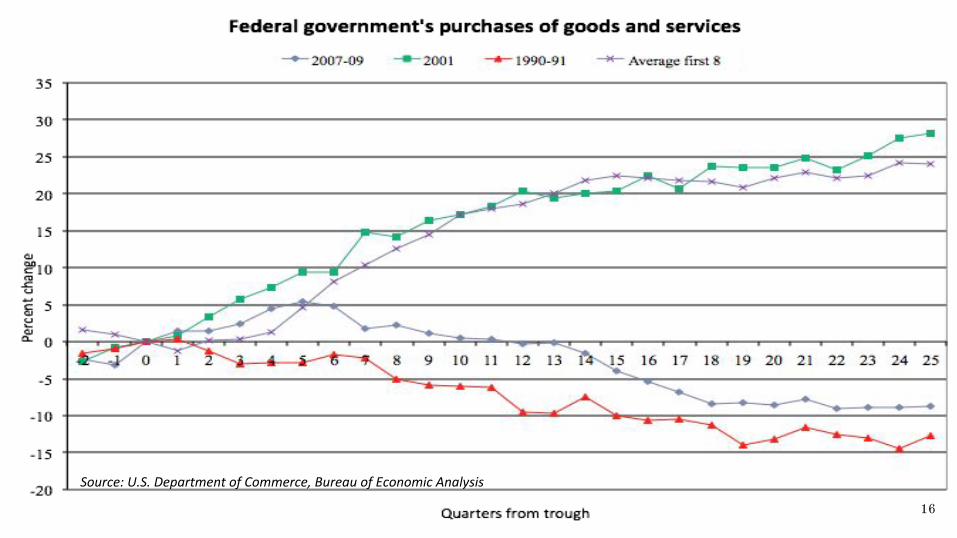

16

Source: U.S. Department of Commerce, Bureau of Economic Analysis

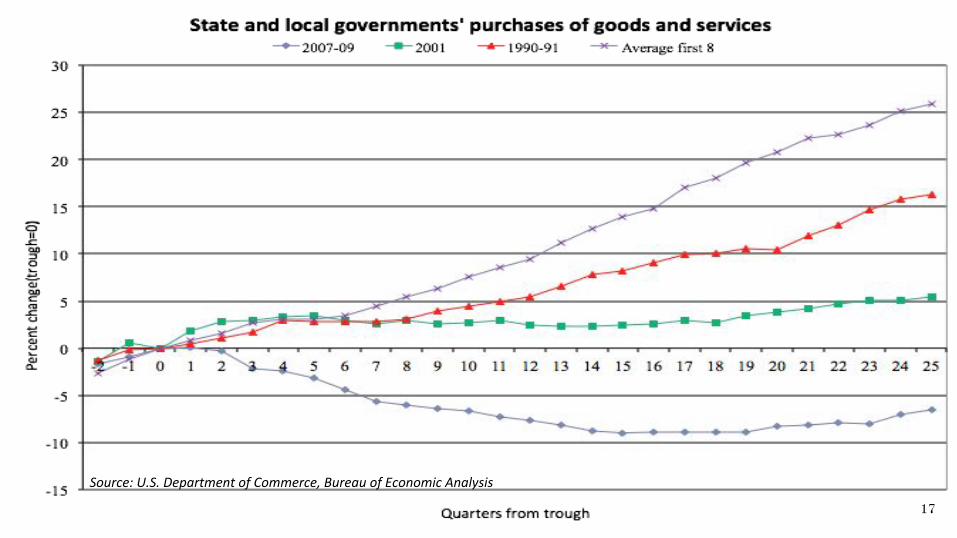

17

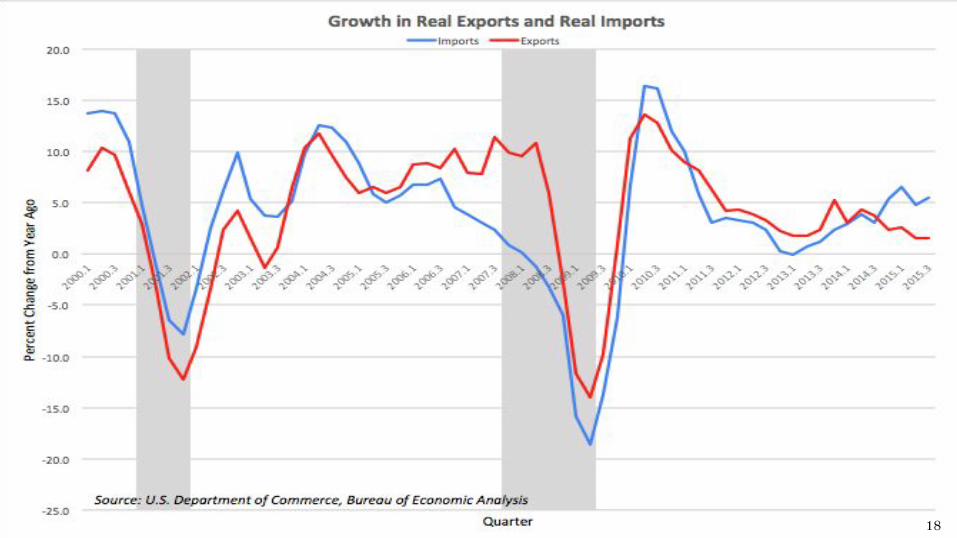

18

19

20

21

Labor Markets

22

Source: U.S. Department of Labor, Bureau of Labor Statistics

23

24

Source: US Department of Labor, Bureau of Labor Statistics

25

26

27

Inflation

28

29

30

31

32

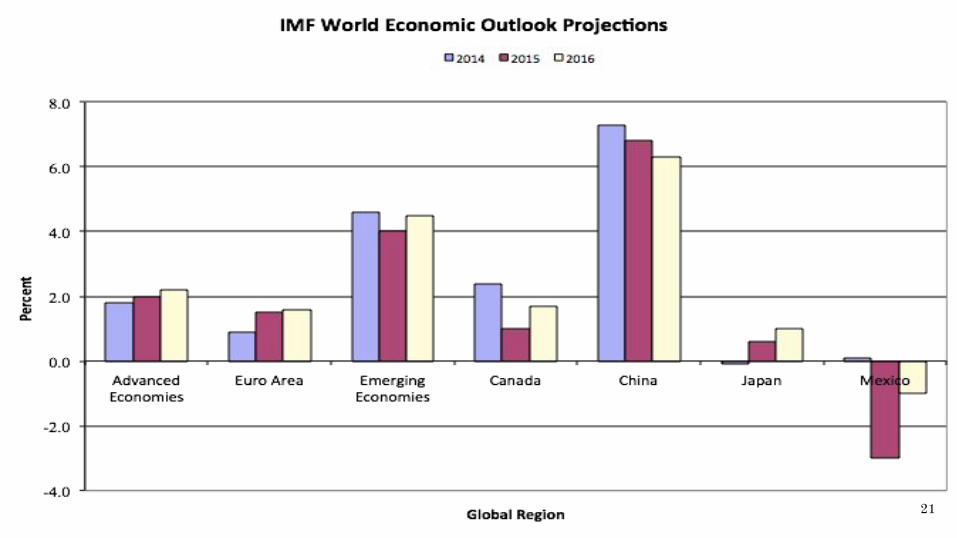

Risks to the Economy● Our output and employment would be adversely affected if China’s and

Europe’s economies do not perform as forecasted in 2016.

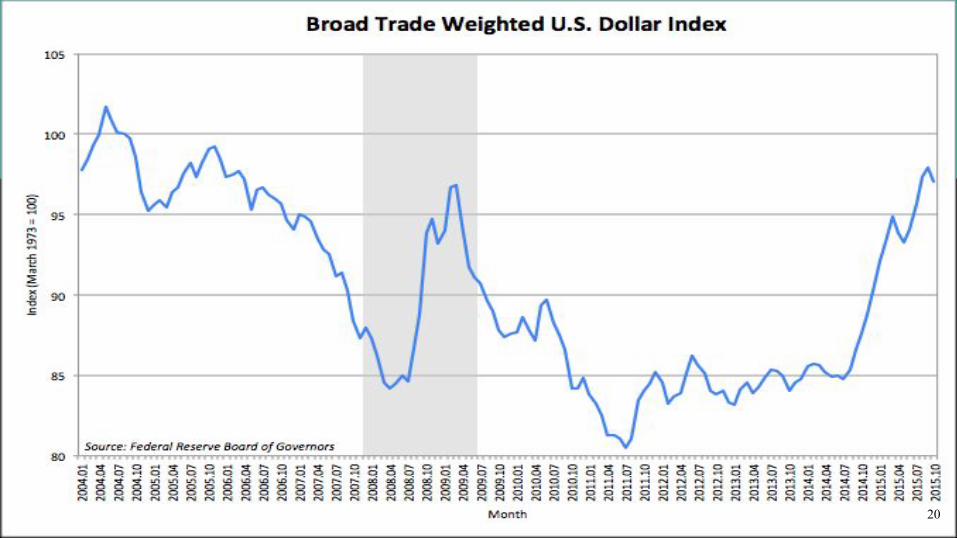

● Inflation would be lower if the dollar continues to strengthen as it has over

the past year.

● The possibility that inflation expectations could become destabilized if

inflation continues to run well below our goal of two percent.

33

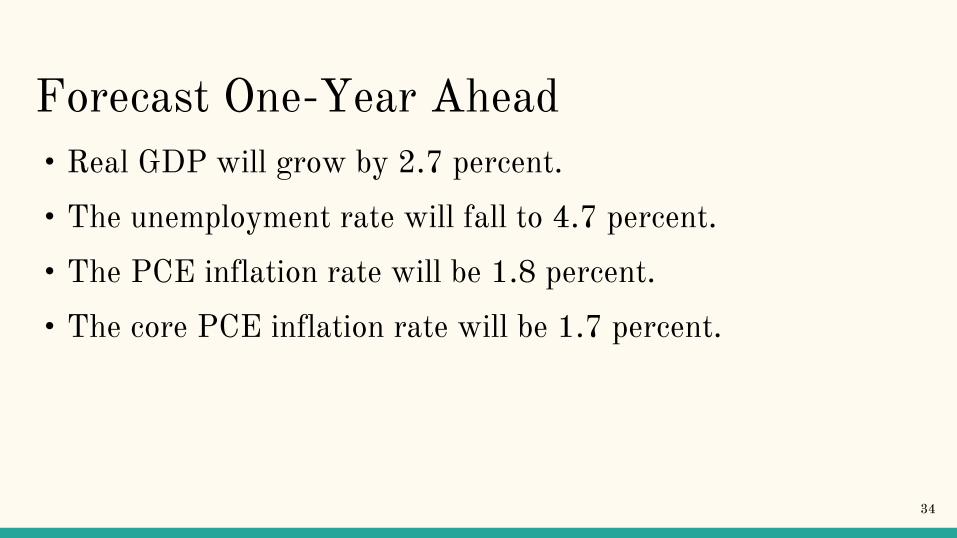

Forecast One-Year Ahead• Real GDP will grow by 2.7 percent.

• The unemployment rate will fall to 4.7 percent.

• The PCE inflation rate will be 1.8 percent.

• The core PCE inflation rate will be 1.7 percent.

34

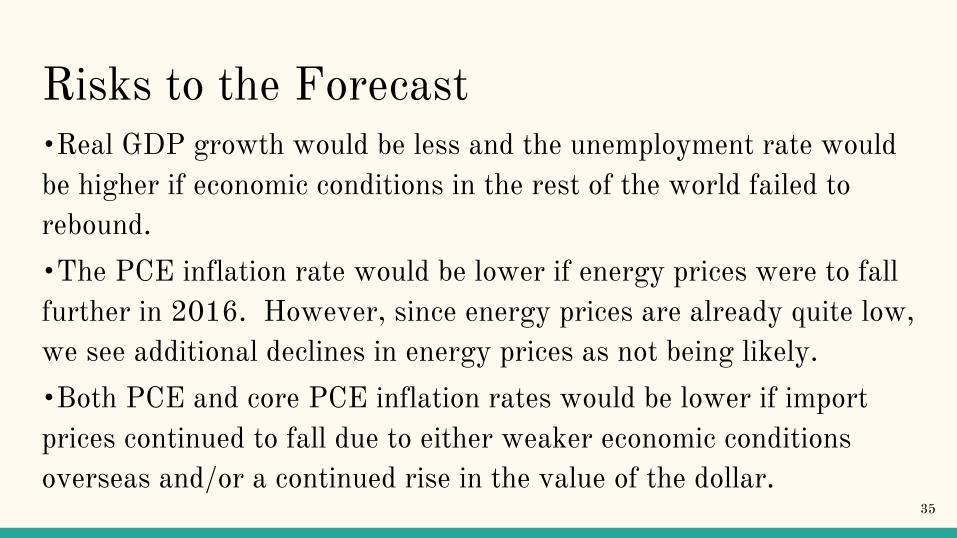

Risks to the Forecast•Real GDP growth would be less and the unemployment rate would be higher if economic conditions in the rest of the world failed to rebound.

•The PCE inflation rate would be lower if energy prices were to fall further in 2016. However, since energy prices are already quite low, we see additional declines in energy prices as not being likely.

•Both PCE and core PCE inflation rates would be lower if import prices continued to fall due to either weaker economic conditions overseas and/or a continued rise in the value of the dollar.

35

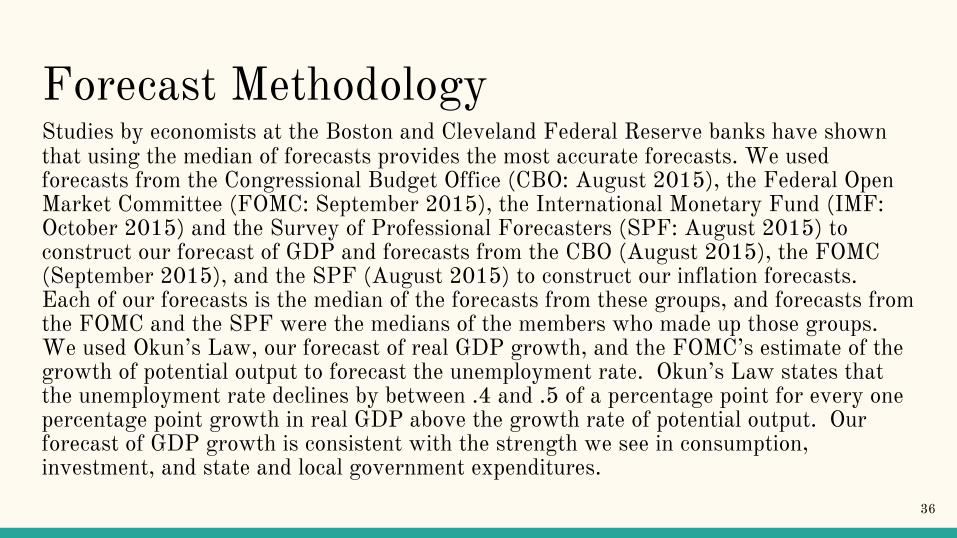

Forecast MethodologyStudies by economists at the Boston and Cleveland Federal Reserve banks have shown that using the median of forecasts provides the most accurate forecasts. We used forecasts from the Congressional Budget Office (CBO: August 2015), the Federal Open Market Committee (FOMC: September 2015), the International Monetary Fund (IMF: October 2015) and the Survey of Professional Forecasters (SPF: August 2015) to construct our forecast of GDP and forecasts from the CBO (August 2015), the FOMC (September 2015), and the SPF (August 2015) to construct our inflation forecasts. Each of our forecasts is the median of the forecasts from these groups, and forecasts from the FOMC and the SPF were the medians of the members who made up those groups. We used Okun’s Law, our forecast of real GDP growth, and the FOMC’s estimate of the growth of potential output to forecast the unemployment rate. Okun’s Law states that the unemployment rate declines by between .4 and .5 of a percentage point for every one percentage point growth in real GDP above the growth rate of potential output. Our forecast of GDP growth is consistent with the strength we see in consumption, investment, and state and local government expenditures.

36

Arguments In Favor of a Rate Increase

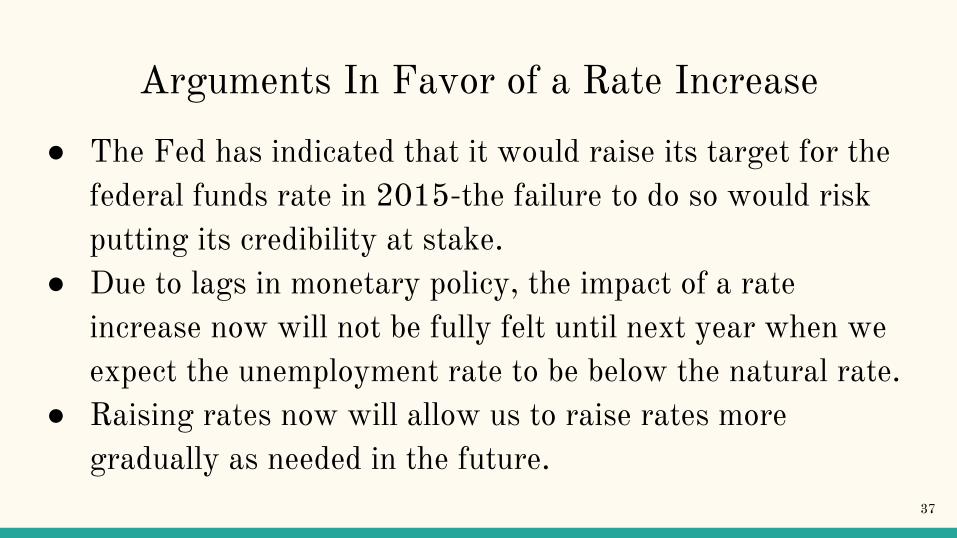

● The Fed has indicated that it would raise its target for the federal funds rate in 2015-the failure to do so would risk putting its credibility at stake.

● Due to lags in monetary policy, the impact of a rate increase now will not be fully felt until next year when we expect the unemployment rate to be below the natural rate.

● Raising rates now will allow us to raise rates more gradually as needed in the future.

37

Arguments Against a Rate Increase

● Despite the unemployment rate being close to the natural rate, there is still evidence of slack in the labor market.

● Inflation continues to run well below our target of two percent.

38

Policy Recommendation● Raise the target range for the federal funds rate to ¼ percent to

½ percent. Before deciding on further rate increases, we will continue to monitor developments in inflation, particularly with respect to energy and import prices, which have been the primary factors holding inflation well below our target of two percent.

● Maintain its policy of rolling over maturing Treasury securities into new issues and reinvesting principal payments on all agency debt and agency mortgage-backed securities in agency mortgage-backed securities.

39