-

CNBC Fed Survey July 28, 2015 Page 1 of 33

FED SURVEY July 28, 2015

These survey results represent the opinions of 35 of the nations

top money managers, investment strategists, and professional

economists. They responded to CNBCs invitation to participate in

our online survey. Their responses were collected

on July 23-24, 2015. Participants were not required to answer

every question. Results are also shown for identical questions in

earlier surveys.

This is not intended to be a scientific poll and its results

should not be extrapolated beyond those who did accept our

invitation.

1. Will the Federal Reserve raise the federal funds rate in

2015?

84%

11%

5%

92%

5% 3%

82%

15%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Yes No Don't know/unsure

Apr 28 Jun 16 Jul 28

-

CNBC Fed Survey July 28, 2015 Page 2 of 33

FED SURVEY July 28, 2015

2. If the Fed does not hike this year, which two factors from

the following list do you believe will most likely be the

reason?

59%

47%

32% 32%

12%

0%

10%

20%

30%

40%

50%

60%

70%

Declininginflation

Weak USeconomicgrowth

Weak overseasgrowth

Weak payrollgrowth

Concern overmarket reaction

to a hike

-

CNBC Fed Survey July 28, 2015 Page 3 of 33

FED SURVEY July 28, 2015

3. Relative to an economy operating at full capacity, what best

describes your view of the amount of resource slack in the U.S.

right now for labor?

July 29August

20Sep 16 Oct 28 Dec 16 Jan 27 Mar 17 Apr 28 Jun 16 Jul 28

Considerably more slack now 48% 34% 20% 18% 16% 16% 13% 6% 5%

12%

Modestly more slack now 36% 40% 60% 69% 55% 50% 63% 64% 54%

47%

No difference 4% 6% 3% 0% 0% 6% 11% 0% 15% 9%

Modestly less slack now 8% 11% 6% 5% 24% 19% 11% 22% 15% 24%

Considerably less slack now 4% 9% 9% 8% 5% 9% 3% 8% 10% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Modestly less slack

Modestly more slack

Considerably less slack

No difference

Considerably more slack

-

CNBC Fed Survey July 28, 2015 Page 4 of 33

FED SURVEY July 28, 2015

Relative to an economy operating at full capacity, what best

describes your view of the amount of resource slack in the U.S.

right now for production capacity?

July 29August

20Sep 16 Oct 28 Dec 16 Jan 27 Mar 17 Apr 28 Jun 16 Jul 28

Considerably more slack now 12% 9% 8% 8% 8% 0% 14% 8% 10%

21%

Modestly more slack now 56% 60% 64% 64% 55% 59% 57% 57% 62%

38%

No difference 8% 14% 8% 15% 13% 19% 14% 5% 8% 15%

Modestly less slack now 16% 9% 14% 8% 24% 13% 11% 19% 13%

21%

Considerably less slack now 4% 9% 3% 5% 0% 9% 5% 11% 8% 6%

0%

10%

20%

30%

40%

50%

60%

70%

No difference

Modestly more slack

Modestly less slack

Considerably less slack

Considerably more slack

-

CNBC Fed Survey July 28, 2015 Page 5 of 33

FED SURVEY July 28, 2015

4. What is your measure of full employment in the U.S.?

0%

5%

10%

15%

20%

25%

30%

35%

Unemployment rate

Apr 28 Jun 16 Jul 28

Averages:

Apr 28: 4.8%

Jun 16: 4.8%

Jul 28: 4.7%

-

CNBC Fed Survey July 28, 2015 Page 6 of 33

FED SURVEY July 28, 2015

5. In July, will the Fed alter its statement to signal a rate

hike is nearing?

34%

63%

3%

0%

10%

20%

30%

40%

50%

60%

70%

Yes No Don't know/unsure

-

CNBC Fed Survey July 28, 2015 Page 7 of 33

FED SURVEY July 28, 2015

6. At what level of year-over-year wage growth would you become

concerned that inflationary pressures are building?

14% chose Theres little connection between wages and overall

price inflation.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0% 1% 2% 3% 4% 5% 6% 7%

Wage growth

Jun 16 Jul 28

Averages:

Jun 16: 3.6%

Jul 28: 3.5%

-

CNBC Fed Survey July 28, 2015 Page 8 of 33

FED SURVEY July 28, 2015

7. At the current level of wage growth, are you ...?

10%

5%

62%

21%

3%

6%

9%

65%

21%

0% 0%

10%

20%

30%

40%

50%

60%

70%

Concernedabout inflation

Concernedabout deflation

Believe therisks areneutral

Theres little connection

between wages and overall

price inflation

Don'tknow/unsure

Jun 16 Jul 28

-

CNBC Fed Survey July 28, 2015 Page 9 of 33

FED SURVEY July 28, 2015

8. What is the minimum rate of average monthly payroll growth

that you believe the Fed will require to:

0%

3%

0%

6%

29%

44%

6%

9%

3%

0%

3%

6%

12%

18%

32%

18%

9%

3%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Less than 100K

100K to 125K

125K to 150K

150K to 175K

175K to 200K

200K to 225K

225K to 250K

More than 250K

Don't know/unsure

Hike rates initially Enact subsequent hikes

-

CNBC Fed Survey July 28, 2015 Page 10 of 33

FED SURVEY July 28, 2015

9. Where do you expect the S&P 500 stock index will be on

?

2075

2149

2111

2194 2187

2128

2156 2159 2135

2311 2296

2247

2259

2293

2254

1,800

1,900

2,000

2,100

2,200

2,300

2,400

Jul 29 Sep 16 Oct 28 Dec 16 Jan 27

'15

Mar 17 Apr 282 Jun 16 Jul 28

Survey Dates

December 31, 2015 December 31, 2016

-

CNBC Fed Survey July 28, 2015 Page 11 of 33

FED SURVEY July 28, 2015

10. What do you expect the yield on the 10-year Treasury note

will be on ?

3.43% 3.45%

3.19%

2.96%

2.54%

2.57%

2.33%

2.64%

2.62%

3.52%

3.04%

3.14%

2.89%

3.24% 3.17%

2.0%

2.5%

3.0%

3.5%

4.0%

Jul 29 Sep 16 Oct 28 Dec 16 Jan 27'15

Mar 17 April 28 Jul 16 Jul 28

Survey Dates

December 31, 2015 December 31, 2016

-

CNBC Fed Survey July 28, 2015 Page 12 of 33

FED SURVEY July 28, 2015

11. What is your forecast for the year-over-year percentage

change in real U.S. GDP for ?

Jan

28, '14Mar 18 Apr 28 Jun 4 Jul 29 Sep 16 Oct 28 Dec 16

Jan

27, '15Mar 17

April

28Jun 16 Jul 28

2015 +2.90 +3.02 +3.00 +2.81 +2.75 +2.90 +2.90 +3.02 +2.99 +2.69

+2.70 +2.25 2.41%

2016 +2.88 +2.80 +2.84 +2.81 +2.78 2.70%

+2.90%

+3.02% +3.00%

+2.81%

+2.75%

+2.90% +2.90%

+3.02% +2.99%

+2.69% +2.70%

+2.25%

2.41%

+2.88%

+2.80%

+2.84% +2.81%

+2.78%

2.70%

2.0%

2.2%

2.4%

2.6%

2.8%

3.0%

3.2%

3.4%

2015 2016

-

CNBC Fed Survey July 28, 2015 Page 13 of 33

FED SURVEY July 28, 2015

12. What is your forecast for the year-over-year percentage

change in the headline U.S. CPI for ?

2.02%

2.29% 2.27%

2.01%

1.74%

1.17%

1.01% 1.00%

1.17%

1.10%

2.17%

2.07%

2.08%

1.96%

2.29%

2.17%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

Jun 4 Jul 29 Sep 16 Oct 28 Dec 16 Jan 27,'15

Mar 17 April 28 Jun 16 Jul 28

Survey Dates

2015 2016

-

CNBC Fed Survey July 28, 2015 Page 14 of 33

FED SURVEY July 28, 2015

13. According to fed fund futures trading at the CME the

probability of a rate hike in September is 38 percent. What rate

hike probability do you believe is too low for the Fed to

actually hike rates?

0%

2%

4%

6%

8%

10%

12%

14%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Rate hike probability

59% responded

"None. The Fed won't consider

this factor"

Average for numerical responses:

31.4%

-

CNBC Fed Survey July 28, 2015 Page 15 of 33

FED SURVEY July 28, 2015

14. When do you expect the Fed to hike the fed funds rate and

allow its balance sheet to decline?

Survey Date Fed Funds Hike

Average Forecast

Balance Sheet

Average Forecast

April 28, 2014 survey July 2015 October 2015

June 4 survey August 2015 March 2016

July 29 survey August 2015 December 2015

August 20 survey July 2015 Not asked

September 16 survey June 2015 December 2015

October 28 survey July 2015 January 2016

December 16 survey July 2015 February 2016

Jan. 27, 2015 survey September 2015 April 2016

March 17 survey August 2015 April 2016

April 28 survey October 2015 May 2016

June 16 survey October 2015 July 2016

July 28 survey November 2015 June 2016

-

CNBC Fed Survey July 28, 2015 Page 16 of 33

FED SURVEY July 28, 2015

15. How would you characterize the Fed's current monetary

policy?

28%

49%

46%

49%

44%

39%

50%

54%

50%

60%

43%

43%

49%

43%

49% 50%

47%

32%

44%

35%

47%

17%

6%

3% 3% 3%

6% 5%

3%

6%

13%

3%

3%

6% 5% 6%

3%

8%

6%

3%

0% 0%

10%

20%

30%

40%

50%

60%

70%

Jul 31,'12

Jul 29,'14

Aug 20 Sep 16 Oct 28 Dec 16 Jan 27,'15

Mar 17 Apr 28 Jun 16 Jul 28

Too accommodative Just right Too restrictive Don't

know/unsure

Too accomodative

Don't know/unsure

Too restrictive

Just right

-

CNBC Fed Survey July 28, 2015 Page 17 of 33

FED SURVEY July 28, 2015

16. Where do you expect the fed funds target rate will be on

?

Jul

30

Sep

17

Oct

29

Dec

17

Jan

28

'14

Mar

18

Apr

28

Jun

4

Jul

29

Aug

20

Sep

16

Oct

28

Dec

16

Jan

27,

'15

Mar

17

April

28

Jun

16

Jul

28

Dec 31, 2015 0.97 0.92 0.82 0.70 0.72 0.83 0.99 0.68 1.05 0.89

0.98 0.89 0.83 0.73 0.71 0.54 0.53 0.47

Dec 31, 2016 1.99 2.13 2.04 1.93 1.75 1.84 1.46 1.56 1.41

0.97% 0.92%

0.82%

0.70% 0.72%

0.83%

0.99%

0.68%

1.05%

0.89%

0.98%

0.89%

0.83%

0.73% 0.71%

0.54% 0.53%

0.47%

1.99%

2.13%

2.04%

1.93%

1.75%

1.84%

1.46%

1.56%

1.41%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Dec 2016

Dec 2015

-

CNBC Fed Survey July 28, 2015 Page 18 of 33

FED SURVEY July 28, 2015

17. At what fed funds level will the Federal Reserve stop hiking

rates in the current cycle? That is, what will be the terminal

rate?

3.16% 3.20%

3.30%

3.17% 3.11%

3.04%

2.85%

3.06%

2.98%

2.0%

2.5%

3.0%

3.5%

4.0%

Aug 20 Sep 16 Oct 28 Dec 16 Jan 27,

'15

Mar 17 Apr 28 Jun 16 Jul 28

Survey Dates

-

CNBC Fed Survey July 28, 2015 Page 19 of 33

FED SURVEY July 28, 2015

18. When do you believe fed funds will reach its terminal

rate?

Survey Date Forecast

August 20 survey Q4 2017

September 16 survey Q3 2017

October 28 survey Q4 2017

December 16 survey Q1 2018

Jan. 27, 2015 survey Q1 2018

March 17 survey Q4 2017

April 28 survey Q1 2018

June 16 survey Q1 2018

July 28 survey Q2 2018

-

CNBC Fed Survey July 28, 2015 Page 20 of 33

FED SURVEY July 28, 2015

19. What is the percentage chance each of the following

countries will leave the euro zone in the next 3 years? (0%=No

chance of leaving, 100%=Certainty of leaving):

41%

13%

12%

9%

8%

3%

39%

11%

8%

7%

5%

3%

5%

50%

12%

10%

8%

5%

2%

3%

49%

13%

12%

11%

7%

3%

3%

0% 10% 20% 30% 40% 50% 60%

Greece

Portugal

Spain

Italy

Ireland

Germany

France

Mar 17 Apr 28 Jun 16 Jul 28

-

CNBC Fed Survey July 28, 2015 Page 21 of 33

FED SURVEY July 28, 2015

20. The recent agreement between Greece and its creditors is

a:

0%

91%

9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Permanent solution Temporary solution Don't know/unsure

-

CNBC Fed Survey July 28, 2015 Page 22 of 33

FED SURVEY July 28, 2015

21. What effect will the Greece deal have on:

15%

9%

68%

9%

18%

59%

15%

9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Positive Neutral Negative Don't know/unsure

Greece's economy The eurozone's economy

-

CNBC Fed Survey July 28, 2015 Page 23 of 33

FED SURVEY July 28, 2015

22. Assuming a new agreement is reached, do you believe that

Greece will pass the first review (that is, enact sufficient

economic reforms to satisfy the initial creditor review)?

47%

24%

29%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Yes No Don't know/unsure

-

CNBC Fed Survey July 28, 2015 Page 24 of 33

FED SURVEY July 28, 2015

23. Has the U.S. stock market already discounted a fed funds

rate hike by the Federal Reserve this year?

56%

53% 53%

47%

61%

50%

36% 38%

47%

50%

39% 38%

8% 9%

0%

3%

0%

12%

0%

10%

20%

30%

40%

50%

60%

70%

Dec 16 Jan 27 Mar 17 Apr 28 Jun 16 Jul 28

Survey dates

Yes No Don't know/unsure

-

CNBC Fed Survey July 28, 2015 Page 25 of 33

FED SURVEY July 28, 2015

Has the U.S. bond market already discounted a fed funds rate

hike by the Federal Reserve this year?

42%

67%

62% 56%

33% 35%

3%

0%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Apr 28 Jun 16 Jul 28

Survey dates

Yes No Don't know/unsure

-

CNBC Fed Survey July 28, 2015 Page 26 of 33

FED SURVEY July 28, 2015

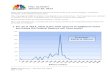

24. What is the single biggest threat facing the U.S. economic

recovery?

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

European recession/financial crisis

Tax/regulatory policies

Slow job growth

Inflation

Deflation

Debt ceiling

Rise in interest rates

Geopolitical risks

Global economic weakness

Slow wage growth

Other

Don't know/unsure

Europeanrecession/financial

crisis

Tax/regulatory

policies

Slow jobgrowth

InflationDeflationDebt

ceiling

Rise ininterest

rates

Geopolitical risks

Globaleconomicweakness

Slow wagegrowth

OtherDon't

know/unsure

Apr 30 20%31%20%0%2%2%11%0%

Jun 18 15%28%20%3%3%0%13%0%

Jul 30 8%30%22%0%2%2%10%14%4%

Sep 17 4%27%22%2%0%4%18%7%2%

Oct 29 8%29%24%3%3%3%8%13%0%

Dec 17 5%32%29%2%0%2%15%2%2%

Jan 28 '14 7%21%30%2%0%0%12%21%0%

Mar 18 10%23%26%3%5%0%5%18%0%

Apr 28 3%26%21%3%5%0%8%18%13%0%

Jul 29 12%29%12%6%3%0%12%12%12%3%

Sep 16 6%26%29%6%3%0%6%11%11%3%

Oct 28 31%18%15%3%3%0%10%8%8%3%

Dec 16 40%14%14%3%6%0%3%14%3%0%

Jan 27 '15 0%13%9%0%0%0%6%16%41%6%16%0%

Mar 17 6%14%0%3%6%0%6%8%28%17%14%0%

April 28 3%11%8%3%0%0%6%11%28%8%19%3%

Jun 16 3%17%3%0%0%0%14%25%22%6%11%0%

Jul 28 6%21%9%0%0%0%12%6%29%9%9%0%

Apr 30 Jun 18 Jul 30 Sep 17 Oct 29 Dec 17 Jan 28 '14 Mar 18 Apr

28

Jul 29 Sep 16 Oct 28 Dec 16 Jan 27 '15 Mar 17 April 28 Jun 16

Jul 28

-

CNBC Fed Survey July 28, 2015 Page 27 of 33

FED SURVEY July 28, 2015

FED SURVEY April 30,

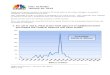

25. In the next 12 months, what percent probability do you place

on the U.S. entering recession? (0%=No chance

of recession, 100%=Certainty of recession)

Aug11,

'11

Sep19

Oct31

Jan23,

'12

Mar16

Apr24

Jul31

Sep12

Dec11

Jan29,

'13

Mar19

Apr30

Jun18

Jul30

Sep6

Oct29

Dec17

Jan28

'14

Mar18

Apr28

Jul29

Sep16

Oct28

Dec16

Jan27

'15

Mar17

April28

Jun16

Jul28

Series1 34.0 36.1 25.5 20.3 19.1 20.6 25.9 26.0 28.5 20.4 17.6

18.2 15.2 16.2 16.9 18.4 17.3 15.3 16.9 14.6 16.2 15.0 15.1 13.6

13.0 16.4 14.7 15.1 17.4

34.0%

36.1%

25.5%

20.3%

19.1%

20.6%

25.9%

26.0%

28.5%

20.4%

17.6%

18.2%

15.2%

16.2% 16.9%

18.4%

17.3%

15.3%

16.9%

14.6%

16.2%

15.0%

15.1%

13.6% 13.0%

16.4%

14.7%

15.1%

17.4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Survey Dates

-

CNBC Fed Survey July 28, 2015 Page 28 of 33

FED SURVEY July 28, 2015

FED SURVEY April 30,

26. What is your primary area of interest?

Comments: Robert Brusca, Fact and Opinion Economics: Monetary

policy is not 'too tight ' as I said because of interest rates that

are 'too high.'

It is bank regulation and the imposition of high capital/asset

ratios IN CONJUNCTION WITH the way Fed stress tests are performed

that make policy restrictive. I still don't think that the Fed

thinks of its policy that way and that is the reason why monetary

policy stays too

tight. Since banks have to keep capital relative to assets in

order to survive the pit of a draconian stress test, the effective

capital asset ratio they have to have is really much greater. It is

why banks are not lending more. Fed policy on banks is really

onerous regulation

and is highly restrictive. Overseas.. EMU IS IMPOSING AUSTERITY.

Where could growth possibly come from, let alone inflation?

Commodity and oil prices are crashing, gold is imploding, the

dollar is strong and the FED is ITCHING to hike rates. Wake me when

this

bad dream is over! Janet! Who really thinks that the economy

will pick up in the second half of the year? Good luck with that.

By the

Economics

49%

Equities 17%

Fixed Income

11%

Currencies

3%

Other 20%

-

CNBC Fed Survey July 28, 2015 Page 29 of 33

FED SURVEY July 28, 2015

FED SURVEY April 30,

way, Greece is still just an accident waiting to happen. It

needs too much debt relief to be able to survive and it will not

get enough of it. Greece is forming a new ring of Hell in Dante's

inferno.

Thomas Costerg, Standard Chartered Bank: We think the FOMC will

adopt a do no harm approach when it meets this week: the statement

is unlikely to give explicit strong guidance about a near-term rate

hike, in our view. The only hint we foresee might be a

more upbeat tone about the domestic economy in the first

paragraph. We still expect a September rate hike, but this hinges

on an improvement in domestic data ahead of the meeting,

particularly signs of an uptrend/bounce in wages/inflation and

signs of

improvement in H2 GDP growth after a meagre performance in H1.

John Donaldson, Haverford Trust Co.: There is an exceptionally wide

range of predictions regarding the Fed. One extreme expects no

action until the middle of 2016. The other extreme calls for a

3% funds rate by the end of 2016. Both do not take the FOMC at its

word that moves will be soon and gradual. We take the FOMC at its

word and expect the first move in September and that subsequent

moves will be very gradual. When a Fed Chair uses a word

(gradual) three times in one comment during Congressional

testimony, you should pay attention.

Mark Elenowitz, TriPoint Global Equities: While countries such

as China and Greece continue on a downward spiral, our domestic

capital markets have proven their resilience to international

pressures and I believe this same resilience will be shown once

the Fed raises rates. Dennis Gartman, The Gartman Letter: I have

too many venues

already in place to make a fool of myself; I needn't supply

others. Kevin Giddis, Raymond James/Morgan Keegan: The market seems

to be saying "no" even as the Fed is saying "yes" to a near-

-

CNBC Fed Survey July 28, 2015 Page 30 of 33

FED SURVEY July 28, 2015

FED SURVEY April 30,

term rate hike. While the Fed ultimately has the stick, they

really need the market to come along so we don't find ourselves in

a highly volatile limited liquidity aftershock of the Fed's

action.

Stuart Hoffman, PNC Financial Services Group: GDP data on 7/30

for 2Q'15 and revisions to 2012-2014 will be "game changers" for

outlook for timing of the first funds rate hike. I expect real GDP

growth will be revised up from the pre-revision 2.3% average

for

2012-2014 along with a smoother quarterly pattern reflecting

less "residual seasonality." I expect 1Q'15 real GDP to be revised

up to near 0.8% and 2Q'15 to top 3% so first-half real GDP will be

up by nearly 2%. This will cause upward revisions to the market's

and

FOMC's consensus forecasts for real GDP in 2015 (4Q-4Q) and

support an initial funds rate hike at the September FOMC meeting.

Then the 2Q ECI data on 7/31 will show workers' wage and fringe

benefit compensation running close to up 2.5% from a year ago,

well

above the AHE data and help "light up" the Yellen labor market

dashboard Art Hogan, Wunderlich Securities: The bond market and

the

strong dollar have already tightened for the Fed. Its time for

the Committee to join the Party.

Hugh Johnson, Hugh Johnson Advisors: There are two important

issues that need to be resolved before the Fed will be

comfortable/justified in moving toward restraint. The first is

inflation. It is still unclear if and when the rate of consumer

inflation will move

to 2.0%. The second issue is China. Given the performance of the

Shanghai Composite it is very unclear what will be the outcome for

the financial markets and economy of China and, by implication,

global financial markets and global economy. There needs to be

a

significantly higher level of confidence that Chinese

policymakers will manage the decline in equities and impact on

Chinese domestic consumption well. This is important.

-

CNBC Fed Survey July 28, 2015 Page 31 of 33

FED SURVEY July 28, 2015

FED SURVEY April 30,

Subodh Kumar, Subodh Kumar & Associates: Unavoidable reality

is one of interest rate increases as Fed Chair Yellen and several

governors have underscored. We believe the Fed rate hikes start

from September 2015. The first tranches of quantitative ease

were necessary. Later ones likely have had side effects like

procrastination on restructuring by governments and companies as

well as complacency in the capital markets. The corporate earnings

reports continue to have expectations being cut to levels then

routinely exceeded in actual reporting but which now risk

diluting market information content. With bifurcation sharp and

buybacks clouding issues, we favor quality of operational and

financial structure. In the critical financial services sector,

which is still

addressing past scandals and globally facing regulatory, capital

structure and business change, we favor the early movers on

restructuring.

Guy LeBas, Janney Montgomery Scott: Leaked economic projections

provided to the FOMC indicate that Fed board staff economists

project only one 25bps rate hike this year. Alternately, we could

see two "micro hikes" of less than 25bps to get to the same

point--the potential for a micro hike is being largely ignored,

but hard to say exactly how market participants would interpret

such an action differently from a single 25bps hike.

John Lonski, Moody's: At the current annual rate of base metals

price deflation, the 10-year Treasury has always been less than its

year-earlier reading, while fed funds has never been hiked. Also,

the

current widening of the high-yield bond spread and the ongoing

climb by the average expected frequency of high-yield defaults

weigh against significantly higher interest rates. What many refer

to as a "lift off" by interest rates might better be described as a

"spurt."

Drew Matus, UBS Investment Research: We believe zero rates are

restraining economic activity. A move off of the zero bound may

boost economic activity.

-

CNBC Fed Survey July 28, 2015 Page 32 of 33

FED SURVEY July 28, 2015

FED SURVEY April 30,

Rob Morgan, Sethi Financial Group: In spite of slow job growth

and low inflation, the Fed needs ammo to fight the next recession

and will hike at least once, and maybe twice, before year-end.

James Paulsen, Wells Capital Management: One of the most

interesting current financial market characteristics is despite

widening concerns about weaker global growth and deflation, 10-year

government bond yields in the U.S. and in Germany remain

near yearly highs. Does this reflect increased certainty of

near-term Fed tightening or is the bond market suggesting yields

maybe have finally bottomed for this recovery cycle?

John Roberts, Hilliard Lyons: While we are early in the Q2

earnings season, cautiousness in forward guidance among some of the

large multinational companies outside of F/X impacts have caused us

to become even more defensive in our recommendation

for client positioning in the equity markets. The length of the

current Bull market only adds to this caution and the potential for

at least a modest pullback. If these early indications of weakness

are confirmed as we move through earnings season, the markets

may

have already reached their highs for the year. Chris Rupkey,

Bank of Tokyo-Mitsubishi: The Fed is behind the

curve. They will break the fixed income markets if they don't

raise rates from zero shortly. Failure to normalize rates is

changing the cyclical nature of interest rates, confusing

corporations who always try to lower interest costs. Fed officials

from other years fought

inflation for too long and the current Fed is fighting

unemployment for too long. We cannot know now what problems their

zero rates policy will cause for the economy in the years to come.

It may be creating a new housing price bubble. Yellen, at her SF

Fed perch,

didn't stop the first bubble so perhaps she doesn't see that her

policy risks a new bubble. Allen Sinai, Decision Economics: U.S.

and global economies are

-

CNBC Fed Survey July 28, 2015 Page 33 of 33

FED SURVEY July 28, 2015

FED SURVEY April 30,

headed for the best years of the expansion in 2016/2017. Diane

Swonk, Mesirow Financial: Limp off for the Fed will be an

interactive process, driven by both data and financial market

reactions to the process; markets will need time to adjust to

normalization in policy Peter Tanous, Lynx Investment Advisory: The

biggest concern

today is the future of China's growth. Will China's efforts to

manage its economy and stock market work? We just don't know. Scott

Wren, Wells Fargo Advisors: The U.S. economy will likely

continue on this modest growth/modest inflation path for several

more years. Stocks can do fine in this environment. International

growth will also be modest and inflation will stay low. Expect 6%

to 10% total return for the S&P 500 over the next couple of

years. We

are likely in the 7th inning of this cycle. We want our clients

to be optimistic and use market volatility to put sidelined funds

to work. Mark Zandi, Moody's Analytics: All the ingredients are in

place for

the Fed to begin normalizing monetary policy.