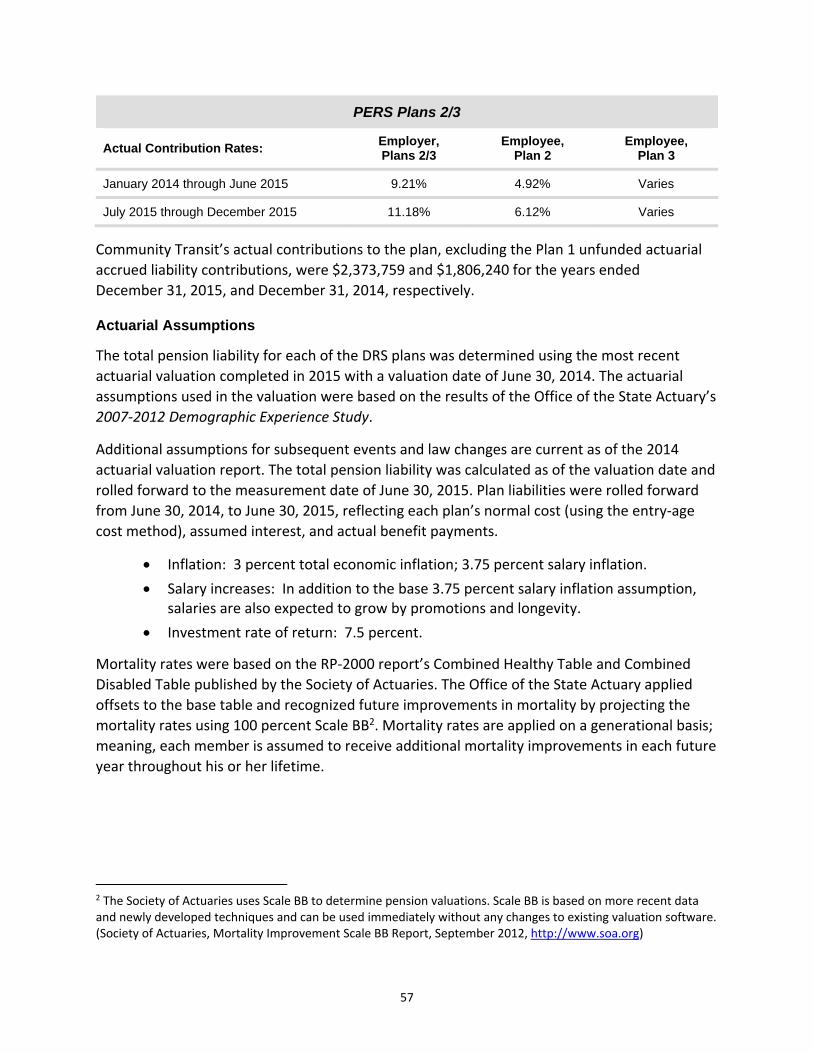

Embed Size (px)

Citation preview

Comprehensive Annual Financial ReportYears Ended December 31, 2015 and December 31, 2014

Community TransitSnohomish County, Washingtonwww.communitytransit.org

2015

Josefina B.Boeing – Canyon Park Commons Bothell

Vanpool/Ferry/TelecommuteChoice Connections 2015Smart Commuter of the 1st Quarter

Innovative transportation programs to reduce traffic congestion and pollution while encouraging healthy travel options

BOARD OF DIRECTORS Board Chair - Mike Todd

Board Vice Chair - Jon NehringBoard Secretary - Stephanie Wright

Board Member - Kim DaughtryBoard Member - Dave Earling

Board Member - Tom HamiltonBoard Member - Leonard KelleyBoard Member - Lance Norton

Board Member - Terry RyanBoard Member - Jerry Smith

BOARD ALTERNATESBoard Alternate - Joe NeigelBoard Alternate - Sid RobertsBoard Alternate - Jan SchuetteBoard Alternate - Dave Somers

Board Alternate - Emily Vanderwielen

CEOChief Executive Officer - Emmett Heath

DIRECTORSChief Communications Officer - Todd Morrow

Chief Technology Officer - Tim ChrobuckDirector of Customer Relations - Bob ThrockmortonDirector of Planning & Development - Joy Munkers

Director of Transportation - Fred Worthen Director of Maintenance - Dave RichardsDirector of Administration - Geri Beardsley

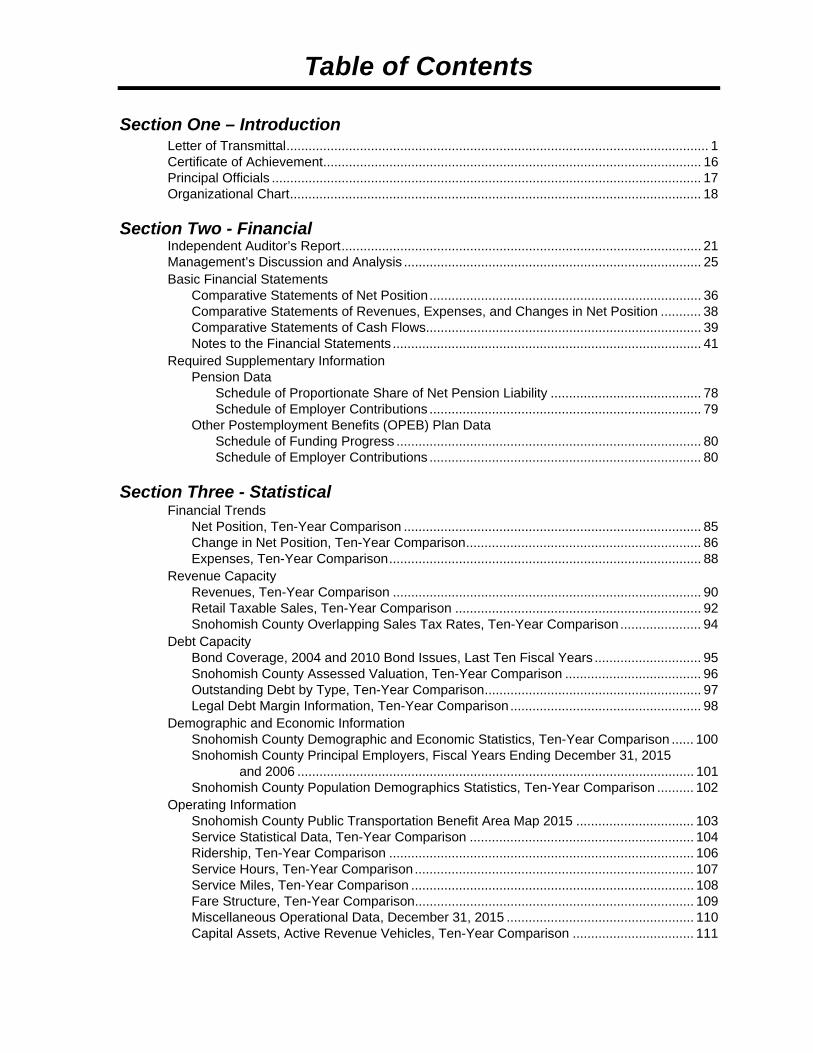

Table of Contents

Section One – Introduction Letter of Transmittal ................................................................................................................... 1 Certificate of Achievement ....................................................................................................... 16 Principal Officials ..................................................................................................................... 17 Organizational Chart ................................................................................................................ 18

Section Two - Financial Independent Auditor’s Report .................................................................................................. 21 Management’s Discussion and Analysis ................................................................................. 25 Basic Financial Statements

Comparative Statements of Net Position .......................................................................... 36 Comparative Statements of Revenues, Expenses, and Changes in Net Position ........... 38 Comparative Statements of Cash Flows........................................................................... 39 Notes to the Financial Statements .................................................................................... 41

Required Supplementary Information Pension Data

Schedule of Proportionate Share of Net Pension Liability ......................................... 78 Schedule of Employer Contributions .......................................................................... 79

Other Postemployment Benefits (OPEB) Plan Data Schedule of Funding Progress ................................................................................... 80 Schedule of Employer Contributions .......................................................................... 80

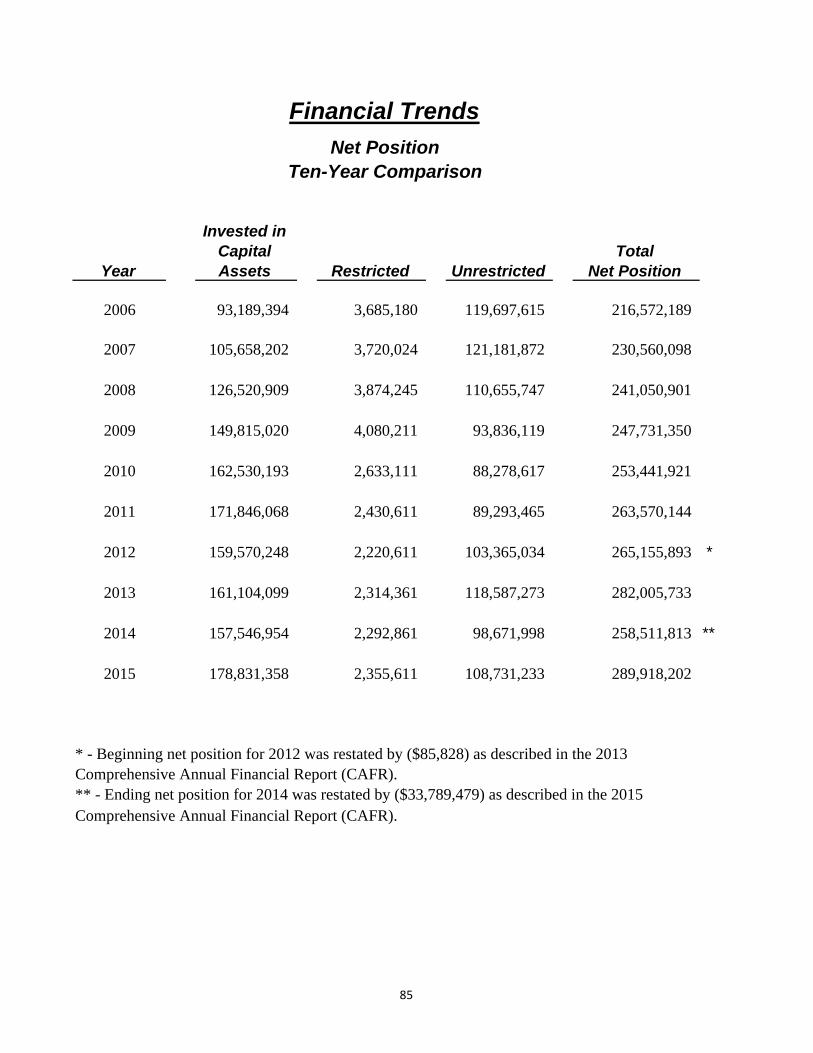

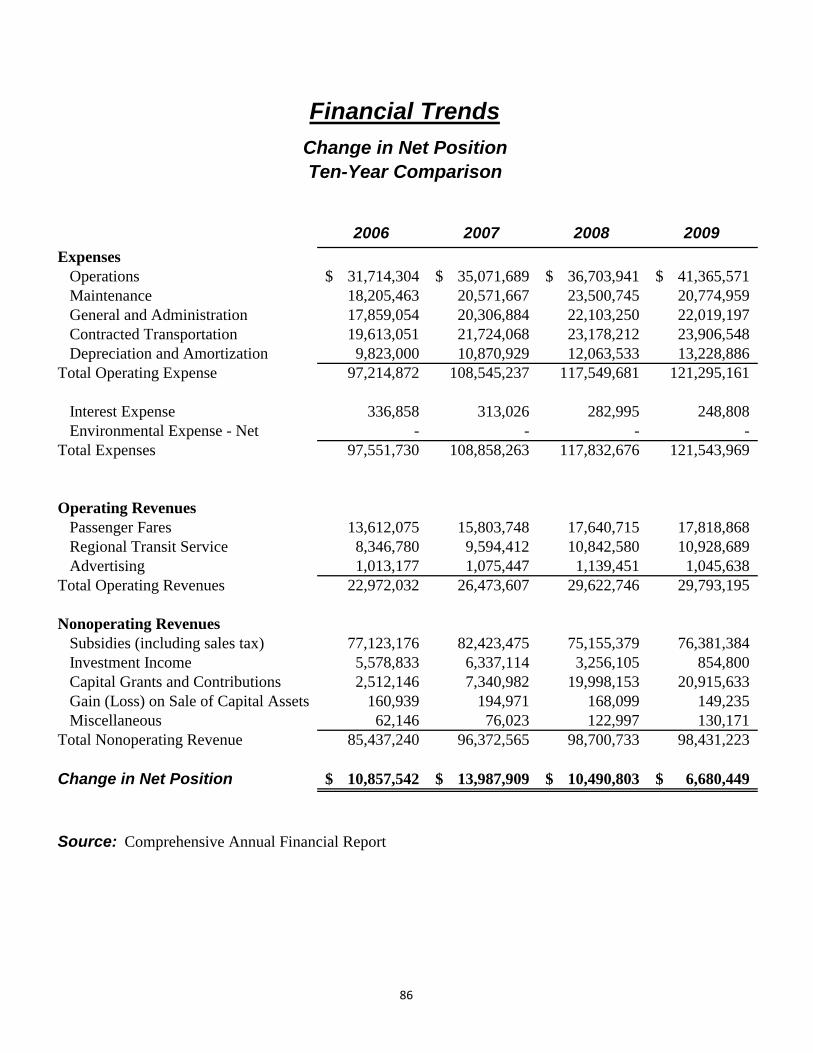

Section Three - Statistical Financial Trends

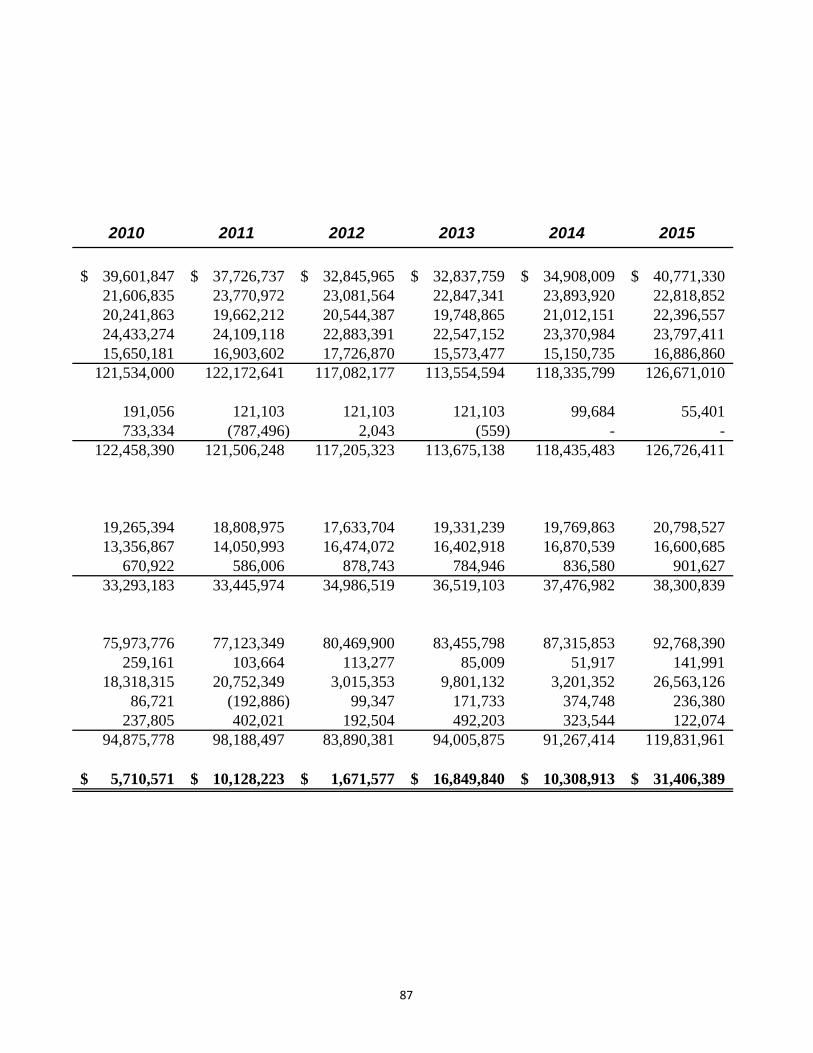

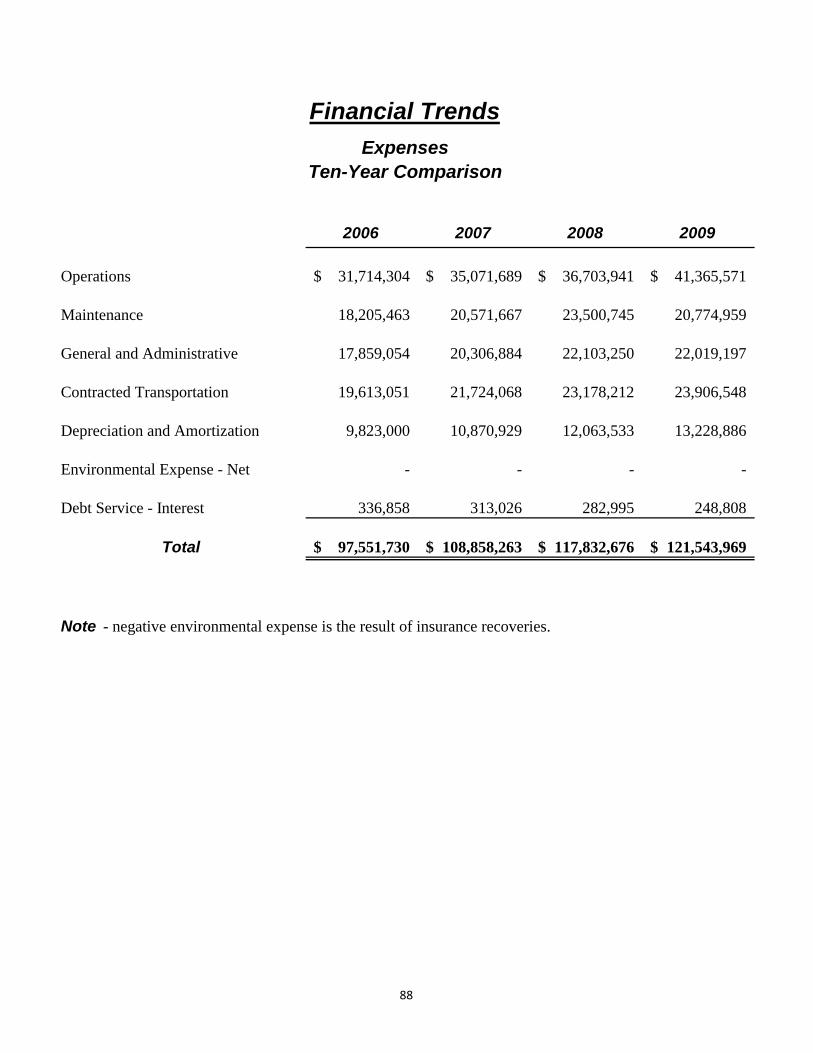

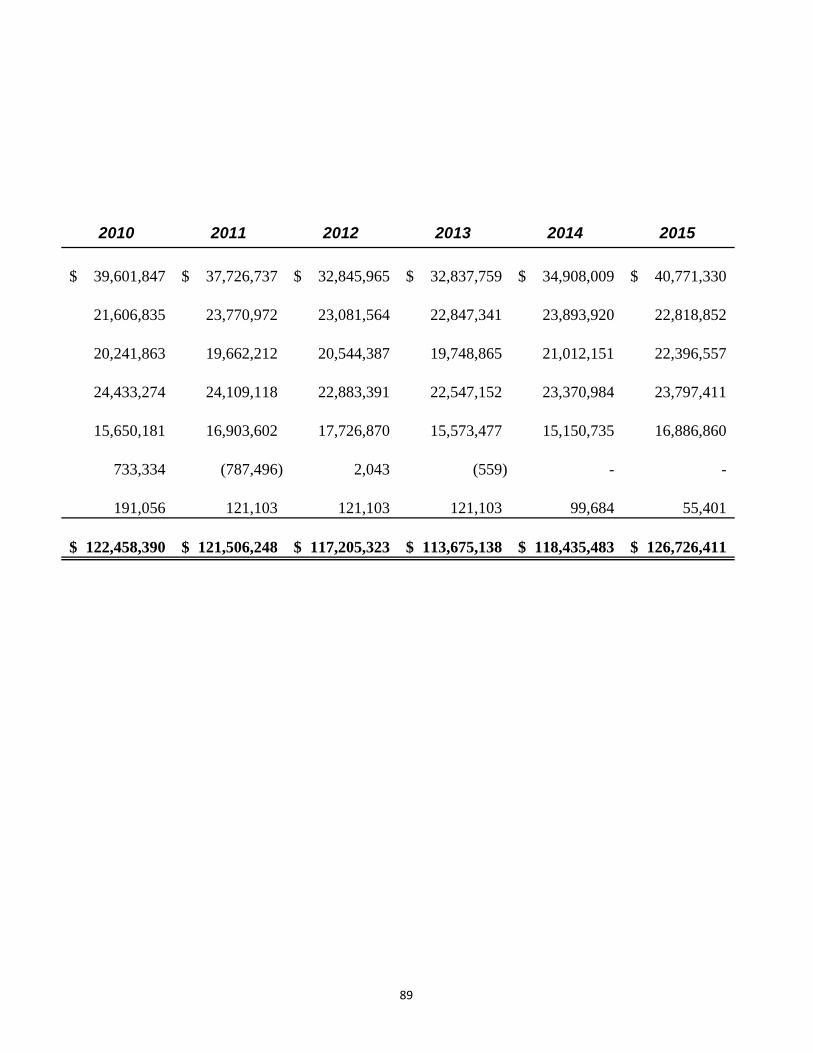

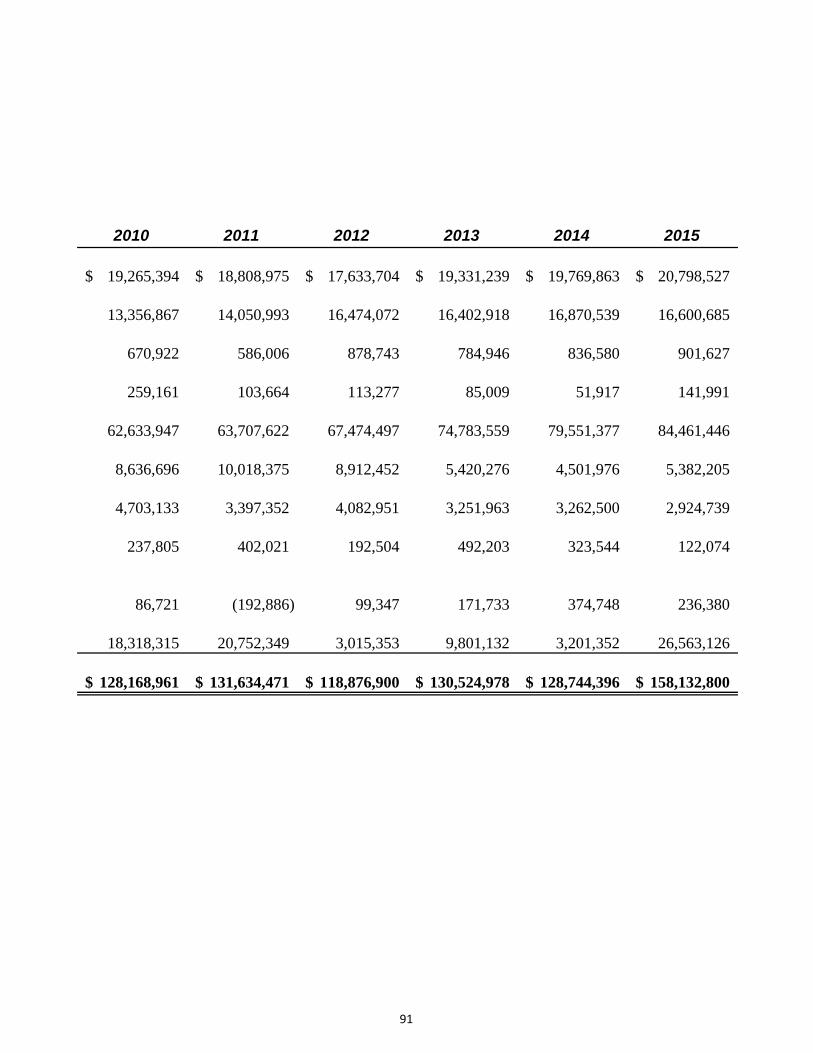

Net Position, Ten-Year Comparison ................................................................................. 85 Change in Net Position, Ten-Year Comparison ................................................................ 86 Expenses, Ten-Year Comparison ..................................................................................... 88

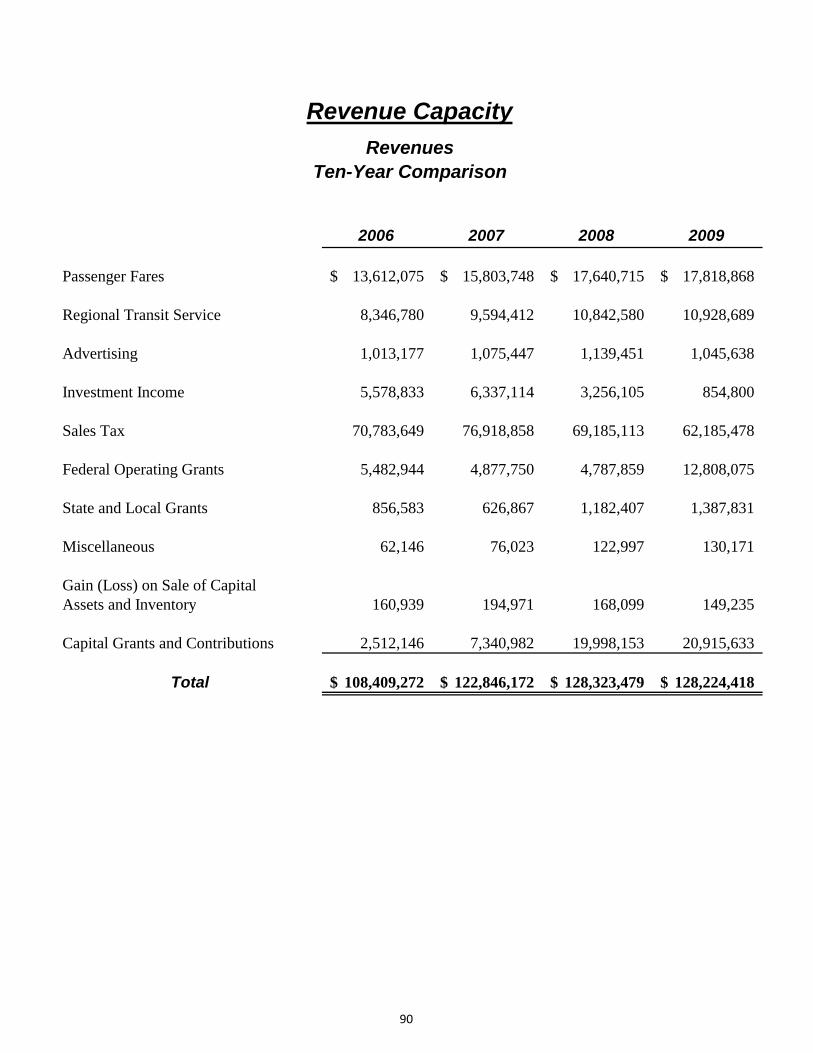

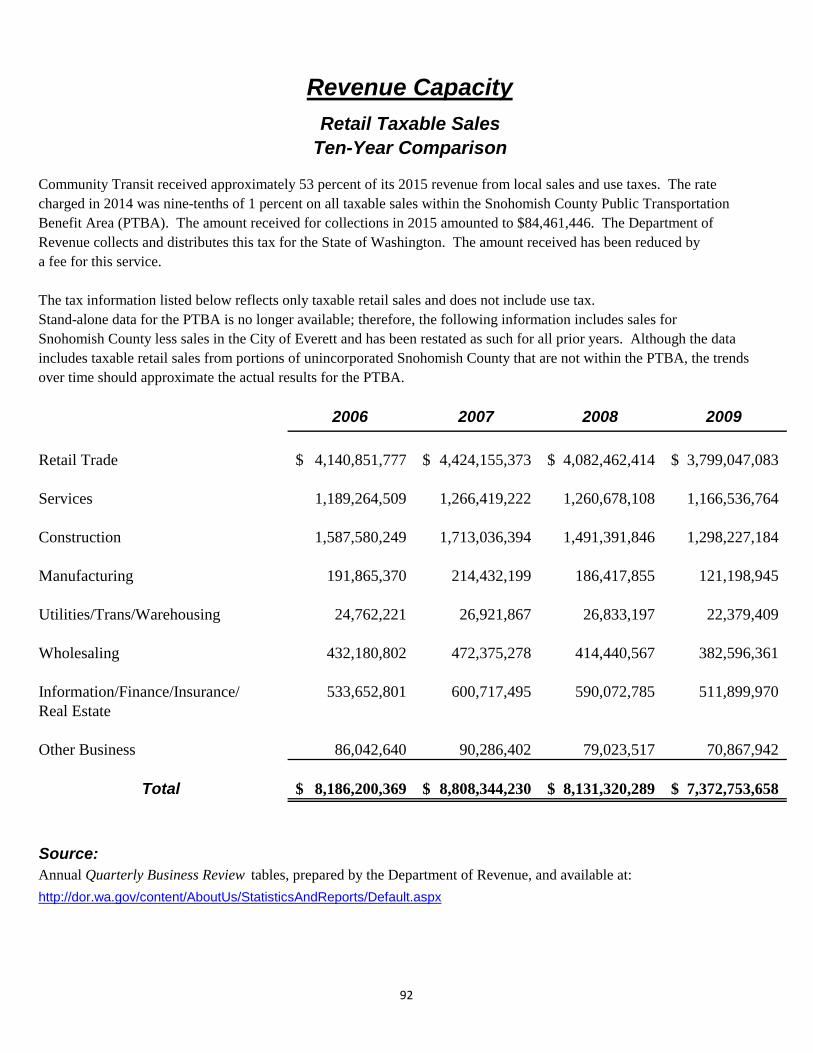

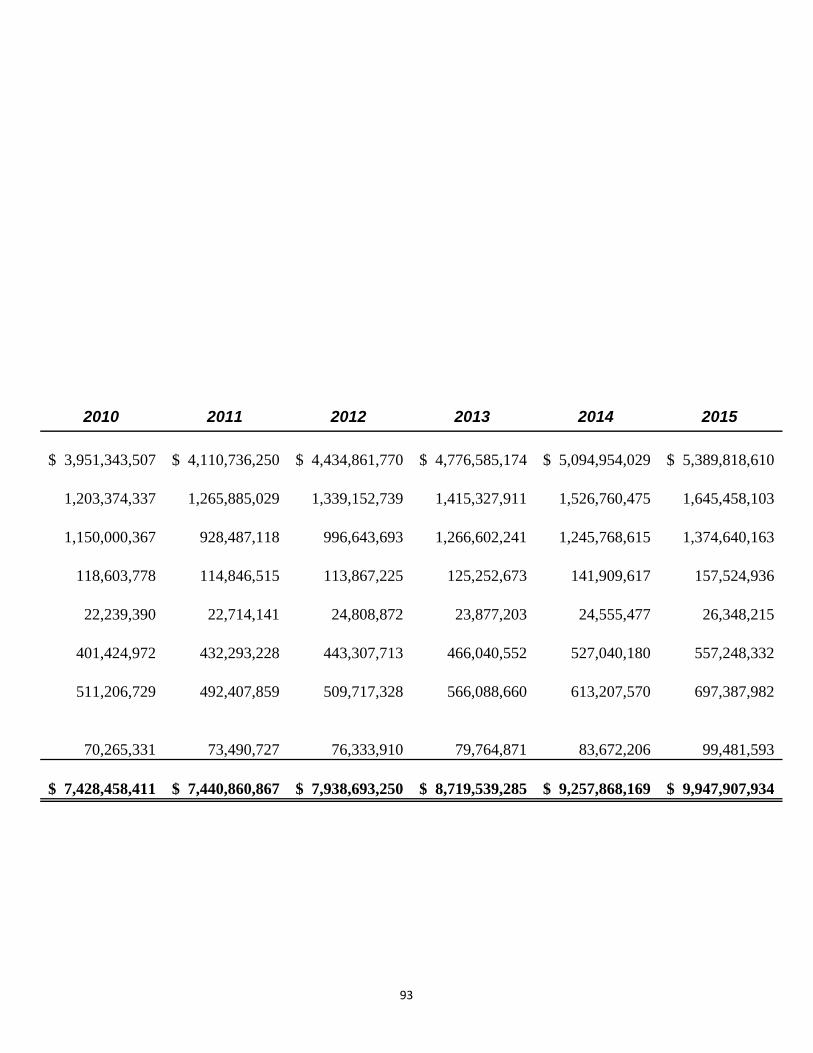

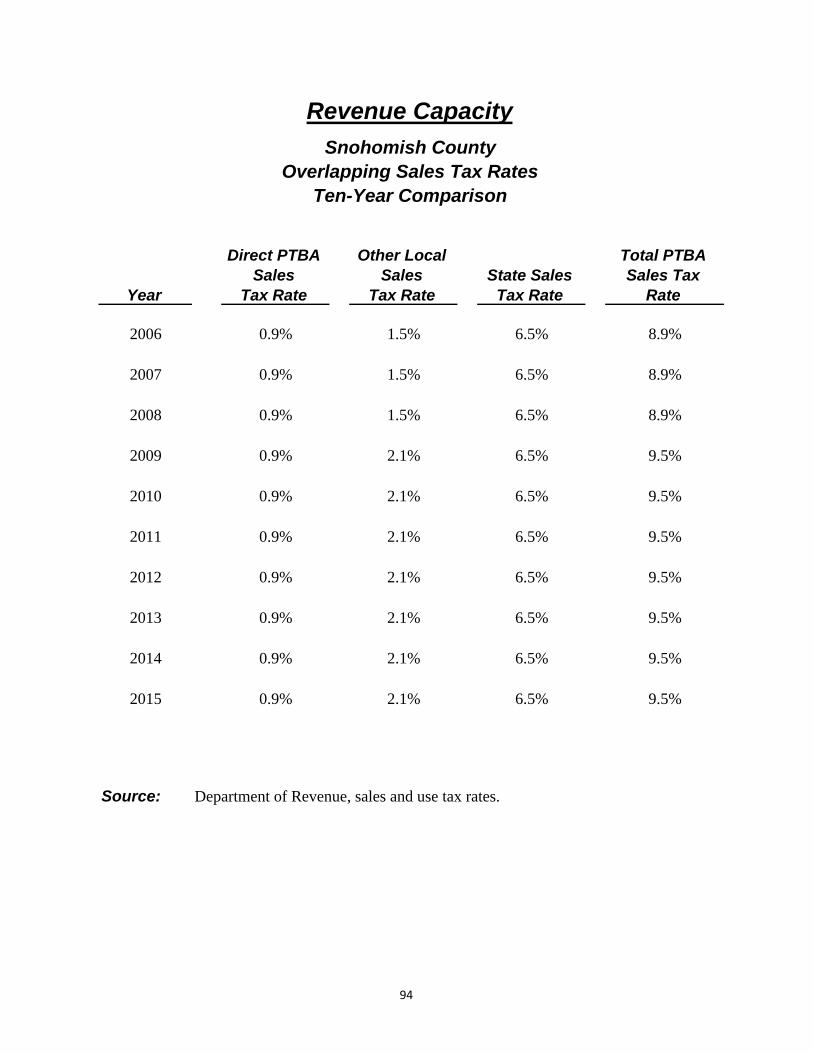

Revenue Capacity Revenues, Ten-Year Comparison .................................................................................... 90 Retail Taxable Sales, Ten-Year Comparison ................................................................... 92 Snohomish County Overlapping Sales Tax Rates, Ten-Year Comparison ...................... 94

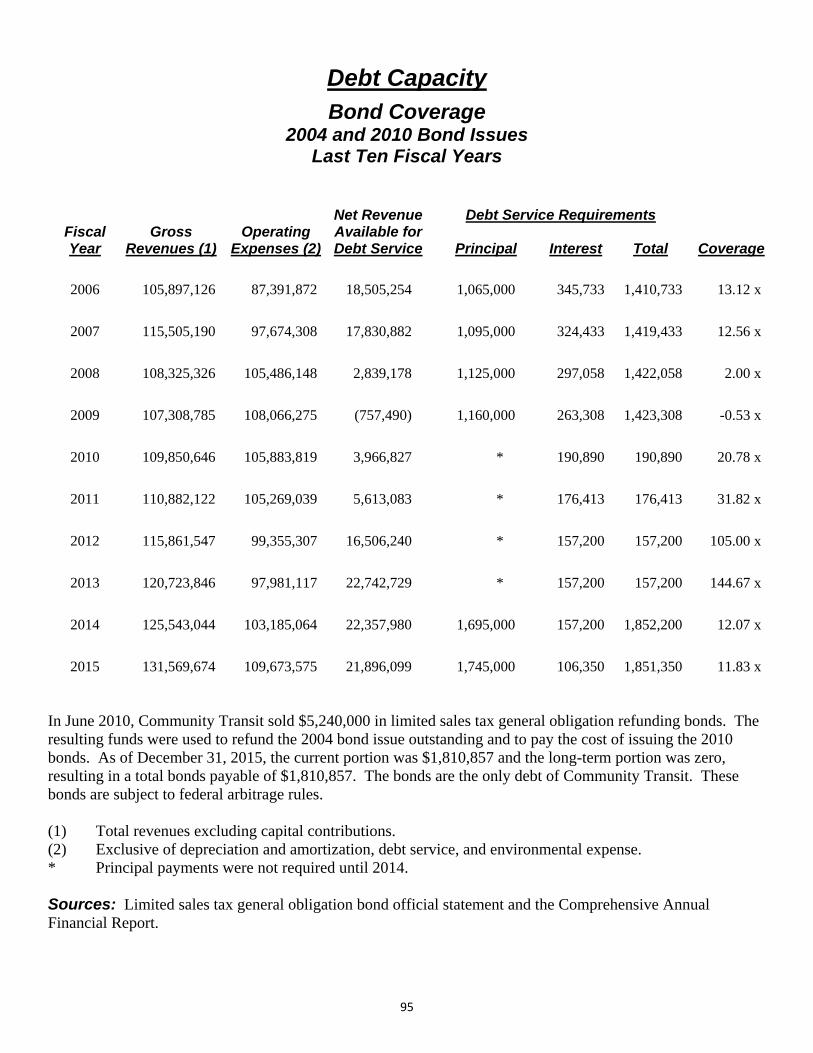

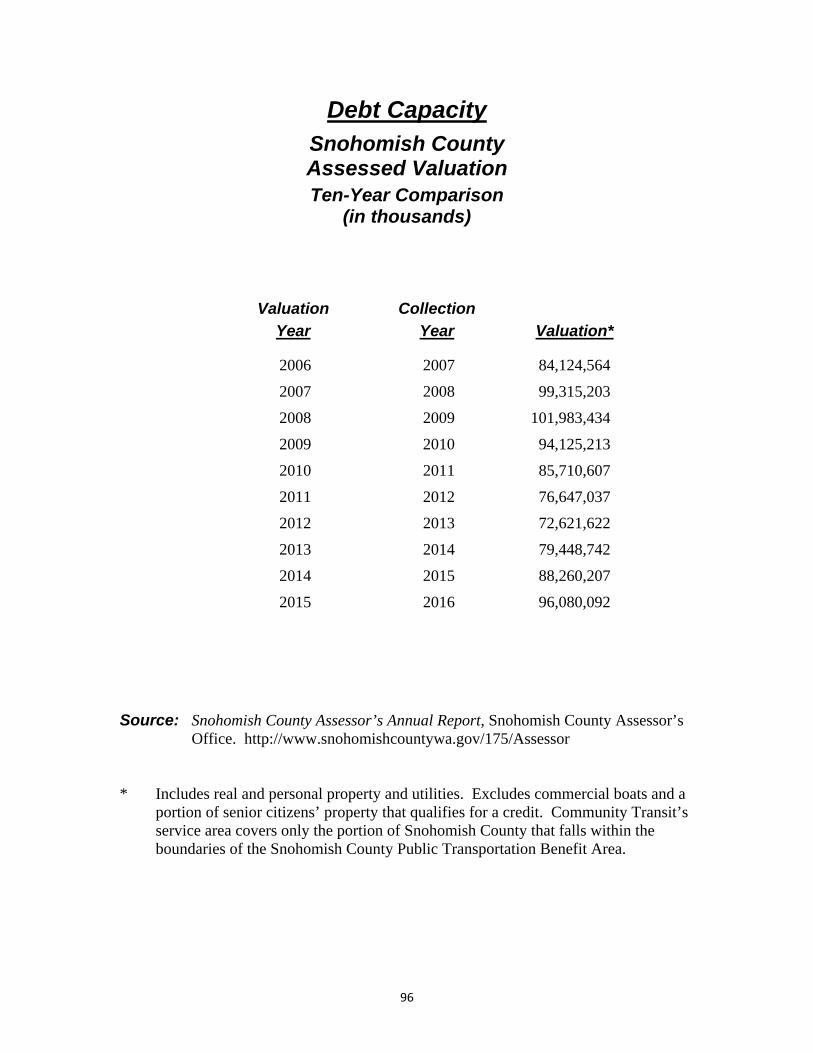

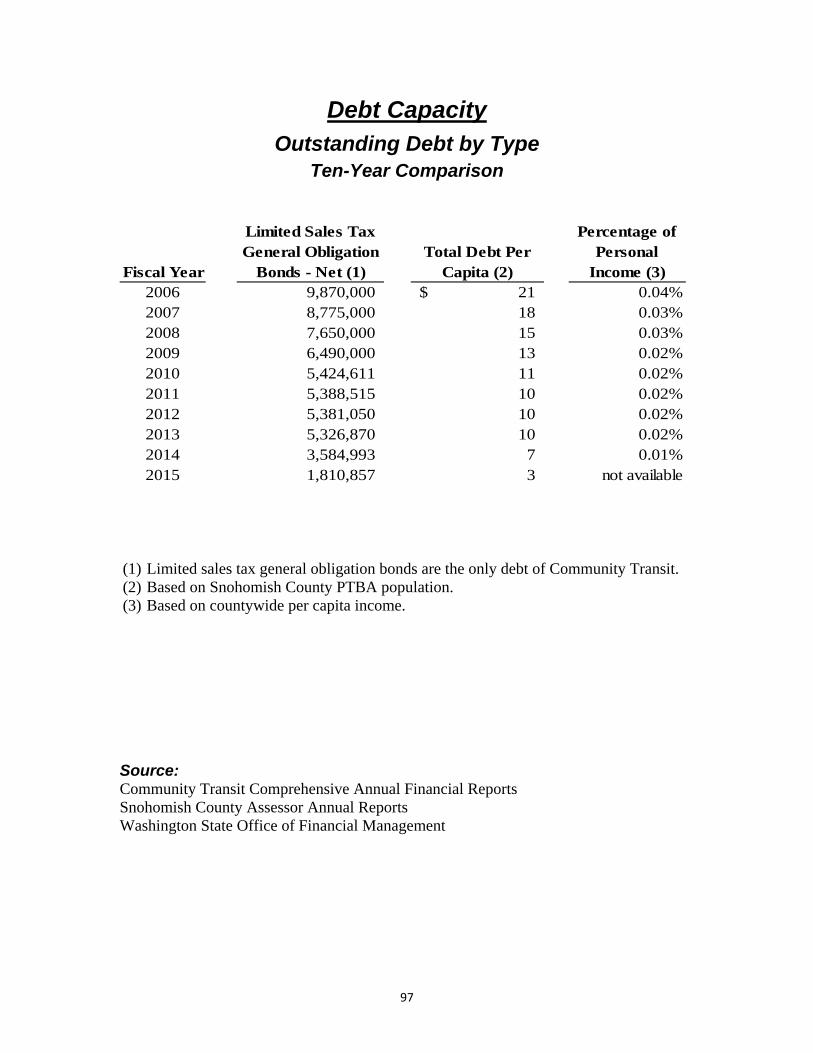

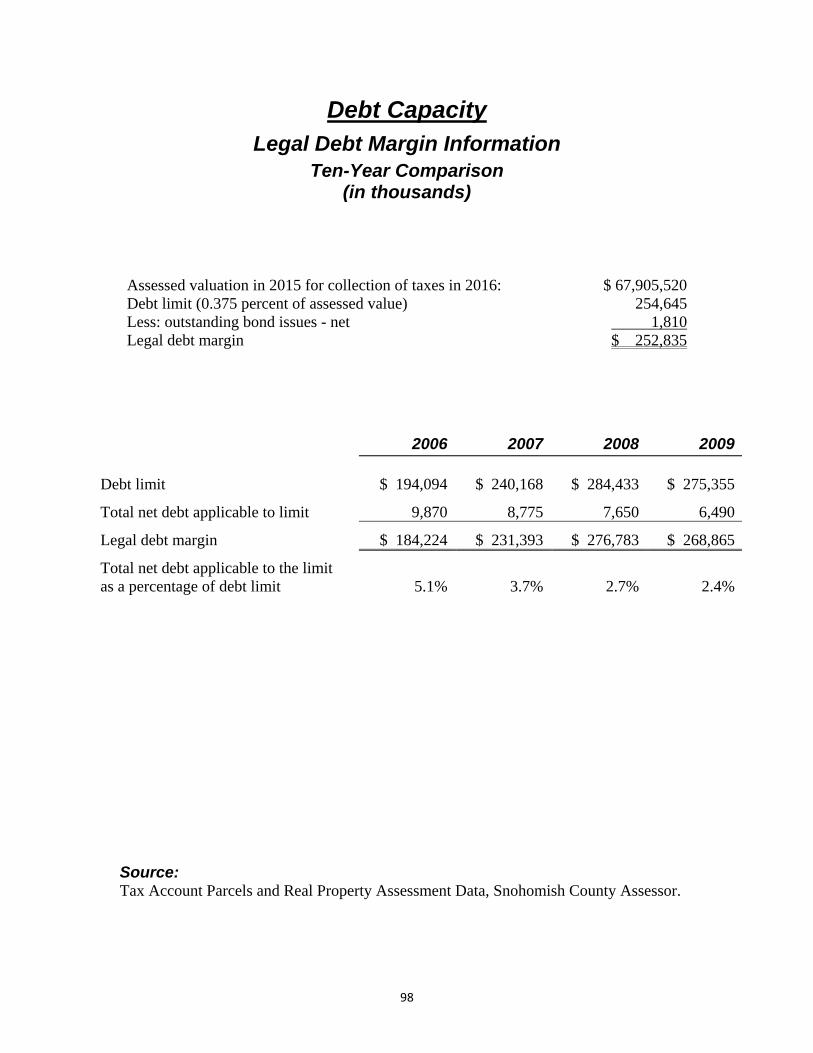

Debt Capacity Bond Coverage, 2004 and 2010 Bond Issues, Last Ten Fiscal Years ............................. 95 Snohomish County Assessed Valuation, Ten-Year Comparison ..................................... 96 Outstanding Debt by Type, Ten-Year Comparison ........................................................... 97 Legal Debt Margin Information, Ten-Year Comparison .................................................... 98

Demographic and Economic Information Snohomish County Demographic and Economic Statistics, Ten-Year Comparison ...... 100 Snohomish County Principal Employers, Fiscal Years Ending December 31, 2015

and 2006 ............................................................................................................ 101 Snohomish County Population Demographics Statistics, Ten-Year Comparison .......... 102

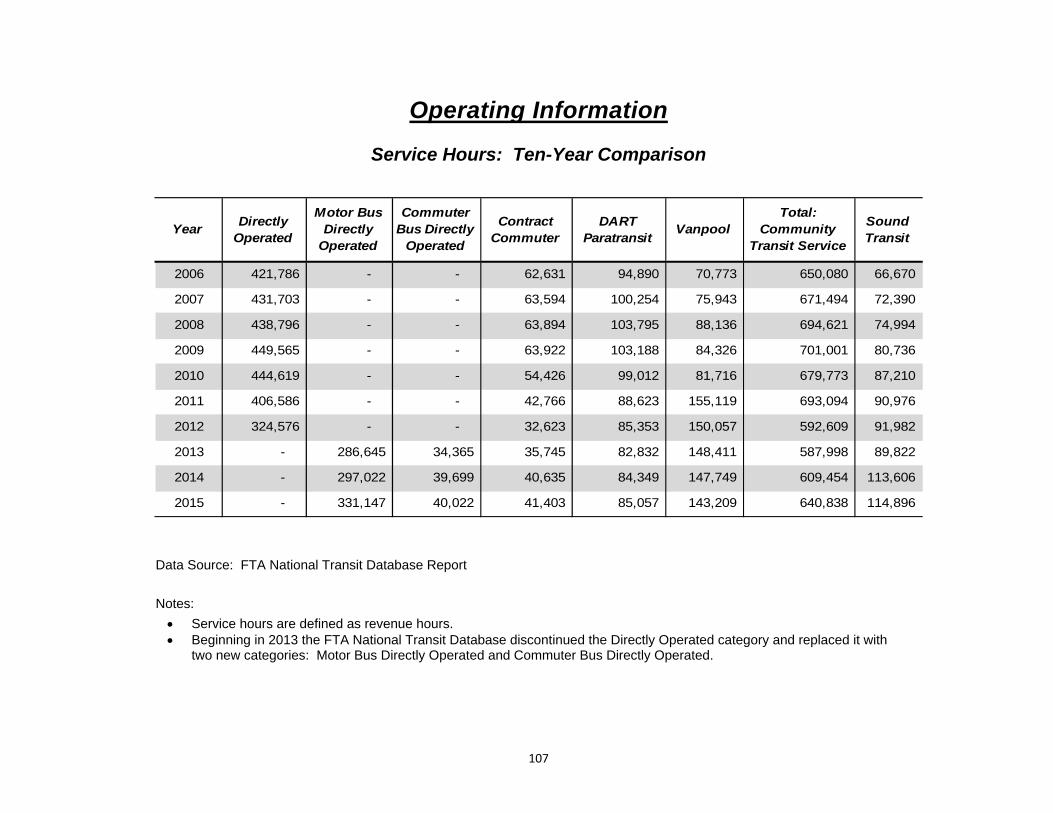

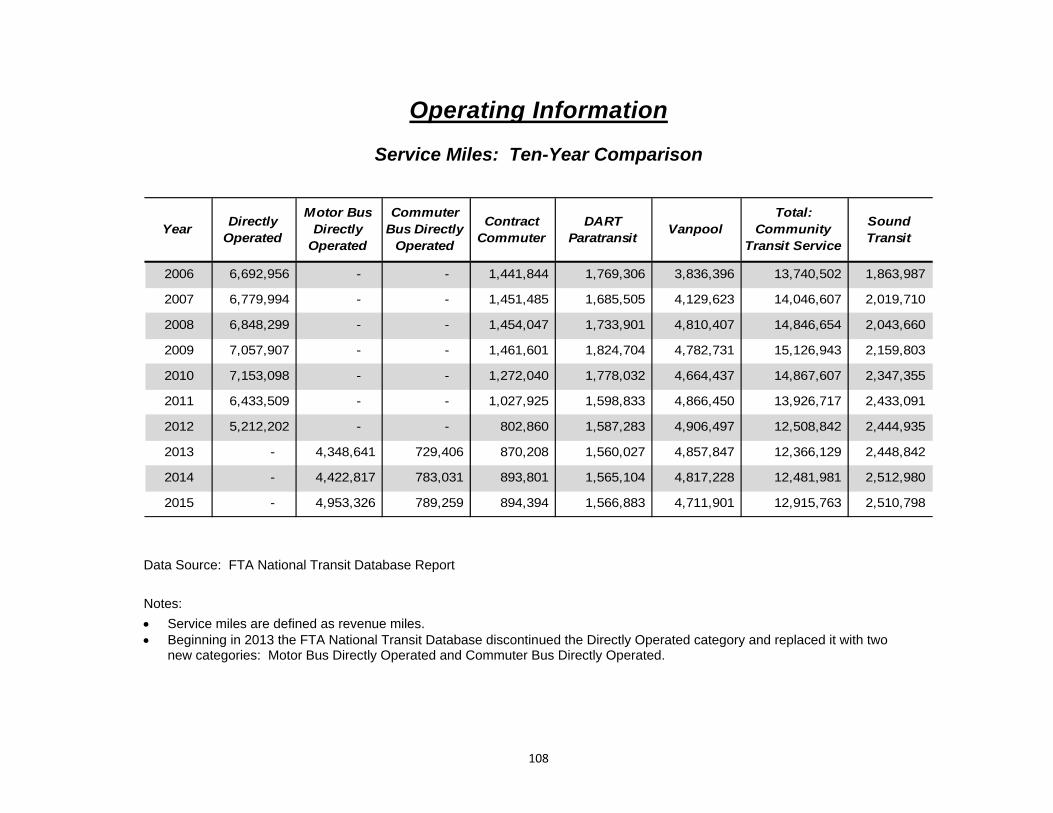

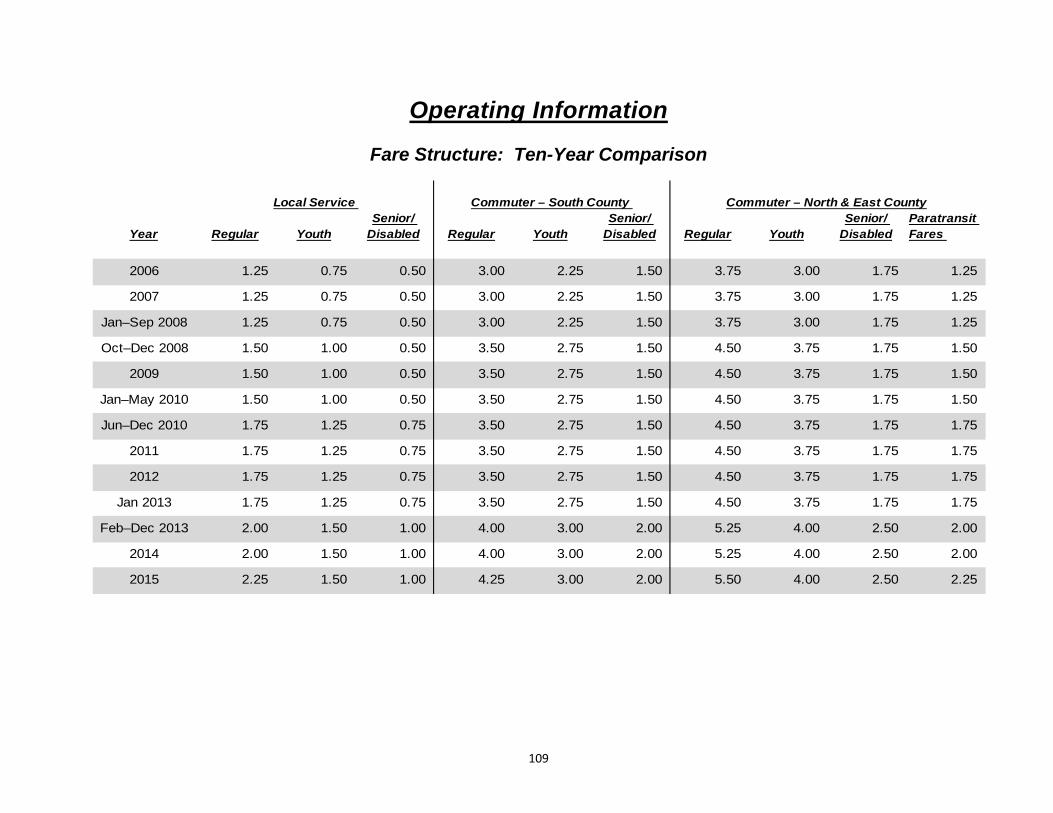

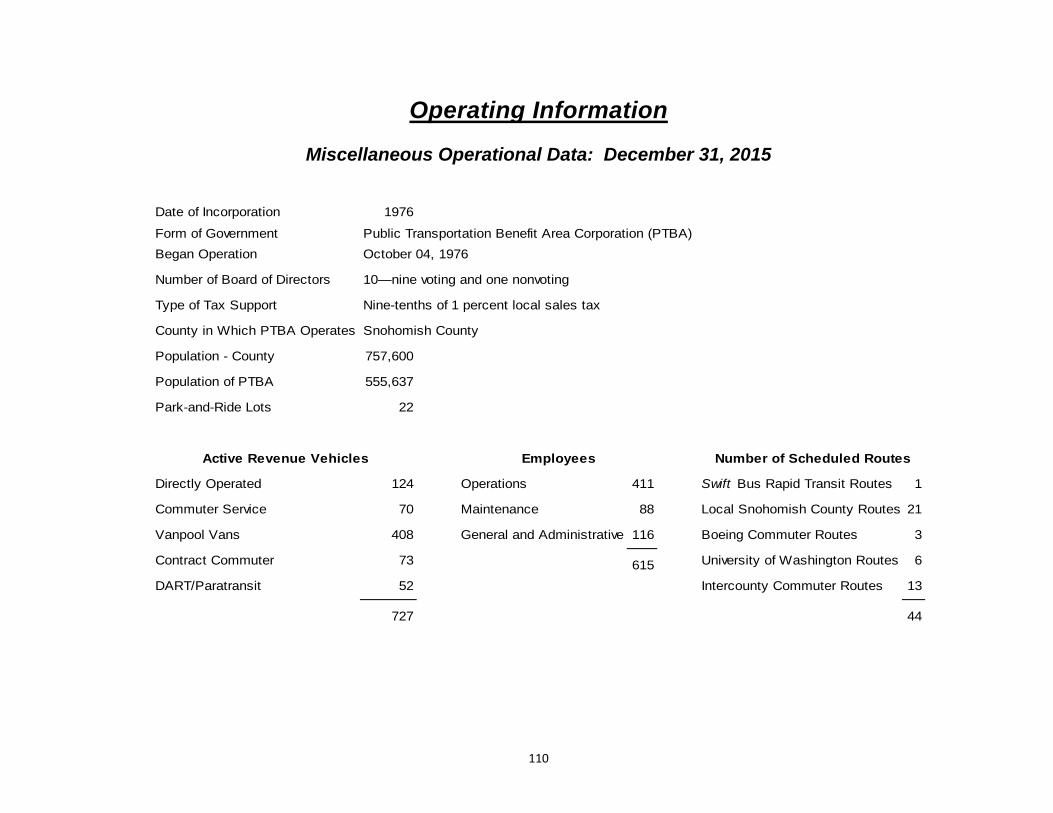

Operating Information Snohomish County Public Transportation Benefit Area Map 2015 ................................ 103 Service Statistical Data, Ten-Year Comparison ............................................................. 104 Ridership, Ten-Year Comparison ................................................................................... 106 Service Hours, Ten-Year Comparison ............................................................................ 107 Service Miles, Ten-Year Comparison ............................................................................. 108 Fare Structure, Ten-Year Comparison ............................................................................ 109 Miscellaneous Operational Data, December 31, 2015 ................................................... 110 Capital Assets, Active Revenue Vehicles, Ten-Year Comparison ................................. 111

This page left blank intentionally.

Intro

duct

ory

Sect

ion

Choice Connections is a Community Transit program that rewards you for choosing a better commute, and offers you the tools and resources to get started.

Samantha B.Cascadia College

Bus/Walk/Carpool/BikeChoice Connections 2015Smart Commuter of the 2nd Quarter

This page left blank intentionally.

1

Board of Directors June 21, 2016

Snohomish County Public Transportation Benefit Area Corporation Snohomish County, Washington

Subject: Comprehensive Annual Financial Report

Honorable Chair and Members of the Board:

This letter of transmittal presents Snohomish County Public Transportation Benefit Area

Corporation’s (dba Community Transit) Comprehensive Annual Financial Report for the years

ended December 31, 2015, and December 31, 2014. The Comprehensive Annual Financial

Report was prepared by Administration Department staff. Responsibility for the accuracy,

completeness, and fairness of the data presented and the clarity of the presentation,

including all disclosures, rests with the management of Community Transit. We believe the

data, as presented, is accurate in all material aspects, that it fairly presents Community

Transit’s financial position and results of operations, and that we have included disclosures

necessary for the reader to gain an understanding of Community Transit’s affairs.

This report was prepared in accordance with guidelines recommended by the Government

Finance Officers Association of the United States and Canada and conforms to generally

accepted accounting principles promulgated by the Governmental Accounting Standards

Board (GASB). This report contains three sections:

1. Introductory Section: Includes this letter of transmittal, a copy of the most recent Government Finance Officers Association Certificate of Achievement for Excellence in Financial Reporting, a list of principal officials, and the agency’s organization chart.

2. Financial Section: Includes the independent auditor’s opinion, management’s discussion and analysis, the basic financial statements with accompanying notes, and required supplementary information.

3. Statistical Section: Includes additional data about Community Transit’s past ten years of operation.

State law requires that Community Transit be audited annually for compliance with existing

statutes, adequacy of internal controls, and accuracy in financial accounting and reporting.

The Washington State Auditor’s Office has issued an unqualified (clean) opinion on

Community Transit’s financial statements for the years ended December 31, 2015, and

December 31, 2014. The independent auditor’s report is located at the front of the Financial

Section of this report.

Letter of Transmittal (cont.)

2

The Management’s Discussion and Analysis (MD&A) provides a narrative introduction,

overview, and analysis to the basic financial statements. This letter of transmittal is designed

to complement the MD&A and should be read in conjunction with it. Community Transit’s

MD&A can be found immediately following the independent auditor’s report.

Community Transit’s Profile

The Agency

Community Transit, a special purpose municipal corporation providing public transportation

services, began operations on October 4, 1976. The agency’s original service area consisted of

Edmonds, Lynnwood, Marysville, Mountlake Terrace, Brier, Snohomish, and Woodway. The

following table shows when residents of other Snohomish County communities approved

annexation into Community Transit’s service area.

Year Communities Added To Community Transit’s Service Area

1977 Lake Stevens and Monroe

1979 Granite Falls, Mukilteo, Stanwood, and Sultan

1980 Arlington

1981 Goldbar, Index, and Startup

1982 Oso and Darrington

1983 Mill Creek

1992 Snohomish County portion of Bothell

1997 Silver Firs and the Tulalip Indian Reservation

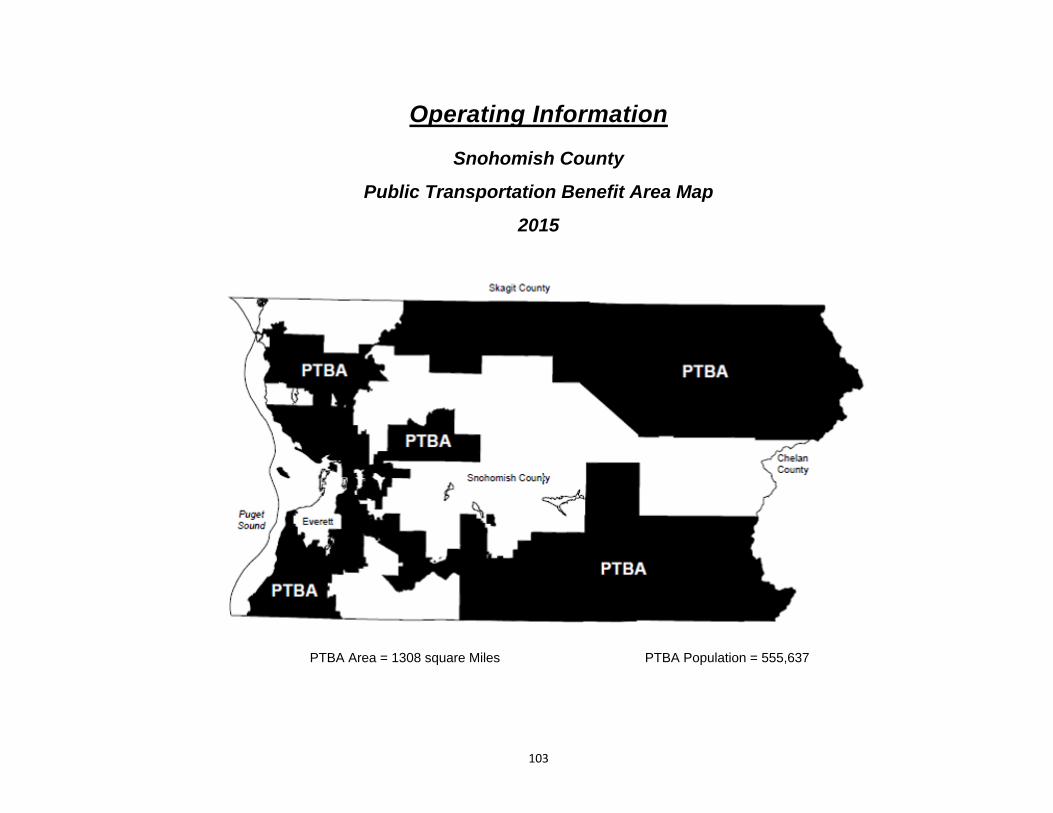

Today, Community Transit’s public transportation benefit area (PTBA) encompasses a land

area slightly in excess of 1,300 square miles including most of urbanized Snohomish County,

except for the City of Everett. On the south, Community Transit’s PTBA borders King County,

which includes the cities of Seattle and Bellevue.

Community Transit serves 555,637 residents, about 73 percent of Snohomish County’s

population. The remainder of the county’s population resides in the City of Everett and in less

populated areas in north and east Snohomish County.

Although the City of Everett is not part of Community Transit’s service area and taxing

authority, Community Transit provides Swift bus rapid transit service to Everett Station and

receives payment from the City of Everett for this service. Community Transit also operates

Everett Transit’s ORCA Call Center service under a separate contract, and Community Transit

and Everett Transit coordinate dial‐a‐ride transportation program (DART) paratransit services

to better serve our customers.

Letter of Transmittal (cont.)

3

Governing Body

Community Transit is governed by a Board of Directors consisting of nine voting members and

one nonvoting member. Voting board members are elected officials appointed by their

respective jurisdictions and elected to two‐year terms by representatives from similarly sized

cities. Voting board members include:

Two members of the Snohomish County Council.

Two elected officials from cities Community Transit serves with populations of more than 30,000.

Three elected officials from cities Community Transit serves with populations between 10,000 and 30,000.

Two elected officials from cities Community Transit serves with populations of less than 10,000.

The nonvoting board member is a labor representative selected as prescribed in RCW

36.57A.050 by the bargaining units who represent approximately 75 percent of Community

Transit’s workforce.

The Chair, Vice‐Chair, and Secretary are elected from among the voting Board members.

During 2015, Councilmember Mike Todd from the City of Mill Creek served as Chair, Mayor

Jon Nehring from the City of Marysville served as Vice‐Chair, and Councilmember Stephanie

Wright from the Snohomish County Council served as Secretary.

Community Transit’s Chief Executive Officer (CEO), Emmett Heath, is responsible for overall

administration of the agency as directed through policy guidance issued from the Board of

Directors. In addition to the CEO, the agency’s principal officers are the Director of

Administration (position vacant on December 31, 2015; filled by Geri Beardsley effective

January 4, 2016), Director of Customer Relations (Bob Throckmorton), Director of Planning

and Development (Joy Munkers), Director of Maintenance (Dave Richards), Director of

Transportation (Fred Worthen), Chief Technology Officer (Tim Chrobuck), and the Chief of

Strategic Communications (Todd Morrow).

Community Transit’s Services

Community Transit’s local, commuter, paratransit, and vanpool services provide riders with a

variety of options to meet their transportation needs. Local fixed‐route service provides all‐

day coverage which links most communities in Snohomish County. Commuter service

operates within Snohomish County and to major destinations in King County. The Everett

Boeing facility is the primary destination for Snohomish County commuter routes, while

commuter routes to King County serve the Seattle central business district and the University

of Washington. Both local and commuter services allow riders to connect with services

provided by King County Metro, Sound Transit, Everett Transit, Skagit Transit, Amtrak, and the

Washington State Ferry System.

Letter of Transmittal (cont.)

4

Community Transit’s DART serves those customers unable to use fixed‐route service because

of disabilities. Vanpool and ride‐matching services enable commuter groups to use vanpools

and carpools to travel to and from Snohomish and King County destinations that are less

accessible by local or commuter bus routes. Community Transit also provides information and

technical support to employers affected by the state’s commute trip reduction legislation.

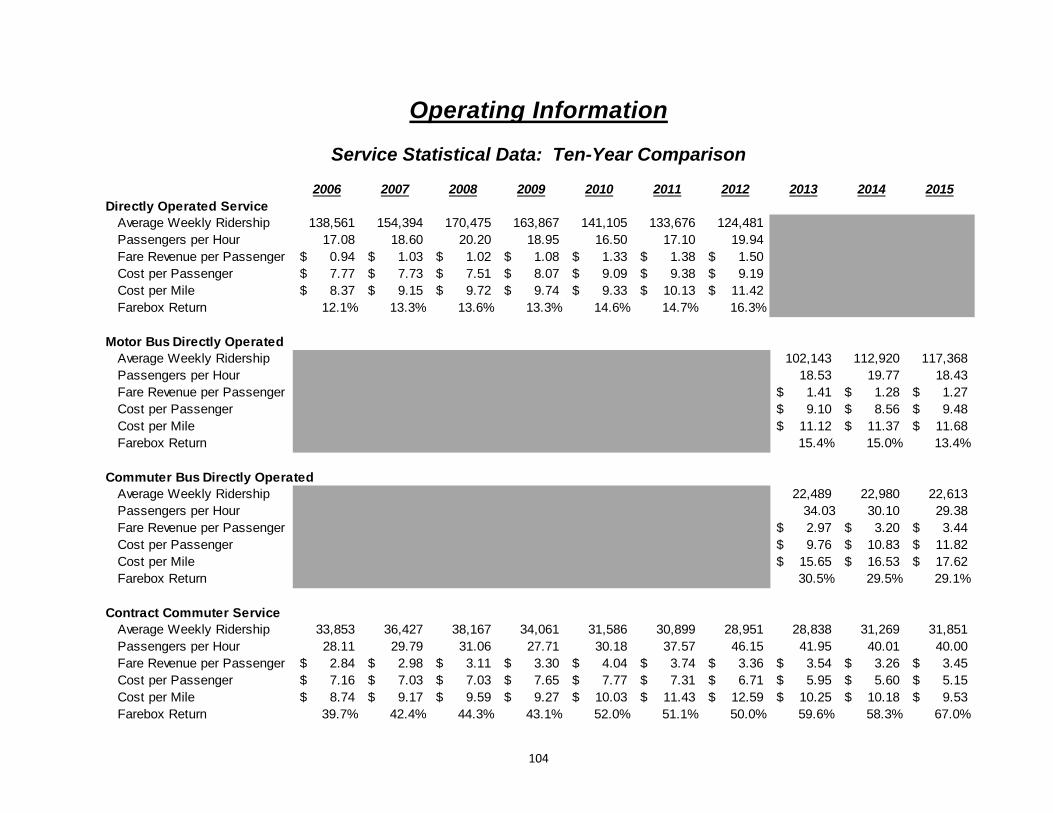

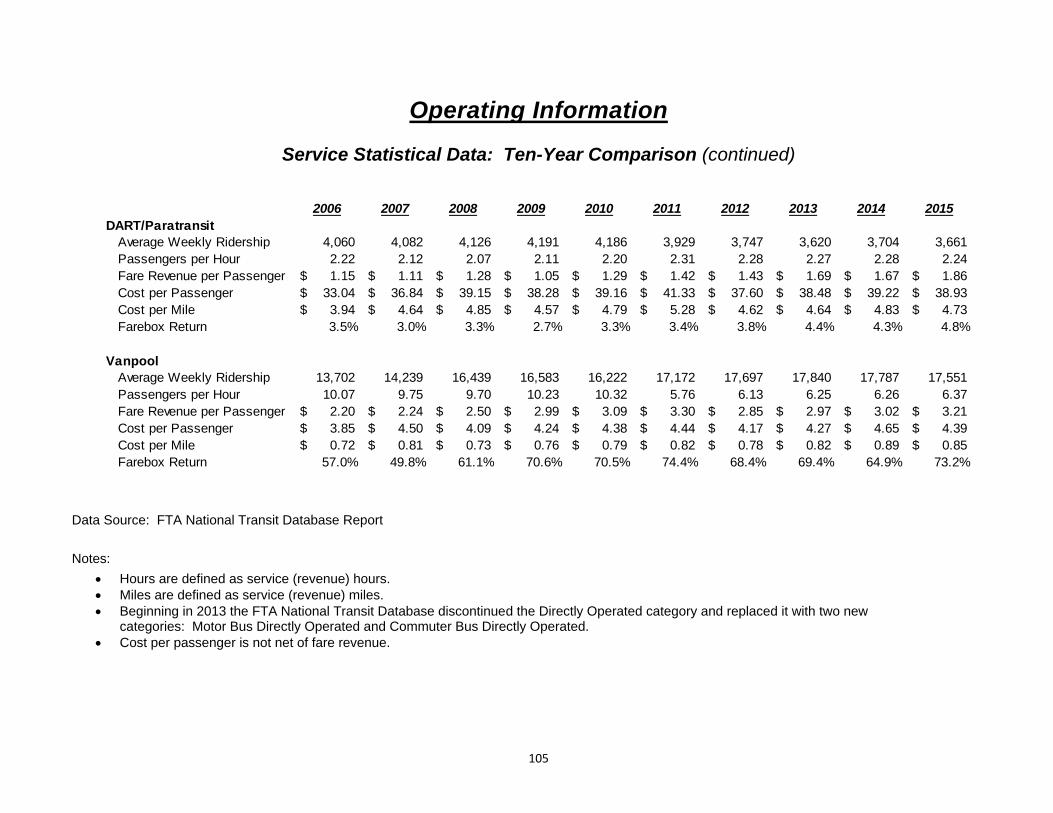

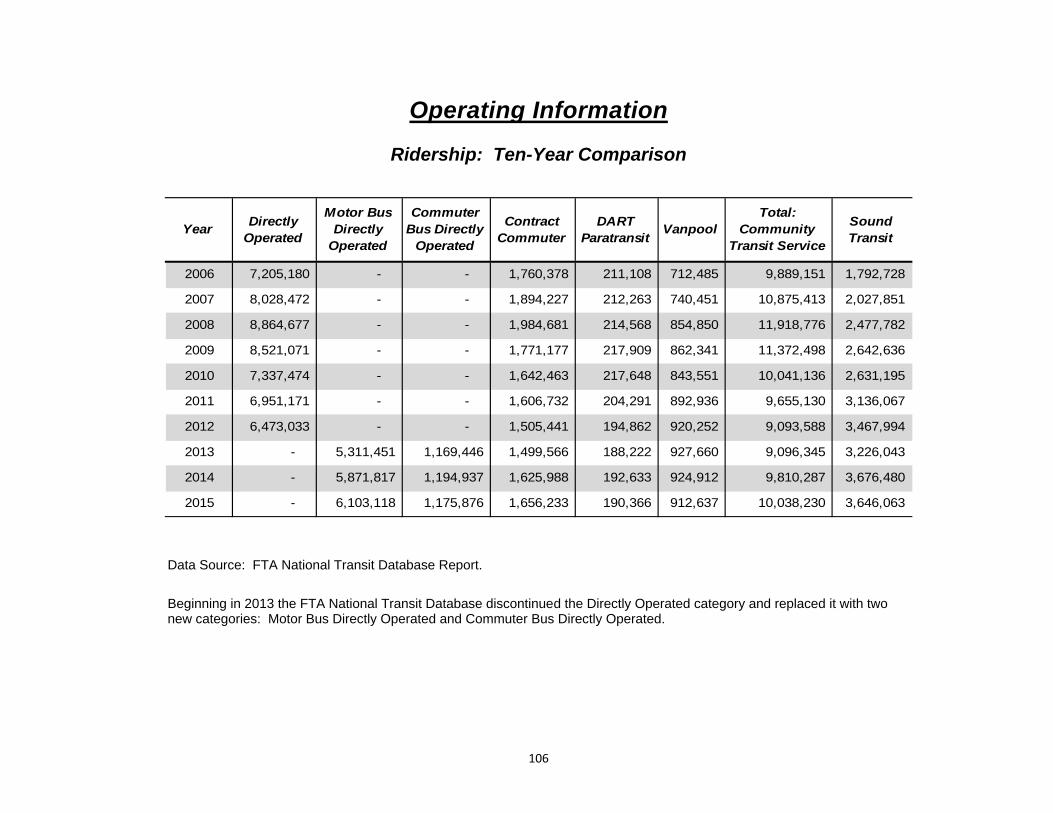

Ridership

Community Transit provided more than 10 million passenger trips in 2015 on bus, DART

paratransit, and vanpool services. Sunday and holiday service was restored in June 2015, after

being eliminated in 2010 due to the economic recession. Overall, ridership was 2 percent

higher than in 2014. There were 8.9 million bus boardings, 0.9 million vanpool boardings, and

0.2 million DART boardings.

As reported in agency system performance reports, 2015 weekday ridership averaged 36,769

boardings. Saturday ridership averaged 11,385 boardings. Sunday ridership averaged 6,538

boardings, and holiday service ridership averaged 4,889 boardings. The number of passenger

trips per hour of service (productivity) was 15.7 boardings per hour for all modes combined

and 21.7 boardings per hour for bus service.

The statistical section of this report contains additional detailed operating information

including ridership, service hours, and fares.

Stewardship of Public Funds

Budget Process and Financial Oversight

The Board of Directors adopts both short‐term and long‐range plans that define the financial

and service goals for the agency. The Six‐Year Transit Development Plan (TDP) is updated

each year and provides parameters for the annual budget. Based on TDP goals, staff develop

an agency business plan which is used to prepare the agency’s annual budget. The Board of

Directors adopts the agency budget after review and public comment.

The annual budget fully funds that year’s operating expense, capital development, and

reserves needed for preservation of capital assets, workers’ compensation, bond covenant

requirements, and replacement of vehicles. The Board monitors the annual budget and

agency financial activities through authorization of all expenditures exceeding $100,000 and

review of monthly expenditure listings, quarterly financial reports, and the Comprehensive

Annual Financial Report.

Financial Practices

Community Transit places emphasis on internal financial controls designed to provide

reasonable (not absolute) assurance regarding protection of assets against loss from

Letter of Transmittal (cont.)

5

unauthorized use or disposition and reliability of financial records used to prepare financial

statements and account for assets. We believe Community Transit’s internal controls

adequately safeguard assets and provide reasonable assurance of proper recording of

financial transactions. For more information about the agency’s accounting system and

budget practices, please see Note 1 to the Financial Statements.

Community Transit’s Procurement staff earned the Outstanding Agency Accreditation

Achievement Award from the National Institute for Government Procurement (NGIP) for a

three‐year period ending in February 2017. Only 5 percent of NGIP members have earned this

recognition. The agency completed their 21st consecutive annual audit with no audit findings,

and earned its 26th consecutive Certificate of Achievement for Excellence in Financial

Reporting from the Government Finance Officers Association (GFOA). These achievements

speak to the quality and integrity of Community Transit’s financial programs and staff.

Accomplishments

Community Transit wants customers to “Think Transit First.” To support that goal, we want

our customer service, technology, transit centers, and buses to be inviting and consumer

friendly. Much of the work that supports “Think Transit First” occurs behind the scenes when

staff determine how much service and what customer amenities our resources can support

and then actively seek funding for future initiatives that will serve current and future riders.

Community Transit accomplished the following initiatives in 2015:

Increased service by 27,000 hours, including restoration of Sunday and holiday bus and DART paratransit service, starting in June 2015.

Completed safety and environmental upgrades at Ash Way and Swamp Creek Park & Rides.

Replaced 17 aging articulated buses with new Double Tall buses and added an additional five Double Talls, resulting in a Double Tall fleet of 45 vehicles.

Continued project development (environment, design, and engineering) for a second Swift line that will run east/west from the Canyon Park regional growth center in Bothell to the Paine Field/Boeing manufacturing and industrial center in Everett. In September 2015, Community Transit submitted for a FTA Small Starts rating for federal grant funds to build the project. Swift II bus rapid transit received a medium rating and has been recommended for FTA Small Starts funding in 2017. By the end of 2016, the Swift II bus rapid transit project, which includes Seaway Transit Center, 128th and I‐5 approach widening, and station corridors, will have reached the 60 percent design threshold. The construction phase of Swift II bus rapid transit is slated to begin in 2017.

Letter of Transmittal (cont.)

6

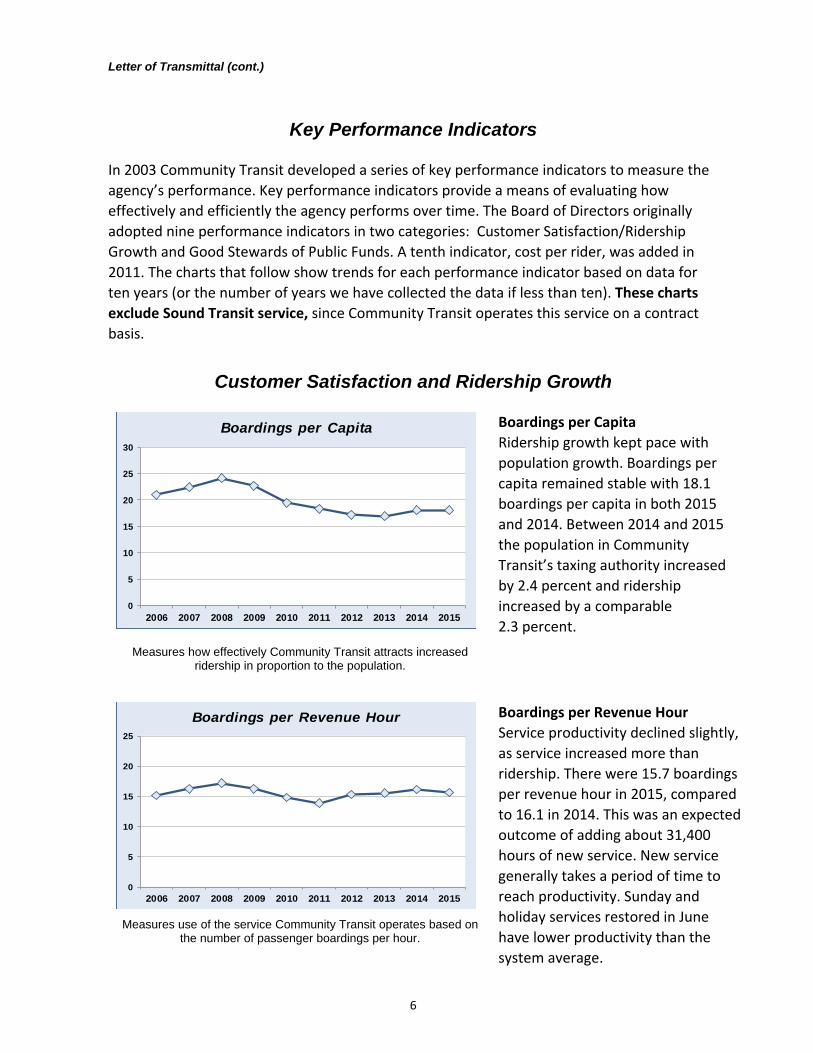

Key Performance Indicators

In 2003 Community Transit developed a series of key performance indicators to measure the

agency’s performance. Key performance indicators provide a means of evaluating how

effectively and efficiently the agency performs over time. The Board of Directors originally

adopted nine performance indicators in two categories: Customer Satisfaction/Ridership

Growth and Good Stewards of Public Funds. A tenth indicator, cost per rider, was added in

2011. The charts that follow show trends for each performance indicator based on data for

ten years (or the number of years we have collected the data if less than ten). These charts

exclude Sound Transit service, since Community Transit operates this service on a contract

basis.

Customer Satisfaction and Ridership Growth

0

5

10

15

20

25

30

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Boardings per Capita

Boardings per Capita

Ridership growth kept pace with

population growth. Boardings per

capita remained stable with 18.1

boardings per capita in both 2015

and 2014. Between 2014 and 2015

the population in Community

Transit’s taxing authority increased

by 2.4 percent and ridership

increased by a comparable

2.3 percent.

Measures how effectively Community Transit attracts increased ridership in proportion to the population.

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Boardings per Revenue Hour Boardings per Revenue Hour

Service productivity declined slightly,

as service increased more than

ridership. There were 15.7 boardings

per revenue hour in 2015, compared

to 16.1 in 2014. This was an expected

outcome of adding about 31,400

hours of new service. New service

generally takes a period of time to

reach productivity. Sunday and

holiday services restored in June

have lower productivity than the

system average.

Measures use of the service Community Transit operates based on the number of passenger boardings per hour.

Letter of Transmittal (cont.)

7

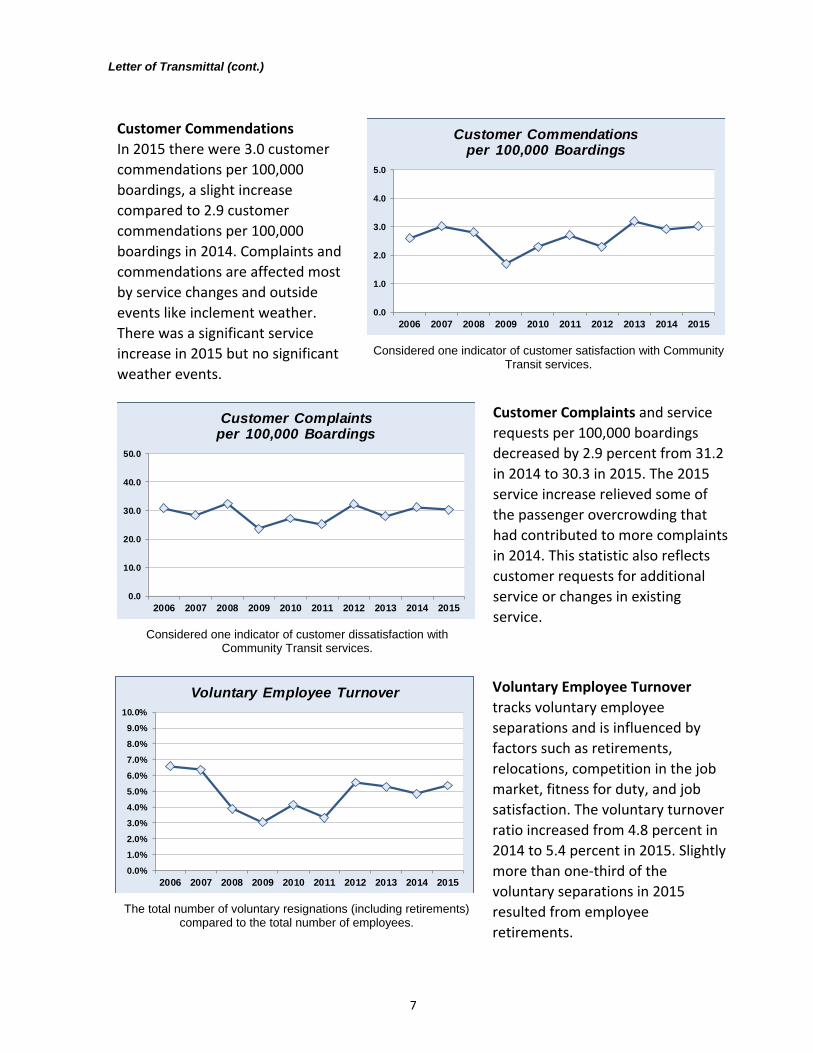

Customer Commendations

In 2015 there were 3.0 customer

commendations per 100,000

boardings, a slight increase

compared to 2.9 customer

commendations per 100,000

boardings in 2014. Complaints and

commendations are affected most

by service changes and outside

events like inclement weather.

There was a significant service

increase in 2015 but no significant

weather events.

0.0

1.0

2.0

3.0

4.0

5.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Customer Commendationsper 100,000 Boardings

Considered one indicator of customer satisfaction with Community Transit services.

0.0

10.0

20.0

30.0

40.0

50.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Customer Complaintsper 100,000 Boardings

Customer Complaints and service

requests per 100,000 boardings

decreased by 2.9 percent from 31.2

in 2014 to 30.3 in 2015. The 2015

service increase relieved some of

the passenger overcrowding that

had contributed to more complaints

in 2014. This statistic also reflects

customer requests for additional

service or changes in existing

service. Considered one indicator of customer dissatisfaction with

Community Transit services.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Voluntary Employee Turnover Voluntary Employee Turnover

tracks voluntary employee

separations and is influenced by

factors such as retirements,

relocations, competition in the job

market, fitness for duty, and job

satisfaction. The voluntary turnover

ratio increased from 4.8 percent in

2014 to 5.4 percent in 2015. Slightly

more than one‐third of the

voluntary separations in 2015

resulted from employee

retirements.

The total number of voluntary resignations (including retirements) compared to the total number of employees.

Letter of Transmittal (cont.)

8

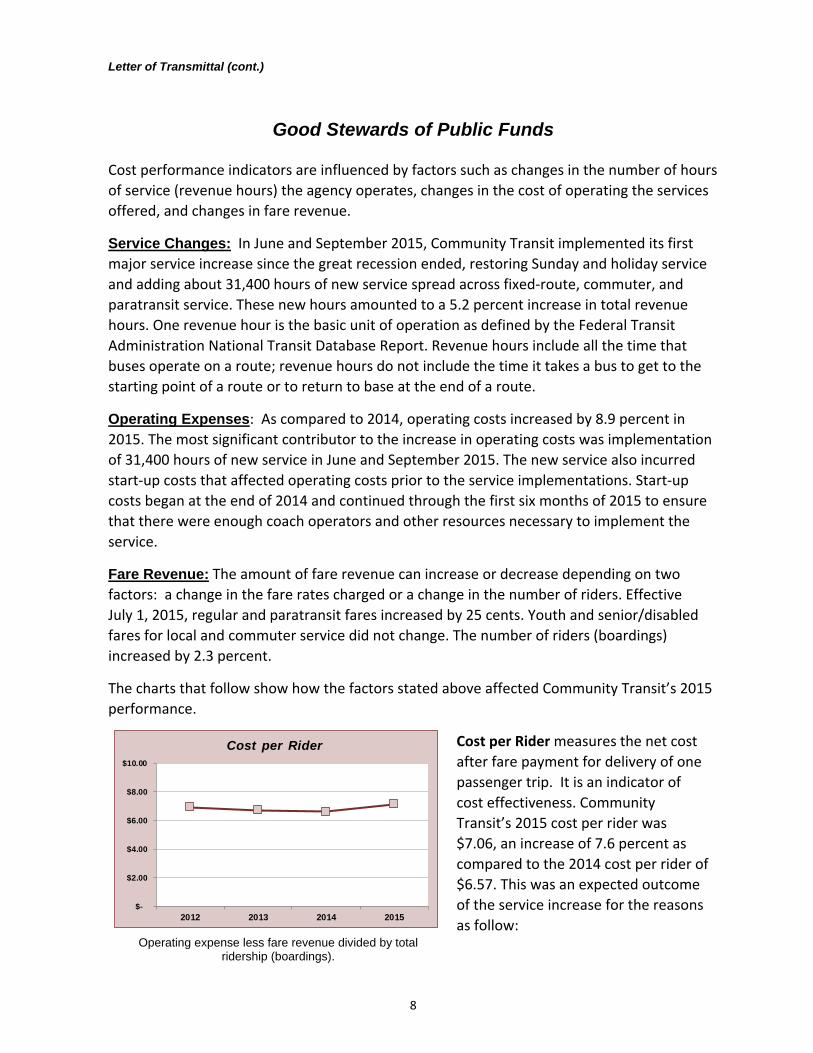

Good Stewards of Public Funds

Cost performance indicators are influenced by factors such as changes in the number of hours

of service (revenue hours) the agency operates, changes in the cost of operating the services

offered, and changes in fare revenue.

Service Changes: In June and September 2015, Community Transit implemented its first

major service increase since the great recession ended, restoring Sunday and holiday service

and adding about 31,400 hours of new service spread across fixed‐route, commuter, and

paratransit service. These new hours amounted to a 5.2 percent increase in total revenue

hours. One revenue hour is the basic unit of operation as defined by the Federal Transit

Administration National Transit Database Report. Revenue hours include all the time that

buses operate on a route; revenue hours do not include the time it takes a bus to get to the

starting point of a route or to return to base at the end of a route.

Operating Expenses: As compared to 2014, operating costs increased by 8.9 percent in

2015. The most significant contributor to the increase in operating costs was implementation

of 31,400 hours of new service in June and September 2015. The new service also incurred

start‐up costs that affected operating costs prior to the service implementations. Start‐up

costs began at the end of 2014 and continued through the first six months of 2015 to ensure

that there were enough coach operators and other resources necessary to implement the

service.

Fare Revenue: The amount of fare revenue can increase or decrease depending on two

factors: a change in the fare rates charged or a change in the number of riders. Effective

July 1, 2015, regular and paratransit fares increased by 25 cents. Youth and senior/disabled

fares for local and commuter service did not change. The number of riders (boardings)

increased by 2.3 percent.

The charts that follow show how the factors stated above affected Community Transit’s 2015

performance.

$-

$2.00

$4.00

$6.00

$8.00

$10.00

2012 2013 2014 2015

Cost per Rider Cost per Rider measures the net cost

after fare payment for delivery of one

passenger trip. It is an indicator of

cost effectiveness. Community

Transit’s 2015 cost per rider was

$7.06, an increase of 7.6 percent as

compared to the 2014 cost per rider of

$6.57. This was an expected outcome

of the service increase for the reasons

as follow: Operating expense less fare revenue divided by total

ridership (boardings).

Letter of Transmittal (cont.)

9

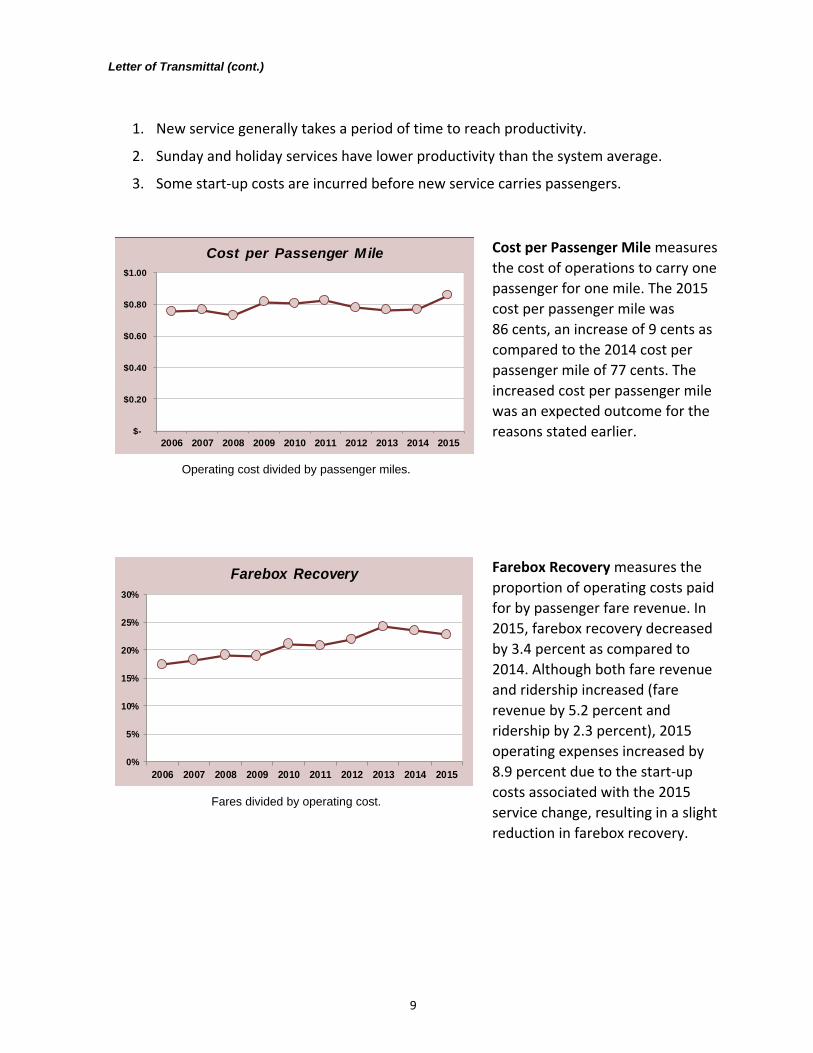

1. New service generally takes a period of time to reach productivity.

2. Sunday and holiday services have lower productivity than the system average.

3. Some start‐up costs are incurred before new service carries passengers.

$-

$0.20

$0.40

$0.60

$0.80

$1.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Cost per Passenger Mile Cost per Passenger Mile measures

the cost of operations to carry one

passenger for one mile. The 2015

cost per passenger mile was

86 cents, an increase of 9 cents as

compared to the 2014 cost per

passenger mile of 77 cents. The

increased cost per passenger mile

was an expected outcome for the

reasons stated earlier.

Operating cost divided by passenger miles.

0%

5%

10%

15%

20%

25%

30%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Farebox Recovery Farebox Recovery measures the

proportion of operating costs paid

for by passenger fare revenue. In

2015, farebox recovery decreased

by 3.4 percent as compared to

2014. Although both fare revenue

and ridership increased (fare

revenue by 5.2 percent and

ridership by 2.3 percent), 2015

operating expenses increased by

8.9 percent due to the start‐up

costs associated with the 2015

service change, resulting in a slight

reduction in farebox recovery.

Fares divided by operating cost.

Letter of Transmittal (cont.)

10

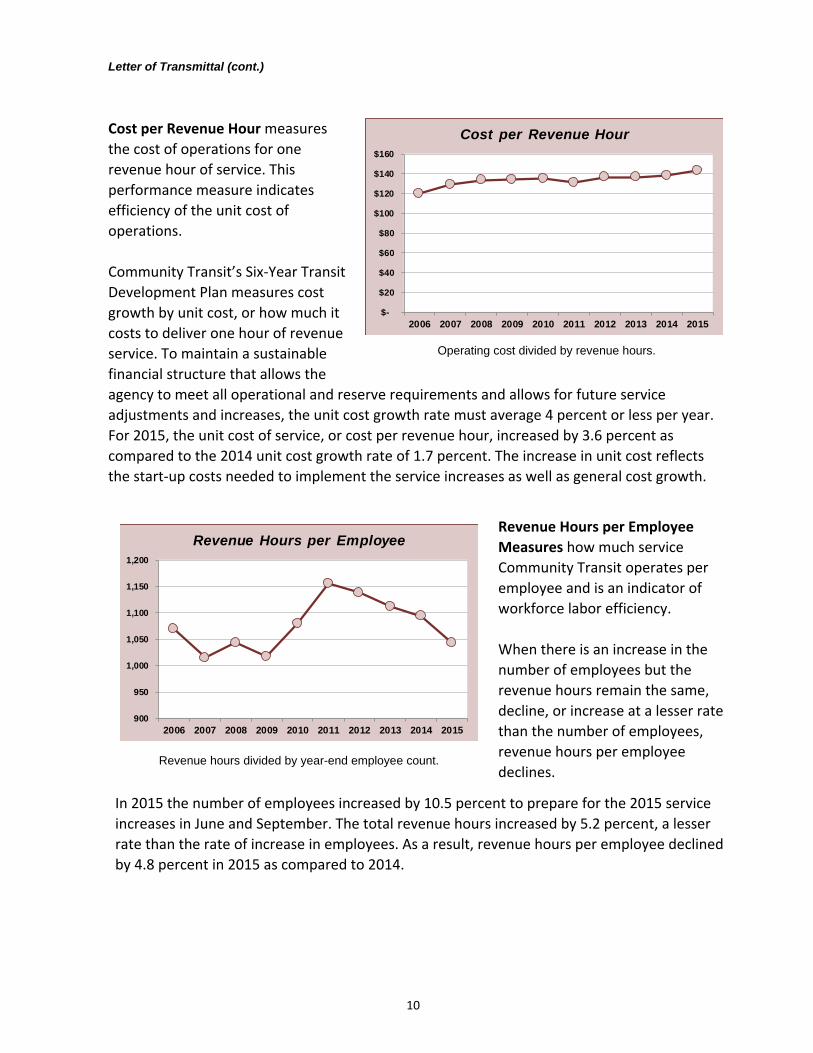

Cost per Revenue Hour measures

the cost of operations for one

revenue hour of service. This

performance measure indicates

efficiency of the unit cost of

operations.

Community Transit’s Six‐Year Transit

Development Plan measures cost

growth by unit cost, or how much it

costs to deliver one hour of revenue

service. To maintain a sustainable

financial structure that allows the

$-

$20

$40

$60

$80

$100

$120

$140

$160

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Cost per Revenue Hour

Operating cost divided by revenue hours.

agency to meet all operational and reserve requirements and allows for future service

adjustments and increases, the unit cost growth rate must average 4 percent or less per year.

For 2015, the unit cost of service, or cost per revenue hour, increased by 3.6 percent as

compared to the 2014 unit cost growth rate of 1.7 percent. The increase in unit cost reflects

the start‐up costs needed to implement the service increases as well as general cost growth.

900

950

1,000

1,050

1,100

1,150

1,200

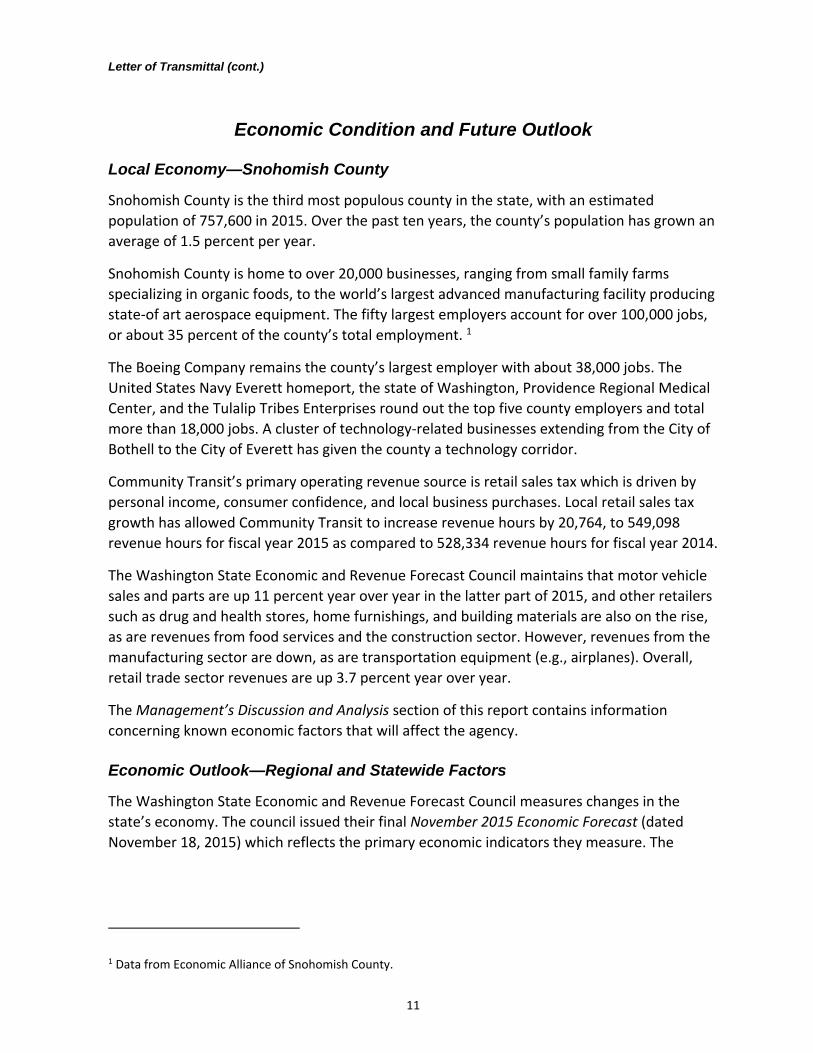

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Revenue Hours per Employee

Revenue Hours per Employee

Measures how much service

Community Transit operates per

employee and is an indicator of

workforce labor efficiency.

When there is an increase in the

number of employees but the

revenue hours remain the same,

decline, or increase at a lesser rate

than the number of employees,

revenue hours per employee

declines. Revenue hours divided by year-end employee count.

In 2015 the number of employees increased by 10.5 percent to prepare for the 2015 service

increases in June and September. The total revenue hours increased by 5.2 percent, a lesser

rate than the rate of increase in employees. As a result, revenue hours per employee declined

by 4.8 percent in 2015 as compared to 2014.

Letter of Transmittal (cont.)

11

Economic Condition and Future Outlook

Local Economy—Snohomish County

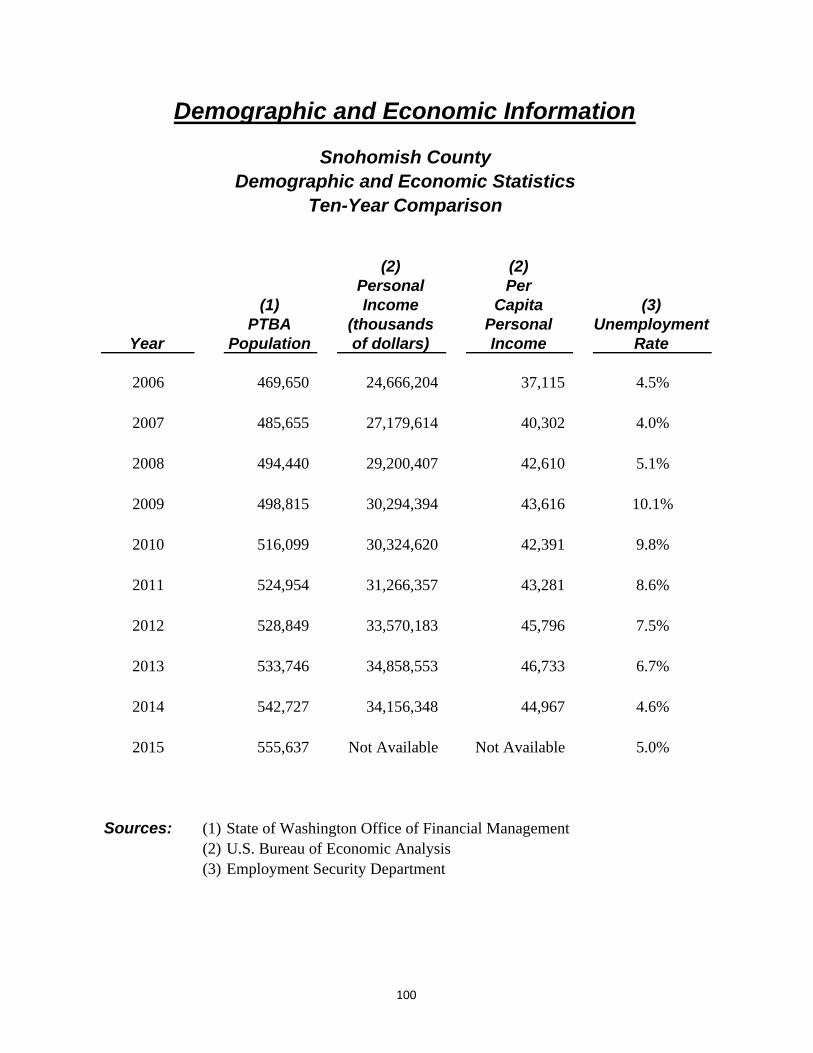

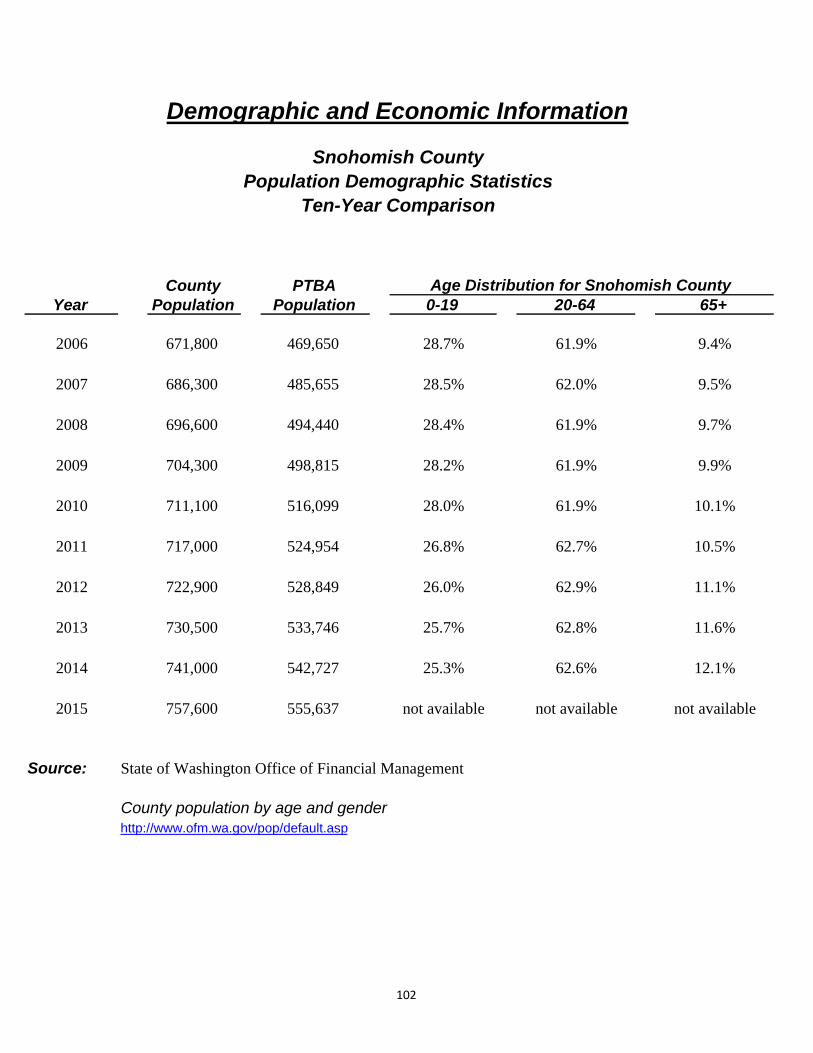

Snohomish County is the third most populous county in the state, with an estimated

population of 757,600 in 2015. Over the past ten years, the county’s population has grown an

average of 1.5 percent per year.

Snohomish County is home to over 20,000 businesses, ranging from small family farms

specializing in organic foods, to the world’s largest advanced manufacturing facility producing

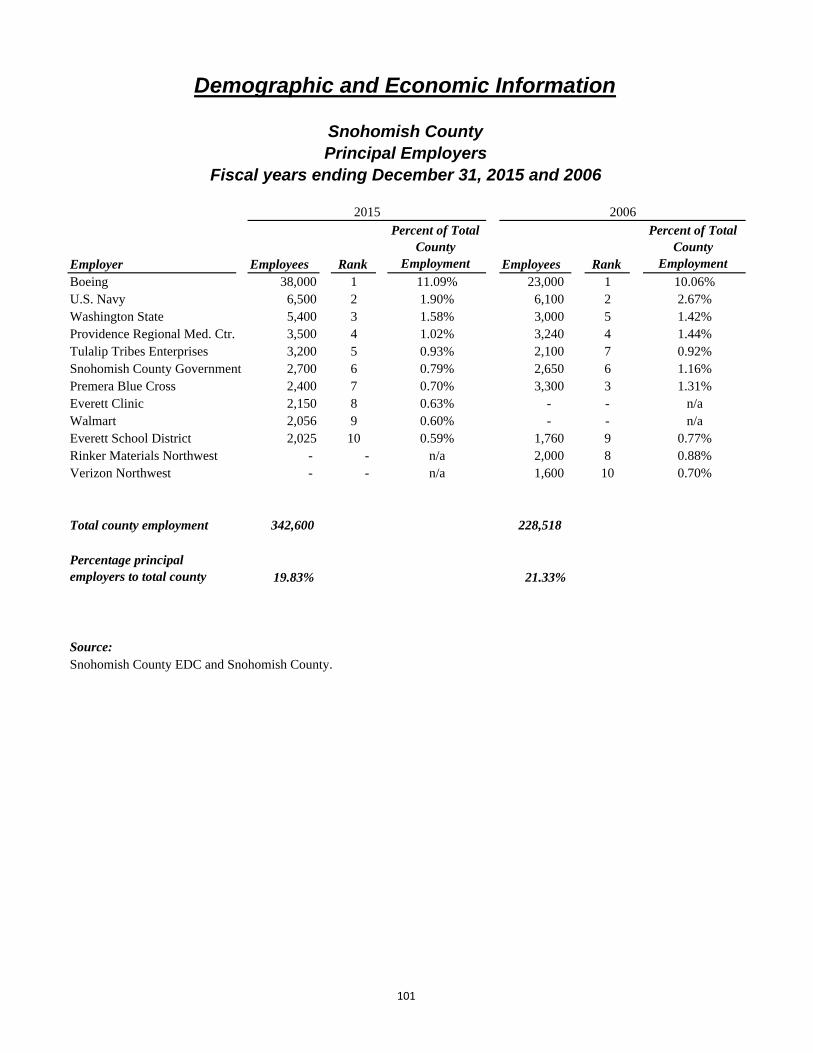

state‐of art aerospace equipment. The fifty largest employers account for over 100,000 jobs,

or about 35 percent of the county’s total employment. 1

The Boeing Company remains the county’s largest employer with about 38,000 jobs. The

United States Navy Everett homeport, the state of Washington, Providence Regional Medical

Center, and the Tulalip Tribes Enterprises round out the top five county employers and total

more than 18,000 jobs. A cluster of technology‐related businesses extending from the City of

Bothell to the City of Everett has given the county a technology corridor.

Community Transit’s primary operating revenue source is retail sales tax which is driven by

personal income, consumer confidence, and local business purchases. Local retail sales tax

growth has allowed Community Transit to increase revenue hours by 20,764, to 549,098

revenue hours for fiscal year 2015 as compared to 528,334 revenue hours for fiscal year 2014.

The Washington State Economic and Revenue Forecast Council maintains that motor vehicle

sales and parts are up 11 percent year over year in the latter part of 2015, and other retailers

such as drug and health stores, home furnishings, and building materials are also on the rise,

as are revenues from food services and the construction sector. However, revenues from the

manufacturing sector are down, as are transportation equipment (e.g., airplanes). Overall,

retail trade sector revenues are up 3.7 percent year over year.

The Management’s Discussion and Analysis section of this report contains information

concerning known economic factors that will affect the agency.

Economic Outlook—Regional and Statewide Factors

The Washington State Economic and Revenue Forecast Council measures changes in the

state’s economy. The council issued their final November 2015 Economic Forecast (dated

November 18, 2015) which reflects the primary economic indicators they measure. The

1 Data from Economic Alliance of Snohomish County.

Letter of Transmittal (cont.)

12

following table provides a summary of key statewide economic indicators from the council’s

November 2015 forecast.

Washington State Economic Indicators 2015 2016 2017 2018 2019 2020

Unemployment 5.5% 5.4% 5.2% 5.1% 5.1% 5.1%

Percent Change in Real Personal Income 3.9% 2.0% 1.6% 1.9% 1.9% 1.8%

Percent Change in Personal Income 5.5% 4.2% 4.6% 5.1% 5.0% 4.8%

Current projections by the Washington State Economic and Revenue Forecast Council point

toward relatively low unemployment rates in Washington State through the year 2020. The

Council also predicts a slight gradual decline in aerospace employment, due to increased

productivity by Boeing in its pursuit of lower costs, but the decline will be moderated by a

backlog of orders for Boeing’s planes.

According to the Washington State Economic and Revenue Forecast Council, statewide

underemployment decreased to 9.9 percent from 11.3 percent in 2015, approximately what

the underemployment rate was in the decade prior to the great recession. In December, the

council reported that Washington employment growth had begun to slow down in the last

few months of 2015. The service and construction sectors continued to add jobs, whereas

manufacturing—mainly aerospace—had declined by about 1,300 jobs.

As of December 31, 2015, the seasonally adjusted unemployment rate for the Seattle‐

Bellevue‐Everett area, as reported by the Washington State Unemployment Security

Department, rose to 5.0 percent from 4.5 percent at the beginning of the year. This rate

remained very low during the first three quarters of the year—4.4 to 4.5 percent—and began

to rise in September, continuing to creep up to 5.0 percent by December.

Changes in Transit Grant Funding

On December 4, 2015, President Obama signed the Fixing America’s Surface Transportation

(FAST) Act into law. This act—the first federal law in over a decade to provide long‐term

funding certainty for surface transportation infrastructure planning and investment—

supports transit funding through fiscal year 2020. It reauthorizes Federal Transit

Administration (FTA) programs and includes changes to improve mobility, streamline capital

project construction and acquisition, and increase the safety of public transportation systems

across the country.

The FAST Act re‐established a competitive Bus Discretionary Program that funds

replacements for aging fleets or facilities and adds a new eligibility to deploy low‐ or no‐

emission vehicles. In fiscal year 2016, $268 million in funding will be available for competitive

grants under this program. Through the FAST Act, funding programs such as FTA Urbanized

Area 5307 and FTA State of Good Repair 5337 will continue to provide crucial formula funds

for Community Transit.

Letter of Transmittal (cont.)

13

The FTA’s Bus and Bus Facilities Grants Program 5339 received an increase in funding of

$268 million over fiscal year 2015 levels, for a total of $696 million for fiscal year 2016. This

competitive program helps transit agencies fund new buses, replace aging fleets and facilities,

and fund bus system improvements not otherwise achievable through formula allocations.

Community Transit will compete for federal grants available through this program.

The FAST Act’s five years of predictable formula funding enables transit agencies to better

manage long‐term assets and address the backlog of state of good repair needs. To learn

more about the FAST act, visit this website: https://www.transit.dot.gov/grants/13070.html

2016 to 2021 Transit Development Plan

Community Transit is required by the Washington State Department of Transportation to

submit an updated six‐year Transit Development Plan (TDP) each year. This plan provides a

refreshed six‐year forecast of agency financials, service levels, and capital projects. It

represents an important forum for communicating strategic goals and helps set the stage for

many agency work programs. The Board of Directors adopted the TDP upon which the 2015

budget was based on May 1, 2014. The 2016 TDP was adopted May 5, 2016, and is available

at http://www.commtrans.org/Programs/Documents/ADOPTED%202016‐

2021%20TDP%2005‐05‐2016.pdf.

As discussed in the 2016 TDP’s Financial Plan, growth in Community Transit’s retail sales tax

revenue in 2015 remained strong (5.6 percent), though not quite at 2014’s growth rate of

7.1 percent. The forecast for 2016 to 2021 anticipates continued positive, but moderated

growth. The forecast shows the rate tapering from 5 percent in 2016 to 4 percent in 2017 and

beyond. This moderated forecast recognizes the potential for an economic recession during

the next six years and reflects the long‐term, 20‐plus year growth trend from retail sales tax in

the agency’s taxing district.

Voters in the PTBA approved Proposition 1 in November 2015, increasing the retail sales tax

rate for Community Transit by three‐tenths of 1 percent (3 cents for every $10 spent) to a

total of 1.2 percent (12 cents for every $10 spent). This increase is forecast to add $17 million

to baseline revenues in 2016 and $29 million by 2017. The increase is effective April 1, 2016,

with distribution of the new funds beginning in June 2016.

The increased funding provided by Proposition 1 will enable a 40 percent service expansion,

as described in the updated TDP. Service expansion will include improvements to existing

routes, more Swift service, including Swift II between Boeing/Paine Field in Everett and

Canyon Park in Bothell, and new routes providing new connections.

Letter of Transmittal (cont.)

14

Major Initiatives Planned

The Puget Sound region is growing with more residents and businesses relocating here.

Growth in our greater urban area means more cars on the road and longer commutes. Our

commuter buses are full and riders are asking for more service. Five years after inception, our

Swift I line on Highway 99 has become our most productive service, with 17 percent of our

riders using it daily. We are implementing technology to make it easier for our riders to use

our services and to ensure that our buses are on schedule. These initiatives are planned to

meet rider demand and expectations. Major initiatives include:

Increasing service by about 37,000 hours in 2016 and 27,000 hours in 2017.

Expanding the number of vehicles available and replace older vehicles for fixed‐route and commuter services as well as for our vanpool fleet. Putting planned vehicle replacements into service for our paratransit service.

Designing the Seaway Transit Center which is planned for the northern terminal of the second Swift line in Everett. Seaway Transit Center will provide an easy transfer point for riders going to Boeing, Fluke, Honeywell, and other Paine Field‐area businesses. In 2015, Community Transit received a regional mobility grant of $6.8 million for construction of the transit center.

Continuing project development for a second Swift line that will run east/west from near the Boeing manufacturing center in Everett to Canyon Park in Bothell and will intersect with the north/south Swift I service on Highway 99.

Replacing the current radio system with a state‐of‐the art wireless communications platform which will provide reliable voice communications while also providing reliable high‐capacity data communications.

Working with our regional partners, begin the process to replace the regional fare coordination system (ORCA fare card) which is nearing the end of its useful life and must be replaced by 2020.

Awards and Acknowledgements

The Government Finance Officers Association (GFOA) of the United States and Canada

awarded a Certificate of Achievement for Excellence in Financial Reporting to Community

Transit for its Comprehensive Annual Financial Report for the fiscal year ended

December 31, 2014. This was the 26th consecutive year that Community Transit has achieved

this prestigious award. To be awarded a Certificate of Achievement, a government must

publish an easily readable and efficiently organized comprehensive annual financial report.

This report must satisfy both generally accepted accounting principles and applicable legal

requirements.

16

17

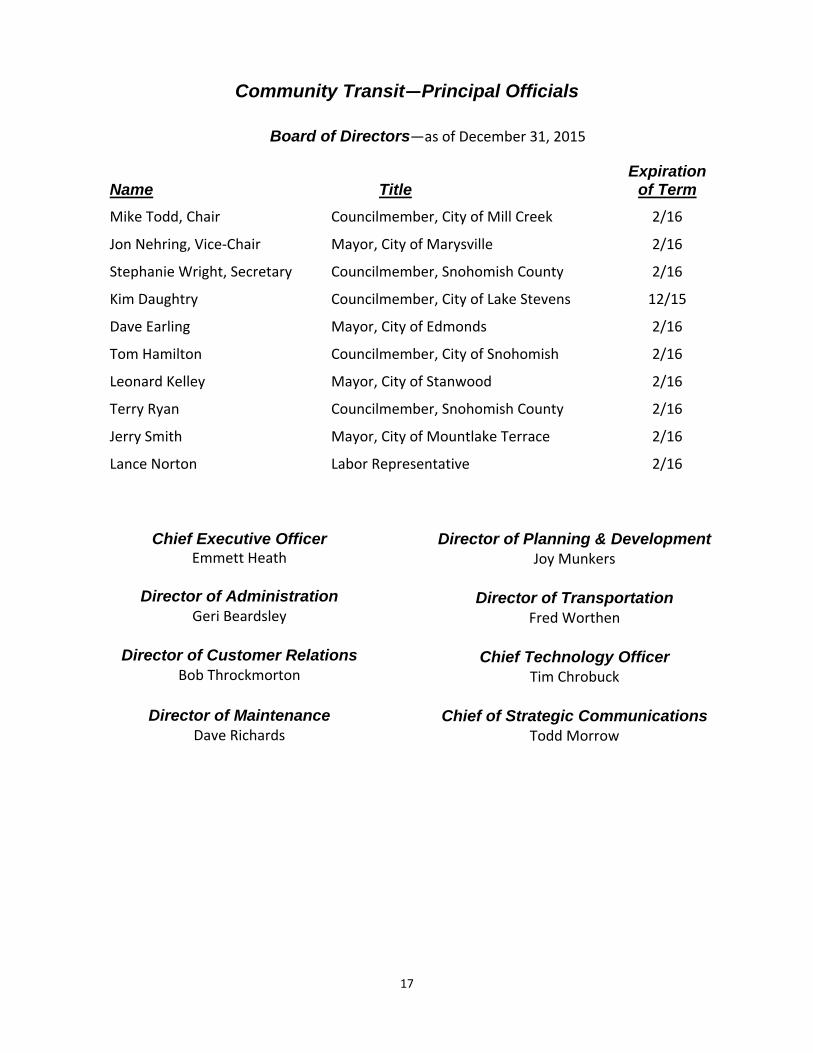

Community Transit—Principal Officials

Board of Directors—as of December 31, 2015

Name Title Expiration

of Term

Mike Todd, Chair Councilmember, City of Mill Creek 2/16

Jon Nehring, Vice‐Chair Mayor, City of Marysville 2/16

Stephanie Wright, Secretary Councilmember, Snohomish County 2/16

Kim Daughtry Councilmember, City of Lake Stevens 12/15

Dave Earling Mayor, City of Edmonds 2/16

Tom Hamilton Councilmember, City of Snohomish 2/16

Leonard Kelley Mayor, City of Stanwood 2/16

Terry Ryan Councilmember, Snohomish County 2/16

Jerry Smith Mayor, City of Mountlake Terrace 2/16

Lance Norton Labor Representative 2/16

Chief Executive Officer

Emmett Heath

Director of Administration Geri Beardsley

Director of Customer Relations

Bob Throckmorton

Director of Maintenance Dave Richards

Director of Planning & Development Joy Munkers

Director of Transportation

Fred Worthen

Chief Technology Officer

Tim Chrobuck

Chief of Strategic Communications

Todd Morrow

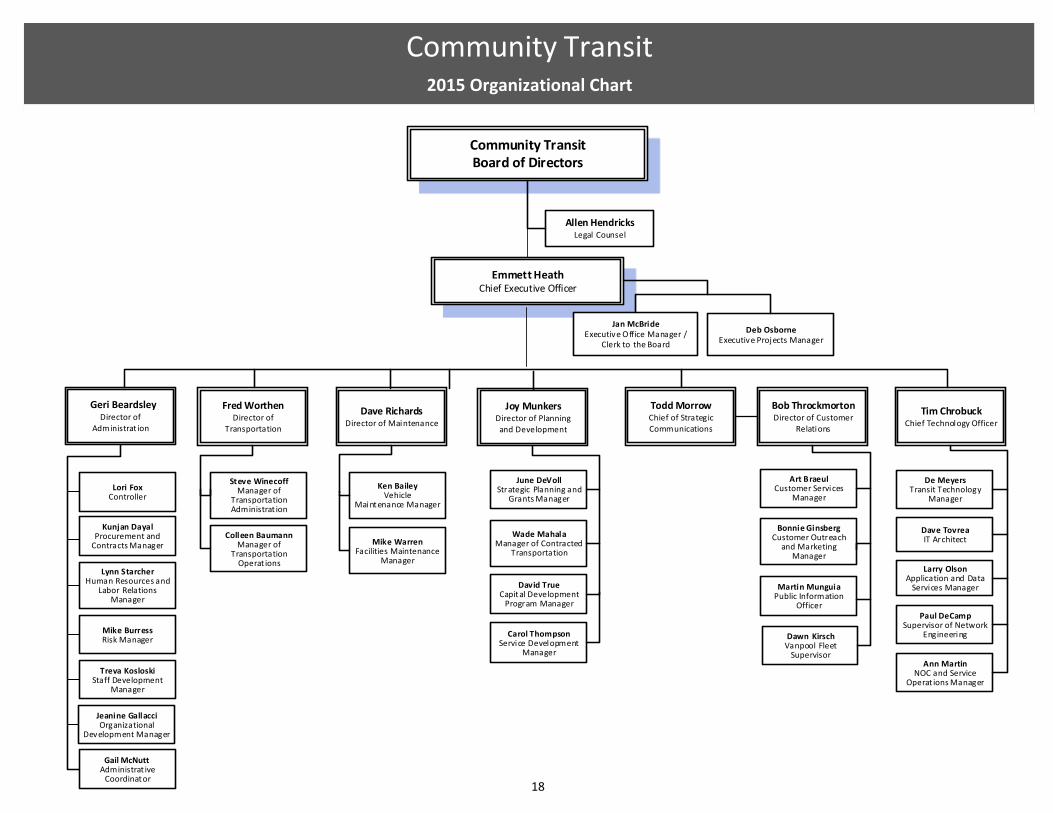

Community Transit2015 Organizational Chart

Emmett HeathChief Executive Officer

Joy MunkersDirector of Planning and Development

Fred WorthenDirector of

Transportation

Tim ChrobuckChief Technology Officer

Dave RichardsDirector of Maintenance

Jan McBrideExecutive O ffice Manager /

Clerk to the Board

Community TransitBoard of Directors

Ken BaileyVehicle

Maintenance Manager

Mike WarrenFacilities Maintenance

Manager

Martin MunguiaPublic Information

Officer

Bonnie GinsbergCustomer Outreach

and Marketing Manager

Dave TovreaIT Architect

De MeyersTransit Technology

Manager

Allen HendricksLegal Counsel

Bob ThrockmortonDirector of Customer

Relations

Deb OsborneExecutive Projects Manager

Larry OlsonApplication and Data

Services Manager

Paul DeCampSupervisor of Network

Engineering

Ann MartinNOC and Service

Operat ions Manager

Todd MorrowChief of Strategic Communications

June DeVollStrategic Planning and

Grants Manager

David TrueCapital Development

Program Manager

Carol ThompsonService Development

Manager

Wade MahalaManager of Contracted

Transportation

Colleen BaumannManager of

Transportation Operat ions

Steve WinecoffManager of

Transportation Administrat ion

Art BraeulCustomer Services

Manager

Dawn KirschVanpool Fleet

Supervisor

Lori FoxController

Lynn StarcherHuman Resources and

Labor Relations Manager

Mike BurressRisk Manager

Treva KosloskiStaff Development

Manager

Geri BeardsleyDirector of

Administrat ion

Gail McNuttAdministrat ive

Coordinator

Kunjan DayalProcurement and

Contracts Manager

Jeanine GallacciOrganizational

Development Manager

18

Fina

ncia

l Sec

tion

Choice Connections also offers innovative commute programs through Community Transit for large and small businesses in Snohomish County and Bothell.

Erin K.AT&T

Walk/Vanpool/Bike/TelecommuteChoice Connections 2015 Smart Commuter of the 3rd Quarter

This page left blank intentionally.

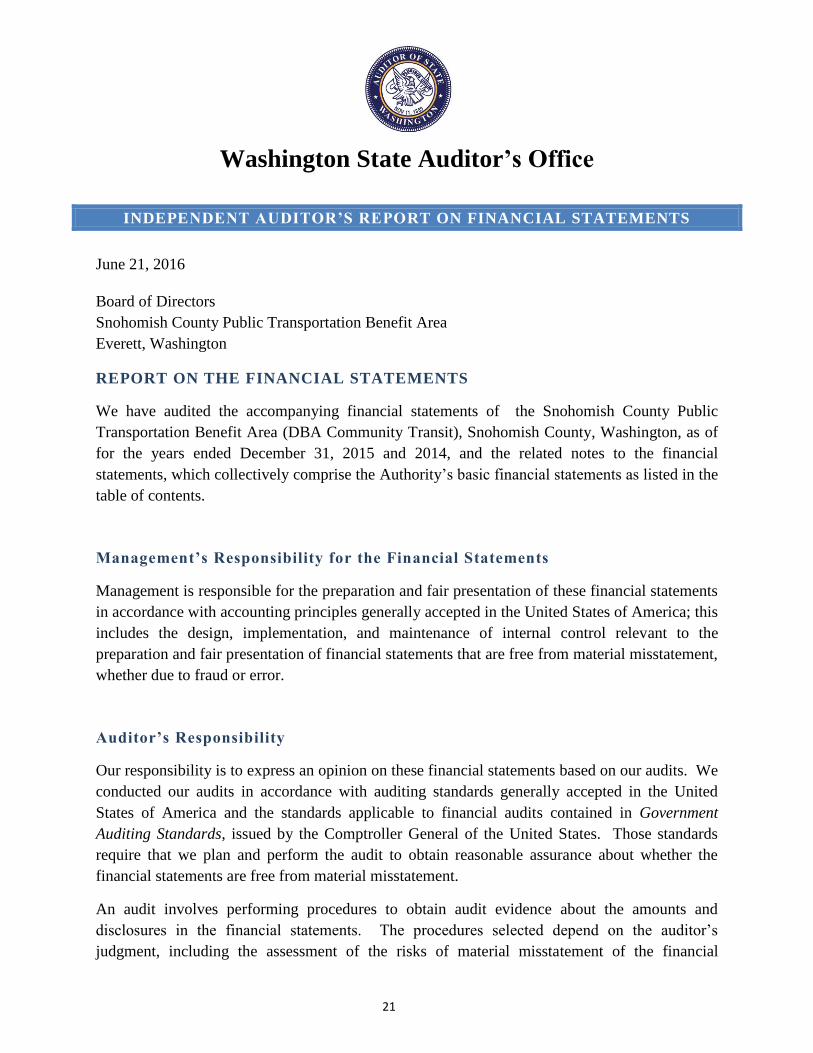

INDEPENDENT AUDITOR’S REPORT ON FINANCIAL STATEMENTS

June 21, 2016

Board of Directors

Snohomish County Public Transportation Benefit Area

Everett, Washington

REPORT ON THE FINANCIAL STATEMENTS

We have audited the accompanying financial statements of the Snohomish County Public

Transportation Benefit Area (DBA Community Transit), Snohomish County, Washington, as of

for the years ended December 31, 2015 and 2014, and the related notes to the financial

statements, which collectively comprise the Authority’s basic financial statements as listed in the

table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements

in accordance with accounting principles generally accepted in the United States of America; this

includes the design, implementation, and maintenance of internal control relevant to the

preparation and fair presentation of financial statements that are free from material misstatement,

whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We

conducted our audits in accordance with auditing standards generally accepted in the United

States of America and the standards applicable to financial audits contained in Government

Auditing Standards, issued by the Comptroller General of the United States. Those standards

require that we plan and perform the audit to obtain reasonable assurance about whether the

financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditor’s

judgment, including the assessment of the risks of material misstatement of the financial

Washington State Auditor’s Office

21

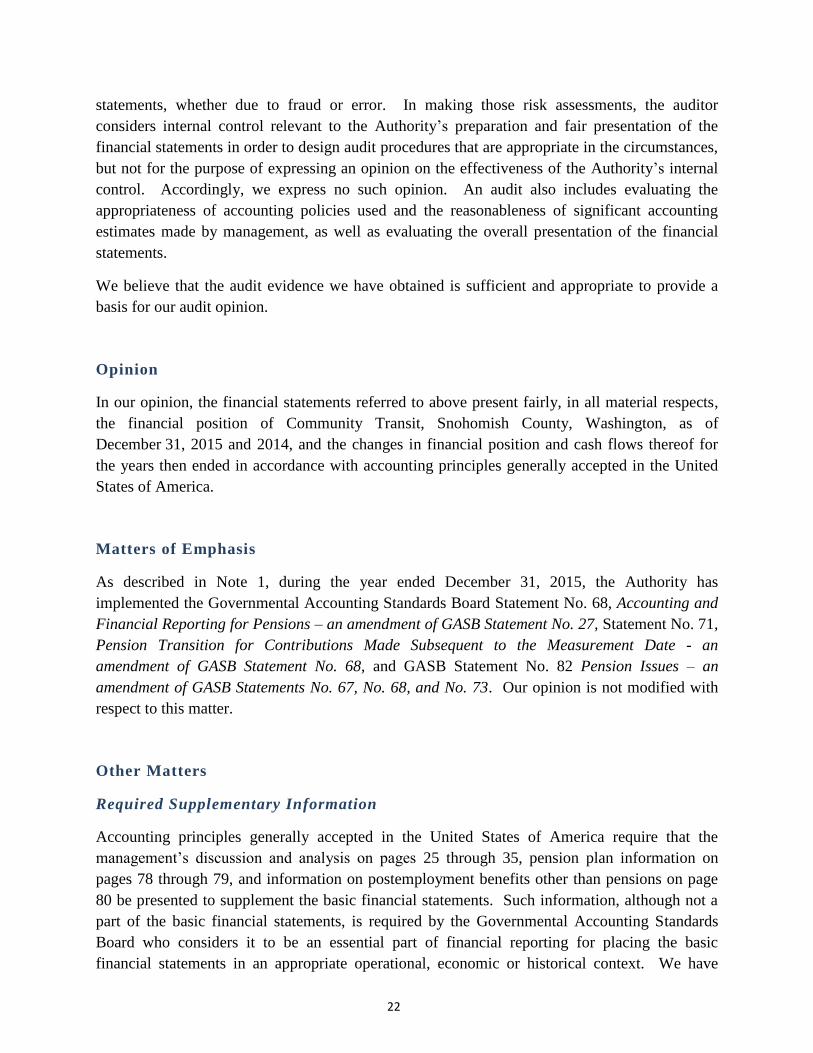

statements, whether due to fraud or error. In making those risk assessments, the auditor

considers internal control relevant to the Authority’s preparation and fair presentation of the

financial statements in order to design audit procedures that are appropriate in the circumstances,

but not for the purpose of expressing an opinion on the effectiveness of the Authority’s internal

control. Accordingly, we express no such opinion. An audit also includes evaluating the

appropriateness of accounting policies used and the reasonableness of significant accounting

estimates made by management, as well as evaluating the overall presentation of the financial

statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a

basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects,

the financial position of Community Transit, Snohomish County, Washington, as of

December 31, 2015 and 2014, and the changes in financial position and cash flows thereof for

the years then ended in accordance with accounting principles generally accepted in the United

States of America.

Matters of Emphasis

As described in Note 1, during the year ended December 31, 2015, the Authority has

implemented the Governmental Accounting Standards Board Statement No. 68, Accounting and

Financial Reporting for Pensions – an amendment of GASB Statement No. 27, Statement No. 71,

Pension Transition for Contributions Made Subsequent to the Measurement Date - an

amendment of GASB Statement No. 68, and GASB Statement No. 82 Pension Issues – an

amendment of GASB Statements No. 67, No. 68, and No. 73. Our opinion is not modified with

respect to this matter.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the

management’s discussion and analysis on pages 25 through 35, pension plan information on

pages 78 through 79, and information on postemployment benefits other than pensions on page

80 be presented to supplement the basic financial statements. Such information, although not a

part of the basic financial statements, is required by the Governmental Accounting Standards

Board who considers it to be an essential part of financial reporting for placing the basic

financial statements in an appropriate operational, economic or historical context. We have

22

applied certain limited procedures to the required supplementary information in accordance with

auditing standards generally accepted in the United States of America, which consisted of

inquiries of management about the methods of preparing the information and comparing the

information for consistency with management’s responses to our inquiries, the basic financial

statements, and other knowledge we obtained during our audit of the basic financial statements.

We do not express an opinion or provide any assurance on the information because the limited

procedures do not provide us with sufficient evidence to express an opinion or provide any

assurance.

Supplementary and Other Information

Our audits were conducted for the purpose of forming an opinion on the financial statements that

collectively comprise the Authority’s basic financial statements. The information identified in

the table of contents as the Introductory and Statistical Sections is presented for purposes of

additional analysis and is not a required part of the basic financial statements of the Authority.

Such information has not been subjected to the auditing procedures applied in the audit of the

basic financial statements and, accordingly, we do not express an opinion or provide any

assurance on it.

OTHER REPORTING REQUIRED BY GOVERNMENT AUDITING

STANDARDS

In accordance with Government Auditing Standards, we will also issue our report dated

June 21, 2016, on our consideration of the Authority’s internal control over financial reporting

and on our tests of its compliance with certain provisions of laws, regulations, contracts and

grant agreements and other matters. That report will be issued under separate cover in the

Authority’s Single Audit Report. The purpose of that report is to describe the scope of our

testing of internal control over financial reporting and compliance and the results of that testing,

and not to provide an opinion on internal control over financial reporting or on compliance. That

report is an integral part of an audit performed in accordance with Government Auditing

Standards in considering the Authority’s internal control over financial reporting and

compliance.

Sincerely,

TROY KELLEY

STATE AUDITOR

OLYMPIA, WA

23

24

This page left blank intentionally.

25

Management’s Discussion and Analysis

This section of Community Transit’s Comprehensive Annual Financial Report (CAFR) represents

management’s overview and analysis of Community Transit’s financial performance for the

fiscal year ended December 31, 2015. This section should be read in conjunction with the

financial statements that follow.

Introduction

Community Transit is a public transportation benefit area corporation providing public

transportation services to the Snohomish County community. Services include:

Local and intercounty bus services.

Paratransit services for the elderly and disabled.

A vanpool program and Ridematch services.

Regional express bus services funded through Sound Transit.

Financial Summary

As of December 31, 2015, Community Transit’s assets exceeded its liabilities by

$289.9 million. Of this amount, $108.7 million is available to meet our primary goal

of providing service to the public and to be invested in future capital improvements

as discussed in Community Transit’s six‐year plan.

Community Transit’s total net position increased by $31.4 million.

Capital grants and contributions amounted to $26.6 million.

Community Transit’s primary source of funding is from local sales taxes. In 2015,

sales tax revenue increased by $4.9 million.

Overview of the Financial Statements

This discussion and analysis section serves as an introduction to Community Transit’s basic

financial statements. Community Transit is a stand‐alone enterprise fund, and our financial

statements report information using the accrual basis of accounting, a method similar to those

used by private‐sector businesses. Under this method, revenues are recorded when earned,

and expenses are recorded as soon as they result in liabilities for benefits received.

The Comparative Statements of Net Position present information about all of Community

Transit’s assets and liabilities. The difference between assets and liabilities is reported as net

position. When net position is compared for several years, increases and decreases may serve

as useful indicators of whether Community Transit’s financial position is improving or

deteriorating.

Management’s Discussion and Analysis (Cont’d)

26

The Comparative Statements of Revenues, Expenses, and Changes in Net Position present

information showing how Community Transit’s net position changed during the fiscal year. All

changes in net position are reported as soon as the event occurs, regardless of the timing of

related cash flows.

The Comparative Statements of Cash Flows present information on Community Transit’s cash

receipts, cash payments, and changes in cash and cash equivalents during the fiscal year.

The basic financial statements can be found following this Management Discussion and

Analysis. The Notes to the Financial Statements provide additional information that is essential

to a full understanding of the data provided in the financial statements. Notes to the Financial

Statements can be found following the basic financial statements.

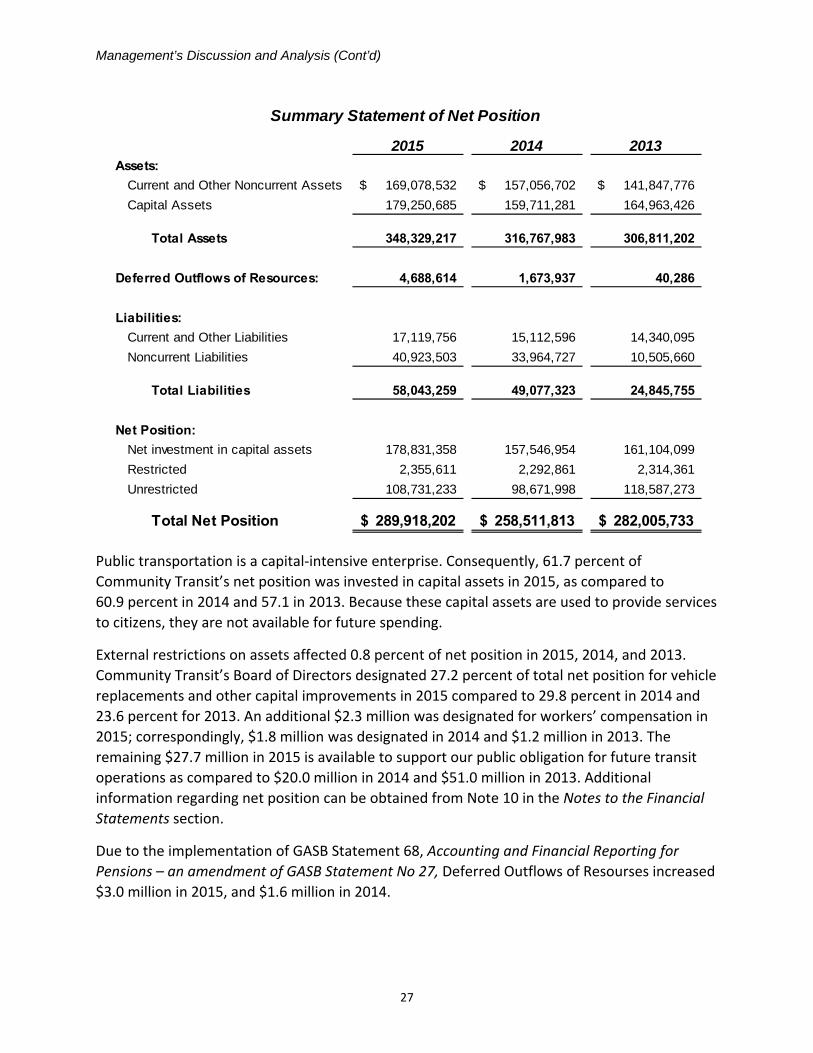

Community Transit’s Financial Position

Community Transit’s overall financial position improved in 2015. Net investment in capital

assets increased by $21.3 million, restricted net position increased by less than $0.1 million,

and unrestricted net position increased by $10.2 million. This resulted in an increase in total net

position of $31.4 million.

Current assets net of current liabilities amounted to $152.0 million for the year ended

December 31, 2015, as compared to $141.9 million for 2014 and $127.5 for 2013.

Sales tax revenues increased by 6.2 percent for 2015, as compared to a 6.4 percent increase for

2014 and a 10.8 percent increase for 2013.

Cash reserves available to meet current and future obligations increased to $123.7 million in

2015 from $131.4 million in 2014 and $114.2 million in 2013. Of these reserves, $2.4 million

was restricted for debt service and workers’ compensation claims. As of December 31, 2015,

Community Transit had no long‐term public financing debt.

Financial Analysis

For the year ended December 31, 2015, Community Transit’s assets exceeded liabilities by

$289.9 million. A summary of Community Transit’s net position follows.

Management’s Discussion and Analysis (Cont’d)

27

2015 2014 2013Assets:

Current and Other Noncurrent Assets 169,078,532$ 157,056,702$ 141,847,776$

Capital Assets 179,250,685 159,711,281 164,963,426

Total Assets 348,329,217 316,767,983 306,811,202

Deferred Outflows of Resources: 4,688,614 1,673,937 40,286

Liabilities:

Current and Other Liabilities 17,119,756 15,112,596 14,340,095

Noncurrent Liabilities 40,923,503 33,964,727 10,505,660

Total Liabilities 58,043,259 49,077,323 24,845,755

Net Position:

Net investment in capital assets 178,831,358 157,546,954 161,104,099

Restricted 2,355,611 2,292,861 2,314,361

Unrestricted 108,731,233 98,671,998 118,587,273

Total Net Position 289,918,202$ 258,511,813$ 282,005,733$

Summary Statement of Net Position

Public transportation is a capital‐intensive enterprise. Consequently, 61.7 percent of

Community Transit’s net position was invested in capital assets in 2015, as compared to

60.9 percent in 2014 and 57.1 in 2013. Because these capital assets are used to provide services

to citizens, they are not available for future spending.

External restrictions on assets affected 0.8 percent of net position in 2015, 2014, and 2013.

Community Transit’s Board of Directors designated 27.2 percent of total net position for vehicle

replacements and other capital improvements in 2015 compared to 29.8 percent in 2014 and

23.6 percent for 2013. An additional $2.3 million was designated for workers’ compensation in

2015; correspondingly, $1.8 million was designated in 2014 and $1.2 million in 2013. The

remaining $27.7 million in 2015 is available to support our public obligation for future transit

operations as compared to $20.0 million in 2014 and $51.0 million in 2013. Additional

information regarding net position can be obtained from Note 10 in the Notes to the Financial

Statements section.

Due to the implementation of GASB Statement 68, Accounting and Financial Reporting for

Pensions – an amendment of GASB Statement No 27, Deferred Outflows of Resourses increased

$3.0 million in 2015, and $1.6 million in 2014.

Management’s Discussion and Analysis (Cont’d)

28

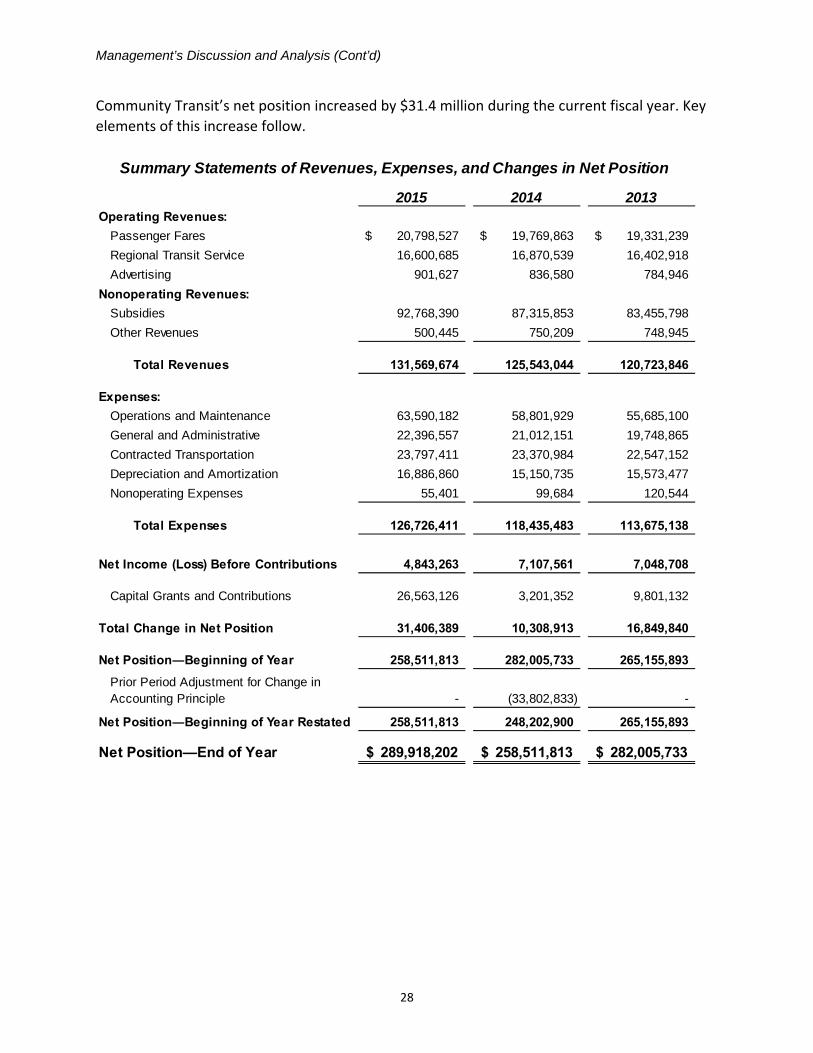

Community Transit’s net position increased by $31.4 million during the current fiscal year. Key

elements of this increase follow.

2015 2014 2013Operating Revenues:

Passenger Fares 20,798,527$ 19,769,863$ 19,331,239$

Regional Transit Service 16,600,685 16,870,539 16,402,918

Advertising 901,627 836,580 784,946

Nonoperating Revenues:

Subsidies 92,768,390 87,315,853 83,455,798

Other Revenues 500,445 750,209 748,945

Total Revenues 131,569,674 125,543,044 120,723,846

Expenses:

Operations and Maintenance 63,590,182 58,801,929 55,685,100

General and Administrative 22,396,557 21,012,151 19,748,865

Contracted Transportation 23,797,411 23,370,984 22,547,152

Depreciation and Amortization 16,886,860 15,150,735 15,573,477

Nonoperating Expenses 55,401 99,684 120,544

Total Expenses 126,726,411 118,435,483 113,675,138

Net Income (Loss) Before Contributions 4,843,263 7,107,561 7,048,708

Capital Grants and Contributions 26,563,126 3,201,352 9,801,132

Total Change in Net Position 31,406,389 10,308,913 16,849,840

Net Position―Beginning of Year 258,511,813 282,005,733 265,155,893

Prior Period Adjustment for Change in Accounting Principle - (33,802,833) -

Net Position―Beginning of Year Restated 258,511,813 248,202,900 265,155,893

Net Position—End of Year 289,918,202$ 258,511,813$ 282,005,733$

Summary Statements of Revenues, Expenses, and Changes in Net Position

Management’s Discussion and Analysis (Cont’d)

29

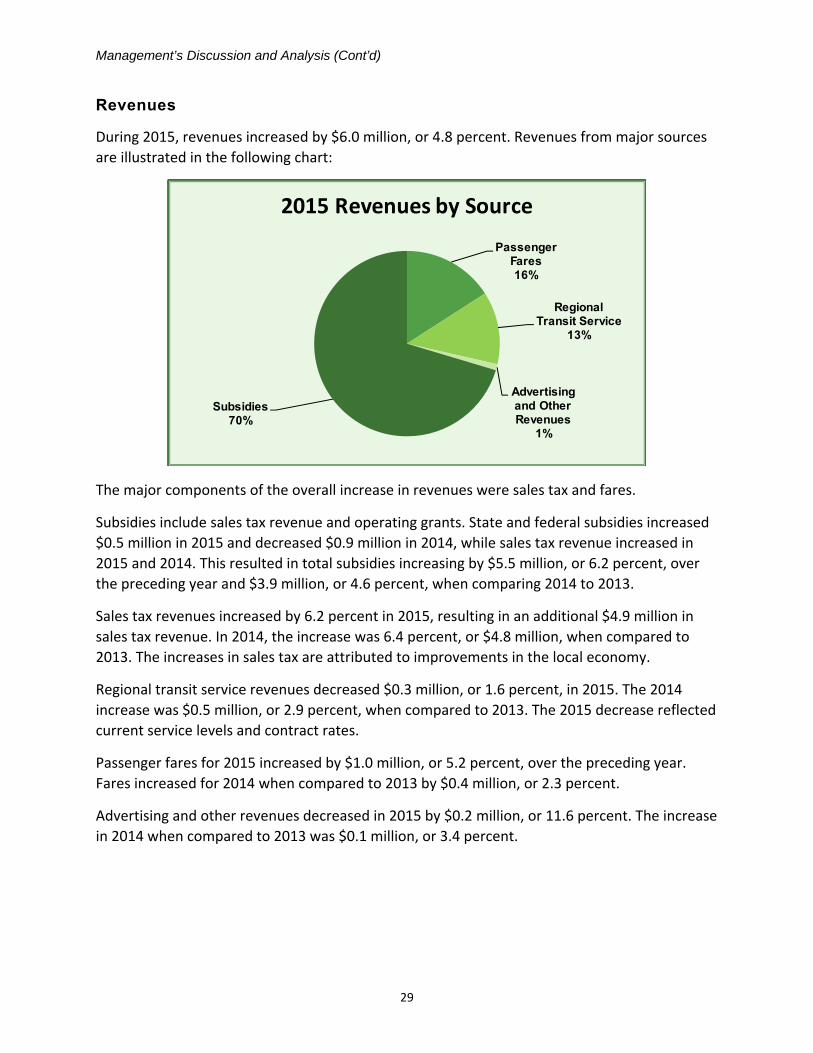

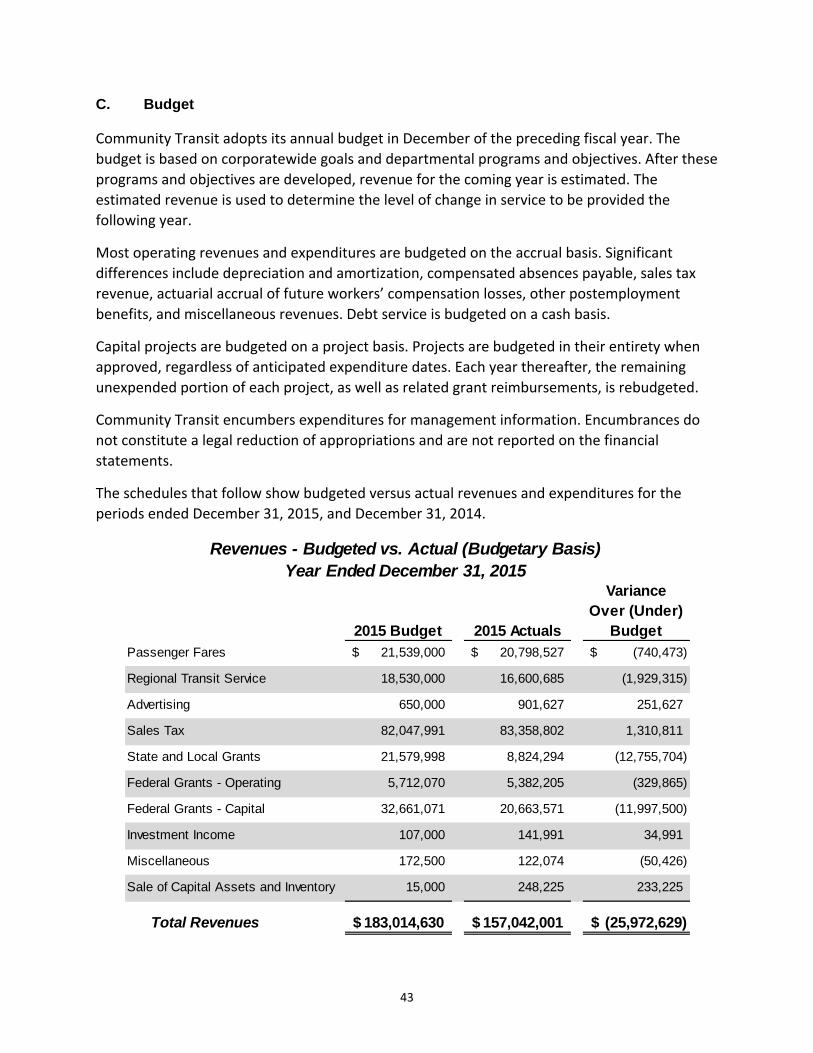

Revenues

During 2015, revenues increased by $6.0 million, or 4.8 percent. Revenues from major sources

are illustrated in the following chart:

Passenger Fares16%

Regional Transit Service

13%

Advertising and Other Revenues

1%

Subsidies70%

2015 Revenues by Source

The major components of the overall increase in revenues were sales tax and fares.

Subsidies include sales tax revenue and operating grants. State and federal subsidies increased

$0.5 million in 2015 and decreased $0.9 million in 2014, while sales tax revenue increased in

2015 and 2014. This resulted in total subsidies increasing by $5.5 million, or 6.2 percent, over

the preceding year and $3.9 million, or 4.6 percent, when comparing 2014 to 2013.

Sales tax revenues increased by 6.2 percent in 2015, resulting in an additional $4.9 million in

sales tax revenue. In 2014, the increase was 6.4 percent, or $4.8 million, when compared to

2013. The increases in sales tax are attributed to improvements in the local economy.

Regional transit service revenues decreased $0.3 million, or 1.6 percent, in 2015. The 2014

increase was $0.5 million, or 2.9 percent, when compared to 2013. The 2015 decrease reflected

current service levels and contract rates.

Passenger fares for 2015 increased by $1.0 million, or 5.2 percent, over the preceding year.

Fares increased for 2014 when compared to 2013 by $0.4 million, or 2.3 percent.

Advertising and other revenues decreased in 2015 by $0.2 million, or 11.6 percent. The increase

in 2014 when compared to 2013 was $0.1 million, or 3.4 percent.

Management’s Discussion and Analysis (Cont’d)

30

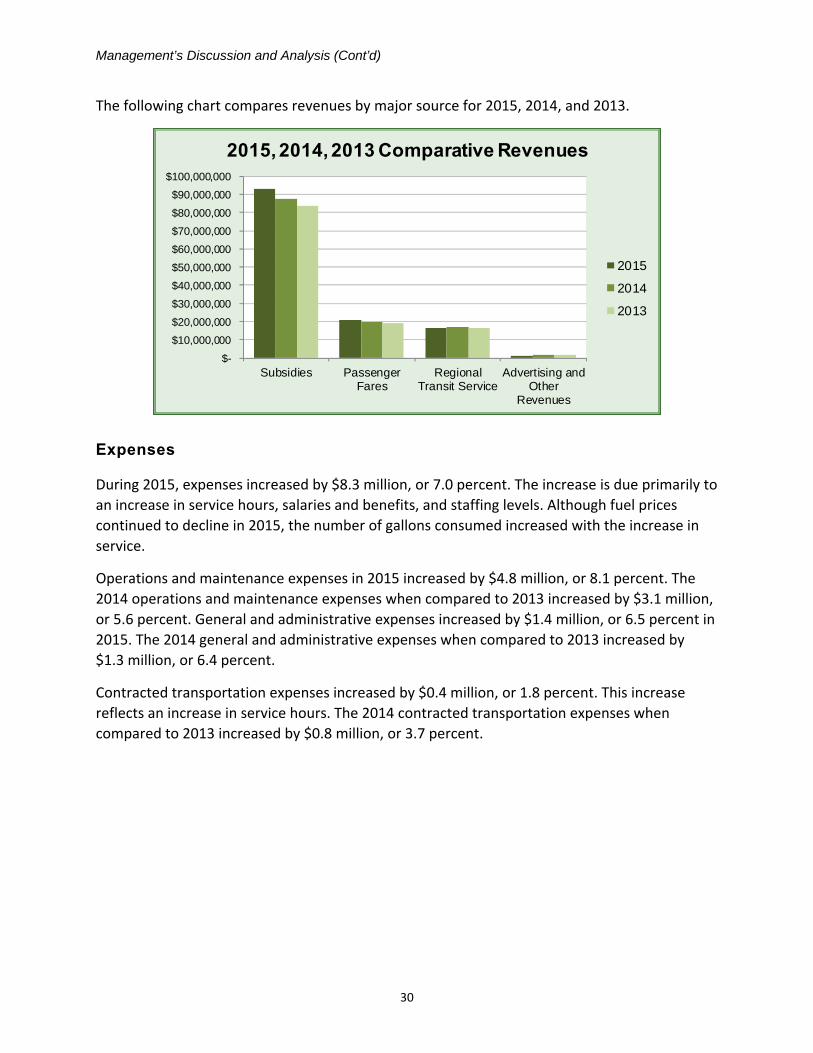

The following chart compares revenues by major source for 2015, 2014, and 2013.

Subsidies PassengerFares

RegionalTransit Service

Advertising andOther

Revenues

$-

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

$70,000,000

$80,000,000

$90,000,000

$100,000,000

2015, 2014, 2013 Comparative Revenues

2015

2014

2013

Expenses

During 2015, expenses increased by $8.3 million, or 7.0 percent. The increase is due primarily to

an increase in service hours, salaries and benefits, and staffing levels. Although fuel prices

continued to decline in 2015, the number of gallons consumed increased with the increase in

service.

Operations and maintenance expenses in 2015 increased by $4.8 million, or 8.1 percent. The

2014 operations and maintenance expenses when compared to 2013 increased by $3.1 million,

or 5.6 percent. General and administrative expenses increased by $1.4 million, or 6.5 percent in

2015. The 2014 general and administrative expenses when compared to 2013 increased by

$1.3 million, or 6.4 percent.

Contracted transportation expenses increased by $0.4 million, or 1.8 percent. This increase

reflects an increase in service hours. The 2014 contracted transportation expenses when

compared to 2013 increased by $0.8 million, or 3.7 percent.

Management’s Discussion and Analysis (Cont’d)

31

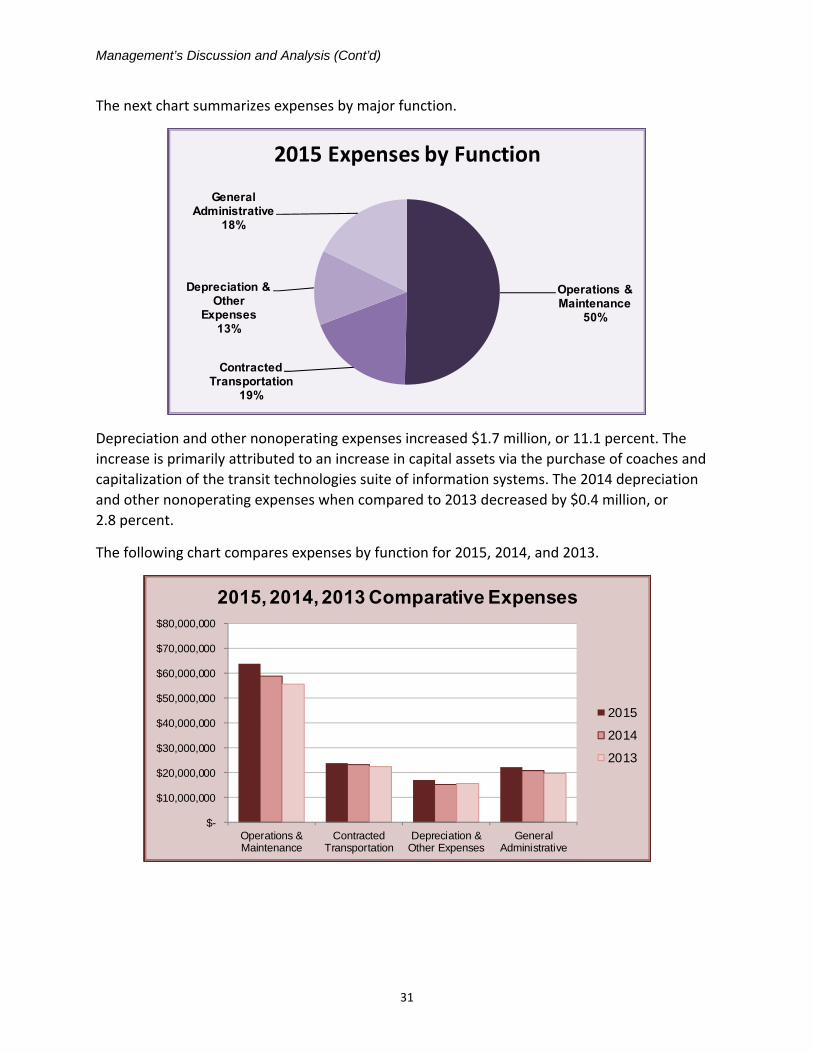

The next chart summarizes expenses by major function.

Operations & Maintenance

50%

Contracted Transportation

19%

Depreciation & Other

Expenses13%

General Administrative

18%

2015 Expenses by Function

Depreciation and other nonoperating expenses increased $1.7 million, or 11.1 percent. The

increase is primarily attributed to an increase in capital assets via the purchase of coaches and

capitalization of the transit technologies suite of information systems. The 2014 depreciation

and other nonoperating expenses when compared to 2013 decreased by $0.4 million, or

2.8 percent.

The following chart compares expenses by function for 2015, 2014, and 2013.

Operations &Maintenance

ContractedTransportation

Depreciation &Other Expenses

GeneralAdministrative

$-

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

$70,000,000

$80,000,000

2015, 2014, 2013 Comparative Expenses

2015

2014

2013

Management’s Discussion and Analysis (Cont’d)

32

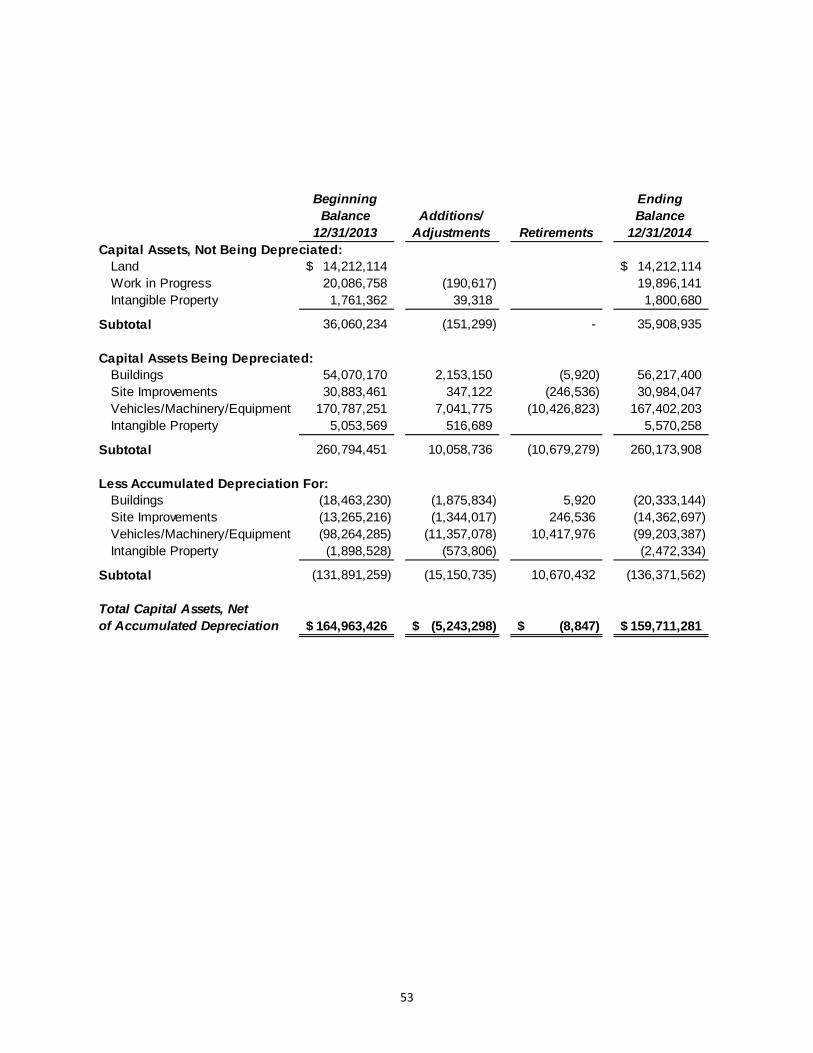

Capital Assets

Capital assets include revenue vehicles, support vehicles, land and buildings, equipment, and

passenger facilities.

As of December 31, 2015, Community Transit’s investment in capital assets amounted to

$179.3 million, net of accumulated depreciation. Capital assets increased by 12.2 percent

during 2015.

Major acquisitions during 2015 included:

16 Double Tall coaches in the amount of $14.4 million.

19 forty‐foot coaches in the amount of $9.2 million.

KPOB pavement replacement in the amount of $3.7 million.

For additional information on Community Transit’s capital assets, please see Note 5 in the

Notes to the Financial Statements section.

Debt Administration

In June 2010, Community Transit sold $5,240,000 in limited sales tax general obligation

refunding bonds. The bonds were sold on a competitive bid basis and carried a rate of

3 percent. Payment of the bonds will be made from a portion of Community Transit sales tax

revenue. The 2010 bond issue was rated Aa2 by Moody’s Investors Service and AA+ by S&P

Global Ratings (formerly Standard and Poor’s Ratings Services). The resulting funds were used

to refund the 2004 bond issue outstanding and to pay the cost of issuing the 2010 bonds. The

monies used to fund the bond reserve account continue to earn interest, while the funds

allocated to pay for the bond issuance costs are reflected in the Comparative Statements of Net

Position. For additional information on Community Transit’s bonds payable, please see Note

9(A) in the Notes to the Financial Statements section.

Under Washington State law, bonds secured by and payable from sales tax revenues are

general obligations of the issuer and are subject to this debt limitation: The bonds may not

exceed 0.375 percent of the value of taxable property within the agency’s boundaries. Larger

amounts may be approved with a public vote.

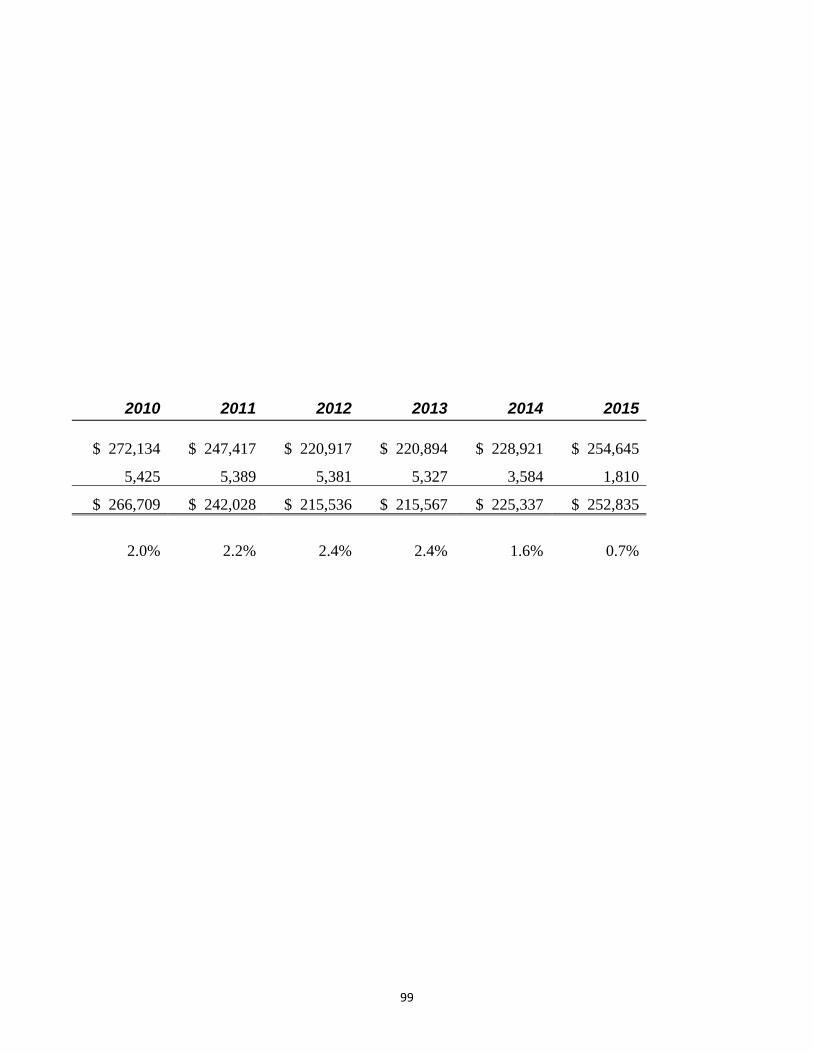

Assessed valuation in 2015 for collection of taxes in 2016 67,905,520,501$

Maximum nonvoted debt capacity at 0.375 percent of valuation 254,645,702

Less outstanding bond issues - net 1,810,857

Nonvoted debt capacity remaining 252,834,845$

Management’s Discussion and Analysis (Cont’d)

33

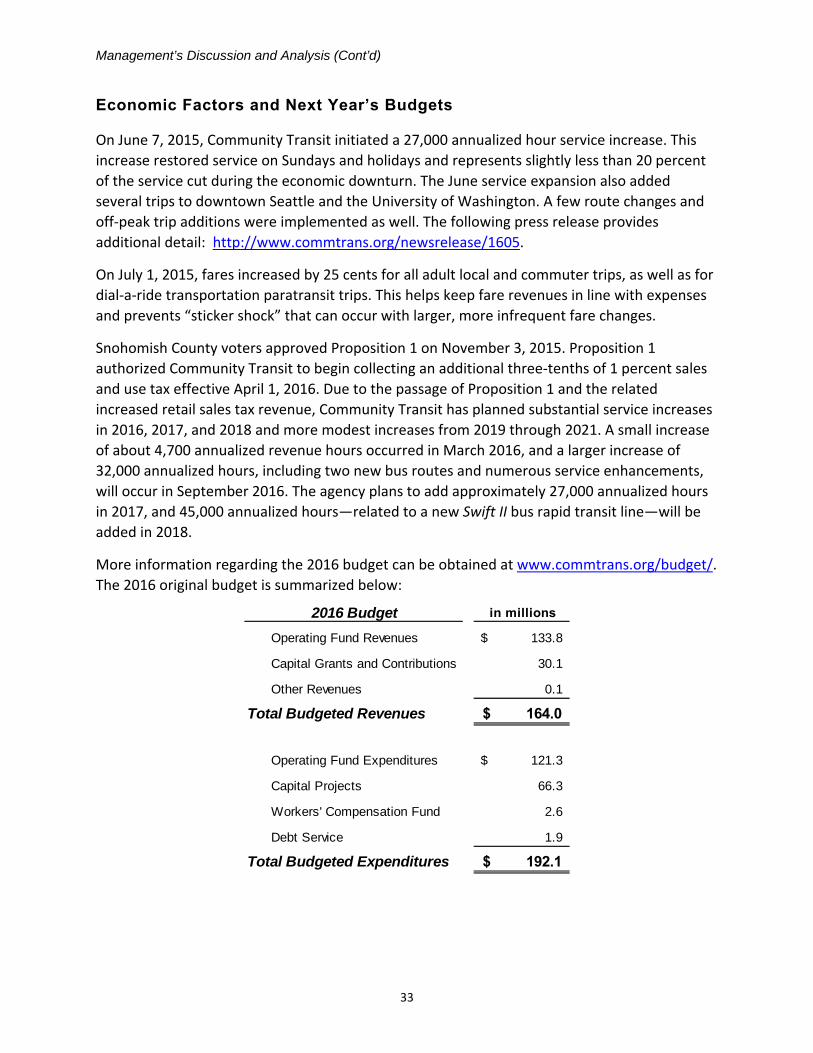

Economic Factors and Next Year’s Budgets

On June 7, 2015, Community Transit initiated a 27,000 annualized hour service increase. This

increase restored service on Sundays and holidays and represents slightly less than 20 percent

of the service cut during the economic downturn. The June service expansion also added

several trips to downtown Seattle and the University of Washington. A few route changes and

off‐peak trip additions were implemented as well. The following press release provides

additional detail: http://www.commtrans.org/newsrelease/1605.

On July 1, 2015, fares increased by 25 cents for all adult local and commuter trips, as well as for

dial‐a‐ride transportation paratransit trips. This helps keep fare revenues in line with expenses

and prevents “sticker shock” that can occur with larger, more infrequent fare changes.

Snohomish County voters approved Proposition 1 on November 3, 2015. Proposition 1

authorized Community Transit to begin collecting an additional three‐tenths of 1 percent sales

and use tax effective April 1, 2016. Due to the passage of Proposition 1 and the related

increased retail sales tax revenue, Community Transit has planned substantial service increases

in 2016, 2017, and 2018 and more modest increases from 2019 through 2021. A small increase

of about 4,700 annualized revenue hours occurred in March 2016, and a larger increase of

32,000 annualized hours, including two new bus routes and numerous service enhancements,

will occur in September 2016. The agency plans to add approximately 27,000 annualized hours

in 2017, and 45,000 annualized hours—related to a new Swift II bus rapid transit line—will be

added in 2018.

More information regarding the 2016 budget can be obtained at www.commtrans.org/budget/.

The 2016 original budget is summarized below:

2016 Budget in millions

Operating Fund Revenues 133.8$

Capital Grants and Contributions 30.1

Other Revenues 0.1

Total Budgeted Revenues 164.0$

Operating Fund Expenditures 121.3$

Capital Projects 66.3

Workers' Compensation Fund 2.6

Debt Service 1.9

Total Budgeted Expenditures 192.1$

Management’s Discussion and Analysis (Cont’d)

34

Requests for Information

This financial report is designed to provide a general overview of Community Transit’s finances

for anyone who has an interest. Questions concerning any of the information presented in this

report or requests for additional financial information should be addressed to:

Lori Fox, Controller Community Transit 7100 Hardeson Road Everett, WA 98203

35

Basic Financial Statements

Community TransitComparative Statements of Net Position

December 31, 2015 and 2014

Assets 2015 2014

Current Assets:Cash and Cash Equivalents 121,382,800$ 129,076,978$

Restricted Assets:

Cash and Cash Equivalents 2,355,611 2,292,861

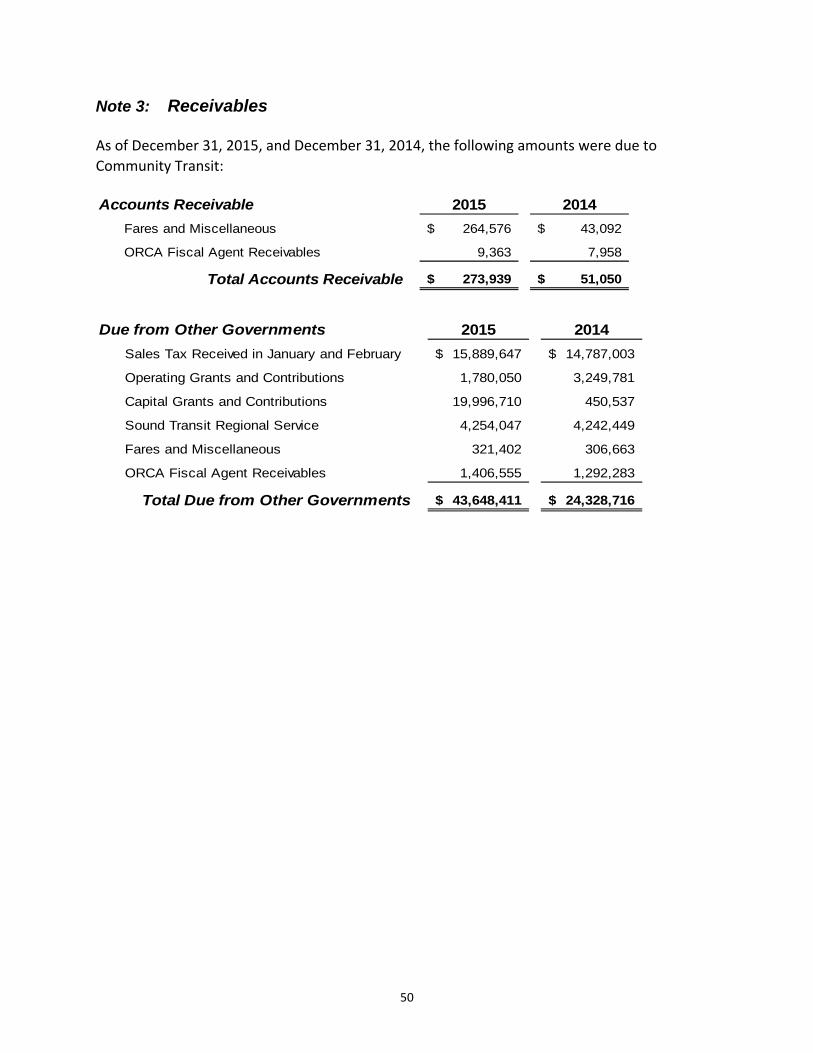

Accounts Receivable and Accrued Interest 273,939 51,050

Due from Other Governments 43,648,411 24,328,716

Maintenance Parts Inventory 1,298,479 1,239,442

Prepaid Expenses 119,292 67,655

Total Current Assets 169,078,532 157,056,702

Noncurrent Assets:Capital Assets Not Being Depreciated:

Land 14,330,617 14,212,114

Intangible Property 1,800,680 1,800,680

Work in Progress 18,517,020 19,896,141

Capital Assets (Net of Accumulated Depreciation):

Buildings 36,181,149 35,884,256

Site Improvements 19,024,186 16,621,349

Vehicles, Machinery, and Equipment 85,698,054 66,447,079

Intangible Property 3,698,979 4,849,662

Capital Assets (Net of Accumulated Depreciation) 179,250,685 159,711,281

Total Noncurrent Assets 179,250,685 159,711,281

Total Assets 348,329,217 316,767,983

Deferred Outflows of Resources

Pensions 4,688,614 1,673,937

Total Deferred Outflows of Resources 4,688,614 1,673,937

Total Assets and Deferred Outflows of Resources 353,017,831$ 318,441,920$

Continued on the following page.

See accompanying notes to the financial statements.

36

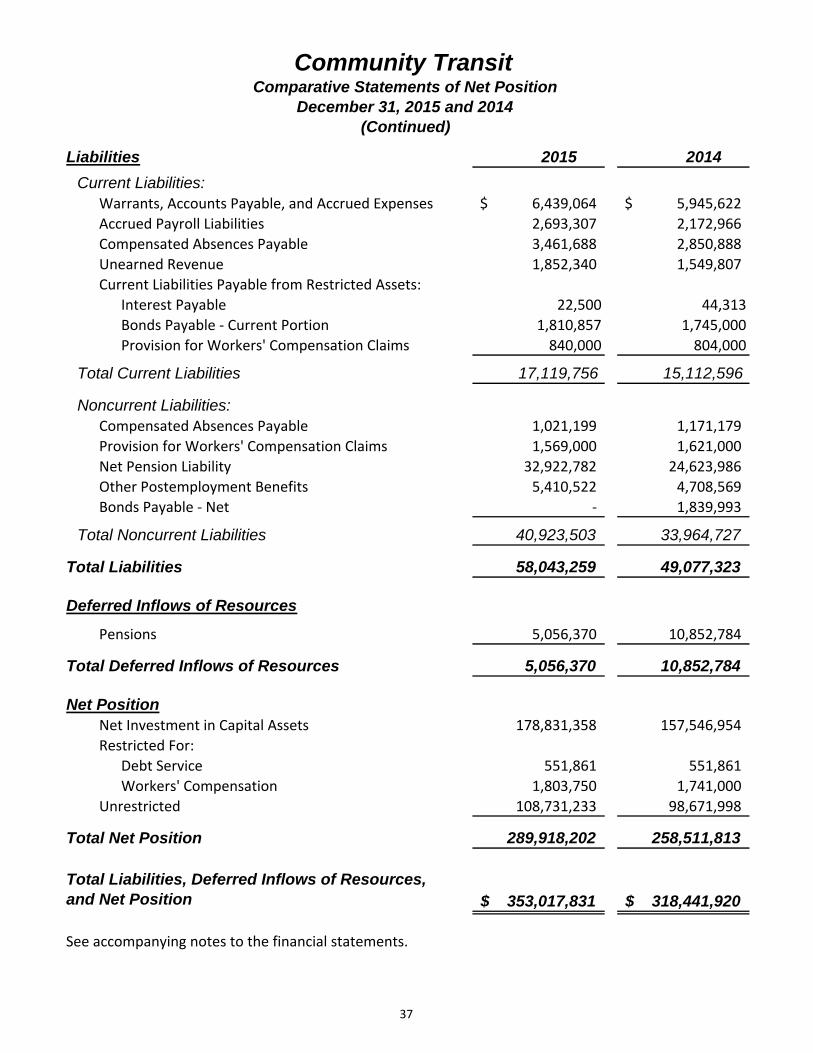

Community TransitComparative Statements of Net Position

December 31, 2015 and 2014(Continued)

Liabilities 2015 2014

Current Liabilities:Warrants, Accounts Payable, and Accrued Expenses 6,439,064$ 5,945,622$

Accrued Payroll Liabilities 2,693,307 2,172,966

Compensated Absences Payable 3,461,688 2,850,888

Unearned Revenue 1,852,340 1,549,807

Current Liabilities Payable from Restricted Assets:

Interest Payable 22,500 44,313

Bonds Payable ‐ Current Portion 1,810,857 1,745,000

Provision for Workers' Compensation Claims 840,000 804,000

Total Current Liabilities 17,119,756 15,112,596

Noncurrent Liabilities:Compensated Absences Payable 1,021,199 1,171,179

Provision for Workers' Compensation Claims 1,569,000 1,621,000

Net Pension Liability 32,922,782 24,623,986

Other Postemployment Benefits 5,410,522 4,708,569

Bonds Payable ‐ Net ‐ 1,839,993

Total Noncurrent Liabilities 40,923,503 33,964,727

Total Liabilities 58,043,259 49,077,323

Deferred Inflows of Resources

Pensions 5,056,370 10,852,784

Total Deferred Inflows of Resources 5,056,370 10,852,784

Net PositionNet Investment in Capital Assets 178,831,358 157,546,954

Restricted For:

Debt Service 551,861 551,861

Workers' Compensation 1,803,750 1,741,000

Unrestricted 108,731,233 98,671,998

Total Net Position 289,918,202 258,511,813

Total Liabilities, Deferred Inflows of Resources,and Net Position 353,017,831$ 318,441,920$

See accompanying notes to the financial statements.

37

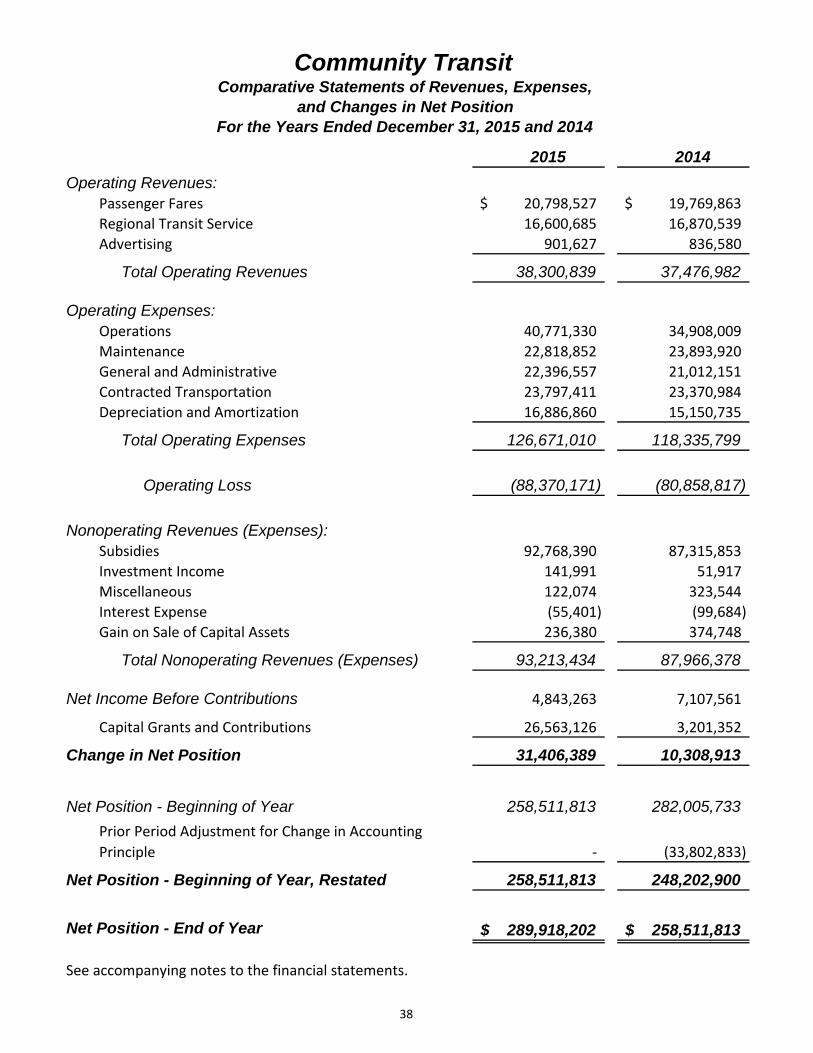

Community TransitComparative Statements of Revenues, Expenses,

and Changes in Net PositionFor the Years Ended December 31, 2015 and 2014

2015 2014

Operating Revenues:Passenger Fares 20,798,527$ 19,769,863$

Regional Transit Service 16,600,685 16,870,539

Advertising 901,627 836,580

Total Operating Revenues 38,300,839 37,476,982

Operating Expenses:Operations 40,771,330 34,908,009

Maintenance 22,818,852 23,893,920

General and Administrative 22,396,557 21,012,151

Contracted Transportation 23,797,411 23,370,984

Depreciation and Amortization 16,886,860 15,150,735

Total Operating Expenses 126,671,010 118,335,799

Operating Loss (88,370,171) (80,858,817)

Nonoperating Revenues (Expenses):Subsidies 92,768,390 87,315,853

Investment Income 141,991 51,917

Miscellaneous 122,074 323,544

Interest Expense (55,401) (99,684)

Gain on Sale of Capital Assets 236,380 374,748

Total Nonoperating Revenues (Expenses) 93,213,434 87,966,378

Net Income Before Contributions 4,843,263 7,107,561

Capital Grants and Contributions 26,563,126 3,201,352

Change in Net Position 31,406,389 10,308,913

Net Position - Beginning of Year 258,511,813 282,005,733

Prior Period Adjustment for Change in Accounting

Principle ‐ (33,802,833)

Net Position - Beginning of Year, Restated 258,511,813 248,202,900

Net Position - End of Year 289,918,202$ 258,511,813$

See accompanying notes to the financial statements.

38

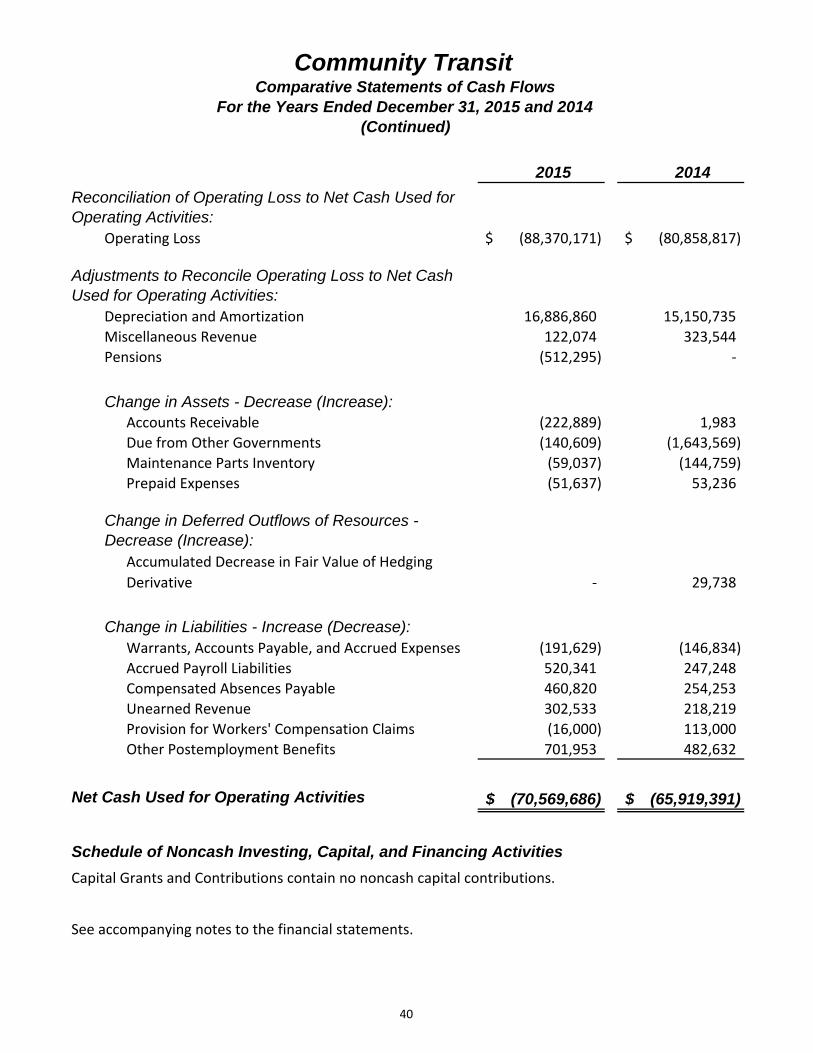

Community TransitComparative Statements of Cash Flows

For the Years Ended December 31, 2015 and 2014

2015 2014

Cash Flows from Operating Activities:Cash Received for Operating Revenues 38,278,296$ 36,031,739$

Cash Received for Miscellaneous Revenue 83,652 345,420

Cash Paid to Vendors for Goods and Services (48,304,719) (48,666,440)

Cash Paid for Employee Services and Benefits (60,626,915) (53,630,110)

Net Cash Used for Operating Activities (70,569,686) (65,919,391)

Cash Flows from Noncapital Financing Activities:Operating Subsidies 93,135,477 88,788,008

Net Cash Provided by Noncapital Financing Activities 93,135,477 88,788,008

Cash Flows from Capital and Related Financing Activities:Acquisition of Capital Assets (35,753,039) (9,705,309)

Capital Grants and Contributions 7,016,953 5,385,444

Principal Payment on Bonds (1,745,000) (1,695,000)

Interest Paid on Bonds (106,350) (157,200)

Proceeds From the Sale of Capital Assets 248,226 383,595

Net Cash Used for Capital and Related Financing Activities (30,339,210) (5,788,470)

Cash Flows from Investing Activities:Investment Income 141,991 51,917

Net Cash Provided by Investing Activities 141,991 51,917

Net Increase (Decrease) in Cash and Cash Equivalents (7,631,428) 17,132,064

Cash and Cash Equivalents - Beginning of Year 131,369,839 114,237,775

Cash and Cash Equivalents - End of Year 123,738,411$ 131,369,839$

Continued on the following page.

See accompanying notes to the financial statements.

39

Community TransitComparative Statements of Cash Flows

For the Years Ended December 31, 2015 and 2014(Continued)

2015 2014

Reconciliation of Operating Loss to Net Cash Used for Operating Activities:

Operating Loss (88,370,171)$ (80,858,817)$

Adjustments to Reconcile Operating Loss to Net Cash Used for Operating Activities:

Depreciation and Amortization 16,886,860 15,150,735

Miscellaneous Revenue 122,074 323,544

Pensions (512,295) ‐

Change in Assets - Decrease (Increase):Accounts Receivable (222,889) 1,983

Due from Other Governments (140,609) (1,643,569)

Maintenance Parts Inventory (59,037) (144,759)

Prepaid Expenses (51,637) 53,236

Change in Deferred Outflows of Resources - Decrease (Increase):

Accumulated Decrease in Fair Value of Hedging

Derivative ‐ 29,738

Change in Liabilities - Increase (Decrease):Warrants, Accounts Payable, and Accrued Expenses (191,629) (146,834)

Accrued Payroll Liabilities 520,341 247,248

Compensated Absences Payable 460,820 254,253

Unearned Revenue 302,533 218,219

Provision for Workers' Compensation Claims (16,000) 113,000

Other Postemployment Benefits 701,953 482,632

Net Cash Used for Operating Activities (70,569,686)$ (65,919,391)$

Schedule of Noncash Investing, Capital, and Financing Activities

Capital Grants and Contributions contain no noncash capital contributions.

See accompanying notes to the financial statements.

40

41

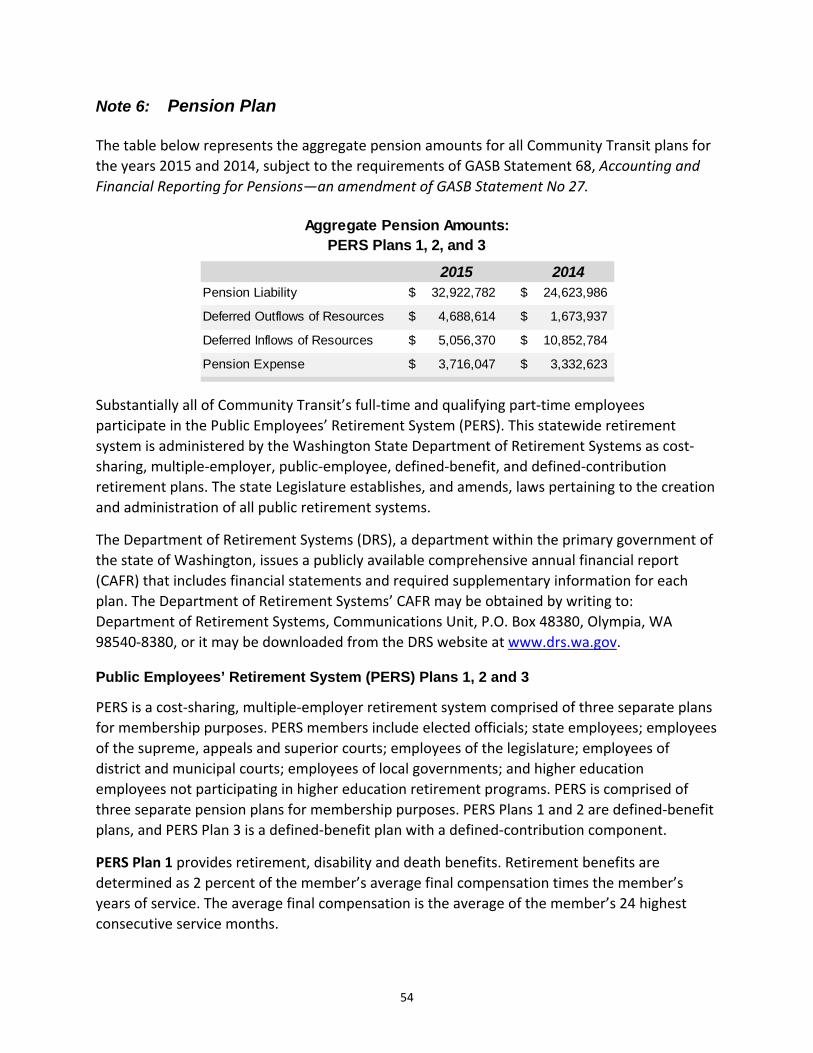

Community Transit Notes to the Financial Statements

December 31, 2015

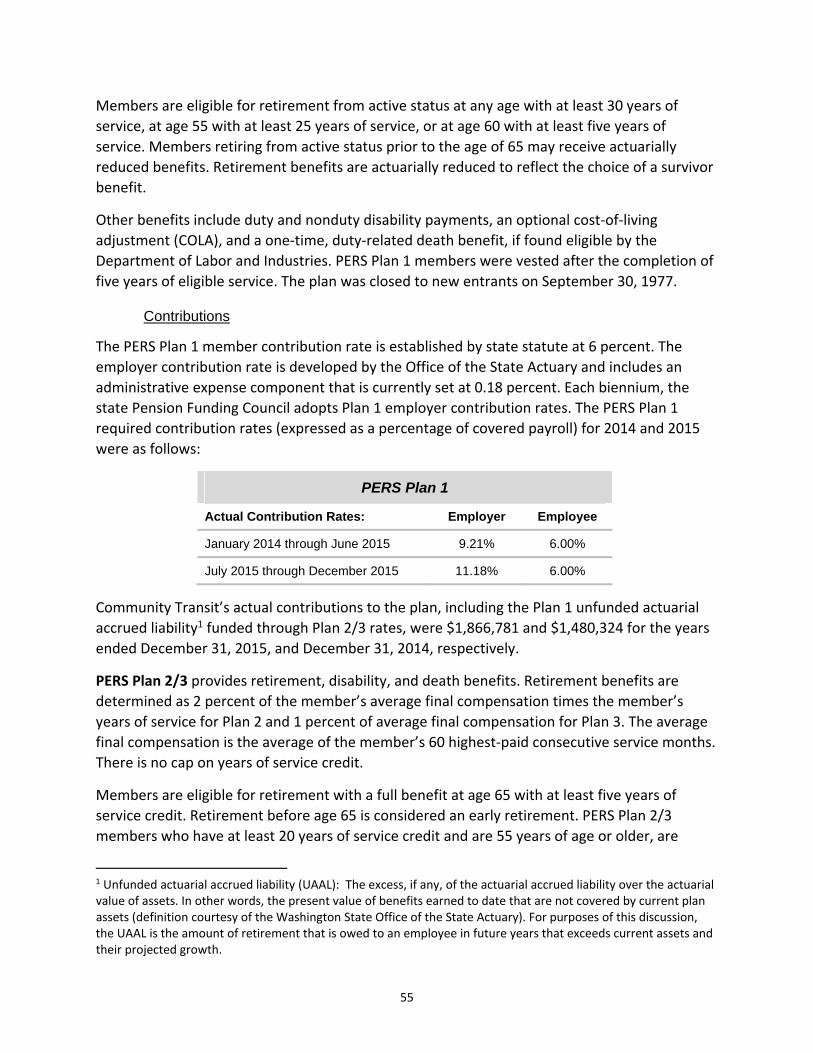

Note 1: Summary of Significant Accounting Policies

A. Reporting Entity

The Snohomish County Public Transportation Benefit Area Corporation, dba Community Transit,

was authorized to begin operation of a public transportation system in 1976. The agency was

incorporated under the provisions of Washington State law pertaining to public transportation

benefit area corporations (RCW 36.57A) and operates under the control of a Board of Directors.

Community Transit has an undivided interest in a nonequity joint venture, jointly governed with

six other agencies for the provision of regional smart card fare (ORCA) collection services.

Community Transit’s undivided interests in the assets, liabilities and operations of the ORCA

smart card are consolidated within these financial statements on a proportionate basis.

In fiscal year 2015, Community Transit implemented Governmental Accounting Standards

Board (GASB) Statement No. 68, Accounting and Financial Reporting for Pensions, GASB