Embed Size (px)

Citation preview

better together... we deliver

annual financial statements 30 June 2013

cont

ents

Our annual financial statements provide extensive cross-references to our other reporting publications, shown below:

Form 20-F, our annual report issued in accordance with the Securities Exchange Act of 1934, which is filed with the United States Securities and Exchange Commission (SEC), in line with the requirement of our New York Stock Exchange listing.

20-F

Contains a full analysis of the group’s financial results, with detailed financial statements, prepared in accordance with International Financial Reporting Standards as well as full corporate governance and remuneration reports.

AFS

SD Our annual report covering environment, social and governance matters. Prepared in accordance with the GRI G3 framework.

IR Our primary annual report to stakeholders. Contains succinct material information and conforms to local and international integrated reporting frameworks.

How to read our annual financial statements

Printed copies of this report are available on request. Refer to the contact information on page 249.

Mrs Christine Ramon CA(SA), chief financial officer is responsible for this set of financial statements and has supervised the preparation thereof in conjunction with the executive: group finance, Mr Paul Victor CA(SA).

Sasol annual integrated report 30 June 2013

IR

better together... we deliver

annual integrated report 30 June 2013

20mm

Sasol annual financial statements 30 June 2013

www.sasol.com better together... we deliver

annual financial statements 30 June 2013

AFS

23mm

www.sasol.com better together... we deliver

Form 20-F 30 June 2013

Form 20-F 30 June 2013

20-F

Sasol sustainable development report 30 June 2013

better together... we deliver

sustainable development report 30 June 2013

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

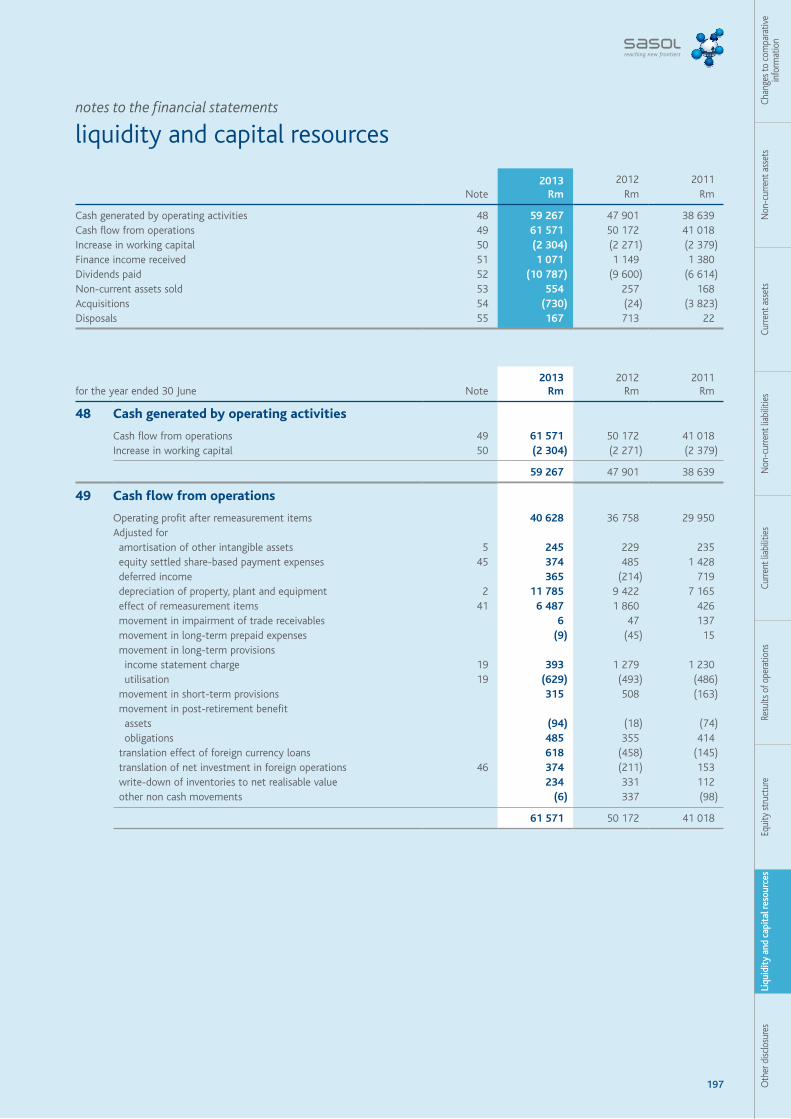

ited

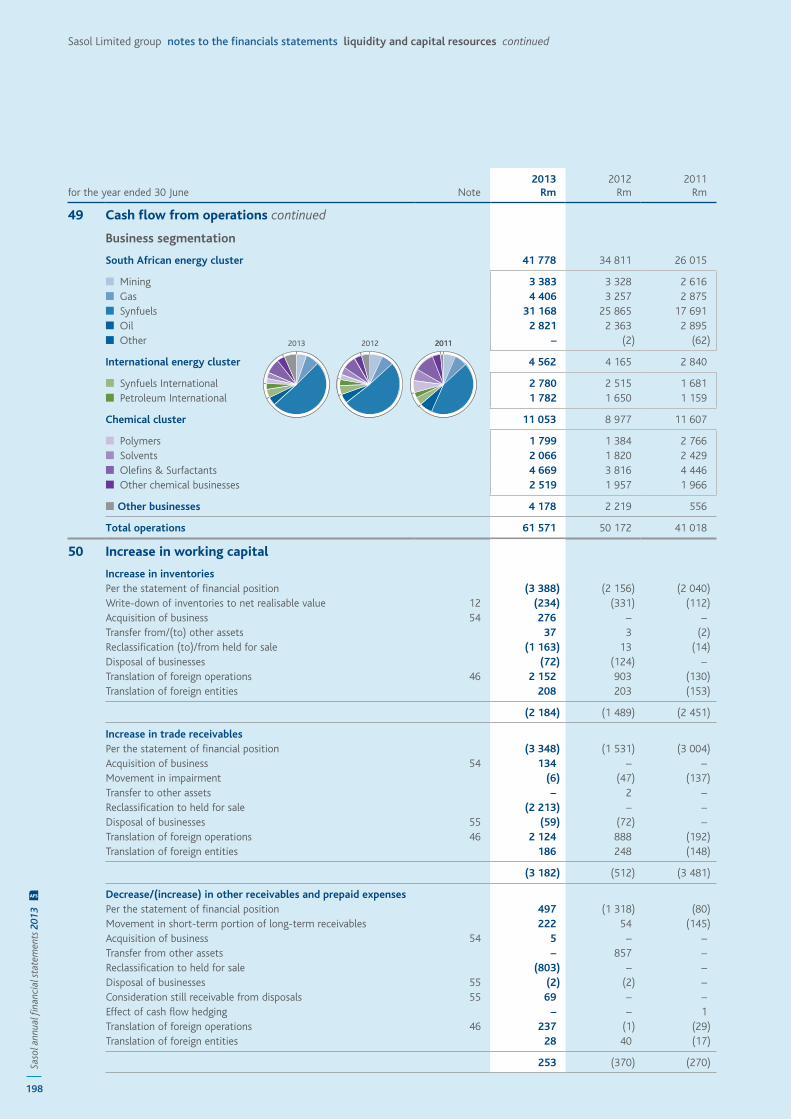

grou

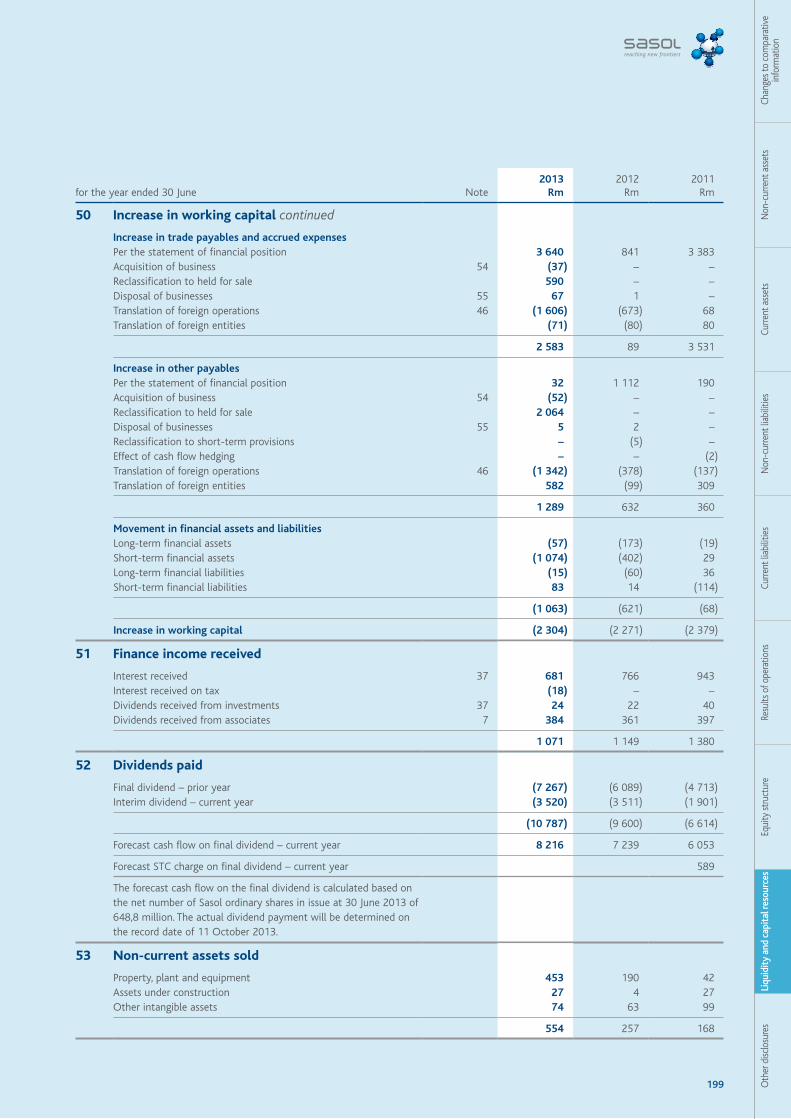

p co

nsol

idat

ed fi

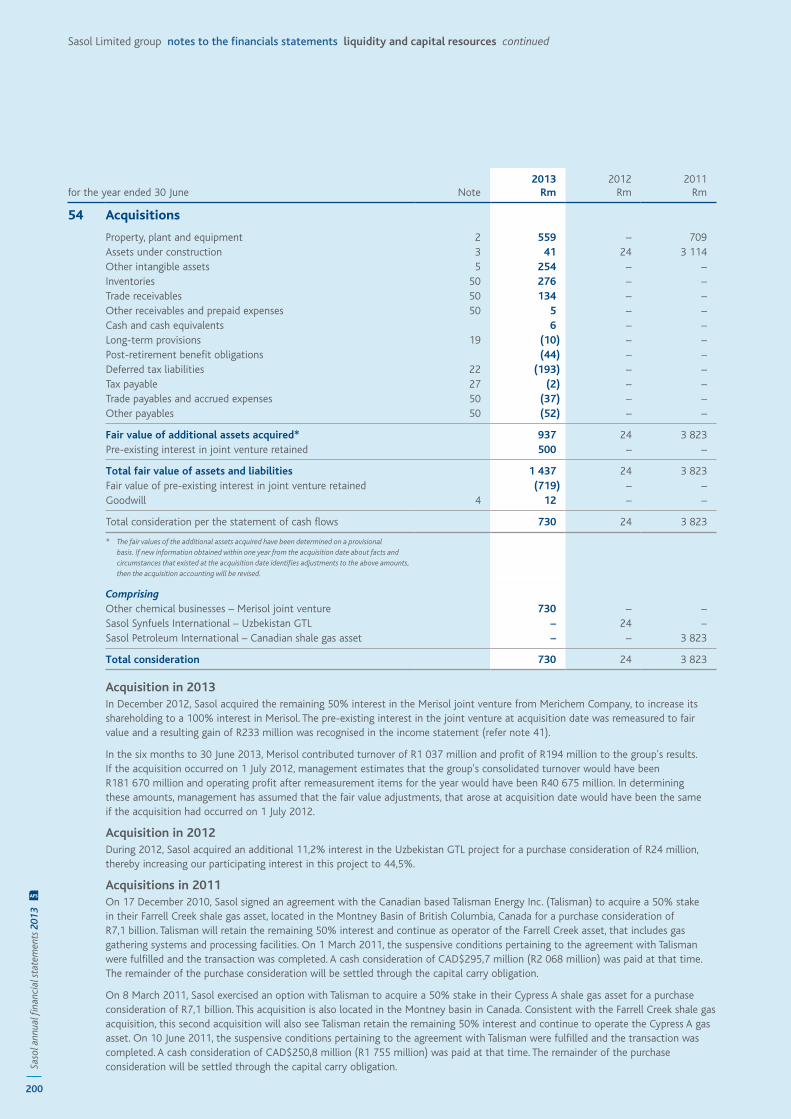

nanc

ial s

tate

men

tsSa

sol o

verv

iew

1

01

2 Chief financial officer’s review

27 Corporate governance

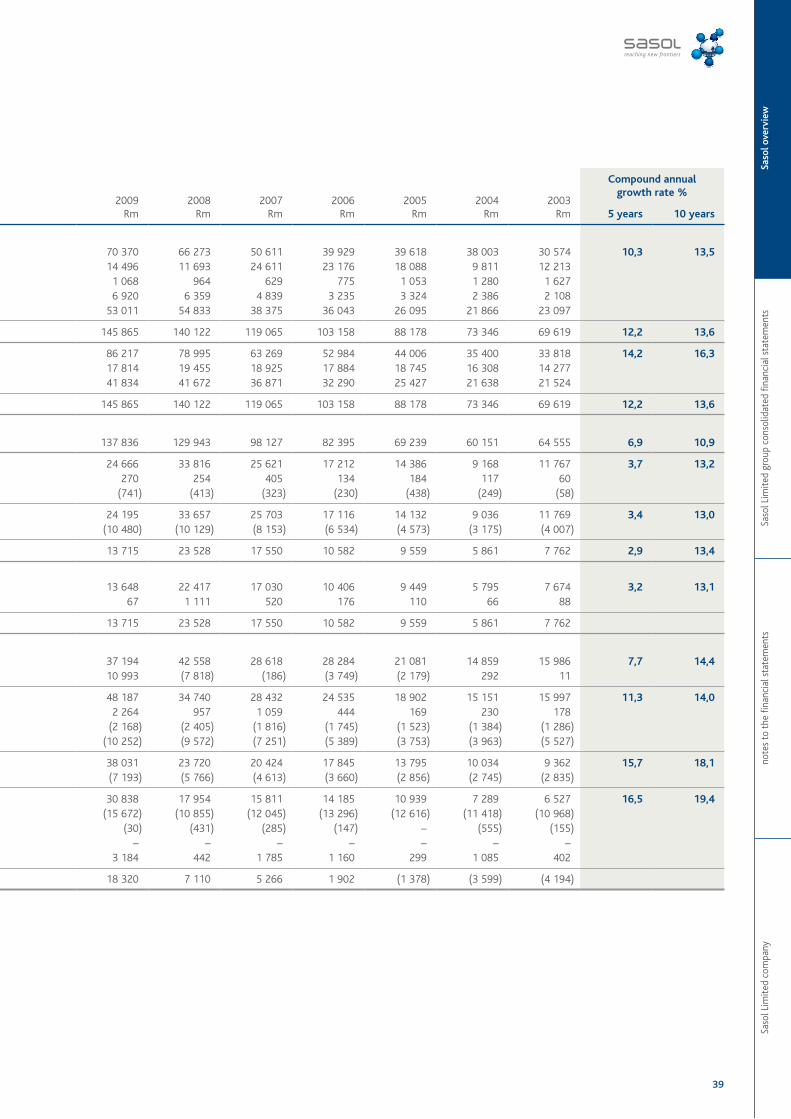

38 Eleven year financial performance

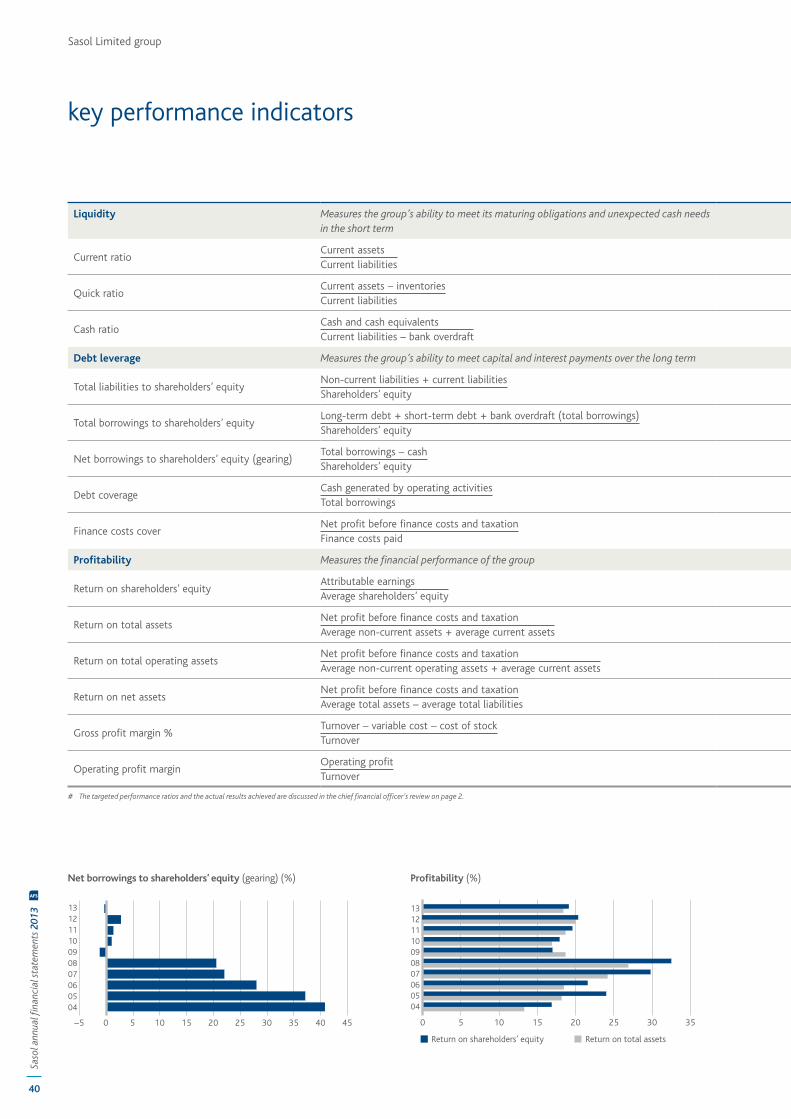

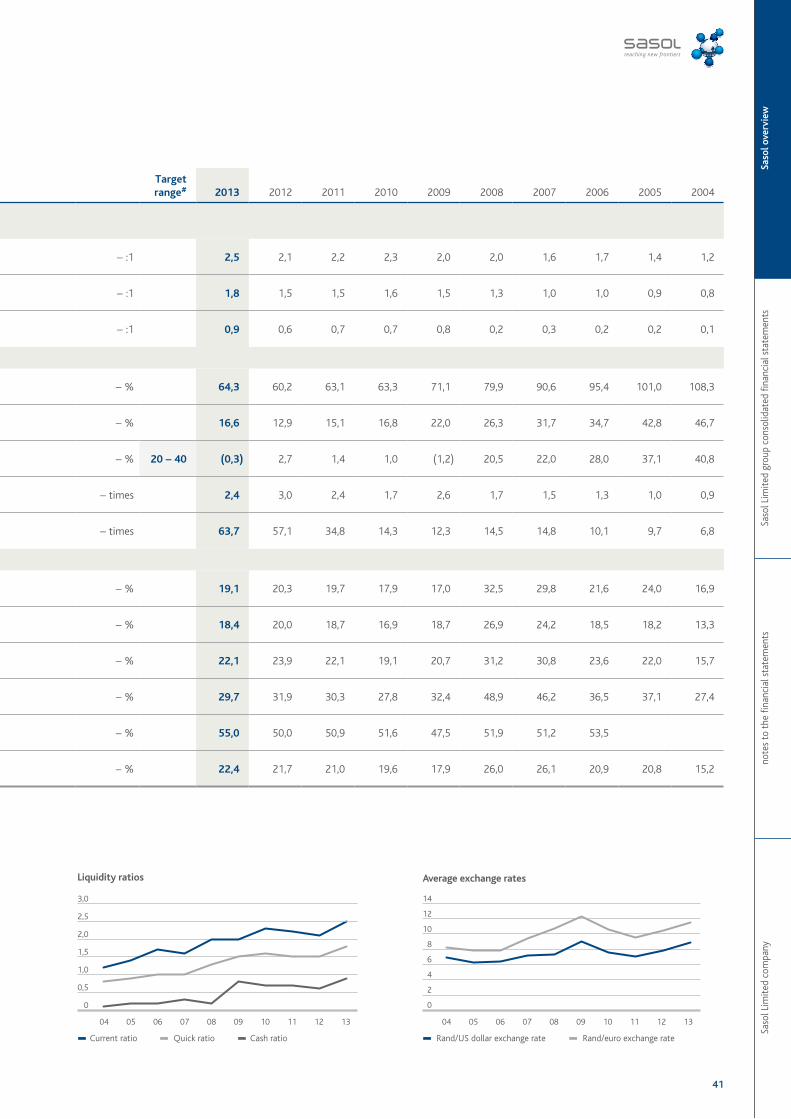

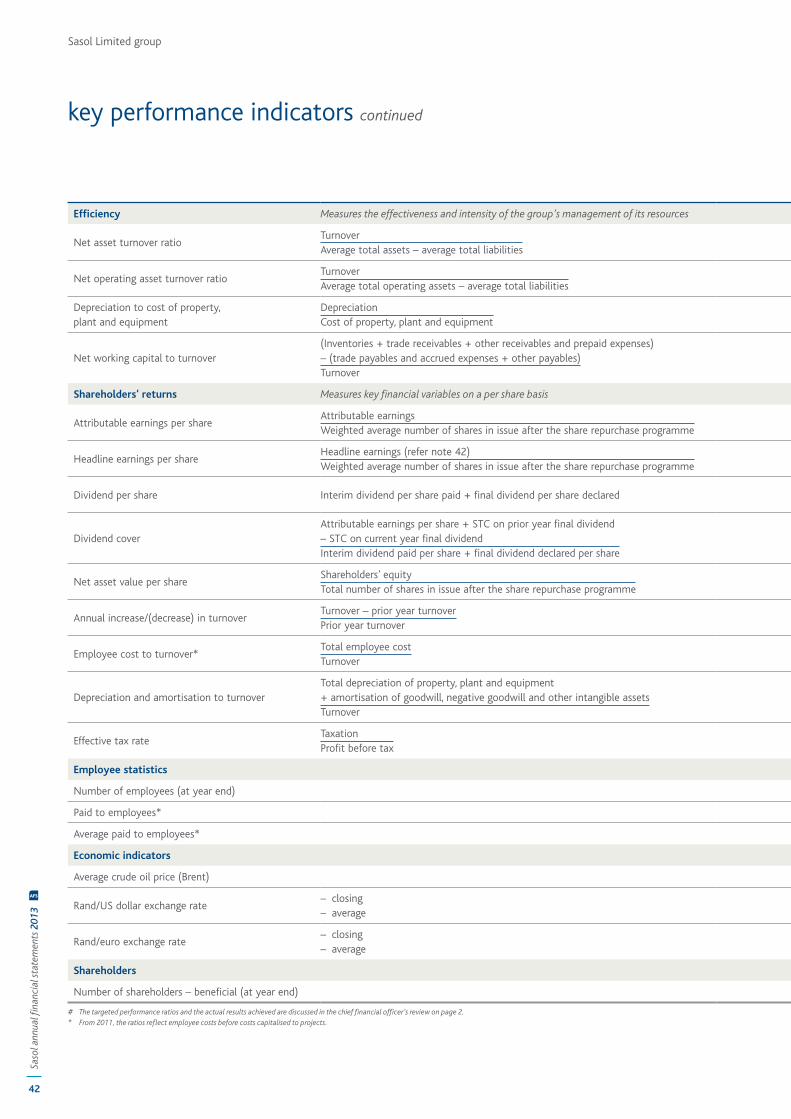

40 Key performance indicators

46 Value added statement

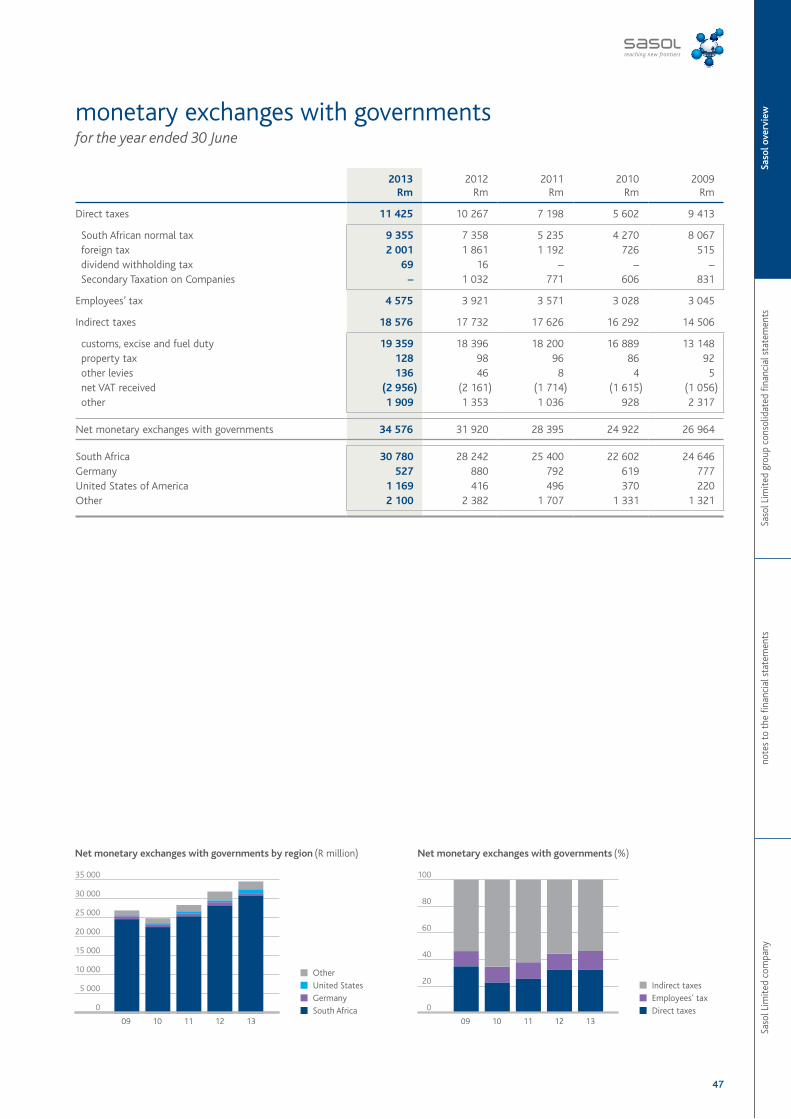

47 Monetary exchanges with governments

48 Audit committee report

51 Approval of the financial statements

51 Certificate of the company secretary

52 Report of the independent auditor

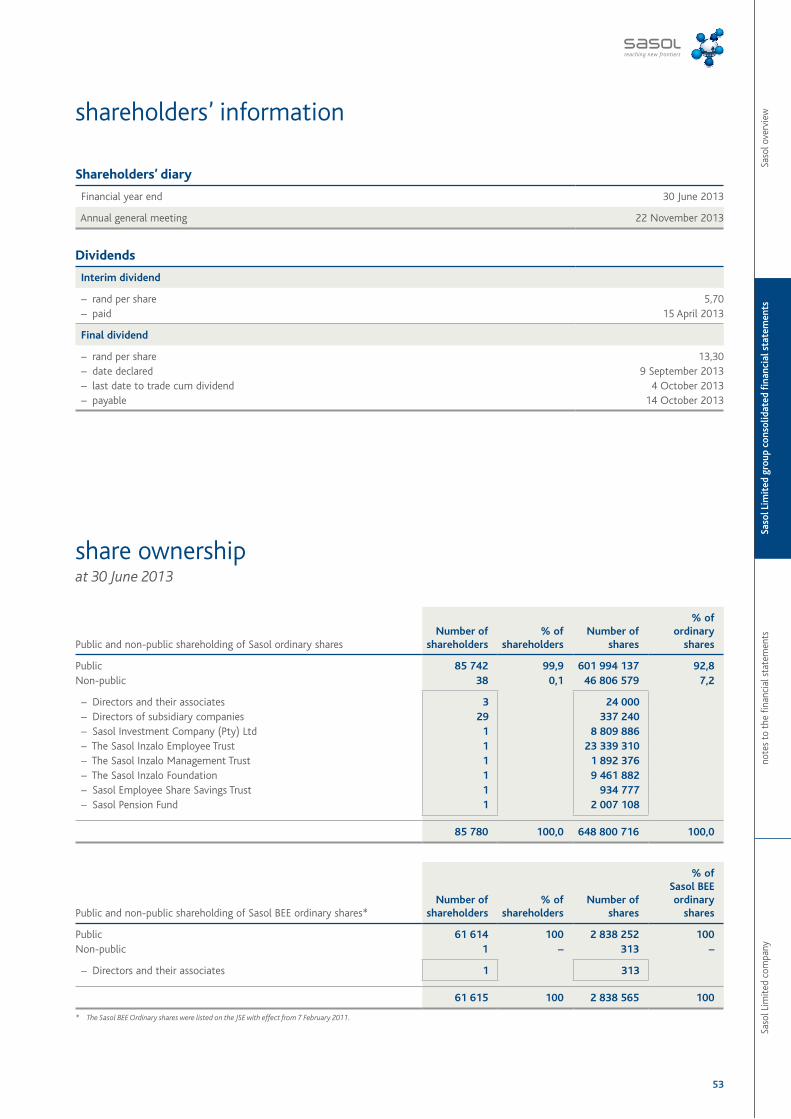

53 Shareholders’ information

53 Share ownership

55 Directors’ report

57 Remuneration report

80 Accounting policies and financial reporting terms

98 Statement of financial position

100 Income statement

100 Statement of comprehensive income

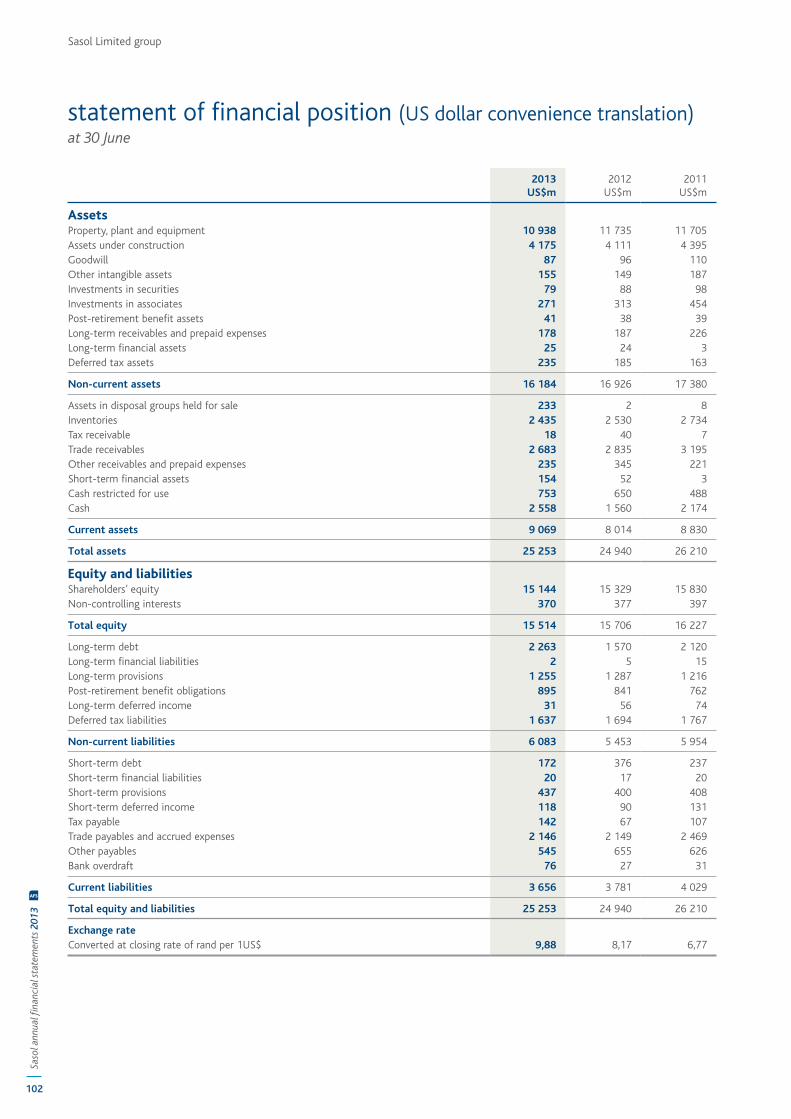

102 Statement of financial position (US dollar convenience translation)

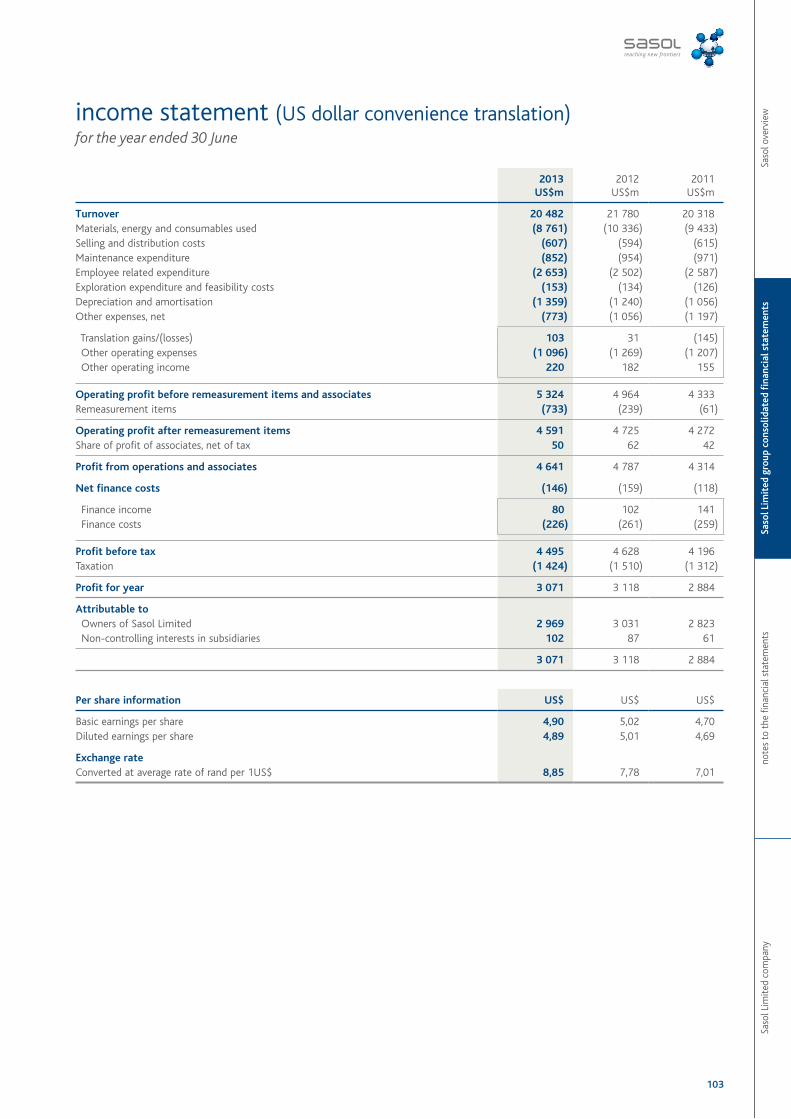

103 Income statement (US dollar convenience translation)

104 Statement of changes in equity

106 Statement of cash flows

108 Business segment information

114 Geographic information

117 Changes to comparative information

117 Non-current assets

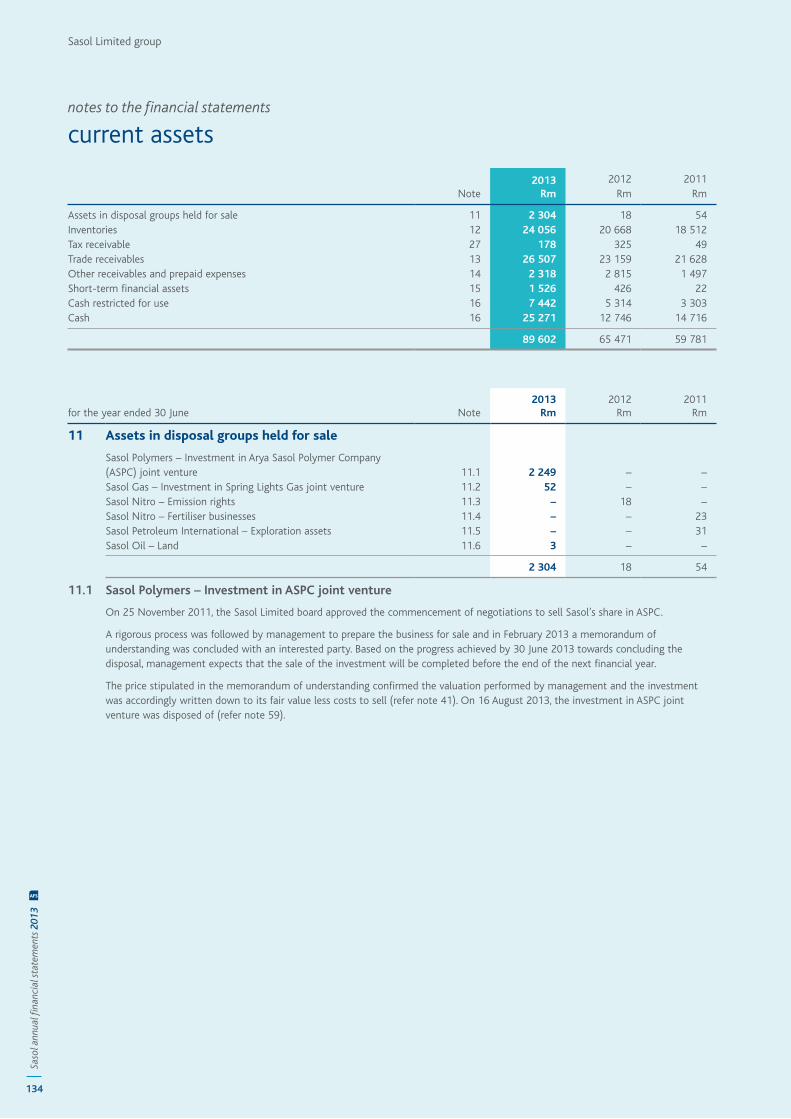

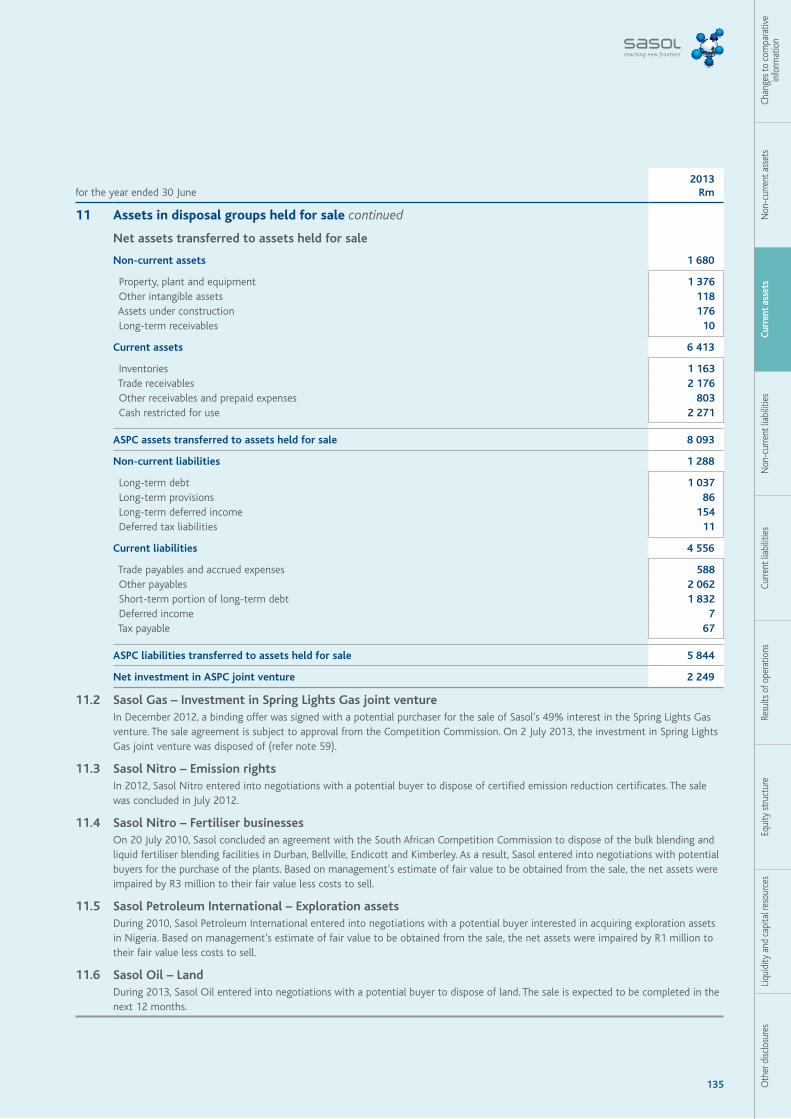

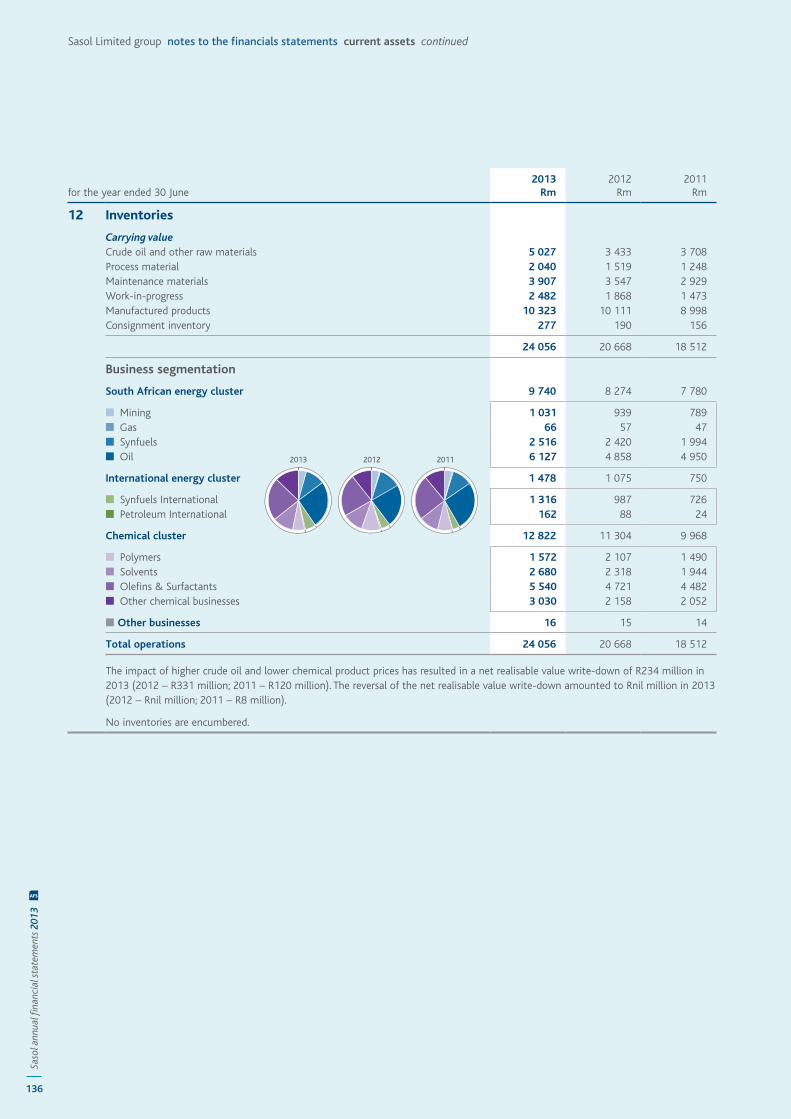

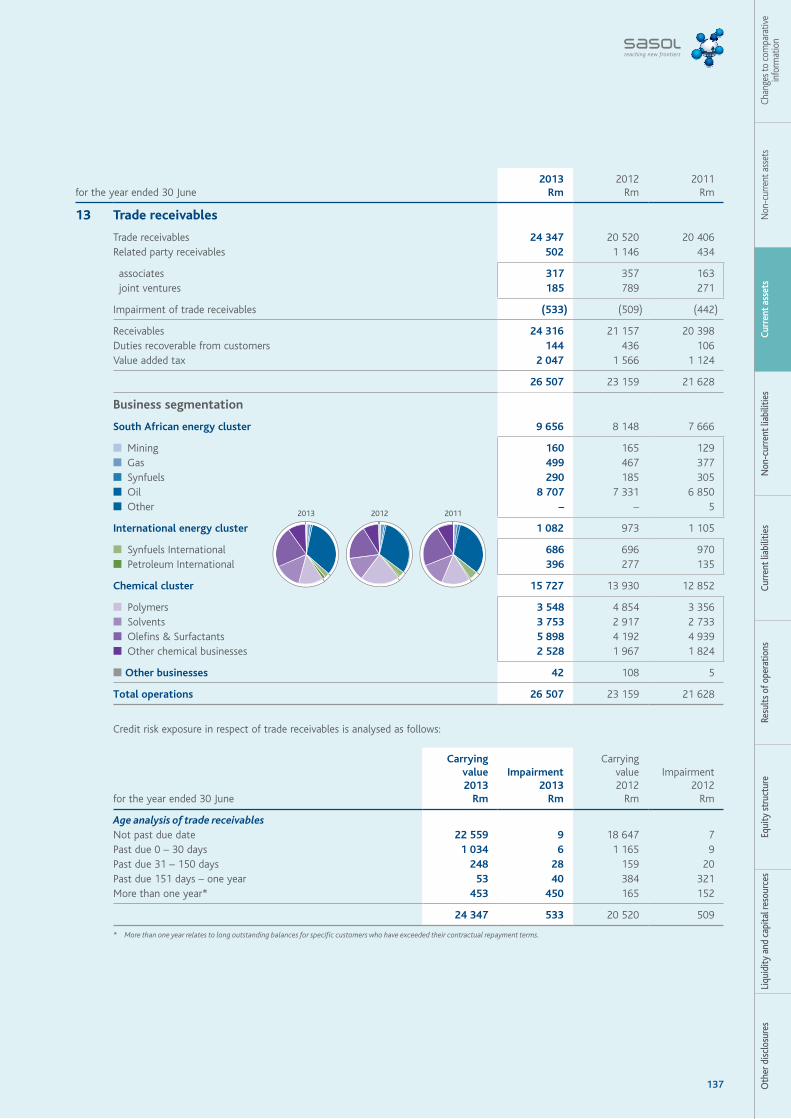

134 Current assets

140 Non-current liabilities

161 Current liabilities

164 Results of operations

176 Equity structure

197 Liquidity and capital resources

203 Other disclosures

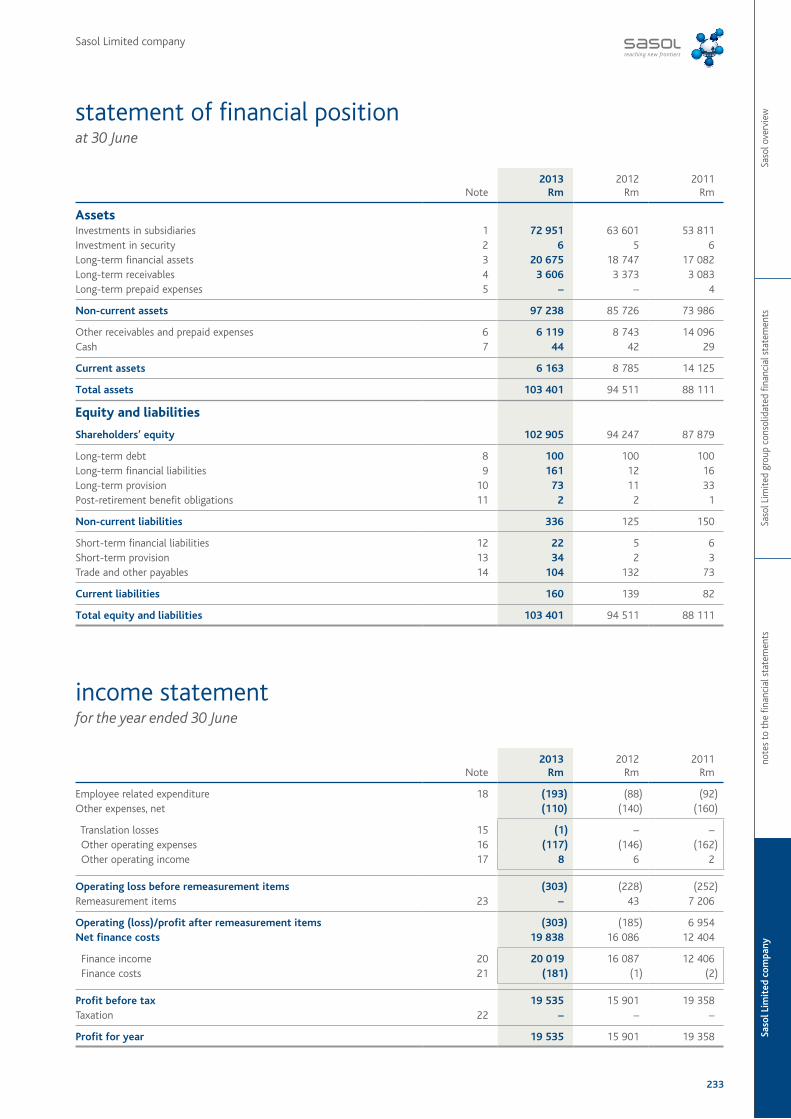

233 Statement of financial position

233 Income statement

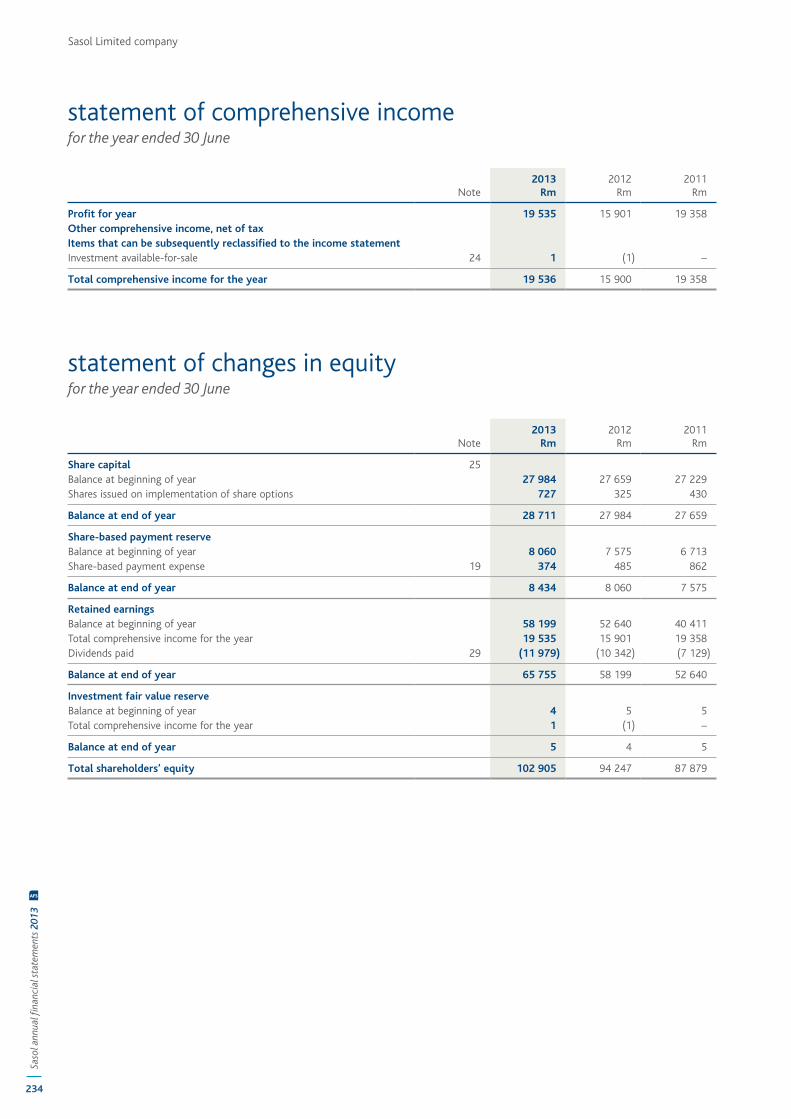

234 Statement of comprehensive income

234 Statement of changes in equity

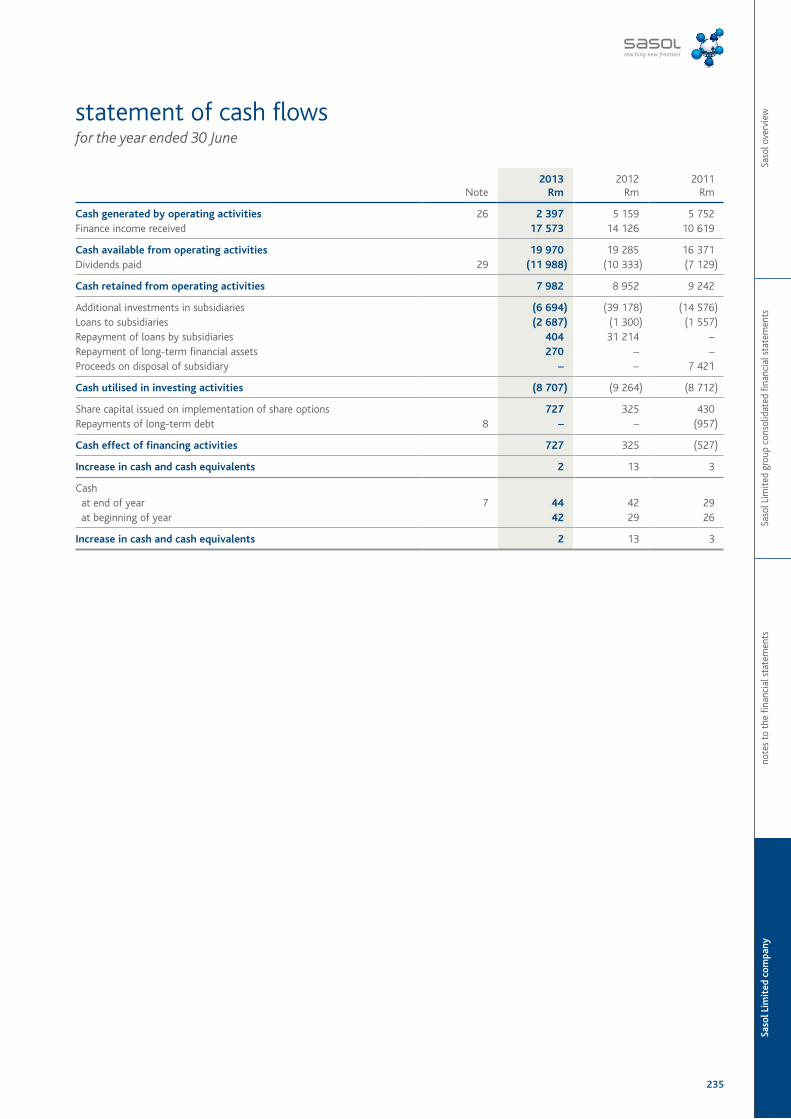

235 Statement of cash flows

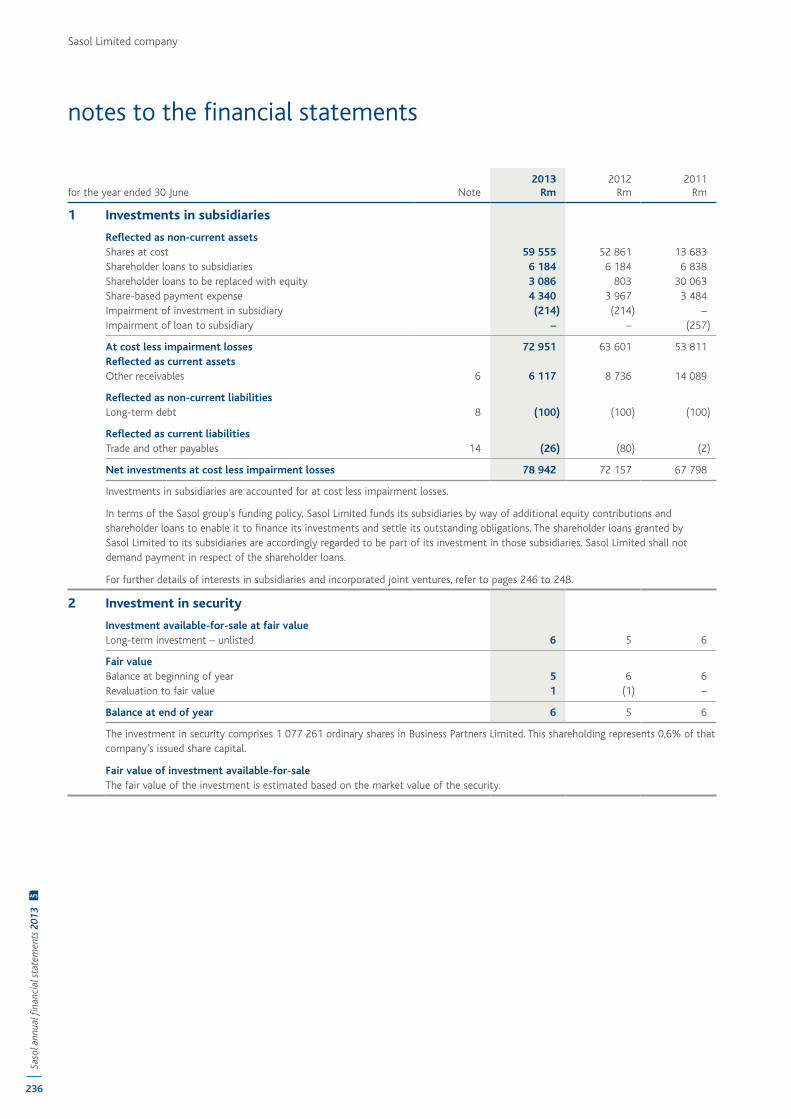

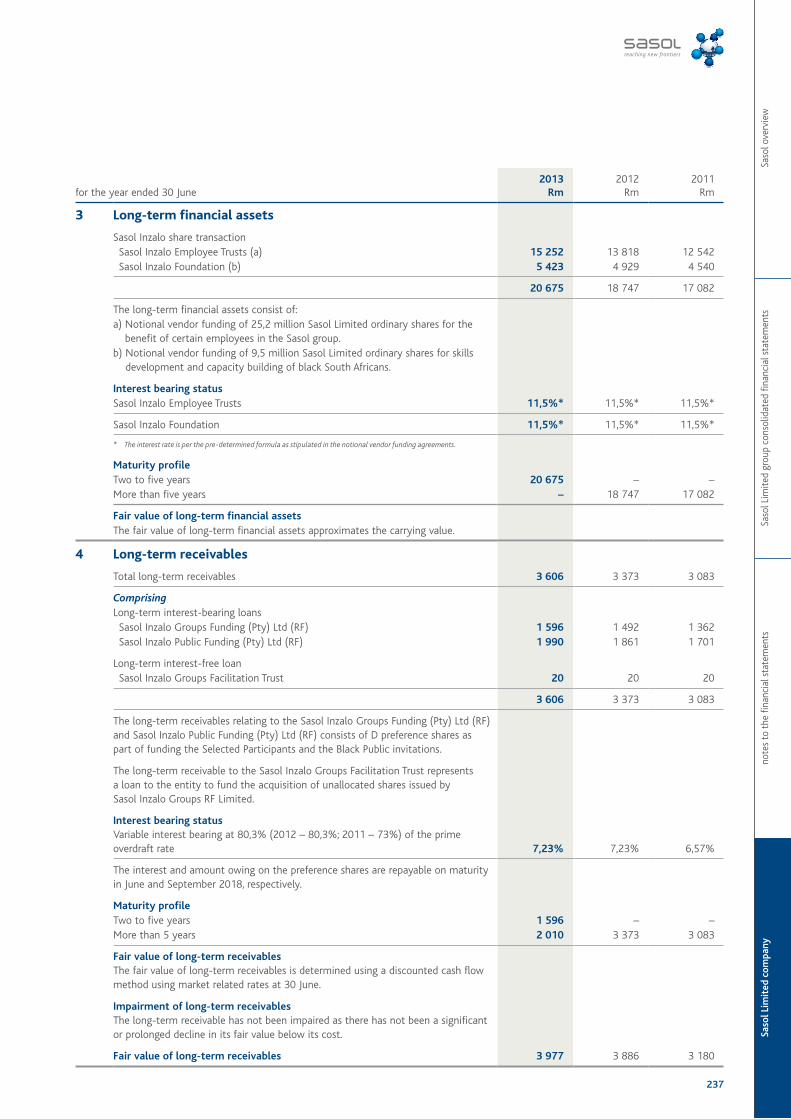

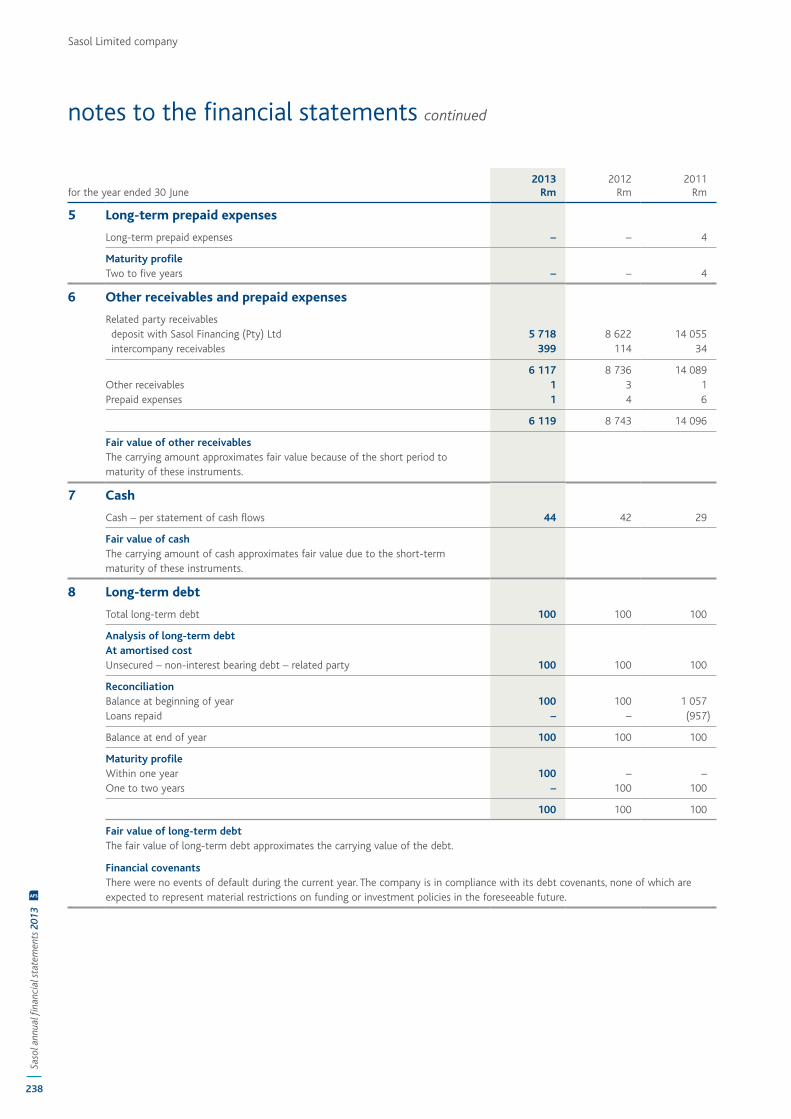

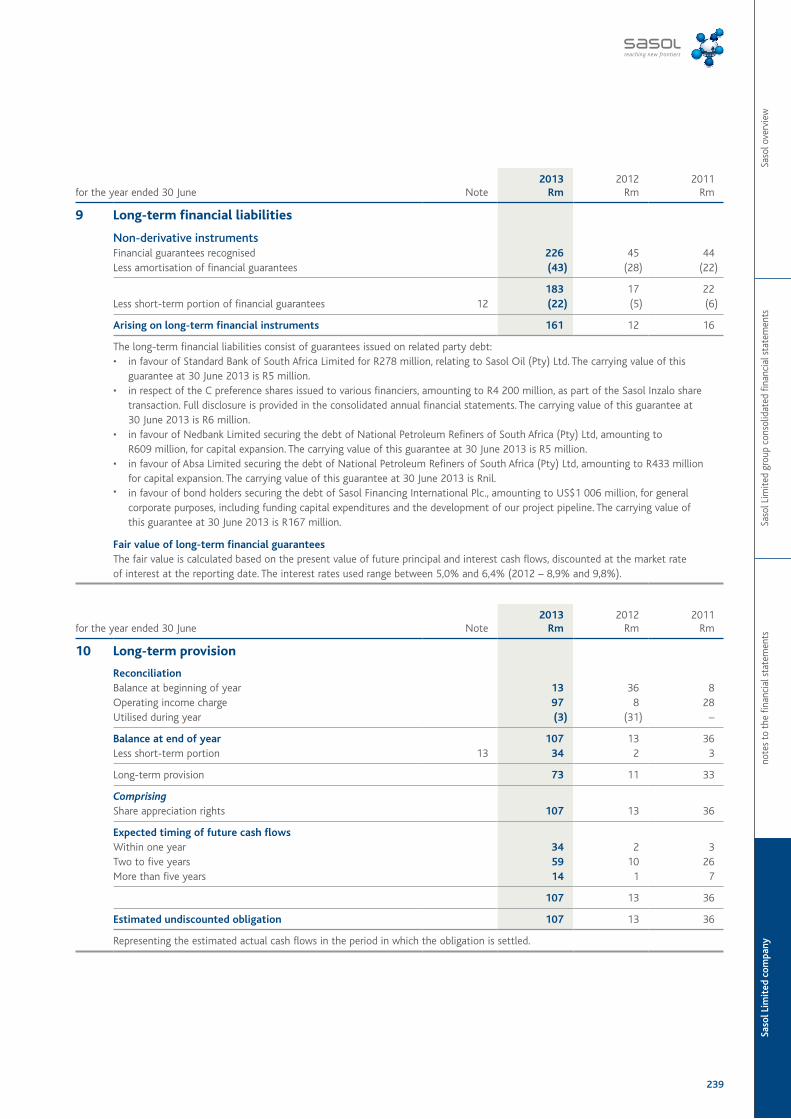

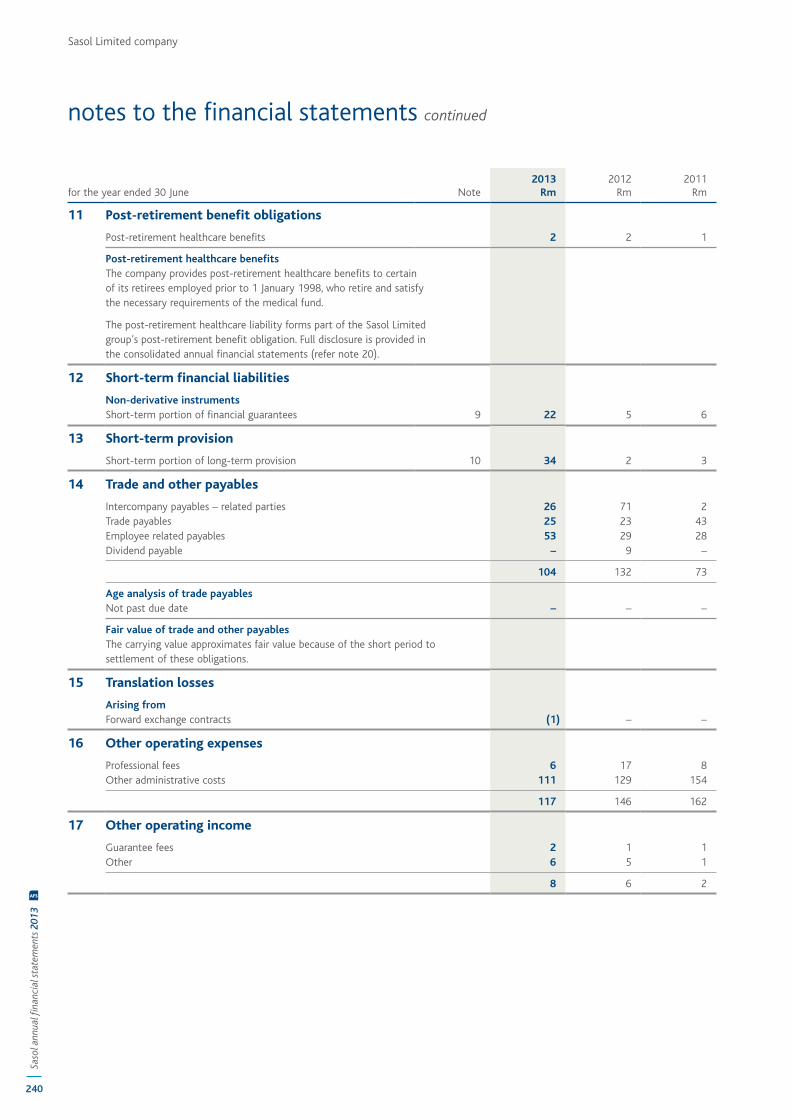

236 Notes to the financial statements

246 Interest in significant operating subsidiaries and incorporated joint ventures

249 Contact information

Sasol overview

02Sasol Limited group consolidated financial statements

03Notes to the financial statements

04Sasol Limited company

Christine Ramon, chief financial officer

better together... means delivering on our financial priorities

chief financial officer’s review

2

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

3

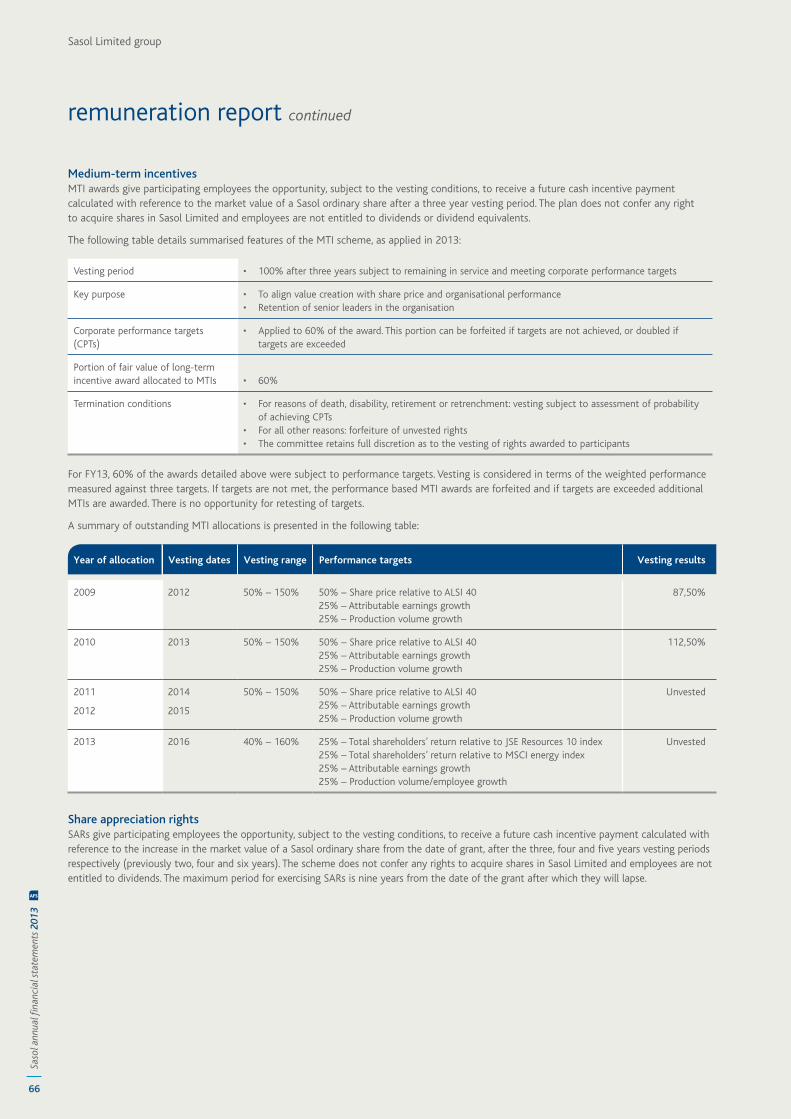

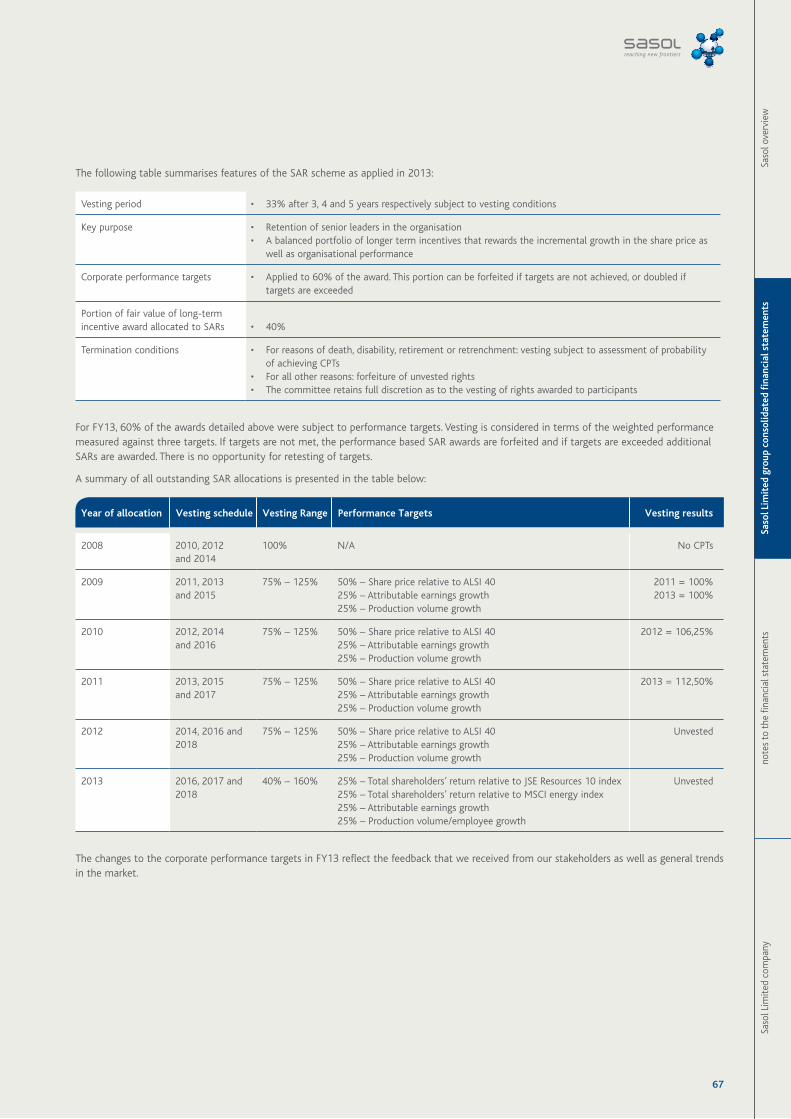

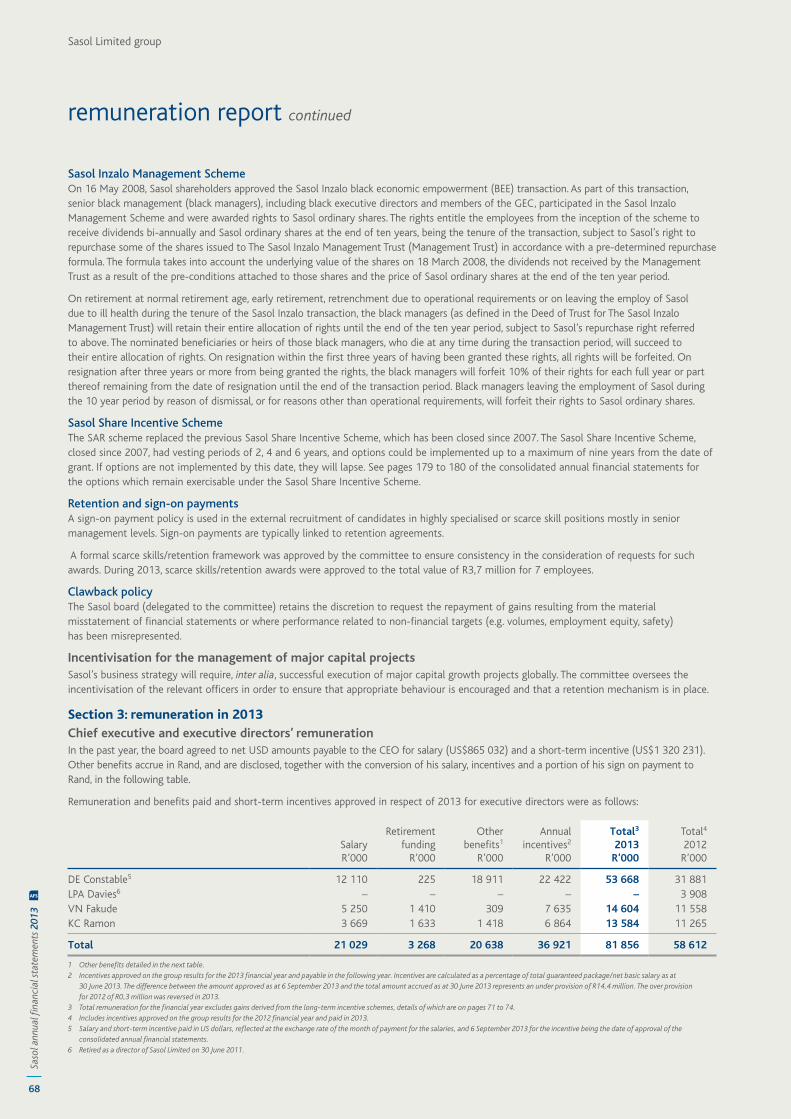

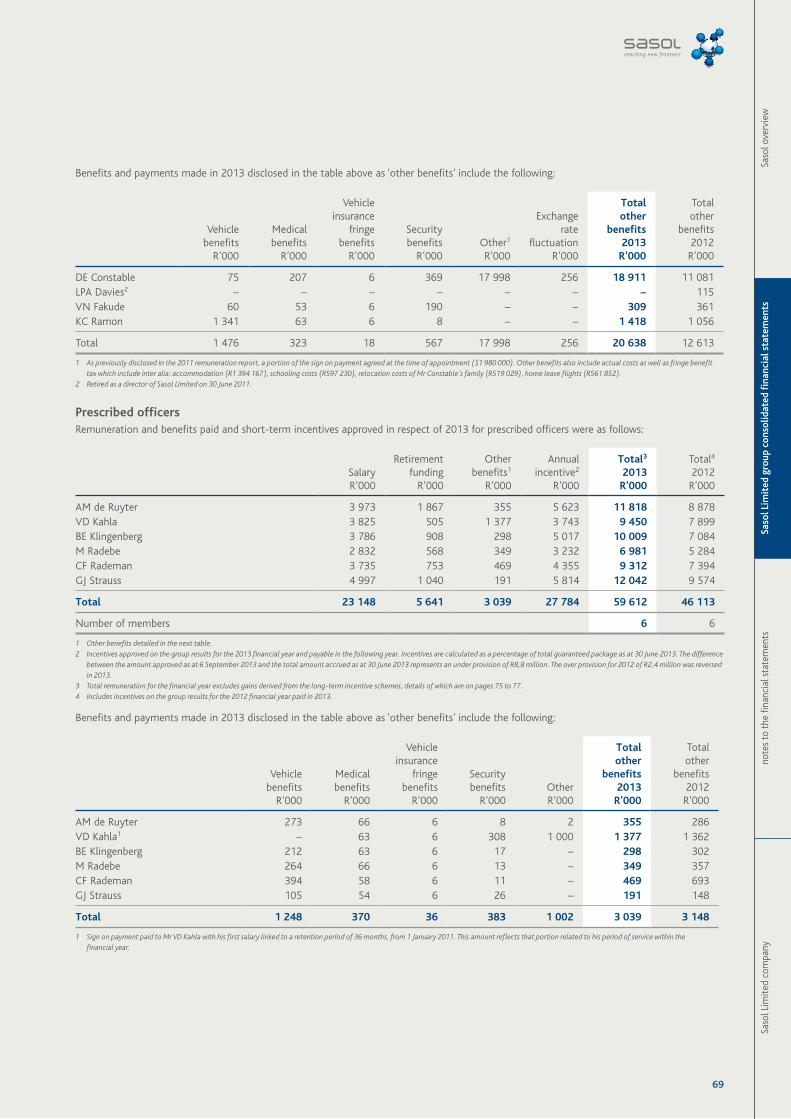

1 Introduction

The 2013 financial year has been challenging, yet rewarding. Sasol has delivered strong results, underpinned by the continued focus on operational efficiencies, delivering better than expected volumes from Sasol Synfuels. Cost containment and margin improvement remain challenging, especially in light of the pressures in the South African environment and the continued volatile macroeconomic environment. During the year, we refined our strategy ensuring that we continue to nurture and grow our foundation businesses and making progress on our growth projects. These actions position Sasol well to deliver on its stakeholder value proposition – being a growing company with a strong pipeline of growth projects, supported by talented, high performing employees around the world, and underpinned by a strong financial position. We have also been able to contribute significantly to the South African economy, through the payment of direct and indirect taxes, as well as to the socio-economic upliftment of the areas in which we operate, by contributing to our communities and undertaking environmental initiatives. Refer to our annual integrated report and sustainable development report for further details on these aspects.

This review is intended to provide our stakeholders with further insight into the financial performance and position of the group. Our primary financial focus is on managing our margins, cash, gearing and return on equity, within the context of the environment in which we operate. Stakeholders are advised to read this review in conjunction with the consolidated annual financial statements presented on pages 55 to 248.

2 Key financial risks and uncertainties affecting our performance

The world is still recovering from the global economic crisis of 2008. While growth in more mature economies is picking up, it is at a slower than expected pace. Economic issues persist in a number of regions: the European financial crisis deepened in the 2012 calendar year, in the United States (US), recovery has been weak coupled with the ‘fiscal cliff’, and in Asia, the economies are still grappling with the effects of natural disasters. However, energy consumption in emerging markets continues to increase on the back of long-term economic growth prospects. This bodes well for commodity prices, but we continue to see significant oil and gas price and commodity volatility.

In order to appreciate the impact of these events on our business, it is important to understand those factors that affect the delivery of our results.

a. Current economic climate and its impact on Sasol Sasol operates in a number of countries across the globe including Sub-Saharan Africa, Europe, the Asia-Pacific region, North

America and the Middle East. As such, developments in the global economy have a significant impact on our business.

During the 2012 calendar year, the global economic recovery evolved largely in line with our expectations. Economic growth remained fragile and unbalanced, with emerging markets generally outperforming the advanced economies. According to the International Monetary Fund’s (IMF) July 2013 World Economic Outlook update, emerging market and developing economies grew by 4,9% in the 2012 calendar year, while gross domestic product (GDP) growth in the advanced economies managed only 1,2% over the same period. Overall, the global economy grew by 3,1% in the 2012 calendar year, down from the previous calendar year’s 3,9% growth.

From early in the 2012 calendar year, three main downside growth risks dominated the global outlook, but most of these risks receded as the year progressed. The risk of a euro area break-up and the knock-on effects that it may have had on the global economy eased, following remarks from the European Central Bank (ECB) president that he would ‘do whatever it takes’ to preserve the currency union. A second risk related to fears that policymakers in the US would not reach a compromise on tax

Sasol Synfuels’ production volumes up by 4%

Cash fixed costs (excluding exchange rate effects) increased by 7%, in real terms

Operating profit up by a record 26%, excluding once-offs

Headline earnings per share up by 25% to R52,62

Total dividend of R19,00 per share, up by 9%

Cash generated by operating activities up by 24%

Highlights 2013

4

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Sasol Limited group

and expenditure adjustments, which faded as policymakers avoided the ‘fiscal cliff’ early in the 2013 calendar year. The third risk related to Chinese economic growth that slowed in the first half of the 2012 calendar year, raising the probability of a so-called economic ‘hard landing’. However, towards the end of that year, growth picked up and the probability of a ‘hard landing’ scenario decreased.

While some of last year’s downside growth risks to the global economic recovery have faded, they have not disappeared and a new risk has emerged. Following weaker-than-expected Chinese macroeconomic indicator releases during the first half of the 2013 calendar year and comments from policymakers on anticipated growth rates, market fears of a potential ‘hard landing’ are resurfacing. Recently, the Federal Reserve in the US has hinted at a gradual withdrawal of quantitative easing (QE) should the economy recover in line with expectations. While it is not clear what the potential impact or long term unintended consequences of QE will be, mention of an end to QE has already contributed to financial market volatility and questions being raised on the impact of potential capital flow reversals on emerging market economic prospects.

Bearing these downside global economic growth risks in mind, it is anticipated that the economic recovery will remain fragile and unbalanced. Sasol expects that global economic growth in the 2013 calendar year will be similar to the approximate 3% growth recorded in the previous year, with growth rising only modestly in the 2014 calendar year.

Considering the perceived fragile state of the global economy and the uncertainties still facing the global economy, it is expected that commodity price and financial market volatility will continue for the foreseeable future.

Country specific factors in brief

South Africa Labour unrest, lower commodity prices, electricity supply constraints, low consumer and business confidence, and lacklustre foreign demand conditions all weighed on South Africa’s economic performance in the 2012 calendar year and into the 2013 calendar year, Real GDP growth slowed from 3,5% in the 2011 calendar year to 2,5% in the 2012 calendar year. After reaching a relatively low 4,9% year-on-year in July 2012, consumer price inflation rose gradually to 5,9% in April 2013 before easing back to 5,5% in June 2013. With little evidence of demand-driven inflation, concerns over weak domestic economic growth prospects and ongoing problems in the euro zone, the Reserve Bank decided to cut the policy rate to 5,0% in July 2012, taking it to its lowest level since the early-1980s. More recently, the Monetary Policy Committee decided to keep the policy interest rate at 5,0% in the face of challenging economic conditions.

Looking forward, South Africa’s economic prospects remain challenging, where we expect GDP to remain below-trend in the 2013 and 2014 calendar years, as labour market uncertainties, a slowdown in household consumption expenditure growth, potential electricity supply constraints, a substantial current account deficit funding requirement and relatively high cost increases continue to weigh on the country’s growth prospects.

United States The US economy grew at a modest 2,2% in the 2012 calendar year as global growth concerns and relatively sluggish domestic demand conditions weighed on growth. During the course of the year, fears of the country hitting the so-called ‘fiscal cliff’ in the early part of the 2013 calendar year lingered, but consumers proved resilient as the housing market strengthened, consumer confidence improved and the unemployment rate declined. The so-called ‘fiscal cliff’ was sidestepped as policymakers reached a compromise on tax and spending reforms. Despite this compromise, these policies are likely to weigh on economic activity in the 2013 calendar year. As the impacts of these policies start to wane from the 2014 calendar year, and should the consumer and housing market recovery prove as durable as we expect, GDP growth is likely to improve modestly.

Meanwhile, from the middle of the 2013 calendar year, there has been an increased focus on the timing of the step-down in QE and the potential end to the programme in the 2014 calendar year. It is believed that markets will remain focused on this for the remainder of the 2013 calendar year and into the 2014 calendar year, with the ebb-and-flow of information likely to contribute to financial and commodity market volatility.

Canada Economic growth in Canada slowed to 1,7% in the 2012 calendar year from 2,5% a year earlier, reflecting slower real income growth, fiscal restraint, a relatively weak external environment and a strong currency that restrained export growth. Despite the slower economic growth, employment prospects remained positive as the unemployment rate fell from 7,5% in January 2012 to 7,1% in June 2013. Consumer price inflation fell to 1,5% in the 2012 calendar year from 2,9% in the prior year on the back of subdued core consumer price inflation and as food and petrol prices rose at a slower rate.

It is believed that fiscal restraint and relatively slow growth in household spending will continue to weigh on Canada’s growth prospects in the 2013 calendar year. However, as the global and US economy continues to recover gradually into the 2014 calendar year, Canada’s economic fortunes should show some improvement.

chief financial officer’s review continued

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

5

Country specific factors in brief

Euro zone Following modest growth of 1,5% in the 2011 calendar year, the euro zone economy contracted 0,6% in the 2012 calendar year. The ongoing process of financial and non-financial sector balance sheet deleveraging, low and declining levels of business and consumer confidence for most of the year, high and rising unemployment, fiscal consolidation, and lingering fears over a potential euro area break-up, contributed to the poor performance of the region’s economy. However, the risk of an imminent euro area break-up reduced significantly following assurances from the president of the ECB. Since then, financial market conditions have stabilised and indicators in the early part of the 2013 calendar year point to a less negative economic environment. However, it is believed that the region’s economy will see another full year decline in economic activity, before posting anaemic economic growth in the 2014 calendar year.

Consumer inflation eased from 2,7% in the 2011 calendar year to 2,5% in the 2012 calendar year, which is still above the ECBs medium-term inflation target of 2%. The above-target inflation stemmed mainly from energy price pressures and indirect tax increases owing to ongoing fiscal consolidation. It is believed that significant excess capacity exists in the region’s economy, which should help keep inflationary pressures at bay. This, together with a generally poor growth outlook, is likely to see interest rates remain at very low levels for an extended period.

China Chinese GDP growth continued to slow in the 2012 calendar year, averaging 7,8% from the previous year’s 9,3%. While weak external demand conditions had a negative impact on Chinese net-exports, government infrastructure investment, accommodative financing conditions and consumption all helped support economic growth. It is believed that policymakers will push ahead with policies aimed at rebalancing the Chinese economy away from investment and export-led growth towards more consumption-driven economic growth. This process, and the Chinese authorities’ apparent comfort with slower, more sustainable growth rates indicate that GDP growth is likely to be around 7,0 – 7,5% in the 2013 and 2014 calendar years.

Consumer price inflation has been relatively subdued during the course of the 2012 and into 2013, reaching 2,7% year-on-year in June 2013. Following a number of years of significant investment resulting in excess capacity in the economy and little sign of food price inflationary pressures at present, it is anticipated that inflation is likely to remain muted over the next two years.

Middle East The economic fortunes of the Middle Eastern region are still being influenced by political and social transitions and accompanying tensions in many countries. World Bank estimates show that international sanctions and rocketing inflation contributed to a contraction in Iran’s economy, while civil conflict in Syria led to a significant fall in output during the 2012 calendar year. In contrast, an increase in Iraqi oil production saw relatively strong growth being sustained.

While some countries may benefit from slightly better growth prospects in the euro area and other parts of the world, it is believed that unpredictable socio-political developments will dictate the economic performance of the region for some time. Given these uncertainties, economic growth in the region is likely to remain relatively weak for the foreseeable future.

Sub-Saharan Africa According to IMF estimates, economic growth in the Sub-Saharan Africa region slowed to 4,9% in the 2012 calendar year from 5,4% the previous year. The still strong growth was supported by private consumption expenditure, investment and export growth, with the oil exporting countries having generally done better than those countries which have close trade ties to the euro area. Consumer inflation in the region weakened from 9,3% in the 2011 calendar year to about 9% in the 2012 calendar year, reflecting a slowdown in global food and energy price increases, the lagged effect of past monetary policy tightening in certain countries and better weather conditions in some parts of the region.

It is expected that relatively strong investment growth in certain sectors will lift the overall growth potential of the Sub-Saharan Africa region, which together with its significant mineral resources, makes for a promising and strong growth environment – albeit that this growth comes off a relatively low base.

6

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Sasol Limited group

In addition to the general macroeconomic environment, Sasol is also affected by the crude oil and natural gas prices, the exchange rate and chemical prices. These are discussed separately on pages 6 to 8.

In order to address the challenges that the global economic climate is presenting, we will continue to focus on those factors that remain within our control. This will ensure that we are best positioned to deliver shareholder value.

b. Volatile crude oil prices We are exposed to the volatility associated with the selling price of fuel marketed by Sasol Oil. This selling price is governed by

the basic fuel price (BFP), as regulated by the South African government. The key factors influencing the BFP include the crude oil price, rand/US dollar exchange rate and the refining margin typically earned by coastal refineries.

Due to the integrated nature of our operations, Sasol Synfuels uses a pricing mechanism for raw materials supplied to the South African chemical business, which matches the BFP. The price charged is the value that Sasol Synfuels could earn by converting these products to fuel and selling it at the BFP.

The crude oil price has remained extremely volatile and we have seen substantial increases in the average Brent crude oil price over the past five years. Following the global economic crisis, the stability in the markets seen in the 2010 financial year was short lived. Unfavourable economic conditions in Europe, which were underpinned by the continuing economic crisis in the euro zone as well as lower than expected growth rates saw the return of volatility in financial markets. However, the overall increase in the average Brent crude oil price was attributable to the uncertainties surrounding supply. This resulted in the crude oil price averaging around US$108,66/barrel (b) for the 2013 financial year, reaching a high of US$119,03/b and a low of US$95,51/b and closed at US$102,46/b at 30 June 2013.

In order to protect the group against the adverse effects of short-term oil price volatility and rand/US dollar exchange rate fluctuations on the purchase cost of crude oil (approximately 60 000 barrels/day) used in our Natref refinery, a combination of forward exchange contracts and crude oil futures is used. However, this hedging mechanism does not protect the group against longer-term trends in crude oil prices.

Should attractive hedges be available in the market, we hedge against the downside risk in the crude oil price to increase the stability and predictability of our cash flows, considering the group’s substantial planned capital investment programme and our sensitivity to oil price volatility and currency fluctuations. Previously, we managed this risk by entering into a zero cost collar in respect of our oil production at certain of our businesses.

While we believe that this hedging strategy has been appropriate in the past, there are other risk mitigation measures, such as cost containment, working capital management, cash conservation and capital prioritisation to consider in conjunction with this strategy and which have already resulted in the strengthening of our balance sheet. For the 2013 financial year, we did not hedge as in the past, as we did not consider there to have been value in the zero cost collars available in the market at this time. The situation is monitored regularly to assess when a suitable time might be to enter into an appropriate hedge again in the future.

In determining the crude oil price for budgeting purposes we review global growth trends in the demand and consumption for oil, global production and supply as well as the marginal cost of production. Global oil markets continue to be affected by oil production exceeding oil consumption during the financial year. On the demand side, 2013 has been characterised by lower than expected growth rates in the global economy, resulting in lower demand for oil. Growth rates in the second half of the 2013 calendar year are expected to be slightly higher than what we have currently seen, due to some anticipated economic recovery in the US, euro zone and some major emerging markets. While these growth rates are expected to continue, the risk of setbacks in these economies does however persist. Demand for oil products, in particular diesel, in the transportation and industrial sectors are expected to support the global oil demand. It is anticipated that demand for crude oil will further increase on the back of structural changes in the seasonal pattern for fuels. The substitution of natural gas for conventional winter fuels is influencing this trend.

chief financial officer’s review continued

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

7

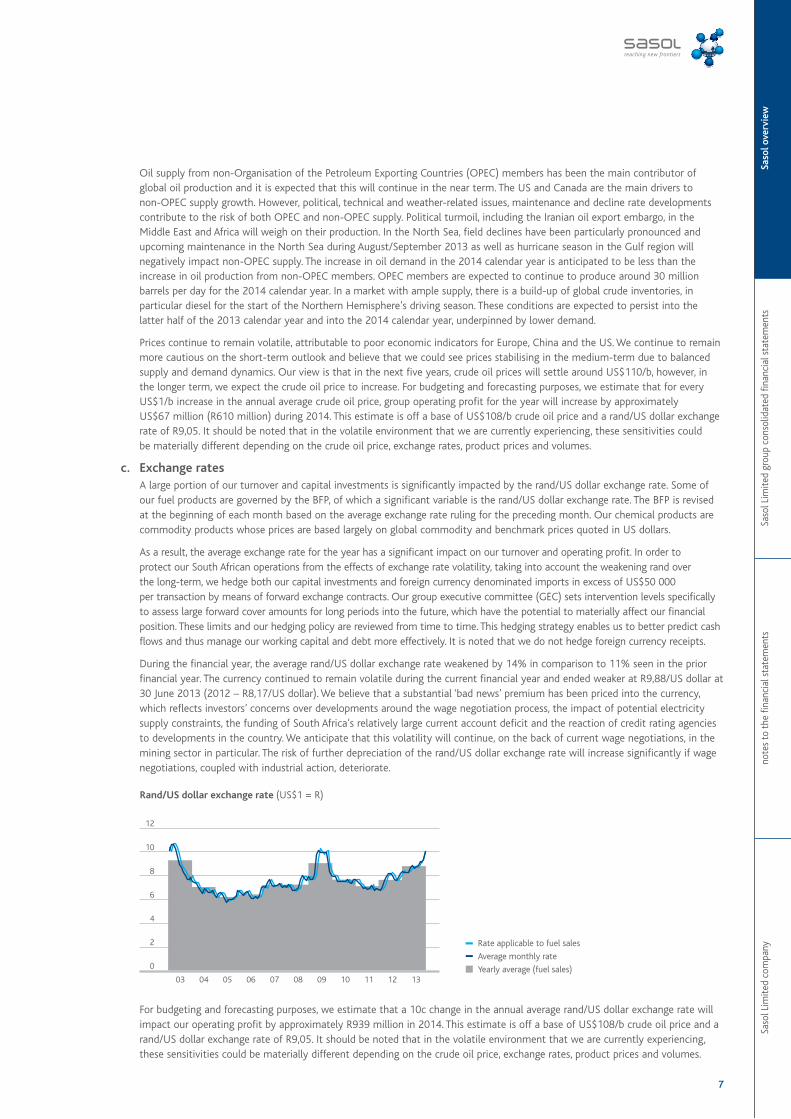

Oil supply from non-Organisation of the Petroleum Exporting Countries (OPEC) members has been the main contributor of global oil production and it is expected that this will continue in the near term. The US and Canada are the main drivers to non-OPEC supply growth. However, political, technical and weather-related issues, maintenance and decline rate developments contribute to the risk of both OPEC and non-OPEC supply. Political turmoil, including the Iranian oil export embargo, in the Middle East and Africa will weigh on their production. In the North Sea, field declines have been particularly pronounced and upcoming maintenance in the North Sea during August/September 2013 as well as hurricane season in the Gulf region will negatively impact non-OPEC supply. The increase in oil demand in the 2014 calendar year is anticipated to be less than the increase in oil production from non-OPEC members. OPEC members are expected to continue to produce around 30 million barrels per day for the 2014 calendar year. In a market with ample supply, there is a build-up of global crude inventories, in particular diesel for the start of the Northern Hemisphere’s driving season. These conditions are expected to persist into the latter half of the 2013 calendar year and into the 2014 calendar year, underpinned by lower demand.

Prices continue to remain volatile, attributable to poor economic indicators for Europe, China and the US. We continue to remain more cautious on the short-term outlook and believe that we could see prices stabilising in the medium-term due to balanced supply and demand dynamics. Our view is that in the next five years, crude oil prices will settle around US$110/b, however, in the longer term, we expect the crude oil price to increase. For budgeting and forecasting purposes, we estimate that for every US$1/b increase in the annual average crude oil price, group operating profit for the year will increase by approximately US$67 million (R610 million) during 2014. This estimate is off a base of US$108/b crude oil price and a rand/US dollar exchange rate of R9,05. It should be noted that in the volatile environment that we are currently experiencing, these sensitivities could be materially different depending on the crude oil price, exchange rates, product prices and volumes.

c. Exchange rates A large portion of our turnover and capital investments is significantly impacted by the rand/US dollar exchange rate. Some of

our fuel products are governed by the BFP, of which a significant variable is the rand/US dollar exchange rate. The BFP is revised at the beginning of each month based on the average exchange rate ruling for the preceding month. Our chemical products are commodity products whose prices are based largely on global commodity and benchmark prices quoted in US dollars.

As a result, the average exchange rate for the year has a significant impact on our turnover and operating profit. In order to protect our South African operations from the effects of exchange rate volatility, taking into account the weakening rand over the long-term, we hedge both our capital investments and foreign currency denominated imports in excess of US$50 000 per transaction by means of forward exchange contracts. Our group executive committee (GEC) sets intervention levels specifically to assess large forward cover amounts for long periods into the future, which have the potential to materially affect our financial position. These limits and our hedging policy are reviewed from time to time. This hedging strategy enables us to better predict cash flows and thus manage our working capital and debt more effectively. It is noted that we do not hedge foreign currency receipts.

During the financial year, the average rand/US dollar exchange rate weakened by 14% in comparison to 11% seen in the prior financial year. The currency continued to remain volatile during the current financial year and ended weaker at R9,88/US dollar at 30 June 2013 (2012 – R8,17/US dollar). We believe that a substantial ‘bad news’ premium has been priced into the currency, which reflects investors’ concerns over developments around the wage negotiation process, the impact of potential electricity supply constraints, the funding of South Africa’s relatively large current account deficit and the reaction of credit rating agencies to developments in the country. We anticipate that this volatility will continue, on the back of current wage negotiations, in the mining sector in particular. The risk of further depreciation of the rand/US dollar exchange rate will increase significantly if wage negotiations, coupled with industrial action, deteriorate.

For budgeting and forecasting purposes, we estimate that a 10c change in the annual average rand/US dollar exchange rate will impact our operating profit by approximately R939 million in 2014. This estimate is off a base of US$108/b crude oil price and a rand/US dollar exchange rate of R9,05. It should be noted that in the volatile environment that we are currently experiencing, these sensitivities could be materially different depending on the crude oil price, exchange rates, product prices and volumes.

8

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Sasol Limited group

d. Expansion of natural gas offering According to the International Energy Outlook 2013, issued by the US Energy Information Administration (EIA) in July 2013,

fossil fuels will continue to supply almost 80% of the world’s energy use through to 2040. Natural gas is the fastest growing fossil fuel, with global natural gas consumption increasing by 1,7% per year. The EIA further indicated that increasing supplies of tight gas, shale gas and coalbed methane support the projected growth in worldwide natural gas consumption. The US ranks third as one of the countries which will account for the largest increases in natural gas production from 2010 to 2040. With this rapid growth of US production, coupled with mounting climate change pressure, the increasing use of natural gas as transportation fuel in the US and elsewhere, bodes well for Sasol’s growth aspirations in North America. Natural gas is an attractive fuel alternative in the industrial and electricity industries, because of its lower carbon intensity compared to coal and oil. The substitution of traditional fuels like oil-based diesel, for fuels derived from natural gas, provides a solid business case for our gas-to-liquids (GTL) investment proposition.

Our 2011 investment in the Canadian shale gas assets, situated in the Montney Basin, supports our strategy to deliver fuel alternatives in support of lowering our carbon dioxide (CO2) emissions. The strong growth outlook for natural gas, especially in the US, Canada and China, coupled with developments in technology, is making shale gas economical worldwide. However, new gas ventures involve risks – while our Canadian shale gas assets are not producing as planned, we do foresee that production will improve in the future once gas prices trigger further economic development, coupled with our final investment decision in respect of our 96 000 barrels per day GTL facility in the US. We anticipate that our shale gas assets will act as a natural price hedge for the feedstock of our GTL project, providing a cover on the price of gas of approximately two-thirds.

Current gas prices in North America remain depressed, however we have seen some improvement in the price over the financial year. The spot natural gas price for the US benchmark (Henry Hub) improved to US$3,57/million metric British thermal units (mmbtu) at 30 June 2013, compared to US$2,74/mmbtu at 30 June 2012.

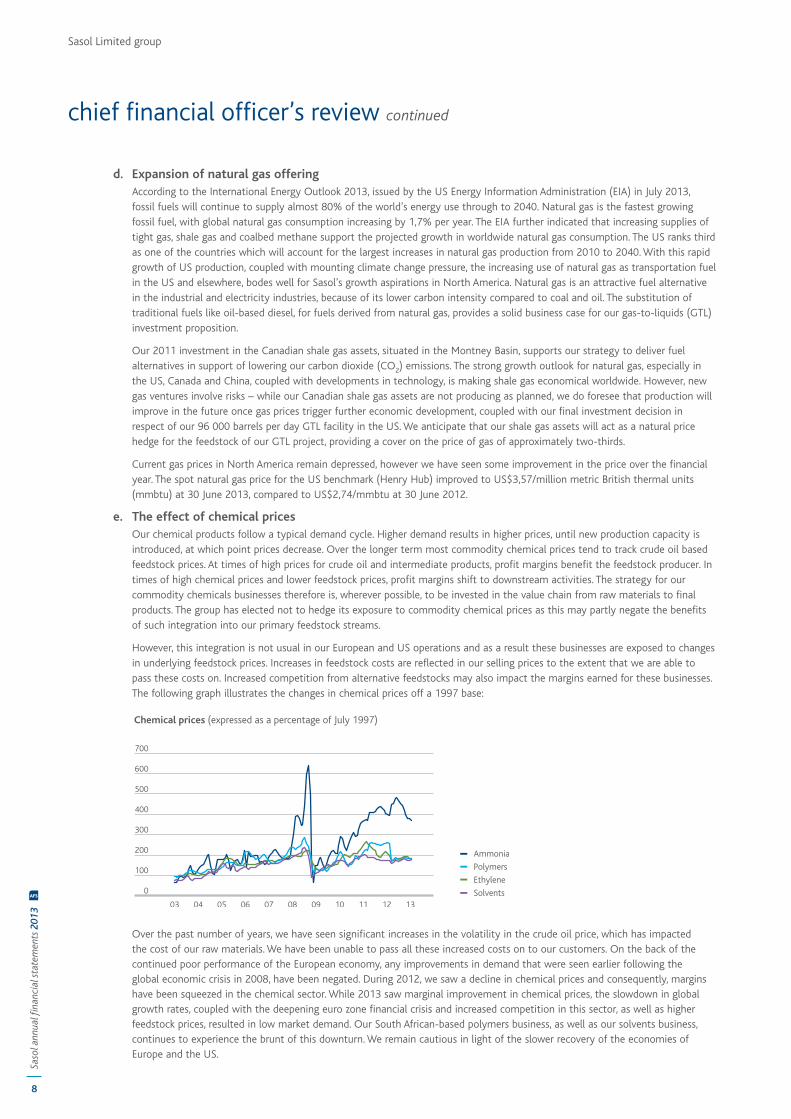

e. The effect of chemical prices Our chemical products follow a typical demand cycle. Higher demand results in higher prices, until new production capacity is

introduced, at which point prices decrease. Over the longer term most commodity chemical prices tend to track crude oil based feedstock prices. At times of high prices for crude oil and intermediate products, profit margins benefit the feedstock producer. In times of high chemical prices and lower feedstock prices, profit margins shift to downstream activities. The strategy for our commodity chemicals businesses therefore is, wherever possible, to be invested in the value chain from raw materials to final products. The group has elected not to hedge its exposure to commodity chemical prices as this may partly negate the benefits of such integration into our primary feedstock streams.

However, this integration is not usual in our European and US operations and as a result these businesses are exposed to changes in underlying feedstock prices. Increases in feedstock costs are reflected in our selling prices to the extent that we are able to pass these costs on. Increased competition from alternative feedstocks may also impact the margins earned for these businesses. The following graph illustrates the changes in chemical prices off a 1997 base:

Over the past number of years, we have seen significant increases in the volatility in the crude oil price, which has impacted the cost of our raw materials. We have been unable to pass all these increased costs on to our customers. On the back of the continued poor performance of the European economy, any improvements in demand that were seen earlier following the global economic crisis in 2008, have been negated. During 2012, we saw a decline in chemical prices and consequently, margins have been squeezed in the chemical sector. While 2013 saw marginal improvement in chemical prices, the slowdown in global growth rates, coupled with the deepening euro zone financial crisis and increased competition in this sector, as well as higher feedstock prices, resulted in low market demand. Our South African-based polymers business, as well as our solvents business, continues to experience the brunt of this downturn. We remain cautious in light of the slower recovery of the economies of Europe and the US.

chief financial officer’s review continued

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

9

f. Delivering on capital projects Our industry is a long-term business in which most of our operations, including the gasification of coal and the manufacture

of synfuels and petrochemical products, are highly dependent upon the development and use of advanced technologies. The decisions affecting our business are made with a time horizon that is measured with a long-term view and span multiple and diverse business cycles. These decisions are in support of expanding and delivering on our growth aspirations in support of our creating shareholder value sustainably. To ensure that we capitalise on the right opportunities, it is an imperative that we focus on those opportunities in the right geographic regions and deliver on those projects within planned timelines. A number of our expansion projects are integrated across a number of our businesses, such as the development of our North American operations, and span a number of our chemical and international energy businesses. Understanding these opportunities provides clarity and is critical in allowing us to deliver on a vital portion of our growth aspirations.

We also need to ensure the stability and reliability of our foundation businesses and that we maintain our operations throughout the world. This requires capital investments to sustain our operations. We monitor our capital investment programme on a continuous basis to ensure that capital is employed effectively from the translation of our strategy into portfolios of delivered projects, which are beneficial to the long-term growth of the group.

Our capital investments are tested through a range of economic scenarios to ensure that risks are appropriately identified, evaluated and managed. This approach ensures that our technologies are developed, commercialised and integrated so that the competitiveness of our products, the continuity of our operations, our feedstock requirements, capacity and efficiency of our production is assured. Emphasis is placed on the selection of effective projects, whose execution will deliver maximum return and asset value for our stakeholders. In selecting these projects, reference is made to our hurdle rate, being 1,3 times the Sasol’s weighted average cost of capital (WACC). In determining our WACC rate, the methodology applied is consistent with global best practice and includes adjustments to take into account country specific risk. Industry differentiation has not been implemented in our WACC methodology due to the integrated nature of the Sasol group. The bond rates and country risk premiums were reviewed and due to the current global market volatility, there is uncertainty that these rates will be sustainable in the long term, therefore the WACC rates for the current year have remained unchanged. Refer to section 7 of this report for details on our capital allocation.

g. Impacts on our cost base Our sustainability and competitiveness depend on our ability to optimise our operating cost base. As we are unable to control

the market price at which the products we produce are sold, it is possible that if inflation in countries in which we operate should begin to increase, it may result in significantly higher future operational costs. Generally, we have seen that the rate of inflation in most major countries in which we operate has been relatively low in recent years. In South Africa, inflation has declined from its highs of 13,8% in August 2008 to lows of 3,2% in September 2010. The weakening rand/US dollar exchange rate remains the greatest impact on inflation. This together with potential labour and electricity cost increases in excess of the South African Reserve Bank (SARB) target range for inflation of 3% to 6%, adds further to inflation risk, placing further pressure on our operating costs. We anticipate that consumer price index (CPI) inflation in South Africa will remain within this range, with the 2013 average CPI inflation rate just within this range at 5,5%. Refer to point 5c for additional information.

We continued to maintain strict cost discipline across the group in 2013, and made further progress on our initiatives, that were implemented in previous years. These initiatives included our shared services structures, asset optimisation and a continued focus on our supply chain process seeking economies of scale in procurement. Part of these initiatives included the commissioning of a 140 megawatts electricity generation plant in Sasolburg, South Africa, during December 2012. This plant will assist with the reduction of our energy costs. We continue to leverage off efficiency and productivity improvements to counter the effects of increased cost trends. However, we realise that in order to move forward with our growth aspirations, further cost optimisation is required. To this end we have initiated a cost optimisation programme, refer to section 11 for additional information.

h. Impairments and reversals of impairments While in the past two years, we have seen signs of global economic recovery, risks including the euro zone crisis, US fiscal policy

and the Chinese ‘hard landing’, continue to persist. As a result, we reassessed the impairment reviews conducted previously on our cash generating units. Based on these assessments, for the year under review, we have evaluated whether the carrying value of our assets are recoverable. In assessing these economic valuations, current market conditions, our latest budgets and the life cycle of the various products are taken into consideration. While the actual outcomes may differ significantly from our forecasts, thus affecting our assessment of future cash flows, management has applied their judgement in making these assessments based on the best information available at the time. In addition, the outcomes have been tested against a range of economic scenarios particular to the circumstances of the business concerned. Further, where these outcomes have indicated that the previously recognised impairments should be reversed due to the economic recovery, management has tested these reversals to ensure that the circumstances indicated, are sustainable based on the current information available.

As a result, net impairments of R5 995 million have been recognised for the year ended 30 June 2013, primarily related to the divestiture of our investment in Arya Sasol Polymer Company (ASPC) and Sasol Wax’s FT wax expansion project. At 30 June 2013, the investment in ASPC is classified as a disposal group held-for-sale. The devaluation of the Iranian currency negatively impacted our earnings, coupled with the deteriorating Iranian environment and the accounting requirement to recognise operating profits which may not be recuperated through the divestiture process and disposal value. Accordingly, we recognised a partial impairment of R3 611 million at 30 June 2013. On 16 August 2013, we entered into a definitive sale and share purchase

10

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Sasol Limited group

agreement to dispose of our 50% interest in ASPC for a purchase consideration of R3 606 million (US$365 million). The purchase consideration is payable in cash for the net assets, dividends and shareholder loans. As a result of this transaction, Sasol has no ongoing investment in Iran. We are currently assessing the impact of the change in the official Iranian Rial exchange rate applicable from the 2014 financial year. This change may result in a loss on disposal of less than US$100 million. The FT wax expansion project is a highly-complex brownfield mega-project, being executed in a volatile macroeconomic and labour constrained environment, where construction delays and poor productivity are being experienced. Accordingly, some uncertainty on the schedule and costs remain. As a consequence, we reassessed the economics of the project and recognised a partial impairment of R2 033 million at 30 June 2013.

In addition, we recognised R442 million in respect of the write-off of an unsuccessful exploration well, Mupeji-1, in Mozambique.

With regards to those assets which we had previously impaired we reassessed those factors impacting the carrying value of these assets. In particular, we reviewed our participation in the Escravos gas-to-liquids (EGTL) project in Nigeria. In 2011, we recognised a partial impairment of our investment in EGTL of R123 million. Based on continuing uncertainties in the Nigerian environment as well as various project risks, the partial impairment has not been reversed in 2013. We further reviewed our Canadian shale gas assets which were partially impaired in 2012 by R964 million. The value in use is particularly sensitive to changes in the gas price, the estimated ultimate recovery factor as well as changes in drilling and completion costs. Based on our review of the shale gas assets, taking into account the development of the natural gas price and the development of the gas field, the partial impairment has not been reversed in 2013.

i. Credit management focus Although economies are showing signs of recovery, the effects of the global economic crisis continue to linger, especially in

Europe which faced a deepening financial crisis in 2012. As uncertain economic times persist, a significant burden is placed on our customers. Management can therefore not ignore the risk that this continues to present to the group. We remain focused on our credit management process to ensure that our exposure to those customers faced with the negative impacts of declining economies remains within acceptable limits. The exposure of our receivables is reviewed across the group, through a centrally co-ordinated credit committee, which undertakes an oversight role to ensure that our group-wide exposure is limited in these uncertain times. Credit management of the receivables remains the responsibility of the individual business units. This focused risk approach continues to stand us in good stead, resulting in insignificant bad debt write-offs in the current economic climate.

j. Net realisable value write downs in inventory The continued financial crisis in the euro zone as well as lower than expected global economic growth, have resulted in softer

demand in certain markets and in certain economies. We continue to take mitigating actions, where appropriate, to eliminate some of this volatility through decreasing production at certain of our plants, especially in Europe, however, our inventory holding across the group is at higher levels than those of the previous year. The weaker demand for product has been coupled with improved prices during the year. Lower average crude oil effects coupled with a weaker rand/US dollar exchange rate and the higher inventory levels, resulted in net realisable value write downs of R234 million during the financial year compared to R331 million in the previous financial year.

k. Delivering sustainable results Managing the social, economic and environmental impacts of our business in a sustainable manner is key to delivering long-term

success. It is also essential that we work on strengthening relationships with all of our key stakeholders. Strong relationships are crucial to delivering on our future aspirations – we need to be attuned to our customers, our business partners and the governments of the countries in which we operate. We also need to ensure that the way in which we carry out our business is sustainable in the longer term, and that this way of thinking is reflected in our daily activities. In addition to our focus on ‘zero harm’ as part of our approach towards safety, we face substantial challenges around climate change and other environmental impacts, including water usage at our South African operations.

In 2011, the South African government approved its National Climate Change Response White Paper, and followed this up by commissioning a greenhouse gas (GHG) mitigation potential study and by releasing a discussion document on carbon tax during 2013. The aim of these activities is to understand the opportunities and policies required to reduce the country’s GHG emissions, in line with the commitments made under the UN Framework Convention on Climate Change. We are continuing to engage with the government to allow a mutual understanding of the opportunities for GHG mitigation, and the impact of policies in this area on our business. We are continuing to seek solutions to the challenges of reducing our GHG emissions, particularly in South Africa. Any solutions also need to be acceptable to our investors and other stakeholders, while at the same time allowing us to contribute towards the economic development and energy security of the countries in which we operate.

Around 25% of Sasol’s emissions in South Africa arise from the generation of electricity, either directly in our own operations or indirectly from imported electricity. Our short-to-medium-term focus is on the generation of lower-carbon electricity from natural gas, which also allows us to assist in alleviating the electricity supply shortfall in South Africa. In December 2012, the R1,4 billion Sasolburg Gas Engine Power Plant started up, allowing us to generate 140 MW of electricity. This project was completed ahead of schedule, and below the initially approved budget. A similar project, Central Termica de Ressano Garcia has been established with Electricidade de Moçambique holding a 51% share and Sasol 49%, and is currently under construction in Mozambique, and scheduled for completion in the 2014 financial year.

chief financial officer’s review continued

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

11

We are also investigating the opportunities for carbon capture and storage, as this forms part of the basket of options under consideration for our long-term GHG mitigation plans. As part of these plans, during 2011 we took up a 2,44% share in the CO2 Technology Centre Mongstad in Norway, which is a collaboration of energy industry players and the Norwegian state aimed at improving the understanding of and gaining operational experience of large-scale carbon capture processes. This facility started up during the year, and has allowed its owners to better understand the risks and opportunities associated with this technology.

l. Credit market risk and its impact on our debt profile Indications by the US Federal Reserve that it may start to reduce the amount of monthly bond purchases as part of its QE

programme prompted a sharp increase in bond yields globally. As a result, the cost of funding for corporates in the debt capital markets also increased sharply. A similar US dollar bond to that which the company issued in November 2012 is likely to attract a 100 basis points higher coupon today.

Conditions in the syndicated loan markets continue to improve, particularly for shorter-term tenures. It is, however, becoming increasingly clear that the new Basel 3 regulations will significantly hamper banks’ abilities to provide term funding over longer tenures, and the cost of long-term funding will become more expensive.

In anticipation of the significant planned capital investments and full project pipeline, our funding requirements are monitored on a continuous basis as part of our enterprise risk management activities and ensuring that appropriate levels of liquidity is maintained.

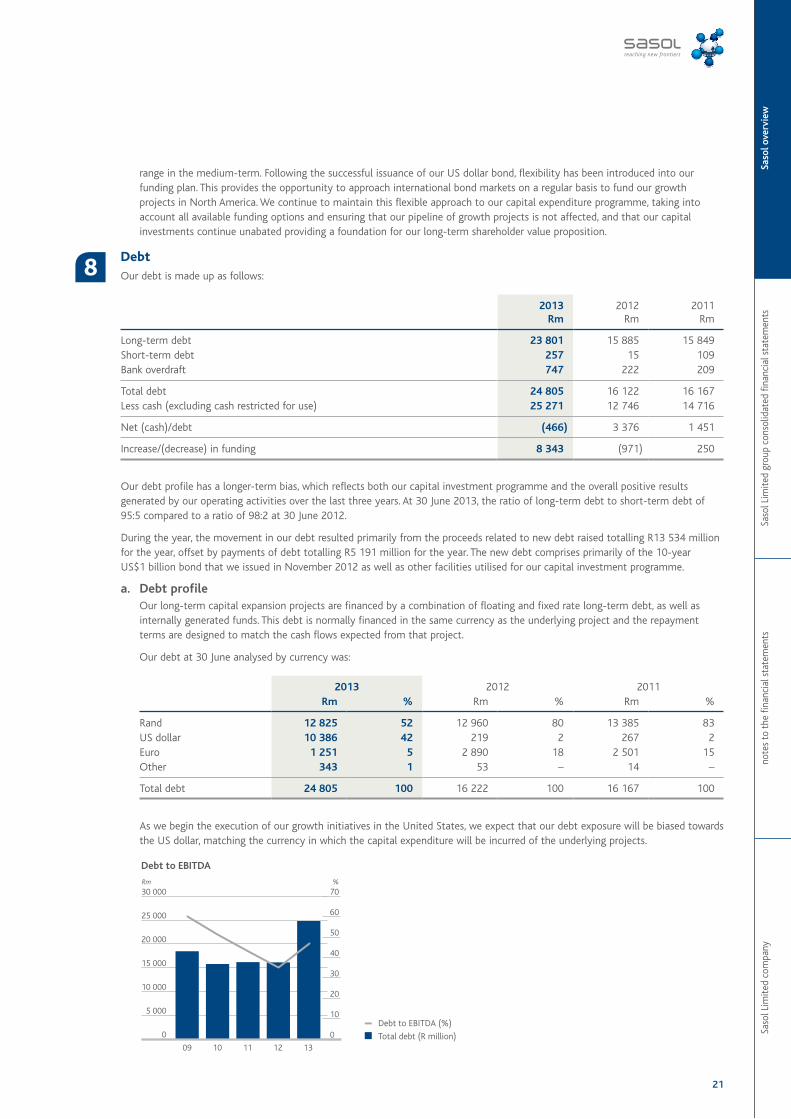

To this end, Sasol issued a US$1 billion corporate bond in November 2012. The bond, with a tenure of 10 years and a fixed coupon rate of 4,5% per annum, was oversubscribed by 3,47 times. The coupon rate is the lowest ever achieved by a South African non-state owned enterprise. This reflects the confidence that investors have in our company and in our ability to deliver value. This corporate bond provides long-term funding to balance the abundant short-term liquidity available to the group. The latter includes our R8 billion commercial paper programme, a revolving credit facility and several committed bank credit lines. Appropriate liquidity and committed funding facilities are also an essential part of retaining Sasol’s investment grade rating.

3 Financial performance

We measure our financial performance in terms of various financial ratios. These ratios relate to a number of performance areas, including managing our margins, cash, gearing and return on equity and are provided below for the year under review:

12

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Sasol Limited group

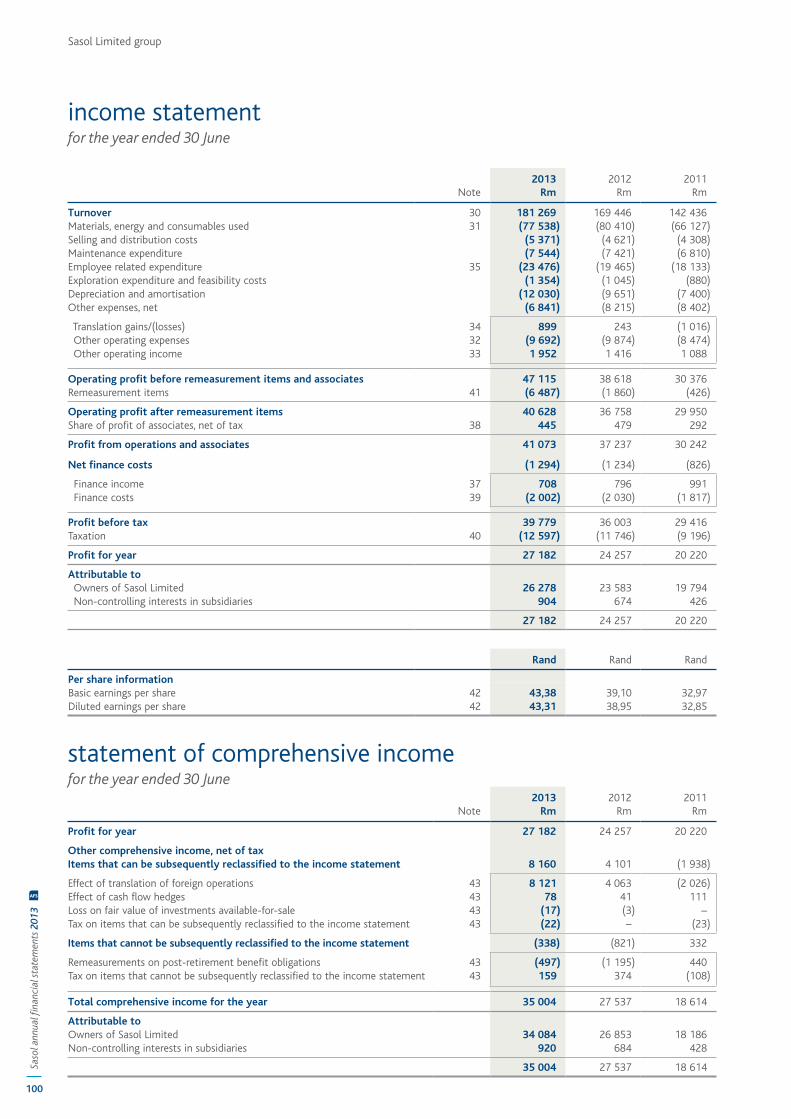

Earnings attributable to shareholders for the year ended 30 June 2013 increased by 11% to R26,3 billion from R23,6 billion in the prior year. Headline earnings per share increased by 25% to R52,62 and earnings per share increased by 11% to R43,38, over the same period.

Sasol recorded an operating profit, excluding share of profit of associates, of R40,6 billion for the year. Excluding the impact of net once-off charges, amounting to R8,5 billion, operating profit increased by 26% compared with the prior year, on the back of an overall improved operational performance. Operating profit was boosted by a 14% weaker average rand/US dollar exchange rate (R8,85/US$ at 30 June 2013 compared with R7,78/US$ at 30 June 2012), despite a 3% lower average Brent crude oil price (average dated Brent was US$108,66/b at 30 June 2013 compared with US$112,42/b at 30 June 2012) and lower product prices.

The operating profit in the current year was negatively impacted by net once-off charges totalling R8,5 billion (30 June 2012 – R2,1 billion). These items relate primarily to the partial impairments of our ASPC investment and the FT wax expansion project of R3 611 million and R2 033 million, respectively, as well as the write-off of an unsuccessful exploration well in Mozambique amounting to R442 million. In addition, included in the once-off charges is an amount of R2 021 million related to translation losses, primarily at our ASPC operations, resulting from the depreciation of the Iranian Rial against the US dollar. These once-off items also include a gain of R233 million relating to the remeasurement to fair value of our existing shareholding in the Merisol business, which arose from the acquisition of the remaining 50% of Merisol. Our operating profit further includes a gain on the valuation of our open Canadian foreign exchange contracts amounting to R439 million.

Operating profit for the second half of the year, compared to the first half of the year, was R2,8 billion higher mainly as a result of the weaker rand/US dollar exchange rate, partly offset by the further impairment of ASPC and the partial impairment of the FT wax expansion project. In addition, translation gains, year-end stock movements as well as the positive impact of the change in discount rates on our provision for environmental rehabilitation contributed further to the higher operating profit.

Sasol Synfuels delivered production volumes for the year of 7,443 million tons (mt), which was 4% higher than the prior year. Stable operations, as well as the performance of the running plant during the phased shutdown resulted in the improved production volumes. These are the highest production volumes delivered by Sasol Synfuels since the 2006 financial year, post Clean Fuels 1 implementation. We continue to optimise our European chemical businesses’ production to match lower demand and optimise margins in light of the continuing weak European market conditions. Production performance at our ORYX GTL operations was in line with our expectations, taking into account the planned maintenance shutdown in February 2013. ASPC achieved a utilisation rate of 80% in line with our production expectations.

Cash fixed costs, excluding once-off and growth costs and the impact of a weaker exchange rate, increased by 7% in real terms, primarily due to a challenging South African cost environment in respect of labour, maintenance and electricity costs. Our current cost inflation is above the indicative South African producers’ price index inflation trends of 6,0% for the 2013 financial year. We are actively looking at opportunities to reduce and contain our cost base sustainably.

The effective tax rate of 31,7% is lower than the prior year’s effective tax rate of 32,6%. This resulted primarily from an increase in non-deductible expenses relating mainly to once-off charges, which was offset by the absence of Secondary Tax on Companies, due to the implementation of dividend withholding tax, as well as the increase in exempt income.

Cash flow generated by operating activities increased by 24% to R59,3 billion compared with R47,9 billion in the prior year. However, this was offset by increased working capital, both as a result of price and volume effects. Capital investments for the year amounted to R32,3 billion.

chief financial officer’s review continued

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

13

4 Effect of significant changes in accounting principles

During the 2013 financial year, we adopted three new accounting standards as set out in our accounting policies. These newly adopted standards did not significantly impact our financial results. In addition, we changed the presentation of our income statement for the 2013 financial year. In terms of International Financial Reporting Standards (IFRS), the income statement can be presented by nature or by function. With effect from 1 July 2012, the group changed the presentation of its income statement from a classification based on function to a classification based on nature. Sasol has elected to change its income statement presentation to better reflect how it effectively manages its business as well as align to peers. The comparative periods presented have been restated to comply with the income statement classification by nature. The change in the income statement presentation did not have an impact on turnover, operating profit or earnings per share. Refer to note 1 of the consolidated annual financial statements.

During the 2014 financial year, we will be adopting the consolidation suite of accounting standards, including IFRS 10 Consolidated Financial Statements, IFRS 11 Joint Arrangements and IFRS 12, Disclosure of Interests in Other Entities. The adoption of the consolidation suite of standards is not expected to have a significant impact on total assets, total liabilities, equity, earnings and earnings per share.

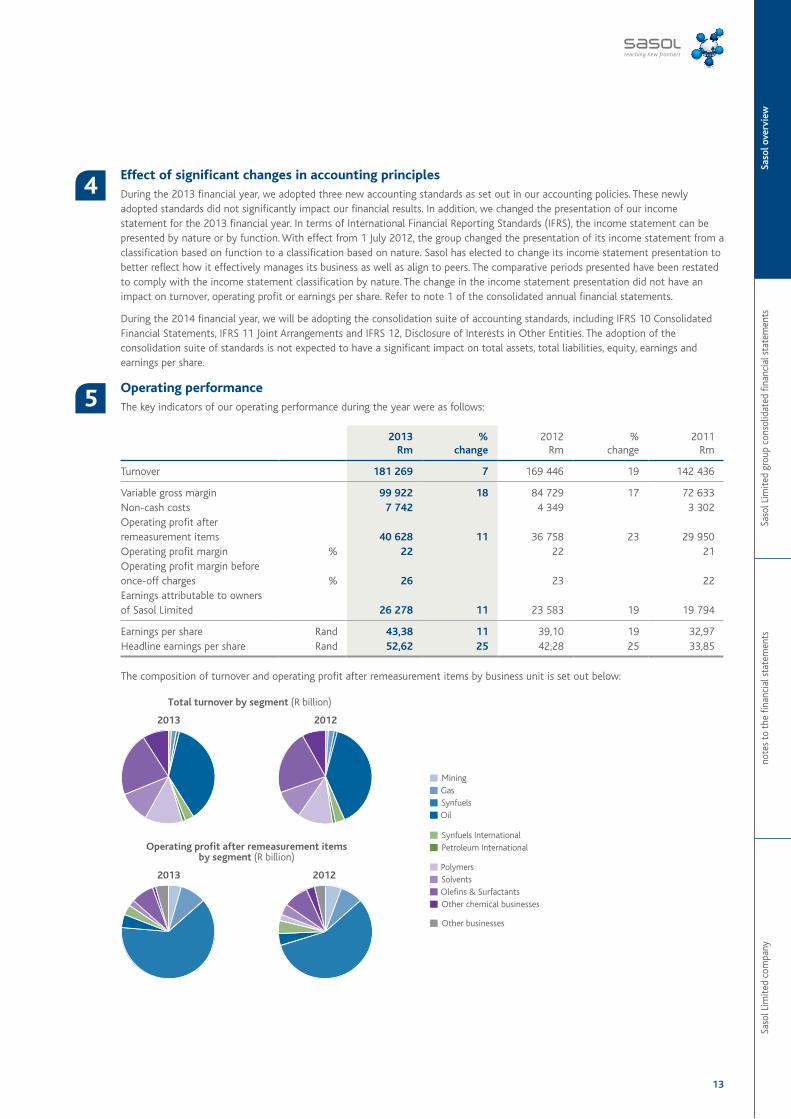

5 Operating performance

The key indicators of our operating performance during the year were as follows:

2013Rm

%change

2012Rm

%change

2011Rm

Turnover 181 269 7 169 446 19 142 436

Variable gross margin 99 922 18 84 729 17 72 633Non-cash costs 7 742 4 349 3 302Operating profit after remeasurement items 40 628 11 36 758 23 29 950Operating profit margin % 22 22 21Operating profit margin before once-off charges % 26 23 22Earnings attributable to owners of Sasol Limited 26 278 11 23 583 19 19 794

Earnings per share Rand 43,38 11 39,10 19 32,97Headline earnings per share Rand 52,62 25 42,28 25 33,85

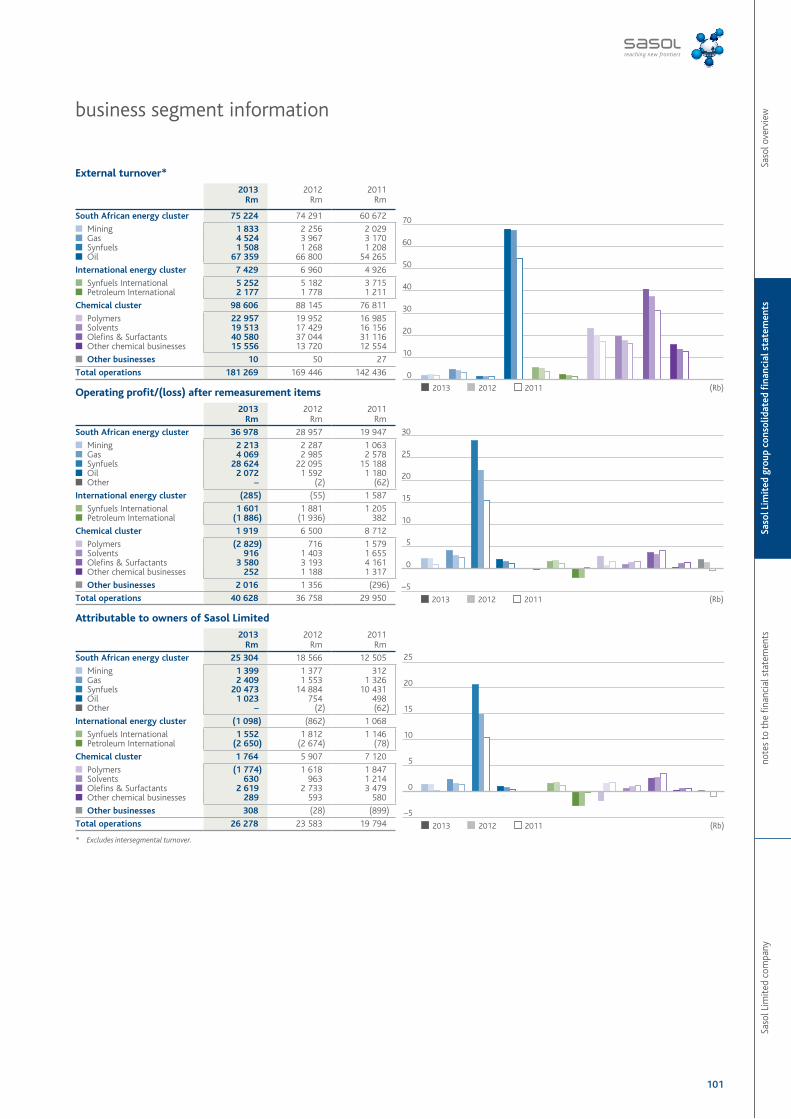

The composition of turnover and operating profit after remeasurement items by business unit is set out below:

14

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Sasol Limited group

a. Trend analysis Turnover has increased by 7%, operating profit by 11% and earnings attributable to shareholders by 11% for this year. The higher

operating profit resulted mainly from improved operational performance and a 14% weaker average rand/US dollar exchange rate, despite a 3% lower average Brent crude oil price. Overall, the group benefitted from improved production performance, with the Sasol Synfuels’ production volumes increasing by 4% compared to the previous financial year. Our operating margin has been enhanced by the cost containment initiatives implemented over the last two years.

Our South African Energy cluster continues to produce solid results, contributing approximately 90% to group profitability in 2013. Compared to the prior year, operating profit increased by 28% to R36 978 million. Sasol Synfuels remained the largest contributor to the group operating profit, contributing over half of the total group operating profit, with an operating margin of 49%. The weaker rand/US dollar exchange rate contributed significantly to the operating profit in this cluster. These positive effects were partially offset by a lower average crude oil price and lower sales volumes at Sasol Oil resulting from an extended planned shutdown at the Natref refinery coupled with reduced trading activities. Our operations in this cluster were further negatively impacted by cost inflation, as well as higher labour and maintenance costs. Production volumes at Sasol Synfuels of 7,443 million tons were 4% higher than the prior year, due to stable operations, as well as the performance of the plant during the planned shut-down.

Our International Energy cluster reflected increased operating losses of R285 million compared to the prior year operating loss of R55 million. Our Sasol Synfuels International (SSI) growth portfolio continued to contribute positively to this cluster. However, SSI reflected a decrease in operating profit due to lower production at the ORYX GTL plant in Qatar, coupled with higher study costs for the US GTL project. A planned statutory shutdown, which commenced in February 2013 and was completed in April 2013, resulted in the lower production volumes at ORYX GTL. This shutdown enabled various key de-bottlenecking projects and has already resulted in operational benefits since start-up, underpinning average throughput consistently above design capacity of 32 400 barrels/day. This performance continues to endorse the commercial viability of our GTL technology.

However, the favourable results at SSI were offset by the operating loss at Sasol Petroleum International (SPI). Production volumes from our combined upstream assets in Mozambique, Canada and Gabon were 16% higher than the previous year. The prior year operating loss at SPI was impacted by the partial impairment related to our Canadian shale gas assets as well as the impairment of Blocks 16&19 in Mozambique and the dry well in Australia, totalling R1,7 billion. The current year has not seen further impairments of these assets, although we did write-off the Mupeji-1 dry well in Mozambique for R442 million. This positive impact has been offset by low gas market prices and higher depreciation at our Canadian operations, in addition to increased exploration costs. Our Canadian asset continues to be under pressure due to the low natural gas prices, coupled with higher than expected drilling and completion costs and sub-surface complexities. Our Canadian shale gas operations continue to contribute on an earnings before interest, tax, depreciation and amortisation basis.

The Chemical cluster was negatively affected by the ongoing European debt crisis, which reduced demand and continued to depress chemical prices. Sasol Olefins and Surfactants (Sasol O&S) remains a strong performer, contributing significantly to the total Chemical cluster’s operating profit of R1 919 million. Sasol O&S managed to maintain its gross margins, and saw improvement in some regions, despite some reductions in volumes. Difficult trading conditions continued to prevail for Sasol Solvents. Margins contracted on the back of continued higher feedstock prices and declining US dollar selling prices, despite higher sales volumes. Sasol Polymers recorded an operating loss of R2 829 million for the period. Although the South African polymer business reflected increases in both production and sales volumes, this increase was offset by the continued margin squeeze experienced in the South African polymers business, where feedstock price increases outweighed the increases in selling prices. ASPC has again performed well during this period and contributed positively to the Sasol Polymers’ business, excluding the partial impairment of our ASPC operations of R3,6 billion and translation losses of R2,0 billion relating to the depreciation of the Iranian Rial against the US dollar. ASPC achieved a capacity utilisation rate of 80% for the year. With effect from 16 August 2013, we disposed of our investment in ASPC for R3 606 million (US$365 million). The purchase consideration is payable in cash for the net assets, dividends and shareholder loans. Our other chemical businesses have performed well, in particular the ammonia

chief financial officer’s review continued

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

15

business housed in Sasol Infrachem. Sasol Wax’s operating profit, excluding the partial impairment of the FT wax expansion project of R2,1 billion, increased by 106% compared to the prior year, on a similar basis.

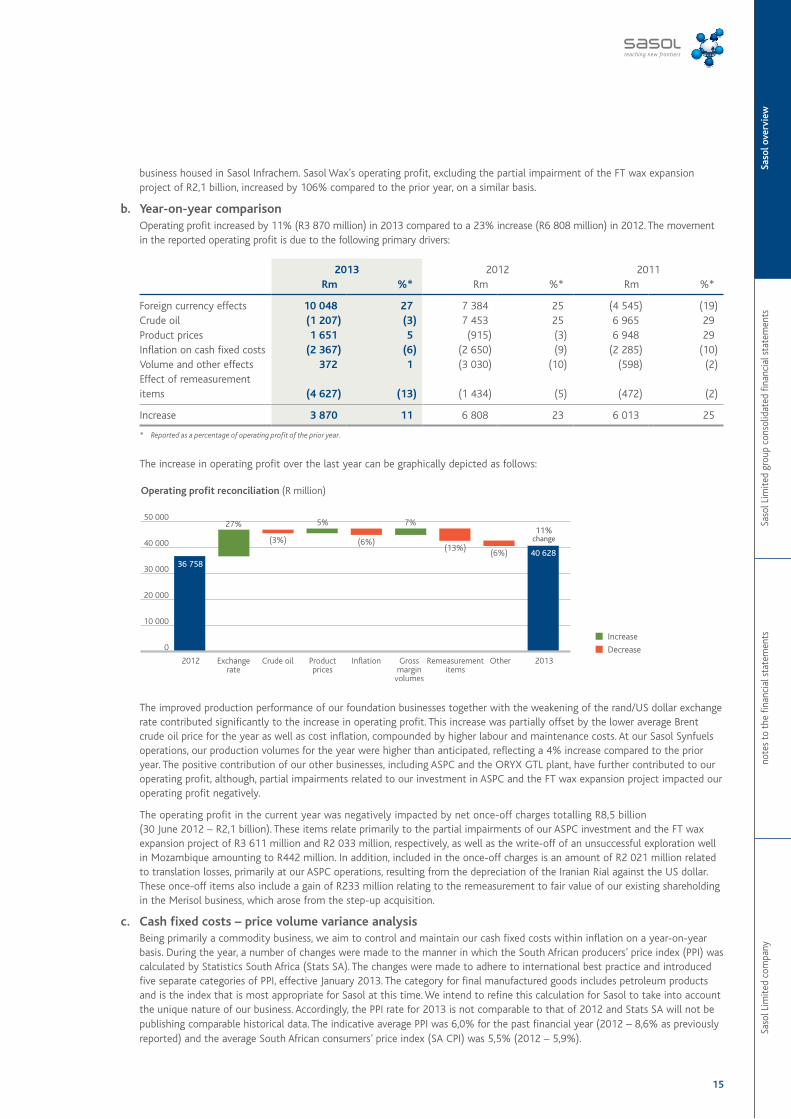

b. Year-on-year comparison Operating profit increased by 11% (R3 870 million) in 2013 compared to a 23% increase (R6 808 million) in 2012. The movement

in the reported operating profit is due to the following primary drivers:

2013 2012 2011Rm %* Rm %* Rm %*

Foreign currency effects 10 048 27 7 384 25 (4 545) (19)Crude oil (1 207) (3) 7 453 25 6 965 29Product prices 1 651 5 (915) (3) 6 948 29Inflation on cash fixed costs (2 367) (6) (2 650) (9) (2 285) (10)Volume and other effects 372 1 (3 030) (10) (598) (2)Effect of remeasurement items (4 627) (13) (1 434) (5) (472) (2)

Increase 3 870 11 6 808 23 6 013 25

* Reported as a percentage of operating profit of the prior year.

The increase in operating profit over the last year can be graphically depicted as follows:

The improved production performance of our foundation businesses together with the weakening of the rand/US dollar exchange rate contributed significantly to the increase in operating profit. This increase was partially offset by the lower average Brent crude oil price for the year as well as cost inflation, compounded by higher labour and maintenance costs. At our Sasol Synfuels operations, our production volumes for the year were higher than anticipated, reflecting a 4% increase compared to the prior year. The positive contribution of our other businesses, including ASPC and the ORYX GTL plant, have further contributed to our operating profit, although, partial impairments related to our investment in ASPC and the FT wax expansion project impacted our operating profit negatively.

The operating profit in the current year was negatively impacted by net once-off charges totalling R8,5 billion (30 June 2012 – R2,1 billion). These items relate primarily to the partial impairments of our ASPC investment and the FT wax expansion project of R3 611 million and R2 033 million, respectively, as well as the write-off of an unsuccessful exploration well in Mozambique amounting to R442 million. In addition, included in the once-off charges is an amount of R2 021 million related to translation losses, primarily at our ASPC operations, resulting from the depreciation of the Iranian Rial against the US dollar. These once-off items also include a gain of R233 million relating to the remeasurement to fair value of our existing shareholding in the Merisol business, which arose from the step-up acquisition.

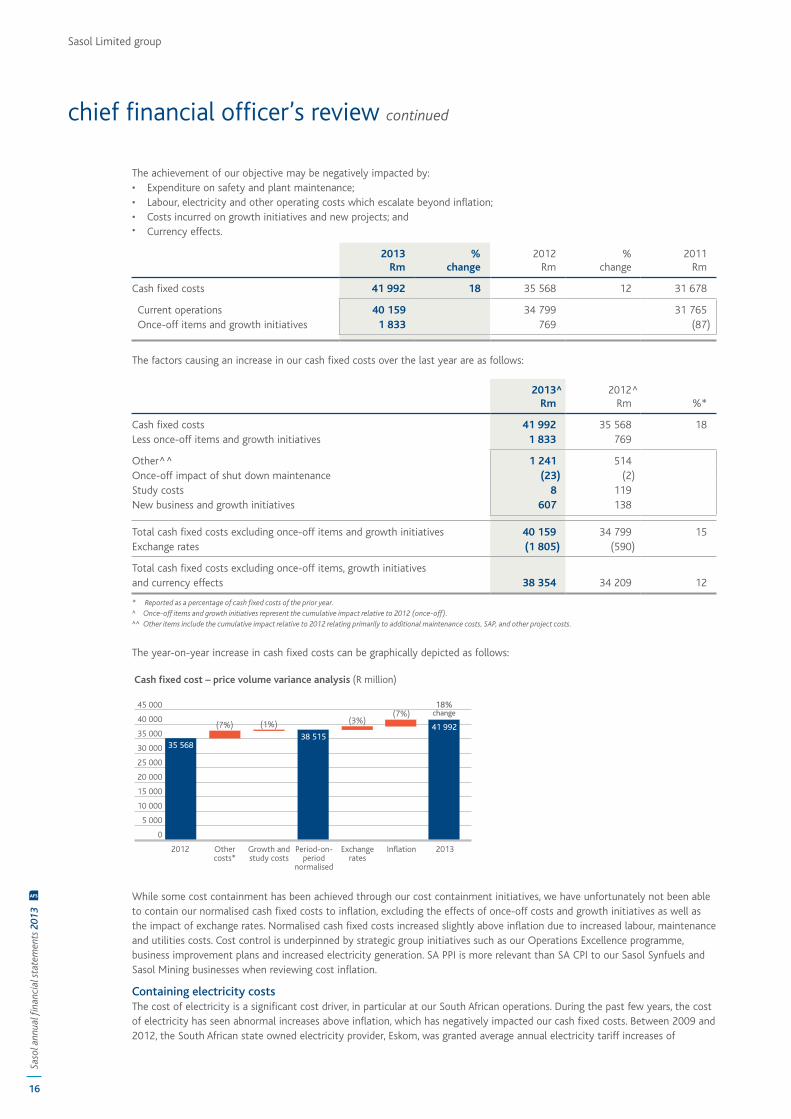

c. Cash fixed costs – price volume variance analysis Being primarily a commodity business, we aim to control and maintain our cash fixed costs within inflation on a year-on-year

basis. During the year, a number of changes were made to the manner in which the South African producers’ price index (PPI) was calculated by Statistics South Africa (Stats SA). The changes were made to adhere to international best practice and introduced five separate categories of PPI, effective January 2013. The category for final manufactured goods includes petroleum products and is the index that is most appropriate for Sasol at this time. We intend to refine this calculation for Sasol to take into account the unique nature of our business. Accordingly, the PPI rate for 2013 is not comparable to that of 2012 and Stats SA will not be publishing comparable historical data. The indicative average PPI was 6,0% for the past financial year (2012 – 8,6% as previously reported) and the average South African consumers’ price index (SA CPI) was 5,5% (2012 – 5,9%).

16

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Sasol Limited group

The achievement of our objective may be negatively impacted by: • Expenditure on safety and plant maintenance; • Labour, electricity and other operating costs which escalate beyond inflation; • Costs incurred on growth initiatives and new projects; and • Currency effects.

2013Rm

%change

2012Rm

%change

2011Rm

Cash fixed costs 41 992 18 35 568 12 31 678

Current operations 40 159 34 799 31 765 Once-off items and growth initiatives 1 833 769 (87)

The factors causing an increase in our cash fixed costs over the last year are as follows:

2013^Rm

2012^Rm %*

Cash fixed costs 41 992 35 568 18Less once-off items and growth initiatives 1 833 769

Other^^ 1 241 514Once-off impact of shut down maintenance (23) (2)Study costs 8 119New business and growth initiatives 607 138

Total cash fixed costs excluding once-off items and growth initiatives 40 159 34 799 15Exchange rates (1 805) (590)

Total cash fixed costs excluding once-off items, growth initiatives and currency effects 38 354 34 209 12

* Reported as a percentage of cash fixed costs of the prior year.^ Once-off items and growth initiatives represent the cumulative impact relative to 2012 (once-off).^^ Other items include the cumulative impact relative to 2012 relating primarily to additional maintenance costs, SAP, and other project costs.

The year-on-year increase in cash fixed costs can be graphically depicted as follows:

While some cost containment has been achieved through our cost containment initiatives, we have unfortunately not been able to contain our normalised cash fixed costs to inflation, excluding the effects of once-off costs and growth initiatives as well as the impact of exchange rates. Normalised cash fixed costs increased slightly above inflation due to increased labour, maintenance and utilities costs. Cost control is underpinned by strategic group initiatives such as our Operations Excellence programme, business improvement plans and increased electricity generation. SA PPI is more relevant than SA CPI to our Sasol Synfuels and Sasol Mining businesses when reviewing cost inflation.

Containing electricity costs The cost of electricity is a significant cost driver, in particular at our South African operations. During the past few years, the cost

of electricity has seen abnormal increases above inflation, which has negatively impacted our cash fixed costs. Between 2009 and 2012, the South African state owned electricity provider, Eskom, was granted average annual electricity tariff increases of

chief financial officer’s review continued

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

17

between 24,8% and 31,3%. In March 2012, the National Energy Regulator of South Africa (NERSA) announced that Eskom’s electricity tariffs will rise by about 16,0% in 2012/13 against an earlier published 26,0% increase. NERSA further confirmed in February 2013, that for the next five years commencing 2013/14, electricity increases would be contained to 8,0% per annum. These increases will continue to have a material adverse effect on our cash fixed costs in the future.

In order to contain the cost of electricity, we have continued to further our own electricity generation initiatives. In South Africa, we have the capacity to generate around 69% of our own electricity requirements. This was facilitated through the construction of the Sasolburg gas engine power plant. In addition, we have also installed power generation facilities at our German operations. We have been able to mitigate this risk to some extent by entering into a Power Purchase Agreement with Eskom following the construction of our power generation facility in Secunda in August 2011.

Managing our labour costs One of our most significant costs is labour. More than 60% of our employees are members of trade unions or works councils

covered by collective agreements entered into with these parties. In South Africa, we have concluded wage negotiations for 2014 for increases between 7,5% and 8,25%, of which increases in the different sectors are as follows: • Mining sector: An increase of 8,0%, effective 1 July 2013, with an additional service increment of 0,5%, effective

1 January 2014; • Chemicals sector: An increase of 7,5% effective 1 July 2013; and • Petroleum sector: A two year agreement was reached with an increase of 8,0%, effective 1 July 2012, and an increase,

effective 1 July 2013, of CPI plus 2,0%, with a guaranteed minimum of 7,0% and a capped maximum of 10,0%.

Our total employee costs, including share-based payment expenses, were R23,5 billion for the year compared to R19,5 billion in the previous year. The increase in labour costs is primarily due to average annual inflationary increases of 7%, increased share-based payment expenses related to the performance of the Sasol ordinary share price, an increase in employee benefit costs, an increase in employee numbers growth, as well as the effects of exchange rates. As part of our cost optimisation project, we are critically reviewing the operational and associated management structures in the group. We will be reviewing the impact on our functions in due course.

6 Cash flow analysis

2013Rm

2012Rm

%change

2011Rm

%change

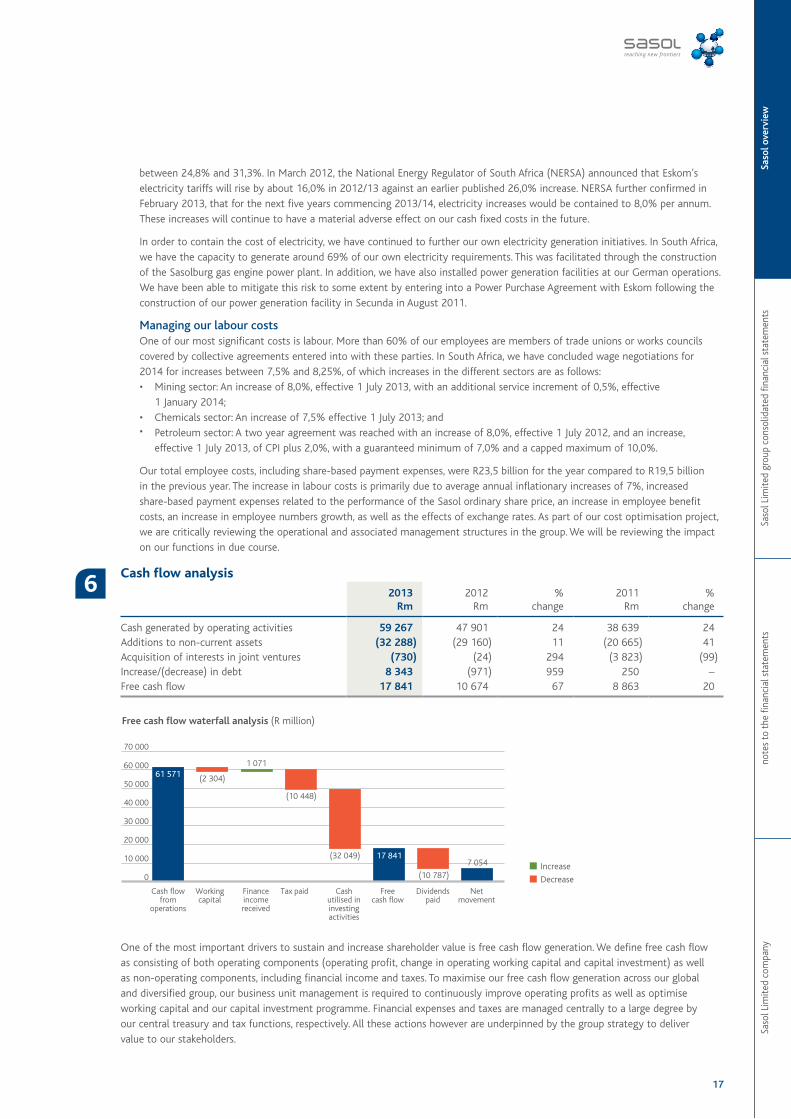

Cash generated by operating activities 59 267 47 901 24 38 639 24Additions to non-current assets (32 288) (29 160) 11 (20 665) 41Acquisition of interests in joint ventures (730) (24) 294 (3 823) (99)Increase/(decrease) in debt 8 343 (971) 959 250 –Free cash flow 17 841 10 674 67 8 863 20

One of the most important drivers to sustain and increase shareholder value is free cash flow generation. We define free cash flow as consisting of both operating components (operating profit, change in operating working capital and capital investment) as well as non-operating components, including financial income and taxes. To maximise our free cash flow generation across our global and diversified group, our business unit management is required to continuously improve operating profits as well as optimise working capital and our capital investment programme. Financial expenses and taxes are managed centrally to a large degree by our central treasury and tax functions, respectively. All these actions however are underpinned by the group strategy to deliver value to our stakeholders.

18

Saso

l ann

ual fi

nanc

ial s

tate

men

ts 2

013

AFS

Sasol Limited group

We firstly apply cash generated from operating activities to repay our debt and tax commitments and then provide a return to our shareholders in the form of dividends. Remaining cash is used to fund our capital investment programme. Any shortfall in the funding of our capital investment programme will be funded from borrowings. As a result, this will impact our gearing ratio. We have the authority to repurchase up to 10% of our issued share capital, should we decide to proceed with our share repurchase programme.

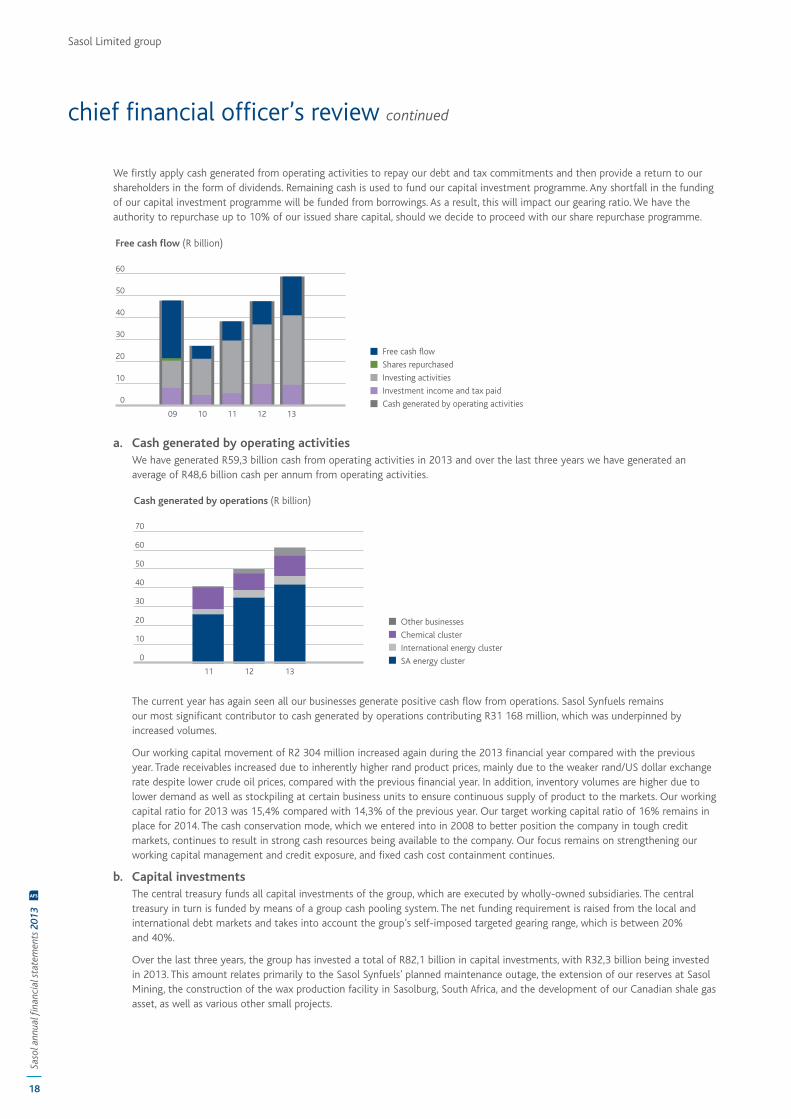

a. Cash generated by operating activities We have generated R59,3 billion cash from operating activities in 2013 and over the last three years we have generated an

average of R48,6 billion cash per annum from operating activities.

The current year has again seen all our businesses generate positive cash flow from operations. Sasol Synfuels remains our most significant contributor to cash generated by operations contributing R31 168 million, which was underpinned by increased volumes.

Our working capital movement of R2 304 million increased again during the 2013 financial year compared with the previous year. Trade receivables increased due to inherently higher rand product prices, mainly due to the weaker rand/US dollar exchange rate despite lower crude oil prices, compared with the previous financial year. In addition, inventory volumes are higher due to lower demand as well as stockpiling at certain business units to ensure continuous supply of product to the markets. Our working capital ratio for 2013 was 15,4% compared with 14,3% of the previous year. Our target working capital ratio of 16% remains in place for 2014. The cash conservation mode, which we entered into in 2008 to better position the company in tough credit markets, continues to result in strong cash resources being available to the company. Our focus remains on strengthening our working capital management and credit exposure, and fixed cash cost containment continues.

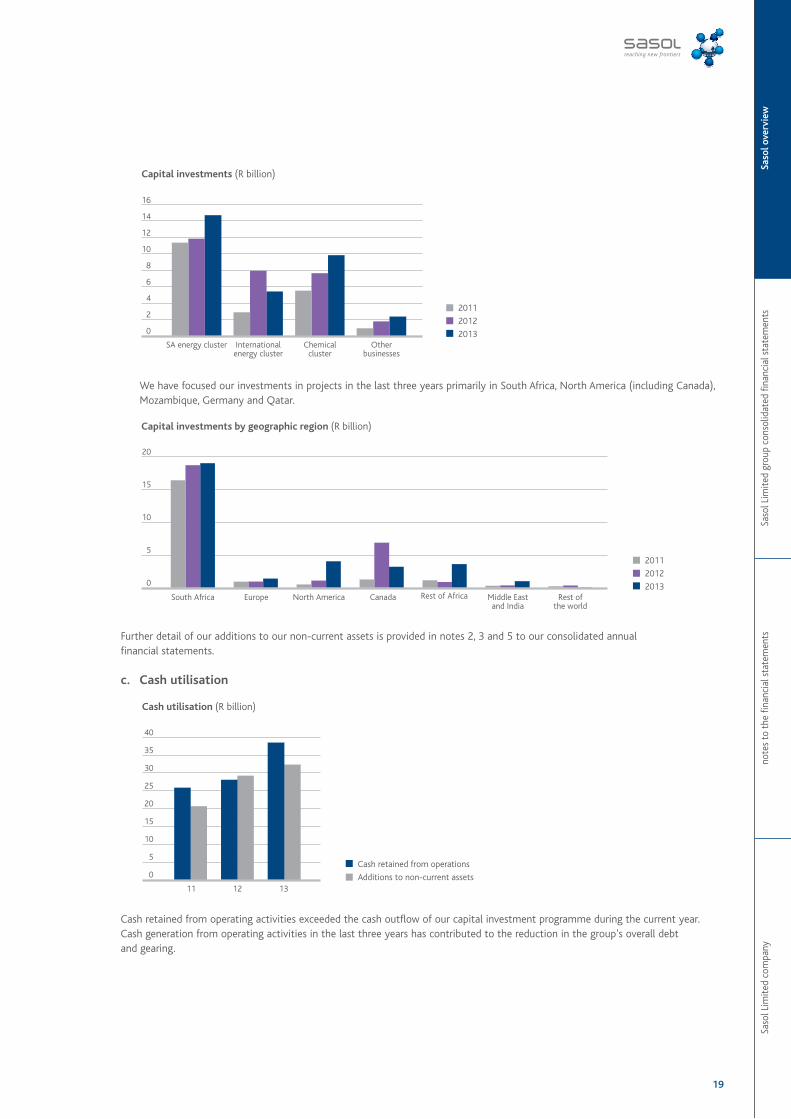

b. Capital investments The central treasury funds all capital investments of the group, which are executed by wholly-owned subsidiaries. The central

treasury in turn is funded by means of a group cash pooling system. The net funding requirement is raised from the local and international debt markets and takes into account the group’s self-imposed targeted gearing range, which is between 20% and 40%.

Over the last three years, the group has invested a total of R82,1 billion in capital investments, with R32,3 billion being invested in 2013. This amount relates primarily to the Sasol Synfuels’ planned maintenance outage, the extension of our reserves at Sasol Mining, the construction of the wax production facility in Sasolburg, South Africa, and the development of our Canadian shale gas asset, as well as various other small projects.

chief financial officer’s review continued

Saso

l Lim

ited

com

pany

note

s to

the

fina

ncia

l sta

tem

ents

Saso

l Lim

ited

grou

p co

nsol

idat

ed fi

nanc

ial s

tate

men

tsSa

sol o

verv

iew

19

We have focused our investments in projects in the last three years primarily in South Africa, North America (including Canada), Mozambique, Germany and Qatar.

Further detail of our additions to our non-current assets is provided in notes 2, 3 and 5 to our consolidated annual financial statements.

c. Cash utilisation

Cash retained from operating activities exceeded the cash outflow of our capital investment programme during the current year. Cash generation from operating activities in the last three years has contributed to the reduction in the group’s overall debt and gearing.

20

Saso

l ann

ual fi

nanc