Embed Size (px)

Citation preview

Presentation

6th March 2015

2014 Results

2014 Results1

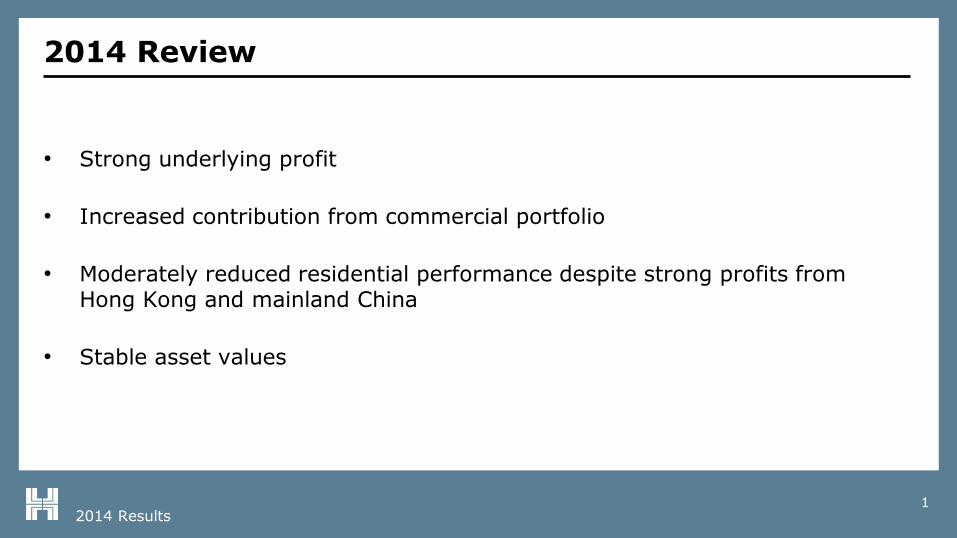

2014 Review

• Strong underlying profit

• Increased contribution from commercial portfolio

• Moderately reduced residential performance despite strong profits from Hong Kong and mainland China

• Stable asset values

2014 Results2

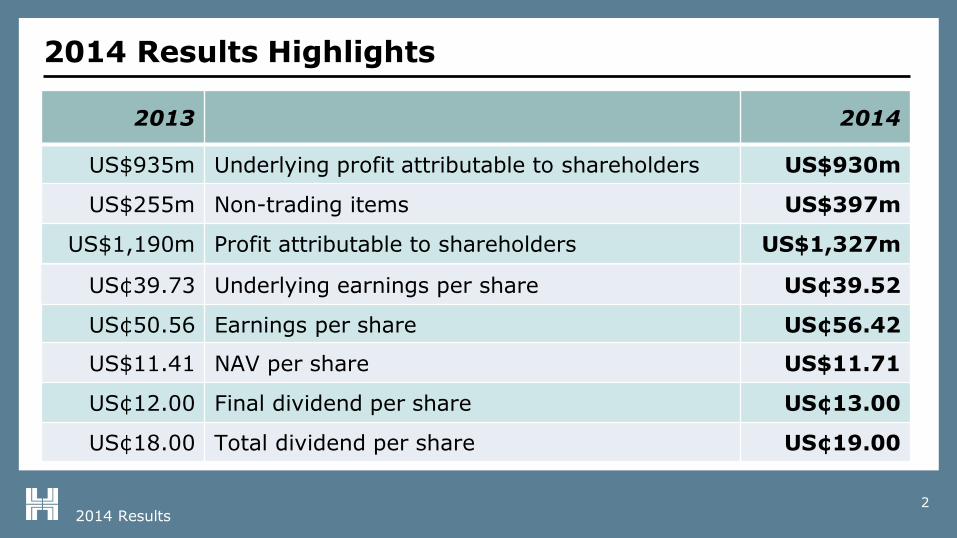

2014 Results Highlights

2013 2014

US$935m Underlying profit attributable to shareholders US$930m

US$255m Non-trading items US$397m

US$1,190m Profit attributable to shareholders US$1,327m

US¢39.73 Underlying earnings per share US¢ 39.52

US¢50.56 Earnings per share US¢ 56.42

US$11.41 NAV per share US$11.71

US¢12.00 Final dividend per share US¢ 13.00

US¢18.00 Total dividend per share US¢ 19.00

2014 Results3

Commercial Property

2014 Results4

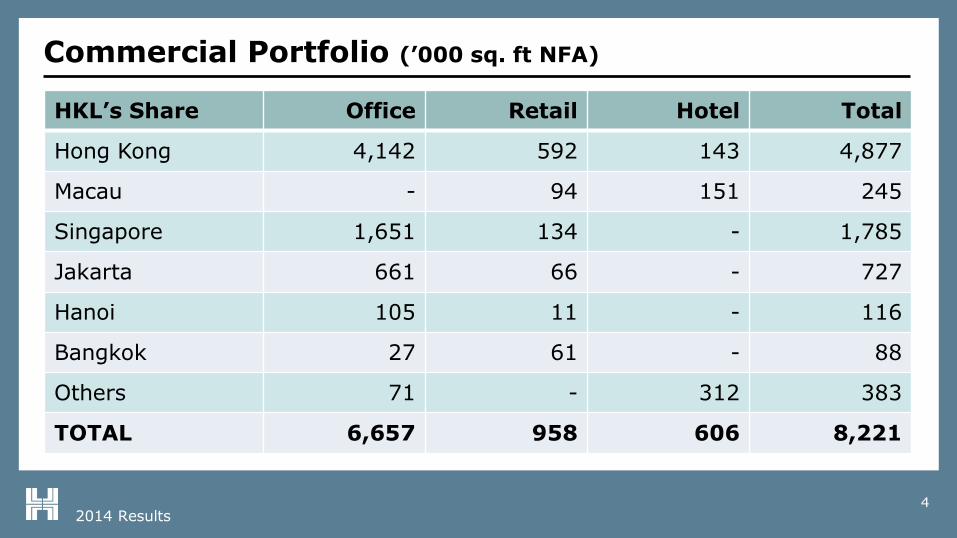

Commercial Portfolio (’000 sq. ft NFA)

HKL’s Share Office Retail Hotel Total

Hong Kong 4,142 592 143 4,877

Macau - 94 151 245

Singapore 1,651 134 - 1,785

Jakarta 661 66 - 727

Hanoi 105 11 - 116

Bangkok 27 61 - 88

Others 71 - 312 383

TOTAL 6,657 958 606 8,221

2014 Results5

Hong Kong

1. One Exchange Square

2. Two Exchange Square

3. Three Exchange Square

4. The Forum

5. Jardine House

6. Chater House

7. Alexandra House

8. Gloucester Tower

9. Edinburgh Tower

9a. The Landmark Mandarin Oriental

10. York House

11. Landmark Atrium

12. Prince’s Building

2014 Results6

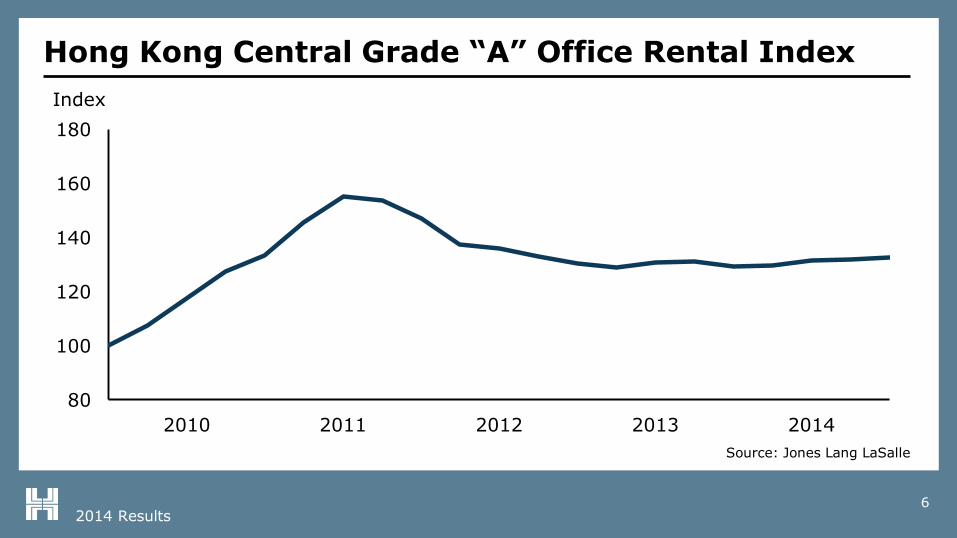

Hong Kong Central Grade “A” Office Rental Index

80

100

120

140

160

180

2010 2011 2012 2013 2014

Index

Source: Jones Lang LaSalle

2014 Results7

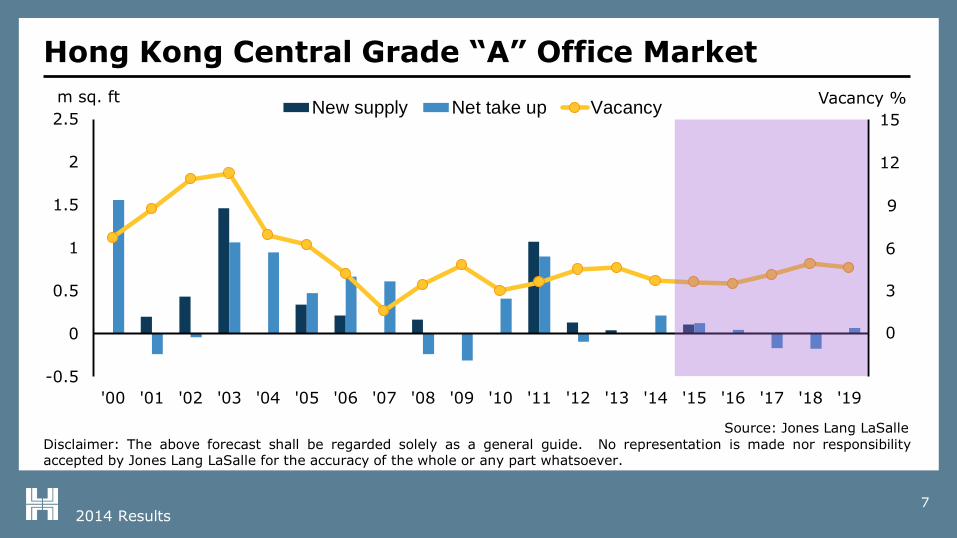

Hong Kong Central Grade “A” Office Market

-0.5

0

0.5

1

1.5

2

2.5

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Vacancy %m sq. ftNew supply Net take up Vacancy

0

3

6

9

12

15

Disclaimer: The above forecast shall be regarded solely as a general guide. No representation is made nor responsibilityaccepted by Jones Lang LaSalle for the accuracy of the whole or any part whatsoever.

Source: Jones Lang LaSalle

2014 Results

-2

0

2

4

6

8

10

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Vacancy %m sq. ftNew supply Net take up Vacancy

8

Hong Kong Grade “A” Office Market

0

3

6

9

12

15

Disclaimer: The above forecast shall be regarded solely as a general guide. No representation is made nor responsibilityaccepted by Jones Lang LaSalle for the accuracy of the whole or any part whatsoever.

Source: Jones Lang LaSalle

2014 Results9

Hongkong Land Central Portfolio: Office

2012 2013 2014

Average Net Rent (HK$ psf/month) 90 99 102

Year-end Vacancy 3.4% 5.0% 5.4%

Weighted Average Lease Expiry (years) 3.7 3.6 3.4

2014 Results10

Hong Kong: Office Tenant Profile

Banks and

other financial

services

39%

Legal

31%

Accounting

8%

Governments

1%

Trading

2%

Property

6%

Others

13%

2014 Results11

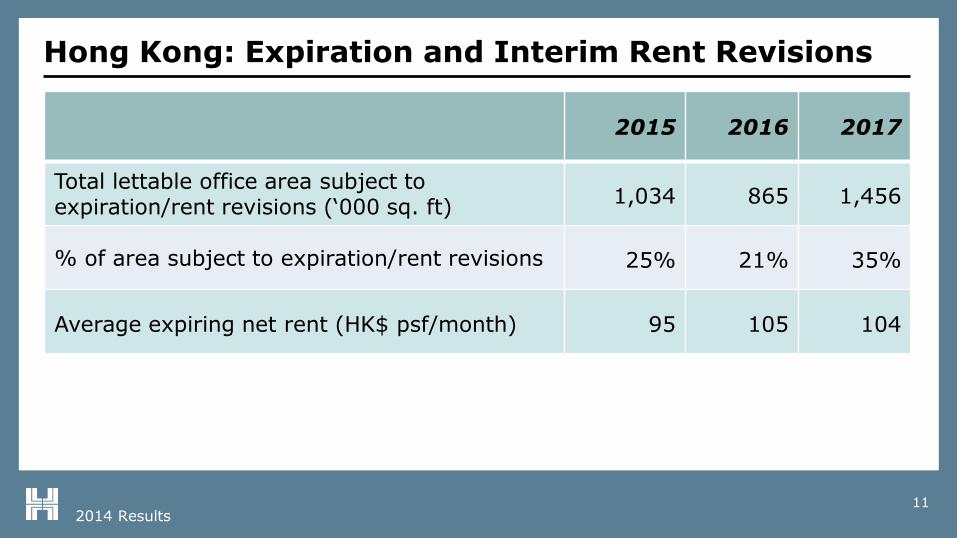

Hong Kong: Expiration and Interim Rent Revisions

2015 2016 2017

Total lettable office area subject toexpiration/rent revisions (‘000 sq. ft)

1,034 865 1,456

% of area subject to expiration/rent revisions 25% 21% 35%

Average expiring net rent (HK$ psf/month) 95 105 104

2014 Results12

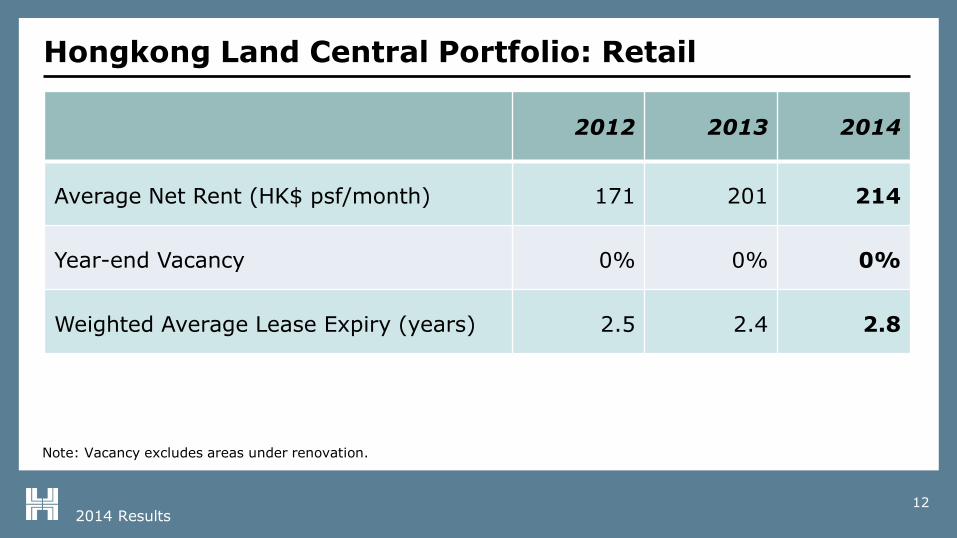

Hongkong Land Central Portfolio: Retail

2012 2013 2014

Average Net Rent (HK$ psf/month) 171 201 214

Year-end Vacancy 0% 0% 0%

Weighted Average Lease Expiry (years) 2.5 2.4 2.8

Note: Vacancy excludes areas under renovation.

2014 Results13

• Retail component 96% let

• 5% increase in average rent

Macau

One Central (47%-owned)

2014 Results

Singapore

One Raffles Link(100%-owned)

Marina Bay Financial Centre(33%-owned)

One Raffles Quay(33%-owned)

14

2014 Results

-1

0

1

2

3

4

5

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Vacancy %m sq. ft New supply Net take up Vacancy

15

Singapore CBD Grade “A” Office Market

CBD – Raffles Place, Shenton Way, Marina Bay & Marina Centre

0

3

6

12

15

9

Disclaimer: The above forecast shall be regarded solely as a general guide. No representation is made nor responsibilityaccepted by Jones Lang LaSalle for the accuracy of the whole or any part whatsoever.

Source: Jones Lang LaSalle

2014 Results16

Office Retail Total HKL’s Share

One Raffles Link 239 73 312 312

One Raffles Quay 1,330 4 1,334 445

Marina Bay Financial Centre 2,906 179 3,085 1,028

TOTAL 4,475 256 4,731 1,785

Singapore Commercial Portfolio (’000 sq. ft NFA)

2014 Results17

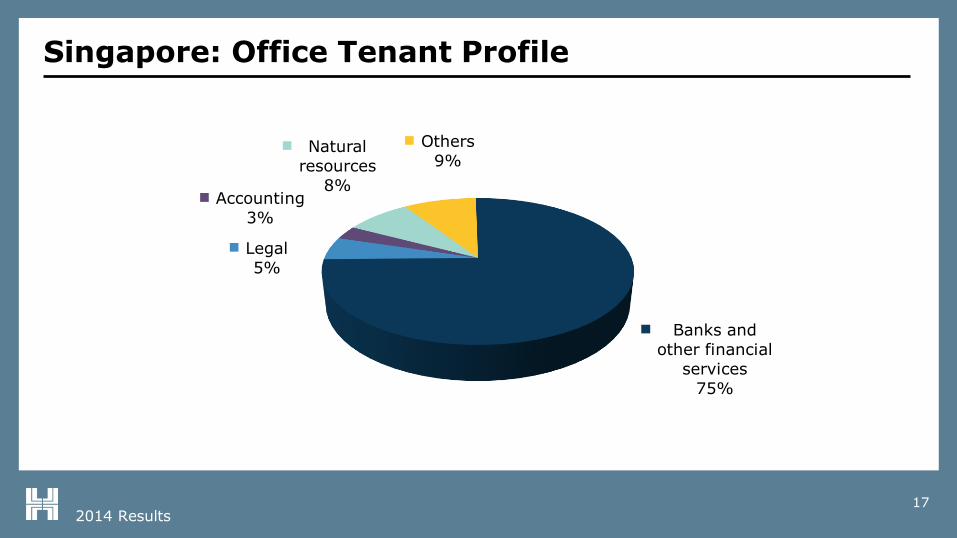

Singapore: Office Tenant Profile

Banks and

other financial

services

75%

Legal

5%

Accounting

3%

Natural

resources

8%

Others

9%

2014 Results18

Singapore: Office Average Rents and Occupancy

Note: According to local market practice, the average office rent includes management charges.

2012 2013 2014

Average Gross Rent (S$ psf/month) 8.7 9.1 9.2

Year-end Vacancy 5.6% 1.7% 1.7%

Weighted Average Lease Expiry (years) 6.6 5.9 5.5

2014 Results19

Singapore: Expiration and Interim Rent Revisions

2015 2016 2017

HKL’s Share: Total lettable office area subject to expiration/rent revisions (‘000 sq. ft)

120 311 317

% of area subject to expiration/rent revisions 7% 19% 19%

Average expiring rent (S$ psf/month) 9.5 11.1 9.2

Note: According to local market practice, the average office rent includes management charges.

2014 Results20

• Existing portfolio features 135,000 sq. m.

• Average gross rent: US$24.0 psm per month(2013: US$21.6 psm per month)

• Occupancy: 95.4%

• Construction begun on new tower, WTC 3

• Strong demand for office space

Jakarta

Jakarta Land (50%-owned)

WTC 3

2014 Results

Hanoi and Bangkok

21

63 Ly Thai To

(74%-owned)

Gaysorn

(49%-owned)

Central Building

(71%-owned)

2014 Results

Phnom Penh

22

EXCHANGE SQUARE (100%-owned)

• Mixed-use complex

• Heart of Phnom Penh

• Completion: 2017

2014 Results23

• Prestigious retail centre, which includes a small luxury hotel

• 43,000 sq. m. lettable retail area

• Completion: end-2016

Beijing

WF CENTRAL (90%-owned)

2014 Results24

• Prime Grade “A” office

• 120,000 sq. m. lettable area

• Completion: 2019

Beijing

CBD (30%-owned)

2014 Results25

Residential Property

2014 Results26

• Final 14 units sold and handed over in 2014

Hong Kong

Serenade

2014 Results27

• Final five units handed over in 2014

Macau

One Central (47%-owned)

2014 Results28

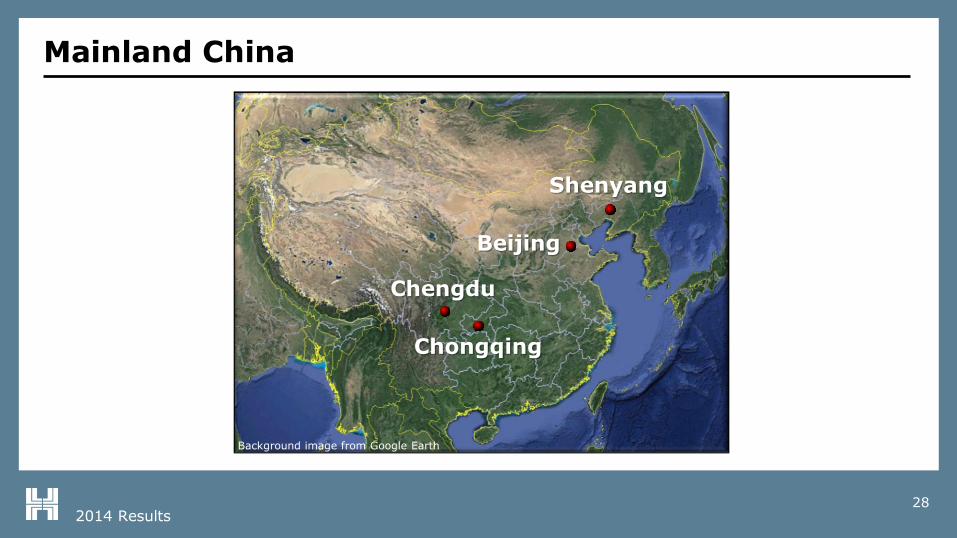

Mainland China

Background image from Google Earth

Shenyang

Beijing

Chengdu

Chongqing

Background image from Google Earth

2014 Results29

Mainland China – Completed Projects, Beijing

Project Project Type

Maple Place (90%)

• 16 units handed over in 2014

• 64 units available for future sale, mostly leased

Central Park (40%) • 72 units of serviced apartments

Maple Place

Central Park

2014 Results30

Project Interest Project Type

Bamboo Grove, Chongqing 50% Primarily Residential

Landmark Riverside, Chongqing 50% Residential (76%), Office, Retail & Others

Yorkville South, Chongqing 100% Primarily Residential

Yorkville North, Chongqing 100% Residential (74%), Office, Retail & Others

Central Avenue, Chongqing 50% Residential (66%), Office & Retail

Chengdu Project 50%Residential (46%), Office (14%), Retail (17%), Hotel & Serviced Apartments (23%)

Shenyang Projects 50% Primarily Residential

Mainland China – Development Projects Summary

2014 Results31

Mainland China – Development Projects Summary

HKL’s Share

ProjectYear of

AcquisitionSite Area

(ha)

DevelopableArea

(m sq. m.)

Constructed(m sq. m.)

Under Construction

(m sq. m.)

Bamboo Grove, Chongqing 2005 39 0.73 0.54 0.09

Landmark Riverside, Chongqing 2009 17 0.75 0.10 0.07

Yorkville South, Chongqing 2010 39 0.88 0.28 0.29

Yorkville North, Chongqing 2011 54 1.09 0.16 0.26

Central Avenue, Chongqing 2013 20 0.55 - 0.04

Chengdu Project 2010 10 0.45 0.03 0.12

Shenyang Projects 2007 58 1.01 0.13 -

TOTAL 237 5.46 1.24 0.87

2014 Results32

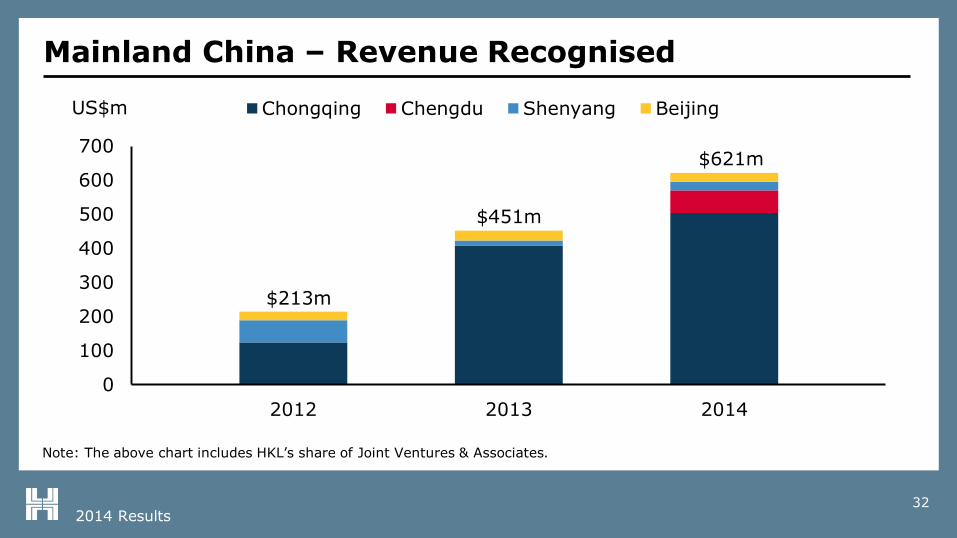

Mainland China – Revenue Recognised

US$m

Note: The above chart includes HKL’s share of Joint Ventures & Associates.

$213m

$451m

$621m

0

100

200

300

400

500

600

700

2012 2013 2014

Chongqing Chengdu Shenyang Beijing

2014 Results33

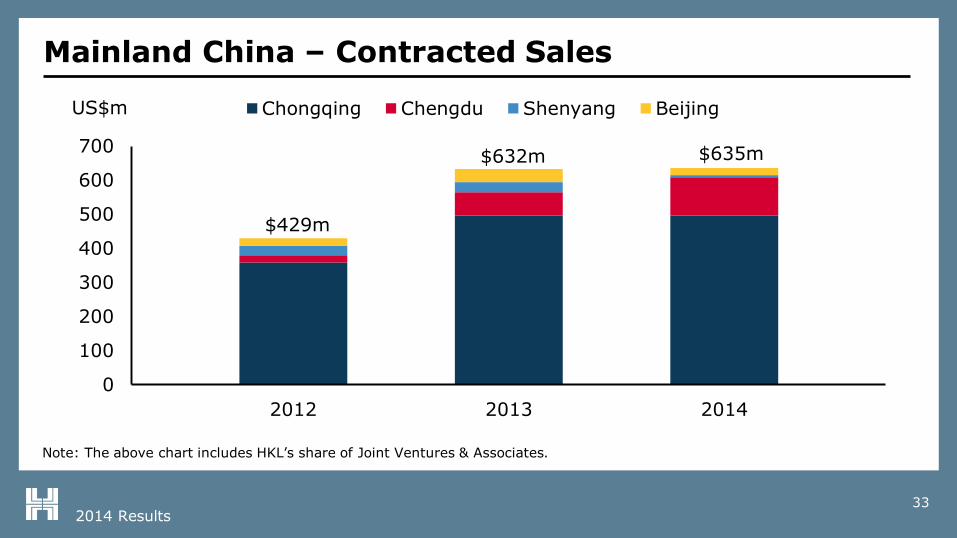

Mainland China – Contracted Sales

$429m

$632m $635m

0

100

200

300

400

500

600

700

2012 2013 2014

Chongqing Chengdu Shenyang Beijing

Note: The above chart includes HKL’s share of Joint Ventures & Associates.

US$m

2014 Results34

Mainland China – Contracted Sales

Note: The above chart includes HKL’s share of Joint Ventures & Associates.

$200m$229m

$369m

$263m $262m

$373m

0

100

200

300

400

500

1H '12 2H '12 1H '13 2H '13 1H '14 2H '14

Chongqing Chengdu Shenyang BeijingUS$m

2014 Results35

Mainland China – Contracted Sales

• At 31st December 2014, US$533m (2013: US$534m) in sold but unrecognised contracted sales

• Some 80% of contracted sales scheduled to be recognised in 2015

2014 Results36

Singapore

Hallmark Residences

Palms @ Sixth Avenue

J Gateway

Uber 388

TerrasseRipple Bay

LakeVille

Marina Bay Suites

Choa Chu Kang GroveParcels A & B

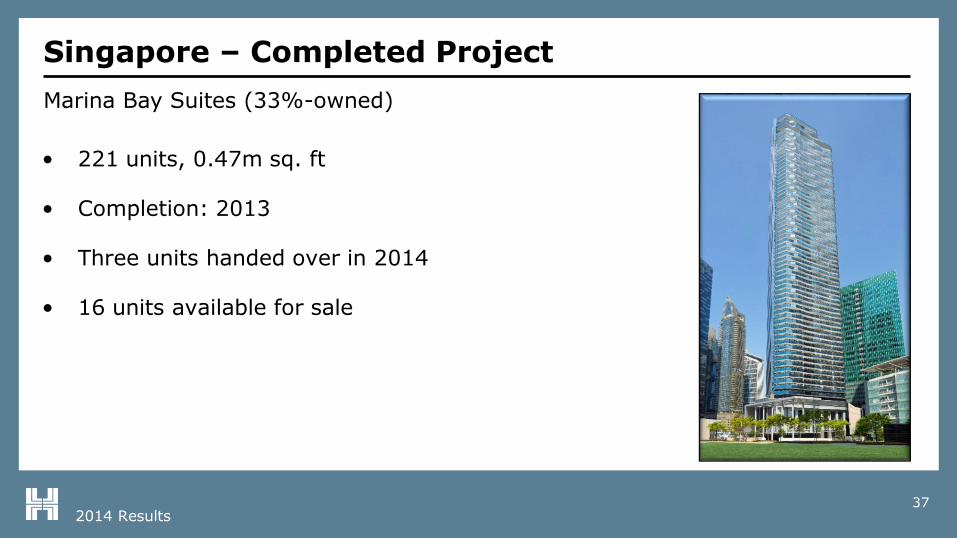

2014 Results37

• 221 units, 0.47m sq. ft

• Completion: 2013

• Three units handed over in 2014

• 16 units available for sale

Singapore – Completed Project

Marina Bay Suites (33%-owned)

2014 Results38

Singapore – Completions in 2014

Project UnitsGFA

(‘000 sq. ft)Sold

Terrasse 414 476 100%

Uber 388 95 98 100%

Terrasse

Uber 388

2014 Results39

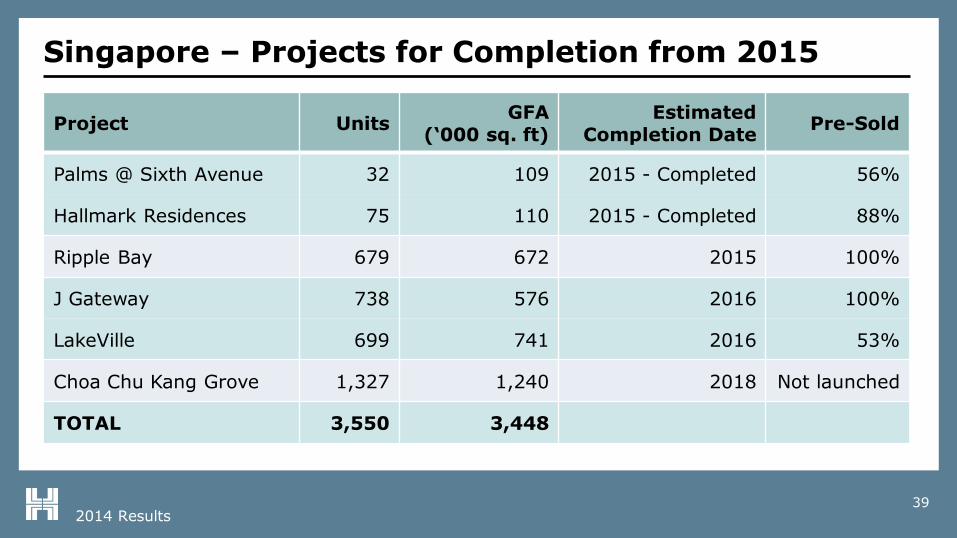

Singapore – Projects for Completion from 2015

Project UnitsGFA

(‘000 sq. ft)Estimated

Completion DatePre-Sold

Palms @ Sixth Avenue 32 109 2015 - Completed 56%

Hallmark Residences 75 110 2015 - Completed 88%

Ripple Bay 679 672 2015 100%

J Gateway 738 576 2016 100%

LakeVille 699 741 2016 53%

Choa Chu Kang Grove 1,327 1,240 2018 Not launched

TOTAL 3,550 3,448

2014 Results40

• JV with PT Bumi Serpong Damai

• Site area: 67 ha

• Southwest of central Jakarta

• 223 units launched for sale; 59% pre-sold

• Completion of 1st phase: 2016

Indonesia

Nava Park, Greater Jakarta (49%-owned)

2014 Results41

• JV with Astra International

• 509 units of luxury apartments; 78% pre-sold

• Completion: 2018

Indonesia

Anandamaya Residences (40%-owned)

2014 Results42

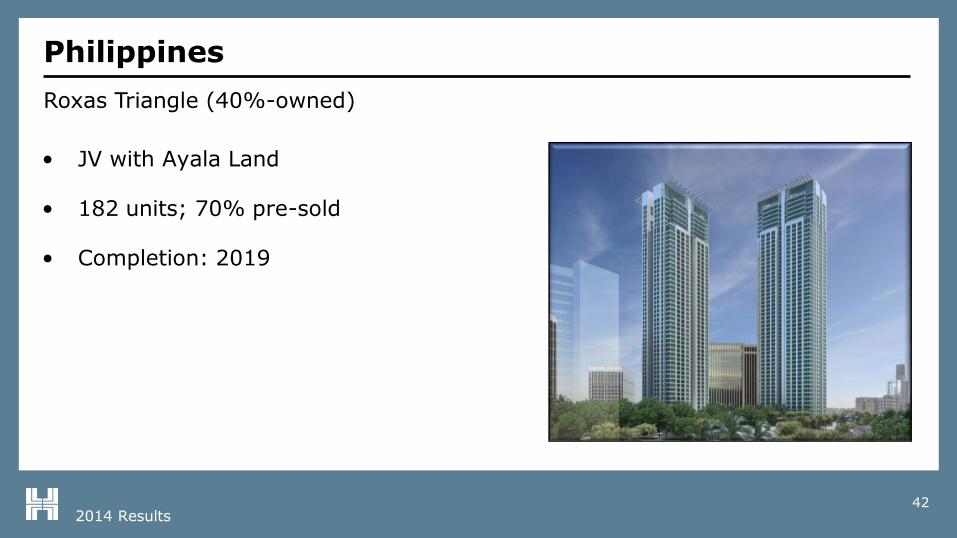

• JV with Ayala Land

• 182 units; 70% pre-sold

• Completion: 2019

Philippines

Roxas Triangle (40%-owned)

2014 Results43

Financial Results

2014 Results44

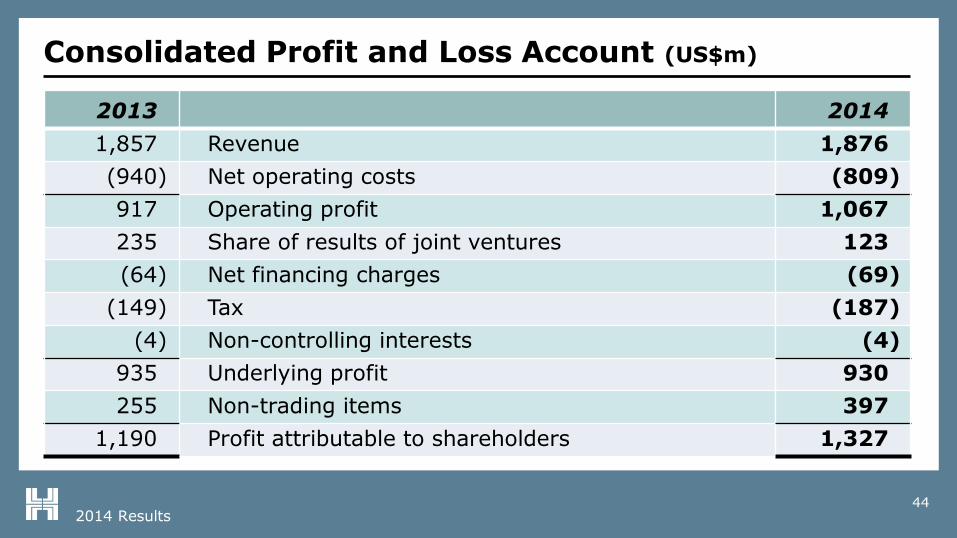

Consolidated Profit and Loss Account (US$m)

2013 2014

1,857 Revenue 1,876

(940) Net operating costs (809)

917 Operating profit 1,067

235 Share of results of joint ventures 123

(64) Net financing charges (69)

(149) Tax (187)

(4) Non-controlling interests (4)

935 Underlying profit 930

255 Non-trading items 397

1,190 Profit attributable to shareholders 1,327

2014 Results45

Revenue (US$m)

2013 2014

925 Commercial revenue 961

932 Residential revenue 915

1,857 Total 1,876

2014 Results46

Underlying Profit by Business (US$m)

2013 2014

914 Commercial property 953

413 Residential property 398

(60) Corporate expenses (62)

1,267 1,289

(103) Net financing charges (103)

(224) Tax (247)

(5) Non-controlling interests (9)

935 Underlying profit 930

2014 Results47

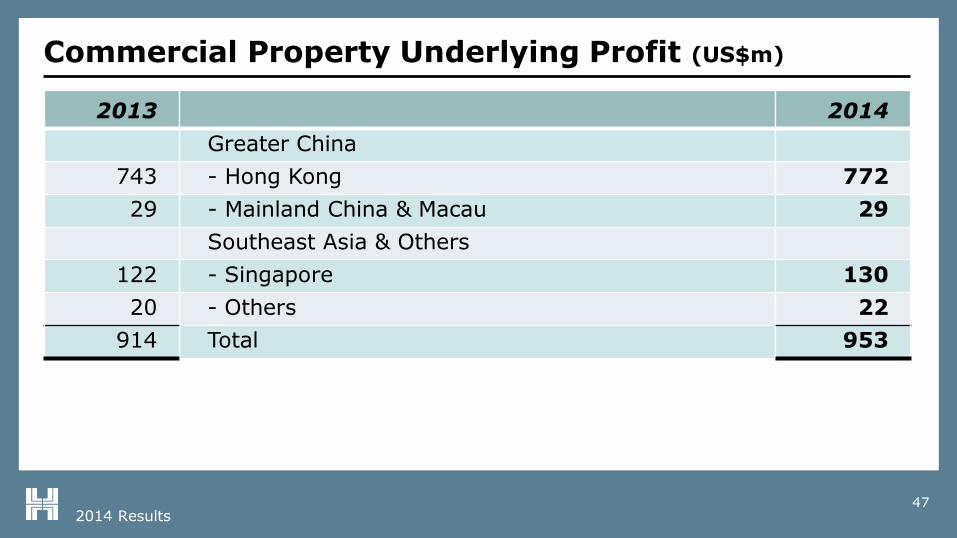

Commercial Property Underlying Profit (US$m)

2013 2014

Greater China

743 - Hong Kong 772

29 - Mainland China & Macau 29

Southeast Asia & Others

122 - Singapore 130

20 - Others 22

914 Total 953

2014 Results48

Residential Property Underlying Profit (US$m)

2013 2014

Greater China

19 - Hong Kong 69

116 - Mainland China & Macau 179

Southeast Asia & Others

278 - Singapore 149

- - Others 1

413 Total 398

2014 Results49

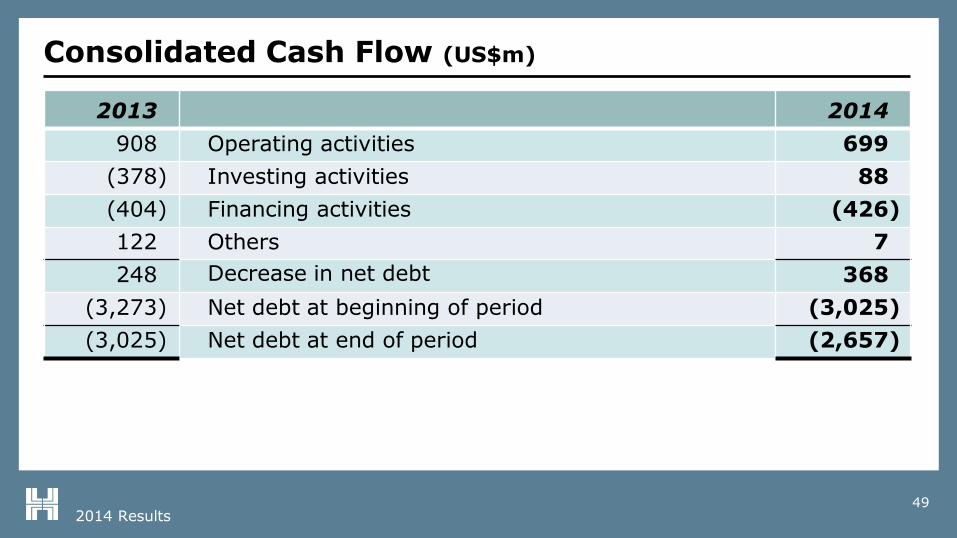

Consolidated Cash Flow (US$m)

2013 2014

908 Operating activities 699

(378) Investing activities 88

(404) Financing activities (426)

122 Others 7

248 Decrease in net debt 368

(3,273) Net debt at beginning of period (3,025)

(3,025) Net debt at end of period (2,657)

2014 Results50

Operating Activities (US$m)

2013 2014

917 Operating profit excluding non-trading items 1,067

(77) Net interest paid (81)

(139) Tax paid (134)

(367) Payments for residential sites (429)

(303) Development expenditure on residential projects (454)

918 Proceeds from residential sales 962

151 Dividends received from joint ventures 153

(192) Others (385)

908 699

2014 Results51

Investing Activities (US$m)

2013 2014

(40) Major renovations capex (38)

(422) Funding of joint ventures (216)

104 Loan repayments from joint ventures 479

(134) Development expenditure (137)

114 Others -

(378) 88

2014 Results52

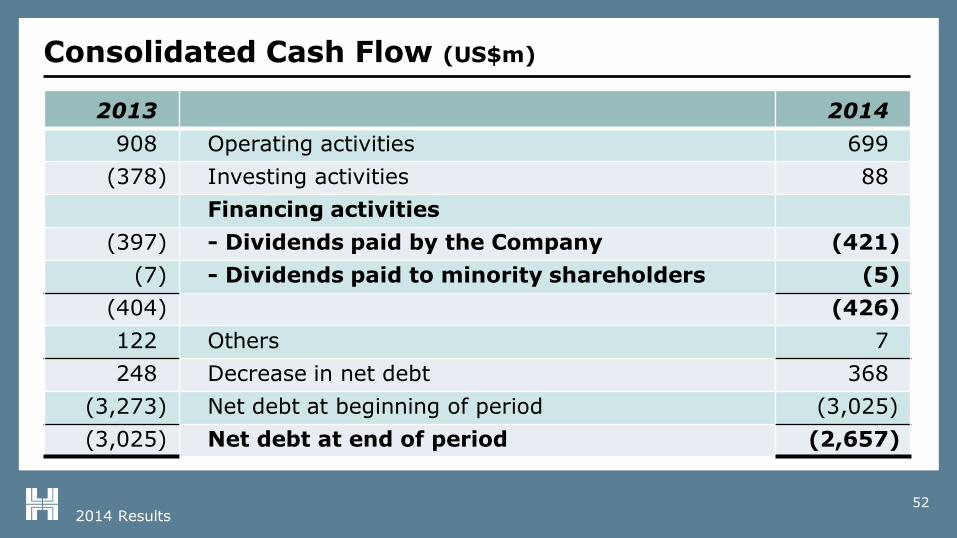

Consolidated Cash Flow (US$m)

2013 2014

908 Operating activities 699

(378) Investing activities 88

Financing activities

(397) - Dividends paid by the Company (421)

(7) - Dividends paid to minority shareholders (5)

(404) (426)

122 Others 7

248 Decrease in net debt 368

(3,273) Net debt at beginning of period (3,025)

(3,025) Net debt at end of period (2,657)

2014 Results53

Consolidated Balance Sheet (US$m)

2013 2014

Investment properties

23,583 - Subsidiaries 23,697

4,167 - Joint ventures 4,474

27,750 28,171

Properties held for sale

2,670 - Subsidiaries 2,923

1,247 - Joint ventures 1,372

3,917 4,295

(1,743) Others (2,211)

29,924 Gross assets (excluding cash) 30,255

Financed by:

26,899 - Total equity 27,598

3,025 - Net debt 2,657

29,924 30,255

2014 Results54

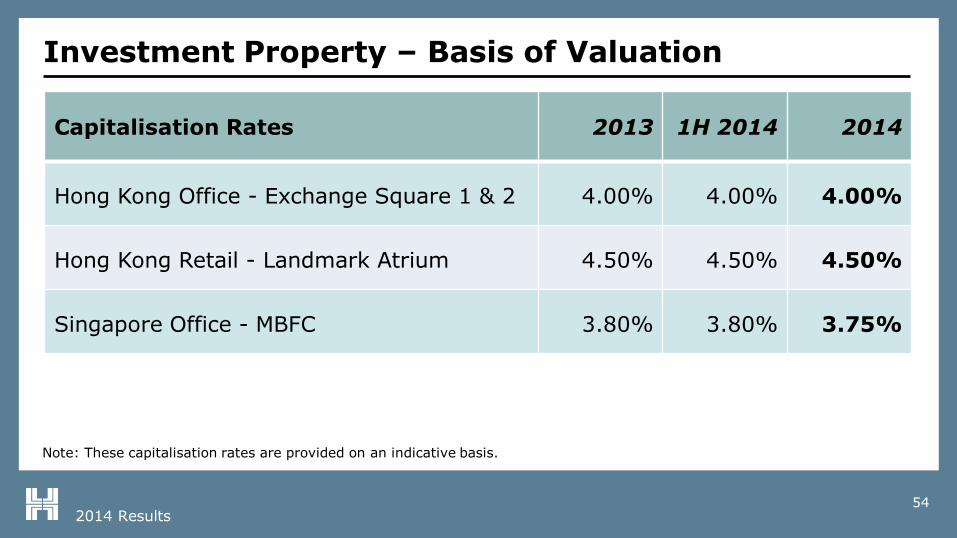

Investment Property – Basis of Valuation

Capitalisation Rates 2013 1H 2014 2014

Hong Kong Office - Exchange Square 1 & 2 4.00% 4.00% 4.00%

Hong Kong Retail - Landmark Atrium 4.50% 4.50% 4.50%

Singapore Office - MBFC 3.80% 3.80% 3.75%

Note: These capitalisation rates are provided on an indicative basis.

2014 Results55

Investment Property – Carrying Values (US$m)

Note: The analysis includes share of Joint Ventures & Associates.

2013 2014

Greater China

22,302 - Hong Kong 22,336

1,368 - Mainland China & Macau 1,650

Southeast Asia & Others

3,603 - Singapore 3,628

477 - Others 557

27,750 Total 28,171

2014 Results56

Properties Held for Sale – Carrying Values (US$m)

Note: The analysis includes share of Joint Ventures & Associates.

2013 2014

Greater China

62 - Hong Kong 23

2,308 - Mainland China & Macau 2,435

Southeast Asia & Others

1,456 - Singapore 1,696

91 - Others 141

3,917 4,295

(923) Pre-sale proceeds (941)

2,994 Net investment 3,354

2014 Results57

Gross Assets at 31st Dec 2014

Commercial 88%

Residential 12%

By Activity

Hong Kong 73%

Mainland China and Macau 11%

Southeast Asia 16%

By Location

2014 Results58

Treasury Management

Summary 2013 2014

Net debt (US$m) 3,025 2,657

Gearing 11% 10%

Average tenor of debt (years) 6.7 7.3

Average interest cost 2.7% 2.9%

Credit ratings

- S & P

- Moody’s

A-

A3

A

A3

2014 Results59

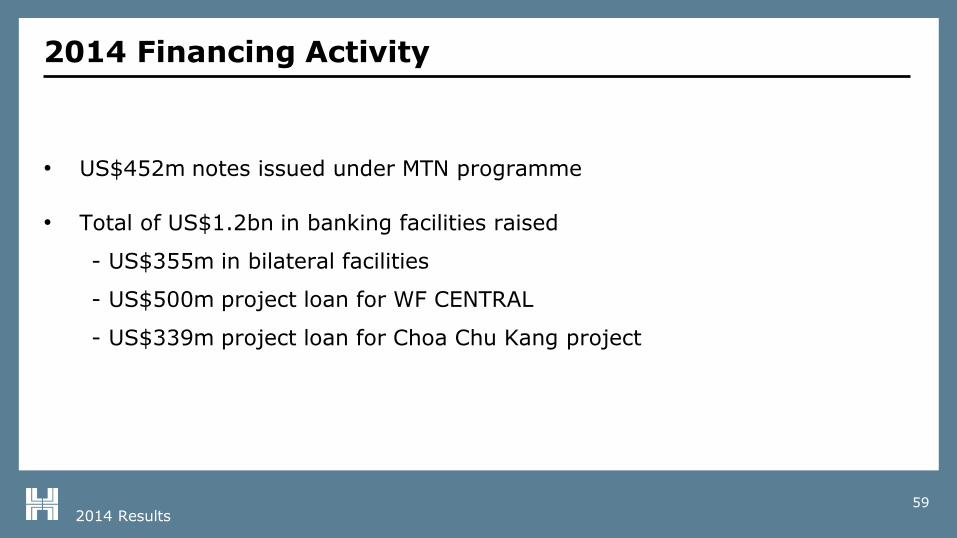

2014 Financing Activity

• US$452m notes issued under MTN programme

• Total of US$1.2bn in banking facilities raised

- US$355m in bilateral facilities

- US$500m project loan for WF CENTRAL

- US$339m project loan for Choa Chu Kang project

2014 Results60

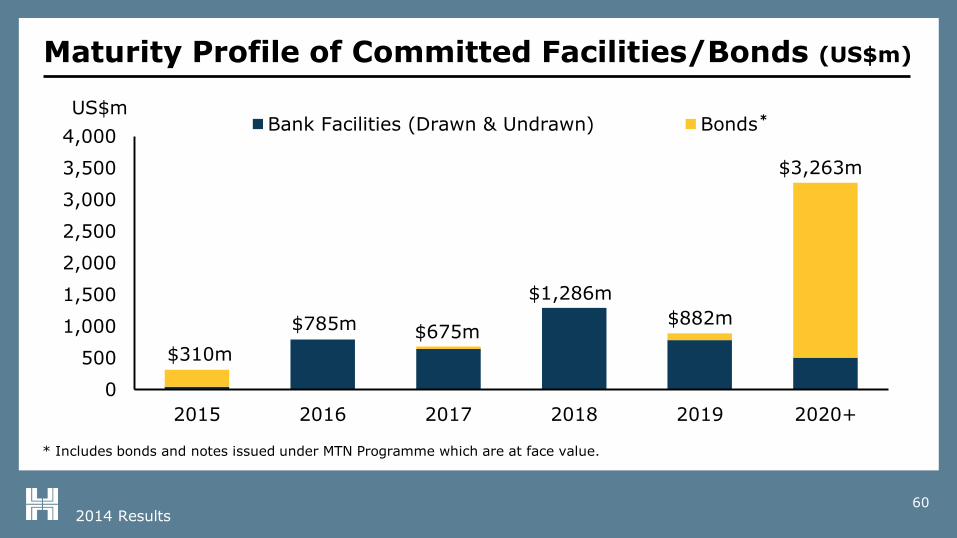

$310m

$785m $675m

$1,286m

$882m

$3,263m

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2015 2016 2017 2018 2019 2020+

Bank Facilities (Drawn & Undrawn) BondsUS$m

Maturity Profile of Committed Facilities/Bonds (US$m)

*

* Includes bonds and notes issued under MTN Programme which are at face value.

2014 Results61

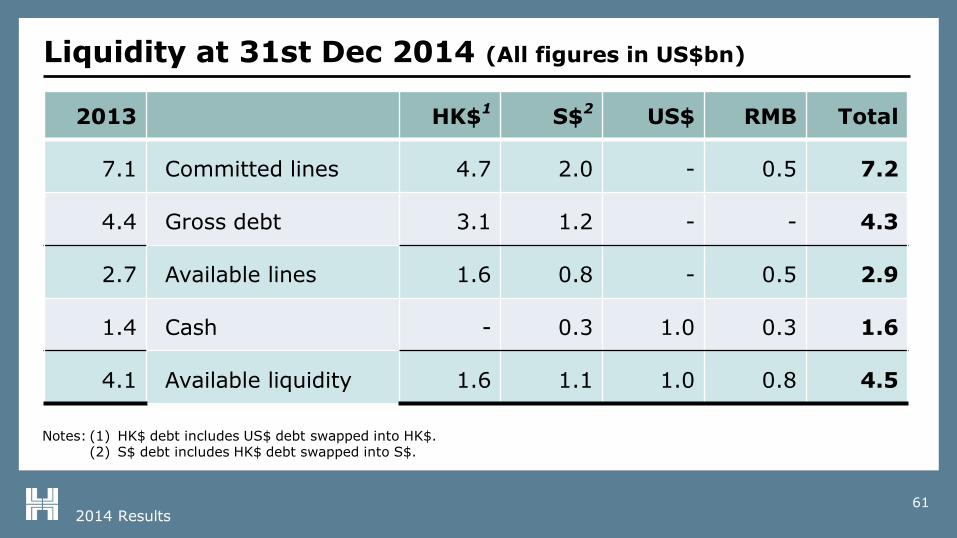

Liquidity at 31st Dec 2014 (All figures in US$bn)

2013 HK$1

S$2

US$ RMB Total

7.1 Committed lines 4.7 2.0 - 0.5 7.2

4.4 Gross debt 3.1 1.2 - - 4.3

2.7 Available lines 1.6 0.8 - 0.5 2.9

1.4 Cash - 0.3 1.0 0.3 1.6

4.1 Available liquidity 1.6 1.1 1.0 0.8 4.5

Notes: (1) HK$ debt includes US$ debt swapped into HK$.(2) S$ debt includes HK$ debt swapped into S$.

2014 Results62

Outlook

• Commercial leasing markets in Hong Kong and Singapore remain stablein 2015

• Further strong profits expected from residential development activitiesin mainland China

• No residential profits in Hong Kong and lower contribution fromSingapore

• The Group continues to seek opportunities in premium commercial andresidential developments in Greater China and Southeast Asia

Hongkong Land

www.hkland.com

Thank you