Embed Size (px)

Citation preview

0 10 10 91 0Years

“Cathedral” Photovoltaics

0 10 20 30 40 50 60 70 8

0 GW-y1 GW-y3 GW-y6 GW-y10 GW-y15 GW-y21 GW-y28 GW-y36 GW-y45 GW-y0 GW-y3 GW-y1 GW-y2 GW-y

Cumulative GW installed

0

500

1,000

1,500

2,000

2,500

3,000

2000 2005 2010 2015 2020 2025 2030 2035 2040

WEO 2002WEO 2004WEO 2006WEO 2008WEO 2010WEO 2012WEO 2014WEO 2015WEO 2016WEO 2017ActualBNEF forecast

Wind Solar

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2005 2010 2015 2020 2025 2030 2035 2040

6⨉ upward revision since

2002

23⨉ upward revision since

2002

Source: IEA World Energy Outlook series, Bloomberg New Energy Finance June 2017 forecast. Slide inspired by Michael Liebreich’s 2016 BNEF Summit keynote

International Energy Agency global wind and solar forecasts

French windpower output, December 2011: forecasted one day ahead vs. actual

Variable Renewables Can Be Forecasted At Least as Accurately as Electricity Demand

Source: Bernard Chabot, 10 April 2013, Fig. 7, www.renewablesinternational.net/wind-power-statistics-by-the-hour/150/505/61845/, data from French TSO RTE

GW

0

0.51

1.52

2.53

3.54

4.55

!10% Downtime

!12% Downtime

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Original loadLoad after efficiency

Geothermal etc.

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation, 2004 renewables data

HVAC ice/EV storageBiomass/biogas

Storage recoveryDemand response

Solar (25 GW)Wind (37 GW)

Spilled power (~5%)

Europe, 2015–17 renewable % of total electricity consumed

Choreographing Variable Renewable Generation

36%

60%Denmark 2015 (42% wind, 11% bio) (2013 windpower peak 136%—55% for all December)

68%Scotland 2017 (53% without hydro)

46%Peninsular Spain (2016, 27% without hydro)

63%Portugal (2016, 29% without hydro) (2011 & 2016 peak 100%; 70% for 1H2013 incl. 26% wind & 34% hydro)

Germany 1H2018 (2016 peak 88%, 2018 ~90–100%)

1980

Transitioning to distributed renewables in DenmarkCentral thermalOther generationWind turbines

2012

Source: Risø

Grid flexibility resources cost

efficient use

demand response

(all values shown are conceptual and illustrative)

accurate forecasting

of wind + PV

diversify renewables by type and

location

dispatchable renewables and

cogeneration

bulk storage

fossil-fueled

backup

distributed electricity storageincl. EVs

thermal storage

ability to accommodatereliably a large share ofvariable renewable power

(hydrogen storage not shown because its quantity is indeterminate)

Flexible loads: goodbye “duck curve”These eight levers combine to make net load far smoother and lower (ERCOT, summer 2050)

-15-10-505

10152025303540455055

0 4 8 12 16 20 24

Load Net Load

GW

2 Res Plug Load

3 Res DHW

4 Comm DHW

5 Res Cooling

6 Comm Cooling

7 Res Heating

8 Comm Heating

1 El Vehicles

New Net Load

Source: RMI analysis by Harry Masters, 2016, in course of publication

In Westchester, NY, 60% of residential consumption in the next decade could come more cheaply from PV

Source: RMI analysis “The Economics of Load Defection,” 2015

Cheaper renewables and batteries change the game

Load control + PVs = grid optional

0"

2"

4"

6"

8"

10"

12"

kW#

Uncontrolled: ~50% of solar PV production is sent to the grid, but if the utility doesn’t pay for that energy, how could customers respond?

EV-charging

!"!!!!

!2.00!!

!4.00!!

!6.00!!

!8.00!!

!10.00!!

!12.00!!

kW#

Unc!Load! Smart!AC! Smart!DHW! Smart!Dryer!

0"

2"

4"

6"

8"

10"

12"

kW#

Controlled: flexible load enables customers to consume >80% of solar PV production onsite. The utility loses nearly all its windfall and most of its ordinary revenue.

AC

DHW

Dryer

Other

Solar PVAC

DHW

Dryer

Other

Solar PVEV-charging

Source: RMI analysis “The Economics of Load Flexibility,” 2015

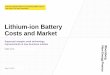

Accelerating plug-in auto growth and falling battery priceGlobal Plug In vehicles, now 4 million, are growing ~50% per year, with battery pack price now below $200/kWh and falling fast

Sources: BNEF, EV-Volumes; S: https://www.greencarreports.com/news/1103667_electric-car-battery-costs-tesla-190-per-kwh-for-pack-gm-145-for-cellsQuattro: https://electrek.co/2017/06/28/audi-electric-car-battery-cost/

for-2016-145kwh-cell-cost-volt-margin-improves-3500/

Battery pack price, 2011–2017 (nominal $)

0

200

400

600

800

1,000

2011 2012 2013 2014 2015 2016 2017

2018 Audi Quattro

$114/kWh

Plug-In Vehicle sales, 2011–2017

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2011 2012 2013 2014 2015 2016 2017United States China Europe Other

2016 Tesla S

$190/kWh

From PIGS to SEALS

Personal Internal-combustion Gasoline Steel Shareable Electric Autonomous Lightweight [mobility-as-a-]Service

中华人民共和国 国民经济和社会发展第十三个五年规划纲要

2016年03月17日

Tripled US end-use efficiency and quintupled renewables by 2050

IRRs: 33% buildings, 21% industry, 17% mobility, 14% all those plus a resilient, 80%-renewable, 50%-distributed electricity system.Real hurdle rates for efficiency investments, based on 2011 sectoral risk/reward tolerances: autos 3-y retail payback, heavy trucks 15%/y, buildings 7%/y, industry 12%/y, electricity generation 5.7%/y (based on investor-owned utilities’ weighted-average cost of capital).Analysis in constant 2009 $; discounting to 2010 present value is at OMB’s 3%/y prescribed for federal energy-efficiency investments.Activity levels and energy prices from USEIA’s 2010 Annual Energy Outlook Reference Case, extrapolated to 2050.Sectoral adoption rates based on stock-and-flow or consumer-choice models consistent with observed market behavior. No material lifestyle changes. No externalities. Many technical conservatisms. No new (post-2010) inventions. No Acts of Congress.

Trilli

on 2

009

chai

ned

$

14.5

15.5

16.5

17.5

2010 2011 2012 2013 2014 2015 2016 2017

RFActual

TWh/

y

400

500

600

700

2010 2011 2012 2013 2014 2015 2016 2017

RFActual

Renewable electricity generation

GDP

kBTU

/

2009

$ c

hain

ed G

DP

5

6

7

8

2010 2011 2012 2013 2014 2015 2016 2017

RF Actual

Primary energy intensity

kWh

/20

09 $

cha

ined

GD

P0.15

0.2

0.25

0.3

2010 2011 2012 2013 2014 2015 2016 2017

RFActual

Electric intensity

2010–2017 U.S. progress toward Reinventing Fire’s 2050 goalsActuals (USEIA) are not weather-adjusted. Reinventing Fire progression based on constant exponential growth rate.

Solutions to:

587%+ 42%in savings经济节约

bigger GDP经济规模

less carbon碳排放减少

RMB21T2010 NPV

0

10

20

30

40

50

60

2010 2020 2030 2040 2050

Gig

aton

CO

2 pe

r yea

r

USA

EU

China

Other OECD

Other Non-OECD

Worldwide RF

IEA 450 scenario

Reinventing Fire applied worldwide will keep within the 2010–2050 carbon budget for 50% probability of 2Cº

2"

Worldwide annual CO2 emissions under Reinventing Fire scenario

2034: cumulative post-2010 emissions exceed 1.5Cº budget

Assumptions: • CO2 emissions are calculated using Reinventing Fire for U.S., Roadmap 2050 for EU, Reinventing Fire: China for China.

Other OECD is calculated using the Reinventing Fire 2010–2050 trajectory; Other Non-OECD using the Reinventing Fire: China 2010–2050 trajectory.

• CO2 budget is calculated by ETH Zürich from IPCC data and assumptions for non-CO2 emissions to define an energy-related CO2 budget.

• Cumulative CO2 emissions for 2010–2050 under the Reinventing Fire scenario are 1121 Gt by 2050, 79 Gt below the 1200 Gt 2010–2050 carbon budget for 50% probability of ≤2C˚ average temperature change, but 331 Gt above the carbon budget for ≤1.5Cº average temperature change.

Business-as-usual

…and with conservatively assessed natural-systems carbon removal…

Av. t

emp.

rise

(C˚)

Detecting an early signal of the energy transitionAnnual percent change in global non-carbon share of total final energy consumption, 1975–2016, and primary energy intensity, 1975–2017

-4%

-2%

0%

2%

4%

6%

8%

1975 1980 1985 1990 1995 2000 2005 2010 2015

y = -0.0013x + 2.64 R² = 0.30

y = 0.0054x - 10.89 R² = 0.51

y = 0.0001x - 0.2375 R² = 0.021

y = -0.0025x + 4.94 R² = 0.66

Sources: TFEC (IEA), renewables (BP, except IEA for renewable heat only); synthetic primary energy intensity (BP, World Bank); no adjustments for weather, economic cycles, or other fluctuations

2016 2 C˚ 1.5 Cº

-1.2%

3.4%

6.7%/y median spread for 1.5C˚ (Rogelj et al., Nature Climate Change, 5 Mar 2018)

3.4%/y median spread for 2C˚ (IPCC AR5)

Global total final commercial energy consumption from non-fossil-fuel sources, 1975–2017 (21% of 2016 total)

0

10

20

30

40

1975 1980 1985 1990 1995 2000 2005 2010 2015

Nuclear

Hydro

Solar

Wind

Geothermal, biomass, wasteBiofuelsRenewable heat

Exaj

oule

s/y

Sources: TFEC (IEA Energy Balances for renewable heat, BP for all others)

Nuclear flatlined, but renewables more than compensated

-3%

-2%

-1%

0%

1981–90 1991–2000 2001–10 2011 2012 2013 2014 2015 2016 2017

Global energy savings are accelerating like renewablesAnnual changes in global primary energy intensity, 1981–2017p

Source: International Energy Agency (Paris), Energy Efficiency Market Report 2017; white line based on IEA, Energy Efficiency Market Report 2016, p. 18, citing IEA’s WEO 450 Scenario (3.7%/y GDP growth 2013–20, 3.8% to 2030, plus expected decarbonization). Preliminary 2017 data from IEA, “Global Energy & CO2 Status Report 2017,” 22 Mar 2017, http://www.iea.org/publications/freepublications/publication/GECO2017.pdf,

Average change 2011–17p: 2.1%/y

Average change 1981–2010: 1.2%/y

–2.9% US–5.9% China

–1.3% EU

IEA’s 450-ppm CO2 scenario calls for 2.6%/y intensity drop to 2030

#1 threat to gas: methane “slip” (vents, flares, leaks, other uncombusted)

CH4 emissions ⨉2.5, 60% human, 25% of warming100- vs 20-y CO2 “equivalence” hides the opportunity~78% is lost upstream, of which ~60–80% is intentional

But CH4 lasts only 9±2 y, so cutting just ~10–25 MT/y could rebalance the global CH4 cycle. Why stop there?

Abating even more (the profitable half of O&G industry emis-sions) could profitably displace 160 GTCO2—fastest way toturn down the thermostat, buying more time to decarbonize

Just closing flares and fixing vents in a few thousand placescould do this profitably! What are entrepreneurs waiting for?

www.earthobservatory.nasa.govInfrared image of a tank battery venting methane from engineered pressure relief valves; vents, flares, and leaks combined emit 76 (2015; coulld well be 80+) MT/y of methane or 2–6 GT/y CO2equiv—$18–36b/y lost revenue at $2–4/million BTU

The world’s 19,000 flares emit ≥6 MT/y of unburned methane (the 2–10% that slips by combustion), equivalent over 100 or 20 y to >180 or 600 MT/y of CO2; closing flares and recovering gas often pays back in a few years

Richard Ward, Director, Methane Program, Rocky Mountain Institute, [email protected], 202 570 3279

13 Source: International Energy Agency – World Energy Outlook 2017

IEA, World Energy Outlook 2017

ABATEMENT NEEDEDTO BALANCE CH4 CYCLE

Price > CostValue >

1900: where’s the first car?

Easter Parades on Fifth Avenue, New York, 13 years apart

1913: where’s the last horse?

Images: L, National Archive, www.archives.gov/research/american-cities/images/american-cities-101.jpg; R, shorpy.com/node/204. Inspiration: Tona Seba’s keynote lecture at AltCar, Santa Monica CA, 28 Oct 2014, http://tonyseba.com/keynote-at-altcar-expo-100-electric-transportation-100-solar-by-2030/

OR

Renewables replacing $38b/y kerosene market

From the Age of Carbon to the Age of Silicon

www.rmi.org | [email protected] | +1 970 927 3129 R

OCKY MOUNTA

IN

INSTIT UTE

Profitable Climate Protectionwith Development and Security

![IMF 2014 WEO data Sampler 3 [kompatibilitätsmodus]](https://img.pdfslide.us/doc/110x75/55a77e2b1a28abc9668b48a2/imf-2014-weo-data-sampler-3-kompatibilitaetsmodus.jpg)