Embed Size (px)

DESCRIPTION

Â

Citation preview

Under embargo until 00:01 Thursday 13th November 2014

November 2014

1

House purchase lending stabilises in October • Lending beginning to recover, as monthly house purchase approvals rise 1.1% in October

• However, house purchase approvals fall 9.2% on a twelve-month basis, from 68,252 in October 2013

• Fewer loans to borrowers with limited deposits: proportion of higher LTV loans makes up just 14.9% of all lending, down from last month’s 17.7%

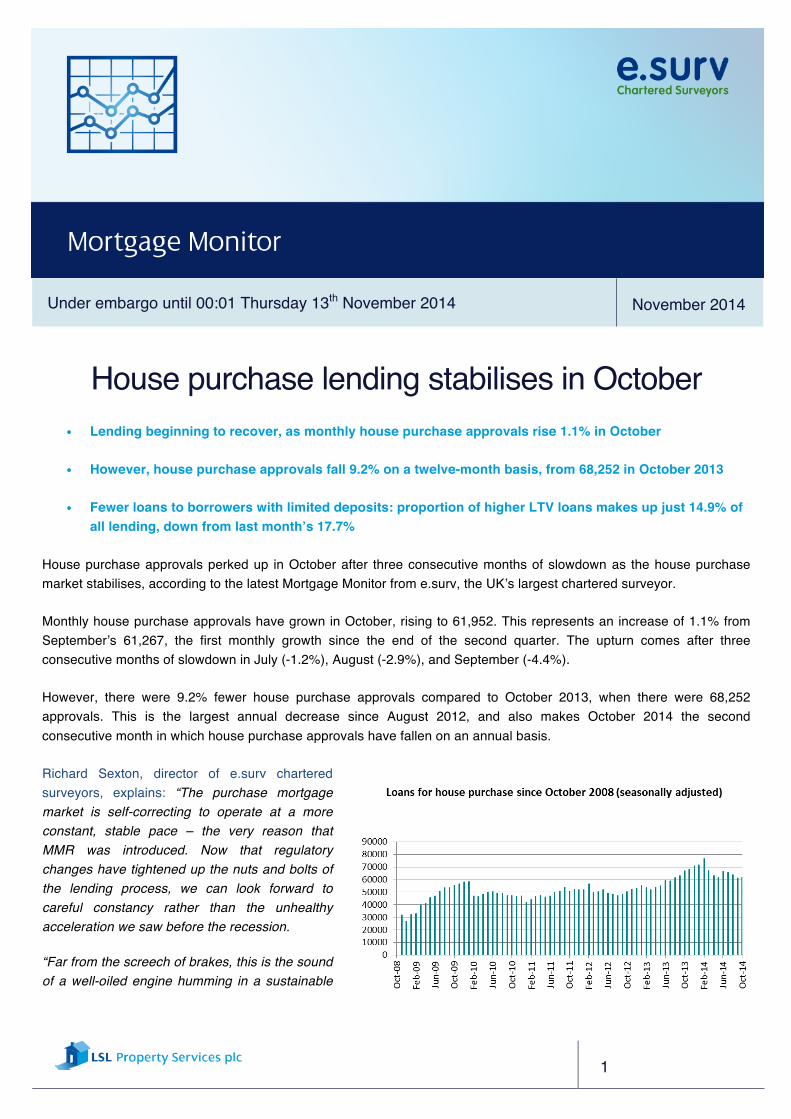

House purchase approvals perked up in October after three consecutive months of slowdown as the house purchase market stabilises, according to the latest Mortgage Monitor from e.surv, the UK’s largest chartered surveyor.

Monthly house purchase approvals have grown in October, rising to 61,952. This represents an increase of 1.1% from September’s 61,267, the first monthly growth since the end of the second quarter. The upturn comes after three consecutive months of slowdown in July (-1.2%), August (-2.9%), and September (-4.4%).

However, there were 9.2% fewer house purchase approvals compared to October 2013, when there were 68,252 approvals. This is the largest annual decrease since August 2012, and also makes October 2014 the second consecutive month in which house purchase approvals have fallen on an annual basis.

Richard Sexton, director of e.surv chartered surveyors, explains: “The purchase mortgage market is self-correcting to operate at a more constant, stable pace – the very reason that MMR was introduced. Now that regulatory changes have tightened up the nuts and bolts of the lending process, we can look forward to careful constancy rather than the unhealthy acceleration we saw before the recession.

“Far from the screech of brakes, this is the sound of a well-oiled engine humming in a sustainable

2

gear.”

Higher LTV loans drop off in October

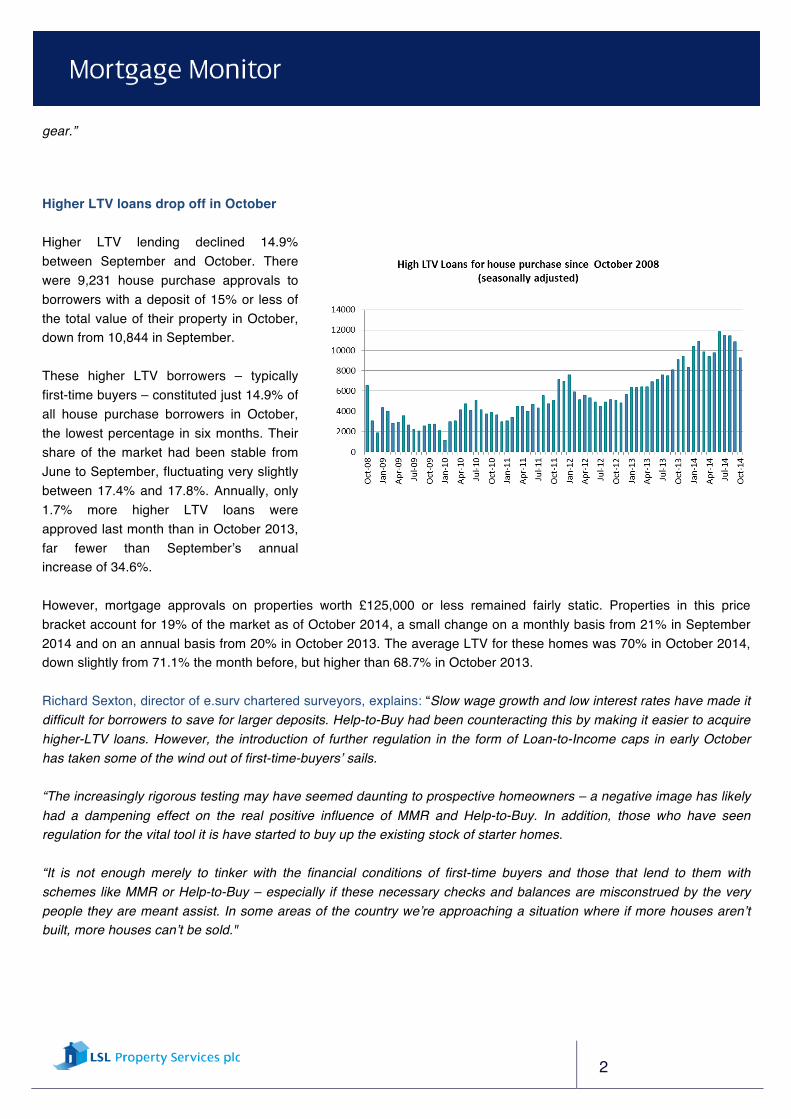

Higher LTV lending declined 14.9% between September and October. There were 9,231 house purchase approvals to borrowers with a deposit of 15% or less of the total value of their property in October, down from 10,844 in September.

These higher LTV borrowers – typically first-time buyers – constituted just 14.9% of all house purchase borrowers in October, the lowest percentage in six months. Their share of the market had been stable from June to September, fluctuating very slightly between 17.4% and 17.8%. Annually, only 1.7% more higher LTV loans were approved last month than in October 2013, far fewer than September’s annual increase of 34.6%.

However, mortgage approvals on properties worth £125,000 or less remained fairly static. Properties in this price bracket account for 19% of the market as of October 2014, a small change on a monthly basis from 21% in September 2014 and on an annual basis from 20% in October 2013. The average LTV for these homes was 70% in October 2014, down slightly from 71.1% the month before, but higher than 68.7% in October 2013.

Richard Sexton, director of e.surv chartered surveyors, explains: “Slow wage growth and low interest rates have made it difficult for borrowers to save for larger deposits. Help-to-Buy had been counteracting this by making it easier to acquire higher-LTV loans. However, the introduction of further regulation in the form of Loan-to-Income caps in early October has taken some of the wind out of first-time-buyers’ sails.

“The increasingly rigorous testing may have seemed daunting to prospective homeowners – a negative image has likely had a dampening effect on the real positive influence of MMR and Help-to-Buy. In addition, those who have seen regulation for the vital tool it is have started to buy up the existing stock of starter homes.

“It is not enough merely to tinker with the financial conditions of first-time buyers and those that lend to them with schemes like MMR or Help-to-Buy – especially if these necessary checks and balances are misconstrued by the very people they are meant assist. In some areas of the country we’re approaching a situation where if more houses aren’t built, more houses can’t be sold."

3

LOANS FOR HOUSE PURCHASE - seasonally adjusted

Month Number Monthly change Annual change

May 61,604 -2.3% +4.2% June 66,758 +8.4% +13.4% July 65,975 -1.2% +7.0%

August 64,054 -2.9% +1.2% September 61,267 -4.4% -8.7%

October 61,952 +1.1% -9.2%

– ENDS –

Notes to Editors

Methodology

e.surv analyses detailed data on over one million mortgage valuations the firm carried out between August 2006 and today. Each month, the researchers analyse tens of thousands of valuations and use these trends to extrapolate from the Bank of England’s mortgage data to publish mortgage approval numbers for the whole of the UK, weeks before the BBA, CML and Bank of England.

The Mortgage Monitor is prepared by The Wriglesworth Consultancy for e.surv. The copyright and all other intellectual property rights in the Mortgage Monitor belong to e.surv. Reproduction in whole or part is not permitted unless an acknowledgement to e.surv as the source is included. No modification is permitted without e.surv’s prior written consent.

Whilst care is taken in the compilation of the report, no representation or assurances are made as to its accuracy or completeness. e.surv reserves the right to vary the methodology and to edit or discontinue the report in whole or in part at any time.

About e.surv

e.surv is a firm of chartered surveyors, directly employing over 380 chartered surveyors, a similar number of consultants, and over 50 graduate surveyors in training. The business is the largest distributor and manager of valuation instructions in the UK and is appointed as panel manager for more than 25 mortgage lenders and other entities with interests in residential property. The business also provides a number of private survey products direct to the home-buying public. e.surv is owned by LSL Property Services plc. For further information, see www.lslps.co.uk

Press contacts

4

Tora Turton, The Wriglesworth Consultancy, [email protected], 020 7427 1445

Justin Blanchard, The Wriglesworth Consultancy, [email protected], 020 7427 1407