Embed Size (px)

Citation preview

10 Financial Planning With Life Insurance

• Primary Purpose of Life Insurance:– Protect someone who depends on you from

financial loss related to your death– Reduces financial burdens of survivors

• Life insurance:– Obtained by purchasing a policy

– The insurance company promises to pay a lump sum (death benefit) to a named beneficiary at the time of the policy holder’s death (or sometimes while they are still alive)

10-1

Objective 1Define Life Insurance and Determine Your Life Insurance NeedsOther reasons to buy life insurance:

– Pay off a mortgage or debts

– Lump-sum endowments for children

– Provide an education or income for children

– Make charitable donations

– Provide retirement income

– Accumulate savings

– Establish a regular income for survivors

– Set up an estate plan (e.g., fund trusts with life insurance)

– Pay estate and gift taxes (e.g., business owners)10-2

The Principle of Life Insurance

• Mortality Tables-provide odds on your dying, based on your age and sex.

• Premium is based on life expectancy and projections for payouts for persons who die (called actuarial tables)– Older people pay more because they will die

sooner

• Face Amount- the dollar value of protection listed in the policy and amount used to calculate the premium (e.g., $100,000)

• Group Term Insurance- issued to people as members of a group rather than as individuals

10-3

Do You Need Life Insurance?

• Do you have people you need to protect financially? Will

your death cause them financial hardship?

• Are you single and have a lot of debt?

• Do you have parents, relatives, or a charity that you want

to support?

Avoid being persuaded to buy unnecessary life insurance!

10-4

Estimating Your Life Insurance Requirements

• The Easy Method– 70% of your salary for seven years while your family adjusts

– Assumes typical family

• The DINK Method– Dual income, no kids

– Assumes spouse earnings will continue

– Cover funeral + ½ debts

• The “Nonworking” Spouse Method– # years until the youngest child reaches 18 X $10,000

• The “Family Need” Method– More thorough than the first three methods

– Considers employer provided insurance, Social Security benefits, income and assets

10-5

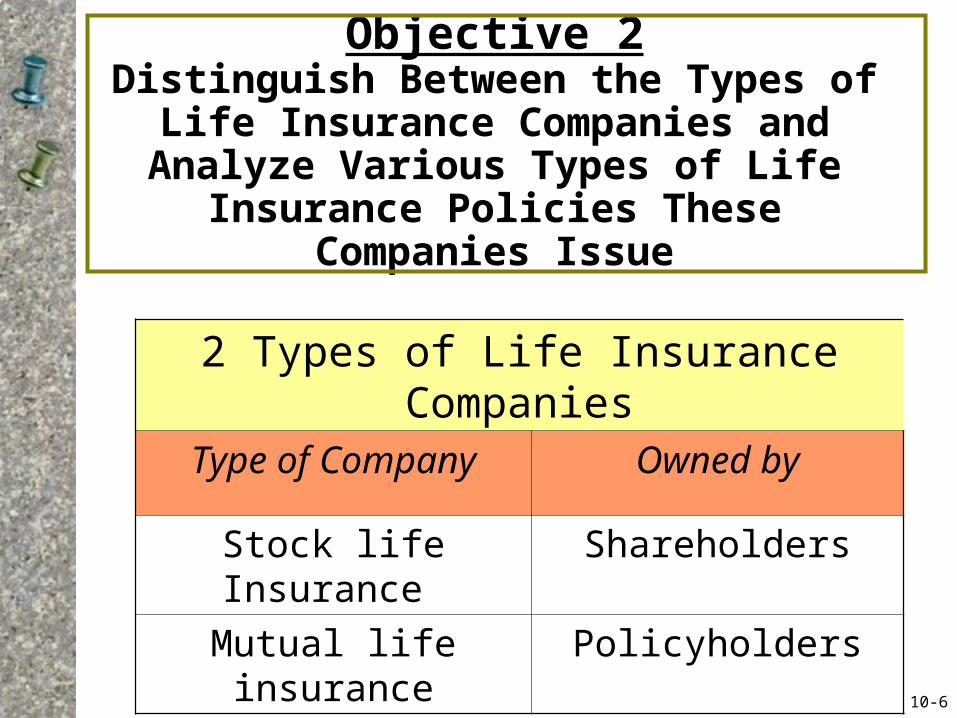

Objective 2Distinguish Between the Types of

Life Insurance Companies and Analyze Various Types of Life

Insurance Policies These Companies Issue

2 Types of Life Insurance Companies

Type of Company Owned by

Stock life Insurance Shareholders

Mutual life insurance Policyholders

10-6

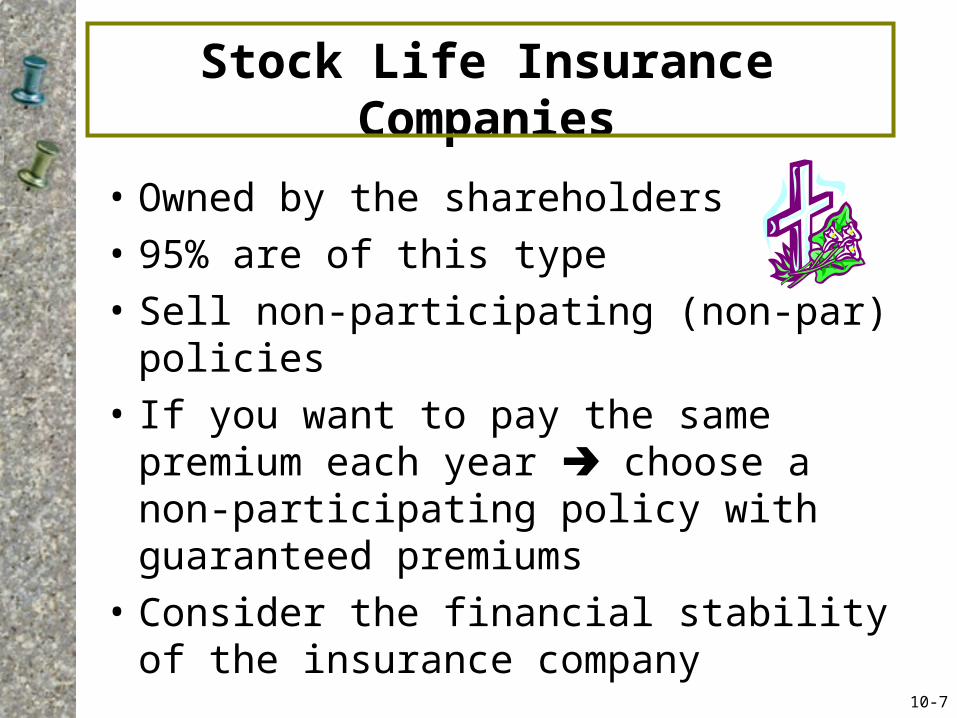

Stock Life Insurance Companies

• Owned by the shareholders

• 95% are of this type

• Sell non-participating (non-par) policies

• If you want to pay the same premium each year choose a non-participating policy with guaranteed premiums

• Consider the financial stability of the insurance company

10-7

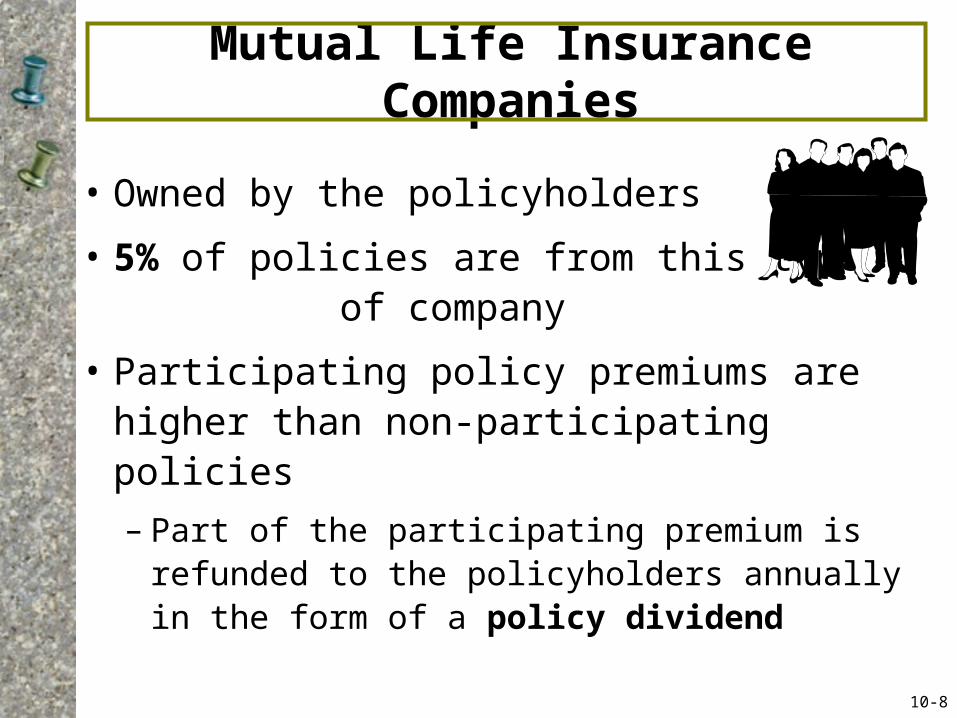

Mutual Life Insurance Companies

• Owned by the policyholders

• 5% of policies are from this type of company

• Participating policy premiums are higher than non-participating policies

– Part of the participating premium is refunded to the policyholders annually in the form of a policy dividend

10-8

Term Life Insurance

Term Life

– Protection for a specified period of time

– At the end of term (or if you stop paying premiums), coverage stops

• Many types:

– Renewable Term- can renew; higher premium charged

– Multiyear Level Term- same premium for set period

– Conversion Term- allows change to permanent policy

– Decreasing Term- face value decreases over time

– Return-of-Premium Term- can get premium back

10-9

Whole Life Insurance

Straight-Life or Whole-Life Insurance– Pay the premium as long as you live– Amount of premium depends on age when you start

the policy– Provides death benefits – Accumulates a cash value you can borrow against or

draw out at retirement– Look carefully at the rate of return your money earnsTypes:

• Limited Payment Policy– You pay premiums for a stipulated period– Policy then “paid up” and you remain insured for life

• Variable Life Policy- Fixed premiums; investment accounts• Adjustable Life Policy- Can change coverage with needs • Universal Life- Can change premium, time period, benefit

10-10

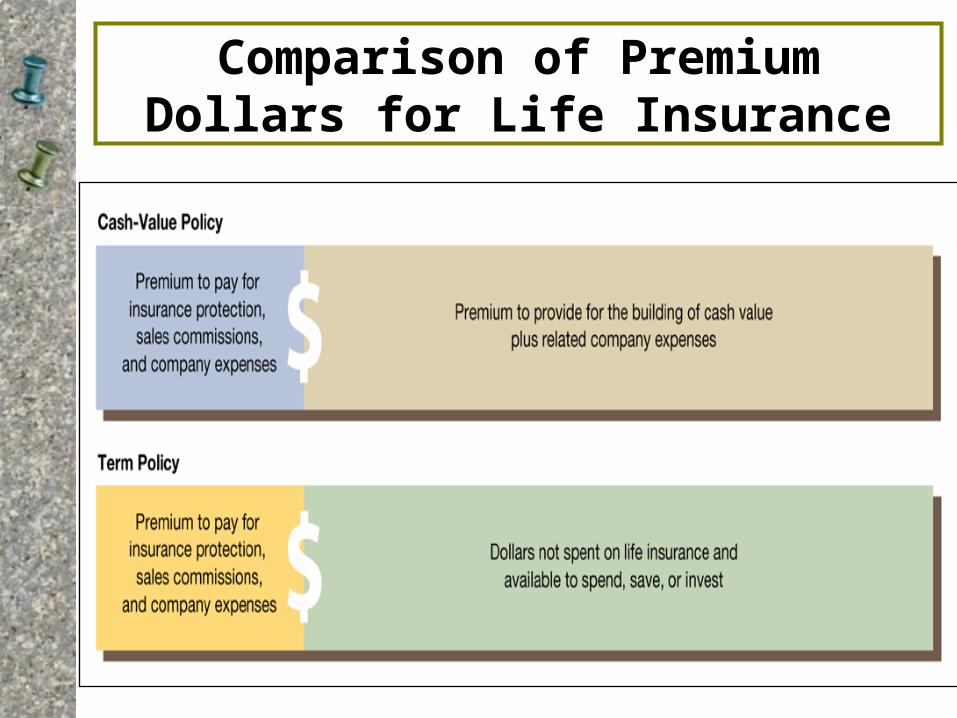

Comparison of Premium Dollars for Life Insurance

Other Types of Life Insurance Policies

• Group life insurance– Term insurance– Often provided by an employer– No physical is required

• Credit life insurance– Debt paid off if you die

• Mortgage, car, furniture

– Also protects lenders– Expensive protection (usually overpriced)

• Endowment Life Insurance- pays policyholder a lump sum if still living at end of the endowment period

10-12

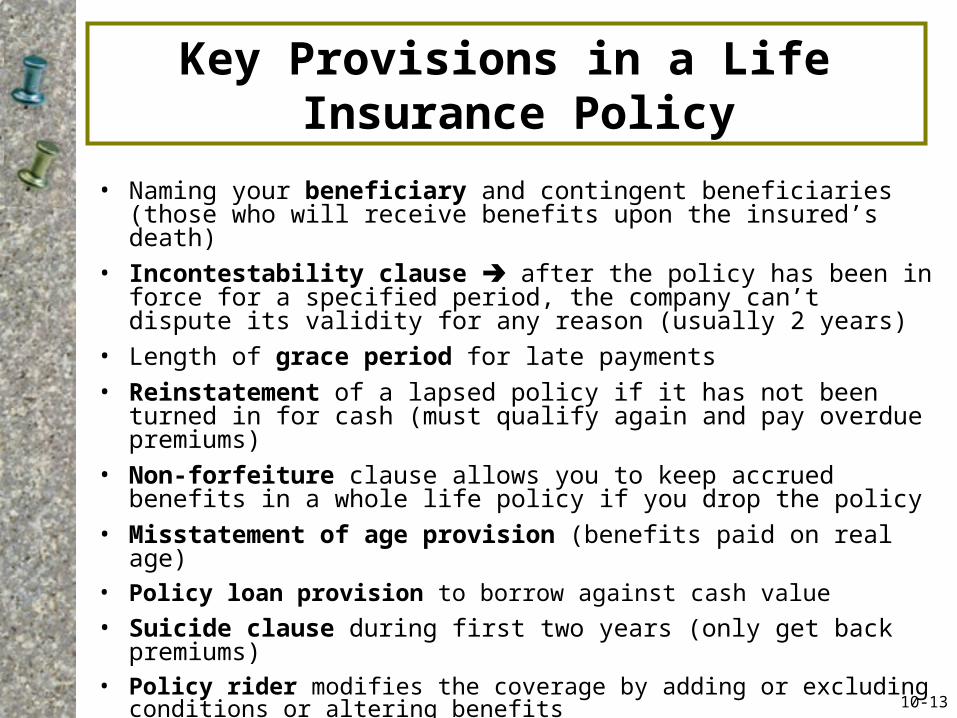

Key Provisions in a Life Insurance Policy

• Naming your beneficiary and contingent beneficiaries (those who will receive benefits upon the insured’s death)

• Incontestability clause after the policy has been in force for a specified period, the company can’t dispute its validity for any reason (usually 2 years)

• Length of grace period for late payments

• Reinstatement of a lapsed policy if it has not been turned in for cash (must qualify again and pay overdue premiums)

• Non-forfeiture clause allows you to keep accrued benefits in a whole life policy if you drop the policy

• Misstatement of age provision (benefits paid on real age)• Policy loan provision to borrow against cash value

• Suicide clause during first two years (only get back premiums)• Policy rider modifies the coverage by adding or excluding

conditions or altering benefits10-13

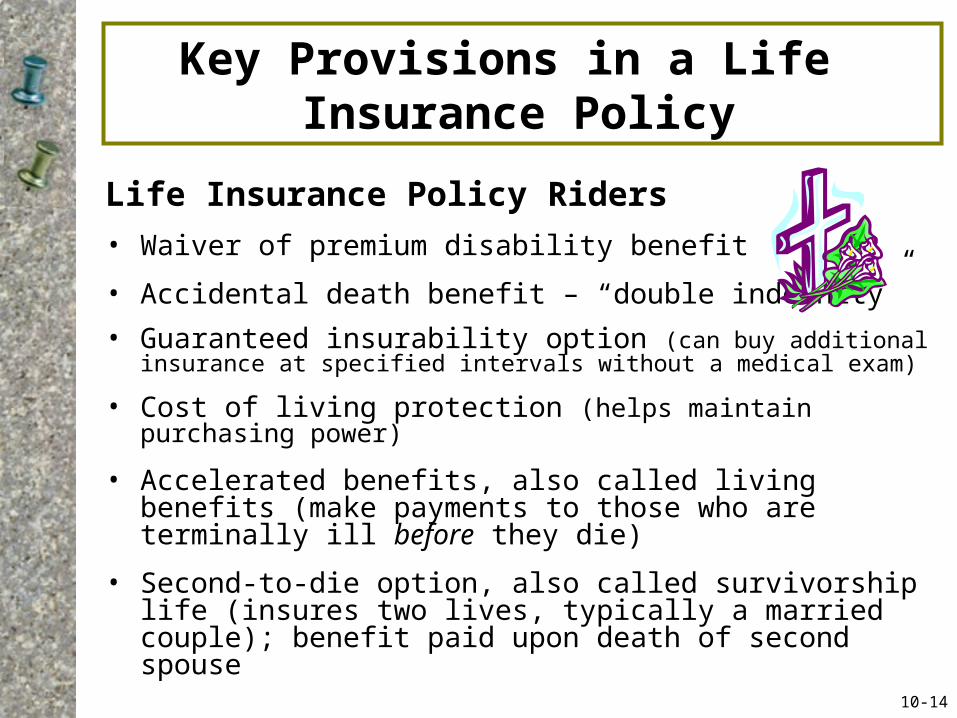

Key Provisions in a Life Insurance Policy

Life Insurance Policy Riders

• Waiver of premium disability benefit

• Accidental death benefit – “double indemnity”

• Guaranteed insurability option (can buy additional insurance at specified intervals without a medical exam)

• Cost of living protection (helps maintain purchasing power)

• Accelerated benefits, also called living benefits (make payments to those who are terminally ill before they die)

• Second-to-die option, also called survivorship life (insures two lives, typically a married couple); benefit paid upon death of second spouse

10-14

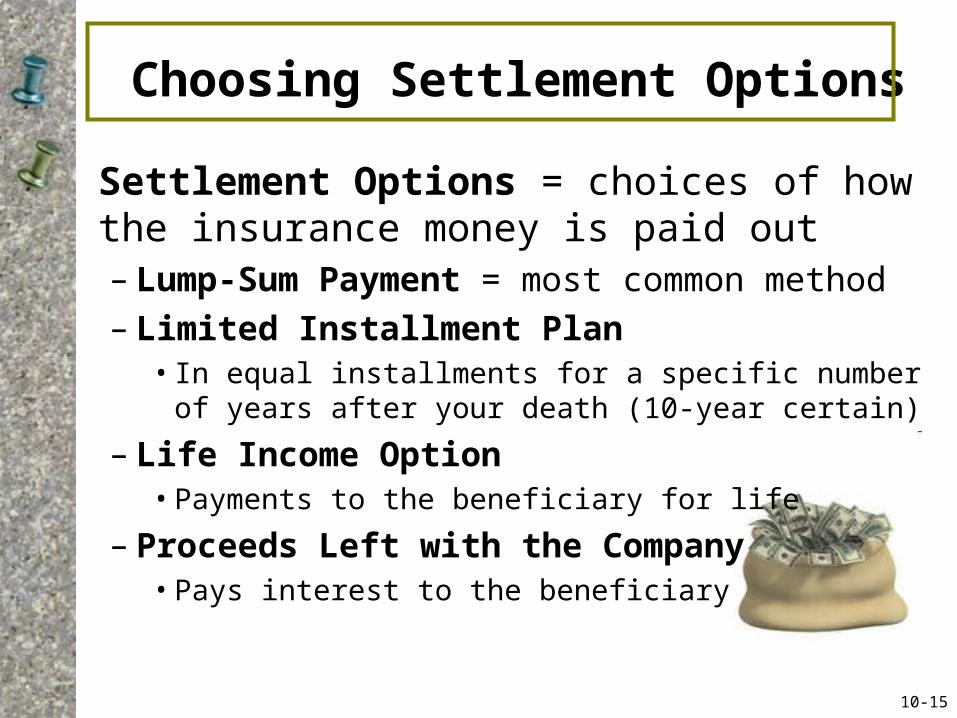

Choosing Settlement Options

Settlement Options = choices of how the insurance money is paid out– Lump-Sum Payment = most common method– Limited Installment Plan

• In equal installments for a specific number of years after your death (10-year certain)

– Life Income Option• Payments to the beneficiary for life

– Proceeds Left with the Company• Pays interest to the beneficiary

10-15

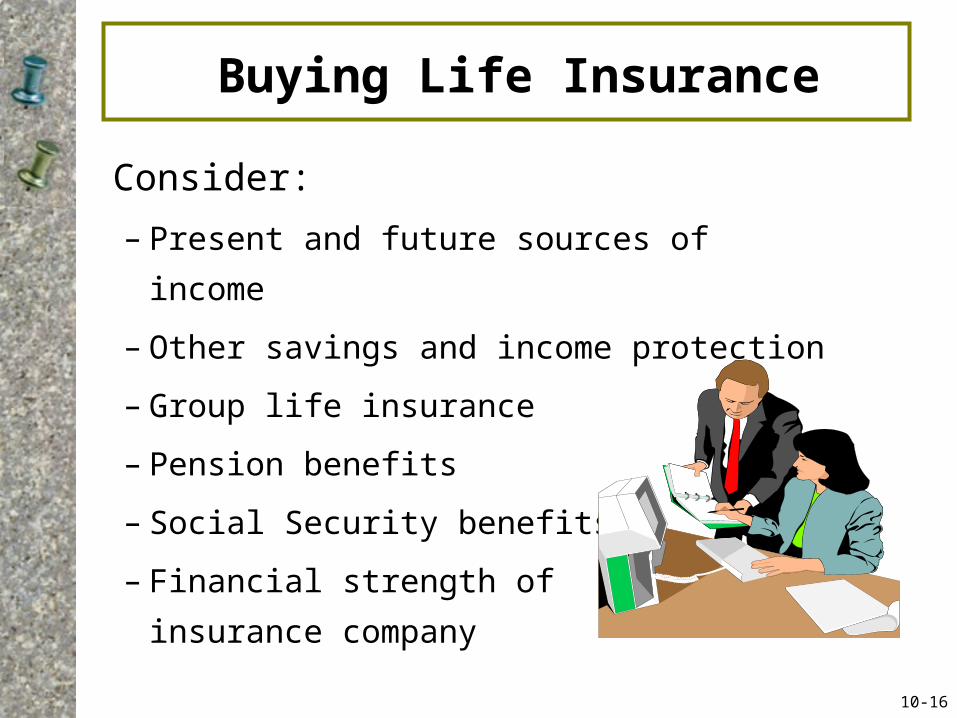

Buying Life Insurance

Consider:

– Present and future sources of income

– Other savings and income protection

– Group life insurance

– Pension benefits

– Social Security benefits

– Financial strength of the

insurance company10-16

Buying Life Insurance

Determine from whom to buy your policy– Examine both private and public sources

– Research the company’s rating by major rating companies:

• A. M. Best

• Standard and Poor’s

• Duff & Phelps

• Moody’s

• Weiss Research

– Talk to friends or colleagues

– Online premium quote services10-17

Choosing an Insurance Agent

• Ask friends, parents, and neighbors for recommendations.

• Does the agent belong to professional groups or is a Chartered Life Underwriter (CLU)?

• Is the agent willing to take the time to answer questions and find a policy that is right for you?

• Does the agent ask about your financial plan?

• Do you feel pressured?• Is the agent available when

needed?10-18

Buying Life Insurance

• Compare policy costs based on:– Company’s cost of doing business– Return on company’s investments– Mortality rate among policyholders– Policy features – Competition from other firms

• Interest-adjusted index – Used to compare policy costs– Lower index = lower cost policy– See sites such as www.quotesmith.com

10-19

Obtaining and Examining a Policy

• First step = apply

• Second step = provide medical history– Usually no physical for a group policy

• Read every word of the contract

• 10-day “free-look” period to change your mind

• Give your beneficiaries and lawyer a photocopy

10-20

Should You Switch Policies?

• Switch if benefits exceed costs of getting another physical and paying policy set-up costs

• The older you are, the higher the premium

• Are you still insurable?• Can you get all the provisions

you want?• Don’t cancel old policy until

new policy is in hand10-21

Objective 4Recognize How Annuities Provide

Financial Security

Financial Planning with Annuities

• An annuity = a financial contract written by an insurance company, providing a regular income

• Can supplement retirement income and shelter income from taxes (tax-deferred)

• Those who expect to live longer than average benefit most from annuities

• Fully fund IRAs and 401(k)s/403(b)s BEFORE considering an annuity (lower costs and tax advantages)

10-22

Why Buy Annuities?

• Provides retirement income for life

• Compounded interest grows tax-free (until money withdrawn)

• No maximum annual contribution (like IRAs)

• Beneficiary guaranteed no less than amount paid in

• Immediate annuity or deferred annuity

Two Types

• Fixed Annuity

– Annuitant receives fixed amount for life

• Variable Annuity

– Amount received depends on investment performance

10-23

Wrap Up

• Chapter Quiz

• Case Study Project Discussion– Form groups– Select cases

• Homework: Concept Checks 10-1, 10-2 (True/False Questions)