Embed Size (px)

Citation preview

1

Jos Gerresewww.ganeshaconsult.nl

The Mobile Commercial Challenge

2

Agenda

• Historic overview• Remedies• Fundamental law of pricing• Infrastructure aspects• Commercial aspects• actors and revenues• Partnering models• Warning• Conclusions

3

Brief Historic Overview 1

• In telecom the Sky was the limit• Governments want piece of the pie• GSM is success; Internet is success

UMTS will be a success too• € 150 billion license costs• € 2000 per capable head in Europe

4

Brief Historic Overview 2

• Infrastructure– Ca. € 125 billion new investments– New handsets– Cell location issues

• End of Hype– Bankruptcies– 550.000 redundancies– Criminal top executives

5

The Remedies 1

• Industry must restore credibility in order to find new investors

• “Newest Economy”: no business without profits

• Develop UMTS applications that satisfy customers so that they render profitable revenues

6

The Remedies 2• Credibility

– Some operators demonstrated possibility to bounce back and find new funding

• Profitability– Competitive environment killed most competitors

• Prices can be raised to profitable levels

• Services and Applications– ?? No killer application– Multi-media messaging– Market segment specific information

7

Fundamental Law of Pricing

• The selling price for any service, goods or application lies between:

– The Minimum level to reach a defined profit to the seller

– The Maximum level being the added business value to the buyer

8

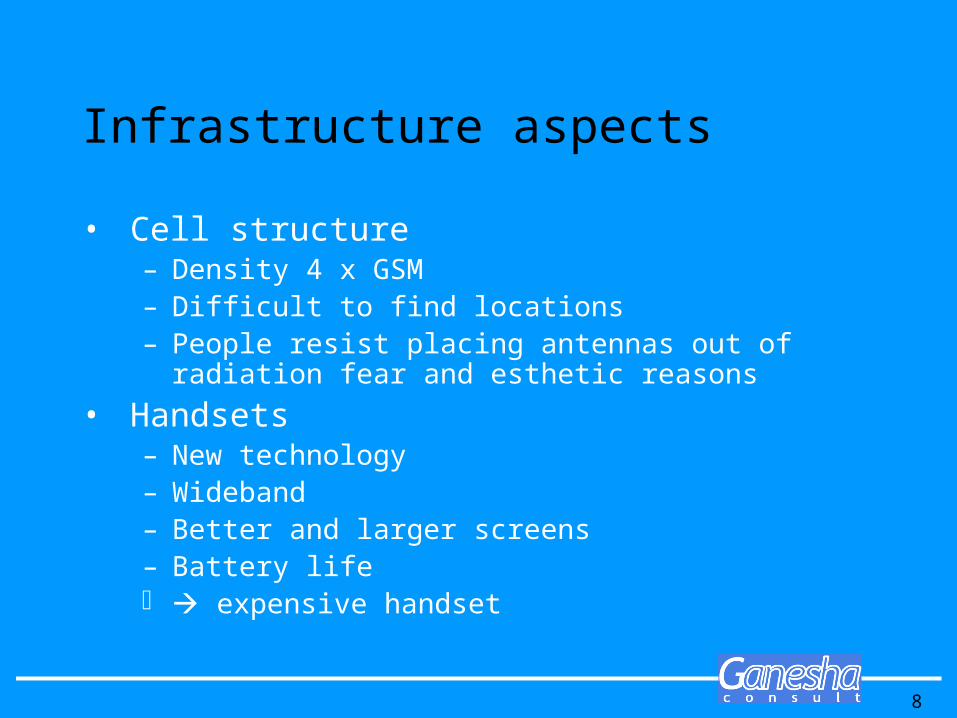

Infrastructure aspects

• Cell structure– Density 4 x GSM– Difficult to find locations– People resist placing antennas out of radiation

fear and esthetic reasons

• Handsets– New technology– Wideband– Better and larger screens– Battery life expensive handset

9

Commercial aspects

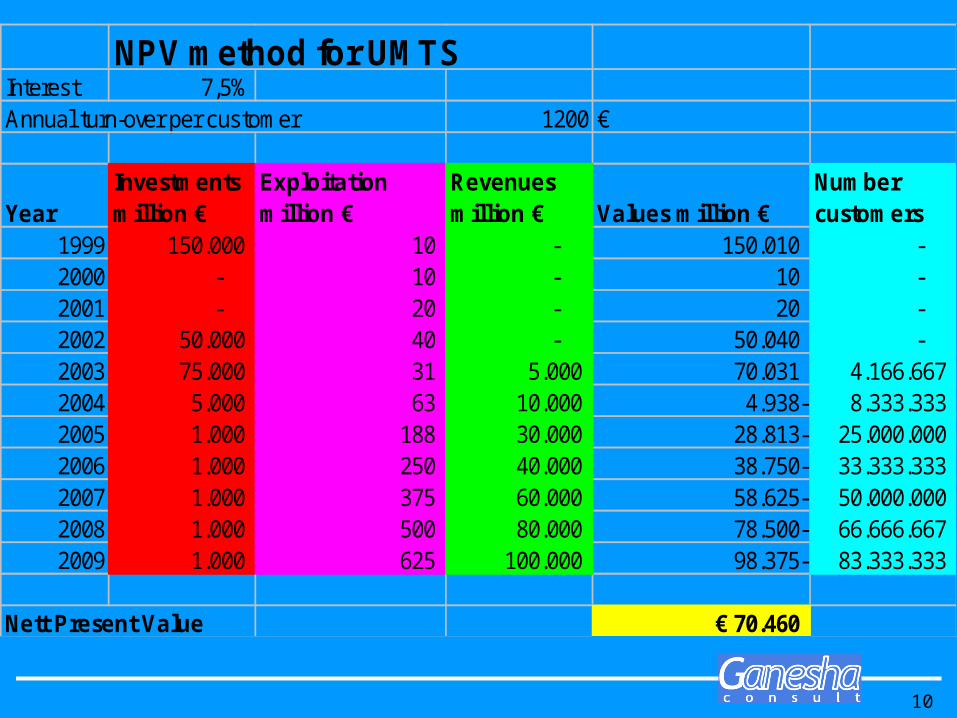

• Can we earn back the € 275 billion ? Quick & Dirty: NPV analysis– Assumptions

• Interest rate 7,5 % • Average annual spend per customer € 1200• Market has 80 million target customers• 1 employee per 10.000 customers € 75.000 p/a• No costs yet for CRM, Billing etc..

10

NPV method for UMTSInterest 7,5%Annual turn-over per customer 1200 €

YearInvestments million €

Exploitation million €

Revenues million € Values million €

Number customers

1999 150.000 10 - 150.010 - 2000 - 10 - 10 - 2001 - 20 - 20 - 2002 50.000 40 - 50.040 - 2003 75.000 31 5.000 70.031 4.166.667 2004 5.000 63 10.000 4.938- 8.333.333 2005 1.000 188 30.000 28.813- 25.000.000 2006 1.000 250 40.000 38.750- 33.333.333 2007 1.000 375 60.000 58.625- 50.000.000 2008 1.000 500 80.000 78.500- 66.666.667 2009 1.000 625 100.000 98.375- 83.333.333

Nett Present Value € 70.460

11

NPV method for UMTS with first License write-offInterest 7,5%Annual turn-over per customer 1200 €

YearInvestments million €

Exploitation million €

Revenues million € Values million €

Number customers

1999 - 10 - 10 - 2000 - 10 - 10 - 2001 - 20 - 20 - 2002 50.000 40 - 50.040 - 2003 75.000 31 5.000 70.031 4.166.667 2004 5.000 63 10.000 4.938- 8.333.333 2005 1.000 188 30.000 28.813- 25.000.000 2006 1.000 250 40.000 38.750- 33.333.333 2007 1.000 375 60.000 58.625- 50.000.000 2008 1.000 500 80.000 78.500- 66.666.667 2009 1.000 625 100.000 98.375- 83.333.333

Nett Present Value € 69.075-

12

Actors and Revenues

• Governments• Licensed Telcos• Telcos with

infrastructure• Application

developers• Hardware

developers• Customers

• Airtime per time unit

• Basic subscriptions

• Service specific subscriptions

• Services pay for use

13

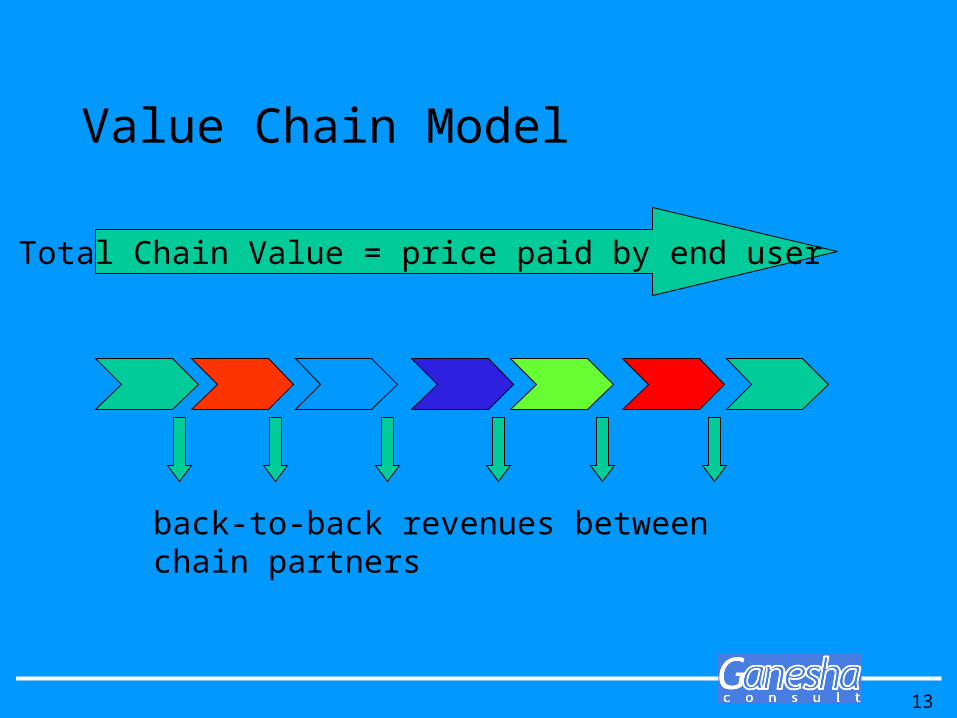

Value Chain Model

Total Chain Value = price paid by end user

back-to-back revenues between chain partners

14

Meshed Interworking Model

Operator

ServiceProvider

Appl.Prov.

CustomerGroup

Operator

Operator

ServiceProvider

ServiceProvider

ServiceProvider

Appl.Prov.

Appl.Prov.

Appl.Prov.

CustomerGroup

CustomerGroup

CustomerGroup

Operator

15

Warning

• We have seen what greed, hype and government forced competition did to the telecom industry

• The power/energy sector is now undergoing the same diseases

• Be aware of your energy supply– If ICT is the oxygen of society than power

supply is the bloodstream• No blood No oxygen !!

16

Conclusions

• Greed, Hype and forced competition brought the industry on its knees

• UMTS is not successful by default• All potential users must use it• A meshed co-operation model has

more chances for success than a chain model

• No profits No business

![Digital CSICdigital.csic.es/bitstream/10261/22884/5/Idolatro_en_unos_ojos.pdf[Tenor] mo mo mo mo vos, vos, vos, vos, vi vi la - jos, jos, jos, jos, ria ria ria ria gra - gra gra -](https://img.pdfslide.us/doc/110x75/6101fc263f4ab80ca032e210/digital-tenor-mo-mo-mo-mo-vos-vos-vos-vos-vi-vi-la-jos-jos-jos-jos-ria.jpg)