Embed Size (px)

Citation preview

1

Establishing an Emerging Manager Fund

Emerging Manager Program

1

2

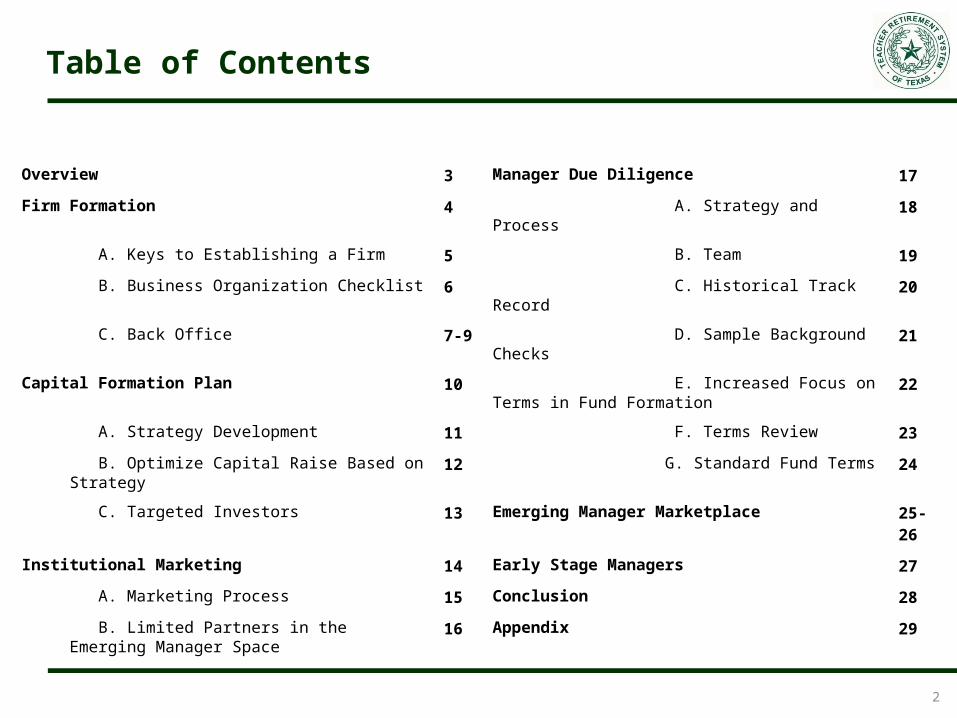

Overview 3 Manager Due Diligence 17

Firm Formation 4 A. Strategy and Process 18

A. Keys to Establishing a Firm 5 B. Team 19

B. Business Organization Checklist 6 C. Historical Track Record 20

C. Back Office 7-9 D. Sample Background Checks 21

Capital Formation Plan 10 E. Increased Focus on Terms in Fund Formation 22

A. Strategy Development 11 F. Terms Review 23

B. Optimize Capital Raise Based on Strategy 12 G. Standard Fund Terms 24

C. Targeted Investors 13 Emerging Manager Marketplace 25-26

Institutional Marketing 14 Early Stage Managers 27

A. Marketing Process 15 Conclusion 28

B. Limited Partners in the Emerging Manager Space 16 Appendix 29

Table of Contents

3

Overview

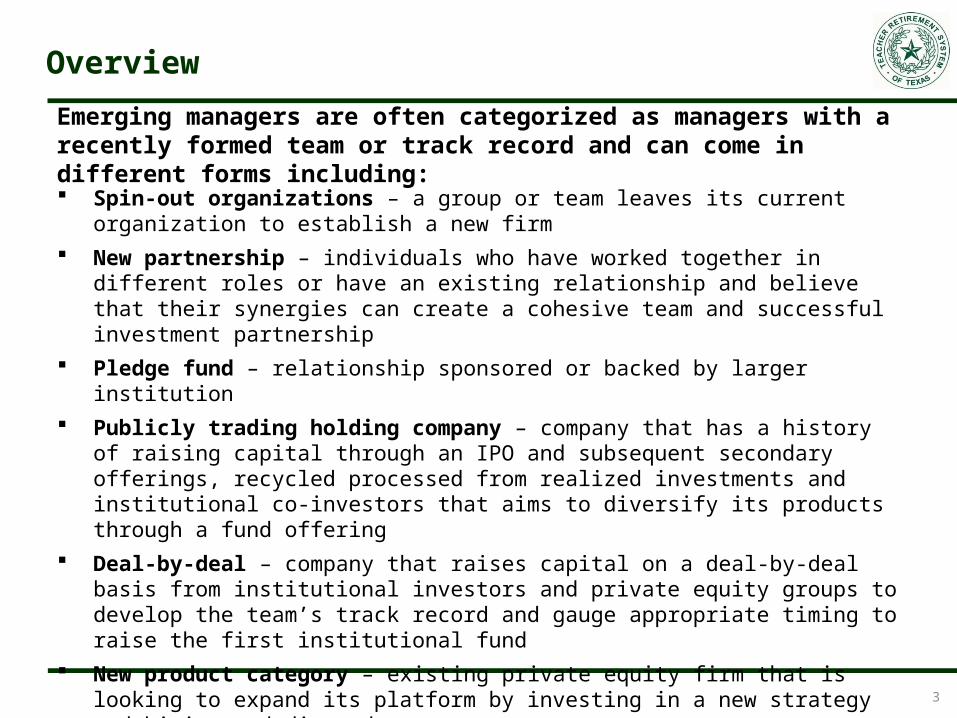

Spin-out organizations – a group or team leaves its current organization to establish a new firm

New partnership – individuals who have worked together in different roles or have an existing relationship and believe that their synergies can create a cohesive team and successful investment partnership

Pledge fund – relationship sponsored or backed by larger institution Publicly trading holding company – company that has a history of raising capital through an

IPO and subsequent secondary offerings, recycled processed from realized investments and institutional co-investors that aims to diversify its products through a fund offering

Deal-by-deal – company that raises capital on a deal-by-deal basis from institutional investors and private equity groups to develop the team’s track record and gauge appropriate timing to raise the first institutional fund

New product category – existing private equity firm that is looking to expand its platform by investing in a new strategy and hiring a dedicated team

Emerging managers are often categorized as managers with a recently formed team or track record and can come in different forms including:

4

Firm Formation

5

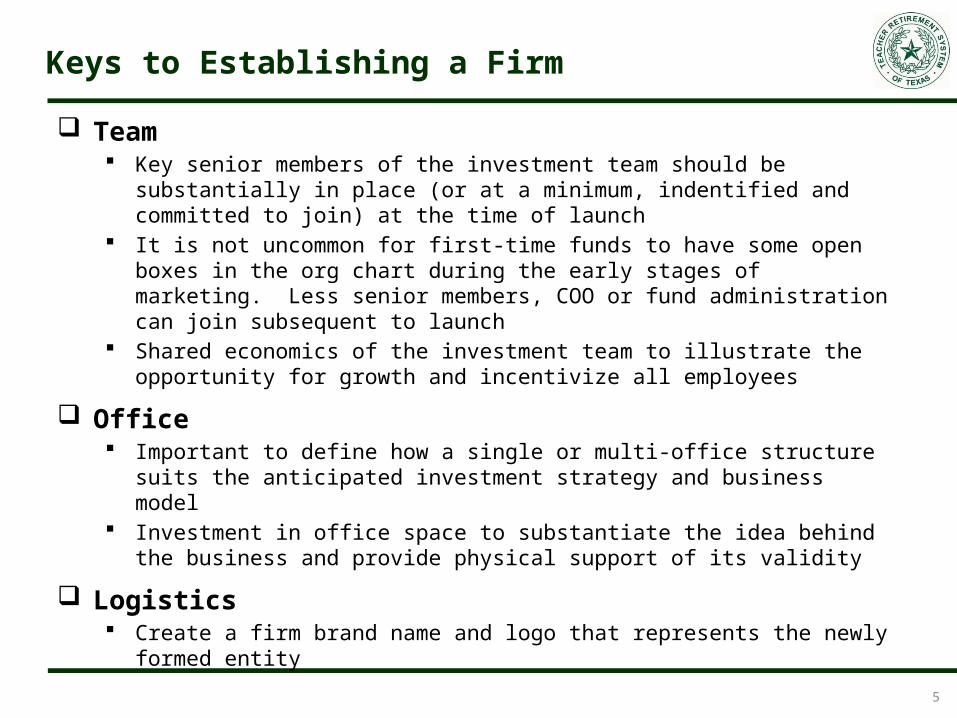

Keys to Establishing a Firm

Team Key senior members of the investment team should be substantially in place (or at a

minimum, indentified and committed to join) at the time of launch It is not uncommon for first-time funds to have some open boxes in the org chart during

the early stages of marketing. Less senior members, COO or fund administration can join subsequent to launch

Shared economics of the investment team to illustrate the opportunity for growth and incentivize all employees

Office Important to define how a single or multi-office structure suits the anticipated

investment strategy and business model Investment in office space to substantiate the idea behind the business and provide

physical support of its validity

Logistics Create a firm brand name and logo that represents the newly formed entity

6

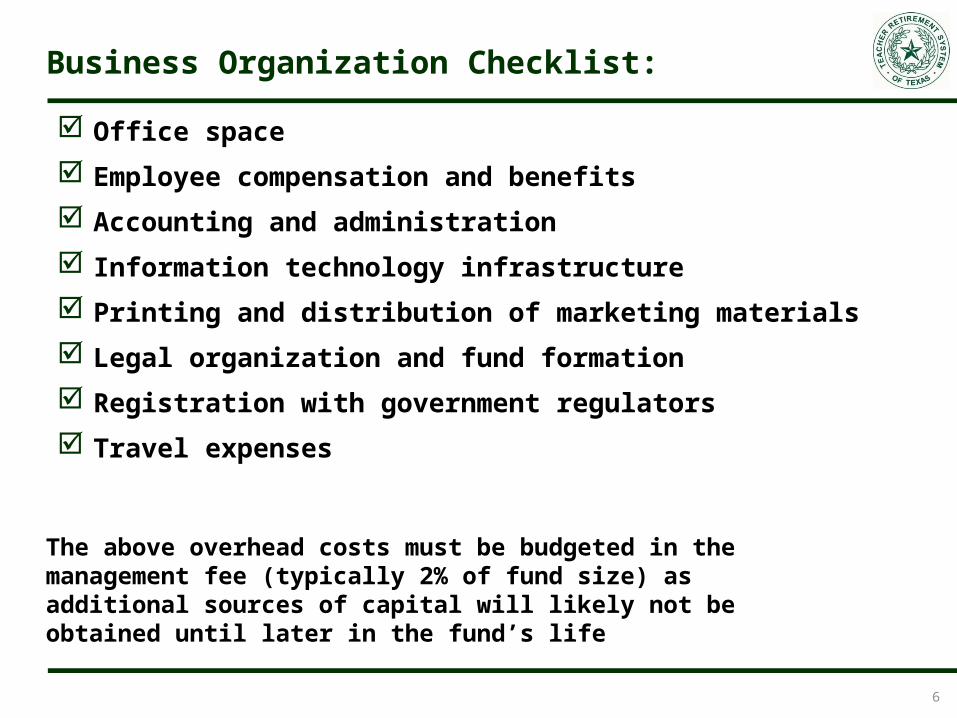

Business Organization Checklist:

Office space

Employee compensation and benefits

Accounting and administration

Information technology infrastructure

Printing and distribution of marketing materials

Legal organization and fund formation

Registration with government regulators

Travel expenses

The above overhead costs must be budgeted in the management fee (typically 2% of fund size) as additional sources of capital will likely not be obtained until later in the fund’s life

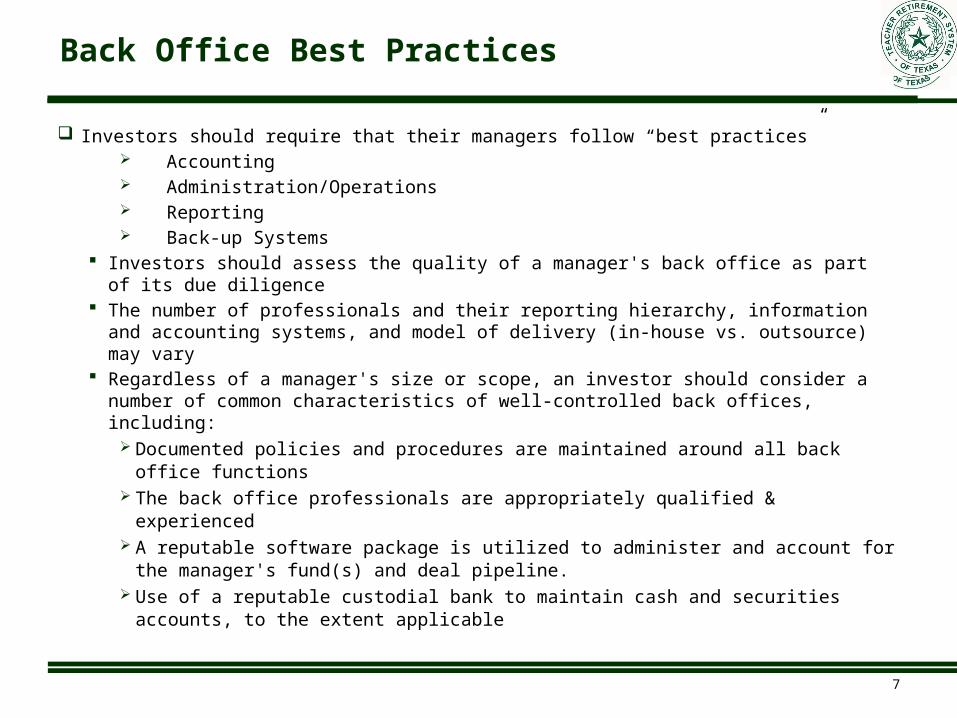

Investors should require that their managers follow “best practices” Accounting Administration/Operations Reporting Back-up Systems

Investors should assess the quality of a manager's back office as part of its due diligence

The number of professionals and their reporting hierarchy, information and accounting systems, and model of delivery (in-house vs. outsource) may vary

Regardless of a manager's size or scope, an investor should consider a number of common characteristics of well-controlled back offices, including:

Documented policies and procedures are maintained around all back office functions

The back office professionals are appropriately qualified & experienced A reputable software package is utilized to administer and account for the

manager's fund(s) and deal pipeline. Use of a reputable custodial bank to maintain cash and securities accounts, to the

extent applicable

7

Back Office Best Practices

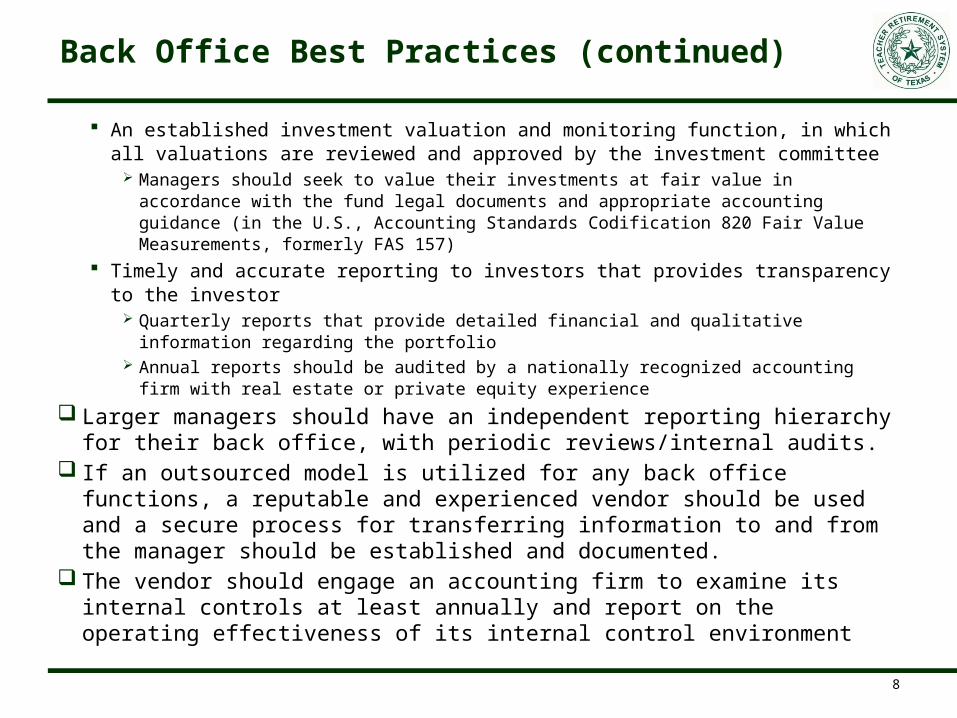

An established investment valuation and monitoring function, in which all valuations are reviewed and approved by the investment committee

Managers should seek to value their investments at fair value in accordance with the fund legal documents and appropriate accounting guidance (in the U.S., Accounting Standards Codification 820 Fair Value Measurements, formerly FAS 157)

Timely and accurate reporting to investors that provides transparency to the investor Quarterly reports that provide detailed financial and qualitative information regarding the

portfolio Annual reports should be audited by a nationally recognized accounting firm with real

estate or private equity experience Larger managers should have an independent reporting hierarchy for their

back office, with periodic reviews/internal audits. If an outsourced model is utilized for any back office functions, a reputable and

experienced vendor should be used and a secure process for transferring information to and from the manager should be established and documented.

The vendor should engage an accounting firm to examine its internal controls at least annually and report on the operating effectiveness of its internal control environment

8

Back Office Best Practices (continued)

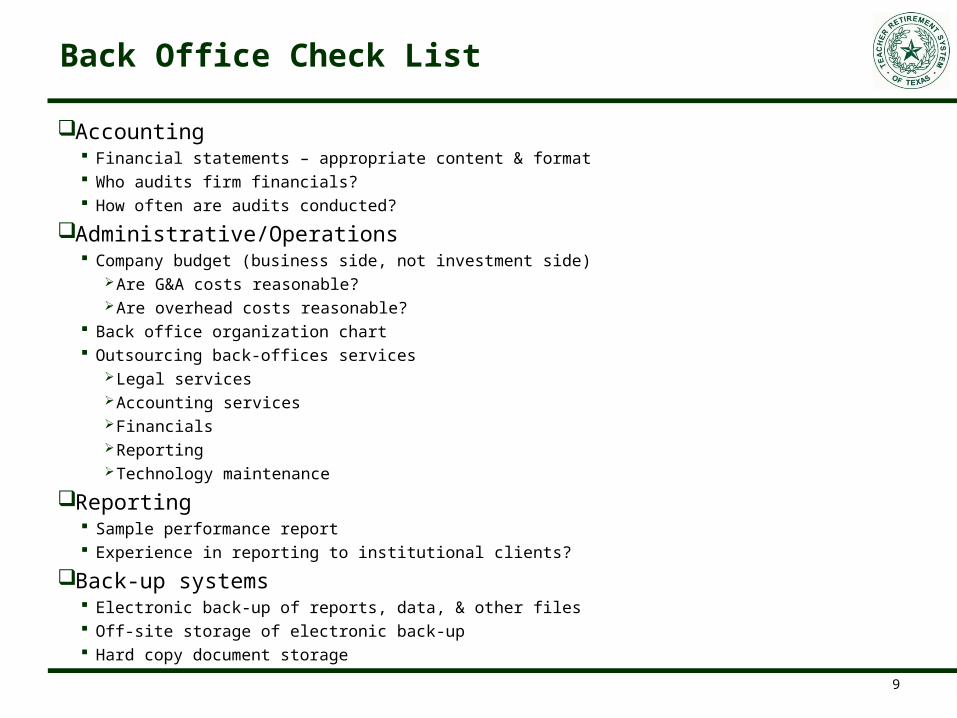

Accounting Financial statements – appropriate content & format Who audits firm financials? How often are audits conducted?

Administrative/Operations Company budget (business side, not investment side)

Are G&A costs reasonable? Are overhead costs reasonable?

Back office organization chart Outsourcing back-offices services

Legal services Accounting services Financials Reporting Technology maintenance

Reporting Sample performance report Experience in reporting to institutional clients?

Back-up systems Electronic back-up of reports, data, & other files Off-site storage of electronic back-up Hard copy document storage

9

Back Office Check List

10

Capital Formation Plan

Managers Should Develop and Communicate a Clearly Defined Strategy to Access Capital Needs

How Do You Make Money? Why Do You Make Money on Your Strategy? When do You Make Money? Why are You Best Suited to Execute Your Strategy? What is the End Goal for Your Strategy and Your Business? How Many Quarters and Years to Get There? Have you Built Out a Timeline and Cost Projections?

11

Strategy Development

12

Optimize Capital Raise Based on Strategy

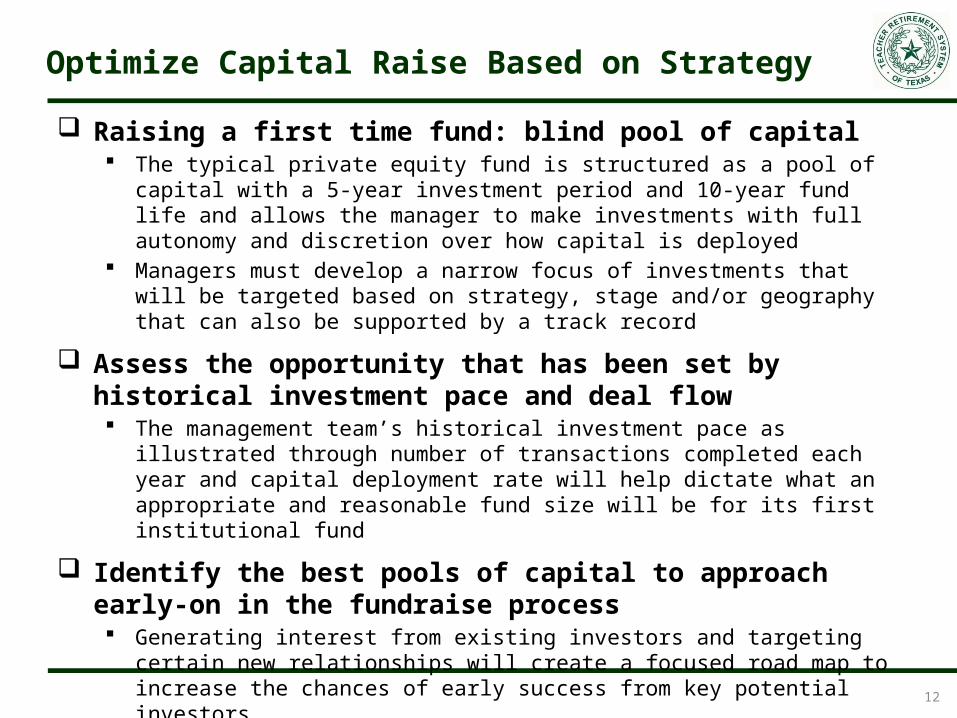

Raising a first time fund: blind pool of capital The typical private equity fund is structured as a pool of capital with a 5-year investment

period and 10-year fund life and allows the manager to make investments with full autonomy and discretion over how capital is deployed

Managers must develop a narrow focus of investments that will be targeted based on strategy, stage and/or geography that can also be supported by a track record

Assess the opportunity that has been set by historical investment pace and deal flow The management team’s historical investment pace as illustrated through number of

transactions completed each year and capital deployment rate will help dictate what an appropriate and reasonable fund size will be for its first institutional fund

Identify the best pools of capital to approach early-on in the fundraise process Generating interest from existing investors and targeting certain new relationships will

create a focused road map to increase the chances of early success from key potential investors

13

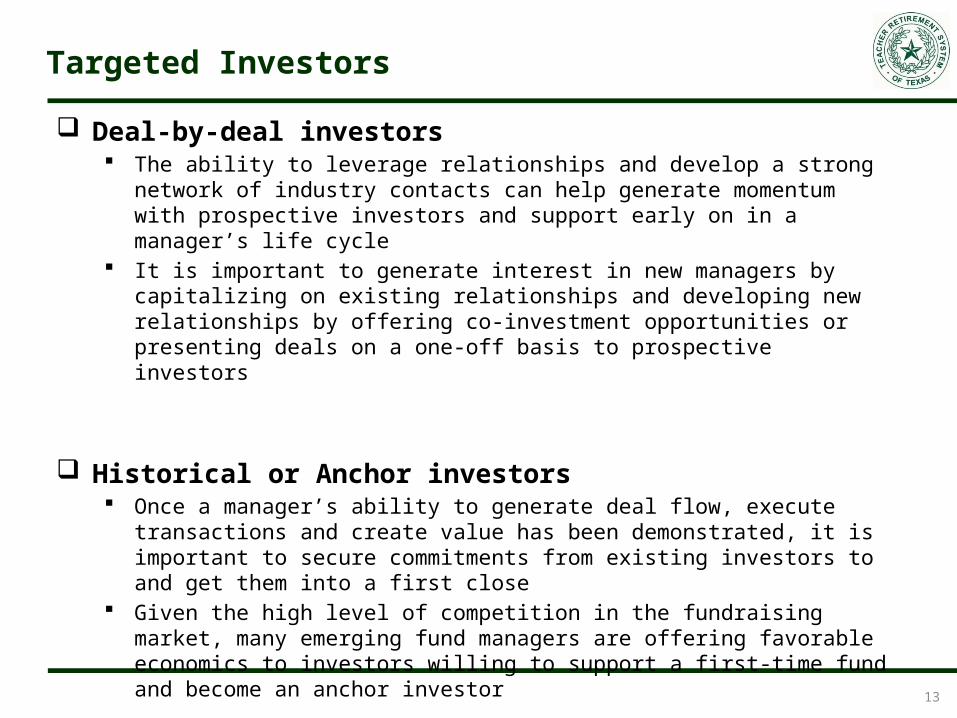

Targeted Investors

Deal-by-deal investors The ability to leverage relationships and develop a strong network of industry contacts

can help generate momentum with prospective investors and support early on in a manager’s life cycle

It is important to generate interest in new managers by capitalizing on existing relationships and developing new relationships by offering co-investment opportunities or presenting deals on a one-off basis to prospective investors

Historical or Anchor investors Once a manager’s ability to generate deal flow, execute transactions and create value

has been demonstrated, it is important to secure commitments from existing investors to and get them into a first close

Given the high level of competition in the fundraising market, many emerging fund managers are offering favorable economics to investors willing to support a first-time fund and become an anchor investor

14

Institutional Marketing

15

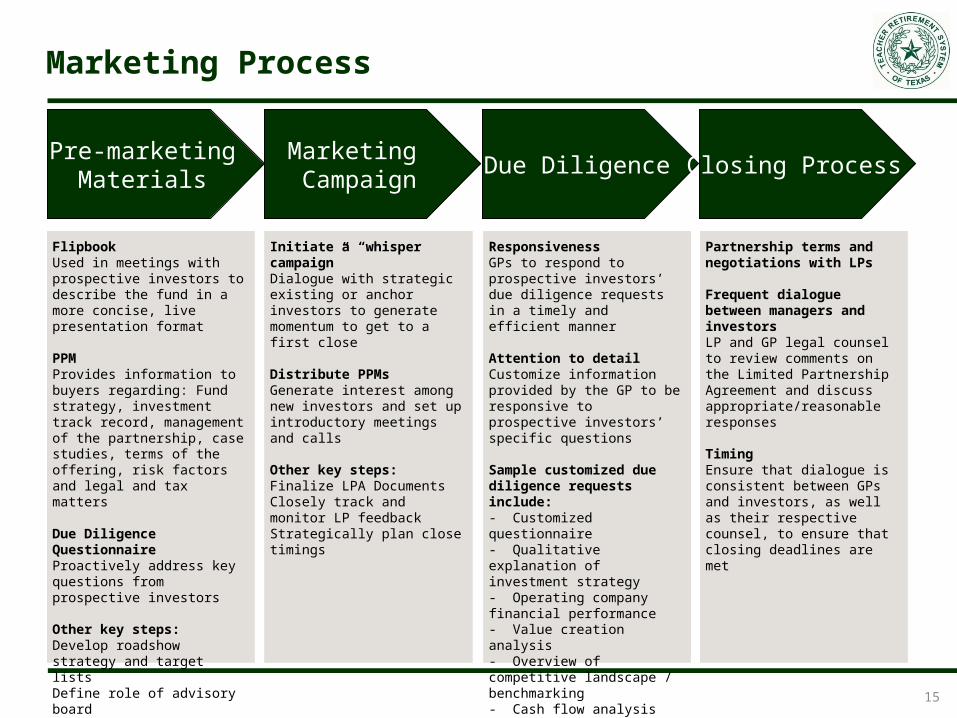

Marketing Process

Pre-marketingMaterials

Marketing Campaign Due Diligence Closing Process

FlipbookUsed in meetings with prospective investors to describe the fund in a more concise, live presentation format

PPM Provides information to buyers regarding: Fund strategy, investment track record, management of the partnership, case studies, terms of the offering, risk factors and legal and tax matters

Due Diligence QuestionnaireProactively address key questions from prospective investors

Other key steps:Develop roadshow strategy and target listsDefine role of advisory board

Initiate a “whisper campaign”Dialogue with strategic existing or anchor investors to generate momentum to get to a first close

Distribute PPMsGenerate interest among new investors and set up introductory meetings and calls

Other key steps:Finalize LPA Documents Closely track and monitor LP feedbackStrategically plan close timings

ResponsivenessGPs to respond to prospective investors’ due diligence requests in a timely and efficient manner

Attention to detailCustomize information provided by the GP to be responsive to prospective investors’ specific questions

Sample customized due diligence requests include:- Customized questionnaire- Qualitative explanation of investment strategy- Operating company financial performance- Value creation analysis- Overview of competitive landscape / benchmarking- Cash flow analysis- Reference information- Market data- Details on changes to terms and conditions since the GP’s prior fund

Partnership terms and negotiations with LPs

Frequent dialogue between managers and investorsLP and GP legal counsel to review comments on the Limited Partnership Agreement and discuss appropriate/reasonable responses

TimingEnsure that dialogue is consistent between GPs and investors, as well as their respective counsel, to ensure that closing deadlines are met

16

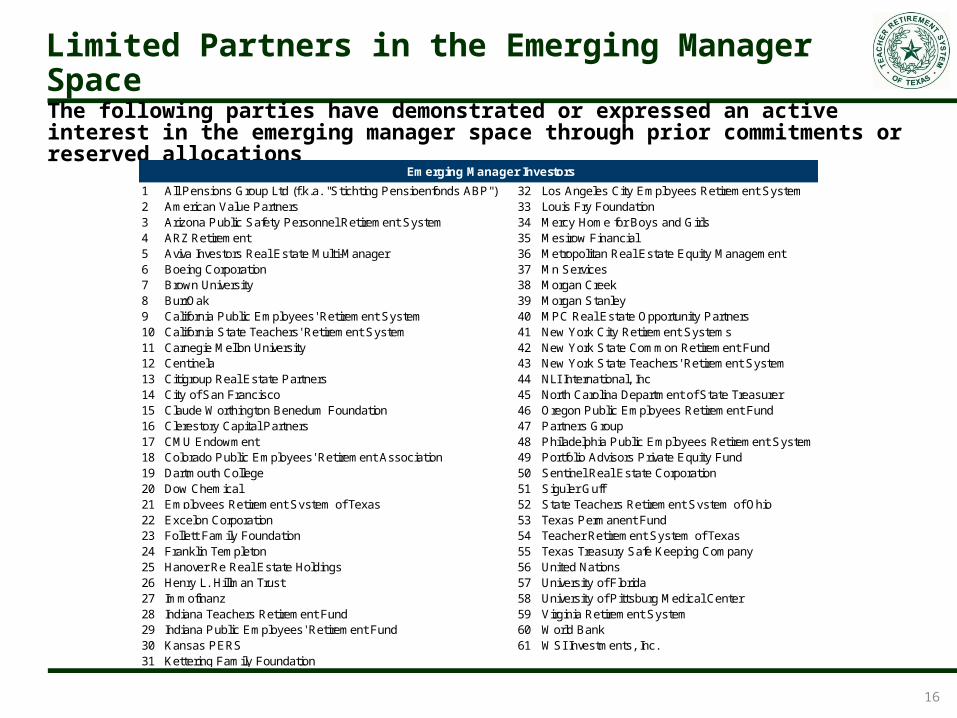

Limited Partners in the Emerging Manager Space

The following parties have demonstrated or expressed an active interest in the emerging manager space through prior commitments or reserved allocations

1 All Pensions Group Ltd (f.k.a. "Stichting Pensioenfonds ABP") 32 Los Angeles City Employees Retirement System2 American Value Partners 33 Louis Fry Foundation3 Arizona Public Safety Personnel Retirement System 34 Mercy Home for Boys and Girls4 ARZ Retirement 35 Mesirow Financial5 Aviva Investors Real Estate Multi-Manager 36 Metropolitan Real Estate Equity Management6 Boeing Corporation 37 Mn Services 7 Brown University 38 Morgan Creek8 BurrOak 39 Morgan Stanley9 California Public Employees' Retirement System 40 MPC Real Estate Opportunity Partners10 California State Teachers' Retirement System 41 New York City Retirement Systems11 Carnegie Mellon University 42 New York State Common Retirement Fund12 Centinela 43 New York State Teachers' Retirement System13 Citigroup Real Estate Partners 44 NLI International, Inc 14 City of San Francisco 45 North Carolina Department of State Treasurer15 Claude Worthington Benedum Foundation 46 Oregon Public Employees Retirement Fund16 Clerestory Capital Partners 47 Partners Group17 CMU Endowment 48 Philadelphia Public Employees Retirement System18 Colorado Public Employees' Retirement Association 49 Portfolio Advisors Private Equity Fund 19 Dartmouth College 50 Sentinel Real Estate Corporation20 Dow Chemical 51 Siguler Guff21 Employees Retirement System of Texas 52 State Teachers Retirement System of Ohio22 Excelon Corporation 53 Texas Permanent Fund23 Follett Family Foundation 54 Teacher Retirement System of Texas24 Franklin Templeton 55 Texas Treasury Safe Keeping Company25 Hanover Re Real Estate Holdings 56 United Nations26 Henry L. Hillman Trust 57 University of Florida27 Immofinanz 58 University of Pittsburg Medical Center28 Indiana Teachers Retirement Fund 59 Virginia Retirement System29 Indiana Public Employees' Retirement Fund 60 World Bank30 Kansas PERS 61 WSI Investments, Inc.31 Kettering Family Foundation

Emerging Manager Investors

17

Manager Due Diligence

18

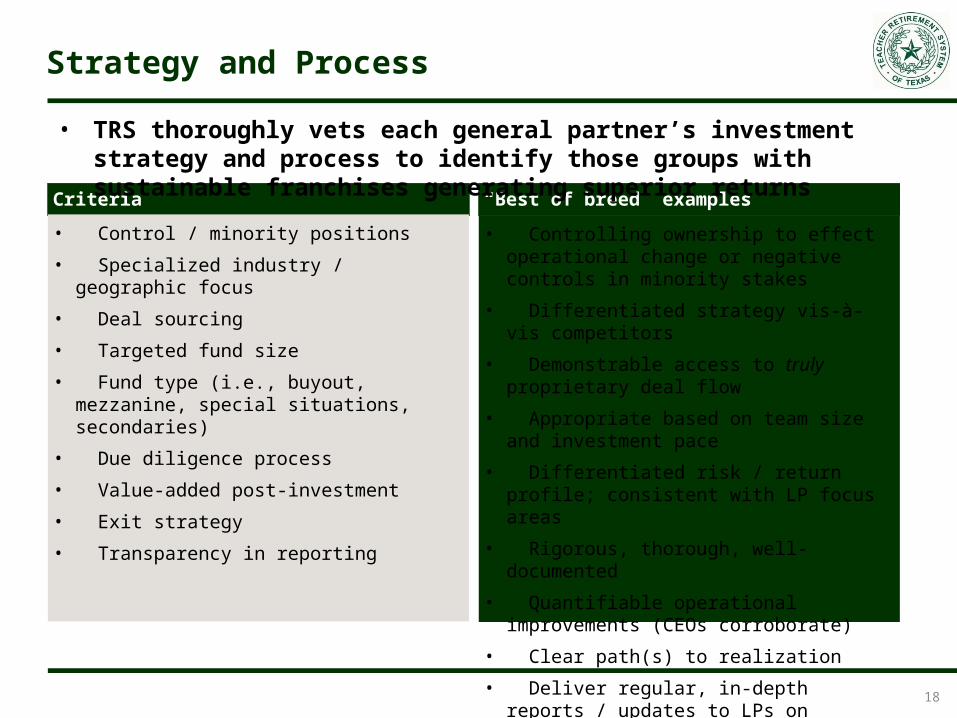

Strategy and Process

Criteria “Best of breed” examples

• Control / minority positions

• Specialized industry / geographic focus

• Deal sourcing

• Targeted fund size

• Fund type (i.e., buyout, mezzanine, special situations, secondaries)

• Due diligence process

• Value-added post-investment

• Exit strategy

• Transparency in reporting

• Controlling ownership to effect operational change or negative controls in minority stakes

• Differentiated strategy vis-à-vis competitors

• Demonstrable access to truly proprietary deal flow

• Appropriate based on team size and investment pace

• Differentiated risk / return profile; consistent with LP focus areas

• Rigorous, thorough, well-documented

• Quantifiable operational improvements (CEOs corroborate)

• Clear path(s) to realization

• Deliver regular, in-depth reports / updates to LPs on portfolio company and fund level performance

• TRS thoroughly vets each general partner’s investment strategy and process to identify those groups with sustainable franchises generating superior returns

19

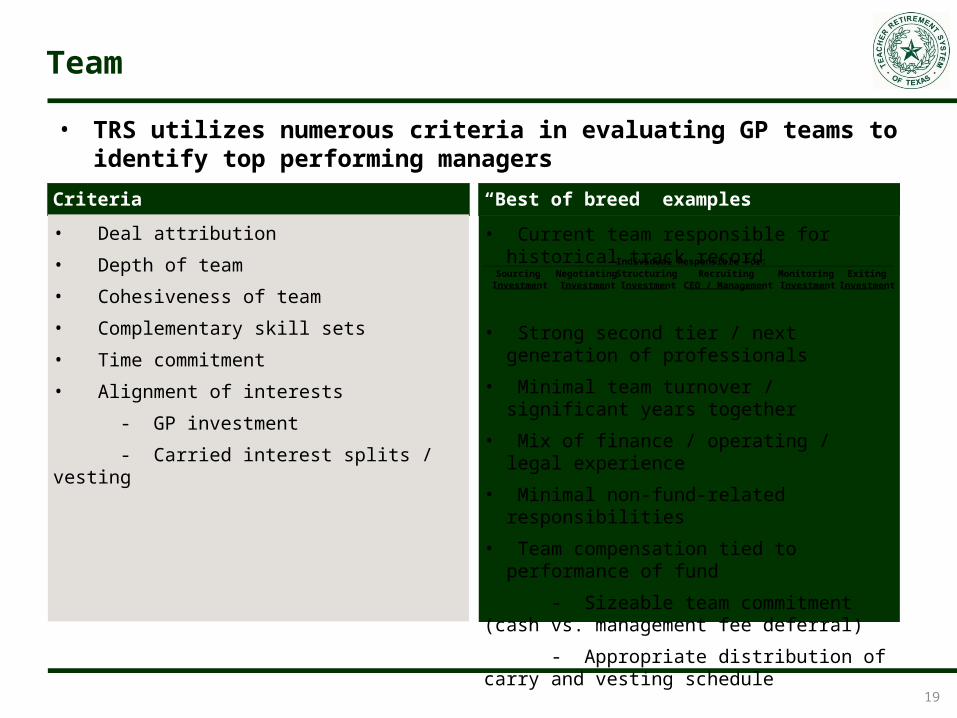

Team

Criteria “Best of breed” examples

• Deal attribution

• Depth of team

• Cohesiveness of team

• Complementary skill sets

• Time commitment

• Alignment of interests

- GP investment

- Carried interest splits / vesting

• Current team responsible for historical track record

• Strong second tier / next generation of professionals

• Minimal team turnover / significant years together

• Mix of finance / operating / legal experience

• Minimal non-fund-related responsibilities

• Team compensation tied to performance of fund

- Sizeable team commitment (cash vs. management fee deferral)

- Appropriate distribution of carry and vesting schedule

• TRS utilizes numerous criteria in evaluating GP teams to identify top performing managers

Individual Responsible For: Sourcing Negotiating Structuring Recruiting Monitoring Exiting

Investment Investment Investment CEO / Management Investment Investment

20

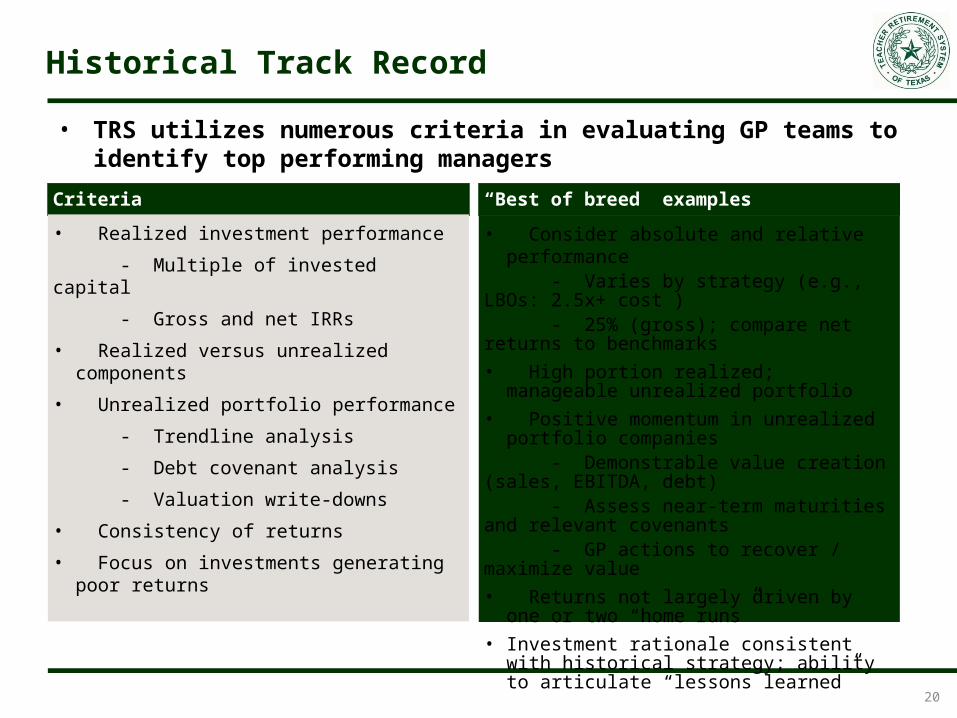

Historical Track Record

Criteria “Best of breed” examples

• Realized investment performance

- Multiple of invested capital

- Gross and net IRRs

• Realized versus unrealized components

• Unrealized portfolio performance

- Trendline analysis

- Debt covenant analysis

- Valuation write-downs

• Consistency of returns

• Focus on investments generating poor returns

• Consider absolute and relative performance - Varies by strategy (e.g., LBOs: 2.5x+ cost ) - 25% (gross); compare net returns to benchmarks• High portion realized; manageable unrealized

portfolio• Positive momentum in unrealized portfolio

companies - Demonstrable value creation (sales, EBITDA, debt) - Assess near-term maturities and relevant covenants - GP actions to recover / maximize value• Returns not largely driven by one or two “home

runs”• Investment rationale consistent with historical

strategy; ability to articulate “lessons learned”

• TRS utilizes numerous criteria in evaluating GP teams to identify top performing managers

21

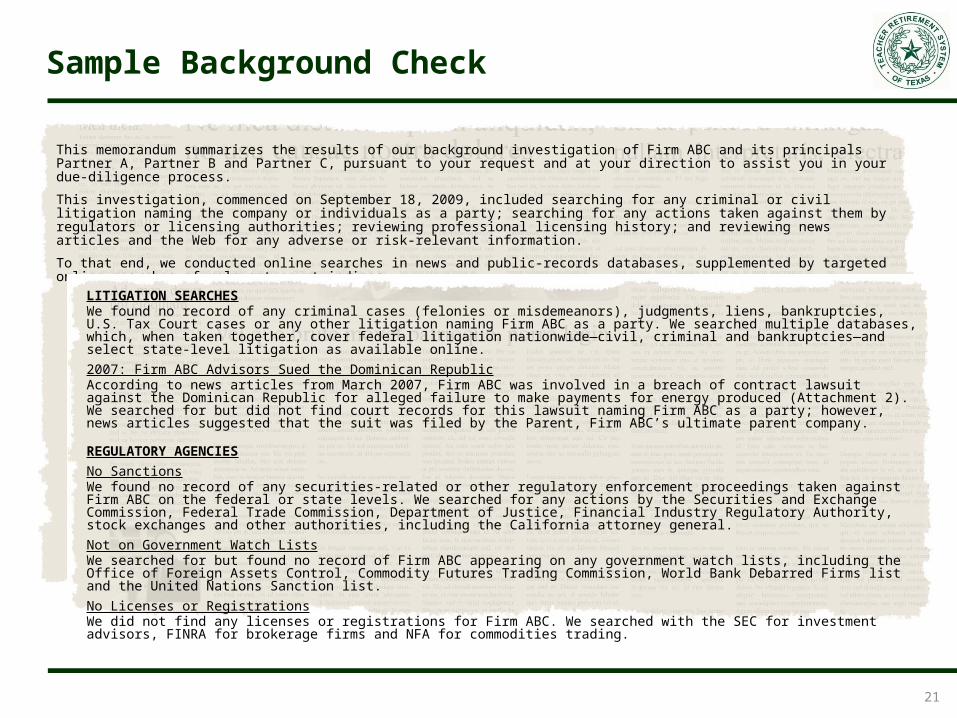

Sample Background Check

This memorandum summarizes the results of our background investigation of Firm ABC and its principals Partner A, Partner B and Partner C, pursuant to your request and at your direction to assist you in your due-diligence process.

This investigation, commenced on September 18, 2009, included searching for any criminal or civil litigation naming the company or individuals as a party; searching for any actions taken against them by regulators or licensing authorities; reviewing professional licensing history; and reviewing news articles and the Web for any adverse or risk-relevant information.

To that end, we conducted online searches in news and public-records databases, supplemented by targeted online searches of relevant court indices.

LITIGATION SEARCHESWe found no record of any criminal cases (felonies or misdemeanors), judgments, liens, bankruptcies, U.S. Tax Court cases or any other litigation naming Firm ABC as a party. We searched multiple databases, which, when taken together, cover federal litigation nationwide—civil, criminal and bankruptcies—and select state-level litigation as available online.

2007: Firm ABC Advisors Sued the Dominican RepublicAccording to news articles from March 2007, Firm ABC was involved in a breach of contract lawsuit against the Dominican Republic for alleged failure to make payments for energy produced (Attachment 2). We searched for but did not find court records for this lawsuit naming Firm ABC as a party; however, news articles suggested that the suit was filed by the Parent, Firm ABC’s ultimate parent company.

REGULATORY AGENCIES

No SanctionsWe found no record of any securities-related or other regulatory enforcement proceedings taken against Firm ABC on the federal or state levels. We searched for any actions by the Securities and Exchange Commission, Federal Trade Commission, Department of Justice, Financial Industry Regulatory Authority, stock exchanges and other authorities, including the California attorney general.

Not on Government Watch ListsWe searched for but found no record of Firm ABC appearing on any government watch lists, including the Office of Foreign Assets Control, Commodity Futures Trading Commission, World Bank Debarred Firms list and the United Nations Sanction list.

No Licenses or RegistrationsWe did not find any licenses or registrations for Firm ABC. We searched with the SEC for investment advisors, FINRA for brokerage firms and NFA for commodities trading.

22

Increased Focus on Terms in Fund Formation

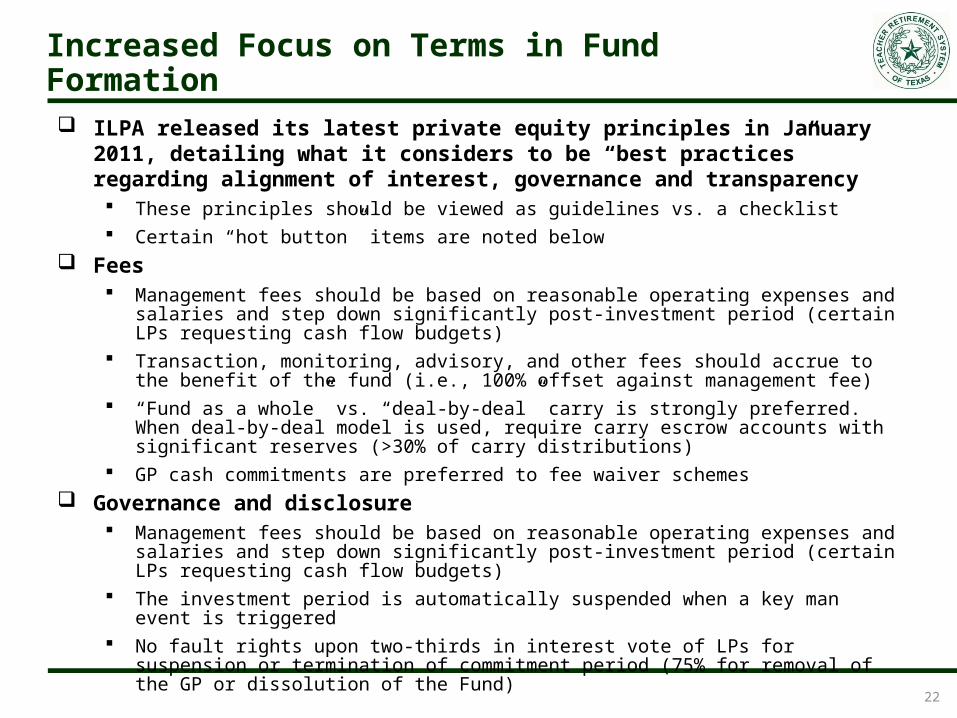

ILPA released its latest private equity principles in January 2011, detailing what it considers to be “best practices” regarding alignment of interest, governance and transparency These principles should be viewed as guidelines vs. a checklist Certain “hot button” items are noted below

Fees Management fees should be based on reasonable operating expenses and salaries and step down

significantly post-investment period (certain LPs requesting cash flow budgets) Transaction, monitoring, advisory, and other fees should accrue to the benefit of the fund (i.e., 100%

offset against management fee) “Fund as a whole” vs. “deal-by-deal” carry is strongly preferred. When deal-by-deal model is used,

require carry escrow accounts with significant reserves (>30% of carry distributions) GP cash commitments are preferred to fee waiver schemes

Governance and disclosure Management fees should be based on reasonable operating expenses and salaries and step down

significantly post-investment period (certain LPs requesting cash flow budgets) The investment period is automatically suspended when a key man event is triggered No fault rights upon two-thirds in interest vote of LPs for suspension or termination of commitment

period (75% for removal of the GP or dissolution of the Fund)

23

Terms Review

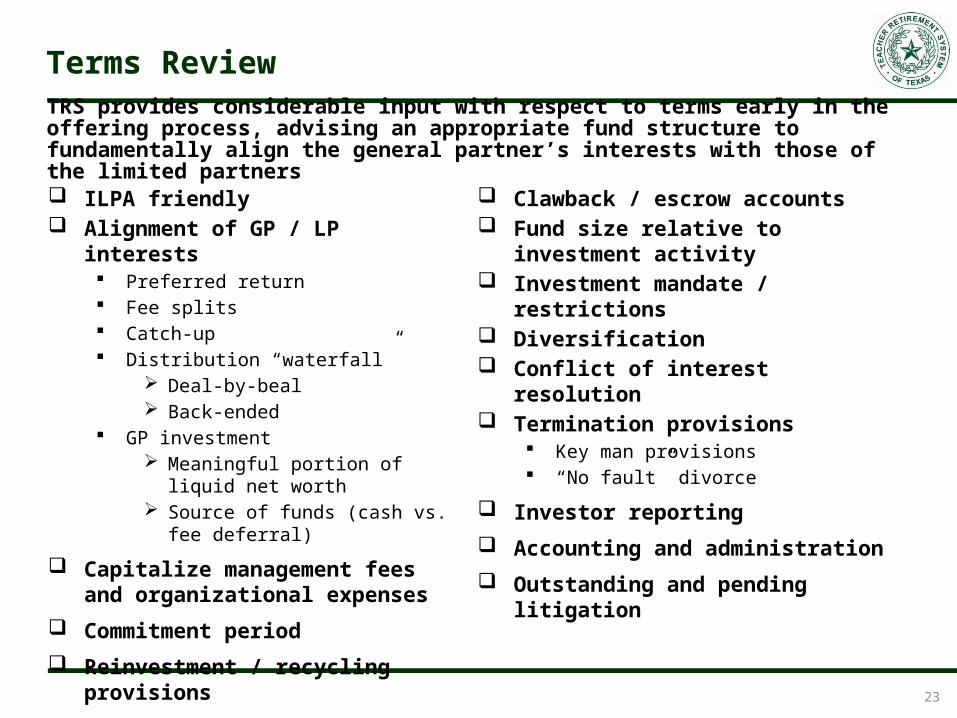

ILPA friendly Alignment of GP / LP interests

Preferred return Fee splits Catch-up Distribution “waterfall”

Deal-by-beal Back-ended

GP investment Meaningful portion of liquid net worth Source of funds (cash vs. fee deferral)

Capitalize management fees and organizational expenses

Commitment period

Reinvestment / recycling provisions

TRS provides considerable input with respect to terms early in the offering process, advising an appropriate fund structure to fundamentally align the general partner’s interests with those of the limited partners

Clawback / escrow accounts Fund size relative to investment activity Investment mandate / restrictions Diversification Conflict of interest resolution Termination provisions

Key man provisions “No fault” divorce

Investor reporting

Accounting and administration

Outstanding and pending litigation

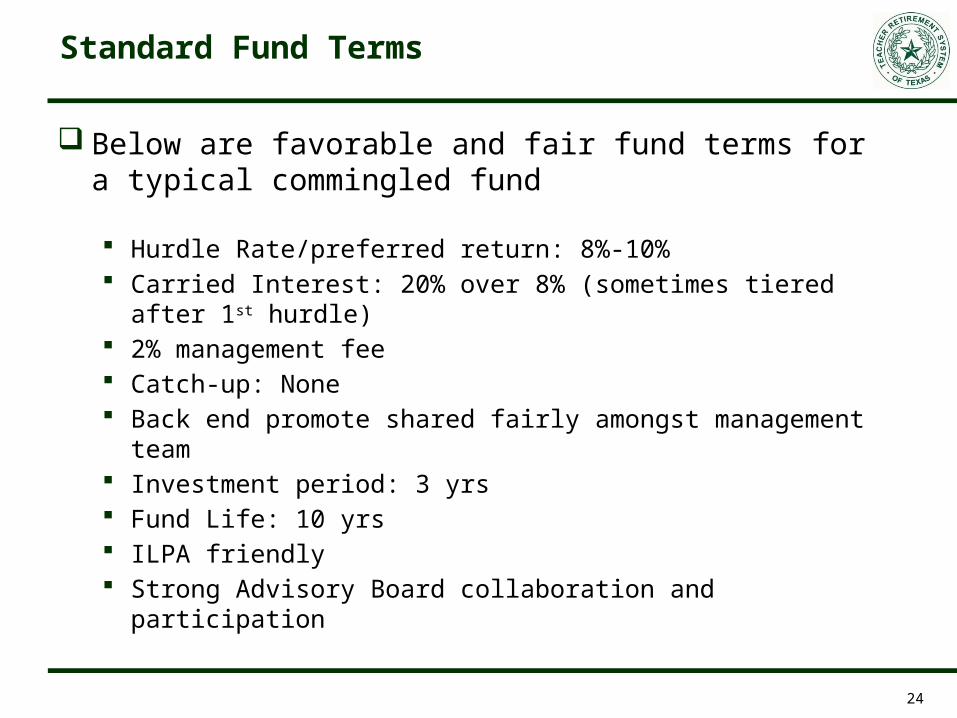

Below are favorable and fair fund terms for a typical commingled fund

Hurdle Rate/preferred return: 8%-10% Carried Interest: 20% over 8% (sometimes tiered after 1st hurdle) 2% management fee Catch-up: None Back end promote shared fairly amongst management team Investment period: 3 yrs Fund Life: 10 yrs ILPA friendly Strong Advisory Board collaboration and participation

24

Standard Fund Terms

25

Emerging Manager Marketplace: Making it to the Finish Line

Who is closing and why A mixture of 1st, 2nd and 3rd time funds Those with successful closings tend to have all or mostly all of the following

characteristics:Clarity of strategyDirect and exceptional operating experienceStrong and attributable track recordInstitutional quality fund and institutional relationshipsExceptional performance in niche plays like senior and student housingWell poised to take advantage of today’s opportunities

Terms of successful closings These funds have quickly gotten to LP friendly terms, generally comprising:

8% hurdle with no catch up9-10% hurdle with a catch up, but often only after a second hurdle of 13-14% gross IRR Back ended promote across the management teamILPA friendlyStrong advisory board rights

26

Emerging Manager Marketplace: Why Many Can’t Get Traction

Common problems Crowded space: Many managers have strategies that are indistinguishable from others and do not have a compelling

story. Multifamily operators in particular have suffered in this respect - buying properties in similar markets at sub 6% cap rates without a distinguishable means to achieve superior returns

Confusing/unfocused strategy: Many managers simply want to buy everything and lack focus & a clear value added strategy

Allocators: Many managers are allocating capital to local managers. While a few have made this a compelling approach, most have not done so

Insufficient track record: Particularly challenging for managers who are raising their 1st fund. Furthermore, in some cases where a team may be spinning out of a larger organization, they may be restricted from disclosing details of the track record they built during their tenure at the prior entity. Their ability to execute deals independently is often very uncertain

Out of the market: Many potential managers are becoming full time fundraisers. Their pipeline is stale and their ability to execute on their strategy is unclear. This is particularly hazardous for 1st time managers who don’t yet have a track record

Poor alignment: The level of GP contribution may be relatively light for initial funds (relative to their personal net worth). More significantly, the promote is not shared well among the team and too often held primarily by a few top executives

Too early stage: Some managers may not have substantially built out their team or established their organization’s infrastructure, particularly in cases where they may be raising their first fund

Confusing structure: Managers that operate a platform that includes multiple business entities may need to convince potential LPs that their proposed fund will be an area of significant focus for the firm. If the fund’s fees are shared across the broader organization, they will also need to demonstrate this will be done appropriately

Fiduciary qualifications: In cases where managers may have limited to no experience in managing institutional funds or separate accounts, they may not have incorporated institutional reporting and compliance systems into their organization

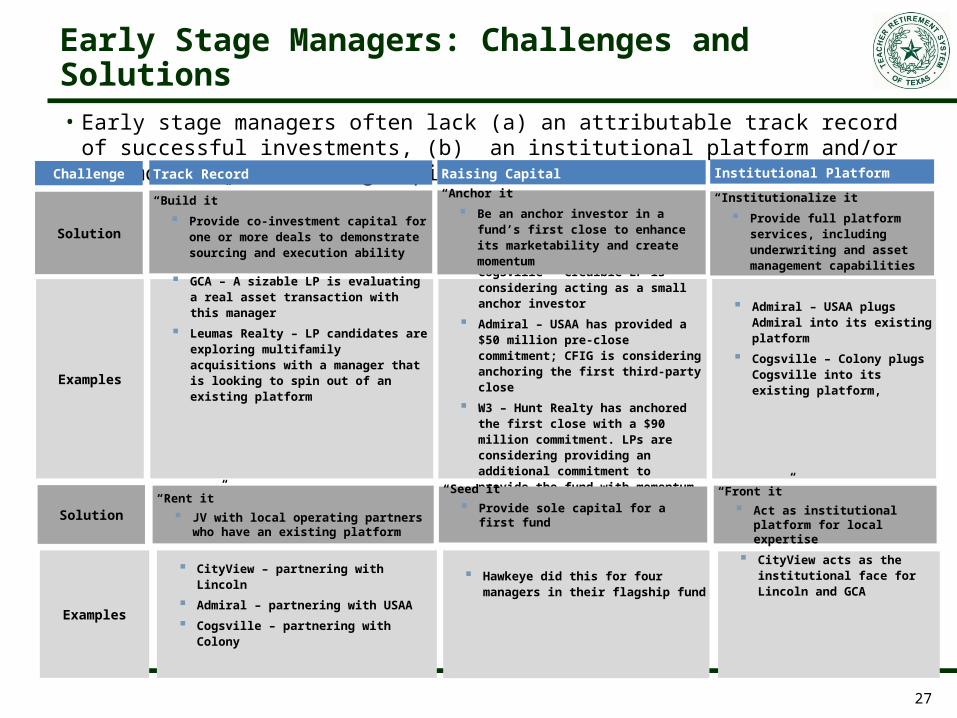

• Early stage managers often lack (a) an attributable track record of successful investments, (b) an institutional platform and/or (c) momentum in raising capital

27

Early Stage Managers: Challenges and Solutions

Examples

GCA – A sizable LP is evaluating a real asset transaction with this manager

Leumas Realty – LP candidates are exploring multifamily acquisitions with a manager that is looking to spin out of an existing platform

Solution

“Build it”

Provide co-investment capital for one or more deals to demonstrate sourcing and execution ability

Solution“Rent it”

JV with local operating partners who have an existing platform

Cogsville – Credible LP is considering acting as a small anchor investor

Admiral – USAA has provided a $50 million pre-close commitment; CFIG is considering anchoring the first third-party close

W3 – Hunt Realty has anchored the first close with a $90 million commitment. LPs are considering providing an additional commitment to provide the fund with momentum

“Anchor it”

Be an anchor investor in a fund’s first close to enhance its marketability and create momentum

“Seed it”

Provide sole capital for a first fund

Admiral – USAA plugs Admiral into its existing platform

Cogsville – Colony plugs Cogsville into its existing platform,

“Institutionalize it”

Provide full platform services, including underwriting and asset management capabilities

“Front it”

Act as institutional platform for local expertise

Examples

CityView – partnering with Lincoln

Admiral – partnering with USAA

Cogsville – partnering with Colony

Hawkeye did this for four managers in their flagship fund

CityView acts as the institutional face for Lincoln and GCA

Challenge Track Record Raising Capital Institutional Platform

28

Conclusion

Establishing a team of professionals with a strong, successful track record and identifiable synergies

Properly align management compensation across firm and LPs Mitigating potential issues early-on by using LP-friendly terms Creating thoughtful and differentiated strategy and marketing materials Strategically planning a list of targets and the best way to approach potential

investors

Keys to success for a first-time fund:

29

Appendix

30

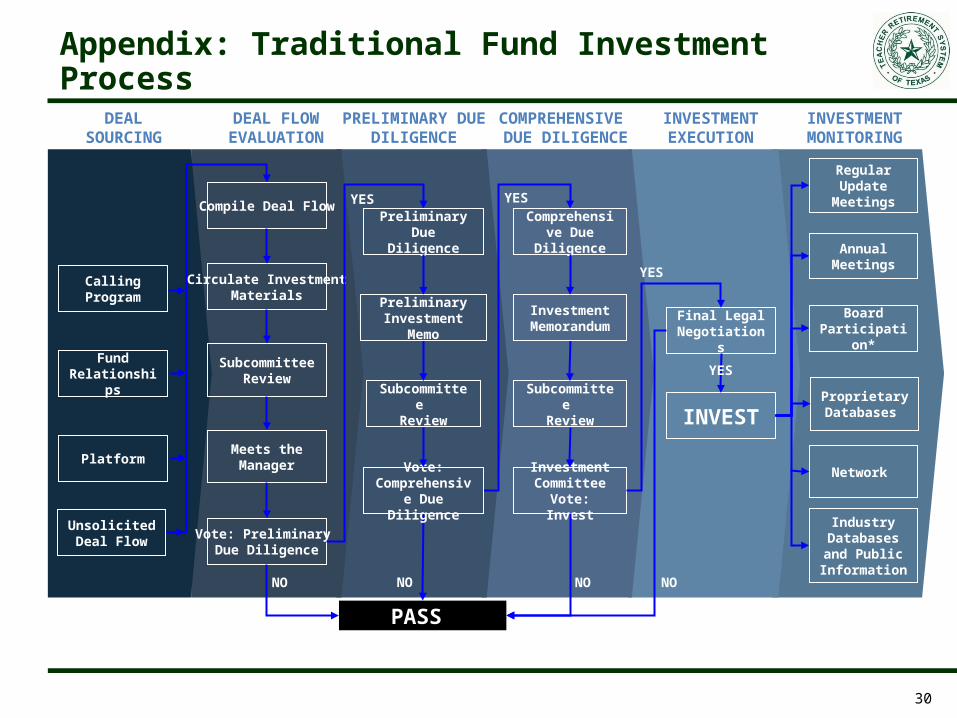

Appendix: Traditional Fund Investment Process

DEAL SOURCING

PRELIMINARY DUE DILIGENCE

COMPREHENSIVE

DUE DILIGENCE

Calling Program

Fund Relationships

Platform

Comprehensive Due

Diligence

Subcommittee Review

Investment Committee Vote: Invest

Final Legal Negotiations

INVEST

Regular Update

Meetings

Annual Meetings

Board Participation*

Proprietary Databases

Industry Databases and Public Information

DEAL FLOW EVALUATION

INVESTMENT MONITORING

Compile Deal Flow

Circulate InvestmentMaterials

Subcommittee Review

Meets the Manager

Vote: Preliminary Due Diligence

NO

PASS

YES YES

NO

YES

YES

NONO

Unsolicited Deal Flow

Network

INVESTMENT EXECUTION

Preliminary Due Diligence

Subcommittee Review

Vote: Comprehensive Due Diligence

Investment Memorandum

Preliminary Investment

Memo