Embed Size (px)

Citation preview

Emerging Trends in Distributed Generation

Elton Hooper Global Marketing Manager – Siemens PG DG

siemens.com/power-gas © Siemens AG 2017 All rights reserved.

June 2017 Page 2 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

Table of Content

• Power Generation – Origins and Growth

• Distributed Generation Technology Today

• 16 Years of Industrial Gas Turbine Sales: 3 – 66 MW Analysis

• Major Trends

• Growth of Market Segment

• Market Economic Drivers

• Siemens Response

June 2017 Page 3 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

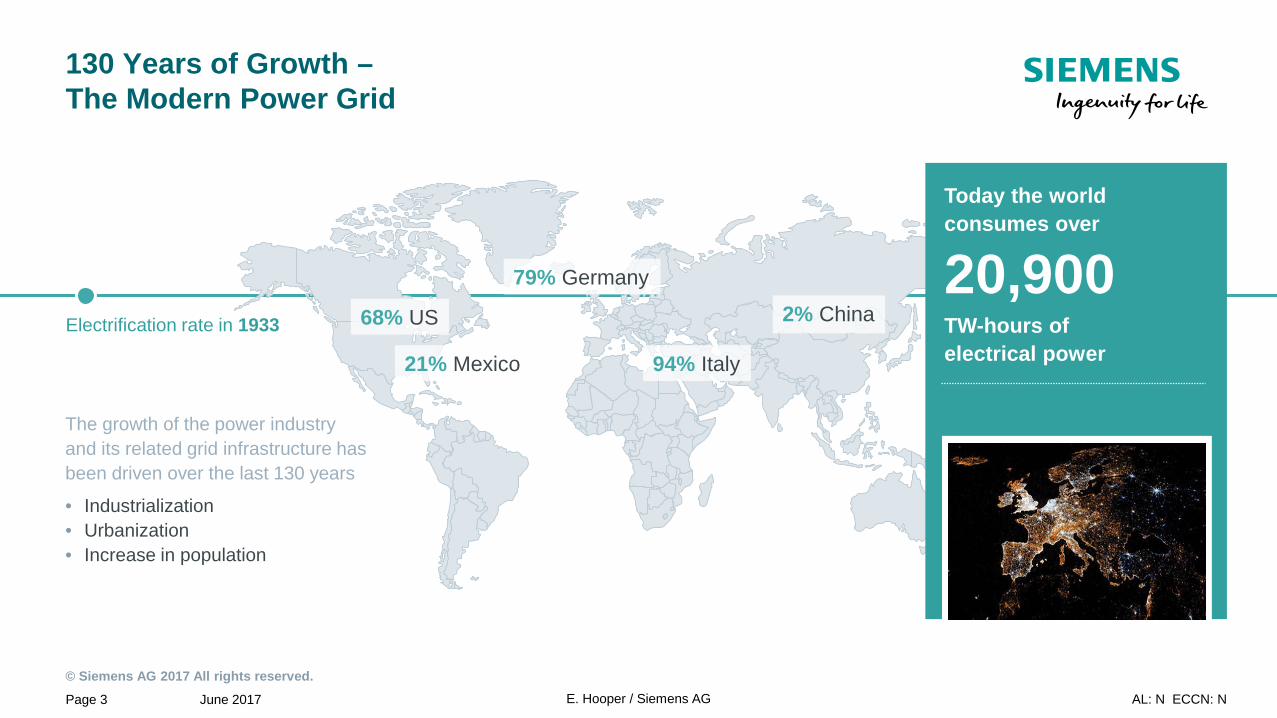

Today the world consumes over

20,900 TW-hours of electrical power

130 Years of Growth – The Modern Power Grid

The growth of the power industry and its related grid infrastructure has been driven over the last 130 years

• Industrialization • Urbanization • Increase in population

Electrification rate in 1933

94% Italy

68% US

79% Germany

21% Mexico

2% China

June 2017 Page 4 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

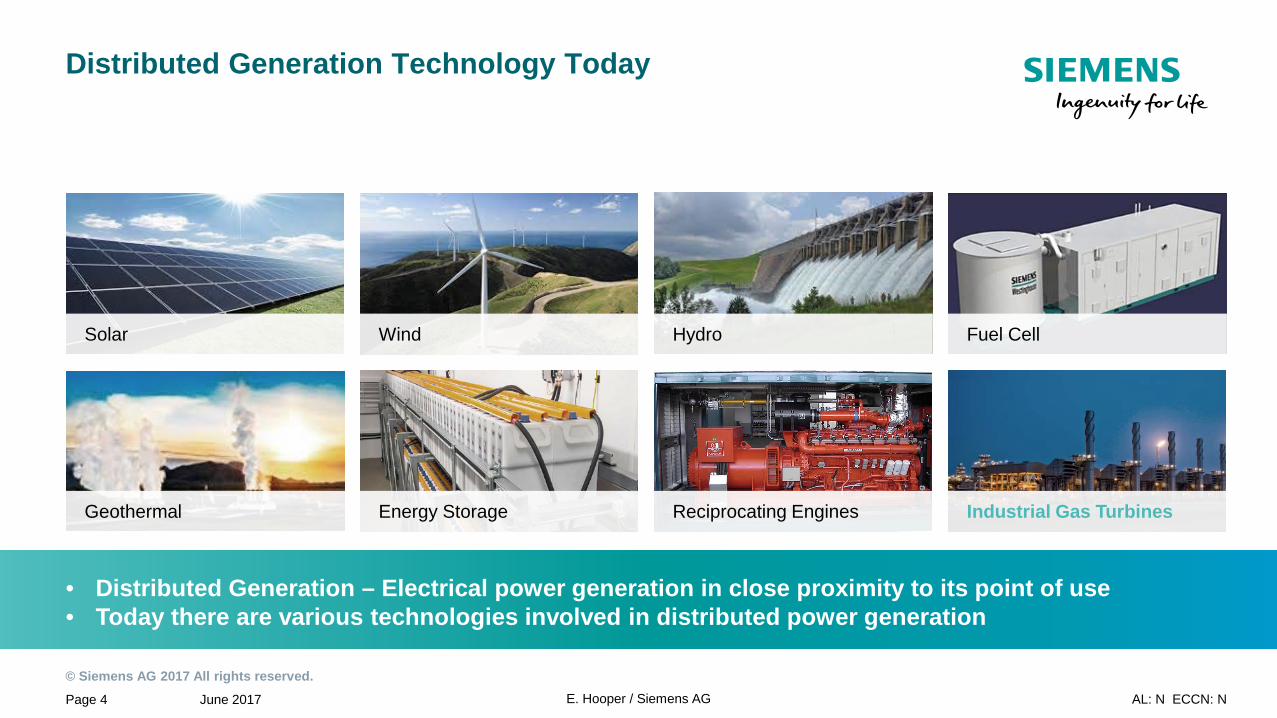

Distributed Generation Technology Today

• Distributed Generation – Electrical power generation in close proximity to its point of use • Today there are various technologies involved in distributed power generation

Reciprocating Engines Industrial Gas Turbines Energy Storage Geothermal

Hydro Fuel Cell Wind Solar

June 2017 Page 5 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

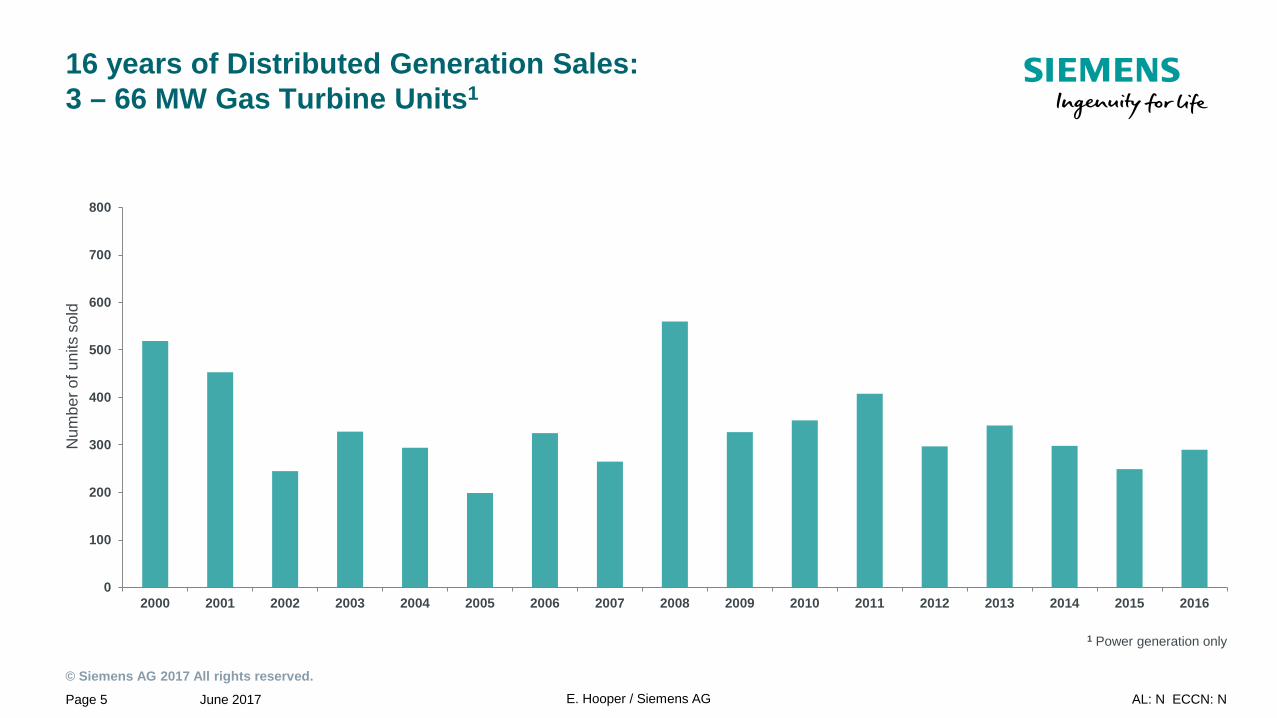

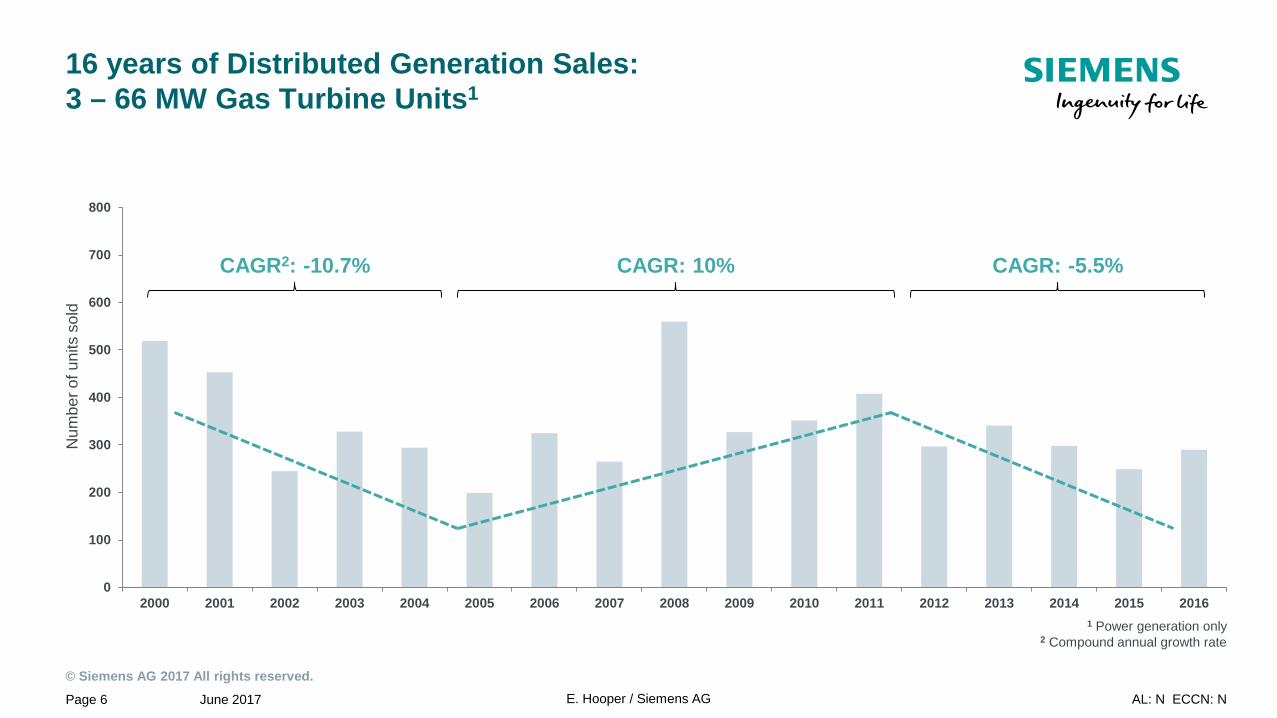

16 years of Distributed Generation Sales: 3 – 66 MW Gas Turbine Units1

0

100

200

300

400

500

600

700

800

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

1 Power generation only

Num

ber o

f uni

ts s

old

June 2017 Page 6 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

16 years of Distributed Generation Sales: 3 – 66 MW Gas Turbine Units1

0

100

200

300

400

500

600

700

800

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

CAGR2: -10.7% CAGR: 10% CAGR: -5.5%

1 Power generation only 2 Compound annual growth rate

Num

ber o

f uni

ts s

old

June 2017 Page 7 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

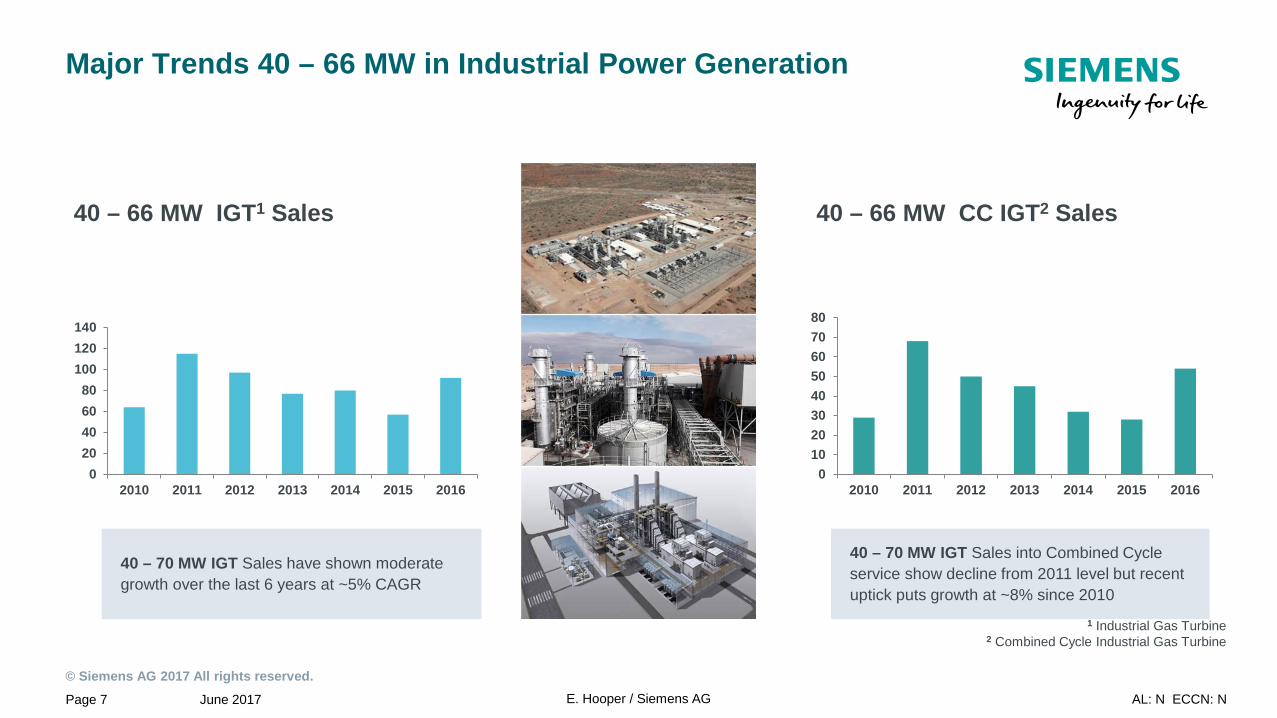

40 – 70 MW IGT Sales have shown moderate growth over the last 6 years at ~5% CAGR

40 – 70 MW IGT Sales into Combined Cycle service show decline from 2011 level but recent uptick puts growth at ~8% since 2010

Major Trends 40 – 66 MW in Industrial Power Generation

020406080

100120140

2010 2011 2012 2013 2014 2015 20160

1020304050607080

2010 2011 2012 2013 2014 2015 2016

40 – 66 MW IGT1 Sales 40 – 66 MW CC IGT2 Sales

1 Industrial Gas Turbine 2 Combined Cycle Industrial Gas Turbine

June 2017 Page 8 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

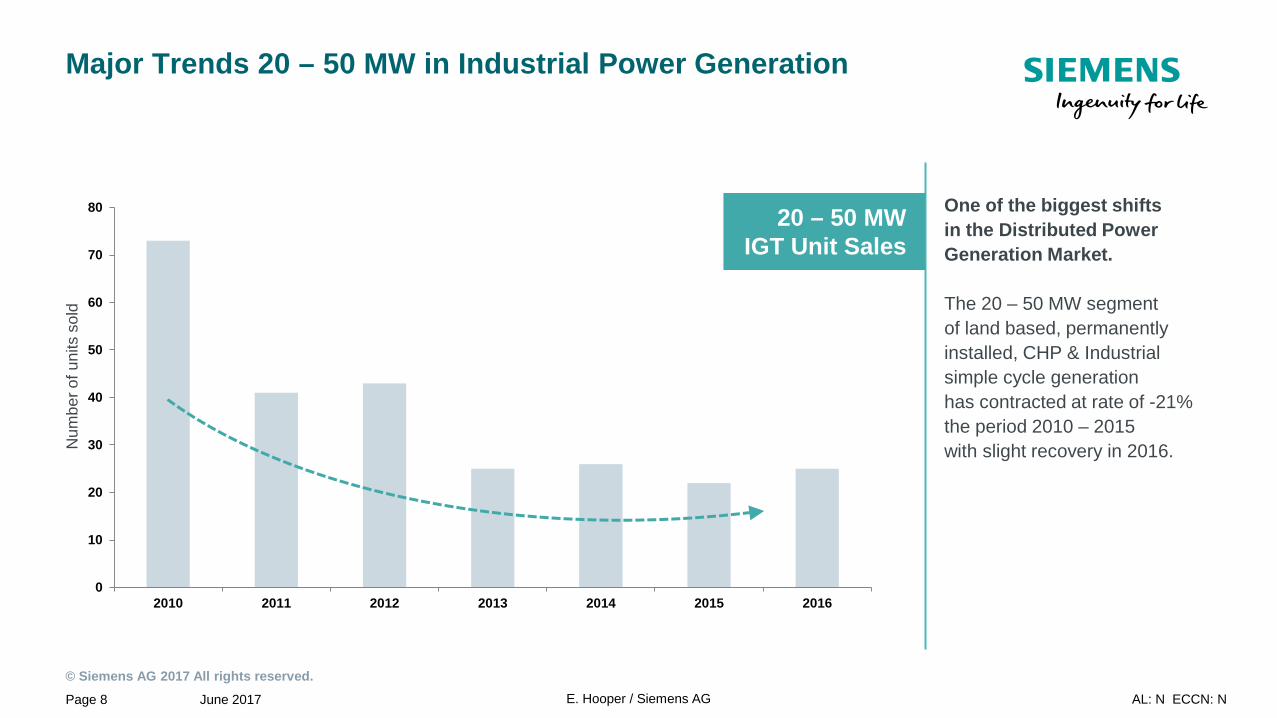

Major Trends 20 – 50 MW in Industrial Power Generation

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013 2014 2015 2016

20 – 50 MW IGT Unit Sales

One of the biggest shifts in the Distributed Power Generation Market. The 20 – 50 MW segment of land based, permanently installed, CHP & Industrial simple cycle generation has contracted at rate of -21% the period 2010 – 2015 with slight recovery in 2016. N

umbe

r of u

nits

sol

d

June 2017 Page 9 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

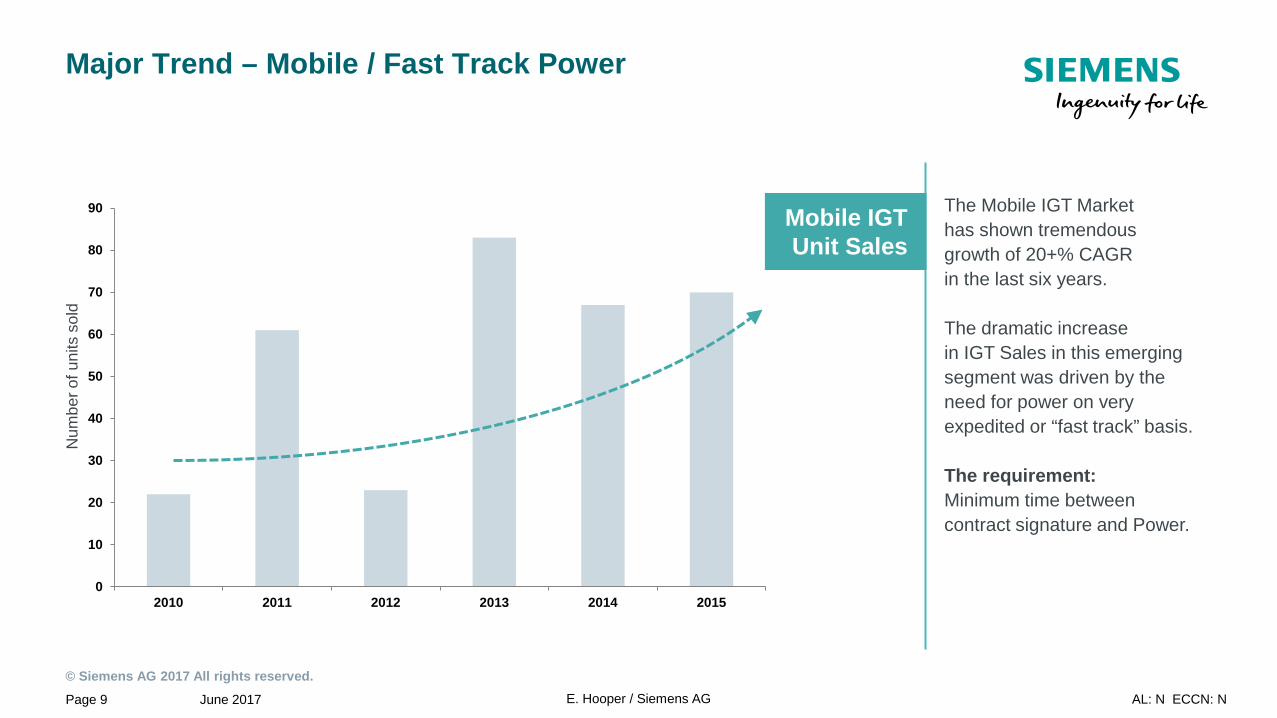

Major Trend – Mobile / Fast Track Power

0

10

20

30

40

50

60

70

80

90

2010 2011 2012 2013 2014 2015

Mobile IGT Unit Sales

The Mobile IGT Market has shown tremendous growth of 20+% CAGR in the last six years. The dramatic increase in IGT Sales in this emerging segment was driven by the need for power on very expedited or “fast track” basis. The requirement: Minimum time between contract signature and Power.

Num

ber o

f uni

ts s

old

June 2017 Page 10 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

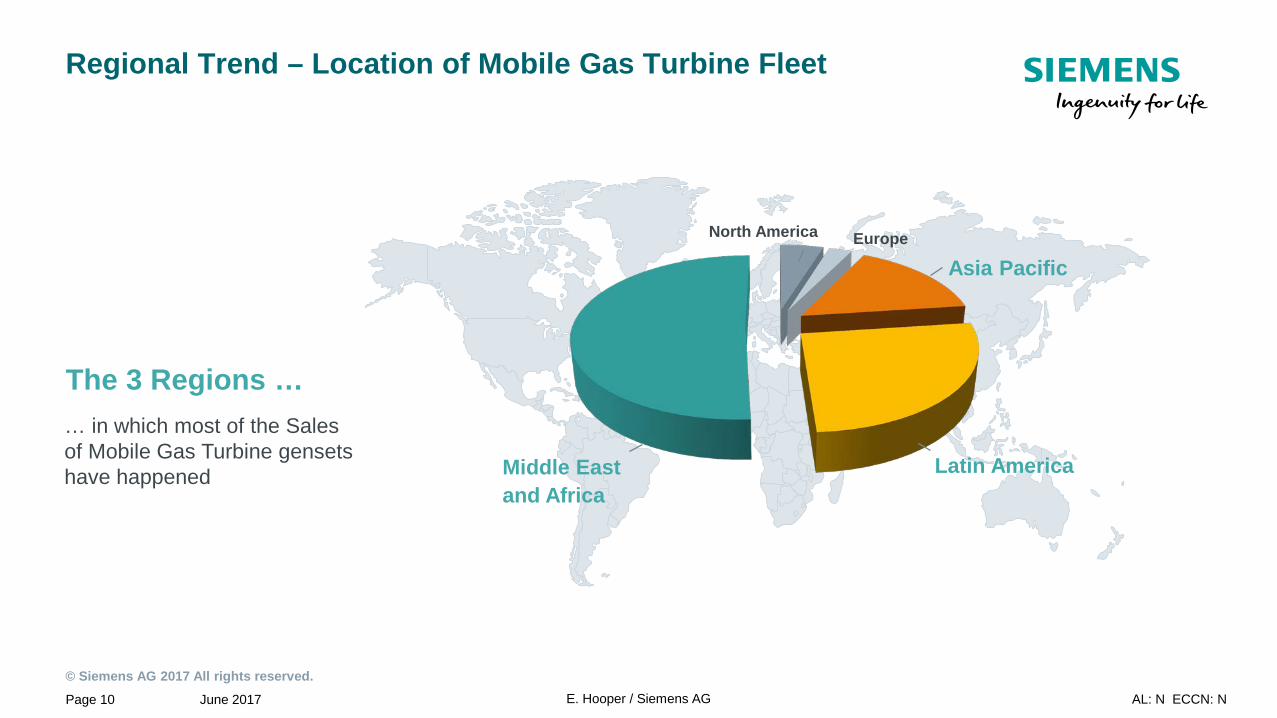

Regional Trend – Location of Mobile Gas Turbine Fleet

Latin America Middle East and Africa

Asia Pacific

North America Europe

… in which most of the Sales of Mobile Gas Turbine gensets have happened

The 3 Regions …

June 2017 Page 11 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

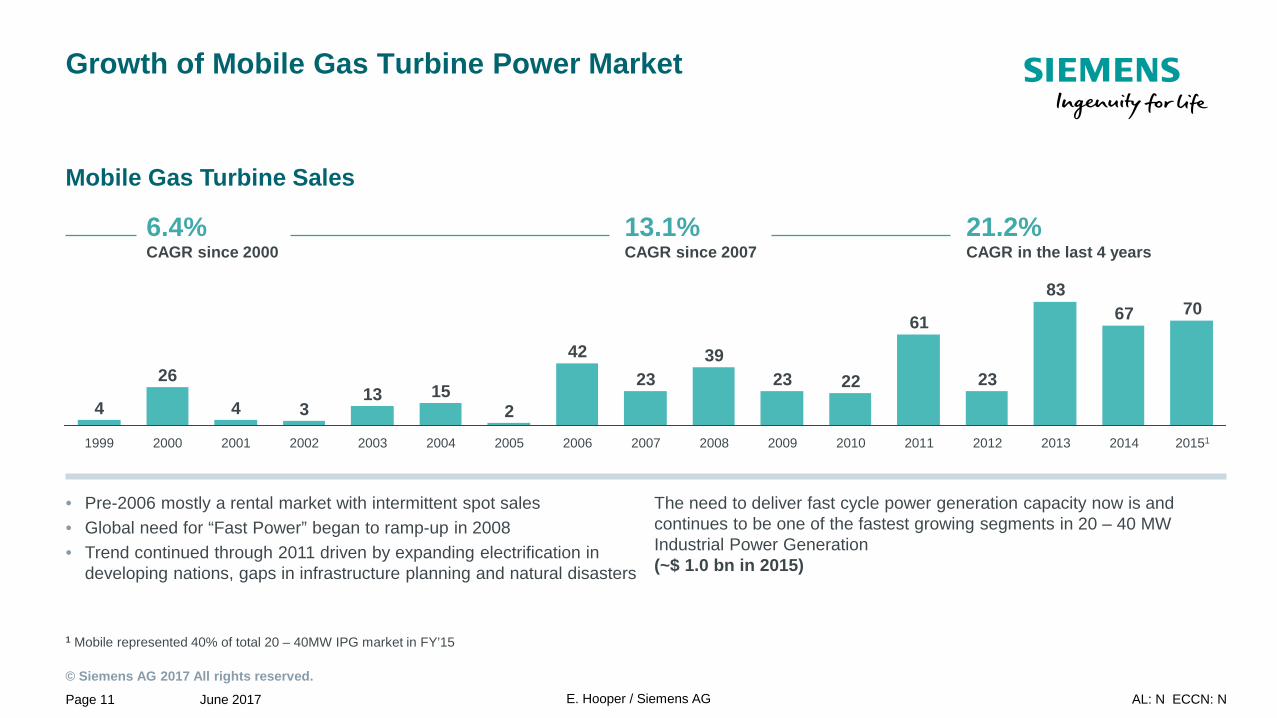

• Pre-2006 mostly a rental market with intermittent spot sales • Global need for “Fast Power” began to ramp-up in 2008 • Trend continued through 2011 driven by expanding electrification in

developing nations, gaps in infrastructure planning and natural disasters

Growth of Mobile Gas Turbine Power Market

20151

70

2014

67

2013

83

2012

23

2011

61

2010

22

2009

23

2008

39

2007

23

2001

4

2000

26

1999

4

2002

3 13

2003

15

2004

2

2005

42

2006

6.4% CAGR since 2000

13.1% CAGR since 2007

21.2% CAGR in the last 4 years

Mobile Gas Turbine Sales

The need to deliver fast cycle power generation capacity now is and continues to be one of the fastest growing segments in 20 – 40 MW Industrial Power Generation (~$ 1.0 bn in 2015)

1 Mobile represented 40% of total 20 – 40MW IPG market in FY’15

June 2017 Page 12 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

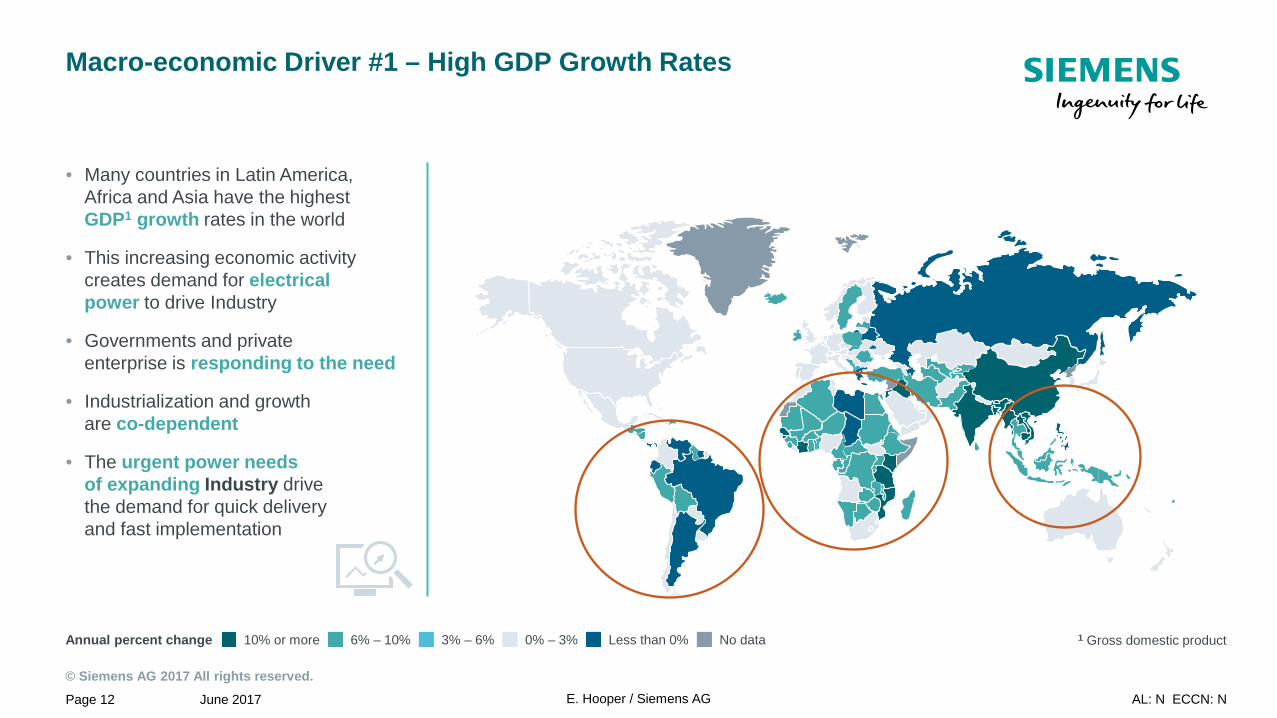

Macro-economic Driver #1 – High GDP Growth Rates

• Many countries in Latin America, Africa and Asia have the highest GDP1 growth rates in the world

• This increasing economic activity creates demand for electrical power to drive Industry

• Governments and private enterprise is responding to the need

• Industrialization and growth are co-dependent

• The urgent power needs of expanding Industry drive the demand for quick delivery and fast implementation

Annual percent change 10% or more 6% – 10% 3% – 6% 0% – 3% Less than 0% No data 1 Gross domestic product

June 2017 Page 13 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

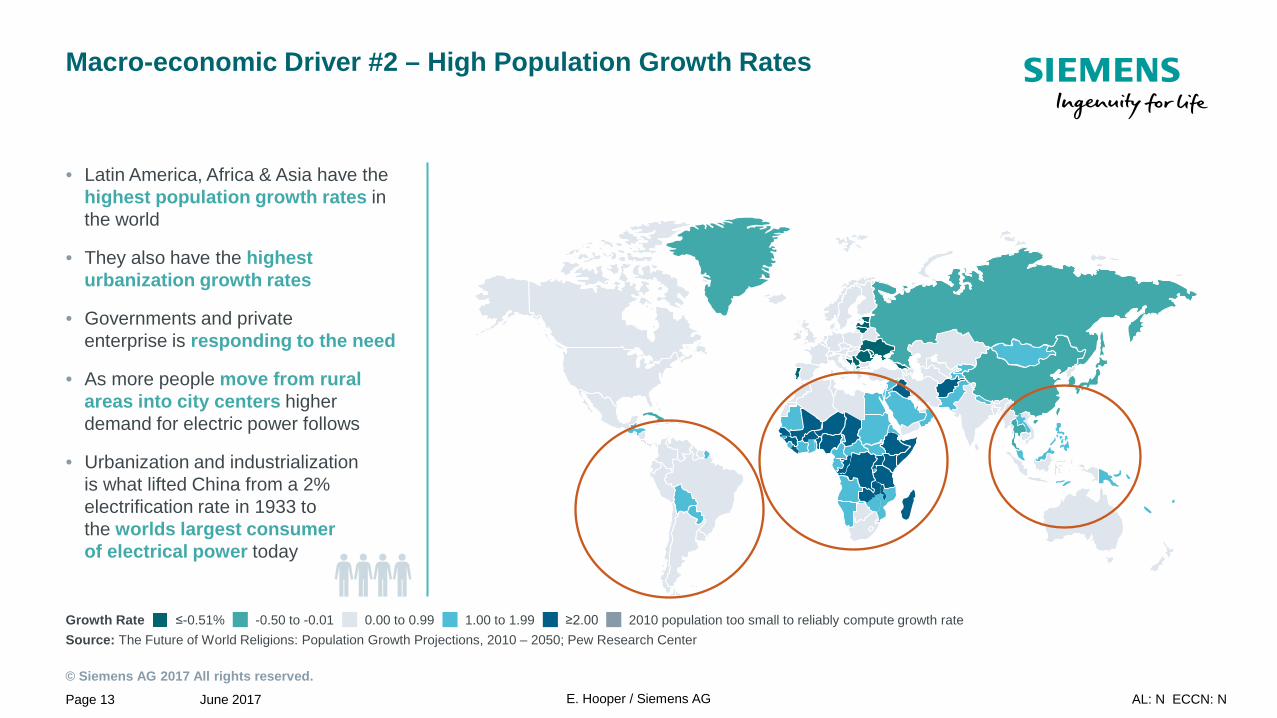

Macro-economic Driver #2 – High Population Growth Rates

• Latin America, Africa & Asia have the highest population growth rates in the world

• They also have the highest urbanization growth rates

• Governments and private enterprise is responding to the need

• As more people move from rural areas into city centers higher demand for electric power follows

• Urbanization and industrialization is what lifted China from a 2% electrification rate in 1933 to the worlds largest consumer of electrical power today

Growth Rate ≤-0.51% -0.50 to -0.01 0.00 to 0.99 1.00 to 1.99 ≥2.00 2010 population too small to reliably compute growth rate Source: The Future of World Religions: Population Growth Projections, 2010 – 2050; Pew Research Center

June 2017 Page 14 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

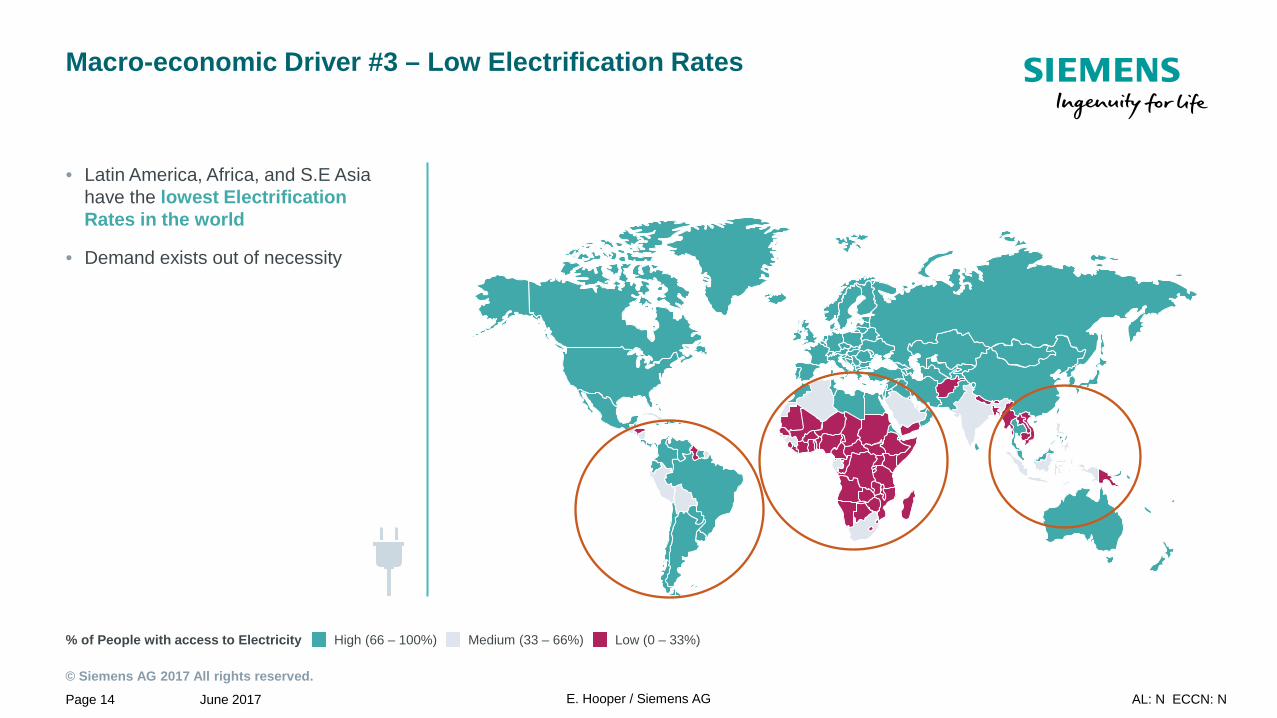

Macro-economic Driver #3 – Low Electrification Rates

• Latin America, Africa, and S.E Asia have the lowest Electrification Rates in the world

• Demand exists out of necessity

% of People with access to Electricity High (66 – 100%) Medium (33 – 66%) Low (0 – 33%)

June 2017 Page 15 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

The Gap between Supply vs. Need drives the Fast Power Market

Large portions of the world are dark.

16% (1.2 billion people) of the global population do not have access to electricity

June 2017 Page 16 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

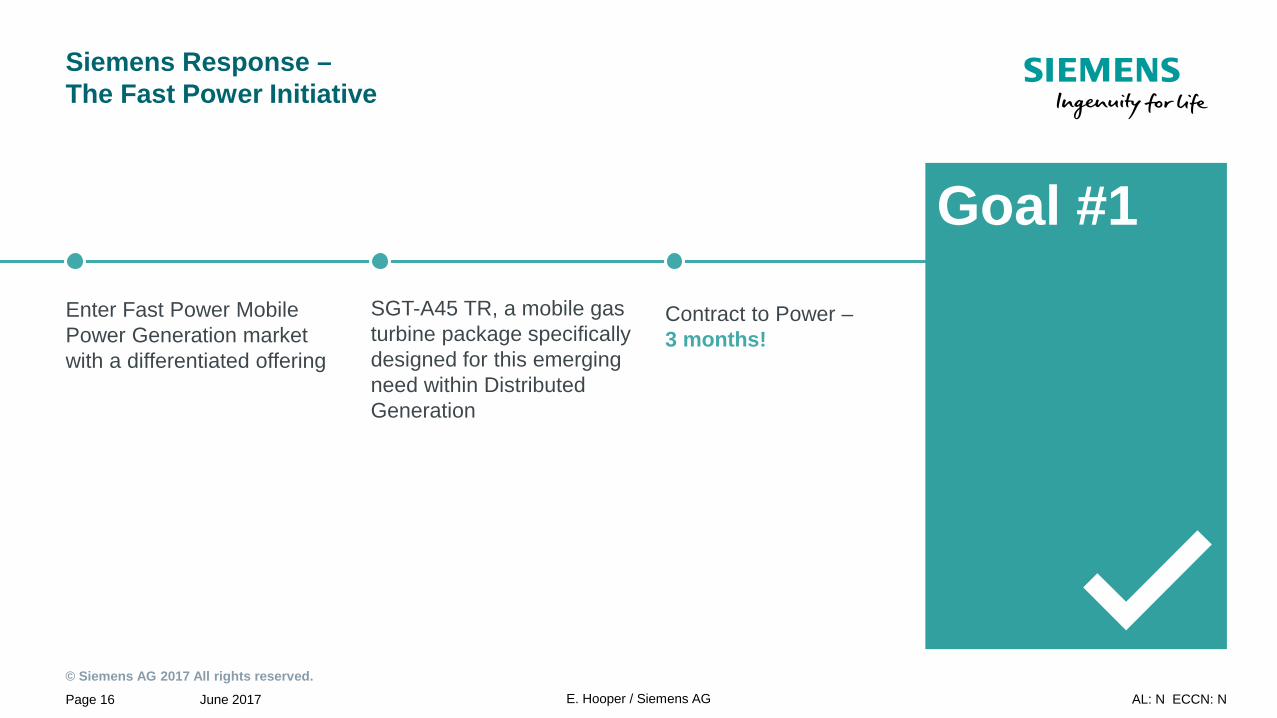

Siemens Response – The Fast Power Initiative

Goal #1 Enter Fast Power Mobile Power Generation market with a differentiated offering

SGT-A45 TR, a mobile gas turbine package specifically designed for this emerging need within Distributed Generation

Contract to Power – 3 months!

June 2017 Page 17 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

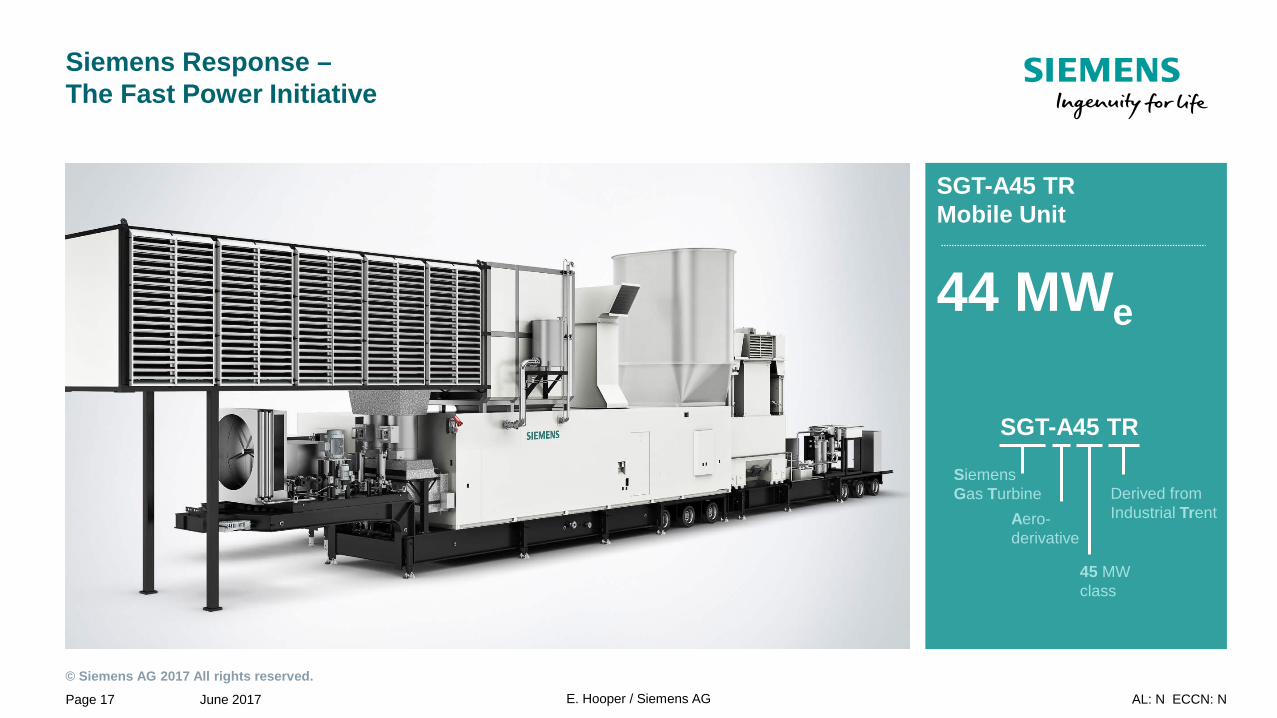

Siemens Response – The Fast Power Initiative

SGT-A45 TR Mobile Unit

44 MWe

SGT-A45 TR

Derived from Industrial Trent

45 MW class

Aero- derivative

Siemens Gas Turbine

June 2017 Page 18 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

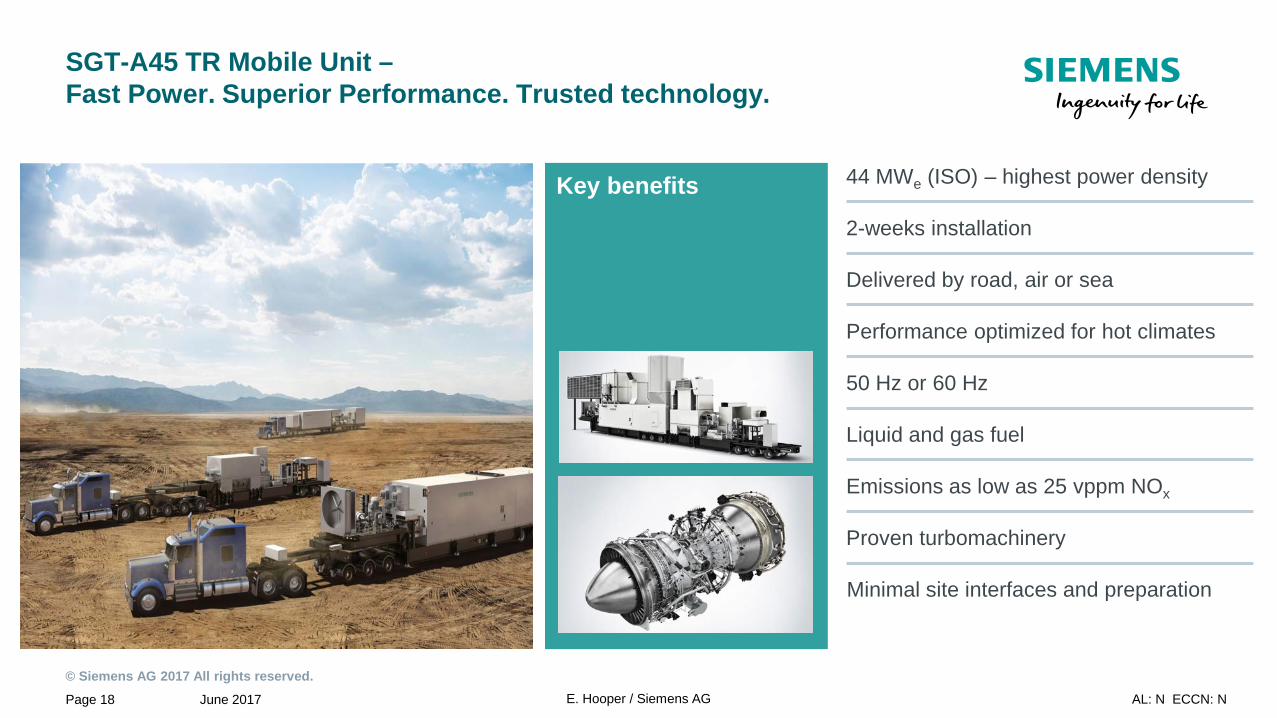

SGT-A45 TR Mobile Unit – Fast Power. Superior Performance. Trusted technology.

Key benefits 44 MWe (ISO) – highest power density

2-weeks installation

Delivered by road, air or sea

Performance optimized for hot climates

50 Hz or 60 Hz

Liquid and gas fuel

Emissions as low as 25 vppm NOx

Proven turbomachinery

Minimal site interfaces and preparation

June 2017 Page 19 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

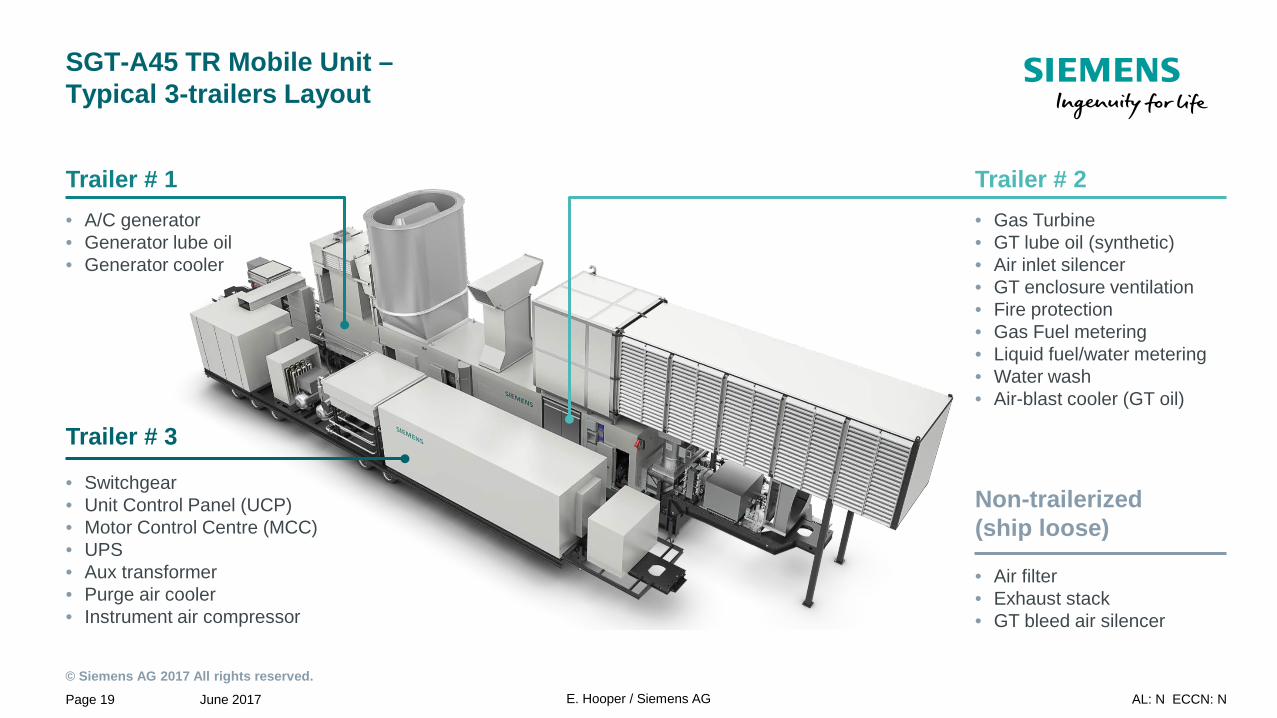

SGT-A45 TR Mobile Unit – Typical 3-trailers Layout

• Gas Turbine • GT lube oil (synthetic) • Air inlet silencer • GT enclosure ventilation • Fire protection • Gas Fuel metering • Liquid fuel/water metering • Water wash • Air-blast cooler (GT oil)

Trailer # 2

• Air filter • Exhaust stack • GT bleed air silencer

Non-trailerized (ship loose)

• A/C generator • Generator lube oil • Generator cooler

Trailer # 1

• Switchgear • Unit Control Panel (UCP) • Motor Control Centre (MCC) • UPS • Aux transformer • Purge air cooler • Instrument air compressor

Trailer # 3

Thank You.

June 2017 Page 21 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

Contact page

Elton Hooper Global Marketing Manager Siemens PG DG

1200 West Sam Houston Parkway Houston, TX USA

Phone: 1-713-253-5492 E-mail: [email protected]

siemens.com/power-gas

June 2017 Page 22 AL: N ECCN: N

© Siemens AG 2017 All rights reserved. E. Hooper / Siemens AG

Disclaimer

This document contains statements related to our future business and financial performance and future events or developments involving Siemens that may constitute forward-looking statements. These statements may be identified by words such as “expect,” “look forward to,” “anticipate” “intend,” “plan,” “believe,” “seek,” “estimate,” “will,” “project” or words of similar meaning. We may also make forward-looking statements in other reports, in presentations, in material delivered to shareholders and in press releases. In addition, our representatives may from time to time make oral forward-looking statements. Such statements are based on the current expectations and certain assumptions of Siemens’ management, of which many are beyond Siemens’ control. These are subject to a number of risks, uncertainties and factors, including, but not limited to those described in disclosures, in particular in the chapter Risks in Siemens’ Annual Report. Should one or more of these risks or uncertainties materialize, or should underlying expectations not occur or assumptions prove incorrect, actual results, performance or achievements of Siemens may (negatively or positively) vary materially from those described explicitly or implicitly in the relevant forward-looking statement. Siemens neither intends, nor assumes any obligation, to update or revise these forward-looking statements in light of developments which differ from those anticipated.

Trademarks mentioned in this document are the property of Siemens AG, its affiliates or their respective owners.

TRENT® and RB211® are registered trade marks of and used under license from Rolls-Royce plc. Trent, RB211, 501 and Avon are trade marks of and used under license of Rolls-Royce plc.