Embed Size (px)

Citation preview

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 0

© WZL/IPT

© WZL/Fraunhofer IPT

Exercise Quality Management

04 Quality and Economics

Dipl.-Ök. Anne Willach

Dipl.-Ök. Anne WillachGroup Perceived Quality & Product Value ManagementDepartment Quality Management

Chair of Metrology and Quality Management

Werkzeugmaschinenlabor WZL der RWTH Aachen UniversitySteinbachstraße 19, D-52074 Aachen, URL: http://www.wzl.rwth-aachen.deTel.: +49 (241) 80-27474, Fax: +49 (241) 80-22193

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 1

© WZL/IPT

Page 1© WZL/Fraunhofer IPT

Contents

� Task 1: Quality-based costs

Task 2: Analysis and provision of quality and cost information

Task 3: Target Costing

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 2

© WZL/IPT

Page 2© WZL/Fraunhofer IPT

Task 1Problem

� Quality and economic efficiency

The objective of this exercise is to point out different aspects of lecture four on the basis of case studies.

� Quality-based costs

As an employee in the department of Quality Management you are responsible for monitoring quality. Beside purely technical issues, it is your responsibility to consider economic issues. To be specific, it is your task to provide information for management on the basis of the data and indicators made available to you by various departments, to set appropriate quality cost targets, to document any deviation from these targets and to initiate appropriate measures.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 3

© WZL/IPT

Page 3© WZL/Fraunhofer IPT

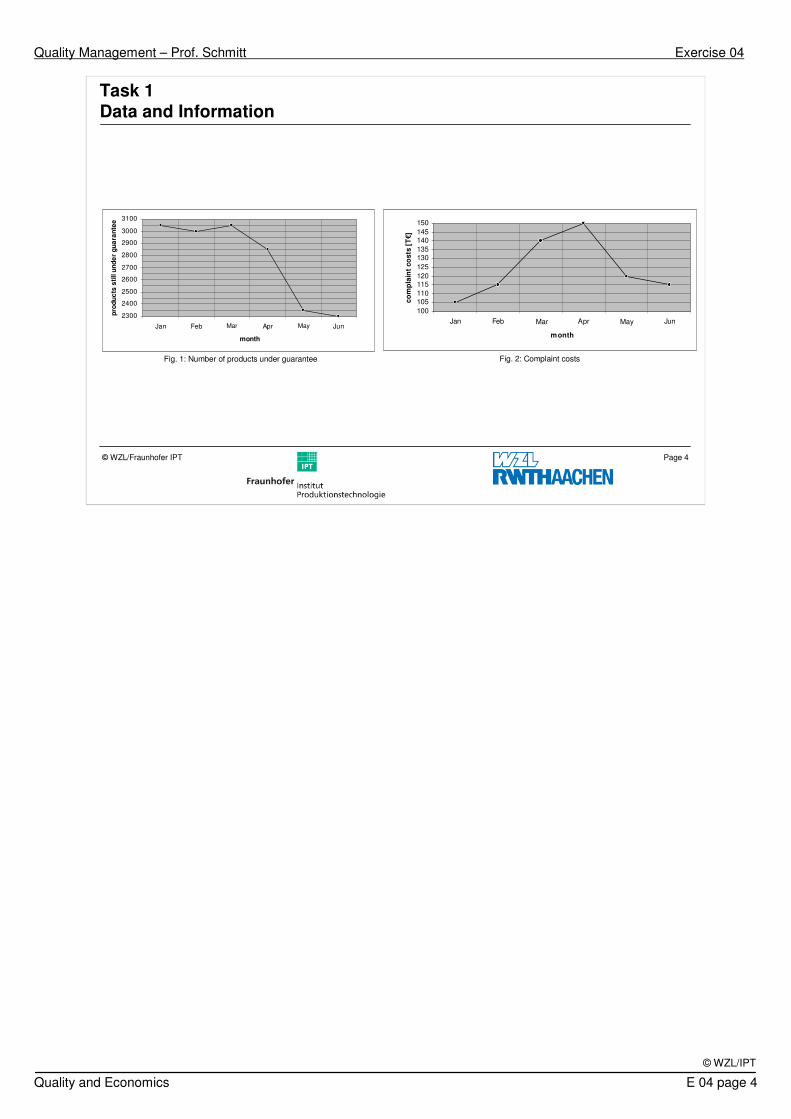

Task 1 Data and Information

The data and information which has been made available to you by the sales, manufacturing, assembly and quality assurance departments are presented below.

General Information:

– The average value of scrap is 1,200.00 €.

� Sales:

– In the month of May all products delivered in February were re-called and a component had to be replaced. The cost incurred by this action was 120.00 € per product.

– You have also been given a copy of the following diagrams:

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 4

© WZL/IPT

Page 4© WZL/Fraunhofer IPT

2300

2400

2500

2600

2700

2800

2900

3000

3100

Jan Feb Mrz Apr Mai Jun

month

pro

du

cts

sti

ll u

nd

er

gu

ara

nte

e

100105110115120125130135140145150

Jan Feb Mrz Apr Mai Jun

month

co

mp

lain

t co

sts

[T

€]

Fig. 1: Number of products under guarantee Fig. 2: Complaint costs

Task 1 Data and Information

Mar MayMar May

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 5

© WZL/IPT

Page 5© WZL/Fraunhofer IPT

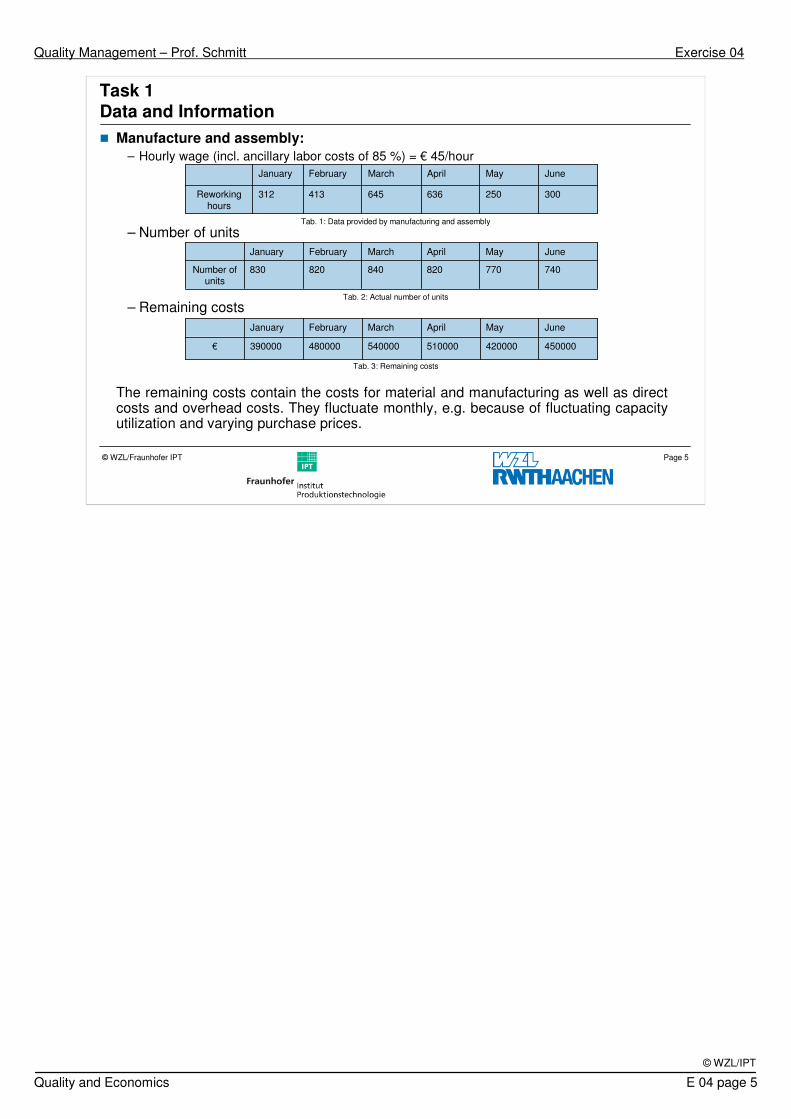

Task 1 Data and Information

� Manufacture and assembly:

– Hourly wage (incl. ancillary labor costs of 85 %) = € 45/hour

– Number of units

– Remaining costs

The remaining costs contain the costs for material and manufacturing as well as direct costs and overhead costs. They fluctuate monthly, e.g. because of fluctuating capacity utilization and varying purchase prices.

300250636645413312Reworkinghours

JuneMayAprilMarchFebruaryJanuary

740770820840820830Number ofunits

JuneMayAprilMarchFebruaryJanuary

450000420000510000540000480000390000€

JuneMayAprilMarchFebruaryJanuary

Tab. 1: Data provided by manufacturing and assembly

Tab. 2: Actual number of units

Tab. 3: Remaining costs

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 6

© WZL/IPT

Page 6© WZL/Fraunhofer IPT

Task 1 Data and Information

� Quality assurance:

– In March and April, 100 %-tests due to considerable shortcomings in quality were carried out. The test costs incurred amount to 40.00 € per product. Every month, random-tests took place. The costs incurred by this measure amount to 25.00 € per product.

– A quality audit is performed 2 times per year. It is anchored in the Quality Policy and its objective is to ensure continuous improvement of products and processes. The Quality Audit is scheduled to take place in January and May. The estimated costs are 80,000.00 € for each audit.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 7

© WZL/IPT

Page 7© WZL/Fraunhofer IPT

Task 1 Data and Information

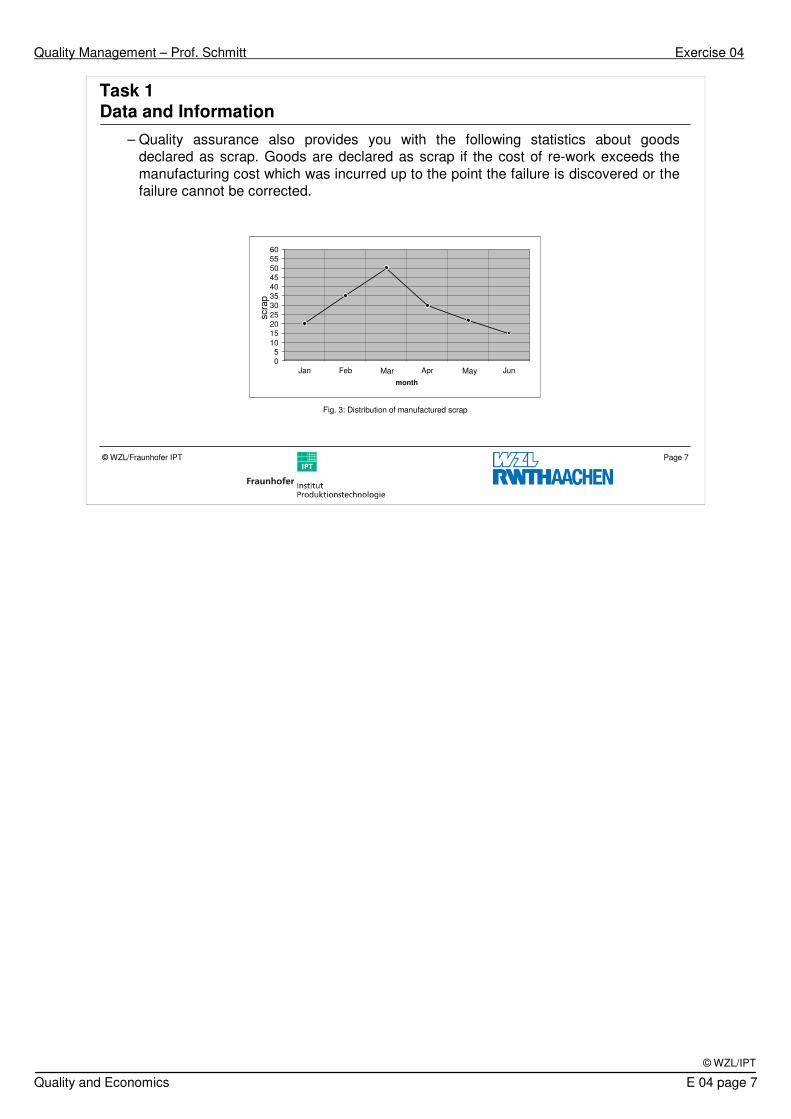

– Quality assurance also provides you with the following statistics about goods declared as scrap. Goods are declared as scrap if the cost of re-work exceeds the manufacturing cost which was incurred up to the point the failure is discovered or the failure cannot be corrected.

Fig. 3: Distribution of manufactured scrap

05

1015202530354045505560

Jan Feb Mrz Apr Mai Jun

month

reje

cts

scra

p

Mar May

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 8

© WZL/IPT

Page 8© WZL/Fraunhofer IPT

Task 1 Question

a) Classify the quality costs in the cost groups conformity and non-conformity costs and show their distributions for the months January through June in a diagram. Consider conformity costs including and not including “remaining costs”. Interpret the result!

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 9

© WZL/IPT

Page 9© WZL/Fraunhofer IPT

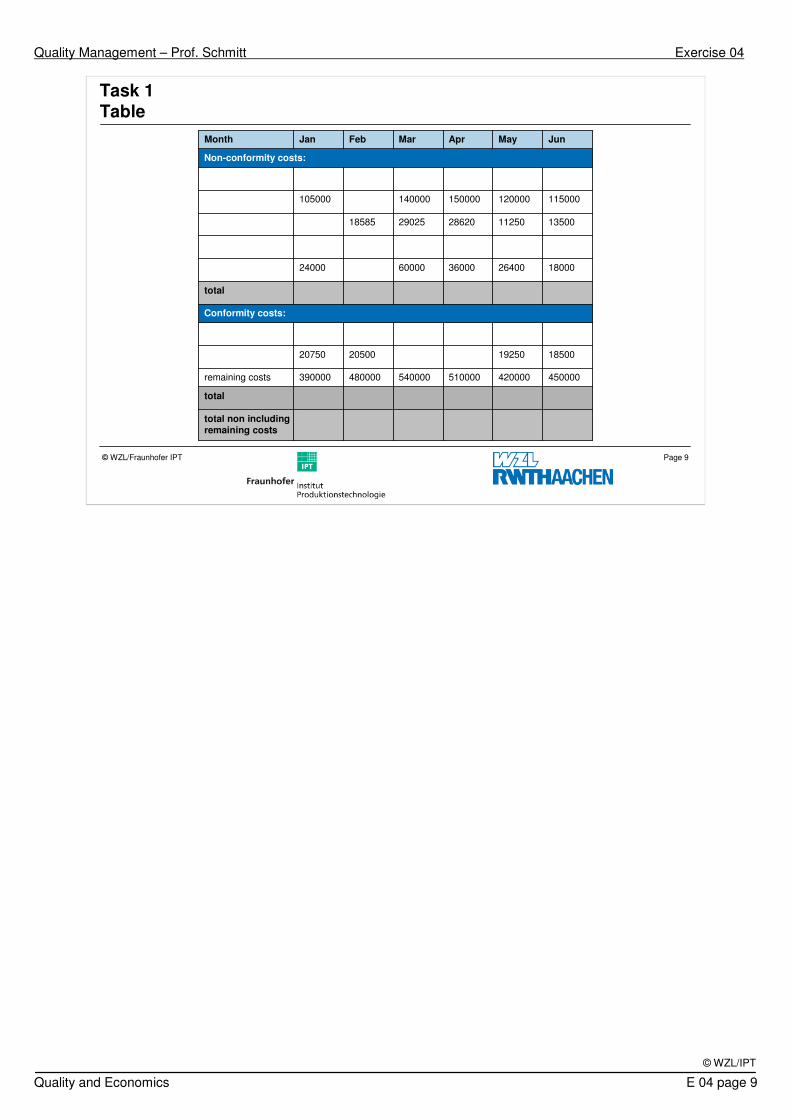

Task 1 Table

total non includingremaining costs

total

450000420000510000540000480000390000remaining costs

18500192502050020750

Conformity costs:

total

1800026400360006000024000

1350011250286202902518585

115000120000150000140000105000

Non-conformity costs:

JunMayAprMarFebJanMonth

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 10

© WZL/IPT

Page 10© WZL/Fraunhofer IPT

Task 1 Diagram

0

75000

150000

225000

300000

375000

450000

525000

600000

Jan Feb Mar Apr May Jun

Month

Co

nfo

rmit

y c

os

ts,

co

nfo

rmit

y c

os

ts

wit

ho

ut

rem

ain

ing

co

sts

N

on

-co

nfo

rmit

y c

osts

no

tin

clu

din

g,

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 11

© WZL/IPT

Page 11© WZL/Fraunhofer IPT

Task 1 Problem

b) Now select an appropriate reference quantity and show the complaint costs as a relative quantity. Interpret the result and compare it with the distribution of the absolute complaint costs.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 12

© WZL/IPT

Page 12© WZL/Fraunhofer IPT

30

35

40

45

50

55

Jan Feb Mrz Apr Mai Jun

month

rel.

co

st

of

co

mp

lain

ts

Task 1 Table

Mar May

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 13

© WZL/IPT

Page 13© WZL/Fraunhofer IPT

Contents

Task 1: Quality-based costs

� Task 2: Analysis and provision of quality and cost information

Task 3: Target Costing

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 14

© WZL/IPT

Page 14© WZL/Fraunhofer IPT

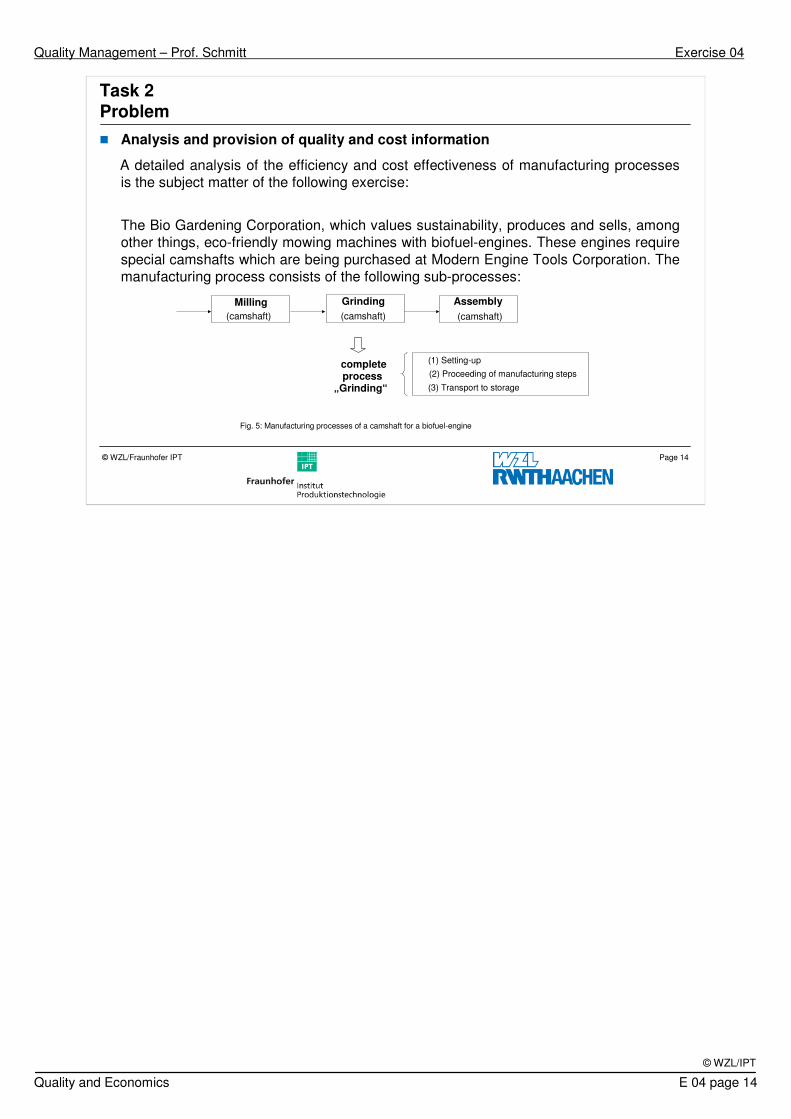

Task 2Problem

� Analysis and provision of quality and cost information

A detailed analysis of the efficiency and cost effectiveness of manufacturing processes is the subject matter of the following exercise:

The Bio Gardening Corporation, which values sustainability, produces and sells, among other things, eco-friendly mowing machines with biofuel-engines. These engines require special camshafts which are being purchased at Modern Engine Tools Corporation. The manufacturing process consists of the following sub-processes:

Fig. 5: Manufacturing processes of a camshaft for a biofuel-engine

(3) Transport to storage

(1) Setting-up

(2) Proceeding of manufacturing stepscomplete process

„Grinding“

(camshaft)

Milling Grinding

(camshaft)

Assembly

(camshaft)

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 15

© WZL/IPT

Page 15© WZL/Fraunhofer IPT

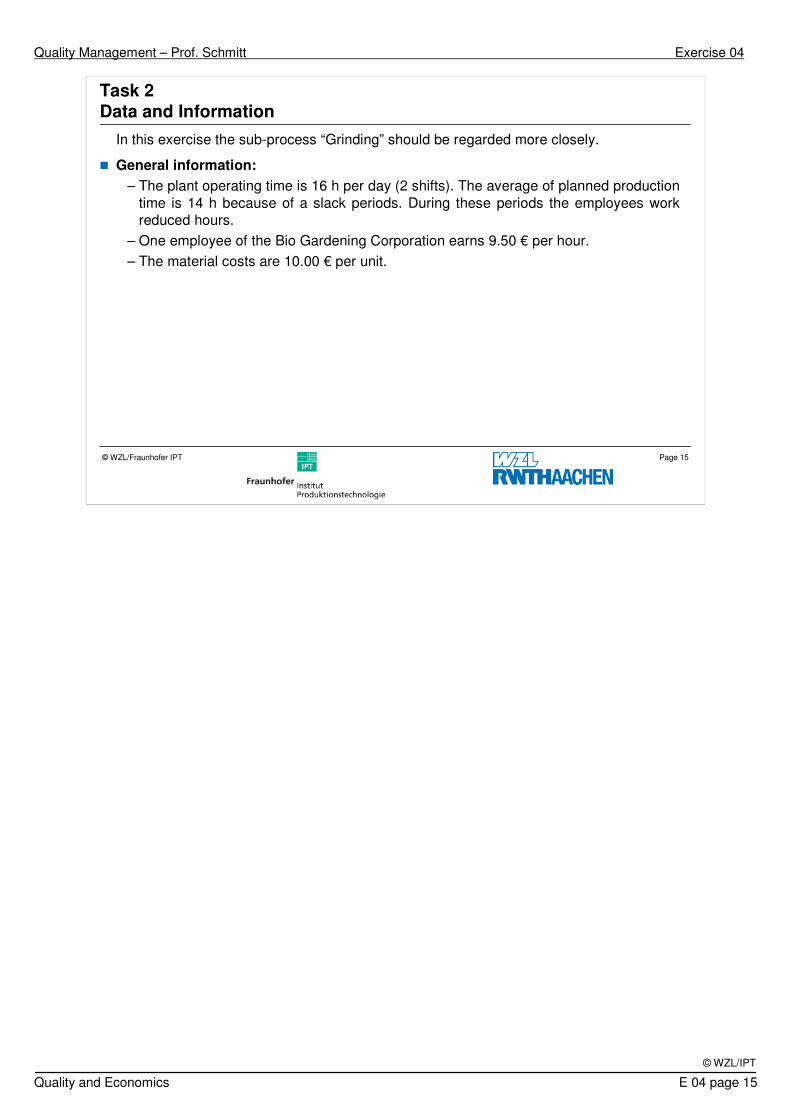

Task 2 Data and Information

In this exercise the sub-process “Grinding” should be regarded more closely.

� General information:

– The plant operating time is 16 h per day (2 shifts). The average of planned production time is 14 h because of a slack periods. During these periods the employees work reduced hours.

– One employee of the Bio Gardening Corporation earns 9.50 € per hour.

– The material costs are 10.00 € per unit.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 16

© WZL/IPT

Page 16© WZL/Fraunhofer IPT

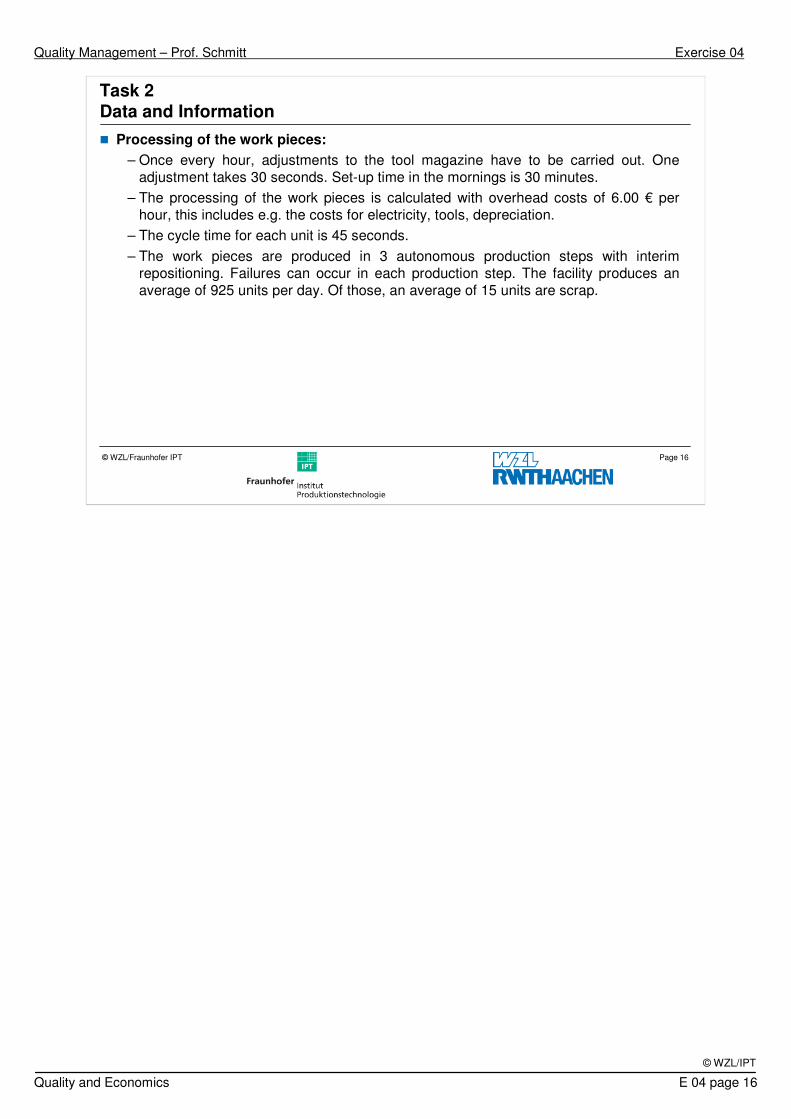

� Processing of the work pieces:

– Once every hour, adjustments to the tool magazine have to be carried out. One adjustment takes 30 seconds. Set-up time in the mornings is 30 minutes.

– The processing of the work pieces is calculated with overhead costs of 6.00 € per hour, this includes e.g. the costs for electricity, tools, depreciation.

– The cycle time for each unit is 45 seconds.

– The work pieces are produced in 3 autonomous production steps with interim repositioning. Failures can occur in each production step. The facility produces an average of 925 units per day. Of those, an average of 15 units are scrap.

Task 2 Data and Information

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 17

© WZL/IPT

Page 17© WZL/Fraunhofer IPT

Task 2 Data and Information

� Transport:

– The work pieces are delivered on pallets.

– While production is in process, the employee removes the finished work piece and places it on a pallet.

– The small storage 1 is situated near the production facility and the assembly (transportation costs can be disregarded). Storage 2 is situated farther away but the employees prefer this storage. They always take the finished pieces there because Heike, a nice and attractive trainee, works there. At the end of each day, one worker brings the loaded pallets to storage 2. This unnecessary transit takes 4 minutes.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 18

© WZL/IPT

Page 18© WZL/Fraunhofer IPT

Task 2 Question

a) Calculate the overall equipment effectiveness!

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 19

© WZL/IPT

Page 19© WZL/Fraunhofer IPT

Task 2 Question

b) During how many hours per day is value-adding work being carried out on the machine?

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 20

© WZL/IPT

Page 20© WZL/Fraunhofer IPT

Task 2 Question

c) Calculate the process efficiency factor!

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 21

© WZL/IPT

Page 21© WZL/Fraunhofer IPT

Task 2 Question

d) Interpret the differences between the indices!

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 22

© WZL/IPT

Page 22© WZL/Fraunhofer IPT

Contents

Task 1: Quality-based costs

Task 2: Analysis and provision ofquality and cost information

� Task 3: Target Costing

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 23

© WZL/IPT

Page 23© WZL/Fraunhofer IPT

Task 3Problem

� Target Costing

The company Cyclo Gras GmbH manufactures lawn mowers that are part of the upper end of the price range. The lawn mower market is well-researched and clearly structured. The required forecasts can therefore be regarded as reliable. Use the data provided to carry out a target cost analysis for a new model, scheduled to displace the current model in 2 years.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 24

© WZL/IPT

Page 24© WZL/Fraunhofer IPT

Task 3 Data and Information

– The current product generation and comparable products manufactured by competitors are available on the market for approx. 1,850.00 €. The most up-to-date forecasts provided by market research institutes indicate, however, that the emergence of new competitors from Southern Asia will decrease the price accepted by the market to 1,700.00 € during the next 2 years.

– In accordance with the targets set by company management, the aim is to reach a profit margin of 12 %.

– One of the project teams has conducted a QFD study on the product, the results are available to you (Tab. 5).

– You also have the cost data concerning individual components/parts of the current product (Tab. 6).

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 25

© WZL/IPT

Page 25© WZL/Fraunhofer IPT

Task 3 Data and Information

€1600total :

€25grass collection bin

€190control unit

€330blades and rotor

€125casing

€210battery

€410engine

€140wheels

€120seat

€50small parts and attachment

Current costsof parts

Components in present generation

Tab. 5: Results of QFD

%100total:

%5grass collection bin

%8control unit

%21blades and rotor

%7casing

%21battery

%23engine

%8wheels

%4seat

%3small parts and attachment

WeightingComponents

Tab. 6: Costs of the components

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 26

© WZL/IPT

Page 26© WZL/Fraunhofer IPT

Task 3 Question

a) Calculate the allowable costs of the new product which will make it possible to reach the prescribed profit margin.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 27

© WZL/IPT

Page 27© WZL/Fraunhofer IPT

Task 3 Question

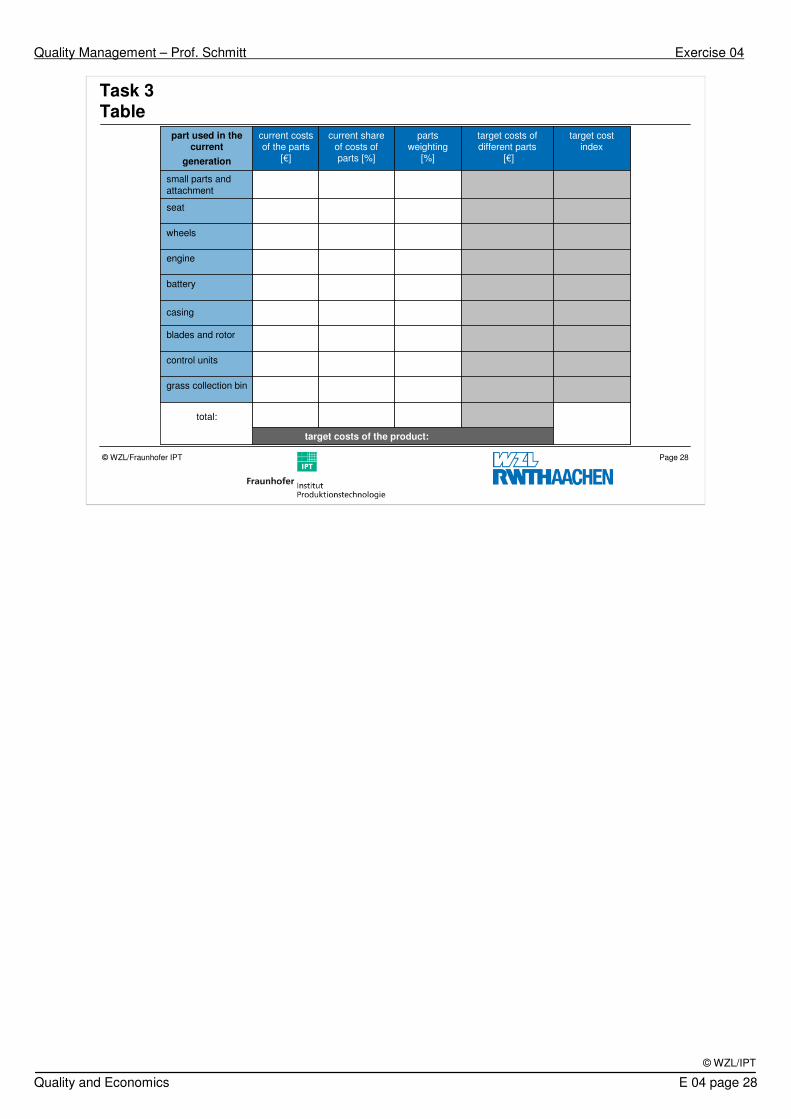

b) Use tables 5 and 6 to calculate the target costs and target cost indices of the different components and enter the values in the table below.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 28

© WZL/IPT

Page 28© WZL/Fraunhofer IPT

Task 3 Table

target costs of the product:

total:

grass collection bin

control units

blades and rotor

casing

battery

engine

wheels

seat

small parts and attachment

target costindex

target costs of different parts

[€]

partsweighting

[%]

current shareof costs of parts [%]

current costsof the parts

[€]

part used in the current

generation

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 29

© WZL/IPT

Page 29© WZL/Fraunhofer IPT

Task 3 Question

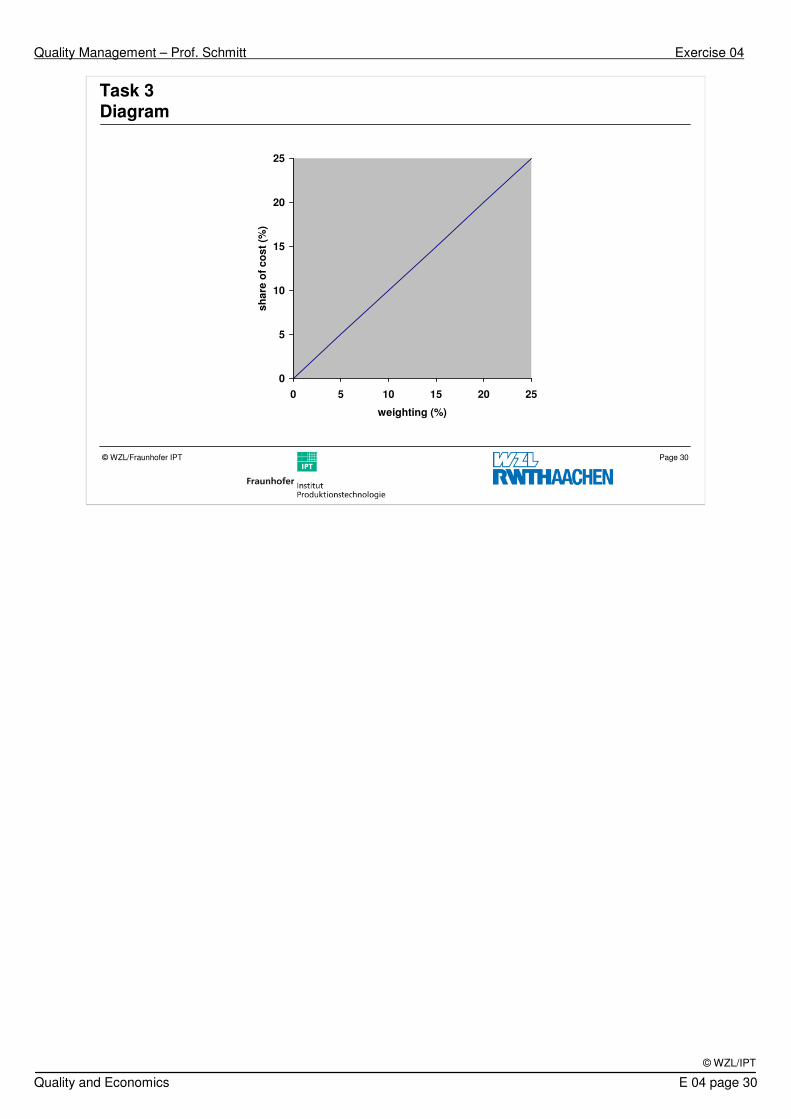

One method to demonstrate whether the target costs are realistic or not, is by drawing up a target cost control diagram.

The limits of the target cost zone are described by the following functions:

Y1 = (X2 - q2)1/2

Y2 = (X2 + q2)1/2

c) Draw the target cost zone for the following values of the decision parameter q:

q=5; q=10

d) Enter the individual parts in the diagram.

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 30

© WZL/IPT

Page 30© WZL/Fraunhofer IPT

0

5

10

15

20

25

0 5 10 15 20 25

weighting (%)

sh

are

of

co

st

(%)

Task 3 Diagram

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 31

© WZL/IPT

Page 31© WZL/Fraunhofer IPT

Task 3 Question

e) Interpret the result.

f) On what criteria would you base the selection of a value for parameter q?

Quality Management – Prof. Schmitt Exercise 04

Quality and Economics E 04 page 32

© WZL/IPT

Page 32© WZL/Fraunhofer IPT

Task 3 Question

g) How would you proceed if a component/part is far outside the target cost zone?

![dìdÄR XÖLWÖK èb]SáÖK Üá©K dáRùá ïätáÖK ïZdL`ÖK … · A/CONF.184/6 QKdkS`áÖK ADEOS Advanced Earth Observing Satellite ld©K bkdÖ ÜbÄSáÖK (ïâLNLîÖK) ÑRL¸ÖK](https://img.pdfslide.us/doc/110x75/5c2780cf09d3f240638b4960/didaer-xoelwoek-ebsaoek-ueak-darua-iaetaoek-izdloek-aconf1846.jpg)

![dìdÄR XÖLWÖK èb]SáÖK Üá©K dáRùá ïätáÖK …A/CONF.184/6 èb¥]SáÖK Ü¥á©K Distr.: General êáLtÖK êîtáZÖK ARABIC Original: English ïZdL`ÖK òLm|ÖK zL˛ÉSgLN](https://img.pdfslide.us/doc/110x75/5e3c7cf862218c776d291ec3/ddr-xlwk-bsk-oek-dr-tk-aconf1846-bsk.jpg)