Embed Size (px)

Citation preview

Customer Service Level 3Principles of Business

Economic sectors

Public – organisations funded by public money. Private – motivation is to increase profit, attract new customers and build on existing

relationships. Voluntary/not-for-profit (the Community and Voluntary Sector) – charities or organisations

operating under a charitable status where money is not raised for a cause, but rather invested back into the operation.

Public sector

Funded by public money (ie taxes) Provide preventative or supportive services to a

wide-ranging client base Profit is not the goal Answer to Parliament or central government Either report to government departments, headed

up by ministers of the political party in power, or non-ministerial government departments that

answer to Parliament.

Private sector

Motivation is to increase profit, attract new customers and build on existing relationships. Types of private organisation: Sole trader Partnership Private limited company Public limited company.

Voluntary/not-for-profit (the Community and Voluntary Sector)

Organisations who aim to raise aid for their stated cause. Voluntary organisations such as the Voluntary Services Organisation. Organisations operating under a charitable status where money is not raised for a cause, but

rather invested back into the operation, e.g. City & Guilds.

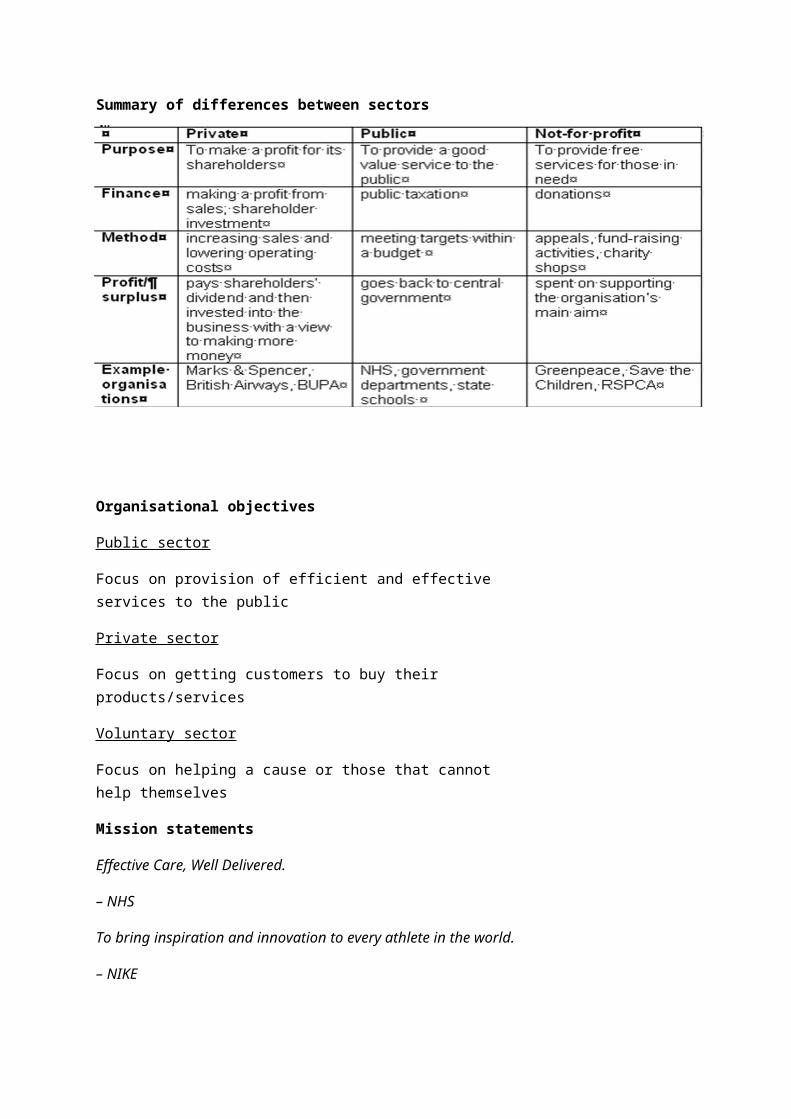

Summary of differences between sectors

Organisational objectives

Public sector

Focus on provision of efficient and effective services to the public

Private sector

Focus on getting customers to buy their products/services

Voluntary sector

Focus on helping a cause or those that cannot help themselves

Mission statements

Effective Care, Well Delivered.

– NHS

To bring inspiration and innovation to every athlete in the world.

– NIKE

We defend the natural world and promote peace by investigating, exposing and confronting environmental abuse, and championing environmentally responsible solutions.

– Greenpeace

Legislation

National Minimum Wage Act Equality Act Employment Rights Act Working Time Regulations Act Data Protection Act Human Rights Act Health and Safety at Work Act

National Minimum Wage Act

Sets a minimum hourly rate of pay for workers: Aged 18–20 Aged 21+.

Equality Act 2010

Protects people from discrimination and incorporates the following previous legislation:

Sex Discrimination Act 1975 Race Relations Act 1976 Disability Discrimination Act 1995.

Employment Rights Act 1996

Protects against unfair dismissal, redundancy Gives time off for parenting Enforces a minimum wage Monitors conditions for agency workers

Working Time Regulations 1998

Protects you from being forced to work long hours. You cannot be forced to work more than an average of 48 hours (including overtime). Your employer must maintain records that show the hours you work. They can ask you to ‘opt out’ of this agreement and ask you to work above this limit of 48

hours. Also allows for employees to have: 11 hours’ rest in every 24 worked and a rest period of 24 hours in every 7 days A 20-minute break when working more than 6 hours 4 weeks’ paid holiday each year.

Data Protection Act 1998

Protects any living, identifiable individual from misuse or unauthorised disclosure of personal data.

Also covers any expression of opinion about the individual.

Covers both paper and computer files. Organisations holding personal data need to register with the Office of the Data Protection

Commissioners. Individuals have the right to access and read the data held on them for a fee.

Principles of the Data Protection Act

Must be obtained and processed fairly and lawfully. Will be obtained and used for only one or more specified and lawful purpose. Should be adequate, relevant and not excessive. Should be accurate and up to date. Should be kept no longer than the purpose(s) requires. Data subjects (individuals) have the: Right to prevent processing which would cause damage or distress Right to access data held about them Right to prevent processing for direct marketing purposes Right to compensation if damage is suffered as a result of the Act not being followed.

Human Rights Act – respecting human rights and freedom

Covers the right to:

Life Fair trial Liberty and security Privacy Freedom of thought and expression Freedom of assembly Marriage

Prohibits:

Discrimination Torture Slavery Abuse of rights

Companies Act

Covers organisations in the private sector: Formation Governance Auditing procedures Accountability

Health and Safety at Work Act 1974

Details the responsibilities of:

Employers Management Staff Visitors External contractors

Other health and safety legislation

Reporting of Injuries, Disease and Dangerous Occurrences Regulations (RIDDOR) 1992 The Management of Health and Safety at Work Regulations 1999 Workplace (Health, Safety and Welfare) Regulations 1992 The Health and Safety (Display Screen Equipment) Regulations 1992 The Provision and Use of Work Equipment Regulations 1998

Public and voluntary sector organisations

Public sector funding

Public sector organisations do not have the facility to ‘make a profit’. They are funded from public taxes. These taxes may be central or local taxes

Transparency

The public has a right to know how public sector organisations spend their money Promotes efficiency

Types of public sector organisations

NHS Health organisations – hospitals, doctors’ surgeries, clinics State education organisations – schools, colleges Local authorities (councils), eg London Borough of Ealing Government departments, eg Department for Health Non-ministerial departments, eg the Foods Standards Agency Executive agencies that operate as separate organisations, eg The Met Office and HM Land

Registry are both executive agencies within the Department of Business, Innovation and Skills (BIS)

Non-Departmental Public Bodies (NDPB) – quangos – eg The Health and Safety Executive

Local authorities

Report to the Secretary of State for Communities and Local Government Responsible for the running of local areas

There are several types:

1. County and district councils 2. Unitary authorities

3. Town and parish councils

Government departments

Central government is separated into separate government departments. Government departments are headed by a Secretary of State or other senior minister. Examples of ministerial departments are: Cabinet Office Department for Health HM Treasury Ministry for Defence

Non-ministerial departments

Examples of non-ministerial departments are: Charity Commission Food Standards Agency HM Revenue & Customs Office of Fair Trading

Executive agencies

Under control of government departments Have a defined business function Operate almost like a separate organisation from the main department Examples of executive agencies are: Highways Agency HM Court and Tribunal Service Identity and Passport Service Jobcentre Plus UK Border Agency

Non-departmental public bodies (NDPBs)

Functions:

Executive Advisory Examples of executive NDPBs are: Competition Commission English Heritage Environment Agency Health and Safety Executive

Examples of advisory NDPBs are:

Advisory Council on the Misuse of Drugs Committee on Standards in Public Life Pay Review Bodies

Public sector legislation

Local Government Act 2000 Sustainable Communities Act 2007 Education and Skills Act 2008 Clean Neighbourhoods and Environment Act 2005

Voluntary/not-for-profit organisations (the Community and Voluntary Sector

Organisations who aim to raise aid for their stated cause Voluntary organisations such as the Voluntary Services Organisation Organisations operating under a charitable

status where money is not raised for a cause, but rather invested back into the operation, eg City & Guilds.

Charities

Charities are registered at the Charities Commission

There are three main charitable entities:

1. Unincorporated associations 2. Charitable trusts3. Private companies limited by guarantee

Unincorporated associations

The most common form within the voluntary sector Has a particular purpose Has a constitution Officers of the organisation can be personally liable if the charity is sued or has debts

Charitable trusts

A relationship between three parties:

1. The donor of some assets2. The trustees who hold the assets 3. Those people eligible to benefit from the charity.

The governing document is the Trust Deed or Declaration of Trust.

Private company limited by guarantee

Has members who act as guarantors instead of shareholders. The guarantors give an undertaking to contribute a nominal amount in the event of the

winding up of the company. Common uses of companies limited by guarantee include clubs and membership

organisations, charities (eg Oxfam).

The Charity Act 2011

Main legislation affecting voluntary sector organisations Sets out the conditions an organisation must

fulfil in order to have charitable status

Private sector organisations

Types of organisation

Sole trader Partnership Private limited company Public limited company Charity

Requirements to set up as a sole trader

Register the business name with the National Business Register Register with the HM Revenue & Customs as self-employed

Setting up a partnerships

‘Nominated partner’ is chosen Responsible for managing the partnership’s tax returns and keeping business records Partnership and nominated partner must be registered for tax self-assessment with HMRC Other partners register separately All the partner’s names as well as the business name should be included on any official

paperwork

Setting up a private limited company

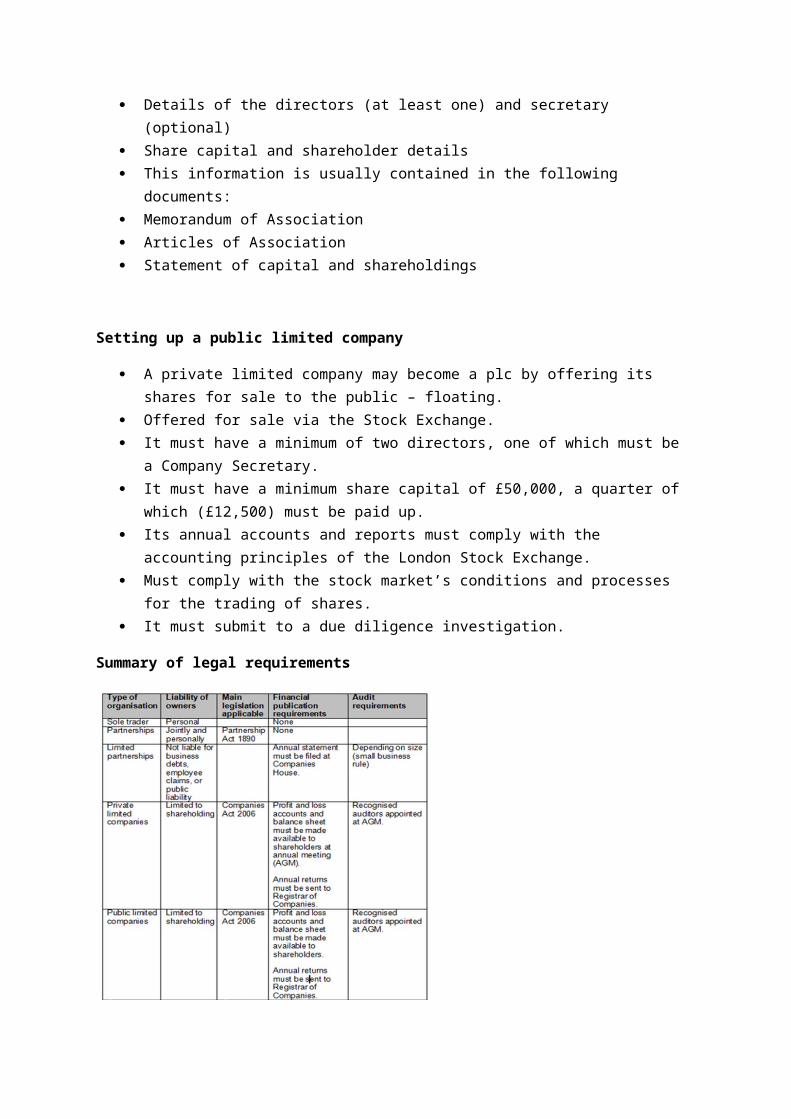

Details that need to be registered at Companies House: Company name and address Details of the directors (at least one) and secretary (optional) Share capital and shareholder details This information is usually contained in the following documents: Memorandum of Association Articles of Association Statement of capital and shareholdings

Setting up a public limited company

A private limited company may become a plc by offering its shares for sale to the public – floating.

Offered for sale via the Stock Exchange. It must have a minimum of two directors, one of which must be a Company Secretary.

It must have a minimum share capital of £50,000, a quarter of which (£12,500) must be paid up.

Its annual accounts and reports must comply with the accounting principles of the London Stock Exchange.

Must comply with the stock market’s conditions and processes for the trading of shares. It must submit to a due diligence investigation.

Summary of legal requirements

Companies House

The main functions of Companies House: Incorporate and dissolve limited companies Examine and store company information delivered under the Companies Act and related

legislation Make this information available to the public

Business markets

Standard Industry Categories (SIC)

The primary sector covers the industries that extract or produce raw materials from the land, eg farming or fishing, extractive industries.

The secondary sector is concerned with industries that process and produce items, such as any kind of manufacturing.

The tertiary sector includes wholesalers and retailers. It also includes services such as banking, insurance, hairdressing, etc.

Characteristics of organisations in the primary sector

Use materials provided by nature Location driven by the materials Customers are other businesses

Characteristics of organisations in the secondary sector

Heavy or light manufacturing Focus on transformation of materials Require:

access to raw materialslabour forcetransportation of product to market.

Located out of town Customers are other businesses

Characteristics of organisations in the tertiary sector

Wholesalers, retailers and service providers Focus on interaction between people Location may be important, eg to attract trade Customers may be businesses or members of the public Use of publicity to attract customers

B2B and B2C

Business to Business (B2B)

Providing raw goods for manufacture, processing Selling of goods to wholesalers or retailers Transportation of raw materials or goods Providing services, eg legal, financial

Business to Customer (B2C)

Sales of goods – retail Delivery of goods Direct services, eg hairdressing, medical care, financial and legal

Reasons why businesses interact

Business transactions – buying and selling and transportation Supply chain Expertise To increase business by offering loyalty points or discounts at allied businesses To increase market share through alliance

To save money mounting joint promotions

Organisational objectives

Long-term aim - objectives Objectives - targets These targets may be in terms of:

1. Profit 2. Quality of service 3. Efficiency4. Development/expansion 5. Change/crisis management.

Factors that contribute to an organisation’s objectives

Economic sector Type Stakeholders Size Objectives are likely to be: Directional – eg market leadership Performance related – eg growth in profit, length of waiting lists Internal – eg efficiency of operation External – eg social responsibility, corporate image.

Objectives of different types of organisation

Private sector – focus on the customer and increasing business Public sector – concentrate on the service they offer Not-for-profit sector – focus on maximising aid to their cause

Mission and vision statements

Vision statement – long-term aspirations Mission statement – broadly states the organisation’s goal

Mission statement

Comes down to primary goals and timelines. Each type of company has a way of defining success through business goals, and the

strategies put into place to achieve those objectives.

A sales-driven firm tends to think about these strategies and objectives in the short term, while a market-driven firm views its goals as long-term benchmarks.

Example private sector mission statement

‘To enable people and businesses throughout the world to realize their full potential.’

Microsoft

Example not-for-profit mission statement

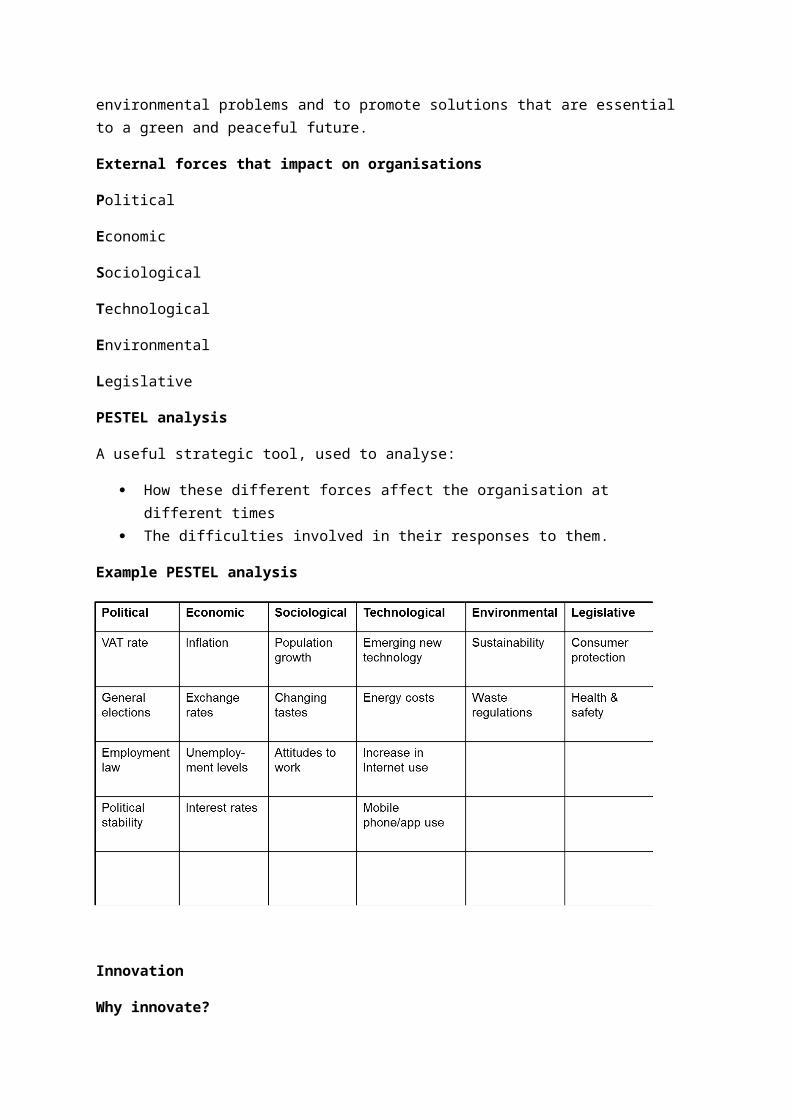

Greenpeace is the leading independent campaigning organization that uses peaceful protest and creative communication to expose global environmental problems and to promote solutions that are essential to a green and peaceful future.

External forces that impact on organisations

Political

Economic

Sociological

Technological

Environmental

Legislative

PESTEL analysis

A useful strategic tool, used to analyse:

How these different forces affect the organisation at different times The difficulties involved in their responses to them.

Example PESTEL analysis

Innovation

Why innovate?

To improve performance To keep ahead of the game To find new and more efficient ways To create value from ideas To seek new approaches to work

Models of business innovation

New ways of doing business Value propositions Innovation ecosystem Social innovations

Innovation may relate to:

Emerging new technologies The market The economic and political climate New regulations or legislation Competitors Environmental issues

Reasons why an organisation reviews the ways it works

Increasing efficiency, profitability, productivity Greater competitiveness Better use of resources Reducing costs Better response to customer requirements Increasing customer satisfaction Reducing in waste

Positive ways of reviewing working methods

Seeking feedback from both customers and staff Effective, two-way communication within an organisation Listening and responding to staff suggestions

Process for developing new products or services

Idea generation Idea screening Concept testing Business analysis Product development Test marketing Commercialisation Review of market performance

Introducing new working methods, products or services

May impact upon one or more of the following:

The business as a whole Management structures Departments within a business Employees in teams Individuals Customers Competitors

Sources of support and advice for business innovation

Department for Innovation & Skills (BIS) Business Innovation Facility (BIF) Grants – government, European funded, local business grant schemes Technology Strategy Board (TSB) Innovation vouchers

Implications of innovation

Approaches to innovation

Continuous improvement Introducing complementary products or services Product development Exploiting technology to create new or improve old

Benefits of introducing innovation

Being the first in the field Improved competitiveness Increasing/widening market share Increasing productivity Reducing staff turnover Increasing staff morale Attracting new customers/clients

Risks associated with introducing innovation

Leakage of ideas Failure – waste of resources Going over budget/risk of return Underestimating development time Over-/underestimation of demand May not be embraced by all customers

Implications of introducing innovation and change

Changed culture Effect on share price Staff training Staff skills gap Impact of change on staff morale

How change affects people

Change can cause concern and anxiety to those it affects.

Many people are resistant to it. Individuals will respond differently depending

on their personalities.

Encouraging and using ideas from staff

Customer-facing staff often the ones to see where improvements could be made. Staff more likely to respond positively to proposed innovations if they have had a hand in

them. They will be convinced of benefits to organisation and to themselves. Sharing of ideas breaks down barriers and can be motivating. If team members feel that they are listened to and their ideas are valued, they will be more

positive and enthusiastic in embracing innovations.

Managing change

How change affects people

Change can cause concern and anxiety to those it affects. Many people are resistant to it. Individuals will respond differently depending on their personalities.

Those affected may experience:

Shock and/or denial Stress and/or discomfort Distrust Regret Anger Acceptance Guilt Hope Depression Excitement and/or expectation Anxiety and/or fear.

Communication

Change must be openly communicated.

It isn’t the change that creates the anxiety, so much as anxiety about the change.

Concerns associated with change

Job security Re-grading Prestige, eg existing skills no longer required Social ties – new team Anxiety about new requirements of work

Motivation

Key motivating factors provide: A sense of achievement Personal growth A chance to take responsibility Recognition for the work done A chance to use initiative Interesting work.

Support for employees when introducing innovation

Involvement/consultation on ways of implementing changes, new systems Training/re-training on new systems, technologies Financial, eg relocation costs

Work with colleagues and employers

The benefits of working with others:

Mutual support Feedback of problems Consistency of service Chance to contribute

The positive aspects of change

Change brings opportunities to gain new experience/promotion Change can provide the opportunity to learn new skills Resistance to change is normal Change increases motivation Change can provide a new challenge, which builds confidence and personal growth Change allows the organisation to keep up with a changing business environment and

remain competitive

Management skills required

Good communication skills Versatility

Patience Knowledge of the change – when, why and how it is to be implemented How to diffuse difficult situations How to evaluate the impact of the change How to be proactive in managing the change

Financial management

Finance

Every organisation needs finance to ensure:

Profitability Survival. Private organisations exist to make a profit. Public organisations must have sufficient finance to fulfil their public service obligations. Voluntary organisations need funds for their cause and to finance their operation.

Cash flow

The movement of money in and out of an organisation. In through sales of goods/services. Out through payment of costs:

1. Raw materials2. Staff/labour3. Transport4. Rent5. Power and lighting.

Liquidity

Liquid assets are those that are easily converted to available cash. Stocks and shares in other organisations = very liquid assets. Premises owned by the organisation = least liquid asset. An organisation is liquid when it has assets that can easily be converted to provide cash for

use immediately or in the near future.

Balance sheet

Lists assets and liabilities of an organisation at a given date

Lists assets in order of realisability Lists liabilities in order of priority Provides a snapshot of the organisation’s liquidity Capital + Liabilities = Assets

Aims of financial management

To ensure:

Cash flows in and out are controlled Enough cash available to pay costs Enough cash available for investment Cash not tied up unprofitably, eg in stock Procedures to realise the cash from revenue, eg that debtors’ invoices are paid on time.

Ways to improve cash flow

Realising or making unused assets work, eg renting out unused premises Rigorous procedures for obtaining payments Offering discounts for fast payment of invoices Using hire purchase/leasing for capital assets to spread payments Negotiating trade terms from suppliers Accurately forecasting cash flow to anticipate and plan for problems

Profit and loss accounts

A statement of revenue and costs for an organisation over a specific period Total income – Total operating costs = Profit/loss A positive result is the net profit A negative result indicates a loss

Functions of financial management in an organisation

To ensure finance is available to meet strategic aims To use finance cost-efficiently through investment To use analysis of internal and external financial information to provide management with

accurate forecasts To ensure compliance with legal requirements for financial reporting To control and monitor use of funds throughout the organisation To inform future financial strategy for the organisation

Consequences of poor financial management

Decrease in profits Inability to expand/raise capital Difficulty in obtaining credit from suppliers Inability to pay wage bill Loss of market share Liquidation/administration

Public sector finance

Public organisations must have sufficient finance to fulfil their public service obligations. Funded by the public through their taxes: Centrally Locally

Sources of finance

Central taxes, eg Income tax VAT Road tax Stamp duty Duty on petrol, tobacco, alcohol, etc. Local taxes, eg Business rates Council tax

Additional sources

Funds from government borrowing Monies received for specific activities from the

European Union Grants from the Treasury via the relevant

government department Locally through car parking fees or hiring of

leisure facilities, etc

Spending reviews

Sets spending budgets over several years for each government department.

Budgets are set according to the Government’s priorities.

Government departments decide how best to manage and distribute this budget within their areas of responsibility

Funding efficiencies

Public organisations operate using public funds Essential not to waste money and use resources effectively. Organisations must: Spend public money effectively Make best use of their resources Behave in an environmentally friendly way Contribute to sustainable economies and communities. Limited funds means: Cuts may have to be made Prioritisation of services.

Commissioning and procurement

Procurement – obtaining required goods or services.

Competitive tendering process – invites companies to quote for the supplying the goods or services to ensure value for money.

Commissioning – checking that a process or project has been carried out as required.

‘... a large amount of public sector activity involves the commissioning and purchasing of goods and services. Doing so effectively requires a clear understanding of what will most appropriately address the needs or wishes of the service user, making use of market research, good planning, financial and performance management, sharing best practice and learning lessons.’

National Audit Office

Monitoring

The National Audit Office monitors central government. The Audit Commission monitors local public services.

Budgets

What are budgets?

A budget is an itemised statement of finances available over a specific period.

Budgets are either:

Capital Operational. Capital budgets relate to planned spending on fixed assets such as equipment or machinery. Operational budgets relate to the planned income and expenditure of a specific activity over

a period of time.

Overall purpose of budgets

To plan, monitor and control spending throughout the organisation. To manage financial resources effectively. To authorise and delegate authority for decision-making based on finance.

Functions of budgets

Investing in necessary equipment (capital) Ensuring sufficient resources for operation (operational) Managing cash flow Allocating resources Establishing priorities Managing financial resources effectively Authorising and delegating authority Co-ordinating and controlling activities Motivating management and staff Providing a framework for responsibility and control Accountability and evaluation of performance

Translating aims and objectives into financial terms

Types of budget

Business start-up Corporate Event management Sales Production Project Marketing

Preparing budgets

The stages in preparing a budget are:

Agree and define the purpose of the budget Agree the source of income – define the limiting factor Identify possible costs involved Research the costs Present the budget Negotiate and amend.

Forecasting

Identify:

Essential and non-essential expenses Priorities Key elements. Estimations of costs should be researched for accuracy. Base estimations on recent past experience, allowing for inflation and contingencies. A contingency is an allowance that is built in to deal with any unforeseen rise in costs and is

usually formed of a percentage amount added on to the budget.

Effect of time, priorities and resources on a budget

The tighter the timescales, the more money and resources will be required in order to achieve them.

Cutting the budget will mean fewer resources are available, and therefore the timescales will increase

Managing budgets

Reasons for monitoring a budget

To ensure finance stays on target for the period Income and expenditure need to be compared against the budget in order to control

finances

To provide reliable information when the budget is analysed, eg for the following year’s provision

Monitoring a budget

You will need to know: The amount of the budget The period it covers How it was built up – what activities/items it covers What has been spent against it What revenue there has been What future commitments there are against it.

Techniques to manage a budget

Responsibility for a budget should be assigned to a named individual

Accurately record income/expenditure Compare actual income/expenditure against

forecast figures Review budget performance reports Control/manage resource usage – particularly consumables Regular meetings between budget-holders and line managers to identify any required

corrective actions

Monitoring budgets – cost codes

Income and expenditure must be recorded and this is usually by means of a cost or budget code

Costs codes are used on invoices, timesheets, requisitions, etc Informs as to the amount left

in the budgets

Variances

Variances are differences between initial estimations of ongoing costs and actual costs Variances need to be investigated and analysed and action taken if possible Favourable budget variance indicates a gain Unfavourable budget variance means a loss or shortfall Often due to recording errors or omissions

Budget revisions

Serious variances require corrective action to: Reduce costs Follow up outstanding income Negotiate a revision to the budget. External factors that may lead to the revision of a budget may include:

Economic factors, such as inflation, recession or growth Employment factors Legislative factors Political factors. Internal factors may be, eg New product development Structural Industrial relations.

Market research

The formal gathering of information about what an organisation’s target customer base wants.

Used to gather statistics/opinions in order: To find out what the target market wants To inform organisational strategy To inform new product/service development To understand how best to market a product/service.

Types of market research

Primary Quantitative Qualitative Secondary

Primary researchAdvantages

Can be targeted specifically to what you need to know Can be designed to gather both quantitative and qualitative data Researcher is in control of how much data is collected

Disadvantages Cost Time-consuming Requires careful planning in order to be useful

Secondary researchAdvantages

Easy to carry out Less time-consuming Cost-effective

Disadvantages Not specific to need Questionable if sources are not properly scrutinised

Methods of carrying out primary market research

Face-to-face interviews, eg in the street, door to door Telephone interviews Postal questionnaires Omnibus surveys

Types of sampling Occasional Random Stratified Quota

Types of information gatheredInformation on:

Market trends Product – existing and potential for development Pricing – competitors’ and customers’ expectations Promotion – effectiveness and strategies Distribution – effectiveness of different methods

Characteristics of market research Has a purpose Systematic and planned Objectives stated in a clear, concise, attainable, measurable and quantifiable way Has a time frame Has a resource allocation, including a budget and facilities Is objective Uses both qualitative and quantitative data Should be a continuous process Collects, records and analyses information Provides solutions for marketing problem

Marketing

Definition of marketing

According to the Chartered Institute of Marketing:

‘Marketing is the management process responsible for identifying, anticipating and satisfying customer requirements profitably.’www.cim.co.uk

Function of marketing

To ensure the organisation produces the right product at the right price and to get that product to the customers who will buy it.

Without marketing, it is unlikely that the organisation will be able to attract customers to buy its product/services.

Roles of marketing

The marketing department is likely to be involved in the following:

Carrying out market research Identifying/sourcing potential new products Product/service development Setting the market price of products Promoting products/services Advertising Identifying potential customers for sales Public relations Customer service Identifying distribution channels for products.

The marketing mix

The 4Ps

Product Price Place Promotion

Product

The right product for customers:

What they want – the product meets their needs Provides quality and value Provides the benefits they are looking for Products can also be intangible – eg a package holiday

Price

The right price to represent value for the customer Must also achieve profit for the organisation Must be competitive The higher the price, the higher the perceived quality

Promotion

The way the organisation communicates the benefits of its products to a customer Must be cost-effective Must be suitable for the product/service Starts with the employees

Place

The right place to attract customers – shop window, Internet

Also covers how the organisation gets the product to the customer – distribution

Right place, right time, right quantity

The 7Ps

A tool appropriate to marketing services rather than physical products

Adds three further criteria to the 4Ps:

People Process Physical evidence.

People

People that provide the service – the staff Must have adequate knowledge and training Must have the right attitude to provide customer satisfaction Are the representatives of the organisation and

all it stands for

Process

Systems the customer has to go through in order to access the service: How they make initial contact Waiting times Ease of use Access to information Helpfulness of the staff

Physical evidence

Evidence that the service has been performed Customer can see that they have received the service Also applies to evidence suggestive of the quality of service before it is received

Marketing strategies and methods of promotion

Market segmentation

Groups customers according to different factors

Helps promotion of products by targeting customers’ needs

Segmentation factors:

1. Primary 2. Geographic3. Demographic

4. Psychographic

Promotion

Way the organisation communicates the benefits of its products to a customer

Above-the-line promotion Below-the-line promotion

Marketing strategies

Use the marketing mix Aim to meet an objective Change according to specific aims Examples of marketing objectives: Increase sales by 20% Launch a new product next year Break into the international market

B2B vs B2C

Strategies differ

B2B strategies focus on the results/benefits the product/service will bring, eg in terms of saving time, money or resources

B2C strategies also focus on emotional elements, eg desirability, as well as different distribution channels

AIDAAttention: to attract the customer’s attentionInterest: to provoke the customer’s interest by highlighting advantages and benefits of the product/serviceDesire: to convince customers that this is the product/service they needAction: to lead customers to purchase or commit

Branding and sales

Function of sales

An organisation needs to sell its products/services in order to survive; the sales function persuades the customer to buy and closes the sale.

Roles of sales

Obtaining new accounts Managing existing accounts Persuading customers to buy Processing orders Directing sales activities

Training sales staff Customer service After-sales services

Sales strategies

Face to face Telephone – telesales Travelling sales representatives Mailshots Business to business

(B2B)

The seven-step sales process

Product knowledge Prospecting Approach Needs assessment Presentation Close Follow up

What is a brand?

Promise an organisation makes to its customers Incorporates the organisation’s character and culture When an organisation fulfils its brand’s promise, the brand can be said to have value.

Elements of a brand

Organisation name Trademark logo Tagline or slogan Graphics Shape used for eg packaging, or a shape element present in the product that creates a

‘family’ trait Colours Sounds, eg Intel’s four musical notes

The value to an organisation of creating a good brand

Positioning Identity Recognition – brand awareness Customer loyalty