Embed Size (px)

Citation preview

TV & Video Forum

Can the Internet handle everything?

Florence LE BORGNE

Head of TV & Digital Content Practice, IDATE

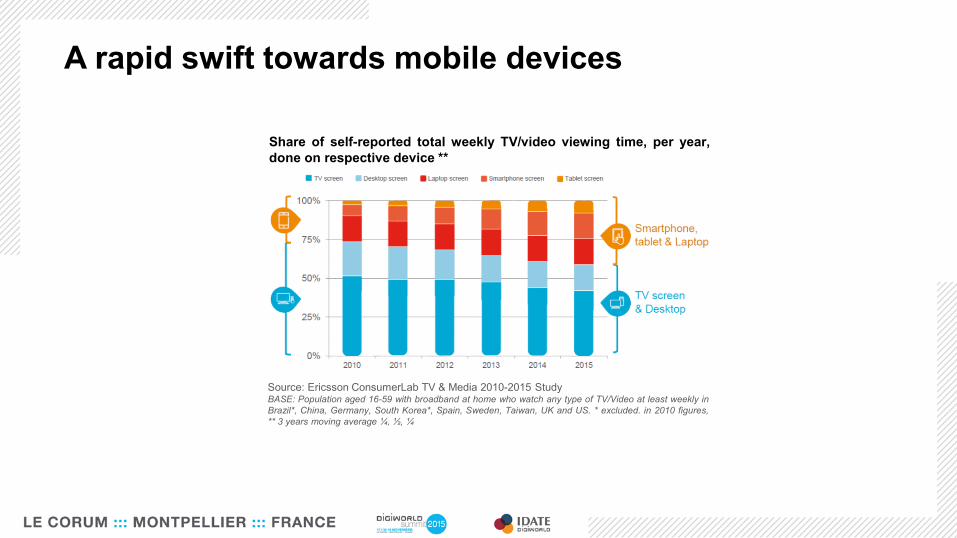

Source: Ericsson ConsumerLab TV & Media 2010-2015 StudyBASE: Population aged 16-59 with broadband at home who watch any type of TV/Video at least weekly in

Brazil*, China, Germany, South Korea*, Spain, Sweden, Taiwan, UK and US. * excluded. in 2010 figures,

** 3 years moving average ¼, ½, ¼

Share of self-reported total weekly TV/video viewing time, per year,

done on respective device **

A rapid swift towards mobile devices

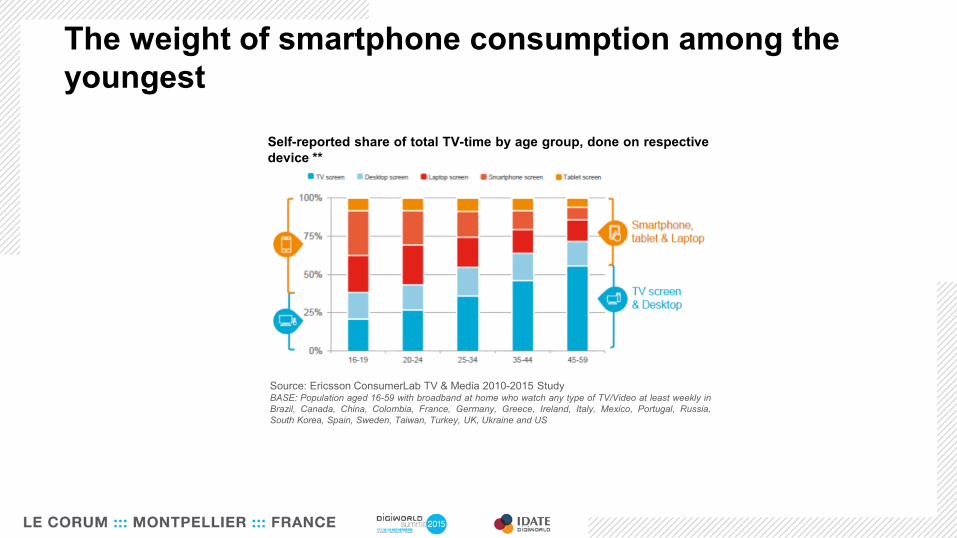

Source: Ericsson ConsumerLab TV & Media 2010-2015 StudyBASE: Population aged 16-59 with broadband at home who watch any type of TV/Video at least weekly in

Brazil, Canada, China, Colombia, France, Germany, Greece, Ireland, Italy, Mexico, Portugal, Russia,

South Korea, Spain, Sweden, Taiwan, Turkey, UK, Ukraine and US

Self-reported share of total TV-time by age group, done on respective

device **

The weight of smartphone consumption among the

youngest

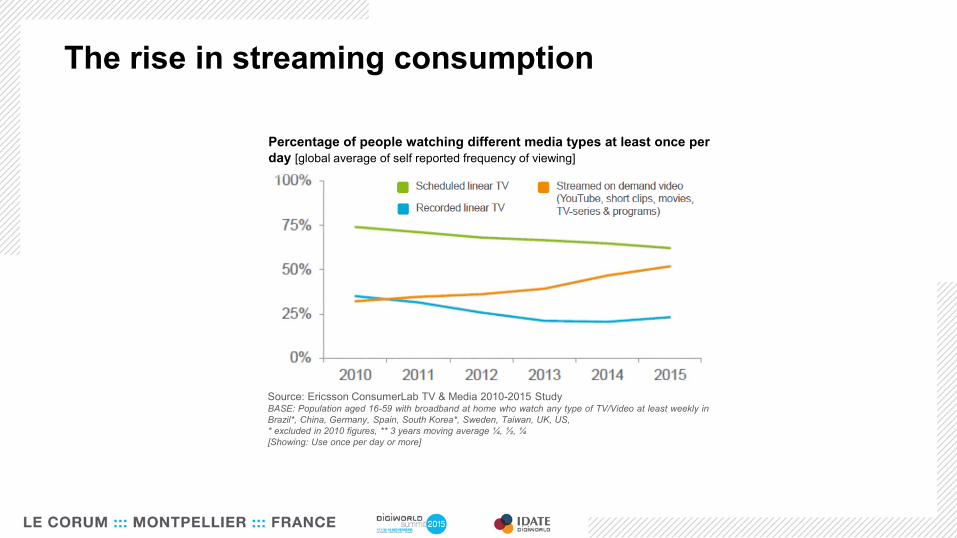

Source: Ericsson ConsumerLab TV & Media 2010-2015 StudyBASE: Population aged 16-59 with broadband at home who watch any type of TV/Video at least weekly in

Brazil*, China, Germany, Spain, South Korea*, Sweden, Taiwan, UK, US,

* excluded in 2010 figures, ** 3 years moving average ¼, ½, ¼

[Showing: Use once per day or more]

Percentage of people watching different media types at least once per

day [global average of self reported frequency of viewing]

The rise in streaming consumption

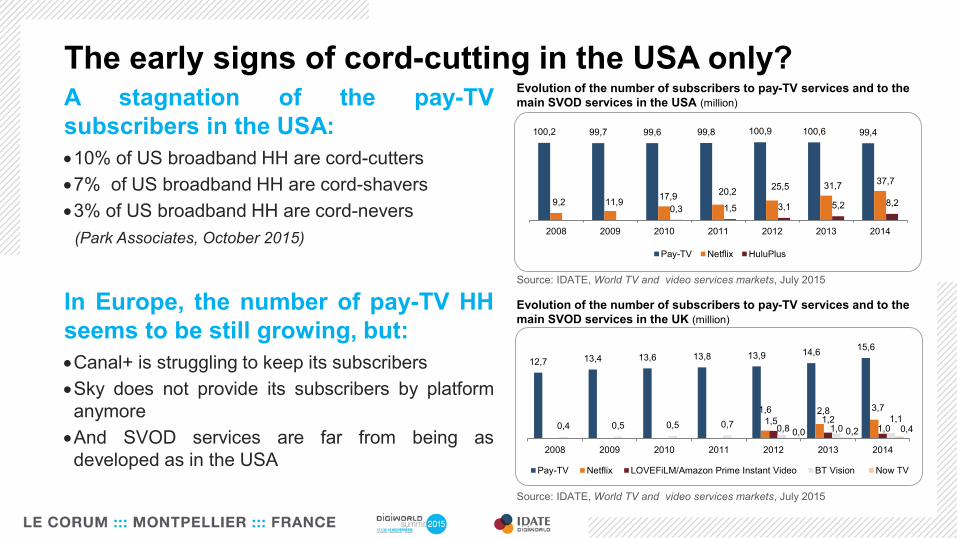

A stagnation of the pay-TV

subscribers in the USA:

10% of US broadband HH are cord-cutters

7% of US broadband HH are cord-shavers

3% of US broadband HH are cord-nevers

(Park Associates, October 2015)

In Europe, the number of pay-TV HH

seems to be still growing, but:

Canal+ is struggling to keep its subscribers

Sky does not provide its subscribers by platform

anymore

And SVOD services are far from being as

developed as in the USA

The early signs of cord-cutting in the USA only?

Source: IDATE, World TV and video services markets, July 2015

Evolution of the number of subscribers to pay-TV services and to the

main SVOD services in the USA (million)

100,2 99,7 99,6 99,8 100,9 100,6 99,4

9,2 11,917,9

20,225,5 31,7

37,7

0,3 1,5 3,1 5,2 8,2

2008 2009 2010 2011 2012 2013 2014

Pay-TV Netflix HuluPlus

12,7 13,4 13,6 13,8 13,9 14,615,6

1,6 2,8 3,7

1,5 1,21,00,4 0,5 0,5 0,7 0,8 1,0

1,1

0,0 0,2 0,4

2008 2009 2010 2011 2012 2013 2014

Pay-TV Netflix LOVEFiLM/Amazon Prime Instant Video BT Vision Now TV

Source: IDATE, World TV and video services markets, July 2015

Evolution of the number of subscribers to pay-TV services and to the

main SVOD services in the UK (million)

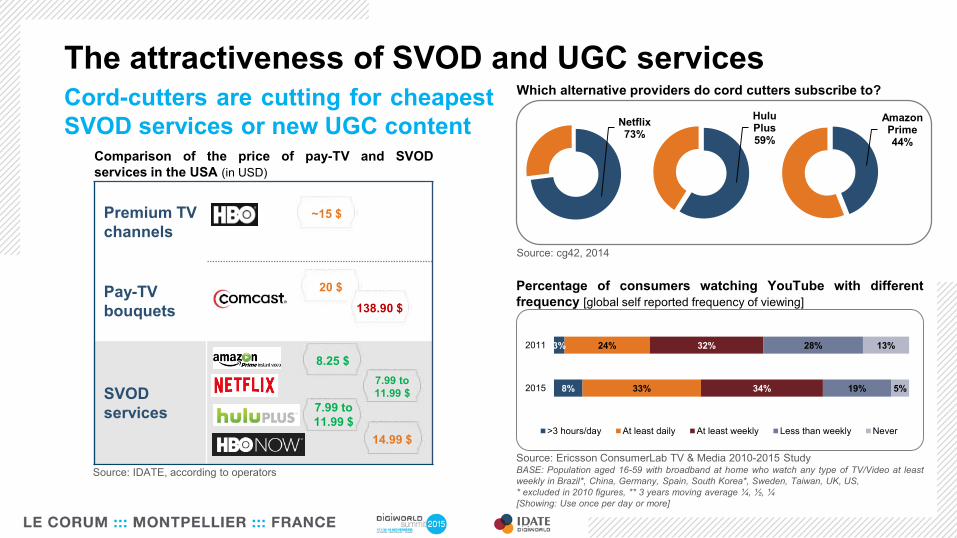

Source: Ericsson ConsumerLab TV & Media 2010-2015 StudyBASE: Population aged 16-59 with broadband at home who watch any type of TV/Video at least

weekly in Brazil*, China, Germany, Spain, South Korea*, Sweden, Taiwan, UK, US,

* excluded in 2010 figures, ** 3 years moving average ¼, ½, ¼

[Showing: Use once per day or more]

Percentage of consumers watching YouTube with different

frequency [global self reported frequency of viewing]

8%

3%

33%

24%

34%

32%

19%

28%

5%

13%

2015

2011

>3 hours/day At least daily At least weekly Less than weekly Never

Cord-cutters are cutting for cheapest

SVOD services or new UGC content

The attractiveness of SVOD and UGC services

Amazon Prime44%

Hulu Plus59%

Netflix73%

Source: cg42, 2014

Which alternative providers do cord cutters subscribe to?

Premium TV

channels

Pay-TV

bouquets

SVOD

services

8.25 $

7.99 to

11.99 $

7.99 to

11.99 $

14.99 $

20 $

138.90 $

~15 $

Source: IDATE, according to operators

Comparison of the price of pay-TV and SVOD

services in the USA (in USD)

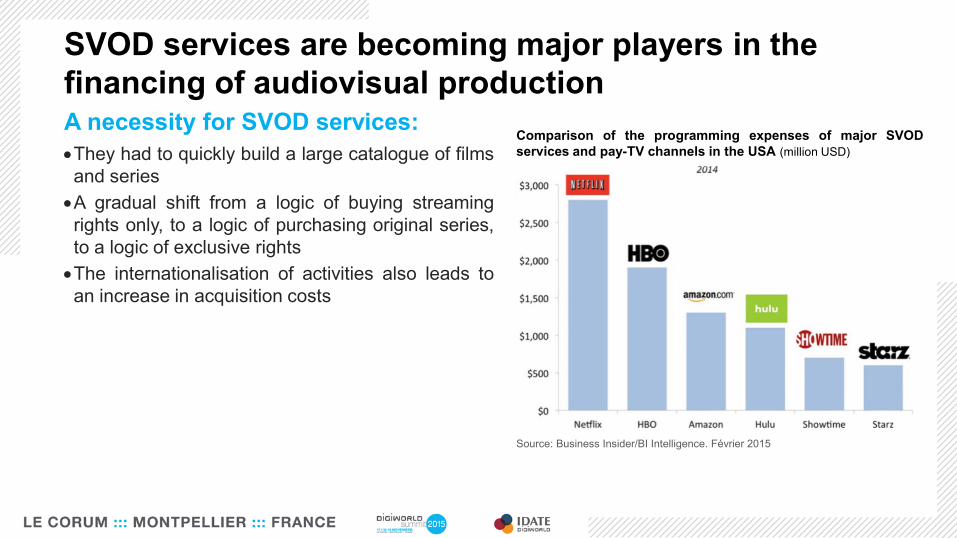

Source: Business Insider/BI Intelligence. Février 2015

Comparison of the programming expenses of major SVOD

services and pay-TV channels in the USA (million USD)

SVOD services are becoming major players in the

financing of audiovisual production A necessity for SVOD services:

They had to quickly build a large catalogue of films

and series

A gradual shift from a logic of buying streaming

rights only, to a logic of purchasing original series,

to a logic of exclusive rights

The internationalisation of activities also leads to

an increase in acquisition costs

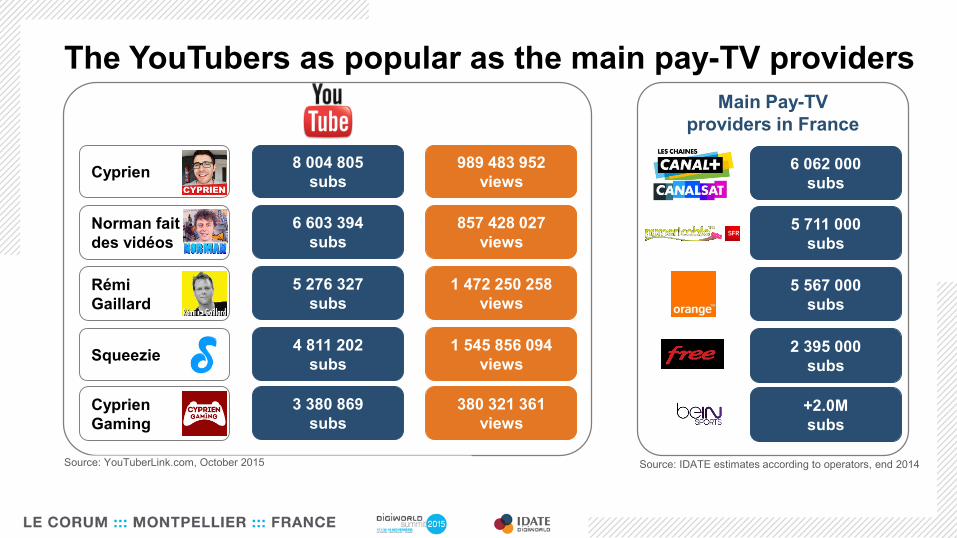

The YouTubers as popular as the main pay-TV providers

Cyprien

Norman fait

des vidéos

Rémi

Gaillard

Squeezie

Cyprien

Gaming

8 004 805

subs

6 603 394

subs

5 276 327

subs

4 811 202

subs

3 380 869

subs

989 483 952

views

857 428 027

views

1 472 250 258

views

1 545 856 094

views

380 321 361

views

Main Pay-TV

providers in France

6 062 000

subs

5 711 000

subs

5 567 000

subs

2 395 000

subs

+2.0M

subs

Source: YouTuberLink.com, October 2015 Source: IDATE estimates according to operators, end 2014

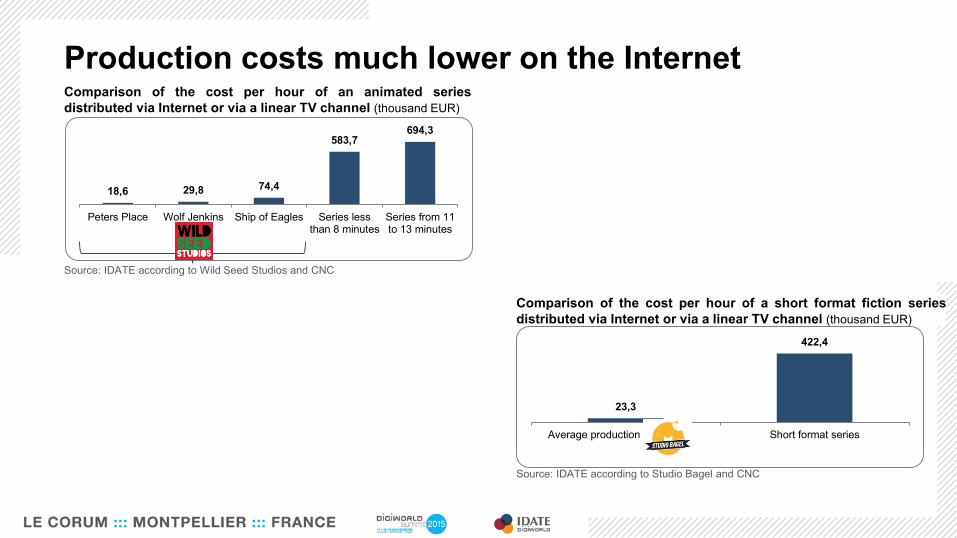

Source: IDATE according to Studio Bagel and CNC

Comparison of the cost per hour of a short format fiction series

distributed via Internet or via a linear TV channel (thousand EUR)

Production costs much lower on the Internet

23,3

422,4

Average production Studio Bagel Short format series

18,6 29,8 74,4

583,7694,3

Peters Place Wolf Jenkins Ship of Eagles Series lessthan 8 minutes

Series from 11to 13 minutes

Source: IDATE according to Wild Seed Studios and CNC

Comparison of the cost per hour of an animated series

distributed via Internet or via a linear TV channel (thousand EUR)

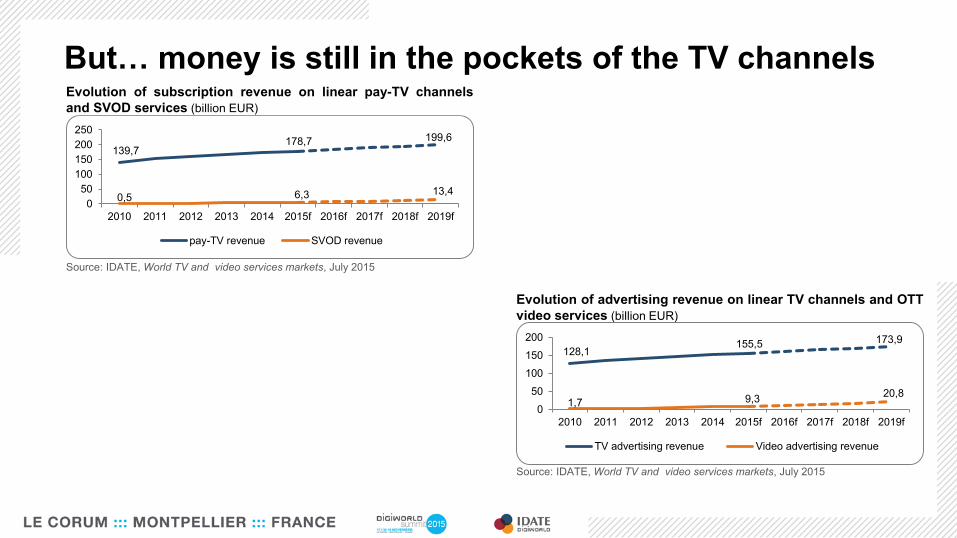

Source: IDATE, World TV and video services markets, July 2015

Evolution of advertising revenue on linear TV channels and OTT

video services (billion EUR)

But… money is still in the pockets of the TV channels

128,1155,5 173,9

1,7 9,320,8

0

50

100

150

200

2010 2011 2012 2013 2014 2015f 2016f 2017f 2018f 2019f

TV advertising revenue Video advertising revenue

139,7178,7 199,6

0,5 6,3 13,4

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015f 2016f 2017f 2018f 2019f

pay-TV revenue SVOD revenue

Source: IDATE, World TV and video services markets, July 2015

Evolution of subscription revenue on linear pay-TV channels

and SVOD services (billion EUR)

The future of TV/Video: Freeview Play…?

… Molotov TV…?

…or YouTube?

![[FR] PR Hangout of the DigiWorld Summit 2015 - #DWS15](https://img.pdfslide.us/doc/110x75/58e669e91a28ab8d758b62db/fr-pr-hangout-of-the-digiworld-summit-2015-dws15.jpg)