Embed Size (px)

Citation preview

Value for Money in the HA sector – An Update 2014/15Mick Warner -Deputy Director Operations

The self-assessment

The VfM standard sets specific expectations that a provider’s self- assessment must:

– enable stakeholders to understand the return on assets measured against the organisation’s objectives;

– set out the absolute and comparative costs of delivering specific services;

– evidence the value for money gains that have been and will be made and how these have and will be realised over time.

Accounts Direction specifies that providers must include a self- assessment in the Operating and Financial Review or Board Report.

The self-assessment is a key focus of the HCA’s regulatory activity

A recap of the 2013 VfM self-assessment reviews

First year in which providers were required to submit VfM self-assessment.

118 ‘partially’ complaint providers received letters.

15 providers had governance downgrades.

‘Unusual’ year end providers adhered to key messages sent out by the Regulator following September 2013 reviews.

Key messages sent out for 2014/15

Higher bar was set for 2014 VfM self-assessments.

Providers should have addressed all weaknesses that were cited in 2013 responses and publicly set out in publications / speeches.

We expect self-assessments to transparently address all the requirements of the standard.

Expectation that providers should develop a strategy to deliver continuous improvement year on year.

Regulator would not provide tailored feedback to compliant providers.

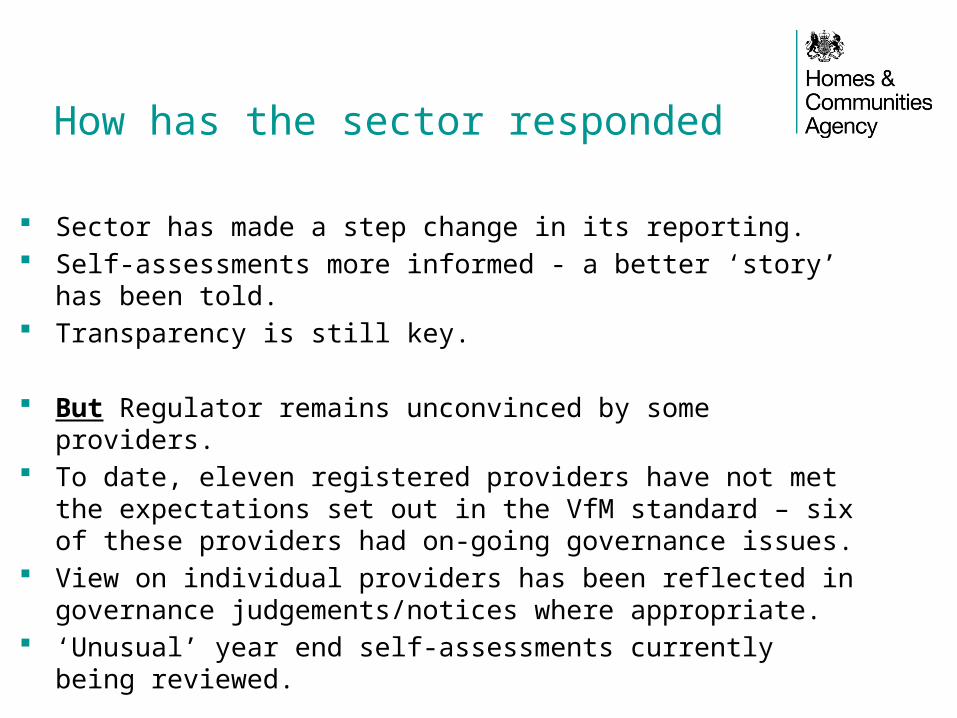

How has the sector responded

Sector has made a step change in its reporting. Self-assessments more informed - a better ‘story’ has been told. Transparency is still key.

But Regulator remains unconvinced by some providers. To date, eleven registered providers have not met the expectations

set out in the VfM standard – six of these providers had on-going governance issues.

View on individual providers has been reflected in governance judgements/notices where appropriate.

‘Unusual’ year end self-assessments currently being reviewed.

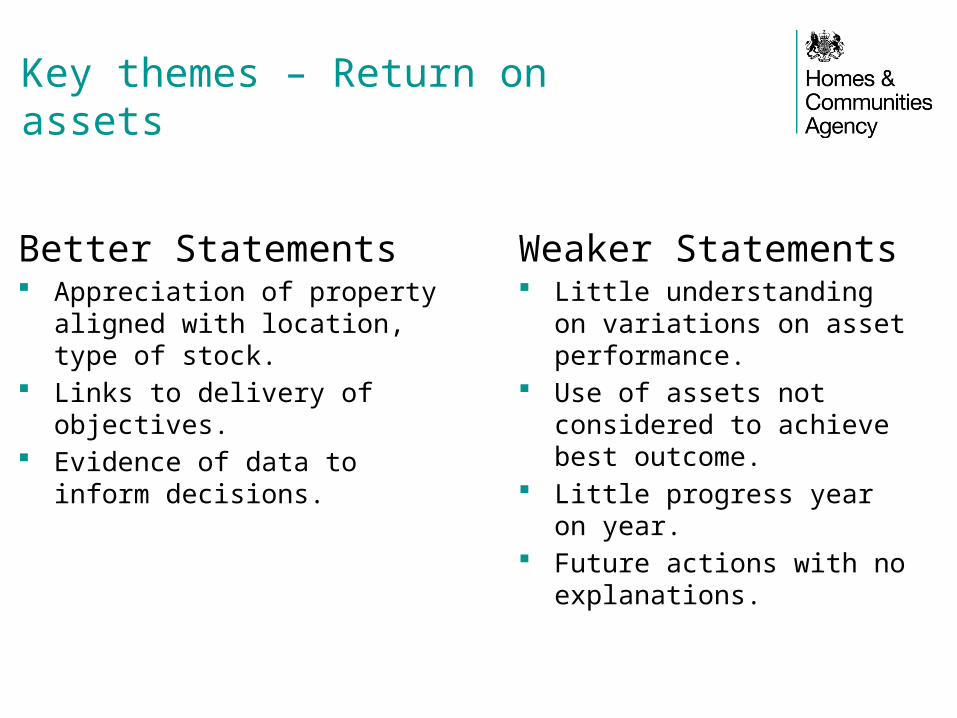

Key themes – Return on assets

Better Statements Appreciation of property aligned

with location, type of stock. Links to delivery of objectives. Evidence of data to inform

decisions.

Weaker Statements Little understanding on

variations on asset performance.

Use of assets not considered to achieve best outcome.

Little progress year on year. Future actions with no

explanations.

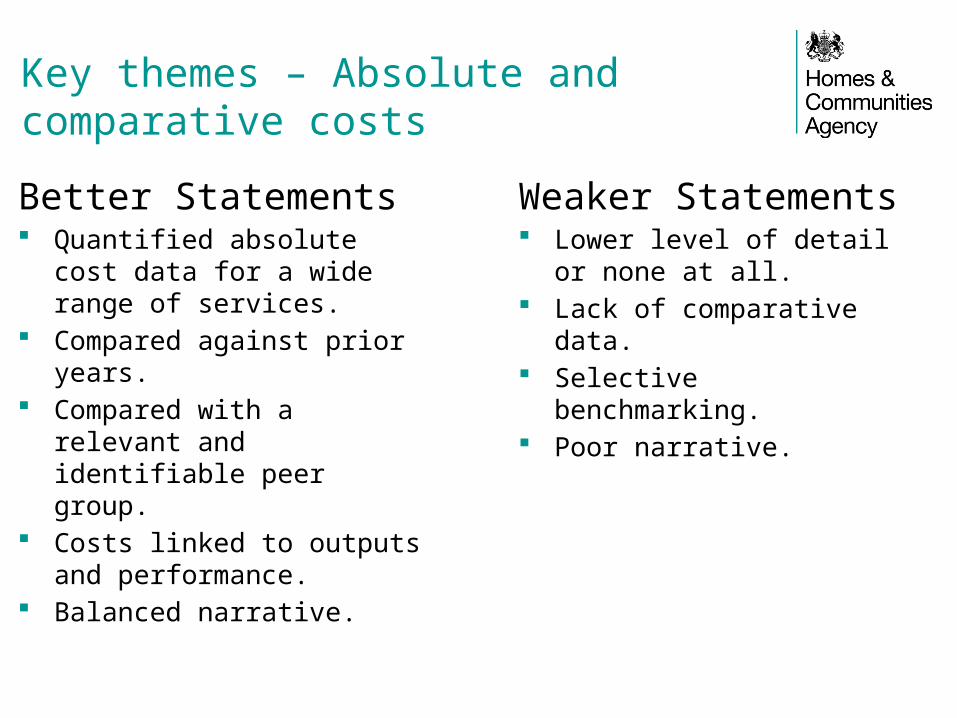

Key themes – Absolute and comparative costs

Better Statements Quantified absolute cost data

for a wide range of services. Compared against prior years. Compared with a relevant and

identifiable peer group. Costs linked to outputs and

performance. Balanced narrative.

Weaker Statements Lower level of detail or none at

all. Lack of comparative data. Selective benchmarking. Poor narrative.

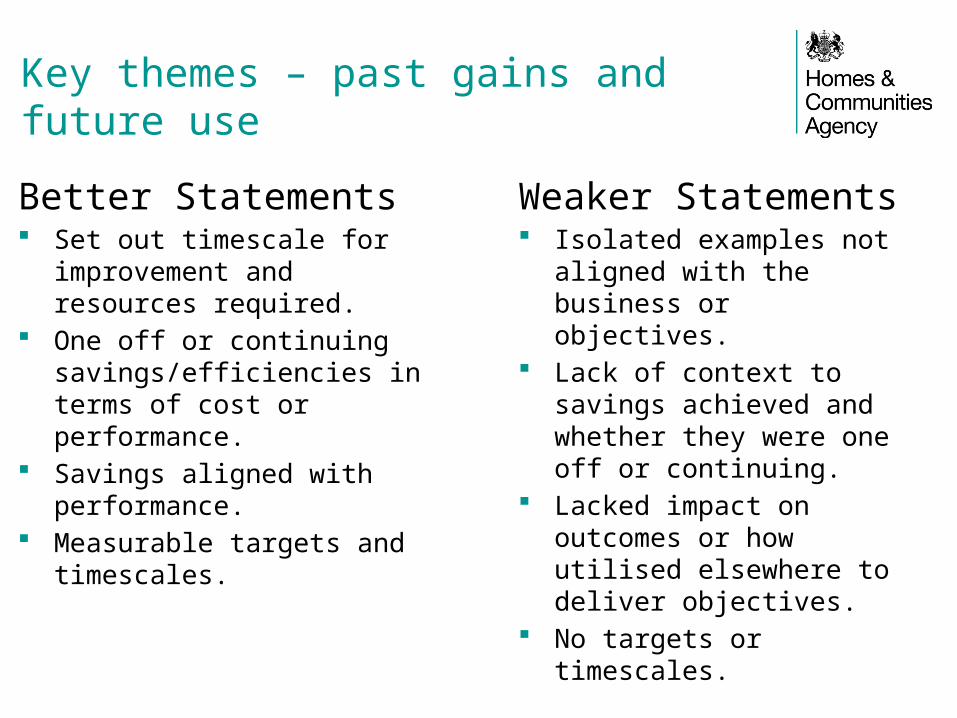

Key themes – past gains and future use

Better Statements Set out timescale for

improvement and resources required.

One off or continuing savings/efficiencies in terms of cost or performance.

Savings aligned with performance.

Measurable targets and timescales.

Weaker Statements Isolated examples not aligned

with the business or objectives.

Lack of context to savings achieved and whether they were one off or continuing.

Lacked impact on outcomes or how utilised elsewhere to deliver objectives.

No targets or timescales.

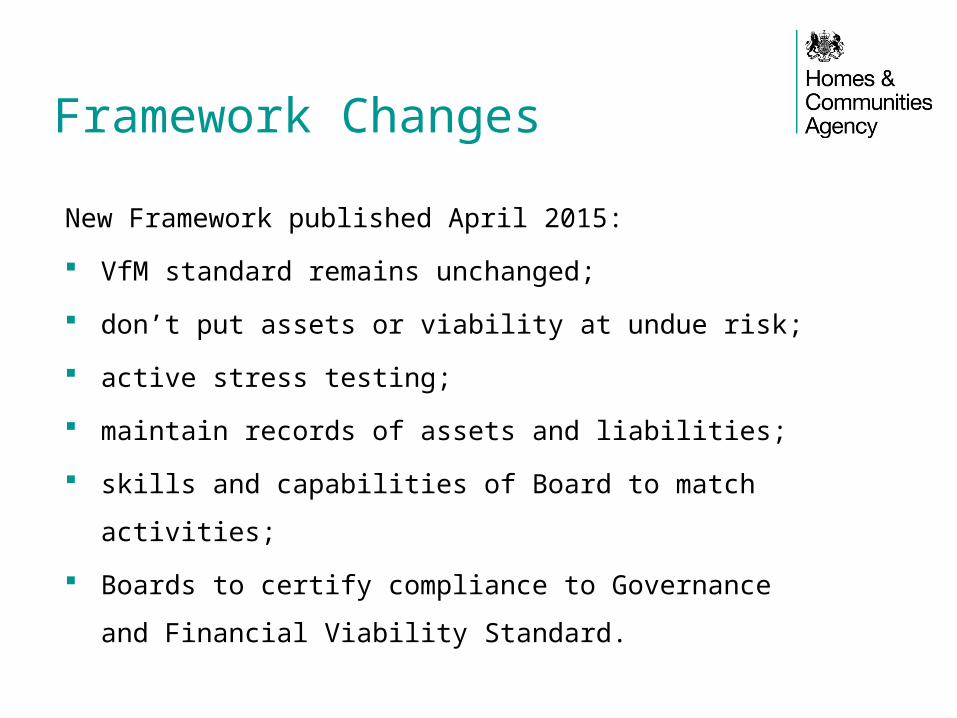

Framework Changes

New Framework published April 2015:

VfM standard remains unchanged;

don’t put assets or viability at undue risk;

active stress testing;

maintain records of assets and liabilities;

skills and capabilities of Board to match activities;

Boards to certify compliance to Governance and Financial

Viability Standard.

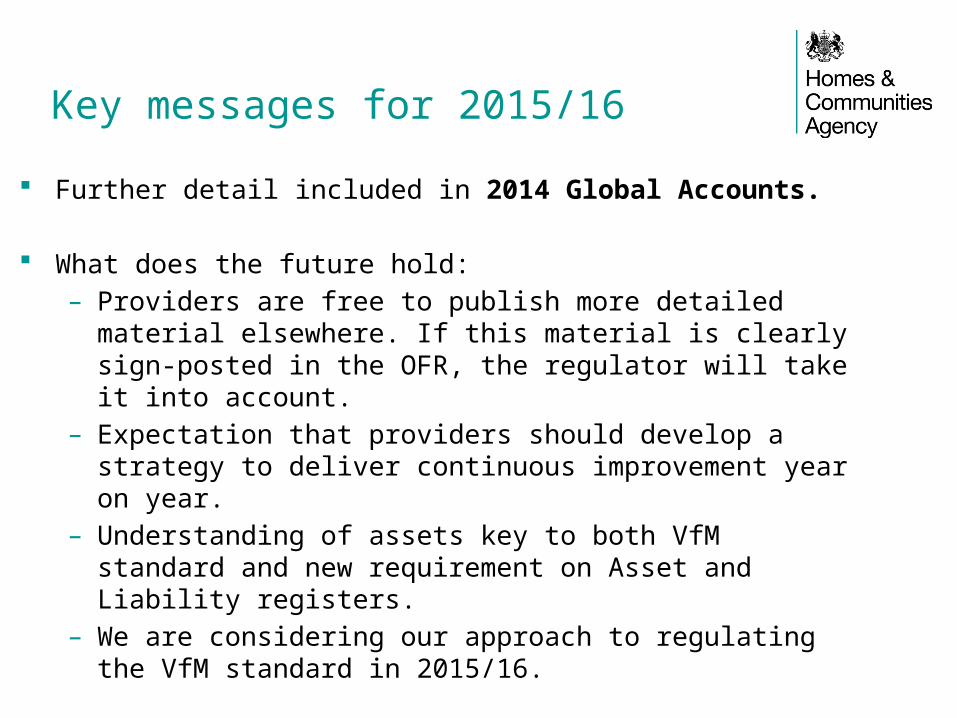

Key messages for 2015/16

Further detail included in 2014 Global Accounts.

What does the future hold:– Providers are free to publish more detailed material elsewhere. If

this material is clearly sign-posted in the OFR, the regulator will take it into account.

– Expectation that providers should develop a strategy to deliver continuous improvement year on year.

– Understanding of assets key to both VfM standard and new requirement on Asset and Liability registers.

– We are considering our approach to regulating the VfM standard in 2015/16.

Questions

![AnnuAl RepoRt2013...stian Riekhof and Joachim Ahrens took part in the event PFH meets Politics. [6] Mourning: Dr. Jörg Biethahn, Founding Professor of the PFH, died in September;](https://img.pdfslide.us/doc/110x75/5f066eaa7e708231d417f741/annual-report2013-stian-riekhof-and-joachim-ahrens-took-part-in-the-event-pfh.jpg)

![Robert Bosch GmbH€¦ · Performance Level a PFH d: ≥ 3 * 10–6 bis < 10–5 [h–1] Performance Level b PFH d: ≥ 10 –6 bis < 3 * 10 [h–1] Performance Level c PFH d: ≥](https://img.pdfslide.us/doc/110x75/605a5a095dc36760486a580d/robert-bosch-gmbh-performance-level-a-pfh-d-a-3-10a6-bis-10a5-ha1.jpg)