Embed Size (px)

Citation preview

Mobile Payments in the United StatesPerry Le DainNeera Jokitalo15.04.2016

Market Demand & Drivers

• Anywhere-anytime banking is becoming more and more common and expected by consumers. Consumer awareness of mobile banking and payment options is increasing.

• Business Insider forecasts that by 2019 mobile payment volume will reach 808 billion USD

• The number of people who make mobile payments at least once a year is projected to grow from 8% in 2014 to 65 % in 2019

• Major players at the moment are Apple Pay, Google Wallet, CurrentC, Samsung Pay. A continuously increasing amount of these providers will drive mobile payment adoption in consumers

• The widespread proliferation of smartphones and tablet PC’s is further driving the adoption of mobile paymentsolutions

• There are numerous regulatory influences in the United States under way in order to make the transition to mobile banking and payments easier. These are being driven by the realization that cashless transactions willhelp boost tax receipts, as well as improve transparency in the financial system and reduce costs associatedwith transactions

• Disruption of banking and new technologies provide many opportunities to the companies working in cybersecurity & data protection, analytics, and mobile payments

• Retailers are also realizing that mobile payment solutions have the potential to increase their revenues, reduceoperating costs, and improve customer satisfaction

• The widespread propogation of 4G/LTE networks will further drive the adoption of mobile payment solutionsby both retailers and consumers

• The time window to act on the opportunity is NOW!

5/16/2016 © Finpro 2

Opportunities in the USA

• Payments infrastructure is still antiquated (about 50% of B2B payments are done with checks). Finnish Fintech expertise can help transform the payments infrastructure in the United States.

• Due to the fragmented banking and crediting industry in the United States (>6500 banks, >6500 credit unions), integrating new payment technologies can be challenging. Finnish know-how can offer a solution to this problem.

• The market entry process takes time and is different to Europe. The companies need to invest time to study the market and opportunities closely.

• The Association of Financing Professionals is an important organization to follow http://www.afponline.org/. Other industry alliances and industry collaborations are being formed continuously: Smart Card Alliance Payments Council, Merchant Customer Exchange, Electronics Transactions Association, NFC Forum, MobeyForum, GSMA, Global Platform, and ITU.

• The Federal Reserve is developing a plan entitled "Strategies for Improving the U.S. Payment System," which presents a multi-faceted plan for collaborating with payment system stakeholders, including large and small businesses, emerging payments firms, card networks, payment processors, consumers and financial institutions to enhance the speed, safety and efficiency of the U.S. payment system.(http://www.federalreserve.gov/newsevents/press/other/20150126a.htm)

5/16/2016 © Finpro 3

Opportunities in Mobile Payments

• No mobile wallet service provider to date has managed to change consumer behavior to the extent that mobile payments are accepted as a mainstream form of paying. In order for mobile payments to become a part of every-day life, systems must provide:– Security– Privacy– Conveniance

• Product and service offerings in conveniance:– Interoperability of multiple payment platforms i.e. Universal Acceptance– P2P – Account aggregation and account-to-account interaction– Data collection and storage of consumption and payment habits– Mobile ticketing

• Product and service offerings in security and privacy:– Electronic signatures– Secure Element Implementation– Tokenization technologies– Trusted Execution Environments– Host Card Emulation– Biometric authentification, Audio-visual biometrics– Mobile fraud detection and prevention technologies– Mobile ID / Bank ID implementation

5/16/2016 © Finpro 4

Why Finland? Relevancy for Finnish companies

• Finland has a very forward-looking banking industry and extensive ICT know-how in key market segments, including mobile banking and payments, interoperability platforms, and fraud detections technologies

• 87% of Finns use online banking services, which are among the most secure in the world, and Finnish mobile operators have a jointly developed mobile payment service

5/16/2016 © Finpro 5

Mobile payment solution providers

which combine conveniance and security

Wone – Connects international mobile

payments and wallets using state of the

art smart contracts and block chain

technology

Moni – P2P payments, spending tracking,

invoicing

Pivo – Finnish mobile wallet

PayIQ – Mobile payments and ticket

service

Uniqul – Face recognition payments

Mobiwallet – Frictionless mobile payment

solutions for retail

Security providers for financial

institutions or retailers:

Crosskey Solutions – Internet banking

platform

Jetico – Data protection software

Movial – Secure mobile, embedded, and

cloud application development

Ariki – Biometric identification systems

for smart access

MePIN – Banking-grade security for

online identities and payments (already

in USA)

Companies with solutions for retailers

adapting to mobile payments

Holvi – Online bank account for SME’s

and organizations (acquired by BBVA)

Riskpointer – Creates mobile payment

applications for retailers, including data

and transaction analysis

Nordledger – Invoicing platform for

retailers/businesses based on block chain

technology

eTasku – Electronic receipts

Frosmo – User interface design

Techila – Middleware

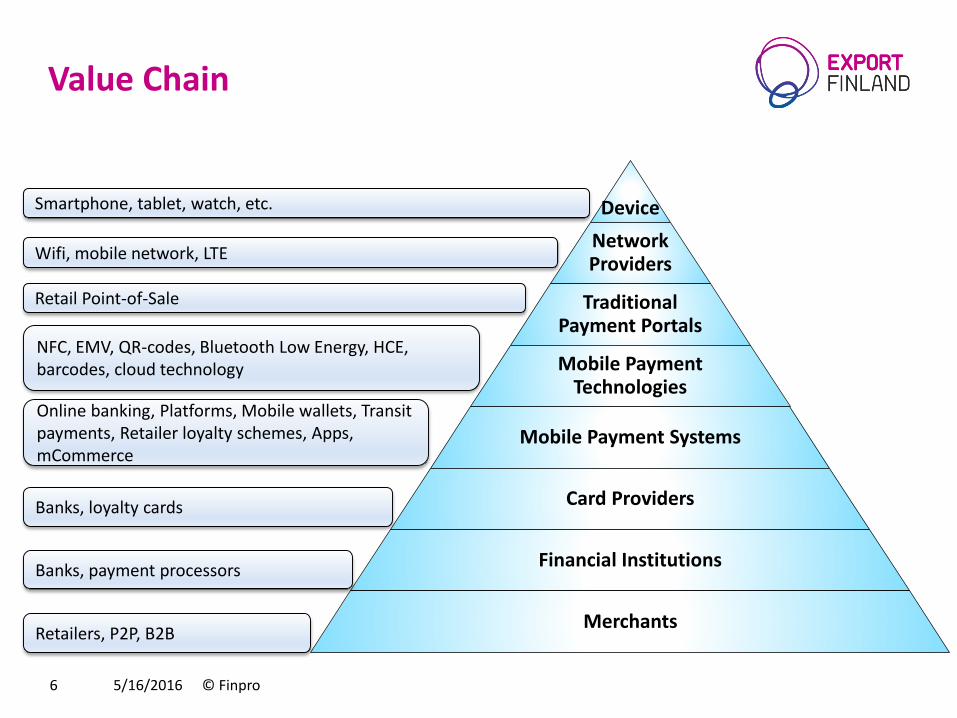

Value Chain

5/16/2016 © Finpro 6

Device

Network Providers

Traditional Payment Portals

Mobile Payment Technologies

Mobile Payment Systems

Card Providers

Financial Institutions

Merchants

Wifi, mobile network, LTE

Retail Point-of-Sale

Smartphone, tablet, watch, etc.

NFC, EMV, QR-codes, Bluetooth Low Energy, HCE, barcodes, cloud technology

Online banking, Platforms, Mobile wallets, Transit payments, Retailer loyalty schemes, Apps, mCommerce

Banks, loyalty cards

Banks, payment processors

Retailers, P2P, B2B

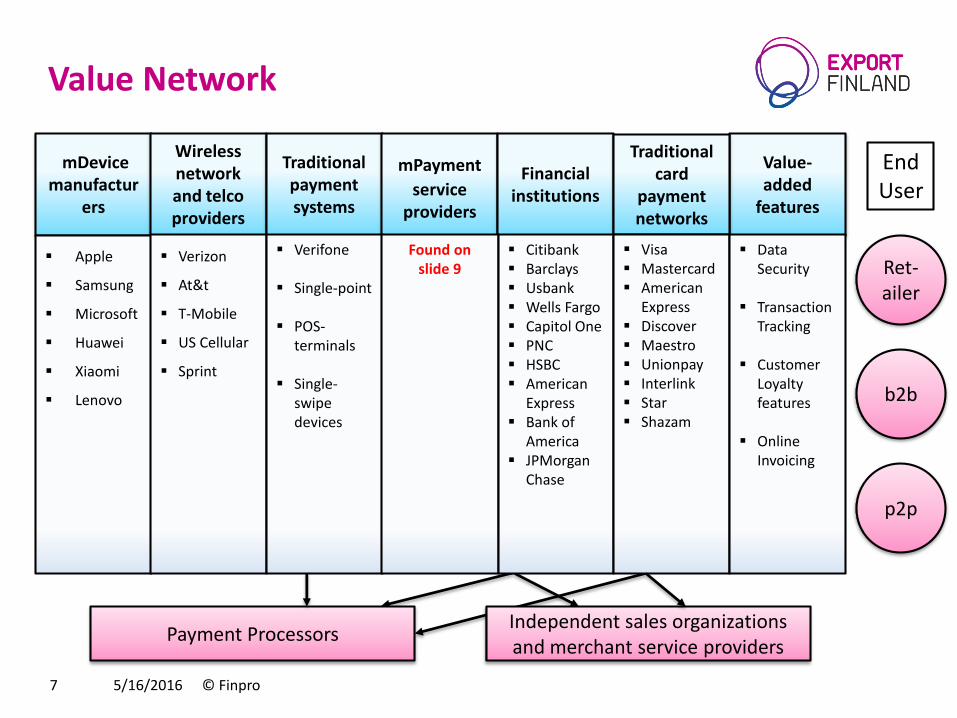

Value Network

5/16/2016 © Finpro 7

Value-added

features

mDevicemanufactur

ers

Wireless networkand telcoproviders

Traditionalpayment systems

mPayment

serviceproviders

Financial institutions

Traditionalcard

payment networks

Apple

Samsung

Microsoft

Huawei

Xiaomi

Lenovo

Verizon

At&t

T-Mobile

US Cellular

Sprint

Verifone

Single-point

POS-terminals

Single-swipedevices

Found on slide 9

Citibank Barclays Usbank Wells Fargo Capitol One PNC HSBC American

Express Bank of

America JPMorgan

Chase

Visa Mastercard American

Express Discover Maestro Unionpay Interlink Star Shazam

Data Security

TransactionTracking

CustomerLoyaltyfeatures

Online Invoicing

Ret-ailer

b2b

p2p

EndUser

Payment ProcessorsIndependent sales organizationsand merchant service providers

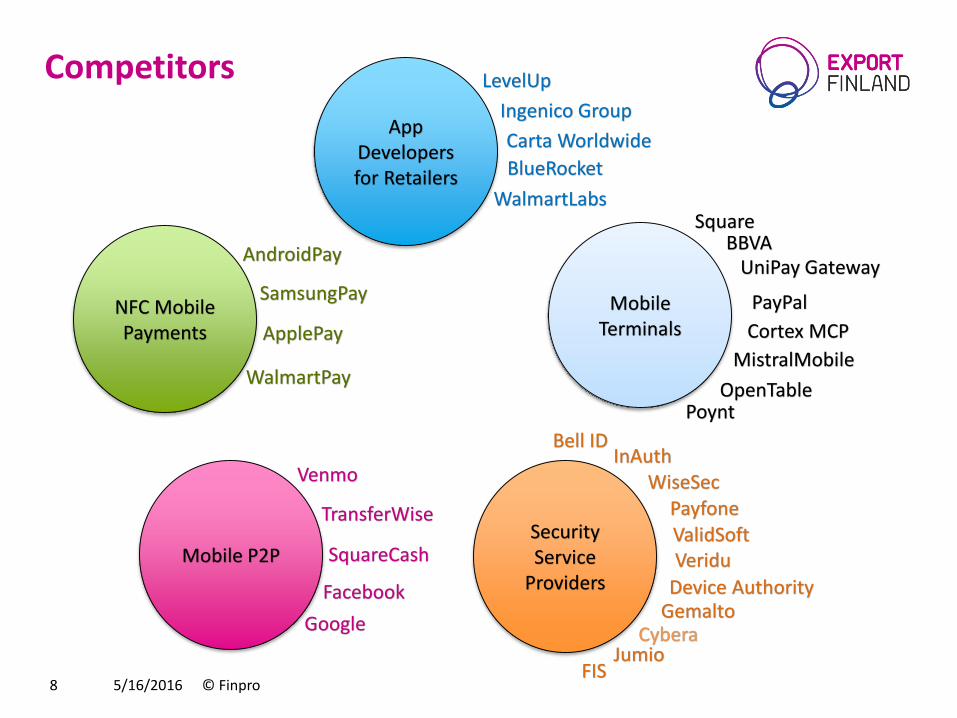

Competitors

5/16/2016 © Finpro 8

AppDevelopersfor Retailers

LevelUp

Ingenico Group

Carta Worldwide

BlueRocket

WalmartLabs

Mobile P2P

Venmo

TransferWise

SquareCash

SamsungPay

ApplePay

AndroidPay

WalmartPay

NFC Mobile Payments

Mobile Terminals

Square

UniPay Gateway

MistralMobile

PayPal

OpenTable

BBVA

Cortex MCP

Poynt

Security Service

Providers

Cybera

Veridu

FIS

Bell ID

GemaltoDevice Authority

Jumio

InAuthWiseSec

ValidSoftPayfone

Alliances and Industry Cooperation

• Smart Card Alliance Payments Council:

– Focuses on facilitating the adoption of chip-enabled payments and payment applications in the U.S. through education programs for consumers, merchants, issuers, acquirers/processors, government regulators, mobile telecommunications providers and payments service providers. The group is bringing together payments industry stakeholders, including payments industry leaders, merchants and suppliers, and is working on projects related to implementing EMV, contactless payments, NFC-enabled payments and applications, mobile payments, and chip-enabled eCommerce

• Merchant Customer Exchange (CurrentC)

– A retailer-led initiative, including major retailers such as Walmart, Target, 7Eleven, Best Buy, CVS, Darden Restaurants, Hy-Vee,Shell, Sunoco and HMSHost, Alon Brands, Hy-Vee Inc, Lowe's Cos Inc, Publix Super Markets Inc, Sears Holdings Corp, Shell Oil Products US, Sunoco Inc.

• Electronic Transactions Association

– A Mobile Payments Committee (ISIS) including industry player such as AT&T, Verizon Wireless, Sprint and T-Mobile USA, but also Google, Isis, VeriFone and PayPal, in addition to financial institutions Wells Fargo and Capital One plus credit card giants American Express, Discover, MasterCard and Visa. http://www.electran.org/about/2013-committees/#mp

• Mobey Forum

• NFC Forum

• GSMA

• GlobalPlatform

• ITU

5/16/2016 © Finpro 9

• Challenges & Barriers:

– Implementation is expensive in the finance industry, which will be a challenge for mobile payment service providers. For example, NFC systems implementation is expensive for retailers, causing manyof them to not embrace mobile payments at all

– Major banking groups have complex legacy systems and are governed by strict legislative and political policies, which may hinder mobile payment adoption services that are connected to banksand financial institutions

– A change in consumer behaviour is required, which can be a slow and challenging process

– Regulation is very fragmented at the moment and will be a challenge until a nationwide consistentregulatory environment exists

• Enablers:

– A rapidly growing market, plenty of room for new innovations

– Various market segments = many opportunities

– The convergance of remote and proximity mobile payments

– There is constant effort to change the regulatory framework

– Cryptocurrencies will offer new and unforeseen opportunities

– Fewer bricks and mortar retail banks will drive a need for mCommerce

– Higher retail bank competition will drive advanced customer care and customer experience solutions

5/16/2016 © Finpro 10

Potential for Finnish Offering- Market entry barriers, challenges and enablers

Key Messages of Opportunity

• The market demand for mobile payment solutions is high in the United States, and expected to keep increasing. The key drivers influencing the increase in demand are: an increasing consumerawareness, propogation of 4G/LTE networks, regulatory influences, smartphone proliferation, and the clear benefits to banks, retailers, and consumers

• The opportunity lies in security, privacy, and conveniance. Mobile payments which provide allthree of these features will be winners in the sector: Finland can provide this!

• Banking and mobile payments markets are both quite fragmented in the United States, providingnumerous pathways for market entry. The mobile payments market is still developing, thereforethe time to act is now.

• Finland already has mobile payment expertise: Mobile payments are quite standard in Finland and we have a high user rate of mobile banking. Finnish companies have proof-of-conceptadvantage over their competition. The finnish ICT sector combined with the start-up boom haslaunched us to the forefront of mobile payment and fintech solutions development

5/16/2016 © Finpro 11

Prospect List – Finnish Companies

• Wone – Connects international mobile payments and wallets using state of the art smart contracts and block chain

technology

• Moni – P2P payments, spending tracking, invoicing

• Pivo – Finnish mobile wallet

• PayIQ – Mobile payments and ticket service

• Uniqul – Face recognition payments

• Mobiwallet – Frictionless mobile payment solutions for retail

• Crosskey Solutions – Internet banking platform

• Jetico – Data protection software

• Movial – Secure mobile, embedded and cloud application development

• Ariki – Biometric ID systems for smart access

• MePIN – Banking grade security for online identities and payments (already in USA)

• Holvi – Online bank account for SME’s and organizations (acquired by BBVA)

• Riskpointer – Creates mobile payment applications for retailers, including data and transaction analysis

• Nordledger – Invoicing platform for retailers/businesses based on block chain technology

• eTasku – Electronic receipts

• Frosmo – User interface design

• Techila – Middleware

5/16/2016 © Finpro 12

Activity Plan - Team Finland

• Supporting activities: – A Fintech Seminar was held in Helsinki on January 26, 2016 by Perry Le Dain and Hartti

Suomela, with a focus on opportunities for Finnish companies in the Fintech sector acrossvarious markets

• Roadmap and suggested activities: – Continue research and determine the current mobile payments environment and more in-

depth evaluation of the value network in the USA– Activate finnish companies and provide training for entering into the US market– Determine capabilities of companies for entering the market– Engage in networking activities

• Attend trade fairs and events (Mobile Payments Conference, Interactive CustomerExperience Summit, eCommerce Show USA, Mobile Payments Innovation Summit, Bank Customer Experience Summit)

• Become members of key alliances and associations– Define and establish key partnerships with merchants/retailers (Gain merchant support),

and determine B2B opportunities– Define and establish key partnerships with financial institutions, banks, and card providers– Work through regulation and legalities and prepare for market entry

5/16/2016 © Finpro 13

5/16/2016 © Finpro 14

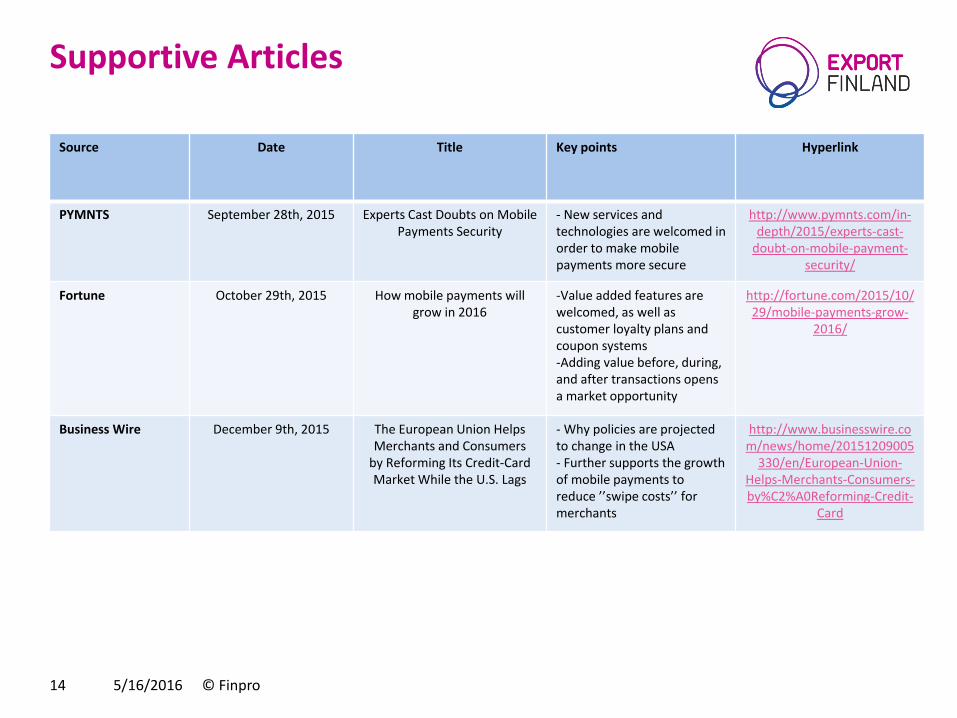

Source Date Title Key points Hyperlink

PYMNTS September 28th, 2015 Experts Cast Doubts on Mobile Payments Security

- New services and technologies are welcomed in order to make mobile payments more secure

http://www.pymnts.com/in-depth/2015/experts-cast-

doubt-on-mobile-payment-security/

Fortune October 29th, 2015 How mobile payments willgrow in 2016

-Value added features arewelcomed, as well as customer loyalty plans and coupon systems-Adding value before, during, and after transactions opensa market opportunity

http://fortune.com/2015/10/29/mobile-payments-grow-

2016/

Business Wire December 9th, 2015 The European Union Helps Merchants and Consumers

by Reforming Its Credit-Card Market While the U.S. Lags

- Why policies are projectedto change in the USA- Further supports the growthof mobile payments to reduce ’’swipe costs’’ for merchants

http://www.businesswire.com/news/home/20151209005

330/en/European-Union-Helps-Merchants-Consumers-by%C2%A0Reforming-Credit-

Card

Supportive Articles

Thank You!