Embed Size (px)

Citation preview

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 1/12

insight

Mobile payments have been highly

touted since it became apparent that

the mobile phone would emergeas a ubiquitous consumer device.

However early market adoption was

stunted by technological challenges,

a lack o standardization, ragmented

commercial eorts, and most impor-

tantly, a lack o sustainable business

models. More recently, however, there

have been signs o renewed interest

in mobile payments. Recent commer-

cial initiatives include NTT DoCoMo

and SK Telecom in Asia as well as

mobile payment trials in the U.S., by PayPal Mobile, Visa and MasterCard.

We believe mobile operators in the U.S. now have a real opportunity

to lead this market development, given their large customer bases, and

control o mobile device eatures, user interace, and subsidies.

We dene mobile payments (m-payments) as any payment transactions,

whether in-store or remote, executed on mobile devices. In this paper,

we rst assess the market opportunity or m-payments in comparison

to other traditional payment methods. We then identiy and evaluate

potential business models based on past and ongoing initiatives. Finally,

we highlight key strategic questions or mobile operators to assess the

mobile payment opportunity.

Mobile Payments: MobileOperator Market Opportunitiesand Business Models

By Hamilton Sekino, John Kwon and Se Han Bong

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 2/12

Potential Drivers for Market

Adoption of Mobile Payments

While mobile operators, nancial services rms,

and retailers have been evaluating the easibilityo m-payments since early 2000, recent

developments on both the supply and demand side

are prompting the key players in the m-payments

value chain to get serious about its potential.

On the supply side, mobile operators

are under pressure to continue looking or

new revenue sources to counteract

voice pricing decline and subscriber growth

saturation. While mobile operators in the

U.S. are gaining traction with mobile data

content and applications, which already

represent 13% o total ARPU, the m-payment

market presents them with an opportunity

to urther expand non-voice revenues. Mobile

operators in mature wireless markets such

as South Korea and Japan, where mobile

data ARPU already reached 19% and 29% o

ARPU respectively, are aggressively leading

their respective m-payment ecosystems. We

estimate that mobile operators in the US

will need to generate more than $40B in non-

voice revenues by 2010 in order to sustain

overall ARPU, and they will be looking at

m-payments as one potential revenue source.

Furthermore, nancial institutions, acing

declining revenue growth rom traditional

credit cards, are also looking at cash-

dominated micro-payments (i.e. transactions

less than $5) to generate new revenue

streams. In 2004, micro-payments processed

through credit and debit cards accounted

or only $13.5 billion out o over $1 trilliontotal spent on micro-payments.

On the demand side, the growing ubiquity o

mobile phones and their increasing multi-

unctionality make mobile phones a compelling

candidate or replacing a physical wallet. In

the U.S. mobile penetration has passed 75%,

with 235M mobile phone users, compared

to 176M people with credit/debit cards.

Surveys reveal that U.S. consumers today

are more likely to leave home without their

wallets than their mobile phones.

In addition, consumers are increasingly

comortable in using their mobile phones or

applications other than voice. This is clearly

the case in Japan and South Korea, which are

leading m-payment deployments. It is reasonable

to expect this trend to carry over to the U.S.

market, where mobile data penetration is

projected to grow rom 21% to 52% by 2011.

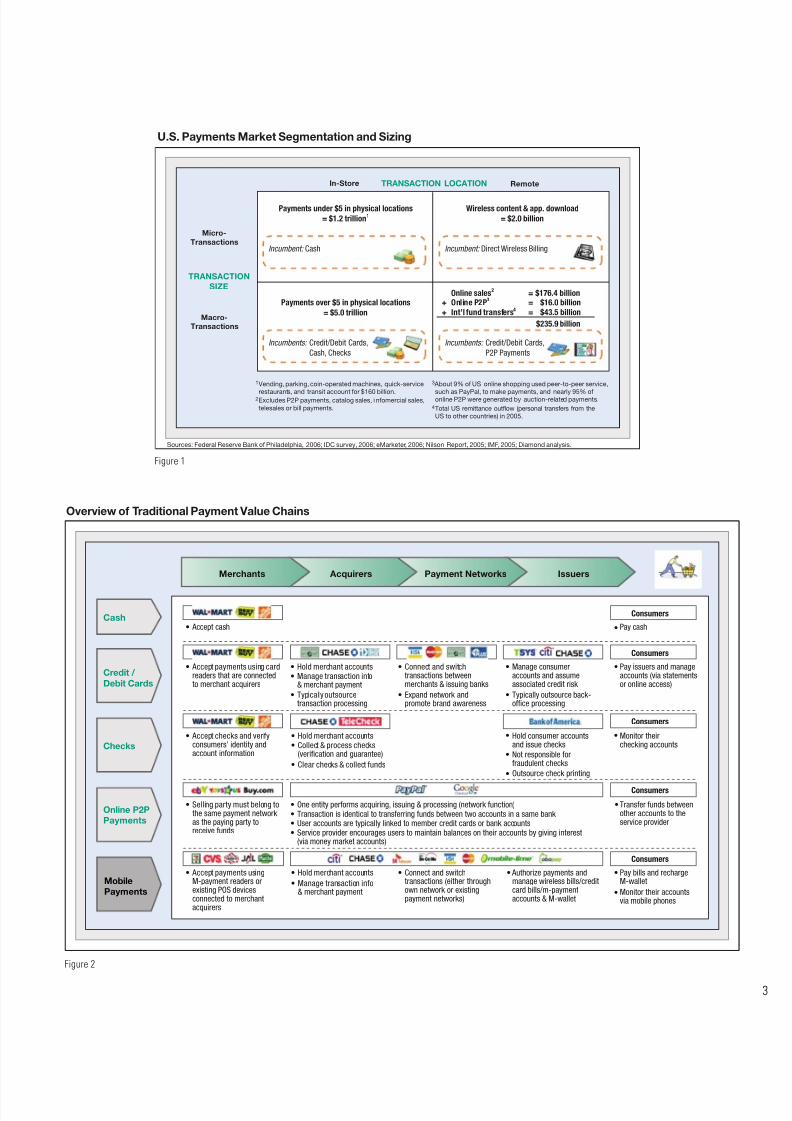

Segmentation and Sizing of the

Mobile Payment Market

To help assess the market potential o mobilepayments, Diamond rst looked at the curren

payments market and identied and sized

segments that are more predisposed

to adopt mobile payments (Figure 1).

The market is segmented into 4 quadrants:

in-store vs. remote and micro vs. macro

transactions, where a micro transaction is

dened as less than $5. From this perspective, w

ocused on in-store transactions, aggregating to

more than $6 trillion in annual transactions, andon peer-to-peer (P2P) and international und

transers, a much smaller market with close t

$60B in annual transactions.

Mobile phones possess key value propositions

that make m-payments ideal or these segments

For in-store segments—in particular the micro-

payments segment—the value proposition is the

convenience and speed o contactless payments

enabled by mobile phones with embedded NFC

(Near Field Communication) chips. For on-line

P2P and international transer markets, the value

proposition is the inherent connectivity, ubiquity,

and near real-time verication capability

o mobile devices (via SMS, WAP, or IVR).

Overview of Payment Value Chains

Beore evaluating and recommending an

optimal new value chain and business model

or mobile operators, it is useul to rst

review existing payment models (Figure 2).

The Mobile Payment

Market Opportunity

For more information contact:

Hamilton Sekino, Partner

The Mobile Payment Market

Opportunity . . . . . . . . . . . . 2

Mobile Payment Business Models . . . 5

Conclusion: Recommendations or

Mobile Operators . . . . . . . . 10

About the Firm . . . . . . . . . . . . 12

About the Authors . . . . . . . . . . 12

table o contents

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 3/12

Overview of Traditional Payment Value Chains

Cash

Credit /

Debit Cards

Checks

Online P2P

Payments

Mobile

Payments

Consumers

• Accept cash Pay cash

Consumers

• Accept payments using cardreaders that are connectedto merchant acquirers

Manage consumeraccounts and assumeassociated credit risk

Typically outsource back-office processing

Pay issuers and manageaccounts (via statementsor online access)

• Hold merchant accounts• Manage transaction info

& merchant payment

• Typically outsourcetransaction processing

• Connect and switchtransactions betweenmerchants & issuing banks

•

•

•

• •

•

•

•

•

Expand network andpromote brand awareness

Consumers

• Accept checks and verifyconsumers’ identity andaccount information

Monitor theirchecking accounts

Hold consumer accountsand issue checks

Not responsible forfraudulent checks

Outsource check printing

• Hold merchant accounts• Collect & process checks

(verification and guarantee)

• Clear checks & collect funds

Consumers

• Accept payments usingM-payment readers orexisting POS devicesconnected to merchantacquirers

Authorize payments andmanage wireless bills/creditcard bills/m-paymentaccounts & M-wallet

Pay bills and rechargeM-wallet

Monitor their accountsvia mobile phones

• Hold merchant accounts

• Manage transaction info& merchant payment

• • •

•

Connect and switchtransactions (either throughown network or existingpayment networks)

Consumers

• •One entity performs acquiring, issuing & processing (network function)• Transaction is identical to transferring funds between two accounts in a same bank • User accounts are typically linked to member credit cards or bank accounts• Service provider encourages users to maintain balances on their accounts by giving interest

(via money market accounts)

• Selling party must belong tothe same payment network as the paying party toreceive funds

Transfer funds betweenother accounts to theservice provider

Issuers AcquirersMerchants Payment Networks

Figure 2

Sources: Federal Reserve Bank of Philadelphia, 2006; IDC survey, 2006; eMarketer, 2006; Nilson Report, 2005; IMF, 2005; Diamond analysis.

TRANSACTION LOCATION

Micro-

Transactions

Macro-Transactions

1Vending, parking, coin-operated machines, quick-service

restaurants, and transit account for $160 billion.2Excludes P2P payments, catalog sales, i nfomercial sales,telesales or bill payments.

3 About 9% of US online shopping used peer-to-peer service,

such as PayPal, to make payments, and nearly 95% ofonline P2P were generated by auction-related payments.

4Total US remittance outflow (personal transfers from theUS to other countries) in 2005.

In-Store Remote

TRANSACTION

SIZE

U.S. Payments Market Segmentation and Sizing

Incumbents: Credit/Debit Cards,

Cash, Checks

Online sales2 = $176.4 billion+ Online P2P3 = $16.0 billion+ Int’l fund transfers4 = $43.5 billion

$235.9 billion

Payments over $5 in physical locations

= $5.0 trillion

Incumbent: Cash

Payments under $5 in physical locations

= $1.2 trillion1

Wireless content & app. download

= $2.0 billion

Incumbents: Credit/Debit Cards,

P2P Payments

Incumbent: Direct Wireless Billing

Figure 1

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 4/12

Traditional payments typically involve a

merchant, acquirer, issuer, and a consumer.

The roles o merchants and consumers

are obvious. Acquirers are responsible oracquiring merchants and enabling merchants

to process payments. Issuers are responsible

or issuing payment devices to consumers

and processing the transer o unds

rom consumer accounts to merchants.

In the case o credit and debit cards and

other electronic orms o payment, a payment

network provider, such as Visa or MasterCard,

resides between acquirers and issuers

to acilitate the transer o inormation and

unds. Payment network providers are

also responsible or expanding their merchant

networks and user membership to ensure

wide acceptance and drive revenue growth.

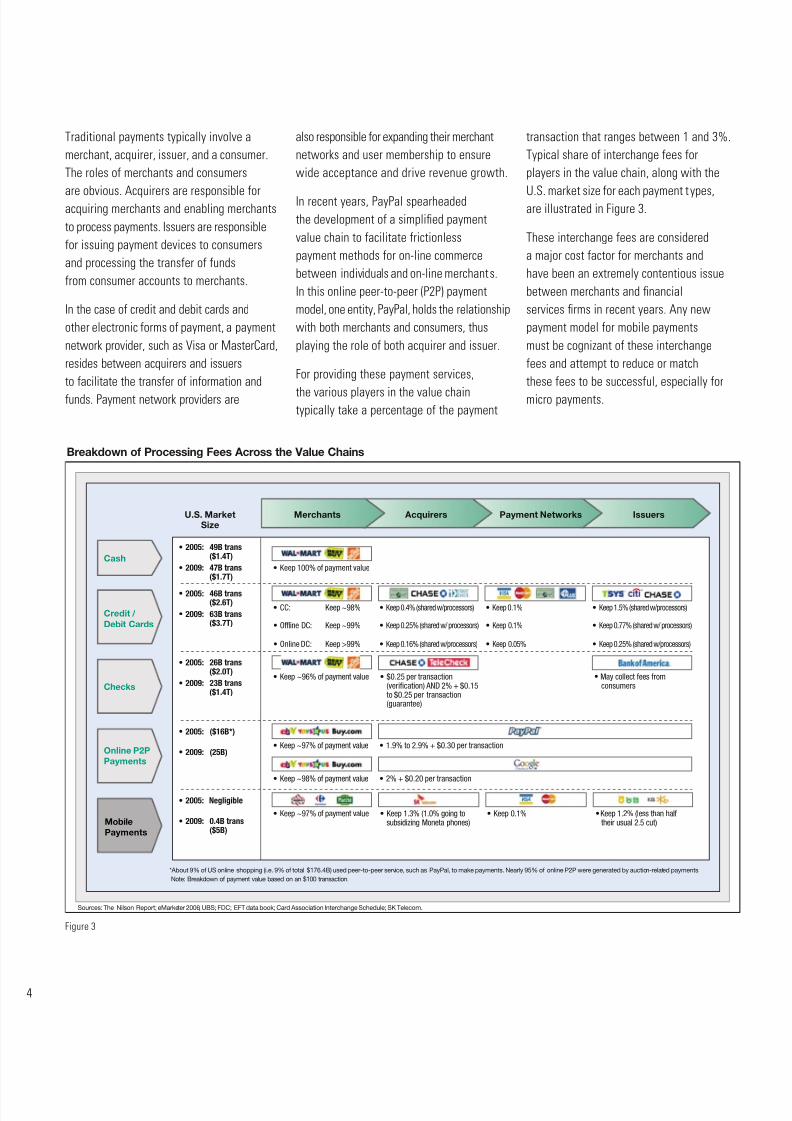

In recent years, PayPal spearheaded

the development o a simplied payment

value chain to acilitate rictionless

payment methods or on-line commerce

between individuals and on-line merchants.

In this online peer-to-peer (P2P) payment

model, one entity, PayPal, holds the relationship

with both merchants and consumers, thus

playing the role o both acquirer and issuer.

For providing these payment services,

the various players in the value chaintypically take a percentage o the payment

transaction that ranges between 1 and 3%.

Typical share o interchange ees or

players in the value chain, along with the

U.S. market size or each payment types,are illustrated in Figure 3.

These interchange ees are considered

a major cost actor or merchants and

have been an extremely contentious issue

between merchants and nancial

services rms in recent years. Any new

payment model or mobile payments

must be cognizant o these interchange

ees and attempt to reduce or match

these ees to be successul, especially or

micro payments.

Breakdown of Processing Fees Across the Value Chains

Cash

Credit /

Debit Cards

Checks

Online P2P

Payments

Mobile

Payments

• Keep 100% of payment value

• CC: • Keep 0.4% (shared w/processors)

• Keep 0.25% (shared w/ processors)

• 2005: 49B trans($1.4T)

• 2009: 47B trans($1.7T)

• 2005: 46B trans($2.6T)

• 2009: 63B trans($3.7T)

• 2005: 26B trans($2.0T)

• 2009: 23B trans($1.4T)

• 2005: ($16B*)

• 2009: (25B)

• 2005: Negligible

• 2009: 0.4B trans($5B)

• Keep 0.16% (shared w/processors)

• Keep 1.5% (shared w/processors)

• Keep 0.77% (shared w/ processors)

• Keep 0.25% (shared w/processors)

•

• Keep 0.1%

• Keep 0.05%

• Offline DC:

• Online DC:

Keep ~98%

Keep ~99%

Keep >99%

Keep 0.1%

•• Keep ~96% of payment value May collect fees fromconsumers

• $0.25 per transaction(verification) AND 2% + $0.15to $0.25 per transaction(guarantee)

• Keep ~97% of payment value Keep 1.2% (less than halftheir usual 2.5 cut)

• Keep 1.3% (1.0% going tosubsidizing Moneta phones)

• •Keep 0.1%

• 1.9% to 2.9% + $0.30 per transaction• Keep ~97% of payment value

• 2% + $0.20 per transaction• Keep ~98% of payment value

Issuers AcquirersMerchantsU.S. MarketSize

Payment Networks

Sources: The Nilson Report; eMarketer 2006; UBS; FDC; EFT data book; Card Association Interchange Schedule; SK Telecom.

*About 9% of US online shopping (i.e. 9% of total $176.4B) used peer-to-peer service, such as PayPal, to make payments. Nearly 95% of online P2P were generated by auction-related payments.

Note: Breakdown of payment value based on an $100 transaction.

Figure 3

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 5/12

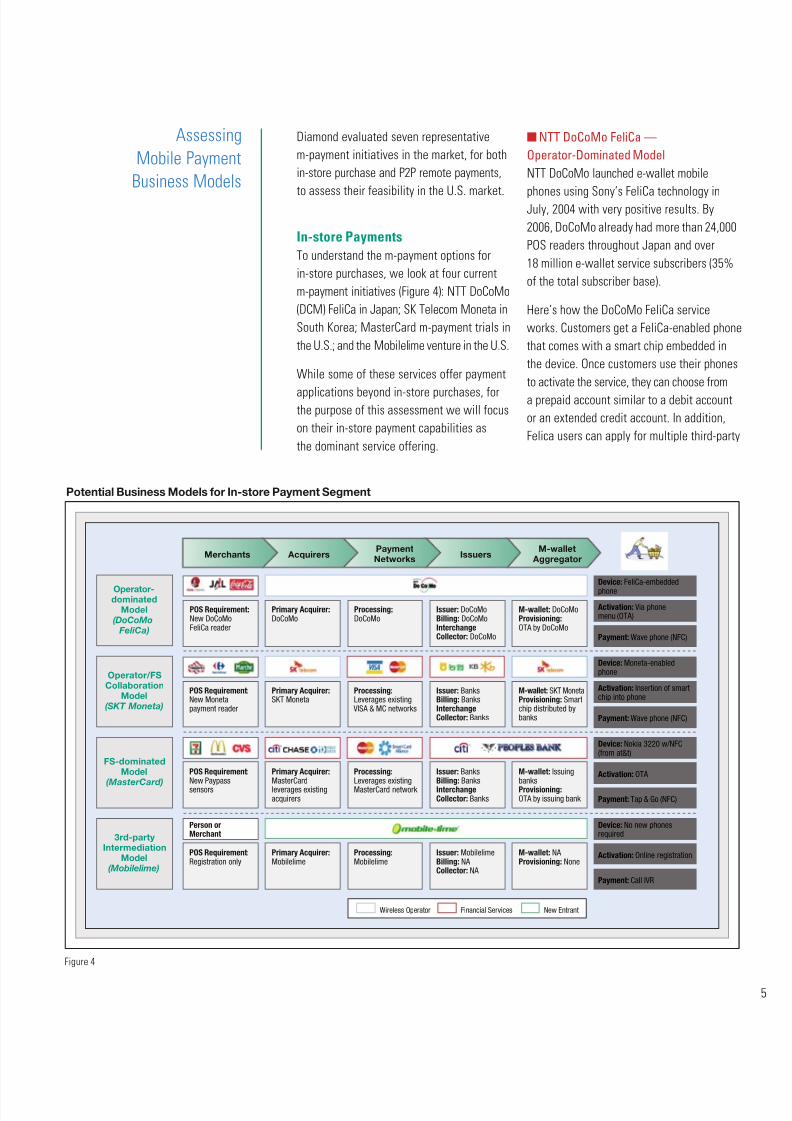

Diamond evaluated seven representative

m-payment initiatives in the market, or both

in-store purchase and P2P remote payments,

to assess their easibility in the U.S. market.

In-store Payments

To understand the m-payment options or

in-store purchases, we look at our current

m-payment initiatives (Figure 4): NTT DoCoMo

(DCM) FeliCa in Japan; SK Telecom Moneta in

South Korea; MasterCard m-payment trials in

the U.S.; and the Mobilelime venture in the U.S.

While some o these services oer payment

applications beyond in-store purchases, orthe purpose o this assessment we will ocus

on their in-store payment capabilities as

the dominant service oering.

nNTT DoCoMo FeliCa —

Operator-Dominated Model

NTT DoCoMo launched e-wallet mobile

phones using Sony’s FeliCa technology inJuly, 2004 with very positive results. By

2006, DoCoMo already had more than 24,000

POS readers throughout Japan and over

18 million e-wallet service subscribers (35%

o the total subscriber base).

Here’s how the DoCoMo FeliCa service

works. Customers get a FeliCa-enabled phone

that comes with a smart chip embedded in

the device. Once customers use their phones

to activate the service, they can choose rom

a prepaid account similar to a debit account

or an extended credit account. In addition,

Felica users can apply or multiple third-party

Assessing

Mobile Payment

Business Models

Potential Business Models for In-store Payment Segment

Operator-dominated

Model(DoCoMo FeliCa)

M-wallet Aggregator

Issuers AcquirersMerchantsPaymentNetworks

POS Requirement:New DoCoMoFeliCa reader

Primary Acquirer:DoCoMo

Processing:DoCoMo

Issuer: DoCoMoBilling: DoCoMoInterchangeCollector: DoCoMo

M-wallet: DoCoMoProvisioning: OTA by DoCoMo

Device: FeliCa-embedded

phone

Activation: Via phonemenu (OTA)

Payment: Wave phone (NFC)

Operator/FSCollaboration

Model(SKT Moneta)

POS Requirement:New Monetapayment reader

Primary Acquirer:SKT Moneta

Processing:Leverages existing

VISA & MC networks

Issuer: BanksBilling: BanksInterchangeCollector: Banks

M-wallet: SKT Moneta

Provisioning: Smartchip distributed bybanks

Device: Moneta-enabledphone

Activation: Insertion of smartchip into phone

Payment: Wave phone (NFC)

FS-dominatedModel

(MasterCard)

POS Requirement:New Paypasssensors

Primary Acquirer:MasterCardleverages existingacquirers

Processing:Leverages existingMasterCard network

Issuer: BanksBilling: BanksInterchangeCollector: Banks

M-wallet: IssuingbanksProvisioning: OTA by issuing bank

Device: Nokia 3220 w/NFC(from at&t)

Activation: OTA

Payment: Tap & Go (NFC)

3rd-partyIntermediation

Model(Mobilelime)

POS Requirement:Registration only

Primary Acquirer:Mobilelime

Processing:Mobilelime

Issuer: MobilelimeBilling: NA Collector: NA

M-wallet: NA Provisioning: None

Device: No new phonesrequired

Activation: Online registration

Payment: Call IVR

Person orMerchant

Wireless Operator Financial Services New Entrant

Figure 4

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 6/12

services such as transit tickets, ID cards, and

electronic keys to be incorporated into their

e-wallet phones.

Unique to the DoCoMo model is its vertical

integration. DoCoMo purchased a bank to

handle account management, credit issuance,

and merchant acquisition processes. In

this model DoCoMo has established an end-

to-end service delivery model: acquisition,

payment network, and issuance.

This model allows the operator great

fexibility in implementing the payment value

chain, particularly in establishing attractive

processing ees. Since there are no otherplayers in the value chain, the operator is ree

to set appropriate device costs and lower

transaction ees to entice new merchants.

In addition, having the ull range o

relationships as a wireless provider and

a banker is likely to increase the

stickiness o the consumer relationship,

thus reducing overall churn.

However, there are added risks and

disadvantages to going it alone. In addition

to the initial investment o acquiring a

bank with credit-issuing capability, DoCoMo

also had to invest in acquiring new

merchants and distributing new POS readers

throughout Japan. Given the geographical

size and population o the U.S., this would be

an even greater challenge or operators

here. DoCoMo was able to establish

partnerships and standards very quickly by

leveraging their dominant market share

in the Japanese mobile market. This may bechallenging in the U.S. market where there

is not a single dominating operator.

n SK Telecom Moneta—Operator

and FS Collaboration Model

Originally trialed in South Korea in 2002 using

inra-red readers, SKT Moneta currently

uses a NFC chip inserted into mobile phones

to acilitate payments. Visa and SKT also

announced that they will be oering Universal

SIM (USIM) cards, which can be personalized

over-the-air (OTA) starting in April 2007.

The SKT Moneta service has over 500,000

POS readers and 2.6 million subscribers

with Moneta phones.

Customers sign up or the SKT Moneta service

via the web or through their local bank branch.

Customers then receive a personalized

chip that they insert into the phone to activate

the service. Starting in April, 2007 customers

are able to sign up and get their mobile

phones provisioned OTA and no longer need

to wait or a new chip. Once activated, the

mobile device can be used as an e-money

account, credit card, transit ticket, membership

loyalty card, and or mobile online trading.

SKT is the m-wallet owner, meaning that

customers are able to hold multiple accounts

rom dierent issuers under one mobile

device that is serviced by SKT.

The SKT Moneta service exemplies a

collaboration model between a mobile

operator and nancial services rms.

Credit/account issuance is perormed bythe partnering banks and payments are

processed through the existing Visa and

MasterCard networks. SKT develops new

payment applications and is responsible

or rolling out new POS readers to merchants.

For those investments, SKT partakes in

a portion o the transaction revenue rom

the payments. SKT receives 1.3% o the

transactions, payment networks 0.1% and

issuing banks 1.2%, which is less than

their usual ee o 2.5% in South Korea.

We believe the operator/nancial services

collaboration model implemented by SKT

may be a better t or U.S. operators than

the operator-dominated model. In this model,

the payment service is issued in partnership

with existing bank issuers. Hence, all credit

issuance and account management are

perormed by the partnering banks and not

by the mobile operator, which may be

a point o concern or U.S. consumers who

preer to receive banking services rom

nancial services rms.

However, while SKT had to invest in the

rollout o new payment readers in South

Korea, U.S. operators should collaborate

with nancial services rms to leverage

the existing payment networks and

their contactless payment inrastructure.

Visa, MasterCard, and American Express

already have a big lead in rolling out

contactless payment readers and they are

likely to continue their investments.

Partnering with those rms would reduce

the investment required in rolling out

new readers and help to expand m-payment

adoption by establishing a single standard

across operators and nancial services rms.

nMasterCard M-Payments Trial—

FS Firm Dominated Model

MasterCard’s m-payment trials in Dallas

and New York illustrate a nancial services-

dominated model. In November, 2006

MasterCard launched its trial o m-paymentservice in Dallas, partnering with Mobile

Virtual Network Operator 7-Eleven Inc.’s Speak

Out Wireless and Peoples Bank o Paris

Texas. MasterCard later launched a similar trial

in New York, partnering with Cingular

and Citibank. In both trials, customers received

a NFC-enabled Nokia 3220 phone that

is activated OTA using the carrier network. Once

activated, customers can “tap and go” to

pay or goods in more than 32,000 merchant

locations that accept Paypass, including7-Eleven stores, McDonald’s, CVS, Duane Reade,

Sheetz, and Regal Entertainment Group.

The m-payment works just like the

MasterCard Paypass cards in that a customer

taps the reader to initiate the payment.

No signature is required or purchases lower

than $25, making it ideal or replacing

cash transactions.

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 7/12

The MasterCard m-payment trial exemplies

a nancial services-dominated model

by leveraging existing payment value chains.

The New York trial works with a customer’sexisting Citibank credit account and payment

is processed using MasterCard’s existing

payment network. While a permanent business

model has yet to be established, currently

the mobile operator’s involvement is limited

to providing the wireless network or

OTA provisioning o the mobile payment

device and participating to provide mobile

banking services.

This model has some advantages in terms o

consumer adoption. Given that the issuer

o the m-wallet is the issuing bank, it works

with existing credit accounts and does

not require customers to apply or new ones.

The trial uses MasterCard’s existing

payment networks and Paypass readers,

avoiding new investments in payment

readers or acquisition o new merchants.

MasterCard and Citibank, the issuing

bank in the New York trial, were able to

leverage their trusted brand names whichshould help to mitigate security concerns

around m-payments.

However, outside o the trial, a permanent

business model that would satisy all

players has yet to be determined. In the

trial, the operator acilitated the OTA

provisioning o the phone via the wireless

network, but all the other aspects o

the payments process are managed and

owned by the nancial services rms.

The mobile operator does not partake in

the interchange ees or own the m-wallet.

Given that U.S. operators have a dominant

relationship with device manuacturers

and heavily subsidize mobile devices, we

believe it is unlikely that operators would

be satised with such a passive role in the

value chain.

nMobilelime—3rd Party

Intermediation Model

Mobilelime’s third party intermediation

model represents another approach.Mobilelime works to combine marketing and

loyalty programs with m-payment service.

Initially designed with marketing and loyalty

programs in mind, Mobilelime and partnering

merchants provide discounts and send

optional promotional inormation to customers

via SMS.

To pay using Mobilelime, customers

call a 1-800 number and enter a PIN along

with a specic vendor location number to

initiate a payment. The vendor then inputs

the last 4 digits o the customer’s phone

number to receive the payment. Once

the payment is veried, Mobilelime transers

the money to the vendor rom a pre-

registered customer credit card similar to

a PayPal online payment. Merchants can

also participate in Mobilelime’s marketing

and loyalty programs to send promotional

inormation via SMS and track consumer

behavior via a customer’s phone number.

Mobilelime banks on consumer desire

or discounts and merchant interest in

maintaining eective loyalty programs to

motivate m-payments. Additionally, their IVR-

based payment method does not require any

new POS readers at the merchant location or

NFC-enabled handsets, which are adoption

barriers or other mobile payment methods

discussed earlier.

However, Mobilelime’s payment processesare cumbersome. Furthermore, Mobilelime

currently lacks the brand awareness and

marketing muscle to acquire new users and

the credibility to acquire merchants in

large numbers. We believe that it will be very

dicult or any third party new entrant to

disintermediate mobile operators and nancial

services incumbents in the value chain.

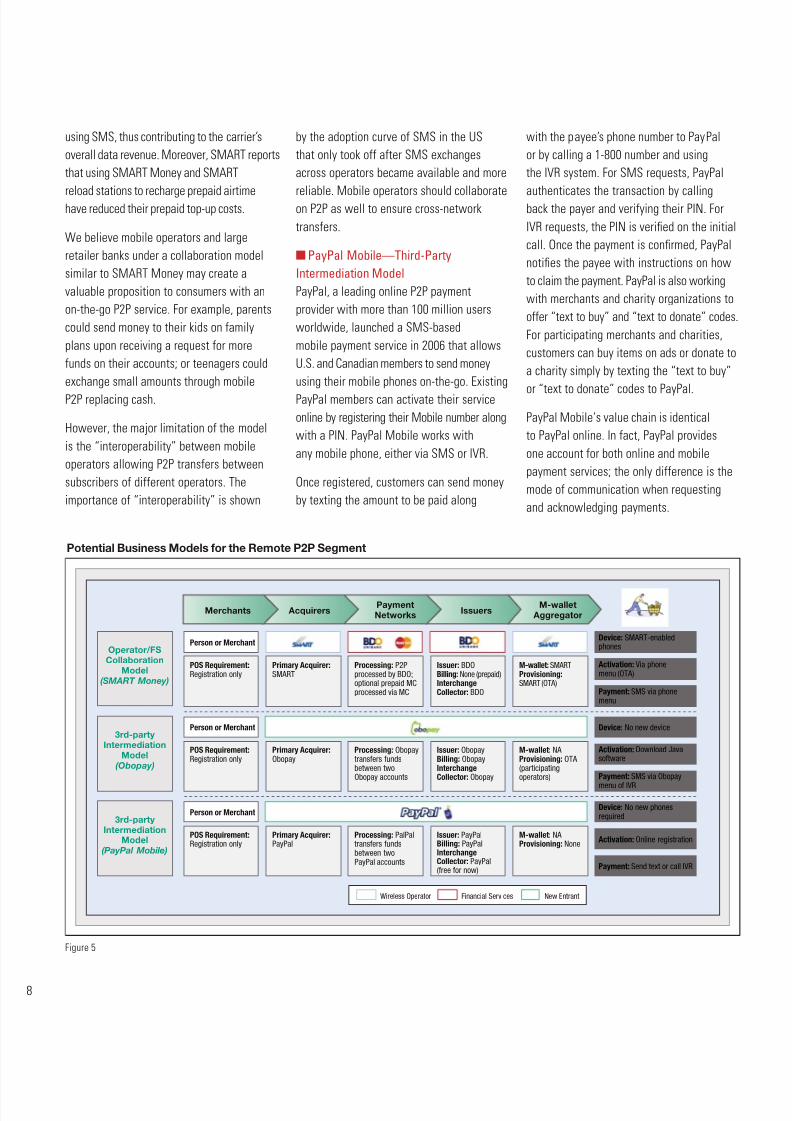

Targeting Remote &

Macro Payments

To understand m-payment options or remote

(mainly P2P) payments Diamond lookedat three m-payment initiatives in the market:

SMART Money in the Philippines and two

mobile services recently launched in the U.S.,

Obopay and PayPal Mobile (Figure 5, page 8).

While some o these services oer payment

applications beyond mobile P2P, or the

purpose o this assessment we will ocus on

their mobile P2P capabilities as the dominant

service oering.

n SMART Money—Operator and

FS collaboration Model

SMART Money, the world’s rst reloadable

e-wallet account, was launched in 2000

by SMART, a leading mobile operator

in the Philippines, and Banco de Oro. Each

SMART phone is shipped with a SMART

Money application pre-loaded on its SIM

card. Customers activate the SMART

Money service OTA using the pre-loaded

SMART Money menu on the phone.

Once activated, customers can use SMART

Money to send unds to other subscribers,

pay merchants, pay utility bills, and pay or

prepaid mobile airtime. Customers can also

reload or deposit cash into their SMART

Money account in over 700,000 retail locations

that participate as SMART Money reloading

stations. SMART also distributes an optional

prepaid MasterCard that can be used to

access unds in SMART Money.

In the SMART Money payment value chain,

all o the account management and payment

processing (except or MasterCard transactions)

is perormed by the partnering bank,

Banco De Oro. SMART handles marketing and

acquisition o new merchants and consumers.

While SMART does not get a portion o the

transaction ees, the transactions are perormed

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 8/12

using SMS, thus contributing to the carrier’s

overall data revenue. Moreover, SMART reports

that using SMART Money and SMART

reload stations to recharge prepaid airtimehave reduced their prepaid top-up costs.

We believe mobile operators and large

retailer banks under a collaboration model

similar to SMART Money may create a

valuable proposition to consumers with an

on-the-go P2P service. For example, parents

could send money to their kids on amily

plans upon receiving a request or more

unds on their accounts; or teenagers could

exchange small amounts through mobile

P2P replacing cash.

However, the major limitation o the model

is the “interoperability” between mobile

operators allowing P2P transers between

subscribers o dierent operators. The

importance o “interoperability” is shown

by the adoption curve o SMS in the US

that only took o ater SMS exchanges

across operators became available and more

reliable. Mobile operators should collaborateon P2P as well to ensure cross-network

transers.

nPayPal Mobile—Third-Party

Intermediation Model

PayPal, a leading online P2P payment

provider with more than 100 million users

worldwide, launched a SMS-based

mobile payment service in 2006 that allows

U.S. and Canadian members to send money

using their mobile phones on-the-go. Existing

PayPal members can activate their service

online by registering their Mobile number along

with a PIN. PayPal Mobile works with

any mobile phone, either via SMS or IVR.

Once registered, customers can send money

by texting the amount to be paid along

with the payee’s phone number to PayPal

or by calling a 1-800 number and using

the IVR system. For SMS requests, PayPal

authenticates the transaction by callingback the payer and veriying their PIN. For

IVR requests, the PIN is veried on the initial

call. Once the payment is conrmed, PayPal

noties the payee with instructions on how

to claim the payment. PayPal is also working

with merchants and charity organizations to

oer “text to buy” and “text to donate” codes.

For participating merchants and charities,

customers can buy items on ads or donate to

a charity simply by texting the “text to buy”

or “text to donate” codes to PayPal.

PayPal Mobile’s value chain is identical

to PayPal online. In act, PayPal provides

one account or both online and mobile

payment services; the only dierence is the

mode o communication when requesting

and acknowledging payments.

Potential Business Models for the Remote P2P Segment

M-wallet Aggregator

Issuers AcquirersMerchantsPaymentNetworks

Operator/FSCollaboration

Model(SMART Money)

POS Requirement:Registration only

Primary Acquirer:SMART

Processing: P2Pprocessed by BDO;optional prepaid MCprocessed via MC

Issuer: BDOBilling: None (prepaid)InterchangeCollector: BDO

M-wallet: SMARTProvisioning: SMART (OTA)

Device: SMART-enabledphones

Activation: Via phonemenu (OTA)

Payment: SMS via phonemenu

3rd-partyIntermediation

Model(Obopay)

POS Requirement:Registration only

Primary Acquirer:Obopay

Processing: Obopaytransfers fundsbetween twoObopay accounts

Issuer: ObopayBilling: ObopayInterchangeCollector: Obopay

M-wallet: NA Provisioning: OTA (participatingoperators)

Device: No new device

Activation: Download Javasoftware

Payment: SMS via Obopay

menu of IVR

3rd-partyIntermediation

Model(PayPal Mobile)

POS Requirement:Registration only

Primary Acquirer:PayPal

Processing: PalPaltransfers fundsbetween twoPayPal accounts

Issuer: PayPalBilling: PayPalInterchangeCollector: PayPal(free for now)

M-wallet: NA Provisioning: None

Device: No new phonesrequired

Activation: Online registration

Payment: Send text or call IVR

Person or Merchant

Person or Merchant

Person or Merchant

Wireless Operator Financial Services New Entrant

Figure 5

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 9/12

nObopay—Third-Party

Intermediation Model

Launched in March, 2006, Obopay oers on-

the-go P2P mobile payment service. Similar

to PayPal, both payee and payer must belong

to Obopay to send and receive unds. Also

similar to PayPal, Obopay links to a user-

provided bank or credit account to replenish

account balances when payment is made.

Customers can send money using an Obopay

application (which can be downloaded OTA or

subscribers o select operators), SMS, or

via a 1-800 number (IVR). The receiving party can

acknowledge payments and request payment

via the same Obopay application. Obopayalso provides an optional prepaid MasterCard

that can be used with the Obopay account

to make purchases at MasterCard locations

and to get cash at ATMs.

Obopay’s business model is based on

a simplied value chain, much like PayPal,

where Obopay holds accounts or both the

payee and payer and manages the transer o

unds between the two customers. Just like

PayPal, Obopay customers rely on existing

payment networks (credit or debit accounts)

to reload their virtual accounts.

The third-party intermediation model being

pursued by PayPal Mobile and Obopay oers

an inherent value proposition by enabling

customers across multiple mobile operators

to request and send money on-the-go at

anytime. Additionally, in PayPal’s case, they

already have a substantial user base and

the payment inrastructure established rom

their online P2P payments.

However, compared to the collaboration model

there are signicant limitations. Because

the third-party intermediation model does not

involve the mobile operators directly, the

user experience may not be ideal. In PayPal’s

case, the payment is initiated by texting

to PayPal’s number or by calling PayPal.

Obopay does oer a downloadable

application or select operator subscribers

but relies on SMS or IVR via a 1-800 number

or other operator subscribers. Even i

the provider has an SMS-based application,

some mobile operators may block messages

to the providers’ short codes, and even i the

provider has a Java-based downloadable

application, it is an issue to ensure that the

application will work across all handsets.

Involving the operators may help to develop

an on-deck application that is conducive to

a better customer experience.

Moreover, without partnerships with mobileoperators or well known nancial services

partners, the provider may also lack the brand

awareness to drive adoption o the service,

a particular challenge or new players such

as Obopay.

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 10/120

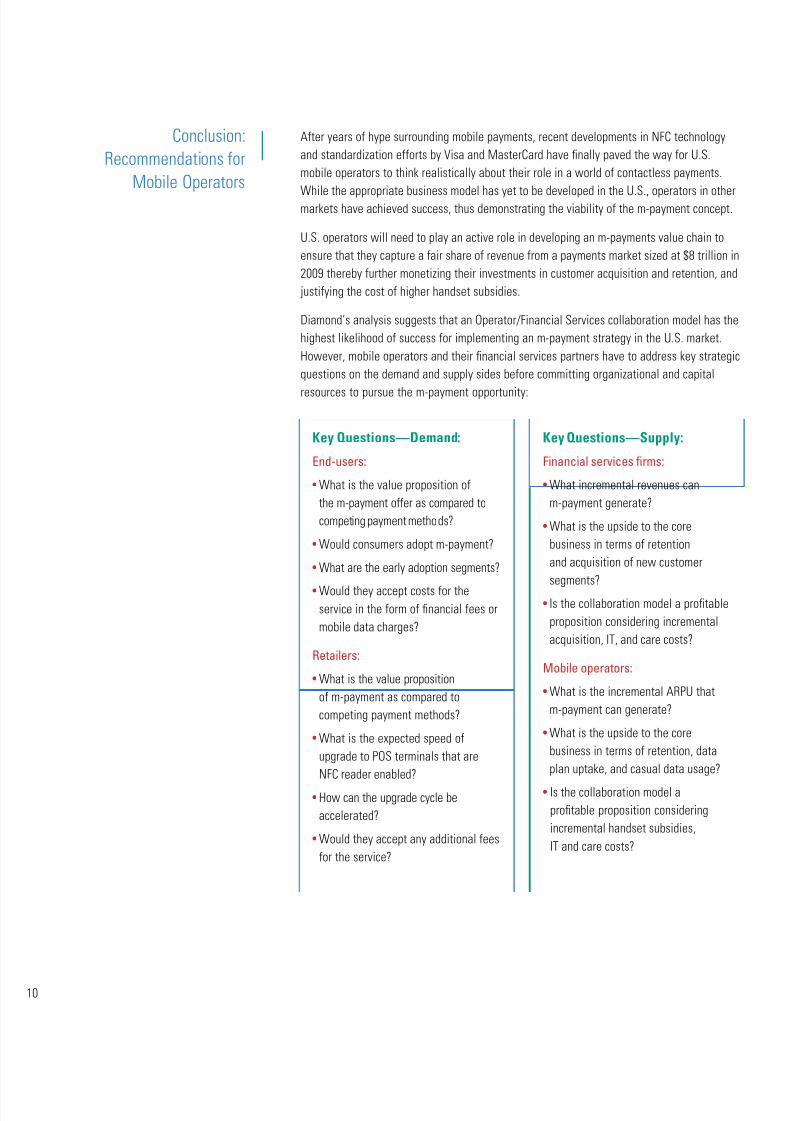

Ater years o hype surrounding mobile payments, recent developments in NFC technology

and standardization eorts by Visa and MasterCard have nally paved the way or U.S.

mobile operators to think realistically about their role in a world o contactless payments.

While the appropriate business model has yet to be developed in the U.S., operators in othermarkets have achieved success, thus demonstrating the viability o the m-payment concept.

U.S. operators will need to play an active role in developing an m-payments value chain to

ensure that they capture a air share o revenue rom a payments market sized at $8 trillion in

2009 thereby urther monetizing their investments in customer acquisition and retention, and

justiying the cost o higher handset subsidies.

Diamond’s analysis suggests that an Operator/Financial Services collaboration model has the

highest likelihood o success or implementing an m-payment strategy in the U.S. market.

However, mobile operators and their nancial services partners have to address key strategic

questions on the demand and supply sides beore committing organizational and capital

resources to pursue the m-payment opportunity:

Conclusion:

Recommendations or

Mobile Operators

Key Questions—Demand:

End-users:

• What is the value proposition o

the m-payment oer as compared to

competing payment methods?

• Would consumers adopt m-payment?

• What are the early adoption segments?

• Would they accept costs or theservice in the orm o nancial ees or

mobile data charges?

Retailers:

• What is the value proposition

o m-payment as compared to

competing payment methods?

• What is the expected speed o

upgrade to POS terminals that are

NFC reader enabled?

• How can the upgrade cycle be

accelerated?

• Would they accept any additional ees

or the service?

Key Questions—Supply:

Financial services frms:

• What incremental revenues can

m-payment generate?

• What is the upside to the core

business in terms o retention

and acquisition o new customer

segments?

• Is the collaboration model a protable

proposition considering incremental

acquisition, IT, and care costs?

Mobile operators:

• What is the incremental ARPU that

m-payment can generate?

• What is the upside to the core

business in terms o retention, data

plan uptake, and casual data usage?

• Is the collaboration model a

protable proposition considering

incremental handset subsidies,

IT and care costs?

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 11/12

8/14/2019 Mobile Payments - Diamond

http://slidepdf.com/reader/full/mobile-payments-diamond 12/12

DiamondSuite 3000 John Hancock Center

875 North Michigan Ave.Chicago, IL 60611T (312) 255 5000 F (312) 255 6000www.diamondconsultants.com

C H I C A G O • H A R T F O R D • L O N D O N • M U M B A I • N E W Y O R K • W A S H I N G T O N , D . C

© 2007 Diamond Management & Technology Consultants, Inc. All rights reserved.