Embed Size (px)

DESCRIPTION

Key Note on Economy on USElection Eve 2008

Citation preview

Peninsula HotelBeverly Hills, California

November 3, 2008

Presentation by Robert H. Edelstein

University of California at Berkeley

A Quagmire of Long-Run and Short-Run Issues

Fundamental International Economic Drivers

• Competition – The World is Flat and Crowded (Friedman)

• Globalization and Economic Integration: A Two-edged Sword (Stiglitz)

• Capital Market Integration and Securitization – The Limits are Imagination

• World Melting Pot of Socio-Political Ideology, Resource Environmental Competitiveness, Technology and Innovations

• Enhanced Volatility and Responsiveness – Integrated, Compacted World

Long View of Fundamental Economic & Financial Determinants: Summary

• International Growth Locomotives: China, India & United States

• Future Growth Determinants: Frontier Technologies, Globalization, Demographics, Environmental Degradation and Energy Resources

GDP Growth

-4

-2

0

2

4

6

8

10

12

14

16

18

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Time (Years)

Ann

ual P

erce

ntag

e C

hang

e in

GD

P

China USA Germany India Japan

Source: IMF (World Economic Outlook)

* Data after 2007 are estimates.

** * * * *

Energy Use Per Capita

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Energy Use per Captia

(

kWh/capita

)

Year 2002

China USA Japan Germany India

Source: International Atomic Energy Agency – Energy and Environment Data Reference Bank

U.S. Economy and the Deadly “D’s”

Deluxe LivingDis-savingDebt – private and PublicDeficits – Trade, Governments and HouseholdsDe-RegulationDegradation – Environment, etc.

Total Credit Market Debt Held by Rest of World as Share of Total US Credit Market Debt Outstanding; 1945-2007

Source: Flow of Funds;Table L 1

Foreign Holdings of US Securities as Share of Total Amount Outstanding

Source: US Treasury TIC data; Federal Reserve Flow of Funds

Source: BIS, IMF

Share of Global Reserves

2007

Share of Chinese Reserves in Dollar Denominated Securities

$, Bill

Source: Peoples Bank of China, US Treasury, Estimates by Authors

56%

73%

Official Institutional Share of Holdings by Foreigners

Source: US Treasury

Capital Markets and M&A OverviewPrivatization Trends – 2005/2006

Drivers for Buyers• Abundant supply of institutional and opportunistic capital• Strong financing markets and attractive interest rates• Reasonable return expectations• Improving fundamentals for many asset types• Arbitrage between public and private markets / Ability to line-up

sales of specific assets / portfolios

Additionally, many Public Companies played a role inPrivatizations through institutional / jv model:

• Boards acted strategically and empowered by strong currencies and availability of low-cost debt and JV equity

• Public markets were much more receptive to strategic transactions than in the past

Capital Markets and M&A OverviewPrivatization Trends – 2005/2006

Motivated seller base influenced by attractive valuationsand purchase price premiums / multiples

Valuations / proposals above most NAV estimatesAggressive suitors and increased review of strategicalternatives

Constraints of public marketShort-term accretion attentionLeverage constraintsAnalyst and Investor perceptions

Active BoardsMore attention to procedures, responses and corporategovernance

Roles for management in private forum, including growth ofplatform

Increased scrutiny and costs of being a public company

Drivers for Sellers

Capital Markets and M&A Overview2007 Mid-Summer Correction - Context for the Current Situation

Since the 2007 mid-summer correction, the capital markets have undergone a significant re-pricing of riskRisk premiums on high yield bonds have ballooned to levels well above their 12-month average of 455 bps and all-time low of 262 bps seen 6/1/2007 (1)In contrast, high yield default rates remain at an historic low of 0.9% - a record gap between risk premiums and defaults (2)

Since July, financial firms have announced $181 billion of write-downs linked to sub-prime exposure (3)Major firms have raised $72.3 billion of new capital to shore up balance sheets (4)

In 2007, an estimated $326 billion of residential mortgage payments reset; $412 billion are scheduled to reset during 2008 (5)(1) Source: BAS High Yield Bond Index.(2) High yield default rates of 0.9% as of 12/2007. Record gap between risk premiums and default rates as per Moody’s economist John Lonski (Source: Wall Street Journal).(3) Source: Bloomberg as of 2/29/08.(4) Source: Bloomberg as of 1/15/2008 and company reports.(5) Source: Deutsche Bank, Loan Performance and Rosen Consulting Group. Includes rate adjustments and IO expirations.

Capital Markets and M&A OverviewCMBS Market Overview

Real Estate Company Valuations

Sources: FactSet, Company reports and Wall Street Research as of 2/1/08.

What Are The Follow-up “D’s”for Now?

De-leveraging – Farewell Cheap DebtDistrust and DismayDeflation – Asset Market “Booms” FarewellDisarrayDefaults

Capital Markets Overview

The M&A market has slowed significantly since its late July 2007 peak as a result of the credit market “backup”The current M&A market slowdown is marked by the following dynamics:

Large, highly levered financings not availableShort-term asset flipping is no longer a viable strategySeller’s pricing expectations have been slow to adjust despite market expectation of

cap rate expansionGoing forward, key capital market themes in M&A will include:

Opportunistic investors, especially sovereign wealth funds, exerting pressure on distressed situationsLikely contraction of valuation multiples / widening of cap ratesCredit re-pricing and overall leverage reductionsIncrease in joint ventures as institutional real estate capital remains availableCapital structures increasingly funded by opportunistic players such as hedge funds, commitments from multiple institutions, or SWF

Market Current Situation & Outlook

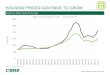

House Prices Inflate to Create an Historic BubbleRelative to underlying household income, the median house price appreciated far to fast.

About two-thirds of the bubble has already been deflated.

Our expectation is for the housing market to overshoot the historic price-to-income ratio.

Median House Price/Avg. HH IncomeFebruary 2008 MML (Recession)

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Rat

io

2005Q3

Wells Bubble Policy Instituted, First in the Nation, 2003Q4

Foreclosuresbreak-out to the upside.

Correction will overshoot.

Start of the housing bubble, 2001Q4

• What Happened to Bear Stearns?• Why did IndyMac Fail?• How do FNMA and FHLMC fit into the

Sub-Prime Crisis? AIG?• The BIG five: G-S, M-S, Lehman, M-L, and B-S

Recent Events of Concern

• Why has the Fed acted as the Ultimate Source of Liquidity?

• Can the U.S. let a Large Institution Fail?• What needs to be done in the Short-Run and

the Long-Run?

Policy Action!?

ABX-HE Index Prices Have DeterioratedThis chart shows the ABX index for AAA bonds backed by home equity loans issued

in February 2007 (as of April 22).

Even AAA bonds have lost about 43% their value in 14 months.

Summary

The financial markets are still under stress. Losses from mortgage derivatives are creating counter-party risk, and they have prevented the normal flow of transactions and credit as a result.

The result is that risk spreads are elevated.

The poor economic outlook has also boosted the risk spread in the corporate sector foreshadowing increased corporate bankruptcies, loan and bond defaults.

The Fed and the Treasury are still engaged!?

Elements for the Short-term and Long-term Resolution of the Subprime and Other Financial Crises

Devise Programs to Stabilize the Housing Market and Housing Finance System

Engender Housing and General Financial Market Viability

Implement Policies that Avoid Recurrence and Moral Hazards

Prepare for Potential Wider Domestic Economic Implication of the Sub-prime Crisis

Recognize and Plan for Potential Global Economic and Financial System Interactions

29

Overview Subprime IssuesDirect Effects

Delinquencies Foreclosureshome prices

Lender Industry and Secondary Market BehaviorNew Profit ModelUnderwriting StandardsFee StructuresAccessibility of Secondary Market

Risk Contagion EffectsNew ConstructionReal Estate ServicesEquity LoansFinancial Institutions

Global EffectsRisk Spread “Adjustments”U.S. Consumption and International Trade, World-wide Stock Market/Bond Market

30

Why Were We So Susceptible to the Subprime Crisis?

31

• Diminution of Underwriting Quality• Inexperience of Owner-Borrowers• Financial “Wizardry”• Aggressive, Risk-Taking Investors

How Exposed Are We?Total US housing stock is 128 million unitsAnnual sales since 2000 represent between 4-6% of stockStates with high levels of price declines account for a large share of housing stock; and larger share of mortgages outstandingNationwide, the ability to buy a home has not changed dramatically, but regional variations show large areas of vulnerabilitySubprime loans are 12 percent of all outstanding mortgages

32

Per Capita Income and Home Price Indices Compared, Far West, 1975-2008

0200400600800

1000120014001600

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

OFHEO index Per Capita Income Index

33

Source: Indices created by authors using Office of Federal Housing Enterprise Oversight index (adjusted to 1975 base); US Bureau of Economic Analysis data.

Understanding Variation in Exposure and Experience Can Help Shape Policy

Wide variation within the US in housing markets (median 2007 home value ranges from $88,000 in Mississippi to $536,000 in California)Wide variation in exposure to subprime loans (low of 6% in South Dakota, high of 20% in Nevada)Share of subprimes in foreclosure range from 3% in Utah to 18% in MichiganFactors, such as age, household size, ownership rates, and government regulation, can influence the level and outcome of exposure.

34

Local and State Revenue Impacts

Loss of Capital Gains TaxLoss of Property Tax BaseOther Transactions Based Fees and Taxes

Some Troubling ConclusionsRegional differences are significant?Homeownership at what social costs?Credit tightening needs to be selective, especially where economies are weak?

36

Policy ObjectivesStability in Housing (and other asset) Markets

Retaining high home ownership ratesArresting drastic value slideMaintaining ownership incentives for households with negative equityNormalizing new and existing market activity

Liquidity in Mortgage (and other asset) MarketsStabilizing financial marketsEfficient securitizationReorganizing Fannie and Freddie to be viable entities (at low social costs)

37

Whose Problem?• Homeowners/Borrowers• Homebuyers• Home-sellers• Builders• Lenders• Securitizers• Investors• Regulators• Taxpayers• Government sector• International Components

38

Policy Evaluation Criteria/Benchmarks

Moral Hazard Issue or Chance of RecurrenceFairness and EquityBang for the Buck (Efficiency)“Good” vs. “Bad” Subprime LoansDistributional (Income and Geographic) ImpactsLinkages of Housing finance System with Broader Financial System and Economy

39

The Secondary Market Enigma1. FNMA and FHLMC2. FDIC and Banks3. IB and Securitization4. Monoline Insurers5. CDS

40

Real Sector Constraints for Policy

Economic EnvironmentJob CreationHousehold FormationWage Growth Prospects

41

Policy PerspectiveNo Single Policy is the Silver BulletComplex Benefits-Costs Analyses Require Multi-faceted SolutionsRegional-State Differences Require Regionally Differentiated ApproachesReinvigorate Securitization ProcessTriage “Bad” Loans

42

Targeting PolicyEconomic Slow-downsCredit TighteningLoss of Confidence in System

43

What Should We Focus on Next?

Credit CrunchSynchronized World RecessionChina Bubbles BurstDollar Crash (Inflation Risk)Geopolitical Risks

Flux = Opportunity

Positive Demographics – Echo – Baby Boom; 72 Million People in Next 10 YearsExpensive Energy Scenarios – Changing Urban Form and Urban DensityFinancing Real Estate – What’s Next?U.S. May Represent Best Real Estate Investment “Opportunistic Plays” During Next Five Years!?

Office – Not Overbuilt, Except O.C., SeattleResidential – Rebound in Values Over the Next Five Years; MF vs. SFRetail – Well-Situated (LxLxL)Hotels – Dangerous Sector?Industrial/Warehouse – If Globalization Continues?!Securitized Real Estate Markets -- ?Land Play – Have a Hunch---Buy a Bunch will Not Work!? -- Not for the Meek!